UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

þ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2017

o TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT

For the transition period from ________ to _________

Commission File Number: 000-55585

Grom Social Enterprises, Inc.

(Exact name of registrant as specified in its charter)

| Florida | 46-5542401 | |

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) |

| 2060 NW Boca Raton Blvd. #6, Boca Raton, Florida | 33431 | |

| (Address of principal executive offices) | (Zip Code) |

Registrant’s telephone number, including area code: (561) 287-5776

Securities registered pursuant to Section 12(b) of the Act: None

Securities registered pursuant to Section 12(g) of the Act: common stock, par value $0.001 per share

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No þ

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No þ

Indicate by checkmark whether the registrant (1) filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes þ No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes þ No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§ 229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” “smaller reporting company” and “emerging growth” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | o | Accelerated filer | o |

| Non-accelerated filer | o (Do not check if a smaller reporting company) | Smaller reporting company | þ |

| Emerging growth company | o |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ¨

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No þ

The aggregate market value of the voting and non-voting common equity held by non-affiliates computed by reference to the price at which the common equity was last sold, or the average bid and asked price of such common equity, as of the last business day of the registrant’s most recently completed second fiscal quarter on June 30, 2017 was $4,300,293.

The number of shares of the registrant’s only class of common stock issued and outstanding was 126,066,419 shares as of April 16, 2018.

DOCUMENTS INCORPORATED BY REFERENCE

None

| i |

ITEM 1. BUSINESS

Overview

Effective August 17, 2017, Grom Social Enterprises, Inc. (the “Company,” “Grom,” “we,” “us,” or “our”), a Florida corporation f/k/a Illumination America, Inc. (“Illumination”), consummated the acquisition of Grom Holdings, Inc. (“Grom Holdings”). Pursuant to the terms of the Share Exchange Agreement (“Share Exchange”) that was entered into on May 15, 2017, the Company amended its Articles of Incorporation to increase its authorized capital to 200,000,000 shares of common stock, as well as to change its name to “Grom Social Enterprises, Inc.” At the closing of the Share Exchange, the Company issued an aggregate of 110,853,883 shares of its common stock to the Grom Holdings shareholders, pro rata to their respective ownership percentage. Each share of Grom Holdings was exchanged for 4.17 shares of Illumination common stock. As a result, the stockholders of Grom Holdings are now stockholders of the Company and own approximately 92% of the Company’s issued and outstanding shares of common stock.

All references to common share totals or values in this Annual Report on Form 10-K (“Annual Report”) unless otherwise stated, have been adjusted, retroactively, to reflect the Share Exchange ratio of 4.17 as of August 17, 2017.

Business Summary

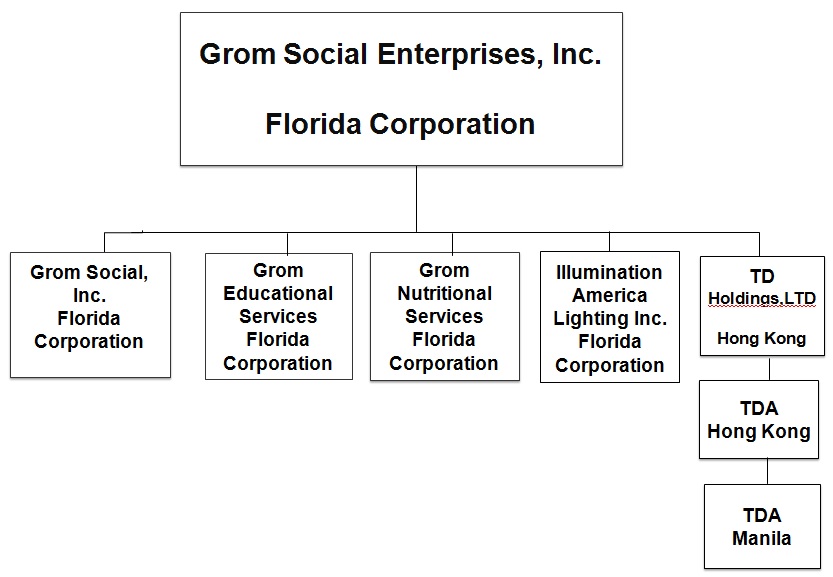

We operate our business through our five wholly-owned subsidiaries, including:

| · | Grom Social, Inc. (“Grom Social”), incorporated in the State of Florida in March 2012, operates our social media network designed for children. |

| · | TD Holdings Limited (“TD Holdings”), which was acquired in July 2016, is incorporated in Hong Kong. Its operations are conducted through its subsidiary companies, Top Draw Animation Hong Kong Limited (“TDAHK”) and Top Draw Animation, Inc (“Top Draw” or “TDA”). The group’s principal activities, based in Manila, Philippines, are the production of animated films. |

| · | Grom Educational Services, Inc. (“GES”), formed in February 2017, is a Florida corporation through which we operate our NetSpective Webfiltering services that we provide to schools and libraries. |

| · | Grom Nutritional Services, Inc. (“GNS”) is a Florida corporation formed in April 2017 through which we intend to market and distribute four flavors of a nutritional supplement to children. |

| · | Illumination America Lighting, Inc. (“IAL”), which operates our LED lighting business that was formerly Illumination, was our principal business prior to the Grom Holdings acquisition. |

Apart from IAL, all of our subsidiary companies have been acquired or formulated with the goal of operating profitably as well to ultimately increase the number of users, through synergistic activities on our Grom Social website. We believe we will be successful in increasing our user base and that this will enhance our ability to generate significant future revenue by monetizing this user database, although there can be no assurances.

| 2 |

Grom Social

Grom Social is a social media company for kids focused on producing original content and generating revenue from our website and synergistic subsidiary companies. Although we have only generated minimal revenue to date, our core business is our Grom Social media website for children, which we refer to as “Grom Social.” The concept for Grom Social was developed in 2012, by Zach Marks, who was 12 years old at the time and is the son of our Chairman and Chief Executive Officer, Darren Marks.

The name “Grom,” is derived from Australian surfing slang, and is defined by us to mean “a promising young individual who is quick to learn.” Visitors to our Grom Social website located at www.gromsocial.com may log on via mobile phone, desktop computer or tablet and chat with friends, view original content or play games created by us.

Grom Social’s business model is based upon providing children ages five through 16 with a safe environment on the Internet while promoting “fun,” “wholesomeness” and “family values.” Since inception, we have generated in excess of 7.0 million users, in over 200 countries and territories. We define a "user" as any child between the ages of 5 and 16 who sign up for a Grom Social account. We require that each child receive parental approval to gain full access to the Grom Social platform. In certain jurisdictions and circumstances, we allow parents, teachers, and guardians (collectively, “parents”) to sign up groups of children at one time. As a result, we have a grand total in excess of 14.0 million individuals in our database that we can contact and potentially monetize in the future, although there can be no assurances.

We communicate with our database both actively, through email and a parent portal; and passively, through messaging on the child’s profile page and through seventeen unique Grom characters. Additionally, we have the ability to communicate with users and parents regardless of where they may be navigating on our Grom Social website. We have established the following safeguards and procedures to ensure that above all else, Grom Social is a safe place for children:

| · | Account Approval: We have set up our account creation procedures to help ensure that only children between the ages of five and 16 can create an account on Grom Social. According to our procedures, if a child submits a request to open an account on Grom Social, we send a notification to his or her parents by email that their child has applied to create a Grom Social account. If the child’s parents approve the account, by using one of three methods that are approved by the Children's Online Privacy Protection Act, or COPPA, guidelines, the account is opened. If a parent’s approval is not given, the account will not be opened, and the child will have limited access to the Grom Social website. |

| · | Parental Involvement: By requiring parental approval to for a child open an account and to enable the child to interact with other users on Grom Social, we hope to ensure that the parents are aware of and involved with Grom Social and their child’s activity on the site. Further, we believe that parental involvement provides us with the ability to market products and services to parents. |

| · | Content Monitoring: We have software that monitors posts for inappropriate content using standard “key word” filter technology. If a post contains inappropriate content, it will not appear on the website and the poster will be sent a warning about offensive content. We believe that through monitoring content we can promote social responsibility and digital citizenship. |

| · | Anti-bullying: We have software that monitors Grom Social for bullying. In addition to monitoring the interaction between children on the website, we also post messages on Grom Social that strongly emphasizes anti-bullying and actively promotes social responsibility and digital citizenship. Additionally, our website has received the “KidSafe Seal of Approval”. The kidSAFE Seal Program is an independent safety certification service and seal-of-approval program designed exclusively for children-friendly websites and technologies, including online game sites, educational services, virtual worlds, social networks, mobile apps, tablet devices, connected toys, and other similar online and interactive services. |

| · | Use of “Gromatars”: Children on Grom Social create animated pictures, which we call “Gromatars,” to represent themselves on Grom Social without providing a real-life photo of themselves. Gromatars are viewed as profile pictures on a user’s home wall, and it’s what other user’s see when the user leaves a comment or “like” on a public page. Kids can build and customize their Gromatars by selecting over 200 different options such as the eyes, nose, hair, teeth, ears, skin color, hair style and color, etc. |

| 3 |

We believe these safeguards are a critical component of our business model. We believe that children are increasingly accessing the internet at younger and younger ages and therefore, the need for safe, age appropriate web venues for younger children to browse and interact with other children is increasing. According to statistics compiled from several sources over the past few years on GuardChild.com (“GuardChild”), an organization focused on providing software and applications to promote safe Internet browsing for children:

| · | Approximately 81% of online 9-17 old’s say they visited a social networking site in the past three months; |

| · | Approximately 41% of teens had a negative experience as a result of using a social networking site; and |

| · | Approximately 88% of teens have seen someone be “mean or cruel” to another person on a social networking site. |

Content

In addition to providing a safe, social media platform for children to interact with their peers, we create our own content for Grom Social consisting of animated characters we created, interactive chats, videos, blogs, and games only available on Grom Social. We believe that the content that we produce for Grom Social meets our goals of providing wholesome family entertainment.

According to Google Analytics, as of November 2016, the average online duration of an Internet user is approximately 18 minutes. Based upon the login statistics for Grom Social, the average online duration of users logged onto Grom Social is approximately 50.4 minutes. We believe the longer duration time is a result of our ability to better engage users through our original content.

Monetizing strategy

Since Grom Social’s inception in 2012 through the date of this Annual Report, we have been focused on growing our user base and in developing original content, technology, branding and marketing the “Grom” name. As a result of our focus on growing our user base instead of monetizing advertisements or subscription programs, Grom Social generated less than $20,000 in revenues in 2017.

While no assurances can be provided, we believe we now have the infrastructure, tools and access to funding to begin to generate meaningful revenues from Grom Social. We hope to generate revenues from Grom Social from the following sources:

| · | Subscription Based Premium Content. We are continuously making software upgrades which will enable us to offer premium “VIP” content to users for which they will be charged a monthly subscription fee. Users that sign up for this VIP program will become Grom Club Members. We expect to be able to offer Grom Club Memberships during the fourth quarter of 2018. Grom Club Members will be able to: |

| Ø | Create and view interactive videos they can share with other Grom Club Members, with non-paying Grom users and with any other third parties; |

| Ø | Receive exclusive Gromatar options and accessories; |

| Ø | Have unlimited access to premium games; |

| Ø | Receive free monthly desktop screen savers and animated gifts; |

| Ø | Engage in exclusive chats with athletes; |

| Ø | Collaborate with Zach and other Grom Club Members with similar interests to create new Grom Social features; |

| 4 |

| Ø | Earn and collect “Grom Coin Packages” that can be used to purchase merchandise, play games or purchase other exclusive content on the Grom Social website. Grom Club Members will earn Grom Coin Packages by participating in activities on Grom Social; and |

| Ø | Receive discounts on Grom merchandise. |

| · | Advertising Revenue. We believe the growing size of our database of children and parents will attract several high-profile companies to advertise on our Grom Social website and mobile platforms. In addition, we intend to emphasize to advertisers what we believe is the unique level of parental involvement on Grom Social. We have been approached by numerous entities to advertise on the Grom Social website and have one program in early non-revenue testing. We expect to enter into an agreement with an advertiser during the third quarter of 2018 and intend to charge each advertiser a fee and/or commission to advertise a particular brand/product or service on our platforms. |

| · | Longer Term Revenue Opportunities. In addition to the foregoing near term initiatives, we expect to add the following features to Grom Social to generate revenue: |

| Ø | Online Game Fees. The games currently available to users on Grom Social are free. We intend to offer Grom Social users an option to pay to play exclusive games and/or pay for game upgrades. These games may be developed by us, such as Grom Skate or obtained from outside developers, and adapted to use on Grom Social. |

| Ø | Licensing Merchandise Revenue. We believe we will generate merchandise revenue when members purchase Grom apparel and other goods through our website and mobile app. We also anticipate entering into Grom licensing and merchandise agreements. |

TD Holdings

TD Holdings which has been in business for nineteen years, conducts its operations through its subsidiary companies, TDAH and TDA. The group’s principal activities, based in Manila, Philippines, are the production of 30-minute animated films.

TDA is a full-service production and pre-production studio working with leading international clients. TDA specializes in producing 2D digital animation production services for series and movies, primarily for international television markets. TDA provides its services on a contract for services basis or under co-production arrangements.

For pre-production TDA produces story boards, location design, model and props design, background color and color styling. For production TDA focuses on library creation, digital asset management, background layout scene assembly, posing, animation and after effects. TDA is recognized by producers and broadcasters as a provider of quality television animation and currently provides services to many high-profile properties, including Tom and Jerry, My Little Pony and Disney Animation’s Penn Zero: Part-Time Hero. TDA produces over two hundred half hour segments of animated content for television annually, which we believe makes it one of the top producers of animation for television anywhere in the world today.

Here is a listing of some of TDA’s notable projects over the past few years:

| Captain Flinn and the Pirate Dinosaurs | 7 x 22 minutes | SLR Productions | |

| Looped | 3 x 22 minutes | DHX Media | |

| Exchange Student Zero | 13 x 22 minutes | Cartoon Network Asia | |

| Transformers: Rescue Bots | 14 x 22 minutes | DHX Media | |

| Julius Junior II | 17 x 11 minutes | Brain Power Studio | |

| My Little Pony | 26 x 22 minutes | DHX Media | |

| My Little Pony - Equestrian Girls | 85 minutes | DHX Media | |

| Guess How Much I Love You | 24 x 11 minutes | SLR Productions | |

| Littlest Pet Shop | 25 x 22 minutes | DHX Media | |

| Peabody & Sherman | 4 x 11 minutes | DHX Media | |

| Supernoobs | 26 x 22 minutes | DHX Media | |

| Jamie's Got Tentacles | 47 x 11 minutes | Samka Productions | |

| Umigo 5 | 4 x 7 minutes | Wild Brain Entertainment | |

| Titeuf | 78 x 7 minutes | Go-N Productions | |

| Tom and Jerry | 15 x 7 minutes | Slap Happy Cartoons |

| 5 |

Recent Developments

Acquisition Strategy

During 2016 and 2017 we made several significant acquisitions. Our acquisition strategy is to acquire synergistic companies, products or intellectual property that will help grow our Grom Social user base and also will become profitable as a stand-alone enterprise or division within the company without the benefit of intercompany. In that regard, during 2016 and 2017 we made four acquisitions that meet those criteria:

Acquisition of TD Holdings Limited

On July 1, 2016, we acquired 100% of the capital stock of TD Holdings, which is incorporated in Hong Kong. Its operations are conducted through its subsidiary companies, TDAHK and TDA. The group’s principal activities, based in Manila, Philippines, are the production of animated films. TDA is a full-service production and pre-production studio working with leading international clients.

In connection with our acquisition of TD Holdings, we paid $4,000,000 in cash, issued a 5% Promissory Note, in the principal amount of $4,000,000 (the “Note”) to the selling shareholders of TDA (“TDA Sellers”) maturing on July 1, 2018. Additionally, we issued 7,367,001 shares of our restricted common stock to the TDA Sellers valued at $4,240,000, or approximately $0.58 per share. Wayne Dearing, the founder and CEO of TD Holdings, and currently one of our executive officers was a 50% owner of TD Holdings. Accordingly, he received 50% of the purchase consideration that we paid (described above).

Additionally, under the terms of the acquisition, Grom is required to make additional payments to the TDA Sellers, up to a maximum of $5,000,000 (“Earnout Payments”), if TD Holdings achieves certain adjusted earnings before interest, taxes, depreciation and amortization (“EBITDA Targets”) during the three-year period following the acquisition (the “Earnout Period”). The Earnout Payments, if any, will be paid 25% in cash and the balance in shares of common stock. The number of shares issuable shall be determined by using a share price equal to the lower of a 10% discount to our last private placement price per share prior to making the Earnout Payment, to a bona fide investor, and priced at arm’s length; or if the Buyer Shares are listed on a recognized stock exchange and publicly traded and not suspended, at a 10% discount to the previous 20 day weighted average closing price per share.

The applicable EBITDA Targets and Earnout Payments for each of the three years during the Earnout Period are as follows:

| EBITDA Target | Earnout Payment |

| $2,400,000 | $1,666,667 |

| $3,700,000 | $3,333,333 |

In the event that TD Holdings achieves an EBITDA in an Earnout Year greater than $2,400,000 but less than $3,700,000, the Earnout Payment is calculated by multiplying $3,333,333 by the sum of “A” divided by “B” where:

“A” equals the sum of $3,700,000 less the EBITDA earned; and

“B” equals $1,300,000 (being the difference between $2,400,000 and $3,700,000).

The foregoing notwithstanding, in the event that TD Holding’s EBITDA in any 12-month period during the Earnout Years is equal to or greater than $3,700,000, the full amount of the Earnout Payment will be paid one month after that EBITDA Target is achieved and no further Earnout Payments shall be made.

No earn out was achieved for the years ended December 31, 2017 and December 31, 2016.

| 6 |

We believe that TDA not only provides us with an important source of revenue, it also provides us with a source for animated content for Grom Social and for original shows that can be viewed on Grom Social. Although there can be no assurances that we will be successful in creating this animated content.

On January 3, 2018, we entered into an amendment to the acquisition agreement with the TDA Sellers (the “Amendment”):

| · | The TDA Sellers agreed to extend the maturity date of the Note one year until July 1, 2019; |

| · | The interest rate on the Note during the one-year extension period from July 2, 2018 to July 1, 2019 was changed to 10%. The interest rate on the Note remained at 5%, payable annually in arrears, until June 30, 2018; |

| · | During the one-year extension period, the interest will be paid quarterly in arrears, instead of annually in arrears. The first such quarterly interest payment of $100,000 is due on September 30, 2018; and |

| · | Under the terms of the terms acquisition agreement, the Sellers had an opportunity to earn up to $5.0 million in contingent Earnout Payments (as describe above). The original Earn out measurement period ended on December 31, 2018. As part of the consideration for the Sellers agreeing to enter the Amendment, we agreed to extend the Earnout Period, one year, to December 31, 2019. |

Also on January 3, 2018 as additional consideration, we issued an additional 800,000 restricted shares of our common stock to the TDA Sellers.

Acquisition of the MamaBear Mobile Software Application Assets of GeoWaggle, LLC (“MamaBear”)

On September 30, 2016, we purchased an online application and website called “MamaBear” for 208,500 shares of our common stock valued at approximately $162,500, or approximately $0.78 per share. By using MamaBear, a parent can follow and protect their child’s online presence by monitoring their social networking/media accounts, including, Facebook, Instagram, Twitter and YouTube. MamaBear is intended to generate revenue through a paid subscription and advertising model. To date, the revenue generated by the MamaBear safety application has been nominal. On April 2, 2018, we launched an upgraded and enhanced version of the MamaBear application. We believe this upgrade will help generate significant revenue from this application although there can be no assurances.

Acquisition of the NetSpective Webfilter Assets and Software from TeleMate.net

On January 1, 2017, we acquired the assets of NetSpective Webfilter (“NetSpective”), a division of TeleMate.net Software (“Telemate”). NetSpective sells proprietary Internet filtering software to over 3,700 schools and more than over 2 million children and generates revenue through a subscription model. NetSpective products comply with The Children's Internet Protection Act, or CIPA, which requires that K-12 schools and libraries in the United States use Internet filters and implement other technology protection measures to protect children from harmful online content as a condition for federal funding.

Under the terms of the agreement, we paid $1,000,000 in consideration in the form of a $1,000,000 redeemable, convertible promissory note. The note bears interest at 0.68% per annum. All note principal and accrued interest is payable January 1, 2020. The note is convertible at the election of the sellers (the “Telemate Sellers”) into the Company’s common stock at a conversion rate of $0.78 per share. Furthermore, if not previously converted by the Sellers, the note may be converted by the Company into shares of the Company’s common stock at a rate of $0.48 per share commencing on November 1, 2019.

Additionally, the Telemate Sellers had the opportunity to achieve an earn-out payment of up to $362,500, payable 100% in our restricted common stock at a price of $0.78 per share or 464,744 shares, if NetSpective generated $362,500 in “net cash flow” as defined by the agreement during the one-year post-closing period ending December 31, 2017. The earn-out payments, if achieved, shall be payable entirely in common stock at the rate of $0.78 per share. During the year ended December 31, 2017, the cash flow threshold necessary for Telemate to receive the full $362,500 earn out was achieved by NetSpective. However, TeleMate failed to remit $146,882 it had collected on our behalf from NetSpective customers. As a result of TeleMate’s non-payment and to avoid litigation, on January 12, 2018 we entered into a First Modification to the Purchase and Sale Agreement (the “Modification”).

| 7 |

Under the terms of the Modification, the TeleMate Sellers agreed to the following terms:

| · | To pay us $10,000 per month against their outstanding balance of $146,822. To date they have paid us $20,000 and are current on their monthly payment obligations. |

| · | They cannot exercise the conversion feature of their $1.0 million promissory note, nor will any of the $362,500 Earnout shares (464,744 shares) be issued, until the outstanding balance is paid in full, by TeleMate. |

| · | The December 31, 2019 maturity date of the promissory is extended indefinitely until all payments are made in full. |

| · | All interest payments ($6,800 annually) due from the Company to the TeleMate Sellers was suspended indefinitely until all payments are made in full. |

Finally, assuming all payments are made and the TeleMate Sellers decide to exercise the conversion feature of their promissory note, they are now bound by a leakout agreement which will limit for a one-year period the amount of shares they can register for sale on a monthly basis

Acquisition of the Assets of Fyoosion LLC

On December 27, 2017, we consummated the acquisition of all of the assets of Fyoosion LLC, a Delaware limited liability company (“Fyoosion”), which assets included goodwill, cash, accounts receivable, prepayments, patents, trademarks, source code, hardware appliances as well as all other documentation, processes, equipment and know how necessary to operate the seller’s business in a manner similar to its current operations.

Fyoosion’s proprietary software utilizes a digital automation marketing platform for businesses of all types to enable companies to efficiently generate sales leads and improve customer retention. We intend to use this marketing software with all our existing businesses and to create new opportunities outside our current scope of business.

In consideration for these assets we issued an aggregate of 300,000 shares of our common stock. These shares are subject to a leakout agreement limiting the number of shares that can be sold during the one-year period following the date of the agreement to 25% of the daily average trading volume during the period prior to such sale. The agreement also provides that up to an additional 200,000 shares of our “restricted” common shares can be earned and will become payable to Fyoosion or its assigns only if the proposed business utilizing the Assets attains $125,000 in pre-tax earnings before interest, taxes, depreciation and amortization (“EBITDA”) calculated using generally accepted accounting principles (“GAAP”) for the one-year period post-closing. This calculation shall be based upon Fyoosion stand-alone performance excluding any of our intercompany revenue and expense and will not include any corporate fees or charges.

Business Strategy

In 2017 and 2016, we generated net sales of $8.3 million and $3.8 million, respectively. Substantially all of our growth from 2016 to 2017 came from acquisitions.

We intend to continue grow our business through a combination of aggressive marketing initiatives and synergistic acquisitions through which we can increase our Grom Social user base to a large enough size to enable us to attract advertisers and paid users for our VIP content. Additionally, as described in this Annual Report, in December 2017 we consummated the acquisition of Fyoosion which utilizes proprietary software and marketing applications for businesses of all types to enable companies to efficiently generate sales leads and improve customer retention. We intend to use this marketing software with all our existing businesses and to create new revenue opportunities outside our current scope of business. Additionally, we intend to use other methods such as direct sales calls, industry and other trade shows along with other methods. There can be no assurance that our strategy will result in additional revenues.

| 8 |

Our Growth Strategy

Our growth strategy is as follows:

· Increase the size of our database of user at Grom Social. Comparable to other successful social media companies, we believe the key strategy to our future success is to grow the size of our database. Although the revenue from Grom Social is now nominal, the database continues to grow due to our production of original content and through synergies from our subsidiary companies. For example, at GES our MamaBear application has in excess of 800,000 downloads since inception; and our web filtering products are being used by over 2.0 million K-12 students each year. We are in the process of making these users aware of the Grom social website. There can be no assurance that we can continue to grow the Grom website and that if we are successful in doing so, we will be able to generate significant revenues from the site.

· Expand Core Products. We manage our existing and new brands through strategic product development initiatives, including introducing new products and by modifying existing intellectual property. Our marketing teams and development team strive to develop enhanced products to offer added technological, aesthetic and functional improvements to our portfolio of products.

· Pursue Strategic Acquisitions. We supplement our internal growth with selected strategic and synergistic acquisitions.

· Capitalize on Our Operating Efficiencies. We believe that our current infrastructure and operating model can accommodate growth without a proportionate increase in our operating and administrative expenses, thereby increasing our operating margins.

The execution of our growth strategy, however, is subject to several risks and uncertainties and we cannot assure you that we will continue to experience growth or maintain our present level of net sales. For example, our growth strategy will place additional demands upon our management, operational capacity and financial resources and systems. The increased demand upon management may necessitate our recruitment and retention of additional qualified management personnel. We cannot assure you that we will be able to recruit and retain qualified personnel or expand and manage our operations effectively and profitably. To effectively manage future growth, we must continue to expand our operational, financial and management information systems and to train, motivate and manage our work force. While we believe that our operational, financial and management information systems will be adequate to support our future growth, no assurance can be given they will be adequate without significant investment in our infrastructure. Failure to expand our operational, financial and management information systems or to train, motivate or manage employees could have a material adverse effect on our business, financial condition and results of operations. See Risk Factors on page 14 of this Annual Report.

Seasonality

We believe that seasonality does not have any impact on our operations.

Competition

Grom Social

We believe that the markets in which we compete are characterized by innovation and new and rapidly evolving technologies. We believe we will face significant and intense competition in every aspect of our intended business, including from Facebook, YouTube, Twitter and Google, which offer a variety of Internet products, services, and content, that will compete for our users Internet time and spending dollars. In addition to facing general competition from these large, well-funded companies, we also face completion from smaller Internet companies that offer products and services that may compete directly with Grom Social for users, such as Yoursphere, Fanlala, Franktown Rocks, Facebook and Sweety High and others. Additionally, as we introduce new services and products, as our existing services and products evolve, or as other companies introduce new products and services, we may become subject to additional competition from:

| · | Companies that offer products that replicate either partial or the full range of capabilities we intend to provide. |

| 9 |

| · | Companies that develop applications, particularly mobile applications, that provide social or other communications functionality, such as messaging, photo-and video-sharing, and micro-blogging. |

| · | Companies that provide web-and mobile-based information and entertainment products and services that are designed to engage our target audience and capture time spent on mobile devices and online. |

Many of these companies have substantially greater resources than us.

We believe that the following features differentiate us from our competitors and provide us with a possible competitive advantage with respect to our target market:

| · | We provide children with a social media experience in a safe and controlled environment; |

| · | We encourage significant direct parental involvement and oversight; |

| · | We produce content developed by “kids and for kids”; |

| · | We have developed a very comprehensive registration process to safely register children on the site; |

| · | We provide 24/7 live monitoring of the Grom Social website by trained individuals to help protect children from malicious content found on other social networking sites available to children, supplemented by standard “bad word” filtering software; and |

We believe that Grom Social is one of the only, if not the only, Internet platform that offers games, chatrooms, educational services, social interaction, exclusive content, global connectivity and group collaboration to develop new content and activities based on user behavior in one platform.

TD Holdings

We have extensive competition in our animation business coming from Korea, Canada, India, Ireland and to a lesser degree, China, Malaysia, Singapore and Thailand. A number of these territories are government subsidized which sometimes makes it difficult to compete due to artificially low pricing levels. Also, the U.S. market has traditionally had a love affair with Korea and continues to for its branded properties.

We expect that TDA’s digitally animated features will compete with family-oriented, animated and live action feature films and other family-oriented entertainment products produced by major movie studios, including Disney, DreamWorks Animation SKG, Inc., Warner Bros. Entertainment, Sony Pictures Entertainment, Fox Entertainment Group Inc., Paramount Pictures, Lucasfilm Ltd., Universal Studios, Inc., MGM/UA, and Studio Ghibli as well as numerous other independent motion picture production companies.

The primary competitors of TD Holdings within the Philippines are Toon City, Animation, Snipple Animation Studio and Synergy 88 Digital. Another significant competitor is Mercury Filmworks in Canada.

The competitive environment in the television industry has changed significantly over the past few years following the deployment of digital set-top boxes, the launch of numerous new television networks and the resulting fragmentation of the market. Competition is based primarily on consumer preferences and extends to the Company’s ability to generate and otherwise acquire popular entertainment and trademark properties and secure licenses to exploit, and effectively distribute and market, such properties.

| 10 |

Grom Educational Services

iBoss, Lightspeed and Securly are the main webfiltering competitors. There are other larger companies that have web filtering as a part of the larger product offering: Forcepoint (Websense), Bluecoat, Palo Alto Networks, Barracuda, Cisco, etc. All of the larger companies are enterprise focused where they sell numerous products, and filtering is a minimal part of their portfolio.

Grom Nutritional Services

Consumer awareness regarding the benefits of dietary supplements and new product availability are the major drivers for the market world-wide. The nutritional supplements markets is an extremely competitive market estimated to be a $175 billion global market by 2020 according to the FN Media Group LLC. The largest companies in this space are Axxess Pharma Inc., Celsius Holdings, Inc., GNC Holdings Inc. and Pfizer Inc.

Illumination America Lighting

Since we are only a distributor of lighting products and do not do any manufacturing, we currently face very intense competition from both traditional lighting companies that provide general lighting products, including incandescent, fluorescent, high intensity discharge (HID), metal halide (MH) and neon lighting. We also have competitors from specialized lighting companies that are engaged in providing LED products. In general, we compete with both groups on the basis of our design, quality of light provided, maintenance costs, safety issues, energy consumption, price, product quality and brightness. Additionally, there are thousands of electrical contractors and lighting distributors of varying scales that install and distribute LED lighting products

Government Regulation

We are subject to several U.S. federal and state and foreign laws and regulations that affect companies conducting business on the Internet. Many of these laws and regulations are still evolving and being tested in courts and could be interpreted in ways that could harm our business. These may involve user privacy and data protection, rights of publicity, content, intellectual property, advertising, marketing, distribution, data security, data retention and deletion, personal information, electronic contracts and other communications, competition, protection of minors, consumer protection, telecommunications, product liability, taxation, economic or other trade prohibitions or sanctions, securities law compliance, and online payment services. In particular, we are subject to federal, state, and foreign laws regarding privacy and protection of people's data. Foreign data protection, privacy, and other laws and regulations can be more restrictive than those in the United States. U.S. federal and state and foreign laws and regulations, which in some cases can be enforced by private parties in addition to government entities, are constantly evolving and can be subject to significant change. In addition, the application, interpretation, and enforcement of these laws and regulations are often uncertain, particularly in the new and rapidly-evolving industry in which we operate and may be interpreted and applied inconsistently from country to country and inconsistently with our current policies and practices. There are also a number of legislative proposals pending before federal, state, and foreign legislative and regulatory bodies, including a data protection regulation that is pending final approval by the European legislature that may include operational requirements for companies that receive personal data that are different than those currently in place in the European Union, and that will include significant penalties for non-compliance. In addition, some countries are considering or have passed legislation implementing data protection requirements or requiring local storage and processing of data or similar requirements that could increase the cost and complexity of delivering our services.

Our website follows the guidelines of the Children's Online Privacy Protection Act of 1998, 15 U.S.C. 6501–6505. COPPA imposes certain requirements on operators of websites or online services directed to children under 13 years of age, and on operators of other websites or online services that have actual knowledge that they are collecting personal information online from a child under 13 years of age.

Additionally, we are subject to CIPA, which was enacted by Congress in 2000 to address concerns about children's access to obscene or harmful content over the Internet. CIPA imposes certain requirements on schools or libraries that receive discounts for Internet access or internal connections through the E-rate program – a program that makes certain communications services and products more affordable for eligible schools and libraries. In early 2001, the FCC issued rules implementing CIPA and provided updates to those rules in 2011.

| 11 |

Intellectual Property

To establish and protect our proprietary rights we rely on a combination of trademarks, copyrights, trade secrets, including know-how, license agreements, confidentiality procedures, non-disclosure agreements with third parties, employee non-disclosure and invention assignment agreements, and other contractual rights. We do not believe that our proprietary website is dependent on any single copyright or groups of related patents or copyrights. We currently own 12 trademarks with two applications pending.

Grom Social, Inc. - Trademark Status Report (Grouped by Date)

Prepared by McHale & Slavin, P.A.

| Client ID | Country | Mark | Status | Class | Class 2 | Class 3 | Serial No | Filing Date | Reg No | Reg Date | Owner Name | Desc | Due Date | ||||||||||

| 4186U.000025 | United States | LIGHT BULB DESIGN | Pending Application | 006 | 87416574 | 04/19/2017 | mm/dd/yyyy | Grom Social, Inc. (FL Corp.) | NOA - SOU/1st EXT Due | 04/24/2018 | |||||||||||||

| 4186U.000023 | United States | JUST BRILLIANT | Pending Application | 032 | 87094908 | 07/06/2016 | mm/dd/yyyy | Grom Social, Inc. (FL Corp.) | NOA - SOU/2nd EXT Due | 05/09/2018 | |||||||||||||

| 4186U.000001 | United States | GROM SOCIAL | Registered | 045 | 85562637 | 03/07/2012 | 4236835 | 11/06/2012 | Grom Social LLC | 8&15 (6th yr) Due | 11/06/2018 | ||||||||||||

| 4186U.000003 | United States | Grom Social and Design (2) (in color) |

Registered | 045 | 85632192 | 05/22/2012 | 4242103 | 11/13/2012 | Grom Social LLC | 8&15 (6th yr) Due | 11/13/2018 | ||||||||||||

| 4186U.000012 | United States | GROMARAMA5 | Registered | 041 | 85865718 | 03/04/2013 | 4380377 | 08/06/2013 | Grom Social, LLC | 8&15 (6th yr) Due | 08/06/2019 | ||||||||||||

| 4186U.000013 | United States | GROMHERO | Registered | 041 | 85865868 | 03/04/2013 | 4380379 | 08/06/2013 | Grom Social, LLC | 8&15 (6th yr) Due | 08/06/2019 | ||||||||||||

| 4186U.000011 | United States | GROMPOUND | Registered | 041 | 85865569 | 03/04/2013 | 4380376 | 08/06/2013 | Grom Social, LLC | 8&15 (6th yr) Due | 08/06/2019 | ||||||||||||

| 4186U.000005 | United States | GROM-ATAR | Registered | 042 | 85808094 | 12/20/2012 | 4379762 | 08/06/2013 | Grom Social LLC | 8&15 (6th yr) Due | 08/06/2019 | ||||||||||||

| 4186U.000008 | United States | GROMSTER | Registered | 042 | 85808663 | 12/21/2012 | 4464934 | 01/14/2014 | Grom Social LLC | 8&15 (6th yr) Due | 01/14/2020 | ||||||||||||

| 4186U.000007 | United States | GROMETTE | Registered | 042 | 85808250 | 12/20/2012 | 4464932 | 01/14/2014 | Grom Social LLC | 8&15 (6th yr) Due | 01/14/2020 | ||||||||||||

| 4186U.000006 | United States | GROM | Registered | 042 | 85808178 | 12/20/2012 | 4464931 | 01/14/2014 | Grom Social LLC | 8&15 (6th yr) Due | 01/14/2020 | ||||||||||||

| 4186U.000009 | United States | GROM-A-TRON | Registered | 042 | 85808653 | 12/21/2012 | 4464933 | 01/14/2014 | Grom Social LLC | 8&15 (6th yr) Due | 01/14/2020 | ||||||||||||

| 4186U.000017 | United States | SOLAR SKATE | Registered | 009 | 86218046 | 03/11/2014 | 4646714 | 11/25/2014 | Grom Social, Inc. | 8&15 (6th yr) Due | 11/25/2020 | ||||||||||||

| 4186U.000018 | United States | TECHTOPIA | Registered | 009 | 86346608 | 07/24/2014 | 4820748 | 09/29/2015 | Grom Social, Inc. | 8&15 (6th yr) Due | 09/29/2021 |

Employees

Grom Social and its subsidiaries, excluding TDH, has 20 full-time employees including our executive officers, and 7 part-time employees in the United States. TDA has approximately 500 full time employees and one executive officer in the Philippines and is expected to add approximately 50-100 more full-time employees during 2018 to address current business opportunities.

| 12 |

ITEM 1A. RISK FACTORS

Risks Related to our Business

Our future performance will depend on the continued engagement of key members of the management team of the Company.

Our future performance depends to a large extent on the continued services of members of the Company’s current management and other key personnel, including Zach Marks. While we have employment agreements with Messrs. Marks, Dearing, and Leiner, the failure to secure the continued services of these or other key personnel for any reason, could have a material adverse effect on our business, operations and prospects. We currently do not carry “key man insurance” on any of our executives.

If we fail to retain existing users or add new users, or if our users decrease their level of engagement with Grom, our revenue, financial results, and business may be significantly harmed.

The size of our user base and our users’ level of engagement are critical to our success. Since inception, we have approximately 7,000,000 Grom Social users between the ages of five and 16 as well as an additional equal number of parents, teachers and guardians in our database as of April 1, 2018. Our future financial performance will be significantly determined by our success in adding, retaining, and engaging users. If people do not perceive our site and the content that we offer to be enjoyable, engaging, reliable, and trustworthy, we may not be able to attract or retain users or otherwise maintain or increase the frequency and duration of their interaction on our site. A number of other social networking companies that achieved early popularity have since seen their active user bases or levels of engagement decline, in some cases precipitously. There is no guarantee that we will not experience a similar erosion of our user base or engagement levels. A decrease in user retention, growth, or engagement could render Grom less attractive to developers and advertisers, which may have a material and adverse impact on our revenue, business, financial condition, and results of operations. Any number of factors could potentially negatively affect our ability to attract and retain user and to increase their engagement on the site, including, but not limited to, if:

| • | our users decide to spend their time on competing sites; |

| • | we fail to introduce new and improved content or if we introduce new content or services that are not favorably received; |

| • | we are unable to successfully balance our efforts to provide a compelling user experience with the decisions we make with respect to the frequency, prominence, and size of ads and other commercial content that we display; |

| • | we are unable to continue to develop products for mobile devices that users find engaging, that work with a variety of mobile operating systems and networks, and that achieve a high level of market acceptance; |

| • | there are changes in user sentiment about the quality or usefulness of our products or concerns related to privacy and sharing, safety, security, or other factors; |

| • | we are unable to manage and prioritize information to ensure users are presented with content that is interesting, useful, and relevant to them; |

| • | there are adverse changes in our products that are mandated by legislation, regulatory authorities, or litigation, including settlements or consent decrees; |

| • | technical or other problems prevent us from delivering our products in a rapid and reliable manner or otherwise affect the user experience; |

| • | we adopt policies or procedures related to areas such as sharing or user data that are perceived negatively by our users or the general public; or |

| • | we fail to provide adequate customer service to users, developers, or advertisers; |

| 13 |

If we are unable to maintain and increase our user base and user engagement, our revenue, financial results, and future growth potential may be adversely affected.

Our strategy at Grom Social to create new and original content could fail to attract or retain users or generate revenue.

Our ability to retain, increase, and engage our user base and to increase our revenue will depend heavily on our ability to create successful new content, both independently and in conjunction with third parties. If new or enhanced content fails to engage users, developers, or advertisers, we may fail to attract or retain users or to generate sufficient revenue, operating margin, or other value to justify our investments, and our business may be adversely affected. In the future, we may invest in new products and initiatives to generate revenue, but there is no guarantee these approaches will be successful. If we are not successful with new approaches to monetization, we may not be able to maintain or grow our revenue as anticipated or recover any associated development costs, and our financial results could be adversely affected.

If we are not able to maintain and enhance our brand, or if events occur that damage our reputation and brand, our ability to expand our user base may be impaired, and our business and financial results may be harmed.

We also believe that maintaining and enhancing the Grom Social brand is central to expanding our base of users and advertisers. Many of our new users are referred by existing users, and therefore we strive to ensure that our users remain favorably inclined towards Grom. Maintaining and enhancing our brand will depend largely on our ability to continue to provide age appropriate, enjoyable, reliable, trustworthy, and innovative content and services, which we may not do successfully. We may introduce new content or terms of service that users do not like, which may negatively affect our brand. Additionally, the actions of third-party developers may affect our brand if users do not have a positive experience using third-party apps and websites integrated with Grom. We also may fail to provide adequate customer service, which could erode confidence in our brand. Our brand may also be negatively affected by the actions of users that are deemed to be hostile or inappropriate to other users, or by users acting under false or inauthentic identities. Maintaining and enhancing our brand may require us to make substantial investments and these investments may not be successful. If we fail to successfully promote and maintain the Grom brand or if we incur excessive expenses in this effort, our business and financial results may be adversely affected.

Our Grom Social platform may be misused by users, despite the safeguards we have in place to protect against such behavior.

Users may be able to circumvent the controls we have in place to prevent abusive, illegal or dishonest activities and behavior on our websites, and may engage in such activities and behavior despite these controls. For example, our Grom Social platform could be used to exploit children and to facilitate individuals seeking to engage in improper communications or contact with children. Such potential behavior of such users would injure our other users and would jeopardize the reputation and integrity of our Grom Social platform. Fraudulent users could also post fraudulent profiles or create false or unauthorized profiles on behalf of other, non-consenting parties. This behavior could expose us to liability or lead to negative publicity that could injure the reputation of our Grom Social platform and materially adversely affect our brand.

We could experience system failures or capacity constraints that could negatively impact our Grom Social platform and business.

Our ability to provide reliable service to our users largely depends on the efficient and uninterrupted operation of our Grom Social platform, relying on people, processes, and technology to function effectively. Any significant interruption to, failure of, or security breaches affecting, our Grom Social platform could result in significant expense, a loss of users, and harm to our business and reputation. Interruptions, system failures or security breaches could result from a wide variety of causes, including disruptions to the Internet, malicious attacks or cyber incidents such as unauthorized access, loss or destruction of data (including confidential and/or personal customer information), account takeovers, computer viruses or other malicious code, and the loss or failure of systems over which we have no control. The failure of our Grom Social platform, or the loss of data, could result in disruption to our operations, damage to our reputation and remediation costs, which could individually or in the aggregate adversely affect our business and brand.

Improper access to or disclosure of our users’ information, or violation of our terms of service or policies, could harm our reputation and adversely affect our business.

Our efforts to protect the information that our users have chosen to share using Grom Social may be unsuccessful due to the actions of third parties, software bugs or other technical malfunctions, employee error or malfeasance, or other factors. In addition, third parties may attempt to fraudulently induce employees or users to disclose information in order to gain access to our data or our users’ data. If any of these events occur, our users’ information could be accessed or disclosed improperly. Our Privacy Policy governs the use of information that users have chosen to share using Grom Social and how that information may be used by us and third parties. Some third-party developers may store information provided by our users through apps on the Grom Social platform or websites integrated with Grom Social. If these third parties or developers fail to adopt or adhere to adequate data security practices or fail to comply with our terms and policies, or in the event of a breach of their networks, our users’ data may be improperly accessed or disclosed.

| 14 |

Any incidents involving unauthorized access to or improper use of the information of our users or incidents involving violation of our terms of service or policies, including our Privacy Policy, could damage our reputation and our brand and diminish our competitive position. In addition, the affected users or government authorities could initiate legal or regulatory action against us in connection with such incidents, which could cause us to incur significant expense and liability or result in orders or consent decrees forcing us to modify our business practices. Any of these events could have a material and adverse effect on our business, reputation, or financial results.

We face intense competition in all aspects of our business including competition in the animation and webfiltering businesses. If we do not provide a features and content that will engage and attract users, advertisers and developers we may not remain competitive, and our potential revenues and operating results could be adversely affected.

We face intense competition in almost every aspect of our business, including from companies such as Facebook, YouTube, Twitter and Google, which offer a variety of Internet products, services, content, and online advertising offerings, as well as from mobile companies and smaller Internet companies that offer products and services that may compete directly with Grom Social for users, such as Yoursphere, Fanlala, Franktown Rocks and Sweety High. As we introduce new services and products, as our existing services and products evolve, or as other companies introduce new products and services, we may become subject to additional competition.

Some of our current and potential competitors have significantly greater resources and better competitive positions than we do. These factors may allow our competitors to respond more effectively than us to new or emerging technologies and changes in market requirements. Our competitors may develop products, features, or services that are similar to ours or that achieve greater market acceptance, may undertake more far-reaching and successful product development efforts or marketing campaigns, or may adopt more aggressive pricing policies. In addition, our users, content providers or application developers may use information shared by our users through Grom Social in order to develop products or features that compete with us. Certain competitors, including Facebook, could use strong or dominant positions in one or more markets to gain competitive advantage against us in areas where we operate including: by creating a social networking experience similar to ours with similar content and features. As a result, our competitors may acquire and engage users at the expense of the growth or engagement of our user base, which may negatively affect our business and financial results.

We believe that our ability to compete effectively depends upon many factors, including:

| • | the age appropriateness, attractiveness, safety, ease of use, performance, and reliability of the Grom Social platform, our content and products compared to our competitors; |

| • | the size and composition of our user base; |

| • | the engagement of our users with our products; |

| • | the timing and market acceptance of content, services and products, including developments and enhancements to our or our competitors’ content, services and products; |

| • | our ability to monetize our products, including our ability to successfully monetize mobile usage; |

| • | the frequency, size, and relative prominence of the ads and other commercial content displayed by us or our competitors; |

| • | customer service and support efforts; |

| • | marketing and selling efforts; |

| • | responding to changes mandated by legislation, regulatory authorities, or litigation, some of which may have a disproportionate effect on us; |

| 15 |

| • | acquisitions or consolidation within our industry, which may result in more formidable competitors; |

| • | our ability to attract, retain, and motivate talented employees, particularly programmers; |

| • | our ability to cost-effectively manage and grow our operations; and |

| • | our reputation and brand strength relative to our competitors. |

If we are not able to effectively compete, our user base and level of user engagement may decrease, which could make us less attractive to developers and advertisers and materially and adversely affect our revenue and results of operations.

Failure to manage our growth effectively could cause our business to suffer and have an adverse effect on our financial condition and operating results.

Failure to manage our growth effectively could cause our business to suffer and have an adverse effect on our financial condition and operating results. We have experienced significant growth in a short period of time. To manage our growth effectively, we must continually evaluate and evolve our organization. We must also manage our employees, operations, finances, technology and development and capital investments efficiently. Our efficiency, productivity and the quality of our Grom Social platform, TDA animation business and NetSpective user services and content may be adversely impacted if we do not if we fail to appropriately coordinate across our organization. Additionally, our rapid growth may place a strain on our resources, infrastructure and ability to maintain the quality of our Grom Social platform. Our failure to manage our growth could disrupt our operations and ultimately prevent us from generating the revenues we expect.

Our recent growth may not be indicative of our future growth and, if we continue to grow rapidly, we may not be able to manage our growth effectively.

Since the launch of Grom Social in November 2012, we have grown to over 7,000,000 users with membership in over 200 countries and territories. You should not consider our recent growth as indicative of future performance. We expect in the near term that our growth rate will increase, however, in the future, as our user base increases, our rate of growth will decline. In addition, we will not be able to grow as fast or at all if we do not accomplish the following:

| • | increase the number of users of our products and services, and in particular the number of unique visitors to the Grom Social website and our mobile applications; |

| • | maintain and expand our content; |

| • | further improve the quality of our existing content, products and services, and introduce high quality new content, products and services; |

| • | We may not successfully accomplish any of these objectives. We plan to continue our investment in future growth. We expect to continue to expend substantial financial and other resources on: |

| • | marketing and advertising, including a significant increase to our television advertising expenditures; |

| • | product development; including investments in our product development team and the development of new products and new features for existing products; and |

In addition, our historical rapid growth has placed and may continue to place significant demands on our management and our operational and financial resources. We have also experienced significant growth in the number of users of our platform as well as the amount of data that we analyze. As we continue to grow, we expect to hire additional personnel. Finally, our organizational structure is becoming more complex as we add additional staff, and we will need to improve our operational, financial and management controls as well as our reporting systems and procedures.

| 16 |

We collect, process, share, retain and use personal information and other data, which subjects us to governmental regulations and other legal obligations related to privacy, and our actual or perceived failure to comply with such obligations could harm our business.

A variety of federal, state and foreign laws and regulations govern privacy and the collection, use, retention, sharing and security of personal information. We collect, process, use, share and retain personal information and other user data, including information about our users as they interact with our platform, and we have a Privacy Policy concerning our use of use data on our platform. We are subject to COPPA which regulates the collection, use and disclosure of personal information from children under 13 years of age. Our Grom Social platform and our content is directed at children between the ages of five and 16 years of age.

Additionally, we are subject to CIPA, which was enacted by Congress in 2000 to address concerns about children's access to obscene or harmful content over the Internet. CIPA imposes certain requirements on schools or libraries that receive discounts for Internet access or internal connections through the E-rate program – a program that makes certain communications services and products more affordable for eligible schools and libraries. In early 2001, the FCC issued rules implementing CIPA and provided updates to those rules in 2011.

Any failure or perceived failure by us to comply with COPPA, CIPA, or other applicable privacy laws and regulations or with our Privacy Policy or any compromise of security that results in the unauthorized release or transfer of sensitive information, which may include personally identifiable information or other user data, may result in governmental enforcement actions or litigation, which could be costly to defend and may require us to pay significant fines or damages. Such failures or perceived failures could also result in public statements against us by consumer advocacy groups, our users or others, which could harm our brand and could cause our users, and their parents, to lose trust in us, which in turn could have an adverse effect on our business. Additionally, if third parties we work with, such as advertisers, vendors, content or platform providers, violate applicable laws or our policies, such violations may also put the information of our users at risk and could in turn have an adverse effect on our business.

We also are or may become required to comply with varying and complex privacy laws and regulations in multiple jurisdictions, and laws and regulations in foreign jurisdictions are sometimes more restrictive than those in the United States. For example, the European Union and its member states traditionally have taken broader views as to types of data that are subject to privacy and data protection and have imposed greater legal obligations on companies in this regard. Proposed legislation and regulations concerning data protection are currently pending at the U.S. federal and state level as well as in certain foreign jurisdictions, and this legislation may impose more stringent operational requirements on us and include significant penalties for non-compliance. In addition, the interpretation and application of privacy and data protection laws in Europe, the United States and elsewhere are still uncertain and in flux. It is possible that these laws may be interpreted and applied in a manner that is inconsistent with our practices. If so, in addition to the possibility of fines, this could result in an order requiring that we change our practices, which could have an adverse effect on our business. Complying with these laws as they evolve could cause us to incur substantial costs or require us to change our business practices in a manner adverse to our business.

As a result of our collection, retention and use of personal data, we are or may become subject to diverse laws and regulations in the United States and foreign jurisdictions mandating notification to affected individuals in the event that personal data (as defined in the various governing laws) is accessed or acquired by unauthorized persons. Complying with such numerous and complex regulations in the event of unauthorized access would be expensive and difficult, and failure to comply with these regulations could subject us to regulatory scrutiny and additional liability.

User trust regarding privacy and data security is very important to our brand and the growth of our business, and privacy or data security concerns relating to our Grom Social platform could damage our reputation and brand and deter current and potential users from using our platform, even if we are in compliance with applicable privacy and data security laws and regulations.

Users may curtail or stop their use of our Grom Social platform if our security measures are compromised, if our platform is subject to attacks that degrade or deny the ability of users to access our platform or if our member data is compromised.

Our Grom Social platform collects, processes, stores, shares, discloses and uses the information of our users and their communications. We are vulnerable to computer viruses, break-ins, phishing attacks, and attempts to overload our servers with denial-of-service and other cyberattacks and similar disruptions from unauthorized use of our computer systems. Our security measures may also be breached due to employee error, malfeasance or otherwise. Several recent, highly publicized data security breaches and denial of service attacks at other companies have heightened public awareness of this issue and may embolden individuals or groups to target our systems. Any of the foregoing could lead to interruptions, delays or platform shutdowns, causing loss of critical data or the unauthorized disclosure or use of personally identifiable or other confidential or sensitive information, such as credit card information or information about our members. If our security is compromised, we could experience platform performance or availability problems, the complete shutdown of our platform or the loss or unauthorized disclosure of confidential or sensitive information. We could be subject to liability and litigation and reputational harm, and our members may be harmed, lose confidence in us and decrease or terminate the use of our platform.

| 17 |

We also rely on certain third parties to provide critical services and to store sensitive customer information. For example, our platform is hosted using data centers operated by third parties. However, we have little or no control over the security measures implemented by these parties, and if these measures are compromised, we could be exposed to similar risks and liabilities to those described above.

Unauthorized parties may also fraudulently induce employees or members to disclose sensitive information in order to gain access to our information or the information of our members or access this information through other means. They might also abuse our systems in other ways, such as by sending spam, which could diminish or otherwise degrade the experience of our members or by compromising or gaining unauthorized access to member accounts. Because the techniques used to obtain unauthorized access, disable or degrade service or sabotage systems change frequently and are becoming increasingly sophisticated, they often are not recognized until launched against a target. Furthermore, such attacks may originate from less regulated and remote areas around the world, and we may be unable to proactively address these techniques or to implement adequate preventative measures. Any or all of these issues could negatively impact our ability to attract new members and increase engagement by existing members, cause existing members to stop using our platform or subject us to lawsuits, regulatory fines or other action or liability, thereby harming our business and operating results.

Moreover, if a high-profile security breach occurs with respect to another social media provider, our users and potential users may lose trust in the security of our platform generally, which could adversely impact our ability to retain existing users or attract new ones.

Future business acquisitions, strategic investments or alliances, if any, as well as recently completed business acquisition transactions could disrupt our business and may not succeed in generating the intended benefits and may, therefore, adversely affect our business, revenue and results of operations.

We recently completed the acquisition of our Animation Division and we may in the future explore potential acquisitions of companies or technologies, strategic investments, or alliances to strengthen our business. Acquisitions involve numerous risks, any of which could harm our business, including:

| • | our due diligence may fail to identify all of the problems, liabilities or other shortcomings or challenges of an acquired business, product or technology, including issues related to intellectual property, product quality or architecture, regulatory compliance practices, or accounting practices or employee issues; |

| • | failure to successfully integrate our recently acquired business; |

| • | diversion of management's attention from operating our business to addressing acquisition integration challenges; |

| • | we may experience difficulties in coordinating geographically disparate organizations and corporate cultures and integrating management personnel with different business backgrounds; |

| • | anticipated benefits may not materialize; |

| • | retention of employees from the acquired company; |

| • | integration of the acquired company's accounting, management information, human resources and other administrative systems; |

| • | coordination of product development and sales and marketing functions; |

| • | liability for activities of the acquired company before the acquisition, including patent and trademark infringement claims, violations of laws, commercial disputes, tax liabilities and other known and unknown liabilities; and |

| • | litigation or other claims in connection with the acquired company, including claims from terminated employees, users, former stockholders or other third parties. |

| 18 |

Failure to appropriately mitigate these risks or other issues related to such strategic investments and acquisitions could result in reducing or completely eliminating any anticipated benefits of transactions and harm our business generally. Future acquisitions could also result in dilutive issuances of our equity securities, the incurrence of debt, contingent liabilities, amortization expenses or the impairment of goodwill, any of which could harm our business, financial condition and operating results.

If any of our relationships with internet search websites terminate, if such websites' methodologies are modified or if we are outbid by competitors, traffic to our websites could decline.

We depend in part on various internet search websites, such as Google.com, Bing.com, Yahoo.com and other websites to direct a significant amount of traffic to our websites. Search websites typically provide two types of search results, algorithmic and purchased listings. Algorithmic listings generally are determined and displayed as a result of a set of unpublished formulas designed by search engine companies in their discretion. Purchased listings generally are displayed if particular word searches are performed on a search engine. We rely on both algorithmic and purchased search results, as well as advertising on other internet websites, to direct a substantial share of visitors to our websites and to direct traffic to the advertiser customers we serve. If these internet search websites modify or terminate their relationship with us or we are outbid by our competitors for purchased listings, meaning that our competitors pay a higher price to be listed above us in a list of search results, traffic to our websites could decline. Such a decline in traffic could affect our ability to generate advertising revenue and could reduce the desirability of advertising on our websites.

We may have difficulty scaling and adapting our existing network infrastructure to accommodate increased traffic and technology advances or changing business requirements, which could cause us to incur significant expenses and lead to the loss of users and advertisers.

To be successful, our network infrastructure has to perform well and be reliable. The greater the user traffic and the greater the complexity of our products and services, the more computer power we will need. We could incur substantial costs if we need to modify our websites or our infrastructure to adapt to technological changes. If we do not maintain our network infrastructure successfully, or if we experience inefficiencies and operational failures, the quality of our products and services and our users' experience could decline. Maintaining an efficient and technologically advanced network infrastructure is particularly critical to our business because of the pictorial nature of the products and services provided on our websites. A decline in quality could damage our reputation and lead us to lose current and potential users and advertisers. Cost increases, loss of traffic or failure to accommodate new technologies or changing business requirements could harm our operating results and financial condition.

We are a holding company organized in Florida, with no operations of our own, and we depend on our subsidiaries, incorporated in Hong Kong, Manila and Florida for cash to fund all of our operations and expenses, including making future dividend payments, if any.