As confidentially submitted to the Securities and Exchange Commission on February 13, 2017

This

draft registration statement has not been publicly filed with the Securities and Exchange Commission

and all information herein remains strictly confidential.

Registration No. 333-

UNITED STATES

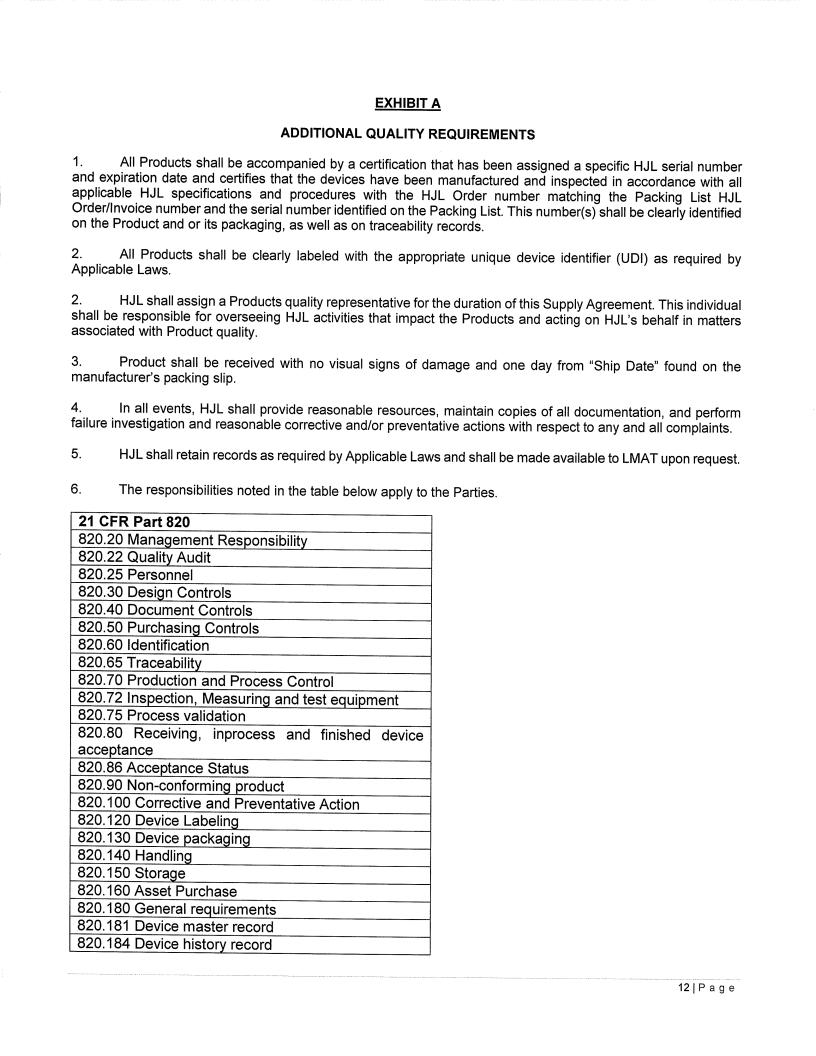

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

Hancock Jaffe Laboratories, Inc.

(Exact name of registrant as specified in its charter)

| Delaware | 3841 | 33-0936180 | ||

(State

or other jurisdiction of |

(Primary

Standard Industrial |

(I.R.S.

Employer |

70 Doppler

Irvine, California 92618

(949) 261-2900

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices)

Benedict Broennimann, M.D.

Chief Executive Officer

Hancock Jaffe Laboratories, Inc.

70 Doppler

Irvine, California 92618

(949) 261-2900

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Approximate date of commencement of proposed sale to the public:

As soon as practicable after the effective date of this registration statement.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, as amended (the “Securities Act”), check the following box. [ ]

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. [ ]

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. [ ]

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. [ ]

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | [ ] | Accelerated filer | [ ] |

| Non-accelerated filer | [ ] (Do not check if a smaller reporting company) | Smaller reporting company | [ ] |

| CALCULATION OF REGISTRATION FEE | ||||||||

| Title of Each Class of Securities to be Registered | Proposed | Amount

of Registration Fee(2) | ||||||

| Common Stock, $0.00001 par value per share | $ | $ | ||||||

| (1) | Estimated solely for the purpose of calculating the amount of the registration fee in accordance with Rule 457(o) under the Securities Act. Includes the offering price of additional shares that the underwriters have the option to purchase to cover over-allotments, if any. | |

| (2) | Registration fee will be paid when registration statement is first publicly filed under the Securities Act. |

The Registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment that specifically states that this registration statement shall thereafter become effective in accordance with section 8(a) of the Securities Act, or until the registration statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said section 8(a), may determine.

The information in this prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and it is not soliciting an offer to buy these securities in any state where the offer or sale is not permitted.

SUBJECT TO COMPLETION, DATED , 2017

PRELIMINARY PROSPECTUS

Shares

Common Stock

This is the initial public offering of our common stock. Prior to this offering there has been no public market for our common stock. We are offering shares of common stock. We currently expect the initial public offering price to be between $ and $ per share.

We intend to apply to list our common stock on the Nasdaq Capital Market, or Nasdaq, under the symbol “ .” Upon the closing of this offering, we expect to be a “controlled company” within the meaning of applicable Nasdaq corporate governance rules.

On July 22, 2016 our board of Directors approved a 2.1144-for-l forward split of our issued and outstanding shares of common stock and, on August 30, 2016, we filed the stock split with the Delaware Secretary of State. All share and per share information in this prospectus gives effect to the 2.1144-for-1 forward split.

We are an “emerging growth company” as that term is defined in the Jumpstart Our Business Startups Act of 2012 and, as such, have elected to take advantage of certain reduced public company reporting requirements for this prospectus and future filings.

Investing in our common stock involves a high degree of risk. Please read “Risk Factors” beginning on page of this prospectus.

| Per Share | Total | |||||||

| Public offering price | $ | $ | ||||||

| Underwriting discounts and commissions(1) | $ | $ | ||||||

| Proceeds to us, before expenses | $ | $ | ||||||

| (1) | We have also agreed to reimburse the underwriters for certain of their expenses. See “Underwriting” on page of this prospectus for more information about these arrangements. |

We have granted to the underwriters an option to purchase up to additional shares of common stock at the public offering price, less the underwriting discounts and commissions, for 30 days after the date of this prospectus.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or passed upon the adequacy or accuracy of this prospectus. Any representation to the contrary is a criminal offense.

Delivery of the shares of common stock is expected to be made on or about , 2017.

The date of this prospectus is , 2017

TABLE OF CONTENTS

We have not, and the underwriters have not, authorized anyone to provide any information or to make any representations other than those contained in this prospectus or in any free writing prospectus prepared by or on behalf of us or to which we have referred you. We and the underwriters take no responsibility for, and can provide no assurance as to the reliability of, any other information that others may give you. This prospectus is an offer to sell only the shares offered hereby, but only under the circumstances and in the jurisdictions where it is lawful to do so. The information contained in this prospectus or in any applicable free writing prospectus is current only as of its date, regardless of its time of delivery or any sale of shares of our common stock. Our business, financial condition, results of operations and prospects may have changed since that date.

For investors outside the United States: We have not, and the underwriters have not, done anything that would permit this offering or possession or distribution of this prospectus or any applicable free writing prospectus in any jurisdiction where action for that purpose is required, other than in the United States. Persons outside the United States who come into possession of this prospectus and any applicable free writing prospectus must inform themselves, and observe any restrictions relating to, the offering of the shares of common stock and the distribution of this prospectus outside the United States.

Through and including , 2017 (25 days after the date of this prospectus), all dealers that buy, sell or trade shares of our common stock, whether or not participating in this offering, may be required to deliver a prospectus. This delivery requirement is in addition to the obligation of dealers to deliver a prospectus when acting as underwriters and with respect to their unsold allotments or subscriptions.

We use our registered trademarks, such as VENOVALVE™, in this prospectus. This prospectus also includes trademarks, trade names and service marks that are the property of other organizations. Solely for convenience, trademarks and trade names referred to in this prospectus appear without the ® and ™ symbols, but those references are not intended to indicate, in any way, that we will not assert, to the fullest extent under applicable law, our rights or that the applicable owner will not assert its rights, to these trademarks and trade names.

| i |

| ● | ProCol® Vascular Bioprosthesis, |

| ● | Bioprosthetic Heart Valve, |

| ● | Coronary Artery Bypass Graft, Coreograft, |

| ● | Bioprosthetic Venous Valve, the VenoValve. |

| Under the current supply agreement, there is an ongoing revenue stream through sub-contract manufacturing and royalty revenue from sales of the ProCol® Vascular Bioprosthesis for hemodialysis patients with end stage renal disease, which has been approved by the U.S. Food and Drug Administration. Operations are focused on development and manufacturing of implantable cardiovascular bioprosthetic devices indicated for the treatment of medical conditions with severe and/or life-threatening disabilities. We are in the process of obtaining necessary FDA approvals to have these devices classified as Class III devices. |

| We have a strong record of regulatory and compliance conduct and operates in strict adherence to a “Quality System” motto to “develop and provide life-enhancing products and technologies in an environment where quality is the goal at every step of the process.” We maintain and preserve a strong proprietary estate of processes, validation procedures and related intellectual property. |

| We develop and foster professional relationships with respected opinion leaders. These associations have helped in formulating routes for FDA approval for our medical devices. |

| Our Products |

| Developed Products |

| ProCol® Vascular Bioprosthesis |

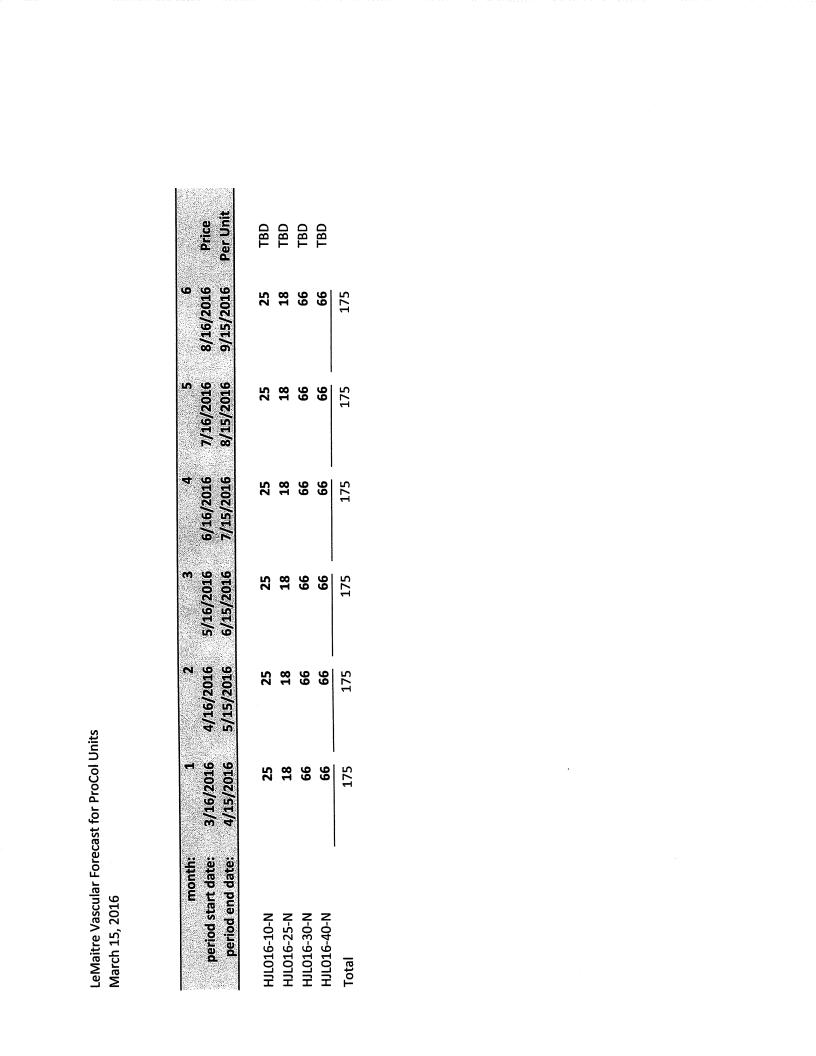

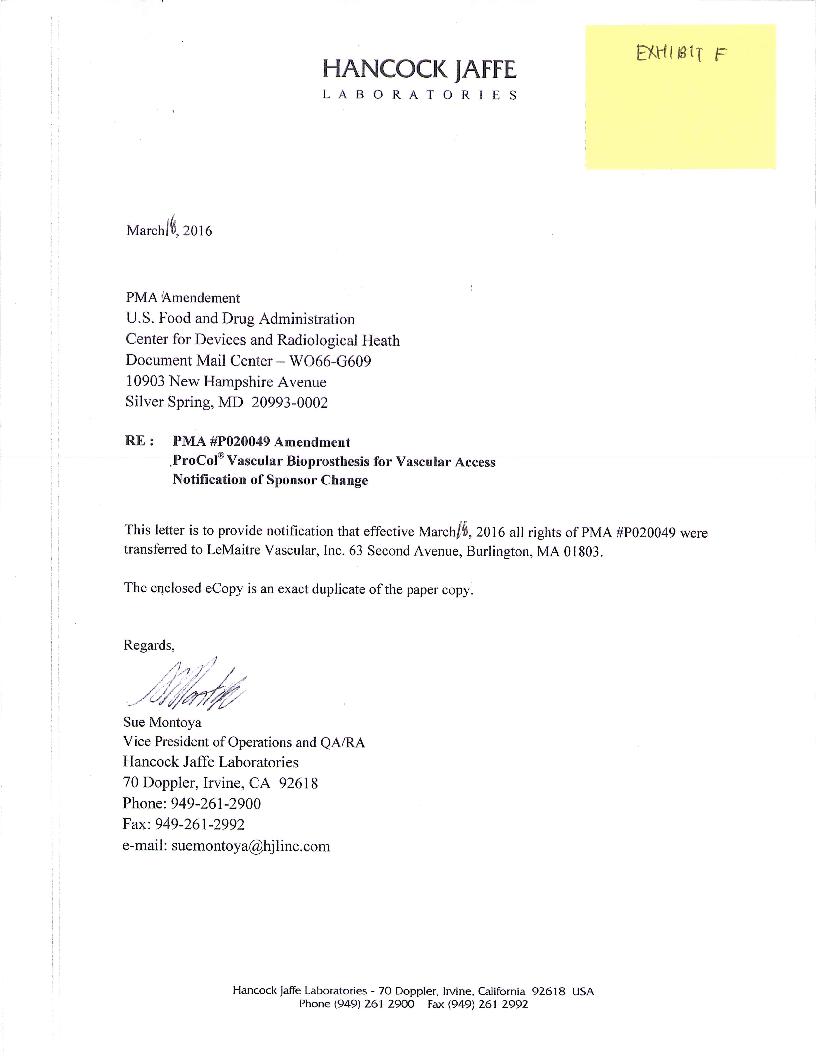

| In March 2016, LeMaitre Vascular, Inc., or LMAT, (Nasdaq: LMAT), a provider of peripheral vascular devices and implants, acquired our ProCol® Vascular Bioprosthesis for dialysis access line of products for $2,805,297 plus a three-year royalty up to a maximum of $5 million. We will provide sub-contract manufacturing transition services to LMAT from its facility for up to three years. |

| The ProCol® Vascular Bioprosthesis is a Class III vascular bioprosthesis for hemodialysis vascular access concomitant with end stage renal disease, or ESRD. The ProCol® Vascular Bioprosthesis is a natural biological graft derived from a bovine mesenteric vein. The patented tissue processing technology and sterilization process ensures a product that is flexible, easy to suture and one which exhibits physiologic pulsatile flow characteristics similar to a native fistula. The ProCol® Vascular Bioprosthesis may be implanted in a straight or loop configuration, according to the specific surgical need and has demonstrated clinical efficacy in the upper arm, forearm, and thigh |

| 1 |

| The ProCol® Vascular Bioprosthesis has received FDA PMA Approval for commercial sale in the United States for use as a vascular access bridge graft in patients who require graft placement or repair subsequent to at least one failed prosthetic graft or consequent to failure of a prosthetic graft in terms of intent to treat. |

| The outcomes of the FDA trials and subsequent studies demonstrate that the cumulative patency for the ProCol® Vascular Bioprosthesis implanted as a first access or after multiple failed prosthetic grafts is fundamentally that usually reported for AVFs as the first access or employed consequent to failed ePTFE grafts. As compared with the present standard of care ePTFE graft, the ProCol® Vascular Bioprosthesis has shown 3.7 times lower relative risk of infection, 1.4 times lower relative risk of interventions, and 1.7 times lower relative risk of thrombosis. We believe this is exemplified by the quantitative and qualitative similarities of the cumulative patency of the ProCol® Vascular Bioprosthesis to that reported for native arteriovenous fistulae in the Dialysis Outcome and Practice Patterns Study. We believe the results of these and other studies consistently demonstrate that as a vascular access bridge graft the ProCol® Vascular Bioprosthesis provides dramatically better cumulative patency compared to ePTFE grafts and exhibits a lower complication rate. Most importantly is the continued patient satisfaction associated with the paucity of complications and uninterrupted dialysis therapy. |

| The PBV is stored in sterile saline, so preparation in the operating room is easily accomplished via a simple, quick rinsing process. The PBV is also highly biocompatible and elicits no antibody reactions in patients. Handling and suturing characteristics of the PBV are similar to a patient’s native tissue making it easy to work with during the implant procedure. The natural tissue of the PBV is easily punctured in the hemodialysis setting affording the ease of access associated with a native fistula and the highly elastic and compliant nature of the PBV enables it to handle high flow rates. Hemostasis is also readily achieved with minimal pressure following the removal of the hemodialysis needles. The PBV graft may be accessed for hemodialysis as soon as two weeks following implant, based upon the physician’s decision and patient tolerance. |

| Products Under Development |

| Over the past eight years we have been developing the following three implantable biomedical devices for heart and cardiovascular disease: |

| ● | Bioprosthetic Heart Valve: a bioprosthetic heart valve designed to function mimetic of a native heart valve providing the recipient over twice the functional performance of presently available devices. The hemodynamics and durability have been especially enhanced for the presently unresolved complications attendant to pediatric and adolescent recipients. |

| ● | Bioprosthetic Coronary Artery Bypass Graft (CoreoGraftTM): a bioprosthetic heart bypass graft for coronary artery bypass procedures, designed to eliminate the need for harvesting a patient’s saphenous vein and/or radial artery to facilitate a more complete revascularization of the heart muscle. |

| ● | Bioprosthetic Venous Valve, the VenoValve: a bioprosthetic venous valve for replacement of dysfunctional valves in the veins of individuals suffering with chronic deep venous insufficiency of the lower limb, a disease with no presently durable medical or surgical treatment available. The device is designed to restore venous flow back to the heart. |

| Bioprosthetic Heart Valve |

| The Bioprosthetic Heart Valve, or BHV, is a next generation bio-prosthetic heart valve designed to mimic and function like a native heart valve providing the recipient over twice the functional performance of presently available devices. The hemodynamics and durability of BHV have been especially enhanced for the presently unresolved complications attendant to pediatric and adolescent recipients and we are aiming to have the BHV become the standard of care for pediatric heart valve replacement. |

| Following an eight-year research and development effort, we completed the designing, prototyping and testing in accordance with the requisite International Organization for Standardization, or ISO, 5840 Part 1 (Cardiovascular Implants, Cardiac Valve Prostheses General Requirements) and Part 2 (Surgically Implanted Heart Valve Substitutes) of what we believe is an innovative ground-breaking heart valve bio-prosthesis for pediatric cardiac heart valve replacement. We believe that we have completed the necessary ISO 5840 pre-clinical data requirements in order to prepare a submission to the FDA to begin First-in-Human clinical trials in the United States in 2017. To that end, we have obtained a patent (U.S. Patent No. 7,815,677 “Reinforcement device for a biological valve and reinforced biological valve”) for the BHV. See “Intellectual Property.” We intend to produce 19 mm, 21 mm and 23 mm diameter bio-prosthetic heart valves to address the specific needs of the pediatric patient cohort undergoing valve replacement for congenital and/or acquired aortic and mitral valve disease. |

| 2 |

| The BHV has been designed to address the specific needs of the pediatric patient cohort undergoing valve replacement for congenital and/or acquired aortic and mitral valve disease. Based upon our patented technology, the BHV eliminates the need for external support structures technically referred to as a “stent” to maintain valve geometry and function. This is accomplished through a use of titanium wires embedded within the wall of the bioprosthetic valve. This greatly increases the size of the bioprosthesis that can be placed in the pediatric patient’s small annulus, the site of the inflow of the patient’s original valve. Thus, the BHV allows for effective functional results equal to a valve size two to three sizes larger than would be possible when implanting with an external stent. In addition, the internalized titanium supports are robust enough so as not to require additional suturing as is the case for weakly supported or stentless valves. This allows for the utilization of a single suture line for attachment of the valve to the recipient’s annulus and for an uninterrupted flow plane, which greatly increases the volume of blood with each heart beat. Conversely, conventional valve design requires that the valve tissue be sewn or mounted inside the external stent diminishing the effective diameter and resulting in poor performance, stress on the leaflets and ultimately to a decreased longevity. When a conventional bioprosthetic heart valve is placed in a small annulus, not only will the valve react adversely to increasing cardiac output but it will require a valve three sizes larger than the annulus to achieve a similar hemodynamic or functional result to the native valve; a feat not advisable or in any event accomplishable even with conventional root enlargement procedures. A patient prosthesis mismatch (the prosthesis is too small with regards to the patient’s size and weight) results in poor quality of life and in impairment of physical development and social integration. |

| Similar flow advantages have been verified for our 23 mm BHV, the most common size implanted for mitral disease. Our 23 mm BHV has proven to provide an effective orifice area that mimics flow conditions of a younger active child. This is approximately 85% greater blood flow than presently available bioprosthetic heart valves with expected decreased recovery time from procedure of up to 75%. |

| Additionally, for a normal heart, the outflow of the mitral valve is immediately adjacent to the outflow tract of the aortic valve. In disease related left ventricular chamber anatomy, this anatomic relationship is extremely susceptible to obstruction of the outflow tract and/or injury to the compromised left ventricular wall by the degree of protrusion of the mitral valve replacement into the left ventricle. The protrusion of our 23 mm BHV is up to 2 mm less when compared to other bioprosthetic valves. Our flatter more planar geometry comes closer to mimicking the native anatomy allowing for physiological, more efficient left ventricular and aortic outflow tract flow patterns. |

| Bioprosthetic Coronary Artery Bypass Graft - CoreoGraftTM |

| The CoreoGraft® CABG is a device for use as an alternate or supplemental coronary vascular conduit in coronary bypass surgery. The Coreograft® CABG is designed to eliminate the need for harvesting the patient’s saphenous vein and/or radial artery and facilitate a more complete revascularization of the injured heart muscle. The device will allow for effective coronary bypass procedures for a significant number of patients who have no adequate vessels for grafting, especially patients undergoing redo procedures and patients suffering from chronic venous insufficiency. This device is fashioned from 3 mm diameter bovine mesenteric veins. The “feel” and suturing quality of the graft are mimetic of mammary arteries and requires no special suture considerations beyond those commonly used for autologous grafts. The Coreograft® CABG graft length is appropriate for all bypass requirements allowing exact trimming to the individually required length. |

| The Coreograft® CABG is both anatomically and functionally similar to a natural artery and has been demonstrated in preliminary studies to sustain effective “coronary” hemodynamics and cardiac function. Outcomes of 25 procedures performed by Dr. Wade Dimitri and colleagues at Walsgrave Hospital, U.K., exemplify the utility of the ProCol® CAGB as an alternate or supplemental coronary vascular conduit in off-pump CABG. This preliminary clinical study was limited to patients without sufficient available autologous grafts or patients who could not be weaned from bypass perfusion because of incomplete cardiac revascularization. Twenty-six grafts were implanted in 24 patients requiring a complete myocardial revascularization subsequent to hospital admission for coronary artery bypass grafting. In all cases, the Coreograftl® CABG was used when it was determined that adequate or suitable autologous conduits were not available as a consequence of prior use, vascular pathology or contraindication associated with a comorbid condition. |

| 3 |

| During December 2016, we had a CE Mark pre-submission meeting with a European Notifying Body in order to receive feedback on the CE Mark submission for the CABG graft currently anticipated to be filed during the first quarter of 2017. Additionally, we believe that we have completed the necessary pre-clinical requirements to prepare an FDA IDE submission to begin human clinical trials in the United States for our bioprosthetic heart bypass graft, which we currently plan to begin in 2017. |

| There are no presently approved biological vascular grafts for coronary artery bypass procedures. We believe that the availability of the readily available “off the shelf” Coreograft® CABG will encourage multiple graft placement without the surgeon forgoing additional procedures that are not cost-effective. |

| Bioprosthetic Venous Valve, The VenoValve |

| We have developed a bioprosthetic Venous Valve, the VenoValve, for use in treatment of lower limb chronic venous insufficiency. The VenoValve is a replacement of dysfunctional valves in the deep venous system in individuals suffering from lower limb chronic venous insufficiency. Restoration of valvular function in the deep system is the “Holy Grail” for treatment of CVI. The VenoValve comprises a biologic leaflet mounted in a supporting frame or “stent” that will allow for surgical insertion of VenoValve into the femoral vein, thereby re-establishing competence and anterograde venous flow back to the heart. |

| Preclinical prototype testing, including in vivo animal studies and in vitro hemodynamic studies have demonstrated that the VenoValve is similar in function to a normal functioning venous valve. Ascending and descending venography of the VenoValve in sheep, demonstrated competency of the valve as well as patency in appropriate flow patterns. |

| During November, 2016, we made an FDA submission through the FDA Expedited Access Program (EAP) in order to obtain expedited approval for commercialization of the HJL Venous Valve in the United States and possible early feasibility study in man. |

| As there are no currently available medical or non-surgical treatment of lower limb chronic venous insufficiency, we believe the VenoValve will provide for a paradigm shift in the treatment of both primary and secondary causes of chronic venous insufficiency disease. |

| Industry Overview |

| Hemodialysis Market |

| Hemodialysis is the main treatment for patients with end stage renal disease (most commonly known as kidney failure and sometimes referred to as ESRD). During a hemodialysis treatment, a machine pumps and cleans a patient’s blood by way of a flexible, plastic tube. In order to perform hemodialysis, an access must be created . This maybe a direct connection between the patient’s own artery and vein or if the vein is not of adequate size, then a connection between the artery and vein is created using a prosthetic device or conduit The most commonly used hemodialysis access grafts consist of various conduit designs fabricated from expanded polytetrafluoroethylene (or ePTFE). Despite historically mediocre performance, ePTFE grafts have continued to play a significant part in the hemodialysis market |

| Several studies1) have shown that the Procol Graft has better patency rate than ePTFE grafts. Also in case of infection of an ePTFE graft, a Procol graft may be used at the same place without getting infected. Studies have shown that the overall patency and infection rate of Procol is superior to ePTFE in the leg position. |

In 2016 an investment analysis of the US market for hemodialysis access grafts estimated the market at approximately $5.1 billion in 2015 growing to $8.6 billion by 2024.2) Hemodialysis access is rapidly becoming one of the largest market segments for vascular grafts and with the average unit selling price rapidly approaching over $1,000. The market is expected to be about $110 million by 2015. Although vascular access is one of the most vital components of the treatment paradigm for ESRD, the yearly total access graft cost represents less than one half of one percent of the total annual ESRD treatment expenditures.

|

| 1. | “Alternative graft materials for hemodialysis access”, Seminars in Vascular Surgery, March 2004; “Multicenter evaluation of the bovine mesenteric vein bioprostheses for hemodialysis access in patients with an earlier failed prosthetic graft”, Journal of the American College of Surgeons, August 2005; 1. “Conduits for hemodialysis access”, Seminars in Vascular Surgery, September 2007. | ||

| 2. | “Vascular Access Device Market to US$8.6 Billion by 2024; Peripheral Catheters to be Most Preferred Device Through 2024, Projects TMR”, Transparency Market Research, September 2016. | ||

| 4 |

| New Bioprosthetic Heart Valve Device Need |

| Bioprosthetic heart valves are used for diseases relating to the aortic and mitral valves. Aortic valve or mitral valve stenosis occurs when the heart’s valves narrow, preventing the valve from opening fully. This obstructs blood flow from the heart and to the rest of the body. When the valves are obstructed, the heart needs to work harder to pump blood to the body, eventually limiting the amount of blood it can pump and may weaken the heart muscle. Valve stenosis, if left untreated, can lead to serious heart problems. |

| Mitral valve stenosis and prolapse, leakage or regurgitation related to inadequate or faulty closing, concerns a defective mitral valve, which is located between the left chambers of the heart. This valve works to keep blood flowing properly and allows blood to pass from the left atrium to the left ventricle but prevents it from flowing backward. When the mitral valve does not work properly, a person can experience symptoms such as fatigue and shortness of breath because the defective valve is allowing blood to flow backwards into the left atrium. Consequently, the heart will not pump enough blood out of the left ventricular chamber to supply the body with oxygen-filled blood. In certain cases, mitral valve disease, may, if left untreated, lead to heart failure or irregular heartbeats (“arrhythmias”), which may be life threatening. |

| Historically, heart valve manufacturers have fabricated replacement heart valve types (mechanical, biological, pericardial, pig-origin) and sizes to accommodate a spectrum of patient age, body mass or special pathologic conditions. Typically, this consists of aortic valve sizes with outside diameters ranging from 19 millimeters (“mm”) to 27 mm in 2 mm increments and mitral valves sizes in 2 mm increments from 27 mm to 31 mm. Hospitals and surgeons generally used one biologic and/or one mechanical valve from a single manufacturer and until about the end of the last century hospitals tended to inventory a complete size range of valves typically from a single manufacturer. As the practice of heart valve replacement surgery developed, it became apparent that the recipient population demanded a more prospective view in terms of the various implant modalities, geometrical configuration and a patient’s comorbidities. Depending on age (patients under age 20 receive a mechanical valve due to their calcium metabolism) surgeons use either mechanical, pericardial or porcine biological valves. Porcine valves have shown better longevity than pericardial valves. |

| Distinctive features of one particular valve may facilitate implantation or meet the particular demands of a patient’s unique pathology. This stimulated the development of various valve configurations, but in the end did not significantly improve hemodynamic performance or advance quality of life concerns. There is no disagreement and considerable evidence that for most cardiac valve related disorders presently available devices will improve graft recipients presenting conditions. |

| However, we believe there is one patient cohort for whom the present devices fall short: very young children and adolescents requiring the smallest valve sizes, typically 19-21 mm in diameter. The primary challenge for these patients is to provide adequate blood flow during growth and development. Typically, this requires more complex procedures or multiple interventions to provide a larger valve replacement. Additionally, biological valves in younger patients will deteriorate as a consequence of what is known as dystrophic mineralization, a phenomenon most likely associated with skeletal growth. Children and adolescent receive historically mechanical valves, which show lower performance. The patient outgrows the valve size several times between age two and twenty, requiring three to five surgeries before adulthood (also referred to as patient prosthetic mismatch). |

| Pediatric patients suffering from mitral valve prolapse, stenosis or rheumatic fever typically face complex issues such as alterations of the morphology and geometrical shape of the left heart chambers, which may compromise the chords that tether the mitral valve and the surrounding annular tissues that maintain the leaflet in a proper position (juxtaposition) leading to leakage or regurgitation. The common course for mitral valve disease in children is repair rather than replacement of the valve due to the potential complexity of pediatric mitral valve disease. However, when the mitral valve is not amenable to repair either as a consequence of surgeon skill and/or experience or the complexity of the pathology, a valve replacement procedure is necessary. Mitral valve stenosis and prolapse, leakage or regurgitation also results in significant changes in the morphology of the wall of the left ventricle, typically manifested as considerable thinning, and/or ventricle enlargement or thickening. For a normal heart, the outflow of the mitral valve is immediately adjacent to the outflow tract of the aortic valve. In disease related left ventricular chamber anatomy, this anatomic relationship is extremely susceptible to obstruction of the outflow tract and/or injury to the compromised left ventricular wall by the degree of protrusion of the mitral valve replacement into the left ventricle. This leads to a restricted passage of the blood through the aortic valve (aortic insufficiency). A too large aortic valve replacement may restrict the function of the mitral valve. It is therefore very important to match the respective valve with the size of the patient’s heart. |

| 5 |

| We believe that the effective orifice size of most, if not all, of the present commercially available small diameter bioprosthetic heart valves suited for pediatric aortic and mitral valve replacement are inadequate to provide the necessary hemodynamic result for up to 80% of the potential valve recipients suffering from congenital or acquired valvular disease. We believe that this shortcoming is a result of the reduced effective diameter of currently available bioprosthetic heart valves that uses conventional supporting structures and/or the resistance of the valve leaflets during the forward flow opening phase of the cardiac cycle. Most commonly, for developing children, the increasing body mass or body surface area as a child grows is frequently incongruent with the valve size that the patient’s heart can accommodate. Consequently, these recipients almost universally develop a condition designated as “patient prosthetic mismatch.” For valve replacement in both younger and older pediatric patients, patient prosthetic mismatch has been shown to be associated with longer recovery periods and diminished improvements in symptoms. This is reflected in decreased exercise capacity, decreased recovery of the thickened left ventricle, as a result of the ventricular adaptation to the flow resistance of the narrowed aortic valve outflow tract, and an increased number of adverse postoperative cardiac events. Older pediatric patients are especially susceptible to patient prosthetic mismatch with a marked persistence of symptoms. This is most likely related to the younger patient’s higher cardiac output requirements in association with a longer exposure to the consequences of patient prosthetic mismatch. |

| According to American Heart Association each year, approximately 10 of every 1,000 children (approximately 1.3 million children) worldwide including 8 of every 1,000 in the U.S. are born with a congenital heart defect requiring immediate or eventual surgical intervention. Of this patient cohort, 30-40% will undergo either aortic or mitral valve replacement surgery during the first two decades of life. This results in approximately 50,000 procedures with the vast majority requiring 19, 21 or 23 mm sized prostheses. The 2016 Global Data Report estimates the global heart valve market to be approximately $2 billion based on an average selling price for standard valve prostheses of $5,000-$9,000. This market is projected to grow to $19.6 billion by 2026.1) These patients above all would benefit from the HJL bioprosthetic heart valve, being safer, cost effective and reducing reoperations in the patient population |

| Bioprosthetic Coronary Artery Bypass Graft Device Need |

| The present standard procedure for coronary bypass surgery employs the use of the patient’s saphenous vein and/or internal mammary artery as conduits to re-establish blood flow, otherwise known as coronary artery bypass grafts (or CABG). While balloon angioplasty with or without stent placement is another option and has been effective for many patients, this procedure is not always appropriate for multiple vessel disease. Balloon angioplasty also has not produced conclusive and consistent results and, in a large number of instances, may only provide short term relief necessitating subsequent and consequently more difficult surgical intervention. Coronary artery bypass remains the most effective procedure to re-vascularize cardiac muscle subsequent to a heart attack. By the end of the last decade, more than 500,000 coronary artery bypass procedures requiring almost one million harvested autologous grafts were performed annually in the U.S. In 2015, 150,000 coronary artery bypass procedures were performed, which accounts for 425,000 bypass grafts.2) |

| We believe that the recent trend toward off pump coronary graft surgery (surgical intervention on a beating heart as opposed to surgery on a stopped heart with extra-corporal circulation; decreases the surgery time by one hour), minimally invasive coronary artery bypass surgery has had considerable bearing on both perioperative and procedural safety and efficacy and has had a significant impact on the future of the procedure and attendant utility of prosthetic bypass grafts. Bypass graft harvest remains the most invasive and complication prone aspect of the minimally invasive bypass procedure. Present standard-of-care complications are described in recent published reports in major medical journals. The percentage of complications Can be as high as 43 percent. Fortunately, less than 50 percent of these wounds require operative intervention, but the ones that do can be major. |

Also recent articles substantiate that saphenous vein graft obstruction is progressive, with failure as high as 50% at 10 years. Acute thrombosis, neointimal hyperplasia, and accelerated atherosclerosis are the 3 mechanisms that lead to venous graft failure. (Saphenous vein graft failure after coronary artery bypass surgery: pathophysiology, management, and future directions. Harskamp RE, Lopes RD, Baisden CE, de Winter RJ, Alexander JH. Ann Surg. 2013 May;257(5):824-33. Off-pump CABG with vein grafts show an increased rate of obstruction versus mammary artery graft CABG. (Ref. Comparison of graft patency between off-pump and on-pump coronary artery bypass grafting: an updated meta-analysis. Zhang B, Zhou J, Li H, Liu Z, Chen A, Zhao Q. Ann Thorac Surg. 2014 Apr;97(4):1335-41. Epub 2014 Jan 7). Also, a significant cost of CABG procedures is associated with graft harvest and the extended recovery and complications related to the harvest procedure.

|

| 1. | “Prosthetic Heart Valve Market: Global Industry & Opportunity Assessment, 2016-2026”, Global Data.com, November 2016. | ||

| 2. | “Understand Your Risk for Congenital Heart Defects” American Heart Association, October 2016. | ||

| 6 |

| The increased incidence of chronic venous diseases of the lower limbs also reduce the possibility of harvesting good quality veins as well as the increase incidence of redo CABG bypasses.. An “off the shelf” bypass conduit would do away with the attendant complications and chronic postoperative discomfort frequently reported for autologous graft harvest and consistently afford sufficient material for more complete cardiac revascularization. The American Heart Association stated in 2015 that “complete revascularization was key to ensure long term survival and quality of life in patients with coronary disease” (Eagle, KA; Guyton RA; Davidoff R; et al. (October 5, 2004). “ACC/AHA 2004 guideline update for coronary artery bypass graft surgery: a report of the American College of Cardiology/American Heart Association Task Force on Practice Guidelines. An efficacious prosthetic bypass graft in concert with off pump and/or minimally invasive surgery would comprise an almost wholly “noninvasive procedure.” We believe the availability and appeal of such a modality would have considerable impact on the therapeutic balance between bypass revascularization and interventional cardiology regimens like stents, balloon catheterization, which only provide temporary relief. |

| Coronary artery bypass surgery departs from the usual one procedure–one device paradigm. When revascularization requires more than an internal mammary graft, a conservative average of 2.5 additional grafts is required. The economics and surgeon reimbursement amounts for bypass procedures presently discourage multiple graft procedures as the time to harvest additional grafts is not economically justified in terms of the reimbursement amounts. Reimbursement codes for a single bypass graft versus five grafts on the same patient only differ by a few hundred dollars but the multiple grafts require up to three times the amount of time and operating costs of a single procedure. We believe that this discourages taking the time and incurring the operating room costs in harvesting additional bypass grafts resulting in suboptimal cardiac revascularization. Moreover patients requiring multiple bypasses for a complete revascularization often show comorbidities like chronic venous insufficiency of the lower limbs as well as redo patients. |

| If only half of the annually performed procedures required multiple graft revascularization, the requisite number for the U.S. alone would be in excess of 110,000. On the basis that - consequent to an approved device - utilization was only 50% of the prospective market potential, market value for the U.S. alone would be approximately $660 million to $770 million for unit pricing of $6,000 to $7,000; the European and Pacific Asia markets combined would have a similar value for a worldwide market of $1-$2.0 billion. (CDC) |

| Bioprosthetic Venous Valve Device Need |

| Lower Limb Chronic Venous Insufficiency (CVI)) is a disease presently affecting tens of millions of patients worldwide with approximately 1.5 million new cases annually. In the U.S., based upon data from the Vascular Disease Foundation, approximately 20% of the population suffers from varicose veins and 5% (15 million) of the U.S. population are expected to develop DVT and approximately 65% (10 million) of the U.S. DVT population are expected to develop CVI. Extrapolation of the Data from the Vascular Disease Foundation reveals that in the U.S., the present population of individuals suffering varying degrees of CVI is approximately 5 million, the incidence of CVI as a consequence of congenital and inflammatory etiology resulted in 70,000 hospitalizations per year, and the incidence of CVI as a consequence of DVT is approximately 400,000 cases per year. In Western Europe, the incident rate of CVI is estimated at one million hospitalizations per year, the prevalent CVI population is estimated at 17.5 million, and the mean prevalence of CVI of the legs in the general population in Western Europe is 30%. Patients with CVI are plaqued with marked disability, either from leg swelling or development of non healing leg ulcers. |

| The hallmark of the disease is the failure of damaged venous valves to allow for lower limb venous blood to return to the heart. It is a mechanical reflux problem. Presently no medical or nonsurgical treatment is available other than compression “garments” for early stage disease or leg elevation for more severe cases, which are, at best, only palliative. When the disease is isolated to the superficial veins, ablation or surgical excision of the affected vein is an option. However, for the deep system, valve transplants has been used but with very poor results or creation of valves using fibrous tissue which is only performed in few centers world wide. Reestablishment of proper direction of venous flow to the heart is the only reasonable remedy to the problem of CVI. |

| 7 |

| Our Strategy |

| Our business strategy is focused primarily on research, development and manufacturing of biomedical device technologies for use in surgical procedures. We are also focused on the relatively large device markets where our technological advances and achievements provide an opportunity to offer our devices in an environment conducive and advantageous to their utilization and clinical benefit. Developing pathways to obtain FDA approval in the most expedient fashion is our main strategy for our products. |

| Research and Development |

| Our present strategy for the VenoValve is to obtain approval from the FDA for a first in man study that will quickly evolve into a study coordinated to demonstrate improvement in the quality of life for patients with CVI. We believe that the VenoValve will provide significant improvement in the quality of life measures for patients living with the disability |

| Our Competitive Strengths |

| Strong Proprietary Estate of Processes, Validation Procedures and Related Intellectual Property |

| We believe that we possess an extensive assemblage of proprietary processing and manufacturing methodology specifically applicable to the design, processing, manufacturing and sterilization of our devices. Additionally, we believe our patents pertaining to unique design advantages and processing methods of valvular tissue as a bioprosthetic device provides intellectual advantage over potential competitors. See “—Intellectual Property.” |

| Development of Facilities |

| We operate a 16,500 square foot manufacturing facility in Irvine, California. Our facility is designed expressly for the manufacture of biologic vascular grafts and is equipped for research and development, prototype fabrication, CGMP manufacturing and shipping for Class III medical devices, including biologic cardiovascular devices. When fully staffed and utilized, we believe production capacity will be approximately 24,000 devices annually. |

| Intellectual Property |

| We possess an extensive proprietary processing and manufacturing methodology specifically applicable to the design, processing, manufacturing and sterilization of our biologic devices. This includes FDA compliant quality control and assurance programs, proprietary tissue processing technologies demonstrated to eliminate recipient immune responses, decades long and trusted relationship with abattoir suppliers, and a combination of tissue preservation and gamma irradiation that extends device longevity, provides device functions and guarantees sterility. The FDA is familiar with the most essential aspects of our methodologies as they have been part of our process development. Our patents pertaining to the unique design advantages and processing methods of valvular tissue as a bioprosthetic device provides further intellectual advantage over potential competitors. |

| We have also developed a unique Class III device cGMP documentation process central to bringing all of the various elements together during the fabrication processes affording a significant “barrier” to potential competitive efforts. Our cGMP documentation cannot be infringed on from a proprietary standpoint because of the specificity of each listed section and the associated validations and permissions. |

| In addition, there are various specific intellectual property items related to each of our devices as described below. |

| Bioprosthetic Heart Valve (BHV) |

| The critical design components and function relationships unique to the BHV are protected by U.S. Patent No. 7,815,677, issued on October 19, 2010, and expires on July 9, 2027. |

| Coreograft® CABG |

| 8 |

| A unique use patent will be filed to protect the specific indication based on the mimetic biomechanical properties of the wall of the Coreograft® CABG as it relates to pulsatile propagation of forward flow characteristic of coronary arteries. |

| The VenoValve |

| The VenoValve encompasses a unique intellectual estate comprising of dozens of proprietary processes and methodology from its initial development and manufacturing, through the finished device. Patents are pending for the unique design of the frame for this device. |

| Leadership |

| Experienced and seasoned leadership in research and development will help make us successful in its endeavors to obtain FDA approval of their devices. |

| Competitive Markets |

| Marketing and Sales |

| We will develop an internal marketing and sales group to manage a combination of direct sales representatives and an independent distribution network. |

| Cardiac surgeons generally develop a preference for one particular company’s device, whether based on an impression of superior performance or on developed relationships with the providers. We believe that by focusing on the pediatric segment we are not subject to this issue as the prospective user can focus on the best ethical approach to the patients need without “abandoning” prior affiliations. We believe the present “commodity” nature of the heart valve industry that the benefits of the BHV will position the device as a standard of care without a competitive “peer.” |

| In addition, according to the American Heart Association – Heart Org Congenital Heart Defects, each year worldwide approximately 10 of every 1,000 children (approximately 1.3 million children) including 8 of every 1,000 in the United States are born with a congenital heart defect requiring immediate or eventual surgical intervention. Of this patient cohort, 30-40% will undergo either aortic or mitral valve replacement surgery during the first two decades of life. This results in approximately 50,000 procedures with the vast majority requiring 19, 21 or 23 millimeter sized prostheses. The 2015 Global Data Report reported the global heart valve market to be approximately $2 billion being based on an average selling price for standard valve prostheses of $5,000-$9,000. Based on these statistics, we believe that at the proposed average selling price of $17,500 per unit for all sizes, the estimated market of the BHV is approximately $300 million in the U.S. and $500-600 million in Western Europe and Pacific Asia. On an equivalent cost basis, we believe the market value of its bioprosthetic valve would represent approximately 25% of the total market on a unit basis. |

| Coreograft® CABG |

| The CABG market is, to a more complex market to estimate on a procedural basis. This is largely due to the evolving attitude toward more complete vascularization of the infarcted heart and the varying number of placed grafts accompanying the cardiopulmonary bypass and off pump or beating heart procedures. In lieu of a multifaceted trend analysis, it is reasonable to approach the potential market on a conservative basis by assigning an average of 2.5 grafts per procedure which for the U.S. would be an equivalent of approximately 375,000 units annually representing a market value of approximately $3.25 billion; an even more conservative estimate based on graduated market penetration has a market potential of over $1 billion. As is the case for devices utilized as part of well- established surgical procedures, the “rest-of-world” market has been consistently equivalent to that of the U.S. |

| When the total costs of coronary artery bypass procedures are estimated in terms of alternate treatments and especially for those patients for whom surgery is strongly indicated it appears that a cost for a device that substitutes for graft harvest, alleviates the inevitable cost of treatment subsequent to incomplete revascularization and limits the adjunct use of high ASP’s for stents would allow for reimbursement equivalent to less than 20% of the total procedure and hospital costs. In consideration of the above the anticipated price to the hospital will be $6,000.00 per unit. |

| 9 |

| HJL Venous Valve, The VenoValve |

| In the U.S., based upon data from the Vascular Disease Foundation, approximately 5% (15 million) of the U.S. population are expected to develop DVT and approximately 65% (10 million) of the U.S. DVT population are expected to develop CVI. Extrapolation of the Data from the Vascular Disease Foundation reveals that in the U.S., the present prevalent population of individuals suffering varying degrees of CVI is approximately 5 million, the incidence of CVI as a consequence of congenital and inflammatory etiology resulted in 70,000 hospitalizations per year, and the incidence of CVI as a consequence of DVT is approximately 400,000 cases per year. For Western Europe, the incident rate of CVI disease is estimated at one million hospitalizations per year, the prevalent CVI disease population is estimated at 17.5 million, and the mean prevalence of CVI disease of the legs in the general population in Western Europe is 30%. |

| Based upon the foregoing, we estimate that for the U.S., the candidate patient population for the VenoValve is at present approximately 5.5 million and at the time of commercialization of the product, the prevalent candidate population is expected to be 6.5-7 million with the candidate incidence rate at over half a million annually. With standardized average selling price across currencies, we estimate that the monetary value of the U.S. and Western European market for the VenoValve is on an incidence basis approximately $10 billion annually with the prevalent market value is in excess of $100 billion. |

| There is no comparable device for purposes of price comparisons and/or reimbursement codes. Therefore, after consulting with industry analysts and vascular surgeons, examining the actual selling price sensitivity in terms of clinical benefit, and analyzing trends in reimbursement for similarly existing devices, we have developed a potential clinical value for the VenoValve. We have estimated a reimbursement of $6,500 - $11,000 per valve. |

| A measure to estimate the cost effectiveness of an intervention is quality-adjusted life-years (or QALY). Presently for CVI, the cost per patient to maintain the status quo of CVI or no substantial improvement in QALY is approximately $50,000 annually. The VenoValve would improve the QALY over a 5-year period by at least 2.5 QALYs and would reduce the annual cost to maintain the improved longevity and life style by 60%. For device recipients, with a return to normal activity without pain, the QALY improvement would be 4; equivalent to reducing annual costs by 75%. Over a 5-year period the health care cost savings associated with use of the venous valve would be $150,000 - $200,000, equivalent to a 5 year savings of hundreds of billions of dollars for the present prevalent and anticipated incident patient population. In consideration of the above the anticipated price to the buyer these factors will be associated with the cost of the device. |

| Summary Risks Related to Our Business |

| Our business is subject to a number of risks, including risks that may prevent us from achieving our business objectives or may adversely affect our business, financial condition, results of operations, cash flows and prospects that you should consider before making a decision to invest in our common stock. These risks are discussed more fully in “Risk Factors” beginning on page of this prospectus. These risks include, but are not limited to, the following: |

| ● | We have a history of incurring net losses and, currently, we are not generating significant revenue. There can be no assurances that we will generate significant revenue in the future, achieve profitable operations or continue as a going concern. | ||

| ● | As a result of our current lack of financial liquidity, our auditors have expressed substantial doubt regarding our ability to continue as a “going concern.” | ||

| ● | We currently have no sales and marketing organization and need to depend on collaborations with third parties for key aspects of our business. If we are unable to secure a sales and marketing partner or establish satisfactory sales and marketing capabilities, we may not successfully commercialize our products. | ||

| ● | We will need substantial additional funding and if we are unable to raise capital when needed, we would be forced to delay, reduce or eliminate our product development and commercialization plans. |

| 10 |

| ● | Raising additional capital may cause dilution to our stockholders, restrict our operations or require us to relinquish rights to our technologies or product candidates. | ||

| ● | Competition in the medical device industry and the target markets for our products and proposed products is intense and we expect competition to increase in the future. Our operating results will suffer if we fail to compete effectively. | ||

| ● | Our products are subject to a lengthy and uncertain domestic regulatory review process. If we do not obtain and maintain the necessary domestic regulatory authorizations, we will not be able to provide our products in the U.S. | ||

| ● | Our products are also subject to extensive governmental regulation in foreign jurisdictions, such as Europe, and our failure to comply with applicable requirements could cause our business, results of operations and financial condition to suffer. | ||

| ● | Our competitive position and commercial success is contingent upon the protection of our intellectual property. It is difficult and costly to protect our proprietary rights and we may not be able to ensure their protection. | ||

| ● | There is no existing market for our common stock and we do not know if one will develop to provide you with adequate liquidity. |

| Corporate Information |

| We were incorporated in Delaware in December 22, 1999. Our principal executive offices are located at 70 Doppler, Irvine, California, 92618, and our telephone number is (949) 261-2900. Our corporate website address is www.hancockjaffe.com. The information contained on or accessible through our website is not a part of this prospectus, and the inclusion of our website address in this prospectus is an inactive textual reference only. |

| Implications of Being an Emerging Growth Company |

| As a company with less than $1.0 billion in revenue during our last fiscal year, we qualify as an “emerging growth company” as defined in Section 2(a) of the Securities Act of 1933, as amended, or the Securities Act, as amended and modified by the Jumpstart Our Business Startups Act of 2012, or JOBS Act, enacted in April 2012. An “emerging growth company” may take advantage of certain exemptions for reduced reporting requirements that are otherwise applicable to public companies. These provisions include, but are not limited to: |

| ● | being permitted to present only two years of audited financial statements and only two years of related “Management’s Discussion and Analysis of Financial Condition and Results of Operations” in this prospectus, in each case, instead of three years; | |

| ● | being permitted to present the same number of years of summary financial data as the years of audited financial statements presented, instead of five years; | |

| ● | not being required to comply with the auditor attestation requirements of Section 404 of the Sarbanes-Oxley Act of 2002, as amended, or the Sarbanes-Oxley Act; | |

| ● | reduced disclosure obligations regarding executive compensation in our periodic reports, proxy statements and registration statements, including the omission of a compensation discussion and analysis; and | |

| ● | exemptions from the requirements of holding a nonbinding advisory vote on executive compensation and stockholder approval of any golden parachute payments. |

| 11 |

| We may take advantage of these provisions until the last day of our fiscal year following the fifth anniversary of the completion of this offering. However, if certain events occur prior to the end of such five-year period, including if we are deemed to be a “large accelerated filer” as defined in Rule 12b-2 under the Securities Exchange Act of 1934, as amended, which would occur if the market value of our common stock held by non-affiliates exceeds $700 million as of the last business day of the second fiscal quarter of such fiscal year, our annual gross revenue exceeds $1.0 billion or we issue more than $1.0 billion of non-convertible debt during the preceding three-year period, we will cease to be an emerging growth company prior to the end of such five-year period. |

| We have elected to take advantage of certain of the reduced disclosure obligations in the registration statement of which this prospectus is a part and may elect to take advantage of other reduced reporting requirements in future filings. As a result, the information that we provide to our stockholders may be different than you might receive from other public reporting companies in which you hold securities. |

| In addition, the JOBS Act provides that an emerging growth company can take advantage of an extended transition period for complying with new or revised accounting standards. This provision allows an emerging growth company to delay the adoption of some accounting standards until those standards would otherwise apply to private companies. We have elected to avail ourselves of this extended transition period. |

| 12 |

| The Offering |

| Common stock offered by us | shares

|

| Option to purchase additional shares | We have granted the underwriters an option for a period of 30 days from the date of this prospectus to purchase an additional shares.

|

| Common stock to be outstanding after this offering | shares

|

| Use of proceeds | We currently intend to use the net proceeds from this offering, together with our existing cash and cash equivalents, to fund our research and development activities and the regulatory review process for our product candidates, and the remainder for working capital and other general corporate purposes, including the additional costs associated with being a public company. See “Use of Proceeds” on page [__].

|

| Risk Factors | See “Risk Factors” on page [__] for a discussion of certain of factors to consider carefully before deciding to purchase any shares of our common stock.

|

| Proposed Nasdaq Capital Market symbol | “ ”

|

| Stock Split | On July 22, 2016 our board of Directors approved a 2.1144-for-l forward split of our issued and outstanding shares of common stock and, on August 30, 2016, we filed the stock split with the Delaware Secretary of State. |

| The number of shares of our common stock to be outstanding after this offering is based on 12,247,358 shares of common stock outstanding as of September 30, 2016, and excludes: | |

| ● | 833,333 shares of common stock issuable upon the exercise of warrants outstanding as of September 30, 2016, at an exercise price of $6.00 per share; and | |

| ● | 3,300,000 shares of our common stock reserved for future issuance under the 2016 Omnibus Incentive Plan. | |

| Unless otherwise indicated, all information contained in this prospectus assumes: | ||

| ● | no exercise by the underwriters of their option to purchase up to an additional shares of our common stock; | |

| ● | no exercise of the outstanding stock options described above; | |

| ● | no exercise of the outstanding warrants described above; | |

| ● | no issuance of 93,570 shares of Series A preferred stock issuable upon the exercise of warrants outstanding as of September 30, 2016, at an exercise price of $5.00 per share; | |

| ● | the automatic conversion of all outstanding shares of our preferred stock into an aggregate of 935,700 shares of our common stock, the conversion of which will occur immediately prior to the closing of this offering; and | |

| ● | the filing of our amended and restated certificate of incorporation and the adoption of our amended and restated bylaws immediately prior to the closing of this offering | |

| 13 |

Summary Consolidated Financial Data

The following tables set forth a summary of our historical financial data as of, and for the periods ended on, the dates indicated. The consolidated statements of operations data for the years ended December 31, 2015 and 2014 and consolidated balance sheet data as of December 31, 2015 and December 31, 2014 are derived from our audited consolidated financial statements included elsewhere in this prospectus. The consolidated statements of operations data for the [nine-month periods ended September 30, 2016 and 2015] and the consolidated balance sheet data as of [September 30, 2016] are derived from our unaudited consolidated financial statements included elsewhere in this prospectus. The unaudited consolidated financial statements were prepared on the same basis as the audited consolidated financial statements. Our management believes that the unaudited consolidated financial statements reflect all adjustments necessary for the fair presentation of the financial condition and results of operations for such periods.

The following summary consolidated financial information should be read in connection with, and is qualified by reference to, our consolidated financial statements related notes thereto and the section titled “Management’s Discussion and Analysis of Financial Condition and Results of Operations” included elsewhere in this prospectus. Our historical results are not necessarily indicative of results to be expected in any future period.

On July 22, 2016 our board of Directors approved a 2.1144-for-l forward split of our issued and outstanding shares of common stock and, on August 30, 2016, we filed the stock split with the Delaware Secretary of State. All shares and per share amounts have been adjusted to reflect the 2.114-for-l forward split of our issued and outstanding shares, retroactively.

| For The Nine Months Ended | For The Years Ended | |||||||||||||||

| September 30, | December 31, | |||||||||||||||

| 2016 | 2015 | 2015 | 2014 | |||||||||||||

| (unaudited) | ||||||||||||||||

| Selected Statement of Operations Data: | ||||||||||||||||

| Revenues | $ | 481,053 | $ | - | $ | - | $ | 236,500 | ||||||||

| Cost of goods sold | 598,295 | - | - | 132,315 | ||||||||||||

| Gross (Loss) Profit | (117,242 | ) | - | - | 104,185 | |||||||||||

| Selling, general and administrative expenses | 3,406,367 | 706,342 | 1,289,851 | 1,056,844 | ||||||||||||

| Loss from Operations | (3,523,609 | ) | (706,342 | ) | (1,289,851 | ) | (952,659 | ) | ||||||||

| Other Expenses | 524,395 | 47,843 | 88,347 | 65,493 | ||||||||||||

| Loss from Continuing Operations | (4,048,004 | ) | (754,185 | ) | (1,378,198 | ) | (1,018,152 | ) | ||||||||

| Income (loss) from discontinued operations | 2,200,768 | (291,881 | ) | (225,815 | ) | (379,841 | ) | |||||||||

| Net Loss | (1,847,236 | ) | (1,046,066 | ) | (1,604,013 | ) | (1,397,993 | ) | ||||||||

| Cumulative dividend to Series A preferred stockholders | (243,938 | ) | - | (4,352 | ) | - | ||||||||||

| Net Loss Attributable to Common Stockholders | $ | (2,091,174 | ) | $ | (1,046,066 | ) | $ | (1,608,365 | ) | $ | (1,397,993 | ) | ||||

| Net loss per share from continuing operations attributable to common stockholders - basic and diluted | $ | (0.35 | ) | $ | (0.06 | ) | $ | (0.12 | ) | $ | (0.08 | ) | ||||

| Income (loss) per share from discontinued operations, net of tax | $ | 0.18 | $ | (0.03 | ) | $ | (0.01 | ) | $ | (0.04 | ) | |||||

| Weighted average number of common shares outstanding - basic and diluted | 12,027,040 | 12,000,000 | 12,000,000 | 12,000,000 | ||||||||||||

| December 31, | ||||||||||||

| September 30, 2016 | 2015 | 2014 | ||||||||||

| (unaudited) | ||||||||||||

| Selected Balance Sheet Data: | ||||||||||||

| Cash | 78,048 | 1,585,205 | 58,026 | |||||||||

| Working capital deficit | (780,580 | ) | (2,770,602 | ) | (3,124,430 | ) | ||||||

| Total assets | 1,907,141 | 2,874,791 | 1,597,575 | |||||||||

| Total liabilities | 1,267,839 | 4,655,211 | 3,609,020 | |||||||||

| Accumulated deficit | (26,188,096 | ) | (24,340,860 | ) | (22,736,847 | ) | ||||||

| Total stockholders’ deficiency | (3,045,441 | ) | (3,576,904 | ) | (2,011,445 | ) | ||||||

| 14 |

An investment in our common stock is speculative and illiquid and involves a high degree of risk, including the risk of a loss of your entire investment. You should carefully consider the risks and uncertainties described below and the other information contained in this prospectus before purchasing any of our common stock. The risks set forth below are not the only ones facing our Company. Additional risks and uncertainties presently unknown to us or that we currently consider immaterial or unlikely to occur could also adversely affect our business, operations and prospects. If any of the following risks actually materialize, our business, financial condition, prospects and operations could suffer. In such event, the value of our common stock could decline, and you could lose all or a substantial portion of the money that you pay for our common stock.

On July 22, 2016 our board of Directors approved a 2.1144-for-l forward split of our issued and outstanding shares of common stock and, on August 30, 2016, we filed the stock split with the Delaware Secretary of State. All shares and per share amounts have been adjusted to reflect the 2.114-for-l forward split of our issued and outstanding shares, retroactively.

Risks Related to Our Business and Industry

We have incurred significant losses since our inception, expert to incur significant losses in the future and may never achieve or sustain profitability.

We have historically incurred substantial net losses, including net losses of $1,847,236 for the nine months ended September 30, 2016, $1,604,013 for the year ended December 31, 2015 and $1,397,993 for the year ended December 31, 2014. As a result of our historical losses, we had an accumulated deficit of $26,188,096 as of September 30, 2016. Our losses have resulted principally from costs related to our research programs and the development of our products, as well as general and administrative costs relating to our operations. Currently, we are not generating significant revenue from operations, and we expect to incur losses for the foreseeable future as we seek to expand our commercial operations and incur increased sales and marketing costs. Additionally, we expect that our general and administrative expenses will increase due to the additional operational and reporting costs associated with being a public company. Due to the numerous risks and uncertainties associated with our commercialization efforts, we are unable to predict when we will become profitable, and we may never become profitable. Even if we do achieve profitability, we may be unable to sustain or increase profitability on a quarterly or annual basis. Our failure to achieve and subsequently sustain profitability could harm or business, financial condition, results of operations and cash flows.

As a result of our current lack of financial liquidity, our independent registered accounting firm has expressed substantial doubt regarding our ability to continue as a “going concern.”

As a result of our current lack of financial liquidity, the report of our independent registered accounting firm that accompanies our audited consolidated financial statements for the years ended December 31, 2015 and 2014, respectively, which are included as part of this prospectus, contains a statement contains going concern qualifications, and our independent registered public accounting firm expressed substantial doubt regarding our ability to continue as a going concern, meaning that we may be unable to continue in operation for the foreseeable future or realize assets and discharge liabilities in the ordinary course of operations. Our lack of sufficient liquidity could make it more difficult for us to secure additional financing or enter into strategic relationships on terms acceptable to us, if at all, and may materially and adversely affect the terms of any financing that we may obtain and our public stock price generally.

In order to continue as a going concern, will need to, among other things, achieve positive cash flow from operations and, if necessary, seek additional capital resources to satisfy our cash needs. Our plans to achieve positive cash flow include engaging in offerings of equity and/or debt securities and negotiating up-front and milestone payments on pipeline products under development and royalties from sales of our products which secure regulatory approval and any milestone payments associated with such approved products. Our failure to obtain additional capital would have an adverse effect on our financial position, results of operations, cash flows, and business prospects, and ultimately on our ability to continue as a going concern.

We currently have no sales and marketing infrastructure and if we are unable to successfully secure a sales and marketing partner or establish a sales and marketing infrastructure, we may be unable to commercialize our products and may never generate sufficient revenues to achieve or sustain profitability.

In order to commercialize products that are approved for commercial sales, we must either collaborate with third parties that have such commercial infrastructure or develop our own sales and marketing infrastructure. At present, we have no sales or marketing personnel and rely on collaborations with third parties for key aspects of our business.

| 15 |

There is a risk that we may not be able to maintain our current collaboration or to enter into additional collaborations on acceptable terms or at all, which would leave us unable to progress our business plan. We will face significant competition in seeking appropriate collaborators. Our ability to reach a definitive agreement for a collaboration will depend, among other things, upon our assessment of the collaborator’s resources and expertise, the terms and conditions of the proposed collaboration and the proposed collaborator’s evaluation of a number of factors. If we are unable to maintain or reach agreements with suitable collaborators on a timely basis, on acceptable terms, or at all, we may have to curtail the development of our product candidates, reduce or delay development programs, delay potential commercialization our product candidates or reduce the scope of any sales or marketing activities, or increase our expenditures and undertake development or commercialization activities at our own expense.

Moreover, even if we are able to maintain and/or enter into such collaborations, such collaborations may pose a number of risks, including the following:

| ● | collaborators may not perform their obligations as expected; | |

| ● | disagreements with collaborators, including disagreements over proprietary rights, contract interpretation or the preferred course of development, might cause delays or termination of the research, development or commercialization of our product candidate, might lead to additional responsibilities for us with respect to such product candidate, or might result in litigation or arbitration, any of which would be time-consuming and expensive; | |

| ● | collaborators could independently develop or be associated with products that compete directly or indirectly with our product candidate; | |

| ● | collaborators could have significant discretion in determining the efforts and resources that they will apply to our arrangements with them, and thus we may have limited or no control over the sales, marketing and distribution activities; | |

| ● | should our product candidate achieve regulatory approval, a collaborator with marketing and distribution rights to our product candidate may not commit sufficient resources to the marketing and distribution of such product; | |

| ● | collaborators may not properly maintain or defend our intellectual property rights or may use our proprietary information in such a way as to invite litigation that could jeopardize or invalidate our intellectual property or proprietary information or expose us to potential litigation; | |

| ● | collaborators may infringe the intellectual property rights of third parties, which may expose us to litigation and potential liability; and | |

| ● | collaborations may be terminated for the convenience of the collaborator and, if terminated, we could be required to either find alternative collaborators (which we may be unable to do) or raise additional capital to pursue further development or commercialization of our product candidate on our own. |

Our business would be materially or perhaps significantly harmed if any of the foregoing or similar risks comes to pass with respect to our key collaborations.

If we elect to establish a sales and marketing infrastructure, we may not realize a positive return on this investment. We will have to compete with established and well-funded medical device companies to recruit, hire, train and retain sales and marketing personnel. Once hired, the training process is lengthy because it requires significant education of new sales representatives to achieve the level of clinical competency with our products expected by specialists. Upon completion of the training, our sales representatives typically require lead time in the field to grow their network of accounts and achieve the productivity levels we expect them to reach in any individual territory. If we are unable to attract, motivate, develop and retain a sufficient number of qualified sales personnel, or if our sales representatives do not achieve the productivity levels in the time period we expect them to reach, our revenue will not grow at the rate we expect and our business, results of operations and financial condition will suffer. Also, to the extent we hire sales personnel from our competitors, we may be required to wait until applicable non-competition provisions have expired before deploying such personnel in restricted territories or incur costs to relocate personnel outside of such territories. In addition, we have been in the past, and may be in the future, subject to allegations that these new hires have been improperly solicited, or that they have divulged to us proprietary or other confidential information of their former employers. Any of these risks may adversely affect our ability to increase sales of our products. If we are unable to expand our sales and marketing capabilities, we may not be able to effectively commercialize our products, which would adversely affect our business, results of operations and financial condition.

| 16 |

We presently rely on our supply agreement with LMAT for substantially all of our revenue, and if the supply agreement were terminated it could have a material adverse effect on our revenue and results of operations.

In March, 2016, we entered into the supply agreement with LMAT for the exclusive distribution and sales rights to the ProCol® Vascular Bioprosthesis for Hemodialysis Vascular Access concomitant with ESRD. We have generated almost all of our total revenue since March 2016 pursuant to the supply agreement. If the supply agreement were terminated, or if either party became unable to perform their obligations under the supply agreement, it would have a material adverse effect on our revenue and results of operation.