United States Securities and Exchange Commission

Washington, D.C. 20549

FORM N-CSR

Certified Shareholder

Report of Registered Management Investment Companies

Investment Company Act file number 811-23121

Clayton

Street Trust

(Exact name of registrant as specified in charter)

151 Detroit Street, Denver,

Colorado 80206

(Address of principal executive offices) (Zip code)

Byron D. Hittle, 151 Detroit

Street, Denver, Colorado 80206

(Name and address of agent for service)

Registrant's telephone number, including area code: 303-333-3863

Date of fiscal year end: 12/31

Date of reporting period:

6/30/20

Item 1 - Reports to Shareholders

SEMIANNUAL REPORT June 30, 2020 | |||

Protective Life Dynamic Allocation Series - Conservative Portfolio | |||

Clayton Street Trust | |||

| |||

HIGHLIGHTS · Portfolio management perspective · Investment strategy behind your portfolio · Portfolio

performance, characteristics |

Table of Contents

Protective Life Dynamic Allocation Series - Conservative Portfolio

Protective Life Dynamic Allocation Series - Conservative Portfolio (unaudited)

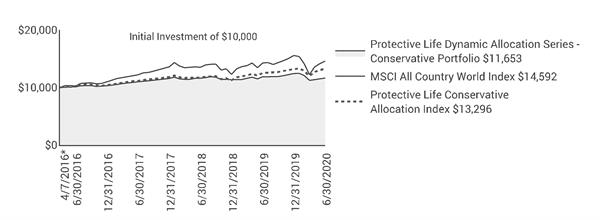

PERFORMANCE OVERVIEW

Protective Life Dynamic Allocation Series – Conservative Portfolio returned -6.40% during the six-month period ended June 30, 2020. This compares with a return of -6.25% for its primary benchmark, the MSCI All Country World IndexSM, and 0.25% for its secondary benchmark, the Protective Life Conservative Allocation Index, which is our internally calculated blended benchmark of 50% MSCI All Country World IndexSM and 50% Bloomberg Barclays U.S. Aggregate Bond Index.

MARKET ENVIRONMENT

Global financial markets were jarred during the period as the world’s economy slid toward recession in the wake of the COVID-19 pandemic. Both personal consumption and business investment – two engines of global growth – plummeted, as did trade flows. Monetary and fiscal authorities were quick to step in with rate cuts, asset purchases and income-support programs in an attempt to limit the economic damage. After sliding into a bear market at a record pace, global equities recovered much lost ground, led by the U.S. and Japan, with Europe and emerging markets trailing. Global bond indices rallied as government debt gained on the rate cuts. Investment-grade corporates finished in positive territory, but high-yield issues – like equities – were unable to make up for all of the early-year losses.

PERFORMANCE DISCUSSION

Underperformance was largely concentrated in the Portfolio’s allocation to large-cap U.S. equities during the peak of the late-winter sell-off. Small-cap U.S. equities also weighed on performance as smaller companies were especially impacted by the March sell-off, continuing their string of underperformance relative to large caps. The largest contributor was the Portfolio’s exposure to U.S. bond markets as interest rates fell considerably. The Portfolio’s allocation to growth-oriented, large-cap U.S. equities contributed to performance as well. A handful of these companies have taken on defensive characteristics given their exposure to secular –often technology-oriented – growth themes.

Thank you for investing in Protective Life Dynamic Allocation Series – Conservative Portfolio.

Asset Allocation - (% of Net Assets) | |||||

Investment Companies | 92.5% | ||||

Repurchase Agreements | 7.8% | ||||

Investments Purchased with Cash Collateral from Securities Lending | 5.6% | ||||

Other | (5.9)% | ||||

100.0% | |||||

Clayton Street Trust | 1 |

Protective Life Dynamic Allocation Series - Conservative Portfolio (unaudited)

Performance

See important disclosures on the next page. |

|

|

|

|

|

|

|

|

| |

|

|

|

|

|

|

|

|

| |

Average Annual Total Return - for the periods ended June 30, 2020 |

|

| Expense Ratios | ||||||

|

| Fiscal

| One

| Since |

|

| Total Annual Fund

| Net Annual Fund

| |

Protective Life Dynamic Allocation Series - Conservative Portfolio |

| -6.40% | -1.78% | 3.68% |

|

| 1.38% | 0.90% | |

MSCI All Country World Index |

| -6.25% | 2.11% | 9.34% |

|

|

|

| |

Protective Life Conservative Allocation Index |

| 0.25% | 5.97% | 6.97% |

|

|

|

| |

Morningstar Quartile - Class S Shares |

| - | 4th | 4th |

|

|

|

| |

Morningstar Ranking - based on total returns for Insurance Allocation--30% to 50% Equity Funds |

| - | 156/172 | 162/166 |

|

|

|

| |

Returns quoted are past performance and do not guarantee future results; current performance may be lower or higher. Investment returns and principal value will vary; there may be a gain or loss when shares are sold. For the most recent month-end performance call 800.456.6330.

Net expense ratios reflect expense waivers, if any, contractually agreed to through at least May 1, 2021.

Investing involves risk and it is possible to lose money by investing. Investment return and value will fluctuate in response to issuer, political, market and economic developments, which can affect a single issuer, issuers within an industry, economic sector or geographic region, or the market as a whole. Please see the prospectus for more information about risks, holdings and other details.

Performance of the Dynamic Allocation Series Portfolios depends on that of the underlying funds. They are subject to risk with respect to the aggregation of holdings of underlying funds which may result in increased volatility as a result of indirectly having concentrated assets in a particular industry, geographical sector, or single company.

No assurance can be given that the investment strategy will be successful under all or any market conditions. Janus Capital Management has limited prior experience using the proprietary methodology co-developed by Janus Capital Management and Protective Life Insurance Company. Although it is designed to achieve the Portfolios’ investment objectives, there is no guarantee that it will achieve the desired results. Because Janus Capital Management is the adviser to the Portfolios and to certain affiliated funds that may be held within the Portfolios, it is subject to certain potential conflicts of interest.

Returns do not reflect the deduction of fees, charges or expenses of any insurance product or qualified plan. If applied, returns would have been lower.

Returns include reinvestment of all dividends and distributions and do not reflect the deduction of taxes that a shareholder would pay on Portfolio distributions or redemptions of Portfolio shares. The returns do not include adjustments in accordance with generally accepted accounting principles required at the period end for financial reporting purposes.

Expenses waived or reimbursed during the first three years of operation may be recovered within three years of such waiver or reimbursement

2 | JUNE 30, 2020 |

Protective Life Dynamic Allocation Series - Conservative Portfolio (unaudited)

Performance

amount, if the expense ratio falls below certain limits.

When an expense waiver is in effect, it may have a material effect on the total return, and therefore the ranking for the period.

© 2020 Morningstar, Inc. All Rights Reserved.

There is no assurance that the investment process will consistently lead to successful investing.

See Notes to Schedule of Investments and Other Information for index definitions.

Index performance does not reflect the expenses of managing a portfolio as an index is unmanaged and not available for direct investment.

See “Useful Information About Your Portfolio Report.”

Effective May 1, 2020, Scott Weiner, Benjamin Wang and Zoey Zhu are Co-Portfolio Managers of the Portfolio.

*The Portfolio’s inception date – April 7, 2016

‡ As stated in the prospectus. See Financial Highlights for actual expense ratios during the reporting period.

Clayton Street Trust | 3 |

Protective Life Dynamic Allocation Series - Conservative Portfolio (unaudited)

Expense Examples

As a shareholder of the Portfolio, you incur two types of costs: (1) transaction costs and (2) ongoing costs, including management fees; 12b-1 distribution and shareholder servicing fees; transfer agent fees and expenses payable pursuant to the Transfer Agency Agreement; and other Portfolio expenses. This example is intended to help you understand your ongoing costs (in dollars) of investing in the Portfolio and to compare these costs with the ongoing costs of investing in other mutual funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds. The example is based upon an investment of $1,000 invested at the beginning of the period and held for the six-months indicated, unless noted otherwise in the table and footnotes below.

Actual Expenses

The information in the table under the heading “Actual” provides information about actual account values and actual expenses. You may use the information in these columns, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number under the heading entitled “Expenses Paid During Period” to estimate the expenses you paid on your account during the period.

Hypothetical Example for Comparison Purposes

The information in the table under the heading “Hypothetical (5% return before expenses)” provides information about hypothetical account values and hypothetical expenses based upon the Portfolio’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Portfolio’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Portfolio and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds. Additionally, for an analysis of the fees associated with an investment in the Portfolio or other similar funds, please visit www.finra.org/fundanalyzer.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transaction costs, such as any charges at the separate account level or contract level. These fees are fully described in the Portfolio’s prospectus. Therefore, the hypothetical examples are useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transaction costs were included, your costs would have been higher.

|

|

|

|

|

|

|

|

| ||

|

|

| Actual |

| Hypothetical

|

| ||||

| Beginning | Ending | Expenses |

| Beginning | Ending | Expenses | Net Annualized | ||

| $1,000.00 | $936.00 | $3.85 |

| $1,000.00 | $1,020.89 | $4.02 | 0.80% | ||

† | Expenses Paid During Period is equal to the Net Annualized Expense Ratio multiplied by the average account value over the period, multiplied by 182/366 (to reflect the one-half year period). Expenses in the examples include the effect of applicable fee waivers and/or expense reimbursements, if any. Had such waivers and/or reimbursements not been in effect, your expenses would have been higher. Please refer to the Notes to Financial Statements or the Portfolio’s prospectus for more information regarding waivers and/or reimbursements. | |||||||||

4 | JUNE 30, 2020 |

Protective Life Dynamic Allocation Series - Conservative Portfolio

Schedule of Investments (unaudited)

June 30, 2020

Shares or | Value | ||||||

Investment Companies – 92.5% | |||||||

Exchange-Traded Funds (ETFs) – 92.5% | |||||||

Franklin FTSE Japan# | 32,864 | $799,910 | |||||

Invesco QQQ Trust Series 1# | 12,224 | 3,026,663 | |||||

iShares Core U.S. Aggregate Bond | 141,809 | 16,763,242 | |||||

Janus Henderson Short Duration Income£ | 57,124 | 2,871,052 | |||||

JPMorgan BetaBuilders Developed Asia ex-Japan# | 36,996 | 828,710 | |||||

Vanguard S&P 500 | 23,455 | 6,647,851 | |||||

Total Investment Companies (cost $28,971,568) | 30,937,428 | ||||||

Repurchase Agreements – 7.8% | |||||||

Credit Agricole, New York, Joint repurchase agreement, 0.0600%, dated 6/30/20, maturing 7/1/20 to be repurchased at $2,600,004 collateralized by $2,528,767 in U.S. Treasuries 2.1250%, 12/31/22 with a value of $2,652,002 (cost $2,600,000) | $2,600,000 | 2,600,000 | |||||

Investments Purchased with Cash Collateral from Securities Lending – 5.6% | |||||||

Investment Companies – 4.5% | |||||||

Janus Henderson Cash Collateral Fund LLC, 0.0368%ºº,£ | 1,508,157 | 1,508,157 | |||||

Time Deposits – 1.1% | |||||||

Royal Bank of Canada, 0.0900%, 7/1/20 | $377,039 | 377,039 | |||||

Total Investments Purchased with Cash Collateral from Securities Lending (cost $1,885,196) | 1,885,196 | ||||||

Total Investments (total cost $33,456,764) – 105.9% | 35,422,624 | ||||||

Liabilities, net of Cash, Receivables and Other Assets – (5.9)% | (1,960,478) | ||||||

Net Assets – 100% | $33,462,146 | ||||||

Schedules of Affiliated Investments – (% of Net Assets)

Dividend Income(1) | Realized Gain/(Loss)(1) | Change in Unrealized Appreciation/ Depreciation(1) | Value at 6/30/20 | |||||||

Investment Companies - 8.6% | ||||||||||

Exchange-Traded Funds (ETFs) - 8.6% | ||||||||||

Janus Henderson Short Duration Income | $ | 22,404 | $ | (12,410) | $ | 86,755 | $ | 2,871,052 | ||

Investments Purchased with Cash Collateral from Securities Lending - 4.5% | ||||||||||

Investment Companies - 4.5% | ||||||||||

Janus Henderson Cash Collateral Fund LLC, 0.0368%ºº | 3,083∆ | - | - | 1,508,157 | ||||||

Total Affiliated Investments - 13.1% | $ | 25,487 | $ | (12,410) | $ | 86,755 | $ | 4,379,209 | ||

(1) For securities that were affiliated for a portion of the period ended June 30, 2020, this column reflects amounts for the entire period endedaaaa June 30, 2020 and not just the period in which the security was affiliated.

Value at 12/31/19 | Purchases | Sales Proceeds | Value at 6/30/20 | |||||||

Investment Companies - 8.6% | ||||||||||

Exchange-Traded Funds (ETFs) - 8.6% | ||||||||||

Janus Henderson Short Duration Income | 496 | 5,809,047 | (3,012,836) | 2,871,052 | ||||||

Investments Purchased with Cash Collateral from Securities Lending - 4.5% | ||||||||||

Investment Companies - 4.5% | ||||||||||

Janus Henderson Cash Collateral Fund LLC, 0.0368%ºº | - | 32,149,503 | (30,641,346) | 1,508,157 | ||||||

See Notes to Schedule of Investments and Other Information and Notes to Financial Statements. | |

Clayton Street Trust | 5 |

Protective Life Dynamic Allocation Series - Conservative Portfolio

Notes to Schedule of Investments and Other Information (unaudited)

MSCI All Country World IndexSM | MSCI All Country World IndexSM reflects the equity market performance of global developed and emerging markets. |

Protective Life Conservative Allocation Index | Protective Life Conservative Allocation Index is an internally-calculated, hypothetical combination of total returns from the MSCI All Country World IndexSM (50%) and the Bloomberg Barclays U.S. Aggregate Bond Index (50%). |

LLC | Limited Liability Company |

ºº | Rate shown is the 7-day yield as of June 30, 2020. |

# | Loaned security; a portion of the security is on loan at June 30, 2020. |

£ | The Portfolio may invest in certain securities that are considered affiliated companies. As defined by the Investment Company Act of 1940, as amended, an affiliated company is one in which the Portfolio owns 5% or more of the outstanding voting securities, or a company which is under common ownership or control. |

∆ | Net of income paid to the securities lending agent and rebates paid to the borrowing counterparties. |

The following is a summary of the inputs that were used to value the Portfolio’s investments in securities and other financial instruments as of June 30, 2020. See Notes to Financial Statements for more information. | ||||||||||||

Valuation Inputs Summary | ||||||||||||

Level 2 - | Level 3 - | |||||||||||

Level 1 - | Other Significant | Significant | ||||||||||

Quoted Prices | Observable Inputs | Unobservable Inputs | ||||||||||

Assets | ||||||||||||

Investments In Securities: | ||||||||||||

Investment Companies | $ | 30,937,428 | $ | - | $ | - | ||||||

Repurchase Agreements | - | 2,600,000 | - | |||||||||

Investments Purchased with Cash Collateral from Securities Lending | - | 1,885,196 | - | |||||||||

Total Assets | $ | 30,937,428 | $ | 4,485,196 | $ | - | ||||||

6 | JUNE 30, 2020 |

Protective Life Dynamic Allocation Series - Conservative Portfolio

Statement of Assets and Liabilities (unaudited)

June 30, 2020

|

|

|

|

|

|

|

Assets: |

|

|

|

| ||

| Unaffiliated investments, at value(1)(2) |

| $ | 28,443,415 |

| |

| Affiliated investments, at value(3) |

|

| 4,379,209 |

| |

| Repurchase agreements, at value(4) |

|

| 2,600,000 |

| |

| Cash |

|

| 45,794 |

| |

| Receivables: |

|

|

|

| |

|

| Investments sold |

|

| 292,912 |

|

|

| Dividends |

|

| 38,463 |

|

| Other assets |

|

| 890 |

| |

Total Assets |

|

| 35,800,683 |

| ||

Liabilities: |

|

|

|

| ||

| Collateral for securities loaned (Note 2) |

|

| 1,885,196 |

| |

| Payables: |

|

| — |

| |

|

| Portfolio shares repurchased |

|

| 300,425 |

|

|

| Investments purchased |

|

| 105,960 |

|

|

| Professional fees |

|

| 13,147 |

|

|

| 12b-1 Distribution and shareholder servicing fees |

|

| 6,531 |

|

|

| Transfer agent fees and expenses |

|

| 2,809 |

|

|

| Non-interested Trustees' fees and expenses |

|

| 2,472 |

|

|

| Custodian fees |

|

| 1,434 |

|

|

| Advisory fees |

|

| 1,281 |

|

|

| Affiliated portfolio administration fees payable |

|

| 1,041 |

|

|

| Accrued expenses and other payables |

|

| 18,241 |

|

Total Liabilities |

|

| 2,338,537 |

| ||

Net Assets |

| $ | 33,462,146 |

| ||

Net Assets Consist of: |

|

|

|

| ||

| Capital (par value and paid-in surplus) |

| $ | 33,432,069 |

| |

| Total distributable earnings (loss) |

|

| 30,077 |

| |

Total Net Assets |

| $ | 33,462,146 |

| ||

Net Assets |

| $ | 33,462,146 |

| ||

| Shares Outstanding, $0.01 Par Value (unlimited shares authorized) |

|

| 3,081,015 |

| |

Net Asset Value Per Share |

| $ | 10.86 |

| ||

(1) Includes cost of $26,564,307. (2) Includes $1,846,643 of securities on loan. See Note 2 in Notes to Financial Statements. (3) Includes cost of $4,292,457. (4) Includes cost of repurchase agreements of $2,600,000. |

See Notes to Financial Statements. | |

Clayton Street Trust | 7 |

Protective Life Dynamic Allocation Series - Conservative Portfolio

Statement of Operations (unaudited)

For the period ended June 30, 2020

|

|

|

|

|

|

Investment Income: |

|

|

| ||

| Dividends | $ | 230,324 |

| |

| Dividends from affiliates |

| 22,404 |

| |

| Affiliated securities lending income, net |

| 3,083 |

| |

| Unaffiliated securities lending income, net |

| 393 |

| |

| Interest |

| 368 |

| |

Total Investment Income |

| 256,572 |

| ||

Expenses: |

|

|

| ||

| Advisory fees |

| 59,800 |

| |

| 12b-1 Distribution and shareholder servicing fees |

| 37,375 |

| |

| Transfer agent administrative fees and expenses |

| 14,950 |

| |

| Other transfer agent fees and expenses |

| 419 |

| |

| Professional fees |

| 24,923 |

| |

| Non-affiliated portfolio administration fees |

| 21,479 |

| |

| Affiliated portfolio administration fees |

| 6,160 |

| |

| Non-interested Trustees’ fees and expenses |

| 4,876 |

| |

| Shareholder reports expense |

| 3,371 |

| |

| Custodian fees |

| 3,251 |

| |

| Other expenses |

| 5,011 |

| |

Total Expenses |

| 181,615 |

| ||

Less: Excess Expense Reimbursement and Waivers |

| (61,027) |

| ||

Net Expenses |

| 120,588 |

| ||

Net Investment Income/(Loss) |

| 135,984 |

| ||

Net Realized Gain/(Loss) on Investments: |

|

|

| ||

| Investments |

| (1,536,918) |

| |

| Investments in affiliates |

| (12,410) |

| |

Total Net Realized Gain/(Loss) on Investments |

| (1,549,328) |

| ||

Change in Unrealized Net Appreciation/Depreciation: |

|

|

| ||

| Investments |

| (649,097) |

| |

| Investments in affiliates |

| 86,755 |

| |

Total Change in Unrealized Net Appreciation/Depreciation |

| (562,342) |

| ||

Net Increase/(Decrease) in Net Assets Resulting from Operations | $ | (1,975,686) |

| ||

|

|

|

|

|

|

See Notes to Financial Statements. | |

8 | JUNE 30, 2020 |

Protective Life Dynamic Allocation Series - Conservative Portfolio

Statements of Changes in Net Assets

|

|

|

|

|

|

|

|

|

|

|

| Period ended |

| Year ended |

| ||

Operations: |

|

|

|

|

|

| ||

| Net investment income/(loss) | $ | 135,984 |

| $ | 555,171 |

| |

| Net realized gain/(loss) on investments |

| (1,549,328) |

|

| (268,942) |

| |

| Change in unrealized net appreciation/depreciation |

| (562,342) |

|

| 2,583,984 |

| |

Net Increase/(Decrease) in Net Assets Resulting from Operations |

| (1,975,686) |

|

| 2,870,213 |

| ||

Dividends and Distributions to Shareholders |

|

|

|

|

|

| ||

| Dividends and Distributions to Shareholders |

| (334,357) |

|

| (1,012,114) |

| |

Net Decrease from Dividends and Distributions to Shareholders |

| (334,357) |

|

| (1,012,114) |

| ||

Capital Shares Transactions |

| 4,339,308 |

|

| 1,588,351 |

| ||

Net Increase/(Decrease) in Net Assets |

| 2,029,265 |

|

| 3,446,450 |

| ||

Net Assets: |

|

|

|

|

|

| ||

| Beginning of period |

| 31,432,881 |

|

| 27,986,431 |

| |

| End of period | $ | 33,462,146 |

| $ | 31,432,881 |

| |

|

|

|

|

|

|

|

|

|

See Notes to Financial Statements. | |

Clayton Street Trust | 9 |

Protective Life Dynamic Allocation Series - Conservative Portfolio

Financial Highlights

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

For a share outstanding during the period ended June 30, 2020 (unaudited) and the year or period ended December 31 | 2020 |

|

| 2019 |

|

| 2018 |

|

| 2017 |

|

| 2016(1) |

| ||||

| Net Asset Value, Beginning of Period |

| $11.73 |

|

| $11.04 |

|

| $11.42 |

|

| $10.28 |

|

| $10.00 |

| ||

| Income/(Loss) from Investment Operations: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||

|

| Net investment income/(loss)(2) |

| 0.05 |

|

| 0.21 |

|

| 0.17 |

|

| 0.16 |

|

| 0.12 |

| |

|

| Net realized and unrealized gain/(loss) |

| (0.80) |

|

| 0.87 |

|

| (0.40) |

|

| 1.11 |

|

| 0.16 |

| |

| Total from Investment Operations |

| (0.75) |

|

| 1.08 |

|

| (0.23) |

|

| 1.27 |

|

| 0.28 |

| ||

| Less Dividends and Distributions: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||

|

| Dividends (from net investment income) |

| (0.08) |

|

| (0.18) |

|

| (0.14) |

|

| (0.13) |

|

| — |

| |

|

| Distributions (from capital gains) |

| (0.04) |

|

| (0.21) |

|

| (0.01) |

|

| — |

|

| — |

| |

| Total Dividends and Distributions |

| (0.12) |

|

| (0.39) |

|

| (0.15) |

|

| (0.13) |

|

| — |

| ||

| Net Asset Value, End of Period |

| $10.86 |

|

| $11.73 |

|

| $11.04 |

|

| $11.42 |

|

| $10.28 |

| ||

| Total Return* |

| (6.40)% |

|

| 9.97% |

|

| (1.99)% |

|

| 12.37% |

|

| 2.80% |

| ||

| Net Assets, End of Period (in thousands) |

| $33,462 |

|

| $31,433 |

|

| $27,986 |

|

| $19,129 |

|

| $8,566 |

| ||

| Average Net Assets for the Period (in thousands) |

| $30,237 |

|

| $29,980 |

|

| $25,401 |

|

| $13,847 |

|

| $4,740 |

| ||

| Ratios to Average Net Assets**: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||

|

| Ratio of Gross Expenses(3) |

| 1.21% |

|

| 1.27% |

|

| 1.24% |

|

| 1.54% |

|

| 4.55% |

| |

|

| Ratio of Net Expenses (After Waivers and Expense Offsets)(3) |

| 0.80% |

|

| 0.79% |

|

| 0.79% |

|

| 0.76% |

|

| 0.79% |

| |

|

| Ratio of Net Investment Income/(Loss)(3) |

| 0.90% |

|

| 1.85% |

|

| 1.48% |

|

| 1.49% |

|

| 1.67% |

| |

| Portfolio Turnover Rate |

| 98% |

|

| 135% |

|

| 73% |

|

| 13% |

|

| 73% |

| ||

* Total return includes adjustments in accordance with generally accepted accounting principles required at the year or period end and are not annualized for periods of less than one full year. Total return does not include fees, charges, or expenses imposed by the variable annuity contracts for which Clayton Street Trust serves as an underlying investment vehicle. ** Annualized for periods of less than one full year. (1) Period from April 7, 2016 (inception date) through December 31, 2016. (2) Per share amounts are calculated based on average shares outstanding during the year or period. (3) Ratios do not include indirect expenses of the underlying funds and/or investment companies in which the Portfolio invests. |

See Notes to Financial Statements. | |

10 | JUNE 30, 2020 |

Protective Life Dynamic Allocation Series - Conservative Portfolio

Notes to Financial Statements (unaudited)

1. Organization and Significant Accounting Policies

Protective Life Dynamic Allocation Series - Conservative Portfolio (the “Portfolio”) is a series of Clayton Street Trust (the “Trust”), which is organized as a Delaware statutory trust and is registered under the Investment Company Act of 1940, as amended (the “1940 Act”), as an open-end management investment company, and therefore has applied the specialized accounting and reporting guidance in Financial Accounting Standards Board (“FASB”) Accounting Standards Codification (“ASC”) Topic 946. The Portfolio operates as a “fund of funds,” meaning substantially all of the Portfolio’s assets may be invested in exchange-traded funds (the “underlying funds”). The Trust offers three portfolios with differing investment objectives and policies. The Portfolio seeks total return through income and growth of capital, balanced by capital preservation. The Portfolio is classified as diversified, as defined in the 1940 Act.

The Portfolio currently offers one class of shares. The shares are offered in connection with investment in and payments under variable annuity contracts issued exclusively by Protective Life Insurance Company and its affiliates ("Protective Life").

Underlying Funds

During the period, the Portfolio invested in a dynamic portfolio of exchange-traded funds across seven different equity asset classes, as well as fixed-income investments, and a short duration allocation that may be comprised of cash, money market instruments and short duration exchange-traded funds. The equity asset classes are adjusted weekly based on market conditions pursuant to a proprietary, quantitative-based allocation program. Over the long term, and when fully invested, the Portfolio seeks to maintain an asset allocation of approximately 50% global equity investments and 50% fixed income investments. Additional details and descriptions of the investment objectives of each of the potential underlying funds are available in the Portfolio's prospectus.

The following accounting policies have been followed by the Portfolio and are in conformity with United States of America generally accepted accounting principles ("US GAAP").

Investment Valuation

Securities held by the Portfolio, including the underlying funds, are valued in accordance with policies and procedures established by and under the supervision of the Trustees (the “Valuation Procedures”). The values of the Portfolio's investments in the underlying funds are based upon the closing price of such underlying funds on the applicable exchange. Most debt securities are valued in accordance with the evaluated bid price supplied by the pricing service that is intended to reflect market value. The evaluated bid price supplied by the pricing service is an evaluation that may consider factors such as security prices, yields, maturities, and ratings. Certain short-term securities maturing within 60 days or less may be evaluated and valued on an amortized cost basis provided that the amortized cost determined approximates market value. Securities for which market quotations or evaluated prices are not readily available or are deemed by Janus Capital Management LLC (“Janus Capital”) to be unreliable are valued at fair value determined in good faith under the Valuation Procedures. Circumstances in which fair value pricing may be utilized include, but are not limited to: (i) a significant event that may affect the securities of a single issuer, such as a merger, bankruptcy, or significant issuer-specific development; (ii) an event that may affect an entire market, such as a natural disaster or significant governmental action; (iii) a nonsignificant event such as a market closing early or not opening, or a security trading halt; and (iv) pricing of a nonvalued security and a restricted or nonpublic security. Special valuation considerations may apply with respect to “odd-lot” fixed-income transactions which, due to their small size, may receive evaluated prices by pricing services which reflect a large block trade and not what actually could be obtained for the odd-lot position.

Valuation Inputs Summary

FASB ASC 820, Fair Value Measurements and Disclosures (“ASC 820”), defines fair value, establishes a framework for measuring fair value, and expands disclosure requirements regarding fair value measurements. This standard emphasizes that fair value is a market-based measurement that should be determined based on the assumptions that market participants would use in pricing an asset or liability and establishes a hierarchy that prioritizes inputs to valuation techniques used to measure fair value. These inputs are summarized into three broad levels:

Level 1 – Unadjusted quoted prices in active markets the Portfolio has the ability to access for identical assets or liabilities.

Level 2 – Observable inputs other than unadjusted quoted prices included in Level 1 that are observable for the asset or liability either directly or indirectly. These inputs may include quoted prices for the identical instrument on

Clayton Street Trust | 11 |

Protective Life Dynamic Allocation Series - Conservative Portfolio

Notes to Financial Statements (unaudited)

an inactive market, prices for similar instruments, interest rates, prepayment speeds, credit risk, yield curves, default rates and similar data.

Assets or liabilities categorized as Level 2 in the hierarchy generally include: debt securities fair valued in accordance with the evaluated bid or ask prices supplied by a pricing service; securities traded on OTC markets and listed securities for which no sales are reported that are fair valued at the latest bid price (or yield equivalent thereof) obtained from one or more dealers transacting in a market for such securities or by a pricing service approved by the Portfolio’s Trustees; and certain short-term debt securities with maturities of 60 days or less that are fair valued at amortized cost. Other securities that may be categorized as Level 2 in the hierarchy include, but are not limited to, preferred stocks, bank loans, swaps, investments in unregistered investment companies, options, and forward contracts.

Level 3 – Unobservable inputs for the asset or liability to the extent that relevant observable inputs are not available, representing the Portfolio’s own assumptions about the assumptions that a market participant would use in valuing the asset or liability, and that would be based on the best information available.

The Portfolio classifies each of its investments in underlying funds as Level 1, without consideration as to the classification level of the specific investments held by the underlying funds. There have been no significant changes in valuation techniques used in valuing any such positions held by the Portfolio since the beginning of the fiscal year.

The inputs or methodology used for fair valuing securities are not necessarily an indication of the risk associated with investing in those securities. The summary of inputs used as of June 30, 2020 to fair value the Portfolio’s investments in securities and other financial instruments is included in the “Valuation Inputs Summary” in the Notes to Schedule of Investments and Other Information.

Investment Transactions and Investment Income

Investment transactions are accounted for as of the date purchased or sold (trade date). Dividend income is recorded on the ex dividend date. Any distributions from the underlying funds are recorded in accordance with the character of the distributions as designated by the underlying funds. Interest income is recorded daily on the accrual basis and includes amortization of premiums and accretion of discounts. The Portfolio classifies gains and losses on prepayments received as an adjustment to interest income. Debt securities may be placed in non-accrual status and related interest income may be reduced by stopping current accruals and writing off interest receivables when collection of all or a portion of interest has become doubtful. Gains and losses are determined on the identified cost basis, which is the same basis used for federal income tax purposes.

Expenses

The Portfolio bears expenses incurred specifically on its behalf. Additionally, the Portfolio, as a shareholder in the underlying funds, will also indirectly bear its pro rata share of the expenses incurred by the underlying funds.

Estimates

The preparation of financial statements in conformity with US GAAP requires management to make estimates and assumptions that affect the reported amount of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements, and the reported amounts of income and expenses during the reporting period. Actual results could differ from those estimates.

Indemnifications

In the normal course of business, the Portfolio may enter into contracts that contain provisions for indemnification of other parties against certain potential liabilities. The Portfolio’s maximum exposure under these arrangements is unknown, and would involve future claims that may be made against the Portfolio that have not yet occurred. Currently, the risk of material loss from such claims is considered remote.

Dividends and Distributions

The Portfolio may make semiannual distributions of substantially all of its investment income and an annual distribution of its net realized capital gains (if any).

Federal Income Taxes

The Portfolio intends to continue to qualify as a regulated investment company and distribute all of its taxable income in accordance with the requirements of Subchapter M of the Internal Revenue Code. Management has analyzed the Portfolio’s tax positions taken for all open federal income tax years, generally a three-year period, and has concluded

12 | JUNE 30, 2020 |

Protective Life Dynamic Allocation Series - Conservative Portfolio

Notes to Financial Statements (unaudited)

that no provision for federal income tax is required in the Portfolio’s financial statements. The Portfolio is not aware of any tax positions for which it is reasonably possible that the total amounts of unrecognized tax benefits will significantly change in the next twelve months.

2. Other Investments and Strategies

Additional Investment Risk

In the aftermath of the 2007-2008 financial crisis, the financial sector experienced reduced liquidity in credit and other fixed-income markets, and an unusually high degree of volatility, both domestically and internationally. In response to the crisis, the United States and certain foreign governments, along with the U.S. Federal Reserve and certain foreign central banks, took a number of unprecedented steps designed to support the financial markets. For example, the enactment of the Dodd-Frank Act in 2010 provided for widespread regulation of financial institutions, consumer financial products and services, broker-dealers, over-the-counter derivatives, investment advisers, credit rating agencies, and mortgage lending, which expanded federal oversight in the financial sector, including the investment management industry. More recently, in response to the COVID-19 pandemic, the U.S. government and the Federal Reserve, as well as certain foreign governments and central banks, have taken extraordinary actions to support local and global economies and the financial markets, including reducing interest rates to record low levels. The withdrawal of this support, a failure of measures put in place in response to such economic uncertainty, or investor perception that such efforts were not sufficient could each negatively affect financial markets generally, and the value and liquidity of specific securities. In addition, policy and legislative changes in the United States and in other countries continue to impact many aspects of financial regulation.

Widespread disease, including pandemics and epidemics, and natural or environmental disasters, such as earthquakes, fires, floods, hurricanes, tsunamis and weather-related phenomena generally, have been and can be highly disruptive to economies and markets, adversely impacting individual companies, sectors, industries, markets, currencies, interest and inflation rates, credit ratings, investor sentiment, and other factors affecting the value of a Portfolio’s investments. Economies and financial markets throughout the world have become increasingly interconnected, which increases the likelihood that events or conditions in one region or country will adversely affect markets or issuers in other regions or countries, including the United States. These disruptions could prevent a Portfolio from executing advantageous investment decisions in a timely manner and negatively impact a Portfolio’s ability to achieve its investment objective(s). Any such event(s) could have a significant adverse impact on the value of a Portfolio. In addition, these disruptions could also impair the information technology and other operational systems upon which the Portfolio’s service providers, including Janus Capital, rely, and could otherwise disrupt the ability of employees of the Portfolio’s service providers to perform essential tasks on behalf of the Portfolio.

A number of countries in the European Union (“EU”) have experienced, and may continue to experience, severe economic and financial difficulties. In particular, many EU nations are susceptible to economic risks associated with high levels of debt. Many non-governmental issuers, and even certain governments, have defaulted on, or been forced to restructure, their debts. Many other issuers have faced difficulties obtaining credit or refinancing existing obligations. Financial institutions have in many cases required government or central bank support, have needed to raise capital, and/or have been impaired in their ability to extend credit. As a result, financial markets in the EU have experienced extreme volatility and declines in asset values and liquidity. Responses to these financial problems by European governments, central banks, and others, including austerity measures and reforms, may not work, may result in social unrest, and may limit future growth and economic recovery or have other unintended consequences. The risk of investing in securities in the European markets may also be heightened due to the referendum in which the United Kingdom voted to exit the EU (known as “Brexit”). The United Kingdom formally left the EU on January 31, 2020 and entered into an eleven-month transition period, during which the United Kingdom will remain subject to EU laws and regulations. There is considerable uncertainty relating to the potential consequences of the United Kingdom’s exit and how negotiations for new trade agreements will be conducted or concluded.

Certain areas of the world have historically been prone to and economically sensitive to environmental events such as, but not limited to, hurricanes, earthquakes, typhoons, flooding, tidal waves, tsunamis, erupting volcanoes, wildfires or droughts, tornadoes, mudslides, or other weather-related phenomena. Such disasters, and the resulting physical or economic damage, could have a severe and negative impact on the Portfolio’s or an underlying fund's investment portfolio and, in the longer term, could impair the ability of issuers in which the Portfolio or an underlying fund invests to conduct their businesses as they would under normal conditions. Adverse weather conditions may also have a

Clayton Street Trust | 13 |

Protective Life Dynamic Allocation Series - Conservative Portfolio

Notes to Financial Statements (unaudited)

particularly significant negative effect on issuers in the agricultural sector and on insurance and reinsurance companies that insure or reinsure against the impact of natural disasters.

Counterparties

Portfolio transactions involving a counterparty are subject to the risk that the counterparty or a third party will not fulfill its obligation to the Portfolio (“counterparty risk”). Counterparty risk may arise because of the counterparty’s financial condition (i.e., financial difficulties, bankruptcy, or insolvency), market activities and developments, or other reasons, whether foreseen or not. A counterparty’s inability to fulfill its obligation may result in significant financial loss to the Portfolio. The Portfolio may be unable to recover its investment from the counterparty or may obtain a limited recovery, and/or recovery may be delayed. The extent of the Portfolio’s exposure to counterparty risk with respect to financial assets and liabilities approximates its carrying value.

The Portfolio may be exposed to counterparty risk through its investments in certain securities, including, but not limited to, repurchase agreements and debt securities. The Portfolio intends to enter into financial transactions with counterparties that Janus Capital believes to be creditworthy at the time of the transaction. There is always the risk that Janus Capital’s analysis of a counterparty’s creditworthiness is incorrect or may change due to market conditions. To the extent that the Portfolio focuses its transactions with a limited number of counterparties, it will have greater exposure to the risks associated with one or more counterparties.

Exchange-Traded Funds

ETFs are typically open-end investment companies, which may be actively managed or passively managed. Passively managed ETFs generally seek to track the performance of a specific index. ETFs are traded on a national securities exchange at market prices that may vary from the net asset value per share (“NAV”) of their underlying investments. Accordingly, there may be times when an ETF trades at a premium or discount to its NAV. As a result, the Portfolio may pay more or less than NAV when it buys ETF shares, and may receive more or less than NAV when it sells those shares. ETFs also involve the risk that an active trading market for an ETF’s shares may not develop or be maintained. Similarly, because the value of ETF shares depends on the demand in the market, the Portfolio may not be able to purchase or sell an ETF at the most optimal time, which could adversely affect the Portfolio’s performance. In addition, ETFs that track particular indices may be unable to match the performance of such underlying indices due to the temporary unavailability of certain index securities in the secondary market or other factors, such as discrepancies with respect to the weighting of securities.

Offsetting Assets and Liabilities

The Portfolio presents gross and net information about transactions that are either offset in the financial statements or subject to an enforceable master netting arrangement or similar agreement with a designated counterparty, regardless of whether the transactions are actually offset in the Statement of Assets and Liabilities.

The following table presents gross amounts of recognized assets and/or liabilities and the net amounts after deducting collateral that has been pledged by counterparties or has been pledged to counterparties (if applicable). For corresponding information grouped by type of instrument, see the Portfolio's Schedule of Investments.

Offsetting of Financial Assets and Derivative Assets | |||||||||

Gross Amounts | |||||||||

of Recognized | Offsetting Asset | Collateral | |||||||

Counterparty | Assets | or Liability(a) | Pledged(b) | Net Amount | |||||

Credit Agricole, New York | $ | 2,600,000 | $ | — | $ | (2,600,000) | $ | — | |

JPMorgan Chase Bank, National Association | 1,846,643 | — | (1,846,643) | — | |||||

Total | $ | 4,446,643 | $ | — | $ | (4,446,643) | $ | — | |

(a) | Represents the amount of assets or liabilities that could be offset with the same counterparty under master netting or similar agreements that management elects not to offset on the Statement of Assets and Liabilities. | ||||||||

(b) | Collateral pledged is limited to the net outstanding amount due to/from an individual counterparty. The actual collateral amounts pledged may exceed these amounts and may fluctuate in value. | ||||||||

14 | JUNE 30, 2020 |

Protective Life Dynamic Allocation Series - Conservative Portfolio

Notes to Financial Statements (unaudited)

All repurchase agreements are transacted under legally enforceable master repurchase agreements that give the Portfolio, in the event of default by the counterparty, the right to liquidate securities held and to offset receivables and payables with the counterparty. For financial reporting purposes, the Portfolio does not offset financial instruments' payables and receivables and related collateral on the Statement of Assets and Liabilities. Repurchase agreements held by the Portfolio are fully collateralized, and such collateral is in the possession of the Portfolio’s custodian or, for tri-party agreements, the custodian designated by the agreement. The collateral is evaluated daily to ensure its market value exceeds the current market value of the repurchase agreements, including accrued interest.

JPMorgan Chase Bank, National Association acts as securities lending agent and a limited purpose custodian or subcustodian to receive and disburse cash balances and cash collateral, hold short-term investments, hold collateral, and perform other custodial functions in accordance with the Non-Custodial Securities Lending Agreement. For financial reporting purposes, the Portfolio does not offset financial instruments' payables and receivables and related collateral on the Statement of Assets and Liabilities. Securities on loan will be continuously secured by collateral which may consist of cash, U.S. Government securities, domestic and foreign short-term debt instruments, letters of credit, time deposits, repurchase agreements, money market mutual funds or other money market accounts, or such other collateral as permitted by the Securities and Exchange Commission (the “SEC”). See “Securities Lending” in the “Notes to Financial Statements” for additional information.

Repurchase Agreements

The Portfolio and other funds advised by Janus Capital or its affiliates may transfer daily uninvested cash balances into one or more joint trading accounts. Assets in the joint trading accounts are invested in money market instruments and the proceeds are allocated to the participating funds on a pro rata basis.

Repurchase agreements held by the Portfolio are fully collateralized, and such collateral is in the possession of the Portfolio’s custodian or, for tri-party agreements, the custodian designated by the agreement. The collateral is evaluated daily to ensure its market value exceeds the current market value of the repurchase agreements, including accrued interest. In the event of default on the obligation to repurchase, the Portfolio has the right to liquidate the collateral and apply the proceeds in satisfaction of the obligation. In the event of default or bankruptcy by the other party to the agreement, realization and/or retention of the collateral or proceeds may be subject to legal proceedings.

Securities Lending

Under procedures adopted by the Trustees, the Portfolio may seek to earn additional income by lending securities to certain qualified broker-dealers and institutions. Effective January 8, 2020, JPMorgan Chase Bank, National Association replaced Deutsche Bank AG as securities lending agent for the Portfolio. JPMorgan Chase Bank, National Association acts as securities lending agent and a limited purpose custodian or subcustodian to receive and disburse cash balances and cash collateral, hold short-term investments, hold collateral, and perform other custodial functions in accordance with the Non-Custodial Securities Lending Agreement. The Portfolio may lend portfolio securities in an amount equal to up to 1/3 of its total assets as determined at the time of the loan origination. There is the risk of delay in recovering a loaned security or the risk of loss in collateral rights if the borrower fails financially. In addition, Janus Capital makes efforts to balance the benefits and risks from granting such loans. All loans will be continuously secured by collateral which may consist of cash, U.S. Government securities, domestic and foreign short-term debt instruments, letters of credit, time deposits, repurchase agreements, money market mutual funds or other money market accounts, or such other collateral as permitted by the SEC. If the Portfolio is unable to recover a security on loan, the Portfolio may use the collateral to purchase replacement securities in the market. There is a risk that the value of the collateral could decrease below the cost of the replacement security by the time the replacement investment is made, resulting in a loss to the Portfolio. In certain circumstances individual loan transactions could yield negative returns.

Upon receipt of cash collateral, Janus Capital may invest it in affiliated or non-affiliated cash management vehicles, whether registered or unregistered entities, as permitted by the 1940 Act and rules promulgated thereunder. Janus Capital currently intends to primarily invest the cash collateral in a cash management vehicle for which Janus Capital serves as investment adviser, Janus Henderson Cash Collateral Fund LLC. An investment in Janus Henderson Cash Collateral Fund LLC is generally subject to the same risks that shareholders experience when investing in similarly structured vehicles, such as the potential for significant fluctuations in assets as a result of the purchase and redemption activity of the securities lending program, a decline in the value of the collateral, and possible liquidity issues. Such risks may delay the return of the cash collateral and cause the Portfolio to violate its agreement to return the cash collateral to a borrower in a timely manner. As adviser to the Portfolio and Janus Henderson Cash Collateral Fund LLC, Janus Capital has an inherent conflict of interest as a result of its fiduciary duties to both the Portfolio and Janus

Clayton Street Trust | 15 |

Protective Life Dynamic Allocation Series - Conservative Portfolio

Notes to Financial Statements (unaudited)

Henderson Cash Collateral Fund LLC. Additionally, Janus Capital receives an investment advisory fee of 0.05% for managing Janus Henderson Cash Collateral Fund LLC and therefore may have an incentive to allocate collateral to the Janus Henderson Cash Collateral Fund LLC rather than to other collateral management options for which Janus Capital does not receive compensation.

The value of the collateral must be at least 102% of the market value of the loaned securities that are denominated in U.S. dollars and 105% of the market value of the loaned securities that are not denominated in U.S. dollars. Loaned securities and related collateral are marked-to-market each business day based upon the market value of the loaned securities at the close of business, employing the most recent available pricing information. Collateral levels are then adjusted based on this mark-to-market evaluation.

The cash collateral invested by Janus Capital is disclosed in the Schedule of Investments (if applicable).

Income earned from the investment of the cash collateral, net of rebates paid to, or fees paid by, borrowers and less the fees paid to the lending agent are included as “Affiliated securities lending income, net” on the Statement of Operations. As of June 30, 2020, securities lending transactions accounted for as secured borrowings with an overnight and continuous contractual maturity are $1,846,643. Gross amounts of recognized liabilities for securities lending (collateral received) as of June 30, 2020 is $1,885,196, resulting in the net amount due to the counterparty of $38,553.

3. Investment Advisory Agreements and Other Transactions with Affiliates

The Portfolio pays Janus Capital an investment advisory fee which is calculated daily and paid monthly. The Portfolio’s contractual investment advisory fee rate (expressed as an annual rate) is 0.40%.

Janus Capital has contractually agreed to waive the advisory fee payable by the Portfolio or reimburse expenses in an amount equal to the amount, if any, that the Portfolio’s normal operating expenses including the investment advisory fee, but excluding the 12b-1 distribution and shareholder servicing fees, administrative services fees payable pursuant to the Transfer Agency Agreement, brokerage commissions, interest, dividends, taxes and extraordinary expenses, exceed the annual rate of 0.55% of the Portfolio’s average daily net assets. Janus Capital has agreed to continue the waivers until at least May 1, 2021. If applicable, amounts reimbursed to the Portfolio by Janus Capital are disclosed as “Excess Expense Reimbursement and Waivers” on the Statement of Operations.

Janus Capital may recover from the Portfolio fees and expenses previously waived or reimbursed during the period beginning with the Portfolio’s commencement of operations and ending on the third anniversary of the commencement of operations (“Recoupment Period”). The Recoupment Period closed on April 7, 2019. Janus Capital may elect to recoup such amounts only if: (i) recoupment is obtained within three years from the date an amount is waived or reimbursed to the Portfolio, and (ii) the Portfolio’s expense ratio at the time of recoupment, inclusive of the recoupment amounts, does not exceed the expense limit at the time of waiver or at the time of recoupment. If applicable, this amount is disclosed as “Recoupment expense” on the Statement of Operations. During the period ended June 30, 2020, Janus Capital reimbursed the Portfolio $56,970 of fees and expenses, of which zero are eligible for recoupment. As of June 30, 2020, the aggregate amount of recoupment that may potentially be made to Janus Capital is $197,303.

Janus Capital has also contractually agreed to waive and/or reimburse a portion of the Portfolio's management fee in an amount equal to the management fee it earns as an investment adviser to any of the affiliated registered mutual funds (including exchange traded funds) in which the Portfolio invests. Janus Capital has agreed to continue the waiver until at least May 1, 2021. Janus Capital may not recover amounts previously waived or reimbursed under this agreement. During the period ended June 30, 2020, Janus Capital waived $4,057 of the Portfolio’s management fee, attributable to the Portfolio’s investment in the Janus Henderson Short Duration Income ETF.

Janus Services LLC (“Janus Services”), a wholly-owned subsidiary of Janus Capital, is the Portfolio’s transfer agent. In addition, Janus Services provides or arranges for the provision of certain other administrative services including, but not limited to, recordkeeping, accounting, order processing, and other shareholder services for the Portfolio. These amounts are disclosed as “Other transfer agent fees and expenses” on the Statement of Operations.

Janus Services receives an administrative services fee at an annual rate of 0.10% of the Portfolio’s average daily net assets for providing, or arranging for the provision by Protective Life of administrative services, including recordkeeping, subaccounting, order processing, or other shareholder services provided on behalf of shareholders of the Portfolio. Janus Services expects to use this entire fee to compensate Protective Life for providing these services to its

16 | JUNE 30, 2020 |

Protective Life Dynamic Allocation Series - Conservative Portfolio

Notes to Financial Statements (unaudited)

customers who invest in the Portfolio. These amounts are disclosed as “Transfer agent administrative fees and expenses” on the Statement of Operations.

Services provided by Protective Life may include, but are not limited to, recordkeeping, subaccounting, order processing, providing order confirmations, periodic statements, forwarding prospectuses, shareholder reports, and other materials to existing contract holders, answering inquiries regarding accounts, and other administrative services. Order processing includes the submission of transactions through the National Securities Clearing Corporation (“NSCC”) or similar systems, or those processed on a manual basis with Janus Services.

Under a distribution and shareholder servicing plan (the "Plan") adopted in accordance with Rule 12b-1 under the 1940 Act, the Portfolio may pay the Trust's distributor, Janus Distributors LLC dba Janus Henderson Distributors ("Janus Henderson Distributors"), a wholly-owned subsidiary of Janus Capital, a fee at an annual rate of up to 0.25% of the average daily net assets of the Portfolio. Under the terms of the Plan, the Trust is authorized to make payments to Janus Distributors for remittance to Protective Life or other intermediaries as compensation for distribution and/or shareholder services performed by Protective Life or its agents, or by such intermediary.

Amounts that have been paid are disclosed as “12b-1 Distribution and shareholder servicing fees” on the Statement of Operations. Such payments are not tied exclusively to actual 12b-1 distribution and servicing fees, and the payments or accruals may exceed 12b-1 distribution and servicing fees actually incurred. If any of the Portfolio’s actual 12b-1 distribution and servicing fees incurred during a calendar year are less than the payments made during a calendar year, the Portfolio will be refunded the difference. Refunds, if any, are included in “12b-1 Distribution and shareholder servicing fees” in the Statement of Operations.

Janus Capital serves as administrator to the Portfolio pursuant to an administration agreement between Janus Capital and the Trust. Under the administration agreement, Janus Capital provides oversight and coordination of the Portfolio’s service providers, recordkeeping, and other administrative services, and is reimbursed by the Portfolio for certain of its costs in providing these services (to the extent Janus Capital seeks reimbursement and such costs are not otherwise waived). In addition, employees of Janus Capital and/or its affiliates may serve as officers of the Trust. The Portfolio pays for some or all of the salaries, fees, and expenses of Janus Capital employees and Portfolio officers, with respect to certain specified administration functions they perform on behalf of the Portfolio. The Portfolio pays these costs based on out-of-pocket expenses incurred by Janus Capital, and these costs are separate and apart from advisory fees and other expenses paid in connection with the investment advisory services Janus Capital provides to the Portfolio. These amounts are disclosed as “Affiliated Portfolio administration fees” on the Statement of Operations. In addition, some expenses related to compensation payable to the Portfolio’s Chief Compliance Officer and certain compliance staff, all of whom are employees of Janus Capital and/or its affiliates are shared with the Portfolio. Total compensation of $33,881 was paid to the Chief Compliance Officer and certain compliance staff by the Trust during the period ended June 30, 2020. The Portfolio's portion is reported as part of “Other expenses” on the Statement of Operations.

Any purchases and sales, realized gains/losses and recorded dividends from affiliated investments during the period ended June 30, 2020 can be found in the “Schedules of Affiliated Investments” located in the Schedule of Investments.

The Portfolio is permitted to purchase or sell securities (“cross-trade”) between itself and other funds or accounts managed by Janus Capital in accordance with Rule 17a-7 under the Investment Company Act of 1940 (“Rule 17a-7”), when the transaction is consistent with the investment objectives and policies of the Portfolio and in accordance with the Internal Cross Trade Procedures adopted by the Trust’s Board of Trustees. These procedures have been designed to ensure that any cross-trade of securities by the Portfolio from or to another fund or account that is or could be considered an affiliate of the Portfolio under certain limited circumstances by virtue of having a common investment adviser, common Officer, or common Trustee complies with Rule 17a-7. Under these procedures, each cross-trade is effected at the current market price to save costs where allowed. During the period ended June 30, 2020, the Portfolio engaged in cross trades amounting to $1,557,852 in purchases and $1,236,847 in sales, resulting in a net realized loss of $12,177. The net realized loss is included within the “Net Realized Gain/(Loss) on Investments” section of the Portfolio’s Statement of Operations.

4. Federal Income Tax

Income and capital gains distributions are determined in accordance with income tax regulations that may differ from accounting principles generally accepted in the United States of America. These differences are due to differing

Clayton Street Trust | 17 |

Protective Life Dynamic Allocation Series - Conservative Portfolio

Notes to Financial Statements (unaudited)

treatments for items such as net short-term gains, deferral of wash sale losses, foreign currency transactions, net investment losses, and capital loss carryovers.

The aggregate cost of investments and the composition of unrealized appreciation and depreciation of investment securities for federal income tax purposes as of June 30, 2020 are noted below. The primary difference between book and tax appreciation or depreciation of investments is wash sale loss deferrals.

Federal Tax Cost | Unrealized | Unrealized

| Net Tax Appreciation/ |

$ 33,634,352 | $ 1,801,870 | $ (13,598) | $ 1,788,272 |

5. Capital Share Transactions

|

|

|

|

|

|

|

|

| Period ended June 30, 2020 |

| Year ended December 31, 2019 | ||

|

| Shares | Amount |

| Shares | Amount |

Shares sold | 647,880 | $7,026,626 |

| 536,015 | $6,031,463 | |

Reinvested dividends and distributions | 31,248 | 334,357 |

| 90,147 | 1,012,114 | |

Shares repurchased | (278,883) | (3,021,675) |

| (479,567) | (5,455,226) | |

Net Increase/(Decrease) | 400,245 | $4,339,308 |

| 146,595 | $1,588,351 | |

6. Purchases and Sales of Investment Securities

For the period ended June 30, 2020, the aggregate cost of purchases and proceeds from sales of investment securities (excluding any short-term securities, short-term options contracts, TBAs, and in-kind transactions, as applicable) was as follows:

Purchases of | Proceeds from Sales | Purchases

of Long- | Proceeds

from Sales |

$29,277,712 | $ 27,665,910 | $ - | $ - |

7. Recent Accounting Pronouncements

The FASB issued Accounting Standards Update 2018-13, Fair Value Measurement (Topic 820), in August 2018. The new guidance removes, modifies and enhances the disclosures to Topic 820. For public entities, the amendments are effective for financial statements issued for fiscal years beginning after December 15, 2019, and interim periods within those fiscal years. An entity is permitted, and Management has decided, to early adopt the removed and modified disclosures in these financial statements. Management is also evaluating the implications related to the new disclosure requirements and has not yet determined the impact to the financial statements.

8. Other Matters

An outbreak of infectious respiratory illness caused by a novel coronavirus known as COVID-19 was first detected in China in December 2019 and has now been declared a pandemic by the World Health Organization. The impact of COVID-19 has been, and may continue to be, highly disruptive to economies and markets, adversely impacting individual companies, sectors, industries, markets, currencies, interest and inflation rates, credit ratings, investor sentiment, and other factors affecting the value of a Portfolio's investments. This may impact liquidity in the marketplace, which in turn may affect the Portfolio's ability to meet redemption requests. Public health crises caused by the COVID-19 pandemic may exacerbate other pre-existing political, social, and economic risks in certain countries or globally. The duration of the COVID-19 pandemic and its effects cannot be determined with certainty, and could prevent a Portfolio from executing advantageous investment decisions in a timely manner and negatively impact a Portfolio's ability to achieve its investment objective.

18 | JUNE 30, 2020 |

Protective Life Dynamic Allocation Series - Conservative Portfolio

Notes to Financial Statements (unaudited)

9. Subsequent Event

Management has evaluated whether any events or transactions occurred subsequent to June 30, 2020 and through the date of issuance of the Portfolio’s financial statements and determined that there were no material events or transactions that would require recognition or disclosure in the Portfolio’s financial statements.

Clayton Street Trust | 19 |

Protective Life Dynamic Allocation Series - Conservative Portfolio

Additional Information (unaudited)

Proxy Voting Policies and Voting Record

A description of the policies and procedures that the Portfolio uses to determine how to vote proxies relating to its portfolio securities is available without charge: (i) upon request, by calling 1-800-525-0020 (toll free); (ii) on the Portfolio’s website at janushenderson.com/proxyvoting; and (iii) on the SEC’s website at http://www.sec.gov.

Quarterly Portfolio Holdings

The Portfolio files its complete portfolio holdings (schedule of investments) with the SEC for the first and third quarters of each fiscal year as an exhibit to Form N-PORT within 60 days of the end of such fiscal quarter. Historically, the Portfolio filed its complete portfolio holdings (schedule of investments) with the SEC for the first and third quarters each fiscal year on Form N-Q. The Portfolio’s Form N-PORT and Form N-Q filings: (i) are available on the SEC’s website at http://www.sec.gov; (ii) may be reviewed and copied at the SEC’s Public Reference Room in Washington, D.C. (information on the Public Reference Room may be obtained by calling 1-800-SEC-0330); and (iii) is available without charge, upon request, by calling Janus Henderson at 1-800-525-0020 (toll free).

Board Considerations Regarding Renewal of Investment Advisory Agreements for the CST Portfolios

The Board of Trustees (the “Board”) of Clayton Street Trust (the “Trust”), including a majority of the Trustees who are not “interested persons” as that term is defined in the Investment Company Act of 1940, as amended (the “Independent Trustees”), met on April 22-23, 2020 to consider the proposed renewal of the investment advisory agreement between Janus Capital Management LLC (the “Adviser”) and the Trust (the “Advisory Agreement”), on behalf of Protective Life Dynamic Allocation Series - Conservative Portfolio (the “Conservative Portfolio”), Protective Life Dynamic Allocation Series - Moderate Portfolio (the “Moderate Portfolio”), and Protective Life Dynamic Allocation Series - Growth Portfolio (the “Growth Portfolio,” and together with the Conservative Portfolio and the Moderate Portfolio, the “Portfolios”). In the course of their consideration of the renewal of the Advisory Agreement, the Independent Trustees met in executive session and were advised by their independent counsel. In this regard, the Independent Trustees evaluated the terms of the Advisory Agreement and reviewed the duties and responsibilities of trustees in evaluating and approving such agreements. In considering renewal of the Advisory Agreement, the Board and the Independent Trustees, as applicable, reviewed the materials provided to them relating to the consideration of the renewal of the Advisory Agreement for the Portfolios and other information provided by counsel and the Adviser, including: (i) information regarding the nature, quality and extent of the services provided to the Portfolios by the Adviser, and the fees charged to each Portfolio therefor; (ii) information concerning the Adviser’s financial condition, business, operations, portfolio management personnel, compliance programs, and profitability with respect to the Trust and each Portfolio; (iii) comparative information describing each Portfolio’s advisory fee structures, operating expenses, and performance information as compared to peer fund groups selected and reported to the Board by an independent third party; (iv) a copy of the Adviser’s current Form ADV; and (v) a memorandum from counsel on the responsibilities of trustees in considering investment advisory arrangements under the 1940 Act. The Board also considered presentations made by, and discussions held with, representatives of the Adviser over the previous year and since the inception of the Portfolios. The Trustees previously met via telephone on March 13, 2020 to discuss certain information provided by the Adviser related to the Trustees consideration of the renewal of the Investment Management Agreement.

During its review of this information, the Board focused on and analyzed the factors that it deemed relevant, including: (i) the nature, extent and quality of the services provided to the Portfolios by the Adviser; (ii) the Adviser’s personnel and operations; (iii) each Portfolio’s expense level; (iv) the profitability to the Adviser under the Advisory Agreement with respect to each Portfolio; (v) any “fall-out” benefits to the Adviser and its affiliates (i.e., the ancillary benefits realized by the Adviser and its affiliates from the Adviser’s relationship with the Trust); (vi) the effect of asset growth on each Portfolio’s expenses; and (vii) potential conflicts of interest.

The Trustees also considered benefits that accrue to the Adviser and its affiliates from their relationships with the Trust and each Portfolio. The Trustees also concluded that, other than the services provided by the Adviser and its affiliates pursuant to agreements with the Portfolios and the fees paid by the Portfolios therefor, the Portfolios and the Adviser may potentially benefit from their relationship with each other in other ways. The Trustees concluded that the success of the Portfolios could attract other business to the Adviser or other Janus Henderson funds, and that the success of the Adviser could enhance the Adviser’s ability to serve the Portfolios.

The Board, including the Independent Trustees, considered the following in respect of the Portfolios:

(a) The nature, extent and quality of services provided by the Adviser; personnel and operations of the Adviser.

20 | JUNE 30, 2020 |

Protective Life Dynamic Allocation Series - Conservative Portfolio

Additional Information (unaudited)

The Board reviewed the services that the Adviser provides to the Portfolios. In connection with the investment advisory services provided by the Adviser, the Board noted the responsibilities that the Adviser has as the Portfolios’ investment adviser, including: the overall supervisory responsibility for the general management and investment of each Portfolio’s securities portfolio; providing oversight of the investment performance and processes and compliance with each Portfolio’s investment objectives, policies and limitations; the implementation of the investment management program of each Portfolio; the management of the day-to-day investment and reinvestment of the assets of each Portfolio; the review of brokerage matters; the oversight of general portfolio compliance with relevant law; and the implementation of Board directives as they relate to the Portfolios.

The Board reviewed the Adviser’s experience, resources and strengths in managing the Portfolios and other pooled investment vehicles, including an assessment of the Adviser’s personnel. Based on its consideration and review of the foregoing information, the Board determined that each Portfolio was likely to continue to benefit from the nature, quality and extent of these services, as well as the Adviser’s ability to render such services based on the Adviser’s experience, personnel, operations and resources.

(b) Comparison of services rendered and fees paid under other investment advisory contracts, and the cost of the services to be provided and profits to be realized by the Adviser from the relationship with the Portfolios; “fall-out” benefits.

The Board then compared both the services rendered and the fees paid under other contracts of the Adviser and under contracts of other investment advisers with respect to similar investment companies. In particular, the Board reviewed a report compiled by an independent third party to compare each Portfolio’s management fee, and expense ratio to other investment companies within each Portfolio’s respective peer grouping, as determined by the independent third party. The comparative reporting indicated that the contractual management fees for the Conservative Portfolio were in the 5th quintile, the Moderate Portfolio was in the 4th quintile and the Growth Portfolio was in the 5th quintile, as compared to each Portfolio’s respective peer grouping. The comparative reporting further indicated that the total expense ratios for the Growth and Moderate Portfolios were in the 3rd quintile and that the total expense ratio for the Conservative Portfolio was in the 4th quintile as compared to each Portfolio’s respective peer grouping. In evaluating the comparative fees of the Portfolios, the Board considered the similarities and differences between the Portfolio’s investment strategies and those of their respective peer group members.