UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K/A

Amendment No. 3

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended June 30, 2017

Commission File Number 333-207109

| APEX RESOURCES INC. |

| (Exact name of registrant as specified in its charter) |

NEVADA

(State or other jurisdiction of incorporation or organization)

150 S. Los Robles Avenue, Suite 650, Pasadena, CA 91101

(Address of principal executive offices, including zip code)

(626) 910-5101

(Telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

None

Securities registered pursuant to section 12(g) of the Act:

Common Stock, $.001 par value

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes o No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act Yes o No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of "large accelerated filer," "accelerated filer" and "smaller reporting company" in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer | ¨ | Non-accelerated filer | ¨ |

| Accelerated filer | ¨ | Smaller reporting company | x |

| (Do not check if a smaller reporting company) | |||

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes o No x

As of June 8, 2018 the registrant had 5,080,000 shares of common stock issued and outstanding. No market value has been computed based upon the fact that no active trading market had been established as of June 8, 2018.

TABLE OF CONTENTS

| 2 |

| Table of Contents |

Forward Looking Statements

This annual report contains forward-looking statements which relate to future events or our future financial performance. In some cases, you can identify forward-looking statements by terminology such as “may”, “should”, “expects”, “plans”, “anticipates”, “believes”, “estimates”, “predicts”, “potential” or “continue” or the negative of these terms or other comparable terminology. These statements are only predictions and involve known and unknown risks, uncertainties and other factors, including the risks in the section entitled “Risk Factors,” that may cause our or our industry’s actual results, levels of activity, performance or achievements to be materially different from any future results, levels of activity, performance or achievements expressed or implied by these forward-looking statements.

While these forward-looking statements, and any assumptions upon which they are based, are made in good faith and reflect our current judgment regarding the direction of our business, actual results will almost always vary, sometimes materially, from any estimates, predictions, projections, assumptions or other future performance suggested herein. Except as required by applicable law, including the securities laws of the United States, we do not intend to update any of the forward-looking statements to conform these statements to actual results.

Our Company

APEX RESOURCES INC was incorporated on March 31, 2015, under the laws of the State of Nevada, for the purpose of engaging in the steam room products distribution business, with the objective of becoming a recognized leader in our targeted market for steam room products.

The primary focus of APEX RESOURCES INC is providing high quality steamroom products at extremely competitive prices all the while providing best customer satisfaction service, creating unique customer experience from initial customer contact to final product order from our company. We have commenced initial selling activities.

We are in the initial stages of our business development and have realized some revenues to date, our accumulated deficit as of June 30, 2017 is $48,894. On June 15, 2015, Mr. Dabasinskas, the officer and director of the company, was issued 4,000,000 shares of our common stock for cash in the amount of $4,000. In November 2016 the Company sold and issued 1,080,000 shares at $0.04 per share pursuant to its offering on a Registration Statement on Form S-1. The shares were issued to 31 independent shareholders for proceeds of $43,200. To date we have received a total of $1,231 through loans from our sole officer and director, Tadas Dabasinskas. The loans are interest free, unsecured and have no term. Proceeds from the loan were used to open the company bank accounts and pay some expenses. The Company’s principal offices are located at Alytaus g. 100, Varėna, Lithuania. Our telephone number is (775)253-3921.

Our financial statements from inception on March 31, 2015, through June 30, 2017, report $282,832 in revenues and cost of sales of $255,279 resulting in a gross profit of $27,553. Our independent auditor has issued an audit opinion for our Company which includes a statement expressing substantial doubt as to our ability to continue as a going concern.

As of the date of this annual report, there is no active public trading market for our common stock and no assurance that an active trading market for our securities will ever develop.

| 3 |

| Table of Contents |

We are an “emerging growth company” within the meaning of the federal securities laws. For as long as we are an emerging growth company, we will not be required to comply with the requirements that are applicable to other public companies that are not “emerging growth companies” including, but not limited to, not being required to comply with the auditor attestation requirements of Section 404 of the Sarbanes-Oxley Act, the reduced disclosure obligations regarding executive compensation in our periodic reports and proxy statements and the exemptions from the requirements of holding a nonbinding advisory vote on executive compensation and shareholder approval of any golden parachute payments not previously approved. We intend to take advantage of these reporting exemptions until we are no longer an emerging growth company. For a description of the qualifications and other requirements applicable to emerging growth companies and certain elections that we have made due to our status as an emerging growth company, see “RISK FACTORS - WE ARE AN `EMERGING GROWTH COMPANY”.

Under U.S. federal securities legislation, our common stock is considered a “penny stock”. Penny stock is any equity that has a market price of less than $5.00 per share, subject to certain exceptions. For any transaction involving a penny stock, unless exempt, the rules require that a broker or dealer approve a potential investor’s account for transactions in penny stocks, and the broker or dealer receive from the investor a written agreement to the transaction, setting forth the identity and quantity of the penny stock to be purchased. In order to approve an investor’s account for transactions in penny stocks, the broker or dealer must obtain financial information and investment experience objectives of the person, and make a reasonable determination that the transactions in penny stocks are suitable for that person and the person has sufficient knowledge and experience in financial matters to be capable of evaluating the risks of transactions in penny stocks. The broker or dealer must also deliver, prior to any transaction in a penny stock, a disclosure schedule prepared by the Commission relating to the penny stock market, which, in highlight form sets forth the basis on which the broker or dealer made the suitability determination. Brokers may be less willing to execute transactions in securities subject to the “penny stock” rules. This may make it more difficult for investors to dispose of our common stock and cause a decline in the market value of our stock. Disclosure also has to be made about the risks of investing in penny stocks in both public offerings and in secondary trading and about the commissions payable to both the broker-dealer and the registered representative, current quotations for the securities and the rights and remedies available to an investor in cases of fraud in penny stock transactions. Finally, monthly statements have to be sent disclosing recent price information for the penny stock held in the account and information on the limited market in penny stocks.

Product Overview

Our objective is to enter into the steam room products distribution industry and to become a recognized leader in our targeted market for steam room products for the US homes.

The primary focus of APEX RESOURCES INC is providing following steam room products: luxury steam room latest models of different sizes and shapes, to satisfy the most demanding customer tastes, also steam room accessories, steam Supplies and other steam products: Folding Steam Room Bench, Steamdoor Adhesive Bulb Seal, Steam Start/Stop Control, Cedar Steam Room Bench + Backrest, HomeWizard Wireless Steam Room Control, Steam Round Steam Head, Steam Square Steam Head, Commercial Steam Head Cover, Aroma Steam Essential Oil Delivery System, Music Therapy Speakers, Aroma Steam Room Oils, Steam Drain Pans, Steam Digital Control Package, Residential steam generators, Day Spa Steam generators ,Commercial steam generators. We will provide steam room products to US wholesalers and we hope will gain popularity within our target market. Steam room products are part of bigger spa industry. That is why our product is "steam room products" and our industry is the spa industry. Our target markets are steam room products wholesale distributors and eventually to individual home owners in the US. Management believes potential clients will purchase from us as our goal is to provide excellent customer service and competitive pricing.

When and if we make enough money from our current business operations, we will proceed to develop, manufacture and market our own brand of steam room products: we believe this way our company will be more profitable than to continue re-selling other company`s products.

We currently have agreements with these suppliers: Decasso International, Guangdong Grand, Hangzhou Oulin, Xiamen Sigmar and Zhongshan Frae, all located in China. When we need products, we ask each of these suppliers for a latest and best quote and we choose one and order from that supplier. A copy of each agreement and terms thereof are attached as Exhibit 10.1 to the Registration Statement on Form S-1 as filed.

Management believes we can compete in this industry because we plan to give customers shorter delivery times, better customer service, and our prices are among the lowest in the industry.

| 4 |

| Table of Contents |

OUR MARKET

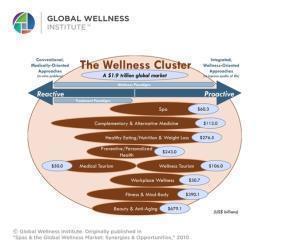

We have conducted a brief market research on the internet, into the likelihood of success of our operations or the acceptance of our product and services by the public. Our research has shown that steam room products are in a great demand within our target market. According to the information provided by the Global Wellness Institute which has commissioned six landmark research studies, three of which were executed by renowned research firm, SRI International. Below are some of the key charts from each report, the updated, topline industry figures and the GWI official definition of wellness, wellness tourism and spa. For more information on our study please visit: http://www.globalwellnessinstitute.com/

THE LATEST NUMBERS

The global wellness industry is a $3.4 trillion market, or 3.4 times larger than the worldwide pharmaceutical industry. Key sectors include:

Healthy Eating/Nutrition/Weight Loss ($574.2 bil.)

Fitness & Mind/Body ($446.4 bil.)

Beauty & Anti-Aging ($1.025 tril.)

Preventative/Personalized Health ($432.7 bil.)

Complementary/Alternative Medicine ($186.7 bil.)

| 5 |

| Table of Contents |

Workplace wellness ($40.7 bil.)

Wellness Lifestyle Real Estate ($100 bil.)

The global wellness tourism market expanded to $494 billion in revenues in 2013, a 12.5 percent gain over 2012, and significantly outpacing SRI’s original growth forecast of 9 percent.

The global spa industry grew from $60 billion in 2007 to $94 billion in 2013– or an annual 7.7 percent growth rate, even across long global recession years.

SRI International also estimates a 27 percent increase in the number of spas worldwide in the last seven years: from 71,762 in 2007, to 105,591 today.

In 2014, SRI undertook the first-ever analysis of the thermal/mineral springs sector, finding that it is a $50 billion global market, spanning 26,847 properties worldwide.

An inherent goal of the Global Spa Economy report was to promote the value of flexibility in defining the term “spa” and to understand its different interpretations by businesses and consumers around the world. With this end in mind, the team from SRI International put forth the following definition for spas:

Spas are defined as establishments that promote wellness through the provision of therapeutic and other professional services aimed at renewing the body, mind, and spirit.

Most consumers and industry executives would agree that at its core – no matter its size, form, or business model – a spa is an establishment that focuses on the promotion of wellness. The concepts of wellness, the healing traditions drawn upon, and the therapeutic techniques applied differ dramatically across both nations and businesses.

Hydrothermal bathing (including saunas, steam rooms, hydrotherapy pools, etc.) dates back thousands of years and is one of the most ancient spa practices.

| 6 |

| Table of Contents |

COMPETITION

There are few barriers of entry in the steam room products distribution business and the level of competition is extremely high. There are many steam room products distribution companies. We will be in direct competition with them. Many large steam room products distribution companies have greater financial capabilities than we do and will be able to provide more favorable services to the potential customers. Many of these companies may have a greater, more established customer base than us. We will likely lose business to such companies.

1. Mr.Steam makes luxurious steam showers, products include towel warmers, aromasteam, chromasteam, in-shower seats, speakers: http://www.mrsteam.com/

2.Cedar brook sauna products include head covers, steam generator controls, folding benches, steam room benches, systems speaker systems ,steam room lighting: www.cedarbrooksauna.com

3. Home Depot products include Steam Showers in the Bath Department: http://www.homedepot.com/

4. Amerec products include steam bath generators: www.amerec.com

| 7 |

| Table of Contents |

5. Thermasol products include steam baths and saunas for domestic and commercial use: www.thermasol.com

6. Tylö products include Steam and Shower products: www.tylo.com

Management believes we can compete in this industry because we plan to give customers shorter delivery times, better customer service, and based upon management’s experience in the industry, our prices are among the lowest in the industry.

MARKETING

We plan to use an active marketing strategy that will be based on developing visibility among our potential customers through participating in exhibitions, such as

1. Minneapolis Home + Garden Show www.homeandgardenshow.com

2. The Great Big Home + Garden Show www.greatbighomeandgarden.com

3. Cincinnati Home & Garden Show www.cincinnatihomeandgardenshow.com. Cincinnati's largest and longest running spring showcase with array of the area's newest and innovative home products and services.

4. Fort Wayne Home & Garden Show www.home-gardenshow.com

5. Home Improvement and Garden Show www.novihomeshow.com

6. Portland Home & Garden Show www.otshows.com The Portland Home & Garden show is Oregon's Largest Home and Garden Show

SALES

We generate revenues by selling our steam room products to wholesale distributors and eventually to individual home owners in the US.

We would only quote customers on the price after they have provided us all the details. This would allow us to customize orders for the customer and more accurately determine the true costs of materials and labor before we give a quote. Usually, the larger the order, the lower the per-item pricing as it requires less labor.

EMPLOYEES; IDENTIFICATION OF CERTAIN SIGNIFICANT EMPLOYEES

We currently have no employees, other than our sole officer and director, Tadas Dabasinskas. Tadas Dabasinskas, our sole officer and director, handles the Company’s day-to-day operations. We intend to hire employees on an as needed basis.

INSURANCE

We do not maintain any insurance and do not intend to maintain insurance in the near future. Because we do not have any insurance, if we are made a party of a legal action, we may not have sufficient funds to defend the litigation. If that occurs a judgment could be rendered against us that could cause us to cease operations.

OFFICE

The Company’s principal office is located at Alytaus g. 100, Varėna, Lithuania.

| 8 |

| Table of Contents |

GOVERNMENT REGULATION

We are required to comply with all regulations, rules and directives of governmental authorities and agencies in any jurisdiction which we would conduct activities in the future. As of now there are no required government approvals present that we need approval from or any existing government regulation on our business.

We currently have not obtained any copyrights, patents or trademarks. We do not anticipate filing any copyright or trademark applications related to any assets over the next 12 months.

RESEARCH AND DEVELOPMENT ACTIVITIES AND COSTS

We have not incurred any research and development costs to date.

REPORTS TO STOCKHOLDERS

We are required to file reports with the SEC pursuant to the Securities Exchange Act of 1934, as amended (the "Exchange Act"). These reports include annual reports on Form 10-K, quarterly reports on Form 10-Q and current reports on Form 8-K. You may obtain copies of these reports from the SEC's Public Reference Room at 100 F Street, N.E., Washington, D.C. 20549, on official business days during the hours of 10 A.M. to 3 P.M. or on the SEC's website, at www.sec.gov. You may obtain information on the operation of the Public Reference Room by calling the SEC at 1-800-SEC-0330.

Because our auditors have issued a going concern opinion, there is substantial uncertainty we will continue operations in which case you could lose your investment.

In their audit report for the year ended June 30, 2017, our auditors stated the financial statements were prepared assuming the company will continue as a going concern. This means that there is substantial doubt that we can continue as an ongoing business. For the period from inception (March 31, 2015) to June 30, 2017, we incurred a deficit of $48,894. We will need to generate significant revenue in order to achieve consistent profitability and we may never become profitable. We estimate the company will require approximately $13,000 over the next twelve months in a limited operations scenario. The going concern paragraph in the independent auditor’s report emphasizes the uncertainty related to our business as well as the level of risk associated with an investment in our common stock.

We have a very limited history of operations and accordingly there is no track record that would provide a basis for assessing our ability to conduct successful commercial activities. We may not be successful in carrying out our business objectives.

We were incorporated on March 31, 2015 and to date, have been involved primarily in organizational activities and obtaining financing. Accordingly we have little track record of successful business activities, strategic decision making by management, fund-raising ability, and other factors that would allow an investor to assess the likelihood that we will be successful in the steam room products distribution business, with the objective of becoming a recognized leader in our targeted market for steam room products. As of June 30, 2017, we had a net deficit of $48,894. New companies in businesses with low barriers to entry, such as ours, often fail to achieve or maintain successful operations, even in favorable market conditions. There is a substantial risk that we will not be successful in our steam room products distribution business activities, or if initially successful, in thereafter generating any operating revenues or in achieving profitable operations.

| 9 |

| Table of Contents |

We depend to a significant extent on certain key personnel, the loss of any of whom may materially and adversely affect our company.

Currently, we have only one employee, Tadas Dabasinskas, who serves as our sole officer and director. Mr. Dabasinskas does not presently owe fiduciary duties to any company or entities other than Apex Resources. We depend entirely on Mr. Dabasinskas for all of our operations. The loss of Mr. Dabasinskas would have a substantial negative effect on our company and may cause our business to fail. Mr. Dabasinskas has not been compensated for his services since our incorporation, and it is highly unlikely that he will receive any compensation unless and until we generate substantial revenues. There is intense competition for skilled personnel and there can be no assurance that we will be able to attract and retain qualified personnel on acceptable terms. The loss of Mr. Dabasinskas’ services could prevent us from completing the development of our plan of operation and our business. In the event of the loss of services of such personnel, no assurance can be given that we will be able to obtain the services of adequate replacement personnel.

We do not have any employment agreements or maintain key person life insurance policies on our sole officer and director. We do not anticipate entering into employment agreements with them or acquiring key man insurance in the foreseeable future.

We have limited business, sales and marketing experience in our industry.

We have garnered our first customer and have generated revenues of 282,832 since inception through June 30, 2017. While we have plans for marketing our steam room products, there can be no assurance that such efforts will be successful. There can be no assurance that our proposed steam room products distribution offering will gain wide acceptance in its target market or that we will be able to effectively market our products. We are entirely dependent on the services of our sole officer and director, Tadas Dabasinskas, to build our customer base. Our company has no prior experience upon which it can rely in order to garner its future prospective customers to use our products and offerings. Prospective customers will be less likely to use our steam room products distribution than a competitor’s because we have no prior experience in our industry.

We are dependent on third parties to purchase our merchandise we need in order to engage in and provide our offerings to potential customers. Any increase in the amounts we have to pay to buy our merchandise or any delay or interruption in production because of our suppliers would negatively affect both our ability to make a timely introduction, generate revenues and our results of operations.

If our current steam room suppliers become inoperable through no fault of our own, we will depend on other suppliers which we do not know now, in order to continue our operations. We will have little or no control over third-party steam room product manufacturers because we cannot control their personnel, schedule or resources. It will be difficult to timely complete steam room product orders from customers if our current steam room suppliers become inoperable through no fault of our own and the current supplier does not immediately ship and / or fulfill our order. Any delay in the fulfillment or shipment of our orders could cause delays in providing our steam room products or timely delivery orders to customers. Any of these factors could cause a steam room product order not to meet our quality standards or expectations, or not to be completed on time or at all. If this happens you could lose your entire investment in our steam room products distribution business.

If we do not attract more new customers, we will not make a substantial profit, which ultimately will result in a cessation of operations.

We currently have one customer who buys our steam room products. We have not identified any more new customers and we cannot guarantee we ever will have any more new customers. Even if we obtain customers, there is no guarantee that we will generate a future substantial profit. If we cannot generate a future substantial profit, we will have to suspend or cease operations. You are likely to lose your entire investment if we cannot sell our steam room products at prices which generate substantial profit for our company.

| 10 |

| Table of Contents |

We may not be able to compete effectively against our competitors.

We expect to face strong competition from well-established companies and small independent companies who also provide steam room products distribution and that may result in price reductions and decreased demand for our steam room products. We will be at a competitive disadvantage in obtaining the facilities, employees, financing and other resources required to provide the steam room products distribution which we believe will be demanded by prospective customers. Our opportunity to obtain customers may be limited by our financial resources and other assets. We expect to be less able than our larger competitors to cope with generally increasing costs and expenses of doing business.

Our current or future competitors may compete more successfully in the steam room products distribution business than we do. In particular, any of our competitors may offer products and services that have significant performance, price, creativity and/or other advantages over our services. These products and services may significantly affect the demand for our services. If we are unable to compete successfully, we could lose sales and market share, assuming we gain any market share. We also could experience difficulty hiring and retaining qualified employees. Any of these consequences would significantly harm our business, results of operations and financial condition. There can be no assurance that we will be able to effectively compete with our competitors or that their present and future offerings would render our product obsolete or noncompetitive. This intense competition may have a material adverse effect on our results of operations and financial condition and prevent us from achieving profitable revenue levels from our product.

Since a majority of our shares of common stock are owned by our sole officer and director, our other stockholders may not be able to influence control of the company or decision making by management of the company, and as such, our sole officer and director may have a conflict of interest with the minority shareholders at some time in the future.

Tadas Dabasinskas, our sole officer and director beneficially owns 79% of our issued and outstanding shares of common stock. The interests of Mr. Dabasinskas may not be, at all times, the same as that of our other shareholders. Mr. Dabasinskas is not simply a passive investor but is also an executive officer of the Company, and as such his interests as an executive may, at times be adverse to those of passive investors. Where those conflicts exist, our shareholders are dependent upon our sole officer and director exercising, in a manner fair to all of our shareholders, his fiduciary duties as an officer and as member of the Company’s board of directors. Also, our sole officer and director will have the ability to control the outcome of most corporate actions requiring shareholder approval, including the sale of all or substantially all of our assets and amendments to our Articles of Incorporation. This concentration of ownership may also have the effect of delaying, deferring or preventing a change of control of us, which may be disadvantageous to minority shareholders.

We are subject to the periodic reporting requirements of the Securities Exchange Act of 1934, as amended, which require us to incur audit fees and legal fees in connection with the preparation of such reports. These additional costs will negatively affect our ability to earn a profit.

We are required to file periodic reports with the Securities and Exchange Commission pursuant to the Securities Exchange Act of 1934 and the rules and regulations thereunder. In order to comply with such requirements, our independent registered auditors have to review our financial statements on a quarterly basis and audit our financial statements on an annual basis. Moreover, our legal counsel may have to review and assist in the preparation of such reports. Factors such as the number and type of transactions that we engage in and the complexity of our reports cannot accurately be determined at this time and may have a major negative effect on the cost and amount of time to be spent by our auditors and attorneys. However, the incurrence of such costs will obviously be an expense to our operations and thus have a negative effect on our ability to meet our overhead requirements and earn a profit.

However, for as long as we remain an “emerging growth company” as defined in the Jumpstart Our Business Startups Act of 2012, we intend to take advantage of certain exemptions from various reporting requirements that are applicable to other public companies that are not “emerging growth companies” including, but not limited to, not being required to comply with the auditor attestation requirements of Section 404 of the Sarbanes-Oxley Act, reduced disclosure obligations regarding executive compensation in our periodic reports and proxy statements, and exemptions from the requirements of holding a nonbinding advisory vote on executive compensation and shareholder approval of any golden parachute payments not previously approved. We intend to take advantage of these reporting exemptions until we are no longer an “emerging growth company.”

| 11 |

| Table of Contents |

We will remain an emerging growth company until the earlier of (i) the last day of the fiscal year (A) following the fifth anniversary of our first sale of common equity securities pursuant to an effective registration statement, (B) in which we have total annual gross revenue of at least $1.0 billion, or (C) the date that we become a “large accelerated filer” as defined in Rule 12b-2 under the Exchange Act, which would occur if the market value of our common stock that is held by non-affiliates exceeds $700 million as of the last business day of our most recently completed second fiscal quarter, and (ii) the date on which we have issued more than $1.0 billion in non-convertible debt during the prior three-year period.

Rule 12b-2 of the Securities Exchange Act of 1934, as amended, defines a “smaller reporting company” as an issuer that is not an investment company, an asset-backed issuer), or a majority-owned subsidiary of a parent that is not a smaller reporting company and that:

|

| · | Had a public float of less than $75 million as of the last business day of its most recently completed second fiscal quarter, computed by multiplying the aggregate worldwide number of shares of its voting and non-voting common equity held by non-affiliates by the price at which the common equity was last sold, or the average of the bid and asked prices of common equity, in the principal market for the common equity; or |

|

| · | In the case of an initial registration statement under the Securities Act or Exchange Act for shares of its common equity, had a public float of less than $75 million as of a date within 30 days of the date of the filing of the registration statement, computed by multiplying the aggregate worldwide number of such shares held by non-affiliates before the registration plus, in the case of a Securities Act registration statement, the number of such shares included in the registration statement by the estimated public offering price of the shares; or |

|

| · | In the case of an issuer whose public float as calculated under paragraph (1) or (2) of this definition was zero, had annual revenues of less than $50 million during the most recently completed fiscal year for which audited financial statements are available. |

We qualify as a smaller reporting company, and so long as we remain a smaller reporting company, we benefit from the same exemptions and exclusions as an emerging growth company. In the event that we cease to be an emerging growth company as a result of a lapse of the five year period, but continue to be a smaller reporting company, we would continue to be subject to the exemptions available to emerging growth companies until such time as we were no longer a smaller reporting company.

After, and if ever, we are no longer an “emerging growth company,” we expect to incur significant additional expenses and devote substantial management effort toward ensuring compliance with those requirements applicable to companies that are not “emerging growth companies,” including Section 404 of the Sarbanes-Oxley Act.

We are an “emerging growth company” and we cannot be certain if the reduced disclosure requirements applicable to emerging growth companies will make our common stock less attractive to investors.

We are an “emerging growth company,” as defined in the Jumpstart our Business Startups Act of 2012, and we may take advantage of certain exemptions from various reporting requirements that are applicable to other public companies, including, but not limited to, not being required to comply with the auditor attestation requirements of Section 404 of the Sarbanes-Oxley Act, reduced disclosure obligations regarding executive compensation in our periodic reports and proxy statements, and exemptions from the requirements of holding a nonbinding advisory vote on executive compensation and shareholder approval of any golden parachute payments not previously approved. We cannot predict if investors will find our common stock less attractive because we will rely on these exemptions. If some investors find our common stock less attractive as a result, there may be a less active trading market for our common stock and our stock price may be more volatile.

| 12 |

| Table of Contents |

Under the Jumpstart Our Business Startups Act, “emerging growth companies” can delay adopting new or revised accounting standards until such time as those standards apply to private companies. We have irrevocably elected not to avail ourselves to this exemption from new or revised accounting standards and, therefore, we will be subject to the same new or revised accounting standards as other public companies that are not “emerging growth companies.”

Since our sole officer and director has the ability to be employed by or consult for other companies, their other activities could slow down our operations.

Tadas Dabasinskas, our sole officer and director, is not required to work exclusively for us and does not devote all of his time to our operations. Therefore, it is possible that a conflict of interest with regard to his time may arise based on his employment by other companies. His other activities may prevent him from devoting full-time to our operations which could slow our operations and may reduce our financial results because of the slowdown in operations. It is expected that Tadas Dabasinskas, our President, will devote between 5 and 10 hours per week to our operations on an ongoing basis, and when required will devote whole days and even multiple days at a stretch if our operations increase. We do not have any written procedures in place to address conflicts of interest that may arise between our business and the business activities of our sole officer and director.

We have no employment or compensation agreement with our sole officer and director and as such he may have little incentive to devote time and energy to the operation of the Company.

Tadas Dabasinskas is not subject to any employment or compensation agreement with the Company. Therefore, it is possible that he may decide to focus his efforts on other projects or companies which have a higher economic benefit to him. Currently, Mr. Dabasinskas is not obligated to spend any time at all on Company business and could opt to leave the Company for other opportunities or focus on other business which could negatively impact the Company’s ability to succeed. We do not have any expectation that Mr. Dabasinskas will enter into an employment or compensation agreement with the Company in the foreseeable future and the loss of either one would be highly detrimental to our ability to conduct ongoing operations.

It will be extremely difficult to acquire jurisdiction and enforce liabilities against our sole officer and director and assets outside the United States.

Substantially all of our assets are currently located outside of the United States. Additionally, our sole officer and director resides outside of the United States, in Lithuania. As a result, it may not be possible for United States investors to enforce their legal rights, to effect service of process upon our sole officer and director or to enforce judgments of United States courts predicated upon civil liabilities and criminal penalties of our sole officer and director under Federal securities laws. Moreover, we have been advised that Lithuania does not have treaties providing for the reciprocal recognition and enforcement of judgments of courts with the United States. Further, it is unclear if extradition treaties now in effect between the United States and Lithuania would permit effective enforcement of criminal penalties of the Federal securities laws.

Our common stock is subject to the “penny stock” rules of the SEC and the trading market in our securities is limited, which makes transactions in our stock cumbersome and may reduce the value of an investment in our stock.

Under U.S. federal securities legislation, our common stock is considered “penny stock”. Penny stock is any equity security that has a market price of less than $5.00 per share, subject to certain exceptions. For any transaction involving a penny stock, unless exempt, the rules require that a broker or dealer approve a potential investor’s account for transactions in penny stocks, and the broker or dealer receive from the investor a written agreement to the transaction, setting forth the identity and quantity of the penny stock to be purchased. In order to approve an investor’s account for transactions in penny stocks, the broker or dealer must obtain financial information and investment experience objectives of the person, and make a reasonable determination that the transactions in penny stocks are suitable for that person and the person has sufficient knowledge and experience in financial matters to be capable of evaluating the risks of transactions in penny stocks. The broker or dealer must also deliver, prior to any transaction in a penny stock, a disclosure schedule prepared by the Commission relating to the penny stock market, which, in highlight form sets forth the basis on which the broker or dealer made the suitability determination. Brokers may be less willing to execute transactions in securities subject to the “penny stock” rules. This may make it more difficult for investors to dispose of our common stock and cause a decline in the market value of our stock. Disclosure also has to be made about the risks of investing in penny stocks in both public offerings and in secondary trading and about the commissions payable to both the broker-dealer and the registered representative, current quotations for the securities and the rights and remedies available to an investor in cases of fraud in penny stock transactions. Finally, monthly statements have to be sent disclosing recent price information for the penny stock held in the account and information on the limited market in penny stocks.

| 13 |

| Table of Contents |

We may, in the future, issue additional common shares, which would reduce investors’ percent of ownership and may dilute our share value.

Our Articles of Incorporation authorize the issuance of 75,000,000 shares of common stock. As of the date of this annual report, the Company had 5,080,000 shares of common stock outstanding. Accordingly, we may issue up to an additional 69,920,000 shares of common stock. The future issuance of common stock may result in substantial dilution in the percentage of our common stock held by our then existing shareholders. We may value any common stock in the future on an arbitrary basis. The issuance of common stock for future services or acquisitions or other corporate actions may have the effect of diluting the value of the shares held by our investors, and might have an adverse effect on any trading market for our common stock.

We are an “emerging growth company” and we cannot be certain if the reduced disclosure requirements applicable to emerging growth companies will make our common stock less attractive to investors.

We are an “emerging growth company,” as defined in the Jumpstart our Business Startups Act of 2012, and we may take advantage of certain exemptions from various reporting requirements that are applicable to other public companies, including, but not limited to, not being required to comply with the auditor attestation requirements of Section 404 of the Sarbanes-Oxley Act, reduced disclosure obligations regarding executive compensation in our periodic reports and proxy statements, and exemptions from the requirements of holding a nonbinding advisory vote on executive compensation and shareholder approval of any golden parachute payments not previously approved. We cannot predict if investors will find our common stock less attractive because we will rely on these exemptions. If some investors find our common stock less attractive as a result, there may be a less active trading market for our common stock and our stock price may be more volatile.

Under the Jumpstart Our Business Startups Act, “emerging growth companies” can delay adopting new or revised accounting standards until such time as those standards apply to private companies. We have irrevocably elected not to avail ourselves to this exemption from new or revised accounting standards and, therefore, we will be subject to the same new or revised accounting standards as other public companies that are not “emerging growth companies.”

Anti-takeover effects of certain provisions of Nevada state law hinder a potential takeover of our company.

Though not now, in the future we may become subject to Nevada’s control share law. A corporation is subject to Nevada’s control share law if it has more than 200 stockholders, at least 100 of whom are stockholders of record and residents of Nevada, and it does business in Nevada or through an affiliated corporation. The law focuses on the acquisition of a “controlling interest” which means the ownership of outstanding voting shares sufficient, but for the control share law, to enable the acquiring person to exercise the following proportions of the voting power of the corporation in the election of directors: (i) one-fifth or more but less than one-third, (ii) one-third or more but less than a majority, or (iii) a majority or more. The ability to exercise such voting power may be direct or indirect, as well as individual or in association with others.

The effect of the control share law is that the acquiring person, and those acting in association with it, obtains only such voting rights in the control shares as are conferred by a resolution of the stockholders of the corporation, approved at a special or annual meeting of stockholders. The control share law contemplates that voting rights will be considered only once by the other stockholders. Thus, there is no authority to strip voting rights from the control shares of an acquiring person once those rights have been approved. If the stockholders do not grant voting rights to the control shares acquired by an acquiring person, those shares do not become permanent non-voting shares. The acquiring person is free to sell its shares to others. If the buyers of those shares themselves do not acquire a controlling interest, their shares do not become governed by the control share law.

| 14 |

| Table of Contents |

If control shares are accorded full voting rights and the acquiring person has acquired control shares with a majority or more of the voting power, any stockholder of record, other than an acquiring person, who has not voted in favor of approval of voting rights is entitled to demand fair value for such stockholder’s shares. Nevada’s control share law may have the effect of discouraging takeovers of the corporation.

In addition to the control share law, Nevada has a business combination law which prohibits certain business combinations between Nevada corporations and “interested stockholders” for three years after the “interested stockholder” first becomes an “interested stockholder,” unless the corporation’s board of directors approves the combination in advance. For purposes of Nevada law, an “interested stockholder” is any person who is (i) the beneficial owner, directly or indirectly, of ten percent or more of the voting power of the outstanding voting shares of the corporation, or (ii) an affiliate or associate of the corporation and at any time within the three previous years was the beneficial owner, directly or indirectly, of ten percent or more of the voting power of the then outstanding shares of the corporation. The definition of the term “business combination” is sufficiently broad to cover virtually any kind of transaction that would allow a potential acquiror to use the corporation’s assets to finance the acquisition or otherwise to benefit its own interests rather than the interests of the corporation and its other stockholders.

The effect of Nevada’s business combination law is to potentially discourage parties interested in taking control of our company from doing so if it cannot obtain the approval of our board of directors.

Because we do not intend to pay any cash dividends on our common stock, our stockholders will not be able to receive a return on their shares unless they sell them.

We intend to retain any future earnings to finance the development and expansion of our business. We do not anticipate paying any cash dividends on our common stock in the foreseeable future. Unless we pay dividends, our stockholders will not be able to receive a return on their shares unless they sell them. There is no assurance that stockholders will be able to sell shares when desired.

In June 2015 the Company purchased for $8,655 a small office located at Alytaus g. 100, Varėna, Lithuania. The Company utilizes the space as a primary office.

We are not currently a party to any legal proceedings, and we are not aware of any pending or potential legal actions.

Item 4. Mine Safety Disclosures

N/A

| 15 |

| Table of Contents |

Item 5. Market for Common Equity and Related Stockholder Matters

Market for Securities

Our shares are quoted on the over-the-counter market, however; to date there has been no active trading. In order for our common stock to continue to be eligible for trading on the Over-the-Counter Bulletin Board we must remain current in our quarterly and annual filings with the SEC. If we are not able to pay the expenses associated with our reporting obligations we will not be able to continue the quotation on the OTC Bulletin Board. There can be no assurance that any market for our stock will develop.

Holders of our Common Stock

As of June 30, 2017, there were 32 registered stockholders, holding 5,080,000 shares of our issued and outstanding common stock.

Dividend Policy

There are no restrictions in our articles of incorporation or bylaws that prevent us from declaring dividends. The Nevada Revised Statutes, however, do prohibit us from declaring dividends where, after giving effect to the distribution of the dividend:

|

| 1. | We would not be able to pay our debts as they become due in the usual course of business; or |

|

| 2. | Our total assets would be less than the sum of our total liabilities plus the amount that would be needed to satisfy the rights of shareholders who have preferential rights superior to those receiving the distribution. |

We have not declared any dividends and we do not plan to declare any dividends in the foreseeable future.

Recent Sales of Unregistered Securities

On June 15, 2015 the Company issued 4,000,000 shares of common stock for a purchase price of $0.001 per share to its sole director. The Company received aggregate gross proceeds of $4,000.

In November 2016 the Company sold and issued 1,080,000 shares at $0.04 per share pursuant to an offering on a Registration Statement on Form S-1. The shares were issued to 31 independent shareholders for proceeds of $43,200.

As of June 30, 2017, the Company had 5,080,000 shares of common stock issued and outstanding.

Purchases of Equity Securities by the Issuer and Affiliated Purchasers

We did not purchase any of our shares of common stock or other securities during our fiscal year ended June 30, 2017.

Securities Authorized for Issuance Under Equity Compensation Plans

We do not have any equity compensation plans.

Penny Stock Rules

The Securities and Exchange Commission has also adopted rules that regulate broker-dealer practices in connection with transactions in penny stocks. Penny stocks are generally equity securities with a price of less than $5.00 (other than securities registered on certain national securities exchanges or quoted on the Nasdaq system, provided that current price and volume information with respect to transactions in such securities is provided by the exchange or system).

| 16 |

| Table of Contents |

A purchaser is purchasing penny stock which limits the ability to sell the stock. Our shares constitute penny stock under the Securities and Exchange Act. The shares will remain penny stocks for the foreseeable future. The classification of penny stock makes it more difficult for a broker-dealer to sell the stock into a secondary market, which makes it more difficult for a purchaser to liquidate his/her investment. Any broker-dealer engaged by the purchaser for the purpose of selling his or her shares in us will be subject to Rules 15g-1 through 15g-10 of the Securities and Exchange Act. Rather than creating a need to comply with those rules, some broker-dealers will refuse to attempt to sell penny stock.

The penny stock rules require a broker-dealer, prior to a transaction in a penny stock not otherwise exempt from those rules, to deliver a standardized risk disclosure document, which:

| · | contains a description of the nature and level of risk in the market for penny stock in both public offerings and secondary trading; | |

|

| ||

| · | contains a description of the broker's or dealer's duties to the customer and of the rights and remedies available to the customer with respect to a violation of such duties or other requirements of the Securities Act of 1934, as amended; | |

|

| ||

| · | contains a brief, clear, narrative description of a dealer market, including "bid" and "ask" price for the penny stock and the significance of the spread between the bid and ask price; | |

|

| ||

| · | contains a toll-free telephone number for inquiries on disciplinary actions; | |

|

| ||

| · | defines significant terms in the disclosure document or in the conduct of trading penny stocks; and | |

|

| ||

| · | contains such other information and is in such form (including language, type, size and format) as the Securities and Exchange Commission shall require by rule or regulation; |

The broker-dealer also must provide, prior to effecting any transaction in a penny stock, to the customer:

| · | the bid and offer quotations for the penny stock; | |

|

| ||

| · | the compensation of the broker-dealer and its salesperson in the transaction; | |

|

| ||

| · | the number of shares to which such bid and ask prices apply, or other comparable information relating to the depth and liquidity of the market for such stock; and | |

|

| ||

| · | monthly account statements showing the market value of each penny stock held in the customer's account. |

In addition, the penny stock rules require that prior to a transaction in a penny stock not otherwise exempt from those rules; the broker-dealer must make a special written determination that the penny stock is a suitable investment for the purchaser and receive the purchaser's written acknowledgment of the receipt of a risk disclosure statement, a written agreement to transactions involving penny stocks, and a signed and dated copy of a written suitability statement. These disclosure requirements will have the effect of reducing the trading activity in the secondary market for our stock because it will be subject to these penny stock rules. Therefore, stockholders may have difficulty selling their securities.

Section 16(a)

Based solely upon a review of Form 3 and 4 furnished by us under Rule 16a-3(d) of the Securities Exchange Act of 1934, we are not aware of any individual who failed to file a required report on a timely basis required by Section 16(a) of the Securities Exchange Act of 1934.

| 17 |

| Table of Contents |

Item 7. Management's Discussion and Analysis of Financial Condition and Results of Operations

We have had $282,832 in operating revenues and $255,279 in cost of goods sold since our inception on March 31, 2015 through June 30, 2017. Our activities have been financed from $27,553 in gross profits, a loan of $1,231 from our sole officer and director, $4,000 from the sale of 4,000,000 shares of common stock to our director and $43,200 in proceeds from the sale of 1,080,000 shares at $0.04 per share to 31 independent shareholders pursuant to the company’s Registration Statement on Form S-1.

For the period from inception through June 30, 2017, we incurred operating expenses of $76,447, consisting primarily of advertising expenses, professional fees and office expenses and recorded a provision for income tax of $1,297 for a net loss of $48,894.

For the year ended June 30, 2017 we generated $125,386 in revenues and $113,880 in cost of goods sold for a gross profit of $11,507. We incurred operating expenses of $63,109, consisting primarily of advertising, general expense and depreciation expense for a net loss of $51,602.

For the year ended June 30, 2016 we generated $125,269 in revenues and $116,882 in cost of goods sold for a gross profit of $8,367. We incurred operating expenses of $3,625, consisting primarily of general expense and depreciation expense for a net loss of $3,625.

Plan of Operation for the next 12 months

Our cash balance is $2,756 as of June 30, 2017. Our cash balance is not sufficient to fund our limited levels of operations.

Even under a limited operations scenario to maintain our corporate existence, we believe we will require a minimum of $10,000 in additional cash over the next 12 months to maintain our regulatory reporting and filings. Management believes the company will require a minimum of approximately $40,000 over the next twelve months to remain in business, either from revenues or funding. We currently have no arrangement in place to cover this shortfall.

If we do not generate revenues, these funds will have to be raised through equity financing, debt financing, or other sources, which may result in the dilution in the equity ownership of our shares. We will also require additional financing to sustain our business operations if we are ultimately not successful in earning revenues. We currently do not have any arrangements regarding the offering or following the offering for further financing and we may not be able to obtain financing when required. Obtaining commercial loans, assuming those loans would be available, will increase our liabilities and future cash commitments.

There are no assurances that we will be able to obtain further funds required for our continued operations. Even if additional financing is available, it may not be available on terms we find favorable. At this time, there are no anticipated sources of additional funds in place. Failure to secure the needed additional financing will have an adverse effect on our ability to remain in business.

Our independent registered public accountant has issued a going concern opinion. This means that there is substantial doubt that we can continue as an on-going business for the next twelve months unless we obtain additional capital to pay our bills. This is because we have generated $282,832 in revenues but no significant increase in revenues are anticipated until we complete our initial business development. There is no assurance we will ever reach that stage. To meet our need for cash we have raised money from an offering pursuant to a Registration Statement filed on Form S-1, however we were only able to raise half the amount we anticipated. If we need additional cash and cannot raise it, we will either have to suspend operations until we do raise the cash, or cease operations entirely.

| 18 |

| Table of Contents |

We have commenced our steam room products distribution business.

During the first stages of our growth, our director will provide all of the labor required to execute our business plan at no charge. Funds will come from cash on hand from revenues or loans from our director.

Our president will devote approximately 10 to 20 hours of his time to our operations. Once we are able to attract more and more customers to buy our product he has agreed to commit more time as required. Because he will only be devoting limited time to our operations, our operations may be sporadic and occur at times which are convenient to him. As a result, operations may be periodically interrupted or suspended which could result in a lack of revenues and a cessation of operations.

Our specific goal is to profitably sell our product. Our plan of operations is as follows:

Negotiation With Potential Customers (Distributors And Brokers)

Months 1-6: We continue to negotiate agreements with national medium-sized wholesale and wholesale Steam Room Distribution companies. To date, several medium-sized wholesale Steam Room Distribution companies have expressed interest in our products. We have contacted buyers from these companies and have engaged in discussion regarding supplying Steam Room Distribution products; we sold to one of the Steam Room Distribution firms who continues to make repeat orders. We have no written agreements with any of them at the current time but we will be providing samples to several buyers in an attempt to secure contracts with these companies. We have purchased samples which will be provided to our main prospects; the cost of $43,100 was split between our offering proceeds and revenues.

Marketing

Months 1-12: We plan to advertise through home improvement trade shows and a road show campaign at the stores of our future customers, distributors and brokers. We continue to develop and maintain a database of potential customers who may want to purchase Steam Room products from us. We follow up with these clients periodically, send them our new catalogues and offer them presentations and special discounts from time to time. We plan to print catalogues and flyers and mail them to potential customers as part of our marketing campaign if we have the funds from revenues to do so. We intend to use marketing strategies, such as web advertisements, direct mailing, samples for main prospects and phone calls to acquire additional customers. We intend to spend $3,000-$5,000 on marketing efforts during the next year. Marketing is an ongoing matter that will continue during the life of our operations.

Development of Our Website

Months 7-12: During this period, we intend to further develop our website, if revenues will support the expense . We may hire a web designer to help us with the design and basic development of our website if our director is unable to accomplish it. We do not have any written agreements with any web designers at current time. The basic website development cost is expected to be $1,700. Updating and improving our website will continue throughout the lifetime of our operations.

| 19 |

| Table of Contents |

It is our plan that when we have enough money we want to start making and selling our own brand of steam room products (steam rooms).

For the current time, our company is focused on getting our second and third customer and selling them more of the steam rooms. I hope we can add second and third customer in the next 12-18 months.

Liquidity and Capital Resources

At June 30, 2017 the Company had $2,756 in cash and there were outstanding liabilities of $12,528. Our director has verbally agreed to continue to loan the company funds for operating expenses in a limited scenario, but he has no legal obligation to do so.

For the period from inception (March 31, 2015) to June 30, 2017, the Company had a net profit (loss) of $(50,394). The Company also has a negative net worth of $3,194. This raises substantial doubt about the Company’s ability to continue as a going concern within one year after the date that the financial statements are issued.

The ability to continue as a going concern is dependent upon the Company’s ability to successfully execute its business plan and generate profitable operations in the future, and/or to obtain the necessary financing to meet its obligations and repay its liabilities arising from normal business operation when they become due. Management intends to finance operating costs over the next twelve months with loans from related parties or the issuance of equity and debt securities.

The failure to achieve the necessary levels of profitability or obtain the additional funding would be detrimental to the Company.

Off-Balance Sheet Arrangements

We do not have any off-balance sheet arrangements that have or are reasonably likely to have a current or future effect on our financial condition, changes in financial condition, revenues or expenses, results of operations, liquidity, capital expenditures or capital resources that is material to investors.

| 20 |

| Table of Contents |

Item 8. Financial Statements

KIRTANE & PANDIT LLP CHARTERED ACCOUNTANTS

H-16, Saraswat Colony, Sitladevi Temple Road, Mahim (W), Mumbai 400016

T: 91-22-24444119 Email:kpcamumbai@kirtanepandit.com

To the Board of Directors and Stockholders'

Apex Resources Inc. Alyataus g. 100

Varna, Lithuania

Report of Independent Registered Public Accounting Firm

Opinion on the Financial Statements

We have audited the accompanying balance sheet of Apex Resources Inc. (the "Company") as of June 30, 2017, and June 30, 2016, the related statements of operations , changes in shareholders' equity, and cash flows for each of the two years in the period ended June 30, 2017 and the related notes ( collectively referred to as the “financial statements”). In our opinion, the financial statements present fairly, in all material respects, the financials position of the Company as of June 30, 2017 and 2016, and the results of its operations and its cash flows for each of the two years in the period ended June 30, 2017, in conformity with accounting principles generally accepted in the United States of America.

Basis of Opinion

The financial statements are the responsibility of the Company’s management. Our responsibility is to express an opinion on the Company’s financial statements based on our audits. We have served as the Company’s auditor since December 2016.

We are public accounting firm registered with the PCAOB and are required to be independent with respect to the Company in accordance with the U.S. federal securities laws and the applicable rules and regulations of the Securities and Exchange Commission and the PCAOB.

We conducted our audits in accordance with the standards of the PCAOB. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement, whether due to error or fraud. Our audits included performing procedures to assess the risks of material misstatement of the financial statements, whether due to error of fraud, and performing procedures that respond to those risks. Such procedures included examining, on a test basis, evidence regarding the amounts and disclosers in the financial statements. Our audits also included evaluating the accounting principles used and significant estimates made by management, as well as evaluating the overall presentation of the financial statements. We believe that our audit provide a reasonable basis for our opinion.

Critical Audit Matters

The accompanying financial statements have been prepared assuming that the company will continue as a going concern. As discussed in Note 3 to the financial statements, the company has incurred a net loss of $50,394 since inception and has a negative net worth of $3,194 as of June 30, 2017. Th is raises substantial doubt about the Company’s ability to continue as a going concern within one year after the date that the financial statements are issued .

The ability to continue as a going concern is dependent upon the Company’s ability to successfully execute its business plan and generate profitable operations in the future, and/or to obtain the necessary financing to meet its obligations and repay its liabilities arising from normal business operation when they become due. Management intends to finance operating costs over the next twelve months with loans from related parties or the issuance of equity and debt securities. Management has also given its plan in regard to these matters which are described in Note 3 to the financial statements. The financial statements do not include any adjustments that might result from the outcome of this uncertainty. Our opinion is not modified with respect to the matter.

For Kirtane & Pandit LLP

Chartered Accountants

FRN: 105215W/W100057

PCAOB FIRM ID NO 5686

Milind Bhave

Partner

Membership No. 047973

Place: Mumbai, India

Date: June 8, 2018

| 21 |

| Table of Contents |

| APEX RESOURCES INC |

| |||||||

| BALANCE SHEETS (Audited) |

| |||||||

|

|

|

|

|

|

|

| ||

|

|

| June 30, 2017 |

|

| June 30, 2016 |

| ||

|

|

|

|

|

|

|

| ||

| ASSETS |

| |||||||

|

|

|

|

|

|

|

| ||

| CURRENT ASSETS |

|

|

|

|

|

| ||

| Cash |

| $ | 2,756 |

|

| $ | 70 |

|

|

|

|

|

|

|

|

|

|

|

| TOTAL CURRENT ASSETS |

|

| 2,756 |

|

|

| 70 |

|

|

|

|

|

|

|

|

|

|

|

| FIXED ASSETS |

|

|

|

|

|

|

|

|

| Building |

| $ | 4,328 |

|

| $ | 4,328 |

|

| Accumulated Depreciation - Building |

|

| (577 | ) |

|

| (289 | ) |

| Land |

|

| 4,328 |

|

|

| 4,328 |

|

|

|

|

|

|

|

|

|

|

|

| TOTAL FIXED ASSETS |

|

| 8,078 |

|

|

| 8,366 |

|

|

|

|

|

|

|

|

|

|

|

| TOTAL ASSETS |

| $ | 10,834 |

|

| $ | 8,436 |

|

|

|

|

|

|

|

|

|

|

|

| LIABILITIES AND STOCKHOLDERS' EQUITY | ||||||||

|

|

|

|

|

|

|

|

|

|

| LIABILITIES |

|

|

|

|

|

|

|

|

| Current Liabilities: |

|

|

|

|

|

|

|

|

| Accounts Payable |

| $ | 10,000 |

|

| $ | - |

|

| Accrued Expenses |

|

| 1,500 |

|

|

| - |

|

| Loan Payable - Due to Director |

|

| 1,231 |

|

|

| 431 |

|

| Income Tax Payable |

|

| 1,297 |

|

|

| 1,297 |

|

|

|

|

|

|

|

|

|

|

|

| TOTAL LIABILITIES |

| $ | 14,028 |

|

| $ | 1,728 |

|

|

|

|

|

|

|

|

|

|

|

| STOCKHOLDERS' EQUITY |

|

|

|

|

|

|

|

|

| Common stock: authorized 75,000,000; $0.001 par value; 5,080,000 and 4,000,000 shares issued and outstanding at June 30, 2017 and June 30, 2016 |

| $ | 5,080 |

|

| $ | 4,000 |

|

| Additional Paid In Capital |

|

| 42,120 |

|

|

| - |

|

| Profit (loss) accumulated during the development stage |

|

| (50,394 | ) |

|

| 2,708 |

|

|

|

|

|

|

|

|

|

|

|

| Total Stockholders' Equity |

| $ | (3,194 | ) |

| $ | 6,708 |

|

|

|

|

|

|

|

|

|

|

|

| TOTAL LIABILITIES AND STOCKHOLDERS' EQUITY |

| $ | 10,834 |

|

| $ | 8,436 |

|

The accompanying notes are an integral part of these financial statements

| 22 |

| Table of Contents |

| APEX RESOURCES INC | ||||||||

| STATEMENTS OF OPERATIONS | ||||||||

| (Audited) | ||||||||

|

|

|

|

|

|

|

| ||

|

|

| Year |

|

| Year |

| ||

|

|

| Ended |

|

| Ended |

| ||

|

|

| June 30, 2017 |

|

| June 30, 2016 |

| ||

| REVENUES |

|

|

|

|

|

| ||

| Sales: |

|

|

|

|

|

| ||

| Merchandise Sales |

| $ | 125,386 |

|

| $ | 125,269 |

|

| Total Income |

|

| 125,386 |

|

|

| 125,269 |

|

|

|

|

|

|

|

|

|

|

|

| Cost of Goods Sold: |

|

|

|

|

|

|

|

|

| Purchases - Resale Items |

| $ | 113,880 |

|

| $ | 116,882 |

|

| Total Cost of Goods Sold |

|

| 113,880 |

|

|

| 116,882 |

|

|

|

|

|

|

|

|

|

|

|

| Gross Profit |

|

| 11,507 |

|

|

| 8,387 |

|

|

|

|

|

|

|

|

|

|

|

| Operating Expenses: |

|

|

|

|

|

|

|

|

| General and administrative |

| $ | 21,221 |

|

| $ | 7,492 |

|

| Depreciation |

|

| 289 |

|

|

| 289 |

|

| Advertising & Promotion |

|

| 43,100 |

|

|

| 4,232 |

|

|

|

|

|

|

|

|

|

|

|

| Total Expenses |

|

| 64,609 |

|

|

| 12,013 |

|

|

|

|

|

|

|

|

|

|

|

| Income Before Income Tax |

| $ | (53,102 | ) |

| $ | (3,625 | ) |

|

|

|

|

|

|

|

|

|

|

| Provision for Income Tax |

|

| - |

|

|

| - |

|

|

|

|

|

|

|

|

|

|

|

| Net Income for Period |

|

| (53,102 | ) |

|

| (3,625 | ) |

|

|

|

|

|

|

|

|

|

|

| Net gain (loss) per share: |

|

|

|

|

|

|

|

|

| Basic and diluted |

| $ | (0.0105 | ) |

| $ | (0.0009 | ) |

|

|

|

|

|

|

|

|

|

|

| Weighted average number of shares outstanding: |

|

|

|

|

|

|

|

|

| Basic and diluted |

|

| 5,080,000 |

|

|

| 4,000,000 |

|

The accompanying notes are an integral part of these financial statements

| 23 |

| Table of Contents |

| APEX RESOURCES INC | ||||||||||||||||||||

| STATEMENTS OF CHANGES IN SHAREHOLDERS' EQUITY (Audited) | ||||||||||||||||||||

| From Inception March 31, 2015 to June 30, 2017 | ||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||

|

|

| Common Stock |

|

|

|

|

|

|

|

| Total |

| ||||||||

|

|

| Number of |

|

|

|

|

| Additional |

|

| Accumulated |

|

| Shareholders' |

| |||||

|

|

| Shares |

|

| Par Value |

|

| Paid in Capital |

|

| Gain (Deficit) |

|

| Equity |

| |||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||

| Balance, March 31, 2015 (Inception) |

|

| - |

|

| $ | - |

|

| $ | - |

|

| $ | - |

|

| $ | - |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Common Shares issued: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| for cash on June 15, 2015 |

|

| 4,000,000 |

|

|

| 4,000 |

|

|

| - |

|

|

|

|

|

|

| 4,000 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Net gain (loss) |

|

| - |

|

|

| - |

|

|

| - |

|

|

| 6,334 |

|

|

| 6,334 |

|

| Balance, June 30, 2015 |

|

| 4,000,000 |

|

| $ | 4,000 |

|

| $ | - |

|

| $ | 6,334 |

|

| $ | 10,334 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Net gain (loss) |

|

| - |

|

|

| - |

|

|

| - |

|

|

| (3,625 | ) |

|

| (3,625 | ) |

| Balance, June 30, 2016 |

|

| 4,000,000 |

|

| $ | 4,000 |

|

| $ | - |

|

| $ | 2,708 |

|

| $ | 6,708 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Common Shares issued: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| for cash in November 2016 |

|

| 1,080,000 |

|

|

| 1,080 |

|

|

| 42,120 |

|

|

|

|

|

|

| 43,200 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Net gain (loss) |

|

| - |

|

|

| - |

|

|

| - |

|

|

| (53,102 | ) |

|

| (53,102 | ) |

| Balance, June 30, 2017 |

|

| 5,080,000 |

|

| $ | 5,080 |

|

| $ | 42,120 |

|

| $ | (50,394 | ) |

| $ | (3,194 | ) |