UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

| (Mark One) | |||||

| ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the fiscal year ended December 31 , 2022

OR

| TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the transition period from to .

Commission file number 001-37754

______________________________________________________________

(Exact name of registrant as specified in its charter)

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | ||||

(Address of principal executive offices, Zip Code)

(702 ) 495-3000

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act

| Title of each class | Trading symbol | Name of each exchange on which registered | ||||||

Securities registered pursuant to Section 12(g) of the Act

None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☑ No ☐

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No ☑

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☑ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☑ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

☑ | Accelerated filer | ☐ | |||||||||

| Non-accelerated filer | ☐ | Smaller reporting company | |||||||||

| Emerging growth company | |||||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C.7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☑

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ☐ No ☑

As of June 30, 2022, the last business day of the registrant’s most recently completed second fiscal quarter, the aggregate market value of the registrant’s Class A common stock held by non-affiliates (all persons other than executive officers or directors) was $1.6 billion, based on the closing price on that date as reported by the NASDAQ Stock Market LLC.

Indicate the number of shares outstanding of each of the registrant’s classes of common stock, as of the latest practicable date.

| Class | Outstanding at February 17, 2023 | |||||||

| Class A Common Stock, $0.01 par value | ||||||||

| Class B Common Stock, $0.00001 par value | ||||||||

Documents Incorporated by Reference

TABLE OF CONTENTS

2

PART I

ITEM 1.BUSINESS

Introduction

Red Rock Resorts, Inc. (“we,” “our,” “us,” “Red Rock” or the “Company”) is a holding company that owns an indirect equity interest in and manages Station Casinos LLC (“Station LLC”), through which we conduct all of our operations. Station LLC is a gaming, development and management company established in 1976 that develops and operates strategically-located casino and entertainment properties. Station LLC owns and operates six major gaming and entertainment facilities and ten smaller casinos (three of which are 50% owned). A subsidiary of Station LLC also managed Graton Resort & Casino (“Graton Resort”) in northern California on behalf of a Native American tribe through February 5, 2021. In addition, in the first quarter of 2022, we commenced construction of Durango Casino & Resort (“Durango”) on our approximately 50-acre development site at the intersection of Durango Drive and Interstate 215 in the southwest Las Vegas valley. Durango is expected to open in the fourth quarter of 2023.

We own all of the outstanding voting interests in Station LLC and have an indirect equity interest in Station LLC through our ownership of limited liability interests in Station Holdco LLC (“Station Holdco,” and such interests, “LLC Units”), which owns all of the economic interests in Station LLC. At December 31, 2022, we held 58% of the economic interests and 100% of the voting power in Station Holdco, subject to certain limited exceptions, and we are designated as the sole managing member of both Station Holdco and Station LLC. We control and operate all of the business and affairs of Station Holdco and Station LLC. Other than tax-related assets and liabilities, our only material assets are our equity interest in Station Holdco and our voting interest in Station LLC. We have no operations outside of our management of Station Holdco and Station LLC.

Our Consolidated Financial Statements in Part II, Item 8 of this Annual Report on Form 10-K (the “Consolidated Financial Statements”) reflect the consolidation of Station LLC and its consolidated subsidiaries and Station Holdco. The financial position and results of operations attributable to LLC Units we do not own are reported separately as noncontrolling interest.

Our casino properties are conveniently located throughout the Las Vegas valley and provide our customers a wide variety of entertainment and dining options. Over 90% of the Las Vegas population is located within five miles of one of our gaming facilities. We provide friendly service and exceptional value in a comfortable environment. We believe we surpass our competitors in offering casino patrons the newest and most popular slot and video games featuring the latest technology. We also believe the high-quality entertainment experience we provide our customers differentiates us from our competitors.

Most of our major properties are master-planned for expansion, enabling us to incrementally expand our facilities as demand dictates. We also control six highly desirable gaming-entitled development sites in Las Vegas.

Our principal source of revenue and operating income is gaming, and our non-gaming offerings include restaurants, hotels and other entertainment amenities. Approximately 80% to 85% of our casino revenue is generated from slot play. The majority of our revenue is cash-based and as a result, fluctuations in our revenues have a direct impact on our cash flows from operations. Because our business is capital intensive, we rely heavily on the ability of our properties to generate operating cash flow to repay debt financing and fund capital expenditures.

Our principal executive offices are located at 1505 South Pavilion Center Drive, Las Vegas, Nevada 89135. The telephone number for our executive offices is (702) 495-3000. We maintain a website at www.redrockresorts.com, the contents of which are expressly not incorporated by reference into this filing.

Impact of Local Economic Conditions and COVID-19

A significant portion of our business is dependent upon customers who live and/or work in the Las Vegas metropolitan area. As of December 2022, the unemployment rate in the Las Vegas metropolitan area was 5.4%, down from 6.0% in December 2021 and 34% in April 2020. Statewide, the unemployment rate for December 2022 was 5.2%, consistent with the prior year, reflecting a significant decrease from the statewide unemployment rate of 30% in April 2020. The median price of an existing single-family home in Las Vegas was $425,000 at December 31, 2022, unchanged from December 31, 2021, according to the Las Vegas Realtors®, but down 11.5% from the all-time high of $480,000 in June 2022. In addition, Las Vegas remains one of the fastest growing metropolitan areas in the United States, posting a 2.1% growth rate in 2022. In light

3

of uncertainty in the economic outlook stemming from inflation, rising interest rates and increased energy costs, we cannot predict whether the recovery in unemployment or the downward trend in housing prices in the Las Vegas area will continue.

During 2020, our business was negatively impacted by the global pandemic caused by a new strain of coronavirus (“COVID-19”). All of our Las Vegas properties were temporarily closed on March 17, 2020 in compliance with a statewide emergency order mandating the closure of all nonessential businesses in Nevada, including casinos. On June 4, 2020, we reopened our Red Rock, Green Valley Ranch, Santa Fe Station, Boulder Station, Palace Station and Sunset Station properties, as well as our Wildfire properties, subject to state-mandated occupancy and other operational restrictions.

In June 2022, we permanently closed our Texas Station, Fiesta Henderson and Fiesta Rancho properties, which had been closed since March 2020 as a result of the COVID-19 pandemic, and we sold the Fiesta Henderson site in December 2022. The facilities at Texas Station and Fiesta Rancho are being demolished in whole or in part to reposition the land for sale. In addition, we permanently closed Wild Wild West in September 2022.

The properties we reopened in June 2020 have continued to experience favorable customer trends in 2022, including strong visitation from our guests, including a younger demographic, increased spend per visit, and increased return of our core customers. These positive trends, in combination with business optimization and cost reduction measures implemented in the second quarter of 2020, have continued to drive strong operating results for our company. However, we cannot predict whether these trends will continue, nor can we predict the extent to which the impacts of inflation, increased energy costs, rising interest rates and the COVID-19 pandemic and its related variants on the United States and Las Vegas economies may affect our business in the future.

Business Strategy

Our primary operating strategy emphasizes attracting and retaining customers, primarily Las Vegas residents and, to a lesser extent, out-of-town visitors. Our properties attract customers through:

•convenient locations with best-in-class assets;

•offering our customers the latest in slot and video poker technology;

•a variety of non-gaming amenities such as hotel resorts, restaurants, bars and entertainment options;

•focused marketing efforts targeting our extensive customer database;

•innovative, frequent promotional programs; and

•convention business.

The Las Vegas regional market is very competitive, and we compete with both large hotel casinos in Las Vegas and smaller gaming-only establishments throughout the Las Vegas valley.

Provide a high quality, value-oriented gaming and entertainment experience. We are committed to providing a high-value entertainment experience for our guests, as our significant level of repeat visitors demand exceptional service, variety and quality in their overall experience. We offer a broad array of gaming options, including the most popular slot and video poker products, and the latest technological innovations in slots, table games and sports wagering. We believe that providing a wide variety of entertainment options is also a significant factor in attracting guests. In particular, we feature multiple dining options at all of our major properties, which is a primary motivation for casino visits. We are dedicated to ensuring a high level of guest satisfaction and loyalty by providing attentive guest service in a convenient, friendly and casual atmosphere. As part of our commitment to providing a high-value entertainment experience and to stimulate visitation, we regularly refresh and enhance our gaming and non-gaming amenities.

Generate revenue growth through targeted marketing and promotional programs. Our advertising programs generate consistent brand awareness and promotional visibility. Our ability to advertise under a single brand across our portfolio also allows us to achieve material economies of scale. While we advertise through traditional media such as television, radio and newspaper to reach our core guests, we continue to expand our focus and spend on social, digital and mobile platforms to respond to the evolving trends in methods through which guests receive information.

We employ an innovative marketing strategy that utilizes our frequent promotional programs to attract and retain guests, while also establishing and maintaining a high level of brand recognition. Through our analytical approach to promotional development, we are also able to optimize reinvestment in those guests who deliver stronger results. Our

4

proprietary customer relationship management systems are highly attuned to how guests interact with our properties and products. This information allows us to focus on targeting guests based on their preferences.

We have installed technology on all of our slot machines which permits us to provide “on device” marketing, bonusing and guest communication, including real-time customized promotions and incentives. We believe that this investment in technology has resulted in an increase in guest loyalty and enhanced the value of our loyalty program. As we continue to introduce new features and brand titles for customized promotional incentives, the technology should continue to help drive participation in our my|Rewards Boarding Pass loyalty program.

Maximize business profitability. During our over 46-year history, we have developed a culture that focuses on operational excellence and cost management. We believe that this focus has contributed to adjusted earnings before interest, taxes, depreciation and amortization (“Adjusted EBITDA”) margins that compare favorably to our public peers over the past several years. Our internally developed proprietary systems and analytical tools provide us with the ability to closely monitor revenues and operational expenses and provide real-time information to management. Benchmarking across our properties also allows us to create and take advantage of best practices in all functional areas of our business. We believe our existing cost structure, which has low variable costs, can support significant incremental revenue growth while maximizing the flow-through of revenue to Adjusted EBITDA.

Utilize flexible capital structure to drive growth and equityholder returns. We maintain a flexible capital structure that we believe allows us to pursue a balance of new growth opportunities and a disciplined return of capital to our equityholders. We believe our scalable platform and extensive development and management expertise provide us the ability to build master-planned expansions, pursue acquisitions and/or seek new development opportunities in an effort to maximize equityholder returns.

Maintain strong employee relations. Station LLC began as a family-run business in 1976 and has maintained close-knit relationships among our management, and we endeavor to instill this same sense of loyalty among our employees. Toward this end, we take a hands-on approach through active and direct involvement with employees at all levels. We believe we have excellent employee relations. See “Human Capital” for more information on our employee relations. In addition, see “Risk Factors—Business, Economic, Market and Operating Risks—Union organization activities could disrupt our business by discouraging patrons from visiting our properties, causing labor disputes or work stoppages, and, if successful, could significantly increase our labor costs.”

Develop and operate Native American projects. We provide development and management services to Native American tribes using our expertise in developing and operating regional entertainment destinations.

5

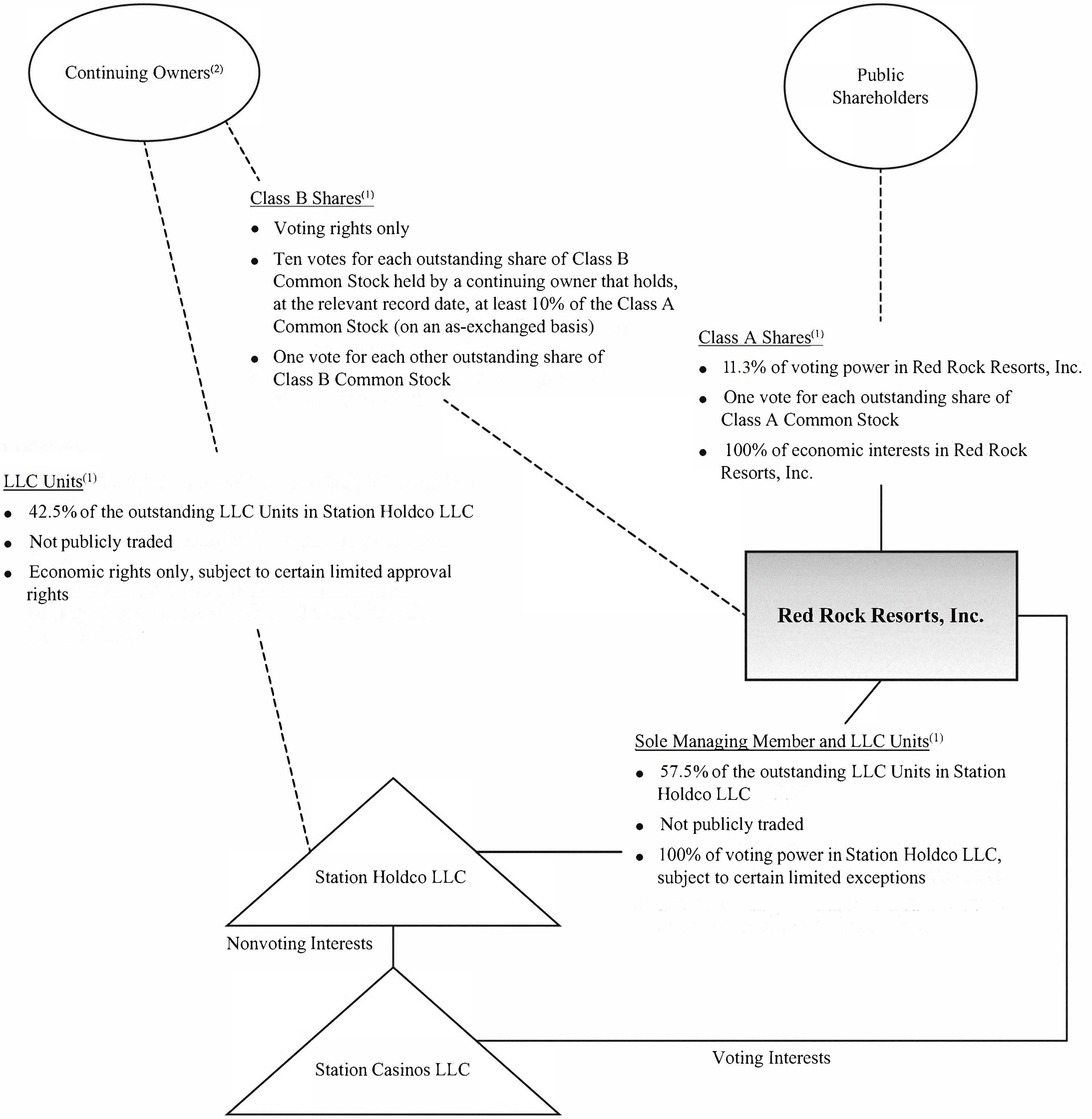

Organizational Structure

The following chart summarizes our organizational structure as of December 31, 2022. This chart is provided for illustrative purposes only and does not purport to represent all legal entities owned or controlled by us:

___________________________________________________________

(1) Shares of Class A common stock and Class B common stock vote as a single class. Each outstanding share of Class A common stock is entitled to one vote; each outstanding share of Class B common stock that is held by a holder that, together with its affiliates, owned at least 30% of the outstanding LLC Units immediately following the consummation of the Company’s public offering in 2016 (the “IPO”) and, at the applicable record date, maintains direct or indirect beneficial ownership of at least 10% of the outstanding shares of Class A common stock (determined on an as-exchanged basis assuming that all of the LLC Units were exchanged for Class A common stock) is entitled to ten votes; and each other outstanding share of Class B common stock is entitled

6

to one vote. The only holders of Class B common stock that satisfy the foregoing criteria are entities controlled by Frank J. Fertitta III, our Chairman of the Board and Chief Executive Officer, and Lorenzo J. Fertitta, our Vice Chairman of the Board and a Vice President. These entities are referred to herein as the “Fertitta Family Entities” or “Principal Equity Holders.” The exchange ratio for LLC Units and shares of Class B common stock for shares of Class A common stock is a fraction, the numerator of which shall be the number of shares of Class A common stock outstanding immediately prior to the applicable exchange and the denominator of which shall be the number of LLC Units owned by Red Rock and its subsidiaries immediately prior to applicable exchange. The initial exchange ratio at the IPO date was one share of Class A common stock for each LLC Unit and share of Class B common stock. The exchange ratio is subject to adjustment in the event that the number of outstanding shares of Class A common stock does not equal the number of LLC Units held by Red Rock, including as a result of purchases of shares of Class A common stock by Red Rock with excess cash on hand that does not result in a reduction in the outstanding number of LLC Units held by Red Rock. At December 31, 2022, the exchange ratio was 0.9340 shares of Class A common stock for each LLC Unit and share of Class B common stock.

(2) “Continuing Owners” refers to the owners of LLC Units at December 31, 2022 who held such units prior to the Company’s IPO in May 2016.

Properties

Set forth below is selected information about our properties at December 31, 2022.

| Hotel Rooms | Slots (1) | Gaming Tables (2) | Acreage | ||||||||||||||||||||

| Las Vegas Properties | |||||||||||||||||||||||

| Red Rock | 795 | 2,621 | 53 | 64 | |||||||||||||||||||

| Green Valley Ranch | 495 | 2,219 | 39 | 40 | |||||||||||||||||||

| Palace Station | 575 | 1,607 | 51 | 30 | |||||||||||||||||||

| Boulder Station | 299 | 2,218 | 23 | 46 | |||||||||||||||||||

| Sunset Station | 457 | 2,011 | 30 | 75 | |||||||||||||||||||

| Santa Fe Station | 200 | 2,145 | 37 | 39 | |||||||||||||||||||

| Wildfire Rancho | — | 157 | — | 5 | |||||||||||||||||||

| Wildfire Boulder | — | 161 | — | 2 | |||||||||||||||||||

| Wildfire Sunset | — | 132 | — | 1 | |||||||||||||||||||

| Wildfire Lake Mead | — | 195 | — | 3 | |||||||||||||||||||

| Wildfire Valley View | — | 35 | — | — | |||||||||||||||||||

| Wildfire Anthem | — | 15 | — | — | |||||||||||||||||||

| 50% Owned Properties | |||||||||||||||||||||||

| Barley’s | — | 184 | — | — | |||||||||||||||||||

| The Greens | — | 40 | — | — | |||||||||||||||||||

| Wildfire Lanes | — | 181 | — | 7 | |||||||||||||||||||

| 2,821 | 13,921 | 233 | 312 | ||||||||||||||||||||

_____________________________________________

(1)Includes slot and video poker machines.

(2)Generally includes blackjack (“21”), craps, roulette, pai gow and baccarat.

Red Rock

Red Rock opened in 2006 and is strategically located at the intersection of Interstate 215 and Charleston Boulevard in the Summerlin master-planned community in Las Vegas, Nevada. Red Rock is adjacent to Downtown Summerlin, a 1.6 million square-foot outdoor shopping, dining and entertainment center; City National Arena, which features two National Hockey League-sized ice sheets for use by both the Vegas Golden Knights team and the public; and Las Vegas Ballpark, the home of the Las Vegas Aviators professional Triple-A baseball team. Red Rock’s gaming amenities include slots, table games, and a race and sports book. Red Rock is a AAA Four Diamond resort featuring an elegant desert oasis theme with a contemporary design featuring luxury amenities. This resort offers six styles of suites, including one-of-a-kind custom villas and penthouse suites, in addition to standard guest rooms. Additional non-gaming amenities include nine full-service restaurants, a 16-screen movie theater complex, approximately 94,000 square feet of meeting and convention space, a full-service spa and salon, a 72-

7

lane bowling center, a Kid’s Quest child care facility and a gift shop. Red Rock also features numerous bars and lounges, new high limit slot and table games rooms and offers a variety of quick-serve restaurants.

Green Valley Ranch

Green Valley Ranch opened in 2001 and is strategically located at the intersection of Interstate 215 and Green Valley Parkway in Henderson, Nevada. Green Valley Ranch is approximately five minutes from Harry Reid International Airport and seven minutes from the Las Vegas Strip. Green Valley Ranch was designed to complement the Green Valley master-planned community. Green Valley Ranch gaming amenities include slots, table games and a race and sports book. Green Valley Ranch is a Mediterranean-style AAA Four Diamond resort featuring standard guest rooms and suites, eight full-service restaurants, a 4,200-square-foot non-gaming arcade, a European Spa with outdoor pools, a 10-screen movie theater complex, a Kid’s Quest child care facility, a gift shop and approximately 65,000 square feet of meeting and convention space which includes the Grand Events Center and El Cielo Ballroom. Green Valley Ranch also offers an eight-acre outdoor complex featuring private poolside cabanas and a contemporary poolside bar and grill. Green Valley Ranch also features several bars and offers a variety of quick-serve restaurants.

Palace Station

Palace Station opened in 1976 and is strategically located at the intersection of Sahara Avenue and Interstate 15, one of Las Vegas’ most heavily traveled areas. Palace Station is a short distance from Harry Reid International Airport and very close to major attractions on the Las Vegas Strip and in downtown Las Vegas. Palace Station’s gaming amenities include slots, table games and a race and sports book. Palace Station’s non-gaming amenities include a resort-style pool area, a nine-screen Regal Cinebarre luxury movieplex, four full-service restaurants, three bars, an approximately 20,000-square-foot meeting and convention center and a gift shop. In addition to its full-service restaurants, Palace Station also offers a variety of quick-serve restaurants.

Boulder Station

Boulder Station opened in 1994 and is strategically located at the intersection of Boulder Highway and Interstate 515. Boulder Station is located approximately four miles east of the Las Vegas Strip and approximately four miles southeast of downtown Las Vegas. Boulder Station features a turn-of-the-20th-century railroad station theme. Gaming amenities include slots, table games and a race and sports book. Non-gaming amenities include three full-service restaurants, a 750-seat entertainment lounge, four bars, an 11-screen movie theater complex, a Kid’s Quest child care facility, a swimming pool, a non-gaming video arcade and a gift shop. Boulder Station also offers a variety of quick-serve restaurants.

Sunset Station

Sunset Station opened in 1997 and is strategically located at the intersection of Interstate 515 and Sunset Road. Situated in a highly concentrated commercial corridor along Interstate 515, Sunset Station has prominent visibility from the freeway and the Sunset commercial corridor. Sunset Station is located approximately 4.5 miles east of Harry Reid International Airport and approximately 5.5 miles southeast of Boulder Station. Sunset Station features a Spanish/Mediterranean style theme. Gaming amenities include slots, table games and a race and sports book. Non-gaming amenities include four full-service restaurants, approximately 13,000 square feet of meeting space, a 500-seat entertainment lounge, a 5,000-seat outdoor amphitheater, six bars, a gift shop, a non-gaming video arcade, a 13-screen luxury seating movie theater complex, a 72-lane bowling center, a Kid’s Quest child care facility and a swimming pool. In addition, the center of the casino features a bar highlighted by over 8,000 square feet of stained glass. Sunset Station also offers a variety of quick-serve restaurants.

Santa Fe Station

We purchased Santa Fe Station in 2000 and subsequently refurbished and expanded the facility. Santa Fe Station is strategically located at the intersection of U.S. Highway 95 and Rancho Drive. Santa Fe Station’s gaming amenities include slots, table games and a race and sports book. Non-gaming amenities include four full-service restaurants, a gift shop, a non-gaming video arcade, a swimming pool, a 500-seat entertainment lounge, four bars and grills, a 60-lane bowling center, a 16-screen luxury seating movie theater complex, a Kid’s Quest child care facility and over 14,000 square feet of meeting and banquet facilities. Santa Fe Station also features a bar which is a centerpiece of the casino. In addition, Santa Fe Station offers a variety of quick-serve restaurants.

8

Wildfire Fremont

We opened Wildfire Fremont in February 2023. Wildfire Fremont is located on Fremont Street approximately three miles northwest of Boulder Station. Wildfire Fremont has approximately 200 slot machines, a sports book, two full-service restaurants and a bar.

Wildfire Rancho

We purchased Wildfire Rancho in 2003. Wildfire Rancho is located on Rancho Drive, approximately five miles southeast of Santa Fe Station. Wildfire Rancho’s gaming amenities include slots and a sports book. Wildfire Rancho’s non-gaming amenities include a lounge, outdoor patio and quick-serve food offerings.

Wildfire Boulder and Wildfire Sunset

We purchased Wildfire Boulder and Wildfire Sunset in 2004. Both properties are located in Henderson, Nevada, and offer gaming amenities which include slots and a sports book. In addition, both properties offer non-gaming amenities which include a quick-serve restaurant and a bar. Wildfire Boulder is located approximately eight miles southeast of Sunset Station. Wildfire Sunset is located next to Sunset Station.

Wildfire Lake Mead

We purchased Wildfire Lake Mead in 2006. Wildfire Lake Mead, which is located in Henderson, Nevada, features slots, a sports book, a bar and quick-serve food offerings.

Wildfire Valley View and Wildfire Anthem

We purchased Wildfire Valley View and Wildfire Anthem in 2013. Wildfire Valley View is located in Las Vegas and Wildfire Anthem is located in Henderson, Nevada. Gaming amenities offered by Wildfire Valley View and Wildfire Anthem include slots. Non-gaming amenities offered by Wildfire Valley View and Wildfire Anthem include a bar and quick-serve food offerings.

Barley’s, The Greens and Wildfire Lanes

We own a 50% interest in three smaller properties in Henderson, Nevada including Barley’s, which features slots, a sports book and a brewpub, The Greens, which features slots, a restaurant and lounge, and Wildfire Lanes, which features slots, a sports book, a quick-serve restaurant, two bars and an 18-lane bowling center.

Closed Properties

In June 2022, we permanently closed our Texas Station, Fiesta Henderson and Fiesta Rancho properties, which had been closed since March 2020 as a result of the COVID-19 pandemic. We sold the Fiesta Henderson property in December 2022. The facilities at Texas Station and Fiesta Rancho are being demolished in whole or in part to reposition the land for sale. In addition, we permanently closed Wild Wild West in September 2022.

Property in Development

Durango Casino & Resort

We are currently developing a new casino resort, Durango, on our approximately 50-acre development site at the intersection of Durango Drive and Interstate 215 in the southwest Las Vegas valley. The site has excellent visibility and access from Interstate 215. As a result of gaming and land use restrictions, there are no major casino sites, other than those owned by us, within approximately five miles of this site. We expect to spend approximately $750 million for the project, which will be funded using a combination of available cash, cash flow from operations and borrowings under our revolving credit facility. We anticipate completion in the fourth quarter of 2023. We expect the project to comprise approximately 533,000 square feet and include 73,000 square feet of casino space with over 2,300 slots and 50 table games, over 200 hotel rooms, four full-service food and beverage outlets, a food hall, a state-of-the-art race and sports book and a resort-style pool.

Developable Land

We own approximately 395 acres of developable land comprised of six strategically-located parcels in Las Vegas, Nevada, each of which is zoned for casino gaming and other commercial uses. Following is a description of our parcels of land held for development:

9

Land Held for Development

•Viva: We own approximately 49 acres of land located at the intersection of Tropicana Boulevard and Interstate 15, less than one-half mile from the Las Vegas Strip. This site has excellent visibility and access from Interstate 15, on which approximately 290,000 cars per day pass by the site. We own a number of commercial and industrial buildings on this site that we lease to third-party tenants.

•Flamingo/I-215: We own approximately 58 acres located between Flamingo Road and Interstate 215 in the master-planned community of Summerlin in Las Vegas. The site has excellent visibility and access from Interstate 215.

•Cactus Avenue: We own approximately 128 acres near the intersection of Las Vegas Boulevard and Cactus Avenue, approximately six miles south of the Las Vegas Strip.

•Via Inspirada/Bicentennial Parkway: We own approximately 45 acres located on Via Inspirada near Bicentennial Parkway in the Las Vegas valley, approximately six miles southwest of Green Valley Ranch. This site is the only casino gaming-entitled property in the master-planned community of Inspirada.

•Skye Canyon: We own approximately 48 acres in northwestern Las Vegas off of U.S. Highway 95 approximately seven miles northwest of Santa Fe Station.

•Losee Road/I-215: We own approximately 67 acres of land near the intersection of Interstate 215 and Losee Road in North Las Vegas.

Native American Development

We have entered into development and management agreements with the North Fork Rancheria of Mono Indians (the “Mono”), a federally recognized Native American tribe located near Fresno, California, under which we will assist the Mono in developing and operating a gaming and entertainment facility (the “North Fork Project”) to be located on a 305-acre site (the “North Fork Site”) located adjacent to U.S. Highway 99 north of the city of Madera in Madera County, California. The North Fork Site was taken into trust for the benefit of the Mono by the United States Department of the Interior in February 2013.

We expect to receive a development fee of 4% of the costs of construction (as defined in the development agreement) for our development services, which will be paid upon the commencement of gaming operations at the facility. The management agreement provides for a management fee of 30% of the facility’s net income. As currently contemplated, the North Fork Project is expected to include approximately 2,000 slot machines, approximately 40 table games and several restaurants. The management agreement and the development agreement have a term of seven years from the opening of the facility.

Development of the North Fork Project is subject to certain governmental and regulatory approvals, including, but not limited to, approval of the management agreement by the National Indian Gaming Commission (“NIGC”).

The development of the North Fork Project is subject to ongoing legal challenges, the receipt of required regulatory approvals and financing. There can be no assurance that the North Fork Project will be successfully completed nor that future events and circumstances will not change our estimates of the timing, scope, and potential for successful completion or that any such changes will not be material. There can be no assurance that we will recover all of our investment in the North Fork Project even if it is successfully completed and opened for business. See Note 6 to the Consolidated Financial Statements for additional information about the North Fork Project.

Intellectual Property

We use a variety of trade names, service marks, trademarks, patents and copyrights in our operations and believe that we have all the licenses necessary to conduct our continuing operations. We have registered several service marks, trademarks, patents and copyrights with the United States Patent and Trademark Office or otherwise acquired the licenses to use those which are material to conduct our business. We file copyright applications to protect our creative artworks, which are often featured in property branding, as well as our distinctive website content.

Seasonality

Our cash flows from operating activities are somewhat seasonal in nature. Our operating results are traditionally strongest in the fourth quarter and weakest in the third quarter.

10

Competition

Our casino properties face competition from all other casinos and hotels in the Las Vegas area, including to some degree, from each other. We compete with other nonrestricted casino/hotels, as well as restricted gaming locations, by focusing on repeat customers and attracting these customers through great service and innovative marketing programs. Our value-oriented, high-quality approach is designed to generate repeat business. Additionally, our casino properties are strategically located and designed to permit convenient access and ample free parking, which are critical factors in attracting local visitors and repeat patrons.

At December 31, 2022, there were approximately 39 major gaming properties located on or near the Las Vegas Strip, 15 located in the downtown area and several located in other areas of Las Vegas. We also face competition from 143 nonrestricted gaming locations in the Clark County area primarily targeted to the local and repeat visitor markets. In addition, our casino properties face competition from restricted gaming locations (sites with 15 or fewer slot machines) in the greater Las Vegas area. At December 31, 2022, there were approximately 1,480 restricted gaming locations in Clark County with approximately 14,370 slot machines. Major additions, expansions or enhancements of existing properties or the construction of new properties by competitors could have a material adverse effect on our business.

The Nevada legislature enacted SB 208 in 1997. This legislation identified certain gaming enterprise districts wherein casino gaming development would be permitted throughout the Las Vegas valley and established more restrictive criteria for the establishment of new gaming enterprise districts. We believe the growth in gaming supply in the Las Vegas regional market has been, and will continue to be, limited by the provisions of SB 208.

To a lesser extent, we compete with gaming operations in other parts of the state of Nevada, such as Reno, Laughlin and Lake Tahoe, and other gaming markets throughout the United States and in other parts of the world, and with state sponsored lotteries, on- and off-track wagering on horse and other races, sports betting, card rooms, online gaming and other forms of legalized gambling. The gaming industry also includes land-based casinos, dockside casinos, riverboat casinos, racetracks with slots and casinos located on Native American land. There is intense competition among companies in the gaming industry, some of which have significantly greater resources than we do. In May 2018, the United States Supreme Court overturned a law prohibiting states from legalizing sports wagering which, together with the expansion of sports gaming as a result of the COVID-19 pandemic, has resulted in a substantial expansion of sports gaming outside the state of Nevada. Several states have legalized or are considering legalizing casino gaming in designated areas. Legalized casino and sports gaming in various states and on Native American land could result in additional competition and could adversely affect our operations, particularly to the extent that such gaming is conducted in areas close to our operations. We also face competition from internet poker and sports betting operators in Nevada. In addition, internet gaming has commenced in Nevada, New Jersey, Delaware, Pennsylvania, Michigan and West Virginia, internet sports betting has commenced in a number of states, and legislation permitting internet gaming has been approved or proposed by a number of other states. Expansion of internet gaming in new or existing jurisdictions and on Native American land could result in additional competition for our Las Vegas operations and for the gaming facilities that we may manage for Native American tribes.

Native American gaming in California, as it currently exists, has had limited impact on our Las Vegas operations to date, although there are no assurances as to the future impact it may have. In total, 76 Native American tribes have Tribal-State Compacts with the State of California or procedures with the Secretary of the Interior to operate Class III gaming in California. At December 31, 2022, there were 67 Native American gaming facilities in operation in the State of California. These Native American tribes are allowed to operate slot machines, lottery games, and banked and percentage games (including “21”) on Native American lands. A banked game is one in which players compete against the licensed gaming establishment rather than against one another. A percentage game is one in which the house does not directly participate in the game, but collects a percentage of the amount of bets made, winnings collected, or the amount of money changing hands. It is not certain whether any additional expansion of Native American gaming in California will affect our Las Vegas operations given that visitors from California make up Nevada’s largest visitor market. Increased competition from Native American gaming in California may result in a decline in our revenues and may have a material adverse effect on our business.

Regulation and Licensing

In addition to gaming regulations, our business is subject to various federal, state and local laws and regulations of the United States and Nevada. These laws and regulations include, but are not limited to, restrictions concerning employment and immigration status, currency transactions, zoning and building codes, protection of human health and safety and the environment, marketing and advertising, privacy and telemarketing. Since we deal with significant amounts of cash in our operations, we are subject to various reporting and anti-money laundering regulations. Any violations of anti-money laundering

11

laws or any of the other laws or regulations to which we are subject could result in regulatory actions, fines, or other penalties. Any material changes, new laws or regulations or material differences in interpretations by courts or governmental authorities or material regulatory actions, fines, penalties or other actions could adversely affect our business and operating results.

Nevada Gaming Laws and Regulations

The ownership and operation of casino gaming facilities and the manufacture and distribution of gaming devices in Nevada are subject to the Nevada Gaming Control Act and the rules and regulations promulgated thereunder (collectively, the “Nevada Act”) and various local ordinances and regulations. Our gaming operations in Nevada are subject to the licensing and regulatory control of the Nevada Gaming Commission (the “Nevada Commission”), the Nevada State Gaming Control Board (the “Nevada Board”), the Las Vegas City Council, the Clark County Liquor and Gaming Licensing Board (the “CCLGLB”), the North Las Vegas City Council, the Henderson City Council and certain other local regulatory agencies. The Nevada Commission, Nevada Board, Las Vegas City Council, CCLGLB, North Las Vegas City Council, Henderson City Council, and certain other local regulatory agencies are collectively referred to as the “Nevada Gaming Authorities.”

The laws, regulations and supervisory procedures of the Nevada Gaming Authorities are based upon declarations of public policy which are concerned with, among other things: (i) the prevention of unsavory or unsuitable persons from having a direct or indirect involvement with gaming at any time or in any capacity; (ii) the establishment and maintenance of responsible accounting practices and procedures; (iii) the maintenance of effective controls over the financial practices of gaming licensees, including the establishment of minimum procedures for internal controls and the safeguarding of assets and revenues, providing reliable record keeping and requiring the filing of periodic reports with the Nevada Gaming Authorities; (iv) the prevention of cheating and fraudulent practices; and (v) providing a source of state and local revenues through taxation and licensing fees. Changes in such laws, regulations and procedures could have an adverse effect on our gaming operations.

Our indirect subsidiaries that conduct gaming operations in Nevada are required to be licensed by the Nevada Gaming Authorities. The gaming licenses require the periodic payment of fees and taxes and are not transferable. NP Red Rock LLC, NP Boulder LLC, NP Palace LLC, NP Sunset LLC, NP Gold Rush LLC, NP Magic Star LLC, NP Rancho LLC, NP Santa Fe LLC, Station GVR Acquisition, LLC, SC SP 2 LLC, NP LML LLC, NP Centerline Holdings LLC and NP River Central LLC hold licenses to conduct nonrestricted gaming operations. NP Opco Holdings is registered as an intermediary company and is licensed as the sole member and manager of NP Opco LLC. NP Opco LLC is registered as an intermediary company, is licensed as the sole member and manager of NP Santa Fe LLC, NP Gold Rush LLC, NP Magic Star LLC, NP Rancho LLC, NP River Central LLC, and Station GVR Acquisition LLC. NP Opco LLC is found suitable as the sole member and manager of NP Green Valley LLC, SC SP Holdco LLC and NP LML LLC. Our ownership in SC SP 2 LLC is held through SC SP Holdco LLC which has a registration as an intermediary company and a license as a member and manager of SC SP 2 LLC. Town Center Amusements, Inc., a Limited Liability Company is licensed to conduct nonrestricted gaming operations at Barley’s. Greens Café, LLC is licensed to conduct nonrestricted gaming operations at The Greens, and Sunset GV, LLC is licensed to conduct nonrestricted gaming operations at Wildfire Lanes. A license to conduct “nonrestricted” operations is a license to conduct an operation of (i) at least 16 slot machines, (ii) any number of slot machines together with any other game, gaming device, race book or sports pool at one establishment, (iii) a slot machine route, (iv) an inter-casino linked system, or (v) a mobile gaming system. SC SP 4 LLC holds a restricted gaming license, which is a state gaming license to operate not more than 15 slot machines and no other gaming device, race book or sports pool. We are required to periodically submit detailed financial and operating reports to the Nevada Commission and provide any other information that the Nevada Commission may require. Substantially all material loans, leases, sales of securities and similar financing transactions by us and our licensed or registered subsidiaries must be reported to or approved by the Nevada Commission and/or the Nevada Board.

We have been found suitable to indirectly own the equity interests in our licensed and registered subsidiaries (the “Gaming Subsidiaries”) and we are registered by the Nevada Commission as a publicly traded corporation for purposes of the Nevada Act (a “Registered Corporation”). On September 22, 2022, the Nevada Commission approved the Eighth Revised Order of Registration for the Company that, among other things, reaffirmed our registration as a publicly traded corporation for the purposes of the Nevada Act (“Eighth Revised Order”). As a Registered Corporation, we are required to periodically submit detailed financial and operating reports to the Nevada Board and provide any other information the Nevada Board may require. No person may become a more than 5% stockholder or holder of more than a 5% interest in, or receive any percentage of gaming revenue from the Gaming Subsidiaries without first obtaining licenses, approvals and/or applicable waivers from the Nevada Gaming Authorities.

The Nevada Gaming Authorities may investigate any individual who has a material relationship to, or material involvement with, a Registered Corporation or its licensed subsidiaries, in order to determine whether such individual is suitable or should be licensed as a business associate of a Registered Corporation or a gaming licensee. Officers, directors and

12

certain key employees of our licensed subsidiaries must file applications and may be required to be licensed or found suitable by the Nevada Gaming Authorities. Our officers, directors and key employees who are actively and directly involved in gaming activities of our licensed subsidiaries may be required to be licensed or found suitable by the Nevada Gaming Authorities. The Nevada Gaming Authorities may deny an application for licensing for any cause that they deem reasonable. A finding of suitability is comparable to licensing, and both require submission of detailed personal and financial information followed by a thorough investigation. The applicant for licensing or a finding of suitability must pay all the costs of the investigation. Changes in licensed positions must be reported to the Nevada Gaming Authorities and, in addition to their authority to deny an application for a finding of suitability or licensure, the Nevada Gaming Authorities have jurisdiction to disapprove a change in corporate position.

If the Nevada Gaming Authorities were to find an officer, director or key employee unsuitable for licensing or unsuitable to continue to have a relationship with us or our licensed subsidiaries, the companies involved would have to sever all relationships with such person. In addition, the Nevada Commission may require our licensed subsidiaries to terminate the employment of any person who refuses to file the appropriate applications. Determinations of suitability or questions pertaining to licensing are not subject to judicial review in Nevada.

If it were determined that the Nevada Act was violated by a licensed subsidiary, the gaming licenses it holds could be limited, conditioned, suspended or revoked, subject to compliance with certain statutory and regulatory procedures. In addition, the Company, our licensed subsidiaries and the persons involved could be subject to substantial fines for each separate violation of the Nevada Act at the discretion of the Nevada Commission. Further, a supervisor could be appointed by the Nevada Commission to operate our properties, and under certain circumstances, earnings generated during the supervisor’s appointment (except for the reasonable rental value of the premises) could be forfeited to the State of Nevada. Limitation, conditioning or suspension of the gaming licenses of the licensed subsidiaries or the appointment of a supervisor could (and revocation of any such gaming license would) have a material adverse effect on our gaming operations.

Any beneficial owner of our equity securities, regardless of the number of shares owned, may be required to file an application, may be investigated, and may be required to obtain a finding of suitability if the Nevada Commission has reason to believe that such ownership would otherwise be inconsistent with the declared policies of the State of Nevada. If the beneficial owner of our equity securities who must be found suitable is a corporation, partnership, limited partnership, limited liability company or trust, it must submit detailed business and financial information, including a list of its beneficial owners, to the Nevada Board. The applicant must pay all costs of investigation incurred by the Nevada Gaming Authorities in conducting any such investigation.

The Nevada Act provides that persons who acquire beneficial ownership of more than 5% of the voting or non-voting securities of a Registered Corporation must report the acquisition to the Nevada Commission. The Nevada Act also requires that beneficial owners of more than 10% of the voting securities of a Registered Corporation must apply to the Nevada Commission for a finding of suitability within thirty days after the Chair of the Nevada Board mails the written notice requiring such filing. An “institutional investor,” as defined in the Nevada Commission’s regulations, which acquires beneficial ownership of more than 10%, but not more than 25%, of our voting securities may apply to the Nevada Commission for a waiver of such finding of suitability if such institutional investor holds the voting securities for investment purposes only. An institutional investor that has obtained a waiver may, in certain circumstances, hold up to 29% of our voting securities and maintain its waiver for a limited period of time. An institutional investor shall not be deemed to hold voting securities for investment purposes unless the voting securities were acquired and are held in the ordinary course of business as an institutional investor and not for the purpose of causing, directly or indirectly, the election of a majority of the members of our board of directors, any change in our corporate charter, bylaws, management policies or our operations, or any of our gaming affiliates, or any other action which the Nevada Commission finds to be inconsistent with holding our voting securities for investment purposes only. Activities which are not deemed to be inconsistent with holding voting securities for investment purposes only include: (i) voting on all matters voted on by stockholders; (ii) making financial and other inquiries of management of the type normally made by securities analysts for informational purposes and not to cause a change in our management, policies or operations; and (iii) such other activities as the Nevada Commission may determine to be consistent with such investment intent.

Any person who fails or refuses to apply for a finding of suitability or a license within thirty days after being ordered to do so by the Nevada Commission, or the Chair of the Nevada Board, may be found unsuitable. The same restrictions apply to a record owner if the record owner, after request, fails to identify the beneficial owner. Any equityholder who is found unsuitable and who holds, directly or indirectly, any beneficial ownership of the common equity of a Registered Corporation beyond such period of time as may be prescribed by the Nevada Commission may be guilty of a criminal offense. We will be subject to disciplinary action if, after we receive notice that a person is unsuitable to be an equityholder or to have any other

13

relationship with us or our licensed or registered subsidiaries, we (i) pay that person any dividend or interest upon our securities, (ii) allow that person to exercise, directly or indirectly, any voting right conferred through securities held by that person, (iii) pay remuneration in any form to that person for services rendered or otherwise, or (iv) fail to pursue all lawful efforts to require such unsuitable person to relinquish his securities including, if necessary, the immediate purchase of said securities for the price specified by the relevant gaming authority or, if no such price is specified, the fair market value as determined by our board of directors. The purchase may be made in cash, notes that bear interest at the applicable federal rate or a combination of notes and cash. Additionally, the CCLGLB has the authority to approve all persons owning or controlling the stock of any corporation controlling a gaming licensee.

The Nevada Commission may, in its discretion, require the holder of any debt security of a Registered Corporation to file applications, be investigated and be found suitable to own the debt security of a Registered Corporation if the Nevada Commission has reason to believe that such ownership would otherwise be inconsistent with the declared policies of the State of Nevada. If the Nevada Commission determines that a person is unsuitable to own such security, then pursuant to the Nevada Act, the Registered Corporation can be sanctioned, including the loss of its approvals, if without the prior approval of the Nevada Commission, it: (i) pays to the unsuitable person any dividend, interest, or any distribution whatsoever; (ii) recognizes any voting right by such unsuitable person in connection with such securities; (iii) pays the unsuitable person remuneration in any form; or (iv) makes any payment to the unsuitable person by way of principal, redemption, conversion, exchange, liquidation or similar transaction.

We are required to maintain a current membership interest ledger in Nevada, which may be examined by the Nevada Gaming Authorities at any time. If any securities are held in trust by an agent or by a nominee, the record holder may be required to disclose the identity of the beneficial owner to the Nevada Gaming Authorities. Failure to make such disclosure may be grounds for finding the record holder unsuitable. We are also required to render maximum assistance in determining the identity of the beneficial owner.

We may not make a public offering of our securities without the prior approval of the Nevada Commission if the securities or proceeds therefrom are intended to be used to construct, acquire or finance gaming facilities in Nevada, or to retire or extend obligations incurred for such purposes. On September 22, 2022, the Nevada Commission granted us prior approval, subject to certain conditions, to make public offerings for a period of three years (the “Shelf Approval”). The Shelf Approval also applies to any affiliated company wholly owned by us which is a publicly traded corporation or would thereby become a publicly traded corporation pursuant to a public offering. The Shelf Approval may be rescinded for good cause without prior notice upon the issuance of an interlocutory stop order by the Chair of the Nevada Board. If the Shelf Approval is rescinded for any reason, it could adversely impact our capital structure and liquidity and limit our flexibility in planning for, or reacting to, changes in our business and industry. The Shelf Approval does not constitute a finding, recommendation or approval by any of the Nevada Gaming Authorities as to the accuracy or adequacy of any offering memorandum or the investment merits of the securities offered thereby. Any representation to the contrary is unlawful.

Changes in control of the Company through merger, consolidation, stock or asset acquisitions (including stock issuances in connection with restructuring transactions), management or consulting agreements, or any act or conduct by a person whereby such person obtains control, may not occur without the prior approval of the Nevada Commission. Entities seeking to acquire control of a Registered Corporation must satisfy the Nevada Board and the Nevada Commission that they meet a variety of stringent standards prior to assuming control of such Registered Corporation. The Nevada Commission may also require controlling equityholders, officers, directors and other persons having a material relationship or involvement with the entity proposing to acquire control, to be investigated and licensed as part of the approval process relating to the transaction.

The Nevada legislature has declared that some corporate acquisitions opposed by management, repurchases of voting securities and corporate defense tactics affecting Nevada corporate gaming licensees, and Registered Corporations that are affiliated with those operations, may be injurious to stable and productive corporate gaming. The Nevada Commission has established a regulatory scheme to ameliorate the potentially adverse effects of these business practices upon Nevada’s gaming industry and to further Nevada’s policy to: (i) assure the financial stability of corporate gaming licensees and their affiliates; (ii) preserve the beneficial aspects of conducting business in the corporate form; and (iii) promote a neutral environment for the orderly governance of corporate affairs. Approvals are, in certain circumstances, required from the Nevada Commission before a Registered Corporation can make exceptional repurchases of voting securities above the current market price thereof and before a corporate acquisition opposed by management can be consummated. The Nevada Act also requires prior approval of a plan of re-capitalization proposed by the Registered Corporation’s board of directors or similar governing entity in response to a tender offer made directly to the Registered Corporation’s equityholders for the purpose of acquiring control of the Registered Corporation.

14

License fees and taxes, computed in various ways depending on the type of gaming or activity involved, are payable to the State of Nevada and to the counties and cities in which the Nevada licensee’s respective operations are conducted. Depending upon the particular fee or tax involved, these fees and taxes are payable either monthly, quarterly or annually and are based upon either: (i) a percentage of the gross revenues received; (ii) the number of gaming devices operated; or (iii) the number of table games operated. A live entertainment tax is also paid by casino operations where admission charges are imposed for entry into certain entertainment venues. Nevada licensees that hold a license as an operator of a slot route or manufacturer’s or distributor’s license also pay certain fees and taxes to the State of Nevada.

Any person who is licensed, required to be licensed, registered, required to be registered, or is under common control with such persons, and who proposes to become involved in a gaming venture outside of Nevada, is required to deposit with the Nevada Board, and thereafter maintain, a revolving fund in the amount of $10,000 to pay the expenses of investigation by the Nevada Board of their participation in such foreign gaming. The revolving fund is subject to increase or decrease at the discretion of the Nevada Commission. The Eighth Revised Order requires us to deposit with the Nevada Board and maintain a revolving fund of $50,000 for all purposes, including foreign gaming and compliance with the Eighth Revised Order. Thereafter, licensees are required to comply with certain reporting requirements imposed by the Nevada Act. Licensees are also subject to disciplinary action by the Nevada Commission if they knowingly violate any laws of the foreign jurisdiction pertaining to the foreign gaming operation, fail to conduct the foreign gaming operation in accordance with the standards of honesty and integrity required of Nevada gaming operations, engage in activities or enter into associations that are harmful to the State of Nevada or its ability to collect gaming taxes and fees, or employ, contract with or associate with a person in the foreign operation who has been denied a license or finding of suitability in Nevada on the grounds of unsuitability or whom a court in the state of Nevada has found guilty of cheating. The loss or restriction of our gaming licenses in Nevada would have a material adverse effect on our business and could require us to cease gaming operations in Nevada.

Nevada Liquor Regulations

There are various local ordinances and regulations as well as state laws applicable to the sale of alcoholic beverages in Nevada. Palace Station, Wildfire Rancho, Wildfire Valley View, Santa Fe Station and Wildfire Fremont are subject to liquor licensing control and regulation by the Las Vegas City Council. Red Rock and Boulder Station are subject to liquor licensing control and regulation by the CCLGLB. Sunset Station, Green Valley Ranch, Barley’s, Wildfire Sunset, Wildfire Boulder, The Greens, Wildfire Anthem, Wildfire Lanes and Wildfire Lake Mead are subject to liquor licensing control and regulation by the Henderson City Council. All liquor licenses are revocable and are, in some jurisdictions, not transferable. The agencies involved have full power to limit, condition, suspend or revoke any such license, and any such disciplinary action could (and revocation would) have a material adverse effect on the operations of our licensed subsidiaries.

Native American Gaming Regulations

The terms and conditions of management contracts and the operation of casinos and all gaming on land held in trust for Native American tribes in the United States are subject to the Indian Gaming Regulatory Act of 1988 (the “IGRA”), which is administered by the NIGC and the gaming regulatory agencies of state and tribal governments. The IGRA is subject to interpretation by the NIGC and may be subject to judicial and legislative clarification or amendment.

The IGRA established three separate classes of tribal gaming: Class I, Class II and Class III. Class I gaming includes all traditional or social games solely for prizes of minimal value played by a Native American tribe in connection with celebrations or ceremonies. Class II gaming includes games such as bingo, pull-tabs, punchboards, instant bingo (and electronic or computer-aided versions of such games) and non-banked card games (those that are not played against the house), such as poker. Class III gaming is casino-style gaming and includes banked table games such as blackjack, craps and roulette, and gaming machines such as slots, video poker, lotteries and pari-mutuel wagering, a system of betting under which wagers are placed in a pool, management receives a fee from the pool, and the remainder of the pool is split among the winning wagers.

The IGRA requires NIGC approval of management contracts for Class II and Class III gaming, as well as the review of all agreements collateral to the management contracts. The NIGC will not approve a management contract if a director or a 10% shareholder of the management company: (i) is an elected member of the governing body of the Native American tribe which is the party to the management contract; (ii) has been or subsequently is convicted of a felony or gaming offense; (iii) has knowingly and willfully provided materially important false information to the NIGC or the tribe; (iv) has refused to respond to questions from the NIGC; or (v) is a person whose prior history, reputation and associations pose a threat to the public interest or to effective gaming regulation and control, or create or enhance the chance of unsuitable activities in gaming or the business and financial arrangements incidental thereto. In addition, the NIGC will not approve a management contract if the management company or any of its agents have attempted to unduly influence any decision or process of tribal government relating to

15

gaming, or if the management company has materially breached the terms of the management contract or the tribe’s gaming ordinance or resolution, or a trustee, exercising the skill and due diligence that a trustee is commonly held to, would not approve the management contract. A management contract can be approved only after the NIGC determines that the contract provides for, among other things: (i) adequate accounting procedures and verifiable financial reports, which must be furnished to the tribe; (ii) tribal access to the daily operations of the gaming enterprise, including the right to verify daily gross revenues and income; (iii) minimum guaranteed payments to the tribe, which must have priority over the retirement of development and construction costs; (iv) a ceiling on the repayment of such development and construction costs; and (v) a contract term not exceeding five years and a management fee not exceeding 30% of net revenues (as determined by the NIGC); provided that the NIGC may approve up to a seven-year term and a management fee not to exceed 40% of net revenues if the NIGC is satisfied that the capital investment required, and the income projections for the particular gaming activity require the larger fee and longer term. There is no periodic or ongoing review of approved contracts by the NIGC. Other than an action by the parties, the only post-approval action that could result in possible modification or cancellation of a contract would be as the result of an enforcement action taken by the NIGC based on a violation of the law or an issue affecting suitability.

The IGRA prohibits all forms of Class III gaming unless the tribe has entered into a written agreement with the state that specifically authorizes the types of Class III gaming the tribe may offer (a “tribal-state compact”) or the Secretary of the Interior has issued procedures pursuant to which the tribe may conduct Class III gaming. These tribal-state compacts provide, among other things, the manner and extent to which each state will conduct background investigations and certify the suitability of the manager, its officers, directors, and key employees to conduct gaming on Native American lands.

Title 25, Section 81 of the United States Code states that “no agreement or contract with an Indian tribe that encumbers Indian lands for a period of 7 or more years shall be valid unless that agreement or contact bears the approval of the Secretary of the Interior or a designee of the Secretary.” An agreement or contract for services relative to Native American lands which fails to conform with the requirements of Section 81 is void and unenforceable. All money or other things of value paid to any person by any Native American or tribe for or on his or their behalf, on account of such services, in excess of any amount approved by the Secretary or his or her authorized representative will be subject to forfeiture. We intend to comply with Section 81 with respect to any other contract with an Indian tribe in the United States.

Native American tribes are sovereign nations with their own governmental systems, which have primary regulatory authority over gaming on land within the tribes’ jurisdiction. Therefore, persons engaged in gaming activities on tribal lands, including the Company, are subject to the provisions of tribal ordinances and regulations. Tribal gaming ordinances are subject to review by the NIGC under certain standards established by the IGRA. The NIGC may determine that some or all of the ordinances require amendment, and those additional requirements, including additional licensing requirements, may be imposed on us.

Several bills have been introduced in Congress that would amend the IGRA. Any amendment of the IGRA could change the governmental structure and requirements within which tribes could conduct gaming, and may have an adverse effect on our results of operations or impose additional regulatory or operational burdens. In addition, any amendment to or expiration of a tribal-state compact may have an adverse effect on our results of operations or impose additional regulatory or operational burdens.

General Gaming Regulations in Other Jurisdictions

If we become involved in gaming operations in any other jurisdictions, such gaming operations will subject us and certain of our officers, directors, key employees, equityholders and other affiliates (“Regulated Persons”) to strict legal and regulatory requirements, including mandatory licensing and approval requirements, suitability requirements, and ongoing regulatory oversight with respect to such gaming operations. Such legal and regulatory requirements and oversight will be administered and exercised by the relevant regulatory agency or agencies in each jurisdiction (the “Regulatory Authorities”). We and the Regulated Persons will need to satisfy the licensing, approval and suitability requirements of each jurisdiction in which we seek to become involved in gaming operations. These requirements vary from jurisdiction to jurisdiction, but generally concern the responsibility, financial stability and character of the owners and managers of gaming operations as well as persons financially interested or involved in gaming operations. In general, the procedures for gaming licensing, approvals and findings of suitability require the Company and each Regulated Person to submit detailed personal history information and financial information to demonstrate that the proposed gaming operation has adequate financial resources generated from suitable sources and adequate procedures to comply with the operating controls and requirements imposed by law and regulation in each jurisdiction, followed by a thorough investigation by such Regulatory Authorities. In general, the Company and each Regulated Person must pay the costs of such investigation. An application for any gaming license, approval or finding of suitability may be denied for any cause that the Regulatory Authorities deem reasonable. Once obtained, licenses and

16

approvals may be subject to periodic renewal and generally are not transferable. The Regulatory Authorities may at any time revoke, suspend, condition, limit or restrict a license, approval or finding of suitability for any cause that they deem reasonable. Fines for violations may be levied against the holder of a license or approval and in certain jurisdictions, gaming operation revenues can be forfeited to the state under certain circumstances. There can be no assurance that we will obtain all of the necessary licenses, approvals and findings of suitability or that our officers, directors, key employees, other affiliates and certain other stockholders will satisfy the suitability requirements in one or more jurisdictions, or that such licenses, approvals and findings of suitability, if obtained, will not be revoked, limited, suspended or not renewed in the future. We may be required to submit detailed financial and operating reports to Regulatory Authorities.

Failure by us to obtain, or the loss or suspension of, any necessary licenses, approval or findings of suitability would prevent us from conducting gaming operations in such jurisdiction and possibly in other jurisdictions, which may have an adverse effect on our results of operations.

Anti-Money Laundering Laws

Our services are subject to federal anti-money laundering laws, including the Currency and Foreign Transactions Reporting Act of 1970 (the “Bank Secrecy Act”). On an ongoing basis, these laws require us, among other things, to: (i) maintain an anti-money laundering program; (ii) designate and maintain individuals to assure compliance; (iii) train relevant personnel; (iv) identify and report large cash transactions and suspicious activity; (v) screen individuals and entities against sanctions and watch lists and; (vi) independently test for compliance.

Anti-money laundering regulations and regulator expectations thereof are constantly evolving. We implement policies and procedures to reasonably assure compliance with anti-money laundering regulations and continuously monitor our compliance with these regulations. We cannot predict how these future regulations and expectations thereof might affect us. Complying with future regulation could be expensive or require us to change the way we operate our business.

Environmental Matters

Compliance with federal, state and local laws and regulations relating to the protection of the environment to date has not had a material effect upon our capital expenditures, earnings or competitive position and we do not anticipate any material adverse effects in the future based on the nature of our current or future operations.

Social Responsibility and Environmental Stewardship

The Company and Station LLC have a longstanding commitment to social responsibility, and we pride ourselves on our established track record of outstanding corporate citizenship. We believe that our programs and our team members’ participation in our programs and the community causes they support have had a significant positive impact on the communities in which we operate. Our decades-long commitment to acting as a responsible corporate citizen has been reflected in recent years through: Station Casinos’ donation of $1 million to the COVID-19 Emergency Response Fund to purchase personal protective equipment and critical medical supplies, including test kits, for use by first responders and healthcare professionals throughout Nevada; our pandemic-related food donations through Three Square Food Bank; our donations to the Public Education Fund to support distance learning initiatives; our longstanding support of the “Smart Start” school program supporting in-need schools in Clark County; and our support of Three Square Food Bank’s “Backpack for Kids” program supporting children experiencing food insecurity; and by our support and encouragement of our team members as they collectively completed thousands of volunteer hours through these and other initiatives. Throughout the pandemic and continuing to the present, we have maintained partnerships with emergency services, local municipalities and charitable organizations through which we have made available our properties for emergency training and preparedness, as well as for COVID-19 testing sites and food distribution centers. During the pandemic, we made COVID-19 vaccines available for free to our team members, their families, and the public.

At the Company, we consider environmental stewardship to be part of our social responsibility. In the last several years, we have sought and obtained Green Globes certification through the Green Building Initiative for all of our six operating resort properties and our corporate building, all of which have obtained at least three globes and several of which have obtained four. In addition, we are considering the addition of rooftop solar arrays at our six operating resort properties. We have also taken an early and leading role in seeking to add charging stations for electric vehicles at our properties and we have charging stations available at each of our resort properties. Notably, we have designed our Durango project with sustainability goals in mind, including incorporation of Green Globes certification into the construction process. In addition, the Durango project will feature bike access with dedicated bike lanes and will utilize water conservation design features. In addition, we have installed

17

water saving fixtures at each of our resort properties and we have removed natural grass features at all of our resort properties to reduce water consumption, well in advance of any mandate to do so.

Since its inception over 46 years ago, Station LLC has been steadfast in its commitment to promoting responsible gaming practices. As a provider of entertainment that can become problematic for some individuals, we do our best to provide information on the available support, treatment, and assistance programs. We are a charter member of the National Center for Responsible Gaming and we have contributed over $150,000 to the organization. We have been a member of the Nevada Council on Problem Gambling since 1996 and have contributed more than $55,000 to the organization. Our benefits programs include insurance coverage for the treatment of problem gambling for our team members who may recognize a gambling problem due to their proximity to the product. In our properties, in compliance with regulation, we post written materials concerning the nature and symptoms of problem gambling and the toll-free 1-800 problem gambling helpline on or near all gaming and cage areas and ATMs. Finally, our team members actively participate in events annually during Responsible Gaming Education Week. These activities are designed to promote awareness among our team members and guests of the need to gamble responsibly and of the treatment options available for problem gamblers.

Human Capital