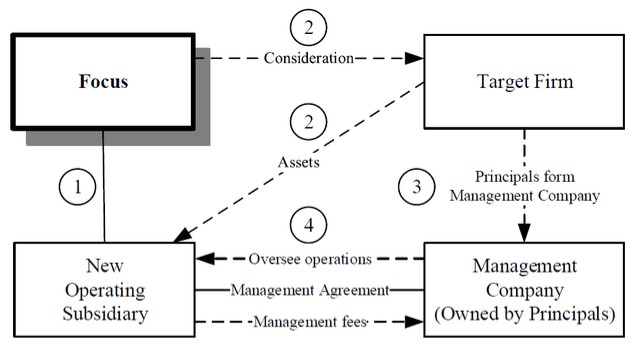

Since 2006, when we began revenue-generating and acquisition activities, we have grown to a partnership with over 85 partner firms. Acquisitions of partner firms to date have been structured as illustrated below, with limited exceptions. Subsidiary mergers at the partner firm level and acquisitions in foreign jurisdictions have been structured differently, and we expect some differences in the future depending on legal and tax considerations.

| (1) | Focus LLC forms a wholly owned subsidiary. |

| (2) | In exchange for cash or a combination of cash and equity and the right to receive contingent consideration, the new operating subsidiary acquires substantially all of the assets or equity of the target firm, which is owned by the selling principals, and becomes the new operating subsidiary of Focus. |

| (3) | The selling principals form a management company. In addition to the selling principals, the management company may include non-selling principals who become newly admitted in connection with the acquisition or thereafter. |

| (4) | The new operating subsidiary, the principals and the management company enter into a management agreement which typically has an initial term of six years subject to automatic renewals for consecutive one-year terms, unless earlier terminated by either the management company or us in certain limited situations. Under the management agreement, the management company is entitled to management fees typically consisting of all future EBPC of the new operating subsidiary in excess of Base Earnings up to Target Earnings, plus a percentage of any EBPC in excess of Target Earnings. Pursuant to the management agreement, the management company provides the personnel who lead the day-to-day operations of the new operating subsidiary. Through the management agreement, we create downside protection for ourselves by retaining a preferred position in each partner firm’s Base Earnings. |

In connection with a typical acquisition, we enter into an acquisition agreement with the target firm and its selling principals pursuant to which we purchase substantially all of the assets or equity of the target firm. The purchase price is a multiple of Base Earnings, which is a percentage of Target Earnings. The purchase price is comprised of a base purchase price and a right to receive contingent consideration in the form of earn out payments. The contingent consideration for acquisitions of new partner firms is generally paid over a six-year period upon the satisfaction of specified growth thresholds in years three and six. These growth thresholds are typically tied to the compound annual growth rate (“CAGR”) of the partner firm’s earnings. Such growth thresholds can be set annually or for different time frames as well, for example, annually over a six-year period. The contingent consideration for acquisitions made by our partner firms is paid upon the satisfaction of specified financial thresholds. These thresholds are typically tied to revenue as adjusted for certain criteria or other operating metrics, based on the retention or growth of the business acquired. These arrangements may result in the payment of additional purchase price consideration to the sellers for periods

8