ff_ex993

TSX:

FF | OTCQX: FFMGF | FRANKFURT: FMG

NOTICE OF MEETING

and

MANAGEMENT INFORMATION CIRCULAR

for the

ANNUAL GENERAL & SPECIAL

MEETING OF SHAREHOLDERS

to be held on

JUNE 30, 2021

Dated

as of May 18, 2021

|

Suite

2070 – 1188 West Georgia Street, Vancouver, British Columbia

V6E 4A2 www.firstmininggold.com

| 1-844-306-8827

|

{5095-001/01637

51254535.10

About First Mining

Headquartered

in Vancouver, British Columbia, First Mining Gold Corp.

(“First Mining”

or, the “Company”) is a Canadian-focused

gold exploration and development company that was created in 2015

by Mr. Keith Neumeyer, founding President and CEO of First Majestic

Silver Corp. and a co-founder of First Quantum Minerals

Ltd.

We are a Canadian gold developer, with our primary focus being the

development and permitting of our Springpole Gold Project (the

“Springpole

Project” or

“Springpole”) in northwestern Ontario.

Springpole is one of the largest undeveloped gold

projects in Canada. We announced the results of a positive

Pre-Feasibility Study for the Springpole Project in January 2021,

and permitting activities are on-going with submission of

an Environmental Impact Statement for Springpole targeted

by the end of 2021. We also hold a large equity position in

Treasury Metals Inc. (“Treasury

Metals”) which is

advancing the Goliath Gold Complex project towards construction.

Our portfolio of gold projects in eastern Canada also includes the

Pickle Crow (being advanced in

partnership with Auteco Minerals Ltd.), Cameron, Hope Brook, Duparquet, Duquesne,

and Pitt gold projects.

We are

publicly listed on the Toronto Stock Exchange (“TSX”) under the trading symbol

“FF”, in the US on the OTCQX under the trading symbol

“FFMGF”, and on the Frankfurt Stock Exchange under the

symbol “FMG”. Our management team has decades of

experience in evaluating, exploring and developing mineral

assets.

Contents

|

|

Page

|

|

Letter to Shareholders

|

ii

|

|

Notice of 2021 Annual General & Special Meeting of

Shareholders

|

iv

|

|

2021 Management Information Circular

|

6

|

|

Questions and Answers

|

6

|

|

Glossary

|

13

|

|

Notice & Access Process

|

22

|

|

About the Meeting

|

22

|

|

Voting

|

25

|

|

Particulars of the Matters to be Acted

Upon

|

34

|

|

Corporate Governance

|

71

|

|

Statement of Executive Compensation

|

78

|

|

Equity Compensation Plan Information

|

96

|

|

Indebtedness of Directors and Executive

Officers

|

97

|

|

Management Contracts

|

97

|

|

Additional Information

|

97

|

|

Board Approval

|

97

|

|

Appendix A – Board Mandate

|

A-1

|

|

Appendix B – Material Terms of Share-Based Compensation

Plan

|

B-1

|

|

Appendix C – Distribution Resolution

|

C-1

|

|

Appendix D – Plan of Arrangement

|

D-1

|

|

Appendix E – Interim Order

|

E-1

|

|

Appendix F – Notice of Hearing of

Petition

|

F-1

|

|

Appendix G – BCBCA Dissent

Provisions

|

G-1

|

Dear

Shareholder:

It is

my pleasure to invite you to our 2021 annual general & special

meeting of shareholders to be held on Wednesday, June 30, 2021 at

10:00 a.m. (Pacific Time) (the “Meeting”). Due to the current

COVID-19 pandemic, we will be holding the Meeting as a completely

virtual

meeting, which will be conducted via live webcast, where all

shareholders regardless of geographic location and equity ownership

will have an equal opportunity to participate at the Meeting and

engage with directors and management of First Mining.

As the

Meeting will be completely virtual, shareholders will not

be able to attend the Meeting in

person. Registered shareholders and duly appointed

proxyholders will be able to attend, participate and vote at the

Meeting online at https://agm.issuerdirect.com/ff.

Non-registered shareholders (being shareholders who hold their

shares through a broker, investment dealer, bank, trust company,

custodian, nominee or other intermediary) who have not duly

appointed themselves as proxyholder will be able to attend and

listen to the Meeting, but will not be

able to vote at the Meeting.

At the

Meeting, shareholders will be asked to, among other things, pass a

special resolution approving a statutory plan of arrangement (the

“Plan of

Arrangement”) whereby First Mining will distribute

23,333,333 common shares (each, a “Treasury Metals Share”) of

Treasury Metals Inc. (“Treasury Metals”) and 35,000,000 common share purchase

warrants (each, a “Treasury

Metals Warrant”) of Treasury Metals to shareholders of

First Mining on a pro rata basis, by way of a reduction in the

capital of the common shares (“Common Shares”) of First Mining

(the “Distribution”). Pursuant to the

Plan of Arrangement, for each Common Share issued and outstanding

on the Distribution Record Date (as defined in the Plan of

Arrangement), the holder of such Common Share shall receive: (i)

that portion of a Treasury Metals Share determined by dividing the

23,333,333 Treasury Metals Shares by the number of Common Shares

issued and outstanding on the Distribution Record Date; and (ii)

that portion of a Treasury Metals Warrant determined by dividing

the 35,000,000 Treasury Metals Warrants (such number of Treasury

Metals Warrants subject to adjustment in connection with a proposed

amendment to the Warrant Indenture dated August 7, 2020 between

Treasury Metals and TSX Trust Company (the “Warrant Indenture”), as described

below) by the number of Common Shares issued and outstanding on the

Distribution Record Date.

First

Mining agreed to complete the Distribution as part of the terms of

the transaction completed on August 7, 2020 whereby Treasury

Metals acquired the Goldlund Gold

Project from First Mining for consideration that included the

Treasury Metals Shares and Treasury Metals Warrants. First Mining

previously announced that 70,000,000 Treasury Metals Shares would

be distributed to shareholders; however, such number has been

adjusted to 23,333,333 Treasury Metals Shares as a result of a

three for one consolidation (the “Consolidation”) of

the Treasury Metals Shares that became effective on August 11,

2020. In addition, as a result of the Consolidation, (i) the number

of Treasury Metals Shares issuable upon exercise of each Treasury

Metals Warrant was adjusted from one Treasury Metals Share to 0.33

of a Treasury Metals Share, and (ii) the exercise price of the

Treasury Metals Warrants was adjusted from $0.50 per Treasury

Metals Share to $1.50 per Treasury Metals Share, all in accordance

with the terms of the Warrant Indenture.

Prior

to the Distribution, the Company intends to work with Treasury Metals and TSX Trust Company to amend the

terms of the Warrant Indenture, such that there will be 11,666,666

Treasury Metals Warrants issued and outstanding, each being

exercisable for one Treasury Metals Share at an exercise price of

$1.50 per Treasury Metals Share. If such amendment takes place, for

each Common Share issued and outstanding on the Distribution Record

Date, the holder of such Common Share shall receive that portion of

a Treasury Metals Warrant determined by dividing the 11,666,666

(rather than 35,000,000) Treasury Metals Warrants by the number of

Common Shares issued and outstanding on the Distribution Record

Date.

After

careful consideration, the board of directors of the Company (the

“Board”) has

unanimously determined that the Distribution is fair to

shareholders and is in the best interests of the Company and its

shareholders. Further information regarding the Distribution is

contained in the enclosed management information circular (the

“Circular”). The

Board has unanimously approved the Distribution and recommends that

shareholders vote in favour of the special resolution approving the

Distribution.

To be

effective, the Distribution must be approved by a special

resolution passed by at least 66⅔% of the votes cast by

shareholders present in person or represented by proxy at the

Meeting, which shareholders are entitled to one vote for each

Common Share held. The Distribution is not subject to the minority

approval requirements of Multilateral Instrument 61-101

Protection of Minority Security

Holders in Special Transactions.

The

Meeting is your opportunity to vote on various items of business

(including the Distribution), meet our Board and management team

virtually via the webcast,

and learn more about our project developments, our performance over

the past year and our future plans. Please take some time to read

the Circular because it includes important information about the

Meeting, voting, the nominated directors, our governance practices

and how we compensate our executives and directors.

Your vote is very important. You can vote online before the proxy

cut-off date and time of Monday, June 28, 2021 at 10:00 a.m.

(Pacific Time) or by phone, fax or mail.

If you have any questions and/or need assistance in voting your

shares, please contact our strategic shareholder advisor and proxy

solicitation agent, Kingsdale Advisors, either by toll-free

telephone in North America at 1-877-659-1822 or collect call

outside North America at 416-867-2272, or by e-mail at contactus@kingsdaleadvisors.com.

Thank

you for your continued support as we move our business

forward.

Yours

sincerely,

/s/

Daniel W. Wilton

Daniel W. Wilton

Chief

Executive Officer and Director

Vancouver,

British Columbia

May 18,

2021

Notice of 2021 Annual

General & Special Meeting of Shareholders

When

Wednesday,

June 30, 2021 at 10:00 a.m. (Pacific Time)

Where

Due to

the current COVID-19 pandemic, we will be holding the Meeting as a

completely virtual

meeting, which will be conducted via live webcast at

https://agm.issuerdirect.com/ff.

Shareholders will

not

be able to attend the Meeting in

person.

We will

cover six items of business at our 2021 annual general &

special meeting (the “Meeting”):

1.

Receive our audited

consolidated financial statements for the financial year ended

December 31, 2020 and the auditor’s report

thereon;

2.

Fix the number of

directors to be elected at the Meeting at five;

3.

Elect five

directors to our board of directors to hold office until the next

annual general meeting of shareholders;

4.

Re-appoint

PricewaterhouseCoopers LLP, Chartered Professional Accountants, as

our independent auditor for the ensuing year and authorize our

directors to set the auditor’s pay;

5.

Consider and, if

deemed appropriate, pass, with or without variation, a special

resolution of the shareholders (the “Distribution Resolution”), the

full text of which is attached as Appendix “C” to the

enclosed management information circular (the “Circular”) approving a statutory

plan of arrangement under section 288 of the Business Corporations Act (British

Columbia) which will effect the distribution (the

“Distribution”)

on a pro rata basis of 23,333,333 common shares of Treasury Metals

Inc. (“Treasury

Metals”) and 35,000,000 common share purchase warrants

of Treasury Metals (such number of common share purchase warrants

subject to adjustment in connection with a proposed amendment to

the Warrant Indenture dated August 7, 2020 between Treasury Metals

and TSX Trust Company, as described in the Circular under the

heading “Particulars of the

Matters to be Acted Upon – 5. Distribution of Treasury Metals

Securities Pursuant to the Plan of Arrangement – Details of

the Distribution”) to shareholders of First Mining, by

way of a reduction in capital of the common shares

(“Common

Shares”) of First Mining; and

6.

Transact such other

business that is properly brought before the Meeting or any

adjournment or adjournments thereof.

Registered

shareholders have a right of dissent in respect of the proposed

Distribution and to be paid the fair value of their Common Shares.

The dissent rights are described in the accompanying Circular and

are attached to the Circular as Appendix “G”. Failure

to strictly comply with the required procedures may result in the

loss of any right of dissent.

Record date

The

record date for the Meeting is May 3, 2021. The record date is the

date for the determination of the registered holders of our Common

Shares entitled to receive notice of, and to vote at, the Meeting

and any adjournment or postponement of the Meeting.

Your vote is important

This

notice is accompanied by the Circular and either a form of proxy

for registered shareholders or a voting instruction form for

beneficial (i.e. non-registered) shareholders. If previously

requested, a copy of our audited consolidated annual financial

statements and management’s discussion and analysis

(“MD&A”) for

the year ended December 31, 2020 will also accompany this notice

(collectively, the “Meeting

Materials”). Copies of our annual and/or interim

financial statements and MD&A are also available◦under◦our◦SEDAR◦profile◦at◦www.sedar.com,◦on◦our◦website◦at

www.firstmininggold.com/investors/reports-filings/financials,

or by request made to First Mining Gold Corp. As described in the

notice and access notification that we have mailed to our

shareholders, we are using the notice and access method for

delivering this notice and the Meeting Materials to our

shareholders, which substantially reduces the paper used in

printing this notice and the Meeting Materials, as well as printing

and mailing costs. This notice and the Meeting Materials will be

available on our website at www.firstmininggold.com/investors/AGM

and under our SEDAR profile at www.sedar.com.

The Circular contains important information about the Meeting, who

can vote and how to vote.

If you

will not be attending the Meeting virtually via the live webcast,

we request that you read, date and sign the accompanying proxy or

voting instruction form, and deliver it according to the

instructions set out therein. Your vote must be received by our

transfer agent, Computershare Investors Services Inc.

(“Computershare”) by 10:00 a.m.

(Pacific Time) on Monday, June 28, 2021 (or before 48 hours,

excluding Saturdays, Sundays and holidays, before any adjournment

of the Meeting at which the proxy is to be used).

Shareholders

who wish to appoint a third-party proxyholder to represent them

virtually at the Meeting must

submit their proxy or voting instruction form (if applicable) prior

to registering their third-party proxyholder with Computershare.

Registering your proxyholder is an additional step once you have

submitted your proxy or voting instruction form. Failure to

register your third-party proxyholder will result in the

proxyholder not receiving a 15-digit Control Number from

Computershare, and therefore not being able to vote during the

virtual Meeting.

To

register a proxyholder, shareholders MUST visit

http://www.computershare.com/FirstMiningGold

by 10:00 a.m. (Pacific Time) on Monday, June 28, 2021 and provide

Computershare with their proxyholder’s contact information,

so that Computershare may provide the proxyholder with a 15-digit

Control Number via e-mail.

Without a Control Number, your third-party proxyholder will not be

able to vote at the Meeting.

If you

would like us to send you a paper copy of the Meeting Materials,

please contact Janet Meiklejohn, our Vice President, Investor

Relations, at 1.844.306.8827 or by e-mail: info@firstmininggold.com.

In order for you to receive the Meeting Materials in advance of the

proxy deposit deadline date and the date of the Meeting, we must

receive requests for printed copies of the Meeting Materials at

least seven business days in advance of the proxy deposit deadline

date and time.

BY ORDER OF THE BOARD OF DIRECTORS,

/s/

Daniel W. Wilton

Daniel W. Wilton

Chief

Executive Officer and Director

Vancouver,

British Columbia

May 18,

2021

|

Throughout this

document, the terms we, us, our,

the Company and First

Mining mean First Mining Gold Corp. and its subsidiaries, in

the context.

|

2021 Management

Information Circular

You

have received this management information circular (the

“Circular”)

because our records indicate you held common shares

(“Common

Shares”) of First Mining as of the close of business

on May 3, 2021 (the “Record

Date”) and we are sending this Circular to you in

connection with the 2021 annual general & special meeting of

our shareholders to be held on Wednesday, June 30, 2021 (the

“Meeting”).

Due to

the current COVID-19 pandemic, we will be holding the Meeting as a

completely virtual

meeting, which will be conducted via live webcast at

https://agm.issuerdirect.com/ff.

Shareholders will

NOT

be able to attend the Meeting in

person.

We encourage you to submit your vote by proxy prior to the Meeting

by the proxy deposit deadline, which is 10:00 a.m. (Pacific Time)

on Monday, June 28, 2021. On behalf of management of the

Company, we will be soliciting votes for this Meeting and any

meeting that is reconvened if it is postponed or adjourned. The

cost of solicitation will be borne by the Company.

This

Circular is dated May 18, 2021. Unless otherwise stated, all

information in this Circular is current as of May 18, 2021, and all

dollar figures are in Canadian dollars.

The

notice and access notification regarding the Meeting is being

mailed to you on May 21, 2021 with a proxy or voting instruction

form, in accordance with applicable laws.

The following briefly addresses some questions that you may have

regarding the Meeting, the proposed distribution of common shares

(the “Treasury Metals

Shares”) of Treasury Metals Inc. (“Treasury Metals”) and common share

purchase warrants of Treasury Metals (the “Treasury Metals Warrants” and,

together with the Treasury Metals Shares, the “Treasury Metals Securities”) to

shareholders, pursuant to a court-approved plan of arrangement and

certain other related matters described in this Circular. These

answers are only a summary and are qualified in their entirety by

the more detailed information that follows. In addition, they may

not address all of the questions that may be important to you as a

shareholder. Accordingly, we urge you to review the more detailed

information contained elsewhere in this Circular.

1.

Who

is entitled to vote at the Meeting?

Shareholders

as of the close of business on May 3, 2021, or their duly appointed

proxies will be entitled to attend the Meeting virtually or

register to vote on all matters to be voted on at the

Meeting.

2.

Who

is soliciting my proxy?

On

behalf of management of the Company, we will be soliciting votes

for this Meeting and any meeting that is reconvened if it is

postponed or adjourned. The cost of solicitation will be borne by

the Company.

The

Company has also engaged Kingsdale Advisors (“Kingsdale”) as strategic

shareholder advisor and proxy solicitation agent and will pay fees

of approximately C$45,000 to Kingsdale for the proxy solicitation

services in addition to certain out-of-pocket expenses.

Shareholders can contact Kingsdale either by toll-free telephone in

North America at 1-877-659-1822or collect call outside North

America at 416-867-2272, or by e-mail at contactus@kingsdaleadvisors.com.

The

Company may utilize the Broadridge QuickVote service to assist

non-objecting beneficial shareholders with voting their Common

Shares. Non-objecting beneficial shareholders may be contacted by

Kingsdale Advisors to conveniently obtain voting instructions

directly over the telephone. Broadridge then tabulates the results

of all instructions received and provides the appropriate

instructions respecting the voting of such Common Shares to be

represented at the Meeting.

3.

If

I am a registered shareholder, how do I vote my

shares?

If you

are a registered shareholder, you may vote on the internet, by

telephone, by fax or by mail. Computershare must receive your proxy

by 10:00 a.m. (Pacific Time) on Monday, June 28, 2021 or at least

48 hours (excluding Saturdays, Sundays and statutory holidays in

the province of British Columbia) prior to the time set for any

adjournment or postponement of the Meeting.

Voting

your proxy using the internet is the most efficient and convenient

way to vote your Common Shares. Go to www.investorvote.com and

follow the instructions on the screen. You will need to input your

15-digit control number, which appears on the first page of your

proxy form.

You may

vote your Common Shares using the telephone by dialling the

following toll-free number from a touch tone telephone:

1.866.732.8683. If you vote using the telephone, you will need your

15-digit control number, which appears on the first page of your

proxy form.

You may

also complete your proxy form, sign and date it, and send it to

Computershare by fax to 1.866.249.7775 (within North America) or

1.416.263.9524 (outside North America) or mail it to: Computershare

Investor Services Inc., Attention: Proxy Department, 100 University

Avenue, 8th Floor, Toronto, ON

M5J 2Y1.

See the

section in this Circular entitled “Voting – How to vote? – Registered

Shareholders”.

4.

How

will my Common Shares be voted if I return my proxy?

The

persons named in the form of proxy will vote your Common Shares in

accordance with your instructions. In the absence of such

instructions, however, your Common Shares will be voted FOR the

Distribution Resolution and the other matters being voted on at the

Meeting.

5.

If

my Common Shares are not registered in my name but are held in the

name of an Intermediary (a bank, trust company, securities broker,

trustee or otherwise), how do I vote my Common Shares?

Generally,

non-registered shareholders who have not waived the right to

receive the Notice of Meeting, this Circular, the audited

consolidated annual financial statements of First Mining for the

year ended December 31, 2020 and the accompanying

management’s discussion and analysis thereon (the

“Meeting Materials”) will either (i) be

given a voting instruction form which is not signed by the

Intermediary and which, when properly completed and signed by the

non-registered shareholder and returned to the Intermediary or its

service company, will constitute your voting instructions (often

called a “voting instruction

form” or a “VIF”) which the Intermediary must

follow, or (ii) be given a proxy form which has already been signed

by the Intermediary (typically by a facsimile, stamped signature),

which is restricted as to the number of Common Shares beneficially

owned by the non-registered shareholder but which is otherwise not

completed by the Intermediary.

If you

are a non-registered shareholder, you should carefully follow the

instructions of your Intermediary in order to submit the voting

instructions for your Common Shares, including those regarding when

and where the completed VIF or proxy form (as applicable) is to be

delivered.

Your

Intermediary may have also provided you with the option of voting

by telephone or through the internet. Your Intermediary must

receive your voting instructions in sufficient time for your

Intermediary to act on them. We strongly encourage all

non-registered shareholders to submit their voting instructions to

their Intermediary online at www.proxyvote.com with

plenty of time before the cut-off. Computershare must receive proxy

vote instructions from your Intermediary by no later than 10:00

a.m. (Pacific Time) on Monday, June 28, 2021, or at least 48 hours

(excluding Saturdays, Sundays and statutory holidays in the

Province of British Columbia) prior to the time set for any

adjournment or postponement of the Meeting.

See the

section in this Circular entitled “Voting – How to vote? –

Non-Registered Shareholders”.

6.

If

I change my mind, can I take back my proxy once I have given

it?

Yes. If

you are a registered shareholder, you can revoke your proxy by

sending a new completed proxy form with a later date, or a written

notice of revocation signed by you, or by your attorney if he or

she has your written authorization. You can also revoke your proxy

in any manner permitted by law.

If you

represent a registered shareholder who is a corporation or

association, your written notice of revocation must have the seal

of the corporation or association, and it must be executed by an

officer or an attorney who has their written authorization. The

written authorization must accompany the written notice of

revocation.

We must

receive the written notice of revocation any time up to and

including the last business day before the day of the Meeting, or

the day the Meeting is reconvened if it was postponed or

adjourned.

If

you’ve sent in your completed proxy form and subsequently

decide to attend the virtual Meeting and vote your Common Shares

online during the Meeting using your 15-digit Control Number, you

will revoke any and all previously submitted proxies. In such a

case, you will be provided the opportunity to vote by ballot on the

matters put forth virtually at the Meeting. If you DO NOT wish to

revoke all previously submitted proxies, please do not vote again

during the virtual Meeting, and instead just join the live webcast

by registering and not clicking on the “Vote My Shares”

button.

If you

are a non-registered shareholder, you can revoke your prior voting

instructions by providing new instructions on a VIF or proxy form

with a later date, or at a later time in the case of voting by

telephone or through the internet, provided that your new

instructions are received by your Intermediary in sufficient time

for your Intermediary to act on them before 10:00 a.m. (Pacific

Time) on Monday, June 28, 2021, or at least 48 hours (excluding

Saturdays, Sundays and statutory holidays in the Province of

British Columbia) prior to the time set for any adjournment or

postponement of the Meeting.

7.

What

am I being asked to vote on at the Meeting?

In

addition to the typical matters to be approved at an annual

meeting, shareholders

will be voting on the approval of the Distribution Resolution which

provides for the distribution of 23,333,333 Treasury Metals Shares

and 35,000,000 Treasury Metals Warrants (such number of Treasury

Metals Warrants subject to adjustment in connection with a proposed

amendment to the Warrant Indenture dated August 7, 2020 between

Treasury Metals and TSX Trust Company (the “Warrant Indenture”), as described

under the heading “Particulars of the Matters to be Acted Upon

– 5. Distribution of Treasury Metals Securities Pursuant to

the Plan of Arrangement – Details of the

Distribution”) to the shareholders, by way of a

reduction in capital of the Common Shares. See the section in this

Circular entitled “Particulars of the Matters to be Acted

Upon”.

8.

Why

is the Distribution being proposed?

First

Mining agreed to complete the Distribution as part of the terms of

the transaction (the “Treasury Metals Transaction”)

completed on August 7, 2020 whereby Treasury Metals acquired the

Goldlund Gold Project from First Mining for consideration that

included the Treasury Metals Shares and Treasury Metals

Warrants.

Our

Board is recommending that shareholders vote FOR the Distribution

Resolution, as it believes the Distribution provides a number of

benefits to shareholders, including, among others:

●

allowing

shareholders to directly benefit from the value-enhancing Treasury

Metals Transaction, by returning value to the shareholders through

a substantial distribution of equity consideration;

and

●

providing

shareholders with the opportunity to participate in the future

success of the Goldlund Gold Project by becoming direct

shareholders of Treasury Metals.

See the

section in this Circular entitled “Particulars of the Matters to be Acted Upon

– 5. Distribution of Treasury Metals Securities pursuant to

the Plan of Arrangement – Reasons for the

Distribution”.

9.

What

approvals are required for the Distribution to become

effective?

For the

Distribution to proceed, the Distribution Resolution must be

approved by at least 66⅔% of the votes cast by shareholders

present in person or represented by proxy at the Meeting, which

shareholders are entitled to one vote for each First Mining Share

held. The Distribution is not subject to the minority approval

requirements of MI 61-101.

In

addition to the necessary shareholder approval, the principal

approval required will be that of the Supreme Court of British

Columbia (the “Court”), which, under the

Business Corporations Act

(British Columbia) (“BCBCA”), must approve the Plan of

Arrangement. It is expected that, assuming the requisite

shareholder approval is received at the Meeting, the hearing of the

Court on the Plan of Arrangement will be held, by teleconference or

by any other manner as the Court may require, on or about July 5,

2021 at 9:45 a.m. (Pacific Time), or as soon thereafter as counsel

may be heard, at 800 Smithe Street, Vancouver, British Columbia, or

at any other date, time and location as the Court may direct. The

Notice of Hearing Petition for the Final Order (the

“Notice of Hearing of

Petition”) in connection with the Final Order is

included as Appendix “F”.

10.

What

are the tax consequences to me if the Distribution is

effected?

For a

more detailed description of the Canadian federal income tax

consequences to shareholders as a result of the Distribution, see

the section in this Circular entitled “Certain Canadian Federal Income Tax

Considerations”. Shareholders should consult their own tax

advisors with respect to their particular

circumstances.

For a

description of the U.S. federal income tax consequences to

shareholders as a result of the Distribution, see the section in

this Circular entitled “Certain United States Federal Income Tax

Considerations”. Shareholders should consult their own tax

advisors with respect to their particular

circumstances.

11.

When

is the Distribution likely to occur?

It is

presently anticipated that, if all required approvals are obtained,

the Distribution Record Date (as defined in the Plan of

Arrangement) will occur on or about July 14, 2021 and the Effective

Date (as defined in the Plan of Arrangement) will occur on or about

July 15, 2021. The Distribution will take place on the Effective

Date.

The

Board will determine the Distribution Record Date and the Effective

Date, and notice of such dates will be made through one or more

news releases issued by First Mining.

12.

If

the Distribution is effected, what will Shareholders

receive?

Shareholders

of record as of the Distribution Record Date will receive, for each

one Common Share held, (i) that portion of a Treasury Metals Share

determined by dividing the 23,333,333 Treasury Metals Shares by the

number of Common Shares issued and outstanding on the Distribution

Record Date; and (ii) that portion of a Treasury Metals Warrant

determined by dividing the 35,000,000 Treasury Metals Warrants

(such number of Treasury Metals Warrants subject to adjustment in

connection with a proposed amendment to the Warrant Indenture, as

described under the heading in this Circular entitled

“Particulars of the Matters

to be Acted Upon – 5. Distribution of Treasury Metals

Securities Pursuant to the Plan of Arrangement – Details of

the Distribution”) by the number of Common Shares

issued and outstanding on the Distribution Record

Date.

First Mining previously announced that 70,000,000 Treasury Metals

Shares would be distributed to shareholders; however, such number

has been adjusted to 23,333,333 Treasury Metals Shares as a result

of a three for one consolidation (the “Consolidation”) of

the Treasury Metals Shares that became effective on August 11,

2020. In addition, as a result of the Consolidation, (i) the number

of Treasury Metals Warrant Shares issuable upon exercise of each

Treasury Metals Warrant was adjusted from one Treasury Metals

Warrant Share to 0.33 of a Treasury Metals Warrant Share, and (ii)

the exercise price of the Treasury Metals Warrants was adjusted

from $0.50 per Treasury Metals Warrant Share to $1.50 per Treasury

Metals Warrant Share, all in accordance with the terms of

the Warrant Indenture.

13.

If

the Distribution is effected, what do Shareholders need to do in

order to receive the Treasury Metals Securities to which they are

entitled?

If you

are a registered shareholder, a Direct Registration System Advice

Statement (“DRS

Advice”) or certificates representing the number of

Treasury Metals Shares and Treasury Metals Warrants (each rounded

down to the nearest whole number) that you are entitled to receive

pursuant to the Plan of Arrangement will be delivered to you

following the Effective Date. If you wish to have your Treasury

Metals Securities deposited into a brokerage account, please

contract your broker for instructions and assistance in this

regard.

Non-registered

shareholders should contact their broker or other intermediary for

instructions and assistance in receiving their Treasury Metals

Securities.

14.

When

must I be a shareholder in order to receive Treasury Metals

Securities?

You

must be a shareholder of record as of the Distribution Record

Date.

Any

shareholder who duly exercises Dissent Rights (as defined herein)

and, following the dissent process under the BCBCA, is ultimately

entitled to be paid the fair value for his, her or its Common

Shares, will instead be entitled to the fair value of such shares

and will not receive Treasury Metals Securities. See the section in

this Circular entitled “Dissent Rights”.

15.

Will

the Treasury Metals Warrants be listed on any stock

exchange?

Pursuant

to the investor rights agreement (the “Investor Rights

Agreement”) dated August 7, 2020 between First

Mining and Treasury Metals, Treasury Metals is required to use

commercially reasonably efforts to list the Treasury Metals

Warrants for trading on the TSX and the OTCQX in the United States.

As of the date of this Circular, neither the TSX nor the OTCQX have

approved the listing of the Treasury Metals Warrants and there is

no assurance that the TSX and/or the OTCQX will approve the listing

of the Treasury Metals Warrants on their respective

exchanges.

16.

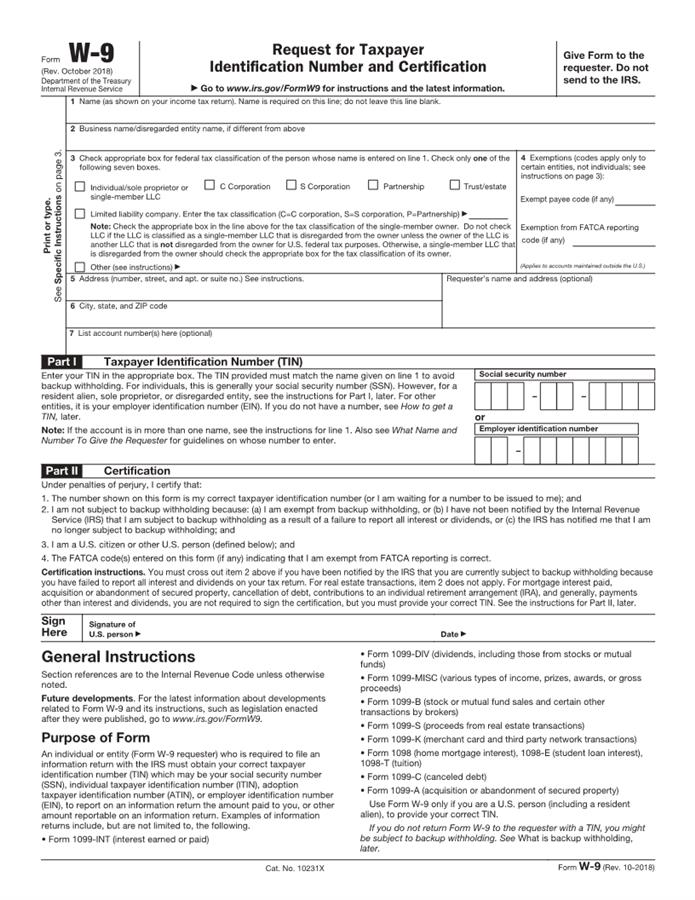

What

should I do with the IRS Form W-9 that was sent to me with the

materials for the Meeting?

If you

are a U.S person (as defined below) or acting on behalf of a U.S.

person, in order to assist the Company in satisfying its

obligations with respect to backup withholding of U.S. Federal

income tax, the Company requests that you please complete an IRS

Form W-9 (enclosed with this Circular) and return it to the Company

by e-mail (info@firstmininggold.com)

or by mailing the completed Form W-9 to:

First

Mining Gold Corp.

Attention: Office

Administrator

Suite

2070 – 1188 West Georgia Street

Vancouver, British

Columbia V6E 4A2

A

“U.S. person”

means: a beneficial owner of Common Shares that, for United States

federal income tax purposes, is (a) a citizen or resident of the

United States, (b) a corporation, or other entity classified as a

corporation for United States federal income tax purposes, that is

created or organized in or under the laws of the United States or

any state in the United States, including the District of Columbia,

(c) an estate if the income of such estate is subject to United

States federal income tax regardless of the source of such income,

(d) a trust if (i) such trust has validly elected to be treated as

a U.S. person for United States federal income tax purposes or (ii)

a United States court is able to exercise primary supervision over

the administration of such trust and one or more U.S. persons have

the authority to control all substantial decisions of such trust,

or (e) a partnership, limited liability company or other entity

classified as a partnership for United States tax purposes that is

created or organized in or under the laws of the United States or

any state in the United States, including the District of

Columbia.

If you

are not a U.S.

person, you can ignore that IRS Form W-9 that was sent to

you.

17.

Who

should I contact if I have questions regarding the Distribution or

voting?

Answers

to many of your questions may be found in the accompanying

Circular. If after reviewing the Circular you have questions about

voting your proxy or about the Distribution, please contact our

strategic shareholder advisor and proxy solicitation agent,

Kingsdale Advisors, either by toll-free telephone in North America

at 1-877-659-1822 or collect call outside North America at

416-867-2272, or by e-mail at contactus@kingsdaleadvisors.com.

18.

How

can I get more information about Treasury Metals?

Additional

information about Treasury Metals can be found on its SEDAR profile

at www.sedar.com.

Glossary

In this

Circular, unless there is something in the subject matter

inconsistent therewith, the following terms will have the

respective meanings set out below, words imparting the singular

number will include the plural and vice versa and words importing

any gender will include all genders.

“1933

Act” means the U.S. Securities Act of 1933, as

amended, and all rules and regulations thereunder.

“ACB”

has the meaning given to it under the heading “Material Income Tax Considerations –

Certain Canadian Federal Income Tax Considerations – Holders

Resident in Canada – Distribution of Treasury Metals Shares

and Treasury Metals Warrants by Reduction of

Capital”.

“allowable

capital loss” has the meaning given to it under the

heading “Material Income Tax

Considerations – Certain Canadian Federal Income Tax

Considerations – Holders Resident in Canada – Taxation

of Capital Gains and Capital Losses”.

“Articles”

means the articles of incorporation of First Mining.

“Audit

Committee” means the Company’s audit

committee.

“BCBCA”

means the Business Corporations

Act (British Columbia), as amended.

“Board”

or “Board of

Directors” means the board of directors of the

Company, as constituted from time to time.

“Business

Day” means a day which is not a Saturday, Sunday or

statutory holiday in Vancouver, British Columbia,

Canada.

“CEO”

means chief executive officer.

“CFO”

means chief financial officer.

“Change

of Control” has the meaning given to it under the

heading “Executive

Compensation – Incentive Plan Awards – Termination and

Change of Control Benefits”.

“Circular”

means this management information circular dated May 18, 2021,

together with all schedules, appendices and exhibits hereto, as

amended, supplemented or otherwise modified from time to

time.

“Code”

means the Company’s Code of Business Conduct and

Ethics.

“Common

Shares” means the common shares in the capital of

First Mining.

“Company”

or “First

Mining” means First Mining Gold Corp., a corporation

existing under the BCBCA.

“Compensation

Committee” means the Company’s compensation

committee.

“Compensation

Committee Chairperson” means the chairperson of the

Compensation Committee.

“Computershare”

means Computershare Trust Company of Canada, at its offices in

Vancouver, British Columbia, in its capacity as registrar and

transfer agent of the Common Shares.

“Consolidation”

means the three for one consolidation of the Treasury Metals Shares

that became effective on August 11, 2020.

“COO”

means chief operating officer.

“Corporate

Governance & Nominating Committee” means the

Company’s corporate governance & nominating

committee.

“Corporate

Governance & Nominating Committee Chairperson”

means the chairperson of the Corporate Governance & Nominating

Committee.

“Court”

means the Supreme Court of British Columbia.

“CPC”

means Capital Pool Company, as defined in Policy 2.4 of the TSX-V

Corporate Finance Manual.

“CRA”

means the Canada Revenue Agency.

“Director

Compensation Plan” has the meaning given to it under

the heading “Statement of

Executive Compensation – Director

compensation”.

“Dissenting

Resident Holder” means a Resident Holder who validly

exercises Dissent Rights.

“Dissenting

Shares” means the Common Shares held by Dissenting

Shareholders in respect of which such Dissenting Shareholders have

given Notice of Dissent.

“Dissenting

Shareholder” mean a registered holder of Common Shares

who duly and validly exercises their Dissent Rights in respect of

the Distribution in strict compliance with the Dissent Procedures

and who has not withdrawn or been deemed to have withdrawn such

exercise of Dissent Rights.

“Dissenting

U.S. Holder” has the meaning given to it under the

heading “Material Income Tax

Considerations – Certain United States Federal Income Tax

Considerations – Dissenting U.S.

Holders”.

“Dissent

Procedures” has the meaning given to it under the

heading “Dissent

Rights”.

“Dissent

Rights” means the right of registered holders of

Common Shares to exercise a right of dissent under the BCBCA in

strict compliance with the Dissent Procedures.

“Distribution”

means the distribution of the Treasury Securities on the terms and

conditions set out in the Plan of Arrangement.

“Distribution

Record Date” means the close of business on the

Business Day immediately preceding the Effective Date for the

purpose of determining the shareholders entitled to receive

Treasury Metals Shares and Treasury Metals Warrants pursuant to the

Plan of Arrangement or such other date as the Board of Directors

may select.

“Distribution

Resolution” means the special resolutions of the

shareholders to approve the Distribution, as required by the

Interim Order and the BCBCA and which shall be in, or substantially

in, the form set out at Appendix “C”.

“Diversity

Policy” has the meaning given to it under the heading

“Corporate Governance

– Director term limits and Board renewal –

Diversity”.

“DRS”

means Direct Registration System.

“DRS

Advice” means Direct Registration System Advice

Statement.

“DSUs”

means deferred share units.

“Effective

Date” shall be the effective date of the Plan of

Arrangement.

“Effective

Time” means 12:01 a.m. (Pacific Time) on the Effective

Date or such other time on the Effective Date as determined by

First Mining.

“Electing

First Mining Shareholder” has the meaning given to it

under the heading “Material

Income Tax Considerations – Certain United States Federal

Income Tax Considerations – Potential Application of the PFIC

Rules to the Distribution”.

“Engquist

Agreement” means the employment agreement dated April

23, 2019 between Kenneth Engquist and First Mining.

“Excess”

has the meaning given to it under the heading “Material Income Tax Considerations –

Certain Canadian Federal Income Tax Considerations – Holders

Resident in Canada – Distribution of Treasury Metals Shares

and Treasury Metals Warrants by Reduction of

Capital”.

“First

Mining Options” means options to purchase the Common

Shares.

“First

Mining Warrants” means share purchase warrants of

First Mining exercisable to acquire the Common Shares.

“Final

Order” means the final order of the Court pursuant to

section 291 of the BCBCA, in a form acceptable to First Mining,

approving the Plan of Arrangement, as such order may be amended by

the Court (with the consent of First Mining) or, if appealed, then

unless such appeal is withdrawn or denied, as affirmed or as

amended on appeal (provided that any such amendment is acceptable

to First Mining).

“Guidelines”

has the meaning given to it under the heading “Corporate

Governance”.

“Holder”

has the meaning given to it under the heading “Material Income Tax Considerations –

Certain Canadian Federal Income Tax

Considerations”.

“IFRS”

means international financial reporting standards as adopted by the

International Accounting Standards Board from time to

time.

“Investor

Rights Agreement” means the investor rights agreement

dated August 7, 2020 between First Mining and Treasury Metals

entered into in connection with the Treasury Metals

Transaction.

“Interim

Order” means the interim order of the Court providing

advice and directions in connection with the Meeting and the Plan

of Arrangement, a copy of which is attached as Appendix

“E”.

“Intermediary”

means an intermediary with which a non-registered shareholder may

deal, including banks, trust companies, securities dealers or

brokers and trustees or administrators of self-directed trusts

governed by registered retirement savings plans, registered

retirement income funds, registered education savings plans (each,

as defined in the Tax

Act) and similar plans, and their nominees.

“IRS”

means the Internal Revenue Service.

“Kingsdale”

means Kingsdale Advisors.

“Lane

Caputo” means Lane Caputo Compensation

Inc.

“Lane

Caputo Report” means the report of Lane Caputo with

respect to executive and Board compensation at the

Company.

“Lines

Agreement” means the employment agreement dated

November 9, 2020 between Stephen Lines and First

Mining.

“MD&A”

means management’s discussion and analysis.

“Mark-to-Market

Election” has the meaning given to it under the

heading “Material Income Tax

Considerations – Certain United States Federal Income Tax

Considerations – Potential Application of the PFIC Rules to

the Distribution”.

“Marshall

Agreement” means the employment agreement dated May

29, 2015 between Andrew Marshall and First Mining.

“Meeting”

means the annual general and special meeting of shareholders to be

held June 30, 2021, and any adjournment(s) or postponement(s)

thereof, held in order to (i) receive the First Mining’s

audited consolidated annual financial statements for the financial

year ended December 31, 2020 and the auditor’s report

thereon, (ii) fix the number of directors to be elected at the

Meeting at five, (iii) elect five directors to the Board to hold

office for the ensuing year, (iv) re-appoint PWC as First

Mining’s independent auditor for the ensuing year and

authorize First Mining’s directors to set the auditor’s

pay, and (v) consider, and if thought fit, approve the Plan of

Arrangement.

“Meeting

Materials” means the Notice of Meeting, this Circular,

the audited consolidated annual financial statements of First

Mining for the year ended December 31, 2020 and the accompanying

MD&A.

“MI

61-101” means Multilateral Instrument 61-101

Protection of Minority

Shareholders in Special Transactions.

“NEOs”

means named executive officers.

“New

Engquist Agreement” means the amended and restated

employment agreement dated January 1, 2021 between Kenneth Engquist

and First Mining.

“New

Marshall Agreement” means the amended and restated

employment agreement dated January 1, 2021 between Andrew Marshall

and First Mining.

“New

Patel Agreement” means the amended and restated

employment agreement dated January 1, 2021 between Samir Patel and

First Mining.

“New

Wilton Agreement” means the amended and restated

employment agreement dated January 1, 2021 between Daniel W. Wilton

and First Mining.

“NI

45-102” means National Instrument 45-102 Resale of Securities of the Canadian

Securities Administrators.

“NI

52-110” means National Instrument 52-110 Audit Committees of the Canadian

Securities Administrators.

“Non-Electing

First Mining Shareholder” has the meaning given to it

under the heading “Material

Income Tax Considerations – Certain United States Federal

Income Tax Considerations – Potential Application of the PFIC

Rules to the Distribution”.

“Non-Electing

U.S. Holder” has the meaning given to it under the

heading “Material Income Tax

Considerations – Certain United States Federal Income Tax

Considerations – U.S. Federal Income Tax Consequences Related

to the Ownership and Disposition of Treasury Metals Securities

– Passive Foreign Investment Company Rules – Default

PFIC Rules Under Section 1291 of the Tax

Code”.

“Non-Resident

Holder” has the meaning given to it under the heading

“Material Income Tax

Considerations – Certain Canadian Federal Income Tax

Considerations – Holders Not Resident in

Canada”.

“non-U.S.

Holder” has the meaning given to it under the heading

“Material Income Tax

Considerations – Certain United States Federal Income Tax

Considerations”.

“Notice

and Access” has the meaning given to it under the

heading “Notice & Access

Process”.

“Notice

of Dissent” has the meaning given to it under the

heading “Dissent

Rights”.

“Notice

of Hearing of Petition” means the Notice of Hearing

Petition for the Final Order, a copy of which is attached as

Appendix “F”.

“Notice

of Meeting” means the notice of annual general and

special meeting in respect of the Meeting.

“Notice

Shares” has the meaning given to it under the heading

“Dissent

Rights”.

“order”

has the meaning given to it under the heading “Particulars of the Matters to be Acted Upon

– 3. Election of Directors for the ensuing year–

Corporate Cease Trade Orders or Bankruptcies, Penalties or

Sanctions”.

“Patel

Agreement” means the employment agreement dated June

2, 2016 between Samir Patel and First Mining.

“Peer

Group” means the group of 19 comparator companies

established in the Lane Caputo Report.

“PFIC”

has the meaning given to it under the heading “Material Income Tax Considerations –

Certain United States Federal Income Tax Considerations –

Receipt of Treasury Metals Securities Pursuant to the

Distribution”.

“PFIC

Asset Test” has the meaning given to it under the

heading “Material Income Tax

Considerations – Certain United States Federal Income Tax

Considerations – U.S. Federal Income Tax Consequences Related

to the Ownership and Disposition of Treasury Metals Securities

– Passive Foreign Investment Company

Rules”.

“PFIC

Income Test” has the meaning given to it under the

heading “Material Income Tax

Considerations – Certain United States Federal Income Tax

Considerations – U.S. Federal Income Tax Consequences Related

to the Ownership and Disposition of Treasury Metals Securities

– Passive Foreign Investment Company

Rules”.

“Plan

of Arrangement” means the plan of arrangement, set

forth in Appendix “D” hereto, and any amendments or

variations thereto made in accordance with the Plan of Arrangement

or upon the direction of the Court in the Final Order.

“Proposed

Amendments” has the meaning given to it under the

heading “Material Income Tax

Considerations – Certain Canadian Federal Income Tax

Considerations”.

“PUC”

has the meaning given to it under the heading “Material Income Tax Considerations –

Certain Canadian Federal Income Tax Considerations – Holders

Resident in Canada – Distribution of Treasury Metals Shares

and Treasury Metals Warrants by Reduction of

Capital”.

“PwC”

means PricewaterhouseCoopers LLP.

“QEF”

has the meaning given to it under the heading “Material Income Tax Considerations –

Certain United States Federal Income Tax Considerations –

Potential Application of the PFIC Rules to the

Distribution”.

“QEF

Election” has the meaning given to it under the

heading “Material Income Tax

Considerations – Certain United States Federal Income Tax

Considerations – Potential Application of the PFIC Rules to

the Distribution”.

“QFC”

means a “qualified foreign corporation”.

“Record

Date” means the record date for notice of and voting

at the Meeting, being fixed as May 3, 2021.

“Registrar”

means the Registrar of Companies appointed pursuant to Section 400

of the BCBCA.

“Regulation

S” means Regulation S promulgated under the 1933

Act.

“Regulations”

has the meaning given to it under the heading “Material Income Tax Considerations –

Certain Canadian Federal Income Tax

Considerations”.

“Resident

Holder” has the meaning given to it under the heading

“Material Income Tax

Considerations – Certain Canadian Federal Income Tax

Considerations – Holders Resident in

Canada”.

“RSUs”

means restricted share units.

“SEDAR”

means the System for Electronic Document Analysis and Retrieval of

the Canadian Securities Administrators, accessible at www.sedar.com.

“Springpole”

or “Springpole

Project” means the Company’s Springpole Gold

Project in northwestern Ontario.

“Subsidiary

PFIC” has the meaning given to it under the heading

“Material Income Tax

Considerations – Certain United States Federal Income Tax

Considerations – U.S. Federal Income Tax Consequences Related

to the Ownership and Disposition of Treasury Metals Securities

– Passive Foreign Investment Company

Rules”.

“Sundance

Acquisition” has the meaning given to it under the

heading “Statement of

Executive Compensation – Compensation discussion and

analysis”.

“taxable

capital gain” has the meaning given to it under the

heading “Material Income Tax

Considerations – Certain Canadian Federal Income Tax

Considerations – Holders Resident in Canada – Taxation

of Capital Gains and Capital Losses”.

“Tax

Act” means the Income

Tax Act (Canada), as amended.

“Tax

Code” means the U.S. Internal Revenue Code of 1986, as

amended.

“third-party

proxyholder” has the meaning given to it under the

heading “Voting –

Voting by Proxy”.

“Treasury

Metals” means Treasury Metals Inc., a company existing

under the laws of Ontario.

“Treasury

Metals Purchase Agreement” means the share purchase

agreement between First Mining and Treasury Metals dated June 3,

2020 pursuant to which the Treasury Metals Transaction was

completed.

“Treasury

Metals Securities” means, together, the Treasury

Metals Shares and Treasury Metals Warrants.

“Treasury

Metals Shares” means 23,333,333 common shares in the

capital of Treasury Metals, which are held by First

Mining.

“Treasury

Metals Transaction” means the transaction completed on

August 7, 2020 whereby Treasury Metals acquired the Goldlund Gold

Project from First Mining for consideration that included the

Treasury Metals Shares and Treasury Metals Warrants.

“Treasury

Metals Warrant Shares” means the common shares in the

capital of Treasury Metals issuable upon exercise of the Treasury

Metals Warrants.

“Treasury

Metals Warrants” means 35,000,000 common share

purchase warrants (such

number of common share purchase warrants subject to adjustment in

connection with a proposed amendment to the Warrant Indenture, as

described under the heading “Particulars of the Matters to be Acted Upon

– 5. Distribution of Treasury Metals Securities Pursuant to

the Plan of Arrangement – Details of the

Distribution”), each exercisable to acquire 0.33 of a

Treasury Metals Warrant Share at an exercise price of $1.50 per

Treasury Metals Warrant Share until August 7, 2023, which are held

by First Mining. The Treasury Metals Warrant Indenture contemplates

that the Treasury Metals Warrants shall be exercisable solely by

means of a “cashless exercise” whereby the holder of

the Treasury Metals Warrants will be entitled to receive a number

of whole Treasury Metals Warrant Shares (rounded down to the

nearest whole number) that will be determined by (a) subtracting

the exercise price from the current market price of Treasury

Metals’ common shares, (b) multiplying such difference by the

number of Treasury Metals Warrant Shares that otherwise would be

issuable upon exercise of the Treasury Metals Warrants if such

exercise were by means of a cash exercise rather than a cashless

exercise, and (c) dividing the resulting product by the current

market price of Treasury Metals’ common shares. For these

purposes the current market price of Treasury Metals’ common

shares will be the volume weighted average price at which the

shares will have traded on the TSX during the five (5) consecutive

trading days ending on the trading day immediately prior to the

date on which the Treasury Metals Warrants are

exercised.

“Treasury

Metals Warrant Indenture” means the Common Share

Purchase Warrant Indenture dated August 7, 2020, between Treasury

Metals and TSX Trust Company, as warrant agent, pursuant to which

the Treasury Metals Warrants have been created and

issued.

“Treasury

Regulations” has the meaning given to it under the

heading “Material Income Tax

Considerations – Certain United States Federal Income Tax

Considerations”.

“Treaty”

means the Canada-US Tax Convention

(1980), as amended.

“TSX”

means the Toronto Stock Exchange.

“TSX-V”

means the TSX Venture Exchange.

“United

States” or “U.S.” means, as the context

requires, the United States of America, its territories and

possessions, any state of the United States, and the District of

Columbia.

“U.S.

Holder” has the meaning given to it under the heading

“Material Income Tax

Considerations – Certain United States Federal Income Tax

Considerations”.

“U.S.

person” means a beneficial owner of Common Shares

that, for United States federal income tax purposes, is (a) a

citizen or resident of the United States, (b) a corporation, or

other entity classified as a corporation for United States federal

income tax purposes, that is created or organized in or under the

laws of the United States or any state in the United States,

including the District of Columbia, (c) an estate if the income of

such estate is subject to United States federal income tax

regardless of the source of such income, (d) a trust if (i) such

trust has validly elected to be treated as a U.S. person for United

States federal income tax purposes or (ii) a United States court is

able to exercise primary supervision over the administration of

such trust and one or more U.S. persons have the authority to

control all substantial decisions of such trust, or (e) a

partnership, limited liability company or other entity classified

as a partnership for United States tax purposes that is created or

organized in or under the laws of the United States or any state in

the United States, including the District of Columbia.

“VIF”

or “voting instruction

form” means a voting instruction form which is not

signed by the Intermediary and which, when properly completed and

signed by a non-registered shareholder and returned to the

Intermediary or its service company, will constitute such

non-registered shareholder’s voting

instructions.

“Wilton

Agreement” means the employment agreement dated

December 20, 2018 between Daniel W. Wilton and First

Mining.

We are

using the notice and access model (“Notice and Access”) provided under

National Instrument 54–101 Communication with Beneficial Owners of

Securities of a Reporting Issuer for the delivery to our

shareholders of the Meeting Materials. We have adopted the Notice

and Access delivery model in order to further our commitment to

environmental sustainability and to reduce our printing and mailing

costs.

Under

Notice and Access, instead of receiving printed copies of the

Meeting Materials, shareholders receive a Notice and Access

notification containing details regarding the date, location and

purpose of the Meeting, as well as information on how they can

access the Meeting Materials electronically. Shareholders with

existing instructions on their account to receive printed materials

will receive a printed copy of the Meeting Materials.

How to request printed Meeting Materials

Shareholders

can request that printed copies of the Meeting Materials be sent to

them by postal delivery at no cost to them up to one year from the

date of the filing of this Circular on SEDAR.

Registered shareholders may make their request by contacting

Janet Meiklejohn, our Vice President, Investor Relations, at

1.844.306.8827 or by e-mail: info@firstmininggold.com.

Non-registered shareholders may make their request online at

www.proxyvote.com

or by telephone at 1.877.907.7643 (North America) or Direct:

1.303.562.9305 (English) or 1.303.562.9306 (French) (outside of North America) by entering the

16-digit control number located on their voting instruction form

and following the instructions provided.

To

receive the Meeting Materials in advance of the proxy deposit

deadline date and the date of the Meeting, First Mining must

receive requests for printed copies of the Meeting Materials at

least seven business days in advance of the proxy deposit deadline

date and time.

|

Our

transfer agent and registrar is Computershare Investor Services

Inc. (“Computershare”).

They

will act as scrutineer of the Meeting and will be responsible for

counting the votes on our behalf.

|

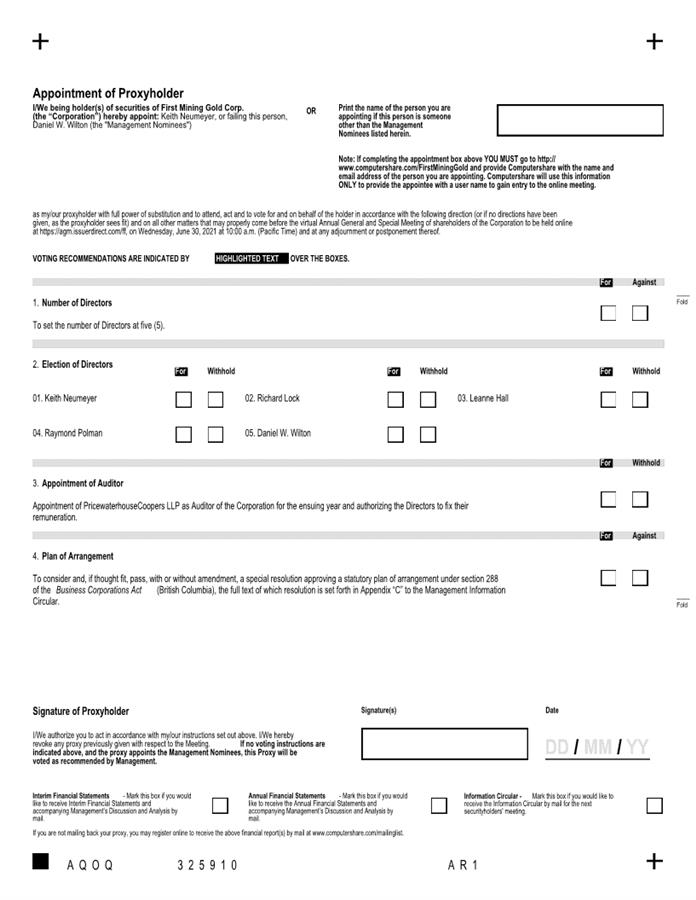

Items of business

1.

Receive our audited consolidated annual financial statements for

the financial year ended December 31, 2020 and the auditor’s

report thereon (see page 31).

Our

audited consolidated annual financial statements for the financial

year ended December 31, 2020, and the auditor’s report

thereon are available on our website at www.firstmininggold.com/investors/reports-filings/financials

and under our SEDAR profile at www.sedar.com.

2.

Fix the number of directors to be elected at the Meeting at five

(see page 31).

Our

board of directors (the “Board”) currently consists of five

directors and we propose to fix the number of directors at five for

the ensuing year.

3.

Elect five directors to our Board to hold office for the ensuing

year (see page 32).

We have

nominated the following individuals as directors for the ensuing

year:

Each of

the above five director nominees is well qualified to serve on our

Board and has expressed his or her willingness to do so. Our

directors are elected for a one-year term, which expires at the end

of our 2022 annual general meeting, unless the person ceases to be

a director before then.

4.

Re-appoint PricewaterhouseCoopers LLP, Chartered Professional

Accountants, as our independent auditor for the ensuing year and

authorize our directors to set the auditor’s pay (see page

37).

We have

recommended that PricewaterhouseCoopers LLP (“PwC”) be re-appointed as our

independent auditor and serve until the end of our 2022 annual

general meeting.

5.

Approve the distribution of the Treasury Metals Securities to

shareholders pursuant to the Plan of Arrangement (see page

37).

The

purpose of the Plan of Arrangement is to distribute the Treasury

Metals Securities to shareholders of First Mining. The Board

recommends that shareholders vote FOR the Distribution Resolution

to be passed at the Meeting.

6.

Transact such other business that is properly brought before the

Meeting (see page 67).

We’ll

also consider other matters that properly come before the Meeting.

As of the date of this Circular, we are not aware of any other

items of business to be considered at the Meeting, other than as

set forth above.

Quorum and approval

We need

a quorum of shareholders to transact business at the Meeting. Under

our articles, a quorum is two or more persons who are, or represent

by proxy, shareholders holding, in the aggregate, at least 5% of

the Common Shares entitled to be voted at the Meeting.

To be

effective, the Plan of Arrangement must be approved by a special

resolution passed by at least 66⅔% of the votes cast by

shareholders present in person or represented by proxy at the

Meeting, which shareholders are entitled to one vote for each

Common Share held.

We

require a simple majority (50% plus 1) of the votes cast at the

Meeting to approve all other items of business, unless otherwise

stated.

Record date

We have

fixed May 3, 2021 as the Record Date for determining the registered

shareholders who will be entitled to notice of the Meeting, and any

adjournment or postponement of the Meeting, and who will be

entitled to vote at the Meeting.

Shares and outstanding principal holders

Our

authorized capital consists of an unlimited number of Common Shares

without par value, each carrying the right to one vote, and an

unlimited number of Preferred Shares issuable in series. There are

no Preferred Shares outstanding. On a vote by show of hands, every

person present at the Meeting who is a shareholder or proxyholder

and entitled to vote on the matter has one vote and, on a poll,

every shareholder entitled to vote on the matter has one vote in

respect of each Common Share entitled to be voted on the matter and

held by that shareholder and may exercise that vote either in

person or by proxy.

We had

a total of 697,717,158 Common Shares outstanding at the close of

business on the Record Date.

To the

knowledge of our directors and executive officers, no persons or

companies beneficially own, or control or direct, directly or

indirectly, Common Shares carrying 10% or more of the voting rights

attached to all outstanding Common Shares as of the Record

Date.

Our

Common Shares are listed on:

●

the TSX under the

symbol “FF”;

●

the US OTCQX market

under the symbol “FFMGF”; and

●

the Frankfurt Stock

Exchange under the symbol “FMG”.

Interest of certain persons in matters to be acted

upon

Other

than as described elsewhere in this Circular, none of the following

individuals has any material interest, direct or indirect, by way

of beneficial ownership of securities or otherwise, in any matter

to be acted upon at the Meeting other than the election of

directors:

●

each person who has

been a director or executive officer of the Company at any time

since January 1, 2020;

●

the nominees for

director; or

●

any associate or

affiliate of any of the above.

Interest of informed persons in material transactions

We are

not aware of any informed person (as defined in National Instrument

51-102 Continuous Disclosure

Obligations) of the Company, or any proposed director, or

any associate or affiliate of the foregoing, who has a direct or

indirect material interest in any transaction we entered into since

January 1, 2020 or any proposed transaction, which has materially

affected or would materially affect the Company or its

subsidiaries.

Who can vote?

You are

entitled to receive notice of and vote at the Meeting if you held

Common Shares as of the close of business on May 3, 2021, the

Record Date for the Meeting.

How to vote?

You can

vote by proxy or you can attend the Meeting virtually and vote your

Common Shares online during the Meeting (if you are a registered

shareholder or a duly appointed and registered third party

proxyholder, or you are a non-registered shareholder and have

appointed yourself as a proxyholder). Voting by proxy is the

easiest way to vote because you’re appointing someone else

(called your proxyholder) to attend the Meeting virtually and vote

your Common Shares for you.

There

are different ways to submit your voting instructions, depending on

whether you are a registered or non-registered shareholder. If you

have any questions and/or need assistance in voting your Common

Shares, please contact our strategic shareholder advisor and proxy

solicitation agent, Kingsdale Advisors, either by toll-free

telephone in North America at 1-877-659-1822 or collect call

outside North America at 416-867-2272, or by e-mail at contactus@kingsdaleadvisors.com.

Registered Shareholders

You are a registered

shareholder if you hold Common

Shares registered in your name and evidenced by either a share

certificate or direct registration statement.

Voting by proxy

Keith Neumeyer, Chairman of the Board, or failing him, Daniel W.

Wilton, Chief Executive Officer, have agreed to act as the First

Mining proxyholders.

You can appoint someone (a “third-party

proxyholder”) other than

First Mining’s proxyholders to represent you virtually at the

Meeting and vote on your behalf. If you want to appoint someone

else, print the name of the person you want as your third-party

proxyholder in the space provided on the enclosed proxy form (this

person need not be a shareholder) and submit your proxy prior to

registering your third-party proxyholder. Registering your third-party proxyholder is an

additional step once you have submitted your proxy. Failure to

register your third-party proxyholder will result in the

third-party proxyholder not receiving a Control Number from

Computershare, and therefore not being able to vote during the

virtual Meeting. Any shareholder who wishes to register a

third-party proxyholder MUST visit

the following website, www.computershare.com/FirstMiningGold,

by Monday, June 28, 2021 at 10:00 a.m. (Pacific Time) and provide

Computershare with their third-party proxyholder’s contact

information, so that Computershare may provide the third-party

proxyholder with a Control Number via e-mail. See the section in

this Circular entitled “Appointment of a third party as

proxy” for further details.

Without a Control Number, your third-party proxyholder will not be

able to vote at the Meeting.

Your proxyholder must vote your Common Shares or withhold your

vote, as applicable, according to your instructions on any ballot

that may be called for and, if you specify a choice on any matter

to be acted upon, your Common Shares will be voted

accordingly. If there are other

items of business that properly come before the Meeting, or

amendments or variations to the items of business, your proxyholder

has the discretion to vote as he or she sees

fit.

If you appoint the First Mining proxyholders but do not tell them

how to vote your Common Shares, your Common Shares will be voted as

follows:

●

FOR fixing the number of directors at

five;

●

FOR electing the five nominated directors listed on

the proxy

form

and in this Circular;

●

FOR re-appointing PwC as the independent auditor,

and

FOR authorizing the Board to set the auditor’s

pay; and

●

FOR the approval of the Distribution

Resolution.

This

is consistent with the voting recommendations by management

and the Board. If there are other items of

business that properlycome before

the Meeting, or amendments or

variations to theitems of business,

the First Mining proxyholders will

voteaccording to

management’s

recommendation.

If you appoint a third-party proxyholder, that person must

attend

the Meeting virtually and cast their vote online during the Meeting

for your