PART I. FINANCIAL INFORMATION

Item 1. Financial Statements and Supplementary Data

ESSA Pharma Inc.

CONDENSED CONSOLIDATED INTERIM FINANCIAL STATEMENTS

(Unaudited)

(Expressed in United States dollars)

FOR THE THREE MONTHS ENDED DECEMBER 31, 2023

8

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM

(Mark One)

For the quarterly period ended

or

For the transition period fromto

Commission file number:

(Exact name of registrant as specified in its charter)

(State or other jurisdiction of | (I.R.S. Employer |

incorporation or organization) | Identification Number) |

(Address of principal executive offices, including zip code) | |

Registrant’s telephone number, including area code: ( | |

Securities registered pursuant to Section 12(b) of the Act: | |

Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer | ☐ | Accelerated filer | ☐ | |

☒ | Smaller reporting company | |||

Emerging growth company |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Securities Exchange Act of 1934). Yes

The number of outstanding Common Shares of the registrant, no par value per share, as of February 12, 2024 was

ESSA PHARMA INC.

QUARTERLY REPORT ON FORM 10-Q

For the Quarter Ended December 31, 2023

Table of Contents

2

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

This Quarterly Report on Form 10-Q includes “forward-looking statements” within the meaning of the U.S. Private Securities Litigation Reform Act of 1995 and “forward-looking information” within the meaning of Canadian securities laws, or collectively, forward-looking statements. Forward-looking statements include statements that may relate to our plans, objectives, goals, strategies, future events, future revenue or performance, capital expenditures, financing needs and other information that is not historical information. Many of these statements appear, in particular, under the headings “Business,” “Risk Factors,” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations”. Forward-looking statements can often be identified by the use of terminology such as “subject to”, “believe,” “anticipate,” “plan,” “expect,” “intend,” “estimate,” “project,” “may,” “might,” “will,” “should,” “would,” “could,” “hope,” “can,” the negatives thereof, variations thereon and similar expressions, or by discussions of strategy. Such forward-looking statements involve known and unknown risks, uncertainties and other factors that may cause the Company’s actual results, performance or achievements to be materially different from any future results, performance or achievements that may be expressed or implied by such forward-looking statements. Examples of such forward looking statements include, but are not limited to statements related to:

| ● | our ability to advance our product candidate and potential future product candidates through, and successfully complete, clinical trials; |

| ● | our ability to recruit sufficient numbers of patients for future clinical trials, and the benefits expected therefrom; |

| ● | our ability to establish and maintain relationships with collaborators with acceptable development, regulatory and commercialization expertise and the benefits to be derived from such collaborative efforts; |

| ● | our ability to obtain funding for operations, including research funding, and the timing and potential sources of such funding; |

| ● | the initiation, timing, cost, location, progress and success of, strategy and plans with respect to our research and development programs (including research programs and related milestones with regards to next-generation drug candidates and compounds), preclinical studies and clinical trials; |

| ● | the therapeutic benefits, properties, effectiveness, pharmacokinetic profile and safety of our product candidate and potential future product candidates, if any, including the expected benefits, properties, effectiveness, pharmacokinetic profile and safety of our next-generation Aniten compounds; |

| ● | our ability to protect our intellectual property and operate our business without infringing upon the intellectual property rights of others; |

| ● | developments relating to our competitors and our industry, including the success of competing therapies that are or may become available; |

| ● | our ability to achieve profitability; |

| ● | the grant (“CPRIT Grant”) under the Cancer Prevention and Research Institute of Texas (“CPRIT”) and payments thereunder, including any residual obligations; |

| ● | sales of our Common Shares, no par value (the “Common Shares”) under the Open Market Sale AgreementSM between the Company and Jefferies LLC, effective November 3, 2023 (the “ATM Sales Agreement”); |

| ● | our intended use of proceeds from past and future offerings of our securities; |

| ● | the implementation of our business model and strategic plans, including strategic plans with respect to patent applications and strategic collaborations and partnerships; |

| ● | our ability to identify, develop and commercialize product candidates; |

| ● | our commercialization, marketing and manufacturing capabilities and strategy; |

| ● | our expectations regarding federal, state, provincial and foreign regulatory requirements, including our plans with respect to anticipated regulatory filings; |

| ● | whether we will receive, and the timing and costs of obtaining, regulatory approvals in the United States, Canada and other jurisdictions; |

| ● | the accuracy of our estimates of the size and characteristics of the markets that may be addressed by our product candidate and potential future product candidates, if any; |

3

| ● | our ability to maintain operations, development programs, preclinical studies, clinical trials and raise capital as a result of global macroeconomic factors including inflation, supply chain issues and any current or future impact related to widespread health concerns, pandemics, or epidemics, and other outbreaks of illness; |

| ● | the rate and degree of market acceptance and clinical utility of our potential future product candidates, if any; |

| ● | the timing of, and our ability and our collaborators’ ability, if any, to obtain and maintain regulatory approvals for our product candidate and potential future product candidates, if any; |

| ● | our expectations regarding market risk, including inflation, interest rate changes and foreign currency fluctuations; |

| ● | our ability to engage and retain the employees required to grow our business; |

| ● | the compensation that is expected to be paid to our employees; |

| ● | our future financial performance and projected expenditures; and |

| ● | estimates of our financial condition, expenses, future revenue, capital requirements and our need for additional financing and potential sources of capital and funding. |

Such statements reflect our current views with respect to future events, are subject to risks and uncertainties and are necessarily based upon a number of estimates and assumptions that are inherently subject to significant medical, scientific, business, economic, competitive, political and social uncertainties and contingencies. Many factors could cause our actual results, performance or achievements to be materially different from any future results, performance, or achievements that may be expressed or implied by such forward-looking statements, including those described under “Risk Factors” in our Annual Report on Form 10-K. All forward-looking statements included in this Quarterly Report on Form 10-Q, are based upon our current expectations and various assumptions. Certain assumptions made in preparing the forward-looking statements include, but are not limited to:

| ● | our ability to conduct clinical studies involving our product candidate and to identify any future product candidates; |

| ● | our ability to obtain regulatory and other approvals to commence clinical trials involving any future product candidates; |

| ● | our ability to obtain positive results from research and development activities, including clinical trials; |

| ● | the availability of sufficient financing on reasonable terms; |

| ● | our ability to obtain required regulatory approvals; |

| ● | our ability to protect patents and proprietary rights; |

| ● | our ability to successfully out-license or sell future products, if any, and in-license and develop new products; |

| ● | the absence of material adverse changes in our industry or the global economy; |

| ● | our ability to attract and retain key personnel; |

| ● | our continued compliance with third-party license terms and non-infringement of third-party intellectual property rights; |

| ● | our ability to maintain good business relationships with our strategic partners; and |

| ● | our ability to understand and predict market competition. |

We believe there is a reasonable basis for our current expectations, views and assumptions, but they are inherently uncertain. We may not realize our expectations and our views and assumptions may not prove correct. Actual results could differ materially from those described or implied by such forward-looking statements. In evaluating forward-looking statements, investors should specifically consider the following uncertainties and factors, among others (including those set forth under the heading “Risk Factors” in our Annual Report on Form 10-K), that could affect future performance and cause actual results to differ materially from those matters expressed in or implied by forward-looking statements

RISK FACTOR SUMMARY

Below is a summary of material factors that make an investment in our Common Shares speculative or risky. Importantly, this summary does not address all of the risks and uncertainties that we face. Additional discussion of the risks and uncertainties summarized in this risk factor summary, as well as other risks and uncertainties that we face, can be found under “Cautionary Note Regarding Forward-Looking Statements” and Part I, Item 1A. “Risk Factors” in our Annual Report on Form 10-K. The below summary is qualified in its entirety by those more complete discussions of such risks and uncertainties. You should consider carefully the risks and uncertainties described under Part I, Item 1A. “Risk Factors”

4

in our Annual Report on Form 10-K as part of your evaluation of an investment in our Common Shares. Important factors that could cause such differences include, among other things, the following:

| ● | risks related to clinical trial development and our ability to conduct the clinical trial of our product candidate and the predictive value of our current or planned clinical trials; |

| ● | risks related to our future success being dependent primarily on identification through preclinical studies, clinical studies, regulatory approval for commercialization of a single product candidate; |

| ● | risks related to our license agreement with third parties; |

| ● | uncertainty related to our ability to obtain required regulatory approvals for our proposed products; |

| ● | risks related to the Company’s ability to conduct a clinical trial or submit a future NDA/NDS or IND/CTA (each, as defined herein); |

| ● | risks related to our ability to successfully commercialize future product candidates; |

| ● | risks related to the possibility that our product candidate and potential future product candidates, if any, may have undesirable side effects when used alone or in combination with other drugs; |

| ● | risks related to our ability to enroll subjects in clinical trials; |

| ● | risks that the FDA may not accept data from trials conducted in locations outside the United States; |

| ● | risks related to our ongoing obligations and continued regulatory review; |

| ● | risks related to potential administrative or judicial sanctions; |

| ● | the risk of increased costs associated with prolonged, delayed or terminated clinical trials; |

| ● | risks related to clinical trials being conducted by third parties under collaboration and clinical supply agreements, including combination studies, using the Company’s product candidate, studies which the Company may not control, and ensuing reputational risk related to clinical trial results; |

| ● | the risk that third parties may not carry out their contractual duties or terminate the relationship; |

| ● | risks related to our lack of experience manufacturing product candidates on a large clinical or commercial scale and our lack of manufacturing facility; |

| ● | risks inherent in foreign operations, including related to foreign sourced raw materials, manufacturing or clinical trials; |

| ● | risks related to disruptions in domestic and foreign supply chains that the Company relies on for the production and shipment of raw materials and clinical trial materials; |

| ● | risks related to our failure to obtain regulatory approval in international jurisdictions; |

| ● | risks related to recently enacted and future legislation in the United States and internationally that may increase the difficulty and cost for us to obtain marketing approval of, and commercialize, our product candidate and potential future products, if any, and affect the prices we may obtain; |

| ● | risks related to new legislation, new regulatory requirements, and the continuing efforts of governmental and third-party payors to contain or reduce the costs of healthcare; |

| ● | uncertainty as to our ability to raise additional funding; |

| ● | risks related to our ability to raise additional capital on favorable terms and the impact of dilution from incremental financing; |

| ● | risks of a deemed default on any residual obligations of the agreement providing for the CPRIT Grant and having to reimburse all of the CPRIT Grant, if such deemed default is not waived by CPRIT; |

| ● | risks related to our incurrence of significant losses in every quarter since inception and our anticipation that it will continue to incur significant losses in the future; |

| ● | risks related to our limited operating history; |

| ● | risks related to our reliance on proprietary technology; |

| ● | risks related to our ability to protect our intellectual property rights throughout the world; |

| ● | risks related to claims by third parties asserting that we, or our employees, contractors or consultants have misappropriated their intellectual property, or claiming ownership of what we regard as our intellectual property; |

| ● | risks related to our ability to comply with governmental patent agency requirements in order to maintain patent protection; |

| ● | risks related to computer system failures or security breaches and increasing cyber threats; |

| ● | risks related to business disruptions that could seriously harm our future revenues and financial condition and increase our costs and expenses; |

5

| ● | risks related to our ability to attract and maintain highly qualified personnel; |

| ● | risks relating to the possibility that third-party coverage and reimbursement and health care cost containment initiatives and treatment guidelines may constrain our future revenues; |

| ● | risks related to potential conflicts of interest between us and our directors and officers; |

| ● | risks related to competition from other biotechnology and pharmaceutical companies; |

| ● | risks related to movements in foreign currency exchange rates, interest rates and rate of inflation; |

| ● | risks related to our ability to convince public payors and hospitals to include our product candidate and potential future products, if any, on their approved formulary lists; |

| ● | risks related to our ability to establish an effective sales force and marketing infrastructure, or enter into acceptable third-party sales and marketing or licensing arrangements; |

| ● | risks related to our ability to manage growth; |

| ● | risks related to our ability to achieve or maintain expected levels of market acceptance for our products; |

| ● | risks related to our ability to realize benefits from acquired businesses or products or form strategic alliances in the future; |

| ● | risks related to collaborations with third parties; |

| ● | risks that employees may engage in misconduct or other improper activities, including noncompliance with regulatory standards and requirements, which could cause significant liability for us and harm our reputation; |

| ● | risks related to product liability lawsuits; |

| ● | risks related to compulsory licensing and/or generic competition; |

| ● | risks related to the costs of and management time devoted to operating as a public company; |

| ● | risks related to being a smaller reporting company; |

| ● | risks related to the possibility that laws and regulations governing international operations may preclude us from developing, manufacturing and selling certain product candidates outside of the United States and Canada and require us to develop and implement costly compliance programs; |

| ● | risks related to laws that govern fraud and abuse and patients’ rights; |

| ● | risks related to our ability to comply with environmental, health and safety laws and regulations; |

| ● | risks related to us being a “passive foreign investment company”; |

| ● | risks related to United States investors’ ability to effect service of process or enforcement of actions against us; |

| ● | risks related to market price and trading volume volatility; |

| ● | risks related to our dividend policy; |

| ● | risks associated with future sales of our securities; |

| ● | risks related to our ability to maintain an active trading market for the Company's Common Shares; |

| ● | risks related to widespread health concerns, pandemics, or epidemics and other outbreaks of illness; |

| ● | risks related to our ability to implement and maintain effective internal controls; |

| ● | risks related to provisions in our charter documents and Canadian law affecting corporate governance; and |

| ● | risks related to analyst coverage. |

If one or more of these risks or uncertainties or a risk that is not currently known to us, materialize, or if our underlying assumptions prove to be incorrect, actual results may vary materially from those expressed or implied by forward-looking statements. The forward-looking statements represent our expectations, plans, estimates and views as of the date of this document. We do not undertake and specifically decline any obligation to update, republish or revise forward-looking statements to reflect future events or circumstances or to reflect the occurrences of unanticipated events, except as required by law. Investors are cautioned that we cannot guarantee future results, events, levels of activity, performance or achievements and that forward-looking statements are inherently uncertain. Accordingly, investors are cautioned not to put undue reliance on forward-looking statements. We advise you that these cautionary remarks expressly qualify in their entirely all forward-looking statements attributable to us or persons acting on our behalf.

6

We express all amounts in this Quarterly Report on Form 10-Q in U.S. dollars, except where otherwise indicated. References to “$” and “US$” are to U.S. dollars and references to “C$” are to Canadian dollars. Except as otherwise indicated, references in this Quarterly Report on Form 10-Q to “ESSA,” “the Company,” “we,” “us” and “our” refer to ESSA Pharma Inc. and its subsidiary.

7

PART I. FINANCIAL INFORMATION

Item 1. Financial Statements and Supplementary Data

ESSA Pharma Inc.

CONDENSED CONSOLIDATED INTERIM FINANCIAL STATEMENTS

(Unaudited)

(Expressed in United States dollars)

FOR THE THREE MONTHS ENDED DECEMBER 31, 2023

8

ESSA PHARMA INC.

CONDENSED CONSOLIDATED INTERIM BALANCE SHEETS

(Unaudited)

(Expressed in United States dollars)

AS OF

December 31, | September 30, | |||||

| 2023 |

| 2023 | |||

ASSETS |

|

|

|

| ||

Current |

|

|

|

| ||

Cash and cash equivalents | $ | |

| $ | | |

Short-term investments (Note 4) | | | ||||

Receivables |

| |

| | ||

Prepaids (Note 5) |

| |

| | ||

| |

| | |||

Deposits | |

| | |||

Operating lease right-of-use assets (Note 7) |

| |

| | ||

Total assets | $ | |

| $ | | |

LIABILITIES AND SHAREHOLDERS’ EQUITY |

|

|

|

| ||

Current |

|

|

|

| ||

Accounts payable and accrued liabilities (Note 6) | $ | |

| $ | | |

Current portion of operating lease liabilities (Note 7) |

| |

| | ||

| |

| | |||

Operating lease liabilities (Note 7) |

| |

| | ||

Total liabilities |

| |

| | ||

Shareholders’ equity |

|

|

|

| ||

Authorized |

|

|

|

| ||

Unlimited common shares, without par value |

|

|

|

| ||

Unlimited preferred shares, without par value | ||||||

Common shares |

| |

| | ||

Additional paid-in capital (Note 8) |

| |

| | ||

Accumulated other comprehensive loss |

| ( |

| ( | ||

Accumulated deficit |

| ( |

| ( | ||

| |

| | |||

Total liabilities and shareholders’ equity | $ | |

| $ | | |

Nature of operations (Note 1)

The accompanying notes are an integral part of these condensed consolidated interim financial statements.

9

ESSA PHARMA INC.

CONDENSED CONSOLIDATED INTERIM STATEMENTS OF OPERATIONS AND COMPREHENSIVE LOSS

(Unaudited)

(Expressed in United States dollars)

FOR THE THREE MONTHS ENDED DECEMBER 31,

For the three months ended | ||||||

December 31, | ||||||

| 2023 |

| 2022 | |||

OPERATING EXPENSES |

|

|

|

| ||

Research and development | $ | |

| $ | | |

Financing costs |

| — |

| | ||

General and administration |

| |

| | ||

Total operating expenses |

| ( |

| ( | ||

Foreign exchange |

| ( |

| | ||

Investment and other income |

| |

| | ||

Net loss for the period | ( | ( | ||||

OTHER COMPREHENSIVE INCOME | ||||||

Unrealized gain on short-term investments (Note 4) |

| |

| | ||

Loss and comprehensive loss for the period | $ | ( |

| $ | ( | |

Basic and diluted loss per common share | $ | ( |

| $ | ( | |

Weighted average number of common shares outstanding |

| |

| | ||

The accompanying notes are an integral part of these condensed consolidated interim financial statements.

10

ESSA PHARMA INC.

CONDENSED CONSOLIDATED INTERIM STATEMENTS OF CASH FLOWS

(Unaudited)

(Expressed in United States dollars)

FOR THE THREE MONTHS ENDED DECEMBER 31,

| 2023 |

| 2022 | |||

CASH FLOWS FROM OPERATING ACTIVITIES |

|

|

|

| ||

Net loss for the period | $ | ( |

| $ | ( | |

Items not affecting cash and cash equivalents: |

|

|

|

| ||

Amortization of right-of-use asset |

| |

| | ||

Accretion of premiums/discounts on short-term investments, net | ( |

| ( | |||

Accretion of lease liability |

| |

| | ||

Accrued Investment income | ( | ( | ||||

Unrealized foreign exchange |

| ( |

| ( | ||

Unrealized loss on short-term investments | ||||||

Share-based payments |

| |

| | ||

Changes in non-cash working capital items: |

|

|

|

| ||

Receivables |

| ( |

| ( | ||

Prepaids |

| ( |

| | ||

Accounts payable and accrued liabilities |

| |

| | ||

Operating lease liabilities | ( | | ||||

Net cash used in operating activities |

| ( |

| ( | ||

CASH FLOWS FROM INVESTING ACTIVITIES |

|

|

|

| ||

Purchase of short-term investments | ( | ( | ||||

Proceeds from short-term investments sold | | | ||||

Net cash provided by (used in) investing activities |

| |

| ( | ||

CASH FLOWS FROM FINANCING ACTIVITIES |

|

|

|

| ||

Options exercised | | | ||||

Shares purchased through employee share purchase plan | | | ||||

Lease payments |

| |

| ( | ||

Net cash provided by financing activities |

| |

| | ||

Effect of foreign exchange on cash and cash equivalents |

| |

| ( | ||

Change in cash and cash equivalents for the period |

| |

| ( | ||

Cash and cash equivalents, beginning of period |

| |

| | ||

Cash and cash equivalents, end of period | $ | |

| $ | | |

Supplemental disclosure of non-cash investing and finance items: | ||||||

Leased assets obtained in exchange for operating lease liabilities | $ | | $ | | ||

The accompanying notes are an integral part of these condensed consolidated interim financial statements.

11

ESSA PHARMA INC.

CONDENSED CONSOLIDATED INTERIM STATEMENT OF CHANGES IN SHAREHOLDERS’ EQUITY

(Unaudited)

(Expressed in United States dollars)

FOR THE THREE MONTHS ENDED DECEMBER 31, 2023 AND 2022

Accumulated | |||||||||||||||||

Additional | other | ||||||||||||||||

Number | Common | paid-in | comprehensive |

| |||||||||||||

| of shares |

| shares |

| capital |

| loss |

| Deficit |

| Total | ||||||

Balance, September 30, 2022 |

| | $ | | $ | | $ | ( | $ | ( |

| $ | | ||||

Shares issued through employee share purchase plan | | | ( | — | — |

| | ||||||||||

Share-based payments |

| — | — | | — | — |

| | |||||||||

Loss and comprehensive loss for the period |

| — | — | — | | ( |

| ( | |||||||||

Balance, December 31, 2022 |

| | $ | | $ | | $ | ( | $ | ( |

| $ | | ||||

Accumulated | |||||||||||||||||

Additional | other | ||||||||||||||||

Number | Common | paid-in | comprehensive |

| |||||||||||||

of shares |

| shares |

| capital |

| loss |

| Deficit |

| Total | |||||||

Balance, September 30, 2023 |

| | $ | | $ | | $ | ( | $ | ( |

| $ | | ||||

Options exercised | | | ( | — | — |

| | ||||||||||

Shares issued through employee share purchase plan | | | ( | — | — |

| | ||||||||||

Share-based payments |

| — | — | | — | — |

| | |||||||||

Loss and comprehensive loss for the period |

| — | — | — | | ( |

| ( | |||||||||

Balance, December 31, 2023 |

| | $ | | $ | | $ | ( | $ | ( |

| $ | | ||||

The accompanying notes are an integral part of these condensed consolidated interim financial statements.

12

ESSA PHARMA INC.

NOTES TO THE CONDENSED CONSOLIDATED INTERIM FINANCIAL STATEMENTS

(Unaudited)

(Expressed in United States dollars)

FOR THE THREE MONTHS ENDED DECEMBER 31, 2023

1. NATURE OF OPERATIONS

Nature of Operations

The Company was incorporated under the laws of the Province of British Columbia on January 6, 2009. The Company’s head office address is Suite 720 – 999 West Broadway, Vancouver, BC, V5Z 1K5. The registered and records office address is the Suite 3500, The Stack, 1133 Melville Street, Vancouver, BC, V6E 4E5. The Company is listed on the Nasdaq Capital Market (“Nasdaq”) under the symbol “EPIX”.

The Company is focused on the development of small molecule drugs for the treatment of prostate cancer. The Company has acquired a license to certain patents (“NTD”) which were the joint property of the British Columbia Cancer Agency and the University of British Columbia. As of December 31, 2023, no products are in commercial production or use.

2. BASIS OF PRESENTATION

Basis of Presentation

These accompanying unaudited condensed consolidated interim financial statements, including comparatives, have been prepared in accordance with United States’ Generally Accepted Accounting Principles (“U.S. GAAP”) and pursuant to the rules and regulations of the United States Securities and Exchange Commission (“SEC”) for interim financial information. Accordingly, these condensed consolidated interim financial statements do not include all of the information and footnotes required for complete consolidated financial statements and should be read in conjunction with the audited consolidated financial statements and notes for the year ended September 30, 2023 and included in the Company’s 2023 Annual Report on Form 10-K filed with the SEC and with the securities commissions in British Columbia, Alberta and Ontario on December 12, 2023.

These unaudited condensed consolidated interim financial statements reflect all adjustments, consisting of normal recurring adjustments, which, in the opinion of management, are necessary for a fair presentation of results for the interim periods presented. The results of operations for the three months ended December 31, 2023 and 2022 are not necessarily indicative of results that can be expected for a full year. These unaudited condensed consolidated interim financial statements follow the same significant accounting policies as those described in the notes to the audited consolidated financial statements of the Company included in the Company’s 2023 Annual Report on Form 10-K for the year ended September 30, 2023, with the exception of any policies described in Note 3. Certain prior period amounts in the unaudited condensed consolidated interim statements of cash flows have been reclassified to conform to the current period presentation.

These accompanying unaudited condensed consolidated interim financial statements include the accounts of the Company and its wholly owned subsidiaries. Inter-company transactions, balances and unrealized gains or losses on transactions are eliminated upon consolidation.

The accompanying condensed consolidated interim financial statements have been prepared on a historical cost basis except for certain financial assets measured at fair value.

All amounts expressed in these accompanying condensed consolidated interim financial statements and the accompanying notes are expressed in United States dollars, except per share data and where otherwise indicated. References to “$” are to United States dollars and references to “C$” are to Canadian dollars.

13

Use of Estimates

The preparation of the accompanying condensed consolidated interim financial statements in conformity with U.S. GAAP requires management to make estimates and assumptions about future events that affect the reported amounts of assets, liabilities, expenses, contingent assets and contingent liabilities as of the end of, or during, the reporting period. Actual results could significantly differ from those estimates. Significant areas requiring management to make estimates include the valuation of equity instruments issued for services. Further details of the nature of these assumptions and conditions may be found in the relevant notes to these condensed consolidated interim financial statements.

The effect of a change in an accounting estimate is recognized prospectively by including it in comprehensive income in the period of the change, if the change affects that period only, or in the period of the change and future periods, if the change affects both. Estimates and assumptions are reviewed quarterly.

3. RECENT ACCOUNTING PRONOUNCEMENTS

Recent accounting pronouncements not yet adopted

Management does not believe that any recently issued, but not yet effective, accounting standards, if currently adopted, would have a material effect on the Company’s condensed consolidated interim financial statements.

Recent accounting pronouncements issued by the FASB, including its Emerging Issues Task Force, the American Institute of Certified Public Accountants, and the Securities and Exchange Commission did not or are not believed by management to have a material impact on the Company’s present or future consolidated financial statement presentation or disclosures.

14

4. SHORT-TERM INVESTMENTS

Short-term investments consist of guaranteed investment certificates (“GICs”) held at financial institutions purchased in accordance with the Company’s treasury policy. These GICs and term deposits bear interest at

Short-term investments also consist of U.S. treasury securities, corporate debt securities and commercial paper. The Company has classified these investments as available-for-sale, as the sale of such investments may be required prior to maturity to implement management strategies, and therefore has classified all investment securities as current assets. Those investments with maturity dates of three months or less at the date of purchase are presented as cash equivalents in the accompanying balance sheets. Short-term investments are carried at fair value with the unrealized gains and losses included in accumulated other comprehensive loss as a component of shareholders’ equity (deficit) until realized. Any premium or discount arising at purchase is amortized or accreted to investment income as an adjustment to yield using the straight-line method over the life of the instrument. The Company records an allowance for credit losses when unrealized losses are due to credit-related factors. Realized gains and losses are calculated using the specific identification method and recorded as investment income.

As of December 31, 2023 | |||||||||||||||

Amortized | Unrealized | Estimated | |||||||||||||

| Cost |

| Gains |

| Losses |

| Investment Income |

| Fair Value | ||||||

U.S. Treasury securities | $ | |

| $ | — |

| $ | ( |

| $ | |

| $ | | |

GICs and Term deposits | | — | — | | | ||||||||||

Corporate debt securities | — | — | — | — | — | ||||||||||

Balance, end of period | $ | |

| $ | — |

| $ | ( |

| $ | |

| $ | | |

As of December 31, 2023, short-term investments have an aggregate fair market value of $

5. PREPAIDS

December 31, | September 30, | |||||

| 2023 |

| 2023 | |||

Prepaid insurance | $ | |

| $ | | |

Prepaid CMC and clinical expenses and deposits |

| |

| | ||

Other deposits and prepaid expenses |

| |

| | ||

Balance, end of period | $ | |

| $ | | |

15

6. ACCOUNTS PAYABLE AND ACCRUED LIABILITIES

December 31, | September 30, | |||||

| 2023 |

| 2023 | |||

Accounts payable | $ | |

| $ | | |

Accrued expenses |

| |

| | ||

Accrued vacation |

| |

| | ||

Balance, end of period | $ | |

| $ | | |

7. OPERATING LEASE

Operating lease right-of-use assets |

|

| |

Balance, September 30, 2023 | $ | | |

Addition |

| | |

Amortization | ( | ||

Balance, December 31, 2023 | $ | | |

Operating lease liabilities |

|

| |

Balance, September 30, 2023 | $ | | |

Addition | | ||

Cost of operating lease | ( | ||

Balance, December 31, 2023 | $ | | |

Operating lease liabilities with expected life of less than one year |

| $ | |

Operating lease liabilities with expected life greater than one year |

| $ | |

The Company recognizes a right-of-use asset for the right to use the underlying asset for the lease term, and a lease liability, which represents the present value of the Company’s obligation to make payments over the lease term. The present value of the lease payments is calculated using an incremental borrowing rate as the Company’s leases do not provide an implicit interest rate. At December 31, 2023, the Company’s incremental borrowing rate was

As at December 31, 2023, the maturity of the Company’s operating lease liability was as follows:

| Operating lease | ||

Within 1 year | $ | | |

1 to 2 years |

| | |

2 to 3 years | | ||

3 to 4 years | | ||

| |||

Less: | |||

Imputed interest | ( | ||

Operating lease liability | $ | | |

16

8. SHAREHOLDERS’ EQUITY

Authorized

Unlimited common shares, without par value.

Unlimited preferred shares, without par value.

Omnibus Incentive Plan

On February 25, 2021, the Company adopted an omnibus incentive plan (“Omnibus Plan”) consistent with the policies and rules of Nasdaq. Pursuant to the Omnibus Plan, the Company may issue stock options, share appreciation rights, restricted shares, restricted share units and other share-based awards. As of September 30, 2023, the Company has not issued any instruments other than stock options under the Omnibus Plan.

Prior to the adoption of the Omnibus Plan, the Company issued equity compensation pursuant to the Company’s amended and restated stock option plan (the “Legacy Option Plan”), Amended and Restated Restricted Share Unit Plan (the “RSU Plan”) and Employee Stock Purchase Plan. Since the adoption of the Omnibus Plan, no further grants have been made under the Legacy Option Plan or RSU Plan, though existing grants under the Legacy Option Plan will continue in effect in accordance with their terms.

As of December 31, 2023, the Omnibus Plan has a maximum of

Employee Share Purchase Plan

The Company has adopted an Employee Share Purchase Plan (“ESPP”) under which qualifying employees may be granted purchase rights (“Purchase Rights”) to the Company’s common shares at not less of

Eligible employees are able to contribute up to

During the three months ended December 31, 2023, the Company issued

For the three months ended | ||||||

December 31, | ||||||

| 2023 |

| 2022 | |||

Research and development expense | $ | |

| $ | | |

General and administrative |

| |

| | ||

$ | | $ | | |||

17

The Company measures the purchase rights based on their estimated grant date fair value using the Black-Scholes option pricing model and the estimated number of shares that can be purchased. The following weighted average assumptions were used for the valuation of purchase rights:

For the three months ended | |||||

December 31, | |||||

2023 |

| 2022 |

| ||

Risk-free interest rate |

| | % | | % |

Expected life of share purchase rights |

|

|

| ||

Expected annualized volatility |

| | % | | % |

Dividend |

| |

| |

|

Stock options

Pursuant to the Legacy Option Plan and Omnibus Plan, options were previously or may be granted, respectively, with expiry terms of up to

Stock option transactions are summarized as follows:

|

| Weighted | |||

Number | Average | ||||

of Options | Exercise Price* | ||||

| |||||

Balance, September 30, 2023 |

| | $ | | |

Options granted |

| |

| | |

Options exercised |

| ( |

| ( | |

Options expired/forfeited |

| ( |

| ( | |

Balance outstanding, December 31, 2023 |

| | $ | | |

Balance exercisable, December 31, 2023 |

| | $ | | |

| * | Options exercisable in Canadian dollars as of December 31, 2023 are translated at current rates to reflect the current weighted average exercise price in U.S. dollars for all outstanding options. |

18

At December 31, 2023, options were outstanding enabling holders to acquire common shares as follows:

| Weighted average remaining | |||||

Exercise price | Number of options | contractual life (years) | ||||

$ | | |||||

$ | | |||||

$ | | |||||

$ | |

| ||||

$ | |

| ||||

$ | |

| * | |||

$ | |

| ||||

$ | |

| ||||

$ | |

| ||||

$ | |

| ||||

$ | |

| ||||

$ | |

| ||||

$ | |

| ||||

$ | |

| ||||

$ | |

| ||||

$ | |

| ||||

$ | |

| ||||

$ | |

| ||||

$ | |

| ||||

$ | |

| ||||

C$ | |

| ||||

C$ | |

| ||||

|

|

*

Share-based compensation

During the three months ended December 31, 2023, the Company granted a total of

The Company recognized share-based payments expense for options granted and vesting, net of recoveries on cancellations of unvested options, during the period ended December 31, 2023 and 2022 with allocations to its functional expense as follows:

For the three months ended | ||||||

December 31, | ||||||

2023 |

| 2022 | ||||

Research and development expense | $ | |

| $ | | |

General and administrative |

| |

| | ||

$ | |

| $ | | ||

19

The following weighted average assumptions were used for the Black-Scholes option-pricing model valuation of stock options granted:

2023 |

| 2022 | |||

Risk-free interest rate |

| | % | | % |

Expected life of options |

| years | years | ||

Expected annualized volatility |

| | % | | % |

Dividend |

| |

| |

Warrants

Warrant transactions are summarized as follows:

|

| Weighted | |||

Number | Average | ||||

of Warrants | Exercise Price | ||||

| |||||

Balance, September 30, 2023 |

| | $ | | |

Warrants expired |

| ( |

| ( | |

Balance outstanding and exercisable, December 31, 2023 |

| | $ | | |

At December 31, 2023, warrants were outstanding enabling holders to acquire common shares as follows:

Number |

|

| ||||

of Warrants | Exercise Price | Expiry Date | ||||

$ | |

| ||||

|

|

|

| |||

9. RELATED PARTY TRANSACTIONS

Included in accounts payable and accrued liabilities at December 31, 2023 is $

10. SEGMENTED INFORMATION

The Company works in

11. FINANCIAL INSTRUMENTS AND RISK

The Company’s financial instruments consist of cash and cash equivalents, short-term investments, receivables and accounts payable and accrued liabilities. The fair value of cash and cash equivalents, GICs and term deposists included in short-term investments, receivables and accounts payable and accrued liabilities approximates their carrying values due to their short term to maturity. The fair value of U.S. treasury securities, corporate debt securities and commercial paper included in short-term investments and the fair value of the money market funds included in cash equivalents are measured using Level 2 inputs based on standard observable inputs, including reported trades, broker/dealer quotes, and bids and/or offers (Note 4).

20

Fair value estimates of financial instruments are made at a specific point in time, based on relevant information about financial markets and specific financial instruments. As these estimates are subjective in nature, involving uncertainties and matters of judgment, they cannot be determined with precision. Changes in assumptions can significantly affect estimated fair values.

Financial Risk Factors

The Company’s risk exposures and the impact on the Company’s financial instruments are summarized below:

Credit risk

Financial instruments that potentially subject the Company to a significant concentration of credit risk consist primarily of cash and cash equivalents, short-term investments and receivables. The Company limits its exposure to credit loss by placing its cash, to the extent possible in segregated funds with major financial institutions. The Company considers highly liquid investments with a maturity of up to twelve months when purchased to be short-term investments. Short-term investments includes investments that may have maturity dates exceeding one year at the date of purchase; however, the Company may liquidate investment positions prior to maturity to implement management strategies. The Company maintains an investment policy which requires certain minimum investment grades over its investment instruments.

As of December 31, 2023, cash and cash equivalents consisted of cash in Canada and the United States, money market funds in the United States and investments in certain instruments which have a maturity of less than three months at the date of purchase. Balances in cash accounts exceed amounts insured by the Canada Deposit Insurance Corporation for up to C$

Liquidity risk

The Company’s approach to managing liquidity risk is to ensure that it will have sufficient liquidity to meet liabilities when due. As of December 31, 2023, the Company had working capital of $

Market risk

Market risk is the risk of loss that may arise from changes in market factors such as interest rates, and foreign exchange rates.

As of December 31, 2023, the Company has cash and cash equivalents balances and short-term investments which are interest bearing. Interest income is not central to the Company’s capital management strategy and not significant to the Company’s projected operational budget. Interest rate fluctuations are not significant to the Company’s risk assessment.

The Company’s foreign currency risk exposure relates to net monetary assets denominated in Canadian dollars and Euro. The Company maintains its cash and cash equivalents in U.S. dollars and converts on an as needed basis to discharge Canadian denominated expenditures. A 10% change in the foreign exchange rate between the Canadian dollar and U.S. dollar in relation to Canadian dollar held at December 31, 2023 would result in a fluctuation of $

21

Item 2. Management’s Discussion and Analysis of Financial Condition and Results of Operations

The following discussion should be read in conjunction with the attached financial statements and notes thereto included in Part I, Item 1 of this Quarterly Report on Form 10-Q, as well as our audited financial statements and related notes thereto and management’s discussion and analysis of financial condition and results of operations for the fiscal year ended September 30, 2023 included in our Annual Report on Form 10-K filed with the U.S. Securities and Exchange Commission (the “SEC”) on December 12, 2023. This Quarterly Report on Form 10-Q, including the following sections, contains forward-looking statements within the meaning of the U.S. Private Securities Litigation Reform Act of 1995 and “forward-looking information” within the meaning of Canadian securities laws, or collectively, forward-looking statements. These statements are subject to risks and uncertainties that could cause actual results and events to differ materially from those expressed or implied by such forward-looking statements. For a detailed discussion of these risks and uncertainties, see “Risk Factors” in our Annual Report on Form 10-K. We caution the reader not to place undue reliance on these forward-looking statements, which reflect management’s analysis only as of the date of this Quarterly Report on Form 10-Q. We undertake no obligation to update forward-looking statements to reflect events or circumstances occurring after the date of this Quarterly Report on Form 10-Q.

Overview

ESSA is a clinical stage pharmaceutical company, focused on developing novel therapies for the treatment of prostate cancer with a primary focus on patients whose disease is still predominantly driven by the androgen axis. ESSA’s development of proprietary small molecule inhibitors of the N-terminal domain (“NTD”) of the androgen receptor (“AR”) is focused on the treatment of these patients in combination with second-generation antiandrogen drugs such as abiraterone, enzalutamide, apalutamide, and darolutamide. The Company believes its latest series of investigational compounds, including its product candidate masofaniten (formerly known as EPI-7386), have the potential to significantly expand the interval of time in which patients with earlier stage prostate cancer can benefit from anti-hormone-based therapies. Specifically, the compounds are designed to disrupt the androgen receptor AR signaling pathway, the primary pathway that drives prostate cancer growth and prevent AR activation through selective binding to the NTD of the AR. In this respect, the Company’s compounds differ mechanistically from classical non-steroid antiandrogens. These classic antiandrogens interfere either with androgen synthesis (i.e., abiraterone), or with the binding of androgens to the ligand-binding domain (“LBD”), located at the opposite end of the receptor from the NTD (i.e., “lutamides”). A functional NTD is essential for the functionality of the AR; blocking the NTD inhibits AR-driven transcription and therefore androgen-driven biology.

The Company believes that the transcription inhibition mechanism of its preclinical compounds is unique and has the potential advantage of bypassing several of the identified mechanisms of resistance to the antiandrogens currently used in the treatment of castration-resistant prostate cancer (“CRPC”). The Company has been granted by the United States Adopted Names (“USAN”) Council a unique USAN stem “-Aniten” to recognize this new first-in-class mechanistic class. The Company refers to this series of proprietary investigational compounds as the “Aniten” series. In preclinical studies, blocking the NTD has demonstrated the capability to prevent AR-driven gene expression. A previously completed Phase 1 clinical trial of ESSA’s first-generation agent, ralaniten acetate (“EPI-506”) administered to patients with metastatic CRPC (“mCRPC”) refractory to current standard of care therapies demonstrated prostate-specific antigen (“PSA”) declines, a sign of inhibition of AR-driven biology. This inhibition, however, was neither deep nor sustained enough to confer clinical benefit and the Company made the decision to develop a more potent next generation drug which would also have a longer half-life. The Company has done so and is now in clinical trial with this next generation Aniten, masofaniten (EPI-7386), focusing on the treatment of earlier stage, more homogeneously androgen-driven tumors, in combination with one or another of the current latest generation classic antiandrogens.

According to the American Cancer Society, in the United States, prostate cancer is the second most frequently diagnosed cancer among men, behind skin cancer. Approximately one-third of all prostate cancer patients who have been treated for local disease with curative intent will subsequently have rising serum levels of PSA, which is an indication of recurrent disease with or without development of distant metastasis. Patients with recurrent disease as indicated by rising PSA or nodal or bone metastasis usually undergo initial androgen ablation therapy using analogues of luteinizing hormone releasing hormone or surgical castration; this approach is termed “androgen deprivation therapy” (“ADT”). Most of these patients initially respond to ADT; however, many experience a recurrence in tumor growth despite the reduction of

22

testosterone to castrate levels, and at that point are considered to have CRPC. Following diagnosis of CRPC, patients have been generally treated with antiandrogens that block the binding of androgens (enzalutamide) to the AR, or inhibit synthesis of androgens (abiraterone). More recently, significant improvements in progression free survival and overall survival have been achieved by utilizing this latest generation of antiandrogens in combination with ADT earlier in the disease natural history (i.e., metastatic hormone-sensitive prostate cancer (“mHSPC”) and non-metastatic castration-resistant prostate cancer (“nmCRPC”)).

Since the mid-20th century, it has been recognized that the growth of prostate tumors is in large part mediated by an activated AR. Generally, there are three means of activating the AR. First, androgens, such as dihydrotestosterone can activate AR by binding to its LBD. Second, CRPC can be driven by variants of AR that lack an LBD, are constitutively activated, and consequently do not require androgen for activation. A third mechanism, of less certain clinical significance, may involve certain signaling pathways that activate AR independent of androgen activity. Generally, current drugs for the treatment of prostate cancer are directed against the first mechanism by either (i) interfering with the production of androgen, or (ii) preventing androgen from binding to the LBD. Over time, these approaches eventually fail due to mechanisms of resistance which involve the LBD end of the receptor, whether at the DNA (AR amplification or LBD mutations) or RNA level (emergence of AR splice variants). With respect to the development of alternative pathway mechanisms of AR activation, tumors may also become insensitive to antiandrogen activity. Finally, in patients who have been treated for years with various antiandrogen therapies, genomic changes may lead to additional, non-AR-related oncogenic drivers, also insensitive to inhibition of AR biology.

The Company believes that through their potential to block androgen-driven gene transcription by using a unique mechanism involving the NTD and thereby bypassing these known mechanisms of resistance to current antiandrogens, the Aniten series of compounds hold the potential to be effective in cases where LBD-based mechanisms of resistance to second generation antiandrogens in otherwise AR-driven disease are operating. The results from both extensive preclinical studies and the initial clinical experience support the Company’s belief. In preclinical studies, the Aniten series of compounds has been observed to shrink AR-dependent prostate cancer xenografts, including tumors both sensitive and resistant to the second-generation antiandrogens, such as enzalutamide. Plasma PSA level declines and increases in PSA doubling time as well as declines in circulating tumor DNA and decreases in radiographic tumor measurements were observed in a subset of patients enrolled in the Phase 1 study of masofaniten (EPI-7386) as described below. Importantly with respect to the potential clinical application of NTD inhibition during the natural history of the disease, recent studies by the Company and its collaborators have also suggested the potential advantage for combinations of the Company’s Aniten compounds with currently approved antiandrogens to inhibit AR-driven biology more completely than AR inhibition from either end of the receptor alone. This hypothesis is supported by the clinical trial results obtained in recent years of the superior overall survival obtained in the hormone-sensitive prostate cancer (“HSPC”) setting by combining ADT and the latest generation antiandrogens earlier in the course of the disease versus the administration of these two therapies sequentially.

While the potential importance of the NTD as a drug target has been appreciated for more than two decades, for technical reasons this has been a difficult target for therapeutic agent development. The NTD of the AR is flexible with a high degree of intrinsic disorder making it difficult for use in classic crystal structure-based drug design. The Company is not currently aware of any clinical-stage NTD AR inhibitors that are in development by other drug development companies. The nature of the highly specific binding of the Aniten compounds to the NTD, and the biological consequences of that binding, have been defined in scientific studies. The selectivity of the binding, based on in vivo imaging as well as in vitro studies, has been consistent with the favorable toxicological results observed in preclinical studies of the first-generation EPI-506 and the subsequent safety results observed in the Phase 1 trial of EPI-506. Subsequent to this trial and following the decision to pursue masofaniten (EPI-7386) as the Company’s lead product candidate, the Company completed a series of biophysical and biological studies revealing the interaction and binding of masofaniten (EPI-7386) to the NTD of the AR and presented these findings at several medical conferences in 2021. See “Completed Phase 1 Clinical Study of EPI-506” and “Next generation Aniten molecules” below.

23

The incidence of both metastatic and non-metastatic CRPC continues to rise. Using a dynamic progression model, Scher et al.1 projected a 2020 incidence of 546,955 and prevalence of 3,072,480.The Company believes that the Aniten series of compounds could ultimately hold potential benefit for many of those patients. In its early clinical development, the Company focused on patients who have failed second-generation antiandrogen therapies (i.e., abiraterone and/or lutamides) for the following reasons:

| ● | CRPC treatment remains a prostate cancer market segment with an apparent and significant unmet therapeutic need and is a potentially large market; |

| ● | the Company believes that the unique mechanism of action of its Aniten compounds is well suited to treat those patients who have failed AR LBD focused therapies and whose biological characterization reveals that their tumors are still largely driven by AR biology; and |

| ● | the Company expects that the relatively large number of patients with an apparent unmet therapeutic need in this area will facilitate timely enrollment in its clinical trials. |

The Company believes that the demonstration of favorable safety and tolerability in the initial Aniten Phase 1 clinical trial, together with the compelling preclinical rationale, enabled and emphasized the importance of the study of the combination of masofaniten (EPI-7386) with second-generation antiandrogens.Furthermore, the Company believes that this application of two independent, complementary mechanisms of AR transcription inhibition may result in greater suppression of androgen activity and the delay or prevention of drug resistance. Recent progress in the clinical treatment of prostate cancer has resulted from the earlier utilization of antiandrogens in combination with classic ADT, consistent with the premise that more effective androgen suppression may yield clinical benefit. The Company believes that the introduction of NTD inhibitors, such as masofaniten (EPI-7386), therefore has the potential to improve androgen suppression, delay the emergence of resistance, and result in improved clinical benefit.

Completed Phase 1 Clinical Study of EPI-506

The Company conducted an initial proof-of-concept Phase 1 clinical study utilizing the first-generation Aniten compound, EPI-506 from 2015 to 2017. The objective of the EPI-506 Phase 1 clinical trial was to explore the safety, tolerability, maximum tolerated dose and pharmacokinetics of EPI-506, in addition to anti-tumor activity in asymptomatic or minimally symptomatic patients with mCRPC who were no longer responding to either abiraterone or enzalutamide treatments, or both. Efficacy endpoints, such as PSA reduction, and other disease progression criteria were evaluated. Details relating to the design of the Phase 1/2 clinical trial of EPI-506 are available on the U.S. National Institutes of Health clinical trials website (see https://clinicaltrials.gov under identifier NCT02606123).

The Investigational New Drug (“IND”) application to the FDA for EPI-506 to begin a Phase 1 clinical trial, was allowed in September 2015, with the first clinical patient enrolled in November 2015. The Company’s Clinical Trial Application (“CTA”) submission to Health Canada was subsequently also cleared. Based on allometric scaling, an initial dose level of EPI-506 of 80 mg was determined. However, following the enrollment of the initial cohorts, it became apparent that EPI-506 exposure was much lower in humans than projected. EPI-506 dosing was escalated aggressively to allow patients in the clinical study greater exposure to the drug. The highest dose patients ultimately received was 3600 mg of EPI-506, administered in a single dose or split into two doses daily. The initial data from the Phase 1 clinical trial was presented at the European Society of Medical Oncology meeting in September 2017.

Conducted at five sites in the United States and Canada, the open-label, single-arm, dose-escalation study evaluated the safety, pharmacokinetics, maximum-tolerated dose and anti-tumor activity of EPI-506 in men with end-stage mCRPC who had progressed after prior enzalutamide and/or abiraterone treatment and who may have received one prior line of chemotherapy. Twenty-eight patients were available for analysis, with each patient having received four or more prior therapies for prostate cancer at the time of study entry. Patients self-administered oral doses of EPI-506 ranging from 80 mg to 3600 mg, with a mean drug exposure of 85 days (range of eight to 535 days). Four patients underwent prolonged treatment (with a median of 318 days; and a range of 219 to 535 days at data cut-off), following intra-patient dose

1 Scher HI, Solo K, Valant J, Todd MB, Mehra M (2015) Prevalence of Prostate Cancer Clinical States and Mortality

in the United States: Estimates Using a Dynamic Progression Model. PLoS ONE 10(10): e0139440.

doi:10.1371/journal.pone.013944

24

escalation. PSA declines, a measure of potential efficacy, ranging from 4% to 37% were observed in five patients, which occurred predominantly in the higher dose cohorts (≥1280 mg).

EPI-506 was generally well-tolerated with favorable safety results observed across all doses up to 2400 mg. At a dose of 3600 mg, gastrointestinal adverse events (nausea, vomiting and abdominal pain) were observed in two patients: one patient in the once-daily (“QD”) dosing cohort and one patient in the 1800 mg twice-daily dosing cohort, leading to study discontinuation and a dose-limiting toxicity (“DLT”) due to more than 25% of doses being missed in the 28-day safety reporting period. A separate patient in the 3600 mg QD cohort experienced a transient Grade 3 increase in liver enzymes (AST/ALT), which also constituted a DLT, and enrollment was consequently concluded in this cohort.

Although the Company believes that the safety results and possible signs of anti-tumor activity observed at higher dose levels support the concept that inhibiting the AR-NTD may provide a clinical benefit to mCRPC patients, the pharmacokinetic and metabolic studies revealed the limitations of the first generation agent EPI-506. Through its discovery research the Company had concluded that it should be feasible to develop a next generation of NTD inhibitor which would demonstrate greater potency, reduced metabolism and other improved pharmaceutical properties. As a result, the Company announced on September 11, 2017 its decision to discontinue the further clinical development of EPI-506 and to implement a corporate restructuring plan to focus research and development resources on its next-generation Anitens targeting the AR-NTD. This next generation Aniten compound includes significantly more potent drugs designed to exhibit increased resistance to metabolism and therefore a longer predicted circulating half-life. The Company’s lead product candidate masofaniten (EPI-7386) has demonstrated these and other favorable characteristics in extensive preclinical characterization and clinical studies which the Company has presented in a series of poster presentations at scientific meetings.

Next generation Aniten molecules

The Company’s family of next-generation investigational Aniten compounds incorporate multiple chemical scaffold changes to the first-generation drugs which in preclinical studies retain NTD inhibition of the AR. In addition, they have shown improvement in a range of attributes when compared to the first-generation compound, EPI-506, in preclinical studies. In in vitro assays measuring inhibition of AR transcriptional activity, these product candidates demonstrated 20 times higher potency than EPI-506 or its active metabolite, EPI-002. In addition, the compounds have demonstrated increased metabolic stability in preclinical studies, suggesting the potential for longer half-lives in humans. Lastly, the compounds have demonstrated more favorable pharmaceutical properties relative to EPI-506. The Company believes that these product candidates, if successfully developed and approved, may offer advancements in ease and cost of large-scale manufacture, drug product stability, and suitability for commercialization globally. Of these next-generation Anitens, masofaniten (EPI-7386) was selected for IND filing and a Phase 1 clinical trial.

Our Strategy

In developing possible therapeutics that involve binding to the NTD, the Company’s strategic approach involves:

| ● | combining Aniten compounds with second generation antiandrogens in earlier lines of therapy. The Company, with industry partners, has been conducting clinical trials of combinations of masofaniten (EPI-7386) and second-generation antiandrogens in patients with nmCRPC, mCRPC, mHSPC and neo-adjuvant prostate cancer surgical therapy in earlier lines of treatment; |

| ● | completing the initial Phase 1 clinical development of masofaniten (EPI-7386) as a monotherapy treatment for patients with mCRPC, who are resistant to the current standard of care, to demonstrate the drug’s characteristics as a single agent as completely as possible, with regards to safety, tolerability, and efficacy together with detailed pharmacological and biological studies. The Company’s assessment of this clinical data will determine its clinical development of masofaniten (EPI-7386) as a single agent therapy and also as a combination therapy, whilst considering the impact of such treatment against the size of the patient population whose tumors have progressed and are prevalently driven by the AR pathway despite heavy pre-treatment of the latest generation antiandrogens; and |

25

| ● | continuing preclinical studies including work on other Aniten molecules and other potential applications for AR NTD inhibitors. |

The identification and characteristics of masofaniten (EPI-7386)

The purpose of the next-generation program has been to identify drug candidates with increased potency, reduced metabolic susceptibility and superior pharmaceutical properties compared to ESSA’s first-generation compounds. Structure-activity relation studies conducted on the chemical scaffold of ESSA’s first-generation compounds have resulted in the generation of a new series of compounds that have demonstrated higher potency and predicted longer half-lives. Multiple changes in the chemical scaffold have also been incorporated with the goal of improving ADME (absorption, distribution, metabolism, and excretion) and pharmaceutical properties of the chemical class.

Several next-generation Aniten molecules met prespecified preclinical target product profile goals regarding potency, stability, selectivity and pharmaceutical properties. On March 26, 2019, the Company announced the nomination of masofaniten (EPI-7386) as its lead clinical candidate for the treatment of mCRPC through inhibition of the NTD of the androgen receptor. In preclinical studies, masofaniten (EPI-7386) has displayed activity in vitro in numerous AR-dependent prostate cancer models including models where second-generation antiandrogens are inactive. In addition, masofaniten (EPI-7386) is significantly more potent, metabolically stable and more effective in preclinical studies compared to ESSA’s first-generation compound, EPI-506. Lastly, masofaniten (EPI-7386) has demonstrated a favorable tolerability profile in all animal studies of the compound conducted to date.

From this series of next-generation compounds, masofaniten (EPI-7386) was selected as the lead candidate for the initial clinical development in mCRPC. An IND was submitted to the FDA on March 30, 2020 and was allowed by the FDA on April 30, 2020. A CTA was filed with Health Canada in April 2020 and clearance was subsequently received. Clinical testing of masofaniten (EPI-7386) commenced in July 2020, allowing for accommodations to the planned timeline as a result of the impact of COVID-19 at clinical trial sites (see “Risk Factors - Widespread health concerns, pandemics or epidemics, and other outbreaks of illness may negatively affect the Company’s ability to maintain operations and execute its business plan” in our Annual report on Form 10-K).

26

Advancing masofaniten (EPI-7386) through clinical development

The Company is advancing masofaniten (EPI-7386) through two clinical trials: EPI-7386-CS-001 and EPI-7386-CS-010. The clinical trial of EPI-7386-CS-001 has two arms that represent a monotherapy and combination component of the study schema, as outlined below:

Notes: “mCRPC” means metastatic castration-resistant prostate cancer; “AAP” means abiraterone acetate/prednisone; “mHSPC” means metastatic hormone-sensitive prostate; and “nmCRPC” means non-metastatic castration-resistant prostate cancer

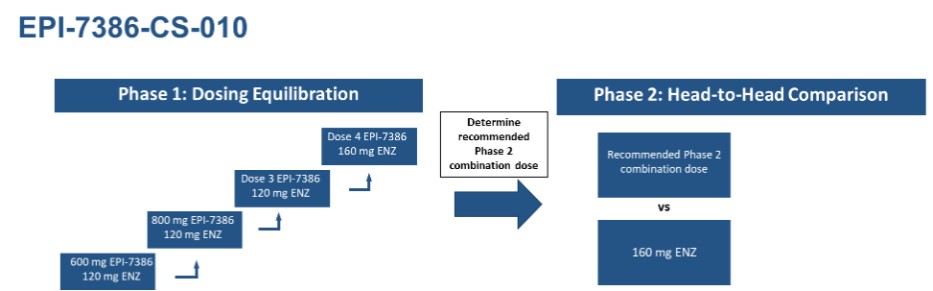

The clinical trial of EPI-7386-CS-010 is a combination trial with enzalutamide with a Phase 1 dose equilibration component and Phase 2 head-to-head comparison component, as outlined in the study schema below:

Notes: “ENZ” means enzalutamide

Phase 1 Clinical Trial - EPI-7386-CS-001- Monotherapy Treatment

The Phase 1 clinical trial of masofaniten (EPI-7386) “Oral EPI-7386 in Patients With Castration-Resistant Prostate Cancer (EPI-7386)” is currently actively enrolling nmCRPC patients naïve to second generation antiandrogens and mCRPC patients who are refractory to standard of care treatments at clinical sites in the U.S. and Canada (www.clinicaltrials.gov under identifier NCT04421222). In September 2021, the Company amended the protocol to allow testing in the Phase 1a for a 800 mg/day and 1200 mg/day dosages, administered as either 400 mg or 600 mg dosed twice daily (“BID”), respectively. In addition, the protocol amendment focused further monotherapy development in less heavily pretreated patients with mCRPC, i.e., patients who have received a maximum of three prior approved systemic therapies for mCRPC, including at least one second-generation antiandrogen and excluded patients with visceral metastasis.

27

Part A Monotherapy - Phase 1a – Dose Escalation

The open-label, dose-escalation Phase 1a clinical trial was designed to determine the safety, tolerability, pharmacokinetics, maximum tolerated dose and/or a recommended Phase 2 range of doses in line with the FDA’s Project Optimus, and to access preliminary anti-tumor activity of the drug.

The design of the Phase 1 clinical trial included the standard 3+3 design per dose cohort for the Part 1a dose escalation phase, with subjects receiving a daily oral dose of masofaniten (EPI-7386) once a day QD until there is objective evidence of clinical disease progression, and or occurrence of an unacceptable toxicity.

The dose escalation Part 1a of the study has completed enrollment. Patients enrolled in the Part 1a of the study were selected clinically, on the basis of having progressive mCRPC as exemplified by rising PSA values and/or radiological disease progression despite latest generation antiandrogen treatment. However, all patients were also retrospectively biologically characterized for underlying tumor genomic characteristics, for evidence of AR pathway activation as well as non-AR oncogenic pathways and during the conduct of the trial, for dose-related biological, pharmacological and pharmacodynamic effects.

The protocol amendments filed with the FDA in September 2021 and July 2022 allow for monotherapy development in less heavily pretreated patients (as described above) in whom the androgen receptor pathway is more likely to be the primary driver of tumor growth. The Company’s goal has been to establish, one or more doses/schedules to be tested in the expansion Phase 1b study in alignment with the FDA Project Optimus guidance, based on multiple inputs, including pharmacokinetic and biological observations, in addition to clinical experience. Two dose levels have been advanced to Phase 1b dose expansion testing: 600 mg QD and 600 mg BID.

Part A Monotherapy - Phase 1b – Dose Expansion

The primary objective of Phase 1b is to further evaluate the safety, tolerability, pharmacokinetics, and preliminary anti-tumor activity (as measured by changes in tumor burden measured by imaging and changes in PSA levels over time) of masofaniten (EPI-7386) at 600 mg BID and 600 mg QD in a patient population enrolled under eligibility criteria similar to the one adopted for the Phase 1a with a focus on chemo-naïve mCRPC patients whose diseases have progressed after two lines of treatment including at least one line of second-generation antiandrogens. The 600 mg BID cohort of 12 patients has been fully enrolled and the 600 mg QD cohort of 12 patients is completing enrollment.

Demonstration of the favorable safety and tolerability profile of masofaniten (EPI-7386) in the Phase 1a, together with clinical evidence for its mechanism of action and efficacy, were necessary to enable the study of patient populations with less advanced and less heavily pre-treated prostate cancer. The experience in the initial Phase 1a trial provided evidence for both an antiandrogen biological effect as well as some clinically relevant anti-tumor activity. The biological characterization of these patients also demonstrated favorable safety profiles.

The Company’s preclinical data and other evidence suggest earlier patient populations are more homogeneously AR-driven, and the favorable safety profile demonstrated in the Phase 1a dose escalation trial justified the study of the combination of masofaniten (EPI-7386) with classic antiandrogens. As a result the Company, together with its collaborators, are conducting a series of clinical trials in this regard. The first Phase 1/2 study involves masofaniten (EPI-7386) evaluated in combination with enzalutamide in patients with mCRPC naïve to second generation antiandrogens. Additional clinical trials involving the combination of masofaniten (EPI-7386) with apalutamide, abiraterone acetate, or darolutamide are in various stages of implementation.

Combination studies – developing a new standard of care for the treatment of prostate cancer

An activated AR is required for the growth and survival of most prostate cancer. Unlike current antiandrogen therapies which can only inhibit full-length AR, NTD inhibition of AR-directed biology occurs both in full length AR and splice variant ARs. Therefore, the Company believes that the AR-NTD is an ideal target for next-generation antiandrogen hormone therapy. If ESSA’s masofaniten (EPI-7386) is successful in treating CRPC patients, it is reasonable to expect

28

that such clinical candidate may be effective in treating earlier stage patients. Preclinical studies suggest particular value to the use of Anitens in combination with the currently widely used second-generation antiandrogens. The Company is conducting clinical trials in line with this strategy.

Clinical Trial - EPI-7386-CS-010 – Combination Treatment with Enzalutamide

The Company has been running a Phase 1/2 study of masofaniten (EPI-7386) in combination with enzalutamide compared with enzalutamide alone in patients with mCRPC. Phase 1 of the study is a single-arm dose escalation study of masofaniten (EPI-7386) in combination with a fixed dose of enzalutamide.