UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

ý | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2015.

OR

o | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the Transition Period from to .

Commission file number 001-36859

PayPal Holdings, Inc.

(Exact Name of Registrant as Specified in Its Charter)

Delaware | 47-2989869 |

(State or Other Jurisdiction of Incorporation or Organization) | (I.R.S. Employer Identification No.) |

2211 North First Street San Jose, California | 95131 |

(Address of Principal Executive Offices) | (Zip Code) |

(408) 967-1000

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

Title of each class | Name of each exchange on which registered |

Common Stock, $0.0001 par value per share | The NASDAQ Stock Market LLC |

Securities registered pursuant to Section 12(g) of the Securities Exchange Act of 1934:

None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yes [x] No [ ]

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Exchange Act. Yes [ ] No [x]

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Exchange Act during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes [x] No [ ]

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter)

during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes [x] No [ ]

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer | ý | Accelerated filer | o |

Non-accelerated filer | o (Do not check if a smaller reporting company) | Smaller reporting company | o |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes [ ] No [x]

As of June 30, 2015, the registrant's common stock was not publicly traded.

As of February 5, 2016, there were 1,222,675,902 shares of common stock outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Part III incorporates information by reference from the definitive proxy statement for the registrant's Annual Meeting of Stockholders expected to be held in May 2016.

TABLE OF CONTENTS

Page | ||

Part I | ||

Item 1. | ||

Item 1A. | ||

Item 1B. | ||

Item 2. | ||

Item 3. | ||

Item 4. | ||

Part II | ||

Item 5. | ||

Item 6. | ||

Item 7. | ||

Item 7A. | ||

Item 8. | ||

Item 9. | ||

Item 9A. | ||

Item 9B. | ||

Part III | ||

Item 10. | ||

Item 11. | ||

Item 12. | ||

Item 13. | ||

Item 14. | ||

Part IV | ||

Item 15. | ||

Presentation of Information

On July 17, 2015, PayPal Holdings, Inc. (“PayPal Holdings”) became an independent publicly-traded company through the pro rata distribution by eBay Inc. (“eBay”) of 100% of the outstanding common stock of PayPal to eBay’s stockholders (which we refer to as the “separation” or the “distribution”). For additional information, see “Business—Separation from eBay Inc.” To accomplish this separation, in January 2015, eBay incorporated PayPal Holdings, Inc. (“PayPal Holdings”) which ultimately became the parent of PayPal, Inc. and holds directly or indirectly all of the assets and liabilities associated with PayPal, Inc. Unless otherwise expressly stated or the context otherwise requires, references to “we,” “our,” “us,” “the Company” or “PayPal” refer to PayPal Holdings, Inc. and its consolidated subsidiaries or, in the case of information as of dates or for periods prior to our separation from eBay, the combined and consolidated entities of the payments business of eBay, including PayPal, Inc. and certain other assets and liabilities that were historically held at the eBay corporate level, but were specifically identifiable and attributable to the payments business, and references to our “Payments Platform” mean our combined payment solution capabilities, including our PayPal, PayPal Credit, Braintree, Venmo and Xoom products.

References in this Annual Report on Form 10-K to “eBay” refer to eBay Inc., a Delaware corporation, and its consolidated subsidiaries, which prior to the separation and distribution, but not after such date, included the business and operations of PayPal.

Trademarks, Trade Names and Service Marks

PayPal owns or has rights to use the trademarks, service marks and trade names that it uses in conjunction with the operation of its business. Some of the more important trademarks that PayPal owns or has rights to use that appear in this Annual Report on Form 10-K include: PayPal®, PayPal Credit®, Braintree, Venmo and Xoom, which may be registered or trademarked in the United States and other jurisdictions. PayPal’s rights to some of these trademarks may be limited to select markets. Each trademark, trade name or service mark of any other company appearing in this Annual Report on Form 10-K is, to PayPal’s knowledge, owned by such other company.

Part I

FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934, including statements that involve expectations, plans or intentions (such as those relating to future business, future results of operations or financial condition, new or planned features or services, or management strategies). You can identify these forward-looking statements by words such as “may,” “will,” “would,” “should,” “could,” “expect,” “anticipate,” “believe,” “estimate,” “intend,” “plan” and other similar expressions. These forward-looking statements involve risks and uncertainties that could cause our actual results to differ materially from those expressed or implied in our forward-looking statements. Such risks and uncertainties include, among others, those discussed in “Item 1A: Risk Factors” of this Annual Report on Form 10-K, as well as in our combined and consolidated financial statements, related notes, and the other information appearing elsewhere in this report and our other filings with the Securities and Exchange Commission (“SEC"). We do not intend, and undertake no obligation, to update any of our forward-looking statements after the date of this report to reflect actual results or future events or circumstances. Given these risks and uncertainties, readers are cautioned not to place undue reliance on such forward-looking statements. You should read the information in this report in conjunction with the audited combined and consolidated financial statements and the related notes that appear elsewhere in this report.

ITEM 1: BUSINESS

Overview

PayPal Holdings, Inc. (“we,” “our,” “us,” “the Company” or “PayPal”) is a leading technology platform company that enables digital and mobile payments on behalf of consumers and merchants worldwide. We believe in providing simple, affordable, secure and reliable financial services and digital payments to help our customers around the world to achieve their financial goals. We strive to increase our relevance for consumers, merchants, friends and family to access and move their money anywhere in the world, anytime, on any platform and through any device (e.g., mobile, tablets, personal computers or wearables). We provide safer and simpler ways for businesses of all sizes to accept payments from merchant websites, mobile devices and applications, and at offline retail locations through a wide range of payment solutions. We also facilitate person to person payments through PayPal, Venmo and Xoom (acquired in November 2015). Our combined payment solution capabilities, including our PayPal, PayPal Credit, Braintree, Venmo, and Xoom products, comprise our proprietary Payments Platform. The terms "we," "our," "us," "the Company," and "PayPal" mean PayPal Holdings, Inc. and, unless otherwise expressly stated or the context requires, its subsidiaries.

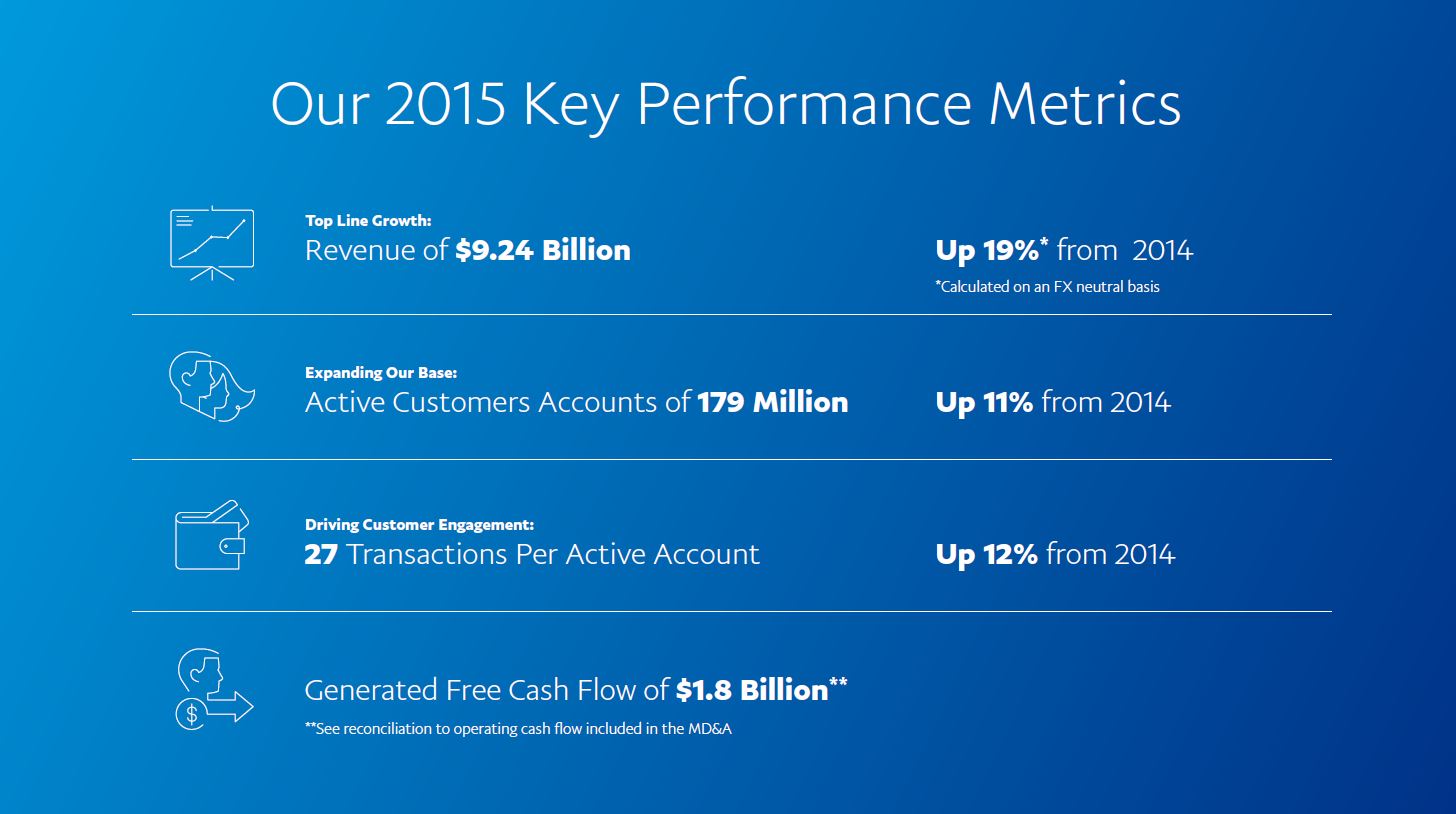

We enable global commerce by providing payment solutions for our approximately 179 million active customer accounts in over 200 markets as of December 31, 2015, while providing customers a choice of how they would like to pay or get paid. A market is a geographic area or political jurisdiction, such as a country, territory, or protectorate, in which we offer our services. A country, territory or protectorate is identified by a distinct set of laws and regulations. An active customer account is a registered account that successfully sent or received at least one payment or payment reversal through our Payments Platform, excluding transactions processed through our gateway and Paydiant products, in the past 12 months. Our gateway products include our Payflow Payments and certain Braintree products. A payment gateway links a merchant’s website to that merchant’s processing network and merchant account.

We offer our customers the flexibility to use their account to both purchase and be paid for goods, as well as transfer and withdraw funds. A consumer can typically fund a purchase using a bank account, a PayPal account balance, a PayPal Credit account, a credit or debit card or other stored value products such as coupons and gift cards. Our PayPal, Venmo, and Xoom products also make it safer and simpler for friends and family to transfer funds to each other, including cross border transfers using several of these funding sources. We offer merchants an end-to-end payments solution that provides authorization and settlement capabilities, as well as instant access to funds. We help merchants connect with their customers and manage risk. PayPal's aim is to create deeper, more relevant relationships with each of its customers. We measure the relevance of our products in the lives of our customers, and therefore the success of our business, through both payment volume and payment transactions. Payment volume is the value of payments, net of payment reversals, successfully completed through our Payments Platform, excluding transactions processed through our gateway and Paydiant products (“Total Payment Volume” or “TPV”). During 2015, our TPV was approximately $282 billion, representing growth of 20% over 2014. “Payment transactions” is the total number of payments, net of payment reversals, successfully completed through our Payments Platform, excluding transactions processed through our gateway and Paydiant products. During 2015, we processed approximately 4.9 billion payment transactions, representing growth of 24% over 2014. This translated to 27.5 payment transactions per active customer account in 2015. This is an increase from 24.5 payment transactions per active customer account in 2014. "Payment transactions per active customer account" reflects the total number of payment transactions within the previous 12 month period, divided by active customer accounts at the end of the period.

1

Our Payments Platform is built to make the existing global financial infrastructure work for people in the digital and mobile age. PayPal allows people to make seamless transactions between different markets and networks. Our Payments Platform connects with financial institutions around the world and allows consumers to make purchases using a broad range of payment methods, regardless of where a merchant is located. Consumers who use our Payments Platform can engage in cross-border shopping by sending payments in more than 200 markets across the globe and in more than 100 currencies. This enables merchants to extend their reach across borders to an expanded customer base.

We generate revenues by charging fees for providing transaction processing and other payment-related services, primarily based on the volume of activity, or TPV, processed through our Payments Platform. We also earn revenue by providing value added services to consumers and merchants, such as our PayPal Credit and Paydiant products. During 2015, we generated revenue of $9.2 billion, representing growth of 15% over 2014 (19% on an foreign currency neutral basis).

Our revenue is influenced by, among other things, consumer spending patterns, merchant adoption of payment methods other than traditional credit or debit cards and cash, the expansion of multi-channel retail, the growth of mobile devices and merchant applications on those devices, the growth of consumers with access to the Internet globally, the pace of transition from paper-based forms of payment to digital forms of payment, our share of the digital payments market, and our ability to innovate new methods of payment that merchants and consumers find to be valuable. Our strategy is to drive growth by:

• | Growing our core businesses globally through expanding our capabilities and base of active customer accounts, increasing our customers’ use of our products and services by better addressing our customers’ everyday needs in managing and moving money and expanding the adoption of our solutions by new merchants and consumers; |

• | Expanding our value proposition for customers by providing risk management, insights from our two-sided Payments Platform, and scale; |

• | Extending our existing business by seeking new areas of growth in markets around the world and focusing on innovation both in the digital and the physical world; and |

• | Enhancing our strong foundation focused on trust, simplicity, and being technology agnostic. |

2

In line with our strategy to drive growth, we focus on the generation of free cash flow. Free cash flow is a non-GAAP financial measure defined as cash flow from operations less purchases of property and equipment. We consider free cash flow to be a key performance measure that provides useful information to management and investors about the amount of operating cash flow generated by the business after the purchases of property and equipment, which can then be used to, among other things, invest in our business, make strategic acquisitions, and return cash to shareholders. In 2015, we generated $1.8 billion in free cash flow; this represents an increase of $96 million from 2014. Please refer to Part II, Item 7 "Management's Discussion and Analysis of Financial Condition and Results of Operations - Non-GAAP Financial Information" for information on how we compute free cash flow and a reconciliation of free cash flow to the most directly comparable GAAP financial measure.

PayPal is a popular form of payment for mobile commerce, and our business has grown with the increased adoption of mobile devices. We believe that our Braintree products strengthen our position in mobile payments and extend our coverage to a new class of retailers who offer their services primarily through mobile applications. These products have expanded our footprint with earlier stage merchants. Our Venmo app is a leading mobile application to move money between friends and family using their mobile device. With Venmo, we have a diversified demographic of consumers. In April 2015, we completed our acquisition of Paydiant to further expand our capabilities in mobile payments. Using Paydiant’s platform, our merchant partners can create their own branded wallets to accelerate mobile-in-store payments and drive consumer engagement through mobile payments, loyalty, offers and the prioritization of preferred payment types, such as store branded credit cards and gift cards. In November 2015, we completed our acquisition of Xoom. Xoom enables consumers to send money, pay bills and send mobile phone reloads to family and friends around the world using mobile devices. We believe that mobile devices are the bridge between online, in-app, and in-store offerings, creating a pathway to a larger addressable market. In addition, mobile becomes a conduit that facilitates the movement and management of money, including remittances, consumer lending, and person-to-person ("P2P") transactions.

We operate globally and in a rapidly evolving regulatory environment characterized by a heightened regulatory focus on all aspects of the payments industry. That focus continues to become even more heightened as regulators on a global basis focus on such important issues as countering terrorist financing, anti-money laundering, privacy and consumer protection. Some of the laws and regulations to which we are subject were enacted recently and the laws and regulations applicable to us, including those enacted prior to the advent of digital and mobile payments, are continuing to evolve through legislative and regulatory action and judicial interpretation. Non-compliance with laws and regulations, increased penalties and enforcement actions related to non-compliance, changes in laws and regulations or their interpretation, and the enactment of new laws and regulations applicable to us could have a material adverse impact on our business, results of operations and financial condition. Therefore, we monitor these areas closely to ensure compliant solutions for our customers who depend on us.

3

Connecting Merchants and Consumers

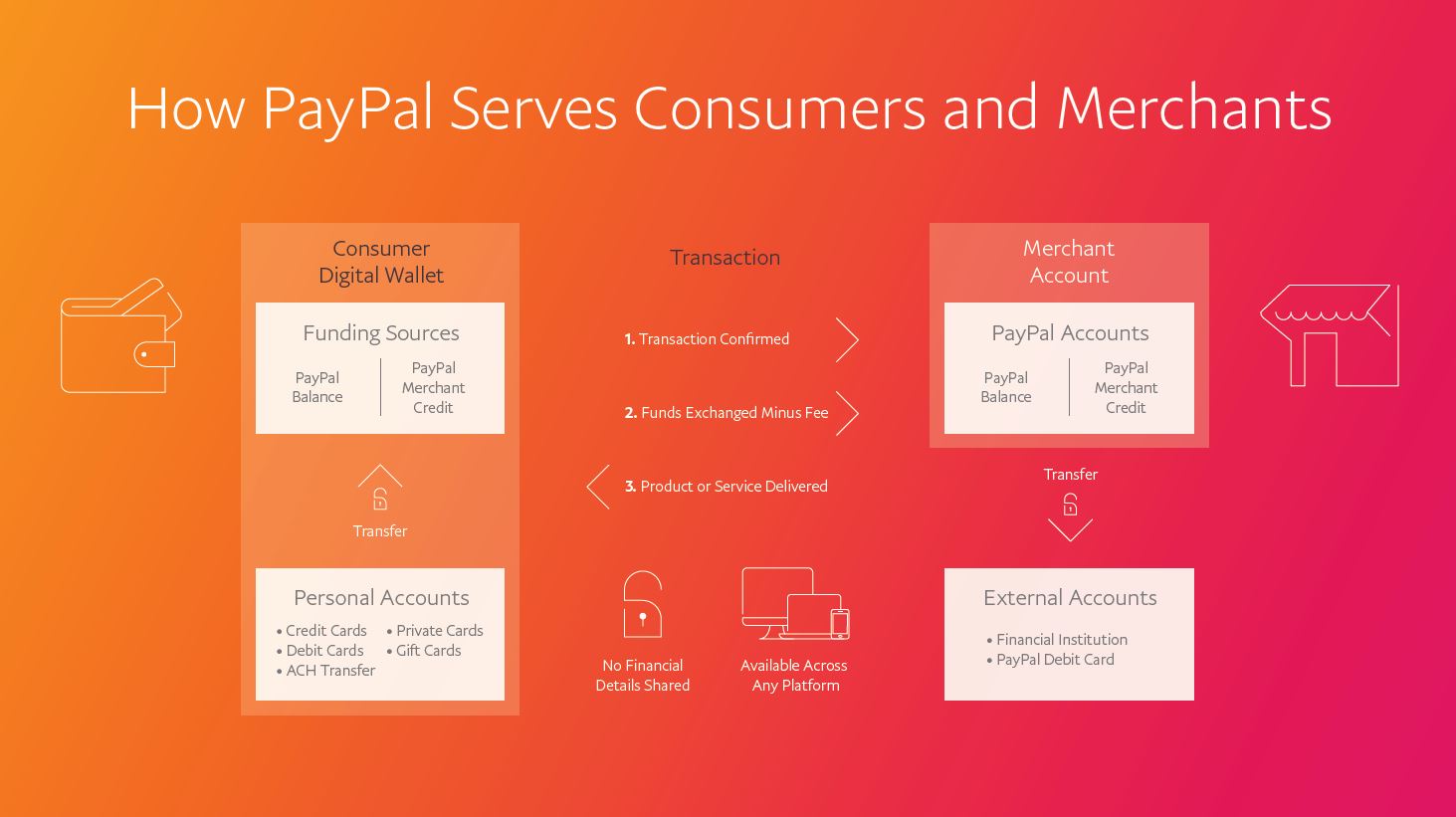

We operate a proprietary global technology platform that links merchants and consumers around the globe to facilitate the processing of payment transactions, allowing us to connect millions of merchants and consumers worldwide. Our Payments Platform facilitates an efficient and secure means for merchants to receive payments, and a convenient, secure way for consumers to make payments. We process transactions through our Payments Platform in more than 200 markets, allowing customers to pay and get paid in more than 100 currencies, withdraw funds to their bank accounts in 57 currencies and hold balances in their PayPal accounts in 26 currencies.

A transaction on our Payments Platform can involve up to three participants in addition to us: a merchant, a consumer and the consumer’s funding source provider. The following diagram illustrates a typical payment transaction between a consumer and a merchant on our Payments Platform:

Consumers

We enable consumers to more safely exchange funds with merchants using their PayPal digital wallet. Our digital wallet provides consumers with the ability to draw funds from a variety of their financial resources, which may include both “internal” sources of funds (i.e., a PayPal account balance or PayPal Credit account) and sources of funds that are “external” to PayPal (e.g., bank transfers, credit and debit cards or gift cards), within one application. We generally do not charge consumers to fund or draw from their accounts; however, we generate revenue from consumers on fees charged to exchange currencies and on interest and fees from consumer loans originated through our PayPal Credit products.

We value our relationship with our consumers and invest in this relationship. We strive to provide efficient customer service, account support, and protection from loss, and to create relevant products. As of December 31, 2015, over 8,000 people in our customer service organization worked to provide our consumers with answers and solutions when and where they need them, in over 20 languages. We have operations centers around the world, including in the U.S., Europe, Asia and South America, that strive to provide high-quality service and support for our customers. We have also developed a number of trust and security programs, including PayPal’s Buyer Protection Program, that provide additional protection to consumers for qualifying purchases by reimbursing the consumer for the full amount of the purchase if a purchased item does not arrive or is significantly different than the seller’s description (see "Revenue Sources—Protecting Merchants and Consumers" below).

Traditional financial institutions often charge fees for basic services provided to their customers, and existing alternatives to these financial institutions, including services to cash a check or pay a bill, can be inconvenient and expensive. We focus on providing

4

affordable consumer products that democratize the access to and movement of money. We believe that managing and moving a consumer’s money should be a right, not a privilege. Through our technology and products, we believe we can change the status quo and make digital payments more efficient and accessible. We expect P2P transfers to contribute to this strategy. We believe that our P2P products have network effects and help to establish relationships with potential PayPal users by allowing them to join the Payments Platform at the time of making or receiving payments, which encourages our natural, customer-driven growth. PayPal offers P2P payment solutions through its website, its PayPal mobile application, through Venmo, a mobile application that enables payment transactions between non-merchant account holders, and through Xoom, a service enabling payments from customers in the United States to family and friends in a secure, fast and cost-effective way, using their mobile phones or computers. Xoom offers money transfer services from the United States to 41 countries, cross-border bill payment services from the United States to 7 countries and prepaid mobile phone reload services in 25 countries.

We also provide the ability for consumers to receive a line of credit through our PayPal Credit consumer products. Consumers access this credit through their PayPal account or directly with merchants. As of December 31, 2015, we have purchased or extended approximately $7.4 billion in credit to consumers, of which $4.0 billion is currently outstanding. We currently fund the purchase of PayPal Credit consumer receivables with international and domestic cash resources. Our chartered financial institution in Luxembourg, or an independent chartered financial institution in the U.S. with whom we partner, extends credit to the consumer, funds the extension of credit at the point of sale (“POS”) and advances funds to the merchant. In the U.S., we subsequently purchase the consumer receivables related to the consumer loans from the independent chartered financial institution with whom we partnered and as a result of that purchase, bear the risk of loss on the related consumer receivables, less a participation interest held by the independent chartered financial institution. As we expand the availability of our credit products, we expect to utilize capital from internal and external sources. In the second quarter of 2015, we concluded an arrangement with certain investors whereby we sold a participation interest in certain consumer receivables originated by PayPal Credit. We will continue to evaluate partnerships and third party sources of funding of our credit portfolio, including, but not limited to, commercial banks, securitization markets, private equity firms, sovereign wealth funds and under certain specific circumstances, the use of customer funds. For additional information concerning our consumer credit products, see “Management’s Discussion and Analysis of Financial Condition and Results of Operations -Future Liquidity and Obligations” and “Note 9—Loans and Interest Receivable Net” to our combined and consolidated financial statements included elsewhere herein.

Merchants

As commerce continues to transition from the physical world to the digital world and from domestic commerce to global commerce, our proprietary Payments Platform provides opportunities for merchants to grow their businesses. We partner with merchants to help them grow and expand their businesses by improving sales conversion, providing global reach, offering alternative payment methods (such as easy integration credit products and mobile capabilities), reducing losses through proprietary protection programs, and leveraging data analytics. We focus on growing merchant acceptance through business development activities and direct relationships with merchants. We enable merchants to more safely and simply receive payments from our active customer accounts, providing global reach while reducing some of the complexity and friction involved in enabling overseas and cross-border trade. For the year ended December 31, 2015, approximately 45% of our TPV involved a merchant outside of the U.S., and approximately 22% was cross-border (i.e., transactions where the merchant or consumer were in different countries).

A merchant can typically open a standard PayPal account and begin accepting payments through PayPal within a few minutes. Most online or mobile merchants can onboard quickly and are not required to invest in new or specialized hardware. Our Payments Platform supports growth with a variety of value added services designed to help businesses of all sizes manage their cash flow, invoice clients, pay bills, and reduce the need for merchants to receive and store sensitive customer financial information. For our standard service, we do not charge merchants setup or recurring fees. A merchant can also integrate with Braintree to begin accepting payments with credit or debit cards, PayPal, Venmo, digital currencies such as Bitcoin, or other payment solutions with a single integration.

Our payment and PayPal Credit products are designed to help merchants increase the conversion rate of consumer purchases on their websites and mobile applications. For example, our One Touch product allows consumers to authenticate their account during their first One Touch purchase. This enables them to skip the login process for future payments and turn shopping into a one touch operation with near-instant authentication. With a faster authentication process, we believe that fewer customers will abandon a potential transaction before completing it. We also provide the ability for merchants to offer (and consumers to fund) payments via a deferred payment option using our PayPal Credit consumer products. In addition, our PayPal Working Capital (“PPWC”) product provides merchants with a working capital advance, which is paid back to PayPal through a percentage of a merchant’s sales that PayPal processes. In 2015, we achieved the milestone of having originated more than $1 billion in working capital advances. As of December 31, 2015, we had $421 million PayPal Working Capital advances and fees receivable outstanding. Our PPWC product allows us to deepen our engagement with our small business customers by offering them additional services. For additional information concerning our merchant credit products, see “Management’s Discussion and Analysis of Financial

5

Condition and Results of Operations -Future Liquidity and Obligations” and “Note 9—Loans and Interest Receivable, Net” to our combined and consolidated financial statements included elsewhere in this Annual Report on Form 10-K.

We value our relationship with merchants and invest in this relationship by providing customer service, account support, developer advocacy and support, and proprietary risk and security solutions. In addition to our consumer protection programs, we have also developed PayPal’s Seller Protection Program. This program provides protection to merchants against claims that a transaction was not authorized by the buyer or claims that an item was not received by covering the seller for the full amount of the payment on eligible sales. By offering dual buyer and seller protection programs, both the consumer and merchant can transact with confidence.

Our Payments Platform and open application programming interfaces (“APIs”) are designed to allow developers to innovate with ease and to offer cutting edge applications to a large ecosystem of merchants and consumers, while at the same time maintaining the security of our customers’ financial information. We provide developers with easy to use, flexible and powerful tools that are designed to leverage our global reach and payment capabilities. Our software developer kits (“SDKs”) are specifically focused on the mobile application market and are designed to remove friction by not requiring a redirect to the PayPal website or an additional log-in. We are using a true “mobile first” approach to make payments simple and intuitive.

Competition

The global payments industry is highly competitive. We compete against businesses in varied industries, many of which are larger than we are, have a dominant and secure position in other industries, or offer other goods and services to consumers and merchants which we do not offer. We compete against all forms of payments, including credit and debit cards; automated clearing house and bank transfers; other online payment services; mobile payments; and offline payment methods, including cash and check.

We compete primarily on the basis of the following:

• | ability to attract, retain and engage both merchants and consumers; |

• | ability to show that merchants will achieve incremental sales by offering our PayPal services; |

• | security of transactions and the ability for consumers to use our PayPal products and services without sharing their financial information with the merchant or the party they are paying; |

• | simplicity of our fee structure; |

• | ability to develop services across multiple commerce channels, including mobile payments and payments at the retail point of sale; |

• | trust in our dispute resolution and buyer and seller protection programs; |

• | customer service; |

• | brand recognition; |

• | website, mobile platform and application onboarding, ease-of-use and accessibility; |

• | system reliability and data security; |

• | ease and quality of integration into third-party mobile applications and operating systems; and |

• | quality of developer tools such as our application programming interfaces and software development kits. |

For additional information concerning competition and our competitors, see Item 1A: “Risk Factors- Substantial and increasingly intense competition worldwide in the global payments industry may harm our business.”

PayPal seeks to differentiate itself from industry participants on the safety of the transaction (our risk management capabilities as well as protection of consumer account details), the simplicity provided for digital transactions, and being both brand and technology agnostic. Further, unlike traditional four-party networks or other mobile payment solutions, PayPal has a direct financial relationship with both its consumers and merchants. As a result of our risk management capabilities, PayPal can provide its customers with protection from fraud and other losses incurred by participants to a transaction.

To compete effectively, we will need to continue to expend significant resources in technology and marketing. During 2015, PayPal incurred $947 million on product innovation and development and enhancing our infrastructure to ensure our customers have the capabilities they need and want to complete transactions safely and simply. Further, in 2015, we incurred over $900 million related to our efforts to promote our brands through advertising, promotions, and other strategic initiatives. Our marketing efforts play an important role in building brand visibility, usage and overall preference among consumers at checkout.

Our strengths

Our business is built on a strong foundation designed to allow PayPal to differentiate itself from our competitors and drive growth.

6

Our competitive capabilities include:

• | Two-sided Platform - our platform connecting merchants and consumers enables PayPal to offer unique end-to-end product experiences while gaining valuable insights into customer behavior through our data. Our platform provides for simple digital and mobile transactions (use of an email address, a mobile phone number, or our One Touch product) while being both brand and technology agnostic. |

• | Risk Management - our risk management system and tokenization allows us to keep our customers safer and to process legitimate transactions around the world while preventing illegal, high-risk, or fraudulent transactions. |

• | Brand -PayPal has built a well-recognized and trusted brand and was named one of Interbrand’s best global brands of 2015. |

• | Scale - our global scale gives us impressive reach. As of December 31, 2015, we had 179 million active customer accounts which included 13 million merchants, and in 2015, PayPal processed $282 billion of total payment volume in more than 200 markets around the world. |

• | Regulatory Capability - we believe that our regulatory licenses that give us the ability to operate in markets around the world are a clear advantage and help our business grow. |

• | Financial Strength - the diversity of our funding mix gives us confidence we can continue to grow profitably. Our strong balance sheet, low debt and cash balance allow us to aggressively pursue new opportunities. |

In addition to the discussion in this section, see “Substantial and increasingly intense competition worldwide in the global payments industry may harm our business” in “Item 1A: Risk Factors” below for further discussion of the potential impact of competition on our business.

Revenue Sources

We earn revenues primarily by processing customer transactions on our Payments Platform and from other value added services. Our revenues are classified into the following two categories:

• | Transaction revenues: Net transaction fees charged to consumers and merchants based on the volume of activity processed through our Payments Platform, including our PayPal, PayPal Credit, Venmo, Braintree and Xoom products. |

7

• | Other value added services: Net revenues derived principally from interest and fees earned on our PayPal Credit loans receivable portfolio, subscription fees, gateway fees, gain on sale of participation interest in certain consumer loans receivable, revenue share we earn through partnerships, interest earned on certain PayPal customer account balances, fees earned through our Paydiant products and other services that we provide to consumers and merchants. |

Transaction revenues are generated from fees charged to consumers and merchants on the TPV that we enable. Growth in TPV is also directly impacted by the number of active customer accounts and the payment transactions that we enable on our payments platform. In 2015, transaction revenues generated from customers and merchants on eBay’s marketplace who completed a transaction using our products constituted 26% of our net revenues, down from 29% in 2014. The decline in percentage of revenues generated from eBay buyers and eBay sellers reflects the growth in adoption of PayPal solutions on platforms other than eBay. No other source of revenue represented more than 10% of our revenues.

Our pricing varies among regions and can be modified for individual merchants through customer-specific agreements which provide merchants with financial incentives and other benefits to issue, accept, route, prioritize and promote our branded products and other payment programs. These financial incentives may be based on TPV or other performance-based criteria, such as issuance of new payment products, increased acceptance of our products, launch of new programs, or execution of marketing initiatives.

Protecting Merchants and Consumers

Protecting merchants and consumers from loss is imperative to successfully competing in the payments industry. Trust and security are essential for our customers, and PayPal invests significantly in providing both merchants and consumers with comprehensive protection. The risk to merchants and consumers (and their payments partners) from fraudulent activities, such as account takeover, identity theft and counterparty malicious intent, is growing. Our ability to protect both consumers and merchants is based largely on our ability to leverage the data we collect on transactions and our analytical capabilities. We believe mobile devices will play an important part in the future of commerce, creating the opportunities to make our ecosystem safer. For example, PayPal is able to use location data from mobile devices and growing protection for the mobile operating environment to reduce risk to merchants and consumers.

We enable consumers to make payments safely and simply without sharing sensitive financial information, such as credit card or debit card numbers, with merchants or other consumers. To make payments using PayPal, consumers need to disclose only their email address or mobile phone number to merchants. The account-based nature of our Payments Platform helps us to better detect and prevent fraud when funds enter, flow through and exit the Payments Platform because our transactions are tokenized and because payment authorization credentials are separated from account holder information. Our ongoing investment in systems and processes designed to enhance the safety and security of our products reflects our goal of having PayPal recognized as one of the world’s most trusted payments brands.

We provide merchants and consumers with protection programs on substantially all transactions completed through our Payments Platform, except for transactions using our gateway and Paydiant products. These programs protect both merchants and consumers from loss primarily due to fraud and counterparty non-performance. Our risk management capabilities allow us to provide these protections, which are generally much broader than those protections provided by other participants in the payments industry. Most payments providers do not offer merchant protection in general, and those that do so generally do not provide protection of online or card not present transactions. As a result, merchants may incur losses for chargebacks and other claims on certain transactions when using other payments providers that they would not incur if they had used PayPal’s payments services. PayPal also provides consumer protection against losses on qualifying purchases and accepts claims for 180 days post transaction in the markets that PayPal serves. This protection is generally consistent with, or better than, that offered by other payments providers. We believe that as a result of these programs, consumers can be confident that they will only be required to pay if they receive the product in the condition as described, and merchants can be confident that they will receive payment for the product that they are delivering to the customer.

Our Payments Platform utilizes a combination of proprietary technologies and services as well as technologies and services provided by third parties. We have developed intuitive user interfaces, customer tools and transaction processing, database and network applications that help enable our users to reliably and securely complete transactions on our sites and help our customers to utilize our suite of services. Our technology infrastructure simplifies the storage and processing of large amounts of data, eases the deployment and operation of large-scale global products and services, and automates much of the administration of large-scale clusters of computers. Our technology infrastructure has been designed around industry-standard architectures to reduce downtime in the event of outages or catastrophic occurrences. We strive to continually improve our technology infrastructure to enhance the customer experience and to increase efficiency, scalability, and security.

8

Our Payments Platform’s architecture enables us to connect parties regardless of whether the transaction is occurring at a traditional physical location, online, or through a mobile device. The Payments Platform incorporates multiple layers of protection, both for continuity purposes and to help address cyber-security challenges. We engage in multiple efforts to protect the Payments Platform against these challenges, including regularly testing our systems to address potential vulnerabilities.

Intellectual Property

The protection of our intellectual property, including our trademarks (particularly those covering the PayPal name), patents, copyrights, domain names, trade dress and trade secrets is critical to our success. We aggressively protect our intellectual property rights by relying on applicable laws and regulations in the U.S. and internationally, as well as a variety of administrative procedures. We also rely on contractual restrictions to protect our proprietary rights in products and services. We have routinely entered into confidentiality and invention assignment agreements with our employees and contractors and nondisclosure agreements with parties with whom we conduct business to control access to and limit disclosure of our proprietary information.

We pursue the registration of our domain names, trademarks and service marks in the U.S. and internationally. Additionally, we have filed U.S. and international patent applications covering certain aspects of our proprietary technology. Effective trademark, copyright, patent, domain name, trade dress and trade secret protection is very expensive to maintain and may require litigation and may not be effective in preventing third parties from infringing upon our intellectual property rights. We must protect our intellectual property and other proprietary rights in an increasing number of jurisdictions, a process that is expensive and time consuming and may not be successful.

We have registered our core brands as trademarks and domain names in the U.S. and a large number of other jurisdictions and have in place an active program to continue to secure trademarks and domain names that correspond to our brands in markets of interest.

Government Regulation

Government regulation impacts key aspects of our business. We are subject to regulations that affect the payments industry in the markets we operate.

Payments Regulation. Various laws and regulations govern the payments industry in the U.S. and globally. In the U.S., several of our subsidiaries hold licenses to operate as a money transmitter (or its equivalent), which, among other things, subjects those subsidiaries to reporting requirements, bonding requirements, limitations on the investment of customer funds and inspection by state regulatory agencies. Outside the U.S., we provide localized versions of our service to customers through various foreign subsidiaries. The activities of those non-U.S. entities are, or may, be supervised by a financial regulatory authority in the jurisdictions in which they operate. Among other regulatory authorities, the Luxembourg Commission de Surveillance du Secteur Financier (the “CSSF”), the Australian Securities and Investment Commission, the Monetary Authority of Singapore, the Reserve Bank of India, and the Central Bank of Russia have asserted jurisdiction over some or all of our activities in a particular country. This list is not exhaustive, as there are numerous other regulatory agencies that have or may assert jurisdiction. The laws and regulations applicable to the payments industry in any given jurisdiction are subject to interpretation and change.

Banking Agency Supervision. We serve our customers in the European Union through PayPal (Europe) S.à.r.l. et Cie, SCA, a wholly-owned subsidiary that is licensed and subject to regulation as a bank in Luxembourg by the CSSF. Consequently, we must comply with rules and regulations of the banking industry, including those related to capitalization, funds management, corporate governance, anti-money laundering, disclosure, reporting and inspection. We also are, or may be, subject to banking-related regulations in other countries now or in the future related to our role in the financial industry. In addition, based on our relationships with our partner financial institutions in the U.S., we are subject to indirect regulation and examination by these financial institutions’ regulators.

Consumer Financial Protection Bureau. The Consumer Financial Protection Bureau (the “CFPB”) has significant authority to regulate consumer financial products in the United States, including consumer credit, deposit, payment, and similar products. The CFPB and other similar regulatory agencies in other jurisdictions may have broad consumer protection mandates that could result in the promulgation and interpretation of rules and regulations that may affect our business.

Anti-Money Laundering and Counter Terrorist Financing. PayPal is subject to anti-money laundering (“AML”) laws and regulations in the U.S. and other jurisdictions outside of the U.S., as well as laws designed to prevent the use of the financial systems to facilitate terrorist activities. We have implemented a comprehensive AML program designed to prevent our payment network from being used to facilitate money laundering, terrorist financing, and other illicit activity, or to do business in countries

9

or with persons and entities included on designated country or person lists promulgated by the U.S. Department of the Treasury’s Office of Foreign Assets Controls (“OFAC”) and equivalent authorities in other countries. Our AML compliance program is comprised of policies, procedures and internal controls, including the designation of a compliance officer, and is designed to address these legal and regulatory requirements and assist in managing money laundering and terrorist financing risks.

Interchange Fees. Interchange fees associated with four-party payments systems are being reviewed or challenged in various jurisdictions. For example, in the European Union, the Multilateral Interchange Fee (“MIF”) Regulation (which became effective in December 2015) caps credit and debit interchange fees for cards payments and provides for business rules to be complied with by any company dealing with card transactions, including PayPal. As a result, the fees that we collect in certain jurisdictions may become the subject of regulatory challenge.

Data Protection and Information Security. Aspects of our operations or business are subject to privacy and data protection regulation in the United States, the European Union and elsewhere. For example, in the United States, we are subject to information safeguarding requirements under the Gramm-Leach-Bliley Act that require the maintenance of a written, comprehensive information security program and in Europe, the operations of our Luxembourg bank are subject to information safeguarding requirements under the Luxembourg Banking Act, among other laws. Regulatory authorities around the world are considering numerous legislative and regulatory proposals concerning privacy and data protection. In addition, the interpretation and application of these privacy and data protection laws in the United States, Europe and elsewhere are often uncertain and in a state of flux.

Anti-Corruption. PayPal is subject to applicable anti-corruption laws, such as the U.S. Foreign Corrupt Practices Act and the U.K. Bribery Act, in the jurisdictions in which it operates. Anti-corruption laws generally prohibit offering, promising, giving, or authorizing others to give anything of value, either directly or indirectly, to a government official or private party in order to influence official action or otherwise gain an unfair business advantage, such as to obtain or retain business. We have implemented policies, procedures, and internal controls that are designed to comply with these laws and regulations.

Additional Regulatory Developments. Various regulatory agencies also continue to examine a wide variety of issues, including virtual currencies, identity theft, account management guidelines, privacy, disclosure rules, security and marketing that would impact PayPal.

For an additional discussion on governmental regulation affecting our business, please see the risk factors related to regulation of our payments business and regulation in the areas of consumer privacy, data use and/or security in “Item 1A: Risk Factors -Risk Factors That May Affect Our Business, Results of Operations and Financial Condition” and Item 3: Legal Proceedings" included elsewhere in this Annual Report on Form 10-K.

Seasonality

The Company does not experience meaningful seasonality. No individual quarter in 2015, 2014 or 2013 accounted for more than 30% of net revenue.

Research and Development

Total research and development expense was $947 million, $890 million and $727 million in 2015, 2014 and 2013, respectively.

Financial Information About Segments

See “Note 10—Segment and Geographical Information” to the combined and consolidated financial statements included in this Annual Report on Form 10-K for certain financial information about segments. Additionally, please see the information in "Item 1A: Risk Factors" under the caption "Our international operations are subject to increased risks, which could harm our business," which describes risks associated with the foreign operations of segments.

10

Employees

As of December 31, 2015, we employed approximately 16,800 people globally, of whom approximately 9,800 were located in the U.S. We consider our relationship with employees to be good.

Separation from eBay Inc.

PayPal Holdings, Inc. was incorporated in Delaware in January 2015 for the purpose of owning and operating eBay’s Payments business in connection with the separation and distribution described below. Prior to the contribution of this business to PayPal Holdings, Inc., which occurred prior to the distribution in July 2015, PayPal Holdings, Inc. had no operations. On July 17, 2015 (the “distribution date”), PayPal became an independent publicly-traded company through the pro rata distribution by eBay of 100% of the outstanding common stock of PayPal to eBay stockholders (which we refer to as the “separation” or the “distribution”). Each eBay stockholder of record as of the close of business on July 8, 2015 received one share of PayPal common stock for every share of eBay common stock held on the record date. Approximately 1.2 billion shares of PayPal common stock were distributed on July 17, 2015 to eBay stockholders. PayPal’s common stock began “regular way” trading under the ticker symbol “PYPL” on The NASDAQ Stock Market on July 20, 2015. Prior to the separation, eBay transferred substantially all of the assets and liabilities and operations of eBay’s payments business to PayPal, which was completed in June 2015.

Available Information

The address of our principal executive offices is PayPal Holdings, Inc., 2211 North First Street, San Jose, California 95131 and our telephone number is (408) 967-1000. We maintain an Internet site at www.paypal.com, and our investor relations site at http://investor.paypal-corp.com. From time to time, we may use our investor relations site and other online and social media channels, including our PayPal Stories Blog, Twitter handle and LinkedIn page to disclose material non-public information and comply with our disclosure obligations under Regulation FD. Our Annual Report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and amendments to those reports are available, without charge, for review on our investor relations site as soon as reasonably practicable after they are electronically filed with, or furnished to, the SEC. The content of our websites and information that we may post on or provide to online and social media channels, including those mentioned above, is not incorporated by reference into this Annual Report on Form 10-K or in any other report or document we file with the SEC, and any references to our websites are intended to be inactive textual references only.

11

ITEM 1A. RISK FACTORS

The following discussion is divided into three sections. The first section, which begins immediately following this paragraph, discusses some of the risks that may affect our business, results of operations and financial condition. The second section, captioned “Risks Related to the Separation and Our Operation as an Independent Publicly Traded Company,” discusses some of the risks relating to our separation into an independent publicly traded company. The third section, captioned “Risks Related to Our Common Stock,” discusses some of the risks relating to an investment in our Common Stock. You should carefully review all of these sections, as well as our combined and consolidated financial statements and notes thereto and the other information appearing in this report, for important information regarding risks that affect us.

Risk Factors That May Affect Our Business, Results of Operations and Financial Condition

Substantial and increasingly intense competition worldwide in the global payments industry may harm our business.

The global payments industry is highly competitive. We compete against businesses in varied industries, many of which are larger than we are, have a dominant and secure position in other industries, or offer other goods and services to consumers and merchants which we do not offer. As online and offline commerce are increasingly converging, the pace of change, innovation and disruption is also increasing. The global payments industry is rapidly changing, highly innovative and increasingly subject to regulatory scrutiny, which may negatively affect the competitive landscape. We compete against a wide range of businesses with varying roles in all forms of payments, including:

• | paper-based transactions (principally cash and checks); |

• | providers of traditional payment methods, particularly credit and debit cards, and Automated Clearing House transactions (in particular, well-established banks); |

• | payment networks which facilitate payments for credit card users; |

• | providers of “digital wallets” which offer customers the ability to pay online and/or on mobile devices through a variety of payment methods, including with mobile applications, through contactless payments, and with a variety of payment cards (these providers include Visa, MasterCard, American Express, Amazon.com, Wal-Mart, the Merchant Customer Exchange (MCX) initiative supported by major U.S. retailers, Apple, Google, and others); |

• | providers of mobile payments solutions that use tokenized card data approaches and Near Field Communication (NFC) functionality (e.g., Apple's mobile Apple Pay) or Host Card Emulation (HCE) functionality to eliminate the need for access to the physical secure element in the device (e.g., Google's Android solution); |

• | payment-card processors that offer their services to merchants, including for “card on file” payments where the merchant invites the consumer to select a payment method for their first transaction, and subsequently uses the same payment method for subsequent transactions; |

• | providers of “person-to-person” payments that facilitate individuals sending money with an email address or mobile phone number, such as Facebook messaging payments, Google and many banks; |

• | merchants and merchant associations providing proprietary payment networks to facilitate payments within their own retail network, such as Wal-Mart; |

• | money remitters, such as MoneyGram, Western Union, Global Payments, Inc. and Euronet; and |

• | providers of card readers for mobile devices and of other point-of-sale and multi-channel technologies. |

We often partner with many of these businesses.

We also face competition and potential competition from:

• | services that provide online merchants the ability to offer their customers the option of paying for purchases from their bank account or paying on credit in the United States and abroad; |

• | issuers of stored value targeted at online payments; |

• | other international online payment-services providers; |

• | other providers of online account-based payments; |

• | payment services targeting users of social networks and online gaming, including those offering billing to the consumer’s mobile phone account; |

• | mobile payment services between bank accounts; |

• | payment services enabling banks to offer their online banking customers the ability to send and receive payments through their bank account; |

• | online shopping services that provide special offers linked to a specific payment provider; and |

• | services that help merchants accept and manage virtual currencies. |

12

Some of these payment providers have greater customer bases, volume, scale, resources, and market share than we do, which may provide significant competitive advantages. Some of our competitors may also be subject to less burdensome licensing, anti-money laundering, counter-terrorist financing, and other regulatory requirements. They may devote greater resources to the development, promotion, and sale of products and services, and they may offer lower prices or more effectively introduce their own innovative programs and services that adversely impact our growth. We also expect new entrants, as well as established banks and other financial institutions that do not currently offer online payments, to offer competitive products and services in the future. In addition, some merchants provide such services for themselves. Competing services tied to established banks and other financial institutions may engender greater consumer confidence in the safety and efficacy of their services. In certain countries, such as Germany, Netherlands and Australia, electronic funds transfer is a leading method of payment for both online and offline transactions with which our products compete.

We compete primarily on the basis of the following:

• | ability to attract, retain and engage both merchants and consumers; |

• | ability to show that merchants will achieve incremental sales by offering our PayPal services; |

• | security of transactions and the ability for consumers to use our PayPal products and services without sharing their financial information with the merchant or the party they are paying; |

• | simplicity of our fee structure; |

• | ability to develop services across multiple commerce channels, including mobile payments and payments at the retail point of sale; |

• | trust in our dispute resolution and buyer and seller protection programs; |

• | customer service; |

• | brand recognition; |

• | website, mobile platform and application onboarding, ease-of-use and accessibility; |

• | system reliability and data security; |

• | ease and quality of integration into third-party mobile applications and operating systems; and |

• | quality of developer tools, such as our application programming interfaces and software development kits. |

If we are not able to differentiate our business from those of our competitors, drive value for our customers, or effectively align our resources with our goals and objectives, we may not be able to compete effectively against our competitors. Our failure to compete effectively against any of the foregoing competitive threats could materially and adversely harm our business.

Our operating and financial results come primarily from transactions involving payments made in a reporting period and are therefore subject to fluctuations that could adversely affect our business, financial condition, results of operations and cash flows, as well as the trading price of our common stock.

Our operating and financial results have varied on a quarterly basis during our operating history and may continue to fluctuate significantly as a result of a variety of factors, including as a result of the risks set forth in this “Risk Factors” section. It is difficult for us to forecast the level or source of our revenues or earnings (loss) accurately. In view of the rapidly evolving nature of our business, period-to-period comparisons of our operating results may not be meaningful, and you should not rely upon them as an indication of future performance. We do not have a backlog, and substantially all of our net revenues each quarter come primarily from transactions involving payments during that quarter. Due to the inherent difficulty in forecasting revenues, it is also difficult to forecast expenses as a percentage of net revenues. Quarterly and annual expenses as a percentage of net revenues reflected in our financial statements may be significantly different from historical or projected rates. Our operating results in one or more future quarters may fall below the expectations of securities analysts and investors. The trading price of our common stock could decline, perhaps substantially, as a result of the factors described in this paragraph.

Global and regional economic conditions could harm our business.

Our operations and performance depend significantly on global and regional economic conditions. Adverse economic conditions and events have negatively impacted regional and global financial markets in the past and will likely continue to do so from time to time in the future. These events and conditions could have a negative and adverse impact on the companies and customers with which we do business. In addition, financial turmoil affecting the banking system or financial markets could cause additional consolidation of the financial services industry, significant financial service institution failures, new or incremental tightening in the credit markets, low liquidity, and extreme volatility or distress in the fixed income, credit, currency, and equity markets. Adverse impacts to the companies and customers with which we do business, the banking system, or financial markets could have a material adverse effect on our business, including a reduction in the volume and prices of transactions on our payments platforms.

13

If we cannot keep pace with rapid technological developments, particularly developments with respect to mobile payments, to provide new and innovative programs, products and services, the use of our products and our revenues could decline.

Rapid, significant, and disruptive technological changes continue to impact the industries in which we operate, including developments in payment card tokenization, ecommerce (e.g., social commerce), mobile, virtual currencies and near field communication and other proximity payment devices, such as contactless payments. We cannot predict the effects of technological changes on our business. In addition to our own initiatives and innovations, we rely in part on third parties, including some of our competitors, for the development of and access to new technologies. We expect that new services and technologies applicable to the industries in which we operate will continue to emerge, which may be superior to, or render obsolete, the technologies we currently use in our products and services. Developing and incorporating new technologies into our products and services may require substantial expenditures, take considerable time, and ultimately may not be successful. In addition, our ability to adopt new services and develop new technologies may be inhibited by industry-wide standards, payments networks, new laws and regulations, resistance to change from consumers or merchants, or third-party intellectual property rights. Our success will depend on our ability to develop and incorporate new technologies and adapt to technological changes and evolving industry standards; if we are unable to do so in a timely or cost-effective manner, our business could be harmed.

For example, mobile devices are increasingly used for ecommerce transactions and payments, and a significant and growing portion of our customers access our Payments Platform through mobile devices. We may lose customers if we are not able to continue to meet our customers’ mobile and multi-screen experience expectations. The variety of technical and other configurations across different mobile devices and platforms increases the challenges associated with this environment. In addition, a number of other companies with significant resources and a number of innovative startups have introduced products and services focusing on mobile markets. Our ability to successfully address the challenges posed by the rapidly evolving market for mobile transactions is crucial to our continued success, and any failure to continue to increase the volume of mobile transactions effected through our Payments Platform could harm our business.

Changes in how consumers fund their PayPal transactions could harm our business.

We pay significant transaction fees when consumers fund payment transactions using credit cards, lower fees when consumers fund payments with debit cards, nominal fees when consumers fund payment transactions by electronic transfer of funds from bank accounts, and nominal fees when consumers fund payment transactions from an existing PayPal account balance or through our PayPal Credit products. Our financial success is highly sensitive to changes in the rate at which our consumers fund payments using credit and debit cards (collectively, “payment cards”), which can significantly increase our costs. Some of our consumers may prefer to use payment cards, especially if these payment cards offer functionality and benefits not associated with the use of their bank accounts. Some of our offerings, including the ability of consumers to make a limited number of “guest” payments without opening a PayPal account, have a higher rate of payment card funding than our basic product offering. An increase in the portion of our payment volume funded using payment cards or in fees associated with our funding mix, or other events or developments that make it more difficult or costly for us to fund transactions by electronic transfer of funds from bank accounts or existing PayPal account balances, could materially and adversely affect our financial performance and significantly harm our business. Some of our plans to lower our funding costs, including our PayPal Credit products and enabling consumers to defer payment for a short period of time on some transactions, may increase the risk to us of nonpayment by consumers.

Our business is subject to cyberattacks and security and privacy breaches.

Our business involves the collection, storage, processing and transmission of customers’ personal data, including financial information. In addition, a significant number of our customers authorize us to bill their payment card or bank accounts directly for all transaction and other fees charged by us. We have built our reputation on the premise that our Payments Platform offers customers a secure way to make payments. An increasing number of organizations, including large on-line and off-line merchants and businesses, other large Internet companies, financial institutions, and government institutions, have disclosed breaches of their information security systems, some of which have involved sophisticated and highly targeted attacks, including on portions of their websites or infrastructure. For example, in May 2014, eBay Inc. publicly announced that criminals were able to penetrate and steal certain data, including user names, encrypted user passwords and other non-financial user data, from certain of eBay's Marketplaces business unit databases, which led to eBay Marketplaces requiring a password reset and fewer eBay Marketplaces transactions using our PayPal services.

The techniques used to obtain unauthorized, improper or illegal access to our systems, our data or customers' data, disable or degrade service, or sabotage systems are constantly evolving, may be difficult to detect quickly, and often are not recognized until launched against a target. Unauthorized parties may attempt to gain access to our systems or facilities through various means, including, among others, hacking into the systems or facilities of us or our partners or customers, or attempting to fraudulently

14

induce our employees, partners, customers or others into disclosing user names, passwords, payment card information, or other sensitive information, which may in turn be used to access our information technology systems. Certain efforts may be state-sponsored and supported by significant financial and technological resources, making them even more difficult to detect. As a result of our prominence, we believe that we are a particularly attractive target for such breaches and attacks. Although we have developed systems and processes that are designed to protect our data and customer data and to prevent data loss and other security breaches, and expect to expend significant additional resources to bolster these protections, these security measures cannot provide absolute security, Our information technology and infrastructure may be vulnerable to cyberattacks or security breaches, and third parties may be able to access our customers’ personal or proprietary information and payment card data that are stored on or accessible through those systems. Our security measures may also be breached due to employee error, malfeasance, system errors or vulnerabilities, or other irregularities. Any actual or perceived breach of our security could interrupt our operations; result in our systems or services being unavailable; result in improper disclosure of data; materially harm our reputation and brand; result in significant legal and financial exposure; lead to loss of customer confidence in, or decreased use of, our products and services; and adversely affect our business and results of operations. Any breaches of network or data security at our partners or customers could have similar effects. In addition, our customers could have vulnerabilities on their own computer systems that are entirely unrelated to our systems, but could mistakenly attribute their own vulnerabilities to PayPal.

In addition, under payment card rules and our contracts with our card processors, if there is a breach of payment card information that we store, or that is stored by our direct payment card processing customers, we could be liable to the payment card issuing banks for their cost of issuing new cards and related expenses. We also expect to expend significant additional resources to protect against security or privacy breaches, and may be required to redress problems caused by breaches. Among other reasons, financial services regulators in various jurisdictions, including the United States and the European Union, have implemented or are considering proposals to impose new authentication requirements on banks and payment processors intended to reduce online fraud, which could impose significant costs, require us to change our business practices, make it more difficult for new customers to join PayPal, and reduce the ease of use of our products, which could harm our business. Additionally, our insurance policies carry low coverage limits, which may not be adequate to reimburse us for losses caused by security breaches, and we may not be able to collect fully, if at all, under these insurance policies.

Systems failures and resulting interruptions in the availability of our websites, applications, products or services could harm our business.

Our systems may experience service interruptions or degradation because of hardware and software defects or malfunctions, computer denial-of-service and other cyberattacks, human error, earthquakes, hurricanes, floods, fires, natural disasters, power losses, disruptions in telecommunications services, fraud, military or political conflicts, terrorist attacks, computer viruses or other malware, or other events. Our systems also may be subject to break-ins, sabotage and intentional acts of vandalism. Some of our systems are not fully redundant, and our disaster recovery planning may not be sufficient for all eventualities. In addition, as a provider of payments solutions, we are subject to increased scrutiny by regulators that may require specific business continuity, resiliency and disaster recovery plans and more rigorous testing of such plans. This increased scrutiny may be costly and time-consuming and may divert our resources from other business priorities.

We have experienced and will likely continue to experience system failures, denial of service attacks and other events or conditions from time to time that interrupt the availability or reduce or affect the speed or functionality of our products and services. These events have resulted and likely will result in loss of revenue. A prolonged interruption in the availability or reduction in the availability, speed or other functionality of our products and services could materially harm our business. Frequent or persistent interruptions in our services could cause current or potential customers to believe that our systems are unreliable, leading them to switch to our competitors or to avoid our products and services, and could permanently harm our reputation and brands. Moreover, to the extent that any system failure or similar event results in damages to our customers or their businesses, these customers could seek significant compensation or contractual penalties from us for their losses and those claims, even if unsuccessful, would likely be time-consuming and costly for us to address, and could have other consequences described in this “Risk Factors” section under the caption “Our business is subject to cyberattacks and security and privacy breaches.”

Our Payments Platform has suffered significant intermittent unavailability. Reliability is particularly critical for us because the full-time availability of our PayPal products and services is critical to our goal of gaining widespread acceptance among consumers and merchants for digital and mobile payments. We have undertaken certain system upgrades and re-platforming efforts designed to improve our reliability and speed. These efforts are costly and time-consuming, involve significant technical risk and may divert our resources from new features and products, and there can be no guarantee that these efforts will succeed. Because we are a regulated financial institution in certain jurisdictions, frequent or persistent site interruptions could lead to regulatory scrutiny, significant fines and penalties, and mandatory and costly changes to our business practices, and ultimately could cause us to lose

15

existing licenses that we need to operate or prevent or delay us from obtaining additional licenses that we need to expand our business.

We also rely on facilities, components and services supplied by third parties, including eBay, and our business may be materially adversely affected to the extent these components or services do not meet our expectations or these third parties cease to provide the services or facilities. We do not carry business interruption insurance sufficient to compensate us for all losses that may result from interruptions in our service as a result of systems failures and similar events.

Changes to payment card networks or bank fees, rules, or practices could harm our business.

We do not directly access the payment card networks, such as Visa and MasterCard, that enable our acceptance of credit cards and debit cards, including some types of prepaid cards. Accordingly, we must rely on banks or other payment processors to process transactions and must pay fees for the services. From time to time, payment card networks have increased, and may increase in the future, the interchange fees and assessments that they charge for each transaction which accesses their networks. Our payment card processors may have the right to pass any increases in interchange fees and assessments on to us as well as increase their own fees for processing. Any changes in interchange fees and assessments could increase our operating costs and reduce our operating income.

In addition, in some jurisdictions, governments have required Visa and MasterCard to reduce interchange fees, or have opened investigations as to whether Visa’s or MasterCard’s interchange fees and practices violate antitrust law. In the United States, the Federal Reserve Board issued a final rule capping debit card interchange fees at significantly lower rates than Visa or MasterCard previously charged. In the European Union, the Multilateral Interchange Fee (“MIF”) Regulation limits credit and debit interchange fees for payments and imposes business rules on card processing services. Any material reduction in credit or debit card interchange rates in the United States or other markets could adversely affect our competitive position against traditional credit and debit card service providers, and may subject us to pricing pressure, although it would also lower our costs. Future changes to those regulations could potentially adversely affect our business.

We are required by our processors to comply with payment card network operating rules, including special operating rules for payment service providers to merchants, and we have agreed to reimburse our processors for any fines they are assessed by payment card networks as a result of any rule violations by us or our merchants. The payment card networks set and interpret the card operating rules. From time to time, the networks have alleged that various aspects of our business model violate these operating rules. If such allegations are not resolved, they may result in material fines and penalties or require changes in our business practices that may be costly. The payment card networks could adopt new operating rules or interpret or re-interpret existing rules that we or our processors might find difficult or even impossible to follow, or costly to implement. As a result, we could lose our ability to give consumers the option of using payment cards to fund their payments or the choice of currency in which they would like their payment card to be charged. If we are unable to accept payment cards or are meaningfully limited in our ability to do so, our business would be adversely affected.