UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM

QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the quarterly period

ended

Commission file number

(Exact name of registrant as specified in its charter)

| (State or other jurisdiction of | (I.R.S. Employer | |

| incorporation or organization) | Identification No.) |

Beijing, People’s Republic of | ||

| (Address of principal executive offices) | (Zip Code) |

| (Registrant’s telephone number, including area code) |

N/A

(Former name, former address and former fiscal year, if changed since last report)

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol | Name of each exchange on which registered | ||

Indicate by check mark whether the registrant

(1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12

months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements

for the past 90 days.

Indicate by check mark whether the registrant

has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405

of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| ☐ | Large accelerated filer | ☐ | Accelerated filer |

| ☒ | Smaller reporting company | ||

| Emerging growth company |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant

is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No

As of May 12 , 2023,

DATASEA INC.

TABLE OF CONTENTS

| Page No. | ||

| Part I - Financial Information | ||

| Item 1 | Financial Statements | 1 |

| Item 2 | Management’s Discussion and Analysis of Financial Condition and Results of Operations | 25 |

| Item 3 | Quantitative and Qualitative Disclosures about Market Risk | 46 |

| Item 4 | Controls and Procedures | 46 |

| Part II - Other Information | ||

| Item 1 | Legal Proceedings | 48 |

| Item 1A | Risk Factors | 48 |

| Item 2 | Unregistered Sales of Equity Securities and Use of Proceeds | 48 |

| Item 3 | Defaults Upon Senior Securities | 48 |

| Item 4 | Mine Safety Disclosures | 48 |

| Item 5 | Other Information | 48 |

| Item 6 | Exhibits | 48 |

i

PART I - FINANCIAL INFORMATION

DATASEA INC.

CONSOLIDATED BALANCE SHEETS

| MARCH 31, 2023 (UNAUDITED) | JUNE 30, 2022 | |||||||

| ASSETS | ||||||||

| CURRENT ASSETS | ||||||||

| Cash | $ | $ | ||||||

| Accounts receivable | ||||||||

| Inventory, net | ||||||||

| Value-added tax prepayment | ||||||||

| Prepaid expenses and other current assets | ||||||||

| Right-of-use assets, net | - | |||||||

| Total current assets | ||||||||

| NONCURRENT ASSETS | ||||||||

| Security deposit for rents | ||||||||

| Long-term investment | ||||||||

| Property and equipment, net | ||||||||

| Intangible assets, net | ||||||||

| Right-of-use assets, net | - | |||||||

| Total noncurrent assets | ||||||||

| TOTAL ASSETS | $ | $ | ||||||

| LIABILITIES AND STOCKHOLDERS’ EQUITY | ||||||||

| CURRENT LIABILITIES | ||||||||

| Accounts payable | $ | $ | ||||||

| Unearned revenue | ||||||||

| Accrued expenses and other payables | ||||||||

| Due to related party | ||||||||

| Loan payables - current | ||||||||

| Operating lease liabilities | ||||||||

| Total current liabilities | ||||||||

| NONCURRENT LIABILITIES | ||||||||

| Operating lease liabilities | ||||||||

| Loan payables - non-current | ||||||||

| Total noncurrent liabilities | ||||||||

| TOTAL LIABILITIES | ||||||||

| COMMITMENTS AND CONTINGENCIES | ||||||||

| STOCKHOLDERS’ EQUITY | ||||||||

| Common stock, $ | ||||||||

| Additional paid-in capital | ||||||||

| Accumulated comprehensive income | ||||||||

| Accumulated deficit | ( | ) | ( | ) | ||||

| TOTAL COMPANY STOCKHOLDERS’ EQUITY (DEFICIT) | ( | ) | ||||||

| Noncontrolling interest | ( | ) | ( | ) | ||||

| TOTAL EQUITY (DEFICIT) | ( | ) | ||||||

| TOTAL LIABILITIES AND EQUITY (DEFICIT) | $ | $ | ||||||

The accompanying notes are an integral part of these consolidated financial statements.

1

DATASEA INC.

CONSOLIDATED STATEMENTS OF OPERATIONS AND COMPREHENSIVE LOSS

(UNAUDITED)

| NINE MONTHS ENDED MARCH 31, | THREE MONTHS ENDED DECEMBER 31, | |||||||||||||||

| 2023 | 2022 | 2022 | 2021 | |||||||||||||

| Revenues | $ | $ | $ | $ | ||||||||||||

| Cost of goods sold | ||||||||||||||||

| Gross profit | ||||||||||||||||

| Operating expenses | ||||||||||||||||

| Selling | ||||||||||||||||

| General and administrative | ||||||||||||||||

| Research and development | ||||||||||||||||

| Total operating expenses | ||||||||||||||||

| Loss from operations | ( | ) | ( | ) | ( | ) | ( | ) | ||||||||

| Non-operating income (expenses) | ||||||||||||||||

| Other income (expense) | ( | ) | ||||||||||||||

| Interest income | ||||||||||||||||

| Total non-operating income (expenses), net | ( | ) | ||||||||||||||

| Loss before income tax | ( | ) | ( | ) | ( | ) | ( | ) | ||||||||

| Income tax | - | - | ||||||||||||||

| Loss before noncontrolling interest | ( | ) | ( | ) | ( | ) | ( | ) | ||||||||

| Less: (loss) income attributable to noncontrolling interest | ( | ) | ( | ) | ( | ) | ||||||||||

| Net loss to the Company | ( | ) | ( | ) | ( | ) | ( | ) | ||||||||

| Other comprehensive item | ||||||||||||||||

| Foreign currency translation gain (loss) attributable to the Company | ( | ) | ( | ) | ||||||||||||

| Foreign currency translation gain (loss) attributable to noncontrolling interest | ( | ) | ||||||||||||||

| Comprehensive loss attributable to the Company | $ | ( | ) | $ | ( | ) | $ | ( | ) | $ | ( | ) | ||||

| Comprehensive (loss) income attributable to noncontrolling interest | $ | ( | ) | $ | ( | ) | $ | $ | ||||||||

| $ | ( | ) | $ | ( | ) | $ | ( | ) | $ | ( | ) | |||||

The accompanying notes are an integral part of these consolidated financial statements.

2

DATASEA INC.

CONSOLIDATED STATEMENTS OF CHANGES IN STOCKHOLDERS’ EQUITY (DEFICIENCY)

NINE AND THREE MONTHS ENDED MARCH 31, 2023 AND 2022

(UNAUDITED)

| Accumulated | ||||||||||||||||||||||||||||

| Additional | other | |||||||||||||||||||||||||||

| Common Stock | paid-in | Accumulated | comprehensive | Noncontrolling | ||||||||||||||||||||||||

| Shares | Amount | capital | deficit | income | Total | interest | ||||||||||||||||||||||

| Balance at July 1, 2022 | $ | $ | $ | ( | ) | $ | $ | $ | ( | ) | ||||||||||||||||||

| Net loss for the period | - | ( | ) | ( | ) | ( | ) | |||||||||||||||||||||

| Stock compensation expense | - | |||||||||||||||||||||||||||

| Foreign currency translation gain (loss) | - | ( | ) | |||||||||||||||||||||||||

| Balance at September 30, 2022 | ( | ) | ( | ) | ||||||||||||||||||||||||

| Net loss for the period | - | ( | ) | ( | ) | ( | ) | |||||||||||||||||||||

| Stock compensation expense | - | |||||||||||||||||||||||||||

| Purchase of minority interest ownership | - | ( | ) | ( | ) | |||||||||||||||||||||||

| Foreign currency translation loss (gain) | - | ( | ) | ( | ) | |||||||||||||||||||||||

| Balance at December 31, 2022 | ( | ) | ( | ) | ( | ) | ||||||||||||||||||||||

| Net loss for the period | - | - | - | ( | ) | - | ( | ) | ( | ) | ||||||||||||||||||

| Stock compensation expense | - | - | - | - | - | |||||||||||||||||||||||

| Foreign currency translation (loss) gain | - | - | - | - | ( | ) | ( | ) | ||||||||||||||||||||

| Balance at March 31, 2023 | $ | $ | $ | ( | ) | $ | $ | ( | ) | $ | ( | ) | ||||||||||||||||

| Balance at July 1, 2021 | $ | $ | $ | ( | ) | $ | $ | $ | ( | ) | ||||||||||||||||||

| Net loss for the period | - | ( | ) | ( | ) | ( | ) | |||||||||||||||||||||

| Issuance of common stock for equity financing | ||||||||||||||||||||||||||||

| Shares issued for stock compensation expense | ||||||||||||||||||||||||||||

| Foreign currency translation loss | - | ( | ) | ( | ) | ( | ) | |||||||||||||||||||||

| Balance at September 30, 2021 | ( | ) | ( | ) | ||||||||||||||||||||||||

| Net loss for the period | - | ( | ) | ( | ) | ( | ) | |||||||||||||||||||||

| Stock compensation expense | ||||||||||||||||||||||||||||

| Foreign currency translation gain | - | |||||||||||||||||||||||||||

| Capital contribution to Shuhai Beijing from a major shareholder | - | |||||||||||||||||||||||||||

| Shares issued for paying officers’ accrued salary | ||||||||||||||||||||||||||||

| Balance at December 31, 2021 | ( | ) | ( | ) | ||||||||||||||||||||||||

| Net loss for the period | - | - | - | ( | ) | - | ( | ) | ||||||||||||||||||||

| Stock compensation expense | - | - | - | - | - | |||||||||||||||||||||||

| Foreign currency translation gain (loss) | - | ( | ) | |||||||||||||||||||||||||

| Balance at March 31, 2022 | $ | $ | $ | ( | ) | $ | $ | $ | ( | ) | ||||||||||||||||||

The accompanying notes are an integral part of these consolidated financial statements.

3

DATASEA INC.

CONSOLIDATED STATEMENTS OF CASH FLOWS

(UNAUDITED)

| NINE MONTHS ENDED MARCH 31 | ||||||||

| 2023 | 2022 | |||||||

| Cash flows from operating activities: | ||||||||

| Loss including noncontrolling interest | $ | ( | ) | $ | ( | ) | ||

| Adjustments to reconcile loss including noncontrolling interest to net cash used in operating activities: | ||||||||

| Loss (gain) on disposal on fixed assets | ( | ) | ||||||

| Depreciation and amortization | ||||||||

| Bad debt expense(reversal) | ( | ) | ||||||

| Operating lease expense | ||||||||

| Stock compensation expense | ||||||||

| Changes in assets and liabilities: | ||||||||

| Accounts receivable | ( | ) | ( | ) | ||||

| Inventory | ( | ) | ( | ) | ||||

| Value-added tax prepayment | ( | ) | ||||||

| Prepaid expenses and other current assets | ( | ) | ||||||

| Accounts payable | ||||||||

| Unearned revenue | ( | ) | ||||||

| Accrued expenses and other payables | ||||||||

| Payment on operating lease liabilities | ( | ) | ( | ) | ||||

| Net cash used in operating activities | ( | ) | ( | ) | ||||

| Cash flows from investing activities: | ||||||||

| Acquisition of property and equipment | ( | ) | ( | ) | ||||

| Cash received from disposal of fixed assets | - | |||||||

| Acquisition of intangible assets | ( | ) | ( | ) | ||||

| Long-term investment | ( | ) | ( | ) | ||||

| Net cash used in investing activities | ( | ) | ( | ) | ||||

| Cash flows from financing activities: | ||||||||

| Due to related parties | ( | ) | ||||||

| Proceeds (repayment) of loan payables | ( | ) | ||||||

| Proceeds from capital contribution from a major shareholder | ||||||||

| Net proceeds from issuance of common stock | ||||||||

| Net cash provided by financing activities | ||||||||

| Effect of exchange rate changes on cash | ( | ) | ||||||

| Net increase (decrease) in cash | ( | ) | ||||||

| Cash, beginning of period | ||||||||

| Cash, end of period | $ | $ | ||||||

| Supplemental disclosures of cash flow information: | ||||||||

| Cash paid for interest | $ | $ | ||||||

| Cash paid for income tax | $ | $ | ||||||

| Supplemental disclosures of non-cash operating, investing and financing activities: | ||||||||

| Right-of-use assets obtained in exchange for operating lease liabilities | $ | $ | ||||||

| Transfer of prepaid software development expenditure to intangible assets | $ | $ | ||||||

| Shares issued for accrued bonus to officers | $ | $ | ||||||

The accompanying notes are an integral part of these consolidated financial statements.

4

DATASEA INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

MARCH 31, 2023 (UNAUDITED) AND JUNE 30, 2022

NOTE 1 – ORGANIZATION AND DESCRIPTION OF BUSINESS

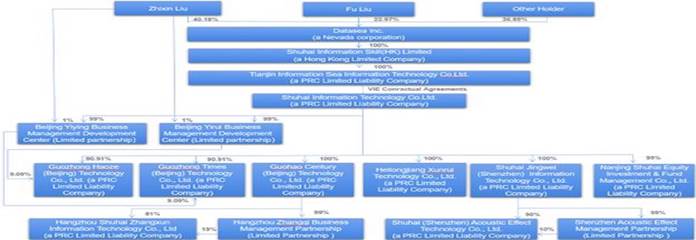

Datasea Inc. (the “Company”, or “we”,

“us”, “our” or similar terminology) was incorporated in the State of Nevada on September 26, 2014 under the name

Rose Rock Inc. and changed its name to Datasea Inc. on May 27, 2015. On May 26, 2015, the Company’s founder, Xingzhong Sun, sold

On October 29, 2015,

Following the Share Exchange, the Shareholders,

Zhixin Liu and her father, Fu Liu, owned approximately

After the Share Exchange, the Company, through its consolidated subsidiaries and VIE provide smart security solutions primarily to schools, tourist or scenic attractions and public communities in China.

On October 16, 2019, Shuhai Beijing incorporated a wholly owned subsidiary, Heilongjiang Xunrui Technology Co. Ltd. (“Xunrui”), which develops and markets the Company’s smart security system products.

On December 3, 2019, Shuhai Beijing formed Nanjing

Shuhai Equity Investment Fund Management Co. Ltd. (“Shuhai Nanjing”), a joint venture in PRC, in which Shuhai Beijing holds

a

In January 2020, the Company acquired ownership in three entities for no consideration from the Company’s management, which set up such entities on the Company’s behalf (described below).

On January 3, 2020, Shuhai Beijing entered into

two equity transfer agreements (the “Transfer Agreements”) with the President, and a Director of the Company.

5

On January 7, 2020, Shuhai Beijing entered into

another equity transfer agreement with the President, the Director described above and an unrelated individual.

On August 17, 2020, Beijing Shuhai formed a new wholly-owned subsidiary Shuhai Jingwei (Shenzhen) Information Technology Co., Ltd (“Jingwei”), to expand the security oriented systems developing, consulting and marketing business overseas.

On November 16, 2020, Guohao Century formed Hangzhou

Zhangqi Business Management Limited Partnership (“Zhangqi”) with ownership of

On November 19, 2020, Guohao Century formed a

On February 16, 2022, Shuhai Jingwei formed Shenzhen

Acoustic Effect Management Limited Partnership (“Shenzhen Acoustic MP”) with

On February 16, 2022, Shuhai Jingwei formed Shuhai

(Shenzhen) Acoustic Effect Technology Co., Ltd (“Shuhai Shenzhen Acoustic Effect”), a PRC Company, in which Shuhai Jingwei

holds

On March 4, 2022, Shuhai Beijing formed Beijing

Yirui Business Management Development Center (“Yirui”) with

On March 4, 2022, Shuhai Beijing formed Beijing

Yiying Business Management Development Center (“Yiying”) with

Impact of Coronavirus Outbreak

In December 7 2022, the joint prevention and control mechanism of the State Council of China issued a notice, announcing ten targeted measures to further optimize epidemic prevention and control (hereinafter referred to as the ” New Ten Rules”). This is a major adjustment made by the Chinese authorities to the previous epidemic control policy. Later, Beijing, Shanghai, Chongqing, Guangzhou and other cities in China announced the follow-up implementation of the “New Ten Rules”. The introduction of the New Ten Rules announced that China’s previous “dynamic zero” epidemic prevention policy had officially come to an end. So far, except for some special medical key places, people do not need to provide nucleic acid test negative reports when traveling. During the period when the new policy was introduced, the number of COVID-19 cases in China has increased significantly, and people’s focus on COVID-19 has shifted from pre protection to better indoor living environment to avoid repeated infection.

6

Facing challenges that are also opportunities, the needs for air sterilization has likely become a permanent way of life for many and will likely continue into common. Datasea has developed five models Air Sterilizers under its in-house advanced acoustic intelligence technology, to target public and private application scenarios such as hospitals, airport, logistic warehouse, cold chain transportation and home care. In 3rd December 2022, the Company unveiled national Hailijia air sterilizer product campaign with an online event and offline product showcases in various cities in China, with more than 50 institutions specializing in trade and distribution from China, Southeast Asia, and the Middle East participated. During the product campaign, Datasea has entered into several marketing and distribution agreements(total amount is approximately $20 Million) in order to expand the business and reach to customers and sell certain Hailijia air sterilizers and purifiers in China.

Currently, after the rapid outbreak of COVID-19 pandemic in China at end of 2023 and earlier 2023, China’s epidemic related control policies have been completely abolished, and retaliatory consumption generated after three years of continuous control and relaxation, but does not include epidemic related products; In addition, the market generally believes that effective antibodies will be available within 6 months after infection, so there may be a phased decline in demand for disinfection products before the possible resurgence of the COVID-19 pandemic in the future and may had a material impact on the Company’s quarterly earnings. However, in the post epidemic era, in the face of the recurrence of COVID-19 and the prevalence of H1N1 influenza in China, the needs for air sterilization and less contact have likely become a permanent way of life for many and may lead to a rebound in demand for new disinfection and sterilization equipment;

In addition, the company actively prepares for the overseas export of disinfection and sterilization equipment to expand the global market. Despite the headwinds of the previous quarter, Datasea’s recent business developments indicate the Company’s resiliency and progress in general business developments, contract acquisitions, product upgrades, marketing efforts, and industry recognition. The company will soon launch non-contact ultrasonic beauty instruments to meet more home care needs.

We currently believe that our financial situation will be benefited us through the new products and rising demands. However, in the event that the demands continues on for a longer period of time, we may need to raise capital to accompany the business development in the future.

NOTE 2 – SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

GOING CONCERN

The accompanying consolidated financial statements

(“CFS”) were prepared assuming the Company will continue as a going concern, which contemplates continuity of operations,

realization of assets, and liquidation of liabilities in the normal course of business. For the nine months ended March 31, 2023 and

2022, the Company had a net loss of approximately $

If deemed necessary, management could seek to raise additional funds by way of admitting strategic investors or. private or public offerings, or by seeking to obtain loans from banks or others, to support the Company’s research and development (“R&D”), procurement, marketing and daily operation. While management of the Company believes in the viability of its strategy to generate sufficient revenues and its ability to raise additional funds on reasonable terms and conditions, there can be no assurances to that effect. The ability of the Company to continue as a going concern depends upon the Company’s ability to further implement its business plan and generate sufficient revenue and its ability to raise additional funds by way of a public or private offering. There is no assurance that the Company will be able to obtain funds on commercially acceptable terms, if at all. There is also no assurance that the amount of funds the Company might raise will enable the Company to complete its initiatives or attain profitable operations. If the Company is unable to raise additional funding to meet its working capital needs in the future, it may be forced to delay, reduce or cease its operations.

7

BASIS OF PRESENTATION AND CONSOLIDATION

The CFS were prepared in accordance with accounting

principles generally accepted in the United States of America (“U.S. GAAP”) and applicable rules and regulations of the SEC

regarding CFS. The accompanying CFS include the financial statements of the Company and its

VARIABLE INTEREST ENTITY

Pursuant to Financial Accounting Standards Board (“FASB”) Accounting Standards Codification (“ASC”) Section 810, “Consolidation” (“ASC 810”), the Company is required to include in its CFS, the financial statements of Shuhai Beijing, its VIE. ASC 810 requires a VIE to be consolidated if the Company is subject to a majority of the risk of loss for the VIE or is entitled to receive a majority of the VIE’s residual returns. A VIE is an entity in which a company, through contractual arrangements, bears the risk of, and enjoys the rewards of such entity, and therefore the Company is the primary beneficiary of such entity.

Under ASC 810, a reporting entity has a controlling financial interest in a VIE, and must consolidate that VIE, if the reporting entity has both of the following characteristics: (a) the power to direct the activities of the VIE that most significantly affect the VIE’s economic performance; and (b) the obligation to absorb losses, or the right to receive benefits, that could potentially be significant to the VIE. The reporting entity’s determination of whether it has this power is not affected by the existence of kick-out rights or participating rights, unless a single enterprise, including its related parties and de - facto agents, have the unilateral ability to exercise those rights. Shuhai Beijing’s actual stockholders do not hold any kick-out rights that affect the consolidation determination.

8

Through the VIE agreements, Tianjin Information, an indirect subsidiary of Datasea is deemed the primary beneficiary of Shuhai Beijing and its subsidiaries. Accordingly, the results of Shuhai Beijing and its subsidiaries were included in the accompanying CFS. Shuhai Beijing has no assets that are collateral for or restricted solely to settle their obligations. The creditors of Shuhai Beijing do not have recourse to the Company’s general credit.

VIE Agreements

Operation and Intellectual Property Service Agreement – The Operation and Intellectual Property Service Agreement allows Tianjin Information Sea Information Technology Co., Ltd (“WFOE”) to manage and operate Shuhai Beijing and collect an operating fee equal to Shuhai Beijing’s pre-tax income, per month. If Shuhai Beijing suffers a loss and as a result does not have pre-tax income, such loss shall be carried forward to the following month to offset the operating fee to be paid to WFOE if there is pre-tax income of Shuhai Beijing the following month. Furthermore, if Shuhai Beijing cannot pay off its debts, WFOE shall pay off the debt on Shuhai Beijing’s behalf. If Shuhai Beijing’s net assets fall lower than its registered capital balance, WFOE shall provide capital for Shuhai Beijing to make up for the deficit.

Under the terms of the Operation and Intellectual Property Service Agreement, Shuhai Beijing entrusts Tianjin Information to manage its operations, manage and control its assets and financial matters, and provide intellectual property services, purchasing management services, marketing management services and inventory management services to Shuhai Beijing. Shuhai Beijing and its stockholders shall not make any decisions nor direct the activities of Shuhai Beijing without Tianjin Information’s consent.

Stockholders’ Voting Rights Entrustment Agreement – Tianjin Information has entered into a stockholders’ voting rights entrustment agreement (the “Entrustment Agreement”) under which Zhixin Liu and Fu Liu (collectively the “Shuhai Beijing Stockholders”) have vested their voting power in Shuhai Beijing to Tianjin Information or its designee(s). The Entrustment Agreement does not have an expiration date, but the parties can agree in writing to terminate the Entrustment Agreement. Zhixin Liu, is the Chairman of the Board, President, CEO of DataSea and Corporate Secretary, and Fu Liu, a Director of the DataSea (Fu Liu is the father of Zhixin Liu).

Equity Option Agreement – the

Shuhai Beijing Stockholders and Tianjin Information entered into an equity option agreement (the “Option Agreement”), pursuant

to which the Shuhai Beijing Stockholders have granted Tianjin Information or its designee(s) the irrevocable right and option to acquire

all or a portion of Shuhai Beijing Stockholders’ equity interests in Shuhai Beijing for an option price of RMB

Equity Pledge Agreement – Tianjin Information and the Shuhai Beijing Stockholders entered into an equity pledge agreement on October 27, 2015 (the “Equity Pledge Agreement”). The Equity Pledge Agreement serves to guarantee the performance by Shuhai Beijing of its obligations under the Operation and Intellectual Property Service Agreement and the Option Agreement. Pursuant to the Equity Pledge Agreement, Shuhai Beijing Stockholders have agreed to pledge all of their equity interests in Shuhai Beijing to Tianjin Information. Tianjin Information has the right to collect any and all dividends, bonuses and other forms of investment returns paid on the pledged equity interests during the pledge period. Pursuant to the terms of the Equity Pledge Agreement, the Shuhai Beijing Stockholders have agreed to certain restrictive covenants to safeguard the rights of Tianjin Information. Upon an event of default or certain other agreed events under the Operation and Intellectual Property Service Agreement, the Option Agreement and the Equity Pledge Agreement, Tianjin Information may exercise the right to enforce the pledge.

9

As of this report date, there was no dividends paid from the VIE to the U.S. parent company or the shareholders of the Company. There has been no change in facts and circumstances to consolidate the VIE. The following financial statement amounts and balances of the VIE were included in the accompanying CFS as of March 31, 2023 and June 30, 2022, and for the nine and three months ended March 31, 2023 and 2022, respectively.

| March 31, 2023 | June 30, 2022 | |||||||

| Cash | $ | $ | ||||||

| Accounts receivable | ||||||||

| Inventory | ||||||||

| Other current assets | ||||||||

| Total current assets | ||||||||

| Property and equipment, net | ||||||||

| Intangible asset, net | ||||||||

| Right-of-use asset, net | ||||||||

| Other non-current assets | ||||||||

| Total non-current assets | ||||||||

| Total assets | $ | $ | ||||||

| Accounts payable | $ | $ | ||||||

| Accrued liabilities and other payables | ||||||||

| Lease liability | ||||||||

| Loans payable | ||||||||

| Other current liabilities | ||||||||

| Total current liabilities | ||||||||

| Loan payable- noncurrent | ||||||||

| Total non-current liabilities | ||||||||

| Total liabilities | $ | $ | ||||||

| For the Nine Months Ended March 31, 2023 | For the Nine Months Ended March 31, 2022 | |||||||

| Revenues | $ | $ | ||||||

| Gross profit | $ | $ | ||||||

| Net income (loss) | $ | ( | ) | $ | ||||

| For the Three Months Ended March 31, 2023 | For the Three Months Ended March 31, 2022 | |||||||

| Revenues | $ | $ | ||||||

| Gross profit | $ | $ | ||||||

| Net income (loss) | $ | ( | ) | $ | ||||

10

USE OF ESTIMATES

The preparation of CFS in conformity with U.S. GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenues and expenses during the reporting periods. Actual results could differ from those estimates. The significant areas requiring the use of management estimates include, but are not limited to, the estimated useful life and residual value of property, plant and equipment, provision for staff benefits, recognition and measurement of deferred income taxes and the valuation allowance for deferred tax assets. Although these estimates are based on management’s knowledge of current events and actions management may undertake in the future, actual results may ultimately differ from those estimates and such differences may be material to the CFS.

CONTINGENCIES

Certain conditions may exist as of the date the CFS are issued, which may result in a loss to the Company but which will only be resolved when one or more future events occur or fail to occur. The Company’s management and legal counsel assess such contingent liabilities, and such assessment inherently involves an exercise of judgment. In assessing loss contingencies related to legal proceedings that are pending against the Company or unasserted claims that may result in such proceedings, the Company’s legal counsel evaluates the perceived merits of any legal proceedings or unasserted claims as well as the perceived merits of the amount of relief sought or expected to be sought. If the assessment of a contingency indicates that it is probable that a material loss has been incurred and the amount of the liability can be estimated, the estimated liability would be accrued in the Company’s CFS.

If the assessment indicates that a potential material loss contingency is not probable but is reasonably possible, or is probable but cannot be estimated, the nature of the contingent liability, together with an estimate of the range of possible loss if determinable and material, would be disclosed. As of March 31, 2023 and June 30, 2022, the Company has no such contingencies.

CASH

Cash include cash on hand and demand deposits that are highly liquid in nature and have original maturities when purchased of three months or less.

ACCOUNTS RECEIVABLE

The Company’s policy is to maintain an

allowance for potential credit losses on accounts receivable. Management reviews the composition of accounts receivable and analyzes

historical bad debts, customer concentrations, customer credit worthiness, current economic trends and changes in customer payment patterns

to evaluate the adequacy of these reserves. As of March 31, 2023 and June 30, 2022, the Company had a $

INVENTORY

Inventory is comprised principally of intelligent

temperature measurement face recognition terminal and identity information recognition products, and is valued at the lower of cost or

net realizable value. The value of inventory is determined using the first-in, first-out method. The Company periodically estimates an

inventory allowance for estimated unmarketable inventories when necessary. Inventory amounts are reported net of such allowances. There

were $

PROPERTY AND EQUIPMENT

Property and equipment are stated at cost, less accumulated depreciation. Major repairs and improvements that significantly extend original useful lives or improve productivity are capitalized and depreciated over the period benefited. Maintenance and repairs are expensed as incurred. When property and equipment are retired or otherwise disposed of, the related cost and accumulated depreciation are removed from the respective accounts, and any gain or loss is included in operations. Depreciation of property and equipment is provided using the straight-line method over estimated useful lives as follows:

| Furniture and fixtures | ||

| Office equipment | ||

| Vehicles | ||

| Leasehold improvement |

Leasehold improvements are depreciated utilizing the straight-line method over the shorter of their estimated useful lives or remaining lease term.

11

INTANGIBLE ASSETS

Intangible assets with finite lives are amortized using the straight-line method over their estimated period of benefit. Evaluation of the recoverability of intangible assets is made to take into account events or circumstances that warrant revised estimates of useful lives or that indicate that impairment exists. All of the Company’s intangible assets are subject to amortization. No impairment of intangible assets has been identified as of the balance sheet date.

Intangible assets include licenses, certificates,

patents and other technology and are amortized over their useful life of

FAIR VALUE (“FV”) OF FINANCIAL INSTRUMENTS

The carrying value of the Company’s short-term financial instruments, such as cash, accounts receivable, prepaid expenses, accounts payable, unearned revenue, accrued expenses and other payables approximates their FV due to their short maturities. FASB ASC Topic 825, “Financial Instruments,” requires disclosure of the FV of financial instruments held by the Company. The carrying amounts reported in the balance sheets for current liabilities qualify as financial instruments and are a reasonable estimate of their FV because of the short period of time between the origination of such instruments and their expected realization and the current market rate of interest.

FAIR VALUE MEASUREMENTS AND DISCLOSURES

FASB ASC Topic 820, “Fair Value Measurements,” defines FV, and establishes a three-level valuation hierarchy for disclosures that enhances disclosure requirements for FV measures. The three levels are defined as follows:

| ● | Level 1 inputs to the valuation methodology are quoted prices (unadjusted) for identical assets or liabilities in active markets. |

| ● | Level 2 inputs to the valuation methodology include other than those in level 1 quoted prices for similar assets and liabilities in active markets, and inputs that are observable for the asset or liability, either directly or indirectly, for substantially the full term of the financial instrument. |

| ● | Level 3 inputs to the valuation methodology are unobservable and significant to the FV measurement. |

As of March 31,2023 and June 30, 2022, the Company did not identify any assets or liabilities required to be presented on the balance sheet at FV on a recurring basis.

IMPAIRMENT OF LONG-LIVED ASSETS

In accordance with FASB ASC 360-10, “Accounting for the Impairment or Disposal of Long-Lived Assets”, long-lived assets such as property and equipment are reviewed for impairment whenever events or changes in circumstances indicate that the carrying value of an asset may not be recoverable, or it is reasonably possible that these assets could become impaired as a result of technological or other changes. The determination of recoverability of assets to be held and used is made by comparing the carrying amount of an asset to future undiscounted cash flows expected to be generated by the asset.

If such assets are considered impaired, the impairment to be recognized is measured as the amount by which the carrying amount of the asset exceeds its FV. FV generally is determined using the asset’s expected future undiscounted cash flows or market value, if readily determinable. Assets to be disposed of are reported at the lower of the carrying amount or FV less cost to sell. For the nine and three months ended March 31, 2023 and 2022, there was no impairment loss recognized on long-lived assets.

12

UNEARNED REVENUE

The Company records payments received in advance from its customers or sales agents for the Company’s products as unearned revenue, mainly consisting of deposits or prepayment for 5G products from the Company’s sales agencies. These orders normally are delivered based upon contract terms and customer demand, and will recognize as revenue when the products are delivered to the end customers.

LEASES

The Company determines if an arrangement is a lease at inception under FASB ASC Topic 842. Right of Use Assets (“ROU”) and lease liabilities are recognized at commencement date based on the present value of remaining lease payments over the lease term. For this purpose, the Company considers only payments that are fixed and determinable at the time of commencement. As most of its leases do not provide an implicit rate, it uses its incremental borrowing rate based on the information available at commencement date in determining the present value of lease payments. The Company’s incremental borrowing rate is a hypothetical rate based on its understanding of what its credit rating would be. The ROU assets include adjustments for prepayments and accrued lease payments. The ROU asset also includes any lease payments made prior to commencement and is recorded net of any lease incentives received. The Company’s lease terms may include options to extend or terminate the lease when it is reasonably certain that it will exercise such options.

ROU assets are reviewed for impairment when indicators of impairment are present. ROU assets from operating and finance leases are subject to the impairment guidance in ASC 360, Property, Plant, and Equipment, as ROU assets are long-lived nonfinancial assets.

ROU assets are tested for impairment individually or as part of an asset group if the cash flows related to the ROU asset are not independent from the cash flows of other assets and liabilities. An asset group is the unit of accounting for long-lived assets to be held and used, which represents the lowest level for which identifiable cash flows are largely independent of the cash flows of other groups of assets and liabilities. The Company recognized no impairment of ROU assets as of March 31 2023 and June 30, 2022.

Operating leases are included in operating lease

ROU and operating lease liabilities (current and non-current), on the consolidated balance sheets. As of March 31, 2023, the net

ROU was $

REVENUE RECOGNITION

The Company follows Accounting Standards Codification Topic 606, Revenue from Contracts with Customers (ASC 606).

The core principle underlying FASB ASC 606 is that the Company will recognize revenue to represent the transfer of goods and services to customers in an amount that reflects the consideration to which the Company expects to be entitled in such exchange. This will require the Company to identify contractual performance obligations and determine whether revenue should be recognized at a point in time or over time, based on when control of goods and services transfers to a customer. The Company’s revenue streams are identified when possession of goods and services is transferred to a customer.

FASB ASC Topic 606 requires the use of a new five-step model to recognize revenue from customer contracts. The five-step model requires the Company (i) identify the contract with the customer, (ii) identify the performance obligations in the contract, (iii) determine the transaction price, including variable consideration to the extent that it is probable that a significant future reversal will not occur, (iv) allocate the transaction price to the respective performance obligations in the contract, and (v) recognize revenue when (or as) the Company satisfies each performance obligation.

13

The Company derives its revenues from product sales and 5G messaging service contracts with its customers, with revenues recognized upon delivery of services and products. Persuasive evidence of an arrangement is demonstrated via product sale contracts and professional service contracts, with performance obligations identified. The transaction price, such as product selling price, and the service price to the customer with corresponding performance obligations are fixed upon acceptance of the agreement. The Company recognizes revenue when it satisfies each performance obligation, the customer receives the products and passes the inspection and when professional service is rendered to the customer, collectability of payment is probable. These revenues are recognized at a point in time after each performance obligations is satisfied. Revenue is recognized net of returns and value-added tax charged to customers.

The following table shows the Company’s revenue by revenue sources:

| For the Nine Months Ended March 31, 2023 | For the Three Months Ended March 31, 2023 | |||||||

| 5G Messaging | $ | $ | ||||||

| 5G messaging | ||||||||

| Aggregate messaging platform | - | |||||||

| Cloud platform construction cooperation project | ||||||||

| Acoustic Intelligence Business | ||||||||

| Ultrasonic Sound Air Disinfection Equipment | ||||||||

| Other | ||||||||

| Smart City business | ||||||||

| Smart community | - | |||||||

| Smart community broadcasting system | ||||||||

| Smart agriculture | - | |||||||

| Total revenue | $ | $ | ||||||

SEGMENT INFORMATION

FASB ASC Topic 280, “Segment Reporting,” requires use of the “management approach” model for segment reporting. The management approach model is based on the method a company’s management organizes segments within the company for making operating decisions and assessing performance. Reportable segments are based on products and services, geography, legal structure, management structure, or any other manners in which management disaggregates a company. Management determining the Company’s current operations constitutes a single reportable segment in accordance with ASC 280. The Company’s only business and industry segment is high technology and advanced information systems (“TAIS”). TAIS include smart city solutions that meet the security needs of residential communities, schools and commercial enterprises, and 5G messaging services including 5G SMS, 5G MMCP and 5G multi-media video messaging.

All of the Company’s customers are in the PRC and all revenues for the nine and three months ended March 31, 2023 and 2022 were generated from the PRC. All identifiable assets of the Company are located in the PRC. Accordingly, no geographical segments are presented.

INCOME TAXES

The Company uses the asset and liability method of accounting for income taxes in accordance with FASB ASC Topic 740, “Income Taxes.” Under this method, income tax expense is recognized for the amount of: (i) taxes payable or refundable for the current period and (ii) deferred tax consequences of temporary differences resulting from matters that have been recognized in an entity’s financial statements or tax returns. Deferred tax assets also include the prior years’ net operating losses carried forward. Deferred tax assets and liabilities are measured using enacted tax rates expected to apply to taxable income in the years in which those temporary differences are expected to be recovered or settled. The effect on deferred tax assets and liabilities of a change in tax rates is recognized in the results of operations in the period that includes the enactment date. A valuation allowance is provided to reduce the deferred tax assets reported if based on the weight of the available positive and negative evidence, it is more likely than not some portion or all of the deferred tax assets will not be realized.

14

The Company follows FASB ASC Topic 740, which prescribes a more-likely-than-not threshold for financial statement recognition and measurement of a tax position taken or expected to be taken in a tax return. FASB ASC Topic 740 also provides guidance on recognition of income tax assets and liabilities, classification of current and deferred income tax assets and liabilities, accounting for interest and penalties associated with tax positions, accounting for income taxes in interim periods, and income tax disclosures.

Under the provisions of FASB ASC Topic 740, when

tax returns are filed, it is likely some positions taken would be sustained upon examination by the taxing authorities, while others

are subject to uncertainty about the merits of the position taken or the amount of the position that would be ultimately sustained. The

benefit of a tax position is recognized in the financial statements in the period during which, based on all available evidence, management

believes it is more likely than not that the position will be sustained upon examination, including the resolution of appeals or litigation

processes, if any. Tax positions taken are not offset or aggregated with other positions. Tax positions that meet the more-likely-than-not

recognition threshold are measured as the largest amount of tax benefit that is more than

RESEARCH AND DEVELOPMENT EXPENSES

Research and development expenses are expensed in the period when incurred. These costs primarily consist of cost of materials used, salaries paid for the Company’s development department, and fees paid to third parties.

NONCONTROLLING INTERESTS

The Company follows FASB ASC Topic 810, “Consolidation,” governing the accounting for and reporting of noncontrolling interests (“NCIs”) in partially owned consolidated subsidiaries and the loss of control of subsidiaries. Certain provisions of this standard indicate, among other things, that NCI (previously referred to as minority interests) be treated as a separate component of equity, not as a liability, that increases and decreases in the parent’s ownership interest that leave control intact be treated as equity transactions rather than as step acquisitions or dilution gains or losses, and that losses of a partially-owned consolidated subsidiary be allocated to non-controlling interests even when such allocation might result in a deficit balance.

The net income (loss) attributed to NCI was separately designated in the accompanying statements of operations and comprehensive income (loss). Losses attributable to NCI in a subsidiary may exceed a non-controlling interest’s interests in the subsidiary’s equity. The excess attributable to NCIs is attributed to those interests. NCIs shall continue to be attributed their share of losses even if that attribution results in a deficit NCI balance.

As of March 31, 2023, Zhangxun was

15

CONCENTRATION OF CREDIT RISK

The Company maintains cash in accounts with state-owned

banks within the PRC. Cash in state-owned banks less than RMB

Cash held in accounts at U.S. financial institutions

is insured by the Federal Deposit Insurance Corporation or other programs subject to certain limitations up to $

FOREIGN CURRENCY TRANSLATION AND COMPREHENSIVE INCOME (LOSS)

The accounts of the Company’s Chinese entities are maintained in RMB and the accounts of the U.S. parent company are maintained in United States dollar (“USD”). The financial statements of the Chinese entities were translated into USD in accordance with FASB ASC Topic 830 “Foreign Currency Matters.” All assets and liabilities were translated at the exchange rate on the balance sheet date; stockholders’ equity is translated at historical rates and the statements of operations and cash flows are translated at the weighted average exchange rate for the period. The resulting translation adjustments are reported under other comprehensive income (loss) in accordance with FASB ASC Topic 220, “Comprehensive Income.” Gains and losses resulting from foreign currency transactions are reflected in the statements of operations.

The Company follows FASB ASC Topic 220-10, “Comprehensive Income (loss).” Comprehensive income (loss) comprises net income (loss) and all changes to the statements of changes in stockholders’ equity, except those due to investments by stockholders, changes in additional paid-in capital and distributions to stockholders.

The exchange rates used to translate amounts in RMB to USD for the purposes of preparing the CFS were as follows:

| March 31, | March 31, | June 30, | ||||||||||

| 2023 | 2022 | 2022 | ||||||||||

| Period-end date USD: RMB exchange rate | ||||||||||||

| Average USD for the reporting period: RMB exchange rate | ||||||||||||

BASIC AND DILUTED EARNINGS (LOSS) PER SHARE (EPS)

Basic EPS is computed by dividing income available

to common shareholders by the weighted average number of common shares outstanding for the period. Diluted EPS is computed similarly,

except that the denominator is increased to include the number of additional common shares that would have been outstanding if the potential

common shares had been issued and if the additional common shares were dilutive. Diluted EPS is based on the assumption that all dilutive

convertible shares and stock options were converted or exercised. Dilution is computed by applying the treasury stock method. Under this

method, options and warrants are assumed to have been exercised at the beginning of the period (or at the time of issuance, if later),

and as if funds obtained thereby were used to purchase common stock at the average market price during the period. For the nine and three

months ended March 31, 2023 and 2022, the Company’s basic and diluted loss per share are the same as a result of the Company’s

net loss.

16

STATEMENT OF CASH FLOWS

In accordance with FASB ASC Topic 230, “Statement of Cash Flows,” cash flows from the Company’s operations are calculated based upon the local currencies. As a result, amounts shown on the statement of cash flows may not necessarily agree with changes in the corresponding asset and liability on the balance sheet.

RECENT ACCOUNTING PRONOUNCEMENTS

In June 2016, the FASB issued ASU No. 2016-13, Financial Instruments-Credit Losses (Topic 326), which requires entities to measure all expected credit losses for financial assets held at the reporting date based on historical experience, current conditions, and reasonable and supportable forecasts. This replaces the existing incurred loss model and is applicable to the measurement of credit losses on financial assets measured at amortized cost. This guidance is effective for fiscal years, and interim periods within those fiscal years, beginning after December 15, 2022. Early application will be permitted for all entities for fiscal years, and interim periods within those fiscal years, beginning after December 15, 2018. The Company is currently evaluating the impact that the standard will have on its CFS.

The Company’s management does not believe that any other recently issued, but not yet effective, authoritative guidance, if currently adopted, would have a material impact on the Company’s financial statement presentation or disclosures.

NOTE 3 – PROPERTY AND EQUIPMENT

Property and equipment are summarized as follows:

| March 31, 2023 | June 30, 2022 | |||||||

| Furniture and fixtures | $ | $ | ||||||

| Vehicle | ||||||||

| Leasehold improvement | ||||||||

| Office equipment | ||||||||

| Subtotal | ||||||||

| Less: accumulated depreciation | ||||||||

| Total | $ | $ | ||||||

Depreciation for the nine months ended March

31, 2023 and 2022 was $

Depreciation for the three months ended March

31, 2023 and 2022 was $

NOTE 4 – INTANGIBLE ASSETS

Intangible assets are summarized as follows:

| March 31, 2023 | June 30, 2022 | |||||||

| Software registration or using right | $ | $ | ||||||

| Patent | ||||||||

| Software and technology development costs | ||||||||

| Value-added telecommunications business license | ||||||||

| Subtotal | ||||||||

| Less: Accumulated amortization | ||||||||

| Total | $ | $ | ||||||

17

Software registration or using right represented the purchase cost of customized software with its source code from third party software developer.

Software and technology development cost represented development costs incurred internally after the technological feasibility was established and a working model was produced and was recorded as intangible asset.

Amortization for the nine months ended March

31, 2023 and 2022 was $

Amortization for the three months ended March

31, 2023 and 2022 was $

NOTE 5 – PREPAID EXPENSES AND OTHER CURRENT ASSETS

Prepaid expenses and other current assets consisted of the following:

| March 31, 2023 | June 30, 2022 | |||||||

| Security deposit | $ | $ | ||||||

| Prepaid expenses | ||||||||

| Other receivables – Heqin | ||||||||

| Advance to third party individuals, no interest, payable upon demand | ||||||||

| Others | ||||||||

| Total | ||||||||

| Less: allowance for other receivables – Heqin | ||||||||

| Total | $ | $ | ||||||

Other receivables - Heqin

On February 20, 2020, Guozhong Times entered

an Operation Cooperation Agreement with an unrelated company, Heqin (Beijing) Technology Co, Ltd. (“Heqin”), for marketing

and promoting the sale of Face Recognition Payment Processing equipment and related technical support, and other products of the Company

including Epidemic Prevention and Control Systems.

The cooperation term is from February 20, 2020

through March 1, 2023; however, Heqin is the exclusive distributor of the Company’s face Recognition Payment Processing products

for the period to July 30, 2020. During March and April 2020, Guozhong Times provided operating funds to Heqin, together with a credit

line provided by Guozhong Times to Heqin from May 2020 through August 2020, for a total borrowing of RMB

No profits will be allocated and distributed

before full repayment of the borrowing. After Heqin pays in full the borrowing, Guozhong Times and Heqin will distribute profits of sale

of Face Recognition Payment Processing equipment and related technical support at

As of March 31, 2023 and June 30, 2022, Heqin

made $

18

NOTE 6 – LONG TERM INVESTMENT

In November, 2021, Shuhai Nanjing invested RMB

In August 2022, Shuhai Nanjing invested RMB

NOTE 7 – ACCRUED EXPENSES AND OTHER PAYABLES

Accrued expenses and other payables consisted of the following:

| March 31, 2023 | June 30, 2022 | |||||||

| Other payables | $ | $ | ||||||

| Due to third parties | ||||||||

| Social security payable | ||||||||

| Salary payable - employees | ||||||||

| Total | $ | $ | ||||||

Due to third parties were the short term advance from third party individual or companies, bear no interest and payable upon demand.

NOTE 8 – LOANS PAYABLE

Loan from bank

On December

On December 21, 2022, Zhangxun entered a loan

agreement with Shenzhen Qianhai WeBank Co., Ltd for the amount of $

On December 12, 2022, Beijing Shuhai entered

a loan agreement with Shenzhen Qianhai WeBank Co., Ltd for the amount of $

On January 13, 2023, Shenzhen Jingwei entered

a loan agreement with Shenzhen Qianhai WeBank Co., Ltd for the amount of $

Loan from an unrelated party

On April 24, 2022, the Company entered a loan

agreement with an unrelated party for $

19

NOTE 9 – RELATED PARTY TRANSACTIONS

In April 2020, the Company’s CEO (also

the major shareholder of the Company) entered into a one-year apartment rental agreement with the Company for an apartment located in

Harbin city as the Company’s branch office with an annual rent of RMB

On October 1, 2020, the Company’s CEO entered

into an office rental agreement with Xunrui. Pursuant to the agreement, the Company rents an office in Harbin city with a total payment

of RMB

On July 1, 2021, the Company’s CEO entered

into a car rental agreement with the Company for one year. Pursuant to the agreement, the Company rents a car from the Company’s

CEO for a monthly rent of RMB

On September 1, 2021, the Company renewed a one-year

lease for senior officers’ dormitory in Beijing, the monthly rent is RMB

Due to related parties

As of March 31, 2023 and June 30, 2022, the Company

had due to related parties of $

NOTE 10 – COMMON STOCK AND WARRANTS

Registered Direct Offering and Concurrent Private Placement in July 2021

On July 20, 2021, the Company entered into a

securities purchase agreement with certain institutional investors, pursuant to which the Company agreed to sell to such investors an

aggregate of

20

Concurrently with the sale of the shares of the

common stock, the Company also sold warrants to purchase

The closing of the sales of these securities

under the securities purchase agreement took place on July 22, 2021. The net proceeds from the transactions were approximately $

Following is a summary of the activities of warrants for the period ended March 31, 2023:

| Number of Warrants | Average Exercise Price | Weighted Average Remaining Contractual Term in Years | ||||||||||

| Outstanding as of June 30, 2022 | $ | |||||||||||

| Exercisable as of June 30, 2022 | $ | |||||||||||

| Granted | ||||||||||||

| Exercised | ||||||||||||

| Forfeited | ||||||||||||

| Expired | ||||||||||||

| Outstanding as of March 31, 2023 | $ | |||||||||||

| Exercisable as of March 31, 2023 | $ | |||||||||||

Shares to Independent Directors as Compensation

During the nine months ended March 31, 2023 and

2022, the Company recorded $

21

Shares to Officers as Compensation

Shares to a Consultant as Compensation

On October 1, 2021, the Company entered into

a one-year advisory agreement with a consultant for a monthly compensation of $

Shares to Officers in Lieu of Salary Payable

On December 30, 2021, the Board of Directors

approved to issue

Amendment for Shares Reserved Under 2018 Equity Incentive Plan

On March 17, 2022, the Board of Directors approved

the amendment to the Company’s 2018 Equity Incentive Plan to increase the number of the Company’s Common Stock to be reserved

from

NOTE 11 – INCOME TAXES

The Company is subject to income taxes by entity on income arising in or derived from the tax jurisdiction in which each entity is domiciled. The Company’s PRC subsidiaries file their income tax returns online with PRC tax authorities. The Company conducts all of its businesses through its subsidiaries and affiliated entities, principally in the PRC.

The Company’s U.S. parent company is subject

to U.S. income tax rate of

The Company’s offshore subsidiary, Shuhai

Skill (HK), a HK holding company is subject to

22

As of March 31, 2023 and June 30, 2022, the Company

has approximately $

The following table reconciles the U.S. statutory rates to the Company’s effective tax rate for the nine months ended March 31, 2023 and 2022:

| 2023 | 2022 | |||||||

| US federal statutory rates | ( | )% | ( | )% | ||||

| Tax rate difference – current provision | ( | )% | ( | )% | ||||

| Effect of PRC tax holiday | % | ( | )% | |||||

| Valuation allowance | % | % | ||||||

| Effective tax rate | % | % | ||||||

The following table reconciles the U.S. statutory rates to the Company’s effective tax rate for the three months ended March 31, 2023 and 2022:

| 2023 | 2022 | |||||||

| US federal statutory rates | ( | )% | ( | )% | ||||

| Tax rate difference – current provision | ( | )% | ( | )% | ||||

| Effect of PRC tax holiday | % | % | ||||||

| Valuation allowance | % | % | ||||||

| Effective tax rate | % | % | ||||||

The Company’s net deferred tax assets as of March 31, 2023 and June 30, 2022 is as follows:

| March 31, 2023 | June 30, 2022 | |||||||

| Deferred tax asset | ||||||||

| Net operating loss | $ | $ | ||||||

| R&D expense | ||||||||

| Depreciation and amortization | ||||||||

| Bad debt expense | ||||||||

| Social security and insurance accrual | ||||||||

| Inventory impairment | ||||||||

| ROU, net of lease liabilities | ( | ) | ||||||

| Total | ||||||||

| Less: valuation allowance | ( | ) | ( | ) | ||||

| Net deferred tax asset | $ | $ | ||||||

NOTE 12 – COMMITMENTS

Leases

On July 30, 2019, the Company entered into an

operating lease for its office in Beijing. Pursuant to the lease, the delivery date of the property was August 8, 2019 but the lease

term started on October 8, 2019 and expires on October 7, 2022, and has a monthly rent of RMB

On July 30, 2019, the Company entered into a

property service agreement for its office in Beijing (described above).

23

The Company adopted FASB ASC Topic 842 on July 1, 2019. The components of lease costs, lease term and discount rate with respect of the Company’s office lease and the senior officers’ dormitory lease with an initial term of more than 12 months are as follows:

| Nine Months Ended March 31, 2023 | Nine Months Ended March 31, 2022 | |||||||

| Operating lease expense | $ | $ | ||||||

| Three Months Ended March 31, 2023 | Three Months Ended March 31, 2022 | |||||||

| Operating lease expense | $ | $ | ||||||

| March 31, 2023 | ||||

| Right-of-use assets | $ | |||

| Lease liabilities - current | ||||

| Lease liabilities - noncurrent | ||||

| Weighted average remaining lease term | ||||

| Weighted average discount rate | % | |||

The following is a schedule, by years, of maturities of the operating lease liabilities as of March 31, 2023:

| 12 Months Ending March 31, | Minimum Lease Payment | |||

| 2023 | $ | |||

| Total undiscounted cash flows | ||||

| Less: imputed interest | ( | ) | ||

| Present value of lease liabilities | $ | |||

NOTE 13 – SUBSEQUENT EVENTS

The Company follows the guidance in FASB ASC 855-10 for the disclosure of subsequent events. The Company evaluated subsequent events through the date the financial statements were issued and determined the Company had the following major subsequent event need to be disclosed.

On April 25, 2023, Shuhai information entered

a loan agreement with China Bank Co., Ltd for the amount of $

On April 5th, 2023, the Company issued

24

ITEM 2. MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

Cautionary Note Regarding Forward-Looking Statements

This report contains forward-looking statements within the meaning of Section 27A of the Securities Act and Section 21E of the Exchange Act. All statements other than statements of historical fact are “forward-looking statements” for purposes of federal and state securities laws, including, but not limited to, any projections of earnings, revenue, or other financial items; any statements of the plans, strategies, and objectives of management for future operations; any statements concerning proposed new services or developments; any statements regarding future economic conditions of performance; and statements of belief; and any statements of assumptions underlying any of the foregoing. Such forward-looking statements involve known and unknown risks, uncertainties, and other factors that may cause our actual results, performance, or achievements to be materially different from any future results, performance, or achievements expressed or implied by such forward-looking statements.

In some cases, you can identify forward-looking statements by terms such as “may,” “intend,” “might,” “will,” “should,” “could,” “would,” “expect,” “believe,” “anticipate,” “estimate,” “predict,” “potential,” or the negative of these terms. These terms and similar expressions are intended to identify forward-looking statements. The forward-looking statements in this report are based upon management’s current expectations, which it believes are reasonable. However, we cannot assess the impact of each factor on our business or the extent to which any factor or combination of factors, or factors we are aware of, may cause actual results to differ materially from those contained in any forward-looking statements. You are cautioned not to place undue reliance on any forward-looking statements. These statements represent our estimates and assumptions only as of the date of this report. Except to the extent required by federal securities laws, we undertake no obligation to update any forward-looking statement to reflect events or circumstances after the date hereof or to reflect the occurrence of unanticipated events.

You should be aware that our actual results could differ materially from those contained in the forward-looking statements due to several factors, including:

| ● | uncertainties relating to our ability to establish and operate our business and generate revenue; |

| ● | uncertainties relating to general economic, political, and business conditions in China; |

| ● | industry trends and changes in demand for our products and services; |

| ● | uncertainties relating to customer plans and commitments and the timing of orders received from customers; |

| ● | announcements or changes in our advertising model and related pricing policies or that of our competitors; |

| ● | unanticipated delays in the development, market acceptance, or installation of our products and services; |

| ● | changes in Chinese government regulations; |

| ● | availability, terms and deployment of capital, relationships with third-party equipment suppliers; and |

| ● | COVID-19’s influence on China’s economy and society. |

Overview

Datasea Inc. (“Datasea,” with its subsidiaries and VIE, as defined below, collectively, the “Company” or “We” or “Us” or “Our”) is a leading provider of products, services, and solutions for enterprise and retail customers in three converging and innovative industries: 5G messaging, acoustic intelligence, and smart city technology. The Company possesses proprietary and cutting-edge technologies that build a solid foundation to design, develop and supply a broad range of solutions in each industry.

25

Datasea’s vision is to become a global leader in Digital Intelligent Technology, to innovate and provide advanced technology to a broad client base, and within a decade, to evolve into a multinational company with a U.S. entity as the core of its business operations.

Datasea Inc. was incorporated in Nevada on September 26, 2014, and is a holding company with no material operations of its own, the Company conducts a substantial majority of its operations through operating entities established in the People’s Republic of China, or the PRC, primarily through a variable interest entity (“VIE”), Shuhai Information Technology Co., Ltd. (“Shuhai Beijing”). The VIE holds eight subsidiaries to explore business opportunities.

We do not have any equity ownership of the VIE, instead the Company controls and receives the economic benefits of the VIE’s business operations through certain contractual arrangements. Our common stock that is currently listed on the Nasdaq Capital Markets are shares of our Nevada holding company that maintains service agreements with the associated operating companies.

As of March 31, 2023, Shuhai Beijing and its subsidiaries own 29 Patents and 117 Software Copyrights in PRC. The newly updated status of Shuhai’s patents and software copyrights are as follows:

Patent

From July 1 2022 to March 31 2023, we obtained the following new patents and soft copyrights in PRC:

| No. | Acceptance Number | Description | Publication Number | |||

| Shuhai Jingwei | ||||||

| 1 | 202221777917.9 | Ultraviolet ultrasonic plasma disinfection equipment | ZL202221777917.9 | |||

| 2 | 202221781894.9 | The handle used for sterilizing the device | 202221781894.9 | |||

| 3 | 202210811431.0 | A high frequency acoustic effect air coupled microbial elimination method and device | 202210811431.0 | |||

| Acoustic Effect Technology | ||||||

| 1 | 202230336646.2 | Acoustic effect disinfection instrument Type Ⅰ (high-end version) | ZL202230336646.2 | |||

| 2 | 20220320646.3 | Acoustic effect disinfection instrument Type Ⅰ (Universal) | ZL20220320646.3 | |||

| 3 | 202230336653.2 | Intelligent acoustic effect handle type Ⅰ | ZL202230336653.2 | |||

| 4 | 202230336336.0 | Acoustic effect disinfection man-machine coexistence instrument type Ⅰ | ZL202230336336.0 | |||

| Xunrui Techonolgy | ||||||

| 1 | 202110163396.1 | A new infrared temperature measuring device and method | ZL202110163396.1 |

26

| Soft Copyrights owned by Shuhai Jingwei | ||||

| 1 | Square intelligent acoustic early warning and recognition system 1.0 | Ruan Zhu Deng Zi No.10322358 | ||

| 2 | Community medical center intelligent acoustic early warning recognition system 1.0 | Ruan Zhu Deng Zi No.10322366 | ||

| 3 | Stadium intelligent acoustic early warning and identification system 1.0 | Ruan Zhu Deng Zi No.10319630 | ||

| 4 | Home intelligent acoustic early warning recognition system 1.0 | Ruan Zhu Deng Zi No.10322359 | ||

| 5 | College intelligent acoustic Early warning and recognition system 1.0 | Ruan Zhu Deng Zi No.10322365 | ||

| 6 | Apartment intelligent acoustic Early warning and recognition system 1.0 | Ruan Zhu Deng Zi No.10322358 | ||

| 7 | Shuhai Jingwei Smart Park Security Cloud Platform 1.0 | Ruan Zhu Deng Zi No. 10688731 | ||

| 8 | Shuhai Jingwei Smart Community Integrated Management Client Platform 1.0 | Ruan Zhu Deng Zi No.10688733 | ||

| 9 | Shuhai Jingwei SOP Management System 1.0 | Ruan Zhu Deng Zi No.10688732 | ||

| 10 | Shuhai Jingwei Message Platform 1.0 | Ruan Zhu Deng Zi No.10688736 | ||

| 11 | Shuhai Jingwei Digital Team Management System 1.0 | Ruan Zhu Deng Zi No.10688737 | ||

| 12 | Shuhai Jingwei Data Collection System 1.0 | Ruan Zhu Deng Zi No.10688734 | ||

| 13 | Shuhai Jingwei 5G message aggregation cloud platform 1.0 | Ruan Zhu Deng Zi No.10688735 | ||

| 14 | Variable frequency acoustic effect coronavirus feature disinfection and sterilization algorithm software V1.0 | Ruan Zhu Deng Zi No.10688738 | ||

| 15 | High frequency sound effect air coupling algorithm platform V1.0 | Ruan Zhu Deng Zi No.10688740 | ||

| 16 | High frequency sound effect air coupling and collaborative UV control algorithm software V1.0 | Ruan Zhu Deng Zi No.10688739 | ||

| 2. Soft copyrights | ||||

| Soft Copyrights owned by Shuhai Jingwei (under review) | ||||

| 1 | Shuhai Jingwei CRM Platform 1.0 | Acceptance No. : 2022R11L2068223 | ||

| 2 | Shuhai Jingwei messaging marketing cloud platform 1.0 | Acceptance No. : 2022R11L2070582 | ||

| 3 | Shuhai Jingwei Data Asset management platform V1.0 | Acceptance No. : 2022R11L2070760 | ||

27

| Software Copyright Owned by Shuhai Beijing | ||||

| No. | Certification | Certificate No. | ||

| 1 | Shuhai Information Food Traceability Management System V1.0 | Ruan Zhu Deng Zi No.10176578 | ||

| 2 | Shuhai information comprehensive canteen management application system V1.0 | Ruan Zhu Deng Zi No.10176482 | ||

| 3 | Shuhai information integrated community intelligent management user platform V1.0 | Ruan Zhu Deng Zi No.10176481 | ||

| 4 | Shuhai Information campus cloud security management system V1.0 | Ruan Zhu Deng Zi No.10176483 | ||

| 5 | Shuhai information physical network edge transmission gateway platform V1.0 | Ruan Zhu Deng Zi No.10176478 | ||

| 6 | Shuhai information aggregation message marketing cloud platform V1.0 | Ruan Zhu Deng Zi No.10176528 | ||

| 7 | Shuhai Communication 5G message application management system V1.0 | Ruan Zhu Deng Zi No.10176582 | ||

| 8 | Shuhai Information integrated community group Shopping Mall system V1.0 | Ruan Zhu Deng Zi No.10176530 | ||

| 9 | Shuhai Information online shopping retail service platform V1.0 | Ruan Zhu Deng Zi No.10176529 | ||

| 10 | Shuhai information integrated community intelligent management platform V1.0 | Ruan Zhu Deng Zi No.10176484 | ||

| Software Copyrights owned by Acoustic Effect Technology | ||||

| 1 | High frequency acoustic effect air coupling algorithm software V1.0 | Softcopy Registration No. 9854777 | ||

| 2 | High frequency acoustic effect air coupling and collaborative ultraviolet control algorithm software V1.0 | Softcopy Registration No. 9877299 | ||

| 3 | Variable frequency acoustic effect coronavirus feature elimination algorithm software V1.0 | Softcopy Registration No. 9864534 | ||

| Softcopy Rights owned by Xunrui Techonolgy | ||||

| 1 | Xunruirong media information marketing platform | Softcopy Registration No. 10318231 | ||

| 2 | Xunrui comprehensive online Office OA System | Softcopy Registration No. 10318229 | ||

| 3 | Xunrui integrated security cloud platform | Softcopy Registration No. 10318227 | ||

| 4 | Xunrui Smart Apartment management system | Softcopy Registration No. 10318271 | ||

| 5 | Xunrui Aggregate payment and settlement system | Softcopy Registration No. 10318221 | ||

| 6 | Xunrui AI intelligent algorithm analysis platform | Softcopy Registration No. 10318230 | ||

| 7 | Xunrui intelligent acoustic recognition system | Softcopy Registration No. 10318269 | ||

| 8 | Xunrui Intelligent Park management system | Softcopy Registration No. 10318270 | ||

| 9 | Xunrui Wisdom Catering System | Softcopy Registration No. 10318268 | ||

| 10 | Xunrui satellite remote sensing - Agricultural Management System | Softcopy Registration No. 10318228 | ||

The primary operational goals are with the company’s core digital technology as the benchmark and include the following:

| 1. | To provide best-in-class products and solutions in 5G messaging, acoustic intelligence, and smart city technology. |

| 2. | Increase global sales of acoustic intelligent series hardware products represented by Hailijia Air Purifiers, and the company will soon launch non-contact ultrasonic beauty instruments to meet more home care needs. |

| 3. | Maximize long-term sustainable growth of earnings and operating funds. |

| 4. | Generate cash flows and returns to shareholders. |

28

Business Strategy

The Company intends to accomplish these objectives by diversifying its product portfolio, improving operating efficiency and accelerating market reach and client acquisition.

Datasea believes sustaining growth and remaining competitive depends on leveraging technological innovation to provide customers with more quality and convenient options. With a combination of comprehensive solutions for hardware and software products, Datasea not only can flexibly meet different needs of customers but also serve customers on a large scale. The Company is committed to staying ahead of emerging market trends, creating diverse revenue resources, and continuously improving its business model.

Meanwhile, Datasea is aware of global environmental issues, and the physical and transitional risks a business will be exposed with the global transition to more sustainable and socially responsible economy. To better assess and manage material ESG risks and impacts on stakeholders, as well as identify opportunities to improve sustainability and stakeholder relations. Datasea decided to adopt an ESG analysis framework to understand and mitigate ESG risks, identify opportunities, and make strategic decisions that support long-term success and resilience.

5G Messaging:

Datasea’s VIE entity, Shuhai Beijing, has subsidiaries, Guohao Century (Beijing) Technology Ltd. (“Guohao Century”) and Hangzhou Shuhai Zhangxun Information Technology Co., Ltd. (“Zhangxun”), that increase and improve how people and businesses communicate, while delivering brands a platform to engage, convert and efficiently nurture buying relationships by leveraging 5G messaging service.

The 5G messaging service is known as RCS (“Rich Communication Suite”) and integrates phones, messages, and contacts. Specifically, this communication suite enables users to enjoy various effective interfaces with integrated messages, including texts, pictures, audio, video and emojis, as well as status, location and other communication capabilities. It has the characteristics of high touch rate, rich media, strong interactivity, convenient service, and high security. By using 5G messaging, can serve the individuals, public and thousands of industries.

5G technology can create a new message ecosystem in which customers and enterprises can directly and efficiently connect via short messages on mobile phone terminals. When businesses apply 5G messaging to marketing initiatives, faster speeds, better transmission quality, and lower latency create new and improved customer experience.

As a leading service provider in China’s 5G communication field, Datasea has several primary products and servicies targeting different customers and needs:

| 1. | 5G Message-Marketing Cloud Platform (“5G MMCP”) .

An all-in-one solution for all the communication and marketing needs of merchants and customers from early communication, sales, and later maintenance. The goal is to use data to empower marketing, drive user growth, lead enterprises to achieve digital innovation, and help enterprises create long-term value for customers. |

| 2. | 5G Integrated Messaging Marketing Cloud Platform (“5G IMMCP”).