UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM

For the quarterly period ended

Commission file number

(Exact name of registrant as specified in its charter)

| (State or other jurisdiction of | (I.R.S. Employer | |

| incorporation or organization) | Identification No.) |

|

| ||

| (Address of principal executive offices) | (Zip Code) |

| (Registrant’s telephone number, including area code) |

N/A

(Former name, former address and former fiscal year, if changed since last report)

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol | Name of each exchange on which registered | ||

Indicate by check mark whether the registrant (1) has filed all reports

required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter

period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Indicate by check mark whether the registrant has submitted electronically

every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the

preceding 12 months (or for such shorter period that the registrant was required to submit such files).

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| ☐ | Large accelerated filer | ☐ | Accelerated filer |

| ☒ | Smaller reporting company | ||

| Emerging growth company |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as

defined in Rule 12b-2 of the Exchange Act). Yes ☐ No

As of May 16, 2022,

DATASEA INC.

TABLE OF CONTENTS

| Page No. | ||

| Part I - Financial Information | 1 | |

| Item 1 | Financial Statements | 1 |

| Item 2 | Management’s Discussion and Analysis of Financial Condition and Results of Operations | 24 |

| Item 3 | Quantitative and Qualitative Disclosures about Market Risk | 42 |

| Item 4 | Controls and Procedures | 42 |

| Part II - Other Information | 43 | |

| Item 1 | Legal Proceedings | 43 |

| Item 1A | Risk Factors | 43 |

| Item 2 | Unregistered Sales of Equity Securities and Use of Proceeds | 43 |

| Item 3 | Defaults Upon Senior Securities | 43 |

| Item 4 | Mine Safety Disclosures | 43 |

| Item 5 | Other Information | 43 |

| Item 6 | Exhibits | 43 |

i

PART I - FINANCIAL INFORMATION

DATASEA INC.

CONSOLIDATED FINANCIAL STATEMENTS

FOR THE QUARTERLY PERIOD ENDED MARH 31, 2022

DATASEA INC.

CONSOLIDATED BALANCE SHEETS

| MARCH 31, 2022 | JUNE 30, 2021 | |||||||

| (Unaudited) | ||||||||

| ASSETS | ||||||||

| CURRENT ASSETS | ||||||||

| Cash | $ | $ | ||||||

| Accounts receivable | ||||||||

| Inventory | ||||||||

| Value-added tax prepayment | ||||||||

| Prepaid expenses and other current assets | ||||||||

| Total current assets | ||||||||

| NONCURRENT ASSETS | ||||||||

| Security deposit for rents | ||||||||

| Long term investment | ||||||||

| Property and equipment, net | ||||||||

| Intangible assets, net | ||||||||

| Right-of-use assets, net | ||||||||

| Total noncurrent assets | ||||||||

| TOTAL ASSETS | $ | $ | ||||||

| LIABILITIES AND STOCKHOLDERS’ EQUITY | ||||||||

| CURRENT LIABILITIES | ||||||||

| Accounts payable | $ | $ | ||||||

| Unearned revenue | ||||||||

| Deferred revenue | ||||||||

| Accrued expenses and other payables | ||||||||

| Due to related party | ||||||||

| Loans payable | ||||||||

| Operating lease liabilities | ||||||||

| Total current liabilities | ||||||||

| NONCURRENT LIABILITIES | ||||||||

| Operating lease liabilities | ||||||||

| Total noncurrent liabilities | ||||||||

| TOTAL LIABILITIES | ||||||||

| COMMITMENTS AND CONTINGENCIES | ||||||||

| STOCKHOLDERS’ EQUITY | ||||||||

| Common stock, $ | ||||||||

| Additional paid-in capital | ||||||||

| Accumulated comprehensive income | ||||||||

| Accumulated deficit | ( | ) | ( | ) | ||||

| TOTAL COMPANY STOCKHOLDERS’ EQUITY | ||||||||

| Noncontrolling interest | ( | ) | ( | ) | ||||

| TOTAL EQUITY | ||||||||

| TOTAL LIABILITIES AND EQUITY | $ | $ | ||||||

The accompanying notes are an integral part of these consolidated financial statements.

1

DATASEA INC.

CONSOLIDATED STATEMENTS OF OPERATIONS AND COMPREHENSIVE LOSS

(UNAUDITED)

| NINE MONTHS ENDED MARCH 31, | THREE MONTHS ENDED MARCH 31, | |||||||||||||||

| 2022 | 2021 | 2022 | 2021 | |||||||||||||

| Revenues | $ | $ | $ | $ | ||||||||||||

| Cost of goods sold | ||||||||||||||||

| Gross profit | ||||||||||||||||

| Operating expenses | ||||||||||||||||

| Selling | ||||||||||||||||

| General and administrative | ||||||||||||||||

| Research and development | ||||||||||||||||

| Total operating expenses | ||||||||||||||||

| Loss from operations | ( | ) | ( | ) | ( | ) | ( | ) | ||||||||

| Non-operating income (expenses) | ||||||||||||||||

| Other income (expenses) | ( | ) | ( | ) | ||||||||||||

| Interest income | ||||||||||||||||

| Total non-operating income (expenses), net | ( | ) | ( | ) | ||||||||||||

| Loss before income tax | ( | ) | ( | ) | ( | ) | ( | ) | ||||||||

| Income tax | ||||||||||||||||

| Loss before noncontrolling interest | ( | ) | ( | ) | ( | ) | ( | ) | ||||||||

| Less: (loss) income attributable to noncontrolling interest | ( | ) | ( | ) | ( | ) | ||||||||||

| Net loss to the Company | ( | ) | ( | ) | ( | ) | ( | ) | ||||||||

| Other comprehensive item | ||||||||||||||||

| Foreign currency translation gain (loss) attributable to the Company | ( | ) | ||||||||||||||

| Foreign currency translation gain (loss) attributable to noncontrolling interest | ( | ) | ( | ) | ( | ) | ||||||||||

| Comprehensive loss attributable to the Company | $ | ( | ) | $ | ( | ) | $ | ( | ) | $ | ( | ) | ||||

| Comprehensive loss (income) attributable to noncontrolling interest | $ | ( | ) | $ | ( | ) | $ | $ | ( | ) | ||||||

| Basic and diluted net loss per share | $ | ( | ) | $ | ( | ) | $ | ( | ) | $ | ( | ) | ||||

| Weighted average shares used for computing basic and diluted loss per share | $ | $ | ||||||||||||||

The accompanying notes are an integral part of these consolidated financial statements.

2

DATASEA INC.

CONSOLIDATED STATEMENTS OF CHANGES IN STOCKHOLDERS’ EQUITY

NINE AND THREE MONTHS ENDED MARCH 31, 2022 AND 2021

(Unaudited)

| Accumulated | ||||||||||||||||||||||||||||||||

| Additional | other | |||||||||||||||||||||||||||||||

| Common Stock | paid-in | Statutory | Accumulated | comprehensive | Noncontrolling | |||||||||||||||||||||||||||

| Shares | Amount | capital | reserves | deficit | income | Total | interest | |||||||||||||||||||||||||

| Balance at July 1, 2021 | $ | $ | $ | $ | ( | ) | $ | $ | $ | ( | ) | |||||||||||||||||||||

| Net loss | - | ( | ) | ( | ) | ( | ) | |||||||||||||||||||||||||

| Foreign currency translation loss | - | ( | ) | ( | ) | ( | ) | |||||||||||||||||||||||||

| Issuance of common stock for equity financing | ||||||||||||||||||||||||||||||||

| Shares issued for stock compensation expense | ||||||||||||||||||||||||||||||||

| Balance at September 30, 2021 | ( | ) | ( | ) | ||||||||||||||||||||||||||||

| Net loss | - | ( | ) | ( | ) | ( | ) | |||||||||||||||||||||||||

| Foreign currency translation gain | - | |||||||||||||||||||||||||||||||

| Capital contribution to Shuhai Beijing from a major shareholder | - | |||||||||||||||||||||||||||||||

| Shares issued for paying officers’ accrued salary | ||||||||||||||||||||||||||||||||

| Shares issued for stock compensation expense | ||||||||||||||||||||||||||||||||

| Balance at December 31, 2021 | ( | ) | ( | ) | ||||||||||||||||||||||||||||

| Net loss | - | ( | ) | ( | ) | |||||||||||||||||||||||||||

| Foreign currency translation gain | - | ( | ) | |||||||||||||||||||||||||||||

| Shares issued for stock compensation expense | - | |||||||||||||||||||||||||||||||

| Balance at March 31, 2022 | $ | $ | $ | $ | ( | ) | $ | $ | $ | ( | ) | |||||||||||||||||||||

| Balance at July 1, 2020 | $ | $ | $ | $ | ( | ) | $ | $ | $ | |||||||||||||||||||||||

| Net loss | - | ( | ) | ( | ) | |||||||||||||||||||||||||||

| Foreign currency translation gain | - | |||||||||||||||||||||||||||||||

| Balance at September 30, 2020 | ( | ) | ||||||||||||||||||||||||||||||

| Net loss | - | ( | ) | ( | ) | ( | ) | |||||||||||||||||||||||||

| Foreign currency translation gain | - | ( | ) | |||||||||||||||||||||||||||||

| Issuance of common stock | ||||||||||||||||||||||||||||||||

| Issuance of common stock for subscription agreement entered in prior period | ( | ) | ||||||||||||||||||||||||||||||

| Balance at December 31, 2020 | ( | ) | ( | ) | ||||||||||||||||||||||||||||

| Net loss | - | ( | ) | ( | ) | ( | ) | |||||||||||||||||||||||||

| Foreign currency translation gain | - | ( | ) | ( | ) | ( | ) | |||||||||||||||||||||||||

| Shares issued for stock compensation expense | ||||||||||||||||||||||||||||||||

| Increase of paid-in capital for subscription agreement entered in prior period | - | |||||||||||||||||||||||||||||||

| Balance at March 31, 2021 | $ | $ | $ | $ | ( | ) | $ | $ | $ | ( | ) | |||||||||||||||||||||

The accompanying notes are an integral part of these consolidated financial statements.

3

DATASEA INC.

CONSOLIDATED STATEMENTS OF CASH FLOWS

(UNAUDITED)

| NINE MONTHS ENDED MARCH 31 | ||||||||

| 2022 | 2021 | |||||||

| Cash flows from operating activities: | ||||||||

| Loss including noncontrolling interest | $ | ( | ) | $ | ( | ) | ||

| Adjustments to reconcile loss including noncontrolling interest to net cash used in operating activities: | ||||||||

| Loss on disposal on fixed assets | ||||||||

| Depreciation and amortization | ||||||||

| Bad debt expense | ||||||||

| Operating lease expense | ||||||||

| Stock compensation expense | ||||||||

| Changes in assets and liabilities: | ||||||||

| Accounts receivable | ( | ) | ( | ) | ||||

| Inventory | ( | ) | ( | ) | ||||

| Value-added tax prepayment | ( | ) | ||||||

| Prepaid expenses and other current assets | ( | ) | ( | ) | ||||

| Accounts payable | ||||||||

| Advance from customers | ||||||||

| Accrued expenses and other payables | ||||||||

| Payment on operating lease liabilities | ( | ) | ( | ) | ||||

| Net cash used in operating activities | ( | ) | ( | ) | ||||

| Cash flows from investing activities: | ||||||||

| Acquisition of property and equipment | ( | ) | ( | ) | ||||

| Acquisition of intangible assets | ( | ) | ( | ) | ||||

| Long-term investment | ( | ) | ||||||

| Net cash used in investing activities | ( | ) | ( | ) | ||||

| Cash flows from financing activities: | ||||||||

| Due to related parties | ( | ) | ||||||

| Payment of loan payable | ( | ) | ||||||

| Proceeds from capital contribution from a major shareholder | ||||||||

| Net proceeds from issuance of common stock | ||||||||

| Net cash provided by financing activities | ||||||||

| Effect of exchange rate changes on cash | ||||||||

| Net increase (decrease) in cash | ( | ) | ||||||

| Cash, beginning of period | ||||||||

| Cash, end of period | $ | $ | ||||||

| Supplemental disclosures of cash flow information: | ||||||||

| Cash paid for interest | $ | $ | ||||||

| Cash paid for income tax | $ | $ | ||||||

| Supplemental disclosures of non-cash investing and financing activities: | ||||||||

| Transfer of prepaid software development expenditure to intangible assets | $ | $ | ||||||

| Right-of-use assets obtained in exchange for new operating lease liabilities | $ | $ | ||||||

| Shares issued for accrued bonus to officers | $ | $ | ||||||

The accompanying notes are an integral part of these consolidated financial statements.

4

DATASEA INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

MARCH 31, 2022 AND JUNE 30, 2021

NOTE 1 – ORGANIZATION AND DESCRIPTION OF BUSINESS

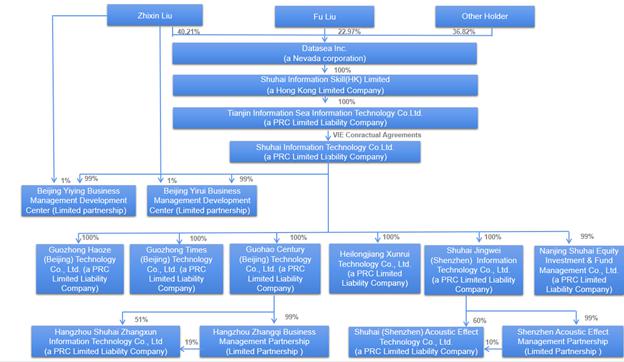

Datasea, Inc. (the “Company” or “Datasea”) is a publicly traded entity with the ticker symbol DTSS on the Nasdaq Capital Market and it was incorporated in Nevada on September 26, 2014. As a holding company with no material operations, the Company conducts a majority of its business activities through organizations established in the People’s Republic of China, or the PRC, primarily by variable interest entity (the “VIE”). The Company does not have any equity ownership of its VIE, instead it controls and receives economic benefits of the VIE’s business operations through certain contractual arrangements. For a description of the Company’s contractual arrangements, please refer to the Company’s annual report on Form 10-K for the year ended June 30, 2021, filed with the Securities and Exchange Commission (the “SEC”) on September 28, 2021.

The vision of Datasea is dedicated in providing advanced technology to business and retail customers. Shuhai Information Technology Co., Ltd. (“Shuhai Beijing”), the VIE that through its various subsidiaries, has cutting-edge technology products and solutions in three industries: 5G messaging, acoustic intelligence and smart city are provided. As of the date of this report, Shuhai Beijing and its subsidiaries own 9 Patents and 53 Software Copyrights, with 12 patent applications pending in core technologies to empower and grow the business.

Impact of Coronavirus Outbreak

In December 2019, a novel strain of coronavirus (COVID-19) was reported, and the World Health Organization declared the outbreak to constitute a “Public Health Emergency of International Concern.” The COVID-19 pandemic has prompted the Company to focus on developing epidemic related products to pursue new business opportunities such as integrating the Company’s security platform and epidemic prevention system for schools and public communities for epidemic prevention. Starting April 2020, the Company resumed normal workflow. Since April 2020 to January 2022, there were some new COVID-19 cases discovered in a few provinces of China, but the number of new cases are not significant due to PRC government’s strict control. Since February 2022, COVID-19 variants cases increased in many cities of China; however, based on available information, management of the Company does not believe that COVID-19 new cases would have a significant impact on the Company’s operations for the rest of fiscal 2022; and does not anticipate any impairment of its assets. Management of the Company believes that its financial resources will be sufficient to handle the challenges associated with COVID-19.

NOTE 2 – SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

GOING CONCERN

The

accompanying unaudited consolidated financial statements (“CFS”) were prepared assuming the Company will continue

as a going concern, which contemplates continuity of operations, realization of assets, and liquidation of liabilities in the normal

course of business. For the nine months ended March 31, 2022 and 2021, the Company had a net loss of approximately

$

5

If deemed necessary, management could seek to raise additional funds by way of private or public offerings, or by seeking to obtain loans from banks or others, to support the Company’s research and development (“R&D”), procurement, marketing and daily operation. While management of the Company believes in the viability of its strategy to generate sufficient revenues and its ability to raise additional funds on reasonable terms and conditions, there can be no assurances to that effect. The ability of the Company to continue as a going concern depends upon the Company’s ability to further implement its business plan and generate sufficient revenue and its ability to raise additional funds by way of a public or private offering. There can be no assurance the Company will be successful in any future fund raising. Based on the Company’s most recent cash flows projection and working capital requirements, management of the Company believes that the Company will be able to continue to operate as a going concern in the foreseeable future and it will have sufficient working capital to meet its operating needs for at least the next 12 months.

BASIS OF PRESENTATION AND CONSOLIDATION

6

VARIABLE INTEREST ENTITY

Pursuant to Financial Accounting Standards Board (“FASB”) Accounting Standards Codification (“ASC”) Section 810, “Consolidation” (“ASC 810”), the Company is required to include in its CFS, the financial statements of Shuhai Beijing, its VIE. ASC 810 requires a VIE to be consolidated if the Company is subject to a majority of the risk of loss for the VIE or is entitled to receive a majority of the VIE’s residual returns. A VIE is an entity in which a company, through contractual arrangements, bears the risk of, and enjoys the rewards normally associated with ownership of the entity, and therefore the Company is the primary beneficiary of the entity.

Under ASC 810, a reporting entity has a controlling financial interest in a VIE, and must consolidate that VIE, if the reporting entity has both of the following characteristics: (a) the power to direct the activities of the VIE that most significantly affect the VIE’s economic performance; and (b) the obligation to absorb losses, or the right to receive benefits, that could potentially be significant to the VIE. The reporting entity’s determination of whether it has this power is not affected by the existence of kick-out rights or participating rights, unless a single enterprise, including its related parties and de - facto agents, have the unilateral ability to exercise those rights. Shuhai Beijing’s actual stockholders do not hold any kick-out rights that affect the consolidation determination.

Through the VIE agreements, the Company is deemed the primary beneficiary of Shuhai Beijing and its subsidiaries. Accordingly, the results of Shuhai Beijing and its subsidiaries were included in the accompanying CFS. Shuhai Beijing has no assets that are collateral for or restricted solely to settle their obligations. The creditors of Shuhai Beijing do not have recourse to the Company’s general credit.

VIE Agreements

Operation

and Intellectual Property Service Agreement – This agreement was entered on October 20, 2015 and allows Tianjin Information

to manage and operate Shuhai Beijing and collect

Shareholders’ Voting Rights Entrustment Agreement – Tianjin Information entered into a shareholders’ voting rights entrustment agreement (the “Entrustment Agreement”) on October 27, 2015, under which Zhixin Liu and Fu Liu (collectively the “Shuhai Beijing Shareholders”) vested their voting power in Shuhai Beijing to Tianjin Information or its designee(s). The Entrustment Agreement does not have an expiration date.

Equity

Option Agreement – the Shuhai Beijing Shareholders and Tianjin Information entered into an equity option agreement

(the “Option Agreement”) on October 27, 2015, pursuant to which the Shuhai Beijing Shareholders granted Tianjin Information

or its designee(s) the irrevocable right and option to acquire all or a portion of Shuhai Beijing Shareholders’ equity interests

in Shuhai Beijing for RMB 0.001 for each capital contribution of RMB 1.00.

Equity Pledge Agreement – Tianjin Information and the Shuhai Beijing Shareholders entered into an equity pledge agreement on October 27, 2015 (the “Equity Pledge Agreement”). The Equity Pledge Agreement guarantees the performance by Shuhai Beijing of its obligations under the Operation and Intellectual Property Service Agreement and the Option Agreement. Pursuant to the Equity Pledge Agreement, Shuhai Beijing Shareholders pledged all of their equity interests in Shuhai Beijing to Tianjin Information. Tianjin Information has the right to collect any and all dividends paid on the pledged equity interests during the pledge period. Pursuant to the terms of the Equity Pledge Agreement, the Shuhai Beijing Shareholders agreed to certain restrictive covenants to safeguard the rights of Tianjin Information. Upon an event of default or certain other agreed events under the Operation and Intellectual Property Service Agreement, the Option Agreement and the Equity Pledge Agreement, Tianjin Information may exercise the right to enforce the pledge.

7

Risk Factors relating to VIE Structure

Datasea Inc., the U.S. parent company, is a holding company with no material operations of its own. The Company conducts its operations in China through its VIE - Shuhai Beijing and its subsidiaries. Investors are not investing in the VIE. Neither the U.S. parent company nor its subsidiaries actually own any share in Shuhai Beijing. Instead, the U.S. parent company controls and receives the economic benefits of Shuhai Beijing business operation through a series of contractual agreements. The Company is subject to certain legal and operational risks associated with being based in China and having a majority of the operations through the contractual arrangements with the VIE. PRC laws and regulations governing the Company’s current business operations are sometimes vague and uncertain, and therefore, these risks may result in a material change in the Company’s operations. The VIE structure is used to replicate foreign investment in Chinese-based companies where Chinese law prohibits direct foreign investment in the operating companies, and that investors may never directly hold equity interests in the Chinese operating entities.

In addition, due to the Company’s corporate structure, the Company is subject to risks due to uncertainty of the interpretation and the application of the PRC laws and regulations, including but not limited to limitation on foreign ownership of internet technology companies, and regulatory review of oversea listing of PRC companies through a special purpose vehicle, and the validity and enforcement of the VIE Agreements.

As of this report date, there was no dividends paid from the VIE to the U.S. parent company or the shareholders of the Company. There has been no change in facts and circumstances to consolidate the VIE. The following financial statement amounts and balances of the VIE were included in the accompanying CFS as of March 31, 2022 and June 30, 2021, and for the nine and three months ended March 31, 2022 and 2021, respectively.

| March 31, 2022 | June 30, 2021 | |||||||

| Cash | $ | $ | ||||||

| Accounts receivable | ||||||||

| Inventory | ||||||||

| Other receivables | ||||||||

| Other current assets | ||||||||

| Total current assets | ||||||||

| Property and equipment, net | ||||||||

| Intangible asset, net | ||||||||

| Right-of-use asset, net | ||||||||

| Other non-current assets | ||||||||

| Total non-current assets | ||||||||

| Total assets | $ | $ | ||||||

| Accounts payable | $ | $ | ||||||

| Accrued liabilities and other payables | ||||||||

| Lease liability | ||||||||

| Loans payable | ||||||||

| Other current liabilities | ||||||||

| Total current liabilities | ||||||||

| Lease liability - noncurrent | ||||||||

| Total non-current liabilities | ||||||||

| Total liabilities | $ | $ | ||||||

8

| For the Nine Months Ended March 31, 2022 | For the Nine Months Ended March 31, 2021 | |||||||

| Revenues | $ | $ | ||||||

| Gross profit | $ | $ | ||||||

| Net income (loss) | $ | $ | ( | ) | ||||

| For the Three Months Ended March 31, 2022 | For the Three Months Ended March 31, 2021 | |||||||

| Revenues | $ | $ | ||||||

| Gross profit | $ | $ | ||||||

| Net income (loss) | $ | $ | ( | ) | ||||

USE OF ESTIMATES

The preparation of CFS in conformity with U.S. GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenues and expenses during the reporting periods. Actual results could differ from those estimates. The significant areas requiring the use of management estimates include, but are not limited to, the estimated useful life and residual value of property, plant and equipment, provision for staff benefits, recognition and measurement of deferred income taxes and the valuation allowance for deferred tax assets. Although these estimates are based on management’s knowledge of current events and actions management may undertake in the future, actual results may ultimately differ from those estimates and such differences may be material to the CFS.

CONTINGENCIES

Certain conditions may exist as of the date the CFS are issued, which may result in a loss to the Company but which will only be resolved when one or more future events occur or fail to occur. The Company’s management and legal counsel assess such contingent liabilities, and such assessment inherently involves an exercise of judgment. In assessing loss contingencies related to legal proceedings that are pending against the Company or unasserted claims that may result in such proceedings, the Company’s legal counsel evaluates the perceived merits of any legal proceedings or unasserted claims as well as the perceived merits of the amount of relief sought or expected to be sought. If the assessment of a contingency indicates that it is probable that a material loss has been incurred and the amount of the liability can be estimated, the estimated liability would be accrued in the Company’s CFS.

If the assessment indicates that a potential material loss contingency is not probable but is reasonably possible, or is probable but cannot be estimated, the nature of the contingent liability, together with an estimate of the range of possible loss if determinable and material, would be disclosed. As of March 31, 2022 and June 30, 2021, the Company has no such contingencies.

CASH AND EQUIVALENTS

Cash and equivalents include cash on hand, demand deposits and short-term cash investments that are highly liquid in nature and have original maturities when purchased of three months or less.

9

INVENTORY

Inventory

is comprised principally of intelligent temperature measurement face recognition terminal and identity information recognition products,

and is valued at the lower of cost or net realizable value. The value of inventory is determined using the first-in, first-out method.

The Company periodically estimates an inventory allowance for estimated unmarketable inventories when necessary. Inventory amounts are

reported net of such allowances. There were $

PROPERTY AND EQUIPMENT

Property and equipment are stated at cost, less accumulated depreciation. Major repairs and improvements that significantly extend original useful lives or improve productivity are capitalized and depreciated over the period benefited. Maintenance and repairs are expensed as incurred. When property and equipment are retired or otherwise disposed of, the related cost and accumulated depreciation are removed from the respective accounts, and any gain or loss is included in operations. Depreciation of property and equipment is provided using the straight-line method over estimated useful lives as follows:

| Furniture and fixtures | ||

| Office equipment | ||

| Vehicles | ||

| Lease improvement |

Leasehold improvements are depreciated utilizing the straight-line method over the shorter of their estimated useful lives or remaining lease term.

INTANGIBLE ASSETS

Intangible assets with finite lives are amortized using the straight-line method over their estimated period of benefit. Evaluation of the recoverability of intangible assets is made to take into account events or circumstances that warrant revised estimates of useful lives or that indicate that impairment exists. All of the Company’s intangible assets are subject to amortization. No impairment of intangible assets has been identified as of the balance sheet date.

Intangible

assets include licenses, certificates, patents and other technology and are amortized over their useful life of

FAIR VALUE (“FV”) OF FINANCIAL INSTRUMENTS

The carrying amounts of certain of the Company’s financial instruments, including cash and equivalents, accrued liabilities and accounts payable, approximate their FV due to their short maturities. FASB ASC Topic 825, “Financial Instruments,” requires disclosure of the FV of financial instruments held by the Company. The carrying amounts reported in the balance sheets for current liabilities qualify as financial instruments and are a reasonable estimate of their FV because of the short period of time between the origination of such instruments and their expected realization and the current market rate of interest.

FAIR VALUE MEASUREMENTS AND DISCLOSURES

FASB ASC Topic 820, “Fair Value Measurements,” defines FV, and establishes a three-level valuation hierarchy for disclosures that enhances disclosure requirements for FV measures. The three levels are defined as follows:

| ● | Level 1 inputs to the valuation methodology are quoted prices (unadjusted) for identical assets or liabilities in active markets. |

| ● | Level 2 inputs to the valuation methodology include other than those in level 1 quoted prices for similar assets and liabilities in active markets, and inputs that are observable for the asset or liability, either directly or indirectly, for substantially the full term of the financial instrument. |

| ● | Level 3 inputs to the valuation methodology are unobservable and significant to the FV measurement. |

10

The carrying value of the Company’s short-term financial instruments, such as cash, accounts receivable, prepaid expenses, accounts payable, advance from customers, accrued expenses and other payables approximates their FV due to their short maturities.

As of March 31, 2022 and June 30, 2021, the Company did not identify any assets or liabilities required to be presented on the balance sheet at FV on a recurring basis.

IMPAIRMENT OF LONG-LIVED ASSETS

In accordance with FASB ASC 360-10, “Accounting for the Impairment or Disposal of Long-Lived Assets”, long-lived assets such as property and equipment are reviewed for impairment whenever events or changes in circumstances indicate that the carrying value of an asset may not be recoverable, or it is reasonably possible that these assets could become impaired as a result of technological or other changes. The determination of recoverability of assets to be held and used is made by comparing the carrying amount of an asset to future undiscounted cash flows expected to be generated by the asset.

If such assets are considered impaired, the impairment to be recognized is measured as the amount by which the carrying amount of the asset exceeds its FV. FV generally is determined using the asset’s expected future undiscounted cash flows or market value, if readily determinable. Assets to be disposed of are reported at the lower of the carrying amount or FV less cost to sell. For the nine and three months ended March 31, 2022 and 2021, there was no impairment loss recognized on long-lived assets.

UNEARNED REVENUE

The Company records payments received in advance from its customers or sales agents for the Company’s products as unearned revenue, mainly consisting of deposits or prepayment for 5G products from the Company’s sales agencies. These orders normally are delivered based upon contract terms and customer demand, and will recognize as revenue when the products are delivered to the end customers.

DEFERRED REVENUE

Deferred revenue consists primarily of local government’s financial support under “2020 Harbin Eyas Plan” to Xunrui for technology innovation of developing the Intelligent Campus Security Management Platform. The Company will record the grant as income when it passes local government’s inspection of the project.

LEASES

The Company determines if an arrangement is a lease at inception under FASB ASC Topic 842. Right of Use Assets (“ROU”) and lease liabilities are recognized at commencement date based on the present value of remaining lease payments over the lease term. For this purpose, the Company considers only payments that are fixed and determinable at the time of commencement. As most of its leases do not provide an implicit rate, it uses its incremental borrowing rate based on the information available at commencement date in determining the present value of lease payments. The Company’s incremental borrowing rate is a hypothetical rate based on its understanding of what its credit rating would be. The ROU assets include adjustments for prepayments and accrued lease payments. The ROU asset also includes any lease payments made prior to commencement and is recorded net of any lease incentives received. The Company’s lease terms may include options to extend or terminate the lease when it is reasonably certain that it will exercise such options.

ROU assets are reviewed for impairment when indicators of impairment are present. ROU assets from operating and finance leases are subject to the impairment guidance in ASC 360, Property, Plant, and Equipment, as ROU assets are long-lived nonfinancial assets.

11

ROU assets are tested for impairment individually or as part of an asset group if the cash flows related to the ROU asset are not independent from the cash flows of other assets and liabilities. An asset group is the unit of accounting for long-lived assets to be held and used, which represents the lowest level for which identifiable cash flows are largely independent of the cash flows of other groups of assets and liabilities. The Company recognized no impairment of ROU assets as of March 31, 2022 and June 30, 2021.

Operating

leases are included in operating lease ROU and operating lease liabilities (current and non-current), on the consolidated balance sheets. As

of March 31, 2022, the net ROU was $

REVENUE RECOGNITION

The Company follows Accounting Standards Codification Topic 606, Revenue from Contracts with Customers (ASC 606).

The core principle underlying FASB ASC 606 is that the Company will recognize revenue to represent the transfer of goods and services to customers in an amount that reflects the consideration to which the Company expects to be entitled in such exchange. This will require the Company to identify contractual performance obligations and determine whether revenue should be recognized at a point in time or over time, based on when control of goods and services transfers to a customer. The Company’s revenue streams are identified when possession of goods and services is transferred to a customer.

FASB ASC Topic 606 requires the use of a new five-step model to recognize revenue from customer contracts. The five-step model requires the Company (i) identify the contract with the customer, (ii) identify the performance obligations in the contract, (iii) determine the transaction price, including variable consideration to the extent that it is probable that a significant future reversal will not occur, (iv) allocate the transaction price to the respective performance obligations in the contract, and (v) recognize revenue when (or as) the Company satisfies each performance obligation.

The Company derives its revenues from product sales and 5G messaging service contracts with its customers, with revenues recognized upon delivery of services and products. Persuasive evidence of an arrangement is demonstrated via product sale contracts and professional service contracts, and invoices. The product selling price and the service price to the customer are fixed upon acceptance of the agreement. The Company recognizes revenue when the customer receives the products and passes the inspection and when professional service is rendered to the customer, collectability of payment is probable. These revenues are recognized at a point in time after all performance obligations are satisfied. Revenue is recognized net of returns and value-added tax charged to customers.

During the

nine and three months ended March 31, 2022, the Company’s revenue of $

12

SEGMENT INFORMATION

FASB ASC Topic 280, “Segment Reporting,” requires use of the “management approach” model for segment reporting. The management approach model is based on the method a company’s management organizes segments within the company for making operating decisions and assessing performance. Reportable segments are based on products and services, geography, legal structure, management structure, or any other manners in which management disaggregates a company. Management determining the Company’s current operations constitutes a single reportable segment in accordance with ASC 280. The Company’s only business and industry segment is high technology and advanced information systems (“TAIS”). TAIS include smart city solutions that meet the security needs of residential communities, schools and commercial enterprises, and 5G messaging services including 5G SMS, 5G MMCP and 5G multi-media video messaging.

All of the Company’s customers are in the PRC and all revenues for the nine and three months ended March 31, 2022 and 2021 were generated from the PRC. All identifiable assets of the Company are located in the PRC. Accordingly, no geographical segments are presented.

INCOME TAXES

The Company uses the asset and liability method of accounting for income taxes in accordance with FASB ASC Topic 740, “Income Taxes.” Under this method, income tax expense is recognized for the amount of: (i) taxes payable or refundable for the current period and (ii) deferred tax consequences of temporary differences resulting from matters that have been recognized in an entity’s financial statements or tax returns. Deferred tax assets also include the prior years’ net operating losses carried forward. Deferred tax assets and liabilities are measured using enacted tax rates expected to apply to taxable income in the years in which those temporary differences are expected to be recovered or settled. The effect on deferred tax assets and liabilities of a change in tax rates is recognized in the results of operations in the period that includes the enactment date. A valuation allowance is provided to reduce the deferred tax assets reported if based on the weight of the available positive and negative evidence, it is more likely than not some portion or all of the deferred tax assets will not be realized.

The Company follows FASB ASC Topic 740, which prescribes a more-likely-than-not threshold for financial statement recognition and measurement of a tax position taken or expected to be taken in a tax return. FASB ASC Topic 740 also provides guidance on recognition of income tax assets and liabilities, classification of current and deferred income tax assets and liabilities, accounting for interest and penalties associated with tax positions, accounting for income taxes in interim periods, and income tax disclosures.

Under the

provisions of FASB ASC Topic 740, when tax returns are filed, it is likely some positions taken would be sustained upon examination by

the taxing authorities, while others are subject to uncertainty about the merits of the position taken or the amount of the position that

would be ultimately sustained. The benefit of a tax position is recognized in the financial statements in the period during which, based

on all available evidence, management believes it is more likely than not that the position will be sustained upon examination, including

the resolution of appeals or litigation processes, if any. Tax positions taken are not offset or aggregated with other positions. Tax

positions that meet the more-likely-than-not recognition threshold are measured as the largest amount of tax benefit that is more than

13

RESEARCH AND DEVELOPMENT EXPENSES

Research and development expenses are expensed in the period when incurred. These costs primarily consist of cost of materials used, salaries paid for the Company’s development department, and fees paid to third parties.

NONCONTROLLING INTERESTS

The Company follows FASB ASC Topic 810, “Consolidation,” governing the accounting for and reporting of noncontrolling interests (“NCIs”) in partially owned consolidated subsidiaries and the loss of control of subsidiaries. Certain provisions of this standard indicate, among other things, that NCI (previously referred to as minority interests) be treated as a separate component of equity, not as a liability, that increases and decreases in the parent’s ownership interest that leave control intact be treated as equity transactions rather than as step acquisitions or dilution gains or losses, and that losses of a partially-owned consolidated subsidiary be allocated to non-controlling interests even when such allocation might result in a deficit balance.

The net income (loss) attributed to NCI was separately designated in the accompanying statements of operations and comprehensive income (loss). Losses attributable to NCI in a subsidiary may exceed a non-controlling interest’s interests in the subsidiary’s equity. The excess attributable to NCIs is attributed to those interests. NCIs shall continue to be attributed their share of losses even if that attribution results in a deficit NCI balance.

As of March 31, 2022, Zhangxun

was

CONCENTRATION OF CREDIT RISK

The Company maintains cash in

accounts with state-owned banks within the PRC. Cash in state-owned banks less than RMB

Cash held in accounts at U.S.

financial institutions is insured by the Federal Deposit Insurance Corporation or other programs subject to certain limitations up to

$

FOREIGN CURRENCY TRANSLATION AND COMPREHENSIVE INCOME (LOSS)

The accounts of the Company’s Chinese entities are maintained in RMB and the accounts of the U.S. parent company are maintained in United States dollar (“USD”). The accounts of the Chinese entities were translated into USD in accordance with FASB ASC Topic 830 “Foreign Currency Matters.” All assets and liabilities were translated at the exchange rate on the balance sheet date; stockholders’ equity is translated at historical rates and the statements of operations and cash flows are translated at the weighted average exchange rate for the period. The resulting translation adjustments are reported under other comprehensive income (loss) in accordance with FASB ASC Topic 220, “Comprehensive Income.” Gains and losses resulting from foreign currency transactions are reflected in the statements of operations.

14

The Company follows FASB ASC Topic 220-10, “Comprehensive Income (loss).” Comprehensive income (loss) comprises net income (loss) and all changes to the statements of changes in stockholders’ equity, except those due to investments by stockholders, changes in additional paid-in capital and distributions to stockholders.

The exchange rates used to translate amounts in RMB to USD for the purposes of preparing the CFS were as follows:

| March 31, | March 31, | June 30, | ||||||||||

| 2022 | 2021 | 2021 | ||||||||||

| Period-end date USD: RMB exchange rate | ||||||||||||

| Average USD for the reporting period: RMB exchange rate | ||||||||||||

BASIC AND DILUTED EARNINGS (LOSS) PER SHARE (EPS)

Basic

EPS is computed by dividing income available to common shareholders by the weighted average number of common shares outstanding for

the period. Diluted EPS is computed similarly, except that the denominator is increased to include the number of additional common

shares that would have been outstanding if the potential common shares had been issued and if the additional common shares were

dilutive. Diluted EPS is based on the assumption that all dilutive convertible shares and stock options were converted or exercised.

Dilution is computed by applying the treasury stock method. Under this method, options and warrants are assumed to have been

exercised at the beginning of the period (or at the time of issuance, if later), and as if funds obtained thereby were used to

purchase common stock at the average market price during the period. For the nine and three months ended March 31, 2021 and 2020,

the Company’s basic and diluted loss per share are the same as a result of the Company’s net loss.

STATEMENT OF CASH FLOWS

In accordance with FASB ASC Topic 230, “Statement of Cash Flows,” cash flows from the Company’s operations are calculated based upon the local currencies. As a result, amounts shown on the statement of cash flows may not necessarily agree with changes in the corresponding asset and liability on the balance sheet.

RECENT ACCOUNTING PRONOUNCEMENTS

In June 2016, the FASB issued ASU No. 2016-13, Financial Instruments-Credit Losses (Topic 326), which requires entities to measure all expected credit losses for financial assets held at the reporting date based on historical experience, current conditions, and reasonable and supportable forecasts. This replaces the existing incurred loss model and is applicable to the measurement of credit losses on financial assets measured at amortized cost. This guidance is effective for fiscal years, and interim periods within those fiscal years, beginning after December 15, 2022. Early application will be permitted for all entities for fiscal years, and interim periods within those fiscal years, beginning after December 15, 2018. The Company is currently evaluating the impact that the standard will have on its CFS.

In August 2020, the FASB issued ASU 2020-06, Debt — Debt with Conversion and Other Options (Subtopic 470-20) and Derivatives and Hedging—Contracts in Entity’s Own Equity (Subtopic 815-40): Accounting for Convertible Instruments and Contracts in an Entity’s Own Equity (“ASU 2020-06”). ASU 2020-06 simplifies the accounting for convertible debt by eliminating the beneficial conversion and cash conversion accounting models. Upon adoption of ASU 2020-06, convertible debt, unless issued with a substantial premium or an embedded conversion feature that is not clearly and closely related to the host contract, will no longer be allocated between debt and equity components. This modification will reduce the issue discount and result in less non-cash interest expense in financial statements. ASU 2020-06 also updates the earnings per share calculation and requires entities to assume share settlement when the convertible debt can be settled in cash or shares. For contracts in an entity’s own equity, the type of contracts primarily affected by ASU 2020-06 are freestanding and embedded features that are accounted for as derivatives under the current guidance due to a failure to meet the settlement assessment by removing the requirements to (i) consider whether the contract will be settled in registered shares, (ii) consider whether collateral is required to be posted, and (iii) assess shareholder rights. ASU 2020-06 is effective for fiscal years beginning after December 15, 2023. Early adoption is permitted, but no earlier than fiscal years beginning after December 15, 2020, and only if adopted as of the beginning of such fiscal year. The Company adopted ASU 2020-06 effective July 1, 2021. The adoption of ASU 2020-06 did not have any impact on the Company’s CFS presentation or disclosures.

15

In May 2021, the FASB issued ASU 2021-04, Earnings Per Share (Topic 260), Debt — Modifications and Extinguishments (Subtopic 470-50), Compensation — Stock Compensation (Topic 718), and Derivatives and Hedging — Contracts in Entity’s Own Equity (Subtopic 815-40): Issuer’s Accounting for Certain Modifications or Exchanges of Freestanding Equity-Classified Written Call Options (“ASU 2021-04”). ASU 2021-04 provides guidance as to how an issuer should account for a modification of the terms or conditions or an exchange of a freestanding equity-classified written call option (i.e., a warrant) that remains classified after modification or exchange as an exchange of the original instrument for a new instrument. An issuer should measure the effect of a modification or exchange as the difference between the fair value of the modified or exchanged warrant and the fair value of that warrant immediately before modification or exchange and then apply a recognition model that comprises four categories of transactions and the corresponding accounting treatment for each category (equity issuance, debt origination, debt modification, and modifications unrelated to equity issuance and debt origination or modification). ASU 2021-04 is effective for all entities for fiscal years beginning after December 15, 2021, including interim periods within those fiscal years. An entity should apply the guidance provided in ASU 2021-04 prospectively to modifications or exchanges occurring on or after the effective date. Early adoption is permitted for all entities, including adoption in an interim period. If an entity elects to early adopt ASU 2021-04 in an interim period, the guidance should be applied as of the beginning of the fiscal year that includes that interim period. The adoption of ASU 2021-04 is not expected to have any impact on the Company’s CFS presentation or disclosures.

The Company’s management does not believe that any other recently issued, but not yet effective, authoritative guidance, if currently adopted, would have a material impact on the Company’s financial statement presentation or disclosures.

NOTE 3 – PROPERTY AND EQUIPMENT

Property and equipment are summarized as follows:

| March 31, 2022 | June 30, 2021 | |||||||

| Furniture and fixtures | $ | $ | ||||||

| Vehicle | ||||||||

| Leasehold improvement | ||||||||

| Office equipment | ||||||||

| Subtotal | ||||||||

| Less: accumulated depreciation | ||||||||

| Total | $ | $ | ||||||

Depreciation for the nine months

ended March 31, 2022 and 2021 was $

Depreciation for the three months

ended March 31, 2022 and 2021 was $

NOTE 4 – INTANGIBLE ASSETS

Intangible assets are summarized as follows:

| March 31, 2022 | June 30, 2021 | |||||||

| Software registration right | $ | $ | ||||||

| Patent | ||||||||

| Software development costs | ||||||||

| Value-added telecommunications business license | ||||||||

| Subtotal | ||||||||

| Less: Accumulated amortization | ||||||||

| Total | $ | $ | ||||||

16

Software registration right represented the purchase cost of customized software with its source code from third party software developer.

Software development cost represented R&D costs incurred internally after the technological feasibility was established and a working model was produced and was recorded as intangible asset.

Amortization for the nine months

ended March 31, 2022 and 2021 was $

Amortization for the three months

ended March 31, 2022 and 2021 was $

NOTE 5 – PREPAID EXPENSES AND OTHER CURRENT ASSETS

Prepaid expenses and other current assets consisted of the following:

| March 31, 2022 | June 30, 2021 | |||||||

| Security deposit | $ | $ | ||||||

| Prepaid expenses | ||||||||

| Prepaid software development | ||||||||

| Prepaid insurance | ||||||||

| Other receivables - Heqin | ||||||||

| Advance from third party individual | ||||||||

| Others | ||||||||

| Total | ||||||||

| Less: allowance for other receivables - Heqin | ||||||||

| Total | $ | $ | ||||||

Other receivables - Heqin

On February

20, 2020,

The cooperation

term is from February 20, 2020 through March 1, 2023; however, Heqin is the exclusive distributor of the Company’s face Recognition

Payment Processing products for the period to July 30, 2020. During March and April 2020, Guozhong Times provided operating funds to Heqin,

together with a credit line provided by Guozhong Times to Heqin from May 2020 through August 2020, for a total borrowing of RMB

No profits

will be allocated and distributed before full repayment of the borrowing. After Heqin pays in full the borrowing, Guozhong Times and Heqin

will distribute profits of sale of Face Recognition Payment Processing equipment and related technical support at

17

As of March

31, 2022 and June 30, 2021, Heqin did not make any repayment to the Company, and the Company made a bad debt allowance of $

NOTE 6 – LONG TERM INVESTMENT

In November, 2021, Shuhai Nanjing invested RMB

NOTE 7 – ACCRUED EXPENSES AND OTHER PAYABLES

Accrued expenses and other payables consisted of the following:

| March 31, 2022 | June 30, 2021 | |||||||

| Other payables | $ | $ | ||||||

| Senior officer’s salary payable | ||||||||

| Salary payable - employees | ||||||||

| Total | $ | $ | ||||||

Other payables mainly consisted of social security and insurance payable.

NOTE 8 – LOANS PAYABLE

As of June 30, 2021, the Company

had several loan agreements with an unrelated party for $

NOTE 9 – RELATED PARTY TRANSACTIONS

In April 2020, the Company’s

CEO entered into a one-year apartment rental agreement with the Company for an apartment located in Harbin city as the Company’s

branch office with an annual rent of RMB

On October 1, 2020, the Company’s

CEO entered into an office rental agreement with Xunrui. Pursuant to the agreement, the Company rents an office in Harbin city with a

total payment of RMB

On July 1, 2021, the Company’s

CEO entered into a car rental agreement with the Company for one year. Pursuant to the agreement, the Company rents a car from the Company’s

CEO for a monthly rent of RMB

18

On September 1, 2021, the Company

renewed a one-year lease for senior officers’ dormitory in Beijing, the monthly rent is RMB

On December 24, 2021, the Company’s

CEO (also the major shareholder of the Company) contributed RMB

Due to related parties

As of March 31, 2022 and June

30, 2021, the Company had due to related parties of $

NOTE 10 – COMMON STOCK AND WARRANTS

Private Placement in October 2020

On October

22, 2020, the Company entered into a common stock purchase agreement with Triton Funds LP (“Triton”). Pursuant to the Purchase

Agreement, subject to certain conditions set forth in the Purchase Agreement, Triton was obligated, pursuant to a purchase notice by the

Company, to purchase up to $

The total number of the shares to be purchased under the Agreement shall not exceed 523,596, or 2.5% of the Company’s outstanding shares of common stock on the Agreement’s execution date, subject to the 9.9% beneficial ownership limitation of the Company’s shares of common stock outstanding by Triton. Closing for sales of common stock will occur no later than three business days following the date on which the Purchased Shares are received by Triton’s custodian. In addition, the Company agreed to (i) at the time of the purchase agreement execution remit $10,000 to Triton, and (ii) at the initial closing pay $5,000 to Triton, to reimburse Triton’s expenses related to the transaction.

On October

29, 2020, the Company issued a notice to sell

Registered Direct Offering and Concurrent Private Placement in July 2021

On July

20, 2021, the Company entered into a securities purchase agreement with certain institutional investors, pursuant to which the Company

agreed to sell to such investors an aggregate of

Concurrently

with the sale of the shares of the common stock, the Company also sold warrants to purchase

19

The closing of the sales of these

securities under the securities purchase agreement took place on July 22, 2021. The net proceeds from the transactions were approximately

$

Following is a summary of the activities of warrants for the period ended March 31, 2022:

| Number of Warrants | Average Exercise Price | Weighted Average Remaining Contractual Term in Years | ||||||||||

| Outstanding as of June 30, 2021 | ||||||||||||

| Exercisable as of June 30, 2021 | ||||||||||||

| Granted | ||||||||||||

| Exercised | - | |||||||||||

| Forfeited | - | |||||||||||

| Expired | - | |||||||||||

| Outstanding as of March 31, 2022 | $ | |||||||||||

| Exercisable as of March 31, 2022 | $ | |||||||||||

Shares to Independent Directors as Compensation

During the

nine months ended March 31, 2022 and 2021, the Company recorded $

Shares to Officers as Compensation

On September 24, 2021, under the 2018 Equity Inventive plan, the Company’s Board of Directors granted 15,000 shares of the Company’s common stock to its CEO each month and 10,000 shares to one of the board members each month staring from July 1, 2021, payable quarterly with the aggregate number of shares for each quarter being issued on the first day of the next quarter at a per share price of the closing price of the day prior to the issuance. During the nine and three months ended March 31, 2022, the Company recorded the fair value of $485,250 and $210,000 stock compensation expense for the shares that are issued to the Company’s CEO and one of the board members for the quarter.

Shares to a Consultant as Compensation

On October

1, 2021, the Company entered into a one-year advisory agreement with a consultant for a monthly compensation of $

20

Shares to Officers in Lieu of Salary Payable

On December

30, 2021, the Board of Directors approved to issue

Amendment for Shares Reserved Under 2018 Equity Incentive Plan

On March 17,

2022, the Board of Directors approved the amendment to the Company’s 2018 Equity Incentive Plan to increase the number of the Company’s

Common Stock to be reserved from

NOTE 11 – INCOME TAXES

The Company is subject to income taxes by entity on income arising in or derived from the tax jurisdiction in which each entity is domiciled. The Company’s PRC subsidiaries file their income tax returns online with PRC tax authorities. The Company conducts all of its businesses through its subsidiaries and affiliated entities, principally in the PRC.

The Company’s

U.S. parent company is subject to U.S. income tax rate of

The Company’s offshore subsidiary, Shuhai Skill (HK), a HK holding company is subject to 16.5% corporate income tax in HK. Shuhai Beijing received a tax holiday with a 15% corporate income tax rate since it qualified as a high-tech company. Tianjin Information, Xunrui, Guozhong Times, Guozhong Haoze, Guohao Century, Jingwei, Shuhai Nanjing, Zhangxun are subject to the regular 25% PRC income tax rate.

As of March

31, 2022 and June 30, 2021, the Company has approximately $

The following table reconciles the U.S. statutory rates to the Company’s effective tax rate for the nine months ended March 31, 2022 and 2021:

| 2022 | 2021 | |||||||

| US federal statutory rates | ( | )% | ( | )% | ||||

| Tax rate difference – current provision | ( | )% | ( | )% | ||||

| Effect of PRC tax holiday | ( | )% | % | |||||

| Valuation allowance | % | % | ||||||

| Effective tax rate | % | % | ||||||

21

The following table reconciles the U.S. statutory rates to the Company’s effective tax rate for the three months ended March 31, 2022 and 2021:

| 2022 | 2021 | |||||||

| US federal statutory rates | ( | )% | ( | )% | ||||

| Tax rate difference – current provision | ( | )% | ( | )% | ||||

| Effect of PRC tax holiday | % | % | ||||||

| Valuation allowance | % | % | ||||||

| Effective tax rate | % | % | ||||||

The Company’s net deferred tax assets as of March 31, 2022 and June 30, 2021 is as follows:

| March 31, 2022 | June 30, 2021 | |||||||

| Deferred tax asset | ||||||||

| Net operating loss | $ | $ | ||||||

| R&D expense | ||||||||

| Accrued expense of officers’ salary | ||||||||

| Depreciation and amortization | ||||||||

| Bad debt expense | ||||||||

| Social security and insurance accrual | ||||||||

| Inventory impairment | ||||||||

| ROU, net of lease liabilities | ||||||||

| Total | ||||||||

| Less: valuation allowance | ( | ) | ( | ) | ||||

| Net deferred tax asset | $ | $ | ||||||

NOTE 12 – COMMITMENTS

Leases

On July 30, 2019, the Company

entered into an operating lease for its office in Beijing.

On July 30, 2019, the Company

entered into a property service agreement for its office in Beijing (described above).

22

The Company adopted FASB ASC Topic 842 on July 1, 2019. The components of lease costs, lease term and discount rate with respect of the Company’s office lease and the senior officers’ dormitory lease with an initial term of more than 12 months are as follows:

| Nine Months Ended March 31, 2022 | Nine Months Ended March 31, 2021 | |||||||

| Operating lease expense | $ | $ | ||||||

| Three Months Ended March 31, 2022 | Three Months Ended March 31, 2021 | |||||||

| Operating lease expense | $ | $ | ||||||

| March 31, 2022 | ||||

| Right-of-use assets | $ | |||

| Lease liabilities - current | ||||

| Lease liabilities - noncurrent | ||||

| Weighted average remaining lease term | ||||

| Weighted average discount rate | % | |||

The following is a schedule, by years, of maturities of the operating lease liabilities as of March 31, 2022:

| 12 Months Ending March 31, | Minimum Lease Payment | |||

| 2023 | $ | |||

| 2024 | ||||

| Total undiscounted cash flows | ||||

| Less: imputed interest | ( | ) | ||

| Present value of lease liabilities | $ | |||

NOTE 13 – SUBSEQUENT EVENTS

The Company follows the guidance

in FASB ASC 855-10 for the disclosure of subsequent events.

23

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

Cautionary Note Regarding Forward-Looking Statements

This report contains forward-looking statements within the meaning of Section 27A of the Securities Act and Section 21E of the Exchange Act. All statements other than statements of historical fact are “forward-looking statements” for purposes of federal and state securities laws, including, but not limited to, any projections of earnings, revenue or other financial items; any statements of the plans, strategies and objectives of management for future operations; any statements concerning proposed new services or developments; any statements regarding future economic conditions of performance; and statements of belief; and any statements of assumptions underlying any of the foregoing. Such forward-looking statements involve known and unknown risks, uncertainties and other factors that may cause our actual results, performance or achievements to be materially different from any future results, performance or achievements expressed or implied by such forward-looking statements.

In some cases, you can identify forward looking statements by terms such as “may,” “intend,” “might,” “will,” “should,” “could,” “would,” “expect,” “believe,” “anticipate,” “estimate,” “predict,” “potential,” or the negative of these terms. These terms and similar expressions are intended to identify forward-looking statements. The forward-looking statements in this report are based upon management’s current expectations and belief, which management believes are reasonable. However, we cannot assess the impact of each factor on our business or the extent to which any factor or combination of factors, or factors we are aware of, may cause actual results to differ materially from those contained in any forward-looking statements. You are cautioned not to place undue reliance on any forward-looking statements. These statements represent our estimates and assumptions only as of the date of this report. Except to the extent required by federal securities laws, we undertake no obligation to update any forward-looking statement to reflect events or circumstances after the date hereof or to reflect the occurrence of unanticipated events.

You should be aware that our actual results could differ materially from those contained in the forward-looking statements due to a number of factors, including:

| ● | uncertainties relating to our ability to establish and operate our business and generate revenue; |

| ● | uncertainties relating to general economic, political and business conditions in China; |

| ● | industry trends and changes in demand for our products and services; |

| ● | uncertainties relating to customer plans and commitments and the timing of orders received from customers; |

| ● | announcements or changes in our advertising model and related pricing policies or that of our competitors; |

| ● | unanticipated delays in the development, market acceptance or installation of our products and services; |

| ● | changes in Chinese government regulations; |

| ● | availability, terms and deployment of capital, relationships with third-party equipment suppliers; and |

| ● | influences of COVID-19 on China’s economy and society. |

Overview

Datasea Inc. (the “Company” or “Datasea”) is a publicly traded entity with the ticker symbol DTSS on the Nasdaq Capital Market. It was incorporated in Nevada on September 26, 2014. As a holding company with no material operations, the Company conducts a majority of business through the organizations established in the People’s Republic of China, or the PRC, primarily by variable interest entity (the “VIE”). The Company does not have any equity ownership of its VIE, instead it controls and receives economic benefits of the VIE’s business operations through certain contractual arrangements.

24

The vision of Datasea is to become a multinational conglomerate in a decade through the mission of innovating and providing advanced technology to a wide range of business customers.

Shuhai Information Technology Co., Ltd. (“Shuhai Beijing”), the VIE that holds its seven subsidiaries, possesses cutting-edge products and solutions in three industries: 5G messaging, acoustic intelligence and smart city. Up to date, Shuhai Beijing and its subsidiaries own 9 Patents and 53 Software Copyrights, with 12 patents applications pending in core technologies to empower and grow our business.

The primary operational goals are to: (i) Provide best-in-class products and solutions in 5G messaging, acoustic intelligence and smart city; (ii) maximize long-term sustainable growth of earnings and operating funds; (iii) generate cash flows and returns to the shareholders. Such objectives will be accomplished by diversifying product portfolio, improving operating efficiency, achieving superior risk-adjusted returns, prudently allocating capital, accelerating market reach and client acquisition.

The metrics for promoting long-term sustainable growth and comparative advantages: (i) leveraging innovation to provide convenience and choice to customers and commit to staying ahead of the emerging market trends. The R&D will be invested consistently and work with the best-in-class research institutes to match the innovative drive with the highest standards of product research and quality. These efforts have been taken into fruition that new launches and upgrades of products in 5G messaging, acoustic intelligence and smart city;(ii) being fast market-movers with great execution, Datasea’s strategic business expansion to 5G messaging and acoustic intelligence all prove the Company is able to identify great opportunities in the market and grasp them with execution;(iii) generating diversified revenue resources and continuous business model improvements. Similar to the importance of diversification to investors, having a diversified product solution can also offset risks and make the company more resilient. Datasea tapped into three different business areas but with great synergies among them. Meanwhile, the Company provides a combination of software and hardware products and solutions which have the flexibility to meet with clients of different needs, but also have the abilities to serve customers at scale. Datasea also keeps improving the business model for having more resources to generate recurring revenues and improve profit margin.

5G Messaging: Fueled by the promising market landscape and sound execution, 5G messaging business sales revenue achieved continuous breakthrough growth in the quarter compared to the same period in fiscal 2021, representing a 12th consecutive month of growth. With the wide acceptance of 5G applications in the nation, especially as China’s three major telecom operators have gradually launched preparations for the commercialization of 5G messaging applications since the beginning of 2022, the popularity of 5G messaging-related services in the Chinese market has gradually increased. According to the news published by Dao Insights on October 4, 2021, the 5G messaging market size of China is estimated to be 300 billion RMB ($46.54 billion) over the next 5 to 7 years.

Enhancements are seen in the product development, customer acquisition, and business model. At present, the Company mainly provides institution customers with three types of services: 5G SMS,5G Integrated message marketing cloud platform (5G IMMCP) and value-added services (5G multimedia video SMS technology system, etc.).The 5G Integrated message marketing cloud platform (“5G IMMCP”), based on 5G message marketing cloud platform (5G MMCP) and the current demand in the Chinese market, expands connection with existing clients through accesses such as SMS, email, WeChat, applet, APP Push and third-party tools and manages users from different platforms all in one 5G IMMCP to form the company’s unique product service capabilities and competitive advantages. As a leading service provider in the field of 5G messaging in China, the number of companies that Datasea provides authorized development of 5G messaging for express delivery, catering, tourism, e-commerce, finance, technology and other industries has increased from about 100 to nearly 200. Datasea’s Business model is built on the seamless and efficient technical support for institutional customers assisting reach to end customers that resulting marketplace effect. This platform, combined with a strong financial position, has continued to drive new customer growth among different regions in China.

25

As the leader in the field of 5G messaging technical supporter in China’s express industry, the Company keeps building momentum and reinforce leadership in the 5G messaging business. Shuhai Beijing cooperated with the National Engineering Laboratory for Logistics Information Technology (“National Engineering Laboratory”) and drafted General Technical Requirements for 5G Messaging Application in Express Industry in China; Shuhai Beijing is one of the directors in the 5G Message Working Group of the Academy of Information and Communications of the Ministry of Industry and Information Technology, a CSP partner of the three major operators, a member of the China Communications Enterprise Association, a member of China Express Association, and a provider of the Tencent Enterprise Microservice. Market recognitions include: Shuhai Beijing assisted ZTO Express and completed the first order of 5G messaging service delivery in China’s express delivery industry; awarded the third place in the 4th National “Blooming Cup” 5G Application Competition and the “Top 10 Enterprises of 5G Messaging in 2021” by New 5G Messaging (New Media) and 5G New Business Center. Being a key player in the 5G messaging business and having the wide product suitability for businesses in different industries may help Shuhai Beijing to continue its growth.

Acoustic Intelligence: Compared with the wide recognition of 5G messaging market potential, Shuhai Beijing and its wholly-owned subsidiary, Shuhai Jingwei (Shenzhen) Information Technology Co., Ltd. (“Shuhai Jingwei”), demonstrates its vision and ability to stay ahead of the emerging market trends in acoustic intelligence. In this quarter, the Company unfolds the acoustic intelligence’s commercial potential and exemplifies how to maximize usage of this technology alone or to upgrade products and solutions in various business areas Shuhai Jingwei commits to tap acoustic intelligence’s full business potential and wields acoustic intelligence across industries in meaningful ways. It sets the goal to become a leading technology and product provider in the field of acoustic intelligence in China and worldwide.

Shuhai Beijing has entered into partnerships with top notch institutions in this area and equipped itself with solid R&D capability. Recently, Shuhai Beijing released China’s inaugural white paper “Industry Development and Technology Application of Acoustic Intelligence in China,” with co-authors, Institute of Cloud Computing and Big Data, China Academy of Information and Communications Technology. The white paper dives into the current and future application cases of acoustic intelligence in China and outlines the introduction of acoustic intelligence, technology development, commercial applications and industrial outlook to provide technical insights and guide industry development. According to the “Feasibility Study Report on China’s Acoustic Device Market 2021-2025” released by Newsijie Research Center, China’s acoustic device market is expected to grow at a compound annual growth rate of 15.6% and reach RMB 46 billion (approximately $7.23 billion) by 2025.

Shuhai Jingwei, a wholly owned subsidiary of Shuhai Beijing, runs the acoustic intelligence business in the Bay Area of Canton-Hong Kong-Macao where is an industry cluster for the benefit of improving the core technology, production, marketing, and logistics. To date, Shuhai Jingwei has completed the technology development, product design, supply chain management and promotion plans for a series of acoustic hardware products in six major industries and application areas, including but not limited to healthcare, medical beauty, environmental protection and agriculture. The four flagship products, including Tianer voice recognition alarm, Ultrasonic sound sterilization and antivirus equipment, Directional sound recognizer, and Brain refreshing acoustic equipment, are expected to be introduced to the market in fiscal year of 2022. Among them, a new JV---Shuhai acoustic effect has jointly launched a logistics virus disinfection channel (the company provides the core ultrasonic sterilization and antivirus components) with its partner institutions 99.99%, reaching the world advanced level.

In order to access the top tier artificial intelligence technology and establish a world class branding, Datasea, the Nevada incorporated company, will be localized in the US for multiple business functions such as design, creation, supply chain management, marketing, sales, and capitalization. By doing so, it will be more efficient to connect with the R&D institutions or to team up with engineering talents in Silicon Valley where the global innovation hub is for developing the most advanced products associated with the Patent Cooperation Treaty to better solve clients’ demand. Also, America has the largest group of abundant consumers with the highest adoption rate of new technology among the world which not only could boost up the revenue, but also can stimulate the value of intangible assets that can help sales expansion all over the world in the coming future. More importantly, the management team strongly believes developing international markets, including the United States, and building a global business structure can change the current single structure in which business revenue is entirely derived from the Chinese market, and improve the single market’s ability to resist risks due to changes and impacts such as policies, epidemics, and inflation, as well as investor information transparency and effective compliance risk reduction. Datasea’s plan to enter the U.S market is pursuant to the growth strategy and commitment to tap acoustic intelligence’s full business potential. The Company plans to introduce in the U.S. the Ultrasonic Sound Sterilization and Antivirus Equipment acoustic intelligence products in agriculture as the first step of the global footprint expansion. The sterilization equipment market is expected to grow at a CAGR of 12% from 2020 to reach 2027 for reaching $23.73 billion. The global smart agricultural market is expected to grow from USD12.9 billion in 2021 to USD 20.8 billion by 2026 at a CAGR of 10.1% according to MarketandMarkets.

26