UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

______________________________________________________

FORM 10-K

______________________________________________________

(Mark One)

| ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the fiscal year ended December 31 , 2022

OR

| TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the transition period from to

Commission file number 000-56050

______________________________________________________

(Exact Name of Registrant as Specified in Its Charter)

______________________________________________________

| (State or Other Jurisdiction of Incorporation or Organization) | (I.R.S. Employer Identification No.) | |||||||

| (Address of Principal Executive Offices) | (Zip Code) | |||||||

(949 ) 417-6500

(Registrant’s Telephone Number, Including Area Code)

______________________________________________________________________

Securities registered pursuant to Section 12(b) of the Act:

| Title of Each Class | Name of Each Exchange on Which Registered | |||||||

| None | None | |||||||

Trading Symbol(s)

______________________________________________________

None

Securities registered pursuant to Section 12(g) of the Act:

Class A common stock, $0.01 par value per share

Class T common stock, $0.01 par value per share

______________________________________________________

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.Yes ¨ No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports) and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes x No ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large Accelerated Filer | ¨ | Accelerated Filer | ¨ | |||||||||||||||||

| ☒ | Smaller reporting company | |||||||||||||||||||

| Emerging growth company | ||||||||||||||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☐

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Securities Exchange Act). Yes ☐ No x

There is no established market for the Registrant’s shares of common stock. On December 6, 2021, the board of directors of the Registrant approved an estimated value per share of its common stock as of September 30, 2021 of $3.38. For a full description of the methodologies used to value the Registrant’s assets and liabilities in connection with the calculation of the estimated value per share as of December 6, 2021, see Part II, Item 5, “Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities - Market Information” of the Registrant’s Annual Report on Form 10-K for the year ended December 31, 2021. On December 15, 2022, the board of directors of the Registrant approved an estimated value per share of its common stock as of September 30, 2022 of $1.16. For a full description of the methodologies used to value the Registrant’s assets and liabilities in connection with the calculation of the estimated value per share as of December 15, 2022, see Part II, Item 5, “Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities - Market Information” in this Annual Report on Form 10-K.

There were approximately 9,791,256 shares of Class A common stock and 310,974 of Class T common stock held by non-affiliates as of June 30, 2022, the last business day of the Registrant’s most recently completed second fiscal quarter.

As of March 6, 2023, there were 9,838,569 outstanding shares of Class A common stock and 307,606 outstanding shares of Class T common stock of the Registrant.

TABLE OF CONTENTS

| ITEM 1. | |||||||||||

| ITEM 1A. | |||||||||||

| ITEM 1B. | |||||||||||

| ITEM 2. | |||||||||||

| ITEM 3. | |||||||||||

| ITEM 4. | |||||||||||

| ITEM 5. | |||||||||||

| ITEM 6. | |||||||||||

| ITEM 7. | |||||||||||

| ITEM 7A. | |||||||||||

| ITEM 8. | |||||||||||

| ITEM 9. | |||||||||||

| ITEM 9A. | |||||||||||

| ITEM 9B. | |||||||||||

| ITEM 9C. | |||||||||||

| ITEM 10. | |||||||||||

| ITEM 11. | |||||||||||

| ITEM 12. | |||||||||||

| ITEM 13. | |||||||||||

| ITEM14. | |||||||||||

| ITEM 15. | |||||||||||

| ITEM 16. | |||||||||||

1

FORWARD-LOOKING STATEMENTS

Certain statements included in this Annual Report on Form 10-K are forward-looking statements. Those statements include statements regarding the intent, belief or current expectations of KBS Growth & Income REIT, Inc. and members of our management team, as well as the assumptions on which such statements are based, and generally are identified by the use of words such as “may,” “will,” “seeks,” “anticipates,” “believes,” “estimates,” “expects,” “plans,” “intends,” “should” or similar expressions. These include statements about our plans, strategies, prospects and the Plan of Liquidation (defined herein) and these statements are subject to known and unknown risks and uncertainties. Readers are cautioned not to place undue reliance on these forward-looking statements. Actual results may differ materially from those contemplated by such forward-looking statements. Further, forward-looking statements speak only as of the date they are made, and we undertake no obligation to update or revise forward-looking statements to reflect changed assumptions, the occurrence of unanticipated events or changes to future operating results over time, unless required by law.

For a discussion of some of the risks and uncertainties, although not all risks and uncertainties, that could cause our actual results to differ materially from those presented in our forward-looking statements, see the risks identified in “Summary Risk Factors” below and in Part I, Item 1A of this Annual Report on Form 10-K (the “Annual Report”).

SUMMARY RISK FACTORS

The following is a summary of the principal risks that could adversely affect our business, financial condition, operations and an investment in our common stock and implementation of the Plan of Liquidation, if approved by our stockholders. This summary highlights certain of the risks that are discussed further in this Annual Report but does not address all the risks that we face. For additional discussion of the risks summarized below and a discussion of other risks that we face, see “Risk Factors” in Part I, Item 1A of this Annual Report. You should interpret many of the risks identified in this summary and under “Risk Factors” as being heightened as a result of the continued disruptions in the financial markets impacting the U.S. commercial real estate industry, especially as it pertains to commercial office buildings.

•The ongoing challenges affecting the U.S. commercial real estate industry, especially as it pertains to commercial office buildings, continues to be one of the most significant risks and uncertainties we face. In particular, the geographic regions where our properties are located have suffered more significant adverse economic effects following the COVID-19 pandemic relative to geographies in other parts of the country. The combination of the continued economic slowdown, rapidly rising interest rates and significant inflation (or the perception that any of these events may continue) as well as a lack of lending activity in the debt markets have contributed to considerable weakness in the commercial real estate markets. Upcoming and recent tenant lease expirations amidst the aforementioned headwinds coupled with slower than expected return-to-office have had direct and material impacts on the value of our real estate and our ability to access the debt markets. Continued disruptions in the financial markets and economic uncertainty could adversely affect our ongoing operations as well as our ability to implement our Plan of Liquidation, if approved by our stockholders, and the liquidation proceeds available for distribution to our stockholders. Further, potential changes in customer behavior, such as the continued acceptance, desirability and perceived economic benefits of work-from-home arrangements, resulting from the COVID-19 pandemic, could materially and negatively impact the future demand for office space, adversely impacting our operations and our ability to implement the proposed Plan of Liquidation and the total return to our stockholders. Moreover, valuations for U.S. office properties continue to fluctuate due to weakness in the current real estate capital markets as a result of the factors above and the lack of transaction volume for U.S. office properties, increasing the uncertainty of valuations in the current market environment.

2

•Although our board of directors has approved the sale of all of our assets and our dissolution pursuant to the terms of a plan of complete liquidation and dissolution (the “Plan of Liquidation”), we can give no assurances whether we will be able to obtain the stockholder approval required to consummate the Plan of Liquidation, or if we do receive such approval, whether we will be able to successfully implement the Plan of Liquidation and sell our assets, pay our debts and distribute the net proceeds from liquidation to our stockholders as we intend. If we are unable to obtain the stockholder approval required to consummate the Plan of Liquidation, we may continue to operate under our current business plan or seek approval of a plan of liquidation at a future date. However, if we are unable to obtain the stockholder approval, we may be unable to meet our maturing debt obligations in the near term, including with respect to the Modified Term Loan maturing in November 2023. If we are unable to meet our payment obligation at maturity because we cannot refinance the Modified Term Loan, the lender could foreclose on the Offices at Greenhouse and the Institute Property, each of which is pledged as collateral to the lender and could potentially pursue damages under the full recourse guaranty provided by KBS GI REIT Properties, LLC (“KBS GI REIT Properties”).

•We can give no assurance regarding the timing of asset dispositions and the sale prices we will receive for assets and the amount and timing of liquidating distributions to be received by our stockholders if the Plan of Liquidation is approved by our stockholders. In particular, our portfolio is highly leveraged and small changes to the values of our real estate assets used to estimate our range in liquidation proceeds have a large impact on our equity and related liquidating distributions to our stockholders.

•We owe substantial fees to and expenses of our advisor and its affiliates. Our advisor and its affiliates have waived some of these fees in connection with the implementation of the Plan of Liquidation. Payment of these fees will be made prior to any liquidating distributions to our stockholders.

•All of our executive officers, one of our directors and other key real estate and debt finance professionals are also officers, directors, managers, key professionals and/or holders of a direct or indirect controlling interest in our advisor, and/or other KBS-affiliated entities. As a result, they face conflicts of interest, including significant conflicts created by our advisor’s and its affiliates’ compensation arrangements with us and other KBS-sponsored programs and KBS-advised investors and conflicts in allocating time among us and these other programs and investors. Although we have adopted corporate governance measures to ameliorate some of the risks posed by these conflicts, these conflicts could result in action or inaction that is not in the best interests of our stockholders.

•As of December 31, 2022, we had a limited portfolio of four real estate investments. As a result, downturns in geographic locations where our properties are located will have a more significant adverse impact on our net asset value than if we had been able to invest in a more diversified investment portfolio. In addition, due to the small size of our limited portfolio, our fixed costs associated with managing the REIT and our portfolio of real estate investments are a large percentage of our net operating income.

•Our advisor waived its asset management fee for the second and third quarters of 2017 and deferred its asset management fee related to the periods from October 2017 through September 30, 2022. In connection with our board of director’s approval of the Plan of Liquidation, our advisor agreed to waive payment of its asset management fee as of October 1, 2022 through our liquidation. In January 2023, our advisor agreed to waive $3.0 million of accrued asset management fees. If our advisor determines to no longer waive or defer certain fees owed to them, our ability to fund our operations and the amount of liquidating distributions to be paid to our stockholders if the Plan of Liquidation is approved by our stockholders may be adversely affected.

•Our policies do not limit us from incurring debt until our aggregate borrowings would exceed 75% of the cost (before deducting depreciation or other non-cash reserves) of our tangible assets, and we may exceed this limit with the approval of the conflicts committee of our board of directors. Our current aggregate borrowings do not exceed this limit based on the cost of our tangible assets. However, as a result of decreased real estate values, we are currently highly leveraged and as a result, the ultimate net proceeds from liquidation paid to stockholders may be significantly impacted by small changes in real estate values as any impact to equity will impact the amount of cash available to make liquidating distributions.

•We have debt obligations with variable interest rates. The interest and related payments will vary with the movement of SOFR or other indexes. Increases in the indexes will increase the amount of our debt payments and limit our ability to pay liquidating distributions to our stockholders.

3

•We depend on tenants for the revenue generated by our real estate investments and, accordingly, the revenue generated by our real estate investments is dependent upon the success and economic viability of our tenants. Revenues from our properties could decrease due to a reduction in occupancy (caused by factors including, but not limited to, tenant defaults, tenant insolvency, early termination of tenant leases and non-renewal of existing tenant leases, which have been more frequent due to the slow return to office resulting from the COVID-19 pandemic), rent deferrals or abatements, tenants becoming unable to pay their rent and/or lower rental rates, making it more difficult for us to meet our debt service obligations and reducing our stockholders’ returns. Further, the resale value of a property depends principally upon the value of the cash flow generated by the leases associated with that property. Non-renewals, terminations or lease defaults could reduce any net sales proceeds received upon the sale of the property and would adversely affect the amount of liquidating distributions our stockholders would receive if the Plan of Liquidation is approved by our stockholders.

•Our investments in real estate may be affected by unfavorable real estate market conditions, the rising interest rate environment, and general economic conditions, which could decrease the value of those assets. Revenues from our properties could decrease. Such events would make it more difficult for us to meet our debt service obligations and successfully implement the Plan of Liquidation, which could in turn reduce our stockholders’ returns and the amount of any liquidating distributions they receive.

•Continued disruptions in the financial markets, including the current economic slowdown, the rising interest rate environment and inflation (or the public perception that any of these events may continue) as well as changes in the demand for office properties and uncertain economic conditions could adversely affect our ability to successfully implement our Plan of Liquidation if approved by our stockholders, which could reduce our stockholders’ returns and the amount of any liquidating distributions they receive.

•Our board of directors terminated our share redemption program, which was only available for death, disability or a determination of incompetence, effective for redemptions in December 2022 and we expect that any future liquidity for our stockholders will be in the form of liquidating distributions.

4

PART I

ITEM 1. BUSINESS

Overview

KBS Growth & Income REIT, Inc. (the “Company”) is a Maryland corporation that elected to be taxed as a real estate investment trust (“REIT”) beginning with the taxable year ended December 31, 2015 and it intends to continue to operate in such a manner. As used herein, the terms “we,” “our” and “us” refer to the Company and as required by context, KBS Growth & Income Limited Partnership, a Delaware limited partnership, which we refer to as our “Operating Partnership,” and to their subsidiaries. Substantially all of our business is conducted through our Operating Partnership, of which we are the sole general partner. Subject to certain restrictions and limitations, our business is externally managed by our advisor pursuant to an advisory agreement. KBS Capital Advisors manages our operations and our portfolio of core real estate properties. KBS Capital Advisors also provides asset-management, marketing, investor-relations and other administrative services on our behalf. Our advisor acquired 20,000 shares of our Class A common stock for an initial investment of $200,000. We have no paid employees.

We commenced capital raising activities in June 2015 with a private placement offering exempt from registration that terminated in April 2016. Immediately following the termination of our private offering, we launched an initial public offering, the primary portion of which terminated in June 2017, with the distribution reinvestment plan offering terminating in August 2020. KBS Capital Markets Group LLC served as dealer manager for the offerings.

In October 2017, we launched a second private placement offering that was suspended in December 2019 and formally terminated in August 2020. We engaged an unaffiliated third-party to act as dealer manager for our second private offering. We raised $94.0 million through the sale of our common stock in our offerings.

As of December 31, 2022, we had redeemed 482,013 and 5,613 Class A and Class T shares, respectively, for $3.9 million. On December 15, 2022, in connection with our approval of the Plan of Liquidation, our board of directors approved the termination of our share redemption program effective December 30, 2022.

We have used substantially all of the net proceeds from our offerings to invest in a portfolio of core real estate properties. We consider core properties to be existing properties with at least 80% occupancy. As of December 31, 2022, we owned four office buildings.

Going Concern Considerations

The accompanying consolidated financial statements and notes have been prepared assuming we will continue as a going concern. We have experienced a decline in occupancy from 90.4% as of December 31, 2020 to 73.0% as of December 31, 2022 and such occupancy may continue to decrease in the future as tenant leases expire due to the slower than expected return-to-office, which has adversely affected our portfolio of commercial office buildings. The decrease in occupancy has resulted in a decrease in cash flow from operations and has negatively impacted the market values of our properties in our portfolio.

As of February 13, 2023, we are in maturity default with respect to the Commonwealth Building Mortgage Loan following our failure to pay the amount outstanding on the loan on its February 1, 2023 due date. Given the reduced rent and occupancy by the building’s tenants, as well as the market conditions in Portland, Oregon, where the property is located, the Commonwealth Building is currently valued at less than the outstanding debt of $46.3 million. Given the depressed office rental rates and the continued social unrest and increased crime in downtown Portland where the property is located, we do not anticipate any near-term recovery in value. We anticipate that we may relinquish ownership of the property to the lender in a foreclosure transaction or other alternative to foreclosure in satisfaction of the mortgage. Additionally, the Modified Term Loan with an outstanding balance of $52.3 million is maturing in November 2023. We do not expect to be able to refinance the Modified Term Loan at current terms and may be required to pay down a portion of the maturing debt in order to refinance the loan. With our limited amount of cash on hand, our ability to make a loan paydown, without the sale of real estate assets, is severely limited. If we are unable to meet our payment obligation at maturity because we cannot refinance the Modified Term Loan, the lender could foreclose on the Offices at Greenhouse and the Institute Property, each of which is pledged as collateral to the lender and could potentially pursue damages under the full recourse guaranty provided by KBS GI REIT Properties. Additionally, in order to attract or retain tenants needed to increase occupancy and sustain operations, we will need to spend a substantial amount on capital leasing costs, however we have limited amounts of liquidity to make these capital commitments. In addition, the fixed costs associated with managing a public REIT, including the significant cost of compliance with all federal, state and local regulatory requirements applicable to us with respect to our business activities, are substantial. These conditions raise substantial doubt about our ability to continue as a going concern. Our ability to continue as a going concern is dependent upon our ability to refinance our mortgage debt or sell the underlying properties prior to debt maturity. No assurances can be given that we will be successful in achieving these objectives.

5

Plan of Liquidation

Our board of directors and a special committee composed of all our independent directors (the “Special Committee”) has approved the sale of all of our assets and our dissolution pursuant to the Plan of Liquidation. The Plan of Liquidation is subject to approval by our stockholders. On February 13, 2023, we commenced distribution of a definitive proxy statement to our stockholders for a liquidation vote to be held on May 9, 2023. The principal purpose of the Plan of Liquidation is to provide liquidity to our stockholders by selling our assets, paying our debts and distributing the net proceeds from liquidation to our stockholders. We can provide no assurances as to the ultimate approval of the Plan of Liquidation by our stockholders or the timing of the liquidation of the company.

If our stockholders approve the Plan of Liquidation, we intend to pursue an orderly liquidation of our company by selling all of our remaining assets, paying our debts and our known liabilities, providing for the payment of unknown or contingent liabilities, distributing the net proceeds from liquidation to our stockholders and winding up our operations and dissolving our company. In the interim, we intend to continue to manage our portfolio of assets to maintain and, if possible, improve the quality and income-producing ability of our properties to enhance property stability and better position our assets for a potential sale.

We cannot complete the sale of all of our assets or our dissolution pursuant to the terms of the Plan of Liquidation unless our stockholders approve the Plan of Liquidation. If the Plan of Liquidation is not approved by our stockholders, our board of directors will meet to determine what other alternatives to pursue in the best interest of the company and our stockholders, including, without limitation, continuing to operate under our current business plan or seeking approval of a plan of liquidation at a future date. However, if we are unable to obtain the stockholder approval, we may be unable to meet our maturing debt obligations in the near term, including with respect to the Modified Term Loan maturing in November 2023. If we are unable to meet our payment obligation at maturity because we cannot refinance the Modified Term Loan, the lender could foreclose on the Offices at Greenhouse and the Institute Property, each of which is pledged as collateral to the lender and could potentially pursue damages under the full recourse guaranty provided by KBS GI REIT Properties.

In connection with its consideration of a plan of liquidation, our board of directors determined to cease regular quarterly distributions with the first quarter of 2022 and terminated the share redemption program effective December 2022. We expect any future liquidity to our stockholders will be provided in the form of liquidating distributions.

Real Estate Portfolio

We have invested in core real estate properties. We acquired our first real estate property on August 12, 2015. As of December 31, 2022, our real estate portfolio, excluding the Commonwealth Building, which we anticipate that we may relinquish to the lender under the mortgage loan secured by the property for the reasons discussed above under “Going Concern Considerations,” was composed of three office buildings containing 374,908 rentable square feet, which were collectively 86.4% occupied. For more information on our real estate investments, including tenant information, see Part I, Item 2, “Properties.”

6

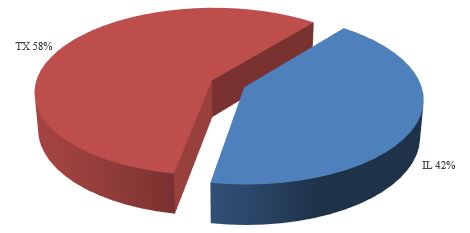

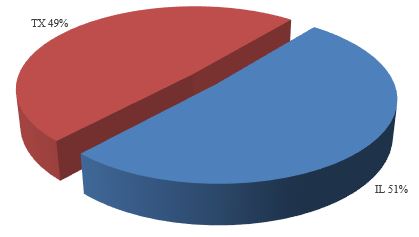

The following charts illustrate the geographic diversification of our real estate properties, excluding the Commonwealth Building, which we anticipate that we may relinquish to the lender under the mortgage loan secured by the property for the reasons discussed above under “Going Concern Considerations,” based on total leased square feet and total annualized base rent as of December 31, 2022:

Leased Square Feet

Annualized Base Rent (1)

_____________________

(1) Annualized base rent represents annualized contractual base rental income as of December 31, 2022, adjusted to straight-line any contractual tenant concessions (including free rent), rent increases and rent decreases from the lease’s inception through the balance of the lease term.

7

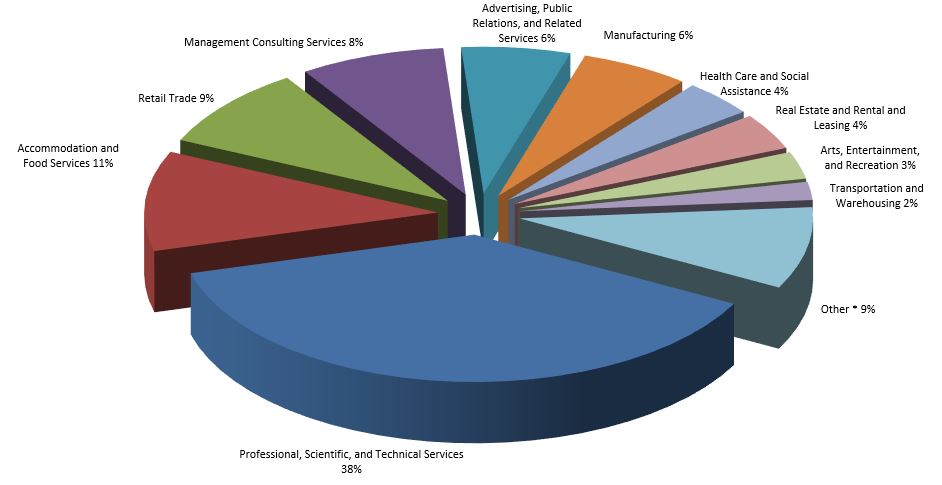

We have a stable tenant base, and we have tried to diversify our tenant base in order to limit exposure to any one tenant or industry. Our top ten tenants leasing space in our real estate portfolio, excluding space at the Commonwealth Building, which we anticipate that we may relinquish to the lender under the mortgage loan secured by the property for the reasons discussed above under “Going Concern Considerations,” represented approximately 75% of our total annualized base rent as of December 31, 2022. The chart below illustrates the diversity of tenant industries in our real estate portfolio based on total annualized base rent as of December 31, 2022:

Annualized Base Rent (1)

_____________________

(1) Annualized base rent represents annualized contractual base rental income as of December 31, 2022, adjusted to straight-line any contractual tenant concessions (including free rent), rent increases and rent decreases from the lease’s inception through the balance of the lease term.

* “Other” includes any industry less than 2% of total.

Financing Objectives

We financed our real estate acquisitions with proceeds raised in our offerings and debt. We use proceeds from borrowings to pay for capital improvements, repairs or tenant build-outs to properties; to refinance existing indebtedness; or to provide working capital and for other liquidity needs.

As of December 31, 2022, we had debt obligations in the aggregate principal amount of $102.2 million, with a weighted-average remaining term of 0.53 years. Of this amount, $46.3 million relates to the mortgage debt on the Commonwealth Building which was in maturity default as of February 13, 2023. Our debt is composed of variable rate notes payable. The weighted-average interest rate of our variable rate debt as of December 31, 2022 was 8.2%. Excluding the Commonwealth Building mortgage loan, the weighted average interest rate of our variable rate debt as of December 31, 2022 was 6.5%. The weighted-average interest rate represents the actual interest rate in effect as of December 31, 2022 (consisting of the contractual interest rate), using interest rate indices as of December 31, 2022, where applicable.

8

The following table shows the current maturities, including principal amortization payments, of our debt obligations as of December 31, 2022 (in thousands):

2023 (1) | $ | 98,603 | ||||||

| 2024 | 3,576 | |||||||

| 2025 | — | |||||||

| 2026 | — | |||||||

| 2027 | — | |||||||

| Thereafter | — | |||||||

| $ | 102,179 | |||||||

_____________________

(1) Amount includes $46.3 million related to Commonwealth Building Mortgage Loan which was in maturity default as of February 13, 2023. We anticipate that we may relinquish the Commonwealth Building to the lender under the mortgage loan for the reasons discussed above under “Going Concern Considerations.”

We expect our debt financing and other liabilities will be between 45% and 65% of the cost of our tangible assets (before deducting depreciation and other non-cash reserves). Though this is our target leverage, our charter does not limit us from incurring debt until our aggregate borrowings would exceed 300% of our net assets (before deducting depreciation and other non-cash reserves), or effectively 75% of the cost of our tangible assets, though we may exceed this limit under certain circumstances. To the extent financing in excess of this limit is available at attractive terms, the conflicts committee may approve debt in excess of this limit. As of December 31, 2022, our aggregate borrowings were approximately 61% of our net assets before deducting depreciation and other non-cash reserves. Due to the current market environment, the value of our assets has been significantly impacted and our aggregate borrowing as a percentage of the current fair value of our assets before depreciation is substantially higher.

Economic Dependency

We depend on our advisor for certain services that are essential to us, including management of the daily operations, leasing and disposition of our portfolio, the implementation of the proposed Plan of Liquidation; and other general and administrative responsibilities. In the event that our advisor is unable to provide these services, we will be required to obtain such services from other sources.

Competitive Market Factors

We face competition from various entities for prospective tenants and to retain our current tenants, including other REITs, pension funds, insurance companies, investment funds and companies, partnerships and developers. Many of these entities have substantially greater financial resources than we do and may be able to accept more risk than we can prudently manage, including risks with respect to the creditworthiness of a tenant. As a result of their greater resources, those entities may have more flexibility than we do in their ability to offer rental concessions to attract and retain tenants. This could put pressure on our ability to maintain or raise rents and could adversely affect our ability to attract or retain tenants. In addition, the COVID-19 pandemic caused many tenants to re-evaluate their space needs, resulting in a significant increase in sublease space available in the office market from tenants wanting to unload un-needed space. We face competition from these tenants, who may be more willing to offer significant discounts to prospective subtenants. As a result, our financial condition, results of operations, cash flow, ability to satisfy our debt service obligations and ability to successfully implement the Plan of Liquidation may be adversely affected.

We also face competition from many of the types of entities referenced above regarding the disposition of properties. These entities may possess properties in similar locations and/or of the same property types as ours and may be attempting to dispose of these properties at the same time we are attempting to dispose of our properties, providing potential purchasers with a larger number of properties from which to choose and potentially decreasing the sales price for such properties. Additionally, these entities may be willing to accept a lower return on their individual investments, which could further reduce the sales price of such properties.

This competition could decrease the sales proceeds we receive for properties that we sell, assuming we are able to sell such properties, which could adversely affect our cash flows and the overall return for our stockholders.

Although we believe that we are well-positioned to compete effectively in each facet of our business, there is enormous competition in our market sector and there can be no assurance that we will compete effectively or that we will not encounter increased competition in the future that could limit our ability to successfully implement the Plan of Liquidation.

9

Compliance with Federal, State and Local Environmental Law

Under various federal, state and local environmental laws, ordinances and regulations, a current or previous real property owner or operator may be liable for the cost of removing or remediating hazardous or toxic substances on, under or in such property. These costs could be substantial. Such laws often impose liability whether or not the owner or operator knew of, or was responsible for, the presence of such hazardous or toxic substances. Environmental laws also may impose liens on property or restrictions on the manner in which property may be used or businesses may be operated, and these restrictions may require substantial expenditures or prevent us from entering into leases with prospective tenants that may be impacted by such laws. Environmental laws provide for sanctions for noncompliance and may be enforced by governmental agencies or, in certain circumstances, by private parties. Certain environmental laws and common law principles could be used to impose liability for the release of and exposure to hazardous substances, including asbestos-containing materials and lead-based paint. Third parties may seek recovery from real property owners or operators for personal injury or property damage associated with exposure to released hazardous substances and governments may seek recovery for natural resource damage. The costs of defending against claims of environmental liability, of complying with environmental regulatory requirements, of remediating any contaminated property, or of paying personal injury, property damage or natural resource damage claims could reduce our cash available for distribution to our stockholders. All of our real estate acquisitions were subject to Phase I environmental assessments prior to acquisition.

Human Capital

We have no paid employees. The employees of our advisor or its affiliates provide management, disposition, advisory and certain administrative services for us.

Principal Executive Office

Our principal executive offices are located at 800 Newport Center Drive, Suite 700, Newport Beach, California 92660. Our telephone number, general facsimile number and website address are (949) 417-6500, (949) 417-6501 and http://www.kbsgireit.com, respectively.

Industry Segments

As of December 31, 2022, we had invested in four office buildings. Substantially all of our revenue and net income (loss) is from real estate, and therefore, we currently operate in one business segment.

Available Information

Access to copies of our annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, proxy statements and other filings with the SEC, including amendments to such filings, may be obtained free of charge from the following website, http://www.kbsgireit.com, through a link to the SEC’s website, http://www.sec.gov. These filings are available promptly after we file them with, or furnish them to, the SEC.

10

ITEM 1A. RISK FACTORS

The following are some of the risks and uncertainties that could cause our actual results, including those related to the Plan of Liquidation if it is approved by our stockholders and our estimated range in liquidating proceeds, to differ materially from those presented in our forward-looking statements. The risks and uncertainties described below are not the only ones we face but do represent those risks and uncertainties that we believe are material to us. Additional risks and uncertainties not presently known to us or that we currently deem immaterial may also harm our business.

Risks Related to the Plan of Liquidation

We can provide no assurances that the Plan of Liquidation will be approved by our stockholders, or if it is, that we will be able to successfully implement the Plan of Liquidation.

Although our board of directors has approved the sale of all of our assets and our dissolution pursuant to the Plan of Liquidation, approval of the Plan of Liquidation requires the affirmative vote of a majority of all of the shares of common stock outstanding, and we can give no assurance that our stockholders will approve the Plan of Liquidation, or if approved, that we will be able to successfully implement the Plan of Liquidation and sell our assets, pay our debts and distribute the net proceeds from liquidation to our stockholders as we expect. Given the uncertainty and current business disruptions as a result of the ongoing challenges affecting the U.S. commercial real estate industry, especially as it pertains to commercial office buildings, including the continued economic slowdown, rapidly rising interest rates and significant inflation (or the perception that any of these events may continue) as well as a lack of lending activity in the debt markets, our implementation of the Plan of Liquidation, if approved by our stockholders, may be materially and adversely impacted.

If the Plan of Liquidation is not approved by our stockholders, our board of directors will meet to determine what other alternatives to pursue in the best interest of the company and our stockholders, including, without limitation, continuing to operate under our current business plan or seeking approval of a plan of liquidation at a future date. However, if we are unable to obtain the stockholder approval, we may be unable to meet our maturing debt obligations in the near term, including with respect to the Modified Term Loan maturing in November 2023. If we are unable to meet our payment obligation at maturity because we cannot refinance the Modified Term Loan, the lender could foreclose on the Offices at Greenhouse and the Institute Property, each of which is pledged as collateral to the lender and could potentially pursue damages under the full recourse guaranty provided by KBS GI REIT Properties.

Our entity value may be adversely affected by adoption of the Plan of Liquidation.

Once our stockholders approve the Plan of Liquidation, we expect to be committed to winding-up our operations. This may adversely affect the value that a potential acquirer might place on the Company. It may also preclude other beneficial courses of action not yet identified by the board of directors.

There can be no assurance that a planned liquidation pursuant to the Plan of Liquidation will maximize stockholder value to a greater extent at this time than would otherwise occur through other alternatives considered by the board of directors and the Special Committee.

If our stockholders approve the Plan of Liquidation, they will no longer participate in any future earnings or benefit from any increases in the value of our properties once such properties are sold. Although the board of directors and the Special Committee each believes that a planned liquidation is in our best interest and the best interest of our stockholders, it is possible that pursuing one or more of the other alternatives considered by the board of directors and the Special Committee would maximize stockholder value to a greater extent at this time. In that case, we will be foregoing those opportunities if we implement the Plan of Liquidation.

In certain circumstances, the board of directors may terminate, amend, modify or delay implementation of the Plan of Liquidation even if it is approved by our stockholders.

The board of directors has adopted and approved the Plan of Liquidation. Nevertheless, prior to the acceptance for record of the Articles of Dissolution by the SDAT, the board of directors may terminate the Plan of Liquidation for any reason, subject to and contingent upon the approval of such termination by our stockholders. Notwithstanding approval of the Plan of Liquidation by our stockholders, the board of directors, or, if a liquidating trust is established, trustees of the liquidating trust, may make certain modifications or amendments to the Plan of Liquidation without further action by or approval of our stockholders to the extent permitted under law. Although the board of directors has no present intention to pursue any alternative to the Plan of Liquidation, the board of directors may conclude that terminating the Plan of Liquidation is in the best interest of the Company and our stockholders. If the board of directors elects to pursue any alternative to the Plan of Liquidation, our stockholders would have to approve the termination of the Plan of Liquidation and may not receive any of the consideration currently estimated to be available for distribution to our stockholders pursuant to the Plan of Liquidation.

11

Our stockholders could, in some circumstances, be held liable for amounts they received from us in connection with our dissolution.

If we fail to create an adequate contingency reserve for payment of our expenses and liabilities, or if we transfer our assets to a liquidating trust and the contingency reserve and the assets held by the liquidating trust are less than the amount ultimately found payable in respect of expenses and liabilities, each of our stockholders could be held liable for the payment to our creditors of such stockholder’s pro rata portion of the excess, limited to the amounts previously received by the stockholder in distributions from us or the liquidating trust, as applicable. If a court holds at any time that we failed to make adequate provision for our expenses and liabilities or if the amount ultimately required to be paid in respect of such liabilities exceeds the amount available from the contingency reserve and the assets of the liquidating trust, our creditors could seek an injunction to prevent us from paying distributions under the Plan of Liquidation on the grounds that the amounts to be distributed are needed to provide for the payment of such expenses and liabilities. Any such action could delay or substantially diminish the amount of liquidating distributions to be paid to our stockholders or holders of beneficial interests of any liquidating trust.

Approval of the Plan of Liquidation may lead to stockholder litigation, which could result in substantial costs and distract our management.

Extraordinary corporate actions by a company, such as our proposed Plan of Liquidation, sometimes lead to lawsuits being filed against that company. We may become involved in this type of litigation in connection with the Plan of Liquidation Proposal. As of the date of this filing, no such lawsuits relative to the Plan of Liquidation were pending or, to our knowledge, threatened. However, if such a lawsuit is filed against us, the litigation could be expensive and divert management’s attention from implementing the Plan of Liquidation.

Pursuing the Plan of Liquidation may cause us to fail to qualify as a REIT, which would dramatically lower the amount of our liquidating distributions.

For so long as we qualify as a REIT and distribute all of our REIT taxable income, we generally are not subject to federal income tax. Although the board of directors does not presently intend to terminate our REIT status prior to paying the final liquidating distribution to our stockholders and our dissolution, the board of directors may take actions pursuant to the Plan of Liquidation that would result in such a loss of REIT status. Upon payment of the final liquidating distribution and our dissolution, our existence and our REIT status will terminate. However, there is a risk that our actions during the liquidation process may cause us to fail to meet one or more of the requirements that must be met in order to qualify as a REIT prior to completion of the Plan of Liquidation. For example, to qualify as a REIT, generally at least 75% of our gross income in each taxable year must come from real estate sources and generally at least 95% of our gross income in each taxable year must come from real estate sources and certain other sources that are itemized in the REIT tax laws, mainly interest and dividends. We may encounter difficulties satisfying these requirements during the liquidation process. In addition, in connection with that process, we may recognize ordinary income in excess of the cash received. The REIT rules require us to pay out a large portion of our ordinary income in the form of a dividend to our stockholders. However, to the extent that we recognize ordinary income without any cash available for distribution, and if we were unable to borrow to fund the required dividend or find another way to meet the REIT distribution requirements, we may cease to qualify as a REIT. Although we expect to comply with the requirements necessary to qualify as a REIT in any taxable year, if we are unable to do so, we will, among other things (unless entitled to relief under certain statutory provisions):

•not be allowed a deduction for dividends paid to stockholders in computing our taxable income;

•be subject to federal income tax, including any applicable alternative minimum tax, on our taxable income, including recognized gains, at regular corporate rates;

•be subject to increased state and local taxes; and

•be disqualified from treatment as a REIT for the taxable year in which we lose our qualification and for the four following taxable years.

As a result of these consequences, our failure to qualify as a REIT could substantially reduce the amount of liquidating distributions we pay to our stockholders.

12

Pursuing the Plan of Liquidation may cause us to be subject to federal income tax, which would reduce the amount of our liquidating distributions.

We generally are not subject to federal income tax to the extent that we distribute to our stockholders during each taxable year (or, under certain circumstances, during the subsequent taxable year) dividends equal to our taxable income for the year. However, we are subject to federal income tax to the extent that our taxable income exceeds the amount of dividends paid to our stockholders for the taxable year. In addition, we are subject to a 4% nondeductible excise tax on the amount, if any, by which certain distributions paid by us with respect to any calendar year are less than the sum of 85% of our ordinary income for that year, plus 95% of our capital gain net income for that year, plus 100% of our undistributed taxable income from prior years. Although we intend to pay distributions to our stockholders sufficient to avoid the imposition of any federal income tax on our taxable income and the imposition of the excise tax, differences in timing between the actual receipt of income and actual payment of deductible expenses, and the inclusion of such income and deduction of such expenses in arriving at our taxable income, could cause us to have to either borrow funds on a short-term basis to meet the REIT distribution requirements, find another alternative for meeting the REIT distribution requirements, or pay federal income and excise taxes. The cost of borrowing or the payment of federal income and excise taxes would reduce the amount of liquidating distributions we pay to our stockholders.

So long as we continue to qualify as a REIT, any net gain from “prohibited transactions” will be subject to a 100% tax. “Prohibited transactions” are sales of property held primarily for sale to customers in the ordinary course of a trade or business. The prohibited transactions tax is intended to prevent a REIT from retaining any profit from the sales of properties held primarily for sale to customers in the ordinary course of business. The Internal Revenue Code of 1986, as amended (the “Code”) provides for a “safe harbor” which, if all its conditions are met, would protect a REIT’s property sales from being considered prohibited transactions. Whether property is held primarily for sale to customers in the ordinary course of a trade or business is a highly factual determination. We believe that all of our properties are held for investment and the production of rental income, and that none of the sales of our properties will constitute a prohibited transaction. We do not believe that the sales of our properties pursuant to the Plan of Liquidation should be subject to the prohibited transactions tax. However, due to the anticipated sales volume and other factors, the contemplated sales may not qualify for the protective safe harbor. There can, however, be no assurances that the U.S. Internal Revenue Service (the “IRS”) will not successfully challenge the characterization of properties we hold for purposes of applying the prohibited transaction tax.

13

Risks Related to an Investment in Our Common Stock

Elevated market and economic volatility due to adverse economic and geopolitical conditions (such as the war in Ukraine), health crisis (such as the continuing impact of the COVID-19 pandemic), concerns over persistent inflation, rising interest rates and slowing economic growth, could have material and adverse effects on our operations including our ability to complete the Plan of Liquidation within our expected timeframe or upon the terms we expect, which could reduce or delay our liquidating distributions.

Our operations, including our ability to successfully implement the Plan of Liquidation and pay liquidating distributions to our stockholders may be adversely affected by market and economic volatility experienced by the U.S. and global economies, the U.S. office market as a whole and/or the local economies in the markets in which our properties are located. Such adverse economic and geopolitical conditions may be due to, among other issues, increased labor market challenges impacting the recruitment and retention of employees, rising inflation and interest rates, volatility in the public equity and debt markets, and international economic and other conditions, including pandemics (such as the continuing impact of the COVID-19 pandemic), geopolitical instability (such as the war in Ukraine), sanctions and other conditions beyond our control. These current conditions, or similar conditions existing in the future, may adversely affect our financial condition and ability to complete the Plan of Liquidation within our expected timeframe or upon the terms we expect as a result of one or more of the following, among other potential consequences:

•revenues from our properties could decrease due to fewer tenants and/or lower rental rates, making it more difficult for us to meet our debt service obligations on debt financing or reducing liquidating distributions available for our stockholders.

•the financial condition of our tenants may be adversely affected, which may result in tenant defaults under leases due to bankruptcy, lack of liquidity, lack of funding, operational failures or for other reasons;

•potential changes in customer behavior, such as the continued acceptance, desirability and perceived economic benefits of work-from-home arrangements, resulting from the COVID-19 pandemic, which could materially and negatively impact the future demand for office space, resulting in slower overall leasing and an adverse impact to our operations and the valuation of our investments;

•significant job losses may occur, which may decrease demand for our office space, causing market rental rates and property values to be negatively impacted;

•our ability to borrow on terms and conditions that we find acceptable, or at all, may be limited, which could reduce our ability to refinance existing debt and increase our future interest expense;

•the ability of potential purchasers of our assets to access the debt markets on favorable terms and conditions may be limited due to the current rising interest rate environment;

•reduced values of our properties and revenues from our properties may (i) limit our ability to dispose of assets at attractive prices, (ii) limit our ability to obtain debt financing secured by our properties, and (iii) reduce the availability of unsecured loans;

•the value and liquidity of our short-term investments and cash deposits could be reduced as a result of a deterioration of the financial condition of the institutions that hold our cash deposits or the institutions or assets in which we have made short-term investments, a dislocation of the markets for our short-term investments, increased volatility in market rates for such investments or other factors; and

•to the extent we enter into derivative financial instruments, one or more counterparties to our derivative financial instruments could default on their obligations to us, or could fail, increasing the risk that we may not realize the benefits of these instruments.

14

Specifically, in order to successfully complete the Plan of Liquidation, we must identify and complete one or more transactions with third parties for the sale of our remaining properties. The success, timing and terms of such transactions may be adversely impacted by the continued impacts of the COVID-19 pandemic on the market for office real estate in the United States. The uncertainty of the long-term demand for office space as employees continue to work from home following the COVID-19 pandemic could result in reduced demand for our properties by third parties or reduced values such parties may ascribe to our assets, as well as potentially affect our own ability to operate. Even if we are able to identify potential buyers, such buyers may have difficulty accessing debt and equity capital on attractive terms, or at all, due to rising interest rates, disruptions in the global financial markets or deteriorations in credit and financing conditions, which may affect their access to capital necessary to consummate the acquisition of our properties. If financing is unavailable to potential buyers of our properties, or if potential buyers are unwilling to engage in various transactions due to the uncertainty in the market, our ability to complete such dispositions within our expected timeframe or on the expected terms would be significantly impaired. In addition, reduced economic activity and general economic decline or recession may impact our tenants’ businesses, financial condition and liquidity and may cause one or more of our tenants to be unable to make rent payments to us timely, or at all. The continuing impact of the COVID-19 pandemic, elevated market and economic volatility due to adverse economic and geopolitical conditions and the impact on potential buyers, our tenants and general economic conditions may adversely affect our ability to close dispositions of our remaining properties and complete our Plan of Liquidation in a timely manner, upon satisfactory terms, or at all, which could cause the liquidating distributions paid to our stockholders to be delayed or reduced.

No public trading market for our shares currently exists and our board of directors has approved the termination of our share redemption program. Therefore, it will be difficult for our stockholders to sell their shares and, if our stockholders are able to sell their shares, they will likely sell them at a loss.

No public market currently exists for our shares. Although the board of directors has approved the Plan of Liquidation, our charter does not require our directors to seek stockholder approval to liquidate our assets and dissolve by a specified date or at all, nor does our charter require our directors to list our shares for trading on a national securities exchange by a specified date or at all. In addition, we can provide no assurances that our stockholders will approve the Plan of Liquidation. Our charter prohibits the ownership of more than 9.8% of our stock by any person, unless exempted by our board of directors, which may inhibit large investors from purchasing our stockholders’ shares. On December 15, 2022, in connection with our approval of the Plan of Liquidation, our board of directors approved the termination of our share redemption program effective December 30, 2022. Therefore, it will be difficult for our stockholders to sell their shares promptly or at all and stockholders likely will not realize the cash value of their shares until we complete our liquidation pursuant to the Plan of Liquidation, provided the Plan of Liquidation is approved by our stockholders. If our stockholders are able to sell their shares, they will likely have to sell them at a loss. It is also likely that our stockholders’ shares will not be accepted as the primary collateral for a loan.

We have a limited portfolio of four real estate investments which may cause the value of our stockholders’ investment in us to fluctuate with the performance of these specific assets and cause our general and administrative expenses to constitute a greater percentage of our revenue.

With a real estate portfolio of four office buildings, we have limited diversification. As a result, downturns in geographic locations where our properties are located or the performance of any single property in the portfolio has a more significant adverse impact on our a stockholders' investment in us than if we had been able to invest in a more diversified investment portfolio. In particular, the Commonwealth Building, which was 42% of our total investments as of December 31, 2022 based on purchase price, and is 37% of its total rentable square feet as of December 31, 2022, is located in Portland, Oregon, a geographic region that has suffered significant and impactful adverse economic developments since the start of the COVID-19 pandemic in 2020. Continued social unrest and increased crime in the downtown Portland area, along with employees continuing to work from home has resulted in many tenants leaving the downtown Portland area for suburban options and resulted in adverse economic consequences for the downtown commercial business district in Portland where the property is located. Occupancy at the Commonwealth Building decreased from 87% at the beginning of 2021 to 51% as of December 31, 2022. Due to these factors, the Commonwealth Building is currently valued at less than the outstanding debt, the borrower is in maturity default on the loan, and we may relinquish ownership of the property to the lender in a foreclosure transaction or other alternative to foreclosure in satisfaction of the mortgage. In addition, the Offices at Greenhouse, another significant property in our portfolio is located in Houston, Texas, where the COVID-19 pandemic added to an already slumping oil and gas industry, resulting in increased vacancy and expanding capitalization rates across the office marketplace. Our stockholders’ investment in our shares will be subject to greater risk to the extent that we lack a diversified portfolio of investments. We have certain fixed operating expenses which will constitute a greater percentage of gross income, reducing our net income and cash flow.

15

Our investment portfolio has limited diversification and downturns relating to certain industries or business sectors or affecting certain tenants may have a more significant adverse impact on our assets than if we had a more diversified investment portfolio.

We have a limited real estate portfolio of four office buildings. As a result, we rely on a limited number of tenants which may be concentrated in a limited number of industries or business sectors. One of our tenants in the engineering industry represented 37% of our annualized base rent, and 36% of the total rentable square feet of our real estate portfolio, as of December 31, 2022, excluding the Commonwealth Building which we anticipate that we may relinquish ownership of to the lender due to the current maturity default on the loan and its value being less than the outstanding debt. Because our portfolio is concentrated in limited industries or business sectors, downturns relating generally to such region, industry or business sector specifically affecting significant tenants may result in defaults on our investments, which may reduce our net income and the value of our common stock.

We may be unable to renew leases, lease vacant space or re-lease space as leases expire, which could adversely affect our business and the implementation of the Plan of Liquidation, if approved by our stockholders.

We seek to renew our leases in the ordinary course of our business. However, we cannot assure our stockholders that we will be able to renew leases or re-lease space at rates equal to or above the current lease rate or at all. Excluding the Commonwealth Building which we anticipate that we may relinquish ownership of to the lender due to the current maturity default on the loan and its value being less than the outstanding debt, approximately 7.1% of our annualized base rent and 5.5% of the total leased square feet of our real estate portfolio, each as of December 31, 2022, is expiring in 2023.

In calculating our range of estimated net proceeds from liquidation, we assumed that we would not experience significant lease terminations not currently known to us and that we would not experience any significant unknown tenant defaults during the liquidation process that were not subsequently cured. Any currently known lease expirations and non-renewals of tenant leases were considered in calculating our range of estimated net proceeds from liquidation. Significant unknown lease terminations and/or tenant defaults during the liquidation process, would adversely affect the resale value of the properties, which would reduce our range of estimated net proceeds from liquidation. To the extent that we receive less rental income than we expect during the liquidation process, our liquidating distributions will be reduced. We may also decide in the event of a tenant default to restructure the lease, which could require us to substantially reduce the rent payable to us under the lease, or make other modifications that are unfavorable to us.

We depend on our advisor and its affiliates to conduct our operations and implement the Plan of Liquidation. Adverse changes in the financial health of our advisor or the loss of or the inability of our advisor to retain or obtain key real estate and debt finance professionals could delay or hinder implementation of the Plan of Liquidation and our operations, which could limit our ability to make liquidating distributions to our stockholders or otherwise decrease the value of an investment in our shares.

Our success depends to a significant degree upon our advisor and the contributions of Mr. Schreiber, who would be difficult to replace. Neither we nor our affiliates have employment agreements with Mr. Schreiber and he may not remain associated with us, our advisor or its affiliates. If Mr. Schreiber were to cease his association with us, our advisor or its affiliates, we may be unable to find a suitable replacement and our operating results and ability to implement the Plan of Liquidation could suffer as a result. We believe that the successful implementation of the Plan of Liquidation depends, in large part, upon our advisor’s and its affiliates’ financial health and ability to attract and retain highly skilled managerial, operational and marketing professionals. Competition for such professionals is intense, and our advisor and its affiliates may be unsuccessful in attracting and retaining such skilled professionals. If we lose or are unable to obtain the services of highly skilled professionals our ability to implement the Plan of Liquidation, if approved, and our operations could be delayed or hindered, reducing the amount of liquidating distributions our stockholders receive and their overall return on investment.

Our rights and the rights of our stockholders to recover claims against our independent directors are limited, which could reduce our stockholders’ and our recovery against our independent directors if they negligently cause us to incur losses.

Maryland law provides that a director has no liability in that capacity if he or she performs his or her duties in good faith, in a manner he or she reasonably believes to be in our best interests and with the care that an ordinarily prudent person in a like position would use under similar circumstances. Our charter provides that none of our independent directors shall be liable to us or our stockholders for monetary damages and that we will generally indemnify them for losses unless they are grossly negligent or engage in willful misconduct. As a result, our stockholders and we may have more limited rights against our independent directors than might otherwise exist under common law, which could reduce our stockholders’ and our recovery from these persons if they act in a negligent manner. In addition, we may be obligated to fund the defense costs incurred by our independent directors (as well as by our other directors, officers, employees (if we ever have employees) and agents) in some cases, which would reduce the amount of liquidating distributions our stockholders receive and their overall return on investments.

16

Risks Related to Conflicts of Interest

Our advisor and its affiliates, including all of our executive officers, our affiliated director and other key real estate and debt finance professionals, face conflicts of interest caused by their compensation arrangements with us and with other KBS-sponsored programs, which could result in actions that are not in the best interests of our stockholders.

All of our executive officers, our affiliated director and other key real estate and debt finance professionals are also officers, directors, managers, key professionals and/or holders of a direct or indirect controlling interest in our advisor, and/or other KBS-affiliated entities. Subject to limitations in our charter and approval by our conflicts committee, KBS Capital Advisors and its affiliates receive fees from us. These fees could influence our advisor’s advice to us as well as the judgment of its affiliates. Among other matters, these compensation arrangements could affect their judgment with respect to their support of the Plan of Liquidation and may cause them to manage our liquidation in a manner not solely in the best interest of our stockholders. Some of the conflicts of interest presented by the liquidation are summarized below.

•All of our executive officers, including Messrs. Schreiber and Waldvogel and Ms. Yamane, are officers of our advisor and/or one or more of our advisor’s affiliates and are compensated by those entities, in part, for their service rendered to us. We currently do not pay any direct compensation to our executive officers. Mr. Schreiber is also one of our directors.

•Our advisor earns asset management fees from us and receives reimbursement of certain of its operating costs. Our advisor has agreed to waive payment of its asset management fee as of October 1, 2022 through our liquidation. Our advisor will receive reimbursements for expenses until our liquidation and dissolution are complete. As of September 30, 2022, we had accrued and deferred payment of $8.9 million of asset management fees related to the period from October 2017 through September 2022. In January 2023, our advisor waived $3.0 million of accrued asset management fees. As a result, $5.9 million of fees will be repaid to our advisor with the liquidation proceeds prior to any distributions to stockholders.

•The Advisor owns a total of 20,404 shares of our Class A common stock, for which we estimate it will receive liquidating distributions of between approximately $8,774 and $20,404 in connection with our liquidation.

•Not including the 20,404 shares owned by our advisor referenced above, one of our directors owns an aggregate of 39,392 shares of our Class A common stock, for which we estimate he will receive aggregate liquidating distributions of between approximately $16,939 and $39,392 in connection with our liquidation.

Consequently, some of our directors and officers and our advisor, in some instances, may be more motivated to support the Plan of Liquidation than might otherwise be the case if they did not expect to receive those payments. Additionally, because of the above potential conflicts of interest, our directors, our officers and our advisor may be motivated to make decisions or take actions based on factors other than the best interest of our stockholders throughout the liquidation process.

Our advisor and its affiliates face potential conflicts of interest relating to the leasing and disposition of properties due to their relationship with other KBS-sponsored programs and/or KBS-advised investors, which could result in decisions that are not in our best interest or the best interests of our stockholders.

We and other KBS-sponsored programs and KBS-advised investors rely on our sponsor, KBS Holdings LLC, our advisor, KBS Capital Advisors, and other key real estate and debt finance professionals at our advisor, including Mr. Schreiber, to supervise the property management and leasing of properties. If the KBS team of real estate professionals directs creditworthy prospective tenants to properties owned by another KBS-sponsored program or KBS-advised investor when it could direct such tenants to our properties, our tenant base may have more inherent risk and our properties’ occupancy may be lower than might otherwise be the case.

In addition, we and other KBS-sponsored programs and KBS-advised investors rely on our sponsor and other key real estate professionals at our advisor to sell our properties. These KBS-sponsored programs and KBS-advised investors may possess properties in similar locations and/or of the same property types as ours and may be attempting to sell these properties at the same time we are attempting to sell some of our properties. If our advisor directs potential purchasers to properties owned by another KBS-sponsored program or KBS-advised investor when it could direct such purchasers to our properties, we may be unable to sell some or all of our properties at the time or at the price we otherwise would, which could reduce the amount of liquidating distributions our stockholders receive and their overall return on investment.

17

All of our executive officers, our affiliated director and the key real estate and debt finance professionals assembled by our advisor face conflicts of interest related to their positions and/or interests in KBS Capital Advisors and its affiliates, which could hinder our ability to implement our business strategy and the Plan of Liquidation.

All of our executive officers, our affiliated director and the key real estate and debt finance professionals assembled by our advisor are also executive officers, directors, managers, key professionals and/or holders of a direct or indirect controlling interest in our advisor and/or other KBS-affiliated entities. Through KBS-affiliated entities, some of these persons also serve as the investment advisors to KBS-advised investors and, through KBS Capital Advisors and KBS Realty Advisors, these persons serve as the advisor to KBS REIT II, KBS REIT III, and other KBS-sponsored programs. In addition, KBS Realty Advisors serves as the U.S. asset manager for Prime U.S. REIT, a real estate investment trust affiliated with Mr. Schreiber. As a result, they owe fiduciary duties to each of these entities, their stockholders, members and limited partners and these investors, which fiduciary duties may from time to time conflict with the fiduciary duties that they owe to us and our stockholders. Their loyalties to these other entities and investors could result in action or inaction that is detrimental to our business, which could harm the implementation of our business strategy. Further, Mr. Schreiber and existing and future KBS-sponsored programs and KBS-advised investors generally are not and will not be prohibited from engaging, directly or indirectly, in any business or from possessing interests in any other business venture or ventures, including businesses and ventures involved in the acquisition, development, ownership, leasing or sale of real estate investments. If we do not successfully implement our business strategy or the Plan of Liquidation, the amount of liquidating distributions our stockholders receive and their overall return on investment may be reduced.

Our affiliated director’s loyalties to KBS REIT II, KBS REIT III and possibly to future KBS-sponsored programs could influence his judgment, resulting in actions that may not be in our stockholders’ best interest or that result in a disproportionate benefit to another KBS-sponsored program at our expense.

Our affiliated director is also an affiliated director of KBS REIT II and KBS REIT III. The loyalties of our director serving on the boards of directors of KBS REIT II and KBS REIT III, or possibly on the boards of directors of future KBS-sponsored programs, may influence the judgment of our affiliated director when considering issues for us that also may affect other KBS-sponsored and advised programs. A decision of our board regarding the timing of property sales could be influenced by concerns that the sales would compete with those of other KBS-sponsored programs. We could enter into transactions with other KBS-sponsored programs, such as property sales or financing arrangements. Such transactions might entitle our advisor or its affiliates to fees and other compensation from both parties to the transaction. For example, property sales to other KBS-sponsored programs might entitle our advisor or its affiliates to acquisition fees in connection with its services to the purchaser. Decisions of our board regarding the terms of those transactions may be influenced by our board’s loyalties to such other KBS-sponsored programs.

Risks Related to Our Corporate Structure

Our charter limits the number of shares a person may own, which may discourage a takeover that could otherwise result in a premium price to our stockholders.

Our charter, with certain exceptions, authorizes our directors to take such actions as are necessary and desirable to preserve our qualification as a REIT. To help us comply with the REIT ownership requirements of the Internal Revenue Code, our charter prohibits a person from directly or constructively owning more than 9.8% of our outstanding shares, unless exempted by our board of directors. This restriction may have the effect of delaying, deferring or preventing a change in control of us, including an extraordinary transaction (such as a merger, tender offer or sale of all or substantially all of our assets) that might provide a premium price for holders of our common stock.

Our charter permits our board of directors to issue stock with terms that may subordinate the rights of our common stockholders or discourage a third party from acquiring us in a manner that could result in a premium price to our stockholders.