OSISKO GOLD ROYALTIES LTD

. . . . . . . . . . . . . . . . . .

Consolidated Financial Statements

For the years

ended

December 31, 2021 and 2020

|

Osisko Gold Royalties Ltd Consolidated Financial Statements |

Management's Report on Internal Control over Financial Reporting

Osisko Gold Royalties Ltd's (the "Company's") management is responsible for establishing and maintaining adequate internal control over financial reporting, as defined in rules 13a-15(f) and 15d-15(f) under the Securities Exchange Act of 1934 (United States), as amended.

The Company's management assessed the effectiveness of the Company's internal control over financial reporting as at December 31, 2021. The Company's management conducted an evaluation of the Company's internal control over financial reporting based on criteria established in Internal Control - Integrated Framework (2013) issued by the Committee of Sponsoring Organizations of the Treadway Commission (COSO). Based on the Company's management's assessment, the Company's internal control over financial reporting is effective as at December 31, 2021.

The effectiveness of the Company's internal control over financial reporting as at December 31, 2021 has been audited by PricewaterhouseCoopers LLP, Independent Registered Public Accounting Firm, as stated in their report which is located on the next pages.

| (signed) Sandeep Singh, Chief Executive Officer | (signed) Frédéric Ruel, Chief Financial Officer |

February 24, 2022

Report of Independent Registered Public Accounting Firm

To the Board of Directors and Shareholders of Osisko Gold Royalties Ltd

Opinions on the Financial Statements and Internal Control over Financial Reporting

We have audited the accompanying consolidated balance sheets of Osisko Gold Royalties Ltd and its subsidiaries (together, the Company) as of December 31, 2021 and 2020, and the related consolidated statements of income (loss), comprehensive income (loss), changes in equity and cash flows for the years then ended, including the related notes (collectively referred to as the consolidated financial statements). We also have audited the Company's internal control over financial reporting as of December 31, 2021, based on criteria established in Internal Control - Integrated Framework (2013) issued by the Committee of Sponsoring Organizations of the Treadway Commission (COSO).

In our opinion, the consolidated financial statements referred to above present fairly, in all material respects, the financial position of the Company as of December 31, 2021 and 2020, and its financial performance and its cash flows for the years then ended in conformity with International Financial Reporting Standards as issued by the International Accounting Standards Board. Also in our opinion, the Company maintained, in all material respects, effective internal control over financial reporting as of December 31, 2021, based on criteria established in Internal Control - Integrated Framework (2013) issued by the COSO.

Basis for Opinions

The Company's management is responsible for these consolidated financial statements, for maintaining effective internal control over financial reporting, and for its assessment of the effectiveness of internal control over financial reporting, included in the accompanying Management's Report on Internal Control over Financial Reporting. Our responsibility is to express opinions on the Company's consolidated financial statements and on the Company's internal control over financial reporting based on our audits. We are a public accounting firm registered with the Public Company Accounting Oversight Board (United States) (PCAOB) and are required to be independent with respect to the Company in accordance with the U.S. federal securities laws and the applicable rules and regulations of the Securities and Exchange Commission and the PCAOB.

We conducted our audits in accordance with the standards of the PCAOB. Those standards require that we plan and perform the audits to obtain reasonable assurance about whether the consolidated financial statements are free of material misstatement, whether due to error or fraud, and whether effective internal control over financial reporting was maintained in all material respects.

Our audits of the consolidated financial statements included performing procedures to assess the risks of material misstatement of the consolidated financial statements, whether due to error or fraud, and performing procedures that respond to those risks. Such procedures included examining, on a test basis, evidence regarding the amounts and disclosures in the consolidated financial statements. Our audits also included evaluating the accounting principles used and significant estimates made by management, as well as evaluating the overall presentation of the consolidated financial statements. Our audit of internal control over financial reporting included obtaining an understanding of internal control over financial reporting, assessing the risk that a material weakness exists, and testing and evaluating the design and operating effectiveness of internal control based on the assessed risk. Our audits also included performing such other procedures as we considered necessary in the circumstances. We believe that our audits provide a reasonable basis for our opinions.

Definition and Limitations of Internal Control over Financial Reporting

A company's internal control over financial reporting is a process designed to provide reasonable assurance regarding the reliability of financial reporting and the preparation of financial statements for external purposes in accordance with generally accepted accounting principles. A company's internal control over financial reporting includes those policies and procedures that (i) pertain to the maintenance of records that, in reasonable detail, accurately and fairly reflect the transactions and dispositions of the assets of the company; (ii) provide reasonable assurance that transactions are recorded as necessary to permit preparation of financial statements in accordance with generally accepted accounting principles, and that receipts and expenditures of the company are being made only in accordance with authorizations of management and directors of the company; and (iii) provide reasonable assurance regarding prevention or timely detection of unauthorized acquisition, use, or disposition of the company's assets that could have a material effect on the financial statements.

Because of its inherent limitations, internal control over financial reporting may not prevent or detect misstatements. Also, projections of any evaluation of effectiveness to future periods are subject to the risk that controls may become inadequate because of changes in conditions, or that the degree of compliance with the policies or procedures may deteriorate.

Critical Audit Matters

The critical audit matter communicated below is a matter arising from the current period audit of the consolidated financial statements that was communicated or required to be communicated to the audit committee and that (i) relates to accounts or disclosures that are material to the consolidated financial statements and (ii) involved our especially challenging, subjective, or complex judgments. The communication of critical audit matters does not alter in any way our opinion on the consolidated financial statements, taken as a whole, and we are not, by communicating the critical audit matter below, providing a separate opinion on the critical audit matter or on the accounts or disclosures to which it relates.

Assessment of impairment indicators of royalty, stream and other interests

As described in Notes 3, 5 and 14 to the consolidated financial statements, the Company's royalty, stream and other interests carrying amount was $1,154.8 million as of December 31, 2021. Management assesses at each reporting date whether there are indicators that the carrying amount may not be recoverable which give rise to the requirement to conduct a formal impairment test. Impairment is assessed at the cash-generating unit (CGU) level, which is usually at the individual royalty, stream and other interest level for each property from which cash inflows are generated. Management uses judgement when assessing whether there are indicators of impairment, including a significant change in mineral reserve and resources, significant negative industry or economic trends, significantly lower production than expected, a significant change in current or forecast commodity prices and other relevant operator and financial information.

The principal considerations for our determination that performing procedures relating to the assessment of impairment indicators of royalty, stream and other interests is a critical audit matter are (i) the judgement by management when assessing whether there were indicators of impairment which would require a formal impairment test to be performed; and (ii) a high degree of auditor judgement, subjectivity and effort in performing procedures to evaluate audit evidence related to management's assessment of impairment indicators related to a significant change in mineral reserve and resources, significant negative industry or economic trends, significantly lower production than expected, a significant change in current or forecast commodity prices and other relevant operator and financial information.

Addressing the matter involved performing procedures and evaluating audit evidence in connection with forming our overall opinion on the consolidated financial statements. These procedures included testing the effectiveness of controls relating to management's assessment of impairment indicators of royalty, stream and other interests. These procedures also included, among others, evaluating the reasonableness of management's assessment of impairment indicators for a sample of royalty, stream and other interests, related to a significant change in mineral reserve and resources, significant negative industry or economic trends, significantly lower production than expected, a significant drop in current or forecast commodity prices and other relevant operator and financial information by considering (i) current and past performance of royalty, stream and other interests; (ii) consistency with external market and industry data; (iii) publicly disclosed or other relevant information of operators of royalty, stream and other interests; and (iv) consistency with evidence obtained in other areas of the audit.

/s/PricewaterhouseCoopers LLP1

Montréal, Canada

February 24, 2022

We have served as the Company's auditor since 2006.

_________________________

1 CPA auditor, CA, public accountancy permit No. A123475

|

Osisko Gold Royalties Ltd Consolidated Balance Sheets As at December 31, 2021 and 2020 |

|

(tabular amounts expressed in thousands of Canadian dollars) |

| December 31, | December 31, | ||||||||

| 2021 | 2020 | ||||||||

| Notes | $ | $ | |||||||

| Assets | |||||||||

| Current assets | |||||||||

| Cash | 8 | 115,698 | 302,524 | ||||||

| Short-term investments | 9 | - | 3,501 | ||||||

| Amounts receivable | 10 | 14,691 | 12,894 | ||||||

| Inventories | 11 | 18,596 | 10,025 | ||||||

| Other assets | 11 | 3,941 | 6,244 | ||||||

| 152,926 | 335,188 | ||||||||

| Non-current assets | |||||||||

| Investments in associates | 12 | 125,354 | 119,219 | ||||||

| Other investments | 13 | 169,010 | 157,514 | ||||||

| Royalty, stream and other interests | 14 | 1,154,801 | 1,116,128 | ||||||

| Mining interests and plant and equipment | 15 | 635,655 | 489,512 | ||||||

| Exploration and evaluation | 16 | 3,635 | 42,519 | ||||||

| Goodwill | 17 | 111,204 | 111,204 | ||||||

| Other assets | 11 | 18,037 | 25,820 | ||||||

| 2,370,622 | 2,397,104 | ||||||||

| Liabilities | |||||||||

| Current liabilities | |||||||||

| Accounts payable and accrued liabilities | 18 | 30,049 | 46,889 | ||||||

| Dividends payable | 21 | 9,157 | 8,358 | ||||||

| Provisions and other liabilities | 19 | 12,179 | 4,431 | ||||||

| Current portion of long-term debt | 20 | 294,891 | 49,867 | ||||||

| 346,276 | 109,545 | ||||||||

| Non-current liabilities | |||||||||

| Provisions and other liabilities | 19 | 60,334 | 41,536 | ||||||

| Long-term debt | 20 | 115,544 | 350,562 | ||||||

| Deferred income taxes | 24 | 68,407 | 54,429 | ||||||

| 590,561 | 556,072 | ||||||||

| Equity | |||||||||

| Share capital | 21 | 1,783,689 | 1,776,629 | ||||||

| Warrants | 22 | 18,072 | 18,072 | ||||||

| Contributed surplus | 42,525 | 41,570 | |||||||

| Equity component of convertible debentures | 20 | 14,510 | 17,601 | ||||||

| Accumulated other comprehensive income | 58,851 | 48,951 | |||||||

| Deficit | (283,042 | ) | (174,458 | ) | |||||

| Equity attributable to Osisko Gold Royalties Ltd's shareholders | 1,634,605 | 1,728,365 | |||||||

| Non-controlling interests | 145,456 | 112,667 | |||||||

| Total equity | 1,780,061 | 1,841,032 | |||||||

| 2,370,622 | 2,397,104 |

APPROVED ON BEHALF OF THE BOARD

| (signed) Sean Roosen, Director | (signed) Joanne Ferstman, Director |

|

Osisko Gold Royalties Ltd Consolidated Statements of Income (Loss) For the years ended December 31, 2021 and 2020 |

|

(tabular amounts expressed in thousands of Canadian dollars, except per share amounts) |

| 2021 | 2020 | ||||||||

| Notes | $ | $ | |||||||

| Revenues | 25 | 224,877 | 213,630 | ||||||

| Cost of sales | 25 | (37,646 | ) | (63,700 | ) | ||||

| Depletion of royalty, stream and other interests | 14 | (48,361 | ) | (45,605 | ) | ||||

| Gross profit | 138,870 | 104,325 | |||||||

| Other operating expenses | |||||||||

| General and administrative | 25 | (41,265 | ) | (25,901 | ) | ||||

| Business development | 25 | (4,168 | ) | (10,290 | ) | ||||

| Exploration and evaluation | 25 | (1,197 | ) | (131 | ) | ||||

| Mining operating expenses | 25 | (12,919 | ) | - | |||||

| Impairments - royalty, stream and other interests | 14 | (2,288 | ) | (26,300 | ) | ||||

| Impairments - mining exploration, evaluation and development | 15,16 | (122,250 | ) | - | |||||

| Operating (loss) income | (45,217 | ) | 41,703 | ||||||

| Interest income | 5,065 | 4,582 | |||||||

| Finance costs | (24,586 | ) | (26,131 | ) | |||||

| Foreign exchange (loss) gain | (554 | ) | 1,023 | ||||||

| Share of loss of associates | 12 | (3,950 | ) | (7,657 | ) | ||||

| Other gains, net | 25 | 25,522 | 13,622 | ||||||

| (Loss) earnings before income taxes | (43,720 | ) | 27,142 | ||||||

| Income tax expense | 24 | (12,955 | ) | (10,913 | ) | ||||

| Net (loss) earnings | (56,675 | ) | 16,229 | ||||||

| Net (loss) earnings attributable to: | |||||||||

| Osisko Gold Royalties Ltd's shareholders | (23,554 | ) | 16,876 | ||||||

| Non-controlling interests | (33,121 | ) | (647 | ) | |||||

| Net (loss) earnings per share | |||||||||

| Basic and diluted | 27 | (0.14 | ) | 0.10 |

Additional information per operating segment is provided in Notes 8 and 31.

|

Osisko Gold Royalties Ltd Consolidated Statements of Comprehensive Income (Loss) For the years ended December 31, 2021 and 2020 |

|

(tabular amounts expressed in thousands of Canadian dollars) |

| 2021 | 2020 | |||||||

| Net (loss) earnings | (56,675 | ) | 16,229 | |||||

| Other comprehensive income (loss) | ||||||||

| Items that will not be reclassified to the consolidated statement of income (loss) | ||||||||

| Changes in fair value of financial assets at fair value through comprehensive income | 7,303 | 40,993 | ||||||

| Income tax effect | (471 | ) | (9,319 | ) | ||||

| Share of other comprehensive (loss) income of associates | (1,665 | ) | 1,506 | |||||

| Items that may be reclassified to the consolidated statement of income (loss) | ||||||||

| Currency translation adjustments | (2,990 | ) | (4,555 | ) | ||||

| Other comprehensive income | 2,177 | 28,625 | ||||||

| Comprehensive (loss) income | (54,498 | ) | 44,854 | |||||

| Comprehensive (loss) income attributable to: | ||||||||

| Osisko Gold Royalties Ltd's shareholders | (17,889 | ) | 45,501 | |||||

| Non-controlling interests | (36,609 | ) | (647 | ) |

|

Osisko Gold Royalties Ltd Consolidated Statements of Cash Flows For the years ended December 31, 2021 and 2020 |

|

(tabular amounts expressed in thousands of Canadian dollars) |

| 2021 | 2020 | ||||||||

| Notes | $ | $ | |||||||

| Operating activities | |||||||||

| Net (loss) earnings | (56,675 | ) | 16,229 | ||||||

| Adjustments for: | |||||||||

| Share-based compensation | 13,280 | 9,361 | |||||||

| Depletion and amortization | 51,934 | 46,904 | |||||||

| Impairment of assets | 126,650 | 34,298 | |||||||

| Finance costs | 7,721 | 8,409 | |||||||

| Share of loss of associates | 3,950 | 7,657 | |||||||

| Net gain on acquisition of investments | (7,638 | ) | (3,827 | ) | |||||

| Change in fair value of financial assets at fair value through profit and loss | (6,286 | ) | (2,387 | ) | |||||

| Net gain on dilution of investments in associates | (1,847 | ) | (10,381 | ) | |||||

| Net gain on disposal of investments | - | (5,357 | ) | ||||||

| Foreign exchange loss (gain) | 675 | (652 | ) | ||||||

| Flow-through shares premium income | (6,971 | ) | - | ||||||

| Deferred income tax expense | 11,724 | 3,760 | |||||||

| Other | (5,423 | ) | 2,230 | ||||||

| Net cash flows provided by operating activities before changes in non-cash working capital items |

131,094 | 106,244 | |||||||

| Changes in non-cash working capital items | 28 | (24,999 | ) | 1,734 | |||||

| Net cash flows provided by operating activities | 106,095 | 107,978 | |||||||

| Investing activities | |||||||||

| Net repayment of short-term investments | 3,501 | 412 | |||||||

| Acquisition of the San Antonio gold project | 7 | - | (52,208 | ) | |||||

| Acquisition of investments | (46,713 | ) | (49,194 | ) | |||||

| Proceeds from disposal of investments | 50,936 | 10,864 | |||||||

| Acquisition of royalty and stream interests | (90,936 | ) | (66,062 | ) | |||||

| Mining assets and plant and equipment | (185,297 | ) | (71,828 | ) | |||||

| Exploration and evaluation expenses, net of tax credits | (3,175 | ) | (202 | ) | |||||

| Restricted cash | (504 | ) | 4,762 | ||||||

| Other | 150 | 357 | |||||||

| Net cash flows used in investing activities | (272,038 | ) | (223,099 | ) | |||||

| Financing activities | |||||||||

| Private placement of common shares | 21 | - | 85,000 | ||||||

| Investments from minority shareholders | 21 | 39,760 | 214,323 | ||||||

| Share issue expenses from investments from minority shareholders | 21 | (3,044 | ) | (5,965 | ) | ||||

| Exercise of share options and shares issued under the share purchase plan | 14,547 | 7,835 | |||||||

| Increase in long-term debt | 54,015 | 71,660 | |||||||

| Repayment of long-term debt | (50,251 | ) | (19,205 | ) | |||||

| Normal course issuer bid purchase of common shares | 21 | (30,791 | ) | (3,933 | ) | ||||

| Dividends paid | (32,464 | ) | (28,914 | ) | |||||

| Capital payments on lease liabilities | (6,582 | ) | (1,155 | ) | |||||

| Withholding taxes on settlement of restricted and deferred share units | (3,715 | ) | (2,555 | ) | |||||

| Other | (1,076 | ) | (230 | ) | |||||

| Net cash flows (used in) provided by financing activities | (19,601 | ) | 316,861 | ||||||

| (Decrease) increase in cash before effects of exchange rate changes on cash | (185,544 | ) | 201,740 | ||||||

| Effects of exchange rate changes on cash | (1,282 | ) | (7,439 | ) | |||||

| (Decrease) increase in cash | (186,826 | ) | 194,301 | ||||||

| Cash - January 1 | 302,524 | 108,223 | |||||||

| Cash - December 31 | 8 | 115,698 | 302,524 |

Additional information per operating segment is provided in Notes 8 and 31.

Additional information related to the consolidated statements of cash flows is presented in Note 28.

|

Osisko Gold Royalties Ltd Consolidated Statement of Changes in Equity For the year ended December 31, 2021 |

|

(tabular amounts expressed in thousands of Canadian dollars) |

| Equity attributed to Osisko Gold Royalties Ltd's shareholders | |||||||||||||||||||||||||||||||||

| Number of | Equity | Accumulated | |||||||||||||||||||||||||||||||

| common | Warrants | component of | other | Non- | |||||||||||||||||||||||||||||

| shares | Share | Contributed | convertible | comprehensive | controlling | ||||||||||||||||||||||||||||

| Notes | outstanding | capital | surplus | debentures | income(i) | Deficit | Total | interests | Total | ||||||||||||||||||||||||

| $ | $ | $ | $ | $ | $ | $ | $ | $ | |||||||||||||||||||||||||

| Balance - January 1, 2021 | 166,647,932 | 1,776,629 | 18,072 | 41,570 | 17,601 | 48,951 | (174,458 | ) | 1,728,365 | 112,667 | 1,841,032 | ||||||||||||||||||||||

| Net loss | - | - | - | - | - | - | (23,554 | ) | (23,554 | ) | (33,121 | ) | (56,675 | ) | |||||||||||||||||||

| Other comprehensive income (loss ) | - | - | - | - | - | 5,665 | - | 5,665 | (3,488 | ) | 2,177 | ||||||||||||||||||||||

| Comprehensive income (loss) | - | - | - | - | - | 5,665 | (23,554 | ) | (17,889 | ) | (36,609 | ) | (54,498 | ) | |||||||||||||||||||

| Net investments from minority shareholders | 21 | - | - | - | - | - | - | - | - | 27,314 | 27,314 | ||||||||||||||||||||||

| Effect of changes in ownership of a subsidiary on non- controlling interest |

- | - | - | - | - | - | (36,482 | ) | (36,482 | ) | 36,482 | - | |||||||||||||||||||||

| Dividends declared | 21 | - | - | - | - | - | - | (35,085 | ) | (35,085 | ) | - | (35,085 | ) | |||||||||||||||||||

| Shares issued - Dividends reinvestment plan | 21 | 120,523 | 1,821 | - | - | - | - | - | 1,821 | - | 1,821 | ||||||||||||||||||||||

| Shares issued - Employee share purchase plan | 20,496 | 311 | - | - | - | - | - | 311 | - | 311 | |||||||||||||||||||||||

| Share options - Share-based compensation | - | - | - | 3,636 | - | - | - | 3,636 | 2,315 | 5,951 | |||||||||||||||||||||||

| Share options exercised | 1,043,903 | 18,069 | - | (3,720 | ) | - | - | - | 14,349 | - | 14,349 | ||||||||||||||||||||||

| Restricted share units to be settled in common shares: | |||||||||||||||||||||||||||||||||

| Share-based compensation | - | - | - | 3,527 | - | - | - | 3,527 | 1,858 | 5,385 | |||||||||||||||||||||||

| Settlement | 215,851 | 2,605 | - | (5,113 | ) | - | - | (671 | ) | (3,179 | ) | - | (3,179 | ) | |||||||||||||||||||

| Income tax impact | - | - | - | (184 | ) | - | - | - | (184 | ) | 82 | (102 | ) | ||||||||||||||||||||

| Deferred share units to be settled in common shares: | |||||||||||||||||||||||||||||||||

| Share-based compensation | - | - | - | 1,162 | - | - | - | 1,162 | 1,259 | 2,421 | |||||||||||||||||||||||

| Settlement | 30,849 | 625 | - | (1,349 | ) | - | - | (237 | ) | (961 | ) | - | (961 | ) | |||||||||||||||||||

| Income tax impact | - | - | - | (95 | ) | - | - | - | (95 | ) | 88 | (7 | ) | ||||||||||||||||||||

| Normal course issuer bid purchase of common shares | 21 | (2,103,366 | ) | (22,471 | ) | - | - | - | - | (8,320 | ) | (30,791 | ) | - | (30,791 | ) | |||||||||||||||||

| Deemed issuance of Osisko shares | 12 | 517,409 | 6,100 | - | - | - | - | - | 6,100 | - | 6,100 | ||||||||||||||||||||||

| Maturity of convertible debenture - equity component | 22 | - | - | - | 3,091 | (3,091 | ) | - | - | - | - | - | |||||||||||||||||||||

| Transfer of realized loss on financial assets at fair value through other comprehensive income, net of income taxes |

- | - | - | - | - | 4,235 | (4,235 | ) | - | - | - | ||||||||||||||||||||||

| Balance - December 31, 2021 | 166,493,597 | 1,783,689 | 18,072 | 42,525 | 14,510 | 58,851 | (283,042 | ) | 1,634,605 | 145,456 | 1,780,061 | ||||||||||||||||||||||

(i) As at December 31, 2021, accumulated other comprehensive income comprises items that will not be recycled to the consolidated statements of income (loss) amounting to $33.7 million and items that may be recycled to the consolidated statements of income (loss) amounting to $25.1 million.

|

Osisko Gold Royalties Ltd Consolidated Statement of Changes in Equity For the year ended December 31, 2020 |

|

(tabular amounts expressed in thousands of Canadian dollars) |

| Equity attributed to Osisko Gold Royalties Ltd's shareholders | |||||||||||||||||||||||||||||||||

| Number of | Equity | Accumulated | |||||||||||||||||||||||||||||||

| common | Warrants | component of | other | Retained | Non- | ||||||||||||||||||||||||||||

| shares | Share | Contributed | convertible | comprehensive | earnings | controlling | |||||||||||||||||||||||||||

| Notes | outstanding | capital | surplus | debenture | income (loss)(i) | (deficit) | Total | interests | Total | ||||||||||||||||||||||||

| $ | $ | $ | $ | $ | $ | $ | $ | $ | |||||||||||||||||||||||||

| Balance - January 1, 2020 | 156,951,952 | 1,656,350 | 18,072 | 37,642 | 17,601 | 13,469 | (249,688 | ) | 1,493,446 | - | 1,493,446 | ||||||||||||||||||||||

| Net earnings (loss) | - | - | - | - | - | - | 16,876 | 16,876 | (647 | ) | 16,229 | ||||||||||||||||||||||

| Other comprehensive income | - | - | - | - | - | 28,625 | - | 28,625 | - | 28,625 | |||||||||||||||||||||||

| Comprehensive income (loss) | - | - | - | - | - | 28,625 | 16,876 | 45,501 | (647 | ) | 44,854 | ||||||||||||||||||||||

| Private placement | 21 | 7,727,273 | 85,000 | - | - | - | - | - | 85,000 | - | 85,000 | ||||||||||||||||||||||

| Issue costs, net of taxes | - | (136 | ) | - | - | - | - | - | (136 | ) | - | (136 | ) | ||||||||||||||||||||

| Income tax impact on prior year issue costs | - | 3,644 | - | - | - | - | - | 3,644 | - | 3,644 | |||||||||||||||||||||||

| Net investments from minority shareholders, net of taxes | 6, 21 | - | - | - | - | - | - | - | - | 209,892 | 209,892 | ||||||||||||||||||||||

| Deemed acquisition of Barolo Ventures Corp. | 6 | - | - | - | - | - | - | - | - | 1,751 | 1,751 | ||||||||||||||||||||||

| Acquisition of the San Antonio gold project | 7 | 1,011,374 | 15,846 | - | - | - | - | - | 15,846 | - | 15,846 | ||||||||||||||||||||||

| Gain on dilution of non-controlling interests | - | - | - | - | - | - | 98,329 | 98,329 | (98,329 | ) | - | ||||||||||||||||||||||

| Acquisition of royalty interests paid in shares | 250,000 | 3,880 | - | - | - | - | - | 3,880 | - | 3,880 | |||||||||||||||||||||||

| Dividends declared | 21 | - | - | - | - | - | - | (32,838 | ) | (32,838 | ) | - | (32,838 | ) | |||||||||||||||||||

| Shares issued - Dividends reinvestment plan | 21 | 268,173 | 3,440 | - | - | - | - | - | 3,440 | - | 3,440 | ||||||||||||||||||||||

| Shares issued - Employee share purchase plan | 30,388 | 391 | - | - | - | - | - | 391 | - | 391 | |||||||||||||||||||||||

| Share options - Shared-based compensation | - | - | - | 3,104 | - | - | - | 3,104 | - | 3,104 | |||||||||||||||||||||||

| Share options exercised | 232,964 | 3,932 | - | (857 | ) | - | - | - | 3,075 | - | 3,075 | ||||||||||||||||||||||

| Replacement share options exercised | 440,506 | 5,976 | - | (1,461 | ) | - | - | - | 4,515 | - | 4,515 | ||||||||||||||||||||||

| Restricted share units to be settled in common shares: | |||||||||||||||||||||||||||||||||

| Share-based compensation | - | - | - | 5,835 | - | - | - | 5,835 | - | 5,835 | |||||||||||||||||||||||

| Settlement | 145,694 | 1,984 | - | (4,247 | ) | - | - | (279 | ) | (2,542 | ) | - | (2,542 | ) | |||||||||||||||||||

| Income tax impact | - | - | - | 358 | - | - | - | 358 | - | 358 | |||||||||||||||||||||||

| Deferred share units to be settled in common shares: | |||||||||||||||||||||||||||||||||

| Share-based compensation | - | - | - | 1,113 | - | - | - | 1,113 | - | 1,113 | |||||||||||||||||||||||

| Settlement | 19,330 | 255 | - | (266 | ) | - | - | (1 | ) | (12 | ) | - | (12 | ) | |||||||||||||||||||

| Income tax impact | - | - | - | 349 | - | - | - | 349 | - | 349 | |||||||||||||||||||||||

| Normal course issuer bid purchase of common shares | 21 | (429,722 | ) | (3,933 | ) | - | - | - | - | - | (3,933 | ) | - | (3,933 | ) | ||||||||||||||||||

| Transfer of realized other comprehensive income of Associates, net of income taxes |

- | - | - | - | - | (414 | ) | 414 | - | - | - | ||||||||||||||||||||||

| Transfer of realized loss on financial assets at fair value through other comprehensive income, net of income taxes |

- | - | - | - | - | 7,271 | (7,271 | ) | - | - | - | ||||||||||||||||||||||

| Balance - December 31, 2020 (ii) | 166,647,932 | 1,776,629 | 18,072 | 41,570 | 17,601 | 48,951 | (174,458 | ) | 1,728,365 | 112,667 | 1,841,032 | ||||||||||||||||||||||

(i) As at December 31, 2020, accumulated other comprehensive income comprises items that will not be recycled to the consolidated statements of income (loss) amounting to $20.8 million and items that may be recycled to the consolidated statements of income (loss) amounting to $28.1 million.

(ii) As at December 31, 2020, there are 167,165,341 common shares issued, of which 517,409 are deemed to have been repurchased given that one of the Company's associates owns some of the Company's common shares.

|

Osisko Gold Royalties Ltd Notes to the Consolidated Financial Statements For the years ended December 31, 2021 and 2020 |

|

(tabular amounts expressed in thousands of Canadian dollars, except per share amounts) |

1. Nature of activities

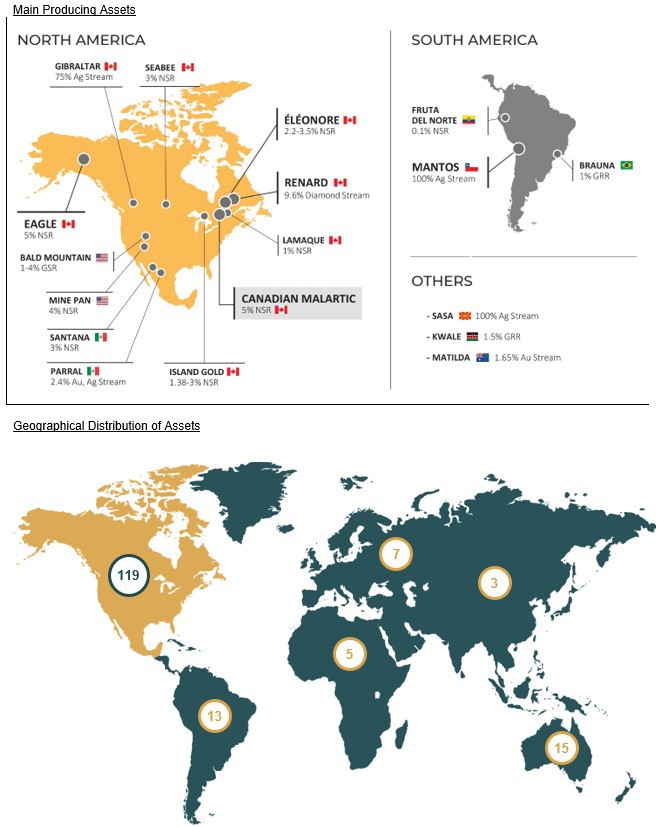

Osisko Gold Royalties Ltd and its subsidiaries (together "Osisko" or the "Company") are engaged in the business of acquiring and managing precious metal and other high-quality royalties, streams and similar interests in Canada and worldwide, except for Osisko Development Corp. and its subsidiaries ("Osisko Development"), which are engaged in the exploration, evaluation and development of mining projects. Osisko is a public company traded on the Toronto Stock Exchange, and the New York Stock Exchange constituted under the Business Corporations Act (Québec) and domiciled in the Province of Québec, Canada. The address of its registered office is 1100, avenue des Canadiens-de-Montréal, Suite 300, Montréal, Québec. The Company owns a portfolio of royalties, streams, offtakes, options on royalty/stream financings and exclusive rights to participate in future royalty/stream financings on various projects. The Company's cornerstone asset is a 5% net smelter return ("NSR") royalty on the Canadian Malartic mine, located in Canada.

In November 2020, Osisko completed the spin-out transaction of its mining assets and certain equity investments to Osisko Development, a newly created company engaged in the exploration, evaluation and development of mining projects in Canada and in Mexico (Note 6). The common shares of Osisko Development began trading on the TSX Venture Exchange (the "TSX-V") on December 2, 2020 under the symbol "ODV". On December 31, 2021, Osisko held an interest of 75.1% in Osisko Development and, as a result, the Company consolidated the assets, liabilities, results of operations and cash flows of the activities of Osisko Development and its subsidiaries. Osisko Development's main asset is the Cariboo gold project in Canada.

2. Basis of presentation

The accompanying consolidated financial statements have been prepared in accordance with the International Financial Reporting Standards ("IFRS") as issued by the International Accounting Standards Board ("IASB"). The accounting policies, methods of computation and presentation applied in these consolidated financial statements are consistent with those of the previous financial year. The Board of Directors approved the audited consolidated financial statements for issue on February 24, 2022.

Uncertainty due to COVID-19

The COVID-19 pandemic has had a significant impact on the global economy and commodity and financial markets. The full extent and impact of the COVID-19 pandemic is unknown at this time and its adverse effects may continue for an extended and unknown period of time, particularly as variant strains of the virus are identified. The impact of the pandemic to date has included volatility in financial markets, a slowdown in economic activity, supply chain and labour issues, and volatility in commodity prices (including gold and silver). Furthermore, as efforts have been undertaken to slow the spread of the COVID-19 pandemic, the operation and development of mining projects have been impacted. Many mining projects, including a number of the properties in which Osisko holds a royalty, stream or other interest have been impacted by the pandemic resulting in the temporary suspension of operations, and other mitigation measures that impacted production. If the operation or development of one or more of the properties in which Osisko holds a royalty, stream or other interest and from which it receives or expects to receive significant revenue is suspended as a result of the continuing COVID-19 pandemic or future pandemics or other public health emergencies, it may have a material adverse impact on Osisko's profitability, results of operations, financial condition and the trading price of Osisko's securities. The extent of the impact of the COVID-19 pandemic on our operational and financial performance will depend on future developments, including a widely available vaccine in each of the countries where are located the assets on which we own a royalty, stream or other interest, the duration and severity of the pandemic and related restrictions, all of which continue to be uncertain and cannot be predicted.

3. Significant accounting policies

The significant accounting policies applied in the preparation of the consolidated financial statements are described below.

a) Basis of measurement

The consolidated financial statements are prepared under the historical cost convention, except for the revaluation of certain financial assets at fair value (including derivative instruments).

|

Osisko Gold Royalties Ltd Notes to the Consolidated Financial Statements For the years ended December 31, 2021 and 2020 |

|

(tabular amounts expressed in thousands of Canadian dollars, except per share amounts) |

3. Significant accounting policies (continued)

b) Business combinations

On the acquisition of a business, the acquisition method of accounting is used whereby the identifiable assets, liabilities and contingent liabilities (identifiable net assets) of the business are measured at fair value at the date of acquisition. Provisional fair values estimated at a reporting date are finalized as soon as the relevant information is available, which period shall not exceed twelve months from the acquisition date and are adjusted to reflect the transaction as of the acquisition date. Any excess of the consideration paid is treated as goodwill, and any bargain gain is immediately recognized in the statement of income (loss) and comprehensive income (loss). If control is lost as a result of a transaction, the participation retained is recognized on the balance sheet at fair value and the difference between the fair value recognized and the carrying value as at the date of the transaction is recognized in the statement of income (loss). Acquisition costs are expensed as incurred.

The Company recognizes any non-controlling interest in the acquiree on an acquisition-by-acquisition basis, either at fair value or at the non-controlling interest's proportionate share of the recognized amounts of acquiree's identifiable net assets.

The results of businesses acquired during the period are consolidated into the consolidated financial statements from the date on which control commences (generally at the closing date when the acquirer legally transfers the consideration).

c) Non-controlling interests

Non-controlling interests represent an equity interest in a subsidiary owned by an outside party. The share of net assets of the subsidiary attributable to the non-controlling interests is presented as a component of equity. Their share of net income or loss and comprehensive income or loss is recognized directly in equity. Changes in the Company's ownership interest in the subsidiary that do not result in a loss of control are accounted for as equity transactions.

d) Consolidation

The Company's financial statements consolidate the accounts of Osisko Gold Royalties Ltd and its subsidiaries. All intercompany transactions, balances and unrealized gains or losses from intercompany transactions are eliminated on consolidation. Subsidiaries are all entities over which the Company has the ability to exercise control. The Company controls an entity when the group is exposed to, or has rights to, variable returns from its involvement with the entity and has the ability to affect those returns through its power over the entity. Subsidiaries are fully consolidated from the date on which control is transferred to Osisko and are de-consolidated from the date that control ceases. Accounting policies of subsidiaries are consistent with the policies adopted by Osisko.

The principal subsidiaries of the Company, their geographic locations, related participation and principal operating segment (Note 31) at December 31, 2021 and 2020 were as follows:

| Entity | Jurisdiction | Participation | Functional currency | Operating Segment |

| Osisko Development Corp.(i) | Québec | 75.1% | Canadian dollar | Exploration/development of mining projects |

| Osisko Bermuda Limited | Bermuda | 100% | United States dollar | Royalties, streams and similar interests |

| Osisko Mining (USA) Inc. | Delaware | 100% | United States dollar | Royalties, streams and similar interests |

(i) The following entities are wholly-owned subsidiaries of Osisko Development since November 25, 2020 (Note 6): Barkerville Gold Mines Ltd. (British Columbia), Coulon Mines Inc. (Canada), General Partnership Osisko James Bay (Québec) and Sapuchi Minera S. de R.L. de C.V. (Mexico) (Pesos as functional currency). Prior to that date, these subsidiaries were wholly-owned by the Company. The participation in Osisko Development on December 31, 2020 was 84.1%.

|

Osisko Gold Royalties Ltd Notes to the Consolidated Financial Statements For the years ended December 31, 2021 and 2020 |

|

(tabular amounts expressed in thousands of Canadian dollars, except per share amounts) |

3. Significant accounting policies (continued)

e) Foreign currency translation

(i) Functional and presentation currency

Items included in the financial statements of each consolidated entity and associate of the Company are measured using the currency of the primary economic environment in which the entity operates (the "functional currency"). The consolidated financial statements are presented in Canadian dollars, which is the functional currency of the parent Company and some of its subsidiaries.

Assets and liabilities of the subsidiaries that have a functional currency other than the Canadian dollar are translated into Canadian dollars at the exchange rate in effect on the consolidated balance sheet date and revenues and expenses are translated at the average exchange rate over the reporting period. Gains and losses from these translations are recognized as currency translation adjustment in other comprehensive income or loss.

(ii) Transactions and balances

Foreign currency transactions, including revenues and expenses, are translated into the functional currency at the rate of exchange prevailing on the date of each transaction or valuation when items are re-measured. Monetary assets and liabilities denominated in currencies other than the operation's functional currencies are translated into the functional currency at exchange rates in effect at the balance sheet date. Foreign exchange gains and losses resulting from the settlement of those transactions and from period-end translations are recognized in the consolidated statement of income (loss).

Non-monetary assets and liabilities are translated at historical rates, unless such assets and liabilities are carried at fair value, in which case, they are translated at the exchange rate in effect at the date of the fair value measurement. Changes in fair value attributable to currency fluctuations of non-monetary financial assets and liabilities such as equities held at fair value through profit or loss are recognized in the consolidated statement of income (loss) as part of the fair value gain or loss. Such changes in fair value of non-monetary financial assets, such as equities classified at fair value through other comprehensive income, are included in other comprehensive income or loss.

f) Financial instruments

Financial assets and liabilities are recognized when the Company becomes a party to the contractual provisions of the instrument. Financial assets are derecognized when the rights to receive cash flows from the assets have expired or have been transferred and the Company has transferred substantially all risks and rewards of ownership.

Financial assets and liabilities are offset and the net amount is reported in the balance sheet when there is an unconditional and legally enforceable right to offset the recognized amounts and there is an intention to settle on a net basis, or realize the asset and settle the liability simultaneously.

All financial instruments are required to be measured at fair value on initial recognition. The fair value is based on quoted market prices, unless the financial instruments are not traded in an active market. In this case, the fair value is determined by using valuation techniques like the Black-Scholes option pricing model or other valuation techniques.

|

Osisko Gold Royalties Ltd Notes to the Consolidated Financial Statements For the years ended December 31, 2021 and 2020 |

|

(tabular amounts expressed in thousands of Canadian dollars, except per share amounts) |

3. Significant accounting policies (continued)

f) Financial instruments (continued)

Measurement after initial recognition depends on the classification of the financial instrument. The Company has classified its financial instruments in the following categories depending on the purpose for which the instruments were acquired and their characteristics.

(i) Financial assets

Debt instruments

Investments in debt instruments are subsequently measured at amortized cost when the asset is held within a business model whose objective is to hold assets in order to collect contractual cash flows and when the contractual terms of the financial asset give rise on specified dates to cash flows that are solely payments of principal and interest on the principal amount outstanding.

Investments in debt instruments are subsequently measured at fair value when they do not qualify for measurement at amortized cost. Financial instruments subsequently measured at fair value, including derivatives that are assets, are carried at fair value with changes in fair value recorded in net income or loss unless they are held within a business model whose objective is to hold assets in order to collect contractual cash flows or sell the assets and when the contractual terms of the financial asset give rise on specified dates to cash flows that are solely payments of principal and interest on the principal amount outstanding, in which case unrealized gains and losses are initially recognized in other comprehensive income or loss for subsequent reclassification to net income or loss through amortization of premiums and discounts, impairment or derecognition.

Equity instruments

Investments in equity instruments are subsequently measured at fair value with changes recorded in net income or loss. Equity instruments that are not held for trading can be irrevocably designated at fair value through other comprehensive income or loss on initial recognition without subsequent reclassification to net income or loss. Cumulative gains and losses are transferred from accumulated other comprehensive income (loss) to retained earnings upon derecognition of the investment. Dividend income on equity instruments measured at fair value through other comprehensive income or loss is recognized in the statement of income (loss) on the ex-dividend date.

(ii) Financial liabilities

Financial liabilities are subsequently measured at amortized cost using the effective interest method, except for financial liabilities at fair value through profit or loss. Such liabilities, including derivatives that are liabilities, are subsequently measured at fair value.

|

Osisko Gold Royalties Ltd Notes to the Consolidated Financial Statements For the years ended December 31, 2021 and 2020 |

|

(tabular amounts expressed in thousands of Canadian dollars, except per share amounts) |

3. Significant accounting policies (continued)

f) Financial instruments (continued)

The Company has classified its financial instruments as follows:

| Category | Financial instrument |

| Financial assets at amortized cost |

Bank balances Short-term debt securities Notes and loans receivable Trade receivables Interest income receivable Amounts receivable from associates and other receivables Reclamation deposits |

|

Financial assets at fair value through profit or loss |

Investments in derivatives and convertible debentures |

|

Financial assets at fair value through other comprehensive income or loss |

Investments in shares and equity instruments, |

| Financial liabilities at amortized cost |

Accounts payable and accrued liabilities Liability component of convertible debentures Borrowings under revolving credit facilities Equipment financings |

Derivatives

Derivatives, other than warrants held in mining exploration and development companies, are only used for economic hedging purposes and not as speculative investments. Derivatives are initially recognised at fair value on the date a derivative contract is entered into and are subsequently measured to their fair value at the end of each reporting period. The accounting for subsequent changes in fair value depends on whether the derivative is designated as a hedging instrument, and if so, the nature of the item being hedged.

g) Impairment of financial assets

At each reporting date, the Company assesses, on a forward-looking basis, the expected credit losses associated with its financial assets carried at amortized cost. The impairment methodology applied depends on whether there has been a significant increase in the credit risk or if a simplified approach has been selected.

The Company has two principal types of financial assets subject to the expected credit loss model:

- Trade receivables; and

- Investments in debt instruments measured at amortized cost.

Amounts receivable

The Company applies the simplified approach permitted by IFRS 9 for trade receivables (including amounts receivable from associates and other receivables), which requires lifetime expected credit losses to be recognized from initial recognition of the receivables.

Investments in debt instruments

To the extent that a debt instrument at amortized cost is considered to have low credit risk, which corresponds to a credit rating within the investment grade category and the credit risk has not increased significantly, the loss allowance is determined on the basis of 12-month expected credit losses. If the credit risk has increased significantly, the lifetime expected credit losses are recognized.

|

Osisko Gold Royalties Ltd Notes to the Consolidated Financial Statements For the years ended December 31, 2021 and 2020 |

|

(tabular amounts expressed in thousands of Canadian dollars, except per share amounts) |

3. Significant accounting policies (continued)

h) Cash

Cash includes demand deposits held with banks.

i) Refundable tax credits for mining exploration expenses

The Company is entitled to refundable tax credits on qualified mining exploration and evaluation expenses incurred in the provinces of Québec and British-Columbia. The credits are accounted for against the exploration and evaluation expenses incurred.

j) Inventories

Inventories are valued at the lower of cost and net realizable value. Cost is determined on a weighted average basis.

k) Investments in associates

Associates are entities over which the Company has significant influence, but not control. The financial results of the Company's investments in its associates are included in the Company's results according to the equity method. Under the equity method, the investment is initially recognized at cost, and the carrying amount is increased or decreased to recognize the Company's share of profits or losses of associates after the date of acquisition. The Company's share of profits or losses is recognized in the consolidated statement of income (loss) and its share of other comprehensive income or loss of associates is included in other comprehensive income or loss.

Unrealized gains on transactions between the Company and an associate are eliminated to the extent of the Company's interest in the associate. Unrealized losses are also eliminated unless the transaction provides evidence of an impairment of the asset transferred. Dilution gains and losses arising from changes in interests in investments in associates are recognized in the consolidated statement of income or loss.

The Company assesses at each reporting date whether there is any objective evidence that its investments in associates are impaired. If impaired, the carrying value of the Company's share of the underlying assets of associates is written down to its estimated recoverable amount (being the higher of fair value less costs of disposal and value-in-use) and charged to the consolidated statement of income or loss.

l) Royalty, stream and other interests

Royalty, stream and other interests consist of acquired royalty, stream and other interests in producing, development and exploration and evaluation stage properties. Royalty, stream and other interests are recorded at cost and capitalized as tangible assets. They are subsequently measured at cost less accumulated depletion and depreciation and accumulated impairment losses. The major categories of the Company's interests are producing, development and exploration and evaluation. Producing assets are those that have generated revenue from steady-state operations for the Company. Development assets are interests in projects that are under development, in permitting or feasibility stage and that in management's view, can be reasonably expected to generate steady-state revenue for the Company in the near future. Exploration and evaluation assets represent properties that are not yet in development, permitting or feasibility stage or that are speculative in nature and are expected to require several years to generate revenue, if ever, or are currently not active.

Producing and development royalty, stream and other interests are recorded at cost and capitalized in accordance with IAS 16 Property, Plant and Equipment. Producing royalty, stream and other interests are depleted using the units-of-production method over the life of the property to which the interest relates, which is estimated using available estimates of proven and probable mineral reserves specifically associated with the properties and may include a portion of resources expected to be converted into mineral reserves. Management relies on information available to it under contracts with the operators and / or public disclosures for information on proven and probable mineral reserves and resources from the operators of the producing royalty, stream and other interests.

|

Osisko Gold Royalties Ltd Notes to the Consolidated Financial Statements For the years ended December 31, 2021 and 2020 |

|

(tabular amounts expressed in thousands of Canadian dollars, except per share amounts) |

3. Significant accounting policies (continued)

l) Royalty, stream and other interests (continued)

On acquisition of a producing or a development royalty, stream and other interest, an allocation of the acquisition cost is made for the exploration potential based on its fair value. The estimated fair value of this acquired exploration potential is recorded as an asset (non-depreciable interest) on the acquisition date. Updated mineral reserve and resource information obtained from the operators of the properties is used to determine the amount to be converted from non-depreciable interest to depreciable interest.

Royalty, stream and other interests for exploration and evaluation assets are recorded at cost and capitalized in accordance with IFRS 6 Exploration for and Evaluation of Mineral Resources. Acquisition costs of exploration and evaluation royalty, stream and other interests are capitalized and are not depleted until such time as revenue-generating activities begin.

Producing and development royalty, stream and other interests are reviewed for impairment at each reporting date if there is any indication that the carrying amount may not be recoverable. Impairment is assessed at the level of Cash-Generating Units (''CGU'') which, in accordance with IAS 36 Impairment of Assets, are identified as the smallest identifiable group of assets that generates cash inflows, which are largely independent of the cash inflows from other assets. This is usually at the individual royalty, stream and other interest level for each property from which cash inflows are generated.

Royalty, stream and other interests for exploration and evaluation assets are assessed for impairment whenever indicators of impairment exist in accordance with IFRS 6. An impairment loss is recognized for the amount by which the asset's carrying value exceeds its recoverable amount, which is the higher of fair value less costs of disposal and value-in-use. An interest that has previously been classified as exploration and evaluation is also assessed for impairment before reclassification to development or producing, and the impairment loss, if any, is recognized in net income.

m) Property and equipment

Property and equipment are stated at cost less accumulated depreciation and accumulated impairment losses. Cost includes expenditures that are directly attributable to the acquisition of an asset. Subsequent costs are included in the asset's carrying amount or recognized as a separate asset, as appropriate, only when it is probable that future economic benefit associated with the item will flow to the Company and the cost can be measured reliably. The carrying amount of a replaced asset is derecognized when replaced.

Depreciation is calculated to amortize the cost of the property and equipment less their residual values over their estimated useful lives using the straight-line method and following periods by major categories:

Leasehold improvements Lease term

Furniture and office equipment 2-7 years

Exploration equipment and facilities 2-20 years

Mining plant and equipment (development) 3-20 years

Right-of-use assets Shorter of useful life and lease term

Residual values, method of depreciation and useful lives of the assets are reviewed annually and adjusted if appropriate.

Gains and losses on disposals of property and equipment are determined by comparing the proceeds with the carrying amount of the asset and are included as part of other gains or losses, net in the consolidated statement of income (loss).

|

Osisko Gold Royalties Ltd Notes to the Consolidated Financial Statements For the years ended December 31, 2021 and 2020 |

|

(tabular amounts expressed in thousands of Canadian dollars, except per share amounts) |

3. Significant accounting policies (continued)

n) Exploration and evaluation expenditures

Exploration and evaluation assets are comprised of exploration and evaluation expenditures and mining properties acquisition costs for exploration and evaluation assets. Expenditures incurred on activities that precede exploration and evaluation, being all expenditures incurred prior to securing the legal rights to explore an area, are expensed immediately. Exploration and evaluation assets include rights in mining properties, paid or acquired through a business combination or an acquisition of assets, and costs related to the initial search for mineral deposits with economic potential or to obtain more information about existing mineral deposits. Mining rights are recorded at acquisition cost less accumulated impairment losses. Mining rights and options to acquire undivided interests in mining rights are depreciated only as these properties are put into commercial production.

Exploration and evaluation expenditures for each separate area of interest are capitalized and include costs associated with prospecting, sampling, trenching, drilling and other work involved in searching for ore like topographical, geological, geochemical and geophysical studies. They also reflect costs related to establishing the technical and commercial viability of extracting a mineral resource identified through exploration and evaluation or acquired through a business combination or asset acquisition.

Exploration and evaluation expenditures include the cost of:

(i) establishing the volume and grade of deposits through drilling of core samples, trenching and sampling activities;

(ii) determining the optimal methods of extraction and metallurgical and treatment processes;

(iii) studies related to surveying, transportation and infrastructure requirements;

(iv) permitting activities; and

(v) economic evaluations to determine whether development of the mineralized material is commercially justified, including scoping, prefeasibility and final feasibility studies.

Exploration and evaluation expenditures include overhead expenses directly attributable to the related activities.

Cash flows attributable to capitalized exploration and evaluation costs are classified as investing activities in the consolidated statement of cash flows under the heading exploration and evaluation.

Exploration and evaluation assets under a farm-out arrangement (where a farmee incurs certain expenditures in a property to earn an interest in that property) are accounted as follows:

(i) the Company uses the carrying value of the interest before the farm-out arrangement as the carrying value for the portion of the interest retained;

(ii) the Company credits any cash consideration received against the carrying amount of the portion of the interest retained, with an excess included as a gain in profit or loss;

(iii) in the situation where a royalty interest is retained by the Company as a result of an interest earned by the farmee, the Company records the royalty interest received at an amount corresponding to the carrying value of the exploration and evaluation property at the time of the transfer in ownership; and

(iv) the Company does not record exploration expenditures made by the farmee on the property.

o) Goodwill

Goodwill is recognized in a business combination if the cost of the acquisition exceeds the fair value of the identifiable net assets acquired. Goodwill is then allocated to the CGU or group of CGUs that are expected to benefit from the synergies of the combination. The Company performs goodwill impairment tests on an annual basis as at December 31 of each year. In addition, the Company assesses for indicators of impairment at each reporting period end and, if an indicator of impairment is identified, goodwill is tested for impairment at that time. If the carrying value of the CGU or group of CGUs to which goodwill is assigned exceeds its recoverable amount, an impairment loss is recognized. Goodwill impairment losses are not reversed.

The recoverable amount of a CGU or group of CGUs is measured as the higher of value in use and fair value less costs of disposal.

|

Osisko Gold Royalties Ltd Notes to the Consolidated Financial Statements For the years ended December 31, 2021 and 2020 |

|

(tabular amounts expressed in thousands of Canadian dollars, except per share amounts) |

3. Significant accounting policies (continued)

p) Provision for environmental rehabilitation

Provision for environmental rehabilitation, restructuring costs and legal claims, where applicable, is recognized when:

(i) The Company has a present legal or constructive obligation as a result of past events.

(ii) It is probable that an outflow of resources will be required to settle the obligation.

(iii) The amount can be reliably estimated.

The provision is measured at management's best estimate of the expenditure required to settle the obligation at the end of the reporting period, and is discounted to present value where the effect is material. The increase in the provision due to passage of time is recognized as finance costs. Changes in assumptions or estimates are reflected in the period in which they occur.

Provision for environmental rehabilitation represents the legal and constructive obligations associated with the eventual closure of the Company's property, plant and equipment. These obligations consist of costs associated with reclamation and monitoring of activities and the removal of tangible assets. The discount rate used is based on a pretax rate that reflects current market assessments of the time value of money and the risks specific to the obligation, excluding the risks for which future cash flow estimates have already been adjusted.

Reclamation deposits

Reclamation deposits are term deposits held for the benefit of the Government of the Province of British Columbia as collateral for possible rehabilitation activities on Osisko Development's mineral properties in connection with permits required for exploration activities. Reclamation deposits are released once the property is restored to satisfactory condition, or as released under the surety bond agreement. As they are restricted from general use, they are included under other assets on the consolidated balance sheets.

q) Current and deferred income tax

The tax expense for the period comprises current and deferred tax. Tax is recognized in the consolidated statement of income (loss), except to the extent that it relates to items recognized in other comprehensive income or loss or directly in equity. In this case, the tax is also recognized in other comprehensive income or loss or directly in equity, respectively.

Current income taxes

The current income tax charge is the expected tax payable on the taxable income for the year, using the tax laws enacted or substantively enacted at the balance sheet date in the jurisdictions where the Company and its subsidiaries operate and generate taxable income. Management periodically evaluates positions taken in tax returns with respect to situations in which applicable tax regulation is subject to interpretation. It establishes provisions where appropriate on the basis of amounts expected to be paid to the tax authorities.

Deferred income taxes

The Company uses the asset and liability method of accounting for income taxes. Under this method, deferred income tax assets and liabilities are recognized for future tax consequences attributable to temporary differences between the financial statement carrying amounts of existing assets and liabilities and their respective tax bases. However, the deferred income tax is not accounted for if it arises from initial recognition of an asset or liability in a transaction other than a business combination that at the time of the transaction affects neither accounting nor taxable profit or loss. Deferred income tax assets and liabilities are measured using enacted or substantively enacted tax rates (and laws) that apply to taxable income in the years in which those temporary differences are expected to be recovered or settled.

Deferred income tax assets are recognized only to the extent that it is probable that future taxable profit will be available against which the temporary differences can be utilized.

Deferred income tax is provided on temporary differences arising on investments in subsidiaries and associates, except where the timing of the reversal of the temporary difference is controlled by the Company and it is probable that the temporary difference will not reverse in the foreseeable future.

|

Osisko Gold Royalties Ltd Notes to the Consolidated Financial Statements For the years ended December 31, 2021 and 2020 |

|

(tabular amounts expressed in thousands of Canadian dollars, except per share amounts) |

3. Significant accounting policies (continued)

q) Current and deferred income tax (continued)

Deferred income taxes (continued)

Deferred income tax assets and liabilities are presented as non-current and are offset when there is a legally enforceable right to offset current tax assets against current tax liabilities and when deferred tax assets and liabilities relate to income taxes levied by the same taxation authority on either the same taxable entity or different taxable entities where there is an intention to settle the balances on a net basis.

r) Convertible debentures

The liability and equity components of convertible debentures are presented separately on the consolidated balance sheet starting from initial recognition.

The liability component is recognized initially at the fair value, by discounting the stream of future payments of interest and principal at the prevailing market rate for a similar liability of comparable credit status and providing substantially the same cash flows that do not have an associated conversion option. Subsequent to initial recognition, the liability component is measured at amortized cost using the effective interest method; the liability component is increased by accretion of the discounted amounts to reach the nominal value of the debentures at maturity.

The carrying amount of the equity component is calculated by deducting the carrying amount of the financial liability from the amount of the debentures and is presented in shareholders' equity as equity component of convertible debenture. The equity component is not re-measured subsequent to initial recognition except on conversion or expiry. A deferred tax liability is recognized with respect to any temporary difference that arises from the initial recognition of the equity component separately from the liability component. The deferred tax is charged directly to the carrying amount of the equity component. Subsequent changes in the deferred tax liability are recognized through the consolidated statement of income (loss). Transaction costs are distributed between liability and equity on a pro-rata basis of their carrying amounts.

s) Share capital

Common shares are classified as equity. Incremental costs directly attributable to the issuance of shares are recognized as a deduction from the proceeds in equity in the period where the transaction occurs.

t) Warrants

Warrants are classified as equity. Incremental costs directly attributable to the issuance of warrants are recognized as a deduction from the proceeds in equity in the period where the transaction occurs.

u) Revenue recognition

Revenue comprises revenues from the sale of commodities received and revenues directly earned from royalty, stream and other interests.

For royalty and stream agreements paid in-kind and for offtake agreements, the Company's performance obligations relate primarily to the delivery of gold, silver or other products to the customers. Revenue is recognized when control is transferred to the customers, which is achieved when a product is delivered, the customer has full discretion over the product and there is no unfulfilled obligation that could affect the customer's acceptance of the product. Control over the refined gold, silver and other products is transferred to the customers when the relevant product received (or purchased) from the operator is physically delivered and sold by the Company (or its agent) to the third party customers. For royalty and stream agreements paid in cash, revenue recognition will depend on the related agreement.

Revenue is measured at fair value of the consideration received or receivable when management can reliably estimate the amount, pursuant to the terms of the royalty, stream and other interest agreements. In some instances, the Company will not have access to sufficient information to make a reasonable estimate of revenue and, accordingly, revenue recognition is deferred until management can make a reasonable estimate. Differences between estimates and actual amounts are adjusted and recorded in the period that the actual amounts are known.

|

Osisko Gold Royalties Ltd Notes to the Consolidated Financial Statements For the years ended December 31, 2021 and 2020 |

|

(tabular amounts expressed in thousands of Canadian dollars, except per share amounts) |

3. Significant accounting policies (continued)

v) Leases

The Company is committed to long-term lease agreements, mainly for office space and mining equipment.

Leases are recognized as a right-of-use asset (presented under non-current other assets on the consolidated balance sheet) and a corresponding liability at the date at which the leased asset is available for use by the Company. Each lease payment is allocated between the liability and finance cost. The finance cost is charged to profit or loss over the lease term so as to produce a constant periodic rate of interest on the remaining balance of the liability for each period. The right-of-use asset is depreciated over the shorter of the asset's useful life and the lease term on a straight-line basis.

Assets and liabilities arising from a lease are initially measured on a present value basis. The lease payments are discounted using the interest rate implicit in the lease. If that rate cannot be readily determined, the Company's incremental borrowing rate is used, being the rate that the Company would have to pay to borrow the funds necessary to obtain an asset of similar value in a similar economic environment with similar terms and conditions.

Payments associated with short-term leases (12 months or less) and leases of low-value assets are recognized on a straight-line basis as an expense in profit or loss.

w) Share-based compensation

Share option plan

Each of the Company and its subsidiary, Osisko Development, offer a share option plan to their respective directors, officers, employees and consultants. Each tranche in an award is considered a separate award with its own vesting period and grant date fair value. Fair value of each tranche is measured at the date of grant using the Black-Scholes option pricing model. Compensation expense is recognized over the tranche's vesting period by increasing contributed surplus based on the number of awards expected to vest. The number of awards expected to vest is reviewed at least annually, with any impact being recognized immediately.

Any consideration paid on exercise of share options is credited to share capital. The contributed surplus resulting from share-based compensation is transferred to share capital when the options are exercised.

Deferred and restricted share units

Each of the Company and its subsidiary, Osisko Development, offer a deferred share units ("DSU") plan to their respective non-executive directors and a restricted share units ("RSU") plan to their officers and employees. DSU may be granted to non-executive directors and RSU may be granted to employees and officers as part of their long-term compensation package, entitling them to receive a payment in the form of common shares, cash (based on the Osisko's share price or Osisko Development's share price at the relevant time) or a combination of common shares and cash, at the sole discretion of Osisko or Osisko Development. The fair value of the DSU and RSU granted by Osisko to be settled in common shares is measured on the grant date and is recognized over the vesting period under contributed surplus with a corresponding charge to share-based compensation. The fair value of the DSU and RSU granted by Osisko Development to be settled in common shares is measured on the grant date and is recognized over the vesting period under non-controlling interests with a corresponding charge to share-based compensation. A liability for the DSU and RSU to be settled in cash is measured at fair value on the grant date and is subsequently adjusted at each balance sheet date for changes in fair value. The liability is recognized over the vesting period with a corresponding charge to share-based compensation.

|

Osisko Gold Royalties Ltd Notes to the Consolidated Financial Statements For the years ended December 31, 2021 and 2020 |

|

(tabular amounts expressed in thousands of Canadian dollars, except per share amounts) |

3. Significant accounting policies (continued)

x) Earnings per share

The calculation of earnings per share ("EPS") is based on the weighted average number of shares outstanding for each period. The basic EPS is calculated by dividing the profit or loss attributable to the equity owners of Osisko by the weighted average number of common shares outstanding during the period.

The computation of diluted EPS assumes the conversion, exercise or contingent issuance of securities only when such conversion, exercise or issuance would have a dilutive effect on the income per share. The treasury stock method is used to determine the dilutive effect of the warrants, share options, DSU and RSU and the if-converted method is used for convertible debentures. When the Company reports a loss, the diluted net loss per common share is equal to the basic net loss per common share due to the anti-dilutive effect of the outstanding warrants, share options, DSU and RSU and convertible debentures.

y) Segment reporting

The operating segments are reported in a manner consistent with the internal reporting provided to the President and Chief Executive Officer ("CEO") who fulfills the role of the chief operating decision-maker. The CEO is responsible for allocating resources and assessing performance of the Company's operating segments. The Company manages its business under two operating segments: (i) acquiring and managing precious metal and other royalties, streams and similar interests, and (ii) the exploration, evaluation and development of mining projects (through Osisko Development).

4. New accounting standards and amendments

New accounting standard

Interest rate benchmark reform - Phase 2

In August 2020, the IASB made amendments to IFRS 9, IAS 39, IFRS 7, IFRS 4 and IFRS 16 to address the issues that arise during the reform of an interest rate benchmark rate, including the replacement of one benchmark with an alternative one. Affected entities need to disclose information about the nature and extent of risks arising from IBOR reform to which the entity is exposed, how the entity manages those risks, and the entity's progress in completing the transition to alternative benchmark rates and how it is managing that transition. The amendments are applicable to financial reporting periods commencing on or after January 1, 2021.

The Company amended its revolving credit facility in 2021 and, as such, the agreement now includes alternative benchmark rates and transition measures. As the amounts drawn under the credit facility are for a period of one to three months, the Company does not expect any significant impact on the transition to a replacement benchmark rate.

Accounting standards issued but not yet effective

The Company has not yet adopted certain standards, interpretations to existing standards and amendments which have been issued but have an effective date of later than December 31, 2021. Many of these updates are not expected to have any significant impact on the Company and are therefore not discussed herein.

Amendments to IAS 16 Property, plant and equipment

The IASB has made amendments to IAS 16 Property, plant and equipment, which will be effective for financial years beginning on or after January 1, 2022. Proceeds from selling items before the related item of property, plant and equipment is available for use should be recognized in profit or loss, together with the costs of producing those items. The Company will therefore need to distinguish between the costs associated with producing and selling items before the item of property, plant and equipment (pre-production revenue) is available for use and the costs associated with making the item of property, plant and equipment available for its intended use. For the sale of items that are not part of a company's ordinary activities, the amendments will require the Company to disclose separately the sales proceeds and related production cost recognized in profit or loss and specify the line items in which such proceeds and costs are included in the statement of comprehensive income (loss). These amendments will have an impact on the Company's consolidated financial statements in 2022.

|

Osisko Gold Royalties Ltd Notes to the Consolidated Financial Statements For the years ended December 31, 2021 and 2020 |

|

(tabular amounts expressed in thousands of Canadian dollars, except per share amounts) |

4. New accounting standards and amendments (continued)

Accounting standards issued but not yet effective (continued)

Amendments to IAS 16 Property, plant and equipment (continued)