UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2016

or

| ¨ | TRANSITION REPORT UNDER SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from ________ to ________

Commission file number 333-201029

| AMERICAN EDUCATION CENTER INC. |

| (Exact name of registrant as specified in its charter) |

| Nevada | 38-3941544 | |

| (State or other jurisdiction of Incorporation or organization) |

(I.R.S. Employer Identification No.) |

| 2 Wall St, Fl. 8 New York, NY | 10004 | |

| (Address of principal executive offices) | (Zip Code) |

Registrant’s telephone number, including area code: (212) 825-0437

Securities registered under Section 12(b) of the Exchange Act: None

Securities registered under Section 12(g) of the Exchange Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act. Yes ¨ No x

Indicate by check mark whether the registrant (1) filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No ¨

Indicate by check mark if disclosure of delinquent filers in response to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendments to this From 10-K. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ¨ | Accelerated filer | ¨ |

| Non-accelerated filer | ¨ | Smaller reporting company | x |

| (Do not check if a smaller reporting company) | |||

| Emerging growth company | x |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised accounting standard provided pursuant to Section 13(a) of the Exchanger Act. ¨

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ¨ No x

The aggregate market value of the voting and non-voting common stock held by non-affiliates of the Registrant as of June 30, 2016 (the last business day of the Registrant’s most recently completed second fiscal quarter) was $6,136,000.{1}

As of April 17, 2017, the registrant had 38,350,000 shares of common stock issued and outstanding.

1 There was no trading for our common stock as of June 30, 2016 and we took reference of the closing price of our common stock on April 14, 2017 (the latest trading information available to us).

EXPLANATORY NOTE

As used in this Annual Report, the terms “we,” “us,” “our,” and words of like import, and the “Company” refers to American Education Center Inc. and all of our subsidiaries unless the context indicates otherwise.

FORWARD LOOKING STATEMENTS

This report contains forward-looking statements and information that are based on the beliefs of our management as well as assumptions made by and information currently available to us. Such statements should not be unduly relied upon. Forward-looking statements include statements about our expectations, beliefs, plans, objectives, intentions, assumptions and other statements that are not historical facts or that are not present facts or conditions. Forward-looking statements and information can generally be identified by the use of forward-looking terminology or words, such as “anticipate,” “approximately,” “believe,” “continue,” “estimate,” “expect,” “forecast,” “intend,” “may,” “ongoing,” “pending,” “perceive,” “plan,” “potential,” “predict,” “project,” “seeks,” “should,” “views” or similar words or phrases or variations thereon, or the negatives of those words or phrases, or statements that events, conditions or results “can,” “will,” “may,” “must,” “would,” “could” or “should” occur or be achieved and similar expressions in connection with any discussion, expectation or projection of future operating or financial performance, costs, regulations, events or trends. The absence of these words does not necessarily mean that a statement is not forward-looking.

Forward-looking statements and information are based on management’s current expectations and assumptions, which are inherently subject to uncertainties, risks and changes in circumstances that are difficult to predict. These statements reflect our current view concerning future events and are subject to risks, uncertainties and assumptions. There are important factors that could cause actual results to vary materially from those described in this report as anticipated, estimated or expected, including, but not limited to, those factors and conditions described under “Item 1A. Risk Factors” as well as general conditions in the economy, petrochemicals industry and capital markets, Securities and Exchange Commission (the “SEC”) regulations which affect trading in the securities of “penny stocks,” and other risks and uncertainties. Except as required by law, we assume no obligation to update any forward-looking statements publicly, or to update the reasons actual results could differ materially from those anticipated in any forward-looking statements, even if new information becomes available in the future. Depending on the market for our stock and other conditional tests, a specific safe harbor under the Private Securities Litigation Reform Act of 1995 may be available. Notwithstanding the above, Section 27A of the Securities Act of 1933, as amended (the “Securities Act”), and Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”), expressly state that the safe harbor for forward-looking statements does not apply to companies that issue penny stock. Because we may from time to time be considered to be an issuer of penny stock, the safe harbor for forward-looking statements may not apply to us at certain times.

| 2 |

PART I

Item 1. Business

Overview

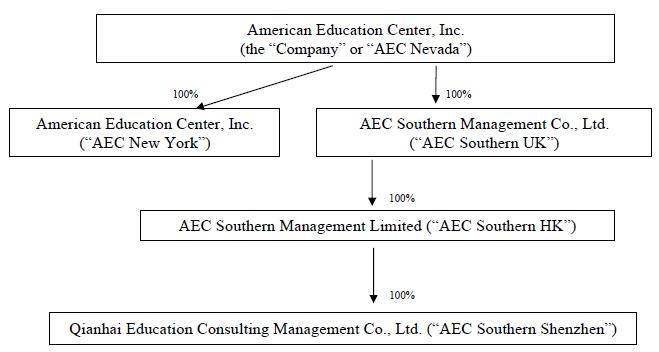

American Education Center Inc. was incorporated in Nevada (“AEC Nevada”) in May 2014 as a holding company, and operates through its wholly owned subsidiaries, American Education Center Inc., incorporated in the state of New York in 1999 (“AEC New York”) and AEC Southern Management Co., LTD, a company formed pursuant to the laws of England and Wales (the “AEC Southern UK”) and the subsidiaries of AEC Southern UK.

AEC New York was approved and licensed by the Education Department of the state of New York in 2003 to engage in education consulting service between the U.S. and China. For over seventeen years, AEC New York has devoted itself to international education exchange between China and the United States, by providing education and career enrichment opportunities for students, teachers, and educational institutions from both countries.

AEC Southern UK provides executive services, specifically, targeted and tailored executive training services to industrial clients in the food-related industries.

AEC Nevada acquired AEC Southern UK and its subsidiaries in 2016 pursuant to a Share Exchange Agreement (defined below), with AEC Southern UK’s wholly owned subsidiary, AEC Southern (Shenzhen) Management Co. Ltd (“AEC Shenzhen”) incorporated as a wholly owned foreign enterprise pursuant to PRC laws. AEC Nevada, AEC New York, AEC Southern UK and its subsidiaries are referred to as the “Company” hereinafter. AEC Southern UK, via AEC Shenzhen, to serve as a local platform for expanding the Company’s business in mainland China. Shenzhen, in the province of Guangdong, is designated by the People’s Republic of China as a Special Economic Zone (“SEZ”) City. SEZs are granted a more free-market oriented economic and regulatory environment, with business and tax policies designed to attract foreign investment and technology.

Our mission is to provide “one-stop comprehensive services” to international students and their families, educators, educational institutions and corporate entities. Our services include admission applications, visa application advice, accommodations and other consulting services to Chinese students who wish to study in the United States, placement services to qualified American educators to teach and live in China, as well as U.S. relocation services to employees of multi-national companies with U.S. operations.

Currently, we provide five types of consulting services:

| · | Student & Family Services, |

| · | Institutional Services, |

| · | Student Exchange Programs, |

| · | Executive Services, and |

| · | Educator Placements. |

Services to our clients are provided through the Company’s principal executive office in New York, NY , and AEC Shenzhen’s office in Shenzhen, China. For marketing, we engage local agents in Shenzhen in Guangdong province, Nanjing in Jiangsu Province, Chengdu in Sichuan Province, and Shanghai in China to promote our services to potential clients, and we plan to engage more agents in China in the future.

Share Exchange with AEC Southern Management Co. LTD.

On November 8, 2016, a certain share exchange agreement (the “Share Exchange Agreement”) was entered into by and among AEC Nevada, AEC Southern UK, Ye Tian (“Tian”), Rongxia Wang (“Wang”) (Tian and Wang, collectively, were the owners of record of 100% equity interest of AEC Southern UK) and Yangying Zou (“Zou”)) where AEC Nevada acquired AEC Southern UK as a 100% subsidiary, for a consideration of 1,500,000 shares of Common Stock. Additionally, AEC Nevada also agreed to appoint Zou to serve as the CEO of AEC Southern UK and agreed to issue to Zou an aggregate of 1,500,000 shares of Common Stock simultaneously as the closing of the transactions underlying the Share Exchange. The transactions underlying the Share Exchange Agreement is referred hereinafter as the Share Exchange Transaction, which was closed on the same day (the “Share Exchange Closing Date”). On March 27, 2017, the parties to the Share Exchange Agreement agreed to amend the Share Exchange Agreement so that the Share Exchange Agreement would take effect on October 31, 2016 and amend the Share Exchange Closing Date to be on October 31, 2016. As of the date of this report, we are in the process of issuing the shares of our Common Stock pursuant to the Share Exchange Agreement.

| 3 |

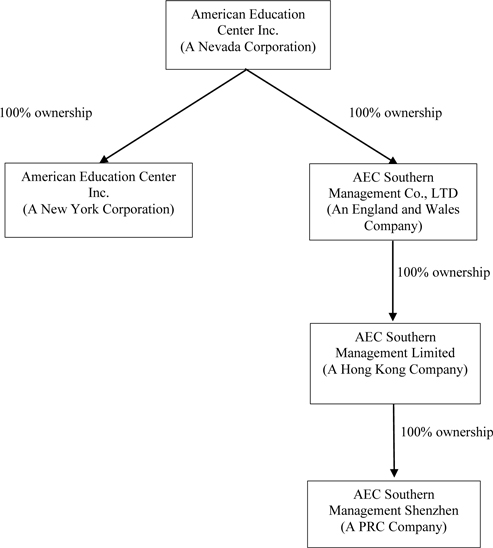

Corporate Structure

The corporate structure of the Company subsequent to the closing of the Share Exchange Agreement is illustrated as follows:

AEC Southern UK was incorporated on December 1, 2015 pursuant to the laws of England and Wales. AEC Southern Management Limited (“AEC HK”) was incorporated on December 29, 2015 pursuant to the laws of Hong Kong, and is a 100% owned subsidiary of AEC Southern UK. AEC Shenzhen was incorporated on April 15, 2016 as a wholly owned foreign enterprise pursuant to PRC laws, and is a 100% owned subsidiary of AEC HK. AEC HK, and AEC Shenzhen are hereinafter referred to as the “AEC Southern Subsidiaries”)

Upon closing of the Share Exchange Transaction, AEC Southern UK and its subsidiaries (AEC HK and AEC Shenzhen) became wholly owned subsidiaries of AEC Nevada.

The address of our principal executive offices and corporate offices is 2 Wall Street, Fl. 8, New York, NY 10005. Our telephone number is (212) 825-0437.

Our Business

American Education Center Inc. was incorporated in Nevada (“AEC Nevada”) in May 2014 as a holding company, and operates in the U.S. through its wholly owned subsidiary, American Education Center Inc., incorporated in the state of New York in 1999 (“AEC New York”), and AEC Southern UK and the AEC Southern Subsidiaries. The Company is devoted to international education exchange and provides education-related consulting services such as educational and career enrichment opportunities to students, educators and educational institutions in both the People’s Republic of China and the United States.

| 4 |

AEC New York was approved and licensed by the Education Department of the State of New York in 2003 to engage in education consulting service between the U.S. and China. For over seventeen years, AEC New York has devoted itself to international education exchange between China and the United States, by providing education and career enrichment opportunities for students, teachers, and educational institutions from both countries.

AEC Southern UK and it subsidiaries were acquired by AEC Nevada in October 2016 pursuant to the Share Exchange Agreement, to serve as a local platform for expanding the Company’s business in mainland China. Shenzhen, in the province of Guangdong, is designated by the People’s Republic of China as a Special Economic Zone (“SEZ”) City. SEZs are granted a more free-market oriented economic and regulatory environment, with business and tax policies designed to attract foreign investment and technology.

Our mission is to provide “one-stop comprehensive services” to international students and their families, educators, educational institutions and corporate entities. Our services include admission applications, accommodations and other consulting services to Chinese students who wish to study in the United States, placement services to qualified American educators to teach and live in China, as well as U.S. relocation services to employees of multi-national companies with U.S. operations.

Currently, we provide five types of consulting services:

| · | Student & Family Services, |

| · | Institutional Services, |

| · | Student Exchange Programs, |

| · | Executive Services, and |

| · | Educator Placements. |

Services to our clients are provided through the Company’s principal executive office in New York, NY, as well as in Hong Kong and China at client sites through AEC Southern UK. For marketing, we engage local agents in Shenzhen in Guangdong province, Nanjing in Jiangsu Province, Chengdu in Sichuan Province, and Shanghai in China to promote our services to potential clients, and we plan to engage more agents in China in the future.

Our Student & Family Services provide guidance and consulting services to help our client students and their families throughout the school application and admission process, and continuing with their studying and living needs while they complete their degrees. Beyond graduation, we can continue to help them secure suitable internships and other career development opportunities in the United States.

Our Student & Family Services fall into three sub-categories: Academic, Life and Career.

The Academic offering focuses on providing admission services for Chinese students to study in the U.S., English as a Second Language (ESL) training program, and the Elite 100 program. For middle school students, we assist in providing information on U.S. high schools. We also help high school graduates with admissions applications to U.S. colleges and universities.

We place ESL teachers in our representative offices in China to conduct ESL programs. Students who enroll in this program receive preparation in taking ESL tests and will obtain certificates upon successfully passing these tests.

AEC’s Elite 100 Program provides consulting services to talented Chinese students to enable them to reach a comprehensive understanding of American politics, business, science, education, culture and other areas. We offer academic consulting services to these top Chinese students to apply to prestigious colleges and universities in the United States. In connection with our admission services, we assist these students in arranging campus tours, writing programs, tailored ESL language programs and interview guidance. After the students are admitted into U.S. colleges/universities, we provide consulting services in connection with applications for a second major, transfers, housing accommodations, accelerated degree applications and other services. We enroll the students in seminars and events in which we partner with other business organizations, governments, non-government organizations (“NGOs”), scholars and universities to help these students build social networks and cultivate their leadership skills. We also help arrange extracurricular activities tailored for each student, such as organized artistic endeavors including dance, music, painting, photography and other performance events to enrich their cultural experience.

Our Life program offers consulting services, including personalized VIP services, to assist our Chinese clients to settle in the U.S. so they can focus effectively on their studies, as well as VIP services for the families of our students to visit and/or settle in the U.S. The Company refers its customers to its business partners in the U.S. to assist the customers with purchasing real estate properties, organizing their personal financial management and investment needs, buying insurance and starting businesses. These VIP services provide “concierge services” personally tailored for our clients to meet almost all aspects of their needs during their stay in the U.S. Every VIP client has an exclusive consultant to help meet his or her needs and monitors their progress along the way, so that a customized career plan can be developed taking into consideration changing conditions. VIP services include high school enrollment, college applications, medical insurance, parental travel support, housing, legal and immigration status, internship, job application and referrals to financial and real estate investment advisory firms and other related services.

| 5 |

Our Career program focuses on clients’ career development by identifying internship and work opportunities that are suitable to their educational background and experience level. Through this program we strive to provide clients with potential career paths, assist them in every step of the way from academic improvement to career assistance. In addition, we introduce our student customers to companies and prospective employers that may potentially provide internships and part-time or full-time work opportunities to our student customers.

Our Institutional Services assist U.S. institutions such as middle schools, high schools, and universities and colleges, to enroll students from China by establishing alliances and strategic business partnerships with colleges and universities in China. Educational institutions in the U.S. retain us to reach, market to and recruit a broad population of prospective students. Although many U.S. educational institutions are interested in attracting more students from China to diversify their student bodies, they often have a difficult time marketing to and enrolling students from China often due to lack of understanding Chinese culture and access to qualified students. We serve as an international liaison to provide marketing services to students in China. We enter into agreements with U.S. schools to market their institutions, academic programs, local environment and their students’ lifestyle on their behalf

Pursuant to our Student Exchange Programs, we recruit and enroll Chinese students in U.S. educational institutions for Exchange Programs, whereby students will finish the remainder of their education and receive their diplomas in China.

Pursuant to our Executive Services, via AEC New York we provide services to Chinese and other multi-national corporate clients whose executives are moving to the U.S. for work. We assist them in all aspects of relocation as well as their preparation for visa applications, as well as offering a full range of family support services. Via AEC Southern UK, we provide targeted and tailored executive training services to industrial clients in the food-related industries. From time to time, our clients request us to create customized training courses for and run the courses for their senior executives in specific areas such as regulatory compliance, human resources management, organizational management, business model development, and government relations. To provide this type of training we work with third-party vendors to design one-week or two-week training programs conforming to our clients’ specifications. We organize and arrange the training sessions, while the instructors are outsourced from our vendors.

Finally, our Educator Placement services are designed to meet the increasing demands for foreign teachers in both the U.S. and China. Our program helps teachers in the U.S. or China who plan to gain experience in another country find the most suitable positions. We also recruit and place native English speaking teachers for our clients and business partners in China, and recruit and place Chinese-speaking teachers in U.S. educational institutions. In order to ensure that educators experience a smooth transition, we also provide local services to educators, which include settlement services, financial services, assistance with insurance coverage, tax services, living services, as well as business consulting services.

Growth Strategy

We intend to expand our business both organically and by acquisition.

Organic Growth. We may our sales efforts to create organic growth from existing clients. From our existing client base, we provide the highest level of individual services to help our clients in any way to have a smooth transition to the U.S., including visa consulting services, travel guides, life advice, investment consulting and other services. In addition, growing our existing relationships is key. Through over 17 years of continuous growth, we have built significant industry credibility and a solid reputation, which enables us to partner with quality third-party businesses in providing services to our clients when needed, which provides quality services efficiently and at a competitive cost.

Growth by Acquisition. We may grow our business through the acquisition of marketing teams and educational institutions, both in the U.S. and abroad, through a careful, gradual and targeted approach mindful of the Company’s financial resources. Our acquisition of AEC Southern and its subsidiaries that has operation in Shenzhen, Guangdong, China, is the first step in the international acquisition process. Using this business as a platform for expansion, in the coming months and years we expect to enhance our educational and industrial training businesses through the addition of China-based companies and personnel in complementary areas of activity.

| 6 |

Industry

The demand for global education is growing rapidly in China, and the United States remains the top choice for Chinese students wishing to study abroad. According to a report published in 2014 by the Ministry of Education of the People’s Republic of China, more than three million Chinese students had studied in a foreign country.

The number of Chinese students entering the U.S. for study grew sharply in 2006, when Congress loosened restrictions on student visas from China for the first time since the tragic events of September 11, 2001, and this trend has continued strongly since then. Accordingly there is a large and growing number of Chinese students in the U.S. seeking a broad range of acclimation support and services, including education consulting services. We strive to become a bridge for these students with our service offerings.

According to Project Atlas, a collaborative global research initiative led by the Institute of International Education, in the academic year 2015-2016, the total number international students studying in the U.S. (in both public and private institutions) was 1,043,839, of which 328,547, or 31.5%, were Chinese nationals. For the academic year 2014-2015, the comparable figures were 974,926 international students in the U.S., of whom 31.2% or 304,040 were Chinese. This growth trend has been in place for several years. However, with the current political environment in Washington, DC regarding visas and immigration, it is not known whether it will continue in the future.

Moreover, the number of U.S. students studying in China, while smaller, is also experiencing steady growth. According to China’s Ministry of Education, this figure was 21,875 in 2015, the most recent available data, representing growth of over 50% over the preceding five years. The Company believes that this figure will continue to grow as well, as both the U.S. and Chinese governments have encouraged public and private programs supporting Chinese-American education exchange and cooperation. At the top levels of government, recent communications between U.S. Secretary of State Rex Tillerson, and China’s Foreign Minister Wang Yi and State Councilor Yang Jiechi have newly emphasized the crucial importance of the U.S.-China bilateral relationship in the global political and economic spheres.

| 7 |

Competition

The education consulting business in China is rapidly evolving, highly fragmented and competitive, and we expect competition in this sector to persist and intensify. We face competition from a number of companies in each of the major service segments we offer and each geographic market in which we operate, including the following:

Boya Elite International, based in China, offers overseas educational programs for students and executives from China.

The Study Abroad Foundation, an international university network based in Indiana, advises study-abroad host educational institutions on attracting international students and structuring study abroad programs according to the needs of international students.

Taisha.org, based in China, provides students high school/college application services including application evaluation, planning (mentor one-on-one), preparation for exams (TOEFL, GMAT, GRE, SAT, etc.), and application processing assistance. They also help students find internship and full-time job opportunities.

New Oriental Education & Technology Group, Inc., NYSE-listed and based in China, offers a range of educational services, including language training, test preparation, K-12 all-subjects training, international study consulting, career services for overseas returnees, global study tours, and online education.

Finally, several China-based enterprises offer English as a Second Language (“ESL”) preparation courses from companies that offer similar preparation courses in China.

With respect to the industrial executive training programs that we offer through our AEC Southern UK and its subsidiaries, we face substantial competition from local providers of similar services, including Weifang Baina Accreditation Consulting Co., Ltd, Deen (Guangzhou) Accreditation Consulting Co. Ltd,, and Zhengzhou Boda Quality System Certification Consulting Co., Ltd.

However, we believe that our competitors do not integrate and provide services in all of the major segments in which we operate (for students, institutions, and educators) as well as we do. We believe that our principal competitive advantages include the following:

| · | provide one-stop integrated services to students, teachers, and institutions; |

| · | brand recognition and reputation; |

| · | a business model that aligns personalized services to the specific needs of students and institutions; |

| · | overall customer satisfaction; |

| · | size and coverage of service network and proximity of services to customers; |

| · | scope, quality and consistency of service. |

Our key competitive strengths lie in our individualized attention to students, our ability to place educators at top universities around the globe and specifically in the US, and our understanding of the globalization needs of top universities in recruiting both international students and faculty in an ever evolving educational landscape, with one-stop service. However, some of our existing and potential competitors may have more resources than we do. These competitors may be able to devote greater resources than we can to the development, promotion and sale of their programs, services and products and respond more quickly than we can to changes in student demands, testing materials, admissions standards, market needs or new technologies.

Operations

Since 1999, the Company has been devoted to international education exchange by providing education-related consulting services such as educational and career enrichment opportunities to students, educators and educational institutions in both the PRC and the United States. The Company’s mission is to provide “one-stop comprehensive services” to international students and their families, educators, educational institutions and corporate entities. Our services include admission applications, visa application advice, accommodations and other consulting services to Chinese students who wish to study in the United States, placement services to qualified American educators to teach and live in China, as well as U.S. relocation services to employees of multi-national companies with U.S. operations.

In addition to supporting AEC New York’s education consulting services, AEC Southern UK and AEC Southern Subsidiaries also provide executive services, specifically targeted and tailored executive training services in its local market. Currently we have two commercial clients in the packaged food import / export business who from time to time request from us customized training courses in specific areas such as food industry regulation compliance in various geographical regions, ISO 9001 compliance, human resources management, organizational management, business model development, and government relations. Our clients provide us with specifications as to the areas in which they wish us to provide training to their executives, whereupon we work with our vendors to design training programs for one-week or two-week or as needed, conforming to our clients’ specifications. We organize and arrange the training sessions, while the instructors are outsourced from our vendors.

We intend at this time to expand this business model to other, similarly regulated industries, such as food supplements and pharmaceuticals.

| 8 |

Marketing Strategies

We employ a variety of marketing and recruiting methods to attract students, institutions and teachers. By doing so, we intend to continue fostering a standard corporate identity across our education network both in China and the US.

We believe prospective students, institutions, and teachers are attracted to our services due to our excellent brand name, our personalized service model and the quality of our programs. We employ the following marketing methods to attract new students, institutions and teachers and retain existing customers:

Referrals. Our student enrollments have benefited from, and are expected to continue to benefit from, word-of-mouth referrals by our current and former customers. We believe good service combined with referrals is a steady way to grow our business and reputation.

Public Events and seminars. For several years we have successfully hosted the ESL (English as a Second Language) Annual Conference in China, which annually hosts over 500 attendees. The Company is planning to continue the annual conference this year. We plan to host marketing events in New York City to promote the Company’s services and brand name. In addition, the Company regularly attends higher education conferences held annually to further promote and market our services.

Sponsorships. We are proud sponsors of Chinese Student Associations in various higher education institutions in the Greater New York Area. We regularly promote our services to members and students of the various Chinese Student Associations and are regularly present at events held by such Associations. This is another steady source of business for us.

Marketing Materials. We plan to publish a “Chinese Visitors Guide Book”. It is planned to be a travel book with plug-in advertisements for the Company, which will assist Chinese visitors to the U.S. and simultaneously promote our services. We will also advertise in e-magazines, prepare and distribute brochures and present at exhibitions as part of our marketing strategy.

Media and social media marketing. We plan to develop a mobile app in the future. We plan to open a business account named “AEC Elite 100 Club” with the popular smart phone instant messenger app WeChat. “Elite U.S. Club” will be a free service platform aiming to market our company and services to potential customers. WeChat users can subscribe to our personalized VIP services through their free accounts opened with “AEC Elite 100 Club”. The subscribers will receive rebates based on their membership levels, which are based on tenure. Our members can upgrade their membership by their cumulative consumption of services available through AEC Elite 100 Club.

Acquisitions. Most importantly, the Company plans to further engage in acquiring other education consulting Chinese companies in our industry or our competitors in China. Mergers and acquisitions will help the Company acquire a broader additional customer base, allowing us to generate more revenue. We hope to acquire such target companies by a combination of cash payment and issuance of equity in AEC Nevada.

Government Regulation

Regulation of the Education Industry in the United States

Government authorities in the United States, at the Federal, state and local level, extensively regulate education and exchange student programs. Such regulations include, among other things, the regulations and policies of the United States Department of Education. However, unlike the systems of most other countries, education in the United States is highly decentralized, and the Federal government and Department of Education are not heavily involved in determining curricula or educational standards. The establishment and grading of such standards has been left to state and local school districts.

| 9 |

A more formalized regulation is the requirement that a citizen of a foreign country who wishes to enter the United States must first obtain a visa, either a nonimmigrant visa for temporary stay, or an immigrant visa for permanent residence. Foreign students must have a student visa to study in the United States. Visas generally require an application and an interview.

The process of obtaining regulatory approvals and the subsequent substantial compliance with appropriate Federal, state, local and foreign statutes and regulations may require the expenditure of substantial time and financial resources.

In addition to the regulatory approval requirements described above, we are or will be, directly, or indirectly, subject to extensive regulation of the educational industry by the Federal and state governments and the governments’ of foreign countries in which our services are provided.

Regulation of the Education Industry in China

The laws that directly or indirectly affect our ability to operate our business in the PRC include the following:

The principal regulations governing private education in China consist of the Education Law of the PRC, the Law for Promoting Private Education (2003). The Implementation Rules for the Law for Promoting Private Education (2004) and the Regulations on Chinese-Foreign Cooperation in Operating Schools. Below is a summary of relevant provisions of these regulations.

On March 18, 1995, the National People’s Congress enacted the Education Law of the PRC, or the Education Law. The Education Law sets forth provisions relating to the fundamental education systems of the PRC, including a school system of pre-school education, primary education, secondary education and higher education, a system of nine-year compulsory education and a system of education certificates. The Education Law stipulates that the government formulates plans for the development of education and establishes and operates schools and other institutions of education and, in principle, enterprises, social organizations and individuals are encouraged to operate schools and other types of education organizations in accordance with PRC laws and regulations. As such, no organization or individual may establish or operate a school or any other educational institution for profit-making purposes. However, according to the Law for Promoting Private Education, private schools may operate for “reasonable returns.”

If our operations are found to be in violation of any of these laws, regulations, rules or policies or any other law or governmental regulation to which we or our customers are or will be subject, or if interpretations of the foregoing changes, we and our commercialization partners may be subject to civil and criminal penalties, damages, fines, and the curtailment or restructuring of our operations. Similarly, if our customers are found non-compliant with applicable laws, they may be subject to sanctions.

Properties/Facilities

Our main executive office is located at 2 Wall Street, Fl. 8, New York, NY 10004. In December 2014, the Company entered into a lease for office space with an unrelated party. The lease was to commence on December 11, 2014, however, due to renovation issues, the lease was changed and commenced on March 1, 2015 and the Company received two months of free rent. This lease agreement requires a monthly rental of $29,558 and expires on July 31, 2025.

| 10 |

The Company leased office space from an unrelated third party for a period from March 2014, to May 31, 2016. This lease agreement required a monthly rental of $13,554, and was terminated in December 2015.

AEC Shenzhen leases office space from an unrelated third party for a period from April 1, 2016 to March 31, 2018. This lease agreement requires a monthly rental of RMB 2,000 (approximately US$290).

We believe our facilities are sufficient for our business operations.

Employees

As of the filing date hereof, the Company has 12 full-time employees, and 33 independent contractors. None of our employees are represented by a labor union. We have not experienced any work stoppages, and we consider our relations with our employees to be good.

Off-Balance Sheet Arrangements

We did not have, during the periods presented, and we are currently not a party to, any off-balance sheet arrangements.

Seasonality

AEC New York typically experiences seasonal fluctuations in its revenues and results of operations, primarily due to quarterly changes in student enrollments resulting from admission seasons. AEC Southern UK does not experience substantial seasonality in its revenues.

ITEM 1A. RISK FACTORS

An investment in our shares of common stock involves a high degree of risk. You should carefully consider the following risk factors, together with the other information contained in this prospectus, before you decide to buy any shares. Any of the following risks could cause our business, results of operations and financial condition to suffer materially, causing the market price of our shares of common stock to decline, in which event you may lose part or all of your investment in our shares of common stock. Additional risks and uncertainties not currently known to us or that we currently do not deem material may also become important factors that may materially and adversely affect our business.

| 11 |

Risks Related to Our Business

If we are not able to continue to attract students to enroll in our courses without a significant decrease in course fees, our revenues may decline and we may not be able to maintain profitability.

The success of our business depends primarily on the number of student enrollments in our courses and the amount of course fees that our students are willing to pay. Therefore, our ability to continue to attract students to enroll in our courses without a significant decrease in course fees is critical to the continued success and growth of our business. This in turn will depend on several factors, including our ability to develop new programs and enhance existing programs to respond to changes in market trends and student demands, expand our geographic reach, manage our growth while maintaining the consistency of our service quality, effectively market our programs to a broader base of prospective students, develop and license additional high-quality educational content and respond to competitive pressures, as well as the ability of our partner colleges and institutions to maintain their faculties’ teaching quality. If we are unable to continue to attract students to enroll in our courses without a significant decrease in course fees, our revenue may decline and we may not be able to operate profitability.

We depend on the dedicated and capable faculties of our partner colleges and institutions, and if our partner colleges and institutions are not able to continue to hire, train and retain qualified teachers, we may not be able to maintain consistent teaching quality throughout our school network and our brand, business and operating results may be materially and adversely affected.

The teachers of our partner colleges and institutions are critical to maintaining the quality of our programs, services and products and building and maintaining our brand and reputation. It is critical for us to continue to attract qualified teachers who have a strong command of the subject areas to be taught and meet our qualification. We also need to hire teachers who are capable of delivering innovative and inspirational instruction. The number of teachers in China with the necessary experience and language proficiency to teach our courses is limited and we must provide competitive compensation packages to attract and retain qualified teachers. In addition, criteria such as commitment and dedication are difficult to ascertain during the recruitment process, in particular as we continue to expand and add teachers to meet rising student enrollment. We must also provide continuous training to our teachers so that they can stay up to date with changes in student demands, admissions and assessment tests, admissions standards and other key trends necessary to effectively teach their respective courses. We may not be able to hire, train and retain enough qualified teachers to keep pace with our anticipated growth while maintaining consistent teaching quality across many different schools, learning centers and programs in different geographic locations. Shortages of qualified teachers or decreases in the quality of our instruction, whether actual or perceived, in one or more of our markets may have a material and adverse effect on our business.

Our business depends on our brand name “American Education Center”, and if we are not able to maintain and enhance our brand, our business and operating results may be harmed.

We believe that market recognition of our name “American Education Center” has contributed significantly to the success of our business. We also believe that maintaining and enhancing the “American Education Center” brand is critical to maintaining our competitive advantage. We offer a diverse set of programs, services and products to primary and middle school students, college students and other adults throughout many provinces and cities in China. As we continue to grow in size, expand our programs, services and product offerings and extend our geographic reach, our ability to maintain and improve the quality and consistency of our services, products and offerings may be more difficult to achieve.

We have invested in brand promotion activities. We cannot assure you that these or our other marketing efforts will be successful in promoting our brand to remain competitive and well recognized. If we are unable to further enhance recognition of our brand and our programs, services and products, or if we incur excessive marketing and promotion expenses, our business and results of operations may be materially and adversely affected. In addition, any negative publicity relating to our Company or our programs and services, regardless of its veracity, could harm our brand image and in turn materially and adversely affect our business and operating results.

| 12 |

If we fail to successfully execute our growth strategies, our business and prospects may be materially and adversely affected.

Our growth strategies include expanding our programs, services and product offerings and our network with schools and learning centers, updating and expanding the content of our programs, services and products in a cost-effective and timely manner, as well as maintaining and continuing to establish strategic relationships with other businesses. The expansion of our programs, services and products in terms of types of offerings and geographic locations may not succeed due to competition, failure to effectively market our new programs, services and products and maintain their quality and consistency, or other factors. In addition, we may be unable to identify new cities with sufficient growth potential to expand our network, and we may fail to attract students and increase student enrollments or recruit, train and retain qualified teachers for our new schools and learning centers. Some cities in China have undergone development and expansion for several decades while others are still at an early stage of urbanization and development. In more developed cities, it may be difficult to increase the number of schools and learning centers because we and/or our competitors already have extensive operations in these cities. In recently developed and developing cities, demand for our programs, services and products may not increase as rapidly as we expect. Furthermore, we may be unable to develop or license additional content on commercially reasonable terms in a timely manner, or at all, to keep pace with changes in market demands. If we fail to successfully execute our growth strategies, we may be unable to maintain and grow our business operation, and our business and prospects may be materially and adversely affected.

We face significant competition in each major program and service that we offer and each geographic market in which we operate, and if we fail to compete effectively, we may lose our market share and our profitability may be adversely affected.

The private education sector in China is rapidly evolving, highly fragmented and competitive, and we expect competition in this sector to persist and intensify. We face competition in each of the major programs we offer and each geographic market in which we operate. For example, we face competition for our student services from Boya Elite International, which offers overseas educational programs for students and business leaders from China. We face competition from The Study Abroad Foundation for our institutional services, which advises study-abroad host educational institutions on attracting international students and better structuring study abroad programs according to the needs of international students. We also face nationwide competition for our English as a Second Language (“ESL”) preparation courses from companies, which offer similar preparation courses in China. Refer to Business – Competition for more detailed information.

Our student enrollments may decrease due to intense competition. Some of our competitors have greater resources than we have. These competitors may be able to devote greater resources than us to the development, promotion and marketing of their programs, services and products and respond more quickly than we can to changes in student needs, testing materials, admissions standards or new technologies. In addition, we face competition from many different smaller sized organizations that only focus on some of our targeted markets, and they may be able to respond faster to changes in student preferences in these markets. Furthermore, the increased use of the Internet, and advances in internet and computer related technologies, such as web-based video conference and online testing simulators, are lowering geographic and cost entry barriers to provide private educational services. As a result, many of our international competitors that offer online test preparation and language training courses may be able to penetrate the China market more effectively. Many of these competitors have strong education brands, which may cause students and parents in China to be more attracted to these companies based in the country that the student wishes to study in or in which the selected language is widely spoken. Moreover, many smaller companies are able to use the Internet to offer their programs, services and products to a large number of students in an expedient and cost-effective manner and with less capital expenditures than was previously required. We may have to lower our course fees or increase our spending in order to retain or attract students or pursue new market opportunities. As a result, our revenues and profitability may decrease. We cannot assure you that we will be able to compete successfully against current or future competitors. If we are unable to maintain our competitive position or otherwise respond to evolving competition effectively, we may lose our market share and our profitability may be adversely affected.

| 13 |

The uncertainty involving the immigration policies of the current administration of the U.S. could have significant adverse effects on the demand for our business, and may negatively impact our results of operation.

The current U.S. administration has evoked uncertainty among international students, and overseas business owners who wish to travel to the U.S. for education opportunities and business opportunities, respectively. Our business model and revenue depends on the demand of international students and overseas business owners, and as such, could have a negative impact in our results of operation.

Failure to adequately and promptly respond to changes in testing materials, admissions standards and technologies could cause our programs, services and products to be less attractive to students.

Admissions and assessment tests undergo continuous changes, with respect to the focus of the subjects and questions asked, the format of the tests and the manner in which the tests are administered. For example, certain admissions and assessment tests in the United States now include an essay component, which require us to hire and train teachers to be able to analyze written essays that tend to be more subjective in nature and require a higher level of English proficiency. In addition, some admissions and assessment tests that were previously offered in paper format only are now offered in a computer-based testing format. These changes require us to continually update and enhance our test preparation materials and our teaching methods, and could lead to an increase in our expenses and a decrease in profitability.

If colleges, universities and other higher education institutions reduce their reliance on admissions and assessment tests, we may experience a decrease in demand for our admission preparation services and our business may be materially and adversely affected.

We provide preparation services for Chinese students seeking admission to colleges and universities in the United States. We derive a significant portion of our revenues from such preparation services for admission to higher education institutions. The success of our admission services depends on the continued use of admission and assessment tests as a requirement for admission or graduation. If these tests are changed and we are unable to maintain a program to keep up with these changes or if these tests are not utilized by the colleges and universities, our business can be materially and adversely affected.

In the United States, there has been a continuing debate regarding the usefulness and effectiveness of admission and standard assessment tests to assess qualifications of applicants and many people have criticized the use of these tests as unfairly discriminatory against certain test takers. If a large number of educational institutions abandon the use of existing admission and standard assessment tests as a requirement for admission, without replacing them with other admission and assessment tests, we may experience a decrease in demand for our test preparation courses and our business may be materially harmed.

New programs, services and products that we develop may compete with our current offerings.

We are constantly developing new programs, services and products to meet changes in student demands and respond to changes in testing materials, admissions standards, market needs and trends and technological changes. While some of the programs, services and products that we develop will expand our current offerings and increase student enrollments, others may compete with or make irrelevant our existing offerings without increasing our total student enrollments. For example, our online courses may take away students from our existing classroom-based courses, and our partnership with new schools and learning centers may take away students from our existing schools and learning centers. If we are unable to expand our program, service and product offerings while increasing our total student enrollments and profitability, our business and growth may be adversely affected.

Our business is subject to fluctuations caused by seasonality or other factors beyond our control, which may cause our operating results to fluctuate from quarter to quarter.

For our AEC New York operations, we have experienced, and expect to continue to experience, seasonal fluctuations in our revenues and results of operations, primarily due to quarterly changes in student enrollments resulting from admission seasons. Historically, we receive deposits for our services during the second and third quarters of our fiscal year that usually lead to increased revenues during the subsequent quarters. However, deposits are refundable and thus, if the student client is not accepted to the college or university (normally in the third and fourth quarters of our fiscal year) our revenues during these quarters may be lower than in previous quarters. In addition, because these deposits can be refundable, revenue cannot be recognized until we successfully complete our services and our student clients receive admission offers to higher education institutions. These fluctuations could result in volatility and adversely affect our operations from one quarter to the next. As our revenues grow, these seasonal fluctuations from AEC New York’s business operations may become more pronounced.

| 14 |

Our historical financial and operating results are not indicative of our future performance; and our financial and operating results are difficult to forecast.

Our financial and operating results to date are not necessarily indicative of future operating results. In addition to the fluctuations described above, our revenues, expenses and operating results may vary from quarter to quarter and from year to year in response to a variety of other factors beyond our control, including, but not limited to:

| · | general economic conditions; |

| · | regulations or actions pertaining to the provision of private educational services in China; |

| · | detrimental negative publicity about us, our competitors or our industry; |

| · | changes in consumers’ spending patterns; and |

| · | non-recurring charges incurred in connection with acquisitions or other extraordinary transactions or unexpected circumstances. |

Due to these and other factors, we believe that quarter-to-quarter comparisons of our operating results may not be indicative of our future performance, and therefore you should not rely on them to predict the future performance of our Company. In addition to the above factors, our past results may not be indicative of future performance because of new businesses developed or acquired by us.

Our business is difficult to evaluate in part because we have limited experience with respect to some of our newer services, programs and offerings.

Historically, our core business has been student admission services for college and graduate degree programs, educator placement, and recruiting and consulting services to higher educational institutions between the United States and China. We continually develop ideas for new services to expand our business and client base and we launch new projects on a regular basis. Some of these new service offerings have not generated significant revenues to date, and we have, necessarily, less experience responding quickly to changes, competing successfully and maintaining and expanding our brand in such new project areas. Consequently, there is limited operating history on which you can base your evaluation of the business and prospects of these relatively newer operations.

The continuing efforts of our senior management team and other key personnel are important to our success, and our business may be harmed if we lose their services.

The continuing services of our senior management team is very important to us, in particular, those of Max Chen, our founder and Chairman, who has been with AEC New York since its inception in 1999. If one or more of our senior executives or other key personnel are unable or unwilling to continue in their present positions, we may not be able to replace them easily, and our business may be disrupted or suffer from their departure. Competition for experienced management personnel in the private education sector is intense, the pool of qualified candidates is limited, and we may not be able to retain the services of our senior executives or key personnel, or attract and retain high-quality senior executives or key personnel in the future. In addition, if any member of our senior management team or any of our other key personnel joins a competitor or forms a competing company, we may lose teachers, students, and key professionals and staff members.

| 15 |

Some of Our Officers and Our Director have limited public company experience, which could result in their inability to properly manage Company affairs. The Company’s needs could exceed the level of experience they may have.

Currently, the responsibility of fulfilling the reporting requirements of a public company falls upon the officers and director of the Company. Our President and sole director, Mr. Max P. Chen and our CEO, both have limited experiences in complying with the various rules and regulations that are required of a public company, and as a result, he may not be able to successfully operate a public company, even if the Company’s operations are successful. Additionally, while each of the Company’s officers and director will use their best judgment to resolve all potential conflicts of interest, we cannot guarantee that any potential conflicts can be avoided or resolved. In the event they are unable to fulfill any aspect of their duties to the Company attributable to potential conflicts of interest, the Company may experience a shortfall or complete lack of sales resulting in little or no profits and eventual closure of its business.

Furthermore, the management of future growth will require, among other things, continued development of the Company’s financial and management controls and management information systems, stringent control of costs, increased marketing activities, ability to attract and retain qualified management, research and marketing personnel. The Company’s business plan currently does not provide for the hiring of any additional employees, other than outlined in its Plan of Operations, until operation can support the expenses. Until that time, the responsibility of developing the Company’s business, and fulfilling the reporting requirements of a public company will fall upon the officers and sole director of the Company.

We are an “emerging growth company,” and we cannot be certain if the reduced reporting requirements applicable to emerging growth companies will make our common stock less attractive to investors.

We are an “emerging growth company,” as defined in the Jumpstart Our Business Startups Act, or the JOBS Act. For as long as we continue to be an emerging growth company, we may take advantage of exemptions from various reporting requirements that are applicable to other public companies that are not emerging growth companies, including not being required to comply with the auditor attestation requirements of Section 404(b) of the Sarbanes-Oxley Act, reduced disclosure obligations regarding executive compensation in our annual reports and proxy statements and exemptions from the requirements of holding a nonbinding advisory vote on executive compensation and shareholder approval of any golden parachute payments not previously approved. We could be an emerging growth company for up to five years, although we could lose that status sooner if our revenues exceed $1,000,000,000, if we issue more than $1,000,000,000 in non-convertible debt in a three year period, or if the market value of our common stock held by non-affiliates exceeds $100,000,000 as of any April 30 before that time, in which case we would no longer be an emerging growth company as of the following April 30. We cannot predict if investors will find our common stock less attractive because we may rely on these exemptions. If some investors find our common stock less attractive as a result, there may be a less active trading market for our common stock and our stock price may be more volatile.

We have elected to use the extended transition period for complying with new or revised accounting standards under Section 102(b)(2) of the Jobs Act, that allows us to delay the adoption of new or revised accounting standards that have different effective dates for public and private companies until those standards apply to private companies. As a result of this election, our financial statements may not be comparable to companies that comply with the public company effective dates.

| 16 |

Risks Related To Doing Business in China

The PRC laws and regulations governing the Company’s business operations are sometimes vague and uncertain. Any changes in such PRC laws and regulations may have a material and adverse effect on the PRC economy and the educational industry in particular, and in turn the Company’s business, so will any changes in PRC economic, political and social conditions. The company may be subject to limitations on its ability to operate consulting services for overseas studies under PRC laws and regulations.

There are substantial uncertainties regarding the interpretation and application of PRC laws and regulations, including but not limited to the laws and regulations governing the Company’s business, or the enforcement and performance of the Company’s arrangements with customers in the event of the imposition of statutory liens, death, bankruptcy and criminal proceedings. The Company and any future subsidiaries are considered foreign persons or foreign funded enterprises under PRC laws, and as a result, the Company is required to comply with PRC laws and regulations. These laws and regulations are sometimes vague and may be subject to future changes, and their official interpretation and enforcement may involve substantial uncertainty.

The effectiveness of newly enacted laws, regulations or amendments may be delayed, resulting in detrimental reliance by foreign investors. New laws and regulations that affect existing and proposed future businesses may also be applied retroactively. The Company cannot predict what effect the interpretation of existing or new PRC laws or regulations may have on the Company’s businesses.

Doing business in the PRC is subject to many uncertainties and changes in the political, economic or social direction of the PRC could have an adverse effort on the Company’s operations.

While the PRC economy has experienced significant growth in the past two to three decades, growth has been uneven, both geographically and among various sectors of the economy. Demand for our educational services depends, in large part, on economic conditions in China. Any significant slowdown in China’s economic growth may cause our potential students to delay or cancel their plans to enroll in our schools, which in turn could reduce our revenue.

The Company’s operations may be adversely affected by significant political, economic and social uncertainties in the PRC. The differing cultures, business preferences, corruption, deserve uncertain government regulations, tax systems and currency regulations are risks that can impact the Company’s operations. Although the PRC government has been pursuing economic reform policies, no assurance can be given that the PRC government will continue to pursue such policies or that such policies may not be significantly attend, especially in the event of a change in leadership, social or political description or unforeseen circumstance, there is also no guarantee that the PRC government’s pursuit of economic reforms will be consistent, effective or continue.

Regarding intermediate and consulting business activities relating to self-funded overseas studying, the Ministry of Education (“MOE”), the Ministry of Public Security and the SAIC jointly issued the Administrative Regulations on Intermediate Services for Overseas Studies with Private Funds and their Implementing Rules in 1999, which require that any intermediate service organization engaged in such services procure from the MOE the Recognition on the Intermediate Service Organization for Self-funded Overseas Studies.

As a U.S. incorporated company headquartered in the U.S., we believe that we are not required to obtain the license aforementioned for our business operation in the United States. Our three representative offices in China engage in consulting services for overseas studies, and other consulting services, are registered with the local administration of industry and commerce, but have not applied for or obtained relevant licenses to engage in consulting services for overseas studies from the local authority. Local government may request our representative offices to obtain such licenses or suspend the business operations of our representative office in China if we fail to obtain such licenses.

| 17 |

Governmental control of currency exchange may affect the value of an investment in the Company and may limit our ability to receive and use our revenues effectively.

At the present time, the Renminbi, the currency of the PRC, is not a freely convertible currency. We receive a significant portion of our revenue in Renminbi, which may need to be converted to other currencies, primarily U.S. dollars, in order to be remitted outside of the PRC. The PRC government imposes controls on the convertibility of Renminbi into foreign currencies and, in certain cases, the remittance of currency out of the PRC. Any future restrictions on currency exchanges may limit our ability to use revenue generated in Renminbi to fund any future business activities outside China or to make dividend or other payments in U.S. dollars.

Effective July 1, 1996, foreign currency “current account” transactions by foreign investment enterprises are no longer subject to the approval of State Administration of Foreign Exchange (“SAFE,” formerly, “State Administration of Exchange Control”), but need only a ministerial review, according to the Administration of the Settlement, Sale and Payment of Foreign Exchange Provisions promulgated in 1996 (the “FX regulations”). “Current account” items include international commercial transactions, which occur on a regular basis, such as those relating to trade and provision of services. Distributions to joint venture parties also are considered “current account transactions.” Non-current account items, including direct investments and loans, known as “capital account” items, remain subject to SAFE approval and companies are required to open and maintain separate foreign exchange accounts for capital account items. There are other significant restrictions on the convertibility of Renminbi, including that foreign-invested enterprises may only buy, sell or remit foreign currencies after providing valid commercial documents at those banks in China authorized to conduct foreign exchange business. Under current regulations, we can obtain foreign currency in exchange for the Renminbi from swap centers authorized by the government. While we do not anticipate problems in obtaining foreign currency to satisfy our requirements, we cannot be certain that foreign currency shortages or changes in currency exchange laws and regulations by the PRC government will not restrict us from freely converting the Renminbi in a timely manner.

Certain PRC regulations, including the M&A Rules and national security regulations, may require a complicated review and approval process, which could make it more difficult for us to pursue growth through acquisitions in China.

The M&A Rules established additional procedures and requirements that could make merger and acquisition activities in China by foreign investors more time-consuming and complex. For example, the MOFCOM must be notified in the event a foreign investor takes control of a PRC domestic enterprise. In addition, certain acquisitions of domestic companies by offshore companies that are related to or affiliated with the same entities or individuals of the domestic companies, are subject to approval by the MOFCOM. In addition, the Implementing Rules Concerning Security Review on Mergers and Acquisitions by Foreign Investors of Domestic Enterprises, issued by the MOFCOM in August 2011, require that mergers and acquisitions by foreign investors in “any industry with national security concerns” be subject to national security review by the MOFCOM. In addition, any activities attempting to circumvent such review process, including structuring the transaction through a proxy or contractual control arrangement, are strictly prohibited.

There is significant uncertainty regarding the interpretation and implementation of these regulations relating to merger and acquisition activities in China. In addition, complying with these requirements could be time-consuming, and the required notification, review or approval process may materially delay or affect our ability to complete merger and acquisition transactions in China. As a result, our ability to seek growth through acquisitions may be materially and adversely affected.

| 18 |

We may be exposed to liabilities under the Foreign Corrupt Practices Act, and any determination that we violated the Foreign Corrupt Practices Act could harm our business.

We are subject to the United States Foreign Corrupt Practices Act, or FCPA, and other laws that prohibit U.S. companies from engaging in bribery or other prohibited payments to foreign officials for the purpose of obtaining or retaining business. Our activities in China create the risk of unauthorized payments or offers of payments by one of the employees, consultants, sales agents or distributors of our Company, even though these parties are not always subject to our control. It is our policy to implement safeguards to discourage these practices by our employees. However, our existing safeguards and any future improvements may prove ineffective, and the employees, consultants, sales agents or distributors of our Company may engage in conduct for which we might be held responsible. Violations of the FCPA may result in severe criminal or civil sanctions, and we may be subject to other liabilities, which could adversely impact our business, operating results and financial condition.

Risks Related to the Shares of our Common Stock

The ownership of our common stock is concentrated among a small number of shareholders, and if our principal shareholders, director and officers choose to act together, they may be able to significantly influence management and operations, which may prevent us from taking actions that may be favorable to you.

Our ownership is concentrated among a small number of shareholders, including our founder, director, officers and entities related to these persons. Accordingly, these shareholders, acting together, will have the ability to exert substantial influence over all matters requiring approval by our shareholders, including the election and removal of directors and any proposed merger, consolidation or sale of all or substantially all of our assets. This concentration of ownership could have the effect of delaying, deferring or preventing a change in control of the Company or impeding a merger or consolidation, takeover or other business combination that could be favorable to you.

The requirements of being a public company may strain our resources and divert management’s attention.

Compliance with the Exchange Act and the Sarbanes-Oxley Act and other applicable securities rules and regulations will increase our legal and financial compliance costs, make some activities more difficult, time-consuming, or costly, and increase demand on our systems and resources. As a result, management’s attention may be diverted from other business concerns, which could harm our business and operating results. In addition, complying with public company disclosure rules makes our business more visible, which we believe may result in threatened or actual litigation, including by competitors and other third parties. If such claims are successful, our business and operating results could be harmed, and even if the claims do not result in litigation or are resolved in our favor, these claims, and the time and resources necessary to resolve them, could divert the resources of our management and harm our business and operating results.

| 19 |

Our common stock is considered a “penny stock” which is subject to restrictions on marketability, so you may not be able to sell your shares.

The SEC has adopted regulations which generally define “penny stock” to be an equity security that has a market price of less than $5.00 per share or an exercise price of less than $5.00 per share, subject to specific exemptions. The market price of our common stock is currently less than $5.00 per share and therefore is designated as a “penny stock” according to SEC rules. This designation requires any broker or dealer selling these securities to disclose some information concerning the transaction, obtain a written agreement from the purchaser and determine that the purchaser is reasonably suitable to purchase the securities. These rules may restrict the ability of brokers or dealers to sell the common stock and may affect the ability of investors to sell their shares. These regulations may likely have the effect of limiting the trading activity of the Company’s common stock and reducing the liquidity of an investment in its common stock. In addition, investors may find it difficult to obtain accurate quotations of the common stock and may experience a lack of buyers to purchase our Company’s stock or a lack of market makers to support the stock price.

We will be subject to the penny stock rules adopted by the Securities and Exchange Commission that require brokers to provide extensive disclosure to their customers prior to executing trades in penny stocks. These disclosure requirements may cause a reduction in the trading activity of our common stock, which in all likelihood would make it difficult for our shareholders to sell their shares.

Because we are not subject to compliance with rules requiring the adoption of certain corporate governance measures, our shareholders have limited protections against interested director transactions, conflicts of interest and similar matters.

The Sarbanes-Oxley Act of 2002, as well as rule changes proposed and enacted by the SEC, the New York and NYSE AMEX Equities exchanges and the Nasdaq Stock Market, as a result of Sarbanes-Oxley, require the implementation of various measures relating to corporate governance. These measures are designed to enhance the integrity of corporate management and the securities markets and apply to securities which are listed on those exchanges or the Nasdaq Stock Market. Because we are not presently required to comply with many of the corporate governance provisions and because we chose to avoid incurring the substantial additional costs associated with such compliance any sooner than necessary, we have not yet adopted these measures.

| 20 |

We do not currently have independent audit or compensation committees. As a result, our sloe director has the ability, among other things, to determine his own level of compensation. Until we comply with such corporate governance measures, regardless of whether such compliance is required, the absence of such standards of corporate governance may leave our shareholders without protections against interested director transactions, conflicts of interest and similar matters and investors may be reluctant to provide us with funds necessary to expand our operations.

There may not be an active, liquid trading market for our equity securities.

Our common stock trades exclusively on the OTCQB Marketplace since September 2016. Trading volumes on the OTCQB Marketplace can fluctuate significantly, which could make it difficult for investors to execute transactions in our securities and could cause declines or volatility in the prices of our common stock.

If the price of our common stock is volatile when we are trading, purchasers of our shares of common stock could incur substantial losses.