UNITED STATES

SECURITIES

AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K/A

Amendment No. 1

| ☒ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended September 30, 2018

| ☐ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from ___________ to ___________

Commission File No.000-1621697

NATURAL HEALTH FARM HOLDINGS INC.

(Exact name of registrant as specified in its charter)

| NEVADA | 98-1032170 | |

|

(State or Other Jurisdiction of Incorporation of Organization) |

(I.R.S. Employer Identification No.) |

No.48 & 49, Jalan Velox 2, Taman Velox, Rawang Industrial Park

48000 Rawang, Selangor, Malaysia

(Address of principal executive offices)

+60(3) 6091 6321

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||

| Common Stock, par value $0.001 per share | NHEL | OTC Markets Group |

Securities registered pursuant to Section 12 (g) of the Act: None

Indicate by check mark whether the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐ No ☒

Indicate by check mark if the registrant is not required to file report pursuant to Section 13 or Section 15(d) of the Act. Yes ☒ No ☐

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for shorter period that the registrant as required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (ss.232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ☒ No ☐

| 1 |

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer. See definition of "accelerated filer and large accelerated filer" in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer ☐ | Accelerated filer ☐ |

| Non-accelerated filer ☐ | Smaller reporting company ☒ |

| Emerging growth company ☒ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act) Yes ☐ No ☒

The number of shares of Common Stock, $0.001 par value, of the registrant outstanding at September 9, 2019 was 162,186,300

DOCUMENTS INCORPORATED BY REFERENCE

None.

| 2 |

Explanatory Note

The sole purpose of this Amendment No. 1 to the Annual Report on Form 10-K of Natural Health Farm Holdings Inc. for the year ended September 30, 2018, originally filed with the Securities and Exchange Commission on December 28, 2018 (the “Form 10-K”), is to restate its previously reported consolidated financial statements as at September 30, 2018. The restatement of the company’s consolidated financial statements followed an internal review of the company’s consolidated financial statements and accounting records that inadvertently excluded the financials reporting for NHF International Limited and its subsidiaries, Natural Tech R&D Sdn. Bhd. and NHF Management & Business Sdn. Bhd. This restatement has presented the periodic consolidated earnings of the company as a group.

The following sections in the Original Filing are revised in this Form 10-K/A, solely as a result of, and to reflect, the restatement:

Part I - Item 1 - Financial Statements

Part I - Item 2 - Management’s Discussion and Analysis of Financial Condition and Results of Operations

Part II - Item 6 – Exhibits

Subsequent to the filing of this revised Annual Report on Form 10-K/A, we expect to file the Quarterly Report on Form 10-Q for period ended December 31, 2018. This report will include restatement of the consolidated financial statements (and related disclosures) for the periods described therein, as set forth in those reports.

No other changes have been made to the Form 10-K. This Amendment No. 1 to the Form 10-K speaks as of the original filing date of the Form 10-K, does not reflect events that may have occurred subsequent to the original filing date and does not modify or update in any way disclosures made in the original Form 10-K.

| 3 |

TABLE OF CONTENTS

| PART I | ||

| Page No. | ||

| ITEM 1 | Description of Business | 5 |

| ITEM 1A | Risk Factors | 7 |

| ITEM 2 | Description of Property | 7 |

| ||

| ITEM 3 | Legal Proceedings | 7 |

| ITEM 4 | Mine Safety Disclosures | 7 |

| PART II | ||

| ITEM 5 | Market for Common Equity and Related Stockholder Matters | 8 |

| ITEM 6 | Selected Financial Data | 9 |

| ITEM 7 |

Management's Discussion and Analysis of Financial Condition and Results of Operations |

10 |

| ITEM 7A | Quantitative and Qualitative Disclosures about Market Risk | 13 |

| ITEM 8 | Financial Statements and Supplementary Data | 14 |

| ITEM 9 |

Changes in and Disagreements with Accountants on Accounting and Financial Disclosure |

15 |

| ITEM 9A. (T) | Controls and Procedures | 15 |

| PART III | ||

| ITEM 10 |

Directors, Executive Officers, Promoters and Control Persons of the Company |

16 |

| ITEM 11 | Executive Compensation | 18 |

| ITEM 12 |

Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters |

19 |

| ITEM 13 | Certain Relationships and Related Transactions | 20 |

| ITEM 14 | Principal Accountant Fees and Services | 21 |

| PART IV | ||

| ITEM 15 | Exhibits | 22 |

| 4 |

PART I

ITEM 1. DESCRIPTION OF BUSINESS

FORWARD-LOOKING STATEMENTS

This annual report contains forward-looking statements. These statements relate to future events or our future financial performance. These statements often can be identified using terms such as "may," "will," "expect," "believe," "anticipate," "estimate," "approximate" or "continue," or the negative thereof. We intend that such forward-looking statements be subject to the safe harbors for such statements. We wish to caution readers not to place undue reliance on any such forward-looking statements, which speak only as of the date made. Any forward-looking statements represent management's best judgment as to what may occur in the future. However, forward-looking statements are subject to risks, uncertainties and important factors beyond our control that could cause actual results and events to differ materially from historical results of operations and events and those presently anticipated or projected. We disclaim any obligation subsequently to revise any forward-looking statements to reflect events or circumstances after the date of such statement or to reflect the occurrence of anticipated or unanticipated events.

Background

The Company is a development stage company and has limited operating history and is expected to experience losses in the near term.

Natural Health Farm Holdings Inc., incorporated in the State of Nevada on July 10, 2014 (inception date), has developed and launched itself into the healthcare industry. The company started as a nutritional consulting service provider by offering a web based naturopathic learning management system that allows distributors, chiropractors and consumers to be educated on health-related aspects of various diseases. The company has positioned itself to be a fully integrated nutraceutical biotechnology company offering products and related services through healthcare practitioners and direct-to-consumers. The company now owns a research & development laboratory in Malaysia, franchisee management services company and an Australia manufacturing facility producing practitioner only naturopathic and homeopathic medicines.

On January 31, 2018, the company acquired the total outstanding share of NHF International Limited at USD$1. Upon the completion of the acquisition, its subsidiaries, both Natural Tech R&D Sdn Bhd and NHF Management & Business Sdn Bhd become wholly subsidiaries of the Group. As this transaction is business combination under common control, as deliberated and determined by Directors of the Company, difference between purchase considerations and net tangible assets acquired is recorded in merger reserves which amounted to $517,300. Natural Tech R&D Sdn Bhd, a BioNexus Status Company in Malaysia, specializes in research and development, cultivation, extraction and commercialization of nutraceuticals based on medicinal fungi and NHF Management & Business Sdn Bhd, providing franchisee management services and consultation, such as point-of-sales system, resources, branding and marketing.

On December 3, 2018, the Company agreed to purchase 51% of the issued and outstanding capital stock of Prema Life Pty Ltd and 60% of the issued and outstanding capital stock of GGLG Properties Pty Ltd, collectively in exchange for 304,500 shares of the Company’s common stock. On December 28, 2018, the parties mutually agreed to extend the closing date of the purchase transaction on January 1, 2019. The Company issued 304,500 shares of its common stock on December 3, 2018 in good faith for consummating the purchase. Prema Life, who has more than 30 years operations, is an Australia manufacturer and supplier of functional foods and supplements, especially practitioner only medicines in naturopathic and homeopathic industry.

Natural Health Farm Holdings Inc. – NHEL- exists to enable healthier life for everyone and believes that a complete healthcare eco-system from farm, research & development, manufacturing, distribution and professional support is necessary of consumers and shall make NHEL a global player in this industry.

Employees

Currently the Company has no employees other than its President/CEO and Secretary who devote approximately 65% and 50%, respectively, of their time to the business of the Company.

Jumpstart Our Business Startups Act

In April 2012, the Jumpstart Our Business Startups Act (“JOBS Act”) was enacted into law. The JOBS Act provides, among other things: Exemptions for emerging growth companies from certain financial disclosure and governance requirements for up to five years and provides a new form of financing to small companies; Amendments to certain provisions of the federal securities laws to simplify the sale of securities and increase the threshold number of record holders required to trigger the reporting requirements of the Securities Exchange Act of 1934; Relaxation of the general solicitation and general advertising prohibition for Rule 506 offerings; Adoption of a new exemption for public offerings of securities in amounts not exceeding $50 million; and Exemption from registration by a non-reporting company offers and sales of securities of up to $1,000,000 that comply with rules to be adopted by the SEC pursuant to Section 4(6) of the Securities Act and such sales are exempt from state law registration, documentation or offering requirements. In general, under the JOBS Act a company is an emerging growth company if its initial public offering (“IPO”) of common equity securities was affected after December 8, 2011 and the company had less than $1 billion of total annual gross revenues during its last completed fiscal year. A company will no longer qualify as an emerging growth company after the earliest of

| 5 |

| (i) | the completion of the fiscal year in which the company has total annual gross revenues of $1 billion or more, | |

| (ii) | the completion of the fiscal year of the fifth anniversary of the company’s IPO; | |

| (iii) | the company’s issuance of more than $1 billion in nonconvertible debt in the prior three-year period; or | |

| (iv) | the company becoming a “larger accelerated filer” as defined under the Securities Exchange Act of 1934. | |

The Company meets the definition of an emerging growth company will be affected by some of the changes provided in the JOBS Act and certain of the new exemptions. The JOBS Act provides additional new guidelines and exemptions for non-reporting companies and for non-public offerings. Those exemptions that impact the Company are discussed below.

Financial Disclosure. The financial disclosure in a registration statement filed by an emerging growth company pursuant to the Securities Act of 1933 will differ from registration statements filed by other companies as follows:

| (i) | audited financial statements required for only two fiscal years; | |

| (ii) | selected financial data required for only the fiscal years that were audited; | |

| (iii) | executive compensation only needs to be presented in the limited format now required for smaller reporting companies. (A smaller reporting company is one with a public float of less than $75 million as of the last day of its most recently completed second fiscal quarter) | |

However, the requirements for financial disclosure provided by Regulation S-K promulgated by the Rules and Regulations of the SEC already provide certain of these exemptions for smaller reporting companies. The Company is a smaller reporting company.

Currently a smaller reporting company is not required to file as part of its registration statement selected financial data and only needs audited financial statements for its two most current fiscal years and no tabular disclosure of contractual obligations.

The JOBS Act also exempts the Company’s independent registered public accounting firm from complying with any rules adopted by the Public Company Accounting Oversight Board (“PCAOB”) after the date of the JOBS Act’s enactment, except as otherwise required by SEC rule.

The JOBS Act also exempts an emerging growth company from any requirement adopted by the PCAOB for mandatory rotation of the Company’s accounting firm or for a supplemental auditor report about the audit.

Internal Control Attestation. The JOBS Act also provides an exemption from the requirement of the Company’s independent registered public accounting firm to file a report on the Company’s internal control over financial reporting, although management of the Company is still required to file its report on the adequacy of the Company’s internal control over financial reporting.

Section 102(a) of the JOBS Act goes on to exempt emerging growth companies from the requirements in 1934 Act § 14A(e) for companies with a class of securities registered under the 1934 Act to hold shareholder votes for executive compensation and golden parachutes.

Other Items of the JOBS Act. The JOBS Act also provides that an emerging growth company can communicate with potential investors that are qualified institutional buyers or institutions that are accredited to determine interest in a contemplated offering either prior to or after the date of filing the respective registration statement. The Act also permits research reports by a broker or dealer about an emerging growth company regardless if such report provides sufficient information for an investment decision. In addition, the JOBS Act precludes the SEC and FINRA from adopting certain restrictive rules or regulations regarding brokers, dealers and potential investors, communications with management and distribution of a research reports on the emerging growth company IPO.

Section 106 of the JOBS Act permits emerging growth companies to submit 1933 Act registration statements on a confidential basis provided that the registration statement and all amendments are publicly filed at least 21 days before the issuer conducts any road show. This is intended to allow the emerging growth company to explore the IPO option without disclosing to the market the fact that it is seeking to go public or disclosing the information contained in its registration statement until the company is ready to conduct a road show.

Election to Opt Out of Transition Period. Section 102(b)(1) of the JOBS Act exempts emerging growth companies from being required to comply with new or revised financial accounting standards until private companies (that is, those that have not had a 1933 Act registration statement declared effective or do not have a class of securities registered under the 1934 Act) are required to comply with the new or revised financial accounting standard.

| 6 |

The JOBS Act provides a company can elect to opt out of the extended transition period and comply with the requirements that apply to non-emerging growth companies but any such an election to opt out is irrevocable. The Company has elected not to opt out of the transition period.

Subsidiaries- The Company owns 100% of NHF International Limited and its subsidiaries, Natural Tech R&D Sdn Bhd and NHF Management & Business Sdn Bhd, 51% of Prema Life Pty Ltd, an Australian corporation and 60% of GGLG Properties Pty Ltd, an Australian corporation.

Employees and Employment Agreements

At present, we have no employees other than our officer and director. We presently do not have pension, health, annuity, insurance, stock options, profit sharing or similar benefit plans; however, we may adopt such plans in the future. There are presently no personal benefits available to any officers, directors or employees.

ITEM 1A. RISK FACTORS

Not applicable to smaller reporting companies.

ITEM 2. DESCRIPTION OF PROPERTY

The Company owns no real estate. We currently maintain our corporate office at No.48 & 49, Jalan Velox 2, Taman Velox, Rawang Industrial Park, 48000 Rawang, Selangor, Malaysia. We believe that this current office space is adequate for our current operations and we do not anticipate that we will require any additional office space in the foreseeable future.

ITEM 3. LEGAL PROCEEDINGS

On 25 January 2019, Craig Popplestone obtained default judgment in Magistrates Court of Queensland proceedings no. M205, M206 and M207 (Magistrates Court Proceedings) against Prema Life Pty Ltd for alleged unpaid invoices. The default judgments were irregularly obtained on the basis that the Uniform Civil Procedure Rules 1999 have not been complied with and Prema Life Pty Ltd was never served with any document filed in the proceedings. The irregular Default Judgments were set aside by the Magistrates Court on 21 June 2019. Prema Life Pty Ltd has a defence to the proceeding on the basis that the parties entered into a Deed of Release in respect of the debt and accordingly, no debt is owed by Prema Life Pty Ltd to Mr Popplestone. Mr Popplestone has until 19 July 2019 to file any claim and statement of claim in the proceeding should he elect to pursue his claim against Prema Life Pty Ltd. To date no such claim and statement of claim has been served on Prema Life Pty Ltd.

On 11 March 2019, Mr Popplestone served a statutory demand on Prema Life Pty Ltd demanding payment of Australian Dollar 49,733 (approximately $34,500),the amount owed pursuant to the default judgments awarded in the Magistrates Court Proceedings. On 1 April 2019, Prema Life Pty Ltd filed an application in the Supreme Court of Queensland proceeding no. 3472 of 2019 seeking to have the statutory demand set aside due to the statutory demand being defective and on the basis that there is a genuine dispute about the nature of the debt. The proceeding has been adjourned to a date to be agreed to by the parties post the hearing of the application to have the default judgments obtained in the Magistrates Court Proceedings set aside as once these default judgments are set aside there will be no debt able to be relied upon by Mr Popplestone for the purpose of the statutory demand.

On March 6, 2019, the company has executed a term sheet to acquire a majority interest in Biodelta (Pty) Ltd (“Biodelta”) and on May 14, 2019, announced termination of the term sheet. The company is investigating the indebtedness of Biodelta regarding the repayment of refundable deposit of $160,000 for the acquisition of the shares and other business assets in Biodelta. Biodelta failed or neglected to repay the funds on demand when the transaction did not occur. A letter of demand has been issued on May 22, 2019 and June 17, 2019 respectively against Biodelta which Biodelta disputes the obligation to repay. The decision has been made to pursue both civil and criminal proceedings against Biodelta and its director Leon Giese. The legal representative has been authorized to travel to South Africa to commence the proceedings.

ITEM 4. MINE SAFETY DISCLOSURES

None.

| 7 |

PART II

ITEM 5. MARKET FOR COMMON EQUITY AND RELATED STOCKHOLDER MATTERS

MARKET FOR COMMON EQUITY AND RELATED STOCKHOLDER MATTERS

Public Market for Common Stock

On March 17, 2018, our common stock was approved for quotation on the OTC Markets under the symbol “NHEL”. The OTC Markets is a regulated quotation service that displays real-time quotes, last-sale prices, and volume information in over-the-counter equity securities. The OTC Markets securities are traded by a community of market makers that enter quotes and trade reports. This market is limited in comparison to the national stock exchanges and any prices quoted may not be a reliable indication of the value of our common stock.

On December 27, 2018, the closing price of our common stock reported on the OTC Markets was $2.48 per share. The following table sets forth, for each of the quarterly periods indicated, the high and low sales prices of our common stock, as reported on the OTCQB.

| Year 2018 | High Bid | Low Bid | ||||||

| Quarter Ended March 31, 2018 | $ | 5.00 | $ | 0.20 | ||||

| Quarter Ended June 30, 2018 | 2.00 | 1.20 | ||||||

| Quarter Ended September 30, 2018 | 2.40 | 2.00 | ||||||

| October 1 to December 27, 2018 | 6.00 | 2.42 | ||||||

As of December 27, 2018, there were approximately 72 shareholders of record of our 161,859,500 shares common stock based upon the shareholders’ listing provided by our transfer agent.

Dividends

We have never paid cash dividends on our common stock. We intend to keep future earnings, if any, to finance the expansion of our business, and we do not anticipate that any cash dividends will be paid in the foreseeable future. Our future payment of dividends will depend on our earnings, capital requirements, expansion plans, financial condition and other relevant factors that our board of directors may deem relevant. Our retained earnings deficit currently limits our ability to pay dividends.

Shares Available for Future Sale

Approximately 81% of all outstanding shares of our common stock are “restricted securities,” as that term is defined under Rule 144 promulgated under the Securities Act, because they were issued in a private transaction not involving a public offering. Accordingly, none of the outstanding shares of our common stock may be resold, transferred, pledged as collateral or otherwise disposed of unless such transaction is registered under the Securities Act or an exemption from registration is available. In connection with any transfer of shares of our common stock other than pursuant to an effective registration statement under the Securities Act, the Company may require the holder to provide to the Company an opinion of counsel to the effect that such transfer does not require registration of such transferred shares under the Securities Act.

Rule 144 is not available for the resale of securities initially issued by companies that are, or previously were, shell companies, like us, unless the following conditions are met:

| ● | the issuer of the securities that was formerly a shell company has ceased to be a shell company; |

| ● | the issuer of the securities is subject to the reporting requirements of Section 13 or 15(d) of the Exchange Act; |

| ● | the issuer of the securities has filed all Exchange Act reports and material required to be filed, as applicable, during the preceding 12 months (or such shorter period that the issuer was required to file such reports and materials), other than Current Reports on Form 8-K; and |

| ● | at least one year has elapsed from the time that the issuer filed current comprehensive disclosure with the SEC reflecting its status as an entity that is not a shell company. |

On February 1, 2018, the Company notified the SEC by through the filing of a Form 8-K that is was no longer a “shell” corporation. In view of this, any time after February 1, 2019, and assuming the Company has been current in its required filings pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934, and all other requirements set forth above are met, shareholders may utilize Rule 144 for the sale of their shares.

| 8 |

Penny Stock Regulations

Our common stock is deemed to be “penny stock” as that term is generally defined in the Securities Exchange Act of 1934 to mean equity securities with a price of less than $5.00. Our shares thus will be subject to rules that impose sales practice and disclosure requirements on broker-dealers who engage in certain transactions involving a penny stock.

Under the penny stock regulations, a broker-dealer selling a penny stock to anyone other than an established customer or accredited investor must make a special suitability determination regarding the purchaser and must receive the purchaser’s written consent to the transaction prior to the sale, unless the broker-dealer is otherwise exempt. Generally, an individual with a net worth in excess of $1,000,000 or annual income exceeding $200,000 individually or $300,000 together with his or her spouse is considered an accredited investor. In addition, under the penny stock regulations the broker-dealer is required to:

Deliver, prior to any transaction involving a penny stock, a disclosure schedule prepared by the SEC relating to the penny stock market, unless the broker-dealer or the transaction is otherwise exempt;

Disclose commissions payable to the broker-dealer and our registered representatives and current bid and offer quotations for the securities;

Send monthly statements disclosing recent price information pertaining to the penny stock held in a customer’s account, the account’s value and information regarding the limited market in penny stocks; and

Make a special written determination that the penny stock is a suitable investment for the purchaser and receive the purchaser’s written agreement to the transaction, prior to conducting any penny stock transaction in the customer’s account.

Because of these regulations, broker-dealers may encounter difficulties in their attempt to buy or sell shares of our common stock, which may affect the ability of selling stockholders or other holders to sell their shares in the secondary market and have the effect of reducing the level of trading activity in the secondary market. These additional sales practice and disclosure requirements could impede the sale of our common stock even if our common stock becomes publicly traded. In addition, the liquidity for our common stock may be decreased, with a corresponding decrease in the price of our common stock. Our shares are likely to be subject to such penny stock rules for the foreseeable future.

Repurchases of Equity Securities

None

Reports to Stockholders

We are currently subject to the information and reporting requirements of the Securities Exchange Act of 1934 and will continue to file periodic reports, and other information with the SEC. We intend to send annual reports to our stockholders containing audited financial statements.

Transfer Agent

Transhare Corporation, 15500 Roosevelt Boulevard, Suite 301, Clearwater, FL 33760 is the registrar and transfer agent for the Company’s common stock.

Recent Sales of Unregistered Securities

None

ITEM 6. SELECTED FINANCIAL DATA

Not applicable.

| 9 |

ITEM 7. MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATION.

This Annual Report Form 10-K contains forward-looking statements. Our actual results could differ materially from those set forth as a result of general economic conditions and changes in the assumptions used in making such forward-looking statements. The following discussion and analysis of our financial condition and results of operations should be read together with the audited financial statements and accompanying notes and the other financial information appearing elsewhere in this report. The analysis set forth below is provided pursuant to applicable Securities and Exchange Commission regulations and is not intended to serve as a basis for projections of future events. Refer also to “Risk Factors” and “Cautionary Note Regarding Forward Looking Statements” in Item 1 above.

Natural Health Farm Holdings Inc., incorporated in the State of Nevada on July 10, 2014 (inception date), has developed and launched itself into the healthcare industry. The company started as a nutritional consulting service provider by offering a web based naturopathic learning management system that allows distributors, chiropractors and consumers to be educated on health-related aspects of various diseases. The company has positioned itself to be a fully integrated nutraceutical biotechnology company offering products and related services through healthcare practitioners and direct-to-consumers. The company now owns a research & development laboratory in Malaysia, franchisee management services company and an Australia manufacturing facility producing practitioner only naturopathic and homeopathic medicines.

On January 31, 2018, the company acquired the total outstanding share of NHF International Limited at USD$1. Upon the completion of the acquisition, its subsidiaries, both Natural Tech R&D Sdn Bhd and NHF Management & Business Sdn Bhd become wholly subsidiaries of the Group. As this transaction is business combination under common control, as deliberated and determined by Directors of the Company, difference between purchase considerations and net tangible assets acquired is recorded in merger reserves which amounted to $517,300. Natural Tech R&D Sdn Bhd, a BioNexus Status Company in Malaysia, specializes in research and development, cultivation, extraction and commercialization of nutraceuticals based on medicinal fungi and NHF Management & Business Sdn Bhd, providing franchisee management services and consultation, such as point-of-sales system, resources, branding and marketing.

On December 3, 2018, the Company agreed to purchase 51% of the issued and outstanding capital stock of Prema Life Pty Ltd and 60% of the issued and outstanding capital stock of GGLG Properties Pty Ltd, collectively in exchange for 304,500 shares of the Company’s common stock. On December 28, 2018, the parties mutually agreed to extend the closing date of the purchase transaction on January 1, 2019. The Company issued 304,500 shares of its common stock on December 3, 2018 in good faith for consummating the purchase.

Prema Life Pty Ltd is a manufacturer and supplier of functional foods, vitamins and supplements, of practitioner only naturopathic and homeopathic medicines in Australia. The Company hosts regular educational webinars and seminars for practitioners to learn about the natural products. The Company operates from a Hazard Analysis and Critical Control Point (“HACCP”) certified manufacturing facility and has the capacity to produce a wide range of powder and liquid products to requirements.

GGLG Properties Pty Ltd. owns industrial property and factory at Brendale in Brisbane, Queensland, Australia. The Company leases this property to Prema Life Pty Ltd, and incurs costs in connection with owning and maintaining that property and recovers these costs through rental charges and rental recoveries pursuant to a long-term lease.

From inception, through the date of this annual report, we reported revenues and incurred expenses and accumulated operating losses, as part of our development activities. We recorded a net loss of $948,614 for the year ended September 30, 2018, working capital deficiency of $213,742, and an accumulated deficit of $1,067,080 at September 30, 2018.

We anticipate that we will need substantial working capital over the next 12 months to continue as a going concern and to expand our operations to distribute, sell and market naturopathic learning management system together with online learning courses. Our independent auditors have expressed substantial doubt as to the ability of the Company to continue as a going concern. Unless we are able to generate sufficient cash flows from operations and/or obtain additional financing, there is a substantial doubt as to the ability of the Company to continue as a going concern. We intend to make an equity offering of our common stock for the acquisition and operation expenses. If we cannot raise the required cash, we will issue additional shares of our common stock in lieu of cash.

Restatement of Financial Results

The company is restating its previously reported consolidated financial statements as at September 30, 2018. The restatement of the company’s consolidated financial statements followed an internal review of the company’s consolidated financial statements and accounting records that inadvertently excluded the financials reporting for NHF International Limited and its subsidiaries, Natural Tech R&D Sdn Bhd and NHF Management & Business Sdn Bhd. This restatement has presented the periodic consolidated earnings of the company as a group.

| 10 |

Results of Operations for the Years Ended September 30, 2018 and 2017

Our results of operations for the year ended September 30, 2018 and 2017 included the operations of the Company, NHF International and its subsidiaries as a common control situation.

Revenues and Cost of Goods Sold

Revenues for the year ended September 30, 2018 were $769,969 ($652,367 from related parties and $117,602 from third parties) compared to $0 for the same comparable period in 2017. Revenues recorded were from licensing fees and other software related revenues relating to web-based naturopathic learning management system and training provided to four customers by NHEL, as well as selling supplements, providing laboratory testing services and providing franchisee and marketing consultation by the subsidiary companies. Cost of goods sold recorded for the year ended September 30, 2018 was $362,847. No revenues and cost of goods sold were realized for the year ended September 30, 2017.

Operating Expenses

Operating expenses for the year ended September 30, 2018 and 2017 were $1,354,462 and $89,359, respectively. Operating expenses for the year ended September 30, 2018 consisted of us engaging outside consultants and business advisors for professional fees totaling $159,862, legal and filing fees of $51,719 upon becoming a public reporting entity, stock compensation expense of $826,295 for grant of stock options to employees, directors and consultants, and general and administrative expenses of $316,586. Operating expenses for the year ended September 30, 2017 consisted of professional fees of $33,986, legal and filing fees of $9,093, and general and administrative expenses of $46,280.

Other Income (Expense)

Interest expense for the year ended September 30, 2018 and 2017 was $1,026 and $0. On June 5, 2018, we executed a promissory note of $40,000 at 8% annual interest, due and payable in full on March 5, 2019. We recorded interest expense of $1,026 for the year ended September 30, 2018.

Net loss

We reported a net loss of $948,614 and $89,359 and for the year ended September 30, 2018 and 2017, respectively.

Liquidity and Capital Resources

Cash and cash equivalents were $439,846 at September 30, 2018 as compared to $0 at September 30, 2017. As reported in the accompanying financial statements, we recorded a net loss of $948,614 for the year ended September 30, 2018. Our working capital deficit and accumulated deficit at September 30, 2018 was $213,742 and $1,067,080, respectively. These factors and our ability to raise additional capital to accomplish our objectives, raises doubt about our ability to continue as a going concern. We expect our expenses will continue to increase during the foreseeable future as a result of increased operational expenses and the development of our current business operations. We anticipate generating only minimal revenues over the next twelve months. Consequently, we are dependent on the proceeds from future debt or equity investments to sustain our operations and implement our business plan. If we are unable to raise sufficient capital, we will be required to delay or forego some portion of our business plan, which would have a material adverse effect on our anticipated results from operations and financial condition. There is no assurance that we will be able to obtain necessary amounts of capital or that our estimates of our capital requirements will prove to be accurate.

We presently do not have any significant credit available, bank financing or other external sources of liquidity. Due to our accumulated operating losses, our operations have not been a source of liquidity. We will need to acquire other profitable entities or obtain additional capital in order to expand operations and become profitable. In order to obtain capital, we may need to sell additional shares of our common stock or borrow funds from private lenders. There can be no assurance that we will be successful in obtaining additional funding.

To the extent that we raise additional capital through the sale of equity or convertible debt securities, the issuance of such securities may result in dilution to existing stockholders. If additional funds are raised through the issuance of debt securities, these securities may have rights, preferences and privileges senior to holders of common stock and the terms of such debt could impose restrictions on our operations. Regardless of whether our cash assets prove to be inadequate to meet our operational needs, we may seek to compensate providers of services by issuance of stock in lieu of cash, which may also result in dilution to existing shareholders. Even if we are able to raise the funds required, it is possible that we could incur unexpected costs and expenses, fail to collect significant amounts owed to us, or experience unexpected cash requirements that would force us to seek alternative financing.

| 11 |

No assurance can be given that sources of financing will be available to us and/or that demand for our equity/debt instruments will be sufficient to meet our capital needs, or that financing will be available on terms favorable to us. If funding is insufficient at any time in the future, we may not be able to take advantage of business opportunities or respond to competitive pressures or may be required to reduce the scope of our planned service development and marketing efforts, any of which could have a negative impact on our business and operating results.

Operating Activities

Net cash flows provided by operating activities for the year ended September 30, 2018 was $730,178 which resulted primarily from our net loss of $946,948, a depreciation of 35,973 and a net change in operating liabilities of 187,684. Net cash flows used in operating activities for the year ended September 30, 2017 was $88,663 resulted due to the net loss of $89,359 and a net change in operating assets of $696.

Investing Activities:

Net cash flows from investing activities for the year ended September 30, 2018 was $137,805 primarily due to cash inflows from merger amounting to $289,208 and net off the purchase of plant and equipment of $57,823 and acquisition of other investments of $93,580. We did not record any cash flows in investing activities for the year ended September 30, 2017.

Financing Activities

Net cash flows provided by financing activities for the year ended September 30, 2018 was $1,032,219, consisting of $11,210 in cash advance from director, drawdowns of borrowings of $40,000 and proceeds from issuance of share of $981,009. Net cash flows provided by financing activities for the year ended September 30, 2017 was $88,663 primarily due to cash received from an affiliate of $80,137 and cash advance from director of $8,526.

As a result of the above activities, we experienced a net increase in cash of $439,846 and $0 for the year ended September 30, 2018 and 2017, respectively. We expect that working capital will continue to be funded through a combination of our existing sales and further issuance of securities or obtaining financing. Our ability to continue as a going concern is still dependent on our success in obtaining additional financing from investors or from sale of our common shares.

Critical Accounting Policies and Significant Judgments and Estimates

Our management’s discussion and analysis of our financial condition and results of operations is based on our financial statements which we have prepared in accordance with U.S. generally accepted accounting principles. In preparing our financial statements, we are required to make estimates and assumptions that affect the reported amounts of assets and liabilities, the disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenues and expenses during the reporting periods. We have identified the following accounting policies that we believe require application of management’s most subjective judgments, often requiring the need to make estimates about the effect of matters that are inherently uncertain and may change in subsequent periods. Our actual results could differ from these estimates and such differences could be material.

While our significant accounting policies are described in more details in Note 2 of our annual financial statements included herein, we believe the following accounting policies to be critical to the judgments and estimates used in the preparation of our financial statements.

JOBS Act Accounting Election

We are an “emerging growth company,” as defined in the JOBS Act. Under the JOBS Act, emerging growth companies can delay adopting new or revised accounting standards issued subsequent to the enactment of the JOBS Act until such time as those standards apply to private companies. We have irrevocably elected not to avail ourselves of this exemption from new or revised accounting standards, and, therefore, will be subject to the same new or revised accounting standards as other public companies that are not emerging growth companies.

Fair value of Financial Instruments and Fair Value Measurements

ASC 820, “Fair Value Measurements and Disclosures”, requires an entity to maximize the use of observable inputs and minimize the use of unobservable inputs when measuring fair value. ASC 820 establishes a fair value hierarchy based on the level of independent, objective evidence surrounding the inputs used to measure fair value. A financial instrument’s categorization within the fair value hierarchy is based upon the lowest level of input that is significant to the fair value measurement.

| 12 |

Off-Balance Sheet Arrangements

We have not engaged in any off-balance sheet arrangements as defined in Item 303(c) of the SEC’s Regulation S-B. We did not have any relationships with unconsolidated organizations or financial partnerships, such as structured finance or special-purpose entities that would have been established for the purpose of facilitating off-balance sheet arrangements or other contractually narrow or limited purposes.

Recent Accounting Pronouncements

We have implemented all new accounting pronouncements that are in effect and that may impact our financial statements and do not believe that there are any other new accounting pronouncements that have been issued that might have a material impact on our financial position or results of operations.

Material Commitments

As of the date of this Annual Report, we do not have any material commitments.

Purchase of Significant Equipment

As of the date of this Annual Report, we do not intend to purchase any significant equipment during the next twelve months.

OFF-BALANCE SHEET ARRANGEMENTS

As of the date of this Annual Report, we do not have any off-balance sheet arrangements that have or are reasonably likely to have a current or future effect on our financial condition, changes in financial condition, revenues or expenses, results of operations, liquidity, capital expenditures or capital resources that are material to investors.

GOING CONCERN

The independent auditors' reports accompanying our September 30, 2018 and September 30, 2017 financial statements contains an explanatory paragraph expressing substantial doubt about our ability to continue as a going concern. The financial statements have been prepared "assuming that we will continue as a going concern," which contemplates that we will realize our assets and satisfy our liabilities and commitments in the ordinary course of business.

ITEM 7A. QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK

Not applicable to smaller reporting companies.

| 13 |

ITEM 8. FINANCIAL STATEMENTS AND SUPPLEMENTARY DATA

| Page | |

| Report of Current Independent Registered Public Accounting Firm | F-1 |

| Balance Sheets | F-2 |

| Statements of Operations | F-3 |

| Statements of Changes in Stockholders’ Deficits | F-4 |

| Statements of Cash Flows | F-5 |

| Notes to Financial Statements | F-6 |

| 14 |

|

TOTAL ASIA ASSOCIATES PLT (LLP0016837-LCA & AF002128) A Firm registered with US PCAOB and Malaysian MIA

C-3-1, Megan Avenue 1, 189 Off Jalan Tun Razak, 50400 Kuala Lumpur. Tel: (603) 2733 9989 |

To the Shareholders and Board of Directors of NATURAL HEALTH FARM HOLDINGS INC.

No.48 & 49, Jalan Velox 2, Taman Velox,

Rawang Industrial Park

48000 Rawang, Selangor, Malaysia

Opinion on the Financial Statements

We have audited the accompanying balance sheets of Natural Health Farm Holdings Inc. (the ‘Company’) as of September 30, 2018 and the related statements of income, stockholders’ equity, and cash flows for the year ended of September 30, 2018 and the related notes (collectively referred to as the “financial statements”). In our opinion, the financial statements present fairly, in all material respects, the financial position of the Company as of September 30, 2018 and the results of its operations and its cash flows for the year ended September 30, 2018, in conformity with accounting principles generally accepted in the United States of America.

Basis for Opinion

These financial statements are the responsibility of the Company’s management. Our responsibility is to express an opinion on the Company’s financial statements based on our audits. We are a public accounting firm registered with the Public Company Accounting Oversight Board (United States) (“PCAOB”) and are required to be independent with respect to the Company in accordance with the U.S. federal securities laws and the applicable rules and regulations of the Securities and Exchange Commission and the PCAOB.

We conducted our audits in accordance with the standards of the PCAOB. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement, whether due to error or fraud. The Company is not required to have, nor were we engaged to perform, an audit of its internal control over financial reporting. As part of our audits we are required to obtain an understanding of internal control over financial reporting but not for the purpose of expressing an opinion on the effectiveness of the Company’s internal control over financial reporting. Accordingly, we express no such opinion.

Our audits included performing procedures to assess the risks of material misstatement of the financial statements, whether due to error or fraud, and performing procedures that respond to those risks. Such procedures included examining, on a test basis, evidence regarding the amounts and disclosures in the financial statements. Our audits also included evaluating the accounting principles used and significant estimates made by management, as well as evaluating the overall presentation of the financial statements. We believe that our audits provide a reasonable basis for our opinion.

The accompanying financial statements have been prepared assuming that the Company will continue as a going concern. As discussed in Note 1 to the financial statements, for the year ended September 30, 2018 the Company incurred a net loss and working capital deficit. These conditions raise substantial doubt about the Company’s ability to continue as a going concern. Management’s plans in regard to these matters are also described in Note 1. The financial statements do not include any adjustments that might result from the outcome of this uncertainty.

| /s/ Total Asia Associates PLT | |

| TOTAL ASIA ASSOCIATES PLT | |

| Kuala Lumpur, Malaysia | |

September 20, 2019 |

| F-1 |

NATURAL HEALTH FARM HOLDINGS INC.

BALANCE SHEETS

| September 30, 2018 | September 30, 2017 | |||||||

| ASSETS | ||||||||

| Current Assets | ||||||||

| Cash and cash equivalents | $ | 439,846 | $ | - | ||||

| Account receivables – Third parties | 162,275 | - | ||||||

| Account receivables – Related parties | 169,292 | - | ||||||

| Other receivables and deposits | 2,061 | - | ||||||

| Tax assets | 5,221 | - | ||||||

| Total Current Assets | 778,695 | - | ||||||

| Non-Current Assets | ||||||||

| Plant and equipment, net | 159,479 | - | ||||||

| Other investments | 93,580 | - | ||||||

| Total Non-Current Assets | 253,059 | - | ||||||

| Total Assets | $ | 1,031,754 | $ | - | ||||

| LIABILITIES AND STOCKHOLDERS' DEFICIT | ||||||||

| Current Liabilities | ||||||||

| Account payables | $ | 71,678 | $ | - | ||||

| Accrued expenses | 36,720 | - | ||||||

| Other payables – related parties | 299,309 | 80,137 | ||||||

| Deferred revenue - related parties | 57,341 | - | ||||||

| Deferred revenue - third parties | 48,694 | - | ||||||

| Note payable | 40,000 | - | ||||||

| Advance from director | 11,210 | - | ||||||

| Total Current Liabilities | 564,952 | 80,137 | ||||||

| Non-Current Liabilities | ||||||||

| Deferred tax liabilities | 8,159 | - | ||||||

| Total Liabilities | 573,111 | 80,137 | ||||||

| Commitments and Contingencies (Note 9) | ||||||||

| Stockholders' Deficit | ||||||||

| Common Stock, $0.001 par value, 500,000,000 shares authorized, 161,555,000 shares and 150,150,000 shares issued and outstanding at September 30, 2018 and 2017, respectively | 161,555 | 150,150 | ||||||

| Additional paid in capital | 1,387,112 | (111,821 | ) | |||||

| Accumulated deficit | (1,067,080 | ) | (118,466 | ) | ||||

| Foreign currency translation reserve | (22,944 | ) | - | |||||

| Total Stockholders' Equity | 458,643 | (80,137 | ) | |||||

| Total Liabilities and Stockholders' Deficit | $ | 1,031,754 | $ | - | ||||

The accompanying notes are an integral part of these financial statements.

| F-2 |

NATURAL HEALTH FARM HOLDINGS INC.

STATEMENTS OF OPERATIONS

| For the Year Ended September 30, | ||||||||

| 2018 | 2017 | |||||||

| Revenues - related parties | $ | 652,367 | $ | - | ||||

| Revenues - non-related parties | 117,602 | - | ||||||

| Total Revenues | 769,969 | - | ||||||

| Cost of goods sold | (362,847 | ) | - | |||||

| Gross Profit | 407,122 | - | ||||||

| Operating Expenses: | ||||||||

| Consulting fees | (159,862 | ) | (33,986 | ) | ||||

| Legal and filing fees | (51,719 | ) | (9,093 | ) | ||||

| Stock compensation | (826,295 | ) | - | |||||

| Other general and administrative | (316,586 | ) | (46,280 | ) | ||||

| Total Operating Expenses | (1,354,462 | ) | (89,359 | ) | ||||

| Loss from Operations | (947,340 | ) | (89,359 | ) | ||||

| Other Income (Expense) | ||||||||

| Other operating income | 1,418 | - | ||||||

| Interest expense | (1,026 | ) | - | |||||

| Total Other Income (expense) | 392 | - | ||||||

| Loss Before Provision for Income Tax | (946,948 | ) | (89,359 | ) | ||||

| Provision for Income Tax | (1,666 | ) | - | |||||

| Net Loss | $ | (948,614 | ) | $ | (89,359 | ) | ||

| Other comprehensive expenses | ||||||||

| Foreign currency translation differences | (22,944 | ) | - | |||||

| Total comprehensive expense for the year | (971,558 | ) | (89,359 | ) | ||||

| Basic and Dilutive Net Loss Per Share | $ | (0.01 | ) | $ | (0.00 | ) | ||

| Weighted Average Number of Shares Outstanding - Basic and Diluted | 154,691,466 | 150,150,000 | ||||||

The accompanying notes are an integral part of these financial statements.

| F-3 |

NATURAL HEALTH FARM HOLDINGS INC.

Statements of Changes in Stockholders' Deficit

| Common Stock | Additional | Accumulated | Foreign Currency | |||||||||||||||||||||

| Number ** | Amount | Paid-in Capital | Deficit | Translation Reserve | Total | |||||||||||||||||||

| Balance, September 30, 2016 | 150,150,000 | $ | 150,150 | $ | (126,050 | ) | $ | (29,107 | ) | - | $ | (5,007 | ) | |||||||||||

| Forgiveness of advance by former directors | - | - | 14,229 | - | - | 14,229 | ||||||||||||||||||

| Net loss | - | - | - | (89,359 | ) | - | (89,359 | ) | ||||||||||||||||

| Balance, September 30, 2017 | 150,150,000 | 150,150 | (111,821 | ) | (118,466 | ) | - | (80,137 | ) | |||||||||||||||

| Stock subscriptions received | - | - | 39,404 | - | - | 39,404 | ||||||||||||||||||

| Shares issued to consultants for services | 1,050,000 | 1,050 | 103,950 | - | - | 105,000 | ||||||||||||||||||

| Stock options granted to employees, directors and consultants | - | - | 526,295 | - | - | 526,295 | ||||||||||||||||||

| Stock compensation expense | 150,000 | 150 | 299,850 | - | - | 300,000 | ||||||||||||||||||

| Shares sold for cash | 10,205,000 | 10,205 | 105 | - | - | 10,310 | ||||||||||||||||||

| Reserves arising from merger of subsidiaries | 529,329 | - | - | |||||||||||||||||||||

| Net loss | - | - | - | (948,614 | ) | (22,944 | ) | (971,558 | ) | |||||||||||||||

| Balance, September 30, 2018 | 161,555,000 | $ | 161,555 | $ | 1,387,112 | $ | (1,067,080 | ) | (22,944 | ) | $ | 458,643 | ||||||||||||

** Adjusted for 30:1 forward stock split on November 4, 2016.

The accompanying notes are an integral part of these financial statements.

| F-4 |

NATURAL HEALTH FARM HOLDINGS INC.

STATEMENTS OF CASH FLOWS

| For the Year Ended September 30, | ||||||||

| 2018 | 2017 | |||||||

| Cash Flows from Operating Activities: | ||||||||

Loss Before Provision for Income Tax | $ | (946,948 | ) | $ | (89,359 | ) | ||

| Adjustment to reconcile net loss to net cash provided by (used in) operating activities | ||||||||

| Depreciation and Amortization of Plant and Equipment | 35,973 | - | ||||||

| Changes in operating assets and liabilities | ||||||||

| Account receivables | (207,900 | ) | 696 | |||||

| Account payables | 395,584 | - | ||||||

| Tax paid | (6,887 | ) | ||||||

| Net Cash Flows Provided by (Used in) Operating Activities | (730,178 | ) | (88,663 | ) | ||||

| Cash Flows from Investing Activities | ||||||||

| Purchase of plant and equipment | (57,823 | ) | - | |||||

| Cash inflows from merger | 289,208 | |||||||

| Acquisition of other investments | (93,580 | ) | - | |||||

| Net Cash Flows From Investing Activities | 137,805 | - | ||||||

| Cash Flows from Financing Activities | ||||||||

| Cash proceeds from affiliate | - | 80,137 | ||||||

| Cash advance from director | 11,210 | 8,526 | ||||||

| Drawdowns of borrowings | 40,000 | - | ||||||

| Cash proceeds from issuance of shares | 981,009 | - | ||||||

| Net Cash Flows Provided by Financing Activities | 1,032,219 | 88,663 | ||||||

| Net Increase in Cash and Cash Equivalents | 439,846 | - | ||||||

| Cash and Cash Equivalents, Beginning of the Year | - | - | ||||||

| Cash and Cash Equivalents, End of the Year | $ | 439,846 | $ | - | ||||

| Supplemental Disclosures of Cash Flow Information: | ||||||||

| Cash paid for Income Taxes | $ | (6,887 | ) | $ | - | |||

| Cash paid for Interest | $ | (1,026 | ) | $ | - | |||

| Supplemental disclosures of non-cash investing and financing activities: | ||||||||

| Forgiveness of debt by a former director | $ | - | $ | 14,229 | ||||

The accompanying notes are an integral part of these financial statements.

| F-5 |

NATURAL HEALTH FARM HOLDINGS INC.

NOTES TO FINANCIAL STATEMENTS

SEPTEMBER 30, 2018

NOTE 1 – NATURE OF OPERATIONS, LIQUIDITY AND GOING CONCERN

Natural Health Farm Holdings Inc. (the “Company”, “We”, “Its”, and “NHEL”) was incorporated under the laws of the State of Nevada on July 10, 2014 (Inception date). The Company has developed web-based business and launched itself into the healthcare industry. The Company has plans to provide through its subsidiaries, retail nutritional supplements, organic foods, personal care, and other health care products. The company has positioned itself to be a fully integrated nutraceutical biotechnology company offering products and related services through healthcare practitioners and direct-to-consumers. The company now owns a research & development laboratory in Malaysia, franchisee management services company and an Australia manufacturing facility producing practitioner only naturopathic and homeopathic medicines.

On November 30, 2016, the Company filed a certificate of amendment to its articles of incorporation with the Nevada Secretary of State to change its name from Amber Group Inc. to Natural Health Farm Holdings Inc. and effectuated a 30:1 forward stock split of its common stock and increased its authorized share capital to 500,000,000 (Five Hundred Million). This amendment was unanimously approved by the Company’s board of directors on November 29, 2016, and with the stockholders holding a majority of the Company’s voting power.

On March 16, 2017, Financial Industry Regulatory Authority (FINRA) approved the corporate name change to Natural Health Farm Holdings Inc., approved the increase in the Company’s authorized shares of common stock to 500,000,000 shares, and approved 30:1 forward stock split effective March 17, 2017. The new trading symbol for our common stock is “NHEL”.

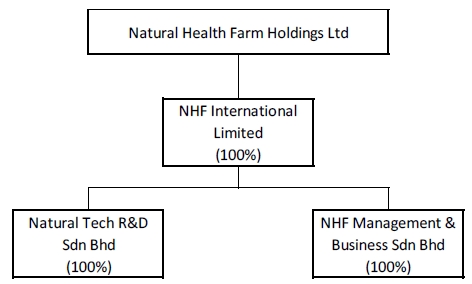

On January 31, 2018, the company acquired the total outstanding share of NHF International Limited at USD$1. Upon the completion of the acquisition, its subsidiaries, both Natural Tech R&D Sdn Bhd and NHF Management & Business Sdn Bhd become wholly subsidiaries of the Group. As this transaction is business combination under common control, as deliberated and determined by Directors of the Company, difference between purchase considerations and net tangible assets acquired is recorded in merger reserves which amounted to $517,300. Natural Tech R&D Sdn Bhd, a BioNexus Status Company in Malaysia, specializes in research and development, cultivation, extraction and commercialization of nutraceuticals based on medicinal fungi and NHF Management & Business Sdn Bhd, providing franchisee management services and consultation, such as point-of-sales system, resources, branding and marketing.

The corporate structure is depicted below:

| F-6 |

Basis of Presentation

These accompanying financial statements have been prepared in accordance with generally accepted accounting principles in the United States of America (“US GAAP”).

Basis of Consolidation

The condensed consolidated financial statements include the accounts of Natural Health Farm Holdings Inc. and all controlled subsidiaries. All intercompany transactions and balances have been eliminated.

The condensed consolidated financial statements as of September 30, 2018 and for the year ended September 30, 2018, in the opinion of management, all adjustments (consisting of normal recurring adjustments and reclassifications) necessary to present fairly the Company's condensed consolidated financial position, results of operations, statements of comprehensive income, and statements of stockholders' equity and cash flows for all periods presented.

Going Concern

The Company’s financial statements are prepared using generally accepted accounting principles in the United States of America applicable to a going concern, which contemplates the realization of assets and the satisfaction of liabilities in the normal course of business. The Company has generated small revenues and has sustained cumulative operating losses since July 10, 2014 (Inception Date) to date and allow it to continue as a going concern. The continuation of the Company as a going concern is dependent upon the continued financial support from its shareholders and affiliates, the ability of the Company to obtain necessary financing to continue operations, and the attainment of profitable operations. The Company recorded a total comprehensive loss of $971,558 for the year ended September 30, 2018 and has an accumulated deficit of $1,067,080 as of September 30, 2018.

These factors, among others, raise a substantial doubt regarding the Company’s ability to continue as a going concern. If the Company is unable to obtain adequate capital, it could be forced to cease operations. The accompanying financial statements do not include any adjustments to reflect the recoverability and classification of recorded asset amounts and classification of liabilities that might be necessary should the Company be unable to continue as a going concern.

NOTE 2 - SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

The following summary of significant accounting policies of the Company is presented to assist in the understanding of the Company’s financial statements. The financial statements and notes are the representation of the Company’s management who is responsible for their integrity and objectivity. These accounting policies conform to accounting principles generally accepted in the United States of America (“GAAP”) in all material respects and have been consistently applied in preparing the accompanying financial statements.

Use of Estimates

The preparation of financial statements in conformity with GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenues and expenses during the reporting period. The Company regularly evaluates estimates and assumptions related to the valuation of accounts payable, accrued liabilities and payable to related parties. The Company bases its estimates and assumptions on current facts, historical experience and various other factors that it believes to be reasonable under the circumstances, the results of which form the basis for making judgments about the carrying values of assets and liabilities and the accrual of costs and expenses that are not readily apparent from other sources. The actual results experienced by the Company may differ materially and adversely from the Company’s estimates. To the extent there are material differences between the estimates and the actual results, future results of operations will be affected.

Cash and Cash Equivalents

The Company considers all highly liquid instruments with maturity of three months or less at the time of issuance to be cash equivalents. The Company had a cash balance of $439,846 and $0 at September 30, 2018 and 2017, respectively.

Accounts Receivable

Accounts receivable represent income earned from the sale of products for which the Company has not yet received payment. Accounts receivable are recorded at the invoiced amount and adjusted for amounts management expects to collect from balances outstanding at period-end. The Company estimates the allowance for doubtful accounts based on an analysis of specific accounts and an assessment of the customer’s ability to pay, among other factors. At September 30, 2018 and 2017, no allowance for doubtful accounts was recorded.

| F-7 |

Equipment Costs

Equipment costs include direct costs incurred for purchase of fixed assets and payments made to independent suppliers. The Company accounts for equipment costs in accordance with the FASB guidance for the costs of equipment to be sold, leased, or otherwise marketed (“ASC Subtopic 985-20”). As for the equipment costs, they are capitalized once the technological feasibility of a product is established and such costs are determined to be recoverable. Technological feasibility of a product encompasses technical design documentation and integration documentation, or the completed and tested product design and working model. Computer software costs are capitalized once technological feasibility of a product is established and such costs are determined to be recoverable against future revenues. Technological feasibility is evaluated on a project-by-project basis. Amounts related to computer software development that are not capitalized are charged immediately to the appropriate expense account. Amounts that are considered ‘research and development’ that are not capitalized are immediately charged to engineering, research, and development expense. Capitalized costs for those products that are cancelled or abandoned are charged to product development expense in the period of cancellation.

Commencing upon product release, capitalized computer software costs are amortized on the straight-line method over a thirty-six months period. The Company evaluates the future recoverability of capitalized computer software costs on an annual basis.

Revenue Recognition and Concentrations

We generate revenue from licensing and other software services from our web-based software to distributors and retailers of nutritional supplements in the healthcare industry. We recognize licensing fees and other software services as revenue over the period of the contract at the time that the computer software is delivered and accepted by the customer, the selling price is fixed, and collection is reasonably assured, provided no significant obligations remain. We consider authoritative guidance on multiple deliverables in determining whether each deliverable represents a separate unit of accounting.

Deferred revenues represent billings or cash received in excess of revenue recognizable on service agreements that are not accounted for as revenues.

Through our subsidiary, Natural Tech R&D Sdn. Bhd., we generate revenue from the sales of health supplement and other health food products, as well as in providing laboratory analytical testing services. As for NHF Management & Business Sdn Bhd, we generate revenue in providing franchisee management and consultation services to client.

Concentration of Risk

Financial instruments that potentially subject the Company to concentrations of credit risk consist principally of cash. The Company places its cash with high quality banking institutions. The Company does not have the cash balances in excess of Federal Deposit Insurance Corporation limit at September 30, 2018 and 2017, respectively.

Income Taxes

The Company accounts for income taxes using the asset and liability method in accordance with ASC 740, “Income Taxes”. The asset and liability method provide that deferred tax assets and liabilities are recognized for the expected future tax consequences of temporary differences between the financial reporting and tax basis of assets and liabilities, and for operating loss and tax credit carry forwards. Deferred tax assets and liabilities are measured using the currently enacted tax rates and laws. The Company records a valuation allowance to reduce deferred tax assets to the amount that is believed more likely than not to be realized.

The Company follows the provisions of ASC 740-10, “Accounting for Uncertain Income Tax Positions.” When tax returns are filed, it is highly certain that some positions taken would be sustained upon examination by the taxing authorities, while others are subject to uncertainty about the merits of the position taken or the amount of the position that would be ultimately sustained. In accordance with the guidance of ASC 740-10, the benefit of a tax position is recognized in the financial statements in the period during which, based on all available evidence, management believes it is more likely than not that the position will be sustained upon examination, including the resolution of appeals or litigation processes, if any. Tax positions taken are not offset or aggregated with other positions. Tax positions that meet the more-likely-than-not recognition threshold are measured as the largest amount of tax benefit that is more than 50 percent likely of being realized upon settlement with the applicable taxing authority. The portion of the benefits associated with tax positions taken that exceeds the amount measured as described above should be reflected as a liability for unrecognized tax benefits in the accompanying balance sheets along with any associated interest and penalties that would be payable to the taxing authorities upon examination.

| F-8 |

Earnings (Loss) Per Common Share

The Company computes net earnings (loss) per share in accordance with ASC 260, “Earnings per Share”. ASC 260 requires presentation of both basic and diluted net earnings per share (“EPS”) on the face of the income statement. Basic EPS is computed by dividing earnings (loss) available to common shareholders (numerator) by the weighted average number of shares outstanding (denominator) during the period. Diluted EPS gives effect to all dilutive potential common shares outstanding during the period using the treasury stock method and convertible note and preferred stock using the if-converted method. In computing diluted EPS, the average stock price for the period is used in determining the number of shares assumed to be purchased from the exercise of stock options or warrants. Diluted EPS excludes all dilutive potential shares if their effect is anti-dilutive. At September 30, 2018 and 2017, respectively, there were options granted to certain employees and independent consultants that when vested convert into 300,000 shares of common stock. At September 30, 2018 and 2017, there were no convertible notes, warrants available for conversion that if exercised, may dilute future earnings per share.

Fair value of Financial Instruments and Fair Value Measurements

ASC 820, “Fair Value Measurements and Disclosures”, requires an entity to maximize the use of observable inputs and minimize the use of unobservable inputs when measuring fair value. ASC 820 establishes a fair value hierarchy based on the level of independent, objective evidence surrounding the inputs used to measure fair value. A financial instrument’s categorization within the fair value hierarchy is based upon the lowest level of input that is significant to the fair value measurement. ASC 820 prioritizes the inputs into three levels that may be used to measure fair value:

Level 1

Level 1 applies to assets or liabilities for which there are quoted prices in active markets for identical assets or liabilities.

Level 2

Level 2 applies to assets or liabilities for which there are inputs other than quoted prices that are observable for the asset or liability such as quoted prices for similar assets or liabilities in active markets; quoted prices for identical assets or liabilities in markets with insufficient volume or infrequent transactions (less active markets); or model-derived valuations in which significant inputs are observable or can be derived principally from, or corroborated by, observable market data. If the asset or liability has a specified (contractual) term, the Level 2 input must be observable for substantially the full term of the asset or liability.

Level 3

Level 3 applies to assets or liabilities for which there are unobservable inputs to the valuation methodology that are significant to the measurement of the fair value of the assets or liabilities.

The Company’s financial instruments consist principally of cash, accounts receivable, accounts payable, accrued expenses and payable to an affiliate. Pursuant to ASC 820, “Fair Value Measurements and Disclosures” and ASC 825, “Financial Instruments”, the fair value of our cash equivalents is determined based on “Level 1” inputs, which consist of quoted prices in active markets for identical assets. The Company believes that the recorded values of all the other financial instruments approximate their current fair values because of their nature and respective maturity dates or durations.

The following table presents assets and liabilities that were measured and recognized at fair value as of September 30, 2018 on a recurring basis:

| Description | Level 1 | Level 2 | Level 3 | |||||||||

| None | $ | - | $ | - | $ | - | ||||||

The following table presents assets and liabilities that were measured and recognized at fair value as of September 30, 2017 on a recurring basis:

| Description | Level 1 | Level 2 | Level 3 | |||||||||

| None | $ | - | $ | - | $ | - | ||||||

| F-9 |

Recent Accounting Pronouncements

In August 2016, the FASB issued ASU 2016-15, “Statement of Cash Flows (Topic 230): Classification of Certain Cash Receipts and Cash Payments” (“ASU 2016-15”). ASU 2016-15 will make eight targeted changes to how cash receipts and cash payments are presented and classified in the statement of cash flows. ASU 2016-15 is effective for fiscal years beginning after December 15, 2018, and interim periods within fiscal years beginning after December 15, 2019. The new standard will require adoption on a retrospective basis unless it is impracticable to apply, in which case it would be required to apply the amendments prospectively as of the earliest date practicable. The Company has not adapted this ASU codification and it does not anticipate that the adoption of this guidance will have any material effect on its financial statements.

In June 2016, the FASB issued Accounting Standards Update (“ASU”) 2016-13, “Financial Instruments - Credit Losses (Topic 326).” The new standard amends guidance on reporting credit losses for assets held at amortized cost basis and available-for-sale debt securities. This ASU is effective for financial statements issued for fiscal years beginning after December 15, 2018, including interim periods within those fiscal years. The Company is currently evaluating this guidance to determine the impact it may have on its financial statements.

In 2015, the FASB issued ASU No. 2015-17, “Income Taxes” (Topic 740): Balance Sheet Classification of Deferred Taxes, which requires all deferred tax assets and liabilities to be classified as noncurrent in a classified balance sheet. Current US GAAP requires an entity to separate deferred tax assets and liabilities into current and noncurrent amounts in a classified balance sheet. For public entities, ASU 2015-17 is effective for financial statements issued for annual periods beginning after December 15, 2016, and interim periods within those annual periods. For all other entities, ASU 2015-17 is effective for annual reporting periods beginning after December 15, 2017, and interim periods within annual periods beginning after December 15, 2018, and may be applied either prospectively or retrospectively, with early application permitted for financial statements that have not been previously issued. The Company has not yet determined the effect of the adoption of this standard on the Company’s financial position and results of operations.

NOTE 3 – PLANT AND EQUIPMENT

The Company purchased web-based naturopathic learning management system computer software, developed by a third party, to educate users with the health-related products for various illnesses, and how the Company’s learning systems could be used to improve their general wellbeing. The amount capitalized include direct costs incurred in developing the software purchased from the third party.

The following table presents details of our computer software costs as of September 30, 2018 and 2017:

Balance at September 30, 2017 | Additions and consolidated through merger of subsidiaries | Amortization | Balance at September 30, 2018 | |||||||||||||

| Plant and equipment | $ | - | $ | 195,452 | $ | (35,973 | ) | $ | 159,479 | |||||||

Plant and equipment costs are being amortized on a straight-line basis over their estimated life of three years.

The future amortization expense of equipment costs as of September 30, 2018 are to be recorded in accordance with their estimated useful lives.

NOTE 4 – OTHER INVESTMENTS

Other investments amounting to $93,580 as at September 30, 2018, represents unquoted investments carried at amortized costs.

NOTE 5 – ACCOUNT PAYABLES AND ACCRUED EXPENSES

Account payables as at September 30, 2018 and September 30, 2017 totaled $71,678 and $0, respectively while the accrued expenses as of September 30, 2018 and September 30, 2017 totaled $36,720 and $0, respectively.

| F-10 |

NOTE 6 – PAYABLE TO AFFILIATES

The Company has received an advance of $11,210 from a director for its working capital needs as of September 30, 2018 (see NOTE 7).