Table of Contents

As filed with the Securities and Exchange Commission on May 6, 2016.

Registration No. 333-

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

Performance Food Group Company

(Exact Name of Registrant as Specified in its Charter)

| Delaware | 5141 | 43-1983182 | ||

| (State or other jurisdiction of incorporation or organization) |

(Primary Standard Industrial Classification Code Number) |

(I.R.S. Employer Identification No.) |

12500 West Creek Parkway

Richmond, Virginia 23238

(804) 484-7700

(Address, including zip code, and telephone number, including area code, of Registrant’s principal executive offices)

A. Brent King

Senior Vice President, General Counsel and Secretary

Performance Food Group Company

12500 West Creek Parkway

Richmond, Virginia 23238

(804) 484-7700

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Copies to:

| Igor Fert, Esq. Simpson Thacher & Bartlett LLP 425 Lexington Avenue New York, NY 10017 Telephone: (212) 455-2000 Facsimile: (212) 455-2502 |

Marc Jaffe, Esq. Cathy Birkeland, Esq. Latham & Watkins LLP 885 Third Avenue New York, NY 10022 Telephone: (212) 906-1200 Facsimile: (212) 751-4864 |

Approximate date of commencement of the proposed sale of the securities to the public: As soon as practicable after the Registration Statement is declared effective.

If any of the securities being registered on this form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. ¨

If this form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ¨ | Accelerated filer | ¨ | |||

| Non-accelerated filer | x (Do not check if a smaller reporting company) | Smaller reporting company | ¨ | |||

CALCULATION OF REGISTRATION FEE

|

| ||||||||

| Title Of Each Class Of Securities To Be Registered |

Amount To Be Registered(1) |

Proposed Maximum Aggregate Offering Price Per Share(1) |

Proposed Maximum Aggregate Offering Price(1)(2) |

Amount of Registration Fee | ||||

| Common Stock, par value $0.01 per share |

13,800,000 |

$26.05 | $359,490,000 | $36,200.64 | ||||

|

| ||||||||

|

| ||||||||

| (1) | Includes shares/offering price of shares of common stock that the underwriters have the option to purchase. See “Underwriting.” |

| (2) | These figures are estimated solely for the purpose of calculating the registration fee in accordance with Rule 457(c) under the Securities Act of 1933, as amended, based on the average of high and low prices of the common stock on May 3, 2016 as reported on the New York Stock Exchange. |

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the Registration Statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

Table of Contents

The information in this prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and it is not soliciting an offer to buy these securities in any jurisdiction where the offer or sale is not permitted.

Subject to Completion. Dated May 6, 2016.

12,000,000 Shares

Performance Food Group Company

Common Stock

The selling stockholders named in this prospectus are offering 12,000,000 shares of common stock of Performance Food Group Company. The selling stockholders will receive all of the net proceeds from this offering and we will not receive any proceeds from the sale of our common stock by the selling stockholders.

Our common stock is listed on the New York Stock Exchange, or NYSE, under the symbol “PFGC”. On May 5, 2016, the closing sales price of our common stock as reported on the NYSE was $27.43 per share.

Investing in our common stock involves risk. See “Risk Factors” beginning on page 16 to read about factors you should consider before buying shares of our common stock.

Neither the Securities and Exchange Commission nor any other regulatory body has approved or disapproved of these securities or passed upon the accuracy or adequacy of this prospectus. Any representation to the contrary is a criminal offense.

| Per Share |

Total | |||

| Public offering price |

$ | $ | ||

| Underwriting discounts and commissions(1) |

$ | $ | ||

| Proceeds, before expenses, to the selling stockholders |

$ | $ |

| (1) | See “Underwriting” for additional information regarding underwriting compensation. |

To the extent that the underwriters sell more than 12,000,000 shares of common stock, the underwriters have the option to purchase up to an additional 1,800,000 shares from the selling stockholders at the public offering price less the underwriting discount and commissions. The selling stockholders will receive all of the proceeds from the sale of any such additional shares to the underwriters.

Delivery of the shares of common stock will be made on or about , 2016.

| Credit Suisse | Barclays |

Prospectus dated , 2016

Table of Contents

PFG Performance Food Group

Headquarters (Richmond, VA) Performance Foodservice (Broadline) Performance Foodservice (ROMA) Customized Vistar Quick Facts: $15,270,000,000 in FY2015 Sales Serving 150,000

customer locations Over 150,000 national and company branded products 69 distribution centers

Table of Contents

PFG Performance Food Group

Founded on food, focused on service.

Table of Contents

| Page | ||||

| ii | ||||

| ii | ||||

| ii | ||||

| 1 | ||||

| 16 | ||||

| 34 | ||||

| 36 | ||||

| 37 | ||||

| 38 | ||||

| 39 | ||||

| 40 | ||||

| MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS |

43 | |||

| 74 | ||||

| Page | ||||

| 75 | ||||

| 93 | ||||

| 131 | ||||

| 135 | ||||

| 137 | ||||

| 143 | ||||

| 151 | ||||

| MATERIAL U.S. FEDERAL INCOME AND ESTATE TAX CONSEQUENCES TO NON-U.S. HOLDERS OF OUR COMMON STOCK |

153 | |||

| 156 | ||||

| 162 | ||||

| 162 | ||||

| 162 | ||||

| F-1 | ||||

Unless otherwise indicated or the context otherwise requires, financial data in this prospectus reflects the consolidated business and operations of Performance Food Group Company and its consolidated subsidiaries.

Neither we nor the selling stockholders have authorized anyone to provide any information or to make any representations other than those contained in this prospectus or in any free writing prospectuses we have prepared. Neither we nor the selling stockholders take responsibility for, and cannot provide assurance as to the reliability of, any other information that others may give you. This prospectus is an offer to sell only the shares offered hereby, but only under circumstances and in jurisdictions where it is lawful to do so. The information contained in this prospectus is current only as of its date.

i

Table of Contents

Market data and industry statistics and forecasts used throughout this prospectus are based on the good faith estimates of management, which in turn are based upon management’s reviews of independent industry publications, reports by market research firms, and other independent and publicly available sources. Unless we indicate otherwise, market data and industry statistics used throughout this prospectus with respect to the aggregate size of the US foodservice distribution industry are for the year ended December 31, 2015 and all other such information is for the year ended December 31, 2014. All references to our industry share refer to our net sales as compared to aggregate revenues for the U.S. foodservice distribution industry.

Although we are not aware of any misstatements regarding the industry data that we present in this prospectus, our estimates involve risks and uncertainties and are subject to change based on various factors, including those discussed under “Risk Factors,” “Forward-Looking Statements,” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” in this prospectus.

TRADEMARKS, SERVICE MARKS AND TRADENAMES

This prospectus contains some of our trademarks, trade names, and service marks, including the following: Performance Foodservice, PFG Customized, Vistar, West Creek, Silver Source, Braveheart 100% Black Angus, Empire’s Treasure, Brilliance, Heritage Ovens, Village Garden, Guest House, Piancone, Luigi’s, Ultimo, Corazo, and Assoluti. Each one of these trademarks, trade names, or service marks is either (i) our registered trademark, (ii) a trademark for which we have a pending application, (iii) a trade name or service mark for which we claim common law rights, or (iv) a registered trademark or application for registration which we have been licensed by a third party to use.

Solely for convenience, the trademarks, service marks, and trade names referred to in this prospectus are without the ® and ™ symbols, but such references are not intended to indicate, in any way, that we will not assert, to the fullest extent under applicable law, our rights or the rights of the applicable licensors to these trademarks, service marks, and trade names. This prospectus contains additional trademarks, service marks, and trade names of others, which are the property of their respective owners. All trademarks, service marks, and trade names appearing in this prospectus are, to our knowledge, the property of their respective owners.

As used in this prospectus, unless otherwise noted or the context otherwise requires, (i) references to the “Company,” “we,” “our,” or “us” refer to Performance Food Group Company and its consolidated subsidiaries; (ii) references to the “Issuer” refer to Performance Food Group Company exclusive of its subsidiaries; (iii) references to “Blackstone” refer to certain investment funds affiliated with The Blackstone Group L.P.; (iv) references to “Wellspring Capital” are to investment funds affiliated with Wellspring Capital Management LLC; (v) references to the “Sponsors” are to Blackstone and Wellspring Capital; (vi) references to the “Investor Group” are, collectively, to the Sponsors, certain other investors, and certain members of our management; and (vii) references to the “underwriters” are to the firms listed on the cover page of this prospectus.

References to “fiscal 2016” are to the 53-week period ending July 2, 2016, references to “fiscal 2015” are to the 52-week period ended June 27, 2015, references to “fiscal 2014” are to the 52-week period ended June 28, 2014, references to “fiscal 2013” are to the 52-week period ended June 29, 2013, references to “fiscal 2012” are to the 52-week period ended June 30, 2012, references to “fiscal 2011” are to the 52-week period ended July 2, 2011, and references to “fiscal 2010” are to the 53-week period ended July 3, 2010.

ii

Table of Contents

This summary highlights certain significant aspects of our business and this offering. This is a summary of information contained elsewhere in this prospectus, is not complete, and does not contain all of the information that you should consider before making your investment decision. You should carefully read the entire prospectus, including the information presented under the section entitled “Risk Factors” and the consolidated financial statements and the notes thereto, before making an investment decision. This summary contains forward-looking statements that involve risks and uncertainties. Our actual results may differ significantly from future results contemplated in the forward-looking statements as a result of certain factors such as those set forth in “Risk Factors” and “Forward-Looking Statements.” When making an investment decision, you should also read the discussion under “Basis of Presentation” for the definition of certain terms used in this prospectus and other matters described in this prospectus.

Our Company

We are the third largest player by revenue in the growing $268 billion U.S. foodservice distribution industry, which supplies the diverse $640 billion U.S. “food-away-from-home” industry. We market and distribute approximately 150,000 food and food-related products from approximately 70 distribution centers to over 150,000 customer locations across the United States. We serve a diverse mix of customers, from independent and chain restaurants to schools, business and industry locations, hospitals, vending distributors, office coffee service distributors, big box retailers, and theaters. We source our products from over 5,000 suppliers and serve as an important partner to our suppliers by providing them access to our broad customer base. In addition to the products we offer to our customers, we provide value-added services by allowing our customers to benefit from our industry knowledge, scale, and expertise in the areas of product selection and procurement, menu development, and operational strategy. Our more than 12,000 employees work across three segments: Performance Foodservice, PFG Customized, and Vistar.

We plan to continue executing the strategies that have successfully delivered net sales, industry share, and profit growth. In the fiscal year ended June 27, 2015, we generated $15.3 billion in net sales and $328.6 million in Adjusted EBITDA, representing compound annual growth rates of 9% and 11%, respectively, since fiscal 2010. In the fiscal year ended June 27, 2015, we generated $56.5 million in net income. During the first nine months of fiscal 2016, we generated $11.7 billion in net sales and $251.9 million in Adjusted EBITDA, representing growth rates of 4% and 11%, respectively, compared to the first nine months of fiscal 2015. During the first nine months of fiscal 2016, we generated $39.1 million in net income. In calendar year 2014, we had an estimated industry share of 6.0% and our sales growth rate since calendar year 2010 is approximately three times the growth rate of the foodservice distribution industry in that same time frame. We believe that our current industry share, the large size of the U.S. foodservice distribution industry, and our track record of growing industry share provide us a significant opportunity for continued sales growth. See “—Summary Historical Consolidated Financial Data” for our definition of “Adjusted EBITDA” and a reconciliation of Adjusted EBITDA to net income, which we believe is the most directly comparable financial measure calculated in accordance with GAAP.

We attribute our sales growth primarily to our customer-centric business model. For us, that means understanding our customers’ business operations and economics so that we can help them be successful; placing our decision-making on how best to serve customers at the local level; and partnering with our suppliers to develop our high quality proprietary brands, which are a key driver for us in winning, retaining, and developing customers. We believe that our customer-centric business model differentiates us from our competitors who make customer-facing decisions outside of the local market and also from competitors who often do not have the scale to develop proprietary brands, provide value-added services, and distribute as effectively as we do.

1

Table of Contents

Since fiscal 2010, our profit growth has outpaced our sales growth as a result of shifting towards a more profitable mix of products and customers, capturing operating efficiencies from our sales growth, and delivering productivity initiatives. Our mix shift is primarily attributable to increased sales of our proprietary brands and sales to independent restaurants, which represent our highest margin products and customers, respectively. In addition, we have established a set of productivity initiatives in the areas of procurement and operations called Winning Together, which, together with increased net sales, continues to drive meaningful profit growth.

Our Segments

We believe that we are well positioned to serve our customers from our three business segments, which are distinguished by their diverse distribution models, the inventory they carry, and the customers they serve: Performance Foodservice, PFG Customized, and Vistar.

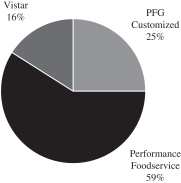

Performance Food Group: Fiscal 2015

| Net sales mix by operating segment

|

Key statistics | |||

|

|

Net sales |

$15.3 billion | ||

| Adjusted EBITDA |

$328.6 million | |||

| Distribution Centers |

69 | |||

| Customer Locations |

150,000+ | |||

| Products |

150,000+ | |||

| Suppliers |

5,000+ | |||

| Vehicles |

2,500+ | |||

| Employees

|

12,000+

| |||

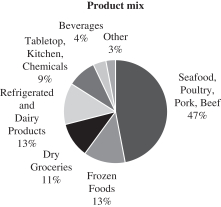

Performance Foodservice. Performance Foodservice is a leading U.S. foodservice distributor with substantial scale along the Eastern Seaboard and in the Southeast. Performance Foodservice operates a network of 25 broadline distribution centers, which supply a “broad line” of products, and 10 Roma distribution centers, which specialize in supplying independent pizzerias and other Italian-themed restaurants. Each of these distribution centers, which we refer to as operating companies or “OpCos,” is run by a business team who understands the local markets and the needs of its particular customers and who is empowered to make decisions on how best to serve them. For fiscal 2015 and fiscal 2014, Performance Foodservice generated $9.1 billion and $8.1 billion, respectively, in net sales. For the first nine months of fiscal 2016, Performance Foodservice generated $7.0 billion in net sales. Over 75% of Performance Foodservice’s sales during each of these periods was to restaurants. This segment serves over 85,000 customer locations with over 125,000 food and food-related products.

We offer our customers a broad product assortment that ranges from “center-of-the-plate” items (such as beef, pork, poultry, and seafood), frozen foods, refrigerated products, and dry groceries to disposables, cleaning and kitchen supplies, and related products used by our customers. In addition to the products we offer, we provide value-added services by enabling our customers to benefit from our industry knowledge, scale, and expertise in the areas of product selection and procurement, menu development, and operational strategy.

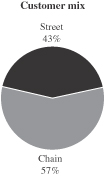

We classify our customers under two major categories: “Street” and multi-unit “Chain.” Street customers predominantly consist of independent restaurants. Chain customers are multi-unit restaurants with five or more

2

Table of Contents

locations, which include fine dining, family and casual dining, fast casual, and quick serve restaurants, as well as hotels, healthcare facilities, and other multi-unit institutional customers. Street customers utilize more of our value-added services, particularly in the areas of product selection and procurement, market trends, menu development, and operational strategy. Street customer purchases typically generate greater gross profit per case compared to sales to Chain customers. Sales to Street customers in fiscal 2015 accounted for 43% of Performance Foodservice sales compared to 37% in fiscal 2010. Case sales to Street customers in the first nine months of fiscal 2016 grew within our 6-10% growth goal range and accelerated modestly between our second and third quarters of fiscal 2016.

Our products consist of our proprietary-branded products, or “Performance Brands,” as well as nationally- branded products and products bearing our customers’ brands. Our Performance Brands typically generate higher gross profit per case than other brands. In fiscal 2015, Performance Brands accounted for 40% of the case volume sold to Street customers, up from 37% in fiscal 2010. Performance Brands accounted for over $2.0 billion of our Performance Foodservice net sales in fiscal 2015.

Performance Foodservice net sales for fiscal 2015 and fiscal 2014 were $9.1 billion and $8.1 billion, respectively, representing year-over-year growth of 12.1%. Performance Foodservice segment EBITDA for the same time period was $254.2 million and $207.5 million, representing year-over-year growth of 22.5%. Performance Foodservice net sales in the first nine months of fiscal 2016 and fiscal 2015 were $7.0 billion and $6.7 billion, respectively, representing year-over-year growth of 4.1%. Performance Foodservice segment EBITDA for the same time period was $206.9 million and $172.6 million, respectively, representing year-over-year growth of 19.9%.

| Performance Foodservice: Fiscal 2015 Net Sales | ||

|

|

|

PFG Customized. PFG Customized is a leading national distributor to the family and casual dining channel. We serve over 5,000 customer locations across the United States from nine distribution centers that provide tailored supply chain solutions to our customers. Our network of distribution centers was developed around our customers and is strategically positioned to provide an efficient supply chain across both inbound and outbound logistics. PFG Customized’s product offerings are determined by each of our customers’ specific menu requirements. We also provide customers with value-added services, such as expertise in fresh product distribution, logistics management, procurement management, and information system interfaces, which enable our customers to run their businesses efficiently.

We serve many of the most recognizable family and casual dining restaurant chains, including Bonefish Grill, Carrabba’s Italian Grill, Chili’s, Cracker Barrel, Joe’s Crab Shack, Logan’s Roadhouse, O’Charley’s, Outback Steakhouse, Ruby Tuesday, and TGI Friday’s, and we have recently entered into an agreement to serve

3

Table of Contents

Red Lobster. PFG Customized’s five largest family and casual dining customers have been with us for an average of more than 15 years. Cracker Barrel was PFG Customized’s first customer and grew from a substantial regional account served by Performance Foodservice to an account whose needs are best served by customized distribution. PFG Customized recently began to utilize its distribution platform to serve fast casual chains such as Fuzzy’s Taco Shop, and PDQ, as well quick serve chains including Church’s Chicken and Wendy’s.

PFG Customized net sales for fiscal 2015 and fiscal 2014 were $3.8 billion and $3.3 billion, respectively, representing year-over-year growth of 13.7%. PFG Customized segment EBITDA for the same time periods was $36.5 million and $37.5 million, representing year-over-year decline of 2.7%. The majority of the increase in sales was attributable to the expansion of services provided to a single existing customer. PFG Customized net sales in the first nine months of fiscal 2016 and fiscal 2015 were $2.8 billion and $2.8 billion, respectively, representing year-over-year growth of 0.6%. PFG Customized segment EBITDA for the same time periods was $26.2 million and $25.6 million, representing year-over-year growth of 2.3%.

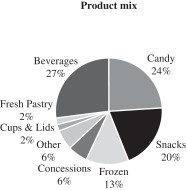

| PFG Customized: Fiscal 2015 Net Sales | ||

|

|

|

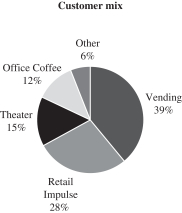

Vistar. Vistar is a leading national distributor of candy, snacks, and beverages to vending and office coffee service distributors, big box retailers, and theaters. The segment provides national distribution of approximately 20,000 different SKUs of candy, snacks, beverages, and other items to approximately 60,000 customer locations from our network of 25 Vistar OpCos and nine Merchant’s Marts locations. Merchant’s Marts are cash-and-carry operators where customers generally pick up orders rather than having them delivered. Vistar’s scale in these channels enhances our ability to procure a broad variety of products for our customers. Vistar OpCos deliver to vending and office coffee service distributors and directly to most theaters and some other locations. The distribution model also includes a “pick and pack” capability, which utilizes third-party carriers and Vistar’s SKU variety to sell to customers whose order sizes are too small to be served effectively by our distribution network. We believe these capabilities, in conjunction with the breadth of our inventory, are differentiating and allow us to serve many distinct customer types. Vistar has successfully built upon our national platform to broaden the channels we serve to include hospitality venues, concessionaires, airport gift shops, college book stores, corrections facilities, and impulse locations in big box retailers such as Home Depot, Dollar Tree, Staples, and others.

4

Table of Contents

Vistar net sales for fiscal 2015 and fiscal 2014 were $2.4 billion and $2.3 billion, respectively, representing year-over-year growth of 6.9%. Vistar segment EBITDA for the same time period was $105.5 million and $88.3 million, respectively, representing year-over-year growth of 19.5%. Vistar net sales for the first nine months of fiscal 2016 and fiscal 2015 were $1.9 billion and $1.8 billion, respectively, representing year-over-year growth of 8.7%. Vistar segment EBITDA for the same time period was $83.7 million and $79.2 million, respectively, representing year-over-year growth of 5.7%.

| Vistar: Fiscal 2015 Net Sales | ||

|

|

|

Our Industry

We distribute to the food-away-from-home industry, a large industry with attractive underlying growth trends. According to the U.S. Department of Commerce, consumer spending on food-away-from-home in the United States totaled $640 billion in 2014, making it one of the largest industries in the country. The industry grew from $331 billion in sales in 1999 to over $640 billion in sales in 2014, representing a compound annual growth rate of approximately 4.5%. Macroeconomic drivers of growth include increases in U.S. gross domestic product, employment levels, and personal consumption expenditures. Microeconomic drivers include increases in the number of restaurants, a continued shift toward value-added products and desire for convenience, smaller sized households, an aging population that spends more per capita at food-away-from-home establishments, and a rebound in the number of dual income households.

We operate in the U.S. foodservice distribution industry, which supplies the food-away-from-home industry and which totaled $268 billion in sales in 2015 according to Technomic. The U.S. foodservice distribution industry consists of four categories of distributors:

| • | Broadline distributors carry a “broad line” of products to serve the needs of many different types of food-away-from-home establishments; |

| • | System distributors carry products that are typically specified by large national and regional chains; |

| • | Specialized distributors carry a variety of products within specific categories, such as produce, meats, or seafood, or they focus on particular customer types, such as schools, vending operations, or fine dining; and |

| • | Cash-and-carry centers where customers come to pick-up their orders. |

We are distinguished from most of our competitors by operating in each of the four categories of distributors mentioned above.

5

Table of Contents

Broadline distribution is the largest segment in the U.S. foodservice distribution industry. According to Technomic, the “Power Distributors,” which they define as the 21 companies with annual sales greater than $250 million, grew sales by 6% from 2012 to 2013, or approximately twice the growth rate for the overall foodservice distribution industry, which we believe is representative of the benefits of scale.

We benefit from being one of the leading companies in the U.S. foodservice distribution industry. We believe that our current industry share, the large size of the U.S. foodservice distribution industry, and our track record of growing industry share provide us a significant opportunity for continued sales growth.

On December 8, 2013, the two largest companies in our industry, Sysco Corporation (“Sysco”) and US Foods, Inc. (“US Foods”), announced that they entered into an agreement and plan of merger. On February 2, 2015, we reached an agreement to purchase 11 US Foods facilities relating to the proposed merger. On February 19, 2015, the Federal Trade Commission filed suit seeking an injunction to prevent the proposed merger and, on June 23, 2015, the United States District Court for the District of Columbia granted the injunction. In June 2015, the proposed merger was terminated. As a result, our agreement to purchase the facilities was also terminated and we received a termination fee of $25 million.

Based on the industry size as estimated by the industry analyst Technomic, we had an estimated industry share of 6.0% for each of calendar 2013 and calendar 2014, and Sysco and US Foods had an estimated industry share of 20.0% and 10.0%, respectively, in calendar 2014.

Our Strengths

Leading Market Positions

We believe that our leading market positions within each of our business segments allow us to compete effectively in attracting new customers, to attract and retain industry talent, and to drive our growth as we execute our business strategy. We have a diverse business model that operates in three segments, allowing us to capitalize on the growth in food-away-from-home consumption. We believe our leading market positions are exhibited in the following way:

| • | Performance Foodservice. We are the third largest broadline distributor by revenue in the United States after Sysco and US Foods, according to Technomic. We have significant scale in markets along the Eastern Seaboard and in the Southeast. Within Performance Foodservice, we believe that our Roma products make us the leading distributor to independent pizzerias in the United States. |

| • | PFG Customized. PFG Customized is a leading national distributor to family and casual dining restaurants, and we believe benefits from longstanding relationships with our customers, strong customer loyalty, and a network that is optimized to serve our customer base efficiently. |

| • | Vistar. Vistar is a leading national distributor of candy, snacks, and beverages to vending and office coffee service distributors, big box retailers, and theater customers, whom we believe benefit from substantial product variety sold at competitive prices. |

Scale Distribution Platforms

We believe we have a competitive advantage over smaller regional and local broadline distributors through economies of scale in purchasing and procurement, which allow us to offer a broad variety of products (including our proprietary Performance Brands) at competitive prices to our customers. Our customers benefit from our ability to provide them with extensive geographic coverage as they continue to grow. We believe we also benefit from supply chain efficiency, including a growing inbound logistics backhaul network that uses our collective

6

Table of Contents

distribution network to deliver inbound products across business segments; best practices in warehousing, transportation, and risk management; the ability to benefit from the scale of our purchases of items not for resale, such as trucks, construction materials, insurance, banking relationships, healthcare, and material handling equipment; and the ability to optimize our networks so that customers are served from the most efficient OpCo, which minimizes the cost of delivery. We believe these efficiencies and economies of scale will lead to continued improvements in our operating margins when combined with incremental fixed-cost advantage.

Customer-Centric Business Model

Our customer-centric business model is based on understanding our customers’ business operations and economics so that we can help them be successful, partnering with our suppliers to develop high quality proprietary brands specifically tailored to our customers’ needs, and placing our decision making on how best to serve customers at the local level so that we remain nimble at the point of transaction. The model embodies how we organize the Company, how our business processes work, and how we design our information systems. Over 12,000 PFG employees share our mission to grow sales by providing excellent service that is locally tailored to each customer. Over 5,000 of our employees interact with customers daily, either in sales or in making deliveries. Our sales associates receive extensive and ongoing product training and earn incentives primarily based on how effectively they grow our business with customers. Our customer-facing employees are supported by hundreds of employees who develop, source, and market over 150,000 food and related products from over 5,000 suppliers and by several thousand warehouse workers focused on filling customer orders accurately, efficiently, and in a timely manner. We believe that our customer-centric business model differentiates us from our competitors who make customer-facing decisions outside the local market and also from competitors who often do not have the scale to develop proprietary brands, provide value-added services, and distribute as effectively as we do.

Proven Ability to Increase Sales to Street Customers and Market our Proprietary Brands

We maintain a strong focus on growing sales to Street customers (our highest profit margin customers), growing sales of Performance Brands (our highest profit margin products), and attracting, retaining, and developing a more effective Street sales force. We believe that offering our Performance Brands enhances customer loyalty and attracts new customers, particularly Street customers. These Performance Brands include exclusive products offered across a wide variety of approximately 10,000 SKUs, which are developed in partnership with our suppliers and customers in order to satisfy the specific needs of our customer base.

From fiscal 2010 through fiscal 2015, we have grown the number of Street customers, case sales to Street customers, and case sales of Performance Brands to Street customers at compound annual growth rates of 8%, 11%, and 13%, respectively. In fiscal 2015, Performance Brands accounted for 40% of the case volume sold to Street customers, up from 37% in fiscal 2010.

Disciplined and Proven Acquirer

We have made 15 acquisitions over the past seven years, beginning with the merger of PFG and Vistar in 2008, when management integrated the two companies with significant synergies. Acquisitions have typically been completed at attractive valuation multiples and have been accretive to our Adjusted EBITDA margins on both a pre- and post-synergy basis.

In recent years, we have made four acquisitions in our Performance Foodservice business, which expanded our footprint in North and South Carolina, Kentucky, Illinois, and northern coastal California. Synergies from these acquisitions typically include introducing Performance Brands to the customers of the acquired company, reducing network mileage, implementing operational best practices, and achieving cost savings, such as expenses associated with insurance and benefit programs.

7

Table of Contents

In our Vistar segment, we entered the hotel pantry business through an acquisition, which we are using as a platform to expand further into the hospitality channel. Vistar also used an acquisition to better develop our small drop fulfillment technology to serve big box retailers with candy, snacks, beverages, and other items, a capability that we believe has application in other channels.

Experienced and Invested Management Team

Our senior management team has extensive experience and proven success in the foodservice industry. With 250 years of combined experience (over 20 years on average for the executive leadership team), we believe that our senior management team’s experience in all parts of the industry has enabled us to grow and diversify our business while improving operational efficiency. Members of management have previous experience at other leading foodservice distributors, including Sysco, US Foods, PYA Monarch, and Alliant Foodservice. Other management team members have experience elsewhere in the food industry, ranging from manufacturers and marketers to retailers and contract feeders. Management has invested over $21 million in the equity of the Company and the substantial majority of management’s incentive compensation is tied to our financial performance. We believe management’s investment and incentive structure align its interests with those of our stockholders.

Substantial Free Cash Flow Generation

Our cash flows benefit from a steady, recurring revenue stream supported by effective cost management and a leading market share in the United States foodservice distribution industry. A significant portion of our sales are based on contract pricing, as either a percentage or fixed fee above costs, which enables us to substantially mitigate cost inflation. In order to minimize costs, we leverage our national scale as the third-largest foodservice distributor in the United States and enter into supplier agreements that maximize promotional allowance rebates. We have made a focused effort to drive sales of our proprietary brands, which carry a higher selling margin per case than branded products.

While we experience some seasonal fluctuations in our working capital needs, we effectively manage them with our stable gross margins and our prudent liquidity management and borrowing practices. Because of the predictable nature of our business, our annual capital expenditure requirement is very moderate, averaging 0.5% of net sales from fiscal 2010 to fiscal 2015. Recently our primary capital expense has been IT and productivity investment, which had effects on cash flow that were offset by gross margin expansion. Our annual free cash flow, defined as Adjusted EBITDA minus capital expenditures, grew 17.6% year-over-year from fiscal 2014 to fiscal 2015.

Our Strategy

We intend to continue to expand our industry share and to grow sales and profits by executing on the following key elements of our strategy.

Continue to Grow Street and Performance Brand Sales

We believe that there is a significant and ongoing opportunity to grow sales to Street customers (our highest profit margin customers) and to expand sales of our Performance Brands (our highest profit margin products). We believe that providing customers with proprietary distributor brands such as Performance Brands has been a key driver for us in winning, retaining, and developing customers, especially Street customers. In addition, we believe that our ability to build and retain an increasingly effective sales force has complemented these results. Street business momentum facilitates further development of our Performance Brand portfolio, which in turn enables us to win and develop more Street customers. Smaller regional competitors often do not have the scale to develop their own distinctive brands, and we believe this is a key reason why our Performance Foodservice segment has increased its sales to Street customers. By continuing to focus on increasing sales to our Street customers and sales of our Performance Brands, we believe that we can continue to drive profitable growth.

8

Table of Contents

Continue to Grow our Customers and Channels

We intend to increase penetration within our existing channels, enter new channels, and continue to win new customers in all three business segments by using our scale, operational excellence, geographic presence, and customer-centric business model.

| • | Performance Foodservice. In addition to our success in growing our Street business, we believe significant opportunity remains to expand our customer base. For example, in the past three years we have won the fast-growing distribution business of Anthony’s Coal Fired Pizza, Blaze Pizza, Chuy’s, Habit Burger, Hwy 55 Burgers Shakes & Fries, Pollo Tropical, Shake Shack, and Taco Cabana. We believe significant opportunity remains to continue expanding our customer base through new multi-unit restaurant chains and other channels such as schools, hospitals, and commercial locations. |

| • | PFG Customized. We intend to continue to grow our traditional customer base and to expand sales to new customer channels. We have recently expanded our customer base to include select fast casual customers including Fuzzy’s Taco Shop and PDQ and quick serve customers including Wendy’s. |

| • | Vistar. We have utilized Vistar’s combination of inventory variety, distribution methods, and national scale to diversify our channel mix. This has enabled Vistar to serve new customers and channels including concessionaires (such as Minor League Baseball), corrections facilities, college bookstores, and hospitality, among others. Additionally, Vistar continues to grow within vending and office coffee service distribution, big box retailers, and theaters. |

Expand Margins through Continuous Productivity Improvements

We are committed to expanding margins through operating efficiencies and specific productivity programs, which will complement the effect of selling a more profitable mix of customers and brands. We have established a program called Winning Together, which complements our sales growth with ongoing initiatives that take advantage of our scale and drive productivity in non-customer facing areas. Winning Together is led by teams whose primary responsibility is to improve our business processes, capture best practices, and maintain a continuous improvement culture in our procurement and operations functions.

The two key components of Winning Together are Winning Together Through Procurement and Winning Together Through Operations. Winning Together Through Procurement uses structured negotiations with our procurement partners, including selected national, regional, and local suppliers, to develop the mutual profitability of the relationship and to encourage suppliers to invest in our growth. Winning Together Through Operations seeks to accelerate efficiencies in our warehouses and our inbound and outbound logistics functions. This program leverages best practices and scale, implements new productivity software, and establishes a model OpCo as a proving ground for new technologies and business processes.

Winning Together drove meaningful cost-saving benefits in fiscal 2015, and we continue to benefit from this program in fiscal 2016.

Continue to Pursue Opportunistic Acquisitions

We have a strong track record of sourcing, executing, and integrating accretive acquisitions. We intend to continue pursuing selective acquisitions in order to further our competitive position in the industry and to allow us both to enter into new geographies and channels as well as to expand in existing ones.

Over the past seven years, we have made 15 acquisitions, including acquiring five broadline locations in Kentucky, North and South Carolina, Illinois, and northern coastal California. These acquisitions have expanded our broadline geographic reach, and we believe further meaningful opportunities exist that would enable us to reach additional customers. In Vistar, our acquisition focus remains on companies in adjacent channels that can benefit from the strength of our inventory and delivery method variety or that can add capabilities or technologies to our portfolio. We believe that there are a number of attractive potential acquisition opportunities in our industry.

9

Table of Contents

Risks Related to Our Business and Our Industry

Investing in our common stock involves substantial risks, and our ability to successfully operate our business and execute our growth plan is subject to numerous risks, including those that are generally associated with operating in the foodservice distribution industry. Some of the more significant challenges and risks include the following:

| • | competition in our industry is intense, and we may not be able to compete successfully; |

| • | our industry has low margins, which may increase the volatility of our results of operations; |

| • | we may not realize anticipated benefits from our operating cost reduction and productivity improvement efforts, including Winning Together; |

| • | our profitability is directly affected by cost inflation or deflation and other factors; |

| • | many of our customers are not obligated to continue purchasing products from us; |

| • | group purchasing organizations may become more active in our industry and increase their efforts to add our customers as members of these organizations; |

| • | changes in consumer eating habits could materially and adversely affect our business, financial condition, or results of operations; |

| • | extreme weather conditions and natural disasters may interrupt our business, or our customers’ businesses, which could have a material adverse effect on our business, financial condition or results of operations; |

| • | our substantial indebtedness could adversely affect our ability to raise additional capital to fund our operations, limit our ability to react to changes in the economy or in our industry, expose us to interest rate risk to the extent of our variable rate debt, and prevent us from meeting our obligations under our indebtedness; |

| • | affiliates of our Sponsors control us; the Sponsors’ interests may conflict with ours or yours in the future; |

| • | upon completion of this offering, we will no longer be a “controlled company” within the meaning of the rules of the NYSE and the rules of the SEC; however, we may continue to rely on exemptions from certain corporate governance requirements that would otherwise provide protection to stockholders of other companies during a one-year transition period; and |

| • | other factors set forth under “Risk Factors” in this prospectus. |

Before you participate in this offering, you should carefully consider all of the information in this prospectus, including matters set forth under the heading “Risk Factors.”

Recent Developments

Multi-Year Distribution Agreement with Red Lobster

In May 2016, we entered into a distribution agreement with Red Lobster, the world’s largest seafood restaurant company. Under the multi-year agreement, we will provide distribution solutions to all of Red Lobster’s more than 670 restaurants in the United States. PFG Customized expects to begin rolling out service to Red Lobster in the first and second quarters of fiscal 2017.

Executive Management Change

On May 3, 2016, Robert D. Evans notified the Company of his intent to retire from his position as Senior Vice President and Chief Financial Officer of the Company. Mr. Evans’s retirement will be effective on the date that the Company appoints a new Chief Financial Officer. The Company is working with an executive search

10

Table of Contents

firm to assist in the search for Mr. Evans’s successor. Following Mr. Evans’s retirement, Mr. Evans will remain available to provide transition and advisory services and consulting services to the Company for a specified period pursuant to a transition agreement with the Company.

Amendment and Restatement of ABL Facility

On February 1, 2016, we amended and restated the credit agreement governing our ABL facility (the “ABL Facility”) to increase the borrowing capacity from $1.4 billion to $1.6 billion, lower interest rates for LIBOR based loans, extend the maturity from May 2017 to February 2021, and modify triggers and provisions related to certain reporting, financial, and negative covenants. The total size of the facility immediately increased the effective borrowing capacity under the ABL Facility since borrowing base assets exceeded the facility size prior to the amendment. We estimate that approximately $6.6 million of fees and expenses have been incurred for the amendment, which were included as deferred financing costs and will be amortized over the remaining term of the ABL Facility. Of this amount, $5.6 million was paid during the nine months ended March 26, 2016. In connection with the closing of this amendment, we borrowed $200.0 million under the ABL Facility and used the proceeds to repay $200.0 million aggregate principal amount of loans under the Term Facility.

Initial Public Offering

On October 6, 2015, we completed an initial public offering (“IPO”) of 16,675,000 shares of common stock for a cash offering price of $19.00 per share ($17.955 per share net of underwriting discounts), including the exercise in full by underwriters of their option to purchase additional shares. We sold an aggregate of 12,777,325 shares of such common stock and certain selling stockholders sold 3,897,675 shares (including the shares sold pursuant to the underwriters’ option to purchase additional shares). The offering was registered under the Securities Act of 1933, as amended (the “Securities Act”), on a registration statement on Form S-1 (Registration No. 333-198654).

We used the net offering proceeds to us, after deducting the underwriting discount and our direct offering expenses, to repay $223.0 million aggregate principal amount of indebtedness under our term loan facility (the “Term Facility”). We used the remainder of the net proceeds for general corporate purposes.

Corporate History and Information

The issuer was formed under the laws of the state of Delaware on September 23, 2002. Our principal executive office is located at 12500 West Creek Parkway, Richmond VA 23238. Our main telephone number is 804-484-7700.

Our Sponsors

Blackstone (NYSE: BX) is one of the world’s leading investment firms. Blackstone’s asset management businesses, with approximately $343.7 billion in assets under management as of March 31, 2016, include investment vehicles focused on private equity, real estate, public debt and equity, non-investment grade debt and secondary funds, all on a global basis. Blackstone also provides various financial advisory services, including financial and strategic advisory, restructuring and reorganization advisory, and fund placement services.

Wellspring Capital Management, a leading middle-market private equity firm, was founded in 1995. By teaming with strong management, Wellspring unlocks underlying value and pursues new growth opportunities through strategic initiatives, operating improvements, and add-on acquisitions. The firm functions as a strategic rather than tactical partner, providing management teams with top-line support, M&A experience, and financial expertise. Wellspring has approximately $3 billion of private equity capital under management.

Immediately after this offering of our common stock, affiliates of Blackstone and Wellspring will beneficially own approximately 47.1% and 15.9% of our common stock, respectively, or approximately 45.4% and 15.9%, respectively, if the underwriters exercise in full their option to purchase additional shares.

11

Table of Contents

THE OFFERING

| Common stock offered by the selling stockholders |

12,000,000 shares. |

| Option to purchase additional shares |

The underwriters have an option to purchase up to 1,800,000 additional shares of our common stock from certain of the selling stockholders. The underwriters can exercise this option at any time within 30 days from the date of this prospectus. |

| Common stock outstanding |

102,614,707 shares, as of April 26, 2016. |

| Use of proceeds |

The selling stockholders will receive all of the net proceeds from the sale of the shares of our common stock in this offering, including upon the sale of shares if the underwriters exercise their option to purchase additional shares, from the selling stockholders in this offering. We will not receive any of the proceeds from the sale of the shares of common stock by the selling stockholders. |

| Dividend policy |

We have no current plans to pay dividends on our common stock. Any decision to declare and pay dividends in the future will be made at the sole discretion of our Board of Directors and will depend on, among other things, our results of operations, cash requirements, financial condition, contractual restrictions in our ABL Facility and Term Loan Facility, and other factors that our Board of Directors may deem relevant. |

| Risk factors |

See “Risk Factors” beginning on page 16 for a discussion of risks you should carefully consider before deciding to invest in our common stock. |

| NYSE trading symbol |

“PFGC.” |

The number of shares of our common stock outstanding is based on 102,614,707 shares of common stock outstanding as of April 26, 2016, which includes 2,883,628 shares of restricted stock. The total number of outstanding shares does not give effect to options relating to 3,822,090 shares of common stock, 288,186 shares issuable pursuant to restricted stock units, 395,019 shares reserved for future issuance under our 2007 Management Option Plan (the “2007 Stock Option Plan”), and an additional 3,774,894 shares reserved for future issuance under the Performance Food Group 2015 Omnibus Incentive Plan (the “2015 Omnibus Incentive Plan”).

12

Table of Contents

SUMMARY HISTORICAL CONSOLIDATED FINANCIAL DATA

The following tables set forth our summary historical consolidated financial data for the periods and as of the dates indicated.

We derived the summary consolidated statement of operations data and the summary consolidated statement of cash flows data for the years ended June 27, 2015, June 28, 2014, and June 29, 2013 and the summary consolidated balance sheet data as of June 27, 2015 and June 28, 2014 from our audited consolidated financial statements included elsewhere in this prospectus. We derived the consolidated balance sheet data as of June 29, 2013 from our unaudited financial statements not included in this prospectus. We derived the summary consolidated statement of operations data and the summary consolidated statement of cash flows data for the nine months ended March 26, 2016 and March 28, 2015 and the summary consolidated balance sheet data as of March 26, 2016 from our unaudited consolidated financial statements included elsewhere in this prospectus. The results from any interim period are not necessarily indicative of the results that may be expected for the full year. Our historical results are not necessarily indicative of the results expected for any future period.

The summary historical consolidated financial data set forth below should be read in conjunction with “Capitalization,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” and the consolidated financial statements and the notes thereto included elsewhere in this prospectus.

| For the nine months ended | For the fiscal year ended | |||||||||||||||||||

| March 26, 2016 |

March 28, 2015 |

June 27, 2015 |

June 28, 2014 |

June 29, 2013 |

||||||||||||||||

| (unaudited) | ||||||||||||||||||||

| (dollars in millions, except per share data) | ||||||||||||||||||||

| Statement of Operations Data: |

||||||||||||||||||||

| Net sales |

$ | 11,731.9 | $ | 11,285.6 | $ | 15,270.0 | $ | 13,685.7 | $ | 12,826.5 | ||||||||||

| Cost of goods sold |

10,283.2 | 9,927.3 | 13,421.7 | 11,988.5 | 11,243.8 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Gross profit |

1,448.7 | 1,358.3 | 1,848.3 | 1,697.2 | 1,582.7 | |||||||||||||||

| Operating expenses |

1,313.3 | 1,251.4 | 1,688.2 | 1,581.6 | 1,468.0 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Operating profit |

135.4 | 106.9 | 160.1 | 115.6 | 114.7 | |||||||||||||||

| Interest expense, net(1) |

65.9 | 64.6 | 85.7 | 86.1 | 93.9 | |||||||||||||||

| Loss on extinguishment of debt |

— | — | — | — | 2.0 | |||||||||||||||

| Other, net |

3.7 | 3.2 | (22.2 | ) | (0.7 | ) | (0.7 | ) | ||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Other expense, net |

69.6 | 67.8 | 63.5 | 85.4 | 95.2 | |||||||||||||||

| Income before taxes |

65.8 | 39.1 | 96.6 | 30.2 | 19.5 | |||||||||||||||

| Income tax expense(2) |

26.7 | 16.8 | 40.1 | 14.7 | 11.1 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Net income |

$ | 39.1 | $ | 22.3 | $ | 56.5 | $ | 15.5 | $ | 8.4 | ||||||||||

| Per Share Data(3): |

||||||||||||||||||||

| Basic net income per share |

$ | 0.41 | $ | 0.26 | $ | 0.65 | $ | 0.18 | $ | 0.10 | ||||||||||

| Diluted net income per share |

$ | 0.40 | $ | 0.25 | $ | 0.64 | $ | 0.18 | $ | 0.10 | ||||||||||

| Weighted-average number of shares used in per share amounts |

||||||||||||||||||||

| Basic |

95,230,548 | 86,874,101 | 86,874,727 | 86,868,452 | 86,864,606 | |||||||||||||||

| Diluted |

96,750,311 | 87,664,715 | 87,613,698 | 87,533,324 | 87,458,530 | |||||||||||||||

| Other Financial Data: |

||||||||||||||||||||

| EBITDA(4) |

$ | 217.9 | $ | 195.4 | $ | 303.6 | $ | 249.0 | $ | 233.4 | ||||||||||

| Adjusted EBITDA(4) |

251.9 | 226.1 | 328.6 | 286.1 | 271.3 | |||||||||||||||

| Capital expenditures |

68.0 | 63.7 | 98.6 | 90.6 | 66.5 | |||||||||||||||

| Summary Statement of Cash Flows Data: |

||||||||||||||||||||

| Net cash provided by (used in) continuing operations: |

||||||||||||||||||||

| Operating activities |

$ | 117.6 | $ | 28.4 | $ | 127.4 | $ | 119.7 | $ | 140.7 | ||||||||||

| Investing activities |

(107.5 | ) | (66.3 | ) | (100.7 | ) | (93.4 | ) | (150.0 | ) | ||||||||||

| Financing activities |

(8.6 | ) | 39.4 | (22.8 | ) | (35.1 | ) | 12.3 | ||||||||||||

13

Table of Contents

| As of | ||||||||||||||||

| March 26, 2016 |

June 27, 2015 |

June 28, 2014 |

June 29, 2013 |

|||||||||||||

| (unaudited) |

||||||||||||||||

| (dollars in millions) | ||||||||||||||||

| Balance Sheet Data: |

||||||||||||||||

| Cash and cash equivalents |

$ | 10.7 | $ | 9.2 | $ | 5.3 | $ | 14.1 | ||||||||

| Total assets |

3,440.1 | 3,390.9 | 3,239.8 | 3,055.4 | ||||||||||||

| Total debt |

1,214.1 | 1,442.5 | 1,459.5 | 1,483.0 | ||||||||||||

| Total shareholders’ equity |

769.8 | 493.0 | 434.1 | 420.0 | ||||||||||||

| (1) | Interest expense, net includes $5.6 million, $6.0 million, $8.0 million, $6.6 million and $11.1 million of reclassification adjustments for changes in fair value of interest rate swaps for the first nine months of fiscal 2016, the first nine months of fiscal 2015, fiscal 2015, fiscal 2014, and fiscal 2013, respectively. In addition, includes $5.8 million loss on extinguishment and $5.5 million accelerated amortization of original issue discount and deferred financing costs during the nine months ended March 26, 2016. |

| (2) | Income tax expense includes $2.2 million, $2.4 million, $3.1 million, $2.6 million, and $4.3 million tax benefit from reclassification adjustments for the first nine months of fiscal 2016, the first nine months of fiscal 2015, fiscal 2015, fiscal 2014, and fiscal 2013, respectively, related to the reclassification adjustments for changes in fair value of interest rate swaps referred to in note (1). |

| (3) | Share and per share amounts have been retroactively adjusted to reflect a reverse stock split of our common stock. |

| (4) | Management measures operating performance based on our EBITDA, defined as net income (loss) before interest expense (net of interest income), income taxes, and depreciation and amortization. EBITDA is not defined under U.S. GAAP and is not a measure of operating income, operating performance, or liquidity presented in accordance with U.S. GAAP and is subject to important limitations. Our definition of EBITDA may not be the same as similarly titled measures used by other companies. |

We believe that the presentation of EBITDA enhances an investor’s understanding of our performance. We believe this measure is a useful metric to assess our operating performance from period to period by excluding certain items that we believe are not representative of our core business. We use this measure to evaluate the performance of our segments and for business planning purposes. We believe that EBITDA will provide investors with a useful tool for assessing the comparability between periods of our ability to generate cash from operations sufficient to pay taxes, to service debt, and to undertake capital expenditures because it eliminates depreciation and amortization expense. We present EBITDA in order to provide supplemental information that we consider relevant for the readers of our consolidated financial statements included elsewhere in this prospectus, and such information is not meant to replace or supersede U.S. GAAP measures.

In addition, our management uses Adjusted EBITDA, defined as net income (loss) before interest expense (net of interest income), income and franchise taxes, and depreciation and amortization, further adjusted to exclude certain unusual, non-cash, non-recurring, cost reduction, and other adjustment items permitted in calculating covenant compliance under our credit agreements (other than certain pro forma adjustments permitted under our credit agreements relating to the Adjusted EBITDA contribution of acquired entities or businesses prior to the acquisition date). Under our credit agreements, our ability to engage in certain activities such as incurring certain additional indebtedness, making certain investments, and making restricted payments and other covenant compliance matters are tied to ratios based on Adjusted EBITDA (as defined in the credit agreements). Our definition of Adjusted EBITDA may not be the same as similarly titled measures used by other companies.

Adjusted EBITDA is not defined under U.S. GAAP, and is subject to important limitations. We believe that the presentation of Adjusted EBITDA is useful to investors because it is frequently used by securities analysts, investors, and other interested parties in their evaluation of the operating performance of companies in industries similar to ours. In addition, targets based on Adjusted EBITDA are among the measures we use to evaluate our management’s performance for purposes of determining their compensation under our incentive plans as further described under “Management—Executive Compensation.”

14

Table of Contents

We believe that the most directly comparable GAAP measure to Adjusted EBITDA is net income (loss). The following table reconciles net income to EBITDA and Adjusted EBITDA for the periods presented:

| For the nine months ended |

For the fiscal year ended | |||||||||||||||||||||||||||

| March 26, 2016 |

March 28, 2015 |

June 27, 2015 |

June 28, 2014 |

June 29, 2013 |

June 30, 2012 |

July 2, 2011 |

||||||||||||||||||||||

| (unaudited) |

||||||||||||||||||||||||||||

| (dollars in millions) | ||||||||||||||||||||||||||||

| Net income |

$ 39.1 | $22.3 | $ | 56.5 | $ | 15.5 | $ | 8.4 | $ | 21.0 | $ | 13.7 | ||||||||||||||||

| Interest expense, net |

65.9 | 64.6 | 85.7 | 86.1 | 93.9 | 76.3 | 78.9 | |||||||||||||||||||||

| Income tax expense |

26.7 | 16.8 | 40.1 | 14.7 | 11.1 | 12.9 | 10.9 | |||||||||||||||||||||

| Depreciation |

58.3 | 57.1 | 76.3 | 73.5 | 58.7 | 46.4 | 43.2 | |||||||||||||||||||||

| Amortization of intangible assets |

27.9 | 34.6 | 45.0 | 59.2 | 61.3 | 55.9 | 55.8 | |||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| EBITDA |

217.9 | 195.4 | 303.6 | 249.0 | 233.4 | 212.5 | 202.5 | |||||||||||||||||||||

| Non-cash items(i) |

13.2 | 2.3 | 4.3 | 4.8 | 1.8 | 3.8 | 0.3 | |||||||||||||||||||||

| Acquisition, integration and reorganization(ii) |

5.9 | 16.1 | 0.4 | 11.3 | 22.9 | 12.9 | 8.2 | |||||||||||||||||||||

| Non-recurring items(iii) |

1.7 | — | 5.1 | 0.4 | 0.4 | 1.5 | 4.5 | |||||||||||||||||||||

| Productivity initiatives(iv) |

7.7 | 6.9 | 8.3 | 16.3 | 3.1 | 1.5 | — | |||||||||||||||||||||

| Multiemployer plan withdrawal(v) |

— | 2.8 | 2.8 | 0.4 | 3.9 | (0.1 | ) | 0.8 | ||||||||||||||||||||

| Other adjustment items(vi) |

5.5 | 2.6 | 4.1 | 3.9 | 5.8 | 8.8 | 3.7 | |||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Adjusted EBITDA |

$ | 251.9 | $ | 226.1 | $ | 328.6 | $ | 286.1 | $ | 271.3 | $ | 240.9 | $ | 220.0 | ||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| (i) | Includes adjustments for non-cash charges arising from employee stock compensation, interest rate swap hedge ineffectiveness, adjustments to reflect certain assets held for sale to their net realizable value, and changes in fair value of fuel collar instruments. Stock compensation cost was $13.6 million and $0.9 million for the first nine months of fiscal 2016 and the first nine months of fiscal 2015, respectively. In addition, this includes a (decrease) increase in the LIFO reserve of $(2.5) million, $(0.4) million, $1.7 million, $3.0 million, and $0.8 million for the first nine months of fiscal 2016, the first nine months of fiscal 2015, fiscal 2015, fiscal 2014, and fiscal 2013, respectively. |

| (ii) | Includes professional fees and other costs related to completed and abandoned acquisitions net of a $25.0 million termination fee related to the terminated agreement to acquire 11 US Foods facilities from Sysco and US Foods, costs of integrating certain of our facilities, facility closing costs, legal fees related to our legal entity reorganization, and advisory fees paid to the Sponsors. For fiscal 2013, this also includes $11.2 million for the impact of the initial fair value of inventory that was acquired as part of acquisitions. |

| (iii) | Consists primarily of an expense related to our withdrawal from a purchasing cooperative, pre-acquisition worker’s compensation claims related to an insurance company that went into liquidation, transition costs related to IT outsourcing, certain severance costs, and the impact of business interruption due to hurricane and other weather related or one-time related events. |

| (iv) | Consists primarily of professional fees and related expenses associated with the Winning Together program and other productivity initiatives. |

| (v) | Includes amounts related to the withdrawal from multiemployer pension plans. For the first nine months of fiscal 2015, fiscal 2015, fiscal 2014 and fiscal 2013, this amount includes $2.8 million, $2.8 million, $0.4 million, and $3.7 million, respectively, for the expense related to the withdrawal from the Central States Southeast and Southwest Areas Pension Fund. See Note 15 Commitments and Contingencies to the audited consolidated financial statements included in this prospectus. |

| (vi) | Consists primarily of costs related to settlements on our fuel collar derivatives, certain financing transactions, lease amendments, and franchise tax expense and other adjustments permitted by our credit agreements. |

15

Table of Contents

Investing in our common stock involves a high degree of risk. You should consider carefully the risks and uncertainties described below and the other information contained in this prospectus, including our consolidated financial statements and the related notes, before you decide whether to purchase our common stock.

Risks Relating to Our Business and Industry

Competition in our industry is intense, and we may not be able to compete successfully.

The foodservice distribution industry is highly competitive. Certain of our competitors have greater financial and other resources than we do. Furthermore, there are two larger broadline distributors, Sysco and US Foods, with national footprints. On December 8, 2013, these competitors entered into an agreement and plan of merger, which was later terminated as described under “Summary—Our Industry.” In addition, there are numerous regional, local, and specialty distributors. These smaller distributors often align themselves with other smaller distributors through purchasing cooperatives and marketing groups to enhance their geographic reach, private label offerings, overall purchasing power, cost efficiencies, and ability to try to meet customer requirements for national or multi-regional distribution. We often do not have exclusive service agreements with our customers and our customers may switch to other distributors if those distributors can offer lower prices, differentiated products, or customer service that is perceived to be superior. We believe that most purchasing decisions in the foodservice business are based on the quality and price of the product and a distributor’s ability to completely and accurately fill orders and provide timely deliveries. We cannot assure you that our current or potential competitors will not provide products or services that are comparable or superior to those provided by us or adapt more quickly than we do to evolving trends or changing market requirements. Accordingly, we cannot assure you that we will be able to compete effectively against current and future competitors, and increased competition may result in price reductions, reduced gross margins, and loss of market share, any of which could materially adversely affect our business, financial condition, or results of operations.

We operate in a low margin industry, which could increase the volatility of our results of operations.

Similar to other resale-based industries, the foodservice distribution industry is characterized by relatively low profit margins. These low profit margins tend to increase the volatility of our reported net income since any decline in our net sales or increase in our costs that is small relative to our total net sales or costs may have a large impact on our net income (loss).

We may not realize anticipated benefits from our cost reduction and productivity improvement efforts, including our Winning Together program.

We have implemented a number of cost reduction and productivity improvement initiatives that we believe are necessary to position our business for future success and growth, including our Winning Together program. Our future success and earnings growth depend upon our ability to achieve a lower cost structure and operate efficiently in the highly competitive foodservice distribution industry, particularly in an environment of increased competitive activity and reduced profitability. A variety of factors could cause us not to realize some of the expected cost savings and productivity enhancements, including, among other things, difficulties in implementation, delays in the anticipated timing of activities related to our cost savings initiatives, lack of sustainability in cost savings over time, and unexpected costs associated with operating our business. If we are unable to realize the anticipated benefits from our cost cutting and productivity improvement efforts, including our Winning Together program, we could become cost disadvantaged in the marketplace, which could adversely affect our competitiveness and our profitability. Furthermore, even if we realize the anticipated benefits of our cost reduction and productivity improvement efforts, we may experience an adverse impact on our employees, customers, suppliers, and purchasing partners that could adversely affect our business, financial condition, or results of operations.

16

Table of Contents

Cost inflation or deflation could affect the value of our inventory and our financial results.

We make a significant portion of our sales at prices that are based on the cost of products we sell, plus a percentage markup. As a result, volatile food costs may have a direct impact upon our profitability. Our profit levels may be negatively affected during periods of product cost deflation, even though our gross profit percentage may remain relatively constant. Prolonged periods of product cost inflation also may have a negative impact on our profit margins and earnings to the extent such product cost increases are not passed on to customers because of their resistance to higher prices. Furthermore, our business model requires us to maintain an inventory of products, and changes in price levels between the time that we acquire inventory from our suppliers and the time we sell the inventory to our customers could lead to unexpected shifts in demand for our products or could require us to sell inventory at a loss. In addition, product cost inflation may negatively impact consumer discretionary spending decisions within our customers’ establishments, which could impact our sales. Our inability to quickly respond to inflationary and deflationary cost pressures could have a material adverse impact on our business, financial condition, or results of operations.

Many of our customers are not obligated to continue purchasing products from us.

Many of our customers buy from us pursuant to individual purchase orders, and we often do not enter into long-term agreements with these customers. Because such customers are not obligated to continue purchasing products from us, we cannot assure you that the volume and/or number of our customers’ purchase orders will remain constant or increase or that we will be able to maintain our existing customer base. Significant decreases in the volume and/or number of our customers’ purchase orders or our inability to retain or grow our current customer base may have a material adverse effect on our business, financial condition, or results of operations.

Group purchasing organizations may become more active in our industry and increase their efforts to add our customers as members of these organizations.

Some of our customers, particularly our larger customers, purchase their products from us through group purchasing organizations, or “GPOs,” in an effort to lower the prices paid by these customers on their foodservice orders, and we have experienced some pricing pressure from these purchasers. These GPOs have recently increased their efforts to include smaller, independent restaurants. If these GPOs are able to add a significant number of our customers as members, we may be forced to lower the prices we charge these customers in order to retain the business, which would negatively affect our business, financial condition, or results of operations. Additionally, if we were unable or unwilling to lower the prices we charge for our products to a level that was satisfactory to the GPOs, we may lose the business of those of our customers that are members of these organizations, which could have a material adverse impact on our business, financial condition, or results of operations

Changes in consumer eating habits could materially and adversely affect our business, financial condition, or results of operations.

Changes in consumer eating habits (such as a decline in consuming food away from home, a decline in portion sizes, or a shift in preferences toward restaurants that are not our customers) could reduce demand for our products. Consumer eating habits could be affected by a number of factors, including changes in attitudes regarding diet and health or new information regarding the health effects of consuming certain foods. If consumer eating habits change significantly, we may be required to modify or discontinue sales of certain items in our product portfolio, and we may experience higher costs associated with the implementation of those changes. Changing consumer eating habits may reduce the frequency with which consumers purchase meals outside of the home. Additionally, changes in consumer eating habits may result in the enactment of laws and regulations that impact the ingredients and nutritional content of our food products, or laws and regulations requiring us to disclose the nutritional content of our food products. Compliance with these laws and regulations, as well as others regarding the ingredients and nutritional content of our food products, may be costly and time-

17

Table of Contents

consuming. We cannot make any assurances regarding our ability to effectively respond to changes in consumer health perceptions or resulting new laws or regulations or to adapt our menu offerings to trends in eating habits.