UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM

(Mark One)

For

the fiscal year ended

or

For the transition period from _____ to _____

COMMISSION

FILE NUMBER:

(Exact name of registrant as specified in its charter)

(State or other jurisdiction of incorporation or organization) |

(I.R.S. Employer Identification Number) |

(Address, including zip code, of principal executive offices

and telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Exchange Act:

| Title of each class | Trading Symbol | Name of each exchange on which registered | ||

Securities registered under Section 12(g) of the Exchange Act: None

Indicate

by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐

Indicate

by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Exchange Act. Yes ☐

Indicate

by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Exchange Act during

the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject

to such filing requirements for the past 90 days.

Indicate

by check mark whether the registrant has submitted electronically every Interactive Date File required to be submitted pursuant to Rule

405 of Regulation S-T (Section 232.405 of the chapter) during the preceding 12 months (or for such shorter period that the registrant

was required to submit such files).

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ☐ | ☒ | |

| Non-accelerated filer | ☐ | Smaller reporting company | |

| Emerging growth company | |||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate

by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness

of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered

public accounting firm that prepared or issued its audit report.

If

securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant

included in the filing reflect the correction of an error to previously issued financial statements.

Indicate

by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation

received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b).

Indicate

by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ☐ No

The

aggregate market value of the registrant’s common stock, other than shares held by persons who may be deemed to be affiliates of

the registrant, computed by reference to the closing sales price for the registrant’s common stock on June 30, 2024, the last business

day of the registrant’s most recently completed second fiscal quarter, as reported on the Nasdaq Capital Market, was approximately

$

As of March 26, 2025, there were shares of the registrant’s common stock, par value $ per share, outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

TABLE OF CONTENTS

| i |

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

Certain statements and other information set forth in this Annual Report on Form 10-K (this “Report”), including in Item 7, “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and elsewhere herein, may relate to future events and expectations, and as such constitute “forward-looking statements” within the meaning of Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”), and Section 27A of the Securities Act of 1933, as amended (the “Securities Act”). Our forward-looking statements include, but are not limited to, statements regarding our business strategy, plans and objectives and our expected or contemplated future operations, results, financial condition, beliefs and intentions. In addition, any statements that refer to projections, forecasts or other characterizations or predictions of future events or circumstances, including any underlying assumptions on which such statements are expressly or implicitly based, are forward-looking statements. The words “anticipate,” “believe,” “continue,” “can,” “could,” “estimate,” “expect,” “intend,” “may,” “might,” “plan,” “possible,” “potential,” “predict,” “project,” “scheduled,” “seek,” “should,” “would” and similar expressions, among others, and negatives expressions including such words, may identify forward-looking statements.

Our forward-looking statements reflect our current expectations about our future results, performance, liquidity, financial condition, prospects and opportunities, and are based upon information currently available to us, our interpretation of what we believe to be significant factors affecting our business and many assumptions regarding future events. Actual results, performance, liquidity, financial condition, prospects and opportunities could differ materially from those expressed in, or implied by, our forward-looking statements. This could occur as a result of various risks and uncertainties, including the following:

| ● | government regulation of our industries; | |

| ● | our ability to compete effectively in our industries; | |

| ● | the effect of evolving technologies on our business; | |

| ● | our ability to renew long-term contracts and retain customers, and secure new contracts and customers; | |

| ● | our ability to maintain relationships with suppliers; | |

| ● | our ability to protect our intellectual property; | |

| ● | our ability to protect our business against cybersecurity threats; | |

| ● | our ability to successfully grow by acquisition as well as organically; | |

| ● | fluctuations due to seasonality; | |

| ● | our ability to attract and retain key members of our management team; | |

| ● | our need for working capital; | |

| ● | our ability to secure capital for growth and expansion; | |

| ● | changing consumer, technology and other trends in our industries; | |

| ● | our ability to successfully operate across multiple jurisdictions and markets around the world; | |

| ● | changes in local, regional and global economic, regulatory and political conditions; and | |

| ● | other factors described in the reports and documents we file from time to time with the U.S. Securities and Exchange Commission (the “SEC”). |

In light of these risks and uncertainties, and others discussed in this report, there can be no assurance that any matters covered by our forward-looking statements will develop as predicted, expected or implied. Readers should not place undue reliance on any forward-looking statements. Except as expressly required by the federal securities laws, we undertake no obligation to publicly update or revise any forward-looking statements, whether as a result of new information, future events, changed circumstances or any other reason. We advise you to carefully review the reports and documents we file from time to time with the SEC.

| ii |

PART I

ITEM 1. BUSINESS.

Overview

Inspired Entertainment, Inc. (the “Company”, “Inspired”, “we” or “us”) is a global gaming technology company, supplying content, platform and other products and services to licensed online and land-based lottery, betting and gaming operators worldwide through a broad range of distribution channels, predominantly on a business-to-business basis. We provide end-to-end digital gaming solutions (i) on our own proprietary and secure network, which accommodates a wide range of devices, including land-based gaming machine terminals, mobile devices and online computer applications and (ii) through third party networks. Our content and other products can be found through the consumer-facing portals of our customers operating digital channels, and, in licensed betting offices, adult gaming centers, pubs, bingo halls, airports, motorway service areas and leisure parks for our customers operating land-based venues.

Our customer base includes licensed operators of lotteries, licensed sports bookmakers, gaming and bingo halls, casinos, online operators, adult gaming centers, pubs, holiday parks, and motorway service areas. Some of our key customers include William Hill, SNAI, Sisal, Betfred, Paddy Power, Betfair, Genting, bet365, Sky Bet, the Greek Organisation of Football Prognostics S.A. (OPAP.), Entain, Draftkings, FanDuel, the Pennsylvania Lottery, Bourne Leisure, Greentube, Stonegate, Mitchells & Butler, Butlins, Moto, Welcome Break, Buzz Bingo, Mecca, Marstons, Greene King, JD Wetherspoon, Parkdean Resort, Centre Parcs Resorts, and Novomatic. Geographically, 73% of our revenue for the year ended December 31, 2024 was generated from our United Kingdom (“UK”) operations, with the remainder generated from Greece, North America and the rest of the world. Our products are designed to operate within applicable gaming, virtual sports and lottery regulations.

We conduct business across different jurisdictions, of which Great Britain, Italy and Greece have historically contributed the most significant recurring revenue. Since 2021, we have begun to conduct a meaningful amount of business in regulated North American markets and states. We are licensed or certified (as applicable) by the Gambling Commission in the UK, (the “UK Gambling Commission”), the Hellenic Gaming Commission in Greece, and registered with L’Agenzia delle Dogane e dei Monopoli (“ADM”) in Italy. We are licensed by regulators in other jurisdictions such as the Malta Gaming Authority (Malta), the Licensing Authority of Gibraltar (Gibraltar), the Alderney Gambling Control Commission (Channel Islands), the Belgian Kansspel Commissie (Belgium), Oficiul National pentru Jocuri de Noroc, Spelinspektionen (Romania), the Swedish Gaming Authority (Sweden) and we hold licenses with the U.S. states of Connecticut, Illinois, Michigan, Delaware, New Jersey, Oregon, Pennsylvania, and West Virginia, and the Canadian provinces of Alberta, Nova Scotia, Manitoba, Quebec, Ontario and Saskatchewan.

We are headquartered in the U.S., with principal operating facilities located in the UK and India. As of December 31, 2024, we had approximately 1,600 employees, approximately 1,420 of which were full-time. We generated total revenue of $297.1 million and adjusted earnings before interest, taxes, depreciation and amortization (“Adjusted EBITDA”) of $100.1 million for the year ended December 31, 2024.

The Company’s common stock is listed on the NASDAQ Capital Market under the symbol INSE. The Company had an equity market capitalization of approximately $240.6 million as of December 31, 2024 (based upon a closing stock price of $9.05 on December 31, 2024).

The Company uses the British Pound as its functional currency for reporting purposes. Our results are affected by changes in foreign currency exchange rates as a result of the translation of foreign functional currencies into our reporting currency and the re-measurement of foreign currency transactions and balances. The impact of foreign currency exchange rate fluctuations represents the difference between current rates and prior-period rates applied to current activity. The geographic region in which the largest portion of our business is operated is the UK and the British pound (“GBP”) is considered to be our functional currency. Our reporting currency is the U.S. dollar (“USD”). Our results are translated from our functional currency of GBP into the reporting currency of USD using average rates for profit and loss transactions and applicable spot rates for period-end balances. The effect of translating our functional currency into our reporting currency, as well as translating the results of foreign subsidiaries that have a different functional currency into our functional currency, is reported separately in Accumulated Other Comprehensive Income

Certain product and company names referred to herein are trademarks™ or registered® trademarks of their respective holders.

Our Products

We operate in four business segments: Gaming, Virtual Sports, Interactive and Leisure, as further described below.

| 1 |

Gaming Segment

Our Gaming segment supplies gaming terminals as well as gaming software and games for the terminals provided to Licensed Betting Offices (“LBOs”), casinos, gaming halls and adult gaming centers (“AGCs”). It supplies products and utilizes our Server Based Gaming (“SBG”) technology to supply gaming content to our customers’ global land-based gaming venues. SBG products offer an extensive portfolio of games through digital terminals. Our games are currently deployed through more than 34,000 terminals. Because our SBG products are fully digital, they interact with a central server and are provided on a “distributed” basis, which allows us to access a wide geographic footprint through the internet, the Company’s, and third parties’ proprietary networks.

Our SBG game portfolio includes a broad selection of popular omni-channel slots titles including Gold Cash Free Spins™, Big Fishing Fortune™, and the Reel King ® family of games, offering a premium player experience across multiple platforms. These games offer users a wide range of volatilities, return-to-player and other special features. We also offer a range of more traditional casino games through our SBG network, such as roulette, blackjack and numbers games.

We distribute games to devices through different game management systems (“GMS”), each tailored to a specific operator or sector. Our CORE™ GMS is designed for distributed street-gaming sectors and uses Inspired cabinets in combination with gaming content from Inspired, as well as a wide portfolio of content from independent game developers. CORE-CONNECT is our American Gaming Association G2S standard-based video lottery terminal (“VLT”) GMS, currently deployed in the Greek VLT sector and North America. Our SBG products comply with all requirements in the UK (B2/B3), Italy (6B), Greece (G2S) and Illinois (G2S).

Our SBG terminals in the UK account for a material portion of all SBG terminal placements, and we offer over 100 games for play across this portfolio. We are also a material supplier to customers in Greece and Italy. Over the past few years, we have grown our business in North America where we have sold products in Illinois, the Western Canada Lottery Corporation (“WCLC”) and Alberta Gaming Liquor & Cannabis Commission (“AGLC”). We offer SBG terminals such as the Flex4k curved screen, Vantage ®, Eclipse™, Valor™, Prismatic™ and Sabre Hydra™, each offering a different size terminal, graphics, technology and price proposition.

As of December 31, 2024, we had a total installed base of 34,900 gaming terminals, which were operated primarily under participation-based contracts. We generate revenue by participating, typically as a function of gross revenue from each machine, as a percentage of the revenue generated by these machines. Because we participate in our customers’ revenue under such contracts, we and our customers benefit from the introduction of our new content, which can drive growth for our installed base. Additionally, we earn revenue through the sale of terminal units, as well as receiving a fixed daily fee for some of our installed units. During 2024, we sold 3,091 units, which are down on last year by over 6,000 terminals due to the refresh of Vantage terminals into two of our major customers in the UK LBO sector in 2023. Of the 2024 sales, 67% were in the UK and 33% came from North America. With our participation-driven business model, approximately 96% of service revenue for our Gaming segment was recurring in nature in 2024 and derived under long-term contracts.

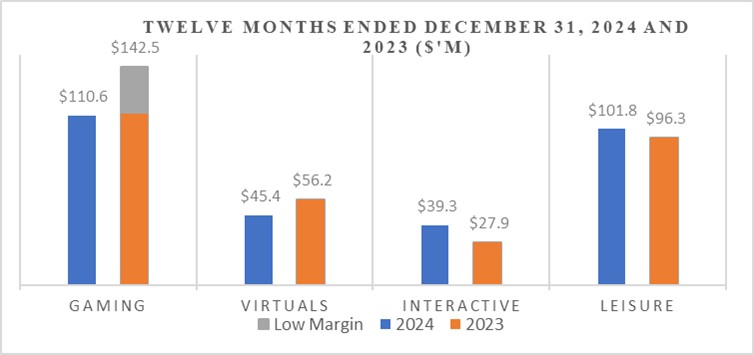

For the year ended December 31, 2024, our Gaming segment generated revenue and Adjusted EBITDA of $110.6 million and $45.3 million, respectively, as compared to the year ended December 31, 2023, during which we generated $142.5 million and $42.8 million in revenue and Adjusted EBITDA, respectively. Revenue in 2024 reduced versus prior year due to significant one-off low margin sales in 2023 of c.$30.6 million. These sales related to approximately 6,400 LBO Vantage terminals which formed part of long-term contract renewals with Betfred and Paddy Power.

Virtual Sports Segment

Our Virtual Sports business designs, develops, markets and distributes games that create an always-on sports wagering experience in betting shops and other locations and online. Our Virtual Sports product comprises a complex software and networking package that provides fixed-odds wagering on an ultra-high definition, computer-rendered simulations of sporting events, such as soccer, football or basketball. This product enables players to place bets on simulated sporting events, without being bound to live event schedules. We have developed this technology using advanced motion capture techniques and a TV and film graphics team to create highly realistic simulations.

We believe we are among the most innovative suppliers of Virtual Sports gaming products worldwide. Our diverse portfolio of sports and numbers-based games is available in approximately 30,000 retail venues and through multiple online platforms. We have operations across 20+ gaming jurisdictions worldwide, including the UK, Italy, Greece, Turkey, Morocco, and the U.S.

| 2 |

Our Virtual Sports portfolio includes titles such as V-Play Soccer™, V-Play Women’s Soccer™, V-Play Football™, V-Play Basketball™, and V-Play Baseball™, along with greyhound racing, horse racing, tennis, motor racing, cycling, cricket, speedway, golf and darts. Furthermore, we have licensing agreements for the use of sports brands, and associated marks or trade-dress archival footage, or a combination of the foregoing, including a partnership with the National Basketball Association (“NBA”), the National Hockey League (“NHL”), Major League Baseball Players Alumni Association (“MLBPAA”) and, pursuant to our licensing arrangements with Aristocrat Gaming, the National Football League (“NFL”).

Our customers include some of the largest operators in lottery, gaming and sports betting globally. We are contracted to supply Virtual Sports to mobile and online operators across key regulated markets, including the United Kingdom; the U.S. states of Nevada, Pennsylvania, New Jersey, and the District of Columbia; Gibraltar and other regulated markets in Europe, including Italy, Greece and Poland. We also supply customers based in Ontario, Turkey and Morocco. Our technology is adaptable to sports betting, lottery, and gaming environments, making it accessible to a wide range of customers in both public and private sectors.

Our Virtual Sports events are available to millions of customers worldwide, through retail, online and mobile platforms, many of which are available 24/7. We offer multiple hosting solutions tailored to customer needs, including our proprietary Virtual Plug and Play (“VPP”) turnkey solution for online and mobile platforms. Additionally, our cloud-based XML sportsbook integration enables fully hosted and managed Virtual Sports solutions for customers seeking seamless product delivery.

Our Virtual Sports products are typically offered to operators on a participation-based revenue model, where we receive a share of the gaming revenue generated, along with an upfront software licensing fee, hosting fees, or a combination of the foregoing. Due to this recurring revenue model, approximately 97% of the total Virtual Sports segment revenue is generated under long to medium-term contracts, with a standard contract duration of three years.

For the year ended December 31, 2024, our Virtual Sports segment generated revenue and Adjusted EBITDA of $45.4 million and $36.0 million, respectively, as compared to the year ended December 31, 2023, during which we generated $56.2 million and $47.6 million in revenue and Adjusted EBITDA, respectively. Revenue in 2024 compared to the prior year is primarily affected by our exposure to a single customer in a particular geography, where revenues have consistently declined throughout the year. This decline is mainly due to the customer pulling back on promotions with virtual sports customers. However, we anticipate this trend will improve as we diversify our customer base, market reach and expand our delivery channels, with several opportunities in the pipeline. During 2024 we consolidated the Virtual Sports product and technical function, that had previously been separate, into the company-wide product and technical group to enhance our ability to take advantage of these opportunities.

Interactive Segment

Our Interactive business uses unique interactive-only content as well as offerings from our Gaming and Virtual Sports segments to create games that are hosted on remote gaming servers. This allows online gaming operators to use our games and content online and on mobile devices worldwide.

Our interactive content includes a wide range of random number generated casino content from feature-rich bonus games to European-style casino free spins and table games incorporating well-known first and third-party brands including Space Invaders®, 20p Roulette™, Super Hot Fruits® and Reel King Megaways™. Inspired releases several new titles per month and new games can be seamlessly deployed to the full estate of operators and aggregators through its proprietary Virgo RGS™. Games are available on over 300 websites across much of regulated Europe and North American territories in the form of New Jersey, Michigan, Pennsylvania, Connecticut, Alberta, Ontario and Quebec. Other prominent territories the segment operates in outside of these include the markets of Brazil and Mexico.

Inspired’s Virgo Remote Gaming System (“RGS™”) is integrated with a number of leading casino brands, including William Hill, Entain, bet365, Flutter, 888, Kindred, Gamesys, Betfred, Rank, Leo Vegas, OPAP, Kaizen, Betano and Stoiximan. We are also live with a number of notable North American operators: Bet MGM, Draft Kings, Caesars, FanDuel, Rush Street Interactive, Golden Nugget and Loto Quebec in Canada.

We have launched our Hybrid Dealer® product which is a new product category for the segment and offers players branded casino and gameshow content without the challenges associated with live-dealer products. This product category was live with BetMGM in 2024, and there is a clear expansion plan as we enter 2025 to roll the product out to an increased number of the Inspired customer base.

| 3 |

Our Interactive products are typically offered to operators on a participation basis, whereby we typically receive a percentage of net gaming revenue generated by the interactive content. For the year ended December 31, 2024, our Interactive segment generated revenue and Adjusted EBITDA of $39.3 million and $25.6 million, respectively, as compared to the year ended December 31, 2023, during which we generated revenue and Adjusted EBITDA of $27.9 million and $15.4 million, respectively. With our participation-driven business model, approximately 100% of revenue for our Interactive segment is recurring in nature and derived under long-term contracts for which our standard term is three years in duration. We have successfully renewed all of our key Interactive contracts expiring over the last three years. EBITDA margins in this segment remain steady and growing due to the low variable costs we expect to incur on incremental revenue, versus our existing base of revenue, but with additional pressures due to new taxes levied in newly regulated markets such as Brazil, where taxes on gross gaming revenue came into force on January 1, 2025 together with withholding taxes on revenue due to licensees being based locally, or in more mature markets such as UK where mandatory levies based on a gross gambling yield (“GGY”) have been introduced as contributions towards the study, prevention and treatment of gambling related harm and/or other measures are to be introduced such as online stake limits.

Leisure Segment

We are a supplier of gaming terminals and amusement machines to the Leisure and Hospitality sectors and are one of the largest operators of “pay to play” gaming terminals and amusement machines in the UK. As of December 31, 2024, we supplied and operated over 10,000 gaming terminals and 3,500 pool tables, prize vending and jukeboxes located in pubs, bingo halls, and adult gaming centers. We also service approximately 2,800 gaming terminals under maintenance only contracts. The increasing majority of gaming terminals we operate are server based, allowing us to distribute content supplied by our “in house” design studios as well as some of the most popular content titles from our strategic partners.

In addition, we also supply and operate approximately 8,000 amusement machines and 1,400 gaming terminals in family entertainment centers and adult gaming centers located in holiday parks, bowling centers and other entertainment venues. These include virtual reality simulators and arcade games, redemption and skill with prize games, basketball, air hockey and cue sports. Commercial arrangements are typically structured as either revenue participation or rental agreements.

Our customers in this segment include large pub operators JD Wetherspoons, Stonegate Pub Company, Greene King, Mitchells and Butler, Whitbread Marstons and Admiral Taverns. In the Bingo sector, we supply gaming terminals and services to Buzz Bingo and Mecca. We supply gaming terminals and services to transport hub operators, Moto and Welcome Break and major airports, including Heathrow. We also operate our own adult gaming centers under the Quicksilver™ brand in Extra Motorway Services. We have joint venture agreements with holiday park operators including Parkdean Resorts, Bourne Leisure (Haven), Butlins and Cove, where we supply machines and trained staff to manage and operate family entertainment centers.

Overall, our Leisure segment had, as of December 31, 2024, an installed base of over 10,000 gaming terminals, which were operated primarily under participation-based contracts. We generate revenue by participating, typically as a function of gross revenue from each machine, in a percentage of volumes generated by these machines. Because we participate in our customers’ revenue under such contracts, we are aligned with our customers in benefiting from the introduction of our new content, which can drive growth in the win per unit per day of our installed base. Additionally, we earn revenue through the sale of units, as well as a fixed daily fee for certain of our installed units. With our participation-driven business model, approximately 97% of revenue for our Leisure segment is recurring in nature and derived under long-term contracts. We installed over six hundred Vantage Cat C cabinets to our Pubs estate during the year and we have successfully renewed or extended contracts with Moto Hospitality, Park Dean Resorts, Buzz Bingo and Mecca Bingo.

For the year ended December 31, 2024, our Leisure segment generated revenue and Adjusted EBITDA of $101.8 million and $23.3 million respectively, as compared to the year ended December 31, 2023, during which we generated revenue and Adjusted EBITDA of $96.3 million and $19.4 million, respectively.

Our Strengths

We believe key factors that give us an advantage in the gaming technology space include:

| 4 |

Established presence across multiple Product Verticals

We have a substantial installed base, including over 32,000 digital terminals in the Gaming segment located across key jurisdictions in the UK, Greece and Italy, with approximately 12,800 terminals installed in UK Licensed Betting Offices and approximately 8,700 terminals installed in Greek venues. In our Leisure segment, we supply and operate an installed base of approximately 11,000 gaming terminals (including approximately 2,800 gaming terminals under maintenance only contracts) and 4,500 pool tables, prize vending and jukeboxes to pubs, bingo halls and adult gaming centers. In addition, we also supply and operate approximately 9,500 amusement machines and 2,200 gaming terminals in family entertainment centers located in holiday parks, bowling centers and other entertainment venues. We have content and products in our Virtual Sports segment, which offers a wide range of sports and numbers games through approximately 32,000 retail venues as well as through various online channels. Our Virtual Sports gaming products are available in approximately 32 gaming jurisdictions worldwide, including the UK, Italy, Greece, Morocco and the U.S., our customers being many of the largest operators of lottery, gaming, and betting operations worldwide. Additionally, our Interactive segment provides a wide range of iGaming content to large operators primarily marketing to customers located in the UK, Italy, Greece and North America, as well as several other regulated countries across Europe through over approximately 250 websites.

Highly Diversified Business Underpinned by Longstanding Customer Relationships

We operate in several business segments and geographic locations that provide a diversified revenue and cash flow stream that has proven to be resilient under various economic environments. While our Gaming segment has represented the largest proportion of our revenue in each of the last three years, our Interactive segment represents substantial growth opportunities in the digital and retail space, which is expected to continue to diversify our business, together with Virtual Sports in Latin America. Additionally, we continue to expand in high growth markets, such as North America, which are expected to drive further geographic diversification across business segments. We have over 700 customers, including major lottery, sports betting and gaming operators (both interactive and location-based) within regulated sectors worldwide. Many of our customer relationships in the UK and European sectors are long-standing and in excess of 10 years. We expect that our diverse customer base will afford us opportunities to sell incremental products to certain of these customers in the future.

Substantial Recurring Revenue Supported by Long-Term Participation-Based Contracts

We believe our robust recurring revenue business model will drive our performance and free cash flow generation. For the year ended December 31, 2024, our recurring revenue, which included revenue generated from participation-based contracts and licensing arrangements, represented 86% of total revenue, as compared to approximately 79% of total revenue for the year ended December 31, 2023. Our content and products, which are provided primarily pursuant to long-term contracts, are essential to generating revenue for our customers and satisfying the demand of our end users. Our long-term contracts typically have an initial duration of three to five years depending on the business segment and the customer and, over the last three years, we have successfully renewed the significant majority of expiring contracts with key customers in our Gaming, Virtual Sports, Interactive and Leisure segments.

Proprietary Technology and Track-Record of Strong Content Development

We are dedicated to being at the forefront of our industry in terms of technology and innovation. We combine complementary expertise in technology and operations, positioning us as a provider of superior content and technical solutions. As of December 31, 2024, we held approximately 25 patents or patent applications and approximately 300 trademarks worldwide. We focus our product development efforts on emerging content and technology trends, utilizing a combination of customer research, design experience and engineering excellence. We are committed to developing innovative products for our customers and are focused on improving player entertainment and customer profitability.

We believe convergence trends in the gaming industry emphasize the importance of proprietary content, including licensed content. Such content is needed to successfully promote a compelling game offering across multiple platforms and to develop distinctive products for operator-clients. Our proprietary content drives engagement across gaming platforms. Our full suite of high-quality gaming products, services and multichannel distribution capabilities, extensive traditional content library, sizeable installed gaming machine base and deep relationships with operator-customers help make us an attractive partner for potential licensors of branded content.

| 5 |

Our Interactive business has expanded rapidly, with revenue growing at an approximate compound annual growth rate of 53% on a functional currency at constant rate basis between 2019 and 2024. We believe this growth has been driven, in part, by our content library of over 100 slot games. Many of our recent game launches, including Gold Cash Free Spins™, Big Fishing Fortune™, and the Reel King ® family of games, have been omni-channel, offering a premium player experience across multiple platforms – though, unlike our older games, they originated online and, once proved successful, were migrated to retail platforms.

Our Virtual Sports products offer a wide range of betting markets and what we consider to be superior graphics. Our Virtual Sports revenue has achieved high EBITDA margins, while providing an attractive recurring revenue base.

Positioned To Benefit From Key Market Trends

With our proprietary digital gaming platform and content comprising an end-to-end product offering and our multi-channel capabilities and robust relationships across the client spectrum, we believe we are well-positioned to benefit from emerging gaming sector trends, including growth stimulated by liberalization of government gaming regulations, the emergence of multi-channel offerings and the increasing importance of proprietary content.

Our multi-channel offerings are well-positioned to benefit from the prevalence of smart phones and tablets and the legalization of online gaming in certain parts of the United States, Canada, Brazil, LATAM more generally and other jurisdictions. Such jurisdictions have provided new growth opportunities for gaming, interactive, sports and lottery operators through the introduction of new channels and portals for delivering games and content to customers. This supplements the existing broad-based online gambling market across Europe. Our multi-channel solutions and customer relationship management capabilities position us to take advantage of new opportunities to extend our gaming solutions across different channels for our customers to reach new players, expand the player demographic base and access players wherever they are whenever they want to play. Our technology extends engagement for existing players and has the capability to reach new player segments. This and other technology help position us for future online real-money gaming opportunities by offering play-for-fun online gaming options in jurisdictions where online real-money gaming may be legalized in the future.

Government initiatives, such as the legalization of casino operations in new jurisdictions, increases in the number of casinos allowed to operate in a given jurisdiction and the legalization of new products, have helped stimulate growth in the gaming market. In the United States, legislative change has led to an increase in the legalization of sports betting or online gaming As of December 31, 2024 online casinos are legal in eight (8) states after Rhode Island went live on March 5, 2024 and several other states have proposed bills for regulation.

Experienced Management Team

Our seasoned management team is led by our Executive Chairman, Lorne Weil, who is known as a gaming industry innovator and whose past leadership includes growing a diversified global gaming technology company both organically and through extensive acquisitions and joint ventures further bolstering the business. In addition to Mr. Weil, who is our principal executive officer, our management team includes Brooks H. Pierce, our President and Chief Executive Officer; James Richardson, our Chief Financial Officer; and Simona Camilleri, our Executive Vice President and General Counsel. The current structure replaces our prior Office of the Executive Chairman. Our management team has broad and deep experience in the gaming industry, working with lotteries, casino operators, betting and gaming platforms, content suppliers and online operators. The members of the management team between them have decades of experience in the gaming industry, including relationships with suppliers and customers around the world, helping them build and sustain revenue growth and achieve strategic objectives.

| 6 |

Our Strategy

We seek to deliver innovative and differentiated products that provide value to our customers and exciting experiences to their players in multiple jurisdictions throughout the world while achieving long-term growth in revenue, profit and cash flow. We place great emphasis on developing creative and wide-ranging solutions, in terms of digital content and play that deliver and sustain superior performance through operators across online, mobile and location-based channels. Our technology often allows us to update our games and operating software remotely, keeping pace with evolving customer and regulatory requirements affecting game software, security, features, reporting, interoperability and in-built technology. We seek to achieve these goals as we:

Extend our positions in each of the sectors in which we operate by developing new content and products which can often be utilized across multiple distribution channels.

We continually invest in new content and product development and delivery channels in each of the business segments in which we operate, believing these to benefit our existing and prospective customers. Our approach seeks to distribute our content across a wide range of channels, sectors, protocols and regulatory standards, on a cost-efficient basis. We have continued to focus on channels where we believe there is considerable growth available – especially in our digital businesses. We believe our technological approach allows us to quickly adapt to changes in player preferences and trends, and to comply with applicable laws.

Continue to invest in content, technology and delivery channels in order to grow our existing customers’ revenue and penetrate new customers in our existing markets.

Over the last few years, a substantial portion of our annual revenue has been recurring and based on long-term contracts with customers, where our revenue typically grows in line with the growth of our customers’ gaming revenue from our content and products. We seek to work closely with our customers to assist in the optimization of their operations so they can achieve growth in their revenue generated by our content and products, which we believe is to our benefit. Accordingly, we continually invest in new content and technology offerings that permit our customers to keep their offerings fresh, offering their players new forms of entertainment. As our content demonstrates successful commercial results, we seek to place it with additional customers who may recognize its value and performance. We believe content development is a key aspect of our overall strategy and we intend to continue this strategic priority for each of the business segments in which we operate.

Add new customers, or extend our collaboration with existing customers, by expanding into new markets.

We believe our historical growth has been driven by our entry into new geographies and supplemented by increasing our share in existing markets. We expect to continue to focus on North and South American markets in the Gaming, Virtual Sports, Lottery and Interactive segments where room for such expansion may exist and where regulations allow. We believe North America is a valuable gaming market in which we currently have more limited participation and a lower market share, but where we expect our products can be positioned for future success. Effective January 1, 2025, Brazil has launched its newly regulated market and we believe that we are well-positioned to continue to pursue our strategy there including the roll out of localized content offerings in Hybrid Dealer, Interactive and Virtual Sports segments in Brazil, and other segments should these become regulated. We also believe there may be further growth opportunities in Latin America which will be available to us in the future, as new regulations permit.

Pursue targeted mergers and acquisitions to expand our product portfolio and distribution footprint.

In addition to growing our business organically, we have pursued, and continue to pursue, merger and acquisition opportunities that we believe will help strengthen and scale our operations and take further advantage of our competitive position. Our management team shares a combination of operating, investing, financial and transactional experience that we believe will serve the Company well as it seeks to identify opportunities for value-adding acquisitions to negotiate and close on potential acquisition transactions.

| 7 |

Industry Overview

We operate within the global gaming and lottery industry. Global gaming and lottery growth has been resilient in the face of economic cycles over the last decade. According to the H2 Database, the global gaming and lottery industry has grown at an estimated 4% compounded annual growth rate from 2014 to 2024.

During this period, the digital online and mobile gaming and lottery sectors have grown at a faster pace than the industry as a whole. According to the H2 Database, these industry sectors have grown at an estimated 17% compounded annual growth rate from 2014 to 2024, driven by rapid growth in the deployment of digital games and technologies, including many of our products, into land-based venues in the primary sectors in which we operate, where regulators have supported the transition to digital, online and retail channels. According to the H2 Database, the total global gaming and lottery industry is projected to grow an average of 6% per year from 2024 to 2029 driven by the projected growth in mobile and online gaming.

As a gaming and lottery business-to-business supplier focused on digital products and technologies, we believe we are well positioned to benefit from the broader global digital and mobile trends further described below.

Influencers of Digital Adoption

We believe the digital segment of the global gaming and lottery industry will continue to grow, including as a result of the following factors:

Governments: Opening of new gaming territories. Many national and state governments operating in developed economies in Europe, LATAM and North America are suffering from structural funding deficits in a post – COVID environment or dealing with a large influx of unregulated gaming offerings usually offered through offshore and remote means. The regulation and taxation of gaming and lottery may be relied upon to raise new sources of revenue for these governments. In some cases, liberalization may favor buildouts of large new destination resort casinos, but in others, regulation may rather focus on smaller distributed gaming (“EDGE”) venues with lottery, gaming and sports betting, combined with remote gaming.

Digital Multi-Channel Offerings: Replacement of legacy analog machines with larger volume of smart digital devices, both interactive and location based. As existing gaming sectors mature, governments and regulatory authorities have implemented regulations to upgrade the established terminal base to digital operation.

Smartphones and Mobile Devices: Rapid adoption of gaming and lottery applications on growing volume focus on smaller distributed gaming (“EDGE”) venues with lottery, gaming and sports betting, combined with online or mobile gaming and betting.

In certain sectors, mobile play on sports betting and gaming now exceeds such play on personal computers. According to the H2 Database, mobile gaming revenue in such sectors exhibited a 27.0% compound annual growth rate between 2010 and 2021. Mobile gaming and lottery are now expanding in other sectors, and mobile play has recently been approved in other sectors for gaming or lottery.

We believe there are significant benefits for our customers in adopting digitally networked gaming and lottery technologies. We believe our digitally-enabled products allow operators to remotely manage their operations with minimal disruption to their businesses. The system centralization enabled by digital operations offers flexibility to rotate or change games, tailor game availability to time-of-day, target specific player demographics and take advantage of seasonal and themed marketing opportunities. New games often can be phased in without the interim revenue declines often associated with replacing games on traditional lottery terminals or slot machines. In addition, digital operations permit more games per terminal, enabling operators to test new games and new suppliers, seek to appeal to a broader base of players with minimal cost or risk, commission games from third-party suppliers on an open game interface and reduce procurement risk. Moreover, digital operations can significantly reduce the need for on-site repairs, improve terminal up-time and should extend terminal life cycles as well as the time period over which capital costs can be depreciated.

| 8 |

Regulatory Framework

We conduct business in a number of different jurisdictions, of which Great Britain, Italy and Greece have historically contributed the most significant recurring revenue. The gaming regulator responsible for our activities in Great Britain is the Gambling Commission. In Italy, the operation of gaming machines and remote gaming is regulated by L’Agenzia delle dogane e dei Monopoli (“ADM”). In Greece, the operation of gaming machines and remote gaming is regulated by the Hellenic Gaming Commission. In addition, we are licensed or certified (as applicable) in a number of other jurisdictions by regulators such as the Malta Gaming Authority, His Majesty’s Government Gibraltar, the Alderney Gambling Control Commission, the Belgian Kansspel Commissie, Romania – Oficiul National pentru Jocuri de Noroc, Autorité Des Marchés Financiers (Quebec), Nova Scotia Alcohol, Gaming, Fuel and Tomabbo Division, Saskatchewan Liquor and Gaming Authority, Alcohol and Gaming Commission (Ontario), Ministerio de Comercio Exterior y Turismo (MINCETEUR) in Peru and state regulators in various jurisdictions in North America such as New Jersey, Pennsylvania, Michigan, Illinois and others.

Great Britain

In the British sector, we supply and distribute Category B3 gaming machines (with maximum betting stakes for players of £2), Category C gaming machines, Category D gaming machines and ETG machines to third parties who are licensed to operate such machines in bricks-and-mortar premises. In addition, we operate a number of Adult Entertainment Centers. We also supply virtual sports software to local retail venues and to online operators who are licensed to target the British sector. We also supply our Interactive product to remote operators who are licensed to target the British sector. The provision of our products and services in relation to the British sector is authorized by a multi-category operating license issued by the UK Gambling Commission, namely remote and non-remote Gaming Machine Technical (Full) operating licenses, a remote casino operating license, a remote and non-remote gambling software license and a remote general betting standard (virtual events) license gaming machine general adult gaming center license and a gaming machine general family entertainment center license.

British Betting and Gaming Laws and Regulations. The Gambling Act 2005 (the “GA05”) is the principal legislation in Great Britain governing gambling (other than in relation to the National Lottery, which is governed by separate legislation). The GA05 applies to both land-based gambling (referred to as “non-remote” gambling) and online and mobile gambling (referred to as “remote” gambling).

The GA05 provides that it is an offense to make a gaming machine available for use without an appropriate operating license. There are a number of different categories of licensable gaming machines (the GA05 provides for category A to D machines, although no category A machines are currently in operation); each category is subject to different levels of maximum stakes and prize limits. In addition, there are limits on the numbers and types of gaming machines that can be operated from licensed premises: for example, a licensed betting office is permitted to house up to four category B3 to D machines, while a large casino may house up to 150 category B to D machines (subject to satisfying certain ratios of machines to gaming tables).

Gaming machine suppliers are required to hold an operating license in order to manufacture, supply, install, adapt, maintain or repair a gaming machine or part of a gaming machine. Gaming machine suppliers must also comply with the Gaming Machine Technical Standards published by the Gambling Commission in relation to each category of machine, and such machines must meet the appropriate testing requirements.

In relation to remote gambling, the GA05 (as amended by the Gambling (Licensing and Advertising) Act 2014 provides that it is an offense to “provide facilities” for remote gambling either (a) using “remote gambling equipment” situated in Great Britain, or (b) which are used by players situated in Great Britain, in each case without a remote gambling operating license. It is also an offense to manufacture, supply, install or adapt gambling software in Great Britain without an appropriate gambling software license.

A remote gambling operating license holder providing facilities for remote gambling to British players is required to use gambling software manufactured and supplied by the holder of a gambling software license (and failure to do so is an offence). Where gambling software is used or supplied for use in relation to the British sector, it must satisfy the Remote Gambling and Software Technical Standards published by the Gambling Commission.

| 9 |

The holder of a British gambling operating license is subject to a variety of ongoing regulatory requirements, including, but not limited to, the following:

| ● | Shareholder disclosure: An entity holding a gambling license must notify the Gambling Commission of the identity of any shareholder holding 3% or more of the equity or voting rights in the entity (whether held or controlled either directly or indirectly). |

| ● | Change of corporate control: Whenever a new person becomes a “controller” (as defined in section 422 of the Financial Services and Markets Act 2000) of a company limited by shares that holds a gambling operating license, the licensed entity must apply to the Gambling Commission for permission to continue to rely on its operating license in light of the new controller. A new controller includes any person who holds or controls (directly or indirectly, including ultimate beneficial owners who hold their interest through a chain of ownership) 10% or more of the equity or voting rights in the licensed entity (or who is otherwise able to exercise “significant influence” over it). The Gambling Commission must be supplied with specified information regarding the new controller (which, in the case of an individual, includes detailed personal disclosure) and this information will be reviewed by the Gambling Commission to assess the suitability of the new controller to be associated with a licensed entity. If the Gambling Commission concludes that it would not have issued the operating license to the licensed entity had the new controller been a controller when the application for the operating license was made, the Gambling Commission is required to revoke the operating license. It is possible to apply for approval in advance from the Gambling Commission prior to becoming a new controller of a licensed entity. | |

| ● | Compliance with the License Conditions and Codes of Practice (LCCP): The LCCP is a suite of license conditions and code provisions which attach to operating licenses issued by the Gambling Commission. The provision of gambling facilities in breach of a license condition is an offense under the GA05. Certain specified “Social Responsibility” code provisions are accorded the same weight as license conditions in this regard (whereas breach of an “ordinary” code provision is not an offense in itself, but may be evidence of unsuitability to continue to hold a gambling license). The LCCP imposes numerous operational requirements on licensees, including compliance with the Gambling Commission’s Remote Gambling and Software Technical Standards, segregation of customer funds, the implementation of a variety of social responsibility tools (such as self-exclusion), anti-money laundering measures, age verification of customers and a host of consumer protection measures. The Gambling Commission regularly reviews and revises the LCCP with the most recent proposals expected to come into effect on 28 February 2025 (Financial vulnerability checks) and 1 May 2025 (Improving customer choice on direct marketing). | |

| ● | Regulatory returns and reporting of key events: The LCCP requires licensees to submit quarterly returns to the Gambling Commission detailing prescribed operational data to ensure licensees are within correct fee categories and also to provide vital information regarding the UK market to enable the UK Gambling Commission to regulate effectively and publish industry statistics. Licensees are also required to notify the Gambling Commission as soon as practicable and in any event within 5 working days of becoming aware of the occurrence of certain specified “key events” which, in summary, are events which could have a significant impact on the nature or structure of the licensee’s business. Licensees are also required to notify suspicion of offenses and suspicious gambling activity. | |

| ● | Personal licenses: Key management personnel are required to maintain personal licenses authorizing them to discharge certain responsibilities on behalf of the operator. These personal licenses are subject to renewal every five years. Personal licenses are subject to compliance with certain license conditions. |

Italy

We operate two different gaming businesses in Italy. We provide platform and games for video lottery terminals and we also supply platforms for bets on Virtual Sports events to betting shops and online platforms. Our businesses are operated through the Italian branches of certain of our UK subsidiaries. These branches hold police licenses and are enrolled in the ADM Register of Gestori, as further described below. We supply our platform and games and Virtual Sports products only to operators licensed under Italian gaming laws and regulations.

Our VLT and Virtual Sports platforms must be connected over the internet to servers operated by the ADM. Information regarding gaming sessions and the amounts wagered and won is provided in real time through the ADM servers, in order to enable the ADM to monitor the operation of machines and games and to verify the amount of taxes due.

| 10 |

Italian Betting and Gaming Laws and Regulations. Operators of betting premises offering VLTs (including the entities managing the networks connecting such VLTs to ADM servers), and operators of betting premises or online platforms offering Virtual Sports products, must hold an Italian gaming license while operators of gaming halls where VLTs are located operate do not need a gaming license. No gaming license is required in order to supply VLTs or Virtual Sports products to such operators. Such VLT platforms, machines and games, and Virtual Sports platforms and games, must be certified and approved by either SOGEI, an entity controlled by the Italian Ministry of Finance and authorized to conduct such certifications or testing labs accredited with ADM. Such certifications and approvals must be obtained by such operators, rather than the suppliers of such VLT platforms, machines and games, and Virtual Sports platforms and games.

Suppliers of gaming machines, including VLTs, must hold a police license (as prescribed by article 86, paragraph 3, of the Italian United Text of Public Security Law provided by the Royal Decree 18 June 1931, No. 773) and be enrolled in a registry prescribed by article 1, paragraph 82 of Law No. 220/2010 and managed by ADM (known as the “ADM Register of Gestori”). If a supplier of gaming machines is not enrolled in the ADM Register of Gestori, any agreement it enters into regarding the supply of gaming machines is null and void. In addition, if the enrollment is not renewed, existing agreements regarding the supply of gaming machines become null and void. Enrollment in the ADM Register of Gestori is subject to, among other things, a review of the suitability of the applicant business entity and its directors. In the event of a change of control of the entity enrolled in the ADM Register of Gestori (but not of such entity’s direct or indirect parent entities), the details of such change must be notified to the ADM and suitability must be reconfirmed.

Suppliers of Virtual Sports products are not required to hold a police license, be enrolled in the Register of Gestori or otherwise be licensed or registered.

Greece

In Greece, we supply VLTs, including the terminal machines themselves, the related online platforms and the games available on the machines, to brick-and-mortar gaming locations operated by OPAP, the country’s sole licensed operator of gaming machines. We supply such VLTs under a certification provided by the Hellenic Gaming Commission. We also supply Virtual Sports products within retail venues operated by OPAP and via self-service betting terminals within OPAP venues and supply interactive games and Virtual Sports to online operators in Greece including Stoiximan, OPAP and Novibet.

Greek Betting and Gaming Laws and Regulations: According to Article 44 par. 2 of Law 4002/2011, as well as according to HGC’s Decision No 225/2/25.10.2016 as well as Ministerial Decision 79314/23.07.2020 (GG B’ 3263/5 August 2020) as amended with Decision 13530 /02.02.2022 (GG B’ 356 03.02.2022) and again with Decision 187634/27.12.2022 (GG B’ 6716/2712.2022) and 79305/05.08.2020 (GG B’ 3262/5 August 2020), all suppliers of gaming machines in Greece must be certified by the HGC in order to legally supply, sell, lease, offer or distribute any VLT or virtual game or any other game of chance (i.e. games including wagers or bets and the result of which games depends, even partly, on the influence of luck). Moreover, for Manufacturers which are defined under the aforesaid Decision 79305 as “the person or entity which manufactures (indicatively, studies, designs, assembles, produces, programs) and in any way makes available to an Operator and/or Importer any Technical Means and Hardware, and has received a Suitability License by the HGC to this end, as well as the person that holds a license for a Studio”, Decision 79305, provides in Article 9 for a Suitability License provided a Manufacturers (type A.1 license) and in Article 10 to Importers/Distributors (type E1 and E2)Accordingly, manufacturers need to obtain a Suitability License Type A1, while importers/distributors need to obtain a Suitability License Type E1 or E2.

As regards online gaming, Articles 45 -52 of Law 4002/2011 (GG A’ 180/22.8.2011), which was recently amended by Law 4635/2019 (GG A’ 167/30.10.2019), introduces several new provisions such as the two exclusive types of online licenses for online gaming operators: a) Online Betting License; and b) a license for Other Online Games (it covers online casino games and online poker games and variants thereof). Furthermore, Article 14 of the HGC’s Decision No 79835/05.08.2020 (GG B’ 3265/5.8.2020) states that all Manufacturers have to submit an application to the HGC, accompanied by the required compliance certificates, for the following elements: i. the Gaming Platform (Betting Platform); ii. the Random Number Generator (RNG) per type/group of Games that the Manufacturer offer to each License Holder; and iii. each individual game or multigame. Lastly, Suitability Licenses for suppliers are also divided into two types: a) Manufacturers Suitability License and b) Importers/Distributors Suitability License (according to articles 9 and 10 of Decision No 79305/05.08.2020). Accordingly, manufacturers need to obtain a Suitability License Type A1 or A2 (depending on whether the manufacturer provides management services to the operator or not), while importers/distributors need to obtain a Suitability License Type E1 or E2.

| 11 |

Gaming Regulation and Changes in Ownership

In a number of the jurisdictions in which we are subject to gaming regulations, regulators require us to keep them informed as to our ownership structure and composition and, to varying extents and in various circumstances, require us to disclose certain information regarding the persons who directly or indirectly hold our shares. Depending on the regulator, we may need to provide such information not only when we first seek licenses or certifications, but also when material changes (measured at different levels) occur in the ownership of our shares. As a result, material changes in our shareholdings may be subject to special procedures or consents in order to ensure the continuation and confirmation of our gaming licenses and certifications.

If one or more gaming authorities were to find that an officer, director, or key employee fails to qualify or is unsuitable for licensing or unsuitable to continue having a relationship with us, we would be required to sever all relationships with such person. Gaming authorities may also require us to terminate the employment of any person who refuses to file appropriate applications.

In many jurisdictions, certain of our stockholders may be required to undergo a suitability investigation similar to that described above. Many jurisdictions require any person who acquires beneficial ownership of more than a certain percentage of our voting securities, typically 5%, to report the acquisition to gaming authorities, and may be required to apply for qualification or a finding of suitability. Most gaming authorities, however, allow an “institutional investor” to apply for a waiver.

Content Development

We continually invest in new product development in each of our Gaming, Virtual Sports, Interactive and Leisure business segments. Inspired has a full stack game development structure, combining its proprietary technology frameworks together with some of the industry’s best math, art, creative and production personnel spread across 3 game studios (Inspired, Astra and Bell Fruit). We release over 100 games each year onto our own priority gaming system, Interactive Remote Gaming Server (“RGS”) and to our G2S clients around the world in markets such as North America, UK, Brazil, Greece, Spain, Belgium, Italy, Sweden and more. Whilst many of our game launches are omni-channel, we have a focus on building the right game for the right market and take pride in tweaking modifying the math and themes for the target player. In Virtual Sports, we combine graphical assets betting market mathematics, proprietary scheduling software allowing us to generate virtual sports markets and results for all our B2B customers. In addition, our VPP (Virtuals Plug and Play) product range leverages our award winning Virtuals assets, along with our RGS (remote gaming server) to produce our “Virtuals Sportsbook in a box product”. VPP allows our customers to operate our Virtuals Sports products without their own sportsbook. We account for our development costs as software development costs, and these are typically amortized over a two-year period.

Suppliers

Our principal supply arrangements concern the supply of our terminals, terminals components, content provision, license holders (branded properties), and outsourced labor. We work closely with our key suppliers to ensure a high level of quality of goods and services is obtained and have worked with many of these suppliers for many years. We have achieved significant cost savings through centralization of purchases.

Customers

Our customer base includes regulated operators of lotteries, licensed sports bookmakers, operators of licensed betting offices, gaming and bingo halls, casinos, pubs, adult gaming centers, holiday parks and regulated online operators. We typically implement design and content variations to customize their terminals and player experiences. Our license agreements with customers for the provision of machines, content and Virtual Sports products include provisions to protect our intellectual property rights in our games and other content.

Customer Contracts – Gaming

Our contracts in the Gaming segment involve supplying gaming terminals and licensing gaming software and games for use and operation in conjunction with the terminals. We supply the terminals on an exclusive or non-exclusive basis on a per customer or per location basis. Under these contracts, we have general obligations to deliver, install, upgrade and service the terminals and software. The contracts may be terminated early in various circumstances such as if we fail to meet performance targets in servicing the machines.

| 12 |

Under some contracts, we receive an upfront fee for the provision of the terminals but more typically generate revenue as a percentage of income generated on terminals. With our participation-driven business model, approximately 94% of service revenue (excluding VAT related income) for our Gaming segment is recurring in nature and derived under long-term contracts that are typically between three and five years (although may be shorter for contract extensions). Major contracts have been renewed over the past three (3) years.

Customer Contracts – Virtual Sports

Our contracts in the Virtual Sports segment typically involve the supply of licenses to operators to make available, either via online or retail channels, virtual sporting events such as horse racing, soccer, football, darts, cricket, or basketball, and to enable end-users to place bets on these events. These are typically one-time non-exclusive licenses specific to the virtual sporting event. We may agree to customize and brand the virtual sporting events for the operator or to provide language variations of the event. The contracts may be terminated early in various circumstances, including, for example, if the operator fails to pay an invoice within 60 days of receipt.

Our Virtual Sports products are typically offered to operators on a participation basis, whereby we receive a royalty for a portion of the gaming revenue generated, plus an upfront software license fee and a hosting fee. With our participation-driven business model, our Virtual Sports segment produces approximately 99% of total revenue on a recurring basis under long-term contracts that average three to four years when entered into and we have historically had a 100% renewal rate over the last three years for contracts that expired.

Customer Contracts – Interactive

Our contracts in the Interactive segment vary but generally involve the provision of a limited, non-exclusive, non-transferable, revocable license to operators to display certain slot and casino content on which online bets are placed or to make our games available for play by end-users of an operator’s online gaming business operations. A number of contracts have been concluded with aggregator platforms to ensure wider distribution via the platform customers and a single integration, The contracts may be terminated early in various circumstances, including material breach or inability to operate due to a change in regulatory status.

Our Interactive products are typically offered to operators or platforms on a participation basis, whereby we receive a percentage of percentage of net gaming revenue generated by reference to amount wagered on our content less winnings, agreed bonus deductions utilized in promoting our content on the relevant platform, and any applicable gaming taxes. With our participation-driven business model, approximately 100% of revenue for our Interactive segment is recurring in nature and derived under long-term contracts that averaged three years. Over the last three years, we have renewed approximately 100% of these contracts for those customers that have continued to trade.

Customer Contracts – Leisure

Our contracts in the Leisure segment vary but generally involve (i) agreement whereby the operator or proprietor of certain leisure resorts contributes premises and we provide, on an exclusive basis, gaming and amusement terminals as well as gaming software and games for the machines provided, (ii) contracts to supply gaming terminals as well as gaming software and games for the terminals provided to leisure operators on a non-exclusive basis, and (iii) rental agreements, which we enter into with certain motorway services providers, whereby we rent unit space in motorway service areas and populate this space with our gaming terminals.

Depending on the contract type, we have general obligations to deliver, install, upgrade and service the terminals and software provided, to acquire licensing for the various prizes and toys, which may be used in the terminals, to keep the premises open for minimum operating hours and not to use the premises for certain business. These contracts may be terminated early in various circumstances, including for material breach or insolvency events.

Under our leisure contracts, we typically generate revenue on a participation-basis by participating, typically as a function of gross revenue from each terminal, in a percentage of volumes generated by these terminals. With our participation-driven or fixed weekly fee business model, approximately 100% of service revenue for our Leisure segment is recurring in nature and derived under long-term contracts that are usually between three and five years. Over the last three years, within the Leisure segment we have successfully renewed or extended the majority of major contracts that have expired.

| 13 |

Operations and Employees

Our operations include game production, platform and hardware design, production, testing, and distribution; the maintenance, management, and extension of our centralized network for product distribution and product monitoring; the delivery and, in certain circumstances, maintenance of SBG terminals; gaming machine engineering, assembly, repair and storage; parts supply; change and release management; remote operational services; problem management; business development; market account management; and general administration and management, including Finance, Legal, People (Human Resources), Investor Relations, Marketing and Communications, Quality, Compliance and Information Security.

As of December 31, 2024, we had approximately 1,600 employees, approximately 1,420 of whom were full-time. Of those employees, approximately 470 were dedicated to delivering our digital gaming platforms, content and hardware and approximately 920 of our employees were involved in UK field operations. Our management, sales and administration teams accounted for approximately 240 employees.

Intellectual Property

Our intellectual property consists principally of the propriety software we develop to operate our network and in the design and distribution of our games. We depend upon agreements relating to trade secrets and proprietary know-how to protect our rights in this intellectual property. We require all our employees, contractors and other collaborators to enter into agreements that prohibit the disclosure of our confidential information to other parties. In addition, it is our policy to require our employees, contractors and other collaborators who have access to proprietary and trade secret material to enter into agreements that require them to assign any and all intellectual property rights to us that arise as a result of their work on our behalf. We also require our employees to review and acknowledge our intellectual property policies regarding how we handle intellectual property. These agreements, acknowledgements and policies may not provide adequate protection for our trade secrets, know-how or other proprietary information in the event of any unauthorized use or disclosure in violation of these agreements, and may not be sufficient to secure for us the value in such developments that they are designed to secure.

We also hold certain patents, trademarks, design rights and other intellectual property rights in respect of our products, systems, web domains, and other intellectual property in Brazil, Canada, the U.S. and Europe. As of December 31, 2024, we held approximately 25 patents and approximately 300 trademarks worldwide. We also rely on certain products and technologies that we license from third parties. Proprietary licenses typically limit our use of intellectual property to specific uses and for specific time periods.

The terms of our intellectual property registrations vary based on the type of registration and the date and jurisdiction of filing or grant. European and UK trademark registration lasts for 10 years but can be renewed indefinitely. European and UK design registration lasts for five years but it can be renewed four times (giving a maximum total of 25 years of protection). European and UK patents can only be renewed for up to 20 years. U.S. design patents expire 15 years from the date of grant, and the term of utility patents generally expires 20 years from the date of filing of the first non-provisional patent application in a family of patents. The actual protection afforded by a patent depends upon the type of patent, the scope of its coverage and the availability of legal remedies in the applicable country.

Competition

We operate in a highly competitive industry, and in highly competitive business segments. We face competition from a number of worldwide businesses, many of which have substantially greater financial resources and operating scale than we do. Such competition could adversely affect our ability to win new contracts and sales and renew existing contracts. We operate in a period of intense price-based competition in some key sectors, which could affect the profitability of the contracts and sales we do win. In certain sectors, our businesses also face competition from suppliers, operators or licensees who offer products for internet gaming in illegal or unregulated sectors, but are still able or permitted to supply products and compete with us in regulated sectors. These competitors often have substantially greater financial resources and operating scale than we do. Some larger competitors hold long term contracts which control access points for some of our products and this may mean we must contract with those competitors rather than directly with the customer to provide our products. Our principal competitors include, among others, certain businesses that have vertically integrated gaming machine and retail betting operations and businesses that operate in both regulated and unregulated sectors and thereby effectively subsidize their regulated operations with unregulated operations.

| 14 |

Corporate Information

We maintain a website at www.inseinc.com. Our Annual Report on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K and any amendments to those reports filed or furnished pursuant to Section 13(a) of the Exchange Act are available free of charge through the Investors link on our website as soon as reasonably practical after they are electronically filed with or furnished to the SEC. Also available on our website are our Code of Ethics, as well as the charters of the audit, compensation and nominating and corporate governance committees of the Board of Directors. Information on our website is not incorporated into this report. The SEC maintains a website that contains reports, proxy statements and other information regarding issuers that file electronically with the SEC. These materials may be obtained electronically by accessing the SEC’s website at www.sec.gov.

ITEM 1A. RISK FACTORS.

Our business is subject to a high degree of risk. You should carefully read and assess our discussion of the risk factors facing our business, below. Any of these risks could materially and adversely affect our business, operating results, financial condition and prospects, and cause the value of our common stock to decline, which could cause investors in our common stock to lose all or part of their investments.

Summary of Risk Factors

Our business is subject to a number of risks, including risks that may prevent us from achieving our business objectives or may adversely affect our business, financial condition, results of operations, cash flows, and prospects. These risks are discussed more fully below and include, but are not limited to, risks related to the following:

| ● | We have identified material weaknesses in our disclosure controls and procedures and internal control over financial reporting, which we are in the process of remediating. Failure to remediate these material weaknesses or any other material weaknesses that we identify in the future could result in material misstatements in our financial statements. | |