UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

(Mark One)

| x | QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the quarterly period ended June 30, 2015

OR

| o | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from ______________ to ______________

001-36844

(Commission file number)

GREAT AJAX CORP.

(Exact name of registrant as specified in its charter)

| Maryland | 47-1271842 | |

| State or other jurisdiction of incorporation or organization |

(I.R.S. Employer Identification No.) |

| 9400 SW Beaverton-Hillsdale Hwy, | 97005 | |

| Suite 131 | (Zip Code) | |

| Beaverton, OR 97005 | ||

| (Address of principal executive offices) |

503-505-5670

Registrant’s telephone number, including area code

Indicate by check mark whether the Registrant

(1) has filed all reports to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12

months (or for such shorter period that the Registrant was required to file such report(s), and (2) has been subject to such filing

requirements for the past 90 days.

Yes x No ¨

Indicate by check mark whether the Registrant has submitted electronically and posted on its corporate Website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the Registrant was required to submit and post such files). Yes x No ¨

Indicate by check mark whether the Registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definition of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (check one):

| Large accelerated filer ¨ | Accelerated filer ¨ |

| Non-accelerated filer x (Do not check if a smaller reporting company) | Smaller reporting company ¨ |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No x

As of August 12, 2015, 15,909,634 shares of the Registrant’s common stock, par value $0.01 per share, were outstanding which includes 624,106 of operating partnership units that are redeemable on a one-for-one basis into shares of the registrant’s common stock.

| -i- |

Item 1. Consolidated Interim Financial Statements

GREAT AJAX CORP. AND SUBSIDIARIES

CONSOLIDATED BALANCE SHEETS

(Dollars in thousands except shares and per share data)

June 30, 2015 | December 31, 2014 | |||||||

| ASSETS | ||||||||

| Cash and cash equivalents | $ | 36,240 | $ | 53,099 | ||||

| Mortgage loans, net(1) | 444,408 | 211,159 | ||||||

| Property held-for-sale | 9,018 | 1,316 | ||||||

| Rental property, net | 121 | 290 | ||||||

| Receivable from servicer | 3,538 | 1,340 | ||||||

| Investment in affiliate | 2,445 | 2,237 | ||||||

| Prepaid expenses and other assets | 6,068 | 3,317 | ||||||

| Total Assets | $ | 501,838 | $ | 272,758 | ||||

| LIABILITIES AND EQUITY | ||||||||

| Liabilities: | ||||||||

| Secured borrowings(1) | $ | 116,349 | $ | 84,679 | ||||

| Borrowings under repurchase agreement | 153,804 | 15,249 | ||||||

| Management fee payable | 441 | 258 | ||||||

| Accrued expenses and other liabilities | 2,794 | 1,292 | ||||||

| Total liabilities | 273,388 | 101,478 | ||||||

| Commitments and contingencies – see Note 7 | ||||||||

| Equity: | ||||||||

| Preferred stock $.01 par value; 25,000,000 shares authorized, none issued or outstanding | - | - | ||||||

| Common stock $.01 par value; 125,000,000 shares authorized, 15,253,998 shares at June 30, 2015 and 11,223,984 shares at December 31, 2014 issued and outstanding | 152 | 112 | ||||||

| Additional paid-in capital | 211,361 | 158,951 | ||||||

| Retained earnings | 7,279 | 2,744 | ||||||

| Equity attributable to common stockholders | 218,792 | 161,807 | ||||||

| Noncontrolling interests | 9,658 | 9,473 | ||||||

| Total equity | 228,450 | 171,280 | ||||||

| Total Liabilities and Equity | $ | 501,838 | $ | 272,758 | ||||

| (1) | Mortgage loans includes $179,808 and $127,559 of loans at June 30, 2015 and December 31, 2014, respectively, transferred to securitization trusts that are variable interest entities (“VIEs”); these loans can only be used to settle obligations of the VIEs. Secured borrowings consist of notes issued by VIEs that can only be settled with the assets and cash flows of the VIEs. The creditors do not have recourse to the primary beneficiary (Great Ajax Corp.). See Note 8—Debt. |

The accompanying notes are an integral part of the consolidated interim financial statements.

| 1 |

GREAT AJAX CORP. AND SUBSIDIARIES

CONSOLIDATED STATEMENTS OF INCOME

(Unaudited)

(Dollars in thousands except shares and per share data)

Three

months | Six

months | |||||||

| INCOME | ||||||||

| Loan interest income | $ | 10,793 | $ | 17,677 | ||||

| Interest expense | (2,269 | ) | (3,344 | ) | ||||

| Net interest income | 8,524 | 14,333 | ||||||

| Other income | 232 | 446 | ||||||

| Total income | 8,756 | 14,779 | ||||||

| EXPENSE | ||||||||

| Related party expense – management fee | 856 | 1,602 | ||||||

| Related party expense – loan servicing fees | 851 | 1,507 | ||||||

| Loan transaction expense | 729 | 989 | ||||||

| Professional fees | 356 | 741 | ||||||

| Other expense | 289 | 450 | ||||||

| Total expense | 3,081 | 5,289 | ||||||

| Income before provision for income taxes | 5,675 | 9,490 | ||||||

| Provision for income taxes | 16 | 16 | ||||||

| Consolidated net income | 5,659 | 9,474 | ||||||

| Less: consolidated net income attributable to the non-controlling interest | 223 | 398 | ||||||

| Consolidated net income attributable to common stockholders | $ | 5,436 | $ | 9,076 | ||||

| Basic earnings per common share | $ | 0.36 | $ | 0.64 | ||||

| Diluted earnings per common share | $ | 0.36 | $ | 0.64 | ||||

| Weighted average shares - basic | 15,237,739 | 14,129,162 | ||||||

| Weighted average shares - diluted | 15,909,634 | 14,801,319 | ||||||

The accompanying notes are an integral part of the consolidated interim financial statements.

| 2 |

GREAT AJAX CORP. AND SUBSIDIARIES

CONSOLIDATED STATEMENTS OF CASH FLOWS

(Unaudited)

(Dollars in thousands)

Six months | |||||

| CASH FLOWS FROM OPERATING ACTIVITIES | |||||

| Consolidated net income | $ | 9,474 | |||

| Adjustments to reconcile net income to net cash from operating activities | |||||

| Stock-based management fee and compensation expense | 921 | ||||

| Non-cash interest income accretion | (11,850 | ) | |||

| Loss on sale of property | 9 | ||||

| Depreciation of property | 1 | ||||

| Amortization of prepaid financing costs | 435 | ||||

| Net change in operating assets and liabilities | |||||

| Prepaid expenses and other assets | (3,186 | ) | |||

| Receivable from servicer | (2,198 | ) | |||

| Undistributed income from investment in affiliate | (275 | ) | |||

| Accrued expenses and other liabilities | 1,685 | ||||

| Net cash from operating activities | (4,984 | ) | |||

| CASH FLOWS FROM INVESTING ACTIVITES | |||||

| Purchase of mortgage loans and related balances | (233,626 | ) | |||

| Principal paydowns on mortgage loans | 7,260 | ||||

| Purchase of property held-for-sale and related balances | (2,794 | ) | |||

| Proceeds from sale of property held-for-sale | 357 | ||||

| Distribution from affiliate | 67 | ||||

| Renovations of rental property and property held for sale | (139 | ) | |||

| Net cash from investing activities | (228,875 | ) | |||

| CASH FLOWS FROM FINANCING ACTIVITIES | |||||

| Proceeds from repurchase agreement | 153,841 | ||||

| Proceeds from sale or issuance of secured notes | 35,213 | ||||

| Repayments on repurchase agreement | (15,286 | ) | |||

| Repayments on secured notes | (3,543 | ) | |||

| Sale of common stock, net of offering costs | 51,529 | ||||

| Distribution to non-controlling interest | (213 | ) | |||

| Dividends paid on common stock | (4,541 | ) | |||

| Net cash from financing activities | 217,000 | ||||

| NET CHANGE IN CASH AND CASH EQUIVALENTS | (16,859 | ) | |||

| CASH AND CASH EQUIVALENTS, beginning of period | 53,099 | ||||

| CASH AND CASH EQUIVALENTS, end of period | $ | 36,240 | |||

| SUPPLEMENTAL DISCLOSURE OF CASH FLOW INFORMATION | |||||

| Cash paid for interest | $ | 2,544 | |||

| Cash paid for income taxes | $ | - | |||

| SUPPLEMENTAL DISCLOSURE OF NONCASH INVESTING AND FINANCING ACTIVITIES | |||||

| Transfer of loans to rental property or property held for sale | $ | 4,965 | |||

| Transfer of rental property to property held for sale | $ | 168 | |||

| Issuance of common stock for management fees | $ | 814 | |||

The accompanying notes are an integral part of the consolidated interim financial statements.

| 3 |

GREAT AJAX CORP. AND SUBSIDIARIES

CONSOLIDATED STATEMENT OF CHANGES IN EQUITY

(Unaudited)

(Dollars in thousands)

Common | Additional Paid-in | Retained | Total | Noncontrolling | Total | |||||||||||||||||||

| Balance at December 31, 2014 | $ | 112 | $ | 158,951 | $ | 2,744 | $ | 161,807 | $ | 9,473 | $ | 171,280 | ||||||||||||

| Issuance of shares | 40 | 51,489 | - | 51,529 | - | 51,529 | ||||||||||||||||||

| Net income | - | - | 9,076 | 9,076 | 398 | 9,474 | ||||||||||||||||||

| Stock-based management fee expense | - | 814 | - | 814 | - | 814 | ||||||||||||||||||

| Stock-based compensation expense | - | 107 | - | 107 | - | 107 | ||||||||||||||||||

| Dividends and distributions | - | - | (4,541 | ) | (4,541 | ) | (213 | ) | (4,754 | ) | ||||||||||||||

| Balance at June 30, 2015 | $ | 152 | $ | 211,361 | $ | 7,279 | $ | 218, 792 | $ | 9,658 | $ | 228,450 | ||||||||||||

The accompanying notes are an integral part of the consolidated interim financial statements.

| 4 |

GREAT AJAX CORP. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

June 30, 2015

(Unaudited)

Note 1 — Organization and basis of presentation

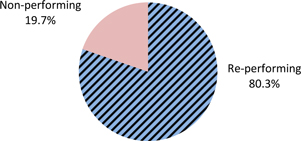

Great Ajax Corp., a Maryland corporation (the “Company”), is an externally managed real estate company formed on January 30, 2014 and capitalized on March 28, 2014 by its then sole stockholder, Aspen Yo LLC (“Aspen Yo”), a company affiliated with the Aspen Capital companies (“Aspen Capital”). The Company was formed to facilitate capital raising activities and to operate as a mortgage real estate investment trust. The Company focuses primarily on acquiring, investing in and managing a portfolio of re-performing and non-performing mortgage loans secured by single-family residences and, to a lesser extent, single-family properties. Re-performing loans are loans on which at least five of the seven most recent payments have been made, or the most recent payment has been made and accepted pursuant to an agreement, or the full dollar amount to cover at least five payments has been paid in the last seven months. Non-performing loans are those loans on which the most recent three payments have not been made. The Company also invests in loans secured by smaller multi-family residential and commercial mixed use retail/residential properties, as well as in the properties directly. The Company’s manager is Thetis Asset Management LLC (the “Manager” or “Thetis”), an affiliated company. The Company owns 19.8% of the Manager. The Company’s mortgage loans and real properties are serviced by Gregory Funding LLC (“Gregory” or “Servicer”), also an affiliated company. The Company expects to qualify and will elect to be taxed as a real estate investment trust, or REIT, under the Internal Revenue Code of 1986, as amended (the “Code”), commencing with the year ended December 31, 2014.

The Company conducts substantially all of its business through its operating partnership, Great Ajax Operating Partnership L.P., a Delaware limited partnership, and its subsidiaries. The Company, through a wholly owned subsidiary, is the sole general partner of the operating partnership. GA-TRS LLC, or Thetis TRS, is a wholly owned subsidiary of the operating partnership that owns the equity interest in the Manager. The Company elected to treat Thetis TRS as a “taxable REIT subsidiary” (“TRS”) under the Code. In September 2014, the Company formed Great Ajax Funding LLC, a wholly owned subsidiary of the operating partnership, to act as the depositor of mortgage loans into securitization trusts and to hold the subordinated securities issued by such trusts and any additional trusts the Company may form for additional securitizations. The Company generally securitizes its mortgage loans and retains subordinated securities from the securitizations. In November 2014, the Company formed AJX Mortgage Trust I, a wholly owned subsidiary of the operating partnership, in connection with a repurchase facility. In addition, the Company, through its operating partnership, holds real estate owned properties (“REO”) acquired upon the foreclosure or other settlement of its owned non-performing loans, as well as through outright purchases. On February 1, 2015, the Company formed GAJX Real Estate LLC, as a wholly owned subsidiary of the operating partnership, to own, maintain, improve and sell REO properties. The Company has elected to treat GAJX Real Estate LLC as a TRS under the Code.

The Company commenced its operations following the completion of its initial private offering in July 2014. On July 8, 2014, the Company closed a private offering, pursuant to which the Company sold 8,213,116 shares of common stock and 453,551 Class A Units of the operating partnership (the “OP Units”), which are redeemable on a 1-for-1 basis into shares of its common stock after one year of ownership. On August 1, 2014, the Company closed the sale of an additional 263,570 shares of common stock and 14,555 OP Units pursuant to the exercise of the option to purchase additional shares granted to the initial purchaser and placement agent. The purchase price per share and per OP Unit was $15.00. In these offerings, which are referred to collectively as the “Original Private Placement,” the net proceeds, including from the additional shares purchased pursuant to the option to purchase additional shares and OP Units, after deducting the initial purchaser’s discount and placement fee and estimated offering expenses payable, was approximately $128.4 million. The Original Private Placement was made in reliance on the exemptions from registration set forth in Section 4(a)(2) of the Securities Act of 1933, as amended (the “Securities Act”), and Rule 506 of Regulation D thereunder and Rule 144A under the Securities Act.

Upon the closing of the Original Private Placement, the Company used $48.8 million of the proceeds to acquire its initial mortgage portfolio through the acquisition of 82% of the equity interests in Little Ajax II, LLC

| 5 |

(“Little Ajax II”). Little Ajax II was an affiliated entity that acquired primarily re-performing mortgage loans and a number of non-performing mortgage loans in a series of transactions between December 1, 2013 and July 7, 2014. In September 2014, the Company completed a transaction to acquire the remaining interests in this initial mortgage-related asset portfolio. The transaction initially had Little Ajax II redeem the 82% membership interest of the operating partnership by distributing to the operating partnership 82% of all Little Ajax II loans, participation interests and real property. The operating partnership then purchased for cash the remaining 18% interest in such real estate assets for an aggregate purchase price of approximately $11.4 million. The operating partnership also purchased from Gregory its 5% interest in the 43 loans in which Little Ajax II held a 95% participation interest for approximately $0.2 million.

On December 16, 2014, the Company closed an additional private placement (the “Second Private Placement”), pursuant to which it sold 2,725,326 shares of common stock and 156,000 OP Units. The purchase price per share was $15.00. The net proceeds from the private placement after deducting the placement fee and offering expenses paid by the Company, was approximately $41.2 million. The Company used the proceeds of the Original Private Placement and the Second Private Placement, referred to collectively as the Private Placements, to purchase re-performing and non-performing loans. The Company completed its initial public offering, or IPO, in February 2015 in which the Company and selling stockholders sold an aggregate of 5,276,797 shares of common stock, including shares sold pursuant to exercise of the option to purchase additional shares granted to the underwriters. The Company sold 3,976,464 shares of common stock and selling stockholders sold 1,300,333 shares of common stock, in each case, including shares sold pursuant to exercise of the option to purchase additional shares granted to the underwriters. The Company used the approximately $53.9 million of proceeds (after deducting the underwriting discount but before deducting estimated offering expenses) to acquire additional mortgage loans and mortgage-related assets.

Basis of presentation and use of estimates

These interim consolidated financial statements should be read in conjunction with the Company’s consolidated financial statements and the notes thereto for the period ended December 31, 2014 included in the Annual Report on Form 10-K filed with the Securities and Exchange Commission (the “SEC”) on March 26, 2015.

Interim financial statements are prepared in accordance with accounting principles generally accepted in the United States (“ U.S. GAAP”) for interim financial information and pursuant to the requirements for reporting on Form 10-Q and Regulation S-X. In the opinion of management, all adjustments, consisting solely of normal recurring accruals considered necessary for the fair presentation of financial statements for the interim period presented, have been included. The current period’s results of operations will not necessarily be indicative of results that ultimately may be achieved for the fiscal year ending December 31, 2015.

The consolidated financial statements have been prepared in accordance with U.S. GAAP, as contained within the Accounting Standards Codification (“ASC”) of the Financial Accounting Standards Board (“FASB”) and the rules and regulations of the SEC, as applied to interim financial statements. Comparative income statement periods have been omitted as the Company had no operations prior to July 8, 2014.

All controlled subsidiaries are included in the consolidated financial statements and all intercompany accounts and transactions have been eliminated in consolidation. The operating partnership is a majority owned partnership that has a non-controlling ownership interest that is included in non-controlling interests on the consolidated balance sheet. As of June 30, 2015, the Company owned 96.1% of the outstanding OP Units and the remaining 3.9% of the OP Units were owned by an unaffiliated holder.

The Company’s 19.8% investment in the Manager is accounted for using the equity method because it exercises significant influence on the operations of the Manager through common officers and directors. There is no traded or quoted price for the interests in the Manager since it is privately held.

The preparation of consolidated financial statements in conformity with U.S. GAAP requires the Company to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities as of the date of the consolidated financial statements and the reported amounts of revenues and expenses during the reporting periods. The Company considers significant estimates to include expected cash flows from mortgage loans and fair value measurements.

| 6 |

Note 2 — Summary of significant accounting policies

Cash and cash equivalents

Highly liquid investments with an original maturity of three months or less when purchased are considered cash equivalents. The Company maintains cash and cash equivalents at insured banking institutions. Certain account balances exceed Federal Deposit Insurance Corporation (“FDIC”) insurance coverage and, as a result, there is a concentration of credit risk related to amounts on deposit in excess of FDIC insurance coverage.

Organizational expenses

Organizational expenses are expensed as incurred or when they become reimbursable. Organizational expenses consisted mainly of legal fees.

Offering costs

Costs associated with the Company’s completed offering of shares of common stock have been netted against, and are reflected as a reduction in additional paid-in capital.

Earnings per share

Basic earnings per share is computed by dividing consolidated net income attributable to common stockholders by the weighted average common stock outstanding during the period. The Company treats unvested restricted stock issued under its stock-based compensation plan, which are entitled to non-forfeitable dividends, as participating securities and applies the two-class method in calculating basic earnings per share. Diluted earnings per share is computed by dividing consolidated net income attributable to common stockholders by the weighted average common stock outstanding for the period plus other potentially dilutive securities, such as stock grants, shares that would be issued in the event that OP Units are redeemed for shares of common stock of the Company and shares issued in respect of the stock-based portion of the base fee payable to the Manager and directors’ fees.

Stock-based payments

The Management Agreement (as defined below) provides for the payment to the Manager of a management fee. The Company pays half of the management fee in cash, and half of the management fee in shares of the Company’s common stock, which are issued to the Manager in a private placement and are restricted securities under the Securities Act. Shares issued to the Manager are determined based on the higher of the most recently reported book value or the average of the closing prices of our common stock on the NYSE on the five business days after the date on which the most recent regular quarterly dividend to holders of our common stock is paid. Management fees paid in common stock are expensed in the quarter incurred and recorded in equity at quarter end.

Pursuant to the Company’s 2014 Director Equity Plan (the “Director Plan”), the Company may make stock-based awards. The Company has issued to each of the independent directors restricted stock awards of 2,000 shares of its common stock, which are subject to a one-year vesting period. In addition, each of the Company’s independent directors receives an annual retainer of $50,000, payable quarterly, half of which is paid in shares of the Company’s common stock on the same basis as the stock portion of the management fee payable to the Manager, and half in cash. Stock-based expense for the directors’ annual retainer is expensed as earned, in equal quarterly amounts during the year, and recorded in equity at quarter end.

Directors’ fees

The expense related to directors’ fees is accrued and reflected in stockholders’ equity in the period in which it is incurred.

| 7 |

Management fee and expense reimbursement

Under the management agreement with the Manager, the Company pays a quarterly base management fee based on its stockholders’ equity and a quarterly incentive management fee based on its cash distributions to its stockholders. Manager fees are expensed in the quarter incurred and the portion payable in common stock is included in stockholders’ equity at quarter-end. See “Note 9 — Related party transactions.”

Servicing fees

Under the servicing agreement, Gregory receives servicing fees ranging from 0.65% – 1.25% annually of unpaid principal balance (“UPB”) (or the fair market value or purchase price of REO that the Company owns or acquires). Gregory is reimbursed for all customary, reasonable and necessary out-of-pocket costs and expenses incurred in the performance of its obligations, including the actual cost of any repairs and renovations undertaken on the Company’s behalf. The total fees incurred by the Company for these services will be dependent upon the UPB and type of mortgage loans that Gregory services, property values, previous UPB of the relevant loan, and the number of REO properties. The agreement will automatically renew for successive one-year terms, subject to prior written notice of non-renewal. In certain cases, the Company may be obligated to pay a termination fee. The Management Agreement will automatically terminate at the same time as the servicing agreement if the servicing agreement is terminated for any reason. See “Note 9 — Related party transactions.”

Fair value of financial instruments

Fair value is defined as the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date. A fair value hierarchy has been established which requires an entity to maximize the use of observable inputs and minimize the use of unobservable inputs when measuring fair value. The standard describes three levels of inputs that may be used to measure fair value:

| · | Level 1 — Quoted prices in active markets for identical assets or liabilities. |

| · | Level 2 — Observable inputs other than Level 1 prices, such as quoted prices for similar assets and liabilities; quoted prices in markets that are not active; or other inputs that are observable or can be corroborated by observable market data for substantially the full term of the assets or liabilities. |

| · | Level 3 — Unobservable inputs that are supported by little or no market activity and that are significant to the fair value of the assets or liabilities. |

The degree of judgment utilized in measuring fair value generally correlates to the level of pricing observability. Assets and liabilities with readily available actively quoted prices or for which fair value can be measured from actively quoted prices generally will have a higher degree of pricing observability and a lesser degree of judgment utilized in measuring fair value. Conversely, assets and liabilities rarely traded or not quoted will generally have little or no pricing observability and a higher degree of judgment utilized in measuring fair value. Pricing observability is impacted by a number of factors, including the type of asset or liability, whether it is new to the market and not yet established, and the characteristics specific to the transaction.

Property held-for-sale is measured at cost at acquisition and subsequently measured at the lower of cost or fair value less cost to sell on a nonrecurring basis. The fair value of property held-for-sale is generally based on estimated market prices from an independently prepared appraisal, an independent broker price opinion (“BPO”), or management’s judgment as to the selling price of similar properties.

Income taxes

The Company intends to elect REIT status upon the filing of its 2014 income tax return, and has conducted its operations in order to satisfy and maintain eligibility for REIT status. Accordingly, the Company does not believe it will be subject to U.S. federal income tax from the year ended December 31, 2014 forward on the portion of the Company’s REIT taxable income that is distributed to the Company’s stockholders as long as certain asset, income and stock ownership tests are met. If after electing to be taxed as a REIT, the Company subsequently fails to qualify as a REIT in any taxable year, it generally will not be permitted to qualify for treatment as a REIT for U.S. federal

| 8 |

income tax purposes for the four taxable years following the year during which qualification is lost. The Company may also be subject to state or local income or franchise taxes.

Thetis TRS, GAJX Real Estate LLC and any other TRS that the Company forms, will be subject to U.S. federal and state income taxes. On January 13, 2015, the Company applied for a private letter ruling from the Internal Revenue Service that would allow it to exclude its proportionate share of gross income from the Manager if it held its interest in the Manager through the operating partnership. If the Company receives such a ruling, it expects that it will hold its interest in the Manager through the operating partnership, instead of through Thetis TRS; however, there is no assurance that such a ruling will be issued. Income taxes are provided for using the asset and liability method. A provision for income taxes of $16,400 was recorded for both the three- and six-month periods ended June 30, 2015. Deferred tax assets and liabilities are recognized for the future tax consequences attributable to differences between the carrying amounts of existing assets and liabilities and their respective tax bases. Deferred tax assets and liabilities are measured using enacted rates expected to apply to taxable income in the years in which management expects those temporary differences to be recovered or settled. The effect on deferred taxes of a change in tax rates is recognized in income in the period in which the change occurs. Subject to the Company’s judgment, it reduces a deferred tax asset by a valuation allowance if it is “more–likely-than-not” that some or all of the deferred tax asset will not be realized. Tax laws are complex and subject to different interpretations by the taxpayer and respective governmental taxing authorities. Significant judgment is required in evaluating tax positions, and the Company recognizes tax benefits only if it is more likely than not that a tax position will be sustained upon examination by the appropriate taxing authority.

The Company evaluates tax positions taken in its consolidated financial statements under the interpretation for accounting for uncertainty in income taxes. As a result of this evaluation, the Company may recognize a tax benefit from an uncertain tax position only if it is “more-likely-than-not” that the tax position will be sustained on examination by taxing authorities.

The Company’s tax returns remain subject to examination and consequently, the taxability of the distributions and other tax positions taken by the Company may be subject to change. Distributions to stockholders generally will be taxable as ordinary income, although a portion of such distributions may be designated as long-term capital gain or qualified dividend income, or may constitute a return of capital. The Company will furnish annually to each stockholder a statement setting forth distributions paid during the preceding year and their U.S. federal income tax treatment.

Mortgage loans

Purchased mortgage loans are initially recorded at the purchase price, net of any acquisition fees or costs at the time of acquisition and are considered asset acquisitions. As part of the determination of the purchase price for mortgage loans, the Company uses a discounted cash flow valuation model to model expected cash flows, and which considers alternate loan resolution probabilities, including liquidation or conversion to real estate owned. Observable inputs to the model include current interest rates, loan amounts, status of payments and property types. Unobservable inputs to the model include discount rates, forecast of future home prices, alternate loan resolution probabilities, resolution timelines, the value of underlying properties and other economic and demographic data.

Under ASC 310-30, acquired loans may be aggregated and accounted for as a pool of loans if the loans being aggregated have some degree of credit quality deterioration since origination and have common risk characteristics. A pool is accounted for as a single asset with a single composite interest rate and an aggregate expectation of cash flows. Re-performing mortgage loans have been determined to have common risk characteristics and are accounted for as a single loan pool for loans acquired within each three-month fiscal quarter. Similarly, non-performing mortgage loans have been determined to have common risk characteristics and are accounted for as a single non-performing pool for loans acquired within each three-month fiscal quarter. Under ASC 310-30, the Company estimates cash flows expected to be collected, adjusted for expected prepayments and defaults expected to be incurred over the life of the loan pool. The Company determines the excess of the loan pool’s contractually required principal and interest payments over the expected cash flows as an amount that should not be accreted, referred to as the non-accretable yield. The difference between expected cash flows and the purchase price (at acquisition) or the present value of the expected cash flows is referred to as the accretable yield, which represents the amount that is expected to be recorded as interest income over the remaining life of the loan pool. For the three-

| 9 |

and six-months ended June 30, 2015, the Company recognized no provision for loan loss. For the three- and six-months ended June 30, 2015, the Company accreted $10.8 million and $17.7 million, respectively, into interest income with respect to its loan portfolio. As of June 30, 2015, the Company’s loan portfolio had a UPB of $596.3 million and a carrying value of $444.4 million and at December 31, 2014, a UPB of $298.6 million and carrying value of $211.2 million, which excludes one loan in which it holds a 40.5% beneficial interest through an equity method investee.

Generally, the Company acquires loans at a discount associated with some degree of credit impairment. The Company elects to aggregate certain pools of loans with common risk characteristics and accrue interest income thereon at a composite interest rate, based on expectations of cash flows to be collected for the pool. Expectations of pool cash flow are reviewed quarterly. Adjustments to a pool’s prospective composite interest rate or an allowance for impairment are made to the extent revised expectations differ from original estimates.

For loans that do not qualify for pool aggregation treatment, including performing loans that are not purchased at discounts resulting from credit-related issues, interest is recognized using the simple-interest method on daily balances of the principal amount outstanding, adjusted for the amortization or accretion of the loan premium or discount over the contractual life of the loan.

Accrual of interest on individual loans is discontinued when management believes that, after considering economic and business conditions and collection efforts, the borrower’s financial condition is such that collection of interest is doubtful. The Company’s policy is to stop accruing interest when a loan’s delinquency exceeds 90 days. All interest accrued but not collected for loans that are placed on non-accrual status or subsequently charged-off are reversed against interest income. Income is subsequently recognized on the cash basis until, in management’s judgment, the borrower’s ability to make periodic principal and interest payments returns and future payments are reasonably assured, in which case the loan is returned to accrual status.

An individual loan is considered to be impaired when, based on current events and conditions, it is probable the Company will be unable to collect all amounts due (both principal and interest) according to the contractual terms of the loan agreement. Impaired loans are carried at the present value of expected future cash flows discounted at the loan’s effective interest rate, the loan’s market price, or the fair value of the collateral if the loan is collateral dependent.

For individual loans, a troubled debt restructuring is a formal restructuring of a loan where, for economic or legal reasons related to the borrower’s financial difficulties, a concession that would not otherwise be considered is granted to the borrower. The concession may be granted in various forms, including providing a below-market interest rate, a reduction in the loan balance or accrued interest, an extension of the maturity date, or a combination of these. An individual loan that has had a troubled debt restructuring is considered to be impaired and is subject to the relevant accounting for impaired loans.

The allowance for loan losses is established through a provision for loan losses charged to expenses. The allowance is an amount that management believes will be adequate to absorb probable losses on existing loans that may become uncollectible, based on evaluations of the collectability of loans.

Purchased non-performing loans that are accounted for as individual loans are recorded at fair value, which is generally the purchase price. Interest income is recognized on a cash basis and loan purchase discount is accreted to income in proportion to the actual principal paid. Loans are tested quarterly for impairment and impairment reserves are recorded to the extent the fair market value of the underlying collateral falls below net book value.

While the Company generally intends to hold its assets as long-term investments, it may sell certain of its loans in order to manage its interest rate risk and liquidity needs, meet other operating objectives and adapt to market conditions. The timing and impact of future sales of loans, if any, cannot be predicted with any certainty. Since the Company expects that its assets will generally be financed, it expects that a significant portion of the proceeds from sales of its assets (if any), prepayments and scheduled amortization will be used to repay balances under its financing sources.

| 10 |

Residential properties

Property is recorded at cost if purchased, or at fair value of the asset less estimated selling costs if obtained through foreclosure by the Company. Property that is currently unoccupied and actively marketed for sale is classified as held-for-sale. Property held-for-sale is carried at the lower of cost or fair market value. Net unrealized losses due to changes in market value are recognized through a valuation allowance by charges to income.

No depreciation or amortization expense is recognized on properties held-for-sale, while holding costs are expensed as incurred. Rental property is property not held-for-sale. Rental properties are intended to be held as long-term investments but may eventually be held-for-sale. Depreciation is provided for using the straight-line method over the estimated useful lives of the assets of three to 27.5 years.

With respect to residential rental properties not held-for-sale, the Company performs an impairment analysis using estimated cash flows if events or changes in circumstances indicate that the carrying value may be impaired, such as prolonged vacancy, identification of materially adverse legal or environmental factors, changes in expected ownership period or a decline in market value to an amount less than cost. This analysis is performed at the property level. These cash flows are estimated based on a number of assumptions that are subject to economic and market uncertainties including, among others, demand for rental properties, competition for customers, changes in market rental rates, costs to operate each property and expected ownership periods.

If the carrying amount of a held-for-investment asset exceeds the sum of its undiscounted future operating and residual cash flows, an impairment loss is recorded for the difference between estimated fair value of the asset and the carrying amount. The Company generally estimates the fair value of assets held for use by using BPOs. In some instances, appraisal information may be available and is used in addition to BPOs.

The Company performs property renovations to maximize the value of the property for its rental strategy. Such expenditures are part of its initial investment in a property and, therefore, are capitalized as part of the basis of the property. Subsequently, the residential property, including any renovations that improve or extend the life of the asset, are accounted for at cost. The cost basis is depreciated using the straight-line method over an estimated useful life of three to 27.5 years. Interest and other carrying costs incurred during the renovation period are capitalized until the property is ready for its intended use. Expenditures for ordinary maintenance and repairs are charged to expense as incurred.

Segment information

The Company’s primary business is acquiring, investing in and managing a portfolio of mortgage loans. The Company operates in a single segment focused on non-performing mortgages and re-performing mortgages.

Emerging growth company

Section 107 of the Jumpstart Our Business Startups Act (the “JOBS Act”) provides that an emerging growth company can take advantage of the extended transition period provided in Section 7(a)(2)(B) of the Securities Act for complying with new or revised accounting standards. In other words, an emerging growth company can delay the adoption of certain accounting standards until those standards would otherwise apply to private companies. The Company has elected to take advantage of the benefits of this extended transition period. Its consolidated financial statements may, therefore, not be comparable to those of companies that comply with such new or revised accounting standards.

Reclassifications

The December 31, 2014 amounts included in the delinquency table in Note 3 – Mortgage loans have been reclassified from delinquent to current to reflect a correction of an error in the presentation of the disclosure that is immaterial to the consolidated financial statements taken as a whole. Such reclassifications did not affect cash flows, net revenues, net income, total assets, total liabilities or total equity.

| 11 |

Recently issued accounting standards

In January 2014, FASB issued Accounting Standards Update (“ASU”) 2014-04, Troubled Debt Restructurings by Creditors. It provides that if a repossession or foreclosure has occurred, and a creditor is considered to have received physical possession of residential real estate property collateralizing a consumer mortgage loan, upon either (1) the creditor obtaining legal title to the residential real estate property upon completion of a foreclosure or (2) the borrower conveying all interest in the residential real estate property to the creditor to satisfy that loan through completion of a deed in lieu of foreclosure or through a similar legal agreement. Additionally, the amendment requires disclosure of both (1) the amount of foreclosed residential real estate property held by the creditor and (2) the recorded investment in mortgage loans collateralized by residential real estate property that are in the process of foreclosure. The amended guidance may be applied using either a prospective transition method or a modified retrospective transition method and is effective for fiscal years, and interim periods within those years, beginning after December 15, 2014, with early adoption permitted. We adopted this standard in the first quarter of 2015 and it did not have a material impact on our financial statements.

In May 2014, the FASB issued ASU 2014-09 Revenue from Contracts with Customers. ASU 2014-09 is a comprehensive new revenue recognition model requiring a company to recognize revenue to depict the transfer of goods or services to a customer at an amount reflecting the consideration it expects to receive in exchange for those goods or services. While ASU 2014-09 specifically references contracts with customers, it may apply to certain other transactions such as the sale of real estate or equipment. ASU 2014-09 may be applied using either a full retrospective or a modified retrospective approach and is effective for fiscal years, and interim periods within those years, beginning after December 15, 2016, and early adoption is not permitted. On April 29, 2015, the FASB proposed a one-year deferral of the effective date for ASU 2014-09. The Company is evaluating the impact of this amendment on its financial position and results of operations.

In February 2015, the FASB issued ASU 2015-02 Amendments to the Consolidation Analysis. These amendments: (1) modify the evaluation of whether limited partnerships and similar legal entities are variable interest entities (“VIEs”) or voting interest entities; (2) eliminate the presumption that a general partner should consolidate a limited partnership; (3) affect the consolidation analysis of reporting entities that are involved with VIEs, particularly those that have fee arrangements and related party relationships; and (4) provide a scope exception from consolidation guidance for reporting entities with interests in legal entities that are required to comply with or operate in accordance with requirements that are similar to those in Rule 2a-7 of the Investment Company Act of 1940 for registered money market funds. ASU 2015-02 is effective for interim and annual reporting periods beginning after December 15, 2015. The Company is evaluating the impact of this amendment on its financial position and results of operations.

In April 2015, the FASB issued ASU 2015-03 Interest – Imputation of Interest. The amendments in this update require that debt issuance costs be presented in the balance sheet as a direct deduction from the carrying amount of a debt liability, consistent with debt discounts. This guidance is effective for interim and annual reporting periods beginning after December 15, 2015, with early adoption permitted. This guidance may be adopted retrospectively or under a modified retrospective method where the cumulative effect is recognized at the date of initial application. The Company is evaluating the impact of this amendment on its financial position and results of operations.

Note 3 — Mortgage loans

The following tables present information regarding the contractually required payments and the estimated cash flows expected to be collected as of the date of the acquisition and changes in the balance of the accretable yield ($ in thousands):

| 12 |

| Three months ended | Six months ended | Period from inception to | ||||||||||||||||||||||

| June 30, 2015 | June 30, 2015 | December 31, 2014 | ||||||||||||||||||||||

Re-performing | Non-performing | Re-performing | Non-performing | Re-performing | Non-performing | |||||||||||||||||||

| Contractually required principal and interest | $ | 332,571 | $ | 31,827 | $ | 486,603 | $ | 65,675 | $ | 393,657 | $ | 257,790 | ||||||||||||

| Non-accretable yield | (132,557 | ) | (18,598 | ) | (198,704 | ) | (38,317 | ) | (173,502 | ) | (184,096 | ) | ||||||||||||

| Expected cash flows to be collected | 200,014 | 13,229 | 287,899 | 27,358 | 220,155 | 73,694 | ||||||||||||||||||

| Accretable yield | (49,626 | ) | (4,185 | ) | (73,680 | ) | (8,038 | ) | (60,495 | ) | (22,071 | ) | ||||||||||||

| Fair value at acquisition | $ | 150,388 | $ | 9,044 | $ | 214,219 | $ | 19,320 | $ | 159,660 | $ | 51,623 | ||||||||||||

| Accretable yield | Three months ended | Six months ended | Period from inception to | |||||||||||||||||||||

June 30, 2015 | June 30, 2015 | December 31, 2014 | ||||||||||||||||||||||

Re-performing | Non-performing | Re-performing | Non-performing | Re-performing | Non-performing | |||||||||||||||||||

| Balance at beginning of period | $ | 74,045 | $ | 22,604 | $ | 54,940 | $ | 20,686 | $ | – | $ | – | ||||||||||||

| Accretable yield additions | 49,626 | 4,185 | 73,680 | 8,038 | 60,495 | 22,071 | ||||||||||||||||||

| Accretion | (7,739 | ) | (3,054 | ) | (12,688 | ) | (4,989 | ) | (5,555 | ) | (1,385 | ) | ||||||||||||

| Balance at end of period | $ | 115,932 | $ | 23,735 | $ | 115,932 | $ | 23,735 | $ | 54,940 | $ | 20,686 | ||||||||||||

During the three- and six-months ended June 30, 2015, the Company recognized $0.7 million and $1.0 million, respectively, for due diligence costs related to these and other transactions in loan transaction expense.

The following table sets forth the carrying value of its mortgage loans, and related UPB by delinquency status as of June 30, 2015 and December 31, 2014 ($ in thousands):

June 30, 2015 | December 31, 2014 | |||||||||||||||||||||||

Number of | Carrying | Unpaid | Number of | Carrying | Unpaid | |||||||||||||||||||

| Current | 1,123 | $ | 209,046 | $ | 267,983 | 439 | $ | 72,727 | $ | 94,993 | ||||||||||||||

| 30 | 406 | 66,969 | 87,292 | 237 | 36,954 | 53,739 | ||||||||||||||||||

| 60 | 194 | 29,611 | 39,647 | 99 | 13,849 | 17,766 | ||||||||||||||||||

| 90 | 534 | 77,407 | 107,345 | 352 | 53,987 | 76,691 | ||||||||||||||||||

| Foreclosure | 362 | 61,375 | 94,021 | 212 | 33,642 | 55,384 | ||||||||||||||||||

| Mortgage loans | 2,619 | $ | 444,408 | $ | 596,288 | 1,339 | $ | 211,159 | $ | 298,573 | ||||||||||||||

These balances do not include one loan in which we hold a 40.5% beneficial interest through an equity method investee.

As of June 30, 2015, the Company held 34 residential properties with a carrying value of $5.1 million that had been foreclosed.

The Company’s mortgage loans are secured by real estate. As such, the Company believes that the credit quality indicators for each of its mortgage loans are the timeliness of payments and the value of the underlying real estate. The Company categorizes mortgage loans as “re-performing” and as “non-performing.” The Company monitors the credit quality of the mortgage loans in its portfolio on an ongoing basis, principally by considering loan payment activity or delinquency status. In addition, the Company assesses the expected cash flows from the mortgage loans, the fair value of the underlying collateral and other factors, and evaluates whether and when it becomes probable that all amounts contractually due will not be collected.

| 13 |

Note 4 — Real estate assets, net

Real estate held for use

As of June 30, 2015, the Company had two REO properties having an aggregate carrying value of $0.1 million held for use as rentals. Both of these properties had been rented.

Real estate held-for-sale

As of June 30, 2015, the Company classified 54 REO properties having an aggregate carrying value of $9.0 million as real estate held for sale as they do not meet its residential rental property investment criteria.

Dispositions

During the three-months ended June 30, 2015, the Company disposed of two held-for-sale residential properties and recognized a loss of $7,000. During the six-months ended June 30, 2015, the Company disposed of three held-for-sale residential properties and recognized a loss of $9,000.

Note 5 — Fair value of financial instruments

The following tables set forth the fair value of financial assets and liabilities by level within the fair value hierarchy as of June 30, 2015 and December 31, 2014 ($ in thousands):

Level 1 | Level 2 | Level 3 | ||||||||||||||

June 30, 2015 | Carrying | Quoted prices | Observable | Unobservable | ||||||||||||

| Not recognized on consolidated balance sheet at fair value (assets) | ||||||||||||||||

| Mortgage loans | $ | 444,408 | — | — | $ | 501,369 | ||||||||||

| Not recognized on consolidated balance sheet at fair value (liabilities) | ||||||||||||||||

| Borrowings under repurchase agreement | 153,804 | — | $ | 153,804 | — | |||||||||||

| Secured borrowings | 116,349 | — | 116,349 | — | ||||||||||||

Level 1 | Level 2 | Level 3 | ||||||||||||||

December 31, 2014 | Carrying | Quoted prices | Observable | Unobservable | ||||||||||||

| Not recognized on consolidated balance sheet at fair value (assets) | ||||||||||||||||

| Mortgage loans | $ | 211,159 | — | — | $ | 235,623 | ||||||||||

| Not recognized on consolidated balance sheet at fair value (liabilities) | ||||||||||||||||

| Borrowings under repurchase agreement | 15,249 | — | $ | 15,249 | — | |||||||||||

| Secured borrowings | 84,679 | — | 84,679 | — | ||||||||||||

The Company has not transferred any assets from one level to another level during the three or six months ended June 30, 2015.

The carrying values of its cash and cash equivalents, related party receivables, accounts payable and accrued liabilities, related party payables and investments in the Manager and affiliate are equal to or approximate

| 14 |

fair value. Property held-for-sale is measured at cost at acquisition and subsequently measured at the lower of cost or fair value less cost to sell on a nonrecurring basis. The fair value of property held-for-sale is generally based on estimated market prices from an independently prepared appraisal, an independent BPO, or management’s judgment as to the selling price of similar properties. No properties held-for-sale were measured at fair value at June 30, 2015.

The fair value of mortgage loans is estimated using the Manager’s proprietary pricing model which estimates expected cash flows with the discount rate used in the present value calculation representing the estimated effective yield of the loan. The value of transfers of mortgage loans to real estate owned is estimated using BPOs.

The significant unobservable inputs used in the fair value measurement of the Company’s mortgage loans are the same as those used to calculate the acquisition price, including discount rates and loan resolution timelines. Significant changes to any of these inputs in isolation could result in a significant change to the fair value measurement. A decline in the discount rate in isolation would increase the fair value. An increase in the loan resolution timeline in isolation would decrease the fair value. The following table sets forth quantitative information about the significant unobservable inputs used to measure the fair value of the Company’s mortgage loans as of June 30, 2015:

|

Input |

Range of Values | |

| Equity discount rate – Re-performing loans | 8% - 14% | |

| Equity discount rate – Non-performing loans | 10% - 18% | |

| Cost of debt | 4.25% | |

| Loan resolution timelines – Re-performing loans (in years) | 4 - 7 | |

| Loan resolution timelines – Non-performing loans (in years) | 1.4 - 4 |

Note 6 — Unconsolidated affiliates

On December 5, 2014, the Company acquired a 40.5% interest in GA-E 2014-12, a Delaware trust, for $2.2 million. GA-E 2014-12 holds an economic interest in a single small-balance commercial loan secured by a commercial property in Portland, Oregon. At December 31, 2014, GA-E 2014-12 had a basis in the loan of $5.4 million. At June 30, 2015, GA-E 2014-12 had a basis in the loan of $5.6 million, and net income of $0.2 million for the three months ended, and $0.4 million for the six months ended June 30, 2015, of which 40.5% is the Company’s share. The Company accounts for this investment using the equity method.

Upon the closing of the Original Private Placement, the Company received a 19.8% equity interest in Thetis. At December 31, 2014, Thetis had total assets of $2.2 million and liabilities of $0.2 million. At June 30, 2015, Thetis had total assets of $2.8 million, liabilities of $0.3 million, and net income of $0.3 million for the three months ended, and $0.5 million for the six months ended June 30, 2015, of which 19.8% is the Company’s share. The Company accounts for its investment in Thetis using the equity method. Thetis is a privately held company and there is no public market for its securities.

Note 7 — Commitments and contingencies

The Company regularly enters into agreements to acquire additional mortgage loans and mortgage-related assets, subject to continuing diligence on such assets and other customary closing conditions. There can be no assurance that the Company will acquire any or all of the mortgage loans identified in any acquisition agreement as of the date of these consolidated financial statements, and it is possible that the terms of such acquisitions may change.

At June 30, 2015, we had commitments to purchase 158 re-performing mortgage loans secured by single and one-to-four family residences with aggregate UPB of $46.8 million and an estimated purchase price of $36.0 million.

Litigation, claims and assessments

From time to time, the Company may be involved in various claims and legal actions arising in the ordinary course of business. As of June 30, 2015, the Company was not a party to, and its properties were not

| 15 |

subject to, any pending or threatened legal proceedings that individually or in the aggregate, are expected to have a material impact on its financial condition, results of operations or cash flows.

Note 8 — Debt

Repurchase agreement

On November 25, 2014, the Company entered into a repurchase facility pursuant to which a newly formed Delaware statutory trust wholly owned by the operating partnership, AJX Mortgage Trust I, the “Seller,” will acquire, from time to time, pools of mortgage loans that are primarily secured by first liens on one-to-four family residential properties from its affiliates and/or third party sellers. The facility was amended on May 13, 2015 to increase the transaction limit. These mortgage loans will generally be sold from time to time by the operating partnership as the “Guarantor” to the Seller pursuant to the terms of a mortgage loan purchase agreement by and between the Guarantor, as seller, and the Seller, as purchaser, in accordance with the terms thereof. Pursuant to the Master Repurchase Agreement (the “MRA”), these mortgage loans, together with the Seller’s 100% ownership interests in its wholly owned subsidiary, a newly formed Delaware limited liability company (“REO I”), and any future REO subsidiaries wholly owned by the Seller and certain other property of the Seller, will be sold by the Seller to Nomura Corporate Funding Americas, LLC, as Buyer, from time to time, pursuant to one or more transactions, not exceeding $200 million, with a simultaneous agreement by the Seller to repurchase such mortgage loans and other property, as provided in the MRA. The obligations of the Seller are guaranteed by the operating partnership. Repurchases under this facility carry interest calculated based on a spread to one-month LIBOR and are fixed for the term of the borrowing. The purchase price for each mortgage loan or REO is generally equal to 65% of the acquisition price for such asset or the then current BPO for the asset. The difference between the market value of the asset and the amount of the repurchase agreement is the amount of equity the Company has in the position and is intended to provide the lender some protection against fluctuations of value in the collateral and/or the failure by the Company to repay the borrowing at maturity. The Company has effective control over the assets associated with this agreement and therefore it is accounted for as a financing arrangement. The facility termination date is November 24, 2015.

Gregory services these mortgage loans and the REO properties pursuant to the terms of a servicing agreement by and among the Servicer, the Seller, REO I and any other REO Subsidiary, which servicing agreement has the same fees and expenses terms as the Company’s servicing agreement described under Note 9 — Related Party Transactions. The operating partnership as Guarantor will provide to the Buyer a limited guaranty of certain losses incurred by the Buyer in connection with certain events and/or the Seller’s obligations under the MLPA, following the breach of certain covenants by the Seller or an REO Subsidiary related to their status as a special purpose entity, the occurrence of certain bad acts by the Seller Parties, the occurrence of certain insolvency events of the Seller or an REO Subsidiary or other events specified in the Guaranty. As security for its obligations under the Guaranty, the Guarantor will pledge the Trust Certificate representing the Guarantor’s 100% beneficial interest in the Seller. While the Guaranty establishes a master netting arrangement, the arrangement does not meet the criteria for offsetting. The amount outstanding on the Company’s repurchase facility and the carrying value of the Company’s loans pledged as collateral are presented as gross amounts in the Company’s balance sheets at June 30, 2015 and December 31, 2014. The following table sets forth the details of the repurchase agreement ($ in thousands):

| June 30, 2015 | December 31, 2014 | |||||||||||||||||||||||||||

| Maturity Date | Maximum borrowing capacity | Amount outstanding | Carrying value of collateral | Interest rate | Amount outstanding | Carrying value of collateral | Interest rate | |||||||||||||||||||||

| November 24, 2015 | $ | 200,000 | $ | 153,804 | $ | 241,689 | 4.00 | % | $ | 15,249 | $ | 23,460 | 4.00 | % | ||||||||||||||

Secured borrowings

From the commencement of operations to June 30, 2015, the Company has completed three securitizations pursuant to Rule 144A under the Securities Act. The securitizations are structured as debt financings and not REMIC sales, and the loans included in the securitizations remain on the Company’s balance sheet as the Company is the primary beneficiary of the securitization trusts, which are variable interest entities (“VIEs”). The securitization VIEs are structured as pass through entities that receive principal and interest on the underlying mortgages and distribute those payments to the holders of the notes. The Company’s exposure to the obligations of the VIEs is

| 16 |

generally limited to its investments in the entities. The notes that are issued by the securitization trusts are secured solely by the mortgages held by the applicable trusts and not by any of the Company’s other assets. The mortgage loans of the applicable trusts are the only source of repayment and interest on the notes issued by such trusts. The Company does not guarantee any of the obligations of the trusts under the terms of the agreement governing the notes or otherwise.

The Company’s securitizations are structured with Class A notes, Class B notes, and a trust certificate representing the residual interests in the mortgages. For each of the Company’s three securitizations, the Company has retained the Class B notes and the trust certificate. The Class A notes are senior, sequential pay, fixed rate notes. The Class B notes are subordinate, sequential pay, fixed rate notes with Class B-2 notes subordinate to the Class B-1 notes. If the Class A notes have not been redeemed by the payment date 36 months after issue, or otherwise paid in full by that date, an amount equal to the aggregate interest payment amount that accrued and would otherwise be paid to the Class B-1 and the Class B-2 notes will be paid as principal to the Class A notes on that date and each subsequent payment date until the Class A notes are paid in full. After the Class A notes are paid in full, the Class B-1 and Class B-2 notes will resume receiving their respective interest payment amounts and any interest that accrued but was not paid to the Class B notes while the Class A notes were outstanding. As the holder of the trust certificates, the Company is entitled to receive any remaining amounts in the trust after the Class A notes and Class B notes have been paid in full.

The following table sets forth the original terms of all securitization notes at their respective cutoff dates as of June 30, 2015:

| Issuing Trust/Issue Date | Security | Original Principal | Interest Rate | |||||||

| Ajax Mortgage Loan Trust 2014-A/ October 2014 | Class A notes due 2057(1) | $ | 45 million | 4.00 | % | |||||

| Class B-1 notes due 2057(2) | $ | 8 million | 5.19 | % | ||||||

| Class B-2 notes due 2057(2) | $ | 8 million | 5.19 | % | ||||||

| Trust certificates(3) | $ | 20.4 million | – | |||||||

| Ajax Mortgage Loan Trust 2014-B / November 2014 | Class A notes due 2054(1) | $ | 41.2 million | 3.85 | % | |||||

| Class B-1 notes due 2054(2) | $ | 13.7 million | 5.25 | % | ||||||

| Class B-2 notes due 2054(2) | $ | 13.7 million | 5.25 | % | ||||||

| Trust certificates(3) | $ | 22.9 million | – | |||||||

| Ajax Mortgage Loan Trust 2015-A / May 2015 | Class A notes due 2054(1) | $ | 35.6 million | 3.88 | % | |||||

| Class B-1 notes due 2054(2) | $ | 8.7 million | 5.25 | % | ||||||

| Class B-2 notes due 2054(2) | $ | 8.7 million | 5.25 | % | ||||||

| Trust certificates(3) | $ | 22.8 million | – | |||||||

| (1) | The Class A notes are senior, sequential pay, fixed rate notes. |

| (2) | The Class B notes are subordinate, sequential pay, fixed rate notes with Class B-2 notes subordinate to the Class B-1 notes. We have retained the Class B notes. |

| (3) | The trust certificate issued by the trust and the beneficial ownership of the trust are retained by Great Ajax Funding LLC as the depositor. As the holder of the trust certificate, we are entitled to receive any remaining amounts in the trust after the Class A notes and Class B notes have been paid in full. |

| 17 |

Servicing for the mortgage loans in 2014-A, 2014-B and 2015-A is provided by the Servicer at a servicing fee rate of 0.65% annually of UPB for re-performing loans and 1.25% annually of UPB for non-performing loans, and is paid monthly by us. The following table sets forth the status of the 2014-A, 2014-B and 2015-A notes held by others at the securitization cutoff date, at December 31, 2014 and at June 30, 2015 ($ in thousands):

| Balances at June 30, 2015 | Balances at December 31, 2014 | Original balances at securitization cutoff date | ||||||||||||||||||||||

| Class of Notes | Carrying value of mortgages | Bond principal balance | Carrying value of mortgages | Bond principal balance | Mortgage UPB | Bond principal balance | ||||||||||||||||||

| 2014-A | $ | 58,313 | $ | 41,681 | $ | 58,905 | $ | 44,016 | $ | 81,405 | $ | 45,000 | ||||||||||||

| 2014-B | 68,379 | 39,344 | 68,654 | 40,663 | 91,535 | 41,191 | ||||||||||||||||||

| 2015-A | 53,116 | 35,324 | — | — | 75,835 | 35,643 | ||||||||||||||||||

| $ | 179,808 | $ | 116,349 | $ | 127,559 | $ | 84,679 | $ | 248,775 | $ | 121,834 | |||||||||||||

The Company’s obligations under its secured borrowings are not fixed, and the payments on these borrowings are predicated upon cash flows received on the underlying mortgage loans. Accordingly, a projection of contractual maturities over the next five years is inapplicable.

Note 9 — Related party transactions

Our consolidated statement of income included the following significant related party transactions ($ in thousands):

Three months ended June 30, 2015 | Six months ended June 30, 2015 | |||||||||||||||

Amount | Counterparty | Consolidated Statement | Amount | Counterparty | Consolidated Statement | |||||||||||

| Management fee | $ | 856 | Thetis | Related party expense – management fee | $ | 1,602 | Thetis | Related party expense – management fee | ||||||||

| Loan servicing fees | 851 | Gregory | Related party expense – loan servicing fees | 1,507 | Gregory | Related party expense – loan servicing fees | ||||||||||

| Due diligence and related loan acquisition costs | 1 | Gregory | Loan transaction expense | 19 | Gregory | Loan transaction expense | ||||||||||

| Expense reimbursements | - | Aspen Yo | Professional fees | 3 | Aspen Yo | Professional fees | ||||||||||

Management Agreement

On July 8, 2014, the Company entered into a 15-year management agreement (the “Management Agreement”) with the Manager. Under the Management Agreement, the Manager implements the Company’s business strategy and manages the Company’s business and investment activities and day-to-day operations, subject to oversight by the Company’s board of directors. Among other services, the Manager, directly or through Aspen affiliates, provides the Company with a management team and necessary administrative and support personnel. The Company does not currently have any employees and does not expect to have any employees in the foreseeable future. Each of the Company’s executive officers is an employee or officer, or both, of the Manager or the Company’s Servicer.

Under the Management Agreement, the Company pays both a base management fee and an incentive fee to the Manager.

The Base Management Fee equals 1.5% of our stockholders’ equity per annum and calculated and payable quarterly in arrears. For purposes of calculating the management fee, the Company’s stockholders’ equity means: (a) the sum of (i) the net proceeds from any issuances of common stock or other equity securities issued by the Company or the operating partnership (without double counting) since inception (allocated on a pro rata daily basis

| 18 |

for such issuances during the fiscal quarter of any such issuance), and (ii) the Company’s and the operating partnership’s (without double counting) retained earnings calculated in accordance with U.S. GAAP at the end of the most recently completed fiscal quarter (without taking into account any non-cash equity compensation expense incurred in current or prior periods), less (A) any amount that the Company or the operating partnership pays to repurchase shares of common stock or OP Units since inception, (B) any unrealized gains and losses and other non-cash items that have affected consolidated stockholders’ equity as reported in the Company’s financial statements prepared in accordance with U.S. GAAP, and (C) one-time events pursuant to changes in U.S. GAAP, and certain non-cash items not otherwise described above, in each case after discussions between the Manager and the Company’s independent directors and approval by a majority of the Company’s independent directors. As a result, the Company’s stockholders’ equity, for purposes of calculating the management fee, could be greater or less than the amount of stockholders’ equity shown on the Company’s consolidated financial statements. 50% of the base management fee is payable in shares of the Company’s common stock so long as the ownership of such additional number of shares by the Manager would not violate the 9.8% stock ownership limit set forth in the Company’s charter, and the balance is payable in cash. The common stock will be determined using the higher of the most recently reported book value or the average of the closing prices of our common stock on the NYSE on the five business days after the date on which the most recent regular quarterly dividend to holders of our common stock is paid. The Manager has agreed to hold any shares of common stock received by it as payment of the base management fee for at least three years from the date such shares of common stock are received by it.

The Manager is also entitled to an incentive management fee that is payable quarterly in arrears in cash in an amount equal to one-fourth of 20% of the dollar amount by which (i) the sum of (A) the aggregate cash dividends, if any, declared out of the REIT taxable income of the Company by the Company’s Board of Directors payable to the holders of the Company’s common stock and (B) the aggregate cash distributions, if any, declared out of the REIT taxable income of the operating partnership (without duplication) by the operating partnership payable to holders of OP Units (other than any OP Units held by the Company as a limited partner) annualized, or the Annualized Dividends and Distributions, in respect of such calendar quarter exceeds (ii) the product of (1) the book value per share of the Company’s common stock as of the end of each such quarter multiplied by the number of shares of the Company’s common stock and OP Units (other than any OP Units held by the Company as a limited partner) outstanding as of the end of such calendar quarter and (2) 8%. Notwithstanding the foregoing, no incentive fee will be payable to the Manager with respect to any calendar quarter unless its cumulative core earnings, as defined in the agreement, is greater than zero for the most recently completed eight calendar quarters, or the number of completed calendar quarters since the closing date of the Original Private Placement, whichever is less.

The Company also reimburses the Manager for all third-party, out-of-pocket costs incurred by the Manager for managing its business, including third-party diligence and valuation consultants, legal expenses, auditors and other financial services. The Company will not reimburse the Manager for lease costs or salaries and expenses of employees of the Manager. The reimbursement obligation is not subject to any dollar limitation. Expenses will be reimbursed in cash on a monthly basis.

The Company will be required to pay the Manager a termination fee in the event that the Management Agreement is terminated as a result of (i) a termination by the Company without cause, (ii) its decision not to renew the Management Agreement upon the determination of at least two thirds of the Company’s independent directors for reasons including the failure to agree on revised compensation, (iii) a termination by the Manager as a result of the Company becoming regulated as an “investment company” under the Investment Company Act of 1940 (other than as a result of the acts or omissions of the Manager in violation of investment guidelines approved by the Company’s board of directors), or (iv) a termination by the Manager if we default in the performance of any material term of the Management Agreement (subject to a notice and cure period). The termination fee will be equal to twice the combined base fee and incentive fees payable to the Manager during the 12-month period ended as of the end of the most recently completed fiscal quarter prior to the date of termination.

Servicing Agreement

On July 8, 2014, the Company entered into a 15-year servicing agreement (the “Servicing Agreement”) with the Servicer. The Company’s overall servicing costs under the servicing agreement will vary based on the types of assets serviced.

| 19 |

Servicing fees range from 0.65% to 1.25% annually of UPB (or the fair market value or purchase price of REO the Company owns or acquires), and are paid monthly. The total fees incurred by us for these services depend upon the UPB and type of mortgage loans that Gregory services pursuant to the terms of the servicing agreement. The fees are determined based on the loan’s status at acquisition and do not change if a performing loan becomes non-performing or vice versa.

The Company will also reimburse Gregory for all customary, reasonable and necessary out-of-pocket costs and expenses incurred in the performance of its obligations, including the actual cost of any repairs and renovations to REO properties. The total fees incurred by us for these services will be dependent upon the property value, previous UPB of the relevant loan, and the number of REO properties.

If the Management Agreement has been terminated other than for cause and/or the Servicer terminates the servicing agreement, the Company will be required to pay a termination fee equal to the aggregate servicing fees payable under the servicing agreement for the immediate preceding 12-month period.

Trademark Licenses

Aspen Yo has granted the Company a non-exclusive, non-transferable, non-sublicensable, royalty-free license to use the name “Great Ajax” and the related logo. The Company also has a similar license to use the name “Thetis.” The agreement has no specified term. If the Management Agreement expires or is terminated, the trademark license agreement will terminate within 30 days. In the event that this agreement is terminated, all rights and licenses granted thereunder, including, but not limited to, the right to use “Great Ajax” in its name will terminate. Aspen Yo also granted to the Manager a substantially identical non-exclusive, non-transferable, non-sublicensable, royalty-free license to use of the name “Thetis.”

Note 10 — Stock-based payments and director fees

Pursuant to the terms of the Management Agreement, the Company pays 50% of the base fee to the Manager in shares of its common stock with the number of shares determined based on the higher of the most recently reported book value or the average of the closing prices of our common stock on the NYSE on the five business days after the date on which the most recent regular quarterly dividend to holders of our common stock is paid. The Company paid the Manager a base fee for the quarter ended June 30, 2015 of $0.9 million of which the Company paid half, or $0.4 million, in 29,790 shares of its common stock. The shares issued to the Manager are restricted securities subject to transfer restrictions, and were issued in a private placement transaction on July 28, 2015.

In addition, each of the Company’s independent directors receives an annual retainer of $50,000, payable quarterly, half of which is paid in shares of the Company’s common stock on the same basis as the stock portion of the management fee payable to the Manager and half in cash. The following table sets forth the Company’s stock-based management fees and independent director fees ($ in thousands except share amounts):

Management fees and director fees

For the three months ended | For the six months ended | |||||||||||||||

Number of | Amount of | Number of | Amount of | |||||||||||||

| Management fees | 29,790 | $ | 441 | 55,877 | $ | 814 | ||||||||||

| Independent director fees | 1,740 | 25 | 3,488 | 50 | ||||||||||||

| 31,530 | $ | 466 | 59,365 | $ | 864 | |||||||||||

(1) All management fees and independent director fees are fully expensed in the period in which they are incurred.

| 20 |