000160980412/312019FYFALSEP1YP1YP2YP3Y33.3333.3333.33P6YP1Y00016098042019-01-012019-12-31iso4217:USD00016098042019-06-30xbrli:shares00016098042020-02-1900016098042019-12-310001609804us-gaap:AdditionalPaidInCapitalMember2019-01-012019-12-3100016098042018-01-012018-12-3100016098042017-01-012017-12-31iso4217:USDxbrli:shares00016098042018-12-3100016098042017-12-3100016098042016-12-310001609804us-gaap:CommonStockMember2016-12-310001609804us-gaap:TreasuryStockMember2016-12-310001609804us-gaap:AdditionalPaidInCapitalMember2016-12-310001609804us-gaap:RetainedEarningsMember2016-12-310001609804us-gaap:AccumulatedOtherComprehensiveIncomeMember2016-12-310001609804us-gaap:RetainedEarningsMember2017-01-012017-12-310001609804us-gaap:AccumulatedOtherComprehensiveIncomeMember2017-01-012017-12-310001609804us-gaap:AdditionalPaidInCapitalMember2017-01-012017-12-310001609804us-gaap:CommonStockMember2017-12-310001609804us-gaap:TreasuryStockMember2017-12-310001609804us-gaap:AdditionalPaidInCapitalMember2017-12-310001609804us-gaap:RetainedEarningsMember2017-12-310001609804us-gaap:AccumulatedOtherComprehensiveIncomeMember2017-12-310001609804us-gaap:RetainedEarningsMember2018-01-012018-12-310001609804us-gaap:AccumulatedOtherComprehensiveIncomeMember2018-01-012018-12-310001609804us-gaap:AdditionalPaidInCapitalMember2018-01-012018-12-310001609804us-gaap:CommonStockMember2018-01-012018-12-310001609804us-gaap:TreasuryStockMember2018-01-012018-12-310001609804us-gaap:CommonStockMember2018-12-310001609804us-gaap:TreasuryStockMember2018-12-310001609804us-gaap:AdditionalPaidInCapitalMember2018-12-310001609804us-gaap:RetainedEarningsMember2018-12-310001609804us-gaap:AccumulatedOtherComprehensiveIncomeMember2018-12-310001609804us-gaap:RetainedEarningsMember2019-01-012019-12-310001609804us-gaap:AccumulatedOtherComprehensiveIncomeMember2019-01-012019-12-310001609804us-gaap:CommonStockMember2019-01-012019-12-310001609804us-gaap:TreasuryStockMember2019-01-012019-12-310001609804us-gaap:CommonStockMember2019-12-310001609804us-gaap:TreasuryStockMember2019-12-310001609804us-gaap:AdditionalPaidInCapitalMember2019-12-310001609804us-gaap:RetainedEarningsMember2019-12-310001609804us-gaap:AccumulatedOtherComprehensiveIncomeMember2019-12-3100016098042019-03-31oec:assetxbrli:pure0001609804oec:RubberCarbonBlackSegmentMemberoec:TenLargestCustomersMemberus-gaap:CustomerConcentrationRiskMemberus-gaap:SalesRevenueNetMember2019-01-012019-12-310001609804oec:SpecialtyCarbonBlackSegmentMemberoec:TenLargestCustomersMemberus-gaap:CustomerConcentrationRiskMemberus-gaap:SalesRevenueNetMember2019-01-012019-12-310001609804oec:TenLargestCustomersMemberus-gaap:CustomerConcentrationRiskMemberus-gaap:SalesRevenueNetMember2019-01-012019-12-31iso4217:EUR0001609804us-gaap:RevolvingCreditFacilityMember2019-12-31oec:financial_institution0001609804us-gaap:RevolvingCreditFacilityMember2019-01-012019-12-310001609804us-gaap:TrademarksAndTradeNamesMember2019-01-012019-12-310001609804oec:DevelopedTechnologyandPatentsMember2019-01-012019-12-310001609804srt:MinimumMemberus-gaap:OtherIntangibleAssetsMember2019-01-012019-12-310001609804srt:MaximumMemberus-gaap:OtherIntangibleAssetsMember2019-01-012019-12-310001609804oec:EvonikMemberus-gaap:CustomerRelationshipsMember2019-01-012019-12-310001609804oec:SocitDuNoirDActylneDeLAubetteSASMemberus-gaap:CustomerRelationshipsMember2019-01-012019-12-31oec:reporting_unitoec:segment0001609804srt:MinimumMemberus-gaap:BuildingMember2019-01-012019-12-310001609804srt:MaximumMemberus-gaap:BuildingMember2019-01-012019-12-310001609804srt:MinimumMemberoec:PlantAndMachineryMember2019-01-012019-12-310001609804srt:MaximumMemberoec:PlantAndMachineryMember2019-01-012019-12-310001609804srt:MinimumMemberus-gaap:FurnitureAndFixturesMember2019-01-012019-12-310001609804srt:MaximumMemberus-gaap:FurnitureAndFixturesMember2019-01-012019-12-3100016098042019-01-010001609804oec:CologneGermanyMember2019-12-310001609804us-gaap:LandMember2019-12-310001609804us-gaap:LandMember2018-12-310001609804oec:LandRightsAndBuildingsMember2019-12-310001609804oec:LandRightsAndBuildingsMember2018-12-310001609804oec:PlantAndMachineryMember2019-12-310001609804oec:PlantAndMachineryMember2018-12-310001609804us-gaap:FurnitureAndFixturesMember2019-12-310001609804us-gaap:FurnitureAndFixturesMember2018-12-310001609804oec:PrepaymentsAndConstructionInProgressMember2019-12-310001609804oec:PrepaymentsAndConstructionInProgressMember2018-12-310001609804oec:TermLoanFacilityMemberoec:TermLoanMember2019-12-310001609804oec:TermLoanFacilityMemberoec:TermLoanMember2018-12-310001609804oec:TermLoanFacilityMemberoec:TermLoanMember2014-07-250001609804oec:TermLoanUSDMemberoec:TermLoanMember2014-07-250001609804oec:TermLoanEURMemberoec:TermLoanMember2014-07-250001609804us-gaap:LondonInterbankOfferedRateLIBORMemberoec:TermLoanUSDMembersrt:MinimumMemberoec:TermLoanMember2014-07-252014-07-250001609804oec:TermLoanEURMemberoec:EuroInterbankOfferedRateEURIBORMembersrt:MinimumMemberoec:TermLoanMember2014-07-252014-07-250001609804oec:TermLoanEURMemberoec:EuroInterbankOfferedRateEURIBORMembersrt:MaximumMemberoec:TermLoanMember2014-07-252014-07-250001609804us-gaap:LondonInterbankOfferedRateLIBORMemberoec:TermLoanUSDMembersrt:MaximumMemberoec:TermLoanMember2014-07-252014-07-250001609804us-gaap:LondonInterbankOfferedRateLIBORMemberoec:TermLoanUSDMemberoec:TermLoanMember2014-07-252014-07-250001609804oec:TermLoanEURMemberoec:EuroInterbankOfferedRateEURIBORMemberoec:TermLoanMember2014-07-252014-07-250001609804oec:TermLoanFacilityMemberoec:TermLoanMember2014-07-252014-07-250001609804oec:TermLoanEURMemberoec:TermLoanMember2015-01-012017-12-310001609804oec:TermLoanUSDMemberoec:TermLoanMember2015-01-012017-12-310001609804us-gaap:LondonInterbankOfferedRateLIBORMemberoec:TermLoanUSDMemberoec:TermLoanMember2019-01-012019-12-310001609804oec:TermLoanEURMemberoec:EuroInterbankOfferedRateEURIBORMemberoec:TermLoanMember2019-01-012019-12-310001609804oec:TermLoanFacilityMemberoec:TermLoanMember2019-01-012019-12-310001609804oec:TermLoanFacilityMemberoec:TermLoanMember2018-01-012018-12-310001609804oec:TermLoanFacilityMemberoec:TermLoanMember2017-01-012017-12-310001609804oec:TermLoanFacilityMemberoec:TermLoanMember2016-01-012016-12-310001609804us-gaap:CashFlowHedgingMemberus-gaap:CrossCurrencyInterestRateContractMemberus-gaap:DesignatedAsHedgingInstrumentMember2018-05-110001609804oec:TermLoanFacilityMemberoec:TermLoanMember2018-05-112018-05-110001609804us-gaap:CurrencySwapMemberus-gaap:NetInvestmentHedgingMemberus-gaap:DesignatedAsHedgingInstrumentMember2015-01-010001609804us-gaap:CurrencySwapMemberus-gaap:NetInvestmentHedgingMemberus-gaap:DesignatedAsHedgingInstrumentMember2019-12-310001609804us-gaap:RevolvingCreditFacilityMember2014-07-250001609804us-gaap:RevolvingCreditFacilityMembersrt:MinimumMemberoec:EURIBORAndLIBORMember2014-07-252014-07-250001609804srt:MaximumMemberus-gaap:RevolvingCreditFacilityMemberoec:EURIBORAndLIBORMember2014-07-252014-07-250001609804us-gaap:RevolvingCreditFacilityMember2017-05-042017-05-040001609804us-gaap:RevolvingCreditFacilityMember2017-05-052017-05-050001609804us-gaap:RevolvingCreditFacilityMember2017-05-050001609804us-gaap:RevolvingCreditFacilityMember2019-04-022019-04-020001609804us-gaap:RevolvingCreditFacilityMember2019-04-010001609804us-gaap:RevolvingCreditFacilityMember2019-04-020001609804us-gaap:RevolvingCreditFacilityMemberus-gaap:EurodollarMember2019-04-022019-04-020001609804srt:MaximumMemberus-gaap:RevolvingCreditFacilityMember2019-04-020001609804us-gaap:RevolvingCreditFacilityMembersrt:MinimumMember2019-04-020001609804us-gaap:RevolvingCreditFacilityMemberus-gaap:EurodollarMember2019-04-012019-04-010001609804us-gaap:RevolvingCreditFacilityMember2018-01-012018-12-310001609804us-gaap:RevolvingCreditFacilityMember2018-12-310001609804oec:DeutscheBankAGMember2019-01-012019-12-310001609804oec:DeutscheBankAGMember2018-01-012018-12-310001609804oec:UnicreditMember2019-01-012019-12-310001609804oec:UnicreditMember2018-01-012018-12-310001609804oec:TermLoanFacilityMember2019-12-310001609804oec:SocitDuNoirDActylneDeLAubetteSASMember2018-10-310001609804oec:SocitDuNoirDActylneDeLAubetteSASMember2018-10-312018-10-310001609804oec:SocitDuNoirDActylneDeLAubetteSASMembersrt:ScenarioPreviouslyReportedMember2018-10-310001609804oec:SocitDuNoirDActylneDeLAubetteSASMember2019-10-012019-12-310001609804oec:SocitDuNoirDActylneDeLAubetteSASMemberoec:FairValueAdjustmentToAssetsAndRelatedDeferredTaxLiabilityMember2019-10-012019-12-310001609804oec:RubberMember2017-12-310001609804oec:SpecialtiesMember2017-12-310001609804oec:RubberMember2018-01-012018-12-310001609804oec:SpecialtiesMember2018-01-012018-12-310001609804oec:RubberMember2018-12-310001609804oec:SpecialtiesMember2018-12-310001609804oec:SpecialtiesMember2019-01-012019-12-310001609804oec:RubberMember2019-01-012019-12-310001609804oec:RubberMember2019-12-310001609804oec:SpecialtiesMember2019-12-310001609804oec:DevelopedTechnologyandPatentsMember2019-12-310001609804oec:DevelopedTechnologyandPatentsMember2018-12-310001609804us-gaap:CustomerRelationshipsMember2019-12-310001609804us-gaap:CustomerRelationshipsMember2018-12-310001609804us-gaap:TrademarksMember2019-12-310001609804us-gaap:TrademarksMember2018-12-310001609804us-gaap:ContractBasedIntangibleAssetsMember2019-12-310001609804us-gaap:ContractBasedIntangibleAssetsMember2018-12-310001609804us-gaap:OtherIntangibleAssetsMember2019-12-310001609804us-gaap:OtherIntangibleAssetsMember2018-12-310001609804srt:MinimumMember2019-01-012019-12-310001609804srt:MaximumMember2019-01-012019-12-310001609804us-gaap:FairValueInputsLevel2Member2019-12-310001609804us-gaap:FairValueInputsLevel2Member2018-12-310001609804oec:CreditFacilityTermLoanMemberus-gaap:FairValueInputsLevel2Member2019-12-310001609804oec:CreditFacilityTermLoanMemberus-gaap:FairValueInputsLevel2Member2018-12-310001609804us-gaap:FairValueInputsLevel2Memberoec:LocalBankLoanMember2019-12-310001609804us-gaap:FairValueInputsLevel2Memberoec:LocalBankLoanMember2018-12-310001609804us-gaap:CashFlowHedgingMemberoec:EuroInterestRateCapStartDate2014Memberus-gaap:DesignatedAsHedgingInstrumentMember2014-11-280001609804us-gaap:CashFlowHedgingMemberoec:EuroInterestRateCapStartDate2014Memberus-gaap:DesignatedAsHedgingInstrumentMember2014-07-250001609804us-gaap:CashFlowHedgingMemberoec:USDInterestRateCapStartDate2014Memberus-gaap:DesignatedAsHedgingInstrumentMember2014-11-280001609804us-gaap:CashFlowHedgingMemberoec:USDInterestRateCapStartDate2014Memberus-gaap:DesignatedAsHedgingInstrumentMember2014-07-250001609804us-gaap:CashFlowHedgingMemberoec:EuroInterestRateCapStartDate2014Memberoec:ThreeMonthEURIBORMemberus-gaap:DesignatedAsHedgingInstrumentMember2014-07-250001609804us-gaap:CashFlowHedgingMemberoec:ThreeMonthUSDLIBORMemberoec:USDInterestRateCapStartDate2014Memberus-gaap:DesignatedAsHedgingInstrumentMember2014-07-250001609804us-gaap:CashFlowHedgingMemberus-gaap:CrossCurrencyInterestRateContractMemberus-gaap:DesignatedAsHedgingInstrumentMember2018-05-150001609804us-gaap:GeographicConcentrationRiskMemberoec:ProjectedBenefitPensionObligationMembercountry:DE2019-01-012019-12-310001609804us-gaap:GeographicConcentrationRiskMemberoec:ProjectedBenefitPensionObligationMembercountry:DE2018-01-012018-12-31oec:program0001609804country:FR2016-01-012016-12-310001609804us-gaap:PensionPlansDefinedBenefitMember2019-12-310001609804us-gaap:OtherPostretirementBenefitPlansDefinedBenefitMember2019-12-310001609804us-gaap:PensionPlansDefinedBenefitMember2018-12-310001609804us-gaap:DefinedBenefitPlanEquitySecuritiesMember2019-12-310001609804us-gaap:DefinedBenefitPlanEquitySecuritiesMember2018-12-310001609804us-gaap:DefinedBenefitPlanDebtSecurityMember2019-12-310001609804us-gaap:DefinedBenefitPlanDebtSecurityMember2018-12-310001609804oec:DefinedBenefitPlanOtherSecuritiesMember2019-12-310001609804oec:DefinedBenefitPlanOtherSecuritiesMember2018-12-310001609804us-gaap:RestrictedStockUnitsRSUMember2019-01-012019-12-310001609804us-gaap:RestrictedStockUnitsRSUMemberoec:ShareBasedPaymentArrangementEmployeeNewHireSignOnMemberoec:ExecutiveCommitteeMember2019-01-012019-12-310001609804us-gaap:RestrictedStockUnitsRSUMemberoec:ShareBasedPaymentArrangementEmployeeNewHireSignOnMemberus-gaap:ShareBasedCompensationAwardTrancheOneMemberoec:ExecutiveCommitteeMember2019-01-012019-12-310001609804us-gaap:RestrictedStockUnitsRSUMemberoec:ShareBasedPaymentArrangementEmployeeNewHireSignOnMemberus-gaap:ShareBasedCompensationAwardTrancheTwoMemberoec:ExecutiveCommitteeMember2019-01-012019-12-310001609804us-gaap:RestrictedStockUnitsRSUMemberus-gaap:ShareBasedCompensationAwardTrancheThreeMemberoec:ShareBasedPaymentArrangementEmployeeNewHireSignOnMemberoec:ExecutiveCommitteeMember2019-01-012019-12-310001609804oec:TwoThousandFifteenPlanMember2019-01-012019-12-310001609804oec:TwoThousandFifteenPlanMember2018-01-012018-12-310001609804oec:TwoThousandFifteenPlanMember2017-01-012017-12-310001609804oec:TwoThousandSixteenPlanMember2019-01-012019-12-310001609804oec:TwoThousandSixteenPlanMember2018-01-012018-12-310001609804oec:TwoThousandSixteenPlanMember2017-01-012017-12-310001609804oec:TwoThousandSeventeenPlanMember2019-01-012019-12-310001609804oec:TwoThousandSeventeenPlanMember2018-01-012018-12-310001609804oec:TwoThousandSeventeenPlanMember2017-01-012017-12-310001609804oec:A2018PanIncentiveMember2019-01-012019-12-310001609804oec:A2018PanIncentiveMember2018-01-012018-12-310001609804oec:A2018PanIncentiveMember2017-01-012017-12-310001609804oec:A2018PlanPaymentTransactionMember2019-01-012019-12-310001609804oec:A2018PlanPaymentTransactionMember2018-01-012018-12-310001609804oec:A2018PlanPaymentTransactionMember2017-01-012017-12-310001609804oec:A2019PlanCEOIncentiveMember2019-01-012019-12-310001609804oec:A2019PlanCEOIncentiveMember2018-01-012018-12-310001609804oec:A2019PlanCEOIncentiveMember2017-01-012017-12-310001609804oec:A2019PlanMember2019-01-012019-12-310001609804oec:A2019PlanMember2018-01-012018-12-310001609804oec:A2019PlanMember2017-01-012017-12-310001609804oec:TwoThousandSixteenPlanMemberus-gaap:PerformanceSharesMember2018-12-310001609804oec:TwoThousandSixteenPlanMemberus-gaap:PerformanceSharesMember2019-01-012019-12-310001609804oec:TwoThousandSixteenPlanMemberus-gaap:PerformanceSharesMember2019-04-012019-04-300001609804oec:TwoThousandSixteenPlanMemberus-gaap:PerformanceSharesMember2019-12-310001609804oec:TwoThousandSeventeenPlanMemberus-gaap:PerformanceSharesMember2018-12-310001609804oec:TwoThousandSeventeenPlanMemberus-gaap:PerformanceSharesMember2019-01-012019-12-310001609804oec:TwoThousandSeventeenPlanMemberus-gaap:PerformanceSharesMember2019-12-310001609804us-gaap:PerformanceSharesMemberoec:TwoThousandEighteenPlanMember2018-12-310001609804us-gaap:PerformanceSharesMemberoec:TwoThousandEighteenPlanMember2019-01-012019-12-310001609804us-gaap:PerformanceSharesMemberoec:TwoThousandEighteenPlanMember2019-12-310001609804oec:TwoThousandNineteenPlanMemberus-gaap:PerformanceSharesMember2018-12-310001609804oec:TwoThousandNineteenPlanMemberus-gaap:PerformanceSharesMember2019-01-012019-12-310001609804oec:TwoThousandNineteenPlanMemberus-gaap:PerformanceSharesMember2019-12-310001609804us-gaap:PerformanceSharesMember2018-12-310001609804us-gaap:PerformanceSharesMember2019-01-012019-12-310001609804us-gaap:PerformanceSharesMember2019-12-310001609804us-gaap:PerformanceSharesMember2017-12-310001609804us-gaap:PerformanceSharesMember2018-01-012018-12-310001609804us-gaap:PerformanceSharesMember2016-12-310001609804us-gaap:PerformanceSharesMember2017-01-012017-12-310001609804us-gaap:RestrictedStockUnitsRSUMemberoec:ShareBasedPaymentArrangementEmployeeNewHireSignOnMemberoec:TwoThousandEighteenPlanMember2018-12-310001609804us-gaap:RestrictedStockUnitsRSUMemberoec:ShareBasedPaymentArrangementEmployeeNewHireSignOnMemberoec:TwoThousandEighteenPlanMember2019-01-012019-12-310001609804us-gaap:RestrictedStockUnitsRSUMemberoec:ShareBasedPaymentArrangementEmployeeNewHireSignOnMemberoec:TwoThousandEighteenPlanMember2019-12-310001609804us-gaap:RestrictedStockUnitsRSUMemberoec:TwoThousandNineteenPlanMemberoec:ShareBasedPaymentArrangementEmployeeNewHireSignOnMember2018-12-310001609804us-gaap:RestrictedStockUnitsRSUMemberoec:TwoThousandNineteenPlanMemberoec:ShareBasedPaymentArrangementEmployeeNewHireSignOnMember2019-01-012019-12-310001609804us-gaap:RestrictedStockUnitsRSUMemberoec:TwoThousandNineteenPlanMemberoec:ShareBasedPaymentArrangementEmployeeNewHireSignOnMember2019-12-310001609804oec:ShareBasedPaymentArrangementEmployeeExistingEmployeesMemberus-gaap:RestrictedStockUnitsRSUMemberoec:TwoThousandNineteenPlanMember2018-12-310001609804oec:ShareBasedPaymentArrangementEmployeeExistingEmployeesMemberus-gaap:RestrictedStockUnitsRSUMemberoec:TwoThousandNineteenPlanMember2019-01-012019-12-310001609804oec:ShareBasedPaymentArrangementEmployeeExistingEmployeesMemberus-gaap:RestrictedStockUnitsRSUMemberoec:TwoThousandNineteenPlanMember2019-12-310001609804us-gaap:RestrictedStockUnitsRSUMember2018-12-310001609804us-gaap:RestrictedStockUnitsRSUMember2019-12-310001609804us-gaap:RestrictedStockUnitsRSUMember2017-12-310001609804us-gaap:RestrictedStockUnitsRSUMember2018-01-012018-12-310001609804us-gaap:RestrictedStockUnitsRSUMember2016-12-310001609804us-gaap:RestrictedStockUnitsRSUMember2017-01-012017-12-310001609804us-gaap:RestrictedStockMemberus-gaap:ShareBasedPaymentArrangementNonemployeeMember2019-12-310001609804us-gaap:PerformanceSharesMemberoec:TwoThousandFifteenPlanMember2018-04-012018-04-300001609804us-gaap:CostOfSalesMember2019-01-012019-12-310001609804us-gaap:CostOfSalesMember2018-01-012018-12-310001609804us-gaap:CostOfSalesMember2017-01-012017-12-310001609804us-gaap:SellingAndMarketingExpenseMember2019-01-012019-12-310001609804us-gaap:SellingAndMarketingExpenseMember2018-01-012018-12-310001609804us-gaap:SellingAndMarketingExpenseMember2017-01-012017-12-310001609804us-gaap:GeneralAndAdministrativeExpenseMember2019-01-012019-12-310001609804us-gaap:GeneralAndAdministrativeExpenseMember2018-01-012018-12-310001609804us-gaap:GeneralAndAdministrativeExpenseMember2017-01-012017-12-310001609804us-gaap:ResearchAndDevelopmentExpenseMember2019-01-012019-12-310001609804us-gaap:ResearchAndDevelopmentExpenseMember2018-01-012018-12-310001609804us-gaap:ResearchAndDevelopmentExpenseMember2017-01-012017-12-310001609804us-gaap:RestrictedStockUnitsRSUMemberus-gaap:ShareBasedCompensationAwardTrancheOneMember2019-01-012019-12-310001609804us-gaap:RestrictedStockUnitsRSUMemberus-gaap:ShareBasedCompensationAwardTrancheTwoMember2019-01-012019-12-310001609804us-gaap:RestrictedStockUnitsRSUMemberus-gaap:ShareBasedCompensationAwardTrancheThreeMember2019-01-012019-12-310001609804us-gaap:EmployeeSeveranceMember2016-12-310001609804us-gaap:FacilityClosingMember2016-12-310001609804oec:GroundRemediationCostsRelatedToRestructuringMember2016-12-310001609804us-gaap:OtherRestructuringMember2016-12-310001609804us-gaap:EmployeeSeveranceMember2017-01-012017-12-310001609804us-gaap:FacilityClosingMember2017-01-012017-12-310001609804oec:GroundRemediationCostsRelatedToRestructuringMember2017-01-012017-12-310001609804us-gaap:OtherRestructuringMember2017-01-012017-12-310001609804us-gaap:EmployeeSeveranceMember2017-12-310001609804us-gaap:FacilityClosingMember2017-12-310001609804oec:GroundRemediationCostsRelatedToRestructuringMember2017-12-310001609804us-gaap:OtherRestructuringMember2017-12-310001609804us-gaap:EmployeeSeveranceMember2018-01-012018-12-310001609804us-gaap:FacilityClosingMember2018-01-012018-12-310001609804oec:GroundRemediationCostsRelatedToRestructuringMember2018-01-012018-12-310001609804us-gaap:OtherRestructuringMember2018-01-012018-12-310001609804us-gaap:EmployeeSeveranceMember2018-12-310001609804us-gaap:FacilityClosingMember2018-12-310001609804oec:GroundRemediationCostsRelatedToRestructuringMember2018-12-310001609804us-gaap:OtherRestructuringMember2018-12-310001609804us-gaap:EmployeeSeveranceMember2019-01-012019-12-310001609804us-gaap:FacilityClosingMember2019-01-012019-12-310001609804oec:GroundRemediationCostsRelatedToRestructuringMember2019-01-012019-12-310001609804us-gaap:OtherRestructuringMember2019-01-012019-12-310001609804us-gaap:EmployeeSeveranceMember2019-12-310001609804us-gaap:FacilityClosingMember2019-12-310001609804oec:GroundRemediationCostsRelatedToRestructuringMember2019-12-310001609804us-gaap:OtherRestructuringMember2019-12-31oec:kmt0001609804oec:RubberMember2016-01-012016-12-3100016098042018-01-012018-06-30oec:plant00016098042018-06-300001609804us-gaap:EmployeeSeveranceMember2018-01-012018-06-300001609804us-gaap:AccumulatedTranslationAdjustmentMember2016-12-310001609804us-gaap:AccumulatedNetGainLossFromDesignatedOrQualifyingCashFlowHedgesMember2016-12-310001609804us-gaap:AccumulatedDefinedBenefitPlansAdjustmentMember2016-12-310001609804us-gaap:AccumulatedTranslationAdjustmentMember2017-01-012017-12-310001609804us-gaap:AccumulatedNetGainLossFromDesignatedOrQualifyingCashFlowHedgesMember2017-01-012017-12-310001609804us-gaap:AccumulatedDefinedBenefitPlansAdjustmentMember2017-01-012017-12-310001609804us-gaap:AccumulatedTranslationAdjustmentMember2017-12-310001609804us-gaap:AccumulatedNetGainLossFromDesignatedOrQualifyingCashFlowHedgesMember2017-12-310001609804us-gaap:AccumulatedDefinedBenefitPlansAdjustmentMember2017-12-310001609804us-gaap:AccumulatedTranslationAdjustmentMember2018-01-012018-12-310001609804us-gaap:AccumulatedNetGainLossFromDesignatedOrQualifyingCashFlowHedgesMember2018-01-012018-12-310001609804us-gaap:AccumulatedDefinedBenefitPlansAdjustmentMember2018-01-012018-12-310001609804us-gaap:AccumulatedTranslationAdjustmentMember2018-12-310001609804us-gaap:AccumulatedNetGainLossFromDesignatedOrQualifyingCashFlowHedgesMember2018-12-310001609804us-gaap:AccumulatedDefinedBenefitPlansAdjustmentMember2018-12-310001609804us-gaap:AccumulatedTranslationAdjustmentMember2019-01-012019-12-310001609804us-gaap:AccumulatedNetGainLossFromDesignatedOrQualifyingCashFlowHedgesMember2019-01-012019-12-310001609804us-gaap:AccumulatedDefinedBenefitPlansAdjustmentMember2019-01-012019-12-310001609804us-gaap:AccumulatedTranslationAdjustmentMember2019-12-310001609804us-gaap:AccumulatedNetGainLossFromDesignatedOrQualifyingCashFlowHedgesMember2019-12-310001609804us-gaap:AccumulatedDefinedBenefitPlansAdjustmentMember2019-12-310001609804us-gaap:AccumulatedDefinedBenefitPlansAdjustmentNetUnamortizedGainLossMemberus-gaap:ReclassificationOutOfAccumulatedOtherComprehensiveIncomeMember2019-01-012019-12-310001609804us-gaap:AccumulatedDefinedBenefitPlansAdjustmentNetUnamortizedGainLossMemberus-gaap:ReclassificationOutOfAccumulatedOtherComprehensiveIncomeMember2018-01-012018-12-310001609804us-gaap:AccumulatedDefinedBenefitPlansAdjustmentNetUnamortizedGainLossMemberus-gaap:ReclassificationOutOfAccumulatedOtherComprehensiveIncomeMember2017-01-012017-12-310001609804us-gaap:ReclassificationOutOfAccumulatedOtherComprehensiveIncomeMember2019-01-012019-12-310001609804us-gaap:ReclassificationOutOfAccumulatedOtherComprehensiveIncomeMember2018-01-012018-12-310001609804us-gaap:ReclassificationOutOfAccumulatedOtherComprehensiveIncomeMember2017-01-012017-12-310001609804country:DE2019-01-012019-12-310001609804country:DE2018-01-012018-12-310001609804country:DE2017-01-012017-12-310001609804us-gaap:ForeignCountryMembercountry:US2017-01-012017-12-310001609804country:BRus-gaap:ForeignCountryMember2019-01-012019-12-310001609804country:BRus-gaap:ForeignCountryMember2018-01-012018-12-310001609804country:BRus-gaap:ForeignCountryMember2017-01-012017-12-310001609804us-gaap:ForeignCountryMembercountry:KR2018-01-012018-12-310001609804oec:TaxYears2019Through2025Member2019-12-310001609804oec:TaxYearsAfter2025Member2019-12-310001609804oec:IndefiniteMember2019-12-31oec:defendant0001609804us-gaap:SettledLitigationMemberus-gaap:UnfavorableRegulatoryActionMember2017-12-222017-12-22oec:facility0001609804country:US2019-01-012019-12-310001609804stpr:LAus-gaap:SettledLitigationMemberus-gaap:UnfavorableRegulatoryActionMember2017-12-222017-12-220001609804stpr:LAus-gaap:SettledLitigationMembersrt:MaximumMemberus-gaap:UnfavorableRegulatoryActionMember2017-12-220001609804oec:TermLoanUSDMemberoec:TermLoanMember2019-12-310001609804oec:TermLoanEURMemberoec:TermLoanMember2019-12-31oec:guarantee0001609804oec:EulerHermesS.A.Member2019-12-310001609804oec:EulerHermesS.A.Member2018-12-310001609804oec:DeutscheBankAGMember2019-12-310001609804oec:DeutscheBankAGMember2018-12-310001609804oec:RubberMemberus-gaap:ProductConcentrationRiskMemberus-gaap:SalesRevenueNetMember2019-01-012019-12-310001609804oec:RubberMemberus-gaap:ProductConcentrationRiskMemberus-gaap:SalesRevenueNetMember2018-01-012018-12-310001609804oec:RubberMemberus-gaap:ProductConcentrationRiskMemberus-gaap:SalesRevenueNetMember2017-01-012017-12-310001609804us-gaap:ProductConcentrationRiskMemberus-gaap:SalesRevenueNetMemberoec:SpecialtiesMember2019-01-012019-12-310001609804us-gaap:ProductConcentrationRiskMemberus-gaap:SalesRevenueNetMemberoec:SpecialtiesMember2018-01-012018-12-310001609804us-gaap:ProductConcentrationRiskMemberus-gaap:SalesRevenueNetMemberoec:SpecialtiesMember2017-01-012017-12-310001609804oec:RubberMemberus-gaap:OperatingSegmentsMember2019-01-012019-12-310001609804us-gaap:OperatingSegmentsMemberoec:SpecialtiesMember2019-01-012019-12-310001609804us-gaap:CorporateNonSegmentMember2019-01-012019-12-310001609804oec:RubberMemberus-gaap:OperatingSegmentsMember2019-12-310001609804us-gaap:OperatingSegmentsMemberoec:SpecialtiesMember2019-12-310001609804us-gaap:CorporateNonSegmentMember2019-12-310001609804oec:RubberMemberus-gaap:OperatingSegmentsMember2018-01-012018-12-310001609804us-gaap:OperatingSegmentsMemberoec:SpecialtiesMember2018-01-012018-12-310001609804us-gaap:CorporateNonSegmentMember2018-01-012018-12-310001609804oec:RubberMemberus-gaap:OperatingSegmentsMember2018-12-310001609804us-gaap:OperatingSegmentsMemberoec:SpecialtiesMember2018-12-310001609804us-gaap:CorporateNonSegmentMember2018-12-310001609804oec:RubberMemberus-gaap:OperatingSegmentsMember2017-01-012017-12-310001609804us-gaap:OperatingSegmentsMemberoec:SpecialtiesMember2017-01-012017-12-310001609804us-gaap:CorporateNonSegmentMember2017-01-012017-12-310001609804oec:RubberMemberus-gaap:OperatingSegmentsMember2017-12-310001609804us-gaap:OperatingSegmentsMemberoec:SpecialtiesMember2017-12-310001609804us-gaap:CorporateNonSegmentMember2017-12-310001609804country:US2018-01-012018-12-310001609804country:US2017-01-012017-12-310001609804country:KR2019-01-012019-12-310001609804country:KR2018-01-012018-12-310001609804country:KR2017-01-012017-12-310001609804country:BR2019-01-012019-12-310001609804country:BR2018-01-012018-12-310001609804country:BR2017-01-012017-12-310001609804country:CN2019-01-012019-12-310001609804country:CN2018-01-012018-12-310001609804country:CN2017-01-012017-12-310001609804country:ZA2019-01-012019-12-310001609804country:ZA2018-01-012018-12-310001609804country:ZA2017-01-012017-12-310001609804oec:OtherMiscellaneousCountriesMember2019-01-012019-12-310001609804oec:OtherMiscellaneousCountriesMember2018-01-012018-12-310001609804oec:OtherMiscellaneousCountriesMember2017-01-012017-12-310001609804oec:OtherEuropeanCountriesMember2019-01-012019-12-310001609804oec:OtherEuropeanCountriesMember2018-01-012018-12-310001609804oec:OtherEuropeanCountriesMember2017-01-012017-12-310001609804oec:RubberMemberus-gaap:CustomerConcentrationRiskMemberus-gaap:SalesRevenueNetMemberoec:CustomerAMember2019-01-012019-12-310001609804oec:RubberMemberus-gaap:CustomerConcentrationRiskMemberus-gaap:SalesRevenueNetMemberoec:CustomerAMember2018-01-012018-12-310001609804oec:RubberMemberus-gaap:CustomerConcentrationRiskMemberus-gaap:SalesRevenueNetMemberoec:CustomerAMember2017-01-012017-12-310001609804country:DE2019-12-310001609804country:DE2018-12-310001609804country:SE2019-12-310001609804country:SE2018-12-310001609804country:IT2019-12-310001609804country:IT2018-12-310001609804country:PL2019-12-310001609804country:PL2018-12-310001609804oec:OtherEuropeanCountriesMember2019-12-310001609804oec:OtherEuropeanCountriesMember2018-12-310001609804srt:EuropeMember2019-12-310001609804srt:EuropeMember2018-12-310001609804country:US2019-12-310001609804country:US2018-12-310001609804country:KR2019-12-310001609804country:KR2018-12-310001609804country:ZA2019-12-310001609804country:ZA2018-12-310001609804country:BR2019-12-310001609804country:BR2018-12-310001609804country:CN2019-12-310001609804country:CN2018-12-310001609804oec:OtherMiscellaneousCountriesMember2019-12-310001609804oec:OtherMiscellaneousCountriesMember2018-12-31oec:related_party0001609804us-gaap:EquityMethodInvesteeMember2018-01-012018-12-310001609804us-gaap:PrincipalOwnerMember2018-01-012018-12-310001609804srt:AffiliatedEntityMember2019-12-310001609804srt:AffiliatedEntityMember2018-12-310001609804srt:AffiliatedEntityMember2019-01-012019-12-310001609804srt:AffiliatedEntityMember2018-01-012018-12-310001609804srt:AffiliatedEntityMember2017-01-012017-12-3100016098042019-01-012019-03-3100016098042019-04-012019-06-3000016098042019-07-012019-09-3000016098042019-10-012019-12-3100016098042018-01-012018-03-3100016098042018-04-012018-06-3000016098042018-07-012018-09-3000016098042018-10-012018-12-31

UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

| | | | | |

| ☒ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(D) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2019

OR

| | | | | |

| ☐ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from _______________ to _______________

Commission file number 001-36563

ORION ENGINEERED CARBONS S.A.

(Exact name of registrant as specified in its charter)

| | | | | | | | | | | | | | |

| Grand Duchy of Luxembourg | | | 00-0000000 | |

(State or other jurisdiction of incorporation or organization) | | | (I.R.S. Employer Identification No.) | |

| | | | |

| 4501 Magnolia Cove Drive Suite 106 | Houston, | Texas | 77345 | |

(Address of Principal Executive Offices) | | | (Zip Code) | |

(281) 318-2959

Registrant's telephone number, including area code

Securities registered pursuant to Section 12(b) of the Act:

| | | | | | | | |

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered |

| Common Shares, no par value | OEC | New York Stock Exchange |

Securities registered pursuant to section 12(g) of the Act:

________________________none_________________________

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yes x No o

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.

Yes o No x

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports); and (2) has been subject to such filing requirements for the past 90 days. Yes x No o

Indicate by check mark whether the registrant has submitted every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

Yes x No o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer”, "smaller reporting company" and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| | | | | | | | | | | |

| Large accelerated filer | x | Accelerated filer | ☐ |

Non-accelerated filer | ☐ | Smaller reporting company | ☐ |

| | Emerging growth company | ☐ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act.

☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ☐ No x

The aggregate market value of voting and non-voting common equity held by non-affiliates, based upon the closing price for the common shares, as reported on the New York Stock Exchange on the last business day of the registrant’s most recently completed second fiscal quarter, of $21.41, was approximately $1.3 billion.

The registrant had outstanding 60,224,147 shares of common stock as of February 19, 2020.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the Registrant's definitive proxy statement for the 2020 annual meeting of shareholders.

TABLE OF CONTENTS

CERTAIN DEFINED TERMS

In this annual report, unless otherwise specified or if the context so requires:

•References in this report to “Orion,” the “Group,” the “Orion Group,” the “Company,” “we,” “us” or “our” are to Orion Engineered Carbons S.A.; a Luxembourg joint stock corporation (société anonyme); and its consolidated subsidiaries;

•References in this report to “Kinove Holdings” are to Kinove Luxembourg Holdings 1 S.à r.l., a Luxembourg limited liability company (société à responsabilité limitée), our previous principal shareholder which was owned by investment funds managed by affiliates of Rhône Capital L.L.C., investment funds managed directly or indirectly by Triton Managers III Limited and TFF III Limited and Luxinva S.A., a wholly-owned subsidiary of the Abu Dhabi Investment Authority, a public institution wholly-owned by the Government of the Emirate of Abu Dhabi;

•References in this report to “Luxco Coinvest” are to Kinove Luxembourg Coinvestment S.C.A., a liquidated investment vehicle previously owned by members of the Company’s management;

•References to the “Acquisition” are to the acquisition of the carbon black business line from Evonik Industries AG, completed on July 29, 2011; and

•References to the “Credit Agreement” are to the Credit Agreement, dated as of July 25, 2014, among the Company, Orion Engineered Carbons Holdings GmbH, Orion Engineered Carbons Bondco GmbH, Orion Engineered Carbons GmbH, OEC Finance US LLC, the revolving borrowers named therein, the guarantors named on the signature page thereto, the lenders named therein, and Goldman Sachs Bank USA as administrative agent, as amended.

•Reference to “Evonik” are to Evonik Industries AG, Germany, Evonik Degussa GmbH, Germany and any affiliated companies.

PRESENTATION OF CERTAIN FINANCIAL AND OTHER INFORMATION

The financial statements included in this report have been prepared in accordance with accounting principles generally accepted in the United States (“U.S. GAAP” or “GAAP”).

Non-GAAP Financial Measures

In this report, we present certain financial measures that are not recognized by GAAP and that may not be permitted to appear on the face of GAAP-compliant financial statements or notes thereto.

The non-GAAP financial measures used in this report are Contribution Margin, Contribution Margin per Metric Ton (collectively, “Contribution Margins”), Adjusted EBITDA, Net Working Capital and Capital Expenditures. We define Contribution Margin as revenue less variable costs (such as raw materials, packaging, utilities and distribution costs). We define Contribution Margin per Metric Ton as Contribution Margin divided by volume measured in metric tons. We define Adjusted EBITDA as operating result (EBIT) before depreciation and amortization, adjusted for acquisition related expenses, restructuring expenses, consulting fees related to Company strategy, share of profit or loss of joint venture and certain other items. Adjusted EBITDA is defined similarly in the Credit Agreement. Adjusted EBITDA is used by our management to evaluate our operating performance and make decisions regarding allocation of capital because it excludes the effects of items that have less bearing on the performance of our underlying core business. We define Net Working Capital as inventories plus current trade receivables minus trade payables. We define Capital Expenditures as cash paid for the acquisition of intangible assets and property, plant and equipment as shown in the consolidated financial statements.

We also use Segment Adjusted EBITDA Margin, which we define as Adjusted EBITDA for the relevant segment divided by the revenue for that segment.

We use Adjusted EBITDA, Contribution Margins and Net Working Capital, as well as Adjusted EBITDA by segment and Segment Adjusted EBITDA Margin, as internal measures of performance to benchmark and compare performance among our own operations. We use these measures, together with other measures of performance under GAAP, to compare the relative performance of operations in planning, budgeting and reviewing the performance of our business. We believe these measures are useful measures of financial performance in addition to consolidated net income for the period, income from operations (EBIT) and other profitability measures under GAAP because they facilitate operating performance comparisons from period to period and company to company and, with respect to Contribution Margin, eliminate volatility in feedstock prices. By eliminating potential differences in results of operations between periods or companies caused by factors such as depreciation and amortization methods, historic cost and age of assets, financing and capital structures and taxation positions or regimes, we believe that Adjusted EBITDA can provide a useful additional basis for comparing the current performance of the underlying operations being evaluated. For these reasons, we believe EBITDA-based measures are often used by the investment community as a means of comparison of companies in our industry. By deducting variable costs (such as raw materials, packaging, utilities and distribution costs) from revenue, we believe that Contribution Margins can provide a useful basis for comparing the current performance of the underlying operations being evaluated by indicating the portion of revenue that is not consumed by these variable costs and therefore contributes to the coverage of all costs and profits.

Different companies and analysts may calculate measures based on EBITDA, contribution margins and working capital differently, so making comparisons among companies on this basis should be done carefully. Adjusted EBITDA, Contribution Margins and Net Working Capital are not measures of performance under GAAP and should not be considered in isolation or construed as substitutes for revenue, consolidated net income for the period, income from operations (EBIT), gross profit and other GAAP measures as an indicator of our operations in accordance with GAAP.

Reconciliation of Non-GAAP Financial Measures

The non-GAAP financial measures contained in this report are unaudited and have not been prepared in accordance with GAAP or the accounting standards of any other jurisdiction and may not be comparable to other similarly titled measures of other companies. For a reconciliation of these non-GAAP financial measures to the most directly comparable GAAP measures, see “Item 7. Management's Discussion and Analysis of Financial Condition and Results of Operations—Reconciliation of non-GAAP Financial Measures.”

NOTE REGARDING FORWARD-LOOKING STATEMENTS

This report contains and refers to certain forward-looking statements with respect to our financial condition, results of operations and business. These statements constitute forward-looking statements within the meaning of Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”). Forward-looking statements are statements of future expectations that are based on management’s current expectations and assumptions and involve known and unknown risks and uncertainties that could cause actual results, performance or events to differ materially from those expressed or implied in these statements. Forward-looking statements include, among others, statements concerning the potential exposure to market risks, statements expressing management’s expectations, beliefs, estimates, forecasts, projections and assumptions and statements that are not limited to statements of historical or present facts or conditions.

Forward-looking statements are typically identified by words such as “anticipate,” “assume,” “assures” “believe,” “confident,” “could,” “estimate,” “expect,” “intend,” “may,” “plan,” “objectives,” “outlook,” “probably,” “project,” “will,” “seek,” “strong,” “target”

“to be,” and other words of similar meaning. These forward-looking statements include, without limitation, statements about the following matters:

•our strategies for (i) strengthening our position in specialty carbon blacks and rubber carbon blacks, (ii) increasing our rubber carbon black margins and (iii) strengthening the competitiveness of our operations;

•the ability to pay dividends at current dividend levels or at all;

•cash flow projections;

•the installation of pollution control technology in our U.S. manufacturing facilities pursuant to the EPA consent decree described herein;

•the outcome of any in-progress, pending or possible litigation or regulatory proceedings; and

•our expectation that the markets we serve will continue to grow.

All these forward-looking statements are based on estimates and assumptions that, although believed to be reasonable, are inherently uncertain. Therefore, undue reliance should not be placed upon any forward-looking statements. There are important factors that could cause actual results to differ materially from those contemplated by such forward-looking statements. These factors include, among others:

•negative or uncertain worldwide economic conditions;

•volatility and cyclicality in the industries in which we operate;

•operational risks inherent in chemicals manufacturing, including disruptions as a result of severe weather conditions and natural disasters;

•our dependence on major customers and suppliers;

•our ability to compete in the industries and markets in which we operate;

•our ability to address changes in the nature of future transportation and mobility concepts which may impact our customers and our business

•our ability to develop new products and technologies successfully and the availability of substitutes for our products;

•our ability to implement our business strategies;

•volatility in the costs and availability of raw materials (including but not limited to any and all effects from restrictions imposed by the MARPOL convention and respective International Maritime Organization (IMO) regulations in particular to reduce sulfur oxides (SOx) emissions from ships) and energy;

•our ability to respond to changes in feedstock prices and quality;

•our ability to realize benefits from investments, joint ventures, acquisitions or alliances;

•our ability to realize benefits from planned plant capacity expansions and site development projects and the potential delays to such expansions and projects;

•information technology systems failures, network disruptions and breaches of data security;

•our relationships with our workforce, including negotiations with labor unions, strikes and work stoppages;

•our ability to recruit or retain key management and personnel;

•our exposure to political or country risks inherent in doing business in some countries;

•geopolitical events in the European Union, and in particular the ultimate future relations between the European Union and the United Kingdom resulting from the “Brexit” which may impact the Euro;

•environmental, health and safety regulations, including nanomaterial and greenhouse gas emissions regulations, and the related costs of maintaining compliance and addressing liabilities;

•possible future investigations and enforcement actions by governmental or supranational agencies;

•our operations as a company in the chemical sector, including the related risks of leaks, fires and toxic releases;

•market and regulatory changes that may affect our ability to sell or otherwise benefit from co-generated energy;

•litigation or legal proceedings, including product liability and environmental claims;

•our ability to protect our intellectual property rights and know-how;

•our ability to generate the funds required to service our debt and finance our operations;

•fluctuations in foreign currency exchange and interest rates;

•the availability and efficiency of hedging;

•changes in international and local economic conditions, including with regard to the Euro, dislocations in credit and capital markets and inflation or deflation;

•potential impairments or write-offs of certain assets;

•required increases in our pension fund contributions;

•the adequacy of our insurance coverage;

•changes in our jurisdictional earnings mix or in the tax laws or accepted interpretations of tax laws in those jurisdictions;

•our indemnities to and from Evonik (as defined below);

•challenges to our decisions and assumptions in assessing and complying with our tax obligations; and

•potential difficulty in obtaining or enforcing judgments or bringing actions against us in the United States.

In light of these risks, our results could differ materially from the forward-looking statements contained in this report and no undue reliance should be placed on those forward-looking statements. For further information regarding factors that could affect our business and financial results and the related forward-looking statements, see “Item 1A. Risk Factors.”

PART I

Item 1. Business

Overview

We are a leading global producer of carbon black. Carbon black is a form of carbon used to improve certain properties of materials into which it is added. It is used as a pigment and as a performance additive in coatings, polymers, printing and special applications (specialty carbon black) and in the reinforcement of rubber in tires and mechanical rubber goods (rubber carbon black).

We are one of the largest global producers of carbon black and our business is divided into two segments: Specialty Carbon Black and Rubber Carbon Black.

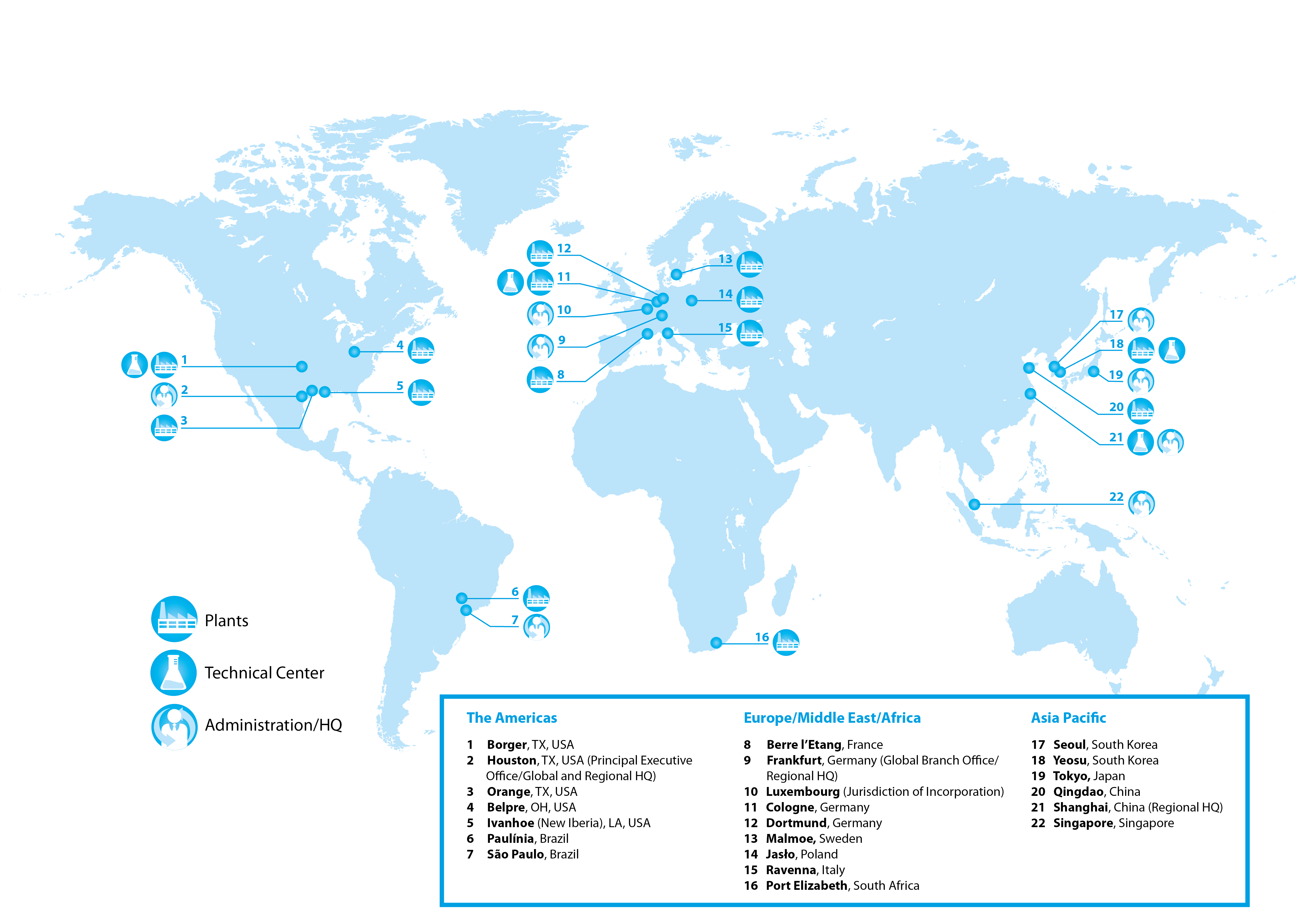

We operate a global supply chain network currently comprising 13 wholly owned production facilities in Europe, North and South America, Asia and South Africa and three sales companies, as well as one jointly-owned production plant in Germany.

Products and Applications

We have a diversified carbon black production platform across the Specialty Carbon Black and Rubber Carbon Black operating segments. In 2019, we offered more than 280 specialty carbon black grades and approximately 60 rubber carbon black grades under a number of well-recognized brand names and trademarks. Our product portfolio is one of the broadest in the industry. Our product and geographic diversity exposes us to a wide variety of applications and industries, which in turn lowers our dependency on individual customers or regions. Our overall product portfolio benefits from higher margin specialty, certain technically superior grade rubber carbon black products (technical grade rubber black) and stable margin rubber carbon black products.

We continuously strive to meet our customers’ changing demands and adjust our products accordingly, as well as to enhance our product portfolio with innovations. In our Specialty Carbon Black segment, we have launched over the years several new post-treated specialty carbon black grades for coatings and printing applications, as well as several new high purity carbon black grades for the fiber industry and conductive carbon black grades for polymers, printing and new markets, such as for battery electrodes. In our Rubber Carbon Black segment, we have developed in the past two product families: PUREX® for mechanical rubber goods (“MRG”) applications, which complies with high cleanliness requirements, and ECORAX® for tires, which is characterized by improved tire properties of wear and fuel consumption.

Specialty Carbon Black

Overview

We are one of the largest global producers of specialty carbon black with an estimated share of global industry sales of approximately 24% in 2019 measured by volume in kmt. We manufacture specialty carbon black at multiple sites for a broad range of specialized applications. Specialty carbon black imparts specific characteristics, such as high-quality pigmentation, UV light protection, viscosity control and electrical conductivity.

In 2019, our Specialty Carbon Black segment generated $508.5 million in revenues, 251.0 kmt in volume, $122.2 million in Segment Adjusted EBITDA and Segment Adjusted EBITDA Margin of 24.0%. The Specialty Carbon Black segment has a product mix divided into four sectors: Coatings, Polymers, Printing and Special Applications. In 2019, Polymer applications accounted for about 69% of our volume measured in kmt, Printing accounted for nearly 15%, while Coatings, Special Applications and cross-sector sales to distributors represented the remainder.

Our Specialty Carbon Black segment generates higher margins per metric ton than our Rubber Carbon Black segment, with the highest margin per metric ton in Coatings. We believe the key driver of attractive margins in specialty carbon black is innovation supported by our innovation group, which works in close coordination with our customers and technical marketing support. We provide assistance to our customers through the whole value chain, including product formulation, technical support, product handling, packaging, logistics, supply chain management and final application.

We are recognized by our customers as a leading innovator and manufacturer of customized products fitting specific application needs. Our specialty carbon black customer base is relatively diverse, with the top five customers accounting for approximately 26% of the Specialty Carbon Black segment volume in 2019. We have been supplying most of our key industry customers for more than 30 years.

Coatings

Product and Application Portfolio

We have a broad Coatings product portfolio, which includes products used for pigmentation in black coatings and enhancement of other coatings (for example, in automotive basecoats and architectural coatings), for conductivity and for tinting in all other coatings, as well as for paints and for light tinting in transparent coatings (for example, for metallic effects and wood glazing). The variety of our

manufacturing processes allows the creation of specialty carbon black with different morphological and chemical properties, thereby giving some of our products unique characteristics.

The following table provides examples of our Coatings applications.

| | | | | | | | | | | | | | | | | | | | |

| Coatings | | Automotive | | General Industrial | | Architectural & Decorative |

| Applications | | Automotive original

equipment manufacturing

Automotive refinish

Automotive parts | | Wood, coil and plastic coatings

Protective and marine

Aerospace Packaging | | Architectural

Decorative |

| Attributes | | Pigmentation, high

jetness and blue

undertone, conductivity | | High-performance tinting

Conductivity | | Tinting |

| Brands | | PRINTEX® NEROX® LAMP BLACK COLOUR BLACK SPECIAL BLACK | | PRINTEX® NEROX® LAMP BLACK COLOUR BLACK SPECIAL BLACK | | PRINTEX® NEROX® LAMP BLACK COLOUR BLACK SPECIAL BLACK |

Customers

We believe that the global Coatings industry consists of a few key suppliers that account for approximately half of the global Coatings capacity. Over time we have demonstrated to leverage our application technology platform to play a substantial role in our Coatings customer's product innovation process and to meet their demanding requirements. The customized nature of Coatings products leads to attractive margins in the industry.

We supply many of the Coatings industry’s key industry players and mid-sized customers and have longstanding relationships with several major global customers. We have been serving several of the key industry players for more than 30 years. The Coatings market is relatively fragmented, although our top five customers accounted for approximately 38% of Coatings volume in 2019.

Polymers

Product and Application Portfolio

Polymers are the largest end-use market for specialty carbon blacks. Our Polymer portfolio is one of the broadest in the industry and, supported by an application technology platform, enables us to cover most of the product demand spectrum.

Our Polymers portfolio is tailored to meet specific industry and customer needs. For example, potable water pipes made of polyethylene, agricultural films, cables and other articles exposed to UV radiation (sunlight) need to be protected against polymer degradation and subsequent deterioration of mechanical strength. We offer tailor-made products that not only provide efficient UV protection but also provide additional benefits, such as good processing properties and easy handling. Products offered also meet special performance criteria, including food-contact compliance and spin-fiber quality.

In addition to UV protection, our portfolio includes products from standard- to high-performance grades designed and modified to provide electrical conductivity, antistatic and reinforcing properties to many different polymer articles, including high-voltage cables, films, boxes and high pressure pipes.

Our portfolio offering targeted at fiber products and technology represents a growth area and provides a combination of a broad range of jetness with good spinnability. Certain of our polymer products have a bluish undertone, which makes these grades especially attractive for high-performance fibers in textiles, with luxury touch and feel. Ultra clean products provide good process stability during the small and thin fiber manufacturing processes.

The following table provides examples of our polymers applications.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Polymers | | Pipe | | Wire & Cable | | Films | | Blow &

Injection

Molding | | Fiber | | Thermal

Insulation | | Other |

| Applications | | Pressure pipes (water, gas) Irrigation Sewage pipes Conductive pipes/hoses | | Power cables (LV to HV) Jacketing | | Agricultural Packaging Geomembrane Foil Laminations | | Packaging Housing Container Automotive | | Textile Industrial Non-Woven | | Construction | | Thermosets TPE profiles Plastics |

| Attributes | | Dispersibility UV protection Conductivity | | Dispersibility UV protection Conductivity | | Dispersibility UV protection Coloring | | Dispersibility UV protection Conductivity | | Dispersibility Coloring | | IR absorption | | Thixotrophy Dispersibility Coloring Reinforcing UV protection |

| Brands | | PRINTEX® AROSPERSE HIBLACK® | | PRINTEX® HIBLACK® | | PRINTEX® AROSPERSE HIBLACK® | | PRINTEX® AROSPERSE HIBLACK® | | PRINTEX® AROSPERSE COLOUR BLACK | | LAMP BLACK AROSPERSE | | PRINTEX® AROSPERSE HIBLACK® LAMP BLACK |

Customers

Due to the diverse nature of Polymer applications (construction, general industrial, engineering, consumer goods, automotive and packaging), the customer base for Polymers tends to be wide-ranging from regional and international master batch producers to global integrated petrochemical and polyolefin producers. We supply many of the plastics industry’s customers and supply leading customers in each region. We have been serving certain of our key customers for more than 30 years. Our top five customers accounted for approximately 34% of Polymers volume in 2019.

Printing

Product and Application Portfolio

We have a broad Printing product portfolio with a large number of grades for different printing technologies and applications. We apply different process technologies to offer highly specialized products that meet specific requirements, including compliance with food-contact regulations and specially formulated products with different coloristic properties (such as undertone, optical density and gloss), rheological effects and dispersibility functions.

We focus on Printing products with the highest potential for specialty applications, such as packaging and specialty niches. Consequently, relatively low-end newspaper and other print media applications represented only a small portion of our overall specialty carbon black sales in 2019. Producers must meet and balance numerous technical properties. These properties include ease of dispersion, processing, handling, formulation requirements, final product performance hold-out, rub resistance and, most importantly, coloristic properties, such as optical density, gloss, light-fastness and color tone. Our specialty carbon black product portfolio supports printing ink manufactures in achieving these attributes.

Packaging inks require special rheology, dispersion and wetting behavior properties. For example, UV curing inks on nonporous substrates require special surface chemistry for wetting, flow, color and stability.

The following table provides examples of our printing applications.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | Packaging | | | | | | Print Media | | | | | | |

| Printing | | High-end

Packaging | | Packaging | | Display

Advertising | | Publication

(magazines) | | Special

Applications | | Books, Posters,

Brochures | | Newspaper |

| Applications | | Liquid inks

UV curing

Sheetfed

Screen | | Liquid inks | | Heatset

Sheetfed

Screen | | Heatset

Sheetfed

Publication

gravure | | Screen

Water-

based

gravure UV

curing | | Sheetfed

UV curing | | Water-based

flexo Coldset |

| Attributes | | Coloring

Gloss Food

contact

regulations

Wettability | | Coloring | | Coloring

Gloss

Moderate

flow

Wettability | | Coloring

Gloss

Good flow

Low abrasion | | Coloring

Gloss

Moderate

flow

Wettability | | Coloring

Gloss

Moderate

flow

Wettability | | Coloring |

| Brands | | NEROX® PRINTEX® SPECIAL BLACK | | PRINTEX® HIBLACK® | | NEROX® HIBLACK® PRINTEX® SPECIAL BLACK | | PRINTEX® HIBLACK® | | PRINTEX® SPECIAL BLACK | | PRINTEX® SPECIAL BLACK | | PRINTEX® HIBLACK® |

Customers

The global Printing industry has been undergoing consolidation over the past few years. Currently, the industry is dominated by a few key players. Sourcing decisions are largely based on specialty carbon black product attributes. For low-end applications, decisions are made based primarily on price. For high-end applications, the required degree of product and technology know-how makes purchasing decisions less price sensitive. We play an important role in helping our customers develop customized Printing solutions and are recognized by customers as a preferred strategic and technical partner. We have been serving certain of our key customers for more than 30 years. Due to the relatively consolidated nature of the Printing industry, our top five Printing customers accounted for approximately 63% of Printing volume in 2019.

Special Applications

The Special Applications product category comprises applications not included into our Coatings, Polymers and Printing portfolios, such as, silicones, non-woven textile, building materials, battery electrodes metallurgical, agrochemicals and carbon brushes. Our top five customers accounted for approximately 37% of Special Applications volume in 2019.

Distribution

We sell most of our specialty carbon black products directly to our customers and only a smaller part of our sales is made via external channel partners and distributors. External channel partners and distributors generally sell our products in smaller lots to smaller customers, who do not negotiate with us directly. These sales are made across all our specialty carbon black applications, including Coatings, Polymers, Printing and Special Applications.

Competition

We are one of the largest global producers of specialty carbon black with an estimated share of global industry sales of approximately 24% measured by volume in kmt in 2019. Cabot and Birla are the other two large global producers of specialty carbon black. Each of the top three producers of specialty carbon black leverages R&D and applications technology platforms to tailor products to customer needs and to introduce its products into new application niches.

Rubber Carbon Black

Overview

We are one of the largest global producers of rubber carbon black. Rubber carbon black sales are largely regional, since transportation costs are high relative to sales price. In 2019, our largest rubber carbon black customer accounted for approximately 20% and the second largest customer for approximately 10% of our rubber carbon black segment net sales with no other customer exceeding 10% of our segment net sales. The largest rubber carbon black customer (Michelin) accounted in addition for approximately 13% of the Company's overall consolidated net sales with no other customer exceeding 10% of our Company's net sales.

In 2019, our Rubber Carbon Black segment generated $967.9 million in revenues, 772.1 kmt in volume, $145.2 million in Segment Adjusted EBITDA and Segment Adjusted EBITDA Margin of 15.0%. Rubber carbon black is primarily used for reinforcement of rubber compounds and to adjust specific performances of rubber articles. Based on the application of rubber carbon black, we have divided the Rubber Carbon Black segment into two categories: Tires and Mechanical Rubber Goods (MRG).

Tires

Product and Application Portfolio

We offer a broad Tire product portfolio, which includes high reinforcing grades and semi-reinforcing grades. Fine particle reinforcing grade carbon blacks are used mostly in the tread of tires. Other reinforcing grade carbon blacks are also used in different components of the tire carcass. In addition to standardized grades, we produce advanced grades tailored to meet specific customer performance requirements, such as ECORAX® grades designed to lower rolling resistance and HP grades for truck tires and high- and ultra-high-performance passenger car tires. Semi-reinforcing grade carbon blacks are used in several components of the tire carcass like sidewall and bead area. We cover the full portfolio of standard semi-reinforcing grade carbon blacks and have a portfolio of special semi-reinforcing grade carbon blacks, which fulfill special customer requirements using special production technology. These special semi-reinforcing grade carbon blacks are part of our ECORAX® product family.

Customers

Given the highly consolidated nature of the tire industry, our top ten customers represented slightly more than 85% of our tires volume in 2019. A significant portion of our Tire products are sold to leading tire manufacturers. We have longstanding relationships with most of these customers and have the capacity to serve them in major global regions. We have been serving certain of our key customers for more than 30 years.

We believe that our customers value the quality, consistency and reliability of our operations and are generally reluctant to switch suppliers without due cause. In addition, because automotive tires have safety implications, tire manufacturers are often required to go through lab and extensive plant approval processes before they change their supplier of carbon black.

Mechanical Rubber Goods

Product and Application Portfolio

We produce a wide range of mechanical rubber goods products for a variety of end-uses, including automotive production, construction, manufacturing of wires and cables, as well as certain food, consumer and medical applications. Our MRG products can be divided into four main groups: (i) standardized ASTM furnace grades, (ii) specialized ASTM furnace grades, (iii) specialized non-ASTM furnace grades and rubber carbon blacks from special production processes lampblack (Durex O) and (iv) thermal black (N990) and gas black (CK3). In the field of special ASTM and non-ASTM blacks we offer an extensive portfolio of “PUREX®” grades. These grades are mainly used in automotive rubber parts like window sealings and hoses. These grades have an exceptionally high purity, high consistency and can be dispersed well in rubber compounds. The grades of the PUREX® family aiming at the adjustment of special requirements like smooth surface, special surface appearance of sealing systems, electrical resistance and other specific requirements. The trend towards light weight construction of cars and the resulting use of aluminum require more attention to electrical resistivity of MRG parts.

The following table presents examples of our mechanical rubber goods applications.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Mechanical Rubber Goods | | Transportation

Construction

and Others | | | | Automotive | | | | Conductive & Isolation | | | | Food &

Medical |

| Applications | | Conveyor belts Construction profiles Mechanical rubber goods | | Extruded and other profiles | | Damping elements Hoses Transmission belts | | Molded goods with high resistance | | Seals rubber- to-metal bonding Unvulcanized sheets and adhesives | | Electrically conductive and antistatic rubber goods | | Profiles Tubing Hoses Sealings |

| Attributes | | Tensile strength Tear and abrasion resistance Reinforcement | | Filler loading Compression Smooth surfaces Processability Consistency | | Processability Injection molding and calendaring | | Low hysteresis Reinforcement Processing | | Scorch safety Tensile strength | | Electrical conductivity or antistatic behavior | | Dispersion Filler loadings |

| Brands | | CORAX® | | PUREX® DUREX® CORAX® N990 | | CORAX® PUREX® DUREX® | | PUREX® | | CK 3 | | PRINTEX® CORAX® PUREX® | | PUREX® CORAX® N990 |

Customers

We serve customers across the entire value chain and MRG applications, including compounders, parts and component manufacturers and automotive system suppliers. The mechanical rubber goods industry is fragmented in nature and supports a large number of suppliers. The industry, however, is undergoing a consolidation process. Our top ten global customers accounted for approximately 50% of our mechanical rubber goods volume in 2019. We have a diversified geographic presence with significant exposure to the European, North and South American and Asian MRG markets. We supply various key industry customers and have longstanding relationships with several of them. We have been serving certain key customers for more than 30 years.

Competition

We are one of the largest global producers of rubber carbon black in the world while Cabot, Birla and Black Cat were the three largest global producers of rubber carbon black in 2019.

Rubber carbon black sales are largely regional, since transportation costs are high relative to sales price. As a result, the global rubber carbon black industry is more fragmented compared to the specialty carbon black industry. The smaller regional suppliers participate mainly in standard tire and mechanical rubber goods applications and are less prevalent in more specialized products for the higher-end tire and mechanical rubber goods applications.

Procurement and Raw Materials

In 2019, raw materials accounted for 75% of our cost of sales. Approximately 79% of the cost of raw material used in the production of carbon black is related to petroleum-based or coal-based feedstock known as carbon black oil, with some limited use of other raw materials, such as nitrogen tetroxide, hydrogen, natural gas and acetylene. Carbon black oil comes from three main sources: (i) fluid catalytic cracking bottoms, a by-product of fuel producing refineries, (ii) steam cracker tar, a by-product of ethylene producing crackers, and (iii) certain coal tar products.

Efficient procurement of carbon black oil is an important factor in achieving optimal production costs and profitability. Our carbon black oil procurement strategy entails global sourcing of carbon black oil, using proprietary optimization tools to maximize value.

Approximately 50% of our carbon black oil supply is covered by short- and long-term contracts with a wide variety of suppliers.

The pricing of carbon black oil is typically indexed to the price of fuel oil. In general, we benchmark against Platts indices in the sourcing regions e.g. USGC, New York, Rotterdam and Singapore. In some areas the Gasoil index is used. While the majority of our purchases are based on underlying fuel oil indices, the ultimate carbon black oil price also depends on carbon black oil specific quality characteristics, differentials (premiums or discounts to Platts indices), freight costs and region-specific supply and demand as well as regulatory factors. Carbon black oil procurement is an important factor in achieving best-in-class production costs.

Characteristics of Production Capability

Production Know-how

With exception of our plant in France, we produce rubber carbon black at all, and specialty carbon blacks at many, of our production sites. We have the production know-how to manufacture a wide range of specialty carbon blacks and rubber carbon blacks worldwide. We believe we are currently the only supplier with core production competencies across all leading production processes (furnace black, gas black, lamp black, thermal black and acetylene black). This provides us flexibility to offer a wide range of specialty carbon black and rubber carbon black products that are best suited to customers’ needs.

Location of Production Facilities

Our production sites are strategically located throughout the world in all major regions. This is important for our rubber carbon black business, which is largely regional. Since specialty carbon black’s freight costs represent a smaller component of the final cost (relative to rubber carbon black), it is commercially viable to ship specialty carbon blacks across geographic regions from our key production sites in Germany, South Korea, China and the United States. The regional spread of our production network also offers access to high-growth regions globally.

Flexibility of Asset Base

We have implemented a flexible and intelligent production and supply chain network under the concept of operating all regional production sites as one large virtual plant. This allows us to shift production of specialty carbon black and rubber carbon black among different plants in order to optimize costs and plant utilization. In most cases, more than one plant is approved by our customers for specific products, which not only increases production flexibility but also ensures a higher supply security for customers.

Innovation

We enjoy a long-standing reputation within the industry for carbon black product and process technology, applications knowledge, and innovation. Carbon black products are highly versatile and meet specific performance requirements across many industries. This creates significant opportunities for product and process innovation. The final properties of the carbon black product depend on the mixture of raw materials used and to a large extent on the configuration and operating conditions of the specific reactor and the further processing of the initial product in beading, drying and after-treatment steps. Minimal changes to just one of the many process parameters can result in completely different carbon black products with different properties and potential end uses.

We maintain multiple product applications and process development centers in Europe, Asia and the Americas. Our innovation group is divided into applications technology and process development teams. The applications technology team works closely with our major clients to develop innovative products and expand the applications range for carbon black products. Success in applications development deepens our understanding of customer and industry requirements gained through these interactions. The process development team works closely with our manufacturing and procurement teams to enhance company competitiveness. This team focuses on efforts that lead to improved production processes, improved product quality and improved cost structure.

Our leading competence center is located in Cologne (Germany) to support and enhance our global innovation group activities. This center includes carbon black technologists, applications technology laboratories and process development staff, co-located with our pilot process development facilities. Staffing in our Cologne technical center includes physicists, chemists and engineers who can effectively and efficiently collaborate to create and analyze various carbon black properties with a goal to develop new products to meet customer requirements. Common processes and information technology tools further enhance coordination and communication with our regional technical centers located in South Korea, China and the United States.

Applications Technology

Our goal is to remain at the forefront of the industry in terms of product development by having dedicated applications technology facilities. Success relies on close collaboration with customers, often through long-term R&D alliances, which create superior technical interfaces. These interactions enable us to develop tailored solutions and meet unique customer requirements.

Our applications technology teams bring together a deep knowledge of carbon black technology with an understanding of the key applications practiced by our customers. This team has access to extensive laboratory and testing facilities using similar formulations, processing and test methods employed by our customers.

Applications technology plays a supporting role in the process of new product launch by providing technical data and presentations, training and support and establishment and monitoring of quality targets. The application technology team works closely with customers to provide support during the qualification cycle, which can be long and may last over one year. This close cooperation decreases the likelihood of customers switching suppliers once a product has been approved.

Process Development

We believe our process development capabilities represent a key competitive advantage. Product customization relies upon extensive process capabilities. Unique products and products that are difficult to replicate add value to customers’ end-products. Our customers have come to rely upon a continuous improvement in product quality and performance. Process development also enables improvements in manufacturing costs and efficiencies.

Our innovation group also operates pilot plants (small scale production facilities used for real-world trials of new carbon black grades) and a family of mini plants which include a smaller furnace reactor for basic studies as well as various facilities for chemical after-treatment, granulation and drying to tailor new products to specific customer requirements, especially in the specialty carbon black area

Spending on innovation, including both applications technology and process development, amounted to $19.9 million in 2019, $20.3 million in 2018 and $18.2 million in 2017 and was mostly directed towards the development of new specialty carbon black products, new applications for carbon black products and the improvement of process efficiencies as well as reduction of emission levels.

Marketing, Sales and Customer Contracts

We have an integrated sales and marketing process that combines key management, regional sales and technical marketing and applications support. This allows us to focus on customer solutions tailored to particular industries or regions.

Sales

Our Sales department is organized into two main groups: Key Account Management and Regional Sales. The Key Account Management team deals with the largest customers and has dedicated sales people by global account. The Regional sales team covers all other customers located in Europe, the Middle East and Africa, in the Americas and in Asia-Pacific. The field sales force operates along geographical regions. In addition to selling carbon black directly, we work with third-party distributors serving our markets with all required smaller volume lots.

Contracts

Most of our long-term contracts contain formula-driven price adjustment mechanisms for changes in raw material and/or energy costs and in some, foreign exchange rates. We sell carbon black under the following two main categories of contracts based on price adjustment mechanisms:

•Contracts with feedstock adjustments (indexed contracts). This category includes contracts with monthly or, in some cases, quarterly automatic feedstock and/or energy costs adjustments, which cover approximately 75% of our global volumes.

•Non-indexed contracts. This category includes short-term contracts (usually shorter than three months) where sales prices of our carbon black products are not linked to carbon black oil market prices.

Many of our indexed contracts allow for monthly price adjustments, while a small portion (by volume sold) allow for quarterly price adjustments. We believe that these contracts have enabled us generally to maintain our Segment Adjusted EBITDA Margins; however, rapid and significant oil or energy price fluctuations have had and are likely to continue to have significant and varying effects on our earnings and results of operations, partly because oil price changes affect our sales prices and our cost of raw materials and energy at different times and amounts, and partly due to other factors, such as differentials affecting the ultimate carbon black oil prices paid by us (versus a particular reference price index), actual carbon black oil usage amounts and our ongoing efficiency initiatives. See “Item 7. Management's Discussion and Analysis of Financial Condition and Results of Operations—Key Factors Affecting Our Results of Operations—Raw Material and Energy Costs” as well as “Item 1A. Risk Factors—Risks Related to Our Business—We are subject to volatility in the costs and availability of raw materials and energy, which could decrease our margins and adversely affect our business, financial condition, results of operations and cash flows.” Sales prices under non-indexed contracts are reviewed on a regular basis to reflect raw material and energy price fluctuations as well as overall market conditions.

Outbound Logistics and Distribution