Exhibit 99.2

Natera, Inc. Investor presentation Fourth Quarter 2022 Earnings Call February 28, 2023

Not for reproduction or further distribution. Safe harbor statement This presentation contains forward - looking statements under the meaning of the Private Securities Litigation Reform Act of 1995. All statements other than statements of historical facts contained in this presentation, including statements regarding our market opportunity, our proposed products and launch schedules, our reimburs eme nt coverage and our product costs, our commercial partners and potential acquisitions, our user experience, our clinical trials and studies, our financial performance, our strategies, our anticipate d r evenue and financial outlook, our goals and general business and market conditions, are forward - looking statements. These forward - looking statements are subject to known and unknown risks and uncertainties that may cause actual results to diffe r materially, including: we face numerous uncertainties and challenges in achieving our financial projections and goals; we may be unable to maintain our business and operations as planned due to dis ruptions and economic uncertainty caused by the COVID - 19 pandemic; we may be unable to further increase the use and adoption of Panorama and Horizon through our direct sales efforts or through ou r laboratory partners; we may be unable to develop and successfully commercialize new products, including Signatera and Prospera; we have incurred losses since our inception and we anticipate t hat we will continue to incur losses for the foreseeable future; our quarterly results may fluctuate from period to period; our estimates of market opportunity and forecasts of market growth may prove to be inaccurate; we may be unable to compete successfully with existing or future products or services offered by our competitors; we may engage in acquisitions, dispositions or other strategic transactions tha t may not achieve our anticipated benefits and could otherwise disrupt our business, cause dilution to our stockholders or reduce our financial resources; we may not be successful in commercializing o ur cloud - based distribution model; our products may not perform as expected; the results of our clinical studies, including our SNP - based Microdeletion and Aneuploidy RegisTry, or SMART, Study, may not be compelling to professional societies or payors as supporting the use of our tests, particularly in the average - risk pregnancy population or for microdeletions screening, or may not be able to be replicate d in later studies required for regulatory approvals or clearances; if either of our primary CLIA - certified laboratory facilities becomes inoperable, we will be unable to perform our tests and our business will be harmed; we rely on a limited number of suppliers or, in some cases, single suppliers, for some of our laboratory instruments and materials and may not be able to find replacements or immediately trans iti on to alternative suppliers; if we are unable to successfully scale our operations, our business could suffer; the marketing, sale, and use of Panorama and our other products could result in substantial damage s a rising from product liability or professional liability claims that exceed our resources; we may be unable to expand, obtain or maintain third - party payer coverage and reimbursement for Panorama, Horizon and our other tests, and we may be required to refund reimbursements already received; third - party payers may withdraw coverage or provide lower levels of reimbursement due to changing policies, bi lling complexities or other factors, such as the increased focus by third - party payers on requiring that prior authorization be obtained prior to conducting a test; if the FDA were to begin actively regula tin g our tests, we could incur substantial costs and delays associated with trying to obtain premarket clearance or approval and incur costs associated with complying with post - market controls; litigation or oth er proceedings, resulting from either third party claims of intellectual property infringement or third party infringement of our technology, is costly, time - consuming and could limit our ability to commercial ize our products or services; any inability to effectively protect our proprietary technology could harm our competitive position or our brand; and we cannot guarantee that we will be able to service and comp ly with our outstanding debt obligations or achieve our expectations regarding the conversion of our outstanding convertible notes. We discuss these and other risks and uncertainties in greater detail in the sections entitled “Risk Factors” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” in our periodic reports on Forms 10 - K and 10 - Q and in other filings we make wi th the SEC from time to time. Moreover, we operate in a very competitive and rapidly changing environment. New risks emerge from time to time. It is not possible for our management to predict all risks, no r can we assess the impact of all factors on our business or the extent to which any factor, or combination of factors, may cause actual results to differ materially from those contained in any forward - looking statement. In light of these risks, uncertainties and assumptions, the forward - looking events and circumstances discussed in this presentation may not occur and our actual results could differ materially and adversely from those anticipated or implied. As a result, you should not place undue reliance on our forward - looking statements. Except as required by law, we undertake no obligation to update publicly any f orward - looking statements for any reason after the date of this presentation to conform these statements to actual results or to changes in our expectations. We file reports, proxy statements, and other in formation with the SEC. Such reports, proxy statements, and other information concerning us is available at http://www.sec.gov . Requests for copies of such documents should be directed to our Investor Relations department at Natera, Inc., 13011 McCallen Pa ss, Building A Suite 100, Austin, TX 78753. Our telephone number is (650) 980 - 9190. 2

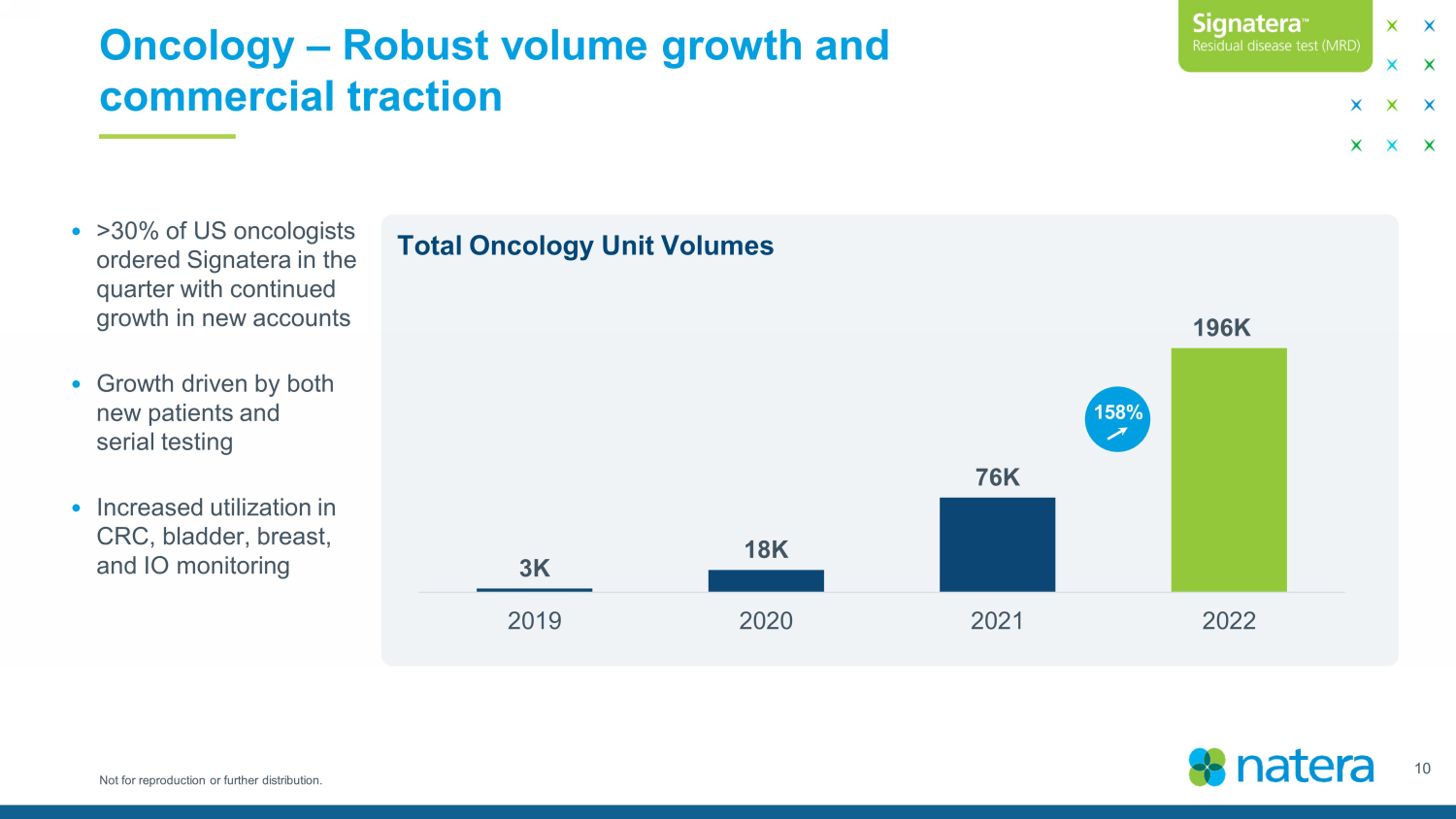

Not for reproduction or further distribution. Recent h ighlights • FY22 total revenues of $820.2M; ~37% growth 1 over 2021. • 2.07M total tests processed in FY22; ~32% growth vs. 2021. • Performed >196K oncology tests in FY22, representing ~158% YoY growth, with 40 published peer - reviewed studies for Signatera to date. • Guiding 2023 total revenue guidance of $980M – $1,000M, reducing cash burn by ~$150M in 2023. • Secured Medicare coverage for breast cancer; fifth coverage decision for Signatera. • Prospective, multi - site CIRCULATE study featured on the cover and lead publication in the January issue of Nature Medicine, which demonstrated Signatera’s ability to predict chemotherapy benefit in colorectal cancer with 18 - months of clinical follow - up. • The American College of Medical Genetics (ACMG) issues new guideline supporting screening for 22q.11.2 deletion syndrome. • The National Society of Genetic Counselors (NSGC) guideline recommends expanded carrier screening be made available to all individuals considering reproduction and all pregnant pairs. • The International Society for Heart and Lung Transplantation (ISHLT) published newly updated guidelines for heart transplant, including dd - cfDNA testing in a Class 1B recommendation. • Seasoned healthcare executive Ruth Williams - Brinkley appointed to the Board, effective 3/2/23. 3 1. Excluding non - recurring revenue of $28.6M from Qiagen arrangement in Q1 2021.

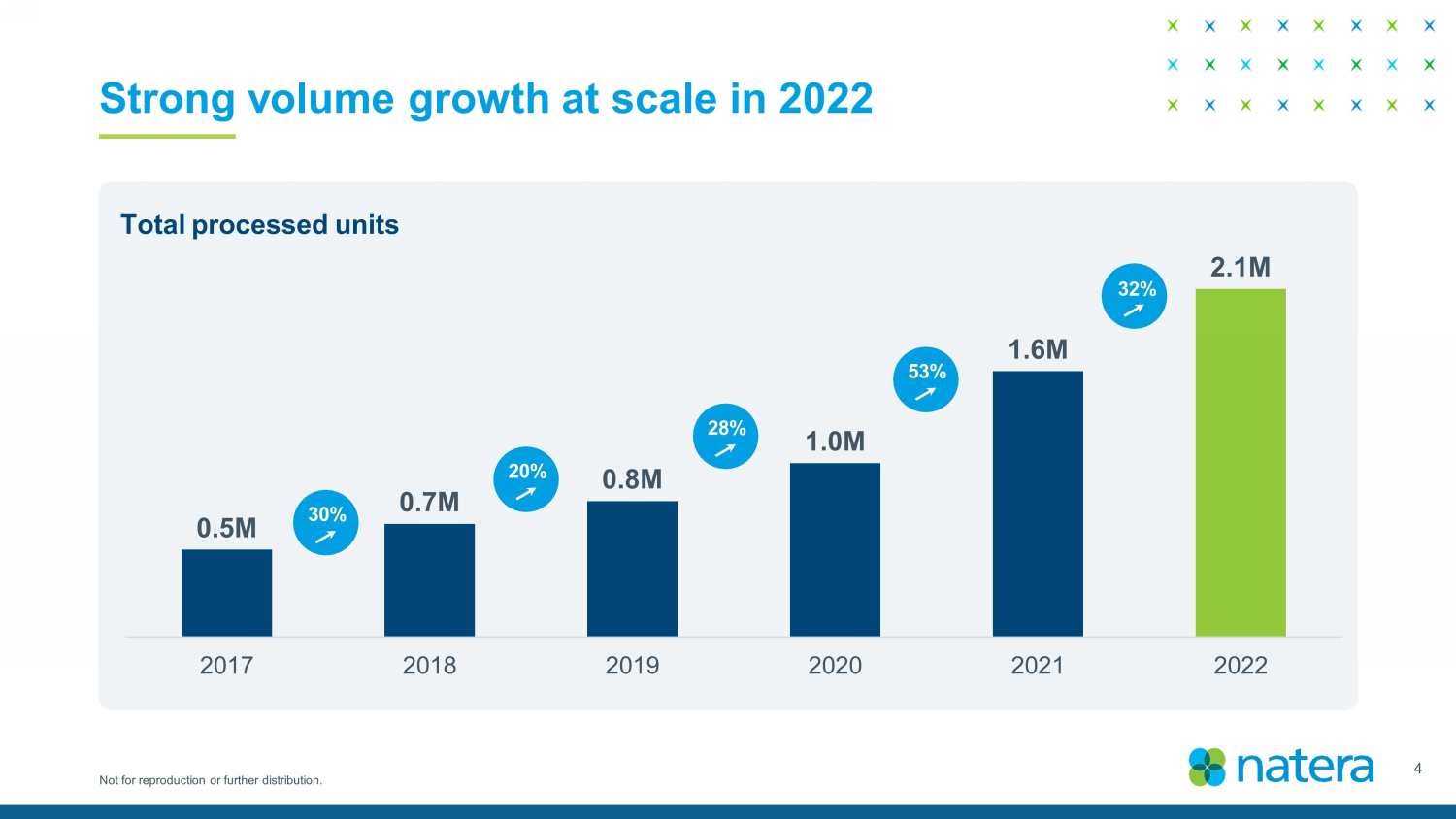

Not for reproduction or further distribution. Strong volume growth at scale in 2022 0.5M 0.7M 0.8M 1.0M 1.6M 2.1M 2017 2018 2019 2020 2021 2022 30 % 20 % 28 % 53 % 32 % Total processed units 4

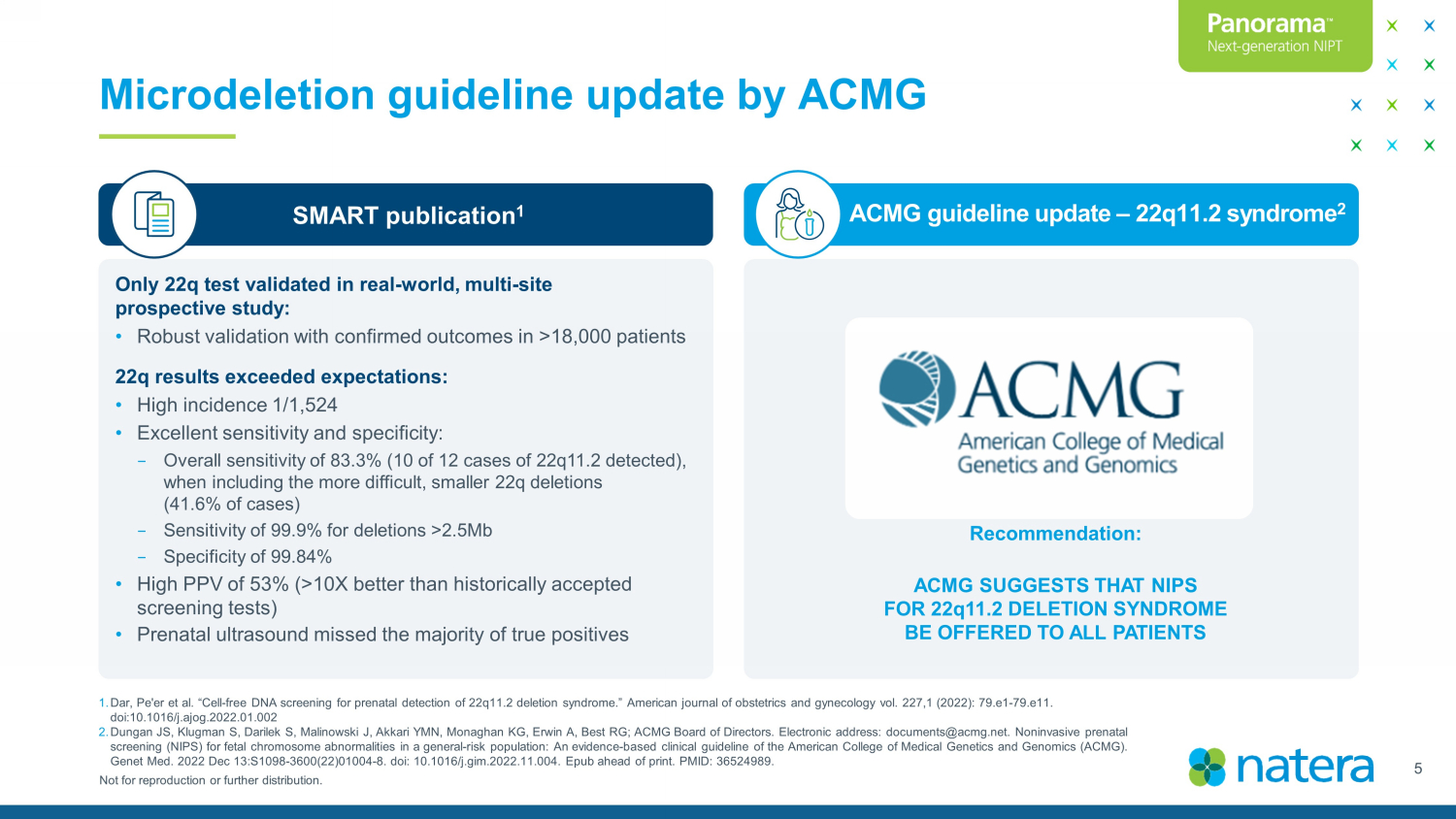

Not for reproduction or further distribution. Microdeletion guideline update by ACMG Only 22q test validated in real - world, multi - site prospective study: • Robust validation with confirmed outcomes in >18,000 patients 22q results exceeded expectations: • High incidence 1/1,524 • E xcellent sensitivity and specificity: − Overall sensitivity of 83.3% (10 of 12 cases of 22q11.2 detected), when including the more difficult, smaller 22q deletions (41.6% of cases) − Sensitivity of 99.9% for deletions >2.5Mb − Specificity of 99.84% • High PPV of 53% (>10X better than historically accepted screening tests) • Prenatal ultrasound missed the majority of true positives SMART publication 1 ACMG guideline update – 22q11.2 syndrome 2 Recommendation: ACMG SUGGESTS THAT NIPS FOR 22q11.2 DELETION SYNDROME BE OFFERED TO ALL PATIENTS 1. Dar, Pe'er et al. “Cell - free DNA screening for prenatal detection of 22q11.2 deletion syndrome.” American journal of obstetrics and gyneco logy vol. 227,1 (2022): 79.e1 - 79.e11. doi:10.1016/j.ajog.2022.01.002 2. Dungan JS, Klugman S, Darilek S, Malinowski J, Akkari YMN, Monaghan KG, Erwin A, Best RG; ACMG Board of Directors. Electronic address: documents@acmg.net. Noninvasive prenatal screening (NIPS) for fetal chromosome abnormalities in a general - risk population: An evidence - based clinical guideline of the Am erican College of Medical Genetics and Genomics (ACMG). Genet Med. 2022 Dec 13:S1098 - 3600(22)01004 - 8. doi : 10.1016/j.gim.2022.11.004. Epub ahead of print. PMID: 36524989. 5

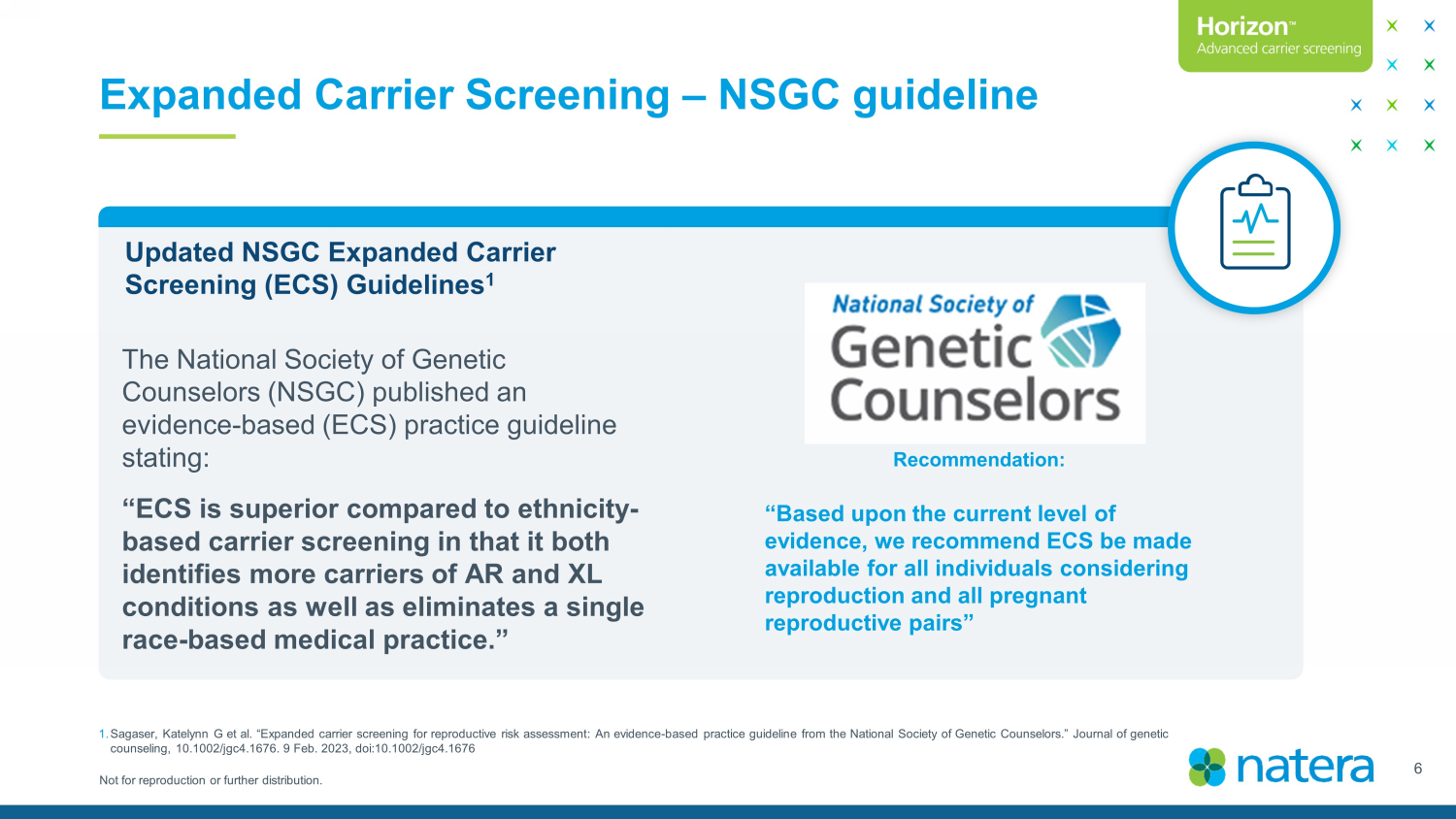

Not for reproduction or further distribution. Expanded Carrier Screening – NSGC guideline 6 Updated NSGC Expanded Carrier Screening (ECS) Guidelines 1 The National Society of Genetic Counselors (NSGC) published an evidence - based (ECS) practice guideline stating: “ECS is superior compared to ethnicity - based carrier screening in that it both identifies more carriers of AR and XL conditions as well as eliminates a single race - based medical practice.” Recommendation: “Based upon the current level of evidence, we recommend ECS be made available for all individuals considering reproduction and all pregnant reproductive pairs ” 1. Sagaser , Katelynn G et al. “Expanded carrier screening for reproductive risk assessment: An evidence - based practice guideline from the National Society of Genetic Counselors.” Journal of genetic counseling, 10.1002/jgc4.1676. 9 Feb. 2023, doi:10.1002/jgc4.1676

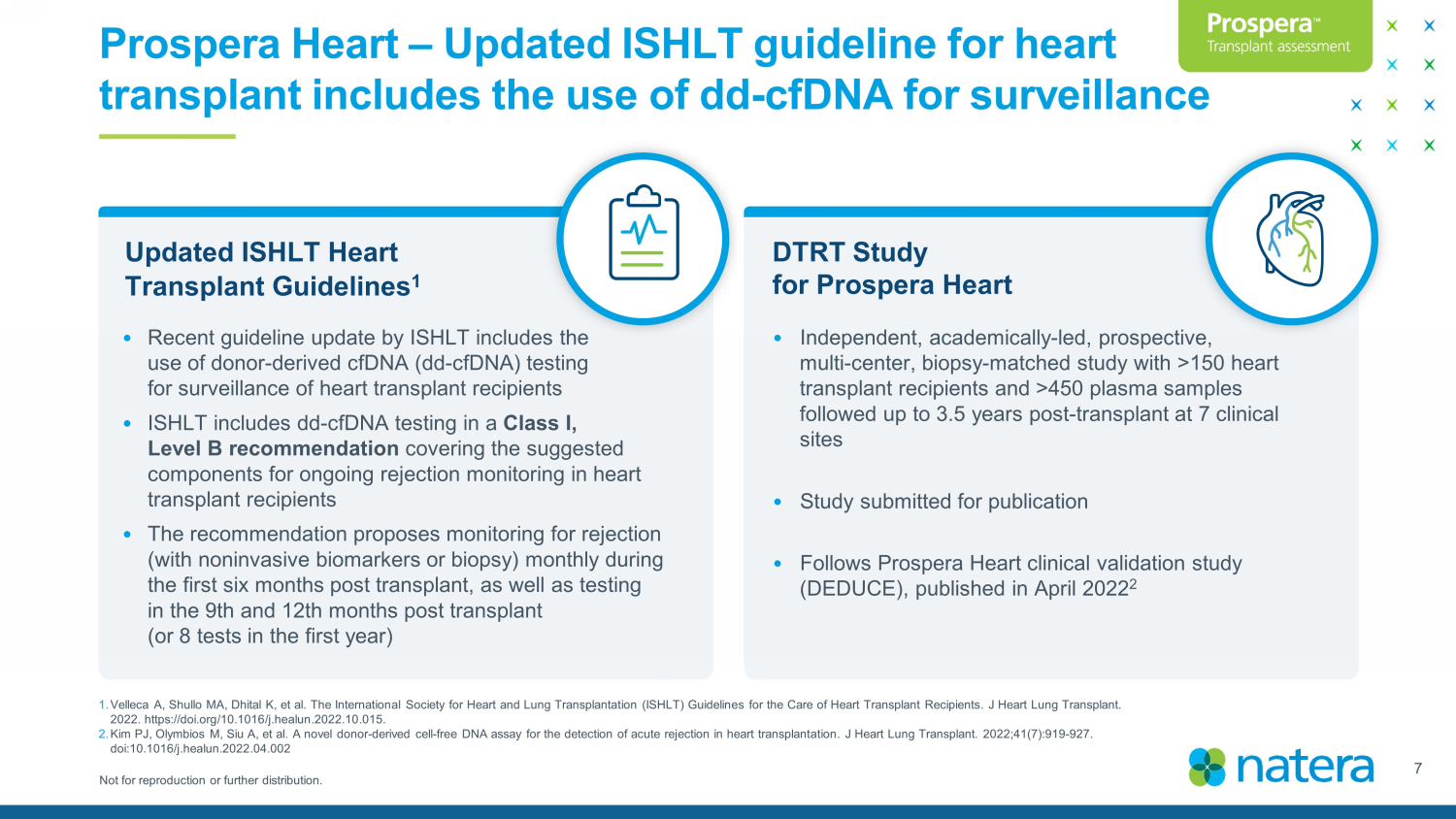

Not for reproduction or further distribution. Prospera Heart – Updated ISHLT guideline for heart transplant includes the use of dd - cfDNA for surveillance DTRT Study for Prospera Heart Updated ISHLT Heart Transplant Guidelines 1 • Recent guideline update by ISHLT includes the use of donor - derived cfDNA (dd - cfDNA) testing for surveillance of heart transplant recipients • ISHLT includes dd - cfDNA testing in a Class I, Level B recommendation covering the suggested components for ongoing rejection monitoring in heart transplant recipients • The recommendation proposes monitoring for rejection (with noninvasive biomarkers or biopsy) monthly during the first six months post transplant, as well as testing in the 9th and 12th months post transplant (or 8 tests in the first year) • Independent, academically - led, prospective, multi - center, biopsy - matched study with >150 heart transplant recipients and >450 plasma samples followed up to 3.5 years post - transplant at 7 clinical sites • Study submitted for publication • Follows Prospera Heart clinical validation study (DEDUCE), published in April 2022 2 7 1. Velleca A, Shullo MA, Dhital K, et al. The International Society for Heart and Lung Transplantation (ISHLT) Guidelines for th e C are of Heart Transplant Recipients. J Heart Lung Transplant. 2022. https://doi.org/10.1016/j.healun.2022.10.015. 2. Kim PJ, Olymbios M, Siu A, et al. A novel donor - derived cell - free DNA assay for the detection of acute rejection in heart transp lantation. J Heart Lung Transplant. 2022;41(7):919 - 927. doi:10.1016/j.healun.2022.04.002

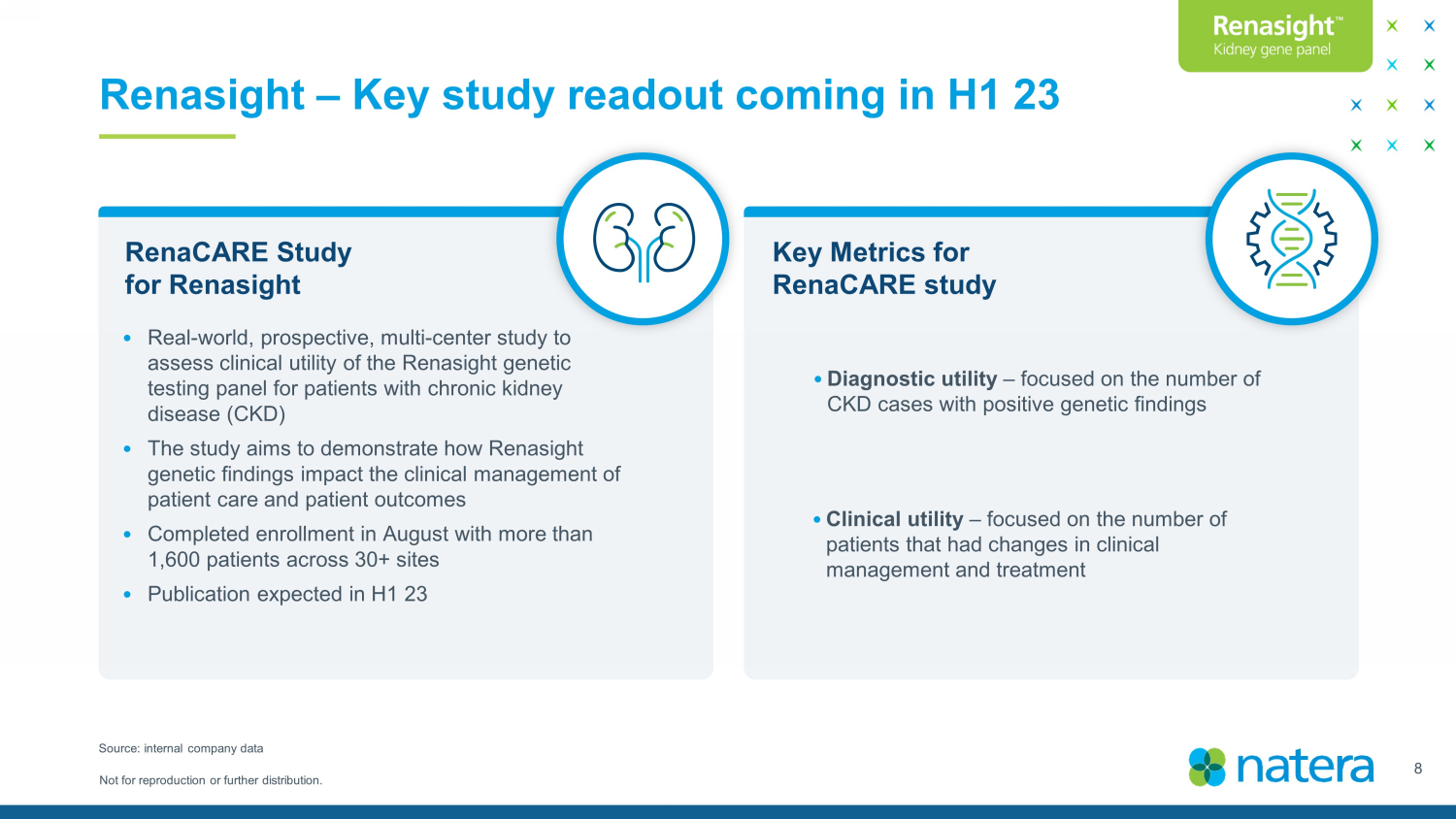

Not for reproduction or further distribution. Renasight – Key study readout coming in H1 23 Key Metrics for RenaCARE study RenaCARE Study for Renasight • Real - world, prospective, multi - center study to assess clinical utility of the Renasight genetic testing panel for patients with chronic kidney disease (CKD) • The study aims to demonstrate how Renasight genetic findings impact the clinical management of patient care and patient outcomes • Completed enrollment in August with more than 1,600 patients across 30+ sites • Publication expected in H1 23 8 Source: internal company data • Diagnostic utility – focused on the number of CKD cases with positive genetic findings • Clinical utility – focused on the number of patients that had changes in clinical management and treatment

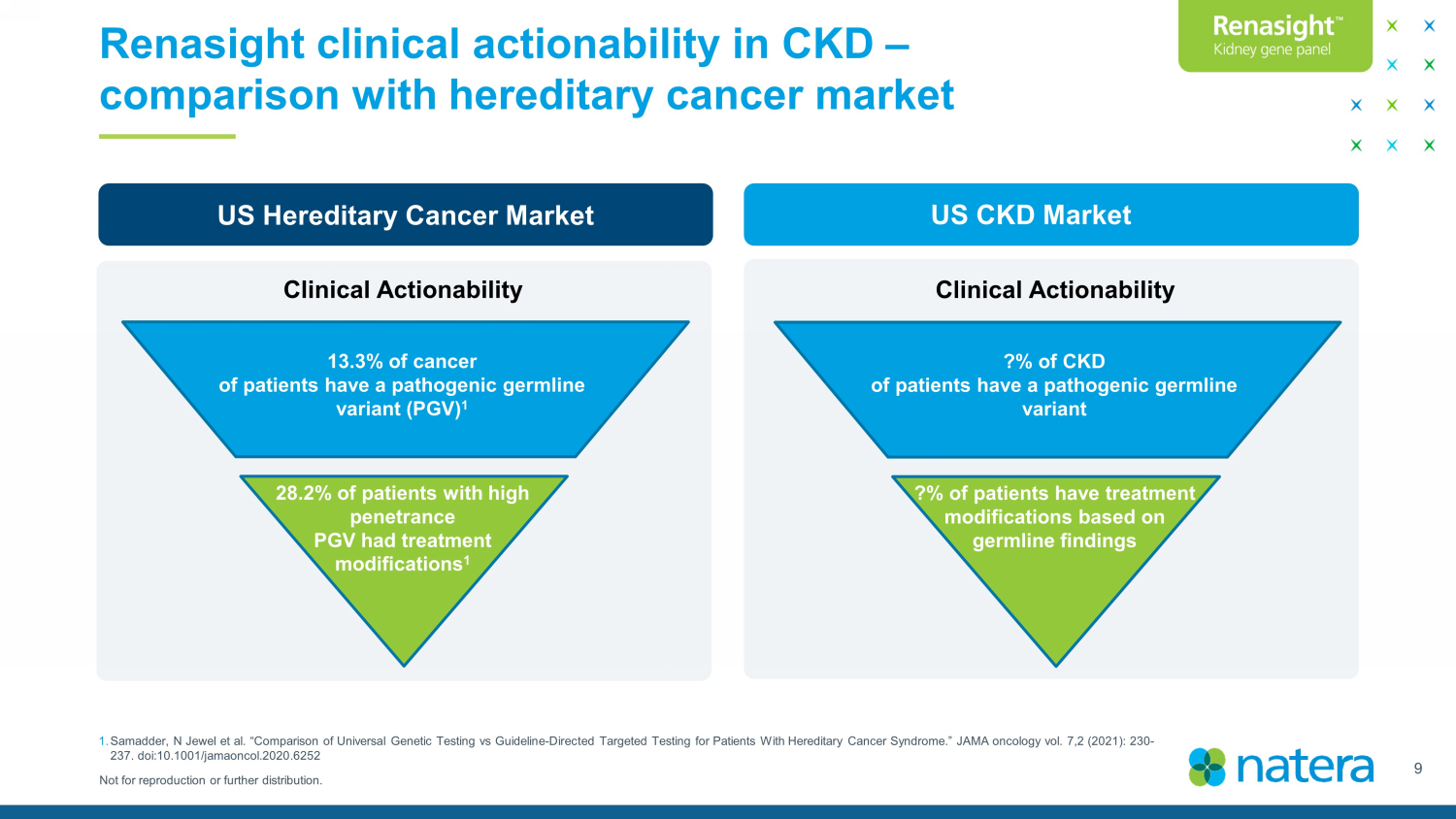

Not for reproduction or further distribution. Renasight clinical actionability in CKD – comparison with hereditary cancer market 9 1. Samadder , N Jewel et al. “Comparison of Universal Genetic Testing vs Guideline - Directed Targeted Testing for Patients With Hereditary Ca ncer Syndrome.” JAMA oncology vol. 7,2 (2021): 230 - 237. doi:10.1001/jamaoncol.2020.6252 [>1M] newly diagnosed patients with CKD US Hereditary Cancer Market 13.3% of cancer of patients have a pathogenic germline variant (PGV) 1 Clinical Actionability 28.2% of patients with high penetrance PGV had treatment modifications 1 US CKD Market ?% of CKD of patients have a pathogenic germline variant Clinical Actionability ?% of patients have treatment modifications based on germline findings

Not for reproduction or further distribution. Oncology – Robust volume growth and commercial traction 3K 18K 76K 196K 2019 2020 2021 2022 158 % Total Oncology Unit Volumes 10 • >30% of US oncologists ordered Signatera in the quarter with continued growth in new accounts • Growth driven by both new patients and serial testing • Increased utilization in CRC, bladder, breast, and IO monitoring

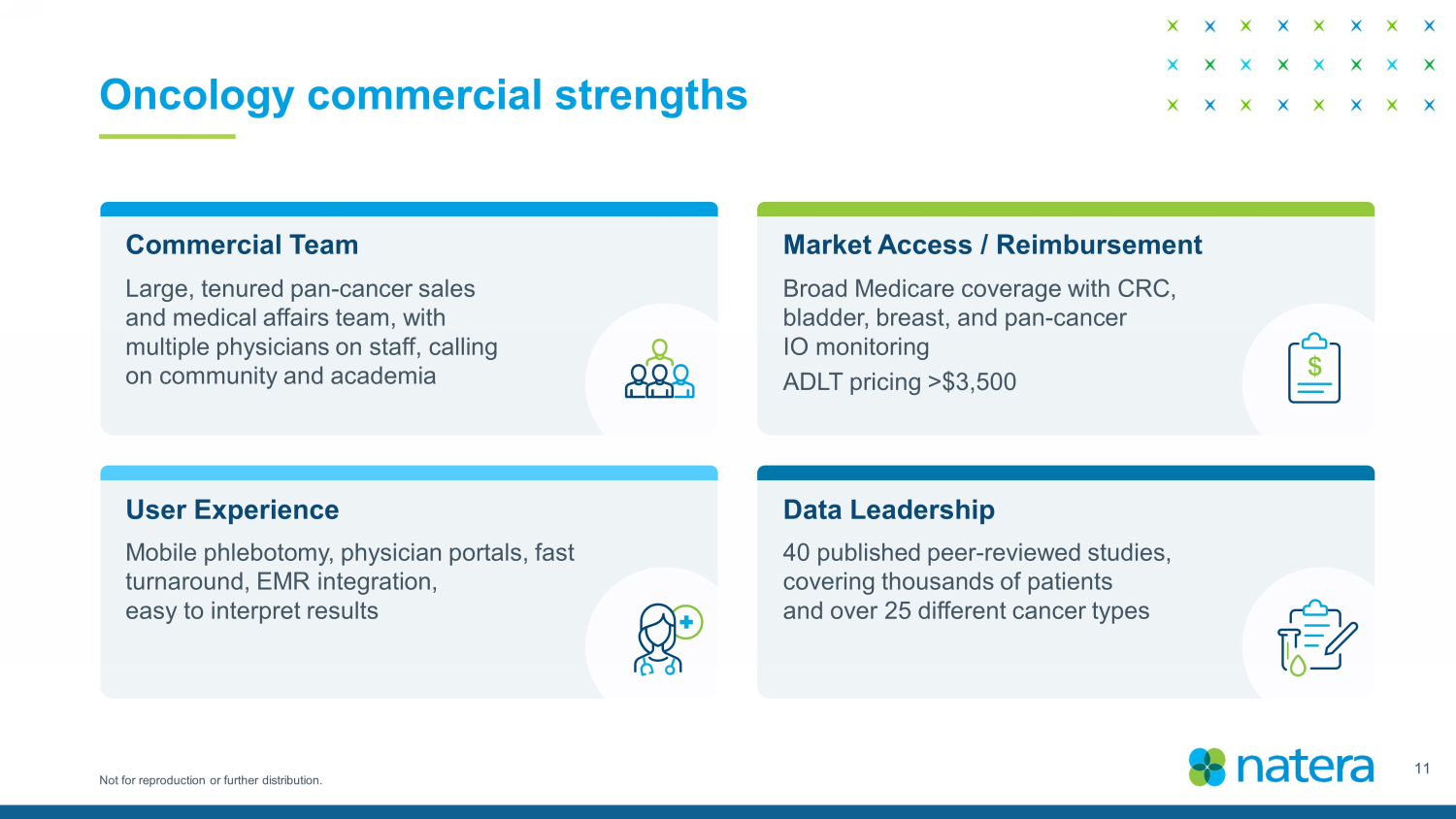

Not for reproduction or further distribution. Commercial Team Market Access / Reimbursement User Experience Data Leadership 40 published peer - reviewed studies, covering thousands of patients and over 25 different cancer types Broad Medicare coverage with CRC, bladder, breast, and pan - cancer IO monitoring ADLT pricing >$3,500 Large, tenured pan - cancer sales and medical affairs team, with multiple physicians on staff, calling on community and academia Mobile phlebotomy, physician portals, fast turnaround, EMR integration, easy to interpret results 11 Oncology commercial strengths

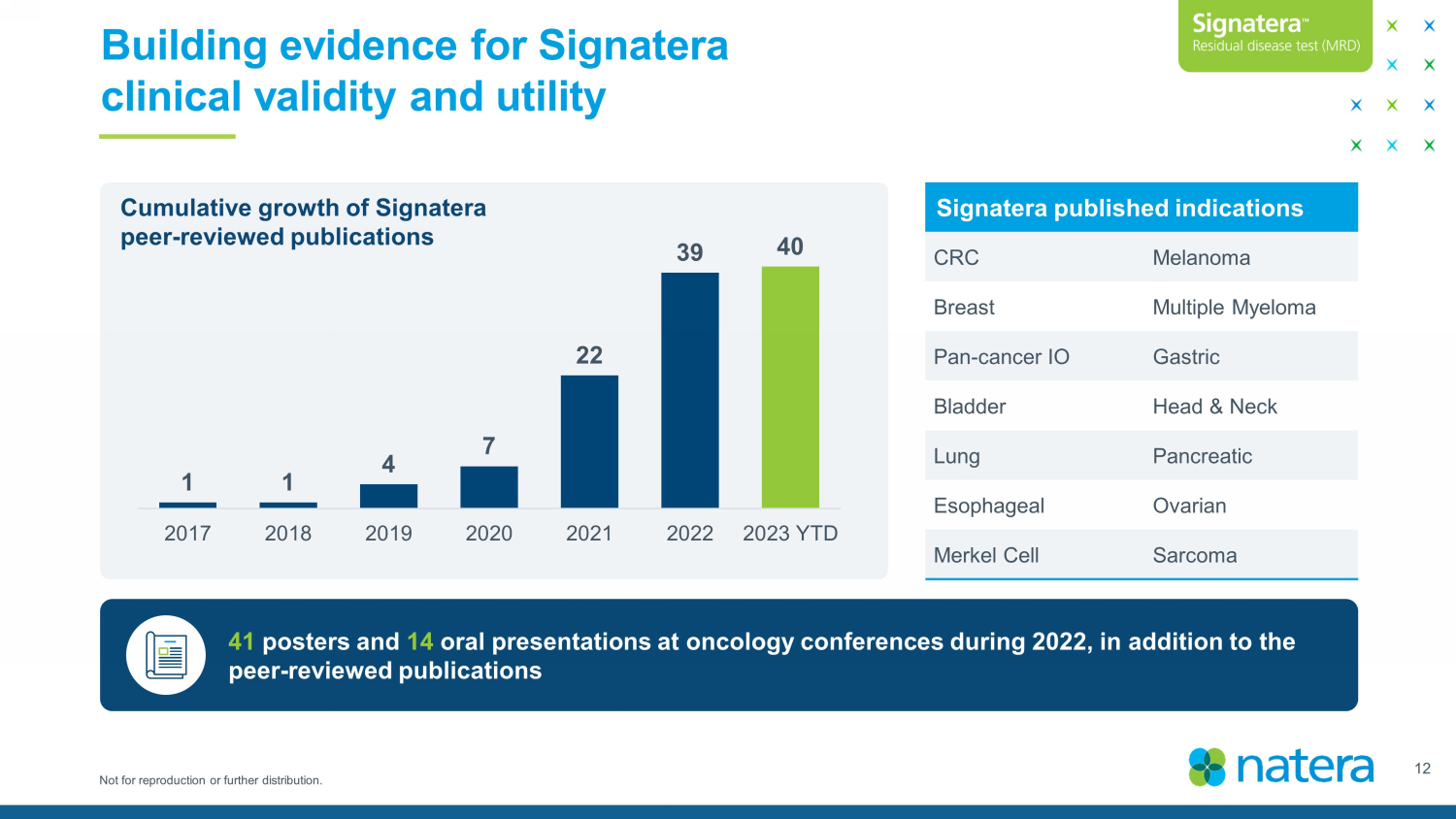

Not for reproduction or further distribution. Building evidence for Signatera clinical validity and utility 12 Signatera published indications CRC Melanoma Breast Multiple Myeloma Pan - cancer IO Gastric Bladder Head & Neck Lung Pancreatic Esophageal Ovarian Merkel Cell Sarcoma 41 posters and 14 oral presentations at oncology conferences during 2022, in addition to the peer - reviewed publications Cumulative growth of Signatera peer - reviewed publications 1 1 4 7 22 39 40 2017 2018 2019 2020 2021 2022 2023 YTD

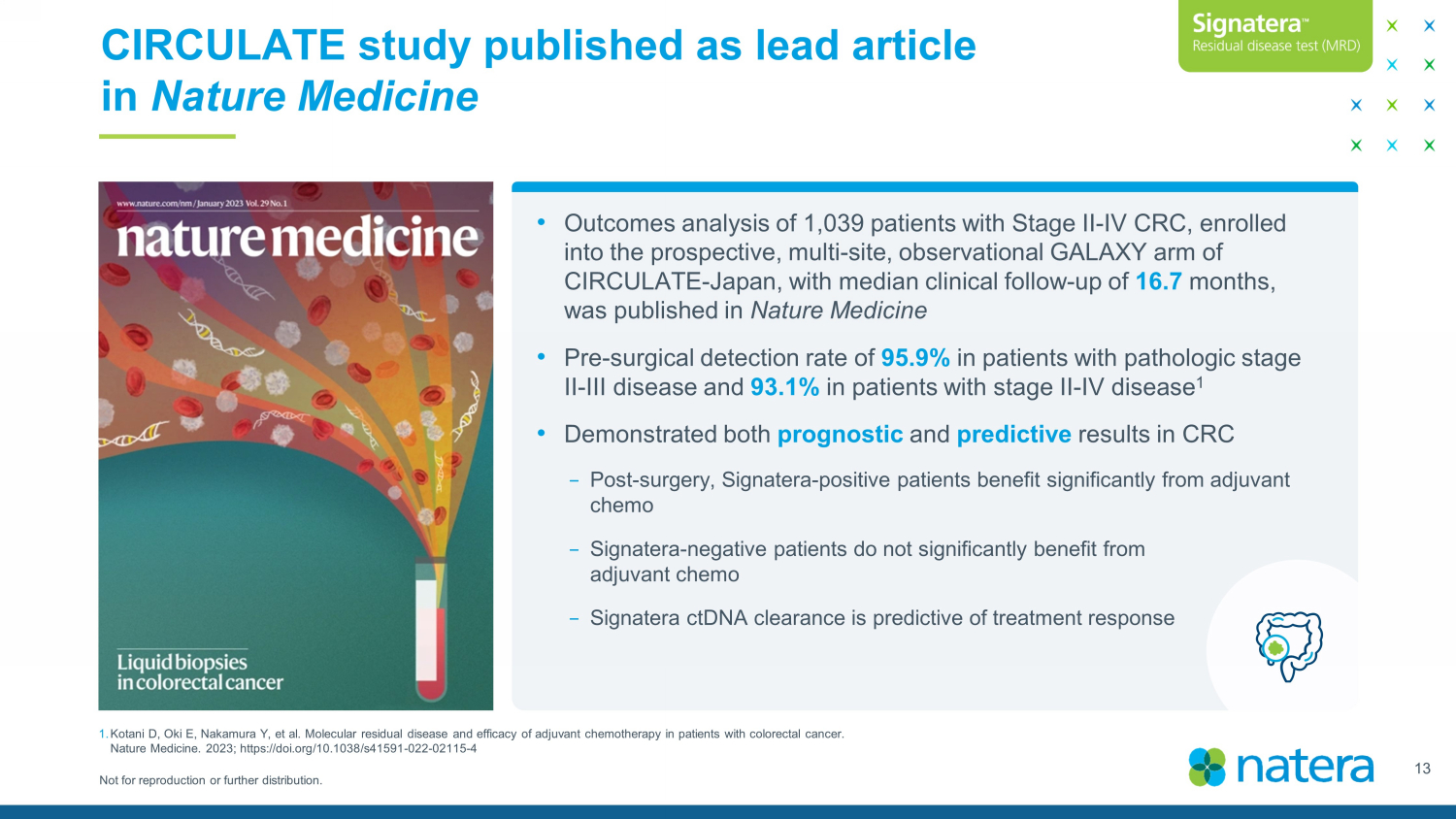

Not for reproduction or further distribution. CIRCULATE study published as lead article in Nature Medicine 13 • Outcomes analysis of 1,039 patients with Stage II - IV CRC, enrolled into the prospective, multi - site, observational GALAXY arm of CIRCULATE - Japan, with median clinical follow - up of 16.7 months, was published in Nature Medicine • Pre - surgical detection rate of 95.9% in patients with pathologic stage II - III disease and 93.1% in patients with stage II - IV disease 1 • Demonstrated both prognostic and predictive results in CRC − Post - surgery, Signatera - positive patients benefit significantly from adjuvant chemo − Signatera - negative patients do not significantly benefit from adjuvant chemo − Signatera ctDNA clearance is predictive of treatment response 1. Kotani D, Oki E, Nakamura Y, et al. Molecular residual disease and efficacy of adjuvant chemotherapy in patients with colorec tal cancer. Nature Medicine. 2023; https://doi.org/10.1038/s41591 - 022 - 02115 - 4

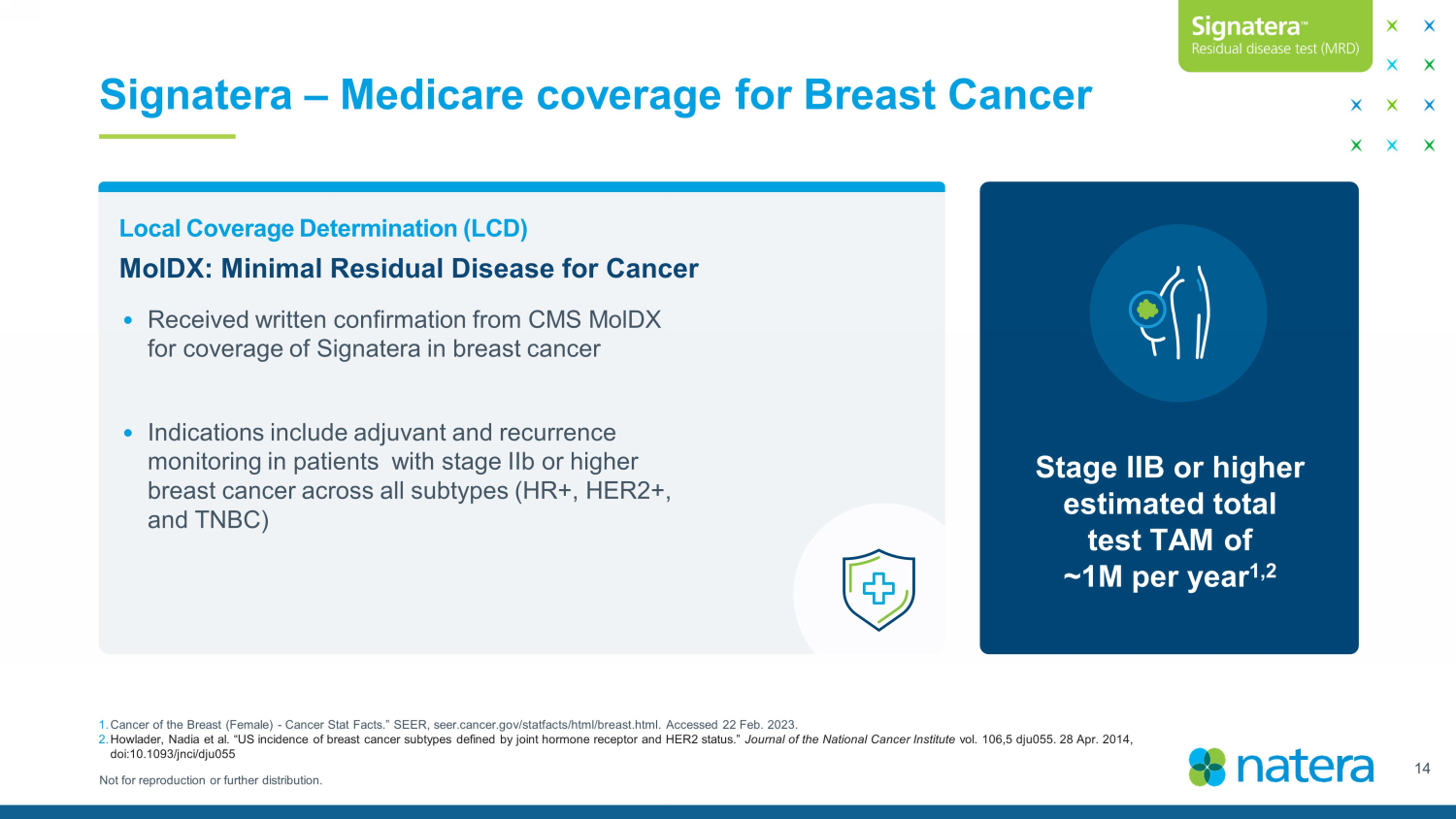

Not for reproduction or further distribution. Signatera – Medicare coverage for Breast Cancer 14 Local Coverage Determination (LCD) • Received written confirmation from CMS MolDX for coverage of Signatera in breast cancer • Indications include adjuvant and recurrence monitoring in patients with stage IIb or higher breast cancer across all subtypes (HR+, HER2+, and TNBC) Stage IIB or higher estimated total test TAM of ~1M per year 1,2 1. Cancer of the Breast (Female) - Cancer Stat Facts.” SEER, seer.cancer.gov/ statfacts /html/breast.html. Accessed 22 Feb. 2023. 2. Howlader , Nadia et al. “US incidence of breast cancer subtypes defined by joint hormone receptor and HER2 status.” Journal of the National Cancer Institute vol. 106,5 dju055. 28 Apr. 2014, doi:10.1093/ jnci /dju055 MolDX : Minimal Residual Disease for Cancer

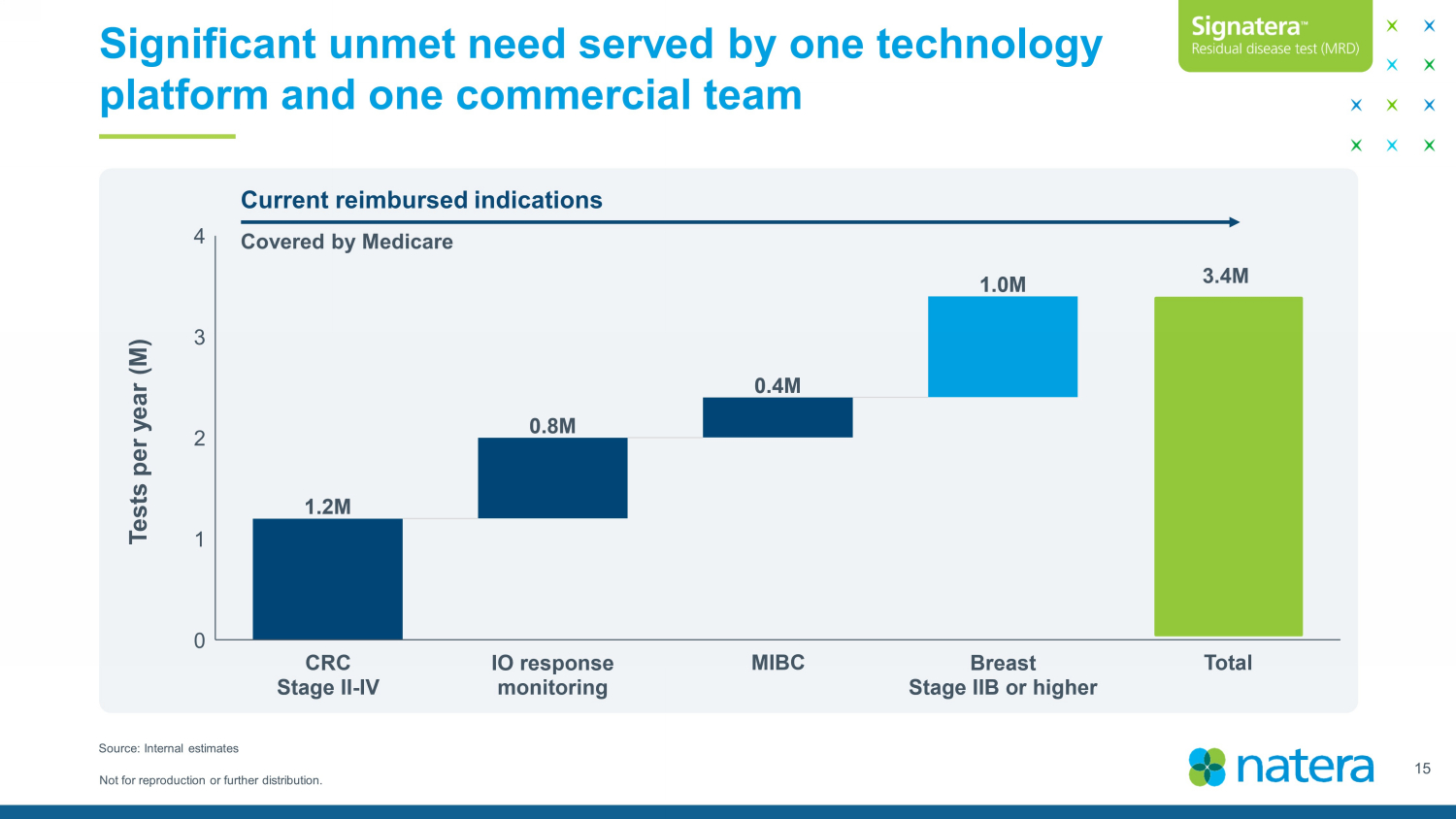

Not for reproduction or further distribution. Significant unmet need served by one technology platform and one commercial team 15 Source: Internal estimates Tests per year (M) Current reimbursed indications Covered by Medicare 3.4M

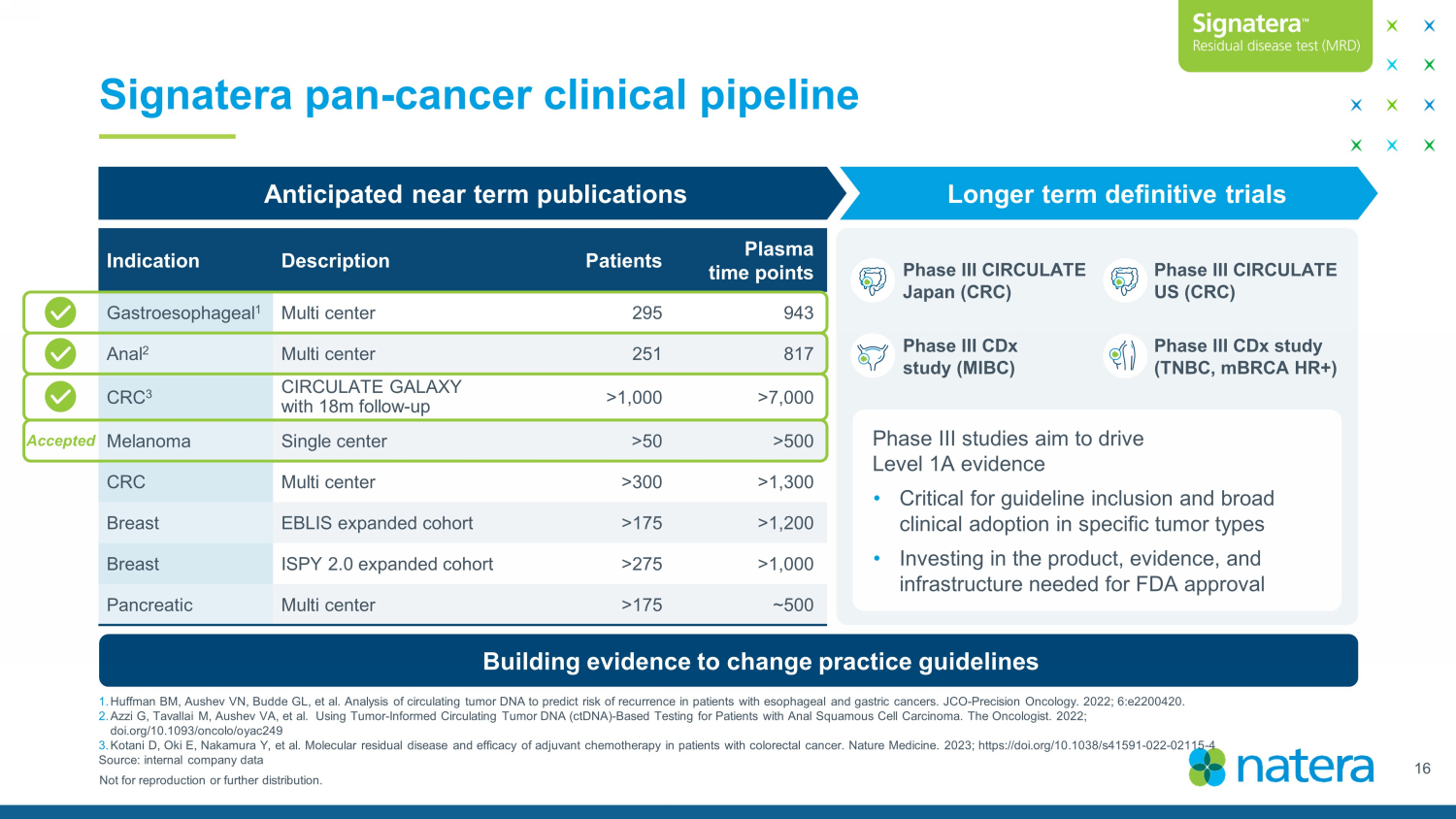

Not for reproduction or further distribution. Signatera pan - cancer clinical pipeline 16 1. Huffman BM, Aushev VN, Budde GL, et al. Analysis of circulating tumor DNA to predict risk of recurrence in patients with esop hag eal and gastric cancers. JCO - Precision Oncology. 2022; 6:e2200420. 2. Azzi G, Tavallai M, Aushev VA, et al. Using Tumor - Informed Circulating Tumor DNA (ctDNA) - Based Testing for Patients with Anal S quamous Cell Carcinoma. The Oncologist. 2022; doi.org/10.1093/oncolo/oyac249 3. Kotani D, Oki E, Nakamura Y, et al. Molecular residual disease and efficacy of adjuvant chemotherapy in patients with colorec tal cancer. Nature Medicine. 2023; https://doi.org/10.1038/s41591 - 022 - 02115 - 4 Source: internal company data Building evidence to change practice guidelines Anticipated near term publications Longer term definitive trials Phase III CIRCULATE Japan (CRC) Phase III CIRCULATE US (CRC) Phase III CDx study (MIBC) Phase III CDx study (TNBC, mBRCA HR+) Phase III studies aim to drive Level 1A evidence • Critical for guideline inclusion and broad clinical adoption in specific tumor types • Investing in the product, evidence, and infrastructure needed for FDA approval Indication Description Patients Plasma time points Gastroesophageal 1 Multi center 295 943 Anal 2 Multi center 251 817 CRC 3 CIRCULATE GALAXY with 18m follow - up >1,000 >7,000 Melanoma Single center >50 >500 CRC Multi center >300 >1,300 Breast EBLIS expanded cohort >175 >1,200 Breast ISPY 2.0 expanded cohort >275 >1,000 Pancreatic Multi center >175 ~500 Accepted

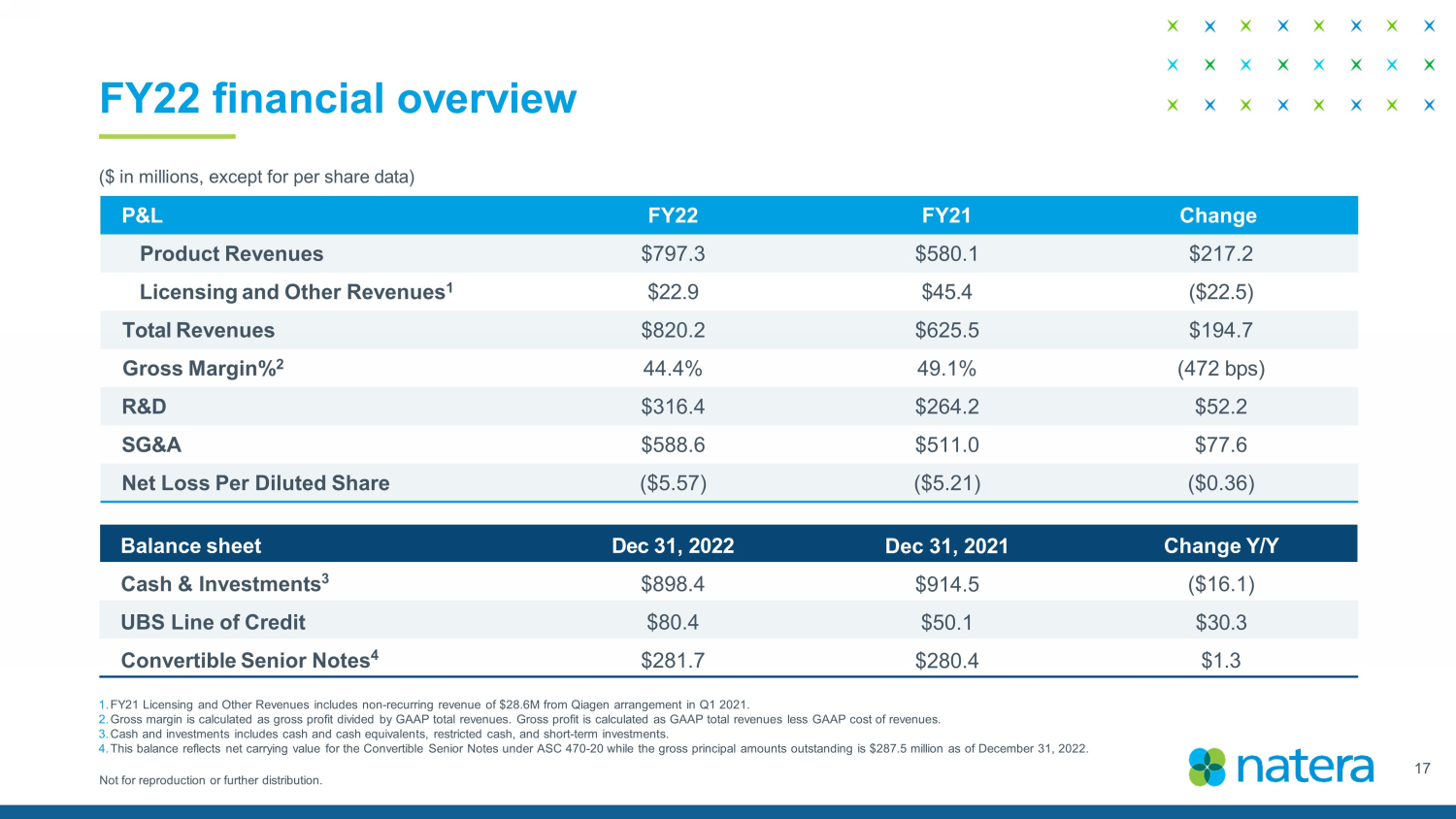

Not for reproduction or further distribution. FY22 financial overview ($ in millions, except for per share data) Balance sheet Dec 3 1 , 2022 Dec 31, 2021 Change Y / Y Cash & Investments 3 $ 898.4 $ 914.5 ($ 16.1 ) UBS Line of Credit $ 80.4 $50.1 $ 30.3 Convertible Senior Notes 4 $ 281.7 $ 280.4 $ 1 . 3 P&L FY22 FY21 Change Product Revenues $ 797.3 $ 580.1 $ 217.2 Licensing and O ther R evenues 1 $ 22.9 $ 45.4 ( $ 22.5) Total Revenues $ 820.2 $ 625.5 $ 194.7 Gross Margin% 2 44. 4 % 4 9.1 % (472 bps ) R&D $ 316.4 $ 264.2 $ 52.2 SG&A $ 588.6 $ 511.0 $ 77.6 Net Loss Per Diluted Share ($ 5 . 57 ) ($ 5.21 ) ( $0. 36) 1. FY21 Licensing and Other Revenues includes non - recurring revenue of $28.6M from Qiagen arrangement in Q1 2021. 2. Gross margin is calculated as gross profit divided by GAAP total revenues. Gross profit is calculated as GAAP total revenues les s GAAP cost of revenues. 3. Cash and investments includes cash and cash equivalents, restricted cash, and short - term investments. 4. This balance reflects net carrying value for the Convertible Senior Notes under ASC 470 - 20 while the gross principal amounts out standing is $287.5 million as of December 31, 2022. 17

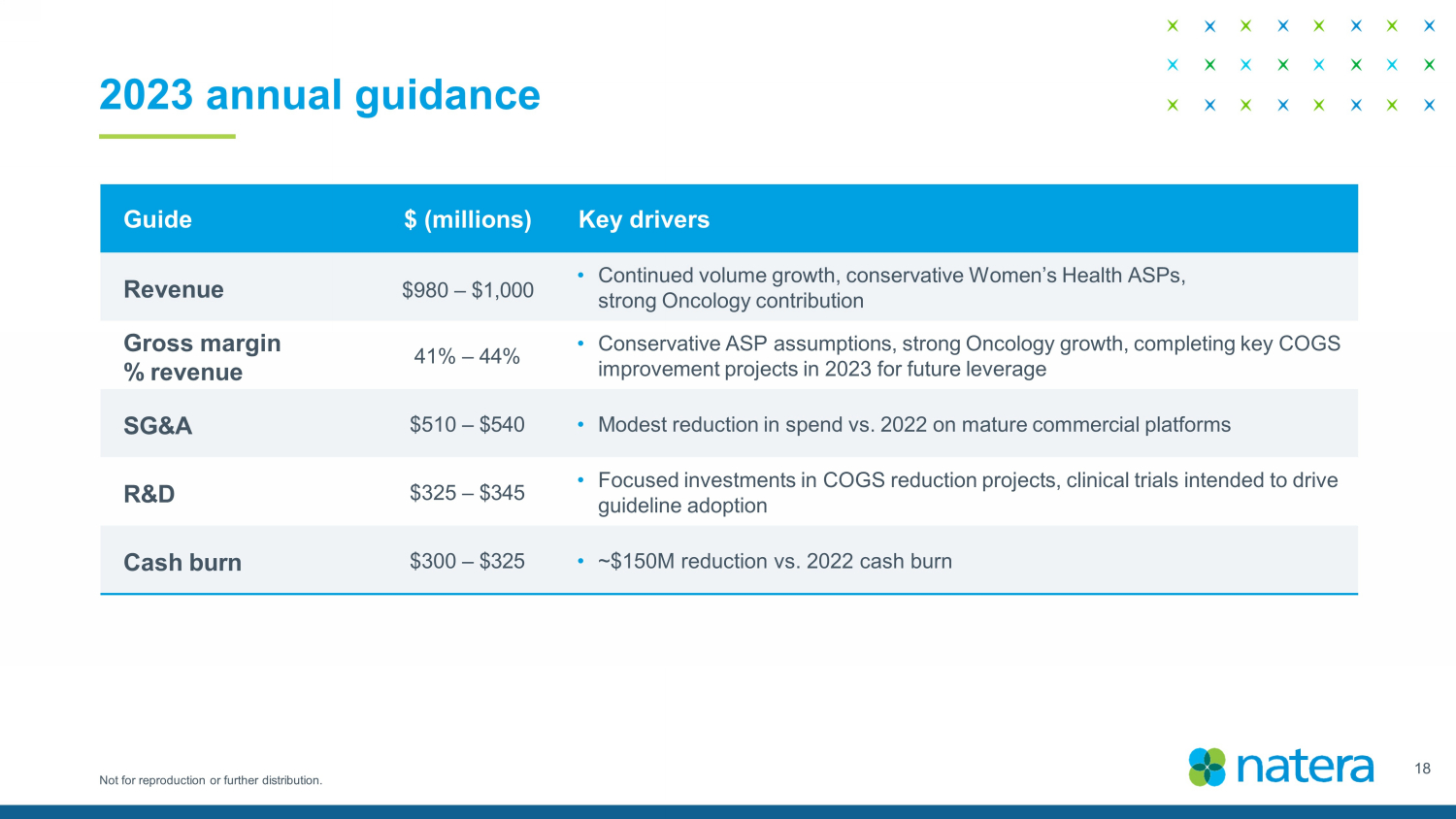

Not for reproduction or further distribution. 2023 annual guidance Guide $ (millions) Key drivers Revenue $ 980 – $ 1,000 • Continued volume growth, conservative Women’s Health ASPs, strong Oncology contribution Gross margin % revenue 4 1 % – 4 4 % • Conservative ASP assumptions, strong Oncology growth, completing key COGS improvement projects in 2023 for future leverage SG&A $5 10 – $5 40 • Modest reduction in spend vs. 2022 on mature commercial platforms R&D $3 25 – $3 45 • Focused investments in COGS reduction projects, clinical trials intended to drive guideline adoption Cash burn $3 00 – $ 325 • ~$150M reduction vs. 2022 cash burn 18

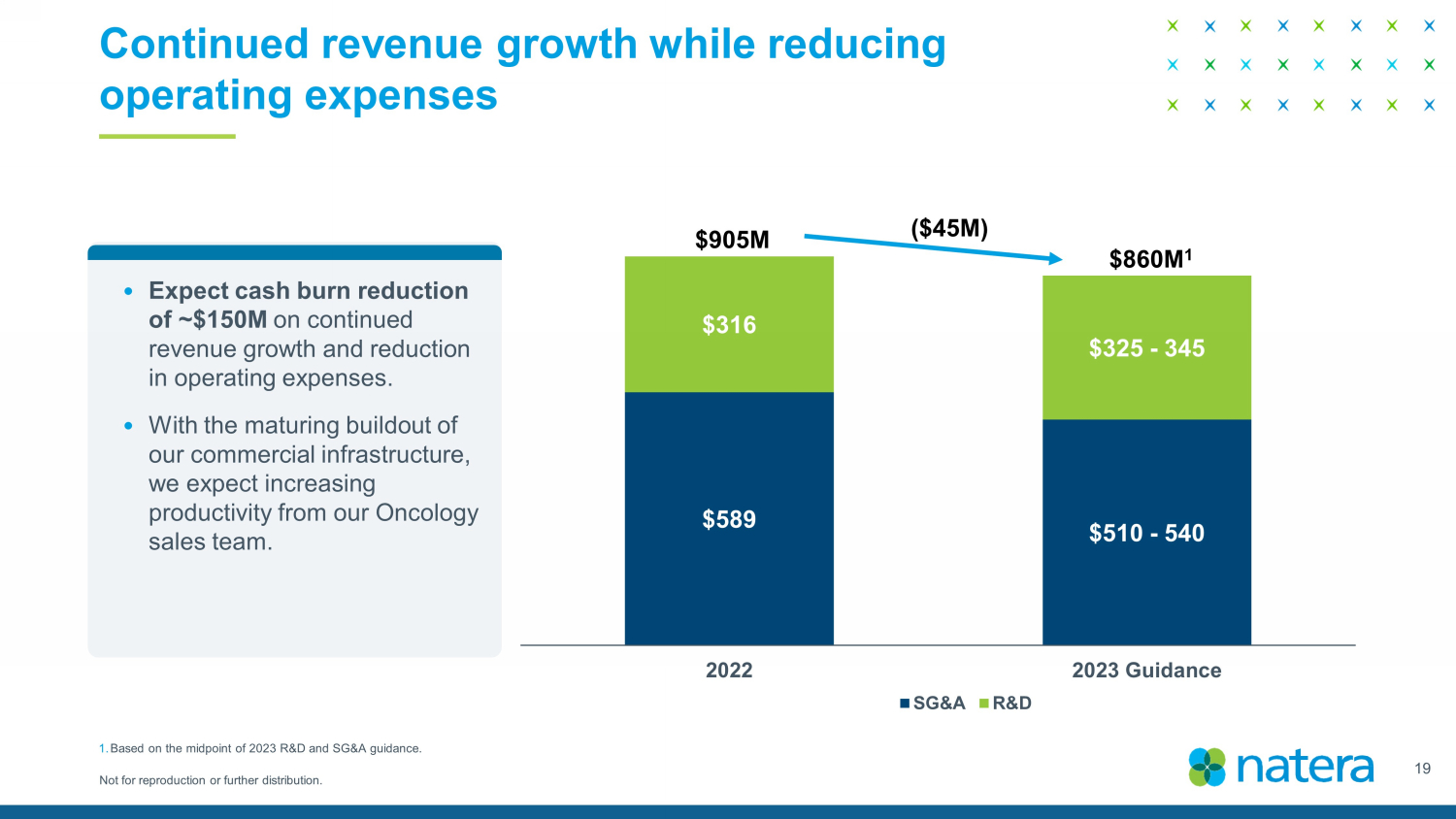

Not for reproduction or further distribution. Continued revenue growth while reducing operating expenses 19 $589 $510 - 540 $316 $325 - 345 2022 2023 Guidance SG&A R&D 53 % $905M $860M 1 ($45M) 1. Based on the midpoint of 2023 R&D and SG&A guidance. • Expect cash burn reduction of ~$150M on continued revenue growth and reduction in operating expenses. • With the maturing buildout of our commercial infrastructure, we expect increasing productivity from our Oncology sales team.

©202 3 Natera, Inc. All Rights Reserved. Not for reproduction or further distribution. ®