UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-K

ý | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the Fiscal Year Ended December 31, 2017 | |

or

¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the Transition Period from to | |

Commission File No. 001-36567

Westlake Chemical Partners LP

(Exact name of registrant as specified in its charter)

Delaware | 32-0436529 | |

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |

2801 Post Oak Boulevard, Suite 600

Houston, Texas 77056

(Address of principal executive offices, including zip code)

(713) 585-2900

(Registrant's telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

Title of each class | Name of each exchange on which registered | |

Common units representing limited partner interests | New York Stock Exchange, Inc. | |

Securities registered pursuant to Section 12(g) of the Act: NONE

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No ý

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No ý

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ý No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ý No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of "large accelerated filer," "accelerated filer" and "smaller reporting company" in Rule 12b-2 of the Exchange Act:

Large accelerated filer ¨ | Accelerated filer x | Non-accelerated filer ¨ | Smaller reporting company ¨ | |||

(Do not check if a smaller reporting company) | ||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ¨

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ¨ No ý

The aggregate market value of registrant's common units held by non-affiliates of the registrant on June 30, 2017, the end of the registrant's most recently completed second fiscal quarter, based on the closing price on June 30, 2017 of $24.75 on the New York Stock Exchange, was approximately $314.0 million. Common units held by executive officers and directors of the registrant and its affiliates are not included in the computation. The registrant, solely for the purpose of this required presentation, has deemed its directors and executive officers and those of its affiliates to be affiliates.

As of February 22, 2018, the registrant had 32,237,266 common units and no subordinated units outstanding.

TABLE OF CONTENTS

Explanatory Note

On August 4, 2014, Westlake Chemical Partners LP completed an initial public offering (the "IPO"). Unless otherwise indicated, references in this Annual Report on Form 10-K (this "report") to "we," "our," "us" or like terms used in the present tense or prospectively, or in reference to the period subsequent to the IPO, refer to Westlake Chemical Partners LP ("Westlake Chemical Partners LP" or the "Partnership"), Westlake Chemical OpCo LP ("OpCo") and Westlake Chemical OpCo GP LLC ("OpCo GP"). Unless the context otherwise requires, references in this report to the "Predecessor" refer to Westlake Chemical Partners LP Predecessor, our predecessor for accounting purposes, and refer to the time periods prior to the IPO. References to "Westlake" refer to Westlake Chemical Corporation and its consolidated subsidiaries other than the Partnership, OpCo GP and OpCo. References to our "board of directors" or our "directors" refer to the board of directors of our general partner and such board's directors, respectively. See Note 1 to our consolidated financial statements for information regarding the closing of the IPO.

Cautionary Statement Regarding Forward-Looking Statements

Certain of the statements contained in this report are forward-looking statements. All statements, other than statements of historical facts, included in this report that address activities, events or developments that we expect, project, believe or anticipate will or may occur in the future are forward-looking statements. Forward-looking statements can be identified by the use of words such as "believes," "intends," "may," "should," "could," "anticipates," "expects," "will" or comparable terminology, or by discussions of strategies or trends. Although we believe that the expectations reflected in such forward-looking statements are reasonable, we cannot give any assurances that these expectations will prove to be correct. Forward-looking statements relate to matters such as:

• | the amount of ethane that we are able to process, which could be adversely affected by, among other things, operating difficulties; |

• | the volume of ethylene that we are able to sell; |

• | the price at which we are able to sell ethylene; |

• | industry market outlook, including prices and margins in third-party ethylene and co-products sales; |

• | the parties to whom we will sell ethylene and on what basis; |

• | volumes of ethylene that Westlake may purchase, in addition to the minimum commitment under the Ethylene Sales Agreement; |

• | timing, funding and results of capital projects; |

• | our intended minimum quarterly distributions and the manner of making such distributions; |

• | our ability to meet our liquidity needs; |

• | timing of and amount of capital expenditures; |

• | potential loans from Westlake to OpCo to fund OpCo's expansion capital expenditures in the future; |

• | expected mitigation of exposure to commodity price fluctuations; |

• | turnaround activities and the variability of OpCo's cash flow; |

• | compliance with present and future environmental regulations and costs associated with environmentally related penalties, capital expenditures, remedial actions and proceedings, including any new laws, regulations or treaties that may come into force to limit or control carbon dioxide and other greenhouse gas emissions or to address other issues of climate change; and |

• | effects of pending legal proceedings. |

We have based these statements on assumptions and analysis in light of our experience and perception of historical trends, current conditions, expected future developments and other factors we believe were appropriate in the circumstances when the statements were made. Forward-looking statements by their nature involve substantial risks and uncertainties that could significantly impact expected results, and actual future results could differ materially from those described in such statements. These statements are subject to a number of assumptions, risks and uncertainties, including those described in "Part 1. Item 1A. Risk Factors" of this report and the following:

• | general economic and business conditions; |

• | the cyclical nature of the chemical industry; |

i

• | the availability, cost and volatility of raw materials and energy; |

• | uncertainties associated with the United States and worldwide economies, including those due to political tensions and unrest in the Middle East, the Commonwealth of Independent States (including Ukraine) and elsewhere; |

• | current and potential governmental regulatory actions in the United States and regulatory actions and political unrest in other countries; |

• | industry production capacity and operating rates; |

• | the supply/demand balance for our product; |

• | competitive products and pricing pressures; |

• | instability in the credit and financial markets; |

• | access to capital markets; |

• | terrorist acts; |

• | operating interruptions (including leaks, explosions, fires, weather-related incidents, mechanical failure, unscheduled downtime, labor difficulties, transportation interruptions, spills and releases and other environmental risks); |

• | changes in laws or regulations; |

• | technological developments; |

• | our ability to integrate acquired businesses; |

• | foreign currency exchange risks; |

• | our ability to implement our business strategies; and |

• | creditworthiness of our customers. |

Many of these factors are beyond our ability to control or predict. Any of the factors, or a combination of these factors, could materially affect our future results of operations and the ultimate accuracy of the forward-looking statements. These forward-looking statements are not guarantees of our future performance, and our actual results and future developments may differ materially from those projected in the forward-looking statements. Management cautions against putting undue reliance on forward-looking statements or projecting any future results based on such statements or present or prior earnings levels. Every forward-looking statement speaks only as of the date of the particular statement, and we undertake no obligation to publicly update or revise any forward-looking statements.

Industry and Market Data

Industry and market data used throughout this report were obtained through internal research, surveys and studies conducted by unrelated third parties and publicly available industry and general publications, including information from IHS Markit (formerly IHS Chemical) ("IHS"). We have not independently verified market and industry data from external sources. While we believe internal partnership estimates are reliable and market definitions are appropriate, neither such estimates nor these definitions have been verified by any independent sources.

Production Capacity

Unless we state otherwise, annual production capacity estimates used throughout this report represent rated capacity of the facilities at December 31, 2017. We calculated rated capacity by estimating the number of days in a typical year that a production unit of a plant is expected to operate, after allowing for downtime for regular maintenance, and multiplying that number by an amount equal to the unit's optimal daily output based on the design feedstock mix. Because the rated capacity of a production unit is an estimated amount, actual production volumes may be more or less than the rated capacity.

ii

PART I

Item 1. Business

General

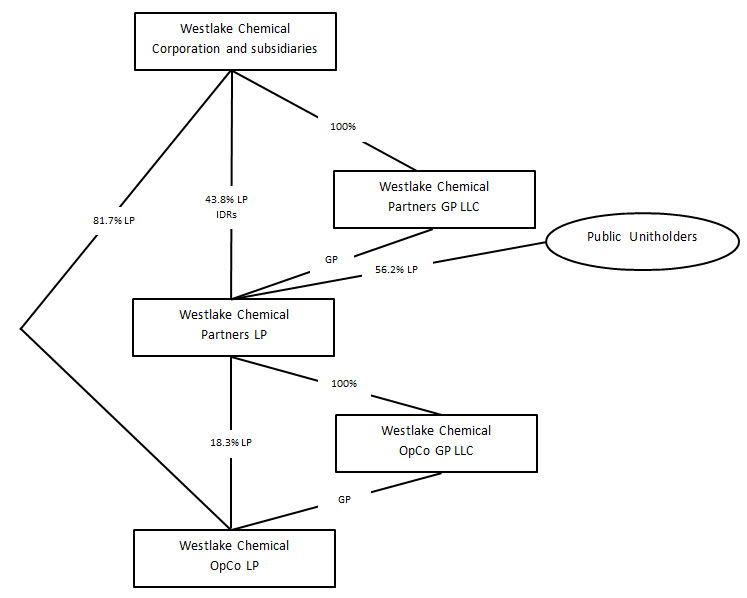

We are a Delaware limited partnership formed by Westlake in March 2014 to operate, acquire and develop ethylene production facilities and related assets. On August 4, 2014, we completed our initial public offering (the "IPO") of 12,937,500 common units representing limited partner interests. In connection with the IPO, we acquired a 10.6% interest in OpCo and a 100% interest in OpCo GP, which is the general partner of OpCo. On April 29, 2015, we purchased an additional 2.7% newly-issued limited partner interest in OpCo, resulting in an aggregate 13.3% limited partner interest in OpCo effective April 1, 2015. Effective August 30, 2017, the subordination period for the 12,686,115 subordinated units owned by Westlake ended and the subordinated units converted into common units on a one-for-one basis and thereafter participate on terms equal with all other common units in distributions of available cash. On September 29, 2017, we completed a secondary offering of 5,175,000 common units at a price of $22.00 per unit and purchased an additional 5.0% newly-issued limited partner interest in OpCo, resulting in an aggregate 18.3% limited partner interest in OpCo, effective as of July 1, 2017.

Our business and operations are conducted through OpCo. Because we own OpCo's general partner, we have control over all of OpCo's assets and operations. As of December 31, 2017, Westlake held an 81.7% limited partner interest in OpCo and held a 43.8% limited partner interest in us (consisting of 14,122,230 common units), our general partner interest and our incentive distribution rights.

OpCo's assets are comprised of three ethylene production facilities, which primarily convert ethane into ethylene and have an aggregate annual capacity of approximately 3.7 billion pounds, and a 200-mile ethylene pipeline. OpCo derives substantially all of its revenue from these ethylene production facilities. Ethylene is the world's most widely used petrochemical in terms of volume and is a key building block used to produce a number of key derivatives, such as polyethylene ("PE") and polyvinyl chloride ("PVC"), which are used in a wide variety of end markets including packaging, construction and transportation. Westlake's downstream PE and PVC production facilities consume a substantial majority of the ethylene produced by OpCo. OpCo generates revenue primarily by selling ethylene to Westlake and others, as well as through the sale of co-products of ethylene production, including propylene, crude butadiene, pyrolysis gasoline and hydrogen. Our sole revenue generating asset is our 18.3% limited partner interest in OpCo.

Our assets and operations are organized into a single reportable segment and are all located and conducted in the United States. See "Item 8. Financial Statements and Supplementary Data" for financial information on our operations and assets; such information is incorporated herein by reference.

Among other agreements entered into in connection with the closing of the IPO, OpCo entered into a 12-year ethylene sales agreement with Westlake, under which Westlake agreed to purchase 95% of OpCo's planned ethylene production each year, on a cost-plus basis that is expected to generate a fixed margin per pound of $0.10 (the "Ethylene Sales Agreement"). Any ethylene not sold to Westlake and all co-products that are produced by OpCo will be sold to third parties on either a spot or contract basis. OpCo also entered into a feedstock supply agreement with Westlake that supplies OpCo with all of the ethane (and any other feedstocks) required for OpCo to produce ethylene under the Ethylene Sales Agreement (the "Feedstock Supply Agreement").

OpCo primarily uses ethane (a component of natural gas liquids, or NGLs) to produce ethylene. OpCo completed an upgrade and capacity expansion of its Petro 1 ethylene unit at our Lake Charles site in 2016. The Petro 1 expansion project increased OpCo's ethylene capacity by approximately 250 million pounds annually. OpCo completed an expansion project to increase the ethylene capacity at our Calvert City facility in the second quarter of 2017. The expansion, along with other initiatives, increased ethylene capacity by approximately 100 million pounds annually.

1

Ownership of Westlake Chemical Partners LP

The following simplified diagram depicts our organizational structure as of December 31, 2017:

Public Common Units | 56.2 | % | |

Interests of Westlake: | |||

Common Units | 43.8 | % | |

Non-Economic General Partner Interest | — | ||

Incentive Distribution Rights | — | (1) | |

100.0 | % | ||

______________________________

(1) | Incentive distribution rights represent a variable interest in distributions and thus are not expressed as a fixed percentage. Distributions with respect to the incentive distribution rights are classified as distributions with respect to equity interests. |

2

Our Assets and Operations

Our sole revenue generating asset is our 18.3% limited partner interest in OpCo. We also own the general partner interest of OpCo. OpCo owns:

• | two ethylene production facilities at Westlake's Lake Charles, Louisiana site ("Petro 1" and "Petro 2," collectively referred to as "Lake Charles Olefins"), with an annual combined capacity of approximately 3.0 billion pounds; |

• | one ethylene production facility at Westlake's Calvert City, Kentucky site ("Calvert City Olefins"), with an annual capacity of approximately 730 million pounds; and |

• | a 200-mile common carrier ethylene pipeline that runs from Mont Belvieu, Texas to the Longview, Texas chemical site, which includes Westlake's Longview PE production facility (the "Longview Pipeline"). |

As the owner of the general partner interest of OpCo, we control all aspects of the management of OpCo, including its cash distribution policy. See "—OpCo's Assets."

OpCo's Assets

Ethylene Production Facilities. OpCo operates three ethylene production facilities that are situated on real property leased to OpCo by Westlake pursuant to two 50-year site lease agreements. See "Our Agreements with Westlake—Site Lease Agreements" for a description of the site leases. Ethylene can be produced from either NGL feedstocks, such as ethane, propane and butane, or from petroleum-derived feedstocks, such as naphtha. Lake Charles Olefins and Calvert City Olefins use primarily ethane as their feedstock. Calvert City Olefins can also use propane as a feedstock and Petro 2 can also use an ethane/propane mix, propane, butane or naphtha as a feedstock.

The following table provides information regarding OpCo's ethylene production facilities as of December 31, 2017:

Plant Location (Description) | Annual Production Capacity (millions of pounds) | Feedstock | Primary Uses of Ethylene | |||||

Lake Charles, Louisiana (Petro 1) | 1,500 | Ethane | PE and PVC | |||||

Lake Charles, Louisiana (Petro 2) | 1,490 | Ethane, ethane/propane mix, propane, butane or naphtha | PE and PVC | |||||

Calvert City, Kentucky (Calvert City Olefins) | 730 | Ethane or propane | PVC | |||||

Total | 3,720 | |||||||

Lake Charles Olefins

Two of OpCo's ethylene production facilities, which we refer to as Petro 1 and Petro 2 and, collectively, as Lake Charles Olefins, are located at Westlake's Lake Charles site. The combined capacity of these two ethylene production facilities is approximately 3.0 billion pounds per year.

Within Westlake's Lake Charles site, Petro 1 and Petro 2 are connected by pipeline systems to Westlake's polyethylene plants. Westlake may use the ethylene it purchases from OpCo at its Lake Charles facility or transfer it to its Geismar facility or its Longview facility, either through physical transportation or via exchange transactions. Westlake may also use the ethylene it purchases from OpCo with chlorine to produce ethylene dichloride and transport it via barge to Westlake's Calvert City site.

In addition, OpCo produces ethylene co-products including chemical grade propylene, crude butadiene, pyrolysis gasoline and hydrogen. OpCo sells its output of these co-products to external customers.

Calvert City Olefins

One of OpCo's ethylene production facilities is located at Westlake's Calvert City site, which we refer to as Calvert City Olefins. The capacity of Calvert City Olefins is approximately 730 million pounds per year.

Pipeline

OpCo owns a 200-mile 10-inch diameter ethylene pipeline system that connects the Equistar Pipeline, the Flint Hills Pipeline and the Lone Star Storage Facility in Mont Belvieu to the Longview, Texas chemical site, which includes Westlake's Longview PE production facility. The system has a capacity of 3.5 million pounds per day of ethylene and is operated as a common carrier pipeline by Buckeye Development & Logistics I LLC. As a common carrier intrastate pipeline in Texas, the

3

system is subject to rate regulation under the Texas Utilities Code, as implemented by the Texas Railroad Commission, or the TRRC, and has a tariff on file with the TRRC.

Technology

OpCo has perpetual and paid-up licenses for steam cracking and process recovery technology used at its ethylene plants.

Our Agreements with Westlake

Except as otherwise indicated, the agreements described below became effective on August 4, 2014, concurrent with the closing of the IPO.

Ethylene Sales Agreement

OpCo and Westlake entered into the Ethylene Sales Agreement, which has an initial term through December 31, 2026 and automatic 12-month renewal periods until terminated at the end of the initial term or any renewal term on 12-months' notice. The Ethylene Sales Agreement requires Westlake to purchase OpCo's planned ethylene production each year, subject to certain exceptions and a maximum commitment of 3.8 billion pounds per year, less product sold by OpCo to third parties equal to approximately 5% of the annual output. If OpCo's actual production is in excess of planned ethylene production, Westlake has the option to purchase up to 95% of production in excess of planned production. Westlake's purchase price for ethylene under the Ethylene Sales Agreement includes a $0.10 per pound margin, the total costs incurred by OpCo for the feedstock and natural gas to produce each pound of ethylene (subject to a usage cap and a floor), and estimated operating costs, maintenance capital expenditures and other turnaround expenditures, less net proceeds from co-products sales. This purchase price is not designed to cover capital expenditures for expansion. Variable costs not incurred by OpCo due to a deficiency in takes are rebated to Westlake. Under specified circumstances, unrecovered costs may be carried forward for recovery in subsequent years.

On August 4, 2016, OpCo and Westlake entered into an amendment to the Ethylene Sales Agreement in order to provide that certain of the pricing components that make up the price for ethylene sold thereunder would be modified to reflect the portion of OpCo's production capacity that is used to process Westlake's purge gas instead of producing ethylene and to clarify that costs specific to the processing of Westlake's purge gas would be recovered under the Services and Secondment Agreement, and not the Ethylene Sales Agreement.

Feedstock Supply Agreement

OpCo and Westlake entered into the Feedstock Supply Agreement, which has an initial term through December 31, 2026 and automatic 12-month renewal periods until terminated at the end of the initial term or any renewal term on 12-months' notice. Under the Feedstock Supply Agreement, Westlake agrees to sell OpCo ethane and other feedstock in amounts sufficient for OpCo to produce the ethylene to be sold under the Ethylene Sales Agreement. The price at which ethane and feedstock is sold includes an indexed price for spot gas liquids at Mont Belvieu and applicable transportation, storage and other costs.

Services and Secondment Agreement

OpCo and Westlake entered into the Services and Secondment Agreement, pursuant to which OpCo will provide Westlake with various utilities and utility services and in exchange for Westlake providing OpCo with various utility services, comprehensive operating services for OpCo's units, services for the maintenance and operation of the common facilities and seconded employees to perform all services required under the agreement.

Site Lease Agreements

OpCo and Westlake entered into two 50-year site lease agreements (the "Site Leases"). Under the Site Leases, OpCo leases the real property underlying Calvert City Olefins and Lake Charles Olefins and is granted certain use and access right related thereto, for a base rental amount of $1 per year per site. Each of the Site Leases is terminable by the lessor upon the occurrence of certain events of default or by OpCo if Calvert City Olefins or Lake Charles Olefins, as applicable, is destroyed by casualty. Pursuant to the Site Leases, the lessor has the right to restore and repurchase the units for fair market value if OpCo fails to expeditiously restore Calvert City Olefins or Lake Charles Olefins, as applicable, following a casualty loss. Subject to the foregoing repurchase right, OpCo may remove its ethylene production facilities and other related improvements for up to one year after expiration or termination of the applicable Site Lease, so long as such removal can be accomplished without material damage or harm to the lessor's property or operations; provided that any assets that are not timely removed by OpCo will be deemed to have been surrendered to the lessor.

4

Omnibus Agreement

We entered into the Omnibus Agreement with Westlake and OpCo, pursuant to which we granted Westlake, among other things, a right of first refusal on any proposed transfer of (1) our equity interests in OpCo, (2) the ethylene production facilities that serve Westlake's other facilities or (3) certain other assets we may acquire from Westlake. The Omnibus Agreement also provides for reimbursement to Westlake for the provision of various administrative services and direct expenses incurred on our behalf and in connection with the operation of our business. Under the Omnibus Agreement, Westlake will indemnify us against certain environmental and other losses, and we will indemnify Westlake against certain environmental and other losses for which Westlake is not otherwise obligated to indemnify us and certain other losses and liabilities to the extent resulting from the provision of services by Westlake to us.

Exchange Agreement

OpCo and Westlake entered into an exchange agreement, which had an initial term through August 1, 2015 and is continuing year to year thereafter, unless and until terminated by either party. Under the exchange agreement, OpCo may require Westlake to deliver up to 200 million pounds of ethylene for OpCo per year from the Site Leases to an ethylene hub in Mt. Belvieu, Texas, for which OpCo would be required to pay Westlake an exchange fee of $0.006 per pound.

OpCo Partnership Agreement

We, OpCo GP and Westlake entered into an agreement of limited partnership for OpCo (the "OpCo LP Agreement"). The OpCo LP Agreement governs the ownership and management of OpCo and designates OpCo GP as the general partner of OpCo. OpCo GP generally has complete authority to manage OpCo's business and affairs. We control OpCo GP, as its sole member, subject to certain approval rights held by Westlake.

Investment Management Agreement

On August 1, 2017, the Partnership, OpCo and Westlake executed an Investment Management Agreement that authorized Westlake to invest the Partnership and OpCo’s excess cash with Westlake for a term of up to a maximum of nine months. Per the terms of the Investment Management Agreement, the Partnership earns a market return plus five basis points and Westlake provides daily availability of the invested cash to meet any liquidity needs of the Partnership or OpCo.

See "Liquidity and Capital Resources" in Item 7. "Management's Discussion and Analysis" for discussions of the Partnership's and OpCo's debt agreements with Westlake and "Interest Rate Risk" in Item 7A. "Quantitative and Qualitative Disclosures about Market Risk" for the Partnership's interest rate contract with Westlake.

Environmental

As is common in our industry, we and OpCo are subject to environmental laws and regulations related to the use, storage, handling, generation, transportation, emission, discharge, disposal and remediation of, and exposure to, hazardous and non-hazardous substances and wastes in all of the countries in which we do business. National, state or provincial and local standards regulating air, water and land quality affect substantially all of our manufacturing locations. Compliance with such laws and regulations has required and will continue to require capital expenditures and increase operating costs. Pursuant to our arrangement with Westlake, Westlake will indemnify us for liabilities that occurred or existed (in connection with compliance with such laws and regulations) prior to August 4, 2014.

It is our policy to comply with all environmental, health and safety requirements in the jurisdictions in which we and OpCo operate and to provide safe and environmentally sound workplaces for our employees. In some cases, compliance can be achieved only by incurring capital expenditures. In 2017, OpCo incurred capital expenditures of $1.3 million related to environmental compliance. We estimate that OpCo will make capital expenditures of approximately $1.2 million in 2018 and $2.2 million in 2019, respectively, related to environmental compliance.

Potential Flare Modifications. For several years, the Environmental Protection Agency ("EPA") has been conducting an enforcement initiative against petroleum refineries and petrochemical plants with respect to emissions from flares. On April 21, 2014, Westlake received a Clean Air Act Section 114 Information Request from the EPA which sought information regarding flares at the Calvert City and Lake Charles facilities. The EPA has informed Westlake that the information provided leads the EPA to believe that some of the flares are out of compliance with applicable standards. The EPA has indicated that it is seeking a consent decree that would obligate Westlake to take corrective actions relating to the alleged noncompliance. The Partnership believes the resolution of these matters may require the payment of a monetary sanction in excess of $100,000.

Risk Management Program Investigation. Region 4 of the EPA has conducted inspections and information requests to assess compliance with Risk Management Program requirements under the Clean Air Act at the Calvert City, Kentucky facility.

5

EPA Region 4 has identified concerns with the facility’s compliance under the Risk Management Program and Release Prevention regulations in connection with certain emissions release events between 2011 and 2015. Westlake has engaged in communications with EPA Region 4 to resolve these concerns. The Partnership believes the resolution of these matters may require the payment of a monetary sanction in excess of $100,000.

Kentucky Notices of Violation. In October 2017, the Enforcement Division of Kentucky Department of Environmental Protection (KDEP) indicated that it intended to proceed with enforcement on two Notices of Violation (NOVs) received by the Calvert City, Kentucky facility in December 2016 and May 2017. The NOVs allege violations of state and federal air requirements in connection with the operation of the olefins unit at the facility. Westlake has engaged in negotiations with KDEP to resolve these alleged violations. The Partnership believes the resolution of these matters may require the payment of a monetary sanction in excess of $100,000.

In addition to the matters described above, the Partnership is involved in various legal proceedings incidental to the conduct of its business. The Partnership does not believe that any of these legal proceedings will have a material adverse effect on its financial condition, results of operations or cash flows.

Also, see the discussion of our environmental matters contained in Item 1A. "Risk Factors" and Item 3"—Legal Proceedings" below.

Employees

Neither we nor OpCo has any employees. Under the Services and Secondment Agreement with Westlake, Westlake seconds employees to OpCo to allow OpCo to operate its facilities. Such seconded employees are under OpCo's control while they work on OpCo's facilities. As of December 31, 2017, 119 employees were seconded to OpCo. Of these, 21 are covered by collective bargaining agreements that expire on November 1, 2019. There have been no strikes or lockouts, and neither OpCo nor Westlake has experienced any work stoppages throughout its history. We believe that Westlake's relationship with the local union officials and bargaining committees is open and positive.

Legal Proceedings

In the ordinary conduct of our business, we and Westlake and our and Westlake's subsidiaries, including OpCo, are subject to periodic lawsuits, investigations and claims, including environmental claims and employee related matters. Although we cannot predict with certainty the ultimate resolution of lawsuits, investigations and claims asserted against us, we do not believe that any currently pending legal proceeding or proceedings to which we or Westlake or any of our or Westlake's subsidiaries, including OpCo, are a party will have a material adverse effect on our business, results of operations, cash flows or financial condition.

Competition

Due to the Ethylene Sales Agreement and integration with Westlake, OpCo does not directly compete with other ethylene producers for 95% of the planned volumes it produces. It is only on the 5% of planned ethylene volumes not sold to Westlake where OpCo competes with other regional merchant ethylene producers, including LyondellBasell Industries, N.V., Royal Dutch Shell, Williams Companies, BASF Corporation and Flint Hills Resources.

Available Information

We file annual, quarterly and current reports and other documents with the SEC under the Securities Exchange Act of 1934 (the "Exchange Act"). You may read and copy any materials we file with the SEC at the SEC's Public Reference Room at 100 F Street, NE, Washington, DC 20549. You may obtain information on the operations of the Public Reference Room by calling the SEC at (800) SEC-0330. In addition, the SEC maintains a website at www.sec.gov that contains reports and other information regarding issuers that file electronically with the SEC.

We also make available free of charge our Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K and any amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Exchange Act, simultaneously with or as soon as reasonably practicable after filing such materials with, or furnishing such materials to, the SEC, and on or through our website, www.wlkpartners.com. The information on our website, or information about us on any other website, is not incorporated by reference into this report.

Item 1A. Risk Factors

Limited partner interests are inherently different from the capital stock of a corporation, although many of the business risks to which we are subject are similar to those that would be faced by a corporation engaged in a similar business. Security

6

holders and potential investors should carefully consider the following risk factors together with all of the other information included in this report. If any of the following risks were actually to occur, our business, financial condition, results of operations or cash flows could be materially adversely affected.

Risks Inherent in Our Business

We are substantially dependent on Westlake for our cash flows. If Westlake does not pay us under the terms of the Ethylene Sales Agreement or if our assets fail to perform as intended, we may not have sufficient cash from operations following the establishment of cash reserves and payment of costs and expenses, including cost reimbursements to our general partner and its affiliates, to enable us to pay the minimum quarterly distribution to our unitholders.

Currently, all of our cash flow is generated from cash distributions from OpCo, and a substantial majority of OpCo's cash flow is generated from payments by Westlake under the Ethylene Sales Agreement. Westlake's obligations to purchase ethylene under the Ethylene Sales Agreement may be temporarily suspended to the extent OpCo is unable to perform its obligations caused by any of certain events outside the reasonable control of OpCo. Such events include, for example, acts of God or calamities which affect the operation of OpCo's facilities; certain labor difficulties (whether or not the demands of the employees are within the power of OpCo to concede); and governmental orders or laws. In addition, Westlake is not obligated to purchase ethylene with respect to any period during which OpCo's facilities are not operating due to scheduled or unscheduled maintenance or turnarounds (which occur approximately every five years) other than under certain circumstances relating to the occurrence of force majeure. We expect that each of OpCo's facilities will have a turnaround once every five years and will not operate for typically between 25 and 45 days during each turnaround by itself. However, the duration of a turnaround by itself may be longer than expected or may cost more than originally estimated. Furthermore, expansions may also coincide with turnarounds, which may complicate and delay the completion of such turnarounds. A suspension of Westlake's obligations under the Ethylene Sales Agreement, including during periods where OpCo's facilities are not operating due to scheduled or unscheduled maintenance or turnarounds, would reduce OpCo's revenues and cash flows, and could materially adversely affect our ability to make distributions to our unitholders.

Westlake may be unable to generate enough cash flow from operations to meet its minimum obligations under the Ethylene Sales Agreement if its business is adversely impacted by competition, operational problems, general adverse economic conditions or the inability to obtain feedstock. For example, sustained lower prices of crude oil, such as the prices experienced since the third quarter of 2014 and continuing through 2017 (as of December 31, 2017, approximately 44% lower than their 2014 peak levels) may lead to lower margins for Westlake in the United States. If Westlake were unable to meet its minimum payment obligations to OpCo as a result of any one or more of these factors, our ability to make distributions to our unitholders would be reduced or eliminated. The level of payments made by Westlake will depend upon its ability to pay its minimum obligations under the Ethylene Sales Agreement and its ability and election to increase volumes above the minimums specified in the Ethylene Sales Agreement, which in turn are dependent upon, among other things, the level of production at Westlake's other facilities. If Westlake is unable to generate sufficient cash flow from its operations to meet its obligations, or otherwise defaults on its obligations, under the Ethylene Sales Agreement, OpCo will not have sufficient available cash to distribute to us to enable us to pay the minimum quarterly distribution, which will fluctuate from quarter to quarter based on the following factors, some of which are beyond our control:

• | severe financial hardship or bankruptcy of Westlake or one of our other customers, or the occurrence of other events affecting our ability to collect payments from Westlake or our other customers, including any of our customers' default; |

• | volatility and cyclical downturns in the chemicals industry and other industries which materially and adversely impact Westlake and our other customers; |

• | Westlake's inability to perform, or any other default on its obligations, under the Ethylene Sales Agreement; |

• | the age of, and changes in the reliability, efficiency and capacity of the various equipment and operating facilities used in OpCo's operations, and in the operations of Westlake and our other customers, business partners and/or suppliers; |

• | the cost of environmental remediation at OpCo's facilities not covered by Westlake or third parties; |

• | changes in the expected operating levels of OpCo's assets; |

• | OpCo's ability to meet minimum volume requirements, yield standards and ethylene quality requirements in the Ethylene Sales Agreement; |

• | OpCo's ability to renew the Ethylene Sales Agreement or to enter into new, long-term agreements for the sale of ethylene under terms similar or more favorable; |

• | changes in the marketplace that may affect supply and demand for ethane or ethylene, including decreased availability of ethane (which may result from greater restrictions on hydraulic fracturing, any reduction in hydraulic fracturing due |

7

to low crude oil prices or exports of natural gas liquids from the United States, for example), increased production of ethylene or export of ethane or ethylene from the United States;

• | changes in overall levels of production, production capacity, pricing and/or margins for ethylene; |

• | OpCo's ability to secure adequate supplies of ethane, other feedstocks and natural gas from Westlake or third parties; |

• | the need to use higher priced or less attractive feedstock due to the unavailability of ethane; |

• | the effects of pipeline, railroad, barge, truck and other transportation performance and costs, including any transportation disruptions; |

• | the availability and cost of labor; |

• | risks related to employees and workplace safety; |

• | the effects of adverse events relating to the operation of OpCo's facilities and to the transportation and storage of hazardous materials (including equipment malfunction, explosions, fires, spills and the effects of severe weather conditions); |

• | changes in product specifications for the ethylene that we produce; |

• | changes in insurance markets and the level, types and costs of coverage available, and the financial ability of our insurers to meet their obligations; |

• | changes in, or new, statutes, regulations or governmental policies by federal, state and local authorities with respect to protection of the environment; |

• | changes in accounting rules and/or tax laws or their interpretations; |

• | nonperformance or force majeure by, or disputes with or changes in contract terms with, Westlake, our other major customers, suppliers, dealers, distributors or other business partners; and |

• | changes in, or new, statutes, regulations, governmental policies and taxes, or their interpretations. |

In addition, the actual amount of cash we will have available for distribution will depend on other factors, including:

• | the amount of cash we or OpCo are able to generate from sales of ethylene, and associated co-products, to third parties, which will be impacted by changes in prices for ethane (or other feedstocks), natural gas, ethylene and co-products and sustained lower prices of crude oil, such as those experienced since the third quarter of 2014 and continuing through 2017, and could be less than the margin we earn from ethylene sales to Westlake; |

• | the level of capital expenditures we or OpCo make; |

• | the cost of acquisitions; |

• | construction costs; |

• | fluctuations in our or OpCo's working capital needs; |

• | our or OpCo's ability to borrow funds (including under our or OpCo's revolving credit facilities) and access capital markets; |

• | our or OpCo's debt service requirements and other liabilities; |

• | restrictions contained in our or OpCo's existing or future debt agreements; and |

• | the amount of cash reserves established by our general partner. |

We will require a significant amount of cash to service our debt and OpCo's debt, including borrowings under our and OpCo's credit facilities with Westlake. Our ability to make payments on and refinance this debt will depend on our ability to generate cash in the future, which is subject to the same factors described above in connection with our ability to pay quarterly distributions to unitholders. Cash that is used to service debt will be unavailable for distributions to our unitholders.

OpCo is subject to the credit risk of Westlake on a substantial majority of its revenues, and Westlake's leverage and creditworthiness could adversely affect our ability to make distributions to our unitholders.

Our ability to make distributions to unitholders is substantially dependent on Westlake's ability to meet its minimum contractual obligations under the Ethylene Sales Agreement. If Westlake defaults on its obligations, our ability to make distributions to our unitholders would be reduced or eliminated. Westlake has not pledged any assets to us as security for the performance of its obligations.

8

Westlake has not agreed with us to limit its ability to incur indebtedness, pledge or sell assets or make investments, and we have no control over the amount of indebtedness Westlake incurs, the assets it pledges or sells or the investments it makes.

OpCo is a restricted subsidiary under Westlake's credit facility and the indentures governing its senior notes. Restrictions in the indentures could limit OpCo's ability to make distributions to us.

All of our cash is currently generated from cash distributions from OpCo. Westlake's credit facility and the indentures governing its senior notes impose significant operating and financial restrictions on OpCo. These restrictions limit OpCo's ability to:

• | make investments and other restricted payments; |

• | incur additional indebtedness or issue preferred stock; |

• | create liens; |

• | sell all or substantially all of its assets or consolidate or merge with or into other companies; and |

• | engage in transactions with affiliates. |

In addition, the indentures governing Westlake's senior notes prevent OpCo from making distributions to us if any default or event of default (as defined in the indentures) exists.

These limitations are subject to a number of important qualifications and exceptions. However, the effectiveness of many of these restrictions in the indentures governing Westlake's senior notes is currently suspended under the indentures because the senior notes are currently rated investment grade by at least two nationally recognized credit rating agencies.

These covenants may adversely affect OpCo's ability to finance future business opportunities. A breach of any of these covenants could result in a default in respect of the related debt. If a default occurred, the relevant lenders could elect to declare the debt, together with accrued interest and other fees, to be immediately due and payable and proceed against any collateral securing that debt, including OpCo and its assets. In addition, any acceleration of debt under Westlake's credit facility will constitute a default under some of Westlake's other debt, including the indentures governing its senior notes

Substantially all of OpCo's sales are generated at three facilities located at two sites. Any adverse developments at any of these facilities or sites could have a material adverse effect on our results of operations and therefore our ability to distribute cash to unitholders.

OpCo's operations are subject to significant hazards and risks inherent in ethylene production operations. These hazards and risks include, but are not limited to, equipment malfunction, explosions, fires and the effects of severe weather conditions, any of which could result in production and transportation difficulties and disruptions, pollution, personal injury or wrongful death claims and other damage to our properties and the property of others. There is also risk of mechanical failure of OpCo's facilities both in the normal course of operations and following unforeseen events. Any adverse developments at any of OpCo's facilities could have a material adverse effect on our results of operations and therefore our ability to distribute cash to unitholders.

Because substantially all of OpCo's sales are generated at three facilities located at two sites, any such events at any facility or site could significantly disrupt OpCo's ethylene production and its ability to supply ethylene to its customers. Any sustained disruption in its ability to meet its supply obligations under the Ethylene Sales Agreement could have a material adverse effect on our results of operations and therefore our ability to distribute cash to unitholders.

The ethylene sales price charged under the Ethylene Sales Agreement is designed to permit OpCo to cover the substantial majority of its operating costs, but not our public partnership and other OpCo costs, which will reduce our net operating profit.

The purchase price under the Ethylene Sales Agreement is based on OpCo's actual ethane, other feedstock and natural gas costs and an annual estimate of other operating costs and maintenance capital expenditures and other turnaround expenditures. The price is designed to permit OpCo to recover the portion of its costs of feedstocks and other costs to operate the ethylene production facilities associated with the percentage of its production capacity purchased by Westlake and generate a fixed margin per pound of ethylene purchased by Westlake. The price is not designed to allow OpCo to recover any capital expenditures related to expansion (such as our plans to upgrade and expand the capacity of Petro 1 and our facility in Calvert City), or operational efficiency. The ethylene sales price also does not increase to cover our public partnership costs. Both of these costs reduce our net operating profit.

9

The fee structure of the Ethylene Sales Agreement may limit OpCo's ability to take advantage of favorable market developments in the future.

The Ethylene Sales Agreement sets a $0.10 per pound margin for a substantial majority of OpCo's ethylene production, limiting OpCo's ability to take advantage of potential decreased ethane and other feedstock prices, potential increased ethylene prices or other favorable market developments. Under these circumstances, OpCo may not be in a position to enable its partners, including us, to benefit from favorable market developments (including any potential ethylene price increase in the future) through increased distributions. In addition, under these circumstances, OpCo may be disadvantaged relative to those of its competitors that are in a better position to take advantage of favorable market developments.

If OpCo is unable to renew or extend the Ethylene Sales Agreement beyond the initial 12-year term or the other agreements with Westlake upon expiration of these agreements, our ability to make distributions in the future could be materially adversely affected and the value of our units could decline.

Westlake's obligations under the Ethylene Sales Agreement, the Feedstock Supply Agreement and the related services and secondment agreement will become terminable by either party commencing December 31, 2026. If OpCo were unable to reach agreement with Westlake on an extension or replacement of these agreements, then our ability to make distributions on our common units could be materially adversely affected and the value of our common units could decline.

OpCo has the right to use the real property underlying Lake Charles Olefins and Calvert City Olefins pursuant to two, 50-year site lease agreements with Westlake. If OpCo is not able to renew the site lease agreements or if the site lease agreements are terminated by Westlake, OpCo may have to relocate Lake Charles Olefins and Calvert City Olefins, abandon the assets or sell the assets to Westlake.

Westlake has (1) leased to OpCo the real property underlying Lake Charles Olefins and Calvert City Olefins and (2) granted OpCo rights to access and use certain other portions of Westlake's facilities that are necessary to operate OpCo's units at such facilities. The site lease agreements each have a term of 50 years and may be renewed if agreed to by the parties. If an event of default with respect to bankruptcy of OpCo occurs, if Westlake terminates the Ethylene Sales Agreement in accordance with its provisions either for cause or due to a force majeure event, or if OpCo ceases to operate Lake Charles Olefins or Calvert City Olefins for six consecutive months (other than due to force majeure or construction following a casualty loss), Westlake may terminate the applicable site lease following notice and expiration of a cure period to remedy the default. In addition, if OpCo fails to act in good faith to expeditiously restore Lake Charles Olefins or Calvert City Olefins following a casualty loss, Westlake has the ability to terminate the applicable site lease agreement, to restore Lake Charles Olefins or Calvert City Olefins, as the case may be, and to purchase such ethylene production facilities at fair market value. If OpCo is unable to renew the site lease agreements or if Westlake terminates one or both of the site lease agreements, OpCo may have to relocate Lake Charles Olefins and Calvert City Olefins, abandon the assets or sell the assets to Westlake, the result of which may have a material adverse effect on our business, results of operations and financial condition.

OpCo depends upon Westlake for numerous services and for its labor force.

Pursuant to a services and secondment agreement, Westlake is obligated to provide OpCo operating services, utility access services and other key site services. Westlake provides the services of certain of its employees, who act as OpCo's agents in operating and maintaining OpCo's ethylene production facilities. If this agreement is terminated or if Westlake or its affiliates fail to satisfactorily provide these services or employees, OpCo would be required to hire labor, provide these services internally or find a third-party provider of these services. Any services or labor OpCo chooses to provide internally may not be as cost effective as those that Westlake or its affiliates provide, particularly in light of OpCo's lack of experience as an independent organization. If OpCo is required to obtain these services or labor from a third party, it may be unable to do so in a timely, efficient and cost-effective manner, the services or labor it receives may be inferior to or more costly than those that Westlake is currently providing, or such services and labor may be unavailable. Moreover, given the integration of OpCo's ethylene production facilities and Westlake's Lake Charles and Calvert City facilities, it may not be practical for us or for a third party to provide site services or labor for OpCo's ethylene production facilities separately.

OpCo's ability to receive greater cash flows from increased production may be limited by the Ethylene Sales Agreement.

OpCo's ability to increase throughput volumes through its assets is constrained by the capacity limitations of those assets, which are currently operating at close to full capacity. OpCo's ability to increase its cash flow by selling ethylene to third parties may be limited by the Ethylene Sales Agreement. OpCo's ability to sell ethylene to third parties is limited to available excess capacity, since Westlake has the right to purchase the substantial majority of production from OpCo's facilities through its minimum purchase commitment and option to purchase additional ethylene under the Ethylene Sales Agreement. The Ethylene Sales Agreement provisions may prohibit OpCo from competing effectively for third party business for this excess

10

production given the limited volumes available for sale. For example, so long as Westlake is not in default under the Ethylene Sales Agreement, Westlake has the right to purchase 95% of OpCo's production in excess of planned capacity.

The amount of cash we have available for distribution to holders of our units depends primarily on our cash flow and not solely on profitability, which may prevent us from making cash distributions during periods when we record net income.

The amount of cash we have available for distribution depends primarily upon our cash flow, including cash flow from reserves and working capital or borrowings (including any under our credit facilities,) and not solely on profitability, which will be affected by non-cash items. As a result, we may pay cash distributions during periods when we record net losses for financial accounting purposes and may be unable to pay cash distributions during periods when we record net income. We may be unable to access our revolving credit facilities when we do not have sufficient cash flows to pay cash distributions.

If we are unable to make acquisitions from Westlake or third parties on economically acceptable terms, our future growth would be limited, and any acquisitions we make may reduce, rather than increase, our cash generated from operations on a per unit basis.

Our strategy to grow our business and increase distributions to unitholders is dependent on our ability to make acquisitions that result in an increase in our cash distributions per unit. If we are unable to make acquisitions of additional interests in OpCo from Westlake on acceptable terms or we are unable to obtain financing for these acquisitions, our future growth and ability to increase distributions will be limited. In addition, we may be unable to make acquisitions from third parties as an alternative avenue to growth. Furthermore, even if we do consummate acquisitions that we believe will be accretive, they may in fact result in a decrease in our cash distributions per unit. Any acquisition involves potential risks, some of which are beyond our control, including, among other things:

• | mistaken assumptions about revenues and costs, including synergies; |

• | the inability to successfully integrate the businesses we acquire; |

• | the inability to hire, train or retain qualified personnel to manage and operate our business and newly acquired assets; |

• | the assumption of unknown liabilities; |

• | limitations on rights to indemnity from the seller; |

• | mistaken assumptions about the overall costs of equity or debt; |

• | the diversion of management's attention from other business concerns; |

• | unforeseen difficulties in connection with operating in new product areas or new geographic areas; and |

• | customer or key employee losses at the acquired businesses. |

If we consummate any future acquisitions, our capitalization and results of operations may change significantly, and unitholders will not have the opportunity to evaluate the economic, financial and other relevant information that we will consider in determining the application of our funds and other resources.

Many of our assets have been in service for many years and require significant expenditures to maintain them. As a result, our maintenance or repair costs may increase in the future. In addition, while we intend to establish cash reserves in order to cover turnaround expenditures, the amounts we reserve may not be sufficient to fully cover such expenditures.

Many of the assets we use to produce ethylene are generally long-lived assets. As a result, some of those assets have been in service for many decades. The age and condition of these assets could result in increased maintenance or repair expenditures. In addition, while we intend to establish cash reserves in order to cover our turnaround expenditures, the amounts we reserve may be insufficient to fully cover such expenditures. Any significant and unexpected increase in these expenditures could adversely affect our results of operations, financial position or cash flows, as well as our ability to pay cash distributions.

Regulations concerning the transportation of hazardous chemicals and the security of chemical manufacturing facilities could result in higher operating costs.

Chemical manufacturing facilities may be at greater risk of terrorist attacks than other potential targets in the U.S. As a result, the chemicals industry responded to the issues surrounding the terrorist attacks of September 11, 2001 by starting initiatives relating to the security of chemicals industry facilities and the transportation of hazardous chemicals in the U.S. Simultaneously, local, state and federal governments began a regulatory process that led to new regulations impacting the security of chemical plant locations and the transportation of hazardous chemicals. Our business or our customers' businesses could be adversely affected because of the cost of complying with these regulations.

11

Our production facilities process volatile and hazardous materials that subject us to operating risks that could adversely affect our operating results.

Our operations are subject to the usual hazards associated with commodity chemical and plastics manufacturing and the related use, storage, transportation and disposal of feedstocks, products and wastes, including:

• | pipeline leaks and ruptures; |

• | explosions; |

• | fires; |

• | severe weather and natural disasters; |

• | mechanical failure; |

• | unscheduled downtime; |

• | labor difficulties; |

• | transportation interruptions; |

• | chemical spills; |

• | discharges or releases of toxic or hazardous substances or gases; |

• | storage tank leaks; |

• | other environmental risks; and |

• | terrorist attacks. |

All these hazards can cause personal injury and loss of life, catastrophic damage to or destruction of property and equipment and environmental damage, and may result in a suspension of operations and the imposition of civil or criminal penalties. We could become subject to environmental claims brought by governmental entities or third parties. A loss or shutdown of operations over an extended period at any one of our three major operating facilities would have a material adverse effect on us. We maintain property, business interruption and casualty insurance that we believe is in accordance with customary industry practices, but we cannot be fully insured against all potential hazards incident to our business, including losses resulting from war risks or terrorist acts. As a result of market conditions, premiums and deductibles for certain insurance policies can increase substantially and, in some instances, certain insurance may become unavailable or available only for reduced amounts of coverage. If we were to incur a significant liability for which we were not fully insured, it could have a material adverse effect on our financial position.

Our operations and assets are subject to extensive environmental, health and safety laws and regulations.

We use hazardous substances and generate hazardous wastes and emissions in our manufacturing operations. Our industry is highly regulated and monitored by various environmental regulatory authorities such as the Environmental Protection Agency (the "EPA"). As such, we are subject to extensive federal, state and local laws and regulations pertaining to pollution and protection of the environment, health and safety, which govern, among other things, emissions to the air, discharges onto land or waters, the maintenance of safe conditions in the workplace, the remediation of contaminated sites, and the generation, handling, storage, transportation, treatment and disposal of waste materials. Some of these laws and regulations are subject to varying and conflicting interpretations. Many of these laws and regulations provide for substantial fines and potential criminal sanctions for violations and require the installation of costly pollution control equipment or operational changes to limit pollution emissions or reduce the likelihood or impact of hazardous substance releases, whether permitted or not. For example, our petrochemical facilities may require improvements to comply with certain changes in process safety management requirements.

Our operations produce greenhouse gas ("GHG") emissions, which have been the subject of increased scrutiny and regulation. The EPA has adopted rules requiring the reporting of GHG emissions from specified large GHG emission sources on an annual basis including our facilities in Lake Charles and Calvert City. Various jurisdictions have considered or adopted laws and regulations on GHG emissions, with the general aim of reducing such emissions. The EPA currently requires certain industrial facilities to report their GHG emissions, and to obtain permits with stringent control requirements before constructing or modifying new facilities with significant criteria pollutant and GHG emissions. As our chemical processing results in GHG emissions, these and other GHG laws and regulations could affect our costs of doing business.

We also may face liability for alleged personal injury or property damage due to exposure to chemicals or other hazardous substances at our facilities or to chemicals that we otherwise manufacture, handle or own. Although these types of claims have

12

not historically had a material impact on our operations, a significant increase in the success of these types of claims could have a material adverse effect on our business, financial condition, operating results or cash flow.

Environmental laws may have a significant effect on the nature and scope of, and responsibility for, cleanup of contamination at our current and former operating facilities, the costs of transportation and storage of raw materials and finished products, the costs of reducing emissions and the costs of the storage and disposal of wastewater. The U.S. Comprehensive Environmental Response, Compensation, and Liability Act ("CERCLA") and similar state laws impose joint and several liability for the costs of remedial investigations and actions on the entities that are deemed responsible for a release of hazardous substances into the environment, including entities that have generated hazardous substances or arranged for their transportation or disposal, as well as the past and present owners and operators of disposal sites. All such potentially responsible parties (or any one of them, including us) may be required to bear all of such costs regardless of fault, legality of the original disposal or ownership of the disposal site. In addition, CERCLA and similar state laws could impose liability for damages to natural resources caused by contamination.

Although we seek to take preventive action, our operations are inherently subject to accidental spills, discharges or other releases of hazardous substances that may make us liable to governmental entities or private parties. This may involve contamination associated with our current and former facilities, facilities to which we sent wastes or by-products for treatment or disposal and other contamination. Accidental discharges may occur in the future, future action may be taken in connection with past discharges, governmental agencies may assess damages or penalties against us in connection with any past or future contamination, or third parties may assert claims against us for damages allegedly arising out of any past or future contamination. In addition, we may be liable for existing contamination related to certain of our facilities for which, in some cases, we believe third parties are liable in the event such third parties fail to perform their obligations.

Failure to adequately protect critical data and technology systems could materially affect our operations.

Information technology system failures, network disruptions and breaches of data security could disrupt our operations by causing delays or cancellation of customer orders, impede the manufacture or shipment of products or cause standard business processes to become ineffective, resulting in the unintentional disclosure of information or damage to our reputation. While Westlake, which manages our security protocol under the omnibus agreement, has taken steps to address these concerns by implementing network security and internal control measures, there can be no assurance that a system failure, network disruption or data security breach will not have a material adverse effect on our business, financial condition, operating results or cash flow.

A terrorist attack or armed conflict could harm our business.

Terrorist activities, anti-terrorist efforts and other armed conflicts involving the U.S. or other jurisdictions could adversely affect the U.S. and global economies and could prevent us from meeting financial and other obligations. We could experience loss of business, delays or defaults in payments from customers or disruptions of fuel supplies and markets if North American and global utilities are direct targets or indirect casualties of an act of terror or war. Terrorist activities and the threat of potential terrorist activities and any resulting economic downturn could adversely affect our results of operations, impair our ability to raise capital or otherwise adversely impact our ability to realize certain business strategies.

Risks Relating to Our Partnership Structure

Westlake owns and controls our general partner, which has sole responsibility for conducting our business and managing our operations. Our general partner and its affiliates, including Westlake, may have conflicts of interest with us and have limited duties, and they may favor their own interests to our detriment and that of our unitholders.

Westlake owns and controls our general partner and appoints all of the directors of our general partner. Although our general partner has a duty to manage us in a manner that it believes is not adverse to our interests, the executive officers and directors of our general partner have a fiduciary duty to manage our general partner in a manner beneficial to Westlake. Therefore, conflicts of interest may arise between Westlake or any of its affiliates, including our general partner, on the one hand, and us or any of our unitholders, on the other hand. In resolving these conflicts of interest, our general partner may favor its own interests and the interests of its affiliates over the interests of our common unitholders. These conflicts include the following situations, among others:

• | our general partner is allowed to take into account the interests of parties other than us, such as Westlake, in exercising certain rights under our partnership agreement; |

• | neither our partnership agreement nor any other agreement requires Westlake to pursue a business strategy that favors us; |

13

• | our partnership agreement replaces the fiduciary duties that would otherwise be owed by our general partner with contractual standards governing its duties, limits our general partner's liabilities and restricts the remedies available to our unitholders for actions that, without such limitations, might constitute breaches of fiduciary duty; |

• | except in limited circumstances, our general partner has the power and authority to conduct our business without unitholder approval; |

• | our general partner determines the amount and timing of asset purchases and sales, borrowings, issuances of additional partnership securities and the level of reserves, each of which can affect the amount of cash that is distributed to our unitholders; |

• | our general partner determines the amount and timing of any cash expenditure and whether an expenditure is classified as a maintenance capital expenditure, which reduces operating surplus, or an expansion capital expenditure, which does not reduce operating surplus. This determination can affect the amount of cash from operating surplus that is distributed to our unitholders which, in turn, may affect the ability of the subordinated units to convert; |

• | our general partner may cause us to borrow funds in order to permit the payment of cash distributions, even if the purpose or effect of the borrowing is to make a distribution on the subordinated units, to make incentive distributions or to accelerate the expiration of the subordination period, or may cause us not to borrow funds to pay cash distributions when we do not otherwise have the funds pay such cash distributions; |

• | our partnership agreement permits us to distribute up to $28.0 million as operating surplus, even if it is generated from asset sales, non-working capital borrowings or other sources that would otherwise constitute capital surplus. This cash may be used to fund distributions on our subordinated units or the incentive distribution rights; |

• | our general partner determines which costs incurred by it and its affiliates are reimbursable by us; |

• | our partnership agreement does not restrict our general partner from causing us to pay it or its affiliates for any services rendered to us or entering into additional contractual arrangements with its affiliates on our behalf; |

• | our general partner intends to limit its liability regarding our contractual and other obligations; |

• | our general partner may exercise its right to call and purchase common units if it and its affiliates own more than 80% of the common units; |

• | our general partner controls the enforcement of obligations that it and its affiliates owe to us; |

• | our general partner decides whether to retain separate counsel, accountants or others to perform services for us; and |

• | our general partner may elect to cause us to issue common units to it in connection with a resetting of the target distribution levels related to Westlake's incentive distribution rights without the approval of the conflicts committee of the board of directors or the unitholders. This election may result in lower distributions to the common unitholders in certain situations. |

In addition, we may compete directly with Westlake and entities in which it has an interest for acquisition opportunities and potentially will compete with these entities for new business or extensions of the existing services provided by us. Please read "Westlake and other affiliates of our general partner may compete with us."

The board of directors may modify or revoke our cash distribution policy at any time at its discretion. Our partnership agreement does not require us to pay any distributions at all.

The board of directors adopted a cash distribution policy pursuant to which we intend to distribute quarterly at least $0.2750 per unit on all of our units to the extent we have sufficient cash after the establishment of cash reserves and the payment of our expenses, including payments to our general partner and its affiliates. However, the board may change such policy at any time at its discretion and could elect not to pay distributions for one or more quarters.

In addition, our partnership agreement does not require us to pay any distributions at all. Accordingly, investors are cautioned not to place undue reliance on the permanence of such a policy in making an investment decision. Any modification or revocation of our cash distribution policy could substantially reduce or eliminate the amount we distribute to our unitholders. The amount of distributions we make, if any, and the decision to make any distribution at all will be determined by the board of directors, whose interests may differ from those of our common unitholders. Our general partner has limited duties to our unitholders, which may permit it to favor its own interests or the interests of Westlake to the detriment of our common unitholders.

14

Our general partner intends to limit its liability regarding our obligations.

Our general partner intends to limit its liability under contractual arrangements between us and third parties so that the counterparties to such arrangements have recourse only against our assets, and not against our general partner or its assets. Our general partner may therefore cause us to incur indebtedness or other obligations that are nonrecourse to our general partner. Our partnership agreement provides that any action taken by our general partner to limit its liability is not a breach of our general partner's duties, even if we could have obtained more favorable terms without the limitation on liability.

We expect to distribute a significant portion of our available cash to our partners, which could limit our ability to grow and make acquisitions.

We plan to distribute most of our available cash, which may cause our growth to proceed at a slower pace than that of businesses that reinvest their cash to expand ongoing operations. To the extent we issue additional units in connection with any acquisitions or expansion capital expenditures, the payment of distributions on those additional units may increase the risk that we will be unable to maintain or increase our per unit distribution level. There are no limitations in our partnership agreement on our ability to issue additional units, including units ranking senior to the common units. The incurrence of additional commercial borrowings or other debt to finance our growth strategy would result in increased interest expense, which, in turn, may impact the cash that we have available to distribute to our unitholders.

Our partnership agreement replaces our general partner's fiduciary duties to holders of our units.

Our partnership agreement contains provisions that eliminate and replace the fiduciary standards to which our general partner would otherwise be held by state fiduciary duty law. For example, our partnership agreement permits our general partner to make a number of decisions in its individual capacity, as opposed to in its capacity as our general partner, or otherwise free of fiduciary duties to us and our unitholders. This entitles our general partner to consider only the interests and factors that it desires and relieves it of any duty or obligation to give any consideration to any interest of, or factors affecting, us, our affiliates or our limited partners. Examples of decisions that our general partner may make in its individual capacity include:

• | how to allocate business opportunities among us and its affiliates; |

• | whether to exercise its call right; |

• | how to exercise its voting rights with respect to the units it owns; |

• | whether to exercise its registration rights; |

• | whether to elect to reset target distribution levels; and |

• | whether or not to consent to any merger or consolidation of the partnership or amendment to the partnership agreement. |

By purchasing a common unit, a unitholder is treated as having consented to the provisions in the partnership agreement, including the provisions discussed above.