Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-K

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended March 31, 2016

OR

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

COMMISSION FILE NO.: 001-36557

ADVANCED DRAINAGE SYSTEMS, INC.

(Exact name of registrant as specified in its charter)

| Delaware | 51-0105665 | |

| (State or other jurisdiction of incorporation or organization) |

(I.R.S. Employer Identification Number) |

4640 Trueman Boulevard, Hilliard, Ohio 43026

(Address of principal executive offices and zip code)

(614) 658-0050

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act: Common Stock, $0.01 par value per share

| Title of Each Class |

Name of Each Exchange On Which Registered | |

| Common Stock, $0.01 par value per share | New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ¨ No x

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. x

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer,” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one)

| Large Accelerated Filer | x | Accelerated Filer | ¨ | |||

| Non-Accelerated Filer | ¨ | Smaller Reporting Company | ¨ |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No x

The aggregate market value of the shares of common stock held by non-affiliates of the registrant (treating all executive officers and directors of the registrant, for this purpose, as affiliates of the registrant) was $997 million as of September 30, 2015, the last business day of the registrant’s most recently completed second fiscal quarter, based on the reported closing price of the shares of common stock as reported on the New York Stock Exchange on September 30, 2015.

As of August 31, 2016, the registrant had 54,887,305 shares of common stock outstanding. The shares of common stock trade on the New York Stock Exchange under the ticker symbol “WMS”. In addition, as of August 31, 2016, 55,348 shares of unvested restricted common stock were outstanding and 24,600,953 shares of ESOP preferred stock, convertible into 18,923,053 shares of common stock, were outstanding. As of August 31, 2016, 73,865,706 shares of common stock were outstanding, inclusive of outstanding shares of unvested restricted common stock and on an as-converted basis with respect to the outstanding shares of ESOP preferred stock.

DOCUMENTS INCORPORATED BY REFERENCE

None.

Table of Contents

i

Table of Contents

CAUTIONARY STATEMENT ABOUT FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K includes forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. Some of the forward-looking statements can be identified by the use of terms such as “believes,” “expects,” “may,” “will,” “should,” “could,” “seeks,” “intends,” “plans,” “estimates,” “anticipates” or other comparable terms. These forward-looking statements include all matters that are not related to present facts or current conditions or that are not historical facts. They appear in a number of places throughout this Annual Report on Form 10-K and include statements regarding our intentions, beliefs or current expectations concerning, among other things, our consolidated results of operations, financial condition, liquidity, prospects, growth strategies, and the industries in which we operate and include, without limitation, statements relating to our future performance.

Forward-looking statements are subject to known and unknown risks and uncertainties, many of which are beyond our control. We caution you that forward-looking statements are not guarantees of future performance and that our actual consolidated results of operations, financial condition, liquidity, and industry development may differ materially from those made in or suggested by the forward-looking statements contained in this Annual Report on Form 10-K. In addition, even if our actual consolidated results of operations, financial condition, liquidity, and industry development are consistent with the forward-looking statements contained in this Annual Report on Form 10-K, those results or developments may not be indicative of results or developments in subsequent periods. A number of important factors could cause actual results to differ materially from those contained in or implied by the forward-looking statements, including those reflected in forward-looking statements relating to our operations and business, the risks and uncertainties discussed in this Annual Report on Form 10-K (including under the heading “Item 1A. Risk Factors”) and those described from time to time in our other filings with the SEC. Factors that could cause actual results to differ from those reflected in forward-looking statements relating to our operations and business include, among other things:

| • | our ability to remediate the material weaknesses in our internal controls over financial reporting described in “Item 9A. Controls and Procedures” of this Annual Report, and discovering further weaknesses of which we are not currently aware or which have not been detected; |

| • | the risk that additional information may arise that would require the Company to make additional adjustments or revisions or to restate further the financial statements and other financial data for certain prior periods and any future periods; |

| • | the effect of any claims, litigation, investigations or proceedings resulting from the restatement of our previously issued financial statements, or the matters related to such restatement, including those described below under “Item 3. Legal Proceedings” of this Annual Report; |

| • | our ability to regain and/or maintain compliance with the New York Stock Exchange’s (“NYSE”) continued listing requirements under the timely filing criteria outlined in Section 802.01E of the NYSE Listed Company Manual; |

| • | any further delay in the filing of any periodic reports with the SEC; |

| • | fluctuations in the price and availability of resins and other raw materials and our ability to pass any increased costs of raw materials on to our customers in a timely manner; |

| • | volatility in general business and economic conditions in the markets in which we operate, including without limitation factors relating to availability of credit, interest rates, fluctuations in capital and business and consumer confidence; |

| • | cyclicality and seasonality of the non-residential and residential construction markets and infrastructure spending; |

| • | the risks of increasing competition in our existing and future markets, including competition from both manufacturers of high performance thermoplastic corrugated pipe and manufacturers of products using alternative materials; |

1

Table of Contents

| • | our ability to continue to convert current demand for concrete, steel and polyvinyl chloride (“PVC”) pipe products into demand for our high performance thermoplastic corrugated pipe and Allied Products; |

| • | the effect of weather or seasonality; |

| • | the loss of any of our significant customers; |

| • | the risks of doing business internationally; |

| • | the risks of conducting a portion of our operations through joint ventures; |

| • | our ability to expand into new geographic or product markets; |

| • | our ability to achieve the acquisition component of our growth strategy; |

| • | the risk associated with manufacturing processes; |

| • | our ability to manage our assets; |

| • | the risks associated with our product warranties; |

| • | our ability to manage our supply purchasing and customer credit policies; |

| • | the risks associated with our self-insured programs; |

| • | our ability to control labor costs and to attract, train and retain highly-qualified employees and key personnel; |

| • | our ability to protect our intellectual property rights; |

| • | changes in laws and regulations, including environmental laws and regulations; |

| • | our ability to project product mix; |

| • | the risks associated with our current levels of indebtedness; |

| • | our ability to meet future capital requirements and fund our liquidity needs; and |

| • | other risks and uncertainties, including those listed under “Item 1A. Risk Factors.” |

You should read this Annual Report on Form 10-K completely and with the understanding that actual future results may be materially different from expectations. All forward-looking statements made in this Annual Report on Form 10-K are qualified by these cautionary statements. All forward-looking statements are made only as of the date of this Annual Report on Form 10-K, and we do not undertake any obligation, other than as may be required by law, to update or revise any forward-looking statements to reflect future events or developments. Comparisons of results for current and any prior periods are not intended to express any future trends, or indications of future performance, unless expressed as such, and should only be viewed as historical data.

2

Table of Contents

PART I

COMPANY OVERVIEW

Unless the context otherwise indicates or requires, as used in this Annual Report on Form 10-K, the terms “we,” “our,” “us,” “ADS” and the “Company” refer to Advanced Drainage Systems, Inc. and its directly- and indirectly-owned subsidiaries as a combined entity, except where it is clear that the terms mean only Advanced Drainage Systems, Inc. exclusive of its subsidiaries.

We are the leading manufacturer of high performance thermoplastic corrugated pipe, providing a comprehensive suite of water management products and superior drainage solutions for use in the underground construction and infrastructure marketplace. Our innovative products are used across a broad range of end markets and applications, including non-residential, residential, agriculture and infrastructure applications. We have established a leading position in many of these end markets by leveraging our national sales and distribution platform, our overall product breadth and scale and our manufacturing excellence. In the United States, our national footprint combined with our strong local presence and broad product offering make us the leader in an otherwise highly fragmented sector comprised of many smaller competitors. We believe the markets we serve in the United States represent approximately $10.8 billion of annual revenue opportunity. In addition, we believe the increasing acceptance of thermoplastic pipe products in international markets represents an attractive growth opportunity. For fiscal year 2016, we generated net sales of $1,290.7 million, net income of $23.5 million and adjusted earnings before interest, taxes, depreciation and amortization (“Adjusted EBITDA”) of $187.3 million and, as of March 31, 2016, we had $351.2 million of total outstanding debt. For a reconciliation of Adjusted EBITDA to the most directly comparable measure calculated in accordance with accounting principles generally accepted in the United States of America (“GAAP”), see “Item 6. Selected Financial and Operating Data.”

Our products are generally lighter, more durable, more cost effective and easier to install than comparable alternatives made with traditional materials. Following our entrance into the non-residential construction market with the introduction of N-12 corrugated polyethylene pipe in the late 1980s, our pipe has been displacing traditional materials, such as reinforced concrete, corrugated steel and PVC, across an ever expanding range of end markets. This has allowed us to consistently gain share and achieve above market growth throughout economic cycles. We expect to continue to drive conversion to our products from traditional materials as contractors, civil design engineers and municipal agencies increasingly acknowledge the superior physical attributes and compelling value proposition of our thermoplastic products. In addition, we believe that overall demand for our products will increase as the regulatory environment continues to evolve.

Our broad product line includes corrugated high density polyethylene (or “HDPE”) pipe, polypropylene (or “PP”) pipe and related water management products. Building on our core drainage businesses, we have aggressively pursued attractive ancillary product categories such as storm and septic chambers, PVC drainage structures, fittings, and water quality filters and separators. We refer to these ancillary product categories as Allied Products. Given the scope of our overall sales and distribution platform, we have been able to drive growth within our Allied Products and believe there are significant growth opportunities going forward.

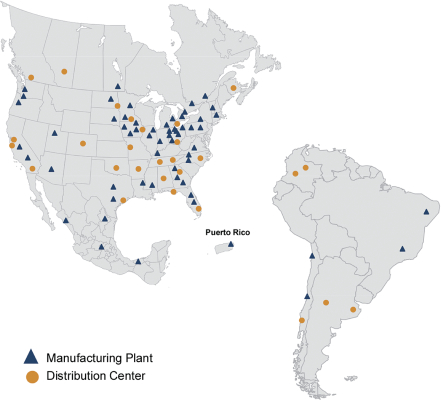

We have an extensive network of 61 manufacturing plants and 31 distribution centers, including the facilities owned or leased by our joint ventures, located across the United States, Puerto Rico, Canada, Mexico, South America and Europe. In the U.S., our network of 47 manufacturing plants and 20 distribution centers allows us to effectively serve all major markets in the United States, which we define as the largest 100 metropolitan statistical areas based on population. The effective shipping radius for our pipe products is approximately 200 miles, thus competition in our industry tends to be on a regional and local basis with minimal competition from distant markets and imports. We are the only supplier of high performance thermoplastic corrugated pipe in our industry with a national footprint in the United States, thereby allowing us to efficiently service those customers that value having one source of supply throughout their entire distribution network. We

3

Table of Contents

believe our extensive national footprint in the United States creates a cost and service advantage versus our HDPE pipe producing competitors, the largest of which has only 11 domestic HDPE pipe manufacturing plants and, according to the July 25, 2016 ranking by Plastics News of Pipe, Profile & Tubing Extruders, recently had estimated sales of $140 million, or approximately nine times less than our net sales in fiscal year 2016. Our International segment consists of 14 manufacturing plants in Canada, Mexico, South America and Puerto Rico and 11 distribution centers located in Canada, South America, and Europe.

The majority of our sales are made through long-standing distribution relationships with many of the largest national and independent waterworks distributors, including Ferguson Enterprises (“Ferguson”), HD Supply Waterworks (“HD Supply”) and WinWholesale, who sell primarily to the storm sewer and sanitary sewer markets. We also utilize a network of hundreds of small to medium-sized independent distributors across the United States. We have strong relationships with major national retailers that carry drainage products, including The Home Depot, Lowe’s, Ace Hardware, Carter Lumber and Do it Best, and also sell to buying groups and co-ops in the United States that serve the plumbing, hardware, irrigation and landscaping markets. The combination of our large sales force, long-standing retail and contractor customer relationships and extensive network of manufacturing and distribution facilities complements and strengthens our broad customer and market coverage.

We believe the ADS brand has long been associated with quality products and market-leading performance. Our trademarked green stripe, which is prominently displayed on many of our products, serves as clear identification of our commitment to the customers and markets we serve.

As illustrated in the charts below, we provide a broad range of high performance thermoplastic corrugated pipe and related water management products to a highly diversified set of end markets and geographies.

Fiscal Year 2016 Revenue

4

Table of Contents

RECENT DEVELOPMENTS

From July 2015 through February 2016, the Company amended the ADS Revolving Credit Facility, the ADS Mexicana Revolving Credit Facility (the “Revolving Credit Facilities”) and the Term Note (collectively, the “Bank Term Loans”), and the Senior Notes, and also obtained various consents from those lenders. These amendments and consents had the effect of: i) extending the time for delivery of our fiscal 2015 audited financial statements and first, second, and third quarter fiscal 2016 quarterly financial information to April 1, 2016, whereby an event of default was waived as long as those items were delivered by that date, ii) modified certain definitions applicable to the Company’s affirmative and negative financial covenants, including the negative covenant on indebtedness, to accommodate the Company’s treatment of its transportation and equipment leases as capital leases rather than operating leases and to accommodate the treatment of the costs related to the Company’s restatement, and iii) permitted the Company’s payment of quarterly dividends on common shares in June, August and December 2015, as well as an annual dividend for preferred shares in March 2016. The Company satisfied the amended reporting requirements prior to April 1, 2016.

In July 2016, the Company obtained additional consents from the lenders of the Bank Term Loans and Senior Notes. These consents had the effect of extending the time for delivery of our fiscal 2016 audited financial statements to August 31, 2016, and first quarter fiscal 2017 quarterly financial information to October 15, 2016, whereby an event of default was waived as long as those items are delivered within a 15 day grace period after those dates. In addition, the consents also permitted the Company’s payment of quarterly dividends of $0.06 per share on common shares in each of June and September 2016, as well as the annual dividend of $0.0195 per share to be paid on shares of preferred stock in March 2017. See “Note 12. Debt” to our consolidated financial statements included in “Item 8. Financial Statements and Supplementary Data” of this Form 10-K.

On July 17, 2015, we acquired an additional 10% of the issued and outstanding membership interests in BaySaver Technologies, LLC (“BaySaver”) for a purchase price of $3.2 million, subject to certain additional post-closing purchase price payments specified in the Purchase Agreement. Concurrent with the acquisition, we also entered into an amendment to the BaySaver joint venture agreement to change the voting rights for the joint venture from an equal vote for each member to a vote based upon the respective ownership interest. As a result of the acquisition and the amendment, the Company increased its ownership interest to 65% of the issued and outstanding membership interests in BaySaver and obtained the majority of the voting rights. As a result, our consolidated financial statements include the consolidation of BaySaver’s financial statements beginning on July 17, 2015. See “Note 3. Acquisitions” to our consolidated financial statements included in “Item 8. Financial Statements and Supplementary Data” of this Form 10-K.

On January 30, 2015, Hancor of Canada, Inc., a wholly-owned subsidiary of the Company, acquired all issued and outstanding shares of Ideal Drain Tile Limited and Wave Plastics Inc., the sole partners of Ideal Pipe, (together “Ideal Pipe”). Ideal Pipe designs, manufactures and markets high performance thermoplastic corrugated pipe and related water management products used across a broad range of Canadian end markets and applications, including nonresidential, residential, agriculture, and infrastructure applications. The acquisition further strengthens our positions in Canada by increasing our size and scale in the market, as well as enhancing our manufacturing, marketing and distribution capabilities. The purchase price of Ideal Pipe was $43.8 million, financed through our existing line of credit facility.

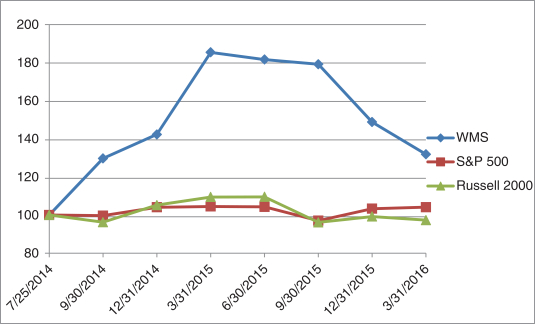

In July 2014, we completed an initial public offering of our common stock. In December 2014, a certain selling stockholder sold 10 million shares of our common stock in a secondary public offering. See “Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations — Recent Developments.” Our common stock is listed on the NYSE under the symbol “WMS.”

SEGMENT INFORMATION

For a discussion of segment and geographic information, see “Note 21. Business Segment Information” to our audited consolidated financial statements included in “Item 8. Financial Statements and Supplementary Data” of this Form 10-K.

5

Table of Contents

OUR MANUFACTURING AND DISTRIBUTION PLATFORM

We have a leading domestic and international manufacturing and distribution infrastructure, serving customers in all 50 U.S. states as well as approximately 80 other countries through 61 manufacturing plants and 31 distribution centers including the facilities owned or leased by our joint ventures. We also operate an in-house fleet of approximately 675 tractor-trailers. Our effective shipping radius is approximately 200 miles from one of our manufacturing plants or distribution centers. Our scale and extensive network of facilities provide a critical cost advantage versus our competitors, as we are able to more efficiently transport products to our customers and end users and to promote faster product shipments due to our proximity to the delivery location.

The combination of a dedicated fleet and team of company drivers allows greater flexibility and responsiveness in meeting dynamic customer jobsite delivery expectations. We strive to achieve less than three-day lead-time on deliveries, and have the added benefit of redeploying fleet and driver assets to respond to short-term regional spikes in sales activity. For deliveries that are outside an economic delivery radius of our truck fleet, common carrier deliveries are tendered using a customized software platform to ensure that lowest delivered freight costs are achieved. In addition, in the United States and Canada, more than 12% of our pipe volume is sold on a pick-up or walk-in basis at our plant and yard locations, further leveraging our footprint and lowering freight cost per pound and per revenue dollar.

Our North American truck fleet incorporates approximately 1,200 trailers that are specially designed to haul our lightweight pipe and fittings products. These designs maximize payload versus conventional over the road trailers and facilitate unassisted unloading of our products at the jobsites by our drivers. The scope of fleet operations also includes backhaul of purchased raw materials providing a lower delivered cost to our plant locations.

We have expanded internationally primarily through joint ventures with local partners. This joint venture strategy has provided us with local and regional access to markets such as Brazil, Chile, Argentina, Mexico, Peru and Colombia. These international facilities produce pipe and related products to be sold in their respective regional markets. Combining a local partner’s customer relationships, brand recognition and local management talent, with our world-class manufacturing and process expertise, broad product portfolio and innovation, creates a powerful platform and exciting opportunities for continued international expansion.

OUR MANUFACTURING PROCESS

We manufacture our corrugated pipe products in 17 different diameters ranging from 2” to 60” using a continuous extrusion process, where molten polyethylene or polypropylene is pushed through a die into a moving series of corrugated U-shaped molds. Blown air and vacuum are used to form the corrugations of the pipe which is pulled through a corrugator and then cut to length. We utilize customized and proprietary production equipment, which we believe is faster and more cost efficient than other pipe making equipment generally available in the market.

Domestically, we operate approximately 121 pipe production lines that collectively are capable of producing more than one billion pounds of pipe annually on a standard five-day per week schedule. Additional capacity is in place to support seasonal production needs and growth in our N-12 pipe sales volume requiring minimal additional capital for molds. Our normal production capacity utilization as a percentage of total capacity was 70%, 68% and 64% for fiscal years 2016, 2015 and 2014, respectively. To produce our broad range of pipe sizes, we own and utilize approximately 350 mold and die setups, which had an original capital cost of approximately $132 million, and most of which are moved between manufacturing plants. Our production equipment is built to accept transportable molds and die tooling over a certain range of sizes so each plant is not required to house the full range of tooling at any given time. This transportability provides us with the flexibility to optimize our capacity through centrally-coordinated production planning, which helps to adapt to shifting sales demand patterns while reducing the capital needed for tooling. With our large manufacturing footprint in place, we can support rapid seasonal growth in demand, focusing on customer service while minimizing transportation costs.

6

Table of Contents

The standard fittings products (tees, wyes, elbows, etc.) that we produce and sell to connect our pipe on jobsites are blow molded or injection molded at four domestic plants. In addition, customized fabricated fittings (e.g., more complex dual wall pipe reducers, bends or structures) are produced in 20 of our North American plants. In addition to the extrusion of pipe, and blow molding and injection molding of fittings, we also use a variety of other processes in our manufacturing facilities. These processes include thermoforming, compression molding, and custom plastic welding and fabrication. The wide variety of production processes and expertise allow us to provide cost-effective finished goods at competitive prices delivered in a timely fashion to our customers.

Our manufacturing plants have no process-related by-products released into the atmosphere, waterways, or solid waste discharge. During pipe production start-ups and size change-overs, non-compliant scrap and any damaged finished goods pipe are recycled through a grinder for internal re-use.

We have two internal quality control laboratory facilities equipped and staffed to evaluate and confirm incoming raw material and finished goods quality in addition to the quality testing that is done at our manufacturing facilities. We conduct annual safety, product and process quality audits at each of our facilities, using centralized internal resources in combination with external third-party services. In the quality area, various national agencies such as National Transportation Product Evaluation Program (“NTPEP”), International Association of Plumbing and Mechanical Officials (“IAPMO”), Bureau de normalisation du Québec (“BNQ”), Intertek for Canadian Standards Association (“CSA”) , Entidad Mexicana de Acreditacion A.C. (“EMA”) and NSF International and numerous state Departments of Transportation (“DOT”) (e.g., Illinois, Michigan) and municipal authorities (e.g., City of Columbus) conduct both scheduled and unscheduled inspections of our plants to verify product quality and compliance to applicable standards.

Core to our commitment and enablement of a safe and productive manufacturing environment are our operational and management training programs. Through our ADS Academy, we deliver targeted role-specific training to our operations team members through a blended curriculum of on-line and hands-on training experiences covering safety, quality, product knowledge and manufacturing process. Our learning management system, which hosts over 475 custom modules, serves as the foundation of our operational training programs and provides us with appropriate scale, efficiency, and governance to support our growth. We have a strong commitment to the training of our manufacturing supervisors and managers in technical, management, and leadership subjects through intense role-based assimilation plans, e-learning and classroom-based development experiences.

OUR PRODUCTS

We design, manufacture and market a complete line of high performance thermoplastic corrugated pipe and related water management products for use in a wide range of end markets. Our product line includes: single, double and triple wall corrugated polypropylene and polyethylene pipe, or Pipe, and a variety of Allied Products including: storm retention/detention and septic chambers, or Chambers; PVC drainage structures, or Structures; fittings, or Fittings; and water quality filters and separators, or Water Quality. We also sell various complementary products distributed through resale agreements, including geotextile products and drainage grates and other, or Other Resale.

7

Table of Contents

An overview of our product offerings is provided below:

| Product Offering |

Description |

Brands/Offerings |

Images | |||

| Pipe (74%, 76% & 76% of Net Sales in Fiscal Years 2016, 2015 & 2014) |

||||||

| High density polyethylene and polypropylene pipe | Dual Wall Corrugated Pipe, HP Storm Pipe, SaniTite HP Pipe, Single Wall Corrugated Pipe, Triple Wall Corrugated Pipe, Smoothwall HDPE Pipe |

| ||||

| Allied Products (26%, 24% & 24% of Net Sales in Fiscal Years 2016, 2015 & 2014) |

||||||

| Chambers |

Underground chambers made from polypropylene or HDPE that can function as stormwater detention, retention, and/or “first flush” storage systems | StormTech, ARC (Septic Chambers), BioDiffuser (Septic Chambers) |

| |||

| Structures |

Drainage structures consisting of inline drains, drain basins, curb inlet structures, and drop-in grates in diameters ranging from 8” to 30” | Nyloplast, Inserta Tee |

| |||

| Fittings |

Standard and fabricated joining systems | Fittings |

| |||

| Water Quality |

Water quality structures and filters | BaySeparator, BayFilter, Water Quality Units, FleXstorm |

| |||

| Other Resale |

Complementary products providing services adjacent to core expertise | Geotextiles |

| |||

Pipe

Dual Wall Corrugated Pipe

Our N-12 pipe is a dual wall HDPE pipe with a corrugated exterior for strength and a smooth interior wall for hydraulics and flow capacity. Our N-12 pipe competes in the storm sewer and drainage markets that are also served by concrete pipe.

Our N-12 pipe is available in 17 different diameters ranging from 2” to 60” and in sections ranging from 10’ to 30’ in length. N-12 provides joint integrity, with integral bell and spigot joints for fast push-together installation, and is sold either with watertight or soil-tight coupling and fitting systems.

8

Table of Contents

Our corrugated polyethylene pipe offers many benefits including ease of installation, job-site handling and resistance to corrosion and abrasion. Corrugated pipe can easily be cut or coupled together, providing precise laying lengths while minimizing installation waste and difficulty.

HP Storm Pipe and SaniTite HP Pipe

Our HP Storm pipe utilizes polypropylene resin, which provides (i) increased pipe stiffness relative to HDPE; (ii) higher Environmental Stress Crack Resistance (“ESCR”); and (iii) improved thermal properties, which improves joint performance. These improved physical characteristics result in a reduced need for select backfill, which creates installation savings for customers and expands the range of possible product applications.

Our SaniTite HP pipe utilizes the same polypropylene resins as our HP Storm pipe but includes a smooth third exterior wall in 30” to 60” pipe. The highly engineered polypropylene resin along with the triple wall design enables SaniTite HP to surpass the 46 pounds per square inch (“psi”), stiffness requirement for sanitary sewer applications. SaniTite HP offers cost and performance advantages relative to reinforced concrete pipe (such as improved hydraulics and better joint integrity) and PVC pipe (such as impact resistance).

Single Wall Corrugated Pipe

Our single wall corrugated HDPE pipe is ideal for drainage projects where flexibility, light weight and low cost are important. Single wall HDPE pipe products have been used for decades in agricultural drainage, highway edge drains, septic systems and other construction applications. In the agricultural market, improved technology has highlighted the favorable impact of drainage on crop yields. For homeowners, it is an economical and easily-installed solution for downspout run-off, foundation drains, driveway culverts and general lawn drainage. Single wall pipe is also used for golf courses, parks and athletic fields to keep surfaces dry by channeling away excess underground moisture.

Standard single wall products are available in 2” to 24” diameters and sold in varying lengths. Pipe with 2” to 6” diameters is typically sold in coils ranging from 25’ to over 3,000’ in length, while larger diameter pipe is typically sold in 20’ lengths. Pipe can be either perforated or non-perforated depending on the particular drainage application.

Triple Wall Corrugated Pipe and Smoothwall HDPE Pipe

Our ADS-3000 Triple Wall pipe, small diameter triple wall corrugated pipe, consists of a corrugated polyethylene core molded between a smooth white outer wall and a smooth black inner wall. This combination of the three wall design adds strength and stiffness, while reducing weight as compared to PVC 2729. Triple Wall is produced in two sizes, 3” and 4”, and sold through our distribution network.

We also manufacture smoothwall HDPE pipe in 3”, 4”, and 6” diameters that are sold into the residential drainage and on-site septic systems markets.

Allied Products

We produce a range of additional water management products that are complementary to our pipe products (“Allied Products”). Our Allied Products offer adjacent technologies to our core pipe offering, presenting a complete drainage solution for our clients and customers. This combination of pipe and Allied Products is a key strategy in our sales growth, profitability and market share penetration. The practice of selling a drainage system is attractive to both distributors and end users, by providing a broad package of products that can be sold on individual projects, and strengthens our competitive advantage in the marketplace. We aggressively seek and evaluate new products, technologies and regulatory changes that impact our customers’ needs for Allied Products.

9

Table of Contents

Using the strength of our overall sales and distribution platform, our Allied Product strategy allows us to more deeply penetrate our end markets and anticipate the evolving needs of our customers. The underground construction industry has historically been project (not product) driven, creating the impetus for owners, engineers and contractors to seek manufacturers that deliver solution-based product portfolios. Many of the components of underground construction are related and require linear compatibility of function, regulatory approval and technology.

Storm and Septic Chambers

Our StormTech chambers are used for stormwater retention, detention and “first flush” underground water storage on non-residential site development and public projects. These highly engineered chambers are injection molded from high density polyethylene and polypropylene resins into a proprietary design which provides strength, durability, and resistance to corrosion. The chambers allow for the efficient storage of stormwater volume, reducing the underground construction footprint and costs to the contractors, developers, and property owners. Our StormTech chambers offer great flexibility in design and layout of underground water storage systems. They are an attractive alternative to open ponds by reducing ongoing maintenance and liability and providing more useable land for development. Stormwater runoff is collected and stored in rows of chambers and gradually reenters the water system base, reducing erosion and protecting waterways. The chambers are open bottom, which allows for high density stacking in both storage and shipment. This freight-efficient feature drives favorable cost-competitiveness in serving long-distance export markets. These chamber systems typically incorporate our other product lines such as corrugated pipe, fabricated fittings, water quality units and geotextiles.

Our ARC and BioDiffuser products are chambers that are used in on-site septic systems for residential and small volume non-residential wastewater treatment and disposal. Rural homes and communities that do not have access to central sewer lines require an on-site septic solution. Our ARC and BioDiffuser chamber products are installed and perform their septic treatment function without gravel, reducing costs to the contractor and homeowner over traditional pipe and stone systems. States and municipalities have different sizing criteria for on-site septic treatment systems based on soil and site conditions. The innovative design of our ARC chamber is generally approved for a footprint reduction, further reducing the cost of the septic system. Injection-molded from high density polyethylene, these products are strong, durable, and chemical-resistant. These interconnecting chambers are favored by septic contractors because they are lightweight, easy to install and offer articulating features which increase site-specific design flexibility.

Structures

Our Nyloplast PVC drainage structures are used in non-residential, residential and municipal site development, road and highway construction, as well as landscaping, recreational, industrial and mechanical applications. The product family includes inline drains, drain basins, curb inlets and water control structures which move surface-collected stormwater vertically down to pipe conveyance systems. These custom structures are fabricated from sections of PVC pipe using a thermo-forming process to achieve exact site-specific hydraulic design requirements. Our Nyloplast products are a preferred alternative to heavier and larger concrete structures, by offering greater design flexibility and improved ease of installation which reduces overall project costs and timelines. The structures incorporate rubber gaskets to ensure watertight connections, preventing soil infiltration which plagues competitive products.

Our Inserta Tee product line consists of a PVC hub, rubber sleeve and stainless steel band. Inserta Tee is compression fit into the cored wall of a mainline pipe and can be used with all pipe material types and profiles. This product offers an easy tap-in to existing sanitary and storm sewers by limiting the excavation needed for installation compared to competitive products.

10

Table of Contents

Fittings

We produce fittings and couplings utilizing blow molding, injection molding and custom fabrication on our pipe products. Our innovative coupling and fitting products are highly complementary to our broader product suite, and include both soil-tight and water-tight capabilities across the full pipe diameter spectrum. Our fittings are sold in all end markets where we sell our current pipe products.

Water Quality

Our BaySaver product line targets the removal of sediment, debris, oils and suspended solids throughout a stormwater rain event by separating and/or filtering unwanted pollutants. Our BaySeparators can be fabricated into multiple sizing combinations to fit a variety of applications and customer requirements. These products assist owners, developers and design engineers in remaining compliant with discharge requirements set forth by the Environmental Protection Agency (“EPA”) as well as state and local regulatory agencies. Our BaySaver product line coupled with our pipe, StormTech chambers, fabricated fittings, Nyloplast structures, FleXstorm inlet protection systems and geotextiles make up a comprehensive stormwater management solution.

Construction Fabrics & Geotextiles

We purchase and distribute construction fabrics and other geosynthetic products for soil stabilization, reinforcement, filtration, separation, erosion control, and sub-surface drainage. Constructed of woven and non-woven polypropylene, geotextile products provide permanent, cost-efficient site-development solutions. Construction fabrics and geotextiles have applications in all of our end markets.

RAW MATERIALS

Virgin high density polyethylene (“HDPE”) and polypropylene (“PP”) resins are derivatives of ethylene and propylene, respectively. Ethylene and propylene are derived from natural gas liquids or crude oil derivatives in the U.S. We currently purchase in excess of 850 million pounds of virgin and recycled resin annually from over 450 suppliers in North America. As a high-volume buyer of resin, we are able to achieve economies of scale to negotiate favorable terms and pricing. Our purchasing strategies differ based on the material (virgin resin v. recycled material) ordered for delivery to our production locations. The price movements of the different materials also vary, resulting in the need to use a number of strategies to reduce volatility and successfully pass on cost increases to our customer through timely selling price increases when needed.

In 2008 we began to further augment our raw material blending and processing technologies to produce an HDPE pipe that incorporates recycled resin. This product, which meets an ASTM International (“ASTM”) standard, replaces a majority of the virgin resin that is used in the American Association of State Highway and Transportation Officials (“AASHTO”) product with recycled materials. To further develop our recycled material strategies, we established Green Line Polymers, Inc. (“GLP”), as our wholly-owned recycling subsidiary in 2012. GLP procures and processes recycled raw materials that can be used in products we produce and sell. Our first production facilities were established in Ohio and Georgia and are focused on processing post-industrial HDPE recycled materials. Based on the success of this strategy, we expanded our efforts toward post-consumer material processing by acquiring the business of a vendor who was supplying clean, post-consumer recycled HDPE to our upper Midwest plants and established a second post-consumer processing plant, in Pennsylvania, to support our plants in Ohio, Michigan and the eastern and southern United States. In fiscal year 2016, 84% of our non-virgin HDPE raw material needs were internally processed (enhanced) through our GLP operations.

We believe that we are well positioned for future growth as we add additional recycled material processing facilities, add capacity to existing facilities, and expand our supplier base for virgin resin. We anticipate continued growth in the availability of ethylene and propylene which are used to manufacture high density polyethylene and polypropylene, respectively.

11

Table of Contents

We have managed a formal resin price risk management program since early in 2010 that entails both physical fixed price and volume contracts along with financial hedges which are designed to apply to a portion of our annual virgin resin purchases. In conjunction with our resin price risk management program, we also maintain supply agreements with our major resin suppliers that provide multi-year terms and volumes that are in excess of our projected consumption. For our polypropylene virgin resin price exposure, we utilize financial hedges of propylene as a proxy for polypropylene. Historically, there has been high correlation in month to month change in market-based pricing between propylene and polypropylene.

We also began a diesel hedging program in 2008 which is executed through several financial swaps covering future months demand for diesel fuel and are designed to decrease our exposure to changing fuel costs. These hedges cover a significant portion of the diesel fuel consumed by the truck fleet that we operate to deliver products to our customers. Our objective is to hedge approximately 50% of our fuel consumption over the next 12 months.

SUPPLIERS

We have developed relationships with all of the North American producers of virgin high density polyethylene and impact copolymer polypropylene producers that produce the grades we need to produce our products, including Braskem Americas, Inc., Chevron Phillips Chemical Co. LP, The Dow Chemical Company, Equistar Chemicals, LP, ExxonMobil Chemical Company, Formosa Plastics Corporation, U.S.A., Ineos Olefins & Polyolefins, USA, Sasol USA, and Phillips 66 Company.

We also maintain relationships with several of the largest environmental companies such as Waste Management, Inc., Republic Services, Inc., and Rumpke, Inc., which provide us with post-consumer HDPE recycled materials. We also maintain relationships with several key post-industrial HDPE suppliers, including E.I. du Pont de Nemours and Company, Silgan Plastics, Consolidated Container Company and Alpla, Inc. which provide us with materials that cannot otherwise be utilized in their respective production processes.

The North American capacity for ethylene derivatives is being expanded primarily as a result of the new supplies of natural gas liquids being produced through sustained oil and gas exploration and production. This low-cost stream of feedstocks (ethane and propane) has positioned several companies such as Lyondell Basell, ExxonMobil Chemical Company, Chevron Phillips Chemical Co. LP and The Dow Chemical Company to execute plans to expand ethylene or propylene capacity. We anticipate that the previously announced projects for ethylene derivative capacity associated with HDPE will begin coming on stream during 2016, extending through 2018. The polypropylene capacity expansion projects to utilize the increased supply of propylene are projected to begin coming on-stream in 2018.

CUSTOMERS

We have a large, active customer base of approximately 20,000 customers, with two customers representing 10% or more of fiscal year 2016 net sales. Ferguson accounted for 11.1% and HD Supply accounted for 10.0% of fiscal year 2016 net sales. Our customer base is diversified across the range of end markets that we serve.

A majority of our sales are made through distributors, including many of the largest national and independent waterworks distributors, with whom we have long-standing distribution relationships. These include Ferguson, HD Supply and WinWholesale, who sell primarily to the storm sewer and sanitary sewer markets. We also utilize a network of hundreds of small to medium-sized independent distributors across the United States. We have strong relationships with major national retailers that carry drainage products, including The Home Depot, Lowe’s, Ace Hardware, Carter Lumber and Do it Best. We offer the most complete line of HDPE products in the industry and are the only national manufacturer that can service the “Big-Box” retailers from coast-to-coast. We also sell to buying groups and co-ops in the United States that serve the plumbing, hardware, irrigation and landscaping markets. Selling to buying groups and co-ops provides us a further presence on a

12

Table of Contents

national, regional and local basis for the distribution of our products. Our preferred vendor status with these groups allows us to reach thousands of locations in an effective manner. Members of these groups and co-ops generally are independent businesses with strong relationships and brand recognition with smaller contractors and homeowners in their local markets. The combination of our large sales force, long-standing retail and contractor customer relationships and extensive network of manufacturing and distribution facilities complements and strengthens our broad customer and market coverage.

An important element of our growth strategy has been our focus on industry education efforts to drive regulatory approvals for our core HDPE products at national, state and local levels. We employ a team of approximately 50 field-based engineers who work closely with government agencies to obtain regulatory approvals for our products, and also with civil engineering firms to specify our products on non-residential construction and road-building projects. We consistently maintain an active dialogue with customers, civil engineers and municipal authorities, continuously educating them on new product innovations and their advantages relative to traditional products. With the introduction of our HP storm and sanitary pipe, we have refocused our efforts calling on state departments of transportation to enhance their approval of our pipe products. Additional state and local regulatory approvals will continue to present new growth opportunities in new and existing geographic markets for us.

Our customer service organization of more than 120 employees is supplemented by the employees of our 61 manufacturing plants, 31 distribution centers and drivers of our approximately 675 tractor-trailers. In conjunction with our field sales and engineering team, this highly-trained and competent staff allows us to maintain more customer touch points and interaction than any of our competitors.

We staff and operate four regional customer service call centers located in three time zones where orders are processed. With some of our larger customers, we process orders electronically via electronic data interchange (EDI). Additionally, we send advance shipment notifications and invoices electronically to these customers. These capabilities strengthen the supply chain integration with large customers such as The Home Depot, Lowes, Ferguson and HD Supply. New orders are entered into our Oracle system, assigned to our closest manufacturing plant or distribution center in that geography, and then consolidated to optimize freight efficiency, payload and lead-time performance to meet customer requirements.

SALES AND MARKETING

We believe we have the largest and most experienced sales and engineering force in the industry, with approximately 350 sales and engineering professionals. Offering the broadest product line in the industry enables our sales force to source the greatest number of new opportunities and more effectively cross-sell products than any of our competitors. We consistently maintain thousands of touch-points with customers, civil engineers and municipal authorities, continuously educating them on new product innovations and their advantages relative to traditional products. We believe we are the industry leader in these efforts and we view this work as an important part of our marketing strategy, particularly in promoting N-12 and SaniTite HP for storm and sanitary sewer systems, as regulatory approvals are essential to the specification and acceptance of these product lines.

Our sales and marketing strategy is divided into four components — comprehensive market coverage, diverse product offerings, readily-available local inventory and specification efforts. Our goal is to provide the distributor/owner with the most complete, readily-available product line in our industry. We strive to use our manufacturing footprint, product portfolio and market expertise to efficiently service our customers.

Our sales and engineering objective is to influence, track and quote all selling opportunities as early in the project life cycle as possible. Conceptual project visibility allows sales and engineering professionals the ability to influence design specifications and increase the probability of inclusion of our products in bid documents. We strive to be meaningfully involved in all phases of the project cycle, including design, bidding, award and installation. In addition to direct channel customers, we also maintain and develop relationships with federal

13

Table of Contents

agencies, municipal agencies, national standard regulators, private consulting engineers and architects. Our consistent interaction with these market participants enables us to continue our market penetration. This ongoing dialogue has positioned us as an industry resource for design guidance and product development and as a respected expert in water management solutions.

SEASONALITY

Historically, sales of our products have been higher in the first and second quarters of each fiscal year due to favorable weather and longer daylight conditions accelerating construction activity during these periods. Seasonal variations in operating results may also be impacted by inclement weather conditions, such as cold or wet weather, which can delay projects.

In the non-residential, residential and infrastructure markets in the northern United States and Canada, construction activity typically begins to increase in late March and is slower in December, January and February. In the southern and western United States, Mexico, Central America and South America, the construction markets are less seasonal. The agricultural drainage market is concentrated in the early spring just prior to planting and in the fall just after crops are harvested prior to freezing of the ground in winter.

PRACTICES RELATED TO WORKING CAPITAL ITEMS

Information about the Company’s working capital practices is incorporated herein by reference to “Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations — Results of Operations — Working Capital and Cash Flows” of this Form 10-K.

COMPETITION

We operate in a highly fragmented industry and hold leading positions in multiple market sectors. Competition, including our competitors and specific competitive factors, varies for each market sector.

We believe the principal competitive factors for our market sectors include local selling coverage, product availability, breadth and cost of products, technical knowledge and expertise, customer and supplier relationships, reliability and accuracy of service, effective use of technology, delivery capabilities and timeliness, pricing of products, and the provision of credit. We believe that our competitive strengths and strategy allow us to compete effectively in our market sectors.

The stormwater drainage industry, in particular, is highly fragmented with many smaller specialty and regional competitors providing a variety of product technologies and solutions. We compete against concrete pipe, corrugated steel pipe and PVC pipe producers on a national, regional and local basis. In addition, there are several HDPE pipe producers in the United States.

In the United States, our primary competitors are concrete pipe producers, including Cemex, Hanson and Oldcastle CRH Precast, as well as smaller, regional competitors. In the corrugated steel pipe sector, our primary national competitor is Contech Engineered Solutions, and we compete with Lane Enterprises, Pacific Corrugated and Southeast Culvert on a regional level, as well as other smaller competitors. In the PVC pipe sector, we compete primarily with JM Eagle, Diamond Plastics and North American Pipe. We believe we are the only corrugated HDPE pipe producer with a national footprint, and our competitors operate primarily on a regional and local level. In the corrugated HDPE pipe sector in the United States, our primary competitors on a regional basis are JM Eagle, Lane Enterprises and Prinsco.

The superior attributes of HDPE and PP and ongoing product innovation have allowed thermoplastic pipe manufacturers generally, and us in particular, to capture market share across all end market categories. This substitution trend is expected to continue as more states and municipalities recognize the benefits of our HDPE N-12 pipe and our polypropylene HP pipe by approving it for use in a broader range of applications.

14

Table of Contents

INTELLECTUAL PROPERTY

Intellectual property is an important aspect of our business. We rely upon a combination of patents, trademarks, trade names, licensing arrangements, trade secrets, know-how and proprietary technology in order to secure and protect our intellectual property rights, both in the United States and in foreign countries.

We seek to protect our new technologies with patents and trademarks and defend against patent infringement allegations. We hold a significant amount of intellectual property rights pertaining to product patents, process patents and trademarks. We continually seek to expand and improve our existing product offerings through product development and acquisitions. Although our intellectual property is important to our business operations and in the aggregate constitutes a valuable asset, we do not believe that any single patent, trademark or trade secret is critical to the success of our business as a whole. We cannot be certain that our patent applications will be issued or that any issued patents will provide us with any competitive advantages or will not be challenged by third parties.

In addition to the foregoing protections, we generally control access to and use of our proprietary and other confidential information through the use of internal and external controls, including contractual protections with employees, distributors and others. Despite these protections, we may be unable to prevent third parties from using our intellectual property without our authorization, breaching any nondisclosure agreements with us, or independently developing products that are similar to ours, particularly in those countries where the laws do not protect our proprietary rights as fully as in the United States.

See “Item 1A. Risk Factors — Risks Relating to Our Business — If we are unable to protect our intellectual property rights, or we infringe on the intellectual property rights of others, our ability to compete could be negatively impacted.”

EMPLOYEES

As of March 31, 2016, in our domestic and international operations the Company and its consolidated and unconsolidated joint ventures had approximately 4,300 employees, consisting of approximately 3,000 hourly personnel and approximately 1,300 salaried employees. As of March 31, 2016, approximately 315 hourly personnel in our Mexican and South American operations were covered by collective bargaining agreements.

REGULATION

Our operations are affected by various statutes, regulations and laws in the markets in which we operate, which historically have not had a material effect on our business. We are subject to various laws applicable to businesses generally, including laws affecting land usage, zoning, the environment, health and safety, transportation, labor and employment practices, competition, immigration and other matters. Additionally, building codes may affect the products our customers are allowed to use, and, consequently, changes in building codes may affect the salability of our products. The transportation and disposal of many of our products are also subject to federal regulations. The U.S. Department of Transportation (“U.S. DOT”) regulates our operations in domestic interstate commerce. We are subject to safety requirements governing interstate operations prescribed by the U.S. DOT. Vehicle dimensions and driver hours of service also remain subject to both federal and state regulation.

We have been able to consistently capitalize on changes in both local and federal regulatory statutes relating to storm and sanitary sewer construction, repair and replacement. Most noteworthy is the Federal Clean Water Act of 1972 and the subsequent EPA Phase I, II and sustainable infrastructure regulations relating to storm sewer construction, storm water quantity, storm water quality, and combined sewer separation. Our diversity of products offering a solution-based selling approach coupled with detailed market knowledge makes us an integral industry resource in both regulatory changes and compliance.

15

Table of Contents

ENVIRONMENTAL, HEALTH AND SAFETY MATTERS

We are subject to a broad range of foreign, federal, state and local environmental, health and safety laws and regulations, including those pertaining to air emissions, water discharges, the handling, disposal and transport of solid and hazardous materials and wastes, the investigation and remediation of contamination and otherwise relating to health and safety and the protection of the environment and natural resources. As our operations, and those of many of the companies we have acquired, to a limited extent involve and have involved the handling, transport and distribution of materials that are, or could be classified as, toxic or hazardous, there is some risk of contamination and environmental damage inherent in our operations and the products we handle, transport and distribute. Our environmental, health and safety liabilities and obligations may result in significant capital expenditures and other costs, which could negatively impact our business, financial condition and results of operations. We may be fined or penalized by regulators for failing to comply with environmental, health and safety laws and regulations, or we may be held responsible for such failures by companies we have acquired. In addition, contamination resulting from our current or past operations, and those of many of the companies we have acquired, may trigger investigation or remediation obligations, which may have a material adverse effect on our business, financial condition and results of operations.

CORPORATE AND AVAILABLE INFORMATION

We were founded in 1966 and are a Delaware corporation. Our principal executive offices are located at 4640 Trueman Boulevard, Hilliard, Ohio 43026, and our telephone number at that address is (614) 658-0050. Our corporate website is www.ads-pipe.com.

Our Annual Report on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K, and amendments to reports filed pursuant to Sections 13(a) and 15(d) of the Securities Exchange Act of 1934, as amended, (“Exchange Act”) are filed with the SEC. We are subject to the informational requirements of the Exchange Act and file or furnish reports, proxy statements, and other information with the SEC. Such reports and other information filed by the Company with the SEC are available free of charge on our website at www.ads-pipe.com when such reports are available on the SEC’s website. We use our www.ads-pipe.com website as a means of disclosing material non-public information and for complying with our disclosure obligations under Regulation FD. Accordingly, investors should monitor such portions of www.ads-pipe.com in addition to following press releases, SEC filings and public conference calls and webcasts.

The public may read and copy any materials filed by the Company with the SEC at the SEC’s Public Reference Room at 100 F Street, NE, Room 1580, Washington, DC 20549. The public may obtain information on the operation of the Public Reference Room by calling the SEC at 1-800-SEC-0330. The SEC maintains an Internet site that contains reports, proxy and information statements and other information regarding issuers that file electronically with the SEC at www.sec.gov.

The contents of the websites referred to above are not incorporated into this filing. Further, our references to the URLs for these websites are intended to be inactive textual references only.

16

Table of Contents

You should carefully consider the risks described below, together with all other information included or incorporated by reference in this Annual Report on Form 10-K. If any of the following risks actually occur, our business, financial condition, results of operations and cash flows could be materially adversely affected. In these circumstances, the market price of our common stock could decline significantly.

Risks Relating to the Restatement and Our Financial Reporting Process

The restatement of our previously issued financial statements and the related claims, investigations and proceedings arising out of the restatement have been time-consuming and expensive and could expose us to additional risks that would adversely affect our financial position, results of operations and cash flows.

As described in our Annual Report on Form 10-K for the fiscal year ended March 31, 2015 (the “Fiscal 2015 Form 10-K”), we have restated our previously issued consolidated financial statements for the fiscal years ended March 31, 2014 and 2013, as well as each of the first three quarters in fiscal year 2015 and for all of the quarterly periods in fiscal year 2014. We also restated our financial results for the fiscal years ended March 31, 2012 and 2011, as summarized in “Item 6. Selected Financial and Operating Data” to our Fiscal 2015 Form 10-K. The restatement was time-consuming and expensive and could expose us to a number of additional risks that would adversely affect our financial position, results of operations and cash flows.

In particular, we have incurred significant expense, including audit, legal, consulting and other professional fees in connection with the restatement of our previously issued consolidated financial statements. Expenses incurred during fiscal 2016 as a result of the restatement were approximately $28 million. We have also incurred significant expense in connection with the ongoing remediation of the weaknesses in our internal control over financial reporting as further described below.

We are also subject to claims, investigations and proceedings arising out of the errors in our previously issued financial statements, including securities class action litigation against us. See “The restatement of our previously issued financial results has resulted in private litigation as well as an ongoing investigation by the SEC, and could result in additional litigation, government investigations and enforcement actions that could have a material adverse impact on our results of operations, financial condition, liquidity and cash flows.” The ongoing costs and expense associated with these matters could also have a material adverse impact on our results of operations, financial condition, liquidity and cash flows, which costs and expenses may be difficult to predict.

We have identified material weaknesses in our internal control over financial reporting which could, if not remediated, adversely affect our ability to report our financial condition and results of operations in a timely and accurate manner, investor confidence in our company and, as a result, the value of our common stock.

We are required to evaluate the effectiveness of our disclosure controls on a periodic basis and publicly disclose the results of these evaluations and related matters in accordance with the requirements of Section 404 of the Sarbanes-Oxley Act of 2002. We have identified certain material weaknesses in internal control over financial reporting in the areas of (i) the Company’s control environment, (ii) accounting for leases, (iii) accounting for inventory, (iv) journal entry and account reconciliation, (v) ADS Mexicana control environment, and (vi) ADS Mexicana revenue recognition cut-off practices as described in “Item 9A. Controls and Procedures” of this Form 10-K. As a result of such material weaknesses, our management concluded that our disclosure controls and procedures were not effective as of March 31, 2016.

A “material weakness” is a deficiency, or a combination of deficiencies, in internal control over financial reporting, such that there is a reasonable possibility that a material misstatement of our annual or interim consolidated financial statements will not be prevented or detected on a timely basis. We are actively engaged in remediation activities designed to address these material weaknesses, but our remediation efforts are not

17

Table of Contents

complete and are ongoing. Although we are working to remedy the ineffectiveness of the Company’s internal control over financial reporting, there can be no assurance as to when the remediation plan will be fully implemented or the aggregate cost of implementation. Until our remediation plan is fully implemented, our management will continue to devote significant time and attention to these efforts. If we do not complete our remediation in a timely fashion, or at all, or if our remediation plan is inadequate, there will continue to be an increased risk that we will be unable to timely file future periodic reports with the SEC and that our future consolidated financial statements could contain errors that will be undetected. If we are unable to report our results in a timely and accurate manner, we may not be able to comply with the applicable covenants in our financing arrangements, and may be required to seek additional amendments or waivers under these financing arrangements, which could adversely impact our liquidity and financial condition. Further and continued determinations that there are material weaknesses in the effectiveness of the Company’s internal control over financial reporting could reduce our ability to obtain financing or could increase the cost of any financing we obtain and require additional expenditures of both money and our management’s time to comply with applicable requirements.

Any failure to implement or maintain required new or improved controls, or any difficulties we encounter in their implementation, could result in additional material weaknesses or material misstatement in our consolidated financial statements. Any new misstatement could result in a further restatement of our consolidated financial statements, cause us to fail to meet our reporting obligations, reduce our ability to obtain financing or cause investors to lose confidence in our reported financial information, leading to a decline in our stock price. We cannot assure you that we will not discover additional weaknesses in our internal control over financial reporting.

Further, we may be the subject of negative publicity focusing on the restatement of our previously issued financial results and related matters, and may be adversely impacted by negative reactions from our stockholders, creditors or others with which we do business. This negative publicity may impact our ability to attract and retain customers, employees and vendors. The occurrence of any of the foregoing could harm our business and reputation and cause the price of our securities to decline.

In addition, beginning with this 2016 Annual Report on Form 10-K, we are required to furnish a report by management, and our independent registered public accounting firm is required to provide an attestation report, on the effectiveness of our internal control over financial reporting pursuant to Section 404 of the Sarbanes-Oxley Act of 2002. As a result of the material weaknesses, our management concluded that we did not maintain effective internal control over financial reporting as of March 31, 2016. This could cause investors to lose confidence in the reliability of our financial statements and could result in a decrease in the value of our common stock. Failure to comply with the Sarbanes-Oxley Act of 2002 could potentially subject us to sanctions or investigations by the SEC, NYSE, or other regulatory authorities.

Furthermore, as we grow our business, our disclosure controls and internal controls will become more complex, and we may require significantly more resources to ensure the effectiveness of these controls. If we are unable to continue upgrading our financial and management controls, reporting systems, information technology and procedures in a timely and effective fashion, additional management and other resources may need to be devoted to assist in compliance with the disclosure and financial reporting requirements and other rules that apply to reporting companies, which could adversely affect our business, financial position and results of operations.

The ongoing remediation of the material weaknesses in our internal control over financial reporting will require us to continue to incur significant cost and expense and may require additional management time and attention, which could adversely affect our financial position, results of operations and cash flows.

We continue to incur significant costs and expenses related to the ongoing remediation of the weaknesses in our internal control over financial reporting. We have taken a number of steps, including both adding internal personnel and hiring outside consultants, and intend to continue to take appropriate and reasonable steps to

18

Table of Contents

strengthen our accounting function and reduce the risk of any future misstatements in our financial statements. For more details about the status of our remediation plan, see “Item 9A. Controls and Procedures” of this Form 10-K. To the extent these steps are not successful, we may have to incur additional time and expense, which could adversely affect our financial position and cash flows. Our management’s attention has also been, and may further be, diverted from the operation of our business in connection with the ongoing remediation of material weaknesses in our internal controls, which efforts could adversely affect our results of operations.

The restatement of our previously issued financial results has resulted in private litigation as well as an ongoing investigation by the SEC, and could result in additional litigation, government investigations and enforcement actions that could have a material adverse impact on our results of operations, financial condition, liquidity and cash flows.

We are subject to a securities class action litigation suit currently pending in the United States District Court for the Southern District of New York as a result of the restatement of our previously issued financial statements. In addition, the Company has received document subpoenas from the SEC’s Division of Enforcement pursuant to a formal investigation. Both the securities class action litigation suit and SEC investigation are further described below under “Item 3 Legal Proceedings.” We could also become subject to additional litigation or government investigations and enforcement actions arising out of our restated financial statements and delinquent Exchange Act filings.

To date our management has devoted significant time and attention related to these matters, and we may be required to devote even more time and attention to such matters in the future, and these and any additional matters that arise could have a material adverse impact on our results of operations, financial condition, liquidity and cash flows. While we cannot estimate our potential exposure in these matters at this time, we have already expended significant amounts investigating the claims underlying the class action litigation and SEC document production and expect to continue to need to expend significant amounts to defend such litigation and respond to the SEC investigation. Although we maintain insurance that may provide coverage for some or all of these expenses, and we have given notice to our insurers of the claims, there is risk that the insurers will rescind or otherwise not renew the policies, that some or all of the claims will not be covered by such policies, or that, even if covered, our ultimate liability will exceed the available insurance. For additional discussion of these matters, see “Note 14. Commitments and Contingencies — Litigation” to our audited consolidated financial statements included in “Item 8. Financial Statements and Supplementary Data”of this Form 10-K.

The New York Stock Exchange could commence procedures to delist our common stock, in the event we do not timely file all required periodic reports with the SEC, in which case the market price of our shares might decline and become more volatile and our shareholders’ ability to trade in our stock could be adversely affected.