| ||||||||

UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

For the fiscal year ended December 31 , 2023

OR

For the transition period from ________ to ________

Commission File Number | Exact name of registrant as specified in its charter, address of principal executive offices and registrant's telephone number | IRS Employer Identification Number | ||||||||||||

(561 ) 694-4000

State or other jurisdiction of incorporation or organization: Delaware

Securities registered pursuant to Section 12(b) of the Act:

Title of each class | Trading Symbol | Name of exchange on which registered | ||||||||||||

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act of 1933. Yes þ No o

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Securities Exchange Act of 1934. Yes o No þ

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months, and (2) has been subject to such filing requirements for the past 90 days. Yes þ No o

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T during the preceding 12 months. Yes þ No o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company.

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Securities Exchange Act of 1934. ¨

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☑

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Securities Exchange Act of 1934). Yes ☐ No þ

Aggregate market value of the voting and non-voting common equity of NextEra Energy Partners, LP held by non-affiliates at June 30, 2023 (based on the closing market price on the Composite Tape on June 30, 2023) was $5,330,331,140 .

Number of NextEra Energy Partners, LP common units outstanding at January 31, 2024: 93,431,516

DOCUMENTS INCORPORATED BY REFERENCE

__________________________________

Portions of NextEra Energy Partners, LP's Proxy Statement for the 2024 Annual Meeting of Unitholders are incorporated by reference in Part III hereof.

DEFINITIONS

Acronyms and defined terms used in the text include the following:

| Term | Meaning | ||||

| ASA | administrative services agreement | ||||

| BLM | U.S. Bureau of Land Management | ||||

| CITC | convertible investment tax credit | ||||

| Code | U.S. Internal Revenue Code of 1986, as amended | ||||

| CSCS agreement | amended and restated cash sweep and credit support agreement | ||||

| FERC | U.S. Federal Energy Regulatory Commission | ||||

| IDR fee | certain payments from NEP OpCo to NEE Management as a component of the MSA which are based on the achievement by NEP OpCo of certain target quarterly distribution levels to its unitholders | ||||

| IPP | independent power producer | ||||

| ITC | investment tax credit | ||||

limited partner interest in NEP OpCo | limited partner interest in NEP OpCo's common units | ||||

| management sub-contract | management services subcontract between NEE Management and NEER | ||||

| Management's Discussion | Item 7. Management's Discussion and Analysis of Financial Condition and Results of Operations | ||||

| MSA | Fourth Amended and Restated Management Services Agreement among NEP, NEE Management, NEP OpCo and NEP OpCo GP | ||||

| MW | megawatt(s) | ||||

| MWh | megawatt-hour(s) | ||||

| NEE | NextEra Energy, Inc. | ||||

| NEECH | NextEra Energy Capital Holdings, Inc. | ||||

| NEE Equity | NextEra Energy Equity Partners, LP | ||||

| NEE Management | NextEra Energy Management Partners, LP | ||||

| NEER | NextEra Energy Resources, LLC | ||||

| NEP | NextEra Energy Partners, LP | ||||

| NEP GP | NextEra Energy Partners GP, Inc. | ||||

| NEP OpCo | NextEra Energy Operating Partners, LP | ||||

| NEP OpCo GP | NextEra Energy Operating Partners GP, LLC | ||||

| NEP OpCo ROFR assets | all assets owned or hereafter acquired by NEP OpCo or its subsidiaries | ||||

| NERC | North American Electric Reliability Corporation | ||||

| Note __ | Note __ to consolidated financial statements | ||||

| NYSE | New York Stock Exchange | ||||

| O&M | operations and maintenance | ||||

| PPA | power purchase agreement | ||||

| PTC | production tax credit | ||||

| renewable energy tax credits | production tax credits and investment tax credits collectively | ||||

| ROFR | right of first refusal | ||||

| RPS | renewable portfolio standards | ||||

| SEC | U.S. Securities and Exchange Commission | ||||

| the board | the board of directors of NEP | ||||

| U.S. | United States of America | ||||

Each of NEP and NEP OpCo has subsidiaries and affiliates with names that may include NextEra Energy, NextEra Energy Partners and similar references. For convenience and simplicity, in this report, the terms NEP and NEP OpCo are sometimes used as abbreviated references to specific subsidiaries, affiliates or groups of subsidiaries or affiliates. The precise meaning depends on the context. Discussions of NEP's ownership of subsidiaries and projects refers to its controlling interest in the general partner of NEP OpCo and NEP's indirect interest in and control over the subsidiaries of NEP OpCo. See Note 1 for a description of the noncontrolling interest in NEP OpCo. References to NEP's projects generally include NEP's consolidated subsidiaries and the projects in which NEP has equity method investments. References to NEP's pipeline investment refers to its equity method investment in contracted natural gas assets.

NEE, NEECH and NEER each has subsidiaries and affiliates with names that may include NextEra Energy, NextEra Energy Resources, NextEra and similar references. For convenience and simplicity, in this report the terms NEE, NEECH and NEER are sometimes used as abbreviated references to specific subsidiaries, affiliates or groups of subsidiaries or affiliates. The precise meaning depends on the context.

2

TABLE OF CONTENTS

| Page No. | ||||||||

FORWARD-LOOKING STATEMENTS

This report includes forward-looking statements within the meaning of the federal securities laws. Any statements that express, or involve discussions as to, expectations, beliefs, plans, objectives, assumptions, strategies, future events or performance (often, but not always, through the use of words or phrases such as may result, are expected to, will continue, anticipate, believe, will, could, should, would, estimated, may, plan, potential, future, projection, goals, target, outlook, predict and intend or words of similar meaning) are not statements of historical facts and may be forward looking. Forward-looking statements involve estimates, assumptions and uncertainties. Accordingly, any such statements are qualified in their entirety by reference to, and are accompanied by, important factors included in Part I, Item 1A. Risk Factors (in addition to any assumptions and other factors referred to specifically in connection with such forward-looking statements) that could have a significant impact on NEP's operations and financial results, and could cause NEP's actual results to differ materially from those contained or implied in forward-looking statements made by or on behalf of NEP in this Form 10-K, in presentations, on its website, in response to questions or otherwise.

Any forward-looking statement speaks only as of the date on which such statement is made, and NEP undertakes no obligation to update any forward-looking statement to reflect events or circumstances, including, but not limited to, unanticipated events, after the date on which such statement is made, unless otherwise required by law. New factors emerge from time to time and it is not possible for management to predict all of such factors, nor can it assess the impact of each such factor on the business or the extent to which any factor, or combination of factors, may cause actual results to differ materially from those contained or implied in any forward-looking statement.

3

PART I

Item 1. Business

NEP is a growth-oriented limited partnership with a strategy that emphasizes acquiring, managing and owning contracted clean energy assets with stable long-term cash flows with a focus on renewable energy projects. At December 31, 2023, NEP owned a controlling, non-economic general partner interest and a 48.6% limited partner interest in NEP OpCo. Through NEP OpCo, NEP owns, or has a partial ownership interest in, a portfolio of contracted renewable energy assets consisting of wind, solar and solar-plus-storage projects and a stand-alone battery storage project, as well as contracted natural gas pipeline assets (pipeline investment).

NEP expects to take advantage of trends in the North American energy industry, including the addition of clean energy projects as aging or uneconomic generation facilities are phased out, increased demand from utilities for renewable energy to meet state RPS requirements and improving competitiveness of energy generated from wind and solar projects relative to energy generated using other fuels. NEP plans to focus on high-quality, long-lived projects operating under long-term contracts that are expected to produce stable long-term cash flows and organic growth through wind turbine repowering opportunities across its portfolio. NEP believes its cash flow profile, geographic, technological and resource diversity, operational excellence and cost-efficient business model provide NEP with a significant competitive advantage and enable NEP to execute its business strategy.

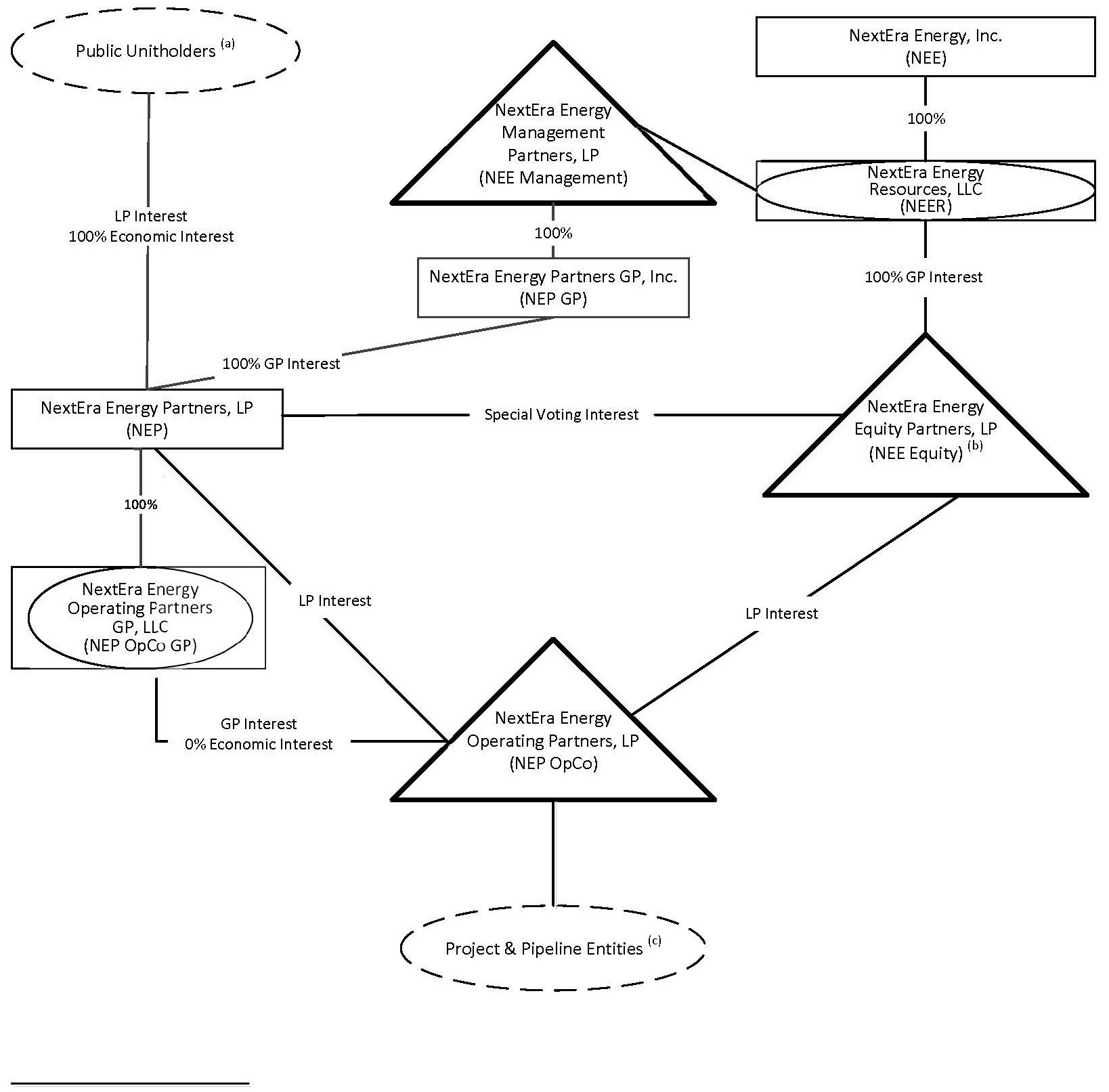

The following diagram depicts NEP's simplified ownership structure at December 31, 2023:

(a) At December 31, 2023, NEE owns 2,377,882 NEP common units.

(b) At December 31, 2023, NEE Equity owns approximately 51.4% of NEP OpCo's common units representing limited partnership interests and

100% of NEP OpCo's Class B partnership interests. NEE Equity may tender its NEP OpCo common units and in exchange receive NEP common units on a one-for-one basis, or the value of such common units in cash, subject to the terms of an exchange agreement.

(c) At December 31, 2023, certain project entities and the pipeline investment are subject to noncontrolling interests. See Note 2 – Noncontrolling Interests.

4

Renewable energy projects – At December 31, 2023, NEP owned interests in a portfolio of clean, contracted renewable energy projects located in 31 states as summarized below:

| NEP Acquisition/Investment Date | Technology | Net MW(a) | Contract Expiration | |||||||||||||||||

| 2014 | Solar Wind | 250 492 | 2030 – 2039 | |||||||||||||||||

| 2015 | Solar Wind | 20 851 | (b) | 2026 – 2041 | ||||||||||||||||

| 2016 | Solar Wind | 132 584 | 2033 – 2040 | |||||||||||||||||

| 2017 | Solar Wind | 143 798 | 2030 – 2046 | |||||||||||||||||

| 2018 | Solar Wind | 20 1,368 | 2031 – 2042 | |||||||||||||||||

| 2019 | Solar Wind | 191 420 | 2030 – 2042 | |||||||||||||||||

| 2020 | Battery Storage Solar Wind | 30 219 280 | 2034 – 2045 | |||||||||||||||||

| 2021 | Battery Storage Solar Wind | 58 558 1,784 | 2025 – 2051 | |||||||||||||||||

| 2022 | Battery Storage Solar Wind | 186 61 931 | 2032 – 2043 | |||||||||||||||||

| 2023 | Solar Wind | 196 546 | 2036 – 2046 | |||||||||||||||||

| 10,118 | (c)(d) | |||||||||||||||||||

____________________

(a) MWs reflect NEP's net ownership in the renewable energy project capacity based on respective ownership interests. NEP has indirect equity method investments in projects with a net generating capacity of approximately 862 MW with ownership interests ranging from 33.3% to 50%. Additionally, NEP has indirect controlling ownership interests ranging from 49% to 67% in projects with a net generation capacity of approximately 2,087 MW and battery storage capacity of 244 MW. See Note 2 – Investments in Unconsolidated Entities and – Noncontrolling Interests.

(b) Reflects the sale of a 62 MW wind project in January 2023. See Note 2 – Disposal of Wind Project.

(c) Third-party investors own noncontrolling Class B membership interests in the NEP subsidiaries that own interests in projects with net generating capacity of approximately 5,622 MW and battery storage capacity of 120 MW. Third-party investors own differential membership interests in projects with net generating capacity of approximately 6,494 MW and battery storage capacity of 274 MW. See Note 2 – Noncontrolling Interests, Note 11 and Note 14 – Class B Noncontrolling Interests. Projects with net generating capacity of approximately 1,539 MW are encumbered by liens against their assets securing various financings.

(d) At December 31, 2023, NEP owns an approximately 50% non-economic ownership interest in three NEER solar projects with a total generating capacity of 277 MW and battery storage capacity of 230 MW. All equity in earnings of these non-economic ownership interests is allocated to net income attributable to noncontrolling interests. See Note 2 – Investments in Unconsolidated Entities.

During 2023, NEP generated approximately 25.8 million MWh and 3.8 million MWh from wind and solar generating facilities, respectively. During 2022, NEP generated approximately 23.8 million MWh and 3.4 million MWh from wind and solar generating facilities, respectively.

Pipeline investment – At December 31, 2023, through its ownership interest in Meade Pipeline Co, LLC, NEP has an indirect equity method investment in the Central Penn Line (CPL), natural gas pipeline assets in Pennsylvania with 191 miles of pipeline with 30 inch and 42 inch diameter pipes which is fully contracted with contract expirations between 2033 and 2041. NEP's net ownership interest represents an approximately 39% aggregate ownership interest in the CPL and net capacity of 0.73 billion cubic feet per day. In December 2023, NEP sold its interests in a portfolio of seven natural gas pipelines assets in Texas (Texas pipelines). See Note 4.

5

The following map shows NEP's ownership interests in clean energy projects in operation, excluding its non-economic ownership interests, and NEP's pipeline investment.

Each of the renewable energy projects sells substantially all of its output and related renewable energy attributes pursuant to long-term, fixed price PPAs to various counterparties. The pipeline assets in which NEP is invested primarily operate under long-term firm transportation contracts under which counterparties pay for a fixed amount of capacity that is reserved by the counterparties and also generate revenues based on the volume of natural gas transported on the pipeline. In 2023, NEP derived approximately 14% of its consolidated revenues from its contracts with Pacific Gas and Electric Company. In 2023, NEP also derived approximately 11% of its consolidated revenues from its contracts with Mex Gas Supply S.L., which was related to the Texas pipelines (see Note 4). See Item 1A for a discussion of risks related to NEP's counterparties.

NEP, NEP OpCo and NEP OpCo GP are parties to the MSA with an indirect wholly owned subsidiary of NEE, under which operational, management and administrative services are provided to NEP under the direction of the board, including managing NEP’s day-to-day affairs and providing individuals to act as NEP’s executive officers, in addition to those services that are provided under O&M agreements and ASAs between NEER subsidiaries and NEP subsidiaries. NEP OpCo pays NEE an annual management fee. See Note 15 – Management Services Agreement.

NEP and NEP OpCo are parties to a ROFR agreement with NEER granting NEER and its subsidiaries (other than NEP OpCo and its subsidiaries) a right of first refusal on any proposed sale of any NEP OpCo ROFR assets. Pursuant to the terms of the ROFR agreement, prior to engaging in any negotiation regarding any sale of a NEP OpCo ROFR asset, NEP OpCo must first negotiate for 30 days with NEER to attempt to reach an agreement on a sale of such asset to NEER or any of its subsidiaries. If an agreement is not reached within the initial 30-day period, NEP OpCo will be able to negotiate with any third party for the sale of such asset for a 30-day period. Prior to accepting any third-party offer, NEP OpCo will be required to restart negotiations with NEER for the next 30 days and will not be permitted to sell the applicable asset to the third party making the offer if NEER agrees to terms substantially consistent with those proposed by such third party. If, by the end of the 30-day period, NEER and NEP OpCo have not reached an agreement, NEP OpCo will have the right to sell such asset to such third party within 30 days.

6

INDUSTRY OVERVIEW

Renewable Energy Industry

Growth in renewable energy is largely attributable to the increasing cost competitiveness of renewable energy driven primarily by government incentives, RPS, improving technology and declining installation costs and the impact of environmental rules and regulations on other types of generation.

U.S. federal, state and local governments have established various incentives to support the development of renewable energy projects. These incentives make the development of renewable energy projects more competitive by providing accelerated depreciation, tax credits or grants for a portion of the development costs, decreasing the costs associated with developing such projects or creating demand for renewable energy assets through RPS programs. In addition, RPS provide incentives to utilities to contract for energy generated from renewable energy providers.

Continuous improvements in renewable energy technology have resulted in wind and solar energy generation becoming the lowest cost energy generation technologies in many regions in the U.S. The improvements in these technologies, including taller wind towers, longer wind turbine blades, improved solar cell production and more efficient energy conversion equipment, allow the renewable energy projects to more efficiently capture resource and produce more energy which is expected to lead to continued growth in the renewable energy industry. Additionally, combining wind and solar energy generation facilities with battery storage projects allows for the utilization of energy stored when the renewable resource is not as strong and alleviates congestion.

Policy Incentives

Policy incentives in the U.S. have the effect of making the development of renewable energy projects more competitive by providing credits for a portion of the development costs or by providing favorable contract prices. A loss of or reduction in such incentives could decrease the attractiveness of renewable energy projects to developers, including NEE, which could reduce NEP's future acquisition opportunities. Such a loss or reduction of incentives could also reduce NEP's willingness to pursue or develop certain renewable energy projects, including wind turbine repowerings, due to higher operating costs or decreased revenues.

U.S. federal, state and local governments have established various incentives to support the development of renewable energy projects. These incentives include accelerated tax depreciation, PTCs, ITCs, cash grants, tax abatements and RPS programs. Pursuant to the U.S. federal Modified Accelerated Cost Recovery System (MACRS), wind and solar generation facilities are depreciated for tax purposes over a five-year period even though the useful life of such facilities is generally much longer than five years.

Owners of wind and solar facilities are eligible to claim an income tax credit (the PTC, or an ITC in lieu of the PTC) upon initially achieving commercial operation. This incentive was created under the Energy Policy Act of 1992 and has been extended several times for wind (the previous PTC for solar expired in 2006). The Inflation Reduction Act of 2022 (IRA) expanded the PTC to include solar generation facilities and extended the 100% PTC and the 30% ITC to wind and solar generation facilities that start construction before the later of 2034 or the end of the calendar year following the year in which greenhouse gas emissions from U.S. electric generation are reduced by 75% from 2022 levels (phaseout). Accordingly, owners of wind and solar generation facilities placed in service in 2022 or later are eligible to claim a PTC (or an ITC in lieu of the PTC) upon initially achieving commercial operation. The PTC is determined based on the amount of electricity produced by the facility during the first ten years of commercial operation. Alternatively, an ITC equal to 30% of the cost of the facility may be claimed in lieu of the PTC. A facility must also meet certain labor requirements to qualify for the 100% PTC or 30% ITC rate or construction must have started on the facility before January 29, 2023. In addition, the PTC is increased by 10% and the ITC rate is increased by 10 percentage points for facilities that satisfy certain tax credit enhancement requirements. Retrofitted wind and solar generation facilities may qualify for a PTC or an ITC if the cost basis of the new investment is at least 80% of the retrofitted facility’s total fair value.

In addition, the IRA expanded the 30% ITC to include storage projects placed in service after 2022 (previously, such projects qualified only if they were connected to and charged by a renewable generation facility that claimed the ITC), subject to the phaseout and certain other requirements. In addition, storage projects claiming an ITC are eligible for a 10 percentage point increase in the ITC rate if the facilities satisfy certain tax credit enhancement requirements.

For taxable years beginning after 2022, renewable energy tax credits generated during the year can be transferred to an unrelated purchaser for cash, providing an additional path, along with sales of differential membership interests, for developers to monetize the value of the renewable energy tax credits.

RPS, currently in place in certain states, require electricity providers in the state to meet a certain percentage of their retail sales with energy from renewable sources. Additionally, other states in the U.S. have set renewable energy goals to reduce greenhouse gas emissions from historic levels. NEP believes that these standards and goals will create incremental demand for renewable energy in the future.

7

BUSINESS STRATEGY

NEP's primary business objective is to deliver cash distributions to common unitholders which it plans to grow over time through accretively acquiring ownership interests in contracted clean energy projects, with a focus on renewable energy projects, from NEER or third parties and wind turbine repowering at existing projects. To achieve this objective, NEP intends to execute the following business strategy:

•Focus on contracted clean energy projects. NEP intends to focus on long-term contracted clean energy projects with newer and more reliable technology, lower operating costs and relatively stable cash flows, subject to seasonal variances, consistent with the characteristics of its portfolio.

•Focus on North America. NEP intends to focus its investments in North America, where it believes industry trends present significant opportunities to acquire contracted clean energy projects in diverse regions and favorable locations and repower existing wind projects. By focusing on North America, NEP believes it will be able to take advantage of NEE’s long-standing industry relationships, knowledge and experience.

•Maintain a sound capital structure and financial flexibility. NEP and its subsidiaries have utilized various financing structures including limited-recourse project-level financings, the sale of differential membership interests and equity interests in certain subsidiaries, preferred units, convertible senior unsecured notes and senior unsecured notes, as well as revolving credit facilities and term loans. NEP intends to continually seek the most competitive cost of capital to finance growth associated with future acquisitions and wind turbine repowerings, with a focus on maintaining a positive spread between its cost to finance an investment or acquisition and the value of the incremental cash flows. Additionally, including for its refinancing, NEP seeks to limit recourse, optimize leverage, manage liquidity, hedge exposure and extend maturities to, among other things, maximize cash distributions to common unitholders.

•Take advantage of NEER’s operational excellence to maintain the value of the projects in NEP's portfolio. NEER provides O&M, administrative and management services to NEP's projects pursuant to the MSA and other agreements. Through these agreements, NEP benefits from the operational expertise that NEER currently provides across its entire portfolio. NEP expects that these services will maximize the operational efficiencies of its portfolio.

•Grow NEP's business and deliver cash distributions through selective acquisitions of ownership interests in operating projects or projects under construction and wind turbine repowering at existing projects. NEP intends to focus on acquiring ownership interests in clean energy projects in operation or under construction, maintaining a disciplined investment approach, taking advantage of opportunities to acquire ownership interests in additional projects from NEER and third parties in the future, and identifying wind turbine repowering opportunities at existing projects.

COMPETITION

Wholesale power generation is a capital-intensive, commodity-driven business with numerous industry participants. While NEP's renewable energy projects are currently contracted, NEP may compete in the future primarily on the bases of price and terms, but also believes the green attributes of NEP's renewable energy generation assets, among other strengths discussed below, are competitive advantages. Wholesale power generation is a regional business that is highly fragmented relative to many other commodity industries and diverse in terms of industry structure. As such, there is a wide variation in terms of the capabilities, resources, nature and identity of the companies NEP competes with depending on the market. In wholesale markets, customers' needs are met through a variety of means, including long-term bilateral contracts, standardized bilateral products such as full requirements service and customized supply and risk management services.

In addition, NEP competes with other companies to acquire well-developed projects with projected stable cash flows. NEP believes its primary competitors for opportunities in North America are regulated utility holding companies, developers, IPPs, pension funds and private equity funds.

NEP's pipeline investment faces competition with respect to retaining and obtaining firm transportation contracts and competes with other pipeline companies based on location, capacity, price and reliability.

NEP believes that it is well-positioned to execute its strategy and deliver cash distributions to its common unitholders over the long term based on the following competitive strengths:

NEE management and operational expertise. NEP believes it benefits from NEE’s experience, operational excellence and cost-efficient operations. Through the MSA and other agreements with NEE and its subsidiaries, NEP's projects will receive the same benefits and expertise that NEE currently provides across its entire portfolio.

Repowering opportunities. NEP is focused on executing wind turbine repowering opportunities across its portfolio and expects that these investments will allow NEP to refresh and enhance the performance of the wind turbine equipment and start a new 10 years of PTCs, collectively resulting in attractive returns.

Contracted projects with stable cash flows. The contracted nature of NEP's portfolio of projects supports expected stable long-term cash flows. The renewable energy projects in NEP's portfolio are contracted under long-term contracts that generally provide for fixed price payments over the contract term. The renewable energy projects have a total weighted average remaining contract term of approximately 13 years at December 31, 2023 based on expected contributions to cash available for distribution.

8

Geographic and resource diversification. NEP's portfolio is geographically diverse across the U.S. In addition, NEP's portfolio consists of wind and solar generation facilities, solar-plus-storage projects, a stand-alone battery storage project and an investment in pipeline assets. A diverse portfolio tends to reduce the magnitude of individual project or regional deviations from historical resource conditions, providing a more stable stream of cash flows over the long term than a non-diversified portfolio. In addition, NEP believes the geographic diversity of its portfolio helps minimize the impact of adverse regulatory conditions in particular jurisdictions.

REGULATION

NEP's projects and the pipeline assets underlying its pipeline investment are subject to regulation by a number of U.S. federal, state and other organizations, including, but not limited to, the following:

•the FERC, which oversees the acquisition and disposition of generation, transmission and other facilities, transmission of electricity and natural gas in interstate commerce and wholesale purchases and sales of electric energy, among other things;

•the NERC, which, through its regional entities, establishes and enforces mandatory reliability standards, subject to approval by the FERC, to ensure the reliability of the U.S. electric transmission and generation system and to prevent major system blackouts;

•the Environmental Protection Agency (EPA), which has the responsibility to maintain and enforce national standards under a variety of environmental laws. The EPA also works with industries and all levels of government, including federal and state governments, in a wide variety of voluntary pollution prevention programs and energy conservation efforts;

•various agencies in Pennsylvania, which oversee safety, environmental and certain aspects of rates and transportation related to the pipeline project in which NEP is invested; and

•the Pipeline and Hazardous Materials Safety Administration, which, among other things, oversees the safety of natural gas pipelines.

In addition, NEP is subject to environmental laws and regulations described in the Environmental Matters section below.

ENVIRONMENTAL MATTERS

NEP is subject to environmental laws and regulations, including extensive federal, state and local environmental statutes, rules and regulations relating to, among others, air quality, water quality and usage, waste management, wildlife protection and historical resources, for the ongoing operations, siting and construction of its facilities. The environmental laws in the U.S., including, among others, the Endangered Species Act (ESA), the Migratory Bird Treaty Act, and the Bald and Golden Eagle Protection Act (BGEPA), provide for the protection of numerous species, including endangered species and/or their habitats, migratory birds, bats and eagles. In 2023, the U.S. Fish and Wildlife Service listed the northern long-eared bat as endangered, with two more bat species expected to be listed in 2024 and 2025. Complying with these environmental laws and regulations could result in, among other things, changes in the design and operation of, and additional costs associated with, existing facilities and changes or delays in the location, design, construction and operation of any new facilities and failure to comply could result in fines, penalties, criminal sanctions or injunctions.

HUMAN CAPITAL

NEP does not have any employees and relies solely on employees of affiliates of the manager under the MSA, including employees of NEE and NEER, to serve as officers of NEP. See further discussion of the MSA and other payments to NEE in Note 15.

WEBSITE ACCESS TO SEC FILINGS

NEP makes its SEC filings, including the annual report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8‑K, and any amendments to those reports, available free of charge on NEP's internet website, www.nexteraenergypartners.com, as soon as reasonably practicable after those documents are electronically filed with or furnished to the SEC. The information and materials available on NEP's website (or any of its subsidiaries' or affiliates' websites) are not incorporated by reference into this Form 10-K.

9

Item 1A. Risk Factors

Limited partnerships and limited partnership interests are inherently different than corporations and shares of capital stock of a corporation, although many of the business risks to which NEP is subject are similar to those that would be faced by a corporation engaged in similar businesses and NEP has elected to be treated as a corporation for U.S. federal income tax purposes. If any of the following risks were to occur, and whether or not expressly stated with respect to any particular risk factor, NEP's business, financial condition, results of operations and ability to grow its business and make cash distributions to its unitholders could be materially and adversely affected. In that case, NEP may not be able to pay distributions to its unitholders, the trading price of its common units could decline and investors could lose all or part of their investment in NEP.

Performance Risks

NEP's ability to make cash distributions to its unitholders is affected by the performance of its renewable energy projects which could be impacted by wind and solar conditions and in certain circumstances by market prices.

The output from NEP's wind projects can vary greatly as local wind speeds and other conditions vary. Similarly, the amount of energy that a solar project is able to produce depends on several factors, including the amount of solar energy that reaches its solar panels. Wind turbine or solar panel placement, interference from nearby wind projects or other structures and the effects of vegetation, snow, ice, land use and terrain also affect the amount of energy that NEP's wind and solar projects generate. In certain circumstances, NEP is exposed to the inherent market price risk created by the differences in pricing between commodity selling and purchasing locations known as basis risk. The failure of some or all of NEP's projects to perform according to NEP's expectations as well as basis risk could have a material adverse effect on its business, financial condition, results of operations and ability to grow its business and make cash distributions to its unitholders.

Operation and maintenance of renewable energy projects and pipelines involve significant risks that could result in unplanned power outages, reduced output or capacity, property damage, personal injury or loss of life.

There are risks associated with the operation of NEP's renewable energy projects and pipelines, including:

•breakdown or failure, including, but not limited to, leaks, fires, explosions, mechanical problems or other major events, of, or damage to, turbines, blades, blade attachments, solar panels, mirrors, pipelines, batteries and other equipment, which could reduce a project’s energy output or a pipeline's ability to transport natural gas at expected levels or result in significant property damage, environmental pollution, personal injury or loss of life;

•catastrophic events, such as fires, earthquakes, hurricanes, severe weather, tornadoes, ice and hail storms, other meteorological conditions, landslides and other similar events beyond NEP's control, which could severely damage or destroy all or a part of a project, pipeline or interconnection and transmission facilities, reduce its energy output or capacity, or result in property damage, personal injury or loss of life;

•technical performance below expected levels, including, but not limited to, the failure of wind turbines, solar panels, mirrors, batteries and other equipment to produce energy as expected due to incorrect measures of expected performance provided by equipment suppliers;

•interference from nearby wind projects or other structures;

•increases in the cost of operating the projects;

•operator, contractor or supplier error or failure to perform or to fulfill any warranty obligations;

•serial design, manufacturing or other defects, which may not be covered by warranty;

•extended events, including, but not limited to, force majeure under certain PPAs that may give rise to a termination right of the customer under such a PPA (renewable energy counterparty);

•failure to comply with permits and the inability to renew or replace permits that have expired or terminated;

•the inability to operate within limitations that may be imposed by current or future governmental permits;

•replacements for failed equipment, which may need to meet new interconnection standards or require system impact studies and compliance that may be difficult or expensive to achieve;

•land use, environmental or other regulatory requirements;

•risks associated with potential harm to wildlife;

•disputes with the BLM, other owners of land on which NEP's projects are located or nearby landowners;

•changes in laws, regulations, policies and treaties;

•government or utility exercise of eminent domain power or similar events;

•existence of liens, encumbrances and other imperfections in title affecting real estate interests; and

•insufficient insurance, warranties or performance guarantees to cover any or all lost revenues or increased expenses from the foregoing.

These and other factors could require the shut down of NEP's renewable energy projects or pipeline investment. For renewable energy projects or pipelines located near populated areas, including, but not limited to, residential areas, commercial business centers, industrial sites and other public gathering areas, or areas more prone to wildfires, the level of damage resulting from certain of these risks could be greater.

These factors could also reduce the useful lives of and degrade equipment, interconnection facilities and transmission facilities, and materially increase maintenance and other costs. Unanticipated costs associated with maintaining or repairing NEP's projects and pipeline investment may reduce profitability. In addition, replacement and spare parts for solar panels, wind turbines, batteries and other key equipment may be difficult or costly to acquire or may be unavailable.

Such events or actions could significantly decrease or eliminate the revenues of a project or pipeline, significantly increase its operating costs, cause a default under NEP's financing agreements or give rise to damages or penalties payable to a PPA or transportation agreement counterparty, another contractual counterparty, a governmental authority or other third parties or cause defaults under related contracts or permits. Any of these events could have a material adverse effect on NEP's business, financial condition, results of operations and ability to grow its business and make cash distributions to its unitholders.

NEP's business, financial condition, results of operations and prospects can be materially adversely affected by weather conditions and related impacts, including, but not limited to, the impact of severe weather.

Weather conditions directly influence the demand for electricity, natural gas and other fuels and affect the price of energy and energy-related commodities. In addition, severe weather and natural disasters, such as hurricanes, floods, tornadoes, droughts, extreme temperatures, icing events, wildfires, severe convective storms and earthquakes, can be destructive and cause power outages, personal injury and property damage, reduce revenue, affect the availability of fuel and water and require NEP to incur additional costs to, for example, restore service and repair damaged facilities, obtain replacement power, access available financing sources, obtain insurance, pay for any associated injuries and damages and fund any associated legal matters and compliance penalties. Furthermore, NEP's physical plants could be placed at greater risk of damage should changes in the global climate produce unusual

10

variations in temperature and weather patterns, resulting in more intense, frequent and extreme weather events and abnormal levels of precipitation. A disruption or failure of electric generation, transmission or distribution systems or natural gas production, transmission, storage or distribution systems in the event of a hurricane, tornado or other severe weather event, or otherwise, could prevent NEP from operating its business in the normal course and could result in any of the adverse consequences described above. Additionally, the actions taken to address the potential for severe weather such as additional winterizing of critical equipment and infrastructure, modifying or alternating plant operations and expanding load shedding options could result in significant increases in costs. Any of the foregoing could have a material adverse effect on NEP's business, financial condition, results of operations and ability to grow its business and make cash distributions to its unitholders.

Changes in weather can also affect the level of wind and solar resource available, and thus the production of electricity, at NEP's power generating facilities. Because the levels of wind and solar resources are variable and difficult to predict, NEP’s results of operations for individual wind and solar facilities specifically, and NEP's results of operations generally, may vary significantly from period to period, depending on the level of available resources. To the extent that resources are not available at planned levels, the financial results from these facilities may be less than expected.

NEP depends on certain of the renewable energy projects and the investment in pipeline assets in its portfolio for a substantial portion of its anticipated cash flows.

NEP depends on certain of the renewable energy projects and the investment in pipeline assets in its portfolio for a substantial portion of its anticipated cash flows. Consequently, the impairment or loss of any one or more of those projects or the pipeline investment could materially and, depending on the relative size of the affected projects or pipeline investment, disproportionately reduce NEP’s cash flows and, as a result, have a material adverse effect on NEP's business, financial condition, results of operations and ability to grow its business and make cash distributions to its unitholders.

The repowering of renewable energy projects requires up-front capital expenditures and could expose NEP to project development risks.

NEP from time to time pursues the repowering of renewable energy projects. Repowering of renewable energy projects involves regulatory, environmental, construction, safety, political and legal uncertainties and may require the expenditure of significant amounts of capital. These projects may not be completed on schedule, at the budgeted cost or at all. There may be cost overruns and construction difficulties. In addition, NEP may agree to pay liquidated damages to counterparties if a project does not achieve commercial operations before a specified date that the parties may agree upon in advance. Any cost overruns NEP experiences or liquidated damages NEP pays could have a material adverse effect on NEP's business, financial condition, results of operations and ability to grow its business and make cash distributions to its unitholders. In addition, NEP may choose to finance all or a portion of the development costs of any repowering project through the sale of additional common units or securities convertible into, or settleable with, common units, which could result in dilution to NEP’s unitholders, or through other financings which could result in additional expense. Any such financings could involve the issuance of securities or indebtedness that could be senior to the common units upon liquidation. The construction related to repowering projects may occur over an extended period of time and NEP may not receive increases in revenues until the projects are placed in service, or at all. Accordingly, NEP's repowering efforts may not result in additional long-term contracted revenue streams that increase, and could decrease, the amount of cash available to execute NEP's business plan and make cash distributions to its unitholders.

Geopolitical factors, terrorist acts, cyberattacks or other similar events could impact NEP's projects, pipeline investment or surrounding areas and adversely affect its business.

Terrorists have attacked energy assets such as substations and related infrastructure in the past and may attack them in the future. Any attacks on NEP’s projects, pipeline investment or the facilities of third parties on which its projects or pipeline investment rely could severely damage such projects or the pipeline investment, disrupt business operations, result in loss of service to customers and require significant time and expense to repair. Projects and pipeline investment in NEP's portfolio, as well as projects it may acquire and the transmission and other facilities of third parties on which NEP's projects rely, may also be targets of terrorist acts and affected by responses to terrorist acts, each of which could fully or partially disrupt the ability of NEP's projects or pipeline investment to operate.

Cyberattacks, including, but not limited to, those targeting information systems or electronic control systems used to operate NEP's energy projects (including, but not limited to, generation transmission tie lines) and the transmission and other facilities of third parties on which NEP's projects rely, could severely disrupt business operations and result in loss of service to customers and significant expense to repair security breaches or system damage. In addition, the advancement of artificial intelligence has given rise to added vulnerabilities and potential entry points for cyberattacks. As cyber incidents continue to evolve, NEP may be required to expend additional resources to continue to modify or enhance NEP's protective measures or to investigate and remediate any vulnerability to cyber incidents.

To the extent geopolitical factors, terrorist acts, cyberattacks or other similar events equate to a force majeure event under NEP's PPAs, the renewable energy counterparty may terminate such PPAs if such a force majeure event continues for a specified period. As a result, a terrorist act, cyberattack or other similar event, and governmental actions in response, could significantly decrease revenues or result in significant reconstruction or remediation costs, significant fines and penalties and reputational damage, any of which could have a material adverse effect on NEP's business, financial condition, results of operations and ability to grow its business and make cash distributions to its unitholders.

The ability of NEP to obtain insurance and the terms of any available insurance coverage could be materially adversely affected by international, national, state or local events and company-specific events, as well as the financial condition of insurers. NEP's insurance coverage does not provide protection against all significant losses.

NEP shares insurance coverage with NEE and its affiliates, for which NEP reimburses NEE. NEE currently maintains liability insurance coverage for itself and its affiliates, including NEP, which covers legal and contractual liabilities arising out of bodily injury, personal injury or property damage to third parties. NEE also maintains coverage for itself and its affiliates, including NEP, for physical damage to assets and resulting business interruption, including, but not limited to, damage caused by terrorist acts. However, such policies do not cover all potential losses and coverage is not always available in the insurance market on commercially reasonable terms. To the extent NEE or any of its affiliates experience covered losses under the insurance policies, the limit of NEP's coverage for potential losses may be decreased. NEE may also reduce or eliminate such coverage at any time. NEP may not be able to maintain or obtain insurance of the type and amount NEP desires at reasonable rates and NEP may elect to self-insure some of its wind and solar projects. The ability of NEE to obtain insurance and the terms of any available insurance coverage could be materially adversely affected by international, national, state or local events and company-specific events, as well as the financial condition of insurers. If NEP cannot or does not obtain insurance coverage, NEP may be required to pay costs associated with adverse future events. A loss for which NEP is not fully insured could have a material adverse effect on NEP's business, financial condition, results of operations and ability to grow its business and make cash distributions to its unitholders.

NEP relies on interconnection and transmission and other pipeline facilities of third parties to deliver energy from its renewable energy projects and to transport natural gas to and from its pipeline investment. If these facilities become unavailable, NEP's projects and pipeline investment may not be able to operate or deliver energy or may become partially or fully unavailable to transport natural gas.

11

NEP depends on interconnection and transmission facilities owned and operated by third parties to deliver energy from its wind and solar projects. In addition, some of the renewable energy projects in NEP's portfolio share essential facilities, including interconnection and transmission facilities, with projects that are owned by other affiliates of NEE. If the interconnection or transmission arrangement for a project is terminated, NEP may not be able to replace it on similar terms to the existing arrangement, or at all, or NEP may experience significant delays or costs in connection with such replacement. NEP also depends upon third-party pipelines and other facilities that transport natural gas to and from its pipeline investment. Because NEP does not own these third-party pipelines or facilities, their continuing operations are not within its control. The unavailability of interconnection, transmission, pipeline or shared facilities could adversely affect the operation of NEP's projects and pipeline investment and the revenues received, which could have a material adverse effect on NEP's business, financial condition, results of operations and ability to grow its business and make cash distributions to its unitholders.

NEP's business is subject to liabilities and operating restrictions arising from environmental, health and safety laws and regulations, compliance with which may require significant capital expenditures, increase NEP’s cost of operations and affect or limit its business plans.

NEP's projects and pipeline investment are subject to numerous environmental, health and safety laws, regulations, guidelines, policies, directives and other requirements governing or relating to the protection of avian, bats and other wildlife; the storage, handling, use and transportation of natural gas as well as other hazardous or toxic substances and other regulated substances, materials, and/or chemicals; air emissions, water quality, releases of hazardous materials into the environment and the prevention of and responses to releases of hazardous materials into soil and groundwater; federal, state or local land use, zoning, building and transportation laws and requirements; the presence or discovery of archaeological, religious or cultural resources at or near NEP's projects or pipeline investment; and the protection of workers’ health and safety, among other things. If NEP's projects or pipeline investment do not comply with such laws, regulations, environmental licenses, permits, inspections or other requirements, NEP may be required to incur significant expenditures, pay penalties or fines, or curtail or cease operations of the affected projects or pipeline investment and may also be subject to criminal sanctions or injunctions, such as restrictions on how it operates its facilities. NEP's projects and pipeline investment also carry inherent environmental, health and safety risks, including, without limitation, the potential for related civil litigation, regulatory compliance actions, remediation orders, fines and other penalties. Proceedings related to any such litigation or actions could result in significant expenditures as well as the restriction or elimination of the ability to operate any affected project. For example, if NEP fails to obtain eagle "take" permits under the BGEPA or incidental take permits under the ESA for certain of its wind facilities and eagles or listed species, like cave bats, perish in collisions with facility turbines, NEP or its subsidiaries could face criminal prosecution under these laws.

Environmental, health and safety laws and regulations have generally become more stringent over time, and NEP expects this trend to continue. Significant capital and operating costs may be incurred at any time to keep NEP's projects or pipeline investment in compliance with environmental, health and safety laws and regulations, including in response to any addition of species, such as additional bat species, to the endangered species list. If it is not economical to make those expenditures, or if NEP's projects or pipeline investment violate any of these laws and regulations, it may be necessary to retire the affected project or pipeline or restrict or modify its operations, which could have a material adverse effect on NEP's business, financial condition, results of operations and ability to grow its business and make cash distributions to its unitholders.

NEP's renewable energy projects and pipeline investment may be adversely affected by new or revised laws or regulations, interpretations of these laws and regulations or a failure to comply with current applicable energy and pipeline regulations.

NEP's renewable energy projects, pipeline investment and PPA counterparties are subject to regulation by U.S. federal, state and local authorities. The wholesale sale of electric energy in the continental U.S., other than portions of Texas, is subject to the jurisdiction of the FERC and the ability of a project to charge the negotiated rates contained in its PPA is subject to that project’s maintenance of its general authorization from the FERC to sell electricity at market-based rates. The FERC may impose penalties or revoke a project's market-based rate authorization if it determines that the project entity can exercise market power in transmission or generation, creates barriers to entry, has engaged in abusive affiliate transactions or fails to meet compliance requirements associated with such rates. The negotiated rates entered into under PPAs could be changed by the FERC if it determines such change is in the public interest or just and reasonable, depending on the standard in the respective PPA. If the FERC decreases the prices paid to NEP for energy delivered under any of its PPAs, NEP’s revenues could be below its projections and its business, financial condition, results of operations and ability to grow its business and make cash distributions to its unitholders could be materially adversely affected.

NEP’s investment in pipeline assets, through the CPL is subject to FERC regulation under the Natural Gas Act of 1938 (NGA) and the Natural Gas Policy Act of 1978 (NGPA) as the CPL is a segment of a larger, interstate pipeline. The NGPA requires that rates charged for transportation services must be fair and equitable, and amounts collected in excess of fair and equitable rates are subject to refund with interest. Further, state regulation of transportation facilities generally includes various safety, environmental and, in some cases, non-discriminatory take requirements and complaint-based rate regulation. If the CPL was found to have provided services or otherwise operated in violation of the NGA or NGPA, that could result in the imposition of civil penalties, as well as a requirement to disgorge amounts collected for such services in excess of the rate established by the FERC.

NEP's renewable energy projects are subject to the mandatory reliability standards of the NERC. The NERC reliability standards are a series of requirements that relate to maintaining the reliability of the North American bulk electric system and cover a wide variety of topics, including, but not limited to, physical and cybersecurity of critical assets, information protocols, frequency response and voltage standards, testing, documentation and outage management. If NEP fails to comply with these standards, NEP could be subject to sanctions, including, but not limited to, substantial monetary penalties. Although the renewable energy projects are not subject to state utility rate regulation because they sell energy exclusively on a wholesale basis, NEP is subject to other state regulations that may affect NEP's projects’ sale of energy and operations. Changes in state regulatory treatment are unpredictable and could have a material adverse effect on NEP's business, financial condition, results of operations and ability to grow its business and make cash distributions to its unitholders.

The structure of the energy industry and regulation in the U.S. is currently, and may continue to be, subject to challenges and restructuring proposals. Additional regulatory approvals may be required due to changes in law or for other reasons. NEP expects the laws and regulation applicable to its business and the energy industry generally to be in a state of transition for the foreseeable future. Changes in the structure of the industry or in such laws and regulations could have a material adverse effect on NEP's business, financial condition, results of operations and ability to grow its business and make cash distributions to its unitholders.

NEP does not own all of the land on which the projects in its portfolio are located and its use and enjoyment of the property may be adversely affected to the extent that there are any lienholders or land rights holders that have rights that are superior to NEP's rights or the BLM suspends its federal rights-of-way grants.

NEP does not own all of the land on which the projects in its portfolio are located and they generally are, and its future projects may be, located on land occupied under long-term easements, leases and rights-of-way. The ownership interests in the land subject to these easements, leases and rights-of-way may be subject to mortgages securing loans or other liens and other easements, lease rights and rights-of-way of third parties that were created prior to NEP's projects’ easements, leases and rights-of-way. As a result, some of NEP's projects’ rights under such easements, leases or rights-of-way may be

12

subject to the rights of these third parties. While NEP performs title searches, obtains title insurance, records its interests in the real property records of the projects’ localities and enters into non-disturbance agreements to protect itself against these risks, such measures may be inadequate to protect against all risk that NEP's rights to use the land on which its projects are or will be located and its projects’ rights to such easements, leases and rights-of-way could be lost or curtailed. Additionally, NEP operations located on properties owned by others are subject to termination for violation of the terms and conditions of the various easements, leases or rights-of-way under which such operations are conducted.

Further, NEP's activities conducted under federal rights-of-way grants are subject to “immediate temporary suspension” of unspecified duration, at any time, at the discretion of the BLM. A suspension of NEP activities within a federal right-of-way may be issued by the BLM to protect public health or safety or the environment. An order to suspend NEP activities may be issued by the BLM prior to an administrative proceeding. Such an order may be issued verbally or in writing, and may require immediate compliance by NEP. Any violation of such an order could result in the loss or curtailment of NEP's rights to use any federal land on which its projects are or will be located.

Any such loss or curtailment of NEP's rights to use the land on which its projects are or will be located as a result of any lienholders or leaseholders that have rights that are superior to NEP's rights or the BLM’s suspension of its federal rights-of-way grants could have a material adverse effect on NEP's business, financial condition, results of operations and ability to grow its business and make cash distributions to its unitholders. In certain instances, rights-of-way may be subordinate to the rights of government agencies, which could result in costs or interruptions to NEP's service. Restrictions on NEP's ability to use rights-of-way could have a material adverse effect on NEP's business, financial condition, results of operations and ability to grow its business and make cash distributions to its unitholders.

NEP is subject to risks associated with litigation or administrative proceedings.

NEP is subject to risks and costs, including, but not limited to, potential negative publicity and reputational damage, associated with litigation and administrative proceedings, including without limitation, those that may contest the operation, construction or repowering of its projects. The impacts of defending, or failing to prevail in, any such proceeding, regardless of the merits, may be material to NEP and harm its reputation.

NEP is subject to, and may also become subject to additional, claims based on alleged negative health effects related to acoustics, shadow flicker or other claims associated with wind turbines from individuals who live near NEP's projects. Any such legal proceedings or disputes could materially increase the costs associated with NEP's operations. In addition, NEP may become subject to legal proceedings or claims contesting the operation, construction or repowering of NEP's projects. Any such legal proceedings or disputes could materially delay NEP's ability to complete construction or repowering of a project in a timely manner, or at all, or materially increase the costs associated with commencing or continuing a project’s commercial operations. Any settlement of claims or unfavorable outcomes or developments relating to these proceedings or disputes, such as judgments for monetary damages, penalties, injunctions or denial or revocation of permits, could have a material adverse effect on NEP's business, financial condition, results of operations and ability to grow its business and make cash distributions to its unitholders.

NEP is subject to risks associated with its ownership interests in projects that it identifies for repowering, which could result in its inability to complete construction at those projects on time or at all, and make those projects too expensive to complete or cause the return on an investment to be less than expected.

NEP from time to time pursues renewable energy projects and in the future may have interests in projects that have not yet commenced operations or are under construction. There may be delays or unexpected developments in completing any future construction projects, which could cause the construction costs of these projects to exceed NEP's expectations, result in substantial delays or prevent the project from commencing commercial operations. Various factors could contribute to construction-cost overruns, construction halts or delays or failure to commence commercial operations, including:

•delays in obtaining, or the inability to obtain, necessary permits and licenses;

•delays and increased costs related to the interconnection of new projects to the transmission system;

•the inability to acquire or maintain land use and access rights;

•the failure to receive contracted third-party services;

•interruptions to dispatch at the projects;

•supply chain disruptions, including as a result of changes in international trade laws, regulations, agreements, treaties, taxes, tariffs, duties or policies of the U.S. or other countries in which NEP's suppliers are located;

•work stoppages;

•labor disputes;

•weather interferences;

•unforeseen engineering, environmental and geological problems, including, but not limited to, discoveries of contamination, protected plant or animal species or habitat, archaeological or cultural resources or other environment-related factors;

•unanticipated cost overruns in excess of budgeted contingencies; and

•failure of contracting parties, including suppliers, to perform under contracts.

In addition, if NEP or one of its subsidiaries has an agreement for a third party to complete construction of any project, NEP is subject to the viability and performance of the third party. NEP's inability to find a replacement contracting party, if the original contracting party has failed to perform, could result in the abandonment of the construction of such project, while NEP could remain obligated under other agreements associated with the project, including, but not limited to, offtake power sales agreements.

Any of these risks could cause NEP's financial returns on these investments to be lower than expected or otherwise delay or prevent the completion of such projects or distribution of cash to NEP, or could cause NEP to operate below expected capacity or availability levels, which could have a material adverse effect on NEP's business, financial condition, results of operations and ability to grow its business and make cash distributions to its unitholders.

Contract Risks

NEP relies on a limited number of customers and is exposed to the risk that they may be unwilling or unable to fulfill their contractual obligations to NEP or that they otherwise terminate their agreements with NEP.

In most instances, NEP sells the energy generated by each of its renewable energy projects to a single PPA counterparty under a long-term PPA. Further, through NEP's pipeline investment, natural gas is transported under long-term natural gas transportation agreements with a limited number of counterparties. NEP's equity method investees also have contracts with a limited number of counterparties.

NEP expects that its existing and future contracts will be the principal source of cash flows available to make distributions to its unitholders. Thus, the actions of even one customer may cause variability of NEP’s revenue, financial results and cash flows that are difficult to predict. Similarly, significant

13

portions of NEP’s credit risk may be concentrated among a limited number of customers and the failure of even one of these key customers to fulfill its contractual obligations to NEP could significantly impact NEP's business and financial results. Any or all of NEP's customers may fail to fulfill their obligations under their contracts with NEP, whether as a result of the occurrence of any of the factors listed below or otherwise.

•Specified events beyond NEP's control or the control of a customer may temporarily or permanently excuse the customer from its obligation to accept and pay for delivery of energy generated by a project. These events could include, among other things, a system emergency, transmission failure or curtailment, adverse weather conditions or labor disputes.

•Certain of NEP’s customers have been impacted by wildfires in California and have been or could be subject to significant liability which have had or could be expected to have a significant impact on their financial condition.

•The ability of NEP's customers to fulfill their contractual obligations to NEP depends on their financial condition. NEP is exposed to the credit risk of its customers over an extended period of time due to the long-term nature of NEP's contracts with them. These customers could become subject to insolvency or liquidation proceedings or otherwise suffer a deterioration of their financial condition when they have not yet paid for services delivered, any of which could result in underpayment or nonpayment under such agreements.

•A default or failure by NEP to satisfy minimum energy requirements or mechanical availability levels under NEP's agreements could result in damage payments to the applicable customer or termination of the applicable agreement.

If NEP's customers are unwilling or unable to fulfill their contractual obligations to NEP, or if they otherwise terminate such contracts, NEP may not be able to recover contractual payments due to NEP. Since the number of customers that purchase wholesale bulk energy or require the transportation of natural gas is limited, NEP or its pipeline investment may be unable to find a new customer on similar or otherwise acceptable terms or at all. In some cases, there currently is no economical alternative counterparty to the original customer. The loss of, or a reduction in sales to, any of NEP's customers could have a material adverse effect on NEP's business, financial condition, results of operations and ability to grow its business and make cash distributions to its unitholders.

NEP or its pipeline investment may not be able to extend, renew or replace expiring or terminated PPAs, natural gas transportation agreements or other customer contracts at favorable rates or on a long-term basis.

NEP's or its pipeline investment's ability to extend, renew or replace its existing PPAs, natural gas transportation agreements or other customer contracts depends on a number of factors beyond its control, including, but not limited to:

•whether the PPA counterparty has a continued need for energy at the time of the agreement’s expiration, which could be affected by, among other things, the presence or absence of governmental incentives or mandates, prevailing market prices, and the availability of other energy sources;

•the amount of commercial natural gas supply available to its pipeline investment's systems and changing natural gas supply flow patterns in North America;

•the satisfactory performance of NEP's and its pipeline investment's obligations under such PPAs, natural gas transportation agreements or other customer contracts;

•the regulatory environment applicable to NEP's contractual counterparties at the time;

•macroeconomic factors present at the time, such as population, business trends, international trade laws, regulations, agreements, treaties or policies of the U.S. or other countries and related energy demand; and

•the effects of regulation on the contracting practices of NEP's contractual counterparties.

If NEP is not able to extend, renew or replace on acceptable terms existing PPAs before contract expiration, or if such agreements are otherwise terminated prior to their expiration, NEP may be required to sell the energy on an uncontracted basis at prevailing market prices, which could be materially lower than under the applicable contract. If there is no satisfactory market for a project’s uncontracted energy, NEP may decommission the project before the end of its useful life. Any failure to extend, renew or replace a significant portion of NEP's or its pipeline investment's existing PPAs, natural gas transportation agreements or other customer contracts, or extending, renewing or replacing them at lower prices or with other unfavorable terms, or the decommissioning of a project could have a material adverse effect on NEP's business, financial condition, results of operations and ability to grow its business and make cash distributions to its unitholders.

If the energy production by or availability of NEP's renewable energy projects is less than expected, they may not be able to satisfy minimum production or availability obligations under their PPAs.

NEP's energy production or its renewable energy projects’ availability could be less than expected due to various factors, including, but not limited to, wind or solar conditions, natural disasters, equipment underperformance, operational issues, changes in law or regulations or actions taken by third parties. The PPAs contain provisions that require NEP to produce a minimum amount of energy or be available a minimum percentage of time over periods specified in the PPAs. A failure to produce sufficient energy or to be sufficiently available to meet NEP's commitments under its PPAs could result in the payment of damages or the termination of PPAs and could have a material adverse effect on NEP's business, financial condition, results of operations and ability to grow its business and make cash distributions to its unitholders.

Acquisition Risks

NEP's ability to acquire assets involves risks.

NEP's ability to acquire contracted clean energy projects, including partial ownership interests, that are either operational or under construction, from NEER and third parties involves risks and requires NEP to identify attractive acquisitions that can provide positive cash flows. Such acquisitions may not be available to NEP on acceptable terms or at all. Various factors could affect the availability of such acquisitions, including, but not limited to, the following factors and those described in more detail in the additional risk factors below:

•competing bids for a project from companies that may have substantially greater purchasing power, capital or other resources or a greater willingness to accept lower returns or more risk than NEP does;

•a failure to agree to commercially reasonable financial or legal terms with sellers with respect to any proposed acquisitions;

•fewer acquisition opportunities than NEP expects, which could result from, among other things, available projects having less desirable economic returns or higher risk profiles than NEP believes suitable for its acquisition strategy and future growth;

•NEP's inability to obtain financing for acquisitions on economically acceptable terms;

•NEP's failure to successfully complete construction of and finance projects, to the extent that it decides to acquire projects that are not yet operational or to otherwise pursue construction activities with respect to new projects;

•NEP's inability to obtain regulatory approvals or other necessary consents to consummate an acquisition; and

•the presence or potential presence of:

◦pollution, contamination or other wastes at the project site;

14

◦protected plant or animal species;

◦archaeological or cultural resources;

◦wind waking or solar shadowing effects caused by neighboring activities, which reduce potential energy production by decreasing wind speeds or reducing available insolation;

◦land use restrictions and other environment-related siting factors; and

◦local opposition to wind and solar projects in certain markets due to concerns about noise, health, environmental or other alleged impacts of such projects.

Any of these above factors could limit NEP's acquisition opportunities and prevent it from executing, or diminish its ability to execute, its acquisition strategy. Additionally, factors could materially and adversely impact the extent to which suitable acquisition opportunities are made available from NEER, including, but not limited to, NEER's financial position, the risk profile of an opportunity, the fit with NEP's operations and other factors. Furthermore, as NEER's ownership interest in NEP is reduced, NEER may be less willing to sell projects to NEP. An inability by NEP to identify, or a failure by NEER to make available, suitable acquisition opportunities could hinder NEP's growth and materially adversely impact its business, financial condition, results of operations and ability to grow its business and make cash distributions to its unitholders.

NEP may not be able to successfully consummate future acquisitions, whether from NEER or third parties. Any acquisition that may be available to NEP may necessitate that it be able to access the debt and equity markets. However, NEP may be unable to access such markets on satisfactory terms or at all. Furthermore, even if NEP does consummate acquisitions that NEP believes will be accretive, such acquisitions may cause a decrease in cash distributions per common unit as a result of incorrect assumptions in NEP's evaluation of such acquisitions or unforeseen consequences or other external events beyond its control. Acquisitions involve numerous risks, including, but not limited to, difficulties in integrating acquired businesses and unexpected costs and liabilities. Any of the events described above could have a material adverse effect on NEP's business, financial condition, results of operations and ability to grow its business and make cash distributions to its unitholders.

Reductions in demand for natural gas in the U.S. and low market prices of natural gas could materially adversely affect NEP's pipeline investment's operations and cash flows.