UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM

(Mark One)

For

the quarterly period ended

or

For the transition period from ______________ to _______________

Commission

File Number:

(Exact name of registrant as specified in its charter)

| (State or other jurisdiction of organization) | (I.R.S. employer identification no.) | |

| (Address of principal executive offices) | (Zip code) |

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||

| The

|

Indicate

by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange

Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2)

has been subject to such filing requirements for the past 90 days.

Indicate

by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule

405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant

was required to submit such files).

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ☐ | Accelerated filer | ☐ |

| ☒ | Smaller reporting company | ||

| Emerging growth company |

If an emerging growth company, indicate by checkmark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate

by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ☐

Indicate the number of shares outstanding of each of the issuer’s classes of common stock as of the latest practicable date: shares of common stock outstanding as of July 14, 2023.

FINGERMOTION, INC.

FORM 10-Q

TABLE OF CONTENTS

-i-

PART 1. FINANCIAL INFORMATION

ITEM 1. FINANCIAL STATEMENTS

-1-

FINGERMOTION, INC.

CONDENSED CONSOLIDATED INTERIM FINANCIAL STATEMENTS

For the three months ended May 31, 2023

(Unaudited - Expressed in U.S. Dollars)

-2-

| FingerMotion, Inc. |

| Condensed Consolidated Balance Sheets |

| May 31, | February 28, | |||||||

| 2023 | 2023 | |||||||

| ASSETS | (Unaudited) | |||||||

| Current Assets | ||||||||

| Cash and cash equivalents | $ | $ | ||||||

| Accounts receivable | ||||||||

| Prepayment and deposit | ||||||||

| Other receivables | ||||||||

| Total Current Assets | ||||||||

| Non-current Assets | ||||||||

| Equipment | ||||||||

| Intangible assets | ||||||||

| Right-of-use asset | ||||||||

| Total Non-current Assets | ||||||||

| TOTAL ASSETS | $ | $ | ||||||

| LIABILITIES AND SHAREHOLDER’S DEFICIT | ||||||||

| Current Liabilities | ||||||||

| Accounts payable | $ | $ | ||||||

| Accrual and other payables | ||||||||

| Stock subscription payables | ||||||||

| Convertible notes payable, current portion | ||||||||

| Lease liability, current portion | ||||||||

| Total Current Liabilities | ||||||||

| Non-current Liabilities | ||||||||

| Convertible notes payable, non-current portion | ||||||||

| Lease liability, non-current portion | ||||||||

| Total Non-current Liabilities | ||||||||

| TOTAL LIABILITIES | $ | $ | ||||||

| SHAREHOLDERS’ EQUITY | ||||||||

| Preferred stock, par value $ per share; Authorized shares; issued and outstanding -- shares. | ||||||||

| Common Stock, par value $ per share; Authorized shares; issued and outstanding shares and issued and outstanding at May 31, 2023 and February 28, 2023 respectively | ||||||||

| Additional paid-in capital | ||||||||

| Additional paid-in capital - stock options | ||||||||

| Accumulated deficit | ( | ) | ( | ) | ||||

| Accumulated other comprehensive income | ( | ) | ||||||

| Stockholders’ equity before non-controlling interests | ||||||||

| Non-controlling interests | ||||||||

| TOTAL SHAREHOLDERS’ EQUITY | ||||||||

| TOTAL LIABILITIES AND SHAREHOLDERS’ EQUITY | $ | $ | ||||||

-3-

| FingerMotion, Inc. |

| Unaudited Condensed Consolidated Statements of Operations |

| Three Months Ended | ||||||||

| May 31, | May 31, | |||||||

| 2023 | 2022 | |||||||

| Revenue | $ | $ | ||||||

| Cost of revenue | ( | ) | ( | ) | ||||

| Gross profit | ||||||||

| Amortization & depreciation | ( | ) | ( | ) | ||||

| General & administrative expenses | ( | ) | ( | ) | ||||

| Marketing Cost | ( | ) | ||||||

| Research & Development | ( | ) | ( | ) | ||||

| Stock compensation expenses | ( | ) | ( | ) | ||||

| Total operating expenses | ( | ) | ( | ) | ||||

| Net loss from operations | ( | ) | ( | ) | ||||

| Other income (expense): | ||||||||

| Interest income | ||||||||

| Interest expense | ( | ) | ( | ) | ||||

| Exchange gain (loss) | ( | ) | ||||||

| Other income | ||||||||

| Total other income (expense) | ( | ) | ( | ) | ||||

| Net loss before income tax | $ | ( | ) | $ | ( | ) | ||

| Income tax expenses | ||||||||

| Net Loss | $ | ( | ) | $ | ( | ) | ||

| Less: Net profit attributable to the non-controlling interest | ( | ) | ||||||

| Net loss attributable to the Company’s shareholders | $ | ( | ) | $ | ( | ) | ||

| Other comprehensive income: | ||||||||

| Foreign currency translation adjustments | ( | ) | ||||||

| Comprehensive loss | $ | ( | ) | $ | ( | ) | ||

| Less: comprehensive income (loss) attributable to non-controlling interest | ( | ) | ( | ) | ||||

| Comprehensive loss attributable to the Company | $ | ( | ) | $ | ( | ) | ||

| NET LOSS PER SHARE | ||||||||

| Loss Per Share - Basic | $ | ( | ) | $ | ( | ) | ||

| Loss Per Share - Diluted | $ | ( | ) | $ | ( | ) | ||

| NET LOSS PER SHARE ATTRIBUTABLE TO THE COMPANY | ||||||||

| Loss Per Share - Basic | $ | ( | ) | $ | ( | ) | ||

| Loss Per Share - Diluted | $ | ( | ) | $ | ( | ) | ||

| Weighted Average Common Shares Outstanding - Basic | ||||||||

| Weighted Average Common Shares Outstanding - Diluted | ||||||||

-4-

| FingerMotion, Inc. |

| Unaudited Condensed Consolidated Statement of Shareholders’ Equity |

| Accumulated | ||||||||||||||||||||||||||||||||||||

| Capital Paid | Additional | Other | ||||||||||||||||||||||||||||||||||

| Common Stock | in Excess | Paid-in capital | Accumulated | Comprehensive | Stockholders’ | Non-controlling | ||||||||||||||||||||||||||||||

| Shares | Amount | of Par Value | stock options | Deficit | Income | equity | interest | Total | ||||||||||||||||||||||||||||

| Balance at March 1, 2023 | ( | ) | ( | ) | ||||||||||||||||||||||||||||||||

| Common stock issued for cash | ||||||||||||||||||||||||||||||||||||

| Common stock issued for professional service | ||||||||||||||||||||||||||||||||||||

| Execution of convertible notes | ||||||||||||||||||||||||||||||||||||

| Accumulated other comprehensive income | — | |||||||||||||||||||||||||||||||||||

| Net (Loss) | — | ( | ) | ( | ) | ( | ) | |||||||||||||||||||||||||||||

| Balance at May 31, 2023 | ( | ) | ||||||||||||||||||||||||||||||||||

| Accumulated | ||||||||||||||||||||||||||||||||||||

| Capital Paid | Additional | Other | ||||||||||||||||||||||||||||||||||

| Common Stock | in Excess | Paid-in capital | Accumulated | Comprehensive | Stockholders’ | Non-controlling | ||||||||||||||||||||||||||||||

| Shares | Amount | of Par Value | stock options | Deficit | Income | equity | interest | Total | ||||||||||||||||||||||||||||

| Balance at March 1, 2022 | ( | ) | ||||||||||||||||||||||||||||||||||

| Common stock issued for cash | ||||||||||||||||||||||||||||||||||||

| Common stock issued for professional service | ||||||||||||||||||||||||||||||||||||

| Accumulated other comprehensive income | — | ( | ) | ( | ) | ( | ) | |||||||||||||||||||||||||||||

| Net (Loss) | — | ( | ) | ( | ) | ( | ) | ( | ) | |||||||||||||||||||||||||||

| Balance at May 31, 2022 | ( | ) | ( | ) | ||||||||||||||||||||||||||||||||

-5-

| FingerMotion, Inc. |

| Unaudited Condensed Consolidated Statements of Cash Flows |

| Three Months Ended | ||||||||

| May 31, | May 31, | |||||||

| 2023 | 2022 | |||||||

| Net (loss) | $ | ( | ) | $ | ( | ) | ||

| Adjustments to reconcile net loss to net cash provided by (used in) operating activities: | ||||||||

| Share based compensation expenses | ||||||||

| Amortization and depreciation | ||||||||

| Change in operating assets and liabilities: | ||||||||

| (Increase) decrease in accounts receivable | ( | ) | ||||||

| (Increase) decrease in prepayment and deposit | ||||||||

| (Increase) decrease in others receivable | ( | ) | ||||||

| Increase (decrease) in accounts payable | ( | ) | ||||||

| Increase (decrease) in accrual and other payables | ( | ) | ||||||

| Increase (decrease) in due to lease liability | ( | ) | ||||||

| Net Cash provided by (used in) operating activities | ( | ) | ( | ) | ||||

| Cash flows from investing activities | ||||||||

| Purchase of equipment | ( | ) | ||||||

| Net cash provided by (used in) investing activities | ( | ) | ||||||

| Cash flows from financing activities | ||||||||

| Proceed from convertible note | ||||||||

| Repayment of convertible note | ( | ) | ||||||

| Common stock issued for cash | ||||||||

| Net cash provided by (used in) financing activities | ( | ) | ||||||

| Effect of exchange rates on cash and cash equivalents | ( | ) | ||||||

| Net change in cash | ( | ) | ||||||

| Cash at beginning of period | ||||||||

| Cash at end of period | $ | $ | ||||||

| Major non-cash transactions: | ||||||||

| Conversion of loan payables to shares | $ | $ | ||||||

| Supplemental disclosures of cash flow information: | ||||||||

| Interest paid | $ | $ | ||||||

| Taxes paid | $ | $ | ||||||

-6-

FINGERMOTION, INC.

Three months ended May 31, 2023 and 2022

Notes to the Condensed Consolidated Financial Statements

Note 1 –Nature of Business and basis of Presentation

FingerMotion, Inc. fka Property Management Corporation of America (the “Company”) was incorporated on January 23, 2014 under the laws of the State of Delaware. The Company then offered management and consulting services to residential and commercial real estate property owners who rent or lease their property to third party tenants.

The Company changed its name to FingerMotion, Inc. on July 13, 2017 after a change in control. In July 2017 the Company acquired all of the outstanding shares of Finger Motion Company Limited (“FMCL”), a Hong Kong corporation that is an information technology company which specialize in operating and publishing mobile games.

Pursuant to the Share Exchange Agreement with FMCL, effective July 13, 2017 (the “Share Exchange Agreement”, the Company agreed to exchange the outstanding equity stock of FMCL held by the FMCL Shareholders for shares of common stock of the Company. At the Closing Date, the Company issued shares of common stock to the FMCL shareholders. In addition, the Company issued shares to other consultants in connection with the transactions contemplated by the Share Exchange Agreement.

The transaction was accounted for as a “reverse acquisition” since, immediately following completion of the transaction, the shareholders of FMCL effectuated control of the post-combination Company. For accounting purposes, FMCL was deemed to be the accounting acquirer in the transaction and, consequently, the transaction is treated as a recapitalization of FMCL (i.e., a capital transaction involving the issuance of shares by the Company for the shares of FMCL). Accordingly, the consolidated assets, liabilities and results of operations of FMCL became the historical financial statements of FingerMotion, Inc. and its subsidiaries, and the Company’s assets, liabilities and results of operations were consolidated with FMCL beginning on the acquisition date. No step-up in basis or intangible assets or goodwill were recorded in this transaction.

As a result of the Share Exchange Agreement and the other transactions contemplated thereunder, FMCL became a wholly owned subsidiary of the Company. FMCL, a Hong Kong corporation, was formed in April 6, 2016.

On October 16, 2018, the Company through its indirect wholly-owned subsidiary, Shanghai JiuGe Business Management Co., Ltd. (“JiuGe Management”), entered into a series of agreements known as variable interest agreements (the “VIE Agreements”) pursuant to which Shanghai JiuGe Information Technology Co., Ltd. (“JiuGe Technology”) became JiuGe Management’s contractually controlled affiliate. The use of VIE agreements is a common structure used to acquire PRC corporations, particularly in certain industries in which foreign investment is restricted or forbidden by the PRC government. The VIE Agreements include a Consulting Services Agreement, a Loan Agreement, a Power of Attorney Agreement, a Call Option Agreement, and a Share Pledge Agreement in order to secure the connection and commitments of the JiuGe Technology.

On March 7, 2019, JiuGe Technology also acquired 99% of the equity interest of Beijing XunLian (“BX”), a subsidiary that provides bulk distribution of SMS messages for JiuGe customers at discounted rates.

Finger Motion Financial Company Limited was incorporated on January 24, 2020 and is 100% owned by FingerMotion, Inc. The company has been activated for the insurtech business during the last quarter of the fiscal year where the Big Data division secured its first contract and recorded revenue.

Shanghai TengLian JiuJiu Information Communication Technology Co., Ltd. was incorporated on December 23, 2020 for the purpose of venturing into the mobile phone sales in China. It is 99% owned by JiuGe Technology.

On February 5, 2021, JiuGe Technology has disposed of its 99% owned subsidiary, Suzhou BuGuNiao Digital Technology Co., Ltd which was established to venture into R&D projects.

-7-

FINGERMOTION, INC.

Three months ended May 31, 2023 and 2022

Notes to the Condensed Consolidated Financial Statements

Note 2 - Summary of Principal Accounting Policies

Principles of Consolidation and Presentation

The condensed consolidated financial statements have been prepared in accordance with U.S. generally accepted accounting principles (“U.S. GAAP”). The condensed consolidated financial statements include the financial statements of the Company, and its wholly-owned subsidiaries. All intercompany accounts, transactions, and profits have been eliminated upon consolidation.

Variable interest entity

Pursuant to Financial Accounting Standards Board (“FASB”) Accounting Standards Codification (“ASC”) Section 810, “Consolidation” (“ASC 810”), the Company is required to include in its consolidated financial statements, the financial statements of its variable interest entities (“VIEs”). ASC 810 requires a VIE to be consolidated if that company is subject to a majority of the risk of loss for the VIE or is entitled to receive a majority of the VIE’s residual returns. VIEs are those entities in which a company, through contractual arrangements, bears the risk of, and enjoys the rewards normally associated with ownership of the entity, and therefore the company is the primary beneficiary of the entity.

Under ASC 810, a reporting entity has a controlling financial interest in a VIE, and must consolidate that VIE, if the reporting entity has both of the following characteristics: (a) the power to direct the activities of the VIE that most significantly affect the VIE’s economic performance; and (b) the obligation to absorb losses, or the right to receive benefits, that could potentially be significant to the VIE. The reporting entity’s determination of whether it has this power is not affected by the existence of kick-out rights or participating rights, unless a single enterprise, including its related parties and de - facto agents, have the unilateral ability to exercise those rights. JiuGe Technology’s actual stockholders do not hold any kick-out rights that affect the consolidation determination.

Through the VIE agreements disclosed in Note 1, the Company is deemed the primary beneficiary of JiuGe Technology. Accordingly, the results of JiuGe Technology have been included in the accompanying consolidated financial statements. JiuGe Technology has no assets that are collateral for or restricted solely to settle their obligations. The creditors of JiuGe Technology do not have recourse to the Company’s general credit.

-8-

FINGERMOTION, INC.

Three months ended May 31, 2023 and 2022

Notes to the Condensed Consolidated Financial Statements

Note 2 - Summary of Principal Accounting Policies (Continued)

The following assets and liabilities of the VIE and VIE’s subsidiaries are included in the accompanying condensed consolidated financial statements of the Company as of May 31, 2023 and February 28, 2023:

Assets and liabilities of the VIE

| May 31, 2023 | February 28, 2023 | |||||||

| (unaudited) | ||||||||

| Current assets | $ | $ | ||||||

| Non-current assets | ||||||||

| Total assets | $ | $ | ||||||

| Current liabilities | $ | $ | ||||||

| Non-current liabilities | ||||||||

| Total liabilities | $ | $ | ||||||

Assets and liabilities of the VIE Subsidiary

| May 31, 2023 | February 28, 2023 | |||||||

| (unaudited) | ||||||||

| Current assets | $ | $ | ||||||

| Non-current assets | ||||||||

| Total assets | $ | $ | ||||||

| Current liabilities | $ | $ | ||||||

| Non-current liabilities | ||||||||

| Total liabilities | $ | $ | ||||||

-9-

FINGERMOTION, INC.

Three months ended May 31, 2023 and 2022

Notes to the Condensed Consolidated Financial Statements

Note 2 - Summary of Principal Accounting Policies (Continued)

Operating Result of VIE

| For the Three Months Ended May 31, 2023 | For the Three Months Ended May 31, 2022 | |||||||

| (unaudited) | (unaudited) | |||||||

| Revenue | $ | $ | ||||||

| Cost of revenue | ( | ) | ( | ) | ||||

| Gross profit | $ | $ | ||||||

| Amortization and depreciation | ( | ) | ( | ) | ||||

| General and administrative expenses | ( | ) | ( | ) | ||||

| Marketing cost | ( | ) | ||||||

| Research & development | ( | ) | ( | ) | ||||

| Total operating expenses | $ | ( | ) | $ | ( | ) | ||

| Loss from operations | $ | ( | ) | $ | ( | ) | ||

| Interest income | ||||||||

| Other income | ||||||||

| Total other income | $ | $ | ||||||

| Tax expense | ||||||||

| Net profit (loss) | $ | ( | ) | $ | ( | ) | ||

Operating Result of VIE Subsidiary

| For the Three Months Ended May 31, 2023 | For the Three Months Ended May 31, 2022 | |||||||

| (unaudited) | (unaudited) | |||||||

| Revenue | $ | $ | ||||||

| Cost of revenue | ( | ) | ( | ) | ||||

| Gross profit | $ | $ | ||||||

| Amortization and depreciation | ( | ) | ( | ) | ||||

| General and administrative expenses | ( | ) | ( | ) | ||||

| Marketing cost | ( | ) | ||||||

| Research & development | ( | ) | ( | ) | ||||

| Total operating expenses | $ | ( | ) | $ | ( | ) | ||

| Loss from operations | $ | $ | ( | ) | ||||

| Interest income | ||||||||

| Other income | ||||||||

| Total other income | $ | $ | ||||||

| Tax expense | ||||||||

| Net profit (loss) | $ | $ | ( | ) | ||||

-10-

FINGERMOTION, INC.

Three months ended May 31, 2023 and 2022

Notes to the Condensed Consolidated Financial Statements

Note 2 - Summary of Principal Accounting Policies (Continued)

Use of Estimates

The preparation of the Company’s financial statements in conformity with generally accepted accounting principles of the United States of America requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenues and expenses during the reporting period. Management makes its best estimate of the ultimate outcome for these items based on historical trends and other information available when the financial statements are prepared. Actual results could differ from those estimates.

Certain Risks and Uncertainties

The Company relies on cloud-based hosting through a global accredited hosting provider. Management believes that alternate sources are available; however, disruption or termination of this relationship could adversely affect our operating results in the near-term.

Identifiable Intangible Assets

Identifiable

intangible assets are recorded at cost and are amortized over

Impairment of Long-Lived Assets

The Company classifies its long-lived assets into: (i) computer and office equipment; (ii) furniture and fixtures, (iii) leasehold improvements, and (iv) finite – lived intangible assets.

Long-lived assets held and used by the Company are reviewed for impairment whenever events or changes in circumstances indicate that the carrying value of such assets may not be fully recoverable. It is possible that these assets could become impaired as a result of technology, economy or other industry changes. If circumstances require a long-lived asset or asset group to be tested for possible impairment, the Company first compares undiscounted cash flows expected to be generated by that asset or asset group to its carrying value. If the carrying value of the long-lived asset or asset group is not recoverable on an undiscounted cash flow basis, an impairment is recognized to the extent that the carrying value exceeds its fair value. Fair value is determined through various valuation techniques, including discounted cash flow models, relief from royalty income approach, quoted market values and third-party independent appraisals, as considered necessary.

The Company makes various assumptions and estimates regarding estimated future cash flows and other factors in determining the fair values of the respective assets. The assumptions and estimates used to determine future values and remaining useful lives of long-lived assets are complex and subjective. They can be affected by various factors, including external factors such as industry and economic trends, and internal factors such as the Company’s business strategy and its forecasts for specific market expansion.

Accounts Receivable and Concentration of Risk

Accounts receivable, net is stated at the amount the Company expects to collect, or the net realizable value. The Company provides a provision for allowances that includes returns, allowances and doubtful accounts equal to the estimated uncollectible amounts. The Company estimates its provision for allowances based on historical collection experience and a review of the current status of trade accounts receivable. It is reasonably possible that the Company’s estimate of the provision for allowances will change.

-11-

FINGERMOTION, INC.

Three months ended May 31, 2023 and 2022

Notes to the Condensed Consolidated Financial Statements

Note 2 - Summary of Principal Accounting Policies (Continued)

Lease

Operating and finance lease right-of-use assets and lease liabilities are recognized at the commencement date based on the present value of the future lease payments over the lease term. When the rate implicit to the lease cannot be readily determined, the Company utilizes its incremental borrowing rate in determining the present value of the future lease payments. The incremental borrowing rate is derived from information available at the lease commencement date and represents the rate of interest that the Company would have to pay to borrow on a collateralized basis over a similar term and amount equal to the lease payments in a similar economic environment. The right-of-use asset includes any lease payments made and lease incentives received prior to the commencement date. Operating lease right-of-use assets also include any cumulative prepaid or accrued rent when the lease payments are uneven throughout the lease term. The right-of-use assets and lease liabilities may include options to extend or terminate the lease when it is reasonably certain that the Company will exercise that option.

Cash and Cash Equivalents

Cash and cash equivalents represent cash on hand, demand deposits, and other short-term highly liquid investments placed with banks, which have original maturities of three months or less and are readily convertible to known amounts of cash.

Property and Equipment

Property and equipment are stated at cost. Depreciation of property and equipment is provided using the straight-line method for financial reporting purposes at rates based on the estimated useful lives of the assets. Estimated useful lives range from three to seven years. Land is classified as held for sale when management has the ability and intent to sell, in accordance with ASC Topic 360-45.

Basic (loss) earnings per share is based on the weighted average number of common shares outstanding during the period while the effects of potential common shares outstanding during the period are included in diluted earnings per share.

FASB Accounting Standard Codification Topic 260 (“ASC 260”), “Earnings Per Share,” requires that employee equity share options, non-vested shares and similar equity instruments granted to employees be treated as potential common shares in computing diluted earnings per share. Diluted earnings per share should be based on the actual number of options or shares granted and not yet forfeited, unless doing so would be anti-dilutive. The Company uses the “treasury stock” method for equity instruments granted in share-based payment transactions provided in ASC 260 to determine diluted earnings per share. Antidilutive securities represent potentially dilutive securities which are excluded from the computation of diluted earnings or loss per share as their impact was antidilutive.

-12-

FINGERMOTION, INC.

Three months ended May 31, 2023 and 2022

Notes to the Condensed Consolidated Financial Statements

Note 2 - Summary of Principal Accounting Policies (Continued)

Revenue Recognition

The Company adopted ASC 606, Revenue from Contracts with Customers (“ASC 606”) beginning on January 1, 2018 using the modified retrospective approach. ASC 606 establishes principles for reporting information about the nature, amount, timing and uncertainty of revenue and cash flows arising from the entity’s contracts to provide goods or services to customers. The core principle requires an entity to recognize revenue to depict the transfer of goods or services to customers in an amount that reflects the consideration that it expects to be entitled to receive in exchange for those goods or services recognized as performance obligations are satisfied.

The Company has assessed the impact of the guidance by reviewing its existing customer contracts and current accounting policies and practices to identify differences that will result from applying the new requirements, including the evaluation of its performance obligations, transaction price, customer payments, transfer of control and principal versus agent considerations. Based on the assessment, the Company concluded that there was no change to the timing and pattern of revenue recognition for its current revenue streams in scope of ASC 606 and therefore there was no material changes to the Company’s consolidated financial statements upon adoption of ASC 606.

The Company recognizes revenue from providing hosting and integration services and licensing the use of its technology platform to its customers. The Company recognizes revenue when all of the following conditions are satisfied: (1) there is persuasive evidence of an arrangement; (2) the service has been provided to the customer (for licensing, revenue is recognized when the Company’s technology is used to provide hosting and integration services); (3) the amount of fees to be paid by the customer is fixed or determinable; and (4) the collection of fees is probable. We account for our multi-element arrangements, such as instances where we design a custom website and separately offer other services such as hosting, which are recognized over the period for when services are performed.

Income Taxes

The Company uses the asset and liability method of accounting for income taxes in accordance with Accounting Standards Codification (“ASC”) 740, “Income Taxes” (“ASC 740”). Under this method, income tax expense is recognized as the amount of: (i) taxes payable or refundable for the current year and (ii) future tax consequences attributable to differences between financial statement carrying amounts of existing assets and liabilities and their respective tax bases. Deferred tax assets and liabilities are measured using enacted tax rates expected to apply to taxable income in the years which those temporary differences are expected to be recovered or settled. The effect on deferred tax assets and liabilities of a change in tax rates is recognized in the results of operations in the period that includes the enactment date. A valuation allowance is provided to reduce the deferred tax assets reported if based on the weight of available evidence it is more likely than not that some portion or all of the deferred tax assets will not be realized.

Non-controlling interest

Non-controlling interests held 1% of the shares of two of our subsidiaries are recorded as a component of our equity, separate from the Company’s equity. Purchase or sales of equity interests that do not result in a change of control are accounted for as equity transactions. Results of operations attributable to the non-controlling interest are included in our consolidated results of operations and, upon loss of control, the interest sold, as well as interest retained, if any, will be reported at fair value with any gain or loss recognized in earnings.

Recently Issued Accounting Pronouncements

The Company does not believe recently issued but not yet effective accounting standards, if currently adopted, would have a material effect on the consolidated financial position, statements of operations and cash flows.

-13-

FINGERMOTION, INC.

Three months ended May 31, 2023 and 2022

Notes to the Condensed Consolidated Financial Statements

Note 3 - Going Concern

The

accompanying condensed consolidated financial statements have been prepared assuming the Company will continue as a going concern, which

contemplates, among other things, the realization of assets and satisfaction of liabilities in the normal course of business. The Company

had an accumulated deficit of $

The Company’s continuation as a going concern is dependent on its ability to obtain additional financing to fund operations, implement its business model, and ultimately, attain profitable operations. The Company will need to secure additional funds through various means, including equity and debt financing or any similar financing. There can be no assurance that the Company will be able to obtain additional equity or debt financing, if and when needed, on terms acceptable to the Company, or at all. Any additional equity or debt financing may involve substantial dilution to the Company’s stockholders, restrictive covenants or high interest costs. The Company’s long-term liquidity also depends upon its ability to generate revenues and achieve profitability.

Note 4 - Revenue

We

recorded $

| For the three months ended | ||||||||

| May 31, 2023 | May 31, 2022 | |||||||

| (unaudited) | (unaudited) | |||||||

| Telecommunication Products & Services | $ | $ | ||||||

| SMS & MMS Business | ||||||||

| Big Data | ||||||||

| $ | $ | |||||||

Note 5 – Equipment

At May 31, 2023 and February 28, 2023, the company has the following amounts related to tangible assets:

| May 31, 2023 | February 28, 2023 | |||||||

| (unaudited) | ||||||||

| Equipment | $ | $ | ||||||

| Less: accumulated depreciation | ( | ) | ( | ) | ||||

| Net equipment | $ | $ | ||||||

No

significant residual value is estimated for the equipment. Depreciation expense for the three months ended May 31, 2023 and 2022 totaled

$

-14-

FINGERMOTION, INC.

Three months ended May 31, 2023 and 2022

Notes to the Condensed Consolidated Financial Statements

Note 6 – Intangible Assets

At May 31, 2023 and February 28, 2023, the company has the following amounts related to intangible assets:

| May 31, 2023 | February 28, 2023 | |||||||

| (unaudited) | ||||||||

| Licenses | $ | $ | ||||||

| Mobile applications | ||||||||

| Less: accumulated amortization | ( | ) | ( | ) | ||||

| Impairment of intangible assets | ( | ) | ( | ) | ||||

| Net intangible assets | $ | $ | ||||||

No

significant residual value is estimated for these intangible assets. Amortization expense for the three months ended May 31, 2023 and

2022 totaled $

Note 7 – Prepayment and Deposit

Prepaid expenses consist of the deposit pledge to the vendor for stocks credits for resale. Our current vendors are China Unicom and China Mobile for our Telecommunication Products & Services business and our SMS & MMS business. Deposits also includes payments placed into the e-commerce platforms where we offer our products and services. The platforms are PinDuoDuo, Tmall and JD.com.

| May 31, 2023 | February 28, 2023 | |||||||

| (unaudited) | ||||||||

| Telecommunication Products & Services | ||||||||

| Deposit Paid / Prepayment | $ | $ | ||||||

| Deposit received | ||||||||

| Net Prepaid expenses for Telecommunication Products & Services | $ | $ | ||||||

| Others prepayment | ||||||||

| Prepayment and deposit | $ | $ | ||||||

| May 31, 2023 | February 28, 2023 | |||||||

| (unaudited) | ||||||||

| SMS & MMS Business | ||||||||

| Deposit Paid / Prepayment | $ | $ | ||||||

| Deposit received | ||||||||

| Net Prepaid expenses for SMS | $ | $ | ||||||

| Others prepayment | ||||||||

| Prepayment and deposit | $ | $ | ||||||

-15-

FINGERMOTION, INC.

Three months ended May 31, 2023 and 2022

Notes to the Condensed Consolidated Financial Statements

Note 8 – Other Receivables

At May 31, 2023 and February 28, 2023, the company has the following amounts related to other receivables:

| May 31, 2023 | February 28, 2023 | |||||||

| (unaudited) | ||||||||

| Other receivables represent: | ||||||||

| Advances to suppliers | $ | $ | ||||||

| In-transit capital injection for a subsidiary | ||||||||

| Loan for capital injection for a subsidiary | ||||||||

| Others | ||||||||

| $ | $ | |||||||

Note 9 – Right-of-use Asset and Lease Liability

The Company has entered into lease agreements with various third parties. The terms of operating leases are one to two years. These operating leases are included in “Right-of-use Asset” on the Company’s Condensed Consolidated Balance Sheet and represent the Company’s right to use the underlying asset for the lease term. The Company’s obligation to make lease payments are included in “Lease liability” on the Company’s Condensed Consolidated Balance Sheet. Additionally, the Company has entered into various short-term operating leases with an initial term of twelve months or less. These leases are not recorded on the Company’s Condensed Consolidated Balance Sheet. All operating lease expense is recognized on a straight-line basis over the lease term in the three months ended May 31, 2023.

Information related to the Company’s right-of-use assets and related lease liabilities were as follows:

| May 31, 2023 | February 28, 2023 | |||||||

| Right-of-use asset | (unaudited) | |||||||

| Right-of-use asset, net | $ | $ | ||||||

| Lease liability | ||||||||

| Current lease liability | $ | $ | ||||||

| Non-current lease liability | ||||||||

| Total lease liability | $ | $ | ||||||

| Remaining lease term and discount rate | May 31, 2023 | |||||||

| Weighted-average remaining lease term | ||||||||

| Weighted-average discount rate | % | |||||||

Commitments

The following table summarizes the future minimum lease payments due under the Company’s operating leases as of May 31, 2023:

| 2023 | $ | |||

| Thereafter | ||||

| Less: imputed interest | ( | ) | ||

| Total lease liability | $ |

-16-

FINGERMOTION, INC.

Three months ended May 31, 2023 and 2022

Notes to the Condensed Consolidated Financial Statements

Note 10 - Convertible Note Payable

A

Note Payable having a Face Value of $

On

April 28, 2023, the Company paid the Note Payable of $

A

secured, two-year, interest-free convertible promissory note with a principal amount of $

An

event of default under the Note occurred on November 4, 2022 and on November 21, 2022 pursuant to section 2.1(e) of the Note in relation

to the closing of our private placements of shares of common stock in the aggregate amount of shares at a price of $ per

share for gross proceeds of $

Section 2.2 of the Note provides for the remedies upon an event of default, which as described in the Note, the holder may at any time at its option declare the Note immediately due and payable at an amount of 110% or 120% of the outstanding principal amount (the “Mandatory Default Amount”) depending on the type of event of default. In addition, upon an event of default, subject to any applicable cure periods, the holder may (a) from time-to-time demand that all or a portion of the outstanding principal amount be converted into shares of our common stock at the lower of (i) the conversion price (currently $2.00 per share) and (ii) 80% of the average of the three (3) lowest daily VWAPs during the twenty (20) days prior to the delivery of the conversion notice, or (b) exercise or otherwise enforce any one or more of the holder’s rights, powers, privileges, remedies and interests under the Note, the Purchase Agreement, the other transaction documents or applicable law.

The

Mandatory Default Amount for an event of default under Section 2.1(e) of the Note is 110% of the outstanding principal amount of the

Note, which is $

On

February 15, 2023 and February 22, 2023, the Investor provided notice of partial conversion of the Note of shares respectively

on each date amounting to a total conversion of $

In addition, section 5.7 of the Purchase Agreement provides that if we issued any equity interests, other than “Exempted Securities” (as defined in the Purchase Agreement), for aggregate proceeds to us of greater than $10,000,000 during the term of the Purchase Agreement, excluding offering costs and other expenses, unless otherwise waived in writing by and at the discretion of the holder, we will direct 25% of such proceeds from such issuance to repay the Note. We have advised the holder that the aggregate Private Placement Proceeds exceeds $10,000,000 and the holder does not seek to waive or require payment of 25% of the proceeds as repayment of the Note.

-17-

FINGERMOTION, INC.

Three months ended May 31, 2023 and 2022

Notes to the Condensed Consolidated Financial Statements

Note 11 - Common Stock

The

Company issued shares of common stock for the year ended February 28, 2022 for consideration of $

The

Company issued shares of common stock during the fiscal year ended February 28, 2022 pursuant to the conversion of promissory

notes in the aggregate amount of $

The Company cancelled shares of common stock during the fiscal year ended February 28, 2022 pursuant to a financial advisory service agreement.

On March 7, 2022 the Company issued 5,000 shares of our common stock at deemed price of $5.00 per share to one entity pursuant to a consulting agreement.

On March 23, 2022, the Company issued 10,000 shares of our common stock at a deemed price of $3.66 per share to one individual pursuant to a consulting agreement.

On March 23, 2022, the Company issued an aggregate of 25,000 shares of our common stock at a deemed price of $2.85 per share to two individuals and one entity pursuant to consulting agreements.

On April 14, 2022, the Company issued 5,000 shares of our common stock at a deemed price of $5.00 per share to one entity pursuant to a consulting agreement.

On April 28, 2022, the Company issued 50,000 shares of our common stock at a deemed price of $2.61 per share to one entity pursuant to a consulting agreement.

On April 28, 2022, the Company issued 5,000 shares of our common stock at a deemed price of $2.56 per share to one entity pursuant to a consulting agreement.

On April 28, 2022, the Company issued 20,000 shares of our common stock at a deemed price of $2.51 per share to one individual pursuant to a consulting agreement.

On May 10, 2022, the Company issued 5,000 shares of our common stock at a deemed price of $5.00 per share to one entity pursuant to a consulting agreement.

On May 10, 2022, the Company issued 5,000 shares of our common stock at a deemed price of $3.66 per share to one individual pursuant to a consulting agreement.

On May 12, 2022, the Company issued 20,000 shares of our common stock at a deemed price of $2.03 per share to one entity pursuant to a consulting agreement as amended.

On July 5, 2022, the Company issued 5,000 shares of our common stock at a deemed price of $5.00 per share to one entity pursuant to a consulting agreement.

On July 5, 2022, the Company issued an aggregate of 25,000 shares of our common stock at a deemed price of $2.85 per share to two individuals and one entity pursuant to consulting agreements.

On August 3, 2022, the Company issued 50,000 shares of our common stock at a deemed price of $1.22 per share to one entity pursuant to a consulting agreement.

On October 19, 2022, the Company issued an aggregate of 25,000 shares of our common stock at a deemed price of $2.85 per share to two individuals and one entity pursuant to consulting agreements.

On October 19, 2022, the Company issued 20,000 shares of our common stock at a deemed price of $1.70 per share to one entity pursuant to a consulting agreement.

-18-

FINGERMOTION, INC.

Three months ended May 31, 2023 and 2022

Notes to the Condensed Consolidated Financial Statements

Note 11 - Common Stock (continued)

On October 19, 2022, the Company issued 10,000 shares of our common stock at a deemed price of $3.66 per share to one individual pursuant to a consulting agreement.

On October 19, 2022, the Company issued 5,000 shares of our common stock at a deemed price of $2.56 per share to one entity pursuant to a consulting agreement.

On October 24, 2022, the Company issued 100,000 shares of our common stock at price of $2.00 per share to two individuals pursuant to the exercise of warrants.

On October 24, 2022, the Company issued 70,000 shares of our common stock at price of $3.00 per share to one individual pursuant to the exercise of warrants.

On November 3, 2022, the Company issued 20,000 shares of our common stock at price of $3.00 per share to two individuals pursuant to the exercise of warrants.

On November 3, 2022, the Company issued 5,000 shares of our common stock at a deemed price of $1.70 per share to one entity pursuant to a consulting agreement.

On November 3, 2022, the Company issued 25,000 shares of our common stock at a deemed price of $1.22 per share to one entity pursuant to a consulting agreement.

On November 3, 2022, the Company issued 200,000 shares of our common stock at a deemed price of $0.74 per share to one individual pursuant to a consulting agreement.

On November 4, 2022, the Company issued an aggregate of 1,887,500 shares of common stock at a price of $4.00 per share to eleven individuals due to the closing of its private placement at $4.00 per share for aggregate gross proceeds of $7,550,000.

In connection with the closing of the private placement on November 4, 2022, the Company issued 91,875 shares of common stock at price of $4.00 per share for a total value of $367,500 to one individual as finder’s fees.

On November 21, 2022, the Company issued 1,000,000 shares of common stock at a price of $4.00 per share to one entity due to the closing of its private placement at $4.00 per share for aggregate gross proceeds of $4,000,000.

On January 19, 2023, the Company issued 5,000 shares of our common stock at a deemed price of $1.70 per share to one entity pursuant to a consulting agreement.

On January 19, 2023, the Company issued an aggregate of 25,000 shares of our common stock at a deemed price of $2.85 per share to two individuals and one entity pursuant to consulting agreements.

On January 19, 2023, the Company issued 125,000 shares of our common stock at a deemed price of $1.44 per share to one entity pursuant to a consulting agreement.

On January 19, 2023, the Company issued 16,313 shares of our common stock at a deemed price of $5.19 per share to one entity pursuant to a consulting agreement.

On January 19, 2023, the Company issued 40,000 shares of our common stock at a deemed price of $4.15 per share to one entity pursuant to a consulting agreement.

On February 7, 2023, the Company issued 1,721,766 shares of common stock at deemed price of $1.75 per share to its primary lender pursuant to the cashless exercise of warrants of the convertible promissory note (the “Note”) issued to the Company’s primary lender on August 9, 2022.

-19-

FINGERMOTION, INC.

Three months ended May 31, 2023 and 2022

Notes to the Condensed Consolidated Financial Statements

Note 11 - Common Stock (continued)

On February 7, 2023, the Company issued 25,000 shares of our common stock at a deemed price of $1.22 per share to one entity pursuant to a consulting agreement.

On

February 15, 2023, the Company issued shares of common stock at price of $2.00

per share to its primary lender pursuant to the conversion of $

On

February 22, 2023, the Company issued shares of common stock at price of $ per

share to its primary lender pursuant to the conversion of $

On February 28, 2023, the Company issued shares of our common stock at a deemed price of $ per share to one individual pursuant to a consulting agreement.

On February 28, 2023, the Company issued 7,500 shares of our common stock at a deemed price of $2.47 per share to one entity pursuant to a consulting agreement.

On

March 17, 2023, we issued shares of common stock at price of $ per share to our primary lender pursuant to the conversion

of $

On April 18, 2023, we issued shares of common stock at a price of $ per share pursuant to the exercise of warrants.

On April 24, 2023, we issued shares of our common stock at a deemed price of $ per share to one entity pursuant to a consulting agreement.

As of May 31, 2023 there were shares of the Company’s common stock issued and outstanding, and none of the preferred shares were issued and outstanding.

-20-

FINGERMOTION, INC.

Three months ended May 31, 2023 and 2022

Notes to the Condensed Consolidated Financial Statements

Share Purchase Warrants

A continuity schedule of outstanding share purchase warrants as at May 31, 2023, and the changes during the periods, is as follows:

| Number of Warrants | Weighted Average Exercise Price | |||||||

| Balance, February 28, 2020 | $ | |||||||

| Issued in Connection with October 2020 Offering | $ | |||||||

| Issued in connection with January 2021 Offering | $ | |||||||

| Exercised | ( | ) | $ | |||||

| Balance, February 28, 2021 | $ | |||||||

| Exercised | ( | ) | $ | |||||

| Balance, February 28, 2022 | $ | |||||||

| Issued in Connection with August 2022 Offering | $ | |||||||

| Expired | ( | ) | $ | |||||

| Issued in Connection with August 2022 Offering | $ | |||||||

| Issued in Connection with September 2022 Offering | $ | |||||||

| Issued in Connection with November 2022 Offering | $ | |||||||

| Issued in Connection with November 2022 Offering | $ | |||||||

| Exercised | ( | ) | $ | |||||

| Exercised | ( | ) | $ | |||||

| Issued in Connection with October 2022 Offering | $ | |||||||

| Cashless Exercised | ( | ) | $ | |||||

| Balance, February 28, 2023 | $ | |||||||

| Exercised | ( | ) | $ | |||||

| Expired | ( | ) | $ | |||||

| Balance, May 31, 2023 | $ | |||||||

During

Fiscal 2023 and Fiscal 2022, we received cash proceeds totaling $

On August 9, 2022, the Company entered into a Securities Purchase Agreement with an investor (the “Investor”), pursuant to which the Company issued to the Investor a common stock purchase warrant (the “Warrant”) to acquire 3,478,261 shares of common stock of the Company, which is subject to reduction by 50% upon effectiveness of the registration statement covering the underlying shares.

On February 6, 2023, the Investor exercised the Warrant on the cashless exercise basis for all 3,478,261 warrants, resulting in the issuance of 1,721,766 shares of common stock.

On October 19, 2022, the Company’s board of directors authorized a six month extension to the expiry date of the common stock purchase warrants that the Company issued on October 19, 2020 which have an expiry date of October 19, 2022 and an exercise price of $2.00 per share (the “October 2020 Warrants”). The new expiry date of the October 2020 Warrants is April 19, 2023. In addition, 50,000 stock purchase warrants at an exercise price of $3.00 per share have expired.

On November 3, 2022, the Company issued 350,000 common stock purchase warrants to purchase 350,000 shares of its common stock at a price of $5.00 per share until September 19, 2024 to one individual pursuant to a consulting agreement.

On November 29, 2022, the Company issued 168,000 common stock purchase warrants to purchase 168,000 shares of its common stock at a price of $1.75 per share until August 9, 2027 to The Benchmark Company, LLC (“Benchmark”) pursuant to a financial advisory agreement.

-21-

FINGERMOTION, INC.

Three months ended May 31, 2023 and 2022

Notes to the Condensed Consolidated Financial Statements

Share Purchase Warrants (continued)

On November 29, 2022, the Company issued 28,312 common stock purchase warrants to purchase 28,312 shares of its common stock at a price of $8.22 per share until November 4, 2025, to Benchmark pursuant to a financial advisory agreement.

On November 29, 2022, the Company issued 10,000 common stock purchase warrants to purchase 10,000 shares of its common stock at a price of $6.70 per share until November 21, 2025, to Benchmark pursuant to a financial advisory agreement.

During the quarter ended November 30, 2022, the Company received $470,000 from the exercise of warrants for the purchase of 100,000 shares of common stock of the Company at a price of $2.00 per share from 2 individuals and the purchase of 90,000 shares of common stock of the Company at a price of $3.00 per shares from 3 individuals.

On January 13, 2023, the Company’s board of directors has authorized a six month extension to the expiry date of the common stock purchase warrants that the Company issued on January 13, 2021 which have an expiry date of January 13, 2023 and an exercise price of $3.00 per share (the “January 2021 Warrants”). The new expiry date of the January 2021 Warrants is July 13, 2023.

On

February 28, 2023, the Company issued common

stock purchase warrants to purchase

On

April 18, 2023, the Company received $ from the

exercise of warrants for the purchase of

On April 19, 2023, stock purchase warrants at an exercise price of $ per share have expired.

A summary of share purchase warrants outstanding and exercisable as at May 31, 2023 is as follows:

| Number of Warrants | Remaining Contractual | |||||||||||||

| Exercise Price | Outstanding | Life (Years) | Expiry Date | |||||||||||

| $ | ||||||||||||||

| $ | ||||||||||||||

| $ | ||||||||||||||

| $ | ||||||||||||||

| $ | ||||||||||||||

| $ | ||||||||||||||

| $ | ||||||||||||||

-22-

FINGERMOTION, INC.

Three months ended May 31, 2023 and 2022

Notes to the Condensed Consolidated Financial Statements

Stock Options

On December 28, 2021, we granted an aggregate of 4,545,000 stock options pursuant to our 2021 Stock Incentive Plan having an exercise price of $8.00 per share and an expiry date of five years from the date of grant to 40 individuals who were directors, officers, employees and consultants of the Company. We relied upon the exemption from registration under the U.S. Securities Act provided by Rule 903 of Regulation S promulgated under the U.S. Securities Act for the grant of stock options to individuals who are non-U.S. persons and upon the exemption from registration under Section 4(a)(2) of the U.S. Securities Act for two individuals who are U.S. persons. The stock options are all subject to vesting provisions of 20% on the date of grant and 20% on each of the first, second, third, and fourth anniversary of the date of grant. At our annual meeting of stockholders held on February 17, 2023, the stockholder approved an amendment to the exercise price of the outstanding stock options from $8.00 to $3.84.

The fair value of these stock options was estimated at the date of grant, using the Black-Scholes Option Valuation Model, with the following weighted average assumptions:

| May 31, 2023 | February 28, 2023 | |||||||

| Expected Risk-Free Interest Rate | % | % | ||||||

| Expected Volatility | % | % | ||||||

| Expected Life in Years | ||||||||

| Expected Dividend Yield | ||||||||

| Weighted-Average Grant Date Fair Value | $ | $ | ||||||

A continuity schedule of outstanding stock options as at May 31, 2023, and the changes during the three months periods, is as follows:

| Number of Stock Options | Exercise Price | |||||||

| Balance, February 28, 2023 | $ | |||||||

| Vested | ||||||||

| Cancelled/Forfeited | ||||||||

| Expired | ||||||||

| Balance, May 31, 2023 | $ | |||||||

The table below sets forth the number of issued shares and cash received upon exercise of stock options:

| May 31, 2023 | February 28, 2023 | |||||||

| Number of Options Exercised on Forfeiture Basis | ||||||||

| Number of Options Exercised on Cash Basis | ||||||||

| Total Number of Options Exercised | ||||||||

| Number of Shares Issued on Cash Exercise | ||||||||

| Number of Shares Issued on Forfeiture Basis | ||||||||

| Total Number of Shares Issued Upon Exercise of Options | ||||||||

| Cash Received from Exercise of Stock Options | $ | $ | ||||||

| Total Intrinsic Value of Options Exercised | $ | $ | ||||||

-23-

FINGERMOTION, INC.

Three months ended May 31, 2023 and 2022

Notes to the Condensed Consolidated Financial Statements

Stock Options (continued)

A continuity schedule of outstanding unvested stock options at May 31, 2023, and the changes during the three months periods, is as follows

| Number of Unvested | Weighted Average | |||||||

| Stock Options | Grant Date Fair Value | |||||||

| Balance, February 28, 2021 | ||||||||

| Granted | $ | |||||||

| Vested | ( | ) | $ | |||||

| Balance, February 28, 2022 | $ | |||||||

| Vested | ( | ) | $ | |||||

| Cancelled / Forfeited | ( | ) | $ | |||||

| Balance, February 28, 2023 | $ | |||||||

| Vested | ||||||||

| Cancelled / Forfeited | ||||||||

| Balance, May 31, 2023 | $ | |||||||

As at May 31, 2023, the aggregate intrinsic value of all outstanding stock options granted was estimated at $0 as the current price is lower than the strike price.

A summary of stock options outstanding and exercisable as at May 31, 2023 is as follows:

| Options Outstanding | Options Exercisable | |||||||||||||||||||||||

Range of Exercise Prices |

Outstanding at May 31, 2023 |

Exercise Price | Weighted Average Remaining Contractual Term (Years) |

Exercisable at May 31, 2023 | Exercise Price | Weighted Average Remaining Contractual Term (Years) |

||||||||||||||||||

| $ to $ | $ | $ | ||||||||||||||||||||||

| $ | $ | |||||||||||||||||||||||

The following table sets forth the computation of basic and diluted earnings per common share:

| For the three months ended | ||||||||

| May 31, 2023 | May 31, 2022 | |||||||

| Numerator - basic and diluted | ||||||||

| Net Loss | $ | ( | ) | $ | ( | ) | ||

| Denominator | ||||||||

| Weighted average number of common shares outstanding — basic | ||||||||

| Weighted average number of common shares outstanding — diluted | ||||||||

| Loss per common share — basic | $ | ( | ) | $ | ( | ) | ||

| Loss per common share — diluted | $ | ( | ) | $ | ( | ) | ||

-24-

FINGERMOTION, INC.

Three months ended May 31, 2023 and 2022

Notes to the Condensed Consolidated Financial Statements

Note 13 - Income Taxes

The Company and its subsidiaries file separate income tax returns.

The United States of America

FingerMotion,

Inc. is incorporated in the State of Delaware in the U.S. and is subject to a U.S. federal corporate income tax of

Hong Kong

Finger

Motion Company Limited is incorporated in Hong Kong and Hong Kong’s profits tax rate is

The People’s Republic of China (PRC)

JiuGe

Management, JiuGe Technology, Beijing XunLian and Shanghai TengLian JiuJiu were incorporated in the People’s Republic of China

and subject to PRC income tax at

Income tax mainly consists of foreign income tax at statutory rates and the effects of permanent and temporary differences. The Company’s effective income tax rates for the three months ended May 31, 2023 and 2022 are as follows:

| For the three months ended | ||||||||

| May 31, 2023 | May 31, 2022 | |||||||

| (unaudited) | (unaudited) | |||||||

| U.S. statutory tax rate | % | % | ||||||

| Foreign income not registered in the U.S. | ( | %) | ( | %) | ||||

| PRC profit tax rate | % | % | ||||||

| Changes in valuation allowance and others | ( | %) | ( | %) | ||||

| Effective tax rate | % | % | ||||||

At

May 31, 2023 and February 28, 2023, the Company has a deferred tax asset of $

| May 31, 2023 | February 28, 2023 | |||||||

| (unaudited) | ||||||||

| Deferred tax asset from operating losses carry-forwards | $ | $ | ||||||

| Valuation allowance | ( | ) | ( | ) | ||||

| Deferred tax asset, net | $ | $ | ||||||

-25-

FINGERMOTION, INC.

Three months ended May 31, 2023 and 2022

Notes to the Condensed Consolidated Financial Statements

Note 14 - Commitments and Contingencies

Legal proceedings

The Company is not aware of any material outstanding claim and litigation against them.

Note 15 - Subsequent Events

Except for the above, the Company has determined that it does not have any material subsequent events to disclose in these consolidated financial statements.

-26-

ITEM 2 – MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

The terms the “Registrant”, “we”, “us”, “our”, “FingerMotion” and the “Company” mean FingerMotion, Inc. or as the context requires, collectively with its consolidated subsidiaries and contractually controlled companies.

Cautionary Note Regarding Forward-Looking Statements

The following management’s discussion and analysis of the Company’s financial condition and results of operations (the “MD&A”) contains forward-looking statements that involve risks, uncertainties and assumptions including, among others, statements regarding our capital needs, business plans and expectations. In evaluating these statements, you should consider various factors, including the risks, uncertainties and assumptions set forth in reports and other documents we have filed with or furnished to the SEC and, including, without limitation, this Quarterly Report on Form 10-Q for the three months ended May 31, 2023, and our Annual Report on Form 10-K for the fiscal year ended February 28, 2023, including the consolidated financial statements and related notes contained therein. These factors, or any one of them, may cause our actual results or actions in the future to differ materially from any forward-looking statement made in this document. Refer to “Cautionary Note Regarding Forward-looking Statements” as disclosed in our Annual Report on Form 10-K for the fiscal year ended February 28, 2023, and Item 1A, Risk Factors, under Part II - Other Information of this Quarterly Report.

Introduction

This MD&A is focused on material changes in our financial condition from February 28, 2023, our most recently completed year end, to May 31, 2023, and our results of operations for the three months ended May 31, 2023, and should be read in conjunction with Item 7, Management’s Discussion and Analysis of Financial Condition and Results of Operations as contained in our Annual Report on Form 10-K for the fiscal year ended February 28, 2023.

Corporate Information

The Company was initially incorporated as Property Management Corporation of America on January 23, 2014 in the State of Delaware.

On June 21, 2017, the Company amended its certificate of incorporation to effect a 1-for-4 reverse stock split of the Company’s outstanding common stock, to increase the authorized shares of common stock to 200,000,000 shares and to change the name of the Company from “Property Management Corporation of America” to “FingerMotion, Inc.” (the “Corporate Actions”). The Corporate Actions and the amended certificate of incorporation became effective on June 21, 2017.

Our principal executive offices are located at 111 Somerset Road, Level 3, Singapore 238164, and our telephone number at that address is (347) 349-5339.

We are a holding company incorporated in Delaware and not an operating company incorporated in the People’s Republic of China (the “PRC” or “China”). As a holding company, we conduct a significant part of our operations through our subsidiaries and through the VIE Agreements with the VIE based in China.

-27-

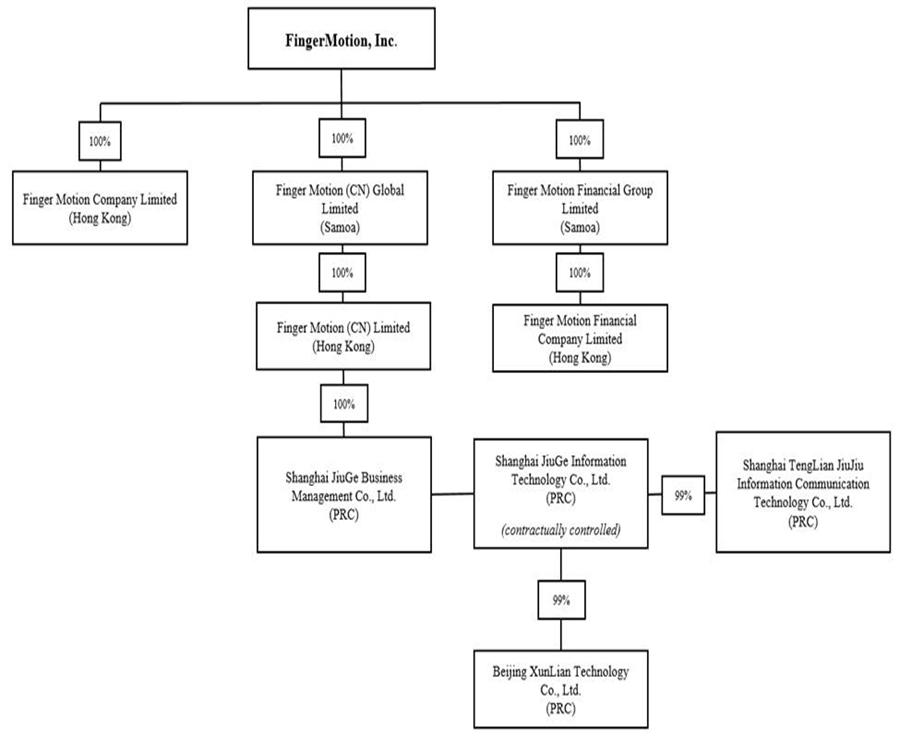

The following diagram depicts our corporate structure:

Our holding company structure presents unique risks as our investors may never directly hold equity interests in our subsidiaries or the VIE, and will be dependent upon contributions from our subsidiaries and the VIE to finance our cash flow needs. Our subsidiaries and the VIE are currently not required to obtain permission from the Chinese authorities including the China Securities Regulatory Commission (the “CSRC”), or Cybersecurity Administration Committee (the “CAC”), to operate or to issue securities to foreign investors. However, as of March 31, 2023, pursuant to the Overseas Listing Trial Measures promulgated by the CSRC, we may have to file with the CSRC with respect to a new offering of our securities. The business of our subsidiaries and the VIE until now are not subject to cybersecurity review with the CAC, given that: (i) data processed in our business does not have a bearing on national security and thus may not be classified as core or important data by the authorities; (ii) we do not possess a large amount of personal information in our business operations. In addition, we are not subject to merger control review by China’s anti-monopoly enforcement agency due to the level of our revenues which provided from us and audited by our auditor and the fact that we currently do not expect to propose or implement any acquisition of control of, or decisive influence over, any company with revenues within China of more than RMB400 million. Currently, these statements and regulatory actions have had no impact on our daily business operations, the ability to accept foreign investments and list our securities on an U.S. or other foreign exchange. However, since these statements and regulatory actions, including the Overseas Listing Trial Measures, are new, it is uncertain what potential impact such modified or new laws and regulations will have on our daily business operation, the ability to accept foreign investments and list our securities on an U.S. or other foreign exchange.

-28-

To operate, the VIE and Beijing XunLian TianXia Technology Co., Ltd. are required to obtain, and have obtained, a value-added telecommunications business licence from PRC authorities. In connection with our previous issuance of securities to foreign investors, under current PRC laws, regulations and regulatory rules, as of the date of this periodic report on Form 10-Q, we, our PRC subsidiaries and the VIE, (i) are not required to obtain permissions from the CSRC except that as of March 31, 2023 we may have to file with the CSRC with respect to a new offering of our securities, (ii) are not required to go through cybersecurity review by the CAC, and (iii) have received or were not denied such requisite permissions by any PRC authority. If we, our subsidiaries or the VIE (i) do not receive or maintain such permissions or approvals, (ii) inadvertently conclude that such permissions or approvals are not required or (iii) applicable laws, regulations, or interpretations change and we are required to obtain such permissions or approvals in the future, we may be subject to government enforcement actions, investigations, penalties, sanctions and fines imposed by the CSRC, the CAC and relevant departments of the State Council. In severe circumstances, the business of our PRC subsidiary may be ordered to suspend and its business qualifications and licences may be revoked.

To address challenges resulting from laws, policies and practices that may disfavor foreign-owned entities that operate within industries deemed sensitive by the Chinese government, we use the VIE structure to provide contractual exposure to foreign investment in the PRC-based companies. We own 100% of the equity of a WFOE, Shanghai JiuGe Business Management Co., Ltd. (“JiuGe Management”), which has entered into the VIE Agreements with the VIE, which is owned by Ms. Li Li the legal representative and general manager, and also the shareholder of the VIE. The VIE Agreements have not been tested in court. As a result of our use of the VIE structure, you may never directly hold equity interests the VIE. Any securities that we offer will be securities of the Company, the Delaware holding company, not of the VIE.

We fund the registered capital and operating expenses of the VIE by extending loans to the shareholders of the VIE. The VIE Agreements governing the relationship between the VIE and our WFOE enable us to (i) direct the activities of the VIE that most significantly impact the VIE’s economic performance, (ii) receive substantially all of the economic benefits of the VIE, and (iii) have an exclusive call option to purchase, at any time, all or part of the equity interests in and/or assets of the VIE to the extent permitted by Chinese laws. As a result of the VIE Agreements, the Company is considered the primary beneficiary of the VIE for accounting purposes and is able to consolidate the financial results of the VIE in its consolidated financial statements in accordance with U.S. GAAP. As a result, investors in our Common Shares are not purchasing an equity interest in the VIE but instead are purchasing equity interest in FingerMotion, Inc., a Delaware holding company.

Share Exchange Agreement

Effective July 13, 2017, the Company entered into that certain Share Exchange Agreement (the “Share Exchange Agreement”) by and among the Company, Finger Motion Company Limited, a Hong Kong corporation (“FMCL”) and certain shareholders of FMCL (the “FMCL Shareholders”). FMCL, a Hong Kong corporation, was formed on April 6, 2016 and is an information technology company that specializes in operating and publishing mobile games. Pursuant to the Share Exchange Agreement, the Company agreed to exchange the outstanding equity stock of FMCL held by the FMCL Shareholders for shares of common stock of the Company. On the closing date of the Share Exchange Agreement, the Company issued 12,000,000 shares of common stock to the FMCL shareholders. In addition, the Company issued 600,000 shares to consultants in connection with the transactions contemplated by the Share Exchange Agreement, and 2,562,500 additional shares to accredited investors, which was a concurrent financing but not a condition of closing the Share Exchange Agreement.

As a result of the Share Exchange Agreement and the other transactions contemplated thereunder, FMCL became a wholly owned subsidiary of the Company. The Company operates its video game division through FMCL. However, in June 2018, the Company decided to pause the operation of the game division as it saw the opportunity in the telecommunication business and have since refocused into this business.

This description of the Share Exchange Agreement does not purport to be complete and is qualified in its entirety by reference to the terms of the Share Exchange Agreement, which was filed as an exhibit to our Current Report on Form 8-K filed with the SEC on July 20, 2017 and incorporated by reference herein.

-29-

VIE Agreements

On October 16, 2018, the Company, through its indirect wholly owned subsidiary, Shanghai JiuGe Business Management Co., Ltd. (“JiuGe Management”), entered into a series of agreements known as variable interest agreements (the “VIE Agreements”) pursuant to which Shanghai JiuGe Information Technology Co., Ltd. (“JiuGe Technology”) became our contractually controlled affiliate. The use of VIE agreements is a common structure used to acquire PRC corporations, particularly in certain industries in which foreign investment is restricted or forbidden by the PRC government. The VIE Agreements include a Consulting Services Agreement, a Loan Agreement, a Power of Attorney Agreement, a Call Option Agreement, and a Share Pledge Agreement in order to secure the connection and commitments of the JiuGe Technology. We operate our mobile payment platform business through JiuGe Technology.

The VIE Agreements included:

| ● | a consulting services agreement through which JiuGe Management is mainly engaged in data marketing, technical services, technical consulting and business consultancy to JiuGe Technology (the “JiuGe Technology Consulting Services Agreement”). This agreement was duly signed among the WFOE and the VIE. Under this agreement, the WFOE will provide the following services to the VIE on an exclusive basis: (i) providing a comprehensive solution for all technical issues required for the VIE’s business; (ii) providing training to the professional technicians of the VIE; (iii) assisting the VIE in collecting technical and commercial information and conducting market surveys; (iv) assisting the VIE in procuring business opportunities to obtain contracts awarded by the telecom carries in China and maintaining the commercial relationship with the telecom carries; (v) introducing clients to the VIE and assisting the VIE in developing commercial and cooperative relationship with the clients; (vi) providing suggestions and opinions on establishment and improvement of the VIE’s corporate structure, management system and departmental organization; (vii) assisting the VIE in formulating annual business plans, the draft of which shall be made available to WFOE by the VIE prior to the end of November each year; (viii) granting license to the VIE to use WFOE’s intellectual property necessary for the services; and (ix) providing other consulting and technical services at the request of the VIE. The VIE will pay to the WFOE service fees equivalent to the after-tax net profits distributable by the VIE to its shareholder each year, as set forth in the audited financial statements in accordance with the PRC accounting standards, ensuring all the distributable profits of the VIE will be dispatched to the WFOE. The VIE may not assign any of its rights and obligations under the JiuGe Technology Consulting Services Agreement without prior written consent of the WFOE. This agreement ensures that the WFOE and investors will be able to legally obtain the profits of the VIE, and transfer them to the WFOE more conveniently in the form of “service fee”; | |

| ● | a loan agreement through which JiuGe Management grants a loan to the Legal Representative of JiuGe Technology for the purpose of capital contribution (the “JiuGe Technology Loan Agreement”). This agreement was duly signed between the WFOE and Ms. Li Li. Under this agreement, the WFOE loaned RMB 10,000,000 to Ms. Li Li, as the sole shareholder of the VIE, solely for the purpose of the capital contribution of the subscribed capital of the VIE. The WFOE has the right to convert the whole or any part of the outstanding principal amount into the equity interests in the VIE and may demand repayment of any or all of the principal amount/ As security for performance and discharge of Ms. Li Li’s obligations under the JiuGe Technology Loan Agreement, Ms. Li Li pledged 100% equity interests in the VIE, representing the entire registered capital of the VIE, by way of first-ranking security to the WFOE. This agreement could constrain Ms. Li Li to cooperate with WFOE’s instructions and avoid damaging the rights and interests of the WFOE and investors; | |

| ● | a power of attorney agreement under which the owner of JiuGe Technology has vested their collective voting control over JiuGe Technology to JiuGe Management and will only transfer their equity interests in JiuGe Technology to JiuGe Management or its designee(s) (the “JiuGe Technology Power of Attorney Agreement”). The Power of Attorney Agreement was duly issued by Ms. Li Li to the WFOE. Under the JiuGe Technology Power of Attorney Agreement, the WFOE is the exclusive agent who may exercise, at WFOE’s sole discretion, all the rights and powers in respect of all the 100% equity interests held by Ms. Li Li in the VIE on Ms. LI Li’s behalf, including without limitation to propose to convene, attend and vote at the shareholder’s meeting of the VIE. Ms. Li Li cannot assign her rights and obligations under the JiuGe Technology Power of Attorney Agreement without prior written consent of the WFOE and the WFOE will bear its own costs, expenses and fees in connection with performance of the JiuGe Technology Power of Attorney Agreement. This agreement ensures that the WFOE can replace Ms. LI Li in the operation and management of the VIE, and controlling its assets; |

-30-

| ● | a call option agreement under which the owner of JiuGe Technology has granted to JiuGe Management the irrevocable and unconditional right and option to acquire all of their equity interests in JiuGe Technology or transfer these rights to a third party (the “JiuGe Technology Call Option Agreement”). This agreement was duly signed by and among Ms. Li Li, the WFOE and the VIE. Under this agreement, the WFOE has an exclusive, irrevocable and unconditional option to purchase or to designate a third party to purchase 100% equity interests of the VIE at RMB one (1) yuan or the lowest amount of consideration permitted under the laws of PRC at any time, giving the WFOE a sole discretion to exercise such option at any time and in any manner as permitted by the laws of PRC. Pursuant to the JiuGe Technology Call Option Agreement, Ms. Li Li may not, without prior written consent of the WFOE: (i) transfer or dispose of the equity interests in the VIE or the assets of the VIE in any manner; (ii) create any encumbrance of any kind over the equity interests in the VIE, other than the VIE Agreements; and (iii) resolve to or procure the VIE to: (a) change its registered capital; (b) amend its articles of association; (c) change any of its shareholders; (d) appoint, remove or replace its senior management; (e) make or receive investment of any kind or merge or consolidate with any entity; (f) change information filed at the competent authorities in the PRC; (g) make any lending or borrowing or provide security of any kind; (h) pay, make or declare any dividend, charge, fee or other distribution of any kind; (i) incure, create or permit to subsist or have any outstanding financial indebtedness; (j) enter into any agreements that conflict with the JiuGe Technology Call Option Agreement; or (k) do any acts that would adversely impair the VIE’s ability to perform the obligations under the VIE Agreements. Neither Ms. Li Li nor the VIE may assign any of its rights and obligations under the agreement without the prior written consent of WFOE or unilaterally terminate the agreement. This agreement is one of the guarantees for WFOE and investors to ensure that the VIE will not have any potential equity changes that endanger the rights and interests of WFOE and investors; and | |