Blueprint

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

(Mark

One)

☑

ANNUAL REPORT PURSUANT TO SECTION

13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF

1934

For the

quarterly period ended June 30, 2017

or

☐

TRANSITION REPORT PURSUANT TO

SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF

1934

For the

transition period from ____________________to

____________________

333-194748

Commission

file number

HotApp International, Inc.

(Exact

name of registrant as specified in its charter)

|

Delaware

|

|

45-4742558

|

|

(State

or other jurisdiction of incorporation or

organization)

|

|

(I.R.S.

Employer Identification No.)

|

|

|

|

|

|

4800 Montgomery Lane, Suite 210, Bethesda MD

|

|

20814

|

|

(Address

of principal executive offices)

|

|

(Zip

Code)

|

301-971-3940

(Registrant’s

telephone number, including area code)

Indicate

by check mark whether the registrant (1) has filed all reports

required by Section 13 or 15(d) of the Securities Exchange Act of

1934 during the preceding 12 months (or for such shorter period

that the registrant was required to file such reports), and (2) has

been subject to such filing requirements for the past 90

day. Yes ☑

No ☐

Indicate

by check mark whether the registrant has submitted electronically

and posted on its corporate Web site, if any, every Interactive

Data File required to be submitted and posted pursuant to Rule 405

of Regulation S-T (§232.405 of this chapter) during the

preceding 12 months (or for such shorter period that the registrant

was required to submit and post such files).

Yes

☐ No ☐

Indicate

by check mark whether the registrant is a large accelerated filer,

an accelerated filer, a non-accelerated filer, smaller reporting

company, or an emerging growth company. See the definitions of

“large accelerated filer,” “accelerated

filer”, “smaller reporting company” and "emerging

growth company" in Rule 12b-2 of the Exchange Act. (Check

one):

|

Large accelerated filer

|

☐

|

Accelerated filer

|

☐

|

|

Non-accelerated

filer

|

☐

(Do not check if a smaller reporting company)

|

Smaller reporting company

|

☒

|

|

|

|

Emerging

growth company

|

☒

|

If an

emerging growth company, indicate by check mark if the registrant

has elected not to use the extended transition period for complying

with any new or revised financial accounting standards provided

pursuant to Section 13(a) of the Exchange Act.

☐

Indicate

by check mark whether the registrant is a shell company (as defined

in Rule 12b-2 of the Exchange Act). Yes ☐ No

☑

Indicate

the number of shares outstanding of each the registrant’s

classes of common stock, as of the latest practicable date. As of

August 14, 2017, there were 506,898,576 shares outstanding of the

registrant’s common stock $0.0001 par value.

Throughout this Report on Form 10-Q, the terms

“Company,” “we,” “us” and

“our” refer to HotApp International, Inc., and

“our board of directors” refers to the board of

directors of HotApp International, Inc.

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

This

report contains forward-looking statements that involve a number of

risks and uncertainties. Although our forward-looking statements

reflect the good faith judgment of our management, these statements

can be based only on facts and factors of which we are currently

aware. Consequently, forward-looking statements are inherently

subject to risks and uncertainties. Actual results and outcomes may

differ materially from results and outcomes discussed in the

forward-looking statements.

Forward-looking

statements can be identified by the use of forward-looking words

such as “may,” “will,”

“should,” “anticipate,”

“believe,” “expect,” “plan,”

“future,” “intend,” “could,”

“estimate,” “predict,” “hope,”

“potential,” “continue,” or the negative of

these terms or other similar expressions. Such forward-looking

statements are based on our management’s current plans and

expectations and are subject to risks, uncertainties and changes in

plans that may cause actual results to differ materially from those

anticipated in the forward-looking statements. You should be aware

that, as a result of any of these factors materializing, the

trading price of our common stock may decline. These factors

include, but are not limited to, the following:

|

|

●

|

the

availability and adequacy of capital to support and grow our

business;

|

|

|

●

|

economic,

competitive, business and other conditions in our local and

regional markets;

|

|

|

●

|

actions

taken or not taken by others, including competitors, as well as

legislative, regulatory, judicial and other governmental

authorities;

|

|

|

●

|

competition

in our industry;

|

|

|

●

|

changes

in our business and growth strategy, capital improvements or

development plans;

|

|

|

●

|

the

availability of additional capital to support development;

and

|

|

|

●

|

other

factors discussed elsewhere in this annual report.

|

The

cautionary statements made in this quarterly report are intended to

be applicable to all related forward-looking statements wherever

they may appear in this report.

We urge

you not to place undue reliance on these forward-looking

statements, which speak only as of the date of this report. We

undertake no obligation to publicly update any forward

looking-statements, whether as a result of new information, future

events or otherwise.

TABLE OF CONTENTS

|

PART I

|

FINANCIAL INFORMATION

|

4

|

|

ITEM 1.

|

INTERIM FINANCIAL STATEMENTS

|

4

|

|

CONDENSED CONSOLIDATED BALANCE SHEETS AS OF JUNE 30, 2017

(UNAUDITED) AND DECEMBER 31, 2016

|

5

|

|

CONDENSED CONSOLIDATED STATEMENTS OF OPERATIONS AND COMPREHENSIVE

LOSS FOR THE THREE AND SIX MONTHS ENDED JUNE 30, 2017 AND 2016

(UNAUDITED)

|

6

|

|

CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS FOR THE SIX MONTHS

ENDED JUNE 30, 2017 AND 2016 (UNAUDITED)

|

7

|

|

NOTES TO INTERIM CONDENSED CONSOLIDATED FINANCIAL

STATEMENTS

|

8

|

|

ITEM 2.

|

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION

AND RESULTS OF OPERATIONS.

|

13

|

|

ITEM 3.

|

QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET

RISK

|

17

|

|

ITEM 4.

|

CONTROLS AND PROCEDURES

|

17

|

|

PART II

|

OTHER INFORMATION

|

19

|

|

ITEM 1.

|

LEGAL PROCEEDINGS

|

19

|

|

ITEM 1A.

|

RISK FACTORS

|

19

|

|

ITEM 2.

|

UNREGISTERED SALES OF EQUITY SECURITIES AND USE OF

PROCEEDS

|

19

|

|

ITEM 3.

|

DEFAULTS UPON SENIOR SECURITIES

|

19

|

|

ITEM 4.

|

MINE SAFETY DISCLOSURES

|

19

|

|

ITEM 5.

|

OTHER INFORMATION

|

19

|

|

ITEM 6.

|

EXHIBITS

|

19

|

INTERIM

FINANCIAL STATEMENTS

|

Condensed

Consolidated Balance Sheets as of June 30, 2017 (unaudited) and

December 31, 2016

|

|

4

|

|

|

|

|

|

Condensed

Consolidated Statements of Operations and Comprehensive Loss for

the three and six months ended June 30, 2017 and 2016

(unaudited)

|

|

5

|

|

|

|

|

|

Condensed

Consolidated Statements of Cash Flows for the six months ended June

30, 2017 and 2016 (unaudited)

|

|

6

|

|

|

|

|

|

Notes

to Condensed Consolidated Financial Statements

|

|

7

|

HOTAPP INTERNATIONAL, INC.

CONDENSED CONSOLIDATED BALANCE SHEETS AS OF JUNE

30, 2017 (UNAUDITED) AND DECEMBER 31, 2016

|

|

|

|

|

ASSETS

|

|

|

|

|

|

|

|

CURRENT

ASSETS:

|

|

|

|

Cash and cash

equivalents

|

$144,720

|

$102,776

|

|

Account

receivable

|

37,602

|

-

|

|

Costs in excess of

billings

|

-

|

30,332

|

|

Prepaid

expenses

|

14,987

|

4,650

|

|

Deposit and other

receivable

|

13,381

|

19,745

|

|

TOTAL CURRENT

ASSETS

|

210,690

|

157,503

|

|

|

|

|

|

Fixed assets,

net

|

36,990

|

46,096

|

|

TOTAL

ASSETS

|

$247,680

|

$203,599

|

|

|

|

|

|

LIABILITIES

AND STOCKHOLDERS' EQUITY (DEFICIT)

|

|

|

|

|

|

|

|

CURRENT

LIABILITIES:

|

|

|

|

Accounts payable

and accrued expenses

|

$205,986

|

$238,315

|

|

Accrued taxes and

franchise fees

|

7,742

|

7,742

|

|

Amount due to

related parties

|

519,058

|

455,857

|

|

TOTAL CURRENT

LIABILITIES

|

732,786

|

701,914

|

|

|

|

|

|

TOTAL

LIABILITIES

|

732,786

|

701,914

|

|

|

|

|

|

STOCKHOLDERS'

EQUITY (DEFICIT):

|

|

|

|

Preferred stock,

$0.0001 par value, 15,000,000 shares authorized, 0 and 13,800,000

issued and outstanding

|

-

|

1,380

|

|

Common stock,

$.0001 par value, 1,000,000,000 and 500,000,000 shares authorized,

506,898,576 and 5,909,687 shares issued and outstanding, as of June

30, 2017 and December 31, 2016, respectively

|

50,690

|

591

|

|

Accumulated other

comprehensive loss

|

(194,997)

|

(73,330)

|

|

Additional paid-in

capital

|

4,604,191

|

4,202,020

|

|

Accumulated

deficit

|

(4,944,990)

|

(4,628,976)

|

|

TOTAL

STOCKHOLDERS' EQUITY (DEFICIT)

|

(485,106)

|

(498,315)

|

|

TOTAL

LIABILITIES AND STOCKHOLDERS' EQUITY

|

$247,680

|

$203,599

|

The

accompanying notes to the consolidated financial statements are an

integral part of these statements.

HOTAPP INTERNATIONAL, INC.

CONDENSED CONSOLIDATED

STATEMENTS OF OPERATIONS AND COMPREHENSIVE LOSS FOR THE THREE AND

SIX MONTHS ENDED JUNE 30, 2017 AND 2016 (UNAUDITED)

|

|

Quarter Ended

June 30, 2017

|

Quarter Ended

June 30, 2016

|

Six Months Ended

June 30, 2017

|

Six Months Ended

June 30, 2016

|

|

|

|

|

|

|

|

Revenues:

|

|

|

|

|

|

Project

fee

|

$37,758

|

$-

|

$103,936

|

$-

|

|

|

37,758

|

-

|

103,936

|

-

|

|

|

|

|

|

|

|

Cost

of revenues

|

2,459

|

-

|

16,564

|

-

|

|

|

|

|

|

|

|

Gross

profit

|

$35,299

|

$-

|

$87,372

|

$-

|

|

|

|

|

|

|

|

Operating

expenses:

|

|

|

|

|

|

Research and

product development

|

$50,109

|

$65,440

|

$102,771

|

$203,887

|

|

Sales and

marketing

|

-

|

(59)

|

-

|

(64,635)

|

|

Deposits written

off

|

17

|

-

|

2,680

|

-

|

|

Depreciation

|

9,431

|

9,866

|

18,067

|

24,075

|

|

Loss on disposal of

fixed assets

|

131

|

-

|

131

|

-

|

|

General and

administrative

|

200,657

|

124,578

|

388,159

|

370,283

|

|

Total

operating expenses

|

260,345

|

199,825

|

511,808

|

533,160

|

|

|

|

|

|

|

|

(Loss)

from operations

|

(225,046)

|

(199,825)

|

(424,436)

|

(533,160)

|

|

|

|

|

|

|

|

Other

income / expense:

|

|

|

|

|

|

Interest

income

|

1

|

1

|

1

|

1

|

|

Foreign exchange

(loss) / gain

|

42,849

|

111,750

|

108,421

|

112,504

|

|

Total

other income (expenses)

|

42,850

|

111,751

|

108,422

|

112,505

|

|

|

|

|

|

|

|

Loss

before taxes

|

(182,196)

|

(88,074)

|

(316,014)

|

(421,105)

|

|

Income tax

provision

|

-

|

-

|

-

|

7,037

|

|

Net

loss applicable to common shareholders

|

$(182,196)

|

$(88,074)

|

$(316,014)

|

$(428,142)

|

|

|

|

|

|

|

|

Net loss per share

- basic and diluted

|

$(0.00)

|

$(0.01)

|

$(0.00)

|

$(0.07)

|

|

|

|

|

|

|

|

Weighted number of

shares outstanding -

|

|

|

|

|

|

Basic and

diluted

|

122,807,094

|

5,909,687

|

64,358,391

|

5,909,687

|

|

|

|

|

|

|

|

Comprehensive

Income Loss:

|

|

|

|

|

|

Net

loss

|

$(182,196)

|

$(88,074)

|

$(316,014)

|

$(428,142)

|

|

Foreign currency

translation gain (loss)

|

(37,663)

|

(111,078)

|

(121,667)

|

(114,321)

|

|

Total

comprehensive loss

|

$(219,859)

|

$(199,152)

|

$(437,681)

|

$(542,463)

|

The

accompanying notes to the consolidated financial statements are an

integral part of these statements.

HOTAPP INTERNATIONAL, INC.

CONDENSED CONSOLIDATED

STATEMENTS OF CASH FLOWS FOR THE SIX MONTHS ENDED JUNE 30, 2017 AND

2016 (UNAUDITED)

|

|

Six Months Ended

June 30, 2017

|

Six Months Ended

June 30, 2016

|

|

CASH

FLOWS FROM OPERATING ACTIVITIES:

|

|

|

|

Net

Loss

|

$(316,014)

|

$(428,142)

|

|

|

|

|

|

Adjustments

to reconcile net loss to cash used in operating

activities:

|

|

|

|

Depreciation

|

18,067

|

24,075

|

|

Deposit written

off

|

2,680

|

-

|

|

Loss on disposal of

fixed asset

|

131

|

-

|

|

Foreign exchange

transaction gain

|

(108,421)

|

(112,504)

|

|

|

|

|

|

Change

in operating assets and liabilities:

|

|

|

|

Costs in excess of

billings and account receivable

|

(7,270)

|

-

|

|

Security deposit

and other receivables

|

3,684

|

-

|

|

Prepaid

expenses

|

(10,337)

|

27,071

|

|

Accounts payable

and accrued expenses

|

(32,329)

|

(40,003)

|

|

Accrued taxes

payable and franchise fees

|

-

|

7,036

|

|

Net

cash used in operating activities

|

$(449,809)

|

$(522,467)

|

|

|

|

|

|

CASH

FLOW FROM INVESTING ACTIVITIES:

|

|

|

|

Acquisition of

fixed asset

|

(9,092)

|

(1,668)

|

|

Disposal of fixed

assets

|

-

|

93,768

|

|

Net

cash (used in)/provided by investing activities

|

$(9,092)

|

$92,100

|

|

|

|

|

|

CASH

FLOW FROM FINANCING ACTIVITIES:

|

|

|

|

Advance from

affiliate

|

514,091

|

-

|

|

Net

cash provided by financing activities

|

$514,091

|

$-

|

|

|

|

|

|

|

|

|

|

NET

DECREASE IN CASH

|

55,190

|

(430,367)

|

|

Effects of exchange

rates on cash

|

(13,246)

|

(1,817)

|

|

|

|

|

|

CASH

AND CASH EQUIVALENTS at beginning of period

|

102,776

|

495,136

|

|

CASH

AND CASH EQUIVALENTS at end of period

|

$144,720

|

$62,952

|

|

|

|

|

|

Supplemental

disclosure of cash flow information

|

|

|

|

Cash paid

for:

|

|

|

|

Interest

|

$-

|

$-

|

|

Income

Taxes

|

$-

|

$-

|

|

|

|

|

|

Supplemental

schedule of non-cash investing and financing

activities

|

|

|

|

Conversion of

shareholder loan into common stock

|

$450,890

|

$-

|

|

|

|

|

The

accompanying notes to the consolidated financial statements are an

integral part of these statements.

HOTAPP INTERNATIONAL, INC.

NOTES

TO INTERIM CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

Note 1. The Company History and Nature of the Business

Hotapp

International, Inc., formerly Fragmented Industry Exchange, Inc.,

(the “Company” or “Group”) was incorporated

in the State of Delaware on March 7, 2012 and established a fiscal

year end of December 31st. The Company’s initial business

plan was to be a financial acquisition intermediary which would

serve buyers and sellers for companies that are in highly

fragmented industries. The Company determined it was in the best

interest of the shareholders to expand its business plan. On

October 15, 2014, through a sale and purchase agreement (the

“Purchase Agreement”) the Company acquired all the

issued and outstanding stock of HotApps International Pte Ltd (the

“HIP”) from Singapore eDevelopment Limited

(“SeD”). HIP owned certain intellectual property

relating to instant messaging for portable devices (the

“HotApp”). HotApp is a cross-platform mobile

application that incorporates instant messaging and ecommerce. It

provides a messaging and calling services for HotApp users (text,

photo, audio). HotApp can be used on any mobile platform (i.e. IOS

Online or Android).

Pursuant

to a Purchase Agreement, the Company issued SeD 1,000,000 shares of

common stock and 13,800,000 shares of newly created convertible

preferred stock. See Note 5 for further description.

As of

June 30, 2017, details of the Company’s subsidiaries are as

follows:

|

Subsidiaries

|

Date of Incorporation

|

Place of Incorporation

|

Percentage of Ownership

|

|

1st Tier Subsidiary:

|

|

|

|

|

HotApps

International Pte Ltd (“HIP”)

|

May 23,

2014

|

Republic

of Singapore

|

100% by

Company

|

|

2nd Tier Subsidiaries:

|

|

|

|

|

HotApps

Call Pte Ltd

|

September

15, 2014

|

Republic

of Singapore

|

100%

owned by HIP

|

|

HotApps

Information Technology Co Ltd

|

November

10, 2014

|

People’s

Republic of China

|

100%

owned by HIP

|

|

HotApp

International Limited*

|

July 8,

2014

|

Hong

Kong (Special Administrative Region)

|

100%

owned by HIP

|

* On

March 25, 2015, HotApps International Pte Ltd acquired 100% of

issued share capital in HotApp International Limited.

The

financial statements have been prepared using accounting principles

generally accepted in the United States of America applicable for a

going concern, which assumes that the Company will realize its

assets and discharge its liabilities in the ordinary course of

business. Since inception, the Company has incurred net losses of

$4,944,990 and has net working capital deficit of $522,096 at June

30, 2017. Management has concluded that due to the conditions

described above, there is substantial doubt about the entities

ability to continue as a going concern through August 14, 2018. We

have evaluated the significance of the conditions in relation to

our ability to meet our obligations and believe that our current

cash balance along with our current operations will not provide

sufficient capital to continue operation through 2017. Our ability

to continue as a going concern is dependent upon achieving sales

growth, the management of operating expenses and the ability of the

Company to obtain the necessary financing to meet its obligations

and pay its liabilities arising from normal business operations

when they come due, and upon profitable operations.

Our

majority shareholder has advised us not to depend solely on it for

financing. We have increased our efforts to raise additional

capital through equity or debt financing from other

sources. However, we cannot be certain that such capital (from

our shareholders or third parties) will be available to us or

whether such capital will be available on terms that are acceptable

to us. Any such financing likely would be dilutive to existing

stockholders and could result in significant financial operating

covenants that would negatively impact our business. If

we are unable to raise sufficient additional capital on acceptable

terms, we will have insufficient funds to operate our business or

pursue our planned growth.

These

financial statements do not include any adjustments relating to the

recoverability and classification of recorded asset amounts, or

amounts and classification of liabilities that might result from

this uncertainty.

Note 2. Summary of Significant Accounting Policies

Basis of presentation

The

condensed consolidated balance sheet at December 31, 2016 was

derived from audited financial statement but does not include all

disclosures required by accounting principles generally accepted in

the United States of America. The other information in these

condensed financial statements are unaudited but, in the opinion of

management, reflect all adjustments necessary for a fair

presentation of the results for the periods covered. All such

adjustments are of a normal recurring nature unless disclosed

otherwise. These condensed financial statements, including notes,

have been prepared in accordance with the applicable rules of the

Securities and Exchange Commission

and do not include all of the information and disclosures required

by accounting principles generally accepted in the United States of

America for complete financial statements. These condensed

financial statements should be read in conjunction with the

financial statements and additional information as contained in our

Annual Report on Form 10-K for the year ended December 31,

2016.

Basis of consolidation

The

consolidated financial statements of the Group include the

financial statements of Hotapp International, Inc. and its

subsidiaries. All inter-company transactions and

balances have been eliminated upon consolidation.

Use of estimates

The

preparation of financial statements in conformity with U.S. GAAP

requires management to make estimates and assumptions that affect

the reported amounts of assets and liabilities and revenues, cost

and expenses in the financial statements and accompanying notes.

Significant accounting estimates reflected in the Group’s

consolidated financial statements include revenue recognition, the

useful lives and impairment of property and equipment, valuation

allowance for deferred tax assets and share-based

compensation.

Cash and cash equivalents

Cash

and cash equivalents consist of cash on hand and highly liquid

investments, which are unrestricted from withdrawal or use, or

which have original maturities of three months or less when

purchased.

Foreign currency risk

Because

of its foreign operations, the Company holds cash in non-US

dollars. As of June 30, 2017, cash and cash equivalents of the

Group include, on an as converted basis to US dollars $51,697,

$59,940 and $18,790 in Hong Kong Dollars (“HK$”),

Reminbi (“RMB”) and Singapore Dollars

(“S$”), respectively.

The

Renminbi (“RMB”) is not a freely convertible

currency. The State Administration for Foreign Exchange, under

the authority of the People’s Bank of China, controls the

conversion of RMB into foreign currencies. The value of the RMB is

subject to changes in central government policies and to

international economic and political developments affecting supply

and demand in the China Foreign Exchange Trading System

market.

Concentration of credit risk

Financial

instruments that potentially expose the Group to concentration of

credit risk consist primarily of cash and cash

equivalents. The Group places their cash with financial

institutions with high-credit ratings and quality.

Fixed assets, net

Property

and equipment are stated at cost less accumulated depreciation.

Depreciation is calculated on a straight-line basis over the

following estimated useful lives:

|

Office

equipment

|

3

years

|

|

Computer

equipment

|

3

years

|

|

Furniture

and fixtures

|

3

years

|

|

Motor

vehicles

|

10

years

|

Fair value

Fair

value is the price that would be received from selling an asset or

paid to transfer a liability in an orderly transaction between

market participants at the measurement date. When determining the

fair value measurements for assets and liabilities required or

permitted to be recorded at fair value, the Group considers the

principal or most advantageous market in which it would transact

and it considers assumptions that market participants would use

when pricing the asset or liability.

Revenue recognition

The

Group recognizes revenue when persuasive evidence of an arrangement

exists, delivery has occurred, the sales price is fixed or

determinable, and collectability is reasonably assured. The Group

currently has $103,936 revenue from its services rendered on

projects, and plans to derive its revenue from membership

subscription services, offering the platform for Enterprise

Collaboration with integration. Revenue is currently recognized

under contract accounting due to the significant software

production required, and the percentage-of-completion method is

used in accordance with ASC 605-35. The Company is recognizing the

percentage-of-completion based on input measures that measured

directly from expenses incurred, and management reviews the

progress to completion. In case of the 3% iGalen revenue sharing,

revenue is recognized in accordance with ASC

985-605-25.

Research and development expenses

Research

and development expenses primarily consist of (i) salaries and

benefits for research and development personnel, and

(ii) office rental, general expenses and depreciation expenses

associated with the research and development

activities. The Company’s research and development

activities primarily consist of the research and development of new

features for its mobile platform and its self-developed mobile

games. Expenditures incurred during the research phase are expensed

as incurred.

Income taxes

Current

income taxes are provided for in accordance with the laws of the

relevant tax authorities. Deferred income taxes are

recognized when temporary differences exist between the tax bases

of assets and liabilities and their reported amounts in the

consolidated financial statements. Net operating loss carry

forwards and credits are applied using enacted statutory tax rates

applicable to future years. Deferred tax assets are reduced by a

valuation allowance when, in the opinion of management, it is

more-likely-than-not that a portion of or all of the deferred tax

assets will not be realized. The components of the deferred tax

assets and liabilities are individually classified as current and

non-current based on their characteristics.

The

impact of an uncertain income tax position on the income tax return

is recognized at the largest amount that is more-likely-than-not to

be sustained upon audit by the relevant tax authority. An uncertain

income tax position will not be recognized if it has less than a

50% likelihood of being sustained. Interest and

penalties on income taxes will be classified as a component of the

provisions for income taxes. The Group did not recognize any income

tax due to uncertain tax position or incur any interest and

penalties related to potential underpaid income tax expenses for

the years ended December 31, 2016 or 2015,

respectively.

Uncertainties

exist with respect to the application of the New EIT Law to our

operations, specifically with respect to our tax

residency. The New EIT Law specifies that legal entities

organized outside of the PRC will be considered residents for PRC

income tax purposes if their “de facto management

bodies” as “establishments that carry on substantial

and overall management and control over the operations, personnel,

accounting, properties, etc. of the

Company.” Because of the uncertainties that have

resulted from limited PRC guidance on the issue, it is uncertain

whether our legal entities outside the PRC constitute residents

under the New EIT Law. If one or more of our legal

entities organized outside the PRC were characterized as PRC

residents, the impact would adversely affect our results of

operations.

Foreign currency translation

The

functional and reporting currency of the Company is the United

States dollar (“U.S. dollar”). The financial records of

the Company’s subsidiaries located in Singapore, Hong Kong

and the PRC are maintained in their local currencies, the Singapore

Dollar (S$), Hong Kong Dollar (HK$) and Renminbi ("RMB"),

which are also the functional currencies of these

entities.

Monetary

assets and liabilities denominated in currencies other than the

functional currency are translated into the functional currency at

the rates of exchange ruling at the balance sheet date.

Transactions in currencies other than the functional currency

during the year are converted into functional currency at the

applicable rates of exchange prevailing when the transactions

occurred. Transaction gains and losses are recognized in the

statement of operations.

The

Company’s entities with functional currency of Renminbi, Hong

Kong Dollar and Singapore Dollar, translate their operating results

and financial positions into the U.S. dollar, the Company’s

reporting currency. Assets and liabilities are translated using the

exchange rates in effect on the balance sheet date. Revenues,

expenses, gains and losses are translated using the average rate

for the year. Translation adjustments are reported as cumulative

translation adjustments and are shown as a separate component of

comprehensive income (loss).

For the

six months ended June 30, 2017, the Company recorded other

comprehensive loss from translation loss of $121,667 in the

consolidated financial statements.

Operating leases

Leases

where the rewards and risks of ownership of assets primarily remain

with the lessor are accounted for as operating leases. Payments

made under operating leases are charged to the consolidated

statements of operations on a straight-line basis over the lease

periods.

Comprehensive income (loss)

Comprehensive

income (loss) include gains (losses) from foreign currency

translation adjustments. Comprehensive income (loss) is reported in

the consolidated statements of operations and comprehensive

loss.

Loss per share

Basic

loss per share is computed by dividing net loss attributable to

shareholders by the weighted average number of shares outstanding

during the period.

The

Company's convertible preferred shares are not participating

securities and have no voting rights until converted to common

stock. As of June 30, 2017, no shares of preferred stock are

eligible for conversion into voting common stock.

Recent accounting pronouncements not yet adopted

In May

2014, the Financial Accounting Standards Board (FASB) issued

Accounting Standards Update No. 2014-09, Revenue from Contracts

with Customers (Topic 606) (ASU 2014-09), which amends the existing

accounting standards for revenue recognition. In August 2015, the

FASB issued ASU No. 2015-14, Revenue from Contracts with Customers

(Topic 606): Deferral of the Effective Date, which delays the

effective date of ASU 2014-09 by one year. The FASB also agreed to

allow entities to choose to adopt the standard as of the original

effective date. We do not expect the adoption of this guidance to

have a significant effect on our consolidated financial

statements.

In

November 2015, the FASB issued Accounting Standards Update No.

2015-17, Income Taxes (Topic 740): Balance Sheet Classification of

Deferred Taxes (ASU 2015-17), which simplifies the presentation of

deferred income taxes by requiring deferred tax assets and

liabilities be classified as noncurrent on the balance sheet. The

updated standard is effective for us beginning on January 1, 2017.

We do not expect the adoption of this guidance to have a

significant effect on our consolidated financial

statements.

On Feb.

25, 2016, the Financial Accounting Standards Board (FASB) released

Accounting Standards Update No. 2016-02, Leases (Topic

842) (the Update). The new leasing standard presents dramatic

changes to the balance sheets of lessees. Lessor

accounting is updated to align with certain changes in the

lessee model and the new revenue recognition standard. The Company

does not expect the adoption of ASU No. 2016-02 to have a material

impact on its financial statements.

Note 3. FIXED ASSETS, NET

Fixed

assets, net consisted of the following:

|

|

|

|

|

|

|

|

|

Computer

equipment

|

$73,739

|

$69,442

|

|

Office

equipment

|

20,876

|

19,671

|

|

Furniture and

fixtures

|

10,400

|

7,156

|

|

|

$105,015

|

$96,269

|

|

Less: accumulated

depreciation

|

(68,025)

|

(50,173)

|

|

Fixed assets,

net

|

$36,990

|

$46,096

|

Depreciation

expenses charged to the consolidated statements of operations for

the six months ended June 30, 2017 and 2016 were $18,067 and

$24,075, respectively.

Note 4. ACCOUNTS PAYABLE AND ACCRUED

EXPENSES

Accrued

expenses and other current liabilities consisted of the

following:

|

|

|

|

|

|

|

|

|

Accrued

payroll

|

$175,328

|

$180,464

|

|

Accrued

professional fees

|

12,474

|

45,612

|

|

Other

|

18,184

|

12,239

|

|

Total

|

$205,986

|

$238,315

|

Note 5. SHARE CAPITALIZATION

The

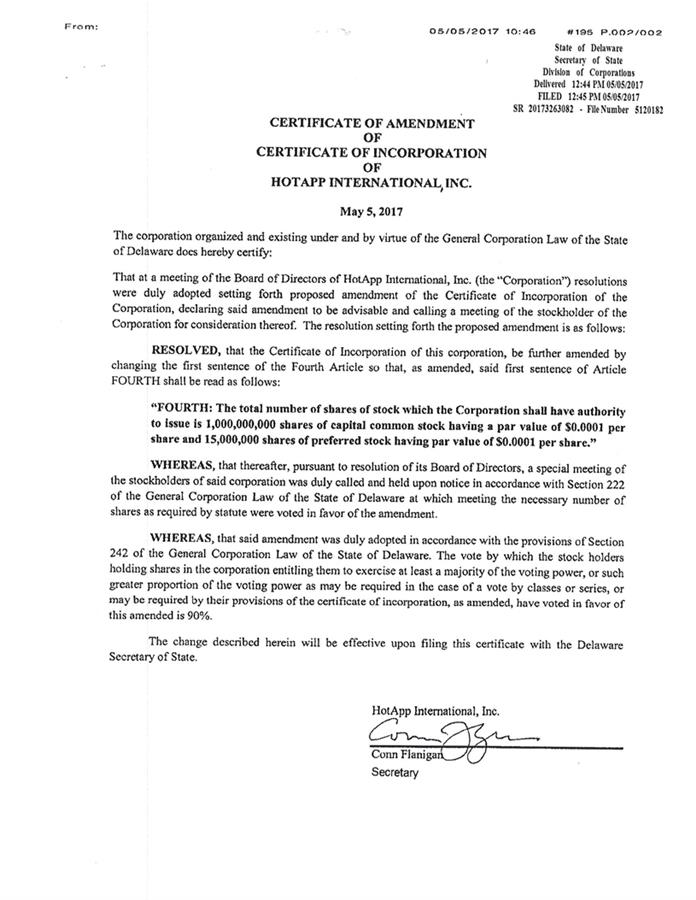

Company is authorized to issue 1 billion shares of common stock and

15 million shares of preferred stock. The authorized share capital

of the Company’s common stock was increased from 500 million

to 1 billion on May 5, 2017. Both share types have a

$0.0001 par value. As of June 30, 2017 and 2016, the

Company had issued and outstanding, 506,898,576 and 5,909,687 of

common stock, respectively and 0 and 13,800,000 shares of preferred

stock, respectively.

Common Shares:

On July

13, 2015, SED acquired 777,687 shares of the Company common stock

by converting outstanding loans made to the Company into common

stock of the Company at a rate of $5.00 per share (rounded to the

nearest full share). After such transactions SED owned 98.17% of

the Company.

On

March 27, 2017, the Company entered into a Loan Conversion

Agreement with SeD, pursuant to which SeD agreed to convert

$450,890 of debt owed by Company to SeD into 500,988,889 common

shares at a conversion price of $0.0009. The captioned shares were

issued on June 9, 2017, and SeD owned 99.979% of the Company after

such transactions.

Preferred Shares:

Pursuant

to the Purchase Agreement, dated October 15, 2014, the Company

issued 1,000,000 shares of common stock to

SED. Such amount represented 19% ownership in the

Company. Pursuant to the Purchase Agreement, dated October

15, 2014, the Company issued 13,800,000 shares of a class of

preferred stock called Perpetual Preferred Stock (“Preferred

Stock”) to SED. The Preferred Stock has no dividend or voting

rights. The Preferred Stock is convertible to common stock of the

Company dependent upon the number of commercial users of the

Software. For each 1,000,000 commercial users of the Software

(without duplication), SED shall have the right to convert

1,464,000 shares of Perpetual Preferred Stock into 7,320,000 shares

of Common Stock, so that there must be a minimum of 9,426,230

commercial users in order for all of the shares of the Perpetual

Preferred Stock to be converted into common stock of the Company

(13,800,000 shares of Preferred Stock convertible into 69,000,000

shares of common stock).

On

March 27, 2017, SeD and the Company entered into a Preferred Stock

Cancellation Agreement, by which SeD agreed to cancel its

13,800,000 shares Perpetual Preferred Stock issued by the Company.

On June 8, 2017, a Certificate of Retirement for 13,800,000 shares

of the Perpetual Preferred Stock has been filed to the office of

Secretary of State of the State of Delaware.

Other

than the conversion rights described above, the Preferred Stock has

no voting, dividend, redemption or other rights.

Note

6. COMMITMENTS AND CONTINGENCIES

On May

9, 2016, the Company entered into a lease agreement for 1,231

square feet of office space in Guangzhou, China. The lease

commenced on May 9, 2016 and runs through May 8, 2018 with monthly

payments of $2,279. The Company was required to put up a security

deposit of $4,557. For the six months ended June 30, 2017, the

Company recorded rent expense of $13,513 for the Guangzhou

office.

On

April 10, 2015, the Company entered into a lease agreement for 347

square feet of office space in Kowloon, Hong Kong. This lease

commenced on April 20, 2015 and runs through April 19, 2017 with

monthly payments of $2,574. The Company was required to put up a

security deposit of $5,147. On March 16, 2017, the Company entered

into a lease agreement for 1,504 square feet of office space in

Kowloon, Hong Kong. This lease commenced on March 16, 2017 and runs

through March 31, 2019 with monthly payments of $3,266. The Company

was required to put up a security deposit of $6,533. For the six

months ended June 30, 2017, the Company recorded rent expense of

$20,721 for these offices.

The

following is a schedule by years of future minimum lease

payments:

|

2017

|

$30,992

|

|

2018

|

9,800

|

|

Total

|

$40,792

|

|

|

|

Note 7. RELATED PARTY BALANCES AND

TRANSACTIONS

For the

period up to June 21, 2017 covered by this report, Mr. Chan Heng

Fai was the Company’s Chief Executive Officer (CEO) and a

member of the Board. Mr. Chan is also the Chief Executive Officer

of Singapore eDevelopment Limited (“SeD”), a Singapore

company. SeD is the majority shareholder of the

Company. On June 21, 2017, Mr. Chan voluntarily resigned as CEO and

President of the Company, and will remain as Chairman of the Board.

On June 21, 2017, the Company appointed Mr. Lum Kan Fai as the

Company’s CEO and President. The Company’s other two

directors included Mr. Lum Kan Fai, who served as the

Company’s Chief Technology Officer during the period covered

by this report and who has entered into an employment arrangement

with the Company’s wholly owned subsidiary, HotApp

International Limited. As of the date of this report, the

Company has not entered into any employment arrangement with any

director or officer.

Note 8. SUBSEQUENT EVENT

The

Company has evaluated subsequent events through the date that the

financials were issued.

MANAGEMENT’S

DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF

OPERATIONS.

FORWARD-LOOKING STATEMENTS

Certain matters discussed herein are forward-looking statements.

Such forward-looking statements contained in this Form 10-Q involve

risks and uncertainties, including statements as to:

|

1.

|

|

our

future operating results;

|

|

2.

|

|

our

business prospects;

|

|

3.

|

|

any

contractual arrangements and relationships with third

parties;

|

|

4.

|

|

the

dependence of our future success on the general

economy;

|

|

5.

|

|

any

possible financings; and

|

|

6.

|

|

the

adequacy of our cash resources and working

capital.

|

These forward-looking statements can generally be identified as

such because the context of the statement will include words such

as we “believe,” “anticipate,”

“expect,” “estimate” or words of similar

meaning. Similarly, statements that describe our future

plans, objectives or goals are also forward-looking statements.

Such forward-looking statements are subject to certain

risks and uncertainties which are described in close proximity to

such statements and which could cause actual results to differ

materially from those anticipated as of the date of filing of this

Form 10-Q. Shareholders, potential investors and other

readers are urged to consider these factors in evaluating the

forward-looking statements and are cautioned not to place undue

reliance on such forward-looking statements. The

forward-looking statements included herein are only made as of the

date of filing of this Form 10-Q, and we undertake no obligation to

publicly update such forward-looking statements to reflect

subsequent events or circumstances.

This discussion contains forward-looking statements that reflect

our plans, estimates and beliefs. Our actual results may differ

materially from those anticipated in these forward-looking

statements.

Background

Hotapp

International, Inc., formerly Fragmented Industry Exchange Inc.,

(the “Company” or “Group”) was incorporated

in the State of Delaware on March 7, 2012 and established a fiscal

year end of December 31st. The Company’s initial business

plan was to be a financial acquisition intermediary which would

serve buyers and sellers for companies that are in highly

fragmented industries. The Company determined it was in the best

interest of the shareholders to expand its business plan. On

October 15, 2014, through a sale and purchase agreement (the

“Purchase Agreement”) the Company acquired all the

issued and outstanding stock of HotApps International Pte Ltd (the

“HIP”) from Singapore eDevelopment Limited

(“SeD”). HIP owned certain intellectual property

relating to instant messaging for portable devices (the

“HotApp”). HotApp is a cross-platform mobile

application that incorporates instant messaging and ecommerce. It

provides a messaging and calling services for HotApp users (text,

photo, audio). HotApp can be used on any mobile platform (i.e. IOS

Online or Android).

As of

June 30, 2017, details of the Company’s subsidiaries are as

follows:

|

Subsidiaries

|

Date of Incorporation

|

Place of Incorporation

|

Percentage of Ownership

|

|

1st Tier Subsidiary:

|

|

|

|

|

HotApps

International Pte Ltd (“HIP”)

|

May 23,

2014

|

Republic

of Singapore

|

100% by

Company

|

|

2nd Tier Subsidiaries:

|

|

|

|

|

HotApps

Call Pte Ltd

|

September

15, 2014

|

Republic

of Singapore

|

100%

owned by HIP

|

|

HotApps

Information Technology Co Ltd

|

November

10, 2014

|

People’s

Republic of China

|

100%

owned by HIP

|

|

HotApp

International Limited*

|

July 8,

2014

|

Hong

Kong (Special Administrative Region)

|

100%

owned by HIP

|

* On

March 25, 2015, HotApps International Pte Ltd acquired 100% of

issued share capital in HotApp International Limited.

The

Group has relied significantly on SeD as its principal sources of

funding during the year. The Board has, in the meantime, reviewed

and approved the restructuring of HotApp, by which has since

reduced by half its personnel resources as compared to 2015. HotApp

has revamped its business model and technology platform to focus on

business-to-business (“B2B”) services, built around

enterprise communications and workflow. Its product line will

target these industries: (i) network and direct marketing; (ii)

enterprise Voice-over-IP; (iii) enterprise messaging; (iv) real

estate; (v) social media; (vi) e-commerce; (vii) investor

relations; (viii) healthcare and wellness; and (ix) hospitality,

combining HotApp applications with hotel-room management. This

strategic shift is intended to create commercial value with a

sharper focus.

Our Business

HotApp,

our software application, is a community communications ecosystem

(the “Platform”), connecting users who wish to seek out

both local and global communities (“Users” or

“Communities”) and equipping them with necessary tools

to communicate effectively across borders. HotApp will monetize the

relationship between brands, Online-2-Offline (“O2O”)

operators and service providers (collectively,

“Enterprises”) and the HotApp Communities, and in the

process mediate something of value to both parties.

With

our Platform, users can discover and build their own communities

and create valuable content. Our Platform tools empower these

communities to share their thoughts and words across multiple

channels. As these communities grow, they provide the critical mass

that attracts enterprises. Enterprises in turn enhance user

experience with premium contents, all of which are facilitated by

the transactions of every stakeholder via e-commerce.

Trends in the Market and Our Opportunity

According

to a November 2016 forecast by eMarketer, a leading research

company for digital business professionals, more than one-quarter

of the world’s population will be using mobile messaging apps

by 2019. eMarketer also projected that mobile phone messaging apps

would be used by more than 1.4 billion people in 2016, an increase

of almost 16% from 2015. The Asia-Pacific region is home to more

than 50% of all chat app users worldwide, with more than 805

million consumers in 2016.

In

addition to the substantial opportunities in consumer messaging

market, Enterprise Messaging and Collaboration Services and Apps

are widely deployed in Small Medium Enterprises (SMEs) and Large

Enterprise as an alternative to Email and Intranet. This emerging

need in Enterprise Messaging and Collaboration offers a huge

opportunity for IT service providers in offering development,

integration and white label services for SMEs and Corporations.

According to Statista, global messaging platform service providers

are expected to bring in US$1.8 billion revenue riding on the

growth in growing demand of Enterprise Messaging.

Based

upon the above trends, we believe significant opportunities

exist for:

●

Enterprise

deploying messaging platform to effective engage different

stakeholders.

●

Continuing growth

in demand for OTT Services encapsulated within a single mobile app

with a clear intent and objectives fulfilling the communication

need for specific communities and industries.

●

Enterprises to

increase usage of OTT Services, such as adoption of Enterprise

messaging Apps alongside with using of email, video and audio

conferencing, collaboration through cloud services, as a new medium

for different stakeholder engagement including customers, to

promote and market their products and services (Collaboration

Framework). HotApp’s approach in white labelling for the

enterprises will augment and fill this demand in the market. White

label refers to packaging HotApp solution under brand name of

clients with some content being customized only for

clients.

●

Industries such as

Network Marketing and Hospitality and Franchising businesses are

utilizing OTT Services to reach out effectively to their marketing

network on a global basis.

Our Plan of Operations and Growth Strategy

We

believe that we have significant opportunities to further enhance

the value we deliver to our Users. We intend

to pursue the following growth strategy:

●

Position HotApp as

an open platform to be ready for integration with third party

technology partnerships such as Payment Services, Loyalty Programs,

and e-commerce.

●

Engage

Mobile App Integration Opportunities for Enterprises globally

through “Powered by HotApp” initiatives, enabling

Offline businesses to go On Line (O2O) with HotApp technology

support. Powered by HotApp, is a business initiative from HotApp

International, that offers modules in HotApp technology for service

and customization, targeting vertical industry such as Hospitality

and Real Estate Agencies.

●

Identify Strategic

Partnership Opportunities globally through “Powered by HotApp ” initiatives,

enabling Offline businesses to go On Line (O2O) with HotApp

technology support.

●

Establish

community and business partnerships (collectively, “HotApp

Partnerships”) to expand our user base and

engagement.

Results of Operations

Summary of Key Results

For the unaudited three months period ending June 30, 2017 and

2016

Revenue

Revenue

consist primarily of the service rendered on projects which require

significant software production. Total revenue for the three months

ended June 30, 2017 and 2016 were $37,758 and $0

respectively.

Cost of revenue

Cost of

revenue consist primarily of salary and outside consulting expenses

incurred directly to the projects. Total cost of revenue for the

three months ended June 30, 2017 and 2016 were $2,459 and $0,

respectively.

Research and Development Expense

Research

and development expenses consists primarily of salary and

benefits. Expenditures incurred during the

research phase are expensed as incurred. We expect

our research and development expenses to maintain with moderate

changes in line with business activities. Total research

and development for the quarters ended June 30, 2017 and 2016

were $50,109 and $65,440, respectively. The

decrease was due to the reduction of development staff which is in

line with the streamlining and restructuring of the

Company.

Sales and Marketing Expense

Sales

and marketing expenses consist primarily of third party

professional service providers. We expect our sales and marketing

expenses to maintain with moderate changes in line with business

activities. Total sales and marketing expenses for the quarters

ended June 30, 2017 and 2016 were $0 and ($59), respectively. The

negative ($59) was due to a reversal of $65,252 provision for

HotApp Credit Points because the program was

eliminated.

General and Administrative

General

and administrative expenses consist primarily of salary and

benefits, professional fees and rental expense. Total general and

administrative expenses for the quarters ended June 30, 2017 and

2016 were $200,657 and $124,578, respectively. The increase

was mainly due to the increase in salary and benefits.

Other Expense (Income)

In the

quarters ended June 30, 2017 and 2016, we have incurred $9,431 and

$9,866 for depreciation, $17 and $0 for the deposits written off,

and $131 and $0 for loss on disposal of fixed assets. In the

quarters ended June 30, 2017 and 2016, we have incurred $(42,849)

and $(111,750) in foreign exchange gain, and $(1) and $(1) in

interest income.

For the unaudited six months period ending June 30, 2017 and

2016

Revenue

Revenue

consist primarily of the service rendered on projects which require

significant software production. Total revenue for the six months

ended June 30, 2017 and 2016 were $103,936 and $0

respectively.

Cost of revenue

Cost of

revenue consist primarily of salary and outside consulting expenses

incurred directly to the projects. Total cost of revenue for the

six months ended June 30, 2017 and 2016 were $16,564 and $0,

respectively.

Research and Development Expense

Research

and development expenses consists primarily of salary and

benefits. Expenditures incurred during the

research phase are expensed as incurred. Total research

and development for the six months ended June 30, 2017 and 2016

were $102,771 and $203,887, respectively. The

decrease was mainly due to the reduction of development staff which

is in line with the streamlining and restructuring of

Company.

Sales and Marketing Expense

Sales

and marketing expenses consist primarily of third party

professional service providers. We expect our sales and marketing

expenses to maintain with moderate changes in line with business

activities. Total sales and marketing expenses for the six months

ended June 30, 2017 and 2016 were $0 and ($64,635), respectively.

The negative ($64,635) was due to a reversal of $65,252 provision

for HotApp Credit Points because the program was

eliminated.

General and Administrative

General

and administrative expenses consist primarily of salary and

benefits, professional fees and rental expense. We

expect our general and administrative expenses to maintain with

moderate changes in line with business activities. Total

general and administrative expenses for the six months ended June

30, 2017 and 2016 were $388,159 and $370,283,

respectively.

Other Expense (Income)

In the

six months ended June 30, 2017 and 2016, we have incurred $18,067

and $24,075 for depreciation, $2,680 and $0 for the deposits

written off, and $131 and $0 for loss on disposal of fixed assets.

In the six months ended June 30, 2017 and 2016, we have incurred

$(108,421) and $(112,504) in foreign exchange gain, and $(1) and

$(1) in interest income.

Liquidity and Capital Resources

At June

30, 2017, we had cash of $144,720 and working capital deficit of

$522,096. Cash had increased during the six months ended June 30,

2017 primarily due to the receipt of payment for the revenue

earned.

We had

a total stockholders’ deficit of $485,106 and an accumulated

deficit of $4,944,990 as of June 30, 2017 compared with a total

stockholders’ deficit of $498,315 and an accumulated deficit

of $4,628,976 as of December 31, 2016. This difference is primarily

due to the net loss incurred during the period and the issuance of

500,988,889 shares of common stock by debt conversion.

For the

six months ended June 30, 2017, we recorded a net loss of $316,014.

We made a positive adjustment of $18,067 due to depreciation, a

positive adjustment of $2,680 due to deposits written off, a

positive adjustment of $131 due to loss on disposal of fixed asset,

and a negative adjustment of $108,421 due to foreign currency

transaction gain. We had a negative change of $7,270 due to costs

in excess of billings and account receivable, a positive change of

$3,684 due to security deposit and other receivables, and a

negative change of $10,337 due to prepaid expenses. We had a

negative change of $32,329 due to accounts payable and accrued

expenses. As a result, we had net cash used in operating activities

of $449,809 for the six months ended June 30, 2017.

For the

six months ended June 30, 2016, we recorded a net loss of $428,142.

We made a positive adjustment of $24,075 due to depreciation and a

negative adjustment of $112,504 due to foreign currency transaction

gain. We had a positive change of $27,071 due to prepaid expenses

and a positive change of $7,036 due to accrued taxes payable and

franchise fees. We had a negative change of $40,003 due to accounts

payable and accrued expenses. As a result, we had net cash used in

operating activities of $522,467 for the six months ended June 30,

2016.

For the

six months ended June 30, 2017, we spent $9,092 on the acquisition

of fixed assets, resulting in net cash used in investing activities

of $9,092 for the period.

For the

six months ended June 30, 2016, we received $93,768 on the disposal

of fixed assets, resulting in net cash provided by investing

activities of $92,100 for the period.

For the

six months ended June 30, 2017, we had net cash provided by

financial activities of $514,091 due to advances from an affiliate

amounting to $514,091.

For the

six months ended June 30, 2016, we did not pursue any financing

activities.

As of

June 30, 2017, we have fixed operating office lease agreements for

Guangzhou’s office amounting to $11,393 from 2017 to 2018,

Hong Kong’s offices minimum lease commitments of $29,399 from

2017 to 2019.

We will

need to raise additional capital through equity or debt financing.

However, we cannot be certain that such capital (from SED or third

party) will be available to us or whether such capital will be

available on a term that is acceptable to us. Any such financing

likely would be dilutive to existing shareholders and could result

in significant financial and operating covenants that would

negatively impact our business. If we are unable to raise

sufficient additional capital on acceptable terms, we will have

insufficient funds to operate our business and pursue our business

plan.

Consistent

with Section 144 of the Delaware General Corporation Law, it is our

current policy that all transactions between us and our officers,

directors and their affiliates will be entered into only if such

transactions are approved by a majority of the disinterested

directors, are approved by vote of the stockholders, or are fair to

us as corporation as of the time it is authorized, approved or

ratified by the board. We will conduct an appropriate review of all

related party transactions on an ongoing basis.

Critical Accounting Policies

Our

discussion and analysis of the financial condition and results of

operations are based upon the Company’s financial statements,

which have been prepared in accordance with generally accepted

accounting principles in the United States (“GAAP”).

The preparation of these financial statements requires us to make

estimates and judgments that affect the reported amounts of assets,

liabilities, revenues and expenses, and related disclosure of

contingent assets and liabilities. We believe that the estimates,

assumptions and judgments involved in the accounting policies

described below have the greatest potential impact on our financial

statements, so we consider these to be our critical accounting

policies. Because of the uncertainty inherent in these matters,

actual results could differ from the estimates we use in applying

the critical accounting policies. Certain of these critical

accounting policies affect working capital account balances,

including the policies for revenue recognition, allowance for

doubtful accounts, inventory reserves and income taxes. These

policies require that we make estimates in the preparation of our

financial statements as of a given date.

Within

the context of these critical accounting policies, we are not

currently aware of any reasonably likely events or circumstances

that would result in materially different amounts being

reported.

Revenue recognition

The

Group recognizes revenue when persuasive evidence of an arrangement

exists, delivery has occurred, the sales price is fixed or

determinable, and collectability is reasonably assured. The Group

currently has $103,936 revenue from its services rendered on

projects, and plans to derive its revenue from membership

subscription services, offering the platform for Enterprise

Collaboration with integration. Revenue is currently recognized

under contract accounting due to the significant software

production required, and the percentage-of-completion method is

used in accordance with ASC 605-35. The Company is recognizing the

percentage-of-completion based on input measures that measured

directly from expenses incurred, and management reviews the

progress to completion. In case of the 3% iGalen revenue sharing,

revenue is recognized in accordance with ASC

985-605-25.

Research and development expenses

Research

and development expenses primarily consist of (i) salaries and

benefits for research and development personnel, and

(ii) office rental, general expenses and depreciation expenses

associated with the research and development

activities. The Company’s research and development

activities primarily consist of the research and development of new

features for its mobile platform and its self-developed mobile

games. Expenditures incurred during the research phase are expensed

as incurred.

Income taxes

Current

income taxes are provided for in accordance with the laws of the

relevant tax authorities. Deferred income taxes are

recognized when temporary differences exist between the tax bases

of assets and liabilities and their reported amounts in the

consolidated financial statements. Net operating loss carry

forwards and credits are applied using enacted statutory tax rates

applicable to future years. Deferred tax assets are reduced by a

valuation allowance when, in the opinion of management, it is

more-likely-than-not that a portion of or all of the deferred tax

assets will not be realized. The components of the deferred tax

assets and liabilities are individually classified as current and

non-current based on their characteristics.

Uncertainties

exist with respect to the application of the New EIT Law to our

operations, specifically with respect to our tax

residency. The New EIT Law specifies that legal entities

organized outside of the PRC will be considered residents for PRC

income tax purposes if their “de facto management

bodies” as “establishments that carry on substantial

and overall management and control over the operations, personnel,

accounting, properties, etc. of the

Company.” Because of the uncertainties resulted

from limited PRC guidance on the issue, it is uncertain whether our

legal entities outside the PRC constitute residents under the New

EIT Law. If one or more of our legal entities organized

outside the PRC were characterized as PRC residents, the impact

would adversely affect our results of operations.

QUANTITATIVE

AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK

Not applicable to a “smaller reporting company” as

defined in Item 10(f)(1) of SEC Regulation S-K.

Our Chief Executive Officer and Chief Financial Officer are

responsible for establishing and maintaining disclosure controls

and procedures for the Company.

(a) Evaluation of

Disclosure Controls and Procedures

Based on the evaluation as of the end of the period covered by this

Quarterly Report on Form 10-Q, our Chief Executive Officer and

Chief Financial Officer concluded that our disclosure controls and

procedures (as defined in Rules 13a-15(e) and 15d-15(e) under the

Securities Exchange Act of 1934, as amended (the “Exchange

Act”) are effective to ensure that information required to be

disclosed by us in reports that we file or submit under the

Exchange Act is recorded, processed, summarized and reported within

the time periods specified in the Securities and Exchange

Commission’s (“SECs”) rules and forms and to

ensure that information required to be disclosed by us in the

reports that we file or submit under the Exchange Act is

accumulated and communicated to our management, including our Chief

Executive Officer and Chief Financial Officer, as appropriate to

allow timely decisions regarding required disclosure.

(b) Changes in the

Company’s Internal Controls over Financial

Reporting

There have been no changes in the Company’s internal control

over financial reporting during the most recently completed fiscal

quarter that have materially affected or are reasonably likely to

materially affect, the Company’s internal control over

financial reporting.

We are not a party to any legal proceedings. Management is not

aware of any legal proceedings proposed to be initiated against us.

However, from time to time, we may become subject to claims and

litigation generally associated with any business venture operating

in the ordinary course.

Not applicable to a “smaller reporting company” as

defined in Item 10(f)(1) of SEC Regulation S-K.

UNREGISTERED

SALES OF EQUITY SECURITIES AND USE OF PROCEEDS

On

March 27, 2017, the Company sold 500,988,889 shares of common stock

to SeD in exchange for the conversion of $450,890.00 of debt owed

by the Company to SeD at a conversion price of $0.0009 per share.

The sale of these shares was made in accordance with the exemption

provided by Section 4(a)(2) of the Securities Act of 1933, as

amended.

DEFAULTS

UPON SENIOR SECURITIES

None.

Not Applicable.

None.

The

following exhibits filed with this Form 10-Q Quarterly

Report:

Exhibit

Number

Description

Certificate of

Amendment to the Company’s Certificate of

Incorporation.

Certification of

Chief Executive Officer pursuant to Section 302 of the

Sarbanes-Oxley Act of 2002.

Certification of

Chief Financial Officer pursuant to Section 302 of the

Sarbanes-Oxley Act of 2002.

Section 1350

Certification of Chief Executive Officer and Chief Financial

Officer

101.INS

XBRL Instance

Document

101.SCH

XBXRL

Taxonomy Extension Schema.

101.CAL

XBRL

Taxonomy Extension Calculation Linkbase.

101.DEF

XBRL

Taxonomy Extenstion Definition Linkbase.

101.LAB

XBRL Taxonomy

Extension Label Linkbase

101.PRE

XBRL Taxonomy Extension

Presentation Linkbase

SIGNATURES

Pursuant

to the requirements of the Securities Act of 1934, the registrant

has duly caused this report to be signed on its behalf by the

undersigned thereunto duly authorized.

|

|

HOTAPP INTERNATIONAL, INC

|

|

|

|

|

|

|

|

|

|

|

|

|

Date:

August 14, 2017

|

By:

|

/s/ Lum

Kan Fai

|

|

|

|

|

Lum Kan

Fai

|

|

|

|

|

Chief

Executive Officer and Director

(Principal

Executive Officer)

|

|

|

|

|

|

|

|

Date:

August 14, 2017

|

By:

|

/s/ Lui

Wai Leung, Alan

|

|

|

|

|

Lui Wai

Leung, Alan

|

|

|

|

|

Chief

Financial Officer

(Principal

Financial Officer and

Principal

Accounting Officer)

|

|

|

|

|

|

|