UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

[X] ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For The fiscal year ended December 31, 2016

or

[ ] TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from ___________ to ___________

Commission File Number 000-55602

Greenpro Capital Corp.

(Exact name of registrant issuer as specified in its charter)

| Nevada | 98-1146821 | |

| (State

or other jurisdiction of incorporation or organization) |

(I.R.S.

Employer Identification No.) |

Suite 2201, 22/F., Malaysia Building,

50 Gloucester Road, Wanchai, Hong Kong

(Address of principal executive offices, including zip code)

Registrant’s phone number, including area code (852) 3111 -7718

Securities registered pursuant to Section 12(b) of the Securities Exchange Act: None

Securities registered pursuant to Section 12(g) of the Securities Exchange Act:

Common

Stock, $0.0001 par value per share

(Title of Class)

OTC Markets Group Inc. QB tier (“OTCQB”)

(Name of exchange on which registered)

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes [ ] No [X]

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes [ ] No [X]

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. YES [X] NO [ ]

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (section 232.405 of this chapter) during the preceding twelve months (or shorter period that the registrant was required to submit and post such files). YES [X] NO [ ]

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§ 229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. [ ]

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

Large Accelerated Filer [ ] Accelerated Filer [ ] Non-accelerated Filer [ ] Smaller reporting company [X]

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes [ ] No [X]

The aggregate market value of voting and non-voting common equity held by non-affiliates of the Registrant as of June 30, 2016 was $29,114,046, based on the last reported sale price.

Indicate the number of shares outstanding of each of the issuer’s classes of common stock, as of the latest practicable date.

| Class | Outstanding at March 27, 2017 | |

| Common Stock, $.0001 par value | 52,865,843 |

Greenpro Capital Corp.

FORM 10-K

For the Fiscal Year Ended December 31, 2016

Index

| 2 |

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K contains forward-looking statements. These forward-looking statements are not historical facts but rather are based on current expectations, estimates and projections. We may use words such as “anticipate,” “expect,” “intend,” “plan,” “believe,” “foresee,” “estimate” and variations of these words and similar expressions to identify forward-looking statements. These statements are not guarantees of future performance and are subject to certain risks, uncertainties and other factors, some of which are beyond our control, are difficult to predict and could cause actual results to differ materially from those expressed or forecasted. These risks and uncertainties include the following:

| ● | The availability and adequacy of our cash flow to meet our requirements; | |

| ● | Economic, competitive, demographic, business and other conditions in our local and regional markets; | |

| ● | Changes or developments in laws, regulations or taxes in our industry; | |

| ● | Actions taken or omitted to be taken by third parties including our suppliers and competitors, as well as legislative, regulatory, judicial and other governmental authorities; | |

| ● | Competition in our industry; | |

| ● | The loss of or failure to obtain any license or permit necessary or desirable in the operation of our business; | |

| ● | Changes in our business strategy, capital improvements or development plans; | |

| ● | The availability of additional capital to support capital improvements and development; and | |

| ● | Other risks identified in this report and in our other filings with the Securities and Exchange Commission or the SEC. |

This report should be read completely and with the understanding that actual future results may be materially different from what we expect. The forward looking statements included in this report are made as of the date of this Annual Report and should be evaluated with consideration of any changes occurring after the date of this Annual Report. We will not update forward-looking statements even though our situation may change in the future and we assume no obligation to update any forward-looking statements, whether as a result of new information, future events or otherwise.

Use of Defined Terms

Except as otherwise indicated by the context, references in this report to:

| ● | The “Company,” “we,” “us,” or “our,” “Greenpro” are references to Greenpro Capital Corp., a Nevada corporation. | |

| ● | “Common Stock” refers to the common stock, par value $.0001, of the Company; | |

| ● | “HK” refers to the Hong Kong; | |

| ● | “U.S. dollar,” “$” and “US$” refer to the legal currency of the United States; | |

| ● | “Securities Act” refers to the Securities Act of 1933, as amended; and | |

| ● | “Exchange Act” refers to the Securities Exchange Act of 1934, as amended. |

| 3 |

Corporate History

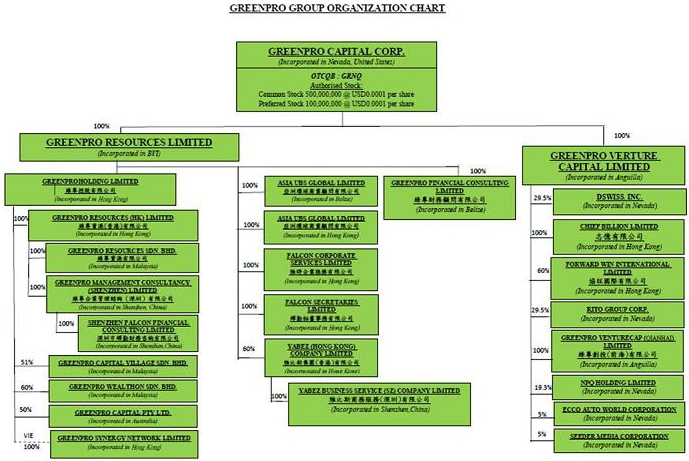

We were incorporated on July 19, 2013 in the state of Nevada under the name Greenpro, Inc. On May 6, 2015, we changed our name to Greenpro Capital Corp. Our corporate structure is set forth below:

A list of our subsidiaries and affiliates together with a brief description of their business is set forth below:

| Name | Business | |

| Greenpro Capital Corp. (Nevada, USA) | Provides cloud system resolution, financial consulting services and corporate accounting services | |

| Greenpro Resources Limited (British Virgin Islands) | Holding company | |

| Greenpro Holding Limited (Hong Kong) | Holds life insurance products | |

| Greenpro Resources (HK) Limited (Hong Kong) | Holds Greenpro intellectual property and currently holds six trademarks and applications thereof | |

| Greenpro Resources Sdn. Bhd. (Malaysia) | Holds real property usable as offices in Malaysia | |

| Greenpro Management Consultancy (Shenzhen) Limited (China) | Provides corporate advisory services such as tax planning, cross-border listing solution and advisory, transaction services in China |

| 4 |

| Shenzhen Falcon Finance Consulting Limited (China) | Provide Hong Kong Company Formation Advisory Services & Company Secretarial Services and Financial Services. Client Base in China | |

| Greenpro Capital Village Sdn Bhd (Formerly known as Greenpro Global Advisory Sdn. Bhd.) (Malaysia) | Provide educational and support services via seminars and courses to new start-up companies or SME. | |

| Greenpro Financial Consulting Limited (Belize) | Provides corporate advisory services such as tax planning, cross-border listing solution and advisory, transaction services | |

| Asia UBS Global Limited (Belize) | Provide business advisory services with main focus on offshore company formation advisory and company secretarial service, such as tax planning, bookkeeping and financial review. It focuses on South-East Asia and China clients. | |

| Asia UBS Global Limited (Hong Kong) | Provide business advisory services with main focus on Hong Kong company formation advisory and company secretarial service, such as tax planning, bookkeeping and financial review. It focuses on Hong Kong clients. | |

| Falcon Corporate Services Limited (Formerly known as Ace Corporate Services Limited) (Hong Kong) | Provide Offshore Company Formation Advisory Services & Company Secretarial Services. Client Base in Hong Kong & China | |

| Falcon Secretaries Limited (Hong Kong) | Provide Hong Kong Company Formation Advisory Services & Company Secretarial Services. Client Base in Hong Kong & China | |

| Yabez (Hong Kong) Company Limited (Hong Kong) | Provides Hong Kong company formation advisory services, corporate secretarial services and IT related services to Hong Kong based clients. | |

| Yabez Business Service (SZ) Company Limited (China) | Provides Shenzhen company formation advisory services, corporate secretarial services and IT related services to China based clients. | |

| Greenpro Venture Capital Limited (Anguilla) | Holding company | |

| Forward Win International Limited (Hong Kong) | Holding Hong Kong real estate for investment purpose | |

| Chief Billion Limited (Hong Kong) | Holding Hong Kong real estate for investment purpose | |

| Greenpro Venturecap (Qianhai) Limited (Formerly known as Greenpro Venture Cap (CGN) Limited) (Anguilla) | Holding company |

Acquisition and Reorganization History

Acquisition of Greenpro Resources Limited

On July 31, 2015, we acquired 100% of the issued and outstanding securities of Greenpro Resources Limited, a British Virgin Islands corporation that was our affiliate at the time of the acquisition (“GRBV”). As consideration thereof, we issued to the shareholders of GRBV 9,070,000 restricted shares of our common stock (valued at $3,174,500 based on the average closing price of the six trading days preceding July 28, 2015, which was $0.35 per share) and paid US$25,500 in cash, representing an aggregate purchase price of US$3,200,000. The purchase price was determined based on the existing business value of GRBV, carrying value of GRBV properties, brand names of GRBV and settlement of GRBV founder initial investment.

GRBV provides corporate advisory services such as tax planning, cross-border listing solutions and advisory and transaction services to start-up and high –growth companies. It also owns real estate in Selangor Darul Ehsan, Malaysia and Kuala Lumpur, Malaysia that are investment properties, which are currently generating rental income. Through our acquisition of GRBV, we hope to expand our customer and revenue base as well as broaden the range of services we offer.

Lee Chong Kuang, our Chief Executive Officer, President and director, was also the Chief Executive Officer, President and director of GRBV at the time of the acquisition. Mr. Lee holds 44.6% of our issued and outstanding securities and held 50% of the issued and outstanding securities of GRBV at the time of the acquisition. Gilbert Loke Che Chan, our Chief Financial Officer, Secretary, Treasurer and director, is also the Chief Financial Officer and director of GRBV. Mr. Loke holds 44.6% of our issued and outstanding securities and held 50% of the issued and outstanding securities of GRBV at the time of the acquisition. Upon the consummation of the acquisition, Messrs. Lee and Loke received, in the aggregate,US$25,500 in cash and 9,070,000 shares of our restricted common stock.

| 5 |

Acquisition of A&G International Limited

On September 30, 2015, we acquired of 100% of the issued and outstanding securities of A&G International Limited, a Belize corporation (“A&G”). In connection therewith, we issued to Yap Pei Ling, the shareholder of A&G, 1,842,000 restricted shares of our common stock, representing an aggregate purchase price of $957,840 based on the average closing price of the ten trading days preceding July 31, 2015, the date of the acquisition agreement, of $0.52 per share. The purchase price was determined based on the existing business value generated from A&G.

Ms Yap Pei Ling, the director and sole shareholder of A&G, is the spouse of Lee Chong Kuang, our Chief Executive Officer, President and director.

A&G provides corporate and business advisory services through its wholly-owned subsidiaries, Asia UBS Global Limited (Hong Kong) and Asia UBS Global Limited (Belize).

On December 30, 2015, A&G International Limited transferred all of the issued and outstanding securities of Asia UBS Global Limited, a Belize Corporation, and Asia UBS Global Limited, a Hong Kong limited company, to Greenpro Resources Limited to simplify our corporate structure. A&G International Limited, now a corporation with no assets, was subsequently transferred back to Ms Yap Pei Ling.

Acquisition of Falcon Secretaries Limited, Ace Corporate Services Limited and Shenzhen Falcon Financial Consulting Limited

On September 30, 2015, we acquired all of the issued and outstanding securities of Falcon Secretaries Limited, Ace Corporate Services Limited and Shenzhen Falcon Financial Consulting Limited (these companies collectively known as “F&A”). As consideration therefor, we issued to Ms. Chen Yan Hong, the sole shareholder of F&A, 2,080,200 restricted shares of our common stock, representing an aggregate purchase price of $1,081,704 based on the average closing price of the ten trading days preceding July 31, 2015, the date of the acquisition agreement, of $0.52 per share. The purchase price was determined based on the existing business value generated from F&A.

Ms, Chen Yan Hong, the director and sole shareholder of F&A, is also the director and legal representative of Greenpro Management Consultancy (Shenzhen) Limited, one of our subsidiaries..

Acquisition of Yabez (Hong Kong) Company Limited

On September 30, 2015, we acquired 60% of the issued and outstanding securities of Yabez (Hong Kong) Company Limited, a Hong Kong corporation (“Yabez”). As consideration therefor, we issued to the shareholders of Yabez 486,171 restricted shares of our common stock, representing an aggregate purchase price of $252,808 based on the average closing price of the ten trading days preceding July 31, 2015, the date of the acquisition agreement, of $0.52 per share. The purchase price was determined based on the existing business value generated from Yabez. Yabez provides Hong Kong company formation advisory services, corporate secretarial services and IT related services to Hong Kong based clients.

Acquisition of Greenpro Venture Capital Limited, an Anguilla corporation

On September 30, 2015, we acquired all of the issued and outstanding securities of Greenpro Venture Capital Limited, an Anguilla corporation, (“GPVC”) from its shareholders, Lee Chong Kuang and Loke Che Chan Gilbert. As consideration thereof, we issued to the shareholders of GPVC an aggregate of 13,260,000 restricted shares of our common stock (valued at $7,956,000 based on the signed Memorandum of Understanding on July 25, 2015 of $0.6 per share) and paid US$6,000 in cash, representing an aggregate purchase price of US$7,962,000. The purchase price was determined based on the existing business value of GPVC, including all customers, fixed assets, investments, cash and cash equivalents and assuming certain liabilities of GPVC. Mr. Lee Chong Kuang, our Chief Executive Officer, President and director, was also the Chief Executive Officer, President and director of GPVC at the time of the acquisition. Mr. Lee holds 43.02% of our issued and outstanding shares and held 50% of the issued and outstanding shares of GPVC at the timed of the acquisition. Mr. Loke Che Chan Gilbert, our Chief Financial Officer, Secretary, Treasurer and director, was also the Chief Financial Officer and director of GPVC. Mr. Loke holds 43.02% of our issued and outstanding shares and held 50% of the issued and outstanding shares of GPVC at the time of the acquisition.

| 6 |

Incorporation of Greenpro Captial Pty Ltd, an Australia company

Greenpro Capital Pty Ltd was formed on May 11, 2016 with 50% held by Greenpro Holding Limited (“GPH”), one of our subsidiaries, and 50% was held by Mohammad Reza Masoumi Al Agha.

Acquisition of Greenpro Wealthon Sdn Bhd, a Malaysia company

On May 23, 2016, our subsidiary. Greenpro Holding Limited (GPHL) acquired 400 shares of Greenpro Wealthon Sdn Bhd. from Mr. Lee Chong Kuang with MYR 1 (approximately US$0.25). On June 7, 2016, GPHL acquired an additional 200 shares of Greenpro Wealthon Sdn Bhd for MYR120,000 (approximately US$30,000), resulting in GPHL owing 60% of Greenpro Wealthon Sdn Bhd. The remaining 40% of Greenpro Wealthon Sdn. Bhd. is held by Mr. Yiap Soon Keong.

VIE Structure And Arrangements

Greenpro Synergy Network Ltd (“GSN”) was incorporated in Hong Kong on March 2, 2016, as a variable interest entity (“VIE”) that is subject to consolidation with the Company. GSN’s principal activities are to hold certain of our universal life insurance policies. Loke Che Chan, Gilbert, our Chief Financial Officer, Secretary, Treasurer and director and Lee Chong Kuang, our Chief Executive Officer, President and director are the sole shareholders of GSN. We control GSN through a series of contractual arrangements (the “VIE Agreements”) between GPHL and GSN. The VIE agreements include (i) an Exclusive Business Cooperation Agreement, (ii) a Loan Agreement, (iii) a Share Pledge Agreement, (iv) a Power of Attorney and (v) an Exclusive Option Agreement with the shareholder of GSN.

Set forth below is a more detailed description of each of the VIE agreement.

Exclusive Business Cooperation Agreement: Pursuant to the Exclusive Business Cooperation Agreement, GPHL serves as the exclusive provider of technical support, consulting services and management services to GSN. In consideration of such services, GSN has agreed to pay a service fee to GPHL, which is based on the time of services rendered multiplied by the corresponding rate, plus amount of the services fees or ratio decided by the board of directors of GPHL. The Agreement has a term of 10 years but may be extended GPHL in its discretion.

Loan Agreement: Pursuant to the Loan Agreement, GPHL granted interest-free loans to the shareholders of the GSN for the sole purpose of increasing the registered capital of the GSN. These loans are eliminated with the capital of GSN during consolidation.

Share Pledge Agreement: Pursuant to the Share Pledge Agreement, the shareholders of GSN pledged to GPHL a first security interest in all of their equity interests in GSN to secure GSN’s timely and complete payment and performance of its obligations under the Exclusive Business Cooperation Agreement. During the term of the Share Pledge Agreement, the pledgors agreed, among other things, not to transfer, place or permit the existence of any security interest or other encumbrance on their interest in GSN without the prior written consent of GPHL. The pledge shall remain in effect until 10 years after the obligations under the principal agreement will have been fulfilled. However, upon the full payment of the consulting and service fees under the Exclusive Business Cooperation Agreement and upon the termination of GSN’s obligations under the Exclusive Business Cooperation Agreement, the Share Pledge Agreement shall be terminated and GPHL shall terminate this agreement as soon as reasonably practicable.

| 7 |

Power of Attorney: Pursuant to the Power of Attorney, Messrs. Lee and Loke, as the sole shareholders of GSN, granted to the GPHL the right to (i) attend shareholders meetings of GSN (ii) exercise all shareholder rights (including voting rights) with respect to such equity interests in GSN and (iii) designate and appoint on behalf of such shareholders the legal representative, directors, supervisors, and other senior management members of GSN. The Power of Attorney is irrevocable and is continuously valid from the date of execution of such Power of Attorney, so long as such persons remain shareholders of GSN.

Exclusive Option Agreement: Pursuant to the Exclusive Option Agreement, the shareholders of GSN granted to the GPHL an irrevocable and exclusive right and option to purchase all of their equity interests in GSN. The purchase price shall be equal to the capital paid in by the shareholders, adjusted pro rata for the purchase of less than all of the equity interests. The Agreement is effective for a term of 10 years, and may be renewed at GPHL’s election

Investment and Divestment via Greenpro Venture Capital Limited during year 2016

On April 1, 2016, we mutually agreed with Lepora Holdings Corporation and CGN Nanotech Inc. to withdraw our investment in the 36,000,000 shares and 21,600,000 shares, respectively, we held in the companies and to release each other from any and all claims and/or obligations arising under the Subscription Agreement. As a result of the agreement, the shares were cancelled and our funds were returned. Since April 1, 2016, the Company has not owned any shares of Lepora Holdings Corporation and CGN Nanotech Inc.

On October 3, 2016, we purchased 4,000,000 shares of ECCO Auto World Corporation Common Stock at a price of US$ .0001 per share for a total purchase price of US$400..

On December 19, 2016 we purchased 1,800,000 shares of Seeder Media Corporation Common Stock at US$ .0001 per share for a total US$180.

Business Overview

We currently operate and provide a wide range of business solution services to small and medium-size businesses located in Asia, with an initial focus on Hong Kong, China and Malaysia. Our comprehensive range of services include cross-border business solutions, record management services, and accounting outsourcing services. Our cross border business services include, among other services, tax planning, trust and wealth management, cross border listing advisory services and transaction services. As part of the cross border business solutions, we have developed a package solution of services (“Package Solution”) that can reduce their business costs and improve their revenues.

In addition to our business solution services, we also operate a venture capital business through Greenpro Venture Capital Limited, an Anguilla corporation. Our venture capital business is focused on (1) establishing a business incubator for start-up and high growth companies to support such companies during critical growth periods, which will include education and support services, and (2) searching the investment opportunities in selected start-up and high growth companies, which can generate exponential return to the Company. We expect to target companies located in Asia and South-East Asia including Hong Kong, Malaysia, China, Thailand, and Singapore. We anticipate our venture capital business will also engage in the purchase, acquisition and rental of commercial properties in the same Asia and South-East Asia region.

We expect to operate our venture capital related education and support services through our subsidiary Greenpro Global Advisory Sdn. Bhd., which was renamed Greenpro Capital Village Sdn. Bhd. on September 23, 2015.

Subsequently, on October 1, 2015, QSC Asia Sdn. Bhdacquired 49% of Greenpro Capital Village Sdn. Bhd. in consideration of $11,000 (RM 49,000) from Greenpro Financial Consulting Limited. Concurrently with such sale, Greenpro Financial Consulting Limited transferred 51% of Greenpro Capital Village Sdn. Bhd. to Greenpro Holding Limited, our subsidiary.

| 8 |

Our Services

We provide a range of services to our clients as part of the Package Solution. We have developed the Package Solution, and we believe that our potential clients can reduce their business costs and improve their revenues by offering our Package Solution.

Cross-Border Business Solutions/Cross-Border Listing Solution

We provide a full range of cross-border services to small to mid-sized businesses to assist them in conducting their business effectively and we generate revenue from such services. Our “Cross-Border Business Solution” include the following services:

| ● | Advising clients on company formation in Hong Kong, U.S., British Virgin Island and other overseas jurisdictions | |

| ● | Providing assistance to set up bank accounts with banks in Hong Kong to facilitate clients’ banking operations | |

| ● | Providing bank loan referrals services | |

| ● | Providing company secretarial services | |

| ● | Assisting companies in applying for business registration certificates with the Inland Revenue Department of Hong Kong | |

| ● | Providing corporate finance consulting services | |

| ● | Providing due diligence investigations and valuation of companies | |

| ● | Advising clients regarding debt and company restructuring | |

| ● | Providing liquidation, insolvency, bankruptcy and individual voluntary arrangement advice and assistance | |

| ● | Designing a marketing strategy and promoting the company’s business, products and services | |

| ● | Providing financial and liquidity analysis | |

| ● | Assisting in setting up cloud invoicing system for clients | |

| ● | Assisting in liaising with capital funds for raising capitals | |

| ● | Assisting in setting up cloud inventory system to assist clients to record, maintain and control their inventories and knowing their inventory levels | |

| ● | Assisting in setting up cloud accounting system to enable clients to keep track of their financial performance | |

| ● | Assisting client’s payroll matters operated in our cloud payroll system | |

| ● | Assisting clients in tax planning, preparing the tax computation and compiling with the filing of profits tax with the Inland Revenue Department of Hong Kong | |

| ● | Cross border listing advisory services | |

| ● | International tax planning in China | |

| ● | Trust and wealth management | |

| ● | Transaction services |

| 9 |

With growing competition and increasing economic sophistication, we believe more companies need strategies for cross-border restructuring and other corporate matters. Our plan is to bundle our Cross Border Business Solution services with our Cloud Accounting Solution.

Accounting Outsourcing Services

We intend to develop relationships with professional firms from Hong Kong, Malaysia and China that can provide company secretarial, business centers and virtual offices, book-keeping, tax compliance and planning, payroll management, business valuation, and wealth management services to our clients. We intend to include local accounting firms within this network to provide general accounting, financial evaluation and advisory services to our clients. Our expectation is that firms within our professional network will refer their international clients to us that may need our book-keeping, payroll, company secretarial and tax compliance services. We believe that this accounting outsourcing service arrangement will be beneficial to our clients by providing a convenient, one-stop firm for their local and international business and financial compliance and governance needs.

Our Service Rates

We intend to have a two-tiered rate system based upon the type of services being offering. We may impose project-based fees, where we charge 10% -25% of the revenues generated by the client on projects that are completed using our services, such as transaction projects contract compliance projects, and business planning projects. We may also charge a flat rate fee or fixed fee based on the estimated complexity and timing of a project when our professionals provide specified expertise to our clients on a project. For example, for the cross-border business solutions, we plan to charge our client a monthly fixed fee.

Our Venture Capital Business Segment

Venture Capital Investment

As a result of our acquisition of Greenpro Venture Capital Limited in 2015, we entered the venture capital business in Hong Kong with a focus on companies located in Asia and South-East Asia, including Hong Kong, Malaysia, China, Thailand, and Singapore. Our venture capital business is focused on (1) establishing a business incubator for start-up and high growth companies to support such companies during critical growth periods and (2) investment opportunities in select start-up and high growth companies. .

We believe that a company’s life cycle can be divided into five stages, including the seed stage, start up stage, expansion stage, mature stage and decline stage.

| ● | Seed stage: Financing is needed for assets, and research and development of an initial business concept. The company usually has relatively low costs in developing the business idea. The ownership model is considered and implemented. | |

| ● | Start-up stage: Financing is needed for product development and initial marketing. Firms in this phase may be in the process of setting up a business or they might have been in operating the business for a short period of time, but may not have sold their products commercially. In this phase, costs are increasing due to. product development, market research and the need to recruit personnel. Low levels of revenues are starting to generate. | |

| ● | Expansion stage: Financing is needed for growth and expansion. Capital may be used to finance increased production capacity, product or marketing development or to hire additional personnel. In the early expansion phase, sales and production increases but there is not yet any profit. In the later expansion stage, the business typically needs extra capital in addition to organically generated profit, for further development, marketing or product development. |

We anticipate that most of a company’s funding needs will occur during these first three stages.

We intend for our business incubators to provide valuable support to young, emerging growth and potential high growth companies at critical junctures of their development. For example, our incubators will offer office space at a below market rental rate. We will also provide our expertise, business contacts, introductions and other resources to assist their development and growth. Depending on each individual circumstance, we may also take an active advisory role in our venture capital companies including board representation, strategic marketing, corporate governance, and capital structuring. We believe that there will be potential investment opportunities for us in these start-up companies.

| 10 |

In addition to our business incubator, we have also taken an equity position in the following companies that we believe have high growth potential.

| Name | Equity Ownership | Business Line | ||

| Rito Group Corp.(Nevada, USA) | 29.5 % | Providing an online platform for merchants and customers to facilitate transactions | ||

| Forward Win International Limited(Hong Kong) | 60 % | Holding Hong Kong real estate for investment purpose | ||

| DSwiss, Inc. (Nevada, USA) | 29.5 % | Retailer in slimming and beauty products | ||

| Chief Billion Limited (Hong Kong) | 100 % | Holding Hong Kong real estate for investment purpose | ||

| Greenpro Venturcap (Qianhai) Limited (Formerly known as Greenpro Venture Cap (CGN) Limited) (Anguilla) | 100 % | Holding company | ||

| NPQ Holdings Limited (Nevada, USA) | 19.28 % | Providing mobile Apps, restaurant management system and cloud ERP | ||

| Seeder Media Corporation (Nevada, USA) | 5% | Providing services in connect with public relations, investor relations and event management | ||

| Ecco Auto World Corporation (Nevada, USA) | 5% | Providing mobile Apps to connect the car owners with nationwide car workshops. |

Our business processes for our investment strategy in select start-up and high growth companies is as follows:

| ● | Step 1. Generating Deal Flow: We expect to actively search for entrepreneurial firms and to generate deal flow through our business incubator and the personal contacts of our executive team. We also anticipate that entrepreneurs will approach us for financing. | |

| ● | Step 2. Investment Decision: We will evaluate, examine and engage in due diligence of a prospective portfolio company, including but not limited to product/services viability, market potential and integrity as well as capability of the management. After that both parties arrive at an agreed value for the deal. Following that is a process of negotiation, which if successful, ends with capital transformation and restructuring. | |

| ● | Step 3. Business Development and Value Adding: In addition to capital contribution, we expect to provide expertise, knowledge and relevant business contacts to the company. | |

| ● | Step 4. Exit: There are several ways to exit an investment in a company. Common exits are: |

| ○ | IPO (Initial Public Offering): The company’s shares are offered in a public sale on an established securities market. | |

| ○ | Trade sale (Acquisition): The entire company is sold to another company. | |

| ○ | Secondary sale: The company’s firm sells only part of its shares.. | |

| ○ | Buyback or MBO: Either the entrepreneur or the management of the company buys back the company’s shares of the firm. | |

| ○ | Reconstruction, liquidation or bankruptcy: If the project fails the company will restructure or close down the operations. |

| 11 |

Our objective for is to achieve a superior rate of return through the eventual and timely disposal of investments. We expect to look for businesses that meet the following criteria:

| ● | high growth prospects | |

| ● | ambitious teams | |

| ● | viability of product or service | |

| ● | experienced management | |

| ● | ability to convert plans into reality | |

| ● | justification of venture capital investment and investment criteria |

Our Venture Capital Related Education and Support Services.

In addition to providing venture capital services through GPVC, we also intend to provide educational and support services that we believe will be synergistic with our venture capital business. We intend to provide these educational services through our subsidiary Greenpro Capital Village Sdn. Bhd. Specifically, we expect to arrange one or more seminars called the CEO & Business Owners Strategic Session (CBOSS) for business owners who are interested in the following:

| ● | Developing their business globally; | |

| ● | Expanding business with increased capital funding; | |

| ● | Creating a sustainable SME business model; | |

| ● | Accelerating the growth of the business; and | |

| ● | Significantly increasing company cash flows. |

The objective the CBOSS seminar is to educate the Chief Executive Officer or business owner on how to acquire “smart capital” and the considerations involved. We expect the seminar to include an introduction to the basic concepts of “smart capital,” “wealth and value creation,” recommendation and planning and similar topics. We believe that this seminar will synergistically support our venture capital business segment.

Sales and Marketing

We plan to deploy three strategies to market the Greenpro brand: leadership, market segmentation, and sales management process development.

| ● | Building Brand Image: Greenpro’s marketing efforts will focus on building the image of the our extensive expertise and knowledge of our professionals. We intend to conduct a marketing campaign through media visibility, seminars, webinars, and the creation of a wide variety of white papers, newsletters, books, and other information. | |

| ● | Market segmentation: We plan to devote marketing resources to the highly measurable and high return on investment tactics that specifically target those industries and areas where Greenpro has particularly deep experience and capabilities. These efforts typically involve local, regional or national trade show and event sponsorships, targeted direct mail, email, and telemarketing campaigns, and practice and industry specific micro-sites, newsletters, etc. in the Asia region. | |

| ● | Social Media: We plan to begin a social media campaign utilizing blogs, twitter, Facebook, and LinkedIn after we secure sufficient financing. A targeted campaign will be made to the following groups of clients: law firms, auditing firms, consulting firms, small to mid-size enterprises in different industries, including biotechnologies, intellectual property, information technologies and real estate. |

| 12 |

Market Opportunities

We intend to assist our clients in the cost-effective preparation of their financial statements and provide security based on such financial information since the data will be stored in the cloud system. We anticipate a market with growing needs in South-East Asia. We believe that today there is an increasing need for enterprises in different industries to maximize their performance with cost-effective methods. We believe our services will create numerous competitive advantages for our clients. We believe our clients can focus on developing their businesses and expanding their own client portfolio.

We believe the main drivers for the growth of our business are the products and services together with the resources such as an office network, professional staff members, and operational tools to make the advisory and consulting business more competitive.

Customers

Before the acquisitions previously described, we generated minimal revenue from three clients in Hong Kong. The revenue generated related to assisting these clients with company formation and secretary services. As a result of the new acquisition, we expect to generate revenues from clients located globally including those from Hong Kong, China, Malaysia, Singapore, Indonesia, Thailand, Australia, Japan, Taiwan, Russia, USA. Our venture capital business segment will initially focus on Hong Kong and South-East Asia start-ups and high growth companies. We hope to generate deal flow through personal contacts of our management team as well as through our business incubator.

We generated net revenues of $2,776,435 during the fiscal year ended December 31, 2016. Our venture capital business accounted for approximately two percent of our net revenue. We are not a party to any long-term agreements with our customers.

Competition

Our industry is highly competitive. We compete with local and international venture capital, financial advisory and corporate business service companies such as Cornerstone Management Group in Hong Kong, CST Tax Advisor in Singapore and Maceda Valencia & Co in Philippines that provide services comparable to our Package Solution. We also compete with numerous local and international financial advisory and corporate business service companies, however those companies do not offer our broad range of services. They typically focus on specialized areas such as tax planning and cross-border solutions.. Some of our competitors may provide a broader selection of services, including investment banking services, which may position them better among customers who prefer to use a single company to meet all of their financial and business advisory needs. In addition, some of our competitors are substantially larger than we are, may have substantially greater resources than we do or may offer a broader range of products and services than we do. We believe that we compete on the basis of a number of factors, including breadth of service and product offerings, one stop convenience, pricing, marketing expertise, service levels, technological capabilities and integration, brand and reputation.

Intellectual Property

We intend to protect our investment in the research and development of our products and technologies. We intend to seek the widest possible protection for significant product and process developments in our major markets through a combination of trade secrets, trademarks, copyrights and patents, if applicable. We anticipate that the form of protection will vary depending upon the level of protection afforded by a particular jurisdiction. Currently, our revenue is derived principally from our operations in Hong Kong and Malaysia, where intellectual property protection may be limited and difficult to enforce. In such instances, we may seek protection of our intellectual property through measures taken to increase the confidentiality of intellectual property.

We intend to register trademarks as a means of protecting the brand names of our companies and products. We intend protect our trademarks against infringement and also seek to register design protection where appropriate.

| 13 |

We rely on trade secrets and un-patentable know-how that we seek to protect, in part, by confidentiality agreements. Our policy is to require some of our employees to execute confidentiality agreements upon the commencement of employment with us. These agreements provide that all confidential information developed or made known to the individual during the course of the individual’s relationship with us is to be kept confidential and not disclosed to third parties except in specific limited circumstances. The agreements also provide that all inventions conceived by the individual while rendering services to us shall be assigned to us as the exclusive property of our company. There can be no assurance, however, that all persons who we desire to sign such agreements will sign, or if they do, that these agreements will not be breached, that we would have adequate remedies for any breach, or that our trade secrets or unpatentable know-how will not otherwise become known or be independently developed by competitors.

Government Regulation

We intend to provide our Package Solution initially in Hong Kong, China and Malaysia, which we believe would welcome outsourcing support services. Further, we believe these markets are the central and regional markets for many customers doing cross border businesses in Asia. We plan to target those customers from South-East Asia doing international business and plan to provide our Package Solution to meet their needs. Our planned Packaged Solution will be structured in Hong Kong but services may be outsourced to lower cost jurisdictions such as Malaysia, which encourage and welcome outsourcing services.

The following regulations are the applicable laws and regulations that may be applicable to us:

Hong Kong

Our businesses located in Hong Kong are subject to the general laws in Hong Kong governing businesses including labor, occupational safety and health, general corporations, intellectual property and other similar laws. Because our website is maintained through the server in Hong Kong, we expect that we will be required to comply with the rules of regulations of Hong Kong governing the data usage and regular terms of service applicable to our potential customers. As the information of our potential customers is preserved in Hong Kong, we will need to comply with the Hong Kong Personal Data (Privacy) Ordinance (Cap 486).

The Employment Ordinance is the main piece of legislation governing conditions of employment in Hong Kong since 1968. It covers a comprehensive range of employment protection and benefits for employees, including Wage Protection, Rest Days, Holidays with Pay, Paid Annual Leave, Sickness Allowance, Maternity Protection, Statutory Paternity Leave, Severance Payment, Long Service Payment, Employment Protection, Termination of Employment Contract, Protection Against Anti-Union Discrimination.

An employer must also comply with all legal obligations under the Mandatory Provident Fund Schemes Ordinance, (CAP485). These include enrolling all qualifying employees in MPF schemes and making MPF contributions for them. Except for exempt persons, employer should enroll both full-time and part-time employees who are at least 18 but under 65 years of age in an MPF scheme within the first 60 days of employment. The 60-day employment rule does not apply to casual employees in the construction and catering industries.

We are required to make MPF contributions for our Hong Kong employees once every contribution period (generally the wage period). Employers and employees are each required to make regular mandatory contributions of 5% of the employee’s relevant income to an MPF scheme, subject to the minimum and maximum relevant income levels. For a monthly-paid employee, the minimum and maximum relevant income levels are $7,100 and $30,000 respectively.

Malaysia

Our businesses located in Malaysia are subject to the general laws in Malaysia governing businesses including labor, occupational safety and health, general corporations, intellectual property and other similar laws including the Computer Crime Act 1997 and The Copyright (Amendment) Act 1997. We believe that the focus of these laws realize it is an issue of censorship in Malaysia. But we believe this issue will not impact our businesses because the censorship focus on media controls and does not relate to cloud based technology we plan to use.

| 14 |

Our real estate investments are subject to extensive local, city, county and state rules and regulations regarding permitting, zoning, subdivision, utilities and water quality as well as federal rules and regulations regarding air and water quality and protection of endangered species and their habitats. Such regulation may result in higher than anticipated administrative and operational costs.

China

A portion of our acquired businesses is located in China and subject to the general laws in China governing businesses including labor, occupational safety and health, general corporations, intellectual property and other similar laws.

Employment Contracts

The Employment Contract Law was promulgated by the National People’s Congress’ Standing Committee on June 29, 2007 and took effect on January 1, 2008. The Employment Contract Law governs labor relations and employment contracts (including the entry into, performance, amendment, termination and determination of employment contracts) between domestic enterprises (including foreign-invested companies), individual economic organizations and private non-enterprise units (collectively referred to as the “employers”) and their employees.

a. Execution of employment contracts

Under the Employment Contract Law, an employer is required to execute written employment contracts with its employees within one month from the commencement of employment. In the event of contravention, an employee is entitled to receive double salary for the period during which the employer fails to execute an employment contract. If an employer fails to execute an employment contract for more than 12 months from the commencement of the employee’s employment, an employment contract would be deemed to have been entered into between the employer and employee for a non-fixed term.

b. Right to non-fixed term contracts

Under the Employment Contract Law, an employee may request for a non-fixed term contract without an employer’s consent to renew. In addition, an employee is also entitled to a non-fixed term contract with an employer if he has completed two fixed term employment contracts with such employer; however, such employee must not have committed any breach or have been subject to any disciplinary actions during his employment. Unless the employee requests to enter into a fixed term contract, an employer who fails to enter into a non-fixed term contract pursuant to the Employment Contract Law is liable to pay the employee double salary from the date the employment contract is renewed.

c. Compensation for termination or expiry of employment contracts

Under the Employment Contract Law, employees are entitled to compensation upon the termination or expiry of an employment contract. Employees are entitled to compensation even in the event the employer (i) has been declared bankrupt; (ii) has its business license revoked; (iii) has been ordered to cease or withdraw its business; or (iv) has been voluntarily liquidated. Where an employee has been employed for more than one year, the employee will be entitled to such compensation equivalent to one month’s salary for every completed year of service. Where an employee has employed for less than one year, such employee will be deemed to have completed one full year of service.

d. Trade union and collective employment contracts

Under the Employment Contract Law, a trade union may seek arbitration and litigation to resolve any dispute arising from a collective employment contract; provided that such dispute failed to be settled through negotiations. The Employment Contract Law also permits a trade union to enter into a collective employee contract with an employer on behalf of all the employees.

| 15 |

Where a trade union has not been formed, a representative appointed under the recommendation of a high-level trade union may execute the collective employment contract. Within districts below county level, collective employment contracts for industries such as those engaged in construction, mining, food and beverage and those from the service sector, etc., may be executed on behalf of employees by the representatives from the trade union of each respective industry. Alternatively, a district-based collective employment contract may be entered into.

As a result of the Employment Contract Law, all of our employees have executed standard written employment agreements with us. We have not experienced any significant labor disputes or any difficulties in recruiting staff for our operations.

On October 28, 2010, the National People’s Congress of China promulgated the PRC Social Insurance Law, which became effective on July 1, 2011. In accordance with the PRC Social Insurance Law, the Interim Regulations on the Collection and Payment of Social Security Fund and other relevant laws and regulations, China establishes a social insurance system including basic pension insurance, basic medical insurance, work-related injury insurance, unemployment insurance and maternity insurance. An employer shall pay the social insurance for its employees in accordance with the rates provided under relevant regulations and shall withhold the social insurance that should be assumed by the employees. The authorities in charge of social insurance may request an employer’s compliance and impose sanctions if such employer fails to pay and withhold social insurance in a timely manner. Under the Regulations on the Administration of Housing Fund effective in 1999, as amended in 2002, PRC companies must register with applicable housing fund management centers and establish a special housing fund account in an entrusted bank. Both PRC companies and their employees are required to contribute to the housing funds.

The Ministry of Human Resources and Social Security promulgated the Interim Provisions on Labor Dispatch on January 24, 2014. The Interim Provisions on Labor Dispatch, which became effective on March 1, 2014, sets forth that labor dispatch should only be applicable to temporary, auxiliary or substitute positions. Temporary positions shall mean positions subsisting for no more than six months, auxiliary positions shall mean positions of non-major business that serve positions of major businesses, and substitute positions shall mean positions that can be held by substitute employees for a certain period of time during which the employees who originally hold such positions are unable to work as a result of full-time study, being on leave or other reasons. The Interim Provisions further provides that, the number of the dispatched workers of an employer shall not exceed 10% of its total workforce, and the total workforce of an employer shall refer to the sum of the number of the workers who have executed labor contracts with the employer and the number of workers who are dispatched to the employer.

Foreign Exchange Control and Administration

Foreign exchange in China is primarily regulated by:

| ● | The Foreign Currency Administration Rules (1996), as amended; and | |

| ● | The Administration Rules of the Settlement, Sale and Payment of Foreign Exchange (1996), or the Administration Rules. |

Under the Foreign Currency Administration Rules, if documents certifying the purposes of the conversion of RMB into foreign currency are submitted to the relevant foreign exchange conversion bank, the RMB will be convertible for current account items, including the distribution of dividends, interest and royalties payments, and trade and service-related foreign exchange transactions. Conversion of RMB for capital account items, such as direct investment, loans, securities investment and repatriation of investment, however, is subject to the approval of SAFE or its local counterpart.

Under the Administration Rules for the Settlement, Sale and Payment of Foreign Exchange, foreign-invested enterprises may only buy, sell and/or remit foreign currencies at banks authorized to conduct foreign exchange business after providing valid commercial documents and, in the case of capital account item transactions, obtaining approval from SAFE or its local counterpart.

| 16 |

As an offshore holding company with a PRC subsidiary, we may (i) make additional capital contributions to our PRC subsidiaries, (ii) establish new PRC subsidiaries and make capital contributions to these new PRC subsidiaries, (iii) make loans to our PRC subsidiaries or consolidated affiliated entities, or (iv) acquire offshore entities with business operations in China in offshore transactions. However, most of these uses are subject to PRC regulations and approvals. For example:

| ● | capital contributions to our PRC subsidiaries, whether existing or newly established ones, must be approved by the Ministry of Commerce or its local counterparts; | |

| ● | loans by us to our PRC subsidiaries, each of which is a foreign-invested enterprise, to finance their activities cannot exceed statutory limits and must be registered with SAFE or its local branches; and | |

| ● | loans by us to our consolidated affiliated entities, which are domestic PRC entities, must be approved by the National Development and Reform Commission and must also be registered with SAFE or its local branches. |

On August 29, 2008, SAFE promulgated the Circular on the Relevant Operating Issues concerning the Improvement of the Administration of Payment and Settlement of Foreign Currency Capital of Foreign-invested Enterprises, or “Circular 142”. On March 30, 2015, SAFE issued the Circular of the State Administration of Foreign Exchange Concerning Reform of the Administrative Approaches to Settlement of Foreign Exchange Capital of Foreign-invested Enterprises, or “Circular 19”, which became effective on June 1, 2015, to regulate the conversion by foreign invested enterprises, or FIEs, of foreign currency into Renminbi by restricting how the converted Renminbi may be used. Circular 19 requires that Renminbi converted from the foreign currency-dominated capital of a FIE shall be managed under the Accounts for FX settlement and pending payment. The expenditure scope of such Account includes: expenditure within the business scope, payment of funds for domestic equity investment and Renminbi deposits, repayment of the Renminbi loans after completed utilization and so forth. A FIE shall truthfully use its capital by itself within the business scope and shall not, directly or indirectly, use its capital or Renminbi converted from the foreign currency-dominated capital for (i) expenditure beyond its business scope or expenditure prohibited by laws or regulations, (ii) disbursing Renminbi entrusted loans (unless permitted under its business scope), repaying inter-corporate borrowings (including third-party advance) and repaying Renminbi bank loans already refinanced to any third party. Where a FIE, other than a foreign-invested investment company, foreign-invested venture capital enterprise or foreign-invested equity investment enterprise, makes domestic equity investment by transferring its capital in the original currency, it shall obey the current provisions on domestic re-investment. Where such a FIE makes domestic equity investment by its Renminbi conversion, the invested enterprise shall first go through domestic re-investment registration and open a corresponding Accounts for FX settlement and pending payment, and the FIE shall thereafter transfer the conversion to the aforesaid Account according to the actual amount of investment. In addition, according to the Regulations of the People’s Republic of China on Foreign Exchange Administration, which became effective on August 5, 2008, the use of foreign exchange or Renminbi conversion may not be changed without authorization.

Violations of the applicable circulars and rules may result in severe penalties, including substantial fines as set forth in the Foreign Exchange Administration Regulations.

In light of the various requirements imposed by PRC regulations on loans to and direct investment in PRC entities by offshore holding companies, we cannot assure you that we will be able to complete the necessary government registrations or obtain the necessary government approvals on a timely basis, if at all, with respect to future loans to our PRC subsidiary or future capital contributions by us to our PRC subsidiary. If we fail to complete such registrations or obtain such approvals, our ability to use the proceeds we expect to receive from this offering and the concurrent private placement and to capitalize or otherwise fund our PRC operations may be negatively affected, which could materially and adversely affect our liquidity and our ability to fund and expand our business.

Seasonality

Our businesses are not subject to seasonality.

| 17 |

Insurance

We do not current maintain property, business interruption and casualty insurance. As our business matures, we expect to obtain such insurance in accordance customary industry practices in Malaysia, Hong Kong and China, as applicable.

Employees

As of March 27, 2017, we have 42 employees, including our Chief Executive Officer and Chief Financial Officer, located in the following territories:

| Country/Territory | Number of Employees | |

| Malaysia | 12 | |

| China | 19 | |

| Hong Kong | 11 |

As a result of the Employment Contract Law, all of our employees in China have executed standard written employment agreements with us.

We are required to contribute to the Employees Provident Fund under a defined contribution pension plan for all eligible employees in Malaysia between the ages of eighteen and fifty-five. We are required to contribute a specified percentage of the participant’s income based on their ages and wage level. The participants are entitled to all of our contributions together with accrued returns regardless of their length of service with the company. For the years ended December 31, 2016 and 2015, the contributions are $19,151 and $3,378, respectively.

We are required to contribute to the MPF for all eligible employees in Hong Kong between the ages of eighteen and sixty five. We are required to contribute a specified percentage of the participant’s income based on their ages and wage level. For the years ended December 31, 2016 and 2015, Greenpro Resources Limited and its subsidiaries did not have employees in Hong Kong. For the years ended December 31, 2016 and 2015, the MPF contributions by Greenpro Capital Corp. were $14,529 and $11,627, respectively. We have not experienced any significant labor disputes or any difficulties in recruiting staff for our operations.

We are required to contribute to the Social Insurance Schemes and Housing fund Schemes for all eligible employees in PRC. For the years ended December 31, 2016 and 2015, the contributions were $9,262 and $1,772, respectively.

Executive Office

Our principal executive office is located at Suite 2201, 22/F, Malaysia Building, 50 Gloucester Road, Wanchai, Hong Kong. Our principal telephone number is +(852) 3111-7718. Our website is at: http://www.greenprocapital.com. The information contained on our website is not, and should not be interpreted to be, a part of this prospectus.

You should carefully consider the risks described below and elsewhere in this report, which could materially and adversely affect our business, results of operations or financial condition. Our business faces significant risks and the risks described below may not be the only risks we face. Additional risks not presently known to us or that we currently believe are immaterial may materially affect our business, results of operations, or financial condition. If any of these risks occur, the trading price of our common stock could decline and you may lose all or part of your investment.

| 18 |

Risks Related to our Business

We have a limited operating history that you can use to evaluate us, and the likelihood of our success must be considered in light of the problems, expenses, difficulties, complications and delays frequently encountered by a small developing company.

We were incorporated in Nevada in July 2013. We have significant financial resources and as of December 31, 2016, we have generated $2,776,435 in revenues and incurred net losses of $222,323. The likelihood of our success must be considered in light of the problems, expenses, difficulties, complications and delays frequently encountered by a small company starting a new business enterprise and the highly competitive environment in which we will operate. We have a limited operating history upon which an evaluation of our future success or failure can be made. Our ability to achieve and maintain profitability and positive cash flow is dependent upon:

| ● | our ability to market our product and services | |

| ● | our ability to generate revenues; and | |

| ● | our ability to raise the capital necessary to continue marketing and developing our product. |

The report of our independent registered public accounting firm has previously expressed substantial doubt about the Company’s ability to continue as a going concern and future reports may similarly express a going concern.

Our auditors indicated in their report on the Company’s financial statements for the fiscal year ended December 31, 2015 that conditions existed that raise a substantial doubt about our ability to continue as a going concern due to our net loss for the year ended December 31, 2015. A similar future “going concern” opinion could impair our ability to finance our operations through the sale of equity, incurring debt, or other financing alternatives and/or negatively affect our relationships with customers and suppliers and/or negatively effect the willingness of our suppliers to allow us to maintain credit with them. Our ability to continue as a going concern will depend upon our ability to grow our operations and integrate newly acquired assets and operations, our ability to acquire additional assets and operations, and our ability to improve operating margins and regain profitability. If we are unable to achieve these goals, our business would be jeopardized and the Company may not be able to continue. If we ceased operations, it is likely that all of our investors would lose their investment.

Our operating results may prove unpredictable which could negatively affect our profit.

Our operating results are likely to fluctuate significantly in the future due to a variety of factors, many of which we have no control. Factors that may cause our operating results to fluctuate significantly include: our inability to generate enough working capital from future equity sales; the level of commercial acceptance by clients of our services; fluctuations in the demand for our service the amount and timing of operating costs and capital expenditures relating to expansion of our business, operations and infrastructure and general economic conditions.

If realized, any of these risks could have a material adverse effect on our business, financial condition and operating results.

If we are unable to gain any significant market acceptance for our service or establish a significant market presence, we may be unable to generate sufficient revenue to continue our business.

Our growth strategy is substantially dependent upon our ability to successfully market our service to prospective clients. However, our planned services may not achieve significant acceptance. Such acceptance, if achieved, may not be sustained for any significant period of time. Failure of our services to achieve or sustain market acceptance could have a material adverse effect on our business, financial conditions and the results of our operations.

Management’s ability to implement the business strategy may be slower than expected and we may be unable to generate a profit.

Our business plans, including offering a cloud auditing system and consulting services, may be slow to develop or may not occur at all. Our services may be slow to achieve profitability, or may not become profitable at all, which will result in losses. We may be unable to enter into our intended markets successfully. The factors that could affect our growth strategy include our success in (a) developing our business plan, (b) obtaining our clients, (c) obtaining adequate financing on acceptable terms, and (d) adapting our internal controls and operating procedures to accommodate our future growth.

| 19 |

Competitors may enter this market with superior services which would adversely affect our business.

We have identified a market opportunity for our business. Potential competitors may enter this sector with superior services. This would have an adverse effect upon our business and the results of our operations. In addition, a high level of support is critical for the successful marketing and recurring sales of our services. Although we currently only have a limited number of customers, we may need to improve our platform and software in order to assist our potential customers in using our platform, and we also need to provide effective support to future clients. Our inability to make necessary improvements and upgrades to our platform in the event of the expansion of our business, would adversely affect the sale of our services to potential customers and would harm our reputation.

Our use of open source and third-party software could impose limitations on our ability to commercialize our services.

We intend to incorporate open source software into our platform. Although we monitor our use of open source closely, the terms of many open source licenses have not been interpreted by U.S. courts or jurisdictions elsewhere, and there is a risk that such licenses could be construed in a manner that could impose unanticipated conditions or restrictions on our ability to commercialize our services. We could also be subject to similar conditions or restrictions should there be any changes in the licensing terms of the open source software incorporated into our products. In either event, we could be required to seek licenses from third parties in order to continue our services in the event re-engineering cannot be accomplished on a timely or successful basis, any of which could adversely affect our business, operating results and financial condition.

We also intend to incorporate certain third-party technologies, including software programs, into our website and may need to utilize additional third-party technologies in the future. However, licenses to relevant third-party technology may not continue to be available to us on commercially reasonable terms, or at all. Therefore, we could face delays in releases of our platform until equivalent technology can be identified, licensed or developed, and integrated into our current products. These delays, if they occur, could materially adversely affect our business, operating results and financial condition. Any disruption in our access to software programs or third-party technologies could result in significant delays in releases of our platform and could require substantial effort to locate or develop a replacement program. If we decide in the future to incorporate into our products any other software program licensed from a third party, and the use of such software program is necessary for the proper operation of our appliances, then our loss of any such license would similarly adversely affect our ability to release our products in a timely fashion.

The security of our computer systems may be compromised and harm our business.

A significant portion of our business operations is conducted through use of our computer network. Although we intend to implement security systems and procedures to protect the confidential information stored on these computer systems, experienced computer programmers and hackers may be able to penetrate our network security and misappropriate our confidential information or that of third parties. As well, they may be able to create system disruptions, shutdowns or effect denial of service attacks. Computer programmers and hackers also may be able to develop and deploy viruses, worms, and other malicious software programs that attack our networks or client computers, or otherwise exploit any security vulnerabilities, or that misappropriate and distribute confidential information stored on these computer systems. Any of the foregoing could result in damage to our reputation and customer confidence in the security of our products and services, and could require us to incur significant costs to eliminate or alleviate the problem. Additionally, our ability to transact business may be affected. Such damage, expenditures and business interruption could seriously impact our business, financial condition and results of operations.

| 20 |

Adverse developments in our existing areas of operation could adversely impact our results of operations, cash flows and financial condition.

Our operations are focused on utilizing our sales efforts which are principally located in South-East Asia. As a result, our results of operations, cash flows and financial condition depend upon the demand for our services in these regions. Due to our current lack of broad diversification in industry type and geographic location, adverse developments in our current segment of the midstream industry, or our existing areas of operation, could have a significantly greater impact on our results of operations, cash flows and financial condition than if our operations were more diversified.

We are an “emerging growth company” and we cannot be certain if the reduced disclosure requirements applicable to emerging growth companies will make our common stock less attractive to investors.

We are an “emerging growth company,” as defined in the JOBS Act, and we may take advantage of certain exemptions from various reporting requirements that are applicable to other public companies that are not “emerging growth companies” including not being required to comply with the auditor attestation requirements of Section 404 of the Sarbanes-Oxley Act, reduced disclosure obligations regarding executive compensation in our periodic reports and proxy statements and exemptions from the requirements of holding a nonbinding advisory vote on executive compensation and shareholder approval of any golden parachute payments not previously approved. We cannot predict if investors will find our common stock less attractive because we may rely on these exemptions. If some investors find our common stock less attractive as a result, there may be a less active trading market for our common stock and our stock price may be more volatile.

In addition, Section 107 of the JOBS Act also provides that an “emerging growth company” can take advantage of the extended transition period provided in Section 7(a)(2)(B) of the Securities Act for complying with new or revised accounting standards. An “emerging growth company” can therefore delay the adoption of certain accounting standards until those standards would otherwise apply to private companies. We are choosing to follow the extended transition period, and as a result, we will delay adoption of certain new or revised accounting standards on the relevant dates on which adoption of such standards is required for non-emerging growth companies.

Risks Related to Doing Business in South-East Asia

Our contractual arrangements may not be as effective in providing control over the variable interest entities as direct ownership.

We rely on contractual arrangements with our variable interest entities to hold part of our assets in Hong Kong. For a description of these contractual arrangements, see “Acquisition and Reorganization History - VIE Structure And Arrangements.” These contractual arrangements may not be as effective as direct ownership in providing us with control over our variable interest entities.

If we had direct ownership of the variable interest entities, we would be able to exercise our rights as an equity holder directly to effect changes in the boards of directors of those entities, which could effect changes at the management and operational level. Under our contractual arrangements, we may not be able to directly change the members of the boards of directors of these entities and would have to rely on the variable interest entities and the variable interest entity equity holders to perform their obligations in order to exercise our control over the variable interest entities. The variable interest entity equity holders may have conflicts of interest with us or our shareholders, and they may not act in the best interests of our company or may not perform their obligations under these contracts. For example, our variable interest entities and their respective equity holders could breach their contractual arrangements with us by, among other things, failing to conduct their operations, including maintaining our websites and using our domain names and trademarks which the relevant variable interest entities have exclusive rights to use, in an acceptable manner or taking other actions that are detrimental to our interests. Pursuant to the call option, we may replace the equity holders of the variable interest entities at any time pursuant to the contractual arrangements. Consequently, the contractual arrangements may not be as effective in ensuring our control over the relevant portion of our business operations as direct ownership.

| 21 |

Our business is subject to the risks of international operations.

Substantially all of our business operations are conducted in South-East Asia. Accordingly, our results of operations, financial condition and prospects are subject to a significant degree to economic, political and legal developments in the Asian countries we intend to develop business. Following the closing of our initial public offering, we will derive a significant portion of our revenue and earnings from the operation in Hong Kong, our principal business place, and also in Malaysia, China and other South-East Asian countries. Operating in multiple foreign countries involves substantial risk. For example, our business activities subject us to a number of laws and regulations, such as anti-corruption laws, tax laws, foreign exchange controls and cash repatriation restrictions, data privacy and security requirements, labor laws, intellectual property laws, privacy laws, and anti-competition regulations. As we expand into additional countries, the complexity inherent in complying with these laws and regulations increases, making compliance more difficult and costly and driving up the costs of doing business in foreign jurisdictions. Any failure to comply with foreign laws and regulations could subject us to fines and penalties, make it more difficult or impossible to do business in that country and harm our reputation.

We may be exposed to liabilities under the Foreign corrupt practices act, and any determination that we violated the foreign corrupt practices act could have a material adverse effect on our business.

We are subject to the Foreign Corrupt Practice Act, or FCPA, and other laws that prohibit improper payments or offers of payments to foreign governments and their officials and political parties by U.S. persons and issuers as defined by the statute for the purpose of obtaining or retaining business. We will have operations, agreements with third parties and make sales in South-East Asia, which may experience corruption. Our proposed activities in Asia create the risk of unauthorized payments or offers of payments by one of the employees, consultants, or sales agents of our Company, because these parties are not always subject to our control. It will be our policy to implement safeguards to discourage these practices by our employees. Also, our existing safeguards and any future improvements may prove to be less than effective, and the employees, consultants, or sales agents of our Company may engage in conduct for which we might be held responsible. Violations of the FCPA may result in severe criminal or civil sanctions, and we may be subject to other liabilities, which could negatively affect our business, operating results and financial condition. In addition, the government may seek to hold our Company liable for successor liability FCPA violations committed by companies in which we invest or that we acquire.

You may have difficulty enforcing judgments against us.