0001596961falseFY2022P3Yhttp://fasb.org/us-gaap/2022#GoodwillAndIntangibleAssetImpairmenthttp://fasb.org/us-gaap/2022#PropertyPlantAndEquipmentNethttp://fasb.org/us-gaap/2022#PropertyPlantAndEquipmentNethttp://fasb.org/us-gaap/2022#AccountsPayableAndAccruedLiabilitiesCurrenthttp://fasb.org/us-gaap/2022#AccountsPayableAndAccruedLiabilitiesCurrenthttp://fasb.org/us-gaap/2022#AccountsPayableAndAccruedLiabilitiesCurrenthttp://fasb.org/us-gaap/2022#AccountsPayableAndAccruedLiabilitiesCurrenthttp://fasb.org/us-gaap/2022#OtherLiabilitiesNoncurrenthttp://fasb.org/us-gaap/2022#OtherLiabilitiesNoncurrenthttp://fasb.org/us-gaap/2022#ConvertibleDebtNoncurrent http://rumbleon.com/20221231#LongTermDebtExcludingNotesPayableCurrentMaturities.0500015969612022-01-012022-12-3100015969612022-06-30iso4217:USD0001596961us-gaap:CommonClassBMember2023-03-16xbrli:shares0001596961us-gaap:CommonClassAMember2023-03-1600015969612022-12-31rmbl:retailLocation00015969612021-01-012021-12-3100015969612021-12-310001596961us-gaap:CommonClassAMember2022-12-31iso4217:USDxbrli:shares0001596961us-gaap:CommonClassAMember2021-12-310001596961us-gaap:CommonClassBMember2021-12-310001596961us-gaap:CommonClassBMember2022-12-310001596961rmbl:PowersportsMember2022-01-012022-12-310001596961rmbl:PowersportsMember2021-01-012021-12-310001596961rmbl:AutomotiveMember2022-01-012022-12-310001596961rmbl:AutomotiveMember2021-01-012021-12-310001596961rmbl:PartsAndOtherRevenueMember2022-01-012022-12-310001596961rmbl:PartsAndOtherRevenueMember2021-01-012021-12-310001596961rmbl:VehicleLogisticsMember2022-01-012022-12-310001596961rmbl:VehicleLogisticsMember2021-01-012021-12-310001596961rmbl:FinanceAndInsuranceMember2022-01-012022-12-310001596961rmbl:FinanceAndInsuranceMember2021-01-012021-12-310001596961us-gaap:CommonStockMemberus-gaap:CommonClassAMember2020-12-310001596961us-gaap:CommonClassBMemberus-gaap:CommonStockMember2020-12-310001596961us-gaap:AdditionalPaidInCapitalMember2020-12-310001596961us-gaap:RetainedEarningsMember2020-12-310001596961us-gaap:TreasuryStockCommonMember2020-12-3100015969612020-12-310001596961us-gaap:CommonClassBMemberus-gaap:CommonStockMember2021-01-012021-12-310001596961us-gaap:AdditionalPaidInCapitalMember2021-01-012021-12-310001596961us-gaap:TreasuryStockCommonMember2021-01-012021-12-310001596961us-gaap:RetainedEarningsMember2021-01-012021-12-310001596961us-gaap:CommonStockMemberus-gaap:CommonClassAMember2021-12-310001596961us-gaap:CommonClassBMemberus-gaap:CommonStockMember2021-12-310001596961us-gaap:AdditionalPaidInCapitalMember2021-12-310001596961us-gaap:RetainedEarningsMember2021-12-310001596961us-gaap:TreasuryStockCommonMember2021-12-310001596961us-gaap:CommonClassBMemberus-gaap:CommonStockMember2022-01-012022-12-310001596961us-gaap:AdditionalPaidInCapitalMember2022-01-012022-12-310001596961us-gaap:RetainedEarningsMember2022-01-012022-12-310001596961us-gaap:CommonStockMemberus-gaap:CommonClassAMember2022-12-310001596961us-gaap:CommonClassBMemberus-gaap:CommonStockMember2022-12-310001596961us-gaap:AdditionalPaidInCapitalMember2022-12-310001596961us-gaap:RetainedEarningsMember2022-12-310001596961us-gaap:TreasuryStockCommonMember2022-12-310001596961rmbl:FreedomTransactionMember2022-12-310001596961us-gaap:BuildingMember2022-01-012022-12-310001596961us-gaap:LeaseholdImprovementsMember2022-01-012022-12-310001596961us-gaap:FurnitureAndFixturesMembersrt:MinimumMember2022-01-012022-12-310001596961us-gaap:FurnitureAndFixturesMembersrt:MaximumMember2022-01-012022-12-310001596961srt:MinimumMemberus-gaap:SoftwareDevelopmentMember2022-01-012022-12-310001596961srt:MaximumMemberus-gaap:SoftwareDevelopmentMember2022-01-012022-12-310001596961rmbl:RideNowMember2021-08-312022-08-310001596961rmbl:FreedomTransactionMember2022-02-182022-02-18rmbl:segment0001596961rmbl:AutomotiveMember2022-01-012022-12-310001596961rmbl:PowersportsMember2022-01-012022-12-310001596961us-gaap:FranchiseRightsMember2022-01-012022-12-31xbrli:pure0001596961rmbl:PublicPlacementWarrantsMember2022-12-310001596961rmbl:HerculesWarrantsMember2022-12-310001596961rmbl:OaktreeWarrantMember2021-08-310001596961rmbl:OaktreeWarrantMember2022-09-300001596961rmbl:RideNowMember2021-08-31rmbl:subsidiaryrmbl:corporation0001596961rmbl:MergedRideNowEntitiesMemberrmbl:RideNowMember2021-08-31rmbl:entity0001596961rmbl:AcquiredRideNowEntitiesMemberrmbl:RideNowMember2021-08-310001596961rmbl:RideNowMember2021-08-312021-08-310001596961rmbl:PublicStockOfferingMember2021-08-312021-08-310001596961rmbl:CreditAgreementMember2021-08-312021-08-310001596961rmbl:NotARelatedPartyMemberrmbl:RideNowMember2021-08-310001596961rmbl:RelatedPartyMemberrmbl:RideNowMember2021-08-310001596961srt:DirectorMember2021-08-31rmbl:note0001596961rmbl:FreedomTransactionMember2022-02-180001596961rmbl:FreedomTransactionMember2022-06-222022-06-220001596961rmbl:DelayedDrawTermLoanFacilityMemberus-gaap:LineOfCreditMemberrmbl:FreedomTransactionMember2022-02-182022-02-180001596961rmbl:FreedomTransactionMember2022-01-012022-12-310001596961rmbl:RideNowMember2022-01-012022-12-310001596961rmbl:RideNowMember2021-01-012021-12-310001596961rmbl:NewVehiclesMember2022-01-012022-12-310001596961rmbl:NewVehiclesMember2021-01-012021-12-310001596961rmbl:PowersportsUsedVehiclesMember2022-01-012022-12-310001596961rmbl:PowersportsUsedVehiclesMember2021-01-012021-12-310001596961rmbl:AutomotiveUsedVehiclesMember2022-01-012022-12-310001596961rmbl:AutomotiveUsedVehiclesMember2021-01-012021-12-310001596961rmbl:UsedVehiclesMember2022-01-012022-12-310001596961rmbl:UsedVehiclesMember2021-01-012021-12-310001596961rmbl:VehicleSalesMember2022-01-012022-12-310001596961rmbl:VehicleSalesMember2021-01-012021-12-310001596961us-gaap:TransferredAtPointInTimeMember2022-01-012022-12-310001596961us-gaap:TransferredAtPointInTimeMember2021-01-012021-12-310001596961us-gaap:TransferredOverTimeMember2022-01-012022-12-310001596961us-gaap:TransferredOverTimeMember2021-01-012021-12-310001596961rmbl:ContractsInTransitMember2022-12-310001596961rmbl:ContractsInTransitMember2021-12-310001596961us-gaap:TradeAccountsReceivableMember2022-12-310001596961us-gaap:TradeAccountsReceivableMember2021-12-310001596961rmbl:FactoryReceivablesMember2022-12-310001596961rmbl:FactoryReceivablesMember2021-12-310001596961us-gaap:FinanceReceivablesMember2022-12-310001596961us-gaap:FinanceReceivablesMember2021-12-310001596961rmbl:NewVehiclesMember2022-12-310001596961rmbl:NewVehiclesMember2021-12-310001596961rmbl:PowersportVehiclesMember2022-12-310001596961rmbl:PowersportVehiclesMember2021-12-310001596961us-gaap:AutomobilesMember2022-12-310001596961us-gaap:AutomobilesMember2021-12-310001596961rmbl:PartsAccessoriesAndOtherMember2022-12-310001596961rmbl:PartsAccessoriesAndOtherMember2021-12-310001596961rmbl:TradeFloorPlanNotesPayableMember2022-12-310001596961rmbl:TradeFloorPlanNotesPayableMember2021-12-310001596961rmbl:NonTradeFloorPlanNotesPayableMember2022-12-310001596961rmbl:NonTradeFloorPlanNotesPayableMember2021-12-310001596961rmbl:SecuredOvernightFinancingRateMembersrt:MinimumMemberrmbl:NonTradeFloorPlanNotesPayableMember2022-01-012022-12-310001596961srt:MaximumMemberrmbl:SecuredOvernightFinancingRateMemberrmbl:NonTradeFloorPlanNotesPayableMember2022-01-012022-12-310001596961rmbl:TradeFloorPlanNotesPayableMemberrmbl:SecuredOvernightFinancingRateMembersrt:MinimumMember2022-01-012022-12-310001596961rmbl:TradeFloorPlanNotesPayableMembersrt:MaximumMemberrmbl:SecuredOvernightFinancingRateMember2022-01-012022-12-310001596961rmbl:FloorPlanNotesPayableMember2022-01-012022-12-310001596961us-gaap:LandMember2022-12-310001596961us-gaap:LandMember2021-12-310001596961us-gaap:BuildingAndBuildingImprovementsMember2022-12-310001596961us-gaap:BuildingAndBuildingImprovementsMember2021-12-310001596961us-gaap:LeaseholdImprovementsMember2022-12-310001596961us-gaap:LeaseholdImprovementsMember2021-12-310001596961us-gaap:EquipmentMember2022-12-310001596961us-gaap:EquipmentMember2021-12-310001596961us-gaap:FurnitureAndFixturesMember2022-12-310001596961us-gaap:FurnitureAndFixturesMember2021-12-310001596961us-gaap:SoftwareDevelopmentMember2022-12-310001596961us-gaap:SoftwareDevelopmentMember2021-12-310001596961us-gaap:VehiclesMember2022-12-310001596961us-gaap:VehiclesMember2021-12-310001596961srt:DirectorMemberrmbl:RideNowLeasesMember2022-12-31rmbl:lease0001596961rmbl:RelatedPartyMember2022-12-310001596961rmbl:NotARelatedPartyMember2022-12-310001596961us-gaap:FranchiseRightsMember2022-12-310001596961us-gaap:FranchiseRightsMember2021-12-310001596961us-gaap:OtherIntangibleAssetsMember2022-12-310001596961us-gaap:OtherIntangibleAssetsMember2021-12-310001596961rmbl:PowersportsMember2020-12-310001596961rmbl:AutomotiveMember2020-12-310001596961rmbl:VehicleLogisticsMember2020-12-310001596961rmbl:PowersportsMember2021-01-012021-12-310001596961rmbl:AutomotiveMember2021-01-012021-12-310001596961rmbl:VehicleLogisticsMember2021-01-012021-12-310001596961rmbl:PowersportsMember2021-12-310001596961rmbl:AutomotiveMember2021-12-310001596961rmbl:VehicleLogisticsMember2021-12-310001596961rmbl:VehicleLogisticsMember2022-01-012022-12-310001596961rmbl:PowersportsMemberrmbl:FreedomPowersportsMember2022-01-012022-12-310001596961rmbl:AutomotiveMemberrmbl:FreedomPowersportsMember2022-01-012022-12-310001596961rmbl:VehicleLogisticsMemberrmbl:FreedomPowersportsMember2022-01-012022-12-310001596961rmbl:FreedomPowersportsMember2022-01-012022-12-310001596961rmbl:PowersportsMemberus-gaap:SeriesOfIndividuallyImmaterialBusinessAcquisitionsMember2022-01-012022-12-310001596961rmbl:AutomotiveMemberus-gaap:SeriesOfIndividuallyImmaterialBusinessAcquisitionsMember2022-01-012022-12-310001596961us-gaap:SeriesOfIndividuallyImmaterialBusinessAcquisitionsMemberrmbl:VehicleLogisticsMember2022-01-012022-12-310001596961us-gaap:SeriesOfIndividuallyImmaterialBusinessAcquisitionsMember2022-01-012022-12-310001596961rmbl:PowersportsMember2022-12-310001596961rmbl:AutomotiveMember2022-12-310001596961rmbl:VehicleLogisticsMember2022-12-310001596961us-gaap:FranchiseRightsMember2020-12-310001596961rmbl:RideNowMemberus-gaap:FranchiseRightsMember2021-01-012021-12-310001596961rmbl:RideNowMemberus-gaap:FranchiseRightsMember2022-01-012022-12-310001596961rmbl:FreedomTransactionMemberus-gaap:FranchiseRightsMember2022-01-012022-12-310001596961us-gaap:SeriesOfIndividuallyImmaterialBusinessAcquisitionsMemberus-gaap:FranchiseRightsMember2022-01-012022-12-310001596961rmbl:HondaMemberus-gaap:FranchiseRightsMember2022-01-012022-12-310001596961us-gaap:FranchiseRightsMemberrmbl:A4WheelMember2022-01-012022-12-310001596961rmbl:TermLoanCreditAgreementMember2022-12-310001596961rmbl:TermLoanCreditAgreementMember2021-12-310001596961rmbl:LineOfCreditRumbleOnFinanceMember2022-12-310001596961rmbl:LineOfCreditRumbleOnFinanceMember2021-12-310001596961rmbl:PPPLoansMember2022-12-310001596961rmbl:PPPLoansMember2021-12-310001596961rmbl:PDMotorcyclesNotePayableMember2022-12-310001596961rmbl:PDMotorcyclesNotePayableMember2021-12-310001596961rmbl:RideNowManagementNotesPayableMember2022-12-310001596961rmbl:RideNowManagementNotesPayableMember2021-12-310001596961us-gaap:LondonInterbankOfferedRateLIBORMembersrt:MinimumMemberrmbl:NonTradeFloorPlanNotesPayableMember2022-01-012022-12-310001596961us-gaap:LondonInterbankOfferedRateLIBORMembersrt:MaximumMemberrmbl:NonTradeFloorPlanNotesPayableMember2022-01-012022-12-310001596961rmbl:TradeFloorPlanNotesPayableMemberus-gaap:LondonInterbankOfferedRateLIBORMembersrt:MinimumMember2022-01-012022-12-310001596961rmbl:TradeFloorPlanNotesPayableMemberus-gaap:LondonInterbankOfferedRateLIBORMembersrt:MaximumMember2022-01-012022-12-310001596961us-gaap:LineOfCreditMemberrmbl:InitialTermLoanFacilityMember2021-08-310001596961rmbl:DelayedDrawTermLoanFacilityMemberus-gaap:LineOfCreditMember2021-08-310001596961rmbl:OaktreeCreditAgreementMemberus-gaap:LineOfCreditMember2022-02-182022-02-180001596961rmbl:OaktreeCreditAgreementMemberus-gaap:LineOfCreditMember2022-12-310001596961rmbl:OaktreeCreditAgreementMemberus-gaap:LineOfCreditMember2022-10-012022-12-310001596961us-gaap:WarrantMemberrmbl:TermLoanCreditAgreementMember2022-12-310001596961us-gaap:LondonInterbankOfferedRateLIBORMemberrmbl:TermLoanCreditAgreementMember2021-08-312021-08-310001596961us-gaap:DebtInstrumentRedemptionPeriodOneMemberrmbl:TermLoanCreditAgreementMemberus-gaap:BaseRateMember2021-08-312021-08-310001596961rmbl:TermLoanCreditAgreementMemberus-gaap:BaseRateMemberus-gaap:DebtInstrumentRedemptionPeriodTwoMember2021-08-312021-08-310001596961rmbl:TermLoanCreditAgreementMember2021-08-310001596961rmbl:TermLoanCreditAgreementMemberus-gaap:BaseRateMember2022-12-310001596961rmbl:TermLoanCreditAgreementMember2022-01-012022-12-3100015969612021-03-1500015969612022-09-300001596961us-gaap:WarrantMemberrmbl:TermLoanCreditAgreementMember2021-03-150001596961us-gaap:WarrantMemberrmbl:TermLoanCreditAgreementMember2021-08-312021-08-310001596961rmbl:RumbleOnFinanceLineOfCreditMember2022-02-040001596961us-gaap:LineOfCreditMemberrmbl:AFCCreditLineMember2022-12-310001596961rmbl:AFCCreditLineMember2022-01-012022-12-310001596961rmbl:AFCCreditLineMember2021-01-012021-12-310001596961rmbl:JPMorganCreditLineMemberus-gaap:LineOfCreditMember2022-12-310001596961rmbl:JPMorganCreditLineMemberus-gaap:LineOfCreditMember2022-01-012022-12-310001596961rmbl:PPPLoansMember2020-05-010001596961us-gaap:ConvertibleNotesPayableMember2022-12-310001596961us-gaap:ConvertibleNotesPayableMember2021-12-310001596961rmbl:AutosportConvertibleNotes1536000Member2019-02-030001596961rmbl:AutosportConvertibleNotes1536000Member2022-12-310001596961rmbl:AutosportConvertibleNotes1536000Member2021-12-310001596961rmbl:NewNotesMember2020-01-100001596961rmbl:NewNotesMember2020-01-142020-01-140001596961rmbl:NewNotesMember2020-01-140001596961rmbl:NewNotesMembersrt:MaximumMember2020-01-142020-01-140001596961us-gaap:CommonClassBMemberrmbl:JMPSecuritiesLLCMemberrmbl:RumbleOnIncMember2020-01-140001596961rmbl:OldNotesMember2020-01-012020-12-31rmbl:tradingDay0001596961rmbl:ConvertibleNotesMember2020-01-142020-01-140001596961rmbl:ConvertibleNotesMember2020-01-140001596961rmbl:ConvertibleNotesMember2022-01-012022-12-310001596961us-gaap:RestrictedStockUnitsRSUMember2022-01-012022-12-310001596961us-gaap:PerformanceSharesMember2022-01-012022-12-310001596961us-gaap:CommonClassBMemberrmbl:EstateOfMrBerrardMember2021-09-302021-09-300001596961us-gaap:RestrictedStockUnitsRSUMember2022-12-310001596961us-gaap:StockOptionMember2022-12-310001596961us-gaap:RestrictedStockUnitsRSUMember2020-12-310001596961us-gaap:RestrictedStockUnitsRSUMember2021-01-012021-12-310001596961us-gaap:RestrictedStockUnitsRSUMember2021-12-310001596961us-gaap:RestrictedStockUnitsRSUMemberrmbl:LTIPPlanMember2022-01-012022-12-310001596961us-gaap:EmployeeStockOptionMember2022-01-012022-12-310001596961us-gaap:EmployeeStockOptionMemberus-gaap:ShareBasedCompensationAwardTrancheOneMember2022-01-012022-12-310001596961us-gaap:ShareBasedCompensationAwardTrancheTwoMemberus-gaap:EmployeeStockOptionMember2022-01-012022-12-310001596961us-gaap:EmployeeStockOptionMemberus-gaap:ShareBasedCompensationAwardTrancheThreeMember2022-01-012022-12-3100015969612020-01-012020-12-310001596961rmbl:PublicStockOfferingMember2020-01-012020-01-310001596961rmbl:PublicStockOfferingMember2020-01-310001596961rmbl:PublicStockOfferingMember2021-04-082021-04-080001596961rmbl:PublicStockOfferingMember2021-04-080001596961rmbl:PublicStockOfferingMember2021-08-3100015969612021-01-012021-03-310001596961us-gaap:WarrantMemberrmbl:TermLoanCreditAgreementMember2021-04-012021-06-300001596961us-gaap:WarrantMemberrmbl:TermLoanCreditAgreementMember2021-06-300001596961us-gaap:WarrantMemberrmbl:TermLoanCreditAgreementMember2021-08-3100015969612020-05-182020-05-180001596961rmbl:PublicStockOfferingMember2017-10-232017-10-230001596961rmbl:PublicPlacementWarrantsMember2017-10-230001596961rmbl:HerculesAprilWarrantsMember2018-04-300001596961rmbl:HerculesAprilWarrantsTrancheTwoMember2018-04-3000015969612018-04-300001596961rmbl:HerculesOctoberWarrantsMember2018-10-310001596961rmbl:UnderwriterWarrantsMember2022-12-310001596961rmbl:HerculesAprilWarrantsMember2022-12-310001596961rmbl:HerculesOctoberWarrantsMember2022-12-310001596961rmbl:UnderwriterWarrantsMember2022-01-012022-12-310001596961rmbl:HerculesAprilWarrantsMember2022-01-012022-12-310001596961rmbl:HerculesOctoberWarrantsMember2022-01-012022-12-310001596961us-gaap:RestrictedStockUnitsRSUMember2022-01-012022-12-310001596961us-gaap:StockOptionMember2022-01-012022-12-310001596961rmbl:OaktreeWarrantMember2022-01-012022-12-310001596961us-gaap:WarrantMember2022-01-012022-12-310001596961us-gaap:CommonClassBMember2022-01-012022-12-310001596961us-gaap:RestrictedStockUnitsRSUMember2021-01-012021-12-310001596961us-gaap:StockOptionMember2021-01-012021-12-310001596961us-gaap:WarrantMember2021-01-012021-12-310001596961rmbl:OtherWarrantMember2021-01-012021-12-310001596961us-gaap:CommonClassBMember2021-01-012021-12-310001596961us-gaap:DomesticCountryMember2022-12-310001596961us-gaap:DomesticCountryMember2021-12-310001596961us-gaap:StateAndLocalJurisdictionMember2022-12-310001596961srt:DirectorMember2022-12-310001596961us-gaap:BridgeLoanMemberrmbl:BRFFinanceMembersrt:AffiliatedEntityMember2021-03-120001596961rmbl:PublicStockOfferingMembersrt:DirectorMember2021-08-312021-08-310001596961rmbl:PublicStockOfferingMembersrt:DirectorMember2021-08-310001596961srt:DirectorMemberrmbl:RideNowLeasesMember2021-08-310001596961srt:DirectorMemberrmbl:RideNowLeasesMember2021-08-312021-08-310001596961rmbl:RideNowReinsuranceProductSalesMembersrt:DirectorMember2022-01-012022-12-310001596961rmbl:CoulterManagementGroupLLLPMembersrt:DirectorMember2022-01-012022-12-310001596961rmbl:CoulterManagementGroupLLLPMember2022-12-31rmbl:director0001596961rmbl:RideNowManagementLLLPMembersrt:DirectorMember2022-01-012022-12-310001596961rmbl:RideNowManagementLLLPMembersrt:DirectorMember2021-01-012021-12-310001596961rmbl:RideNowManagementLLLPMember2022-12-310001596961rmbl:RideNowManagementLLLPMember2022-06-272022-06-270001596961rmbl:RNBeachLLCMembersrt:DirectorMember2021-12-312021-12-310001596961rmbl:BidpathSoftwareLicenseMembersrt:DirectorMember2022-12-310001596961rmbl:BidpathSoftwareLicenseMembersrt:DirectorMember2022-01-192022-01-190001596961rmbl:ReadyTeamGrowLLCRecruitingServicesMember2022-01-012022-12-310001596961us-gaap:OperatingSegmentsMemberrmbl:PowersportsMember2022-12-310001596961us-gaap:OperatingSegmentsMemberrmbl:AutomotiveMember2022-12-310001596961us-gaap:OperatingSegmentsMemberrmbl:VehicleLogisticsMember2022-12-310001596961us-gaap:IntersegmentEliminationMember2022-12-310001596961us-gaap:OperatingSegmentsMemberrmbl:PowersportsMember2022-01-012022-12-310001596961us-gaap:OperatingSegmentsMemberrmbl:AutomotiveMember2022-01-012022-12-310001596961us-gaap:OperatingSegmentsMemberrmbl:VehicleLogisticsMember2022-01-012022-12-310001596961us-gaap:IntersegmentEliminationMember2022-01-012022-12-310001596961us-gaap:OperatingSegmentsMemberrmbl:PowersportsMember2021-12-310001596961us-gaap:OperatingSegmentsMemberrmbl:AutomotiveMember2021-12-310001596961us-gaap:OperatingSegmentsMemberrmbl:VehicleLogisticsMember2021-12-310001596961us-gaap:IntersegmentEliminationMember2021-12-310001596961us-gaap:OperatingSegmentsMemberrmbl:PowersportsMember2021-01-012021-12-310001596961us-gaap:OperatingSegmentsMemberrmbl:AutomotiveMember2021-01-012021-12-310001596961us-gaap:OperatingSegmentsMemberrmbl:VehicleLogisticsMember2021-01-012021-12-310001596961us-gaap:IntersegmentEliminationMember2021-01-012021-12-310001596961rmbl:DisputesAndClaimsWithFormerMinorityShareholdersOfRideNowMember2022-01-012022-12-310001596961rmbl:RumbleOnFinanceLineOfCreditMember2022-12-310001596961rmbl:RumbleOnFinanceLineOfCreditMemberus-gaap:SubsequentEventMember2023-01-310001596961rmbl:RumbleOnFinanceLineOfCreditMemberus-gaap:SubsequentEventMember2023-03-162023-03-16

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-K

| | | | | |

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2022 | | | | | |

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from ________________ to________________

Commission file number 001-38248

RumbleOn, Inc.

(Exact name of registrant as specified in its charter)

| | | | | | | | |

| Nevada | | 46-3951329 |

(State or other jurisdiction of

incorporation or organization) | | (I.R.S. Employer

Identification No.) |

901 W Walnut Hill Lane Irving Texas | | 75038 |

| (Address of Principal Executive Offices) | | (Zip Code) |

(214) 771-9952

(Registrant's telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

| | | | | | | | | | | | | | |

| Title of each class | | Trading Symbol(s) | | Name of exchange on which registered |

| Class B Common Stock, $0.001 par value | | RMBL | | The Nasdaq Stock Market LLC |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes x No ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of "large accelerated filer," "accelerated filer," "smaller reporting company," and "emerging growth company" in Rule 12b-2 of the Exchange Act.

| | | | | | | | | | | |

| Large accelerated filer | ¨ | Accelerated filer | x |

| Non-accelerated filer | ¨ | Smaller reporting company | x |

| | | Emerging growth company | ¨ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report Yes ☒ No ☐

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ¨ No x

As of June 30, 2022, the aggregate market value of shares of common stock held by non-affiliates of the registrant was approximately $149.7 million.

The number of shares of Class B Common Stock, $0.001 par value, outstanding on March 15, 2023 was 16,273,768 shares. In addition, 50,000 shares of Class A Common Stock, $0.001 par value, were outstanding on March 15, 2023.

Portions of the registrant’s proxy statement relating to its 2023 Annual Meeting of Stockholders to be filed with the SEC within 120 days after the end of the year ended December 31, 2022 are incorporated herein by reference in Part III.

Annual Report on Form 10-K

for the Year Ended December 31, 2022

Table of Contents

Annual Report on Form 10-K

for the Year Ended December 31, 2022

ITEM 1. BUSINESS.

In this Annual Report on Form 10-K for the year ended December 31, 2022 (the "2022 Form 10-K"), "we," "our," "us," "RumbleOn," and the "Company" refer to RumbleOn, Inc. and its consolidated subsidiaries at December 31, 2022, unless the context requires otherwise.

Forward-Looking and Cautionary Statements

This 2022 Form 10-K contains forward-looking statements as defined in the Private Securities Litigation Reform Act of 1995. Forward-looking statements generally can be identified by words such as "anticipates," "believes," "estimates," "expects," "intends," "plans," "predicts," "projects," "will be," "will continue," "will likely result," and similar expressions. These forward-looking statements are based on current expectations and assumptions that are subject to risks and uncertainties, which could cause our actual results to differ materially from those reflected in forward-looking statements. Factors that could cause or contribute to such differences in our actual results include, but are not limited to, those discussed in this 2022 Form 10-K, and in particular, the risks discussed under the caption "Risk Factors" in Item 1A and those discussed in other documents we file with the Securities and Exchange Commission (the "SEC"). Given these risks and uncertainties, readers are cautioned not to place undue reliance on such forward-looking statements. We undertake no obligation to revise or update forward-looking statements, except as required by law.

Market and Industry Data

Some of the market and industry data contained in this 2022 Form 10-K is based on independent industry publications or other publicly available information. Although we believe that these independent sources are reliable, we have not independently verified and cannot assure you as to the accuracy or completeness of this information. As a result, you should be aware that the market and industry data contained herein, and our beliefs and estimates based on such data, may not be reliable.

Our Company

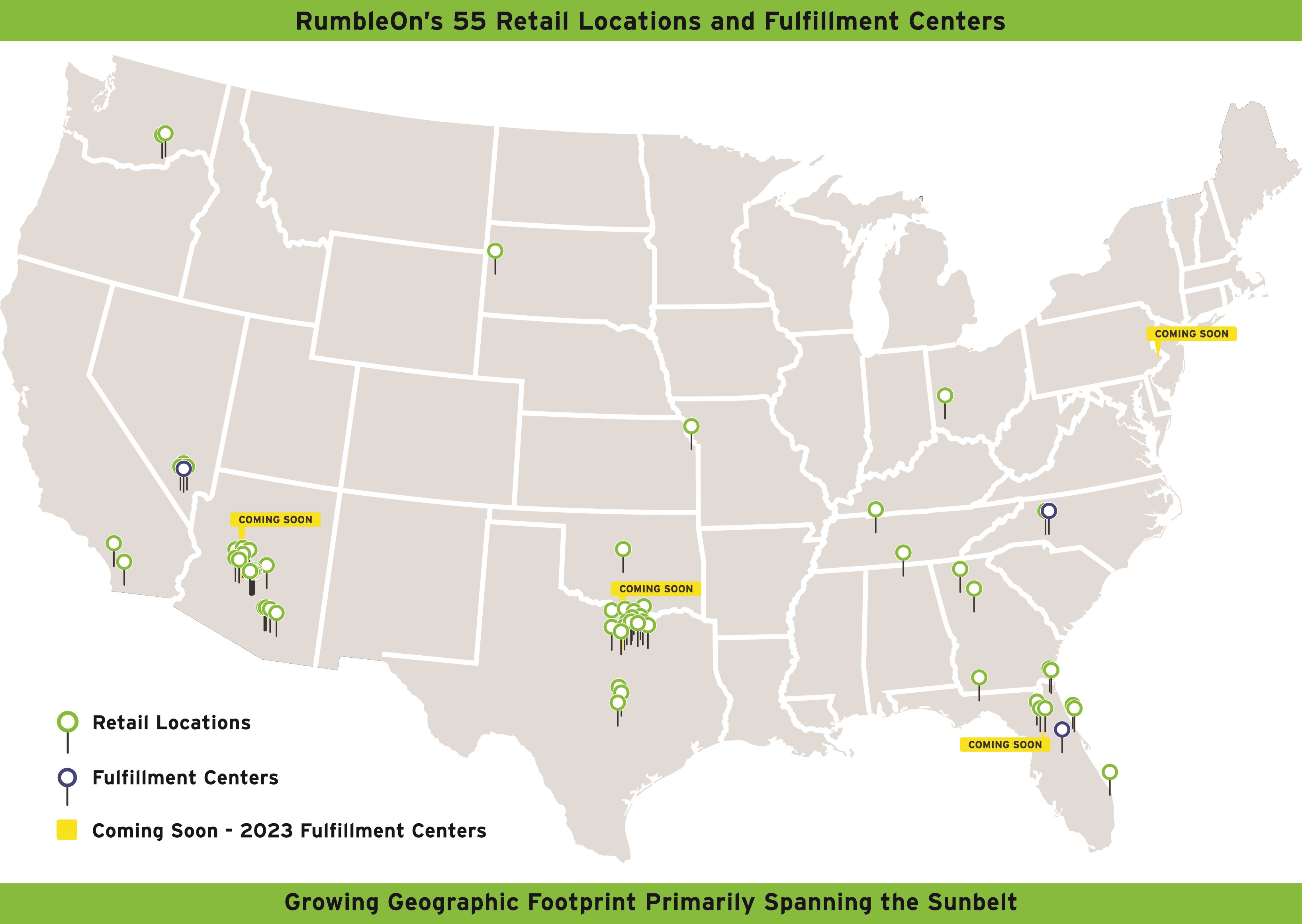

RumbleOn is the nation's first, largest, and only publicly-traded, technology-based platform in the powersports industry. Headquartered in the Dallas Metroplex, RumbleOn is revolutionizing the customer experience for outdoor enthusiasts across the country and making powersport vehicles accessible to more people in more places than ever before. We are transforming the powersports customer experience by giving consumers what they want - a wide selection, great value and quality, transparency, and an easy, friction-free transaction. Every element of our business, from inventory procurement to fulfillment to overall ease of transactions, whether online or on-site at one of our 55 retail locations, has been built for a singular purpose – to create a customer experience without peer in the powersports industry.

Although our primary focus is on the customer experience and building market share in the powersports industry, during 2022 we participated in the wholesale automotive industry through our wholly-owned distributors of used automotive inventory, Wholesale, Inc. ("Wholesale Inc") and our exotics retailer AutoSport USA, Inc., which does business under the name Got Speed. In the third quarter of 2022, we announced we would be winding down our wholesale automotive business, which we expect to complete during the first half of 2023. Our logistics services company, Wholesale Express, LLC ("Wholesale Express"), provides freight brokerage services facilitating transportation for dealers and consumers.

Incorporated in Nevada in 2013, we have been building the RumbleOn brand and vision since 2016. Led by our co-founder, chairman, and Chief Executive Officer Marshall Chesrown, we have achieved and built upon key milestones:

•April 2017: launched RumbleOn.com.

•October 2017: celebrated our initial listing on The Nasdaq Stock Market.

•October 2018: acquired Wholesale Inc and Wholesale Express.

•August 2021: acquired the RideNow companies (the “RideNow Transaction”), a collection of 41 retail powersports locations with a geographic footprint spanning primarily the Sunbelt.

•September 2021: processed the first powersports vehicle through our Orlando Fulfillment Center.

•February 2022: completed the initial funding of our captive consumer finance facility, RumbleOn Finance.

•February 2022: acquired Freedom Powersports (the “Freedom Transaction”), adding ten retail locations in North Texas, one in Alabama, and two in Georgia.

•February 2022: unveiled the regional management structure, anchored by tenured team members of RideNow.

•September 2022: opened our Fulfillment Center in Concord, North Carolina.

•November 2022: acquired Powersports Honda franchise in North Texas.

•December 2022: acquired two full line Polaris franchises in North Texas.

•January 2023: opened our Fulfillment Center in Las Vegas, Nevada.

•February 2023: acquired Red Hills powersports, a single retail location representing 10 brands, in Tallahassee, Florida.

•March 2023: entered into an engagement letter with J.P. Morgan to review our balance sheet initiatives and options.

These key events well-position RumbleOn as the first mover in transforming the powersports industry through our customer experience focused, technology based, Omnichannel platform.

Our Industry and Opportunity

We operate primarily in the powersports industry, offering significant scale and breadth of products and our platform from which we will provide our only of its kind powersports customer experience. From our view, powersports includes motorcycles, side-by-sides, ATV, UTV, snowmobile, and personal watercraft ("PWC") along with related parts and components. If you add in the largely unaccounted for but significant peer-to-peer market in used powersports, which RumbleOn believes represents up to 70% of used powersports transactions, the total addressable powersports market is likely in excess of $100 billion.

The powersports marketplace in the United States is highly fragmented. We face competition from traditional franchised dealers who sell both new and used vehicles; independent used powersports dealers; online and mobile sales platforms; and private parties. We believe that the principal competitive factors in our industry are delivering an outstanding consumer experience, competitive sourcing of quality inventory, breadth and depth of product selection, and value pricing.

Our competitors vary in size and breadth of their product offerings. We believe that our principal competitive advantages in powersports sales include our ability to provide a high degree of customer satisfaction with the buying experience by virtue of our platform. We provide customers the opportunity to experience RumbleOn's offerings online, in-store, and through our mobile app, or any combination of those three options. Our ability to make a cash offer to purchase a vehicle with our customer-friendly purchase process, and our breadth of selection of the most popular makes and models available online and in-store provides competitive sourcing and sales.

RumbleOn's Solution - Creating the Future of Powersports

RumbleOn is creating a best-in-class experience in powersports for our customers. Doing so requires offering unmatched choice and selection and replicating an outstanding customer experience throughout the lifecycle of powersports ownership, one customer and one transaction at a time.

Customers come to RumbleOn's 55 retail locations as well as our more than 60 websites to shop for new and highest-quality used powersports products as well as for parts, accessories and merchandise. We address the entire powersports market. We are reimagining and revolutionizing the customer experience on our technology-led, internet-based platforms, and we are doing so for everyone - from the powersports enthusiast to the novice, and everyone in between - with a focus on four key initiatives:

•Creating an end-to-end ownership experience means we are not focused solely on the initial transaction with a customer. Rather, our customer experience enables building lifelong connectivity to each customer. With each customer interaction, we focus on key touch points that continue to keep our customers engaged throughout their powersports ownership experience. Quality assurance, clear and consistent pricing, professional pickup and delivery, customization, after sales service, and guarantees are just a few of the ways we are building a reliable and consistent customer experience. Our offerings, and our entire customer experience, are designed to turn a single transaction into a lifetime relationship.

•Providing the largest and best selection of highest-quality inventory enables us to provide many offerings to all powersports customers coast to coast. We are well-positioned to acquire high-quality used vehicles through the strength of our online Cash Offer Tool, a unique and important competitive advantage for RumbleOn. Affording our customers the ability to visit a retail location and receive cash for their used powersports unit instantaneously gives them peace of mind, and provides us the opportunity to drive a meaningful amount of incremental used inventory onto our platform. We are also leveraging robust data from the Cash Offer Tool and from the information acquired from our acquisitions and now being gathered from our 55 RideNow Powersports retail locations to ensure that the right vehicle is in the right place at the right time - with the right price.

•Building the premier destination for new and used powersports vehicles and introducing more used inventory to our showrooms as well as online attracts new customers to our platform and, most importantly, new riders to the industry due to affordability. We are focused on both new and used, retail sales, however, the opportunity to dramatically increase the number of used powersports unit sales presents our greatest near-term opportunity, as new vehicle inventory supply normalizes. We can better control used inventory than new because used is not dependent on a manufacturer's production, allocation, or distribution constraints. In fact, our broad access to used inventory is - and will continue to be - an important differentiator for RumbleOn in any market environment.

Our Growth Strategies

The key metric to our powersports business is retail vehicle unit sales, both online and in-store. Unit sales drives revenue and provides the opportunity to build additional revenue through financing, parts, merchandise, and accessories, each of which are higher margin revenue streams. As we scale our business, we will create additional opportunities to expand revenue streams. However, additional revenue opportunities begin with retail vehicle unit sales and, as a result, our growth strategy is focused on this metric.

Our ability to increase vehicle unit sales is a function of our market penetration in existing markets, the number of markets we operate in, and our ability to build and maintain our brands by offering great value, transparency, and an outstanding customer experience.

Optimize Our Inventory Selection and Centralization

We continue to optimize and broaden the selection of new and used powersports vehicles we make available to our customers. Expanding our inventory selection enhances the customer experience by ensuring each visitor, either online or in-store, finds a vehicle that matches his or her preferences. Optimizing our new inventory significantly depends on continuing our outstanding relationships with our manufacturers ("OEM"). As a result of these relationships, during 2022, we added 60 new franchises to our retail locations, primarily organically, and including three key tuck-in acquisitions in our North Texas market. Optimizing our used inventory selection depends on our ability to source and acquire enough high-quality used vehicles, and our ability to use data to ensure each used vehicle is at the right place, at the right time, at the right price.

We continue implementing our fulfillment strategy with near real-time inventory replenishment to make the right powersports units available in the right quantities at the right locations. This centralization of inventory will launch company-

wide virtual selling through access to all company-owned inventory rather than only those vehicles that might be available at an individual location. Fulfillment will increase the probability that our customers can find their powersports unit of choice on our platform, thereby enhancing the customer experience while eliminating geographic boundaries. With digital inventory integration and over 60 individual websites sharing content and increasing available data, RumbleOn will be top-of-mind for powersports searches. All of the technology infrastructure required has been launched or is under development and will be implemented throughout 2023 and beyond.

Continue to Innovate and Extend Our Technology Leadership

We continue expanding our competitive dominance with leading-edge technology. From our founding, we have been laying the groundwork to offer a friction-free and fully integrated customer experience both online and in-store. We are building the technology engine to enable this integration, while methodically expanding our retail footprint, driving towards online selling without geographic boundaries. With this goal in mind, we intend to launch our new corporate website under the RumbleOn brand during the first half of 2023 and our all new RideNow-branded website later in the second quarter of 2023. Our RideNow website will have unmatched features for our customers, allowing them to see all inventory in one place and it will have the ability to push inventory to individual dealer websites, resulting in a better online presence and customer experience. The plan calls for the constant roll out of new features, as our online presence improves and matures. In conjunction with our integrated CRM, we plan to launch online soft and hard credit pulls and lending pre-qualifications, just to name a few of the exciting features. Lastly, in the first half of 2023, we intend to roll out a new internally developed reporting technology that will increase visibility across our enterprise, improve sales reporting, and provide real time actionable data at the store level. Store managers will now see how they are performing versus expectations and how they compare in real time with their peers across the country.

From the start of RumbleOn, one key differentiator and a lynch pin to the competitive advantage we have built in powersports is our Cash Offer Tool, which supplies proprietary data for thousands of unique Vehicle Identification Number (VIN) inputs. In addition to actual retail sales and transaction data from the acquired RideNow and Freedom Powersports' databases. Marrying this data creates a data-driven "market maker" that does not exist in the industry today. Integrating real-time pricing and sales data from in-store transactions will also enable us to further optimize offers and pricing.

We will continue to make significant investments in improving and adding to our online customer offering, subject to our performance and available operating cash flow as we intend to self-fund these initiatives. We believe that the complexity of the traditional powersports retail transaction provides substantial opportunity for our planned technology investments and that our leadership and continued growth will enable us to invest responsibly in further enhancing the customer experience.

Enhancing Our In-store Experience

Beyond innovative technology and inventory integration, we use our retail locations to augment the online experience- and vice versa - to offer a simple, friction-free customer experience. A key component to transforming the customer experience to support our growth strategy is enhancing the in-store experience and we are strategically expanding our geographic retail footprint. In early 2022, we added 13 additional retail locations, entrenching our position in the North Texas market and expanding our geographic foot print to Alabama and Georgia. In addition, during the first quarter of 2023, we acquired an important multi-line retail location in Tallahassee, Florida, further expanding our dominance in North Florida. We currently operate in 55 retail locations, three fulfillment or hybrid fulfillment/retail locations to open (with four more expected during 2023), one used powersports center, as shown below.

We employ three primary considerations for expanding our brick-and-mortar presence: (1) attract great people, (2) identify desired locations, and (3) implement appropriate and balanced brand mix.

Attracting Great People. We believe any great customer experience in powersports begins with great people providing consumers the opportunity to fulfill their passion. From our executive team to our customer facing professionals to our back-office and corporate personnel, the RumbleOn team is singularly focused on transforming the customer experience in powersports, both online and in-store. As we expand our physical presence, whether through new retail locations or as we build out our fulfillment centers, finding great people who believe in our mission is key.

Identifying Desired Locations. We believe desired geography means more than finding new markets; it also means making sure we can put the right powersports vehicle in the right place at the right price to maximize our return on the asset. This is a key goal of our fulfillment centers. And of course, we are always looking for strategic acquisition candidates, whether a large group such as Freedom Powersports or a key tuck-in opportunity to improve the capabilities of an existing location.

Implementing Appropriate Brand Mix. Powersports retail provides the opportunity to put many different new brands under one roof along with the proper mix of used inventory. Of course, having that opportunity and taking advantage of that opportunity correctly are two different things. Our outstanding relationships with our OEMs have provided us the opportunity to organically add more than 60 new franchises to our existing retail locations. And we continue leveraging our used inventory sourcing advantage to keep our retail locations fully stocked with the right mix of preferred brands based on data and market share, and thereby further enhance the customer experience.

A fourth consideration also plays a role as we enhance our in-store experience through organic and acquisitive growth: any such investments remain subject to a prudent use of our financial and other resources based on our performance and our available cash from operations as we intend to self-fund our growth.

Develop Broad Consumer Awareness of Our Brand

We believe that creating a unified customer experience, requires a single consumer-facing brand for all our retail locations. During 2022, we began rolling out the “RideNow Powersports” brand across all our retail locations and the

foundation will be our technology, our infrastructure, and our corporate culture. We are in the early stages of this rollout, and we are encouraged by the impact on performance and the excitement it has clearly created.

RumbleOn Technology

Innovative technology continues to underpin every endeavor at RumbleOn through our ongoing mission to disrupt the powersports industry and our focus on the customer experience. We leverage technology and data to drive change. At a high-level, we believe there are five main areas where leveraging these innovations provides us a competitive advantage and improves the customer experience: (1) our proprietary supply chain pricing and distribution software; (2) our Omnichannel and mobile-first web application; (3) centralized CRM and Inventory; (4) Dealer network support channels; and (5) Data warehousing & reporting, enterprise wide.

(1) RumbleOn's proprietary supply chain and distribution software:

•Looks at the overall supply chain and reconfigures inventory for the purpose of acquisition and distribution. Our technology aggregates multiple data sources in real-time, tracking and cataloging inventory across the country.

•Analyzes real-time market data to inform our acquisition decisions, continually capturing and archiving such data using advanced algorithms to calibrate pricing and estimate freight and reconditioning expenses. The values are then used in our Cash Offer Tool to quickly determine a fair and reasonable, non-negotiable offer.

(2) RumbleOn's mobile-first web application strategy:

•Enhances our website and mobile application to provide a compelling customer experience, from the front-end user interface and powerful search tools to enabling secure data, document, and payment exchanges between parties. We also optimize search engine marketing to provide a lower overall cost of customer acquisition.

(3) Centralized customer relationship management and centralized inventory

•Enhanced hub of combined RumbleOn, RideNow, and Freedom Powersports customer repositories for marketing, support and service.

•Enterprise-wide centralized inventory, enhancing distribution, pricing, allocation and growth.

(4) Dealer network support channels

•New enhancements for our dealerships, provides on-demand pricing, transfers of allocation through streamlined workflows at the pace of business to benefit the needs of our customers.

(5) Data warehousing and reporting, enterprise-wide

•The combined digital intelligence from RideNow, Freedom Powersports, and RumbleOn has produced a rich eco-system of available data to promote growth across all facets of the business concerning parts, service, sales, marketing, and retention.

To deliver our supply chain software and on-line strategies, RumbleOn leverages its proprietary and exclusive-use technology portfolio, which includes:

•A series of modeling tools & technologies for consolidating internal and external data to provide profitability estimates for inventory available for purchase;

•A proprietary series of inventory management and business intelligence technologies that tracks the lifecycle of a vehicle from acquisition through delivery;

•An automated photography technology that combines high-quality photos to produce an interactive, 360-degree virtual tour of the vehicle;

•A catalog of websites that includes advanced filtering and search technology that assist multi-lead generation across participating partners; and

•A proprietary transportation management system and assignment technology to optimize the transport of purchased inventory for acquisition and dealer distribution.

In addition to our proprietary/exclusive use technology, we also rely on third party technology, including the following:

•A cloud based network infrastructure for hosting websites, inventory data, CRM-Data/reporting;

•Software libraries, development environments, and tools;

•Services to allow customers to digitally sign contracts; select local services; and

•Online customer service call center management software.

In short, our business is driven by data and technology at all stages of the process, from acquisition, inventory purchasing, reconditioning, photography, transportation, and annotation through in-store or online merchandising, sales, financing, trade-ins, logistics, and delivery.

We protect our technology and other intellectual property through a combination of trademarks, domain names, copyrights, trade secrets, patented technology, and contractual provisions and restrictions on access and use of our proprietary information and technology. We have a portfolio of trademark registrations in the United States, including registrations for "RumbleOn," the RumbleOn logo, "RideNow," and the RideNow logo. We are the registered holder of a variety of domestic and international domain names, including "rumbleon.com."

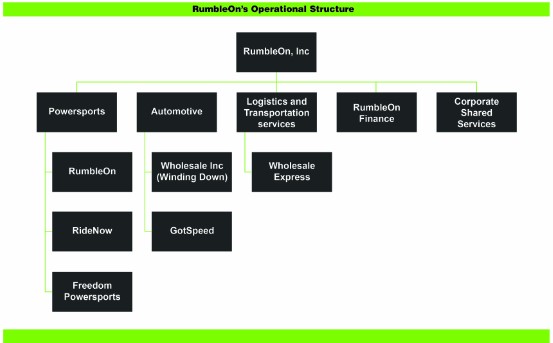

Operational Structure

The following chart summarizes our organizational structure as of December 31, 2022. This chart is provided for illustrative purposes only and does not reflect all legal entities owned or controlled by us:

Seasonality

Historically, the powersports industry has been seasonal with traffic and sales strongest in the spring and summer quarters. Sales and traffic are typically slowest in the winter quarter but increase typically in the spring season, coinciding with tax refunds and improved weather conditions. Given this seasonality, we expect our quarterly results of operations, including

our revenue, gross profit, net income (loss), and cash flow to vary accordingly. Over time, we expect to normalize to seasonal trends, using data and logistics to move inventory to the right place, at the right time, at the right price.

Government Regulation

Various aspects of our business are or may be subject, directly or indirectly, to U.S. federal and state laws and regulations. Failure to comply with such laws or regulations may result in the suspension or termination of our ability to do business in affected jurisdictions or the imposition of significant civil and criminal penalties, including fines or the award of significant damages against us and our dealers in class action or other civil litigation.

Vehicle Sales. Our sale and purchase of vehicles, both new and pre-owned, related products and services, and third-party finance products, are subject to the state and local dealer licensing requirements in the jurisdictions in which we have retail or wholesale locations. Regulators of jurisdictions where our customers reside, but in which we do not have a dealer or financing license could require that we obtain a license or otherwise comply with various state regulations. Despite our belief that we are not subject to the licensing requirements of those jurisdictions in which we do not have a physical presence, regulators may seek to impose punitive fines for operating without a license or demand we seek a license in those jurisdictions, any of which may inhibit our ability to do business in those jurisdictions, increase our operating expenses and adversely affect our financial condition and results of operations.

Consumer Finance. The financing we offer customers is subject to federal and state laws regulating the advertising and provision of consumer finance options, the collection of consumer credit and financial information, along with requirements related to online payments and electronic funds transfers, the regulations and state licenses applicable depend upon whether RumbleOn Finance or a third-party is the entity extending credit to such customers. Most states regulate retail installment sales, including setting a maximum interest rate, caps on certain fees, or maximum amounts financed. In addition, certain states require that finance companies file a notice of intent or have a sales finance license or an installment sellers license in order to solicit or originate installment sales in that state.

Logistics and Transportation. Our Wholesale Express logistics operations, which brokers and facilitates the transportation of vehicles primarily between and among dealers, is subject to motor-carrier rules and regulations promulgated by the United States Department of Transportation ("DOT") and the states through which their customers' vehicles are transported. Additionally, the vendors whom Wholesale Express relies upon are subject to federal and state regulation concerning transport vehicle dimensions, transport vehicle conditions, driver motor vehicle record history, driver alcohol and drug testing, and driver hours of service. More restrictive limitations on vehicle weight and size, condition, trailer length and configuration, methods of measurement, driver qualifications, or driver hours of service may increase the costs charged to Wholesale Express by its vendors, which may adversely affect our financial condition, operating results, and cash flows. If we fail to comply with the DOT regulations or if those regulations become more stringent, we could be subject to increased inspections, audits, or compliance burdens. Regulatory authorities could take remedial action including imposing fines, suspending, or shutting down our Wholesale Express operations.

Environmental Laws and Regulations. We are subject to a variety of federal, state, and local environmental laws and regulations that pertain to our operations. The regulations concern material storage, air quality, waste handling, and water pollution control. The regulations also regulate our use and operation of gasoline storage tanks, gasoline dispensing equipment, oil tanks, and paint booths among other things. Our business involves the use, handling, and disposal of hazardous materials and wastes, including motor oil, gasoline, solvents, lubricants, paints, and other substances. We manage our compliance through permitting and operational control.

Facilities and Personnel. Our facilities and business operations are subject to laws and regulations relating to environmental protection and health and safety, and our employment practices are subject to various laws and regulations, including complex federal, state, and local wage and hour and anti-discrimination laws. We may also be liable for employee misconduct and violations of laws or regulations to which we are subject.

Federal Advertising Regulations. The Federal Trade Commission ("FTC") has authority to take actions to remedy or prevent advertising practices that it considers to be unfair or deceptive and that affect commerce in the United States. If the FTC takes the position in the future that any aspect of our business constitutes an unfair or deceptive advertising practice, responding to such allegations could require us to pay significant damages, settlements, and civil penalties, or could require us to make adjustments to our products and services, any or all of which could result in substantial adverse publicity, loss of participating dealers, lost revenue, increased expenses, and decreased profitability.

Federal Antitrust Laws. The antitrust laws prohibit, among other things, any joint conduct among competitors that would lessen competition in the marketplace. Some of the information that we may obtain from dealers may be sensitive and, if

disclosed inappropriately, could impede competition or otherwise diminish independent pricing activity. A governmental or private civil action alleging the improper exchange of information, or unlawful participation in price maintenance or other unlawful or anticompetitive activity, even if unfounded, could be costly to defend and adversely impact our ability to maintain and grow our business.

In addition, governmental or private civil actions related to the antitrust laws could result in orders suspending or terminating our ability to do business or otherwise altering or limiting certain of our business practices, including the manner in which we handle or disclose pricing information, or the imposition of significant civil or criminal penalties, including fines or the award of significant damages against us in class action or other civil litigation.

Other. In addition to these laws and regulations that apply specifically to our business, we are also subject to laws and regulations affecting public companies, including securities laws and the listing rules of The Nasdaq Stock Market ("Nasdaq"). The violation of any of these laws or regulations could result in administrative, civil, or criminal penalties or in a cease-and-desist order against our business operations, any of which could damage our reputation and have a material adverse effect on our business, sales and results of operations. We have incurred and will continue to incur capital and operating expenses and other costs to comply with these laws and regulations.

The foregoing description of laws and regulations to which we are or may be subject is not exhaustive, and the regulatory framework governing our operations is subject to continuous change. The enactment of new laws and regulations or the interpretation of existing laws and regulations in an unfavorable way may affect the operation of our business, directly or indirectly, which could result in substantial regulatory compliance costs, civil or criminal penalties, including fines, adverse publicity, loss of participating dealers, lost revenue, increased expenses, and decreased profitability. Further, investigations by government agencies, including the FTC, into allegedly anticompetitive, unfair, deceptive or other business practices by us, could cause us to incur additional expenses and, if adversely concluded, could result in substantial civil or criminal penalties and significant legal liability.

Employees

As of December 31, 2022, we had approximately 2,717 full time and 84 part-time employees.

Available Information

Our Internet website is www.rumbleon.com. Our Annual Report on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K, and amendments to reports filed or furnished pursuant to Sections 13(a) and 15(d) of the Securities and Exchange Act of 1934, as amended (the "Exchange Act"), are available, free of charge, under the Investor Relations tab of our website as soon as reasonably practicable after we electronically file such material with, or furnish it to, the SEC. Additionally, the SEC maintains a website located at www.sec.gov that contains the information we file or furnish electronically with the SEC.

ITEM 1A. RISK FACTORS.

Described below are certain risks to our business and the industry in which we operate. You should carefully consider the risks described below, together with the financial and other information contained in this 2022 Form 10-K and in our other public disclosures. If any of the following risks occurs, our business, financial condition, results of operations, cash flows, or prospects could be materially and adversely affected. As a result, our future results could differ materially from historical results and from guidance we may provide regarding our expectations for future financial performance and the trading price of our Class B common stock could decline.

Risks Relating to Our Business

We have identified a material weakness in our internal control over financial reporting. If we are unable to effectively remediate this material weakness and maintain an effective system of internal control over financial reporting, we may not be able to accurately report our financial results or prevent fraud. As a result, investors could lose confidence in our financial and other public reporting, which would harm our business.

We are required to comply with Section 404 of the Sarbanes-Oxley Act (“SOX”). Section 404 of SOX requires public companies to maintain effective internal control over financial reporting (“ICOFR”). In particular, we must perform system and process evaluation and testing of our ICOFR allowing management to report on the effectiveness of our ICOFR. In addition, we are required to have our independent registered public accounting firm attest to the effectiveness of our ICOFR. The standard of effectiveness for ICOFR is that we have controls and procedures in place that provide “reasonable assurance that we can produce accurate financial statements on a timely basis.” This process of implementation, evaluation, and attestation is costly and time-consuming. We have hired and may need to continue to employ both internal and external resources with appropriate public company experience and technical accounting knowledge to maintain and evaluate our ICOFR.

In our Annual Report on Form 10-K for the year ended December 31, 2021 (the “2021 Form 10-K”), we identified material weaknesses in our ICOFR relating to our legacy RumbleOn operations. As discussed in this 2022 Form 10-K, we have remediated and subsequently tested the impacted controls and have determined that the material weaknesses identified in the 2021 Form 10-K have been remediated as of December 31, 2022. In addition, as discussed in this 2022 Form 10-K, we identified a material weakness in our ICOFR for the year ended December 31, 2022 relating to our control environment following the integration of the RideNow business and incorporation of the acquired business into the Company’s control environment. If we are unable to effectively remediate this material weakness and maintain effective internal control over financial reporting, we may fail to prevent or detect material misstatements in our financial statements, in which case investors may lose confidence in the accuracy and completeness of our financial statements.

We have incurred significant indebtedness, which could adversely affect us, including our business flexibility, and will increase our interest expense.

In connection with the RideNow Transaction and Freedom Transaction, we substantially increased indebtedness which has had and will continue to have the effect, among other things, of reducing our flexibility to respond to changing business and economic conditions and substantially increasing our interest expense. The increased levels of indebtedness, including the applicable interest payments, could also reduce funds available for working capital, capital expenditures, and other general corporate purposes, and may create competitive disadvantages for us relative to competitors with lower debt levels. If our financial performance does not meet our current expectations, then our ability to service the indebtedness may be adversely impacted.

We are subject to interest rate risk in connection with our floorplan payables, revolving credit facility, and our other debt instruments that could have a material adverse effect on our profitability.

Our floorplan payables, revolving credit facility, and other debt instruments are subject to variable interest rates. Accordingly, our interest expense will fluctuate with changing market conditions and will increase if interest rates rise. Instability or disruptions of the capital markets, including credit markets, or the deterioration of our financial condition due to internal or external factors, could restrict or prohibit our access to capital markets and increase our financing costs. In addition, our net new inventory carrying cost (new vehicle floorplan interest expense net of floorplan assistance that we receive from powersports manufacturers) may increase due to changes in interest rates, inventory levels, and manufacturer assistance. We cannot assure you that a significant increase in interest rates or decrease in manufacturer floorplan assistance would not have a material adverse effect on our business, financial condition, results of operations, or cash flows.

The powersports industry is sensitive to unfavorable changes in general economic conditions and various other factors that could affect demand for our products and services, which could have a material adverse effect on our business, our ability to implement our strategy and our results of operations.

Our future performance will be impacted by general economic conditions including among other things: changes in employment levels; consumer demand, preferences and confidence levels; the availability and cost of credit; fuel prices; levels of discretionary personal income; inflation; and interest rates. Recently, inflation has increased throughout the U.S. economy. Inflation can adversely affect us by increasing the costs of labor, fuel and other costs as well as by reducing demand for powersports vehicles. In addition, rapid changes in fuel prices can cause shifts in consumer preferences which are difficult to accommodate given the long lead-time of inventory acquisition. Inflation is also often accompanied by higher interest rates, which could reduce the fair value of our outstanding debt obligations. Changes in interest rates can also significantly impact new and used vehicle sales and vehicle affordability due to the direct relationship between interest rates and monthly loan payments, a critical factor for many powersports buyers, and the impact interest rates have on customers’ borrowing capacity and disposable income. We have experienced, and continue to experience, increases in the prices of labor, fuel, and other costs of providing service.

Powersports consumers may not accept our transformative business model.

As described throughout this 2022 Form 10-K, we are transforming the traditional powersports customer experience and building the first and only true Omnichannel experience in the industry. Also, in building this Omnichannel experience, we expect to incur significant expenses and face various other challenges, such as expanding our customer experience team and building out a fulfillment and logistics network. If customers do not accept our products, services, and offerings we may not benefit from the investments needed to build this transformative customer experience to the extent anticipated or at all. Any of these risks, if realized, could materially and adversely affect our business, financial condition, and results of operations.

We may not be able to acquire the number of vehicles to satisfy consumer demand or our expectations for the business.

A material part of our plan is predicated on being able to have sufficient inventory, both new and used, to satisfy customer demand or meet our financial objectives. New inventory is ultimately controlled by our OEMs and their willingness to allocate inventory to us and their ability to manufacture and distribute a sufficient number of vehicles given the ongoing environment of manufacturing slowdowns, computer chip shortages, and logistic/transportation challenges (collectively, the “Demand/Supply Imbalances”). Used inventory is acquired directly from consumers via our online Cash Offer Tool or consumer trade-in transactions. If the channels for new or used vehicle acquisition were disrupted, for example as a result of another COVID-like lockdown, technology challenges, non-acceptance of online transactions, poor customer ratings, or other such events, the Company may not have enough inventory to meet customer demand, which may adversely affect our business, financial condition, and results of operations.

We may require additional financing or capital to pursue our growth challenges or unforeseen circumstances. If financing or capital is not available on terms acceptable to us or at all, we may not be able to develop and grow our business as anticipated and our business, operating results, and financial condition may be harmed.

We intend to continue making investments to support the development and growth of our business. Additional financing or capital may not be available when we need it, on terms that are acceptable to us, or at all.

Although we intend to self-fund our growth initiatives, if we determine to raise additional capital through issuances of equity or debt, our existing stockholders could suffer significant dilution, and any new equity securities we issue could have rights, preferences, and privileges superior to those of holders of our common stock. If we are unable to obtain adequate financing or financing on terms satisfactory to us, when we require it, could adversely impact our ability to continue to pursue our business objectives and to respond to business opportunities, challenges, or unforeseen circumstances could be significantly limited, and our business, operating results, financial condition, and prospects could be adversely affected.

Investments made in the development, growth, and expansion of our business may not yield our expected results and may not result in successful growth of our business.

We expect to make significant investments in the further development and expansion of our business and these investments may not result in the development, growth, or expansion of our business on a timely basis or at all. We may not generate sufficient revenue and we may incur significant losses in the future for several reasons, including a lack of demand for our products and services, increasing competition, and weakness in the powersports industry generally. We may encounter

unforeseen expenses, difficulties, complications, and delays, relating to the development and operation of our business, as well as our organic and acquisition growth strategies. Accordingly, we may not be able to successfully develop, grow, and expand our business, generate revenue, or achieve and maintain profitability.

We have and may continue to acquire strategic retail locations and other complementary businesses and technologies, which could divert management's attention, and otherwise disrupt our operations and impact our operating results.

Our success will depend, in part, on our ability to grow our business in response to the demands of consumers, other constituents within the powersports industry, and competitive pressures. In the past, we have met these demands in part by acquiring complementary businesses and technologies.

The identification of suitable acquisition candidates can be difficult; time-consuming, and costly, and we may not be able to successfully complete identified acquisition opportunities. The risks we face in connection with our acquisition strategy include:

•diversion of management time and focus from operating our business to addressing acquisition integration challenges;

•integration of the acquired company's accounting, management information, human resources, and other administrative systems;

•coordination of technology, research and development, and sales and marketing functions;

•retention of employees from the acquired company;

•cultural challenges associated with integrating employees from the acquired company into our organization;

•the need to implement or improve controls, procedures, and policies at a business that before the acquisition may have lacked effective controls, procedures, and policies;

•potential write-offs of intangibles or other assets acquired in such transactions that may have an adverse effect on our operating results in a given period; and

•liability for activities of the acquired company before the acquisition.

Our failure to address these risks or other matters encountered in connection with future acquisitions and investments could cause us to fail to realize the anticipated benefits of these acquisitions or investments, cause us to incur unanticipated liabilities, and harm our business generally. As discussed in the preceding risk factors elsewhere in this 2022 Form 10-K, we currently intend to self-fund our growth initiatives, and acquisition growth. Nevertheless, some future acquisitions could result in dilutive issuances of our equity securities, the incurrence of debt, contingent liabilities, amortization expenses, or the impairment of goodwill, any of which could harm our financial condition.

We may experience difficulties integrating acquired businesses.

Achieving the anticipated benefits of our acquisitions will depend in significant part upon our integrating any acquired entity's businesses, operations, processes, and systems in an efficient and effective manner. We may not be able to accomplish the integration process smoothly, successfully, or on a timely basis, which may result in unforeseen expenses or the failure to recognize the anticipated benefits of acquired businesses. The necessity of coordinating geographically separated organizations, systems of controls, and facilities, in addition to addressing possible differences in business backgrounds, corporate cultures, and management philosophies may increase the difficulties of integration. Companies operate numerous systems and controls, including those involving management information, accounting and finance, legal and regulatory compliance, inventory intake and control, sales, billing, employee benefits, and payroll. The integration of an acquired company's operations requires the dedication of significant internal and external resources, which may divert management’s attention from the day-to-day business of the company and be costly. Employee uncertainty and lack of focus during the integration process may also disrupt the business of the Company. Any inability of management to successfully and timely integrate an acquired company could have a material adverse effect on the business and results of operations of the Company and result in not achieving the anticipated benefits of the acquisition.

To the extent we acquire additional businesses, we may incur substantial costs.

We have incurred, and expect to continue to incur, a number of non-recurring costs associated with our acquisitions. The substantial majority of these non-recurring costs will consist of transaction and regulatory costs related to acquisitions. We will also incur transaction fees and costs related to formulating and implementing integration plans, including system consolidation costs and employment-related costs. We continue to assess the magnitude of these costs, and additional unanticipated costs may be incurred from the acquisitions and integration. Although we anticipate that the elimination of duplicative costs and the realization of other efficiencies and synergies related to the integration should allow us to offset integration-related costs over time, this net benefit may not be achieved in the near term, or at all.

We depend on key personnel to operate our business, and if we are unable to retain, attract, and integrate qualified personnel, our ability to develop and successfully grow our business could be harmed.

We believe our success will depend on the efforts and talents of our executives and employees, including Marshall Chesrown, our Chairman and Chief Executive Officer. In addition, the loss of any senior management, regional operations directors, or other key employees could materially adversely affect our ability to execute our business plan and strategy, and we may not be able to find adequate replacements on a timely basis, or at all. Our future success depends on our continuing ability to attract, develop, motivate, and retain highly qualified and skilled employees. Qualified individuals are in high demand, and we may incur significant costs to attract and retain them. We cannot ensure that we will be able to retain the services of any members of our senior management or other key employees. If we fail in attracting well-qualified employees or retaining and motivating existing employees, our business could be materially and adversely affected.

Our annual and quarterly operating results may fluctuate significantly or may fall below the expectations of investors or securities analysts, each of which may cause our stock price to fluctuate or decline.

We expect our operating results to be subject to annual and quarterly fluctuations and these results will be affected by numerous factors, including:

•a change in consumer discretionary spending and other macroeconomic conditions;

•a shift in the mix and type of vehicles we sell, which could result in lower sales price and lower gross profit;

•the timing and cost of development and operating activities relating to our business, which may change from time to time;

•expenditures that we may incur to advance our growth strategies; and

•future accounting pronouncements or changes in our accounting policies.

If our annual or quarterly operating results fall below the expectations of investors or securities analysts, the price per share of our Class B common stock could fluctuate or decline substantially. We believe that annual and quarterly comparisons of our financial results are not necessarily meaningful and should not be relied upon as an indication of our future performance.

The failure to develop and maintain our brands could harm our reputation among current customers or adversely impact our ability to attract new customers.

Developing and maintaining the RideNow and RumbleOn brands will depend largely on the success of our efforts to maintain the trust of and deliver value to our users. If our current and potential users perceive that we are not focused on providing them with a better pre-owned powersports experience, our reputation and the strength of our brand will be adversely affected.

Consumers are increasingly shopping for new and used vehicles, vehicle repair and maintenance services, and other vehicle products and services online and through mobile applications, including through third-party online and mobile sales platforms, with which we compete. If we fail to preserve the value of our retail brands, maintain our reputation, or attract consumers to our Omnichannel offering, our business could be adversely impacted.

Complaints or negative publicity about our business practices, our marketing and advertising campaigns, our compliance with applicable laws and regulations, data privacy and security issues, and other aspects of our business, irrespective of their validity, could diminish users' confidence in and the use of our products and services and adversely affect our brands. There can be no assurance that we will be able to develop, maintain, or enhance our brands, and failure to do so would harm our business growth prospects and operating results.

The success of our business relies heavily on our marketing and branding efforts, especially with respect to our RideNow brand at retail locations, the RideNow and RumbleOn websites, and our branded mobile applications, and these efforts may not be successful.

We believe that an important component of our development and growth will be the business derived from the RideNow retail brand and the RumbleOn website and branded mobile applications. Because RideNow and RumbleOn are consumer brands, we rely heavily on marketing and advertising to increase the visibility of this brand with potential users of our products and services.