UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

| FORM | |||||

| ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | ||||||||

For the fiscal year ended June 30, 2023

or

| TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | ||||||||

For the transition period from to

Commission File Number: 001-36587

| (Exact name of registrant as specified in its charter) | ||||||||

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |||||||

| (Address of principal executive offices) | (Zip Code) | |||||||

Registrant’s telephone number, including area code: (732) 537-6200

____________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||||||

Securities registered pursuant to Section 12(g) of the Act: None

____________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No ☒

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes o No ☒

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

ý | Accelerated filer | ¨ | |||||||||||||||

| Non-accelerated filer | ¨ | Smaller reporting company | |||||||||||||||

| Emerging growth company | |||||||||||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. o

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☒

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. o

1

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to § 240.10D-1(b). o

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). o Yes ☒ No

As of December 31, 2022, the aggregate market value of the registrant’s voting and non-voting common equity held by non-affiliates was $7.90 billion. On November 30, 2023, there were 180,641,272 shares of the Registrant’s Common Stock, par value $0.01 per share, issued and outstanding.

CATALENT, INC.

INDEX TO ANNUAL REPORT ON FORM 10-K

For the Fiscal Year Ended June 30, 2023

| Item | Page | |||||||

| PART I | ||||||||

| Item 1. | ||||||||

| Item 1A. | ||||||||

| Item 1B. | ||||||||

| Item 2. | ||||||||

| Item 3. | ||||||||

| Item 4. | ||||||||

| PART II | ||||||||

| Item 5. | ||||||||

| Item 6. | ||||||||

| Item 7. | ||||||||

| Item 7A. | ||||||||

| Item 8. | ||||||||

| Item 9. | ||||||||

| Item 9A. | ||||||||

| Item 9B. | ||||||||

| Item 9C. | ||||||||

| PART III | ||||||||

| Item 10. | ||||||||

| Item 11. | ||||||||

| Item 12. | ||||||||

| Item 13. | ||||||||

| Item 14. | ||||||||

| PART IV | ||||||||

| Item 15. | ||||||||

| Item 16. | ||||||||

2

3

PART I

Special Note Regarding Forward-Looking Statements

In addition to historical information, this Annual Report on Form 10-K for the fiscal year ended June 30, 2023 (this “Annual Report”) of Catalent, Inc. (“Catalent” or the “Company”) contains “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933, as amended (the “Securities Act”), and Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”), which are subject to the “safe harbor” created by those sections. All statements, other than statements of historical facts, included in this Annual Report are forward-looking statements. In some cases, you can identify these forward-looking statements by the use of words such as “outlook,” “believes,” “expects,” “potential,” “continues,” “may,” “will,” “should,” “could,” “seeks,” “predicts,” “intends,” “plans,” “estimates,” “anticipates,” “future,” “forward,” “sustain,” or the negative version of these words or other comparable words.

These statements are based on assumptions and assessments made by our management in light of their experience and their perception of historical trends, current conditions, expected future developments, and other factors they believe to be appropriate. Any forward-looking statement is subject to various risks and uncertainties. Accordingly, there are or will be important factors that could cause actual outcomes or results to differ materially from those indicated in these statements.

Some of the factors that may cause actual results, developments, and business decisions to differ materially from those contemplated by such forward-looking statements include, but are not limited to, those described under the section entitled “Risk Factors” in this Annual Report, which are summarized below:

Summary of Principal Risk Factors

Any investment, including an investment in our common stock, par value $0.01 (the “Common Stock”), involves risk. The following summary highlights certain risks that an investor in our Common Stock should consider. The following should be read in conjunction with the fuller discussion of risk factors we face set forth in “Item 1A. - Risk Factors.”

Risks Relating to Our Business and the Industry in Which We Operate

•Actions of activist shareholders could impact the pursuit of our business strategies and adversely affect our results of operations, financial condition, or share price.

•We anticipate being subject to increasing focus by our investors, regulators, customers, and other stakeholders on environmental, social, and governance (“ESG”) matters.

•We are a part of the highly regulated healthcare industry, subject to stringent regulatory standards and other applicable laws and regulations, which can change unexpectedly or be the subject of unexpected changes in interpretation or enforcement, any of which may adversely impact our business.

•Any failure to implement fully, monitor, and continuously improve our quality management strategy could lead to quality or safety issues and expose us to significant costs, potential liability, and adverse publicity.

•We have experienced, and may continue to experience, productivity issues and higher-than-expected costs at certain of our facilities, which have resulted in, and may continue to result in, material and adverse impacts on our financial condition and results of operations.

•The declining demand for various COVID-19 vaccines and treatments from both patients and governments around the world has affected and may continue to affect sales of the COVID-19 products we manufacture and our financial condition.

•The demand for our offerings depends in part on our customers’ research and development and the clinical and market success of their products.

•Our results of operations are subject to fluctuations in the costs, availability, and suitability of the components of the products we manufacture, including active pharmaceutical ingredients, excipients, purchased components, and raw materials, and other supplies or equipment we need to run our business.

•Our goodwill has been subject to impairment and may be subject to further impairment in the future, which could have a material adverse effect on our results of operations, financial condition, or future operating results.

•Our ability to use our net operating loss carryforwards and certain other tax attributes may be limited.

•We may acquire businesses and offerings that complement or expand our business or divest non-strategic businesses or assets. We may not be able to complete desired transactions, and such transactions, if executed, pose significant risks, including risks relating to our ability to successfully and efficiently integrate acquisitions or

4

execute on dispositions and realize anticipated benefits therefrom. The failure to execute or realize the full benefits from any such transaction could have a negative effect on our operations and profitability.

•We may become subject to litigation, other proceedings, and government investigations relating to us or our operations, and the ultimate outcome of any such matter may have an impact on our business, prospects, financial condition, and results of operations.

•Our global operations are subject to economic and political risks, including risks resulting from continuing inflation, disruptions to global supply chains, destabilization of a regional or national banking system, or from the Ukrainian-Russian war or the effect of the evolving nature of the recent war in Gaza between Israel and Hamas, which could affect the profitability of our operations or require costly changes to our procedures

•We use advanced information and communication systems to run our operations, compile and analyze financial and operational data, and communicate among our employees, customers, and counterparties, and the risks generally associated with information and communications systems could adversely affect our results of operations. We continuously work to install new, and upgrade existing, systems and provide employee awareness training around phishing, malware, and other cybersecurity risks to enhance the protections available to us, but such protections may be inadequate to address malicious attacks or inadvertent compromises affecting data security or the operability of such systems.

•Artificial intelligence-based platforms present new risks and challenges to our business.

•Our cash, cash equivalents, and financial investments could be adversely affected if the financial institutions in which we hold our cash, cash equivalents, and financial investments fail.

Risks Relating to Our Indebtedness

•The size of our indebtedness and the obligations associated with it could adversely affect our ability to raise additional capital to fund our operations, limit our ability to react to changes in the economy or in our industry or to deploy capital to grow our business, expose us to interest-rate risk to the extent of our variable-rate debt, or prevent us from meeting our obligations under our indebtedness. These risks may be increased in a recessionary environment, particularly as sources of capital may become less available or more expensive.

•Despite our high indebtedness level, we and our subsidiaries are still capable of incurring significant additional debt, which could further exacerbate the risks associated with our substantial indebtedness.

•Our interest expense on our variable-rate debt may continue to increase if and to the extent that policymakers combat inflation through interest-rate increases on benchmark financial products.

•Despite the limitations in our debt agreements, we retain the ability to take certain actions that may interfere with our ability to timely pay our substantial indebtedness.

•We may not be able to pay our indebtedness when it becomes due.

•We are currently using and may in the future use derivative financial instruments to reduce our exposure to market risks from changes in interest rates on our variable-rate indebtedness or changes in currency exchange rates, and any such instrument may expose us to risks related to counterparty credit worthiness or non-performance of these instruments.

Risks Relating to Ownership of Our Common Stock

•We do not presently maintain effective disclosure controls and procedures due to material weaknesses we have identified in our internal control over financial reporting. Failure to remediate these material weaknesses or any other material weakness or significant deficiencies have resulted in a revision of our financial statements, in the future could result in material misstatements in our financial statements and have caused, and in the future could cause us to fail to timely meet our periodic reporting obligations.

•Our stock price has historically been and may continue to be volatile, and a holder of shares of our Common Stock may not be able to resell such shares at or above the price such stockholder paid, or at all, and could lose all or part of such investment as a result.

•Future sales, or the perception of future sales, of our Common Stock, by us or our existing stockholders could cause the market price for our Common Stock to decline.

•We are no longer eligible to use the Form S-3 registration statement, which could impair our capital-raising activities.

•Provisions in our organizational documents could delay or prevent a change of control.

5

We caution you that the risks, uncertainties, and other factors referenced above may not contain all of the risks, uncertainties, and other factors that are important to you. In addition, we cannot assure you that we will realize the results, benefits, or developments that we expect or anticipate or, even if substantially realized, that they will result in the consequences or affect us or our business in the way expected. There can be no assurance that (i) we have correctly measured or identified all of the factors affecting our business or the extent of these factors’ likely impact, (ii) the available information with respect to these factors on which such analysis is based is complete or accurate, (iii) such analysis is correct, or (iv) our strategy, which is based in part on this analysis, will be successful. All forward-looking statements in this report apply only as of the date of this report or as of the date they were made, and we undertake no obligation to publicly update or review any forward-looking statement, whether as a result of new information, future developments, or otherwise, except as required by law.

We file annual, quarterly, and current reports and other information with and furnish additional information to the U.S. Securities and Exchange Commission (the “SEC”). Our filings with the SEC are available to the public on the SEC’s website at www.sec.gov. Those filings are also available to the public on, or accessible through, our website (catalent.com) for free via the “Investors” section as soon as reasonably practicable after we file such material, or furnish it to, the SEC. We also use our website, Facebook page (facebook.com/CatalentPharmaSolutions), LinkedIn page (linkedin.com/company/catalent-pharma-solutions/) and Twitter account (@catalentpharma) as channels of distribution of information concerning our activities, our offerings, our various businesses, and other related matters. The information we post through these channels may be deemed material. Accordingly, investors should monitor these channels, in addition to following our press releases, SEC filings, and public conference calls and webcasts. The information we file with or furnish to the SEC (other than the information set forth or incorporated in this Annual Report) or contained on or accessible through our website, our social media channels, or any other website that we may maintain is not a part of this Annual Report.

Catalent References and Fiscal Year

Unless the context otherwise requires, in this Annual Report, the terms “Catalent,” “the company,” “we,” “us,” and “our” refer to Catalent, Inc. and its subsidiaries. All references to years in this Annual Report, unless otherwise stated, refer to fiscal years beginning July 1 and ending June 30. All references to quarters, unless otherwise stated, refer to fiscal quarters. Fiscal years are referred to by the calendar year in which they end. For example, “fiscal 2023” refers to the fiscal year ending June 30, 2023.

Trademarks and Service Marks

We have U.S. or foreign registrations for the following marks, among others: Bettera®, Catalent®, Clinicopia®, CosmoPod®, Easyburst®, FastChain®, FlexDirect®, Follow the Molecule®, Galacorin®, GPEx®, GPEx® Boost, GPEx® Lightning, Graphicaps®, Liqui-Gels®, Manufacturing Miracles®, Micron Technologies®, OmegaZero®, OneBio®, OneXpress Solution®, OptiDose®, OptiForm®, OptiGel®, OptiGel® Bio, OptiGel® DR, OptiMelt®, OptiShell®, PEEL-ID®, Pharmatek®, RP Scherer®, Savorgel®, Scherer®, SMARTag®, Softdrop®, Staby®, StabyExpress®, SupplyFlex®, Vegicaps®, Zydis®, and Zydis Ultra®. This Annual Report also includes trademarks and trade names owned by other parties, and these trademarks and trade names are the property of their respective owners. We use certain other trademarks and service marks, some on an unregistered basis and some have been applied for, but remain pending examination in trademark agencies in the U.S. and abroad, including, FlexDoseSM, Catalent Xpress PharmaceuticsSM, OptiPact™, ProteoSuiteSM, StartScoreSM, and VirtuosoSM.

Solely for convenience, the trademarks, service marks, and trade names identified in this Annual Report may appear without the ®, SM, and ™ symbols, but such references are not intended to indicate, in any way, that we will not assert, to the fullest extent under applicable law, our rights or the rights of the applicable licensors to these trademarks, service marks, and trade names.

6

ITEM 1. BUSINESS

Overview

We provide differentiated development and manufacturing solutions for drugs, protein-based biologics, cell and gene therapies, vaccines, and consumer health products at over fifty facilities across four continents under rigorous quality and operational standards. Our oral, injectable, and respiratory delivery technologies, along with our state-of-the-art protein, plasmid, viral, and cell and gene therapy manufacturing capacity, address a wide and growing range of modalities and therapeutic and other categories across the biopharmaceutical, pharmaceutical, and consumer health industries. Through our extensive capabilities, growth-enabling capacity, and deep expertise in product development, regulatory compliance, and clinical trial and commercial supply, we can help our customers take products to market faster, including more than half of new drug products approved by the U.S. Food and Drug Administration (the “FDA”) in the last decade. Our development and manufacturing platforms, our proven formulation, supply, and regulatory expertise, and our broad and deep development and manufacturing know-how enable our customers to advance and then bring to market more products and better treatments for patients and consumers. Our commitment to reliably supply our customers’ and their patients’ needs is the foundation for the value we provide; annually, we produce approximately 70 billion unit doses for nearly 8,000 customer prescription and consumer health products, or approximately 1 in every 26 unit doses of such products taken each year by patients and consumers around the world. We believe that, through our investments in state-of-the-art facilities and capacity expansion, including investments in facilities focused on new treatment modalities and other attractive market segments, our continuous improvement activities devoted to operational and quality excellence, the sales of existing and introduction of new customer products, and, in some cases, our innovation activities and patents, we will continue to attract premium opportunities and realize the growth potential from these areas.

We continue to focus on enhancing both our product and service offerings and our sales and marketing activities in order to grow the number of active commercial manufacturing and development programs for our customers. This sustains our extensive, long-duration relationships and long-term contracts with a broad and diverse range of industry-leading customers. In fiscal 2023, we conducted business with 87 of the top 100 branded drug and consumer health marketers and 82 of the top 100 biologics marketers, measured on a global basis. Selected key customers include Bayer, Bristol-Myers Squibb, GlaxoSmithKline, Haleon, Johnson & Johnson, Moderna, Pfizer, and Sarepta Therapeutics.

We have many long-standing relationships with our customers, particularly those with commercial products, as we provide support and reliable supply through each stage of a product's lifecycle. Our relationship with an innovator of a prescription pharmaceutical product will often last many years—in several cases, two decades or more—extending from pre-clinical development through more mature commercial stages of the product's life cycle. We serve customers requiring some combination of innovative product development, superior quality, state-of-the-art manufacturing, and skilled technical services to support their development and marketed product needs. Our broad and diverse range of technologies closely integrates with all aspects of our customers’ final formulations and dose forms, and this generally results in the inclusion of our facilities as manufacturing and testing sites in our customers’ prescription product regulatory filings. Both factors frequently translate to long-duration supply relationships at an individual product level.

We believe our customers value us because our depth of development solutions and state-of-the-art manufacturing technologies, continuous innovations and improvements, consistent and reliable supply, geographic reach, and substantial expertise enable us to create a broad range of business and product solutions that can be customized to fit their individual needs. Today we employ more than 9,000 highly trained direct manufacturing associates, as well as more than 3,000 formulation, analytical development, and process scientists and technicians. Our customers can also benefit from more than 1,800 patents and patent applications in advanced delivery platforms, drug and biologics formulation, and manufacturing. The aim of our offerings is to reliably supply our customers' commercial needs and also allow them to bring more products to market faster and develop and market differentiated products that improve patient outcomes. We believe our leading market position and diversity of customers, offerings, regulatory categories, products, and geographies reduce our exposure to potential strategic and product shifts within our industries.

We provide a wide variety of proprietary and non-proprietary, differentiated technologies, products, and service offerings to our customers across our development and manufacturing platforms, which we have advanced and grown over more than 90 years through internal development, strategic alliances, in-licensing, and acquisitions. We initially introduced our softgel capsule technologies in the 1930s and have continuously expanded our range of offerings. In recent years, we have launched more than a dozen internally developed new technology platform offerings. We have also augmented our portfolio through acquisitions. Among the technologies we currently offer are softgel capsules, including both gelatin and non-gelatin formulations, our Zydis orally disintegrating tablets, gummy and soft chew oral forms, protein production using advanced mammalian cell lines, adeno-associated virus (“AAV”) and other viral vectors, induced pluripotent stem cells (“iPSCs”) and

7

other cell types, plasmid DNA (“pDNA”), and a range of other oral, injectable, and respiratory delivery technologies. The technologies and service offerings within our development solution platforms span the full drug development process, ranging from our OptiForm Solution Suite for enhancement of bioavailability and other characteristics of early-stage small molecules, Gene Product Expression (“GPEx”), GPEx Boost, and GPEx Lightning for advanced cell line development, pDNA development and manufacturing and SMARTag platforms for development of biologics and antibody-drug conjugates (“ADCs”), to formulation, analytical, and bioanalytical services, early-stage clinical development, drug-device combination development and supply, fill and finish operations for injectable products, and clinical trials supply, including our unique FlexDirect direct-to-patient and FastChain demand-led clinical supply solutions. Our offerings serve a critical need in the development and manufacture of products across a broad range of product types. We focus on serving as an accelerator for new therapeutic modalities and formulation, delivery, and manufacturing technologies. Our expertise enables us to bring advanced products to market at scale, faster.

In large part due to acquisitions and investments, their subsequent organic growth, the revenue contribution from our Biologics segment has grown from approximately 17% in fiscal 2016 to 46% in fiscal 2023. We believe our own internal innovation and investments, supplemented by current and future external partnerships and acquisitions, will continue to extend our leadership positions in the development, reliable supply, and delivery of drugs, protein-based biologics, cell and gene therapies, and consumer health products.

History

We trace our history to the 1933 founding of the R.P. Scherer Corporation, which developed the first rotary die machine for the manufacture of soft gelatin capsules, and we assumed our current form in April 2007. We regularly review our portfolio of offerings and operations in the context of our strategic growth plan, and, where appropriate, have added to or divested from our portfolio of offering and sites, which has led to significant growth of the overall business. In July 2014, we completed the initial public offering of our Common Stock, which is listed on the New York Stock Exchange (the “NYSE”) under the symbol “CTLT.”

We are a holding company that indirectly owns Catalent Pharma Solutions, Inc. (“Operating Company”), which owns, directly or indirectly, all of our operating assets.

Our Competitive Strengths

Available, State-of-the-art Manufacturing Capacity in Attractive Market Segments

We have invested several billion dollars over the last few years to broaden our portfolio of offerings and expand our capacity with state-of-the-art manufacturing and development capabilities that focus on anticipating and meeting the needs of the evolving biopharmaceutical, pharmaceutical, and consumer health industries. In addition, we have hired and trained thousands of new direct manufacturing associates in our quality-focused culture of operational excellence. The capacity and capabilities we have built and purchased, along with our continuing efforts to assure operational and quality excellence, have and will continue to enable us to secure attractive new business opportunities in the expanding market for outsourced product development and supply.

Vibrant, Patient First-Driven Culture

From the manufacturing line to the executive suite, for all our critical decisions, we ask the question, “What would the impact be to the patient?”, and our culture is built on our cornerstone value of Patient First. We believe this mindset, which aligns closely with our customers’ values, enables a pervasive focus on patient safety, impact, and outcomes, and an uncompromising approach to product quality and compliance, by reminding us of those who depend upon our vigilance concerning the safety, quality, reliability, and sustainability of our product supply. Along with other key cultural strengths, including our commitments to diversity and inclusion and to science-based environmental sustainability, we believe our culture brings us both a unique reputation and an operating capability that is difficult to replicate.

Diversified Operating Platform

We are diversified by virtue of our broad range of product and service offerings, our geographic scope, our large customer portfolio, the extensive range of products we produce, and our ability to provide solutions at every stage of a product’s lifecycle. In fiscal 2023, we produced nearly 8,000 distinct products across multiple categories. Our fiscal 2023 net revenue was distributed by relevant product regulatory/marketing status as follows: biologics 51%, branded drugs 30%, generic prescription drugs 2%, over-the-counter drugs 7%, and consumer health and other 10% combined. In fiscal 2023, our top 20

8

products represented 37% of our total net revenue, with one customer accounting for approximately 10% of net revenue whose largest individual product accounted for approximately 9% of our net revenue. We serve more than 1,200 customers in more than 80 countries, with 35% of our fiscal 2023 net revenue coming from outside the U.S. This diversity, combined with long product lifecycles and close customer relationships, has contributed to the long-term stability of our business. It has also allowed us to reduce our exposure to the risks associated with potential strategic, customer, and product shifts as well as to payer-driven pricing pressures experienced by our drug and biologic customers.

Longstanding, Extensive Relationships with a Diverse Customer Portfolio

We have longstanding, extensive relationships with leading pharmaceutical, biotechnology, and consumer health customers. In fiscal 2023, we did business with 87 of the top 100 branded drug and consumer health marketers and 82 of the top 100 biologics marketers, measured on a global basis, as well as with more than 1,200 other customers, including emerging and specialty biotech and pharmaceutical companies, which are often more reliant on outside partners as a result of their more virtual business models. Regardless of size, our customers seek innovative product development, superior quality, advanced manufacturing, and skilled technical services to support their development and marketed product needs.

We believe our customers value us because our broad range of product and service offerings, recently expanded capacity in state-of-the-art manufacturing facilities, including facilities offering new treatment modalities, reliable supply, geographic reach, commitment to operational and quality excellence, and substantial expertise that enable us to create a broad range of tailored solutions, many of which are unavailable from other individual providers.

Deep, Broad, and Growing Advanced Technology Foundation

Our breadth of offerings employing advanced technologies and state-of-the-art manufacturing systems and long track record of innovation substantially differentiate us from other industry participants. Our leading softgel platforms, including Liqui-Gels, OptiShell, OptiGel DR, and Vegicaps capsules, our gummy and soft chew oral forms, and our modified release technologies, including the Zydis family of orally disintegrating tablets, our spray drying capabilities, and our OptiPact and OptiMelt technologies, provide formulation expertise to solve complex delivery challenges for our customers. We offer advanced technologies for delivery of small molecules and biologics via oral, respiratory, and injectable routes and also provide advanced biologics formulation options, including GPEx, GPEx Boost, and GPEx Lightning mammalian cell lines for protein production, SMARTag ADC technology, AAV vectors for cell and gene therapies, iPSC development and manufacturing, and pDNA development and manufacturing. We have a leadership position within respiratory delivery, including dry powder inhalers and intra-nasal forms. We have reinforced our leadership position in advanced technologies over the last three years, as we have launched more than a dozen new technology platforms and applications, and recently purchased or expanded our businesses developing and manufacturing consumer health products, protein-based biologics, fill and finish for injectable drugs and biologics, cell and gene therapies, and other new therapeutic modalities. Our culture of creativity, problem-solving, and innovation is grounded in our advanced technologies, the substantial expertise and experience of our scientists and engineers, and, in some cases, our patents and proprietary manufacturing processes. Our global product development and innovation teams drive a focused application of resources to opportunities for both new customer product introductions and platform technology development. As of June 30, 2023, we had more than 1,500 product development programs in active development across our businesses.

Long-Duration Relationships Provide Sustainability

Our broad and diverse range of technologies closely integrates with our customers’ molecules to yield safe and effective final formulations and dose forms, and this generally results in the inclusion of Catalent in our customers’ prescription product regulatory filings. Both factors translate to long-duration supply relationships at an individual product level, to which we apply our expertise in contracting to produce long-duration commercial supply agreements. These agreements typically have initial terms of two to seven years with regular renewals of one to three years (see “—Contractual Arrangements” for more detail). Approximately three-quarters of our fiscal 2023 net revenue from our product development and delivery offerings and related services were covered by such long-term contractual arrangements. We believe this base provides us with a sustainable competitive advantage.

Significant Recent Growth Investments

We have made over time, and expect to continue to make, significant investments in our manufacturing network, which is capable of serving customers and patients worldwide, and today employ approximately 8 million square feet of manufacturing, laboratory, and related space across four continents. We have deployed approximately $2.61 billion in the last five fiscal years in gross capital expenditures, not including approximately $3.58 billion spent acquiring new facilities and businesses. Growth-related investments in facilities, capacity, and capabilities across our businesses have positioned us for future growth in areas

9

aligned with anticipated future demand, including in pDNA, cell and gene therapies, fill and finish for injectable drugs and biologics, and other new therapeutic modalities. Through our continuing commitment to operational, quality, and regulatory excellence, we drive continuous improvements in safety, productivity, sustainability and reliable supply, which we believe further differentiates us. Our manufacturing network and capabilities allow us the flexibility to reliably supply the changing needs of our customers while consistently meeting their quality, delivery, sustainability, and regulatory compliance expectations.

High Standards of Regulatory Compliance and Operational and Quality Excellence

We operate our plants in accordance with current good manufacturing practices (“cGMP”) or other applicable requirements, following our own high standards that are consistent with those of many of our large global pharmaceutical and biotechnology customers. We have approximately 1,900 employees around the globe focused on quality and regulatory compliance. All of our facilities are registered where required with the FDA or other applicable regulatory agencies, such as the European Medicines Agency (the “EMA”). In many cases, our facilities are registered with multiple food, drug, or biologics regulatory agencies around the world. In fiscal 2023, we were subject to 58 regulatory audits, and, over the last five fiscal years, we successfully completed approximately 300 regulatory audits. We also undergo more than 700 customer and internal audits annually. We believe our quality and regulatory track record to be a favorable competitive differentiator.

Strong and Experienced Management Team

Our executive leadership team collectively has approximately 550 years of combined and diverse experience within the pharmaceutical and healthcare industries. With an average of approximately 28 years of functional experience, this team possesses deep knowledge and a wide network of industry relationships.

Our Strategy

Our strategic ambition, guided by and operationalized through our values, is to power the innovation and growth of the life science industry by becoming its leading development and commercial partner in reliable supply, conventional and advanced technologies, first-to-scale innovation, and therapeutic modalities, and integrated solutions. To achieve this, we continue to pursue the following key growth initiatives:

Capabilities & Capacity — Continued Expansion in Biologics and Other Attractive Markets

Recognizing the strategic importance of protein-based biologics, cell and gene therapies, pDNA, and other new biopharmaceutical modalities, we began to build a differentiated biologics platform in 2002. Since 2019, we have invested over $3.42 billion in our biologics business, including capital investments and approximately $1.83 billion for acquisitions of biologics-focused businesses and sites. Today, we are a recognized leader in biologics, including AAV vectors for gene therapies; development and supply for cell therapies; advanced cell-line development; formulation and fill-finish into vials, pre-filled syringes, and cartridges; specialized manufacturing of biologic drug substances; and bioanalytical analysis. We have partnered with customers from around the world to develop advanced cell expression for more than 1,100 cell lines, many using our advanced GPEx, GPEx Boost, and GPEx Lightning technologies, and have actively collaborated on developing and scaling up more than 125 cell and gene therapies. In the recent fiscal years, we expanded our existing cell therapy development and manufacturing capabilities, began offering pDNA production services, and acquired several facilities including a commercial-scale cell therapy manufacturing facility in Princeton, New Jersey (“Princeton”) and a developer and manufacturer of iPSCs located near Dusseldorf, Germany. We have also invested in a second-generation ADC technology, SMARTag, and see continued progress in this technology’s capabilities and our customers’ SMARTag product-development activities.

In addition to our expansion in biologics, we have invested additional capital in our facilities in order to expand in attractive markets, including significant expansion of our oral solid controlled release production capacity in Winchester, Kentucky, and the addition of specialized capabilities and capacity in early development. We acquired a leading position in consumer-preferred gummy and soft-chew formats for consumer health products with our acquisition of Bettera Holdings, LLC (“Bettera Wellness”) in fiscal 2022. We expanded our capacity for oral and injectable products via our fiscal 2020 acquisition of a facility in Anagni, Italy, and our capacity for spray dried dispersion and dry powder inhaler manufacturing via our fiscal 2021 acquisition of a facility located near Boston, Massachusetts.

Use Our Proprietary Technologies and Substantial Expertise to Help Our Customers Develop New Products

We have broad and diverse technology platforms that are supported by deep scientific and technical expertise, extensive know-how, and more than 1,800 patents and patent applications in approximately 170 families across advanced delivery platforms, drug and biologics formulation, and manufacturing. For example, we have significant softgel fill and formulation know-how, databases of formulated products, and substantial softgel regulatory approval expertise. As a result, nearly 90% of

10

approvals by the FDA over the last 25 years of new chemical entities presented in a softgel format have been developed and supplied by us.

In addition to resolving delivery challenges for our customers’ products, we have applied our technology platforms and development expertise to proactively develop proof-of-concept products, whether improved versions of existing drugs, new generic formulations, or innovative consumer health products. In the consumer health area, we file product dossiers with regulators in relevant jurisdictions for self-created products, which help contribute sustainable growth to our consumer health business. We expect to continue to seek proactive development opportunities and other non-traditional relationships to increase demand for and value realized from our technology platforms. These activities have provided us with opportunities to capture an increased share of end-market value through out-licensing, profit-sharing, and other arrangements.

Operational Leverage — Deploy Existing Infrastructure and Operational Discipline to Drive Profitable Growth

Through our existing infrastructure, including our global network of operating locations and programs, we promote operational discipline and drive margin expansion. With our active focus on continuous improvement and sustainability enhancement, global procurement function, and conversion cost productivity metrics in place, we continuously seek to enhance our culture of functional excellence and cost accountability. Along with the ongoing increase in the share of revenues from higher margin biologics offerings, we expect this discipline to further leverage our operational network for profitable growth.

Strategic Acquisitions and Licensing — Build on our Existing Platform

We operate in the markets for outsourced development solutions and commercial supply, generally provided by contract development and manufacturing organizations (“CDMO”), where we estimate current industry spending at more than $70 billion globally. Our broad platform, global infrastructure, and diversified customer portfolio provide us with a strong foundation from which to consolidate within these markets, to enter new markets, and generate operating leverage through acquisitions. Since fiscal 2013, we have executed 22 transactions, investing approximately $4.91 billion, and have demonstrated an ability to efficiently and effectively integrate these acquisitions.

While we are rigorously focused on driving our organic growth, we have in recent years substantially increased our participation in biologics, including protein-based biologics, cell and gene therapies, pDNA development and production, and drug product fill and finish, via strategy-driven inorganic transactions. We intend to identify and execute strategic transactions to optimize our portfolio of offerings and businesses, within the context of our long-term capital allocation strategy. We have a dedicated corporate development team in place to pursue these transactions, enabled by a rigorous and financially disciplined process for evaluating and executing these transactions.

“Follow the Molecule”® by Providing Solutions to our Customers across all Phases of the Product Lifecycle

We intend to continue to use our development and manufacturing solutions across the entire lifecycle of our customers’ products to drive future growth. Our development solutions span the drug development process, starting with our platforms for early pre-clinical development of small molecules, protein-based biologics, and cell and gene therapies; through formulation and analytical services, development and manufacturing of clinical trial supplies, and fill and finish of injectable products; to regulatory consulting. Once a molecule is ready for clinical trials and subsequent commercialization, we provide our customers with a range of advanced technologies and expert, state-of-the-art manufacturing solutions that allow them to deliver their molecules to the end-users in safe, effective, and, in some cases, patient-preferred dosage forms, to produce biologic drug substances needed for protein-based biologics and cell and gene therapies, and to provide primary and secondary packaging solutions and cold-storage distribution services. Our relationship with a molecule typically starts with developing and manufacturing the innovator product and can extend throughout the molecule’s commercial life. For prescription products, we are often the sole or primary outsourced provider and are frequently reflected in customers’ product approval applications. Our revenue from our development and manufacturing activities are primarily driven by volumes, and, as a result, the loss of an innovator drug’s market exclusivity may be mitigated if we supply customers offering generic or biosimilar equivalents.

An example of the long and mutually productive relationships we foster can be found in a leading over-the-counter anti-allergy brand, which today uses both our proprietary Zydis orally disintegrating tablets and Liqui-Gels softgel technology. We originally began development of the prescription format of this product for our multinational pharmaceutical company partner in 1992 to address specific patient sub-segment needs. After four years of development, we then commercially supplied the prescription product in our Zydis format for six years, and we have continued to provide the Zydis form since the switch to over-the-counter status in the U.S. and other markets in the early 2000s. Subsequently, we proactively brought a softgel product concept for the brand to the customer, which the customer elected to develop and launch as well. By following this molecule, we have built a strong, 3 decade-long relationship across multiple formats and markets.

11

Customer Product Pipeline — Continuing to Grow Through New Projects and Product Launches

We intend to continue to supplement our existing diverse base of commercialized customer products with new development programs. As of June 30, 2023, our product development teams were working on more than 1,500 customer development programs in active development across our business. Our base of active development programs has expanded in recent years from growing market demand, as well as from our expanded capabilities and technology platforms. Although there are many complex factors that affect the development and commercialization of pharmaceutical, protein-based biologic, cell and gene therapy, and consumer health products, we expect that a portion of these programs will reach full development and market approval in the future and thereby add to our long-duration commercial revenues under long-term contracts and grow our existing product base. In fiscal 2023, we introduced 216 new products for our customers.

Catalent continues to be a leader in providing chemistry, manufacturing, and controls-based product development services to the global pharmaceutical, biotechnology, and consumer health industries, driven by thousands of projects annually. In fiscal 2023, we recognized $1.95 billion of net revenue related to the development of products, down 16% from the prior year, principally driven by the substantial decrease in net revenue from the development of COVID-19 related products. In addition, substantially all of the revenue associated with the Clinical Supply Services business relates to our support of customer products in development.

Our Reportable Segments

At the beginning of fiscal 2023, in connection with the appointment of a new President and Chief Executive Officer, who also serves as the Company’s Chief Operating Decision Maker, the Company changed its operating structure and reorganized its executive leadership team. This new organizational structure includes operating and reporting in two segments: (i) Biologics and (ii) Pharma and Consumer Health.

Biologics

Our Biologics segment provides formulation, development, and manufacturing for biologic proteins, cell gene, and other nucleic acid therapies; pDNA, iPSCs, oncolytic viruses, and vaccines; formulation, development, and manufacturing for parenteral dose forms, including vials, prefilled syringes, and cartridges; and analytical development and testing services for large molecules. The business has extensive expertise in development, scale up, and commercial manufacturing. Representative customers of our Biologics segment include Bristol-Myers Squibb, Johnson & Johnson, Moderna, and Sarepta Therapeutics, along with a broad range of innovative small and mid-tier biopharmaceutical customers.

Our biologics offering includes cell-line development based on our advanced, patented GPEx suite of technologies, which are used to develop stable, high-yielding mammalian cell lines for both innovator and biosimilar biologic compounds. GPEx technology can provide rapid cell-line development, high biologics production yields, flexibility, and versatility. Our development and manufacturing facility in Madison, Wisconsin has the capability and capacity to produce cGMP quality biologics drug substance from 250L to 4000L scale using single-use technology across five suites to provide maximum efficiency, redundancy, and flexibility. Additionally, our Madison, Wisconsin facility features two flexible cGMP suites that are used to manufacture mRNA or other small-scale biomolecules. Our Bloomington, Indiana facility brings additional biologics development, clinical, and commercial drug substance manufacturing, and formulation development capabilities and capacity. Both Bloomington and our Anagni, Italy facility provide substantial capacity for finished-dose drug product manufacturing and packaging. Our SMARTag next-generation ADC technology, based in Emeryville, California, is a clinical-stage technology that enables development of ADCs and other protein conjugates with improved efficacy, safety, and manufacturability.

At our pDNA, cell therapy, and gene therapy global centers of excellence in Belgium, Maryland, and New Jersey, we develop and manufacture advanced therapeutics, including AAV, lentivirus, oncolytic virus, CAR-T, and other cell or virus modalities together with critical pDNA biological starting material for cell, mRNA, viral-based therapies and next-generation vaccines. In fiscal 2022, we acquired a fully operational, commercial-scale cell therapy campus in Princeton with 16 suites available for both autologous and allogeneic clinical and commercial manufacturing. The Princeton campus works in conjunction with our Gosselies, Belgium cell therapy center of excellence and our iPSC manufacturing center of excellence in Dusseldorf, Germany, to support our customers’ global cell therapy needs. Additionally, we have expanded our gene therapy flagship manufacturing campus in Harmans, Maryland, creating a total of 18 penthouse-style viral-vector suites, and added our Virtuoso AAV platform that reduces AAV development time by half, enabling our customers to reach first-in-human studies faster. Our specialized expertise in AAV vectors, the most commonly used delivery system for gene therapies, and iPSCs for next-generation allogeneic cell therapy manufacturing, together with our substantial global cell therapy manufacturing, capacity for clinical- through commercial-scale batches, and our capabilities in mRNA and pDNA manufacturing, position us to capitalize on strong industry demand and expansions in the use of newer modalities in the cell and gene therapy market.

12

Our range of injectable manufacturing offerings includes manufacturing drug substances and filling small molecules or biologics into vials, syringes, and cartridges, with flexibility to accommodate other formats within our existing network. In addition to primary packaging, our network provides secondary packaging capabilities, including auto-injector and safety device assembly for commercial launch and life-cycle management. Our clinical supply services business provides a global network for clinical distribution, as well as labeling, packaging, and cold-chain storage for clinical trials and commercial supply of biotherapeutics and cell and gene therapies. Our fill and finish services are largely focused on complex pharmaceuticals and biologics. With our range of technologies, we are able to meet a wide range of specifications, timelines, and budgets. We believe that the complexity of the manufacturing process, the importance of experience and know-how, a proven history of regulatory compliance, and substantial state-of-the-art capacity provide us with a meaningful competitive advantage in the market.

We also offer analytical development and testing services for proteins, gene and cell therapies, and other biologic modalities, including bioassay, biophysical characterization, and cGMP release and stability testing. Our OneBio Suite provides customers with the potential to seamlessly integrate drug substance, drug product, and clinical supply management for products in development, and for integrated commercial supply across both drug substance and drug product. We provide a broad range of technologies and services supporting the development and launch of new biologic entities, biosimilars, biobetters, and cell and gene therapies to bring a product from gene to commercialization, faster.

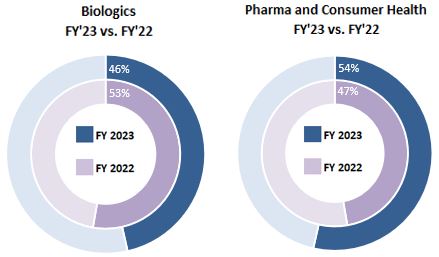

Our Biologics segment represented 46%, 53%, and 48% of our aggregate net revenue before inter-segment eliminations for fiscal 2023, 2022, and 2021, respectively.

Pharma and Consumer Health

Through our Pharma and Consumer Health segment, we provide market-leading capabilities for complex oral solids, softgel formulations, Zydis fast-dissolve technologies, and gummy, soft chew, and lozenge dosage forms; formulation, development, and manufacturing platforms for oral, nasal, inhaled, and topical dose forms; and clinical trial development and supply services.

Representative customers of our Pharma and Consumer Health segment include Bayer, Bristol-Myers Squibb, GlaxoSmithKline, Haleon, Pfizer, and Procter & Gamble.

Our Pharma and Consumer Health segment represented 54%, 47%, and 52% of our aggregate net revenue before inter-segment eliminations for fiscal 2023, 2022, and 2021, respectively.

Formulation and development

Through our comprehensive pharmaceutical formulation and development platform, we provide pre-clinical screening, formulation, and analytical development, and cGMP manufacturing at both clinical and commercial scale for our market-leading softgel capsule and Zydis fast-dissolve tablet platforms, traditional and advanced complex oral solid-dose formats, dry powder inhalers, and nasal delivery devices. We have substantial, proven experience in developing and scaling up orphan and rare disease products, especially those requiring accelerated development timelines, solubility enhancement, specialized handling (e.g., potent or controlled substance materials), complex technology transfer and specialized manufacturing processes. We provide fluid bed coating, spray drying, hot melt extrusion, micronization, and lipid formulation capabilities, all of which are used to enhance a drug’s administration and release profile and its clinical performance. We offer comprehensive analytical method development and scientific capabilities, including stability testing and global regulatory services to support both fully integrated development programs or standalone fee-for-service work. We have a network of early development sites focused on earlier phase compounds (i.e., pre-clinical and Phase I) to engage with more customer molecules earlier in their development, with the intent to also support these molecules downstream as they progress towards commercial approval and supply. Demand for our offerings is driven by the need for scientific expertise, the depth and breadth of integrated services offered, as well as the reliability of our supply performance across quality and operational parameters.

Manufacturing

Our large-scale cGMP pharmaceutical manufacturing solutions typically include clinical trial supplies, registration batches, and commercial production across a broad range of formats, and may also involve finished dose packaging or advanced processing of intermediates to achieve the desired clinical performance of the prescription or over-the-counter pharmaceutical product. Finished dose forms include softgel capsules, our Zydis fast-dissolve tablets, and traditional and advanced complex oral solid-doses, including coated and uncoated tablets, pellet/bead/powder-filled two-piece hard capsules, granulated powders, and other immediate and modified release forms. Advanced intermediate processing may include coating, extrusion, or spheronization to achieve specific functional outcomes, including site- or time-specific drug release, taste

13

masking, or enhanced bioavailability. We have deep experience at managing complex technical transfers of clinical or commercial programs, whether from Catalent’s early development network, other contract development sites, or from customers directly.

Softgel technology platform

We provide formulation, development, and manufacturing services for soft capsules, or “softgels,” as well as large-scale manufacturing of oral solid dose forms for pharmaceutical and consumer health markets, along with supporting ancillary services. Our softgel manufacturing technology was first commercialized by our predecessor in the 1930s, and we have continually enhanced the platform since then. We are the market leader in overall softgel development and manufacturing and hold the leading market position in innovator drug softgels. Our principal softgel technologies include traditional softgel capsules, in which the shell is made of animal-derived gelatin, and Vegicaps and OptiShell capsules, in which the shell is made from plant-derived materials. Softgel capsules are used in a broad range of customer products, including prescription drugs, over-the-counter medications, dietary supplements, unit-dose cosmetics, and animal health medicinal preparations. Softgel capsules encapsulate liquid, paste, or oil-based formulations of active compounds in solution or suspension within an outer shell. In the manufacturing process, the capsules are formed, filled, and sealed simultaneously. We typically perform encapsulation for a product within one of our softgel facilities, with active ingredients provided by customers or sourced directly by us. Softgels have historically been used to solve formulation challenges or technical issues for a specific drug, to help improve the clinical performance of compounds, to provide important market differentiation, particularly for over-the-counter medications, and to provide safe handling of hormonal, highly potent, and cytotoxic drugs. We also participate in the softgel vitamin, mineral, and supplement business in selected regions around the world. Our plant-derived softgel shells, available as Vegicaps and OptiShell capsules, allow innovators and consumer health customers to extend the softgel dose form to a broader range of active ingredients and serve patient and consumer populations that were previously inaccessible due to religious, dietary, or cultural preferences. Our Vegicaps and OptiShell capsules are protected by patents in most major global markets. Physician and patient studies we have conducted have demonstrated a preference for softgels versus traditional tablet and hard capsule dose forms in terms of ease of swallowing, real or perceived speed of delivery, ability to remove or eliminate unpleasant odor or taste, and, for physicians, perceived improved patient adherence with dosing regimens.

In addition to softgel capsules, following our fiscal 2022 acquisition of Bettera Wellness, we also conduct formulation, development, and manufacturing of gummies, soft chews, and lozenges in a variety of sizes and shapes serving the dietary supplements market at three facilities in the United States. We use dietary and food ingredients provided by our customers or sourced directly by us, and we also provide ancillary services such as analytical testing and packaging.

Clinical Supply Services

Our Pharma and Consumer Health segment also provides clinical supply services through manufacturing, packaging, storage, distribution, and inventory management for small-molecule drugs, protein-based biologics, and cell and gene therapies in clinical trials. We offer customers flexible solutions for clinical supplies production and provide distribution and inventory management support for both simple and complex clinical trials. This includes over-encapsulation where needed; supplying placebos, comparator drug procurement, and clinical packages and kits for physicians and patients; inventory management; investigator kit ordering and fulfillment; cold-chain storage and distribution; and return supply reconciliation and reporting. We support trials in all regions of the world through our facilities and distribution network. In recent years, we have extended our network, with significant expansions at our Philadelphia, Pennsylvania and Shanghai, China free trade zone locations and facilities in California, China, and Japan. We also continue to develop new solutions for the evolving clinical trial environment, including FlexDirect direct-to-patient, CT Success clinical supply planning, and extensive cold-chain investments. We are the leading provider of integrated development solutions and one of the leading providers of clinical trial supplies.

We have partnered with companies who focus on the development of cannabis-based prescription medicines and high-value cannabinoid drug therapies whose goal is to achieve full regulatory approval under the strictest legal standards in effect in any jurisdiction affected, including cannabidiol and tetrahydrocannabinol pharmaceutical products using our Zydis technology in clinical trials across a range of indications, including multiple sclerosis spasticity, chemotherapy-induced nausea and vomiting, chronic pain for cancer, and epilepsy. Our total net revenue related to such development programs was less than 1% of total revenue generated in fiscal 2023. We do not provide any services for or otherwise partner with any company that does not comply with all applicable laws, including the U.S. federal controlled substances laws (or non-U.S. equivalent laws), relating to cannabis products.

14

Integrated Development and Product Supply Chain Solutions

In addition to our proprietary offerings, we are also differentiated in the market by our ability to bring together our development solutions and state-of-the-art product manufacturing to offer integrated development and product supply solutions that can be combined or tailored in many ways to enable our customers to take their drugs, biologics, and consumer health products from laboratory to market, faster. Once a product is on the market, we can provide comprehensive, integrated product supply, from the sourcing or supply of the bulk active ingredient to comprehensive manufacturing and packaging, to the testing required for release, and to cold-chain or ambient temperature distribution. The customer- and product-specific solutions we develop are flexible, scalable, and creative, so that they meet the unique needs of both large and emerging biopharmaceutical, pharmaceutical, and consumer health companies and are appropriate for products of all sizes. We believe that our development and product supply solutions, such as OptiForm Solution Suite and OneBio Suite, will continue to contribute to our future growth.

Sales and Marketing

Our target customers include large pharmaceutical and biotechnology companies, mid-size, emerging, and specialty pharmaceutical and biotechnology companies, and consumer health companies, along with companies in other selected healthcare market segments such as animal health and medical devices, and companies in adjacent industries, such as cosmetics. We have longstanding, extensive relationships with leading pharmaceutical, biotechnology, and consumer health customers. In fiscal 2023, we did business with 87 of the top 100 branded drug and consumer health marketers and 82 of the top 100 biologics marketers, measured on a global basis, as well as with more than 1,200 other customers. Faced with access, pricing, and reimbursement pressures as well as other market challenges, large pharmaceutical and biotechnology companies have increasingly sought partners to enhance the clinical competitiveness of their drugs and biologics and improve the productivity of their research and development activities, while reducing their fixed cost bases. Many mid-size, emerging, and specialty pharmaceutical and biotechnology companies, while facing the same pricing and market pressures, have chosen not to build a full infrastructure, but rather to partner with other companies through licensing agreements or outsourcing to access the critical skills, technologies, and services required to bring their products to market. Consumer health companies require rapidly developed, innovative dose forms and formulations to keep up with the fast-paced over-the-counter medication, dietary supplement, and personal care markets. These market segments are all important to our growth, but require distinct solutions, marketing and sales approaches, and market strategy.

We follow a hybrid demand-generation organization model, with strategic account teams offering the full breadth of Catalent’s solutions, and technical specialist teams providing the in-depth technical knowledge and practical experience essential for each individual offering, both supported by a dedicated team of deeply experienced scientific advisors. Our sales organization currently consists of more than 200 full-time, experienced sales professionals, supported by inside sales and sales operations. We also have built a dedicated strategic marketing team, providing strategic market and product planning and management for our offerings. As part of our marketing efforts, we participate in major trade shows relevant to our offerings globally and ensure adequate visibility to our offerings and solutions through a comprehensive advertising and publicity program. We believe that Catalent is a strong brand with high overall awareness in our established markets and universe of target customers, and that our brand identity is a competitive advantage for us.

Global Accounts

We manage select accounts globally due to their substantial current business or growth potential. We recorded approximately one-third of our total net revenue in fiscal 2023 from these global accounts. Each global account is assigned a lead business development professional with substantial industry experience. These account leaders, along with other members of the sales and executive leadership teams, are responsible for managing and extending the overall account relationship. Account leaders work closely with the rest of the sales organization as well as operational, quality, and project management personnel to ensure alignment around critical priorities for the accounts.

Emerging, Specialty, and Virtual Accounts

Emerging, specialty, and virtual pharmaceutical and biotechnology companies are expected to be critical drivers of industry growth globally and account for more than three-quarters of the active drug and biologic development pipeline. Historically, many of these companies have chosen not to build a full infrastructure, but rather partner with other companies to formulate, develop, analyze, test, and manufacture their products. We expect them to continue to do so in the future, providing a critical source for future integrated solutions demand. We expect to continue to increase our penetration of geographic clusters of emerging companies in North America, Europe, Central and South America, and Asia. We regularly use active pipeline and product screening and customer targeting to identify the optimal candidates for partnering based on product profiles, funding status, and relationships, to ensure that our technical sales specialists and field sales representatives develop custom solutions

15

designed to address the specific needs of these customers. In order to reach these emerging, specialty, and virtual companies, we actively partner with leading venture capital investors and biotech incubators.

Seasonality; Fluctuations in Operation Results

Our annual financial reporting period ends on June 30. As discussed further in “Item 7. - Management's Discussion and Analysis of Financial Condition and Results of Operations - Factors Affecting our Performance,” our revenue and net earnings are generally higher in the third and fourth quarters of each fiscal year, with our first fiscal quarter typically generating our lowest revenue of any quarter, and our last fiscal quarter typically generating our highest revenue. These fluctuations are primarily the result of the timing of our, and our customers’ annual operational maintenance periods at locations in the U.S. and Europe, the seasonality associated with pharmaceutical and biotechnology budgetary spending decisions, clinical trial and research and development schedules, the timing of new product launches and length of time needed to obtain full market penetration, and, to a lesser extent, the time of the year some of our customers’ products are in higher demand, or are being produced to support future seasonal demand.

Contractual Arrangements

We generally enter into a broad range of contractual arrangements with our customers, including agreements with respect to feasibility, development, supply, licenses, quality, and confidentiality. The terms of these contracts vary significantly depending on the offering and customer requirements. Some of our agreements may include a variety of revenue arrangements, such as fee-for-service, unit pricing in one or more tiers, minimum volume commitments, royalties, manufacturing preparation services, profit-sharing, and fixed fees. We generally secure pricing and other contract mechanisms in our supply agreements to allow for periodic resetting of pricing terms, and, in some cases, these agreements permit us to raise or renegotiate pricing in the event of certain price increases for the raw materials or other inputs we use to make products. Our typical supply agreements include indemnification from our customers for product liability and intellectual property matters and caps on our contractual liabilities, subject in each case to negotiated exclusions. The terms of our manufacturing supply agreements range from two to seven years with regular renewals of one to three years, although some of our agreements are terminable upon much shorter notice periods, such as 30 or 45 days. For our development solutions offerings, we may enter into master service agreements, which provide for standardized terms and conditions and make it easier and faster for customers with multiple development needs to access our offerings.

Backlog

While we generally have long-term supply agreements that provide for a revenue stream over a period of years, our backlog represents, as of a point in time, future service revenues from work not yet completed. For our Biologics segment and a majority of our Pharma and Consumer Health segment, backlog represents firm orders for manufacturing services and includes minimum volumes, where applicable. Manufacturing businesses backlog represents firm orders for manufacturing services and includes minimum volumes, where applicable. For the clinical supply services offered through our Pharma and Consumer Health segment, backlog represents estimated future service revenue from work not yet completed under signed contracts. Using these methods of reporting backlog, as of June 30, 2023, our backlog was $2.53 billion, compared to $2.85 billion as of June 30, 2022, including $557 million and $549 million, respectively, related to our scientific and clinical services offerings in our Pharma and Consumer Health segment. We expect to recognize as revenue by the end of fiscal 2024 approximately 83% of the value of the backlog in existence as of June 30, 2023.

To the extent projects are delayed, the timing of our revenue could be affected. If a customer cancels an order, we may be reimbursed for the costs we have incurred. For orders that are placed inside a contractual firm period or that involve minimum volume commitments, we generally have a contractual right to payment in the event of cancellation. Fluctuations in our reported backlog levels also result from the timing and order pattern of our customers, which often seek to manage their level of inventory on hand. Because of customer ordering patterns, the matters discussed in this paragraph, and other factors, our backlog reported for certain periods may fluctuate and may not be indicative of future results.

Manufacturing Capabilities

We operate manufacturing facilities, development centers, and sales offices throughout the world. As of June 30, 2023, we had 52 facilities (3 geographical locations operate as multiple facilities because they support more than one reporting segment, with one location including both a manufacturing facility and our corporate headquarters) on four continents with approximately 8 million square feet of manufacturing, laboratory, office, and related space. Our manufacturing capabilities generally include the full suite of competencies relevant to the support of each site’s activities, including regulatory, quality assurance, and in-house validation.

16

We operate our manufacturing facilities and development centers in accordance with cGMP or other applicable requirements. All of these sites are registered where required with the FDA or other applicable regulatory agencies, such as the EMA. In some cases, our sites are registered with multiple regulatory agencies.

We have invested $1.93 billion in our manufacturing and development facilities since fiscal 2021 for improvements and expansions, including $583 million in capital expenditures during fiscal 2023. We believe that our sites and equipment are in good condition, are well maintained, and are able to operate at or above present levels for the foreseeable future, in all material respects.

Our manufacturing operations are focused on employee health and safety, regulatory compliance, operational excellence, continuous improvement, and process standardization across the organization. In fiscal 2023, we achieved approximately 95% on-time shipment delivery versus customer request date across our network as a result of this focus. Our manufacturing operations are structured around an enterprise management philosophy and methodology that utilizes principles and tools common to a number of quality management programs, including Lean Six Sigma and Lean Manufacturing, which we brought together in a system that we refer to as “The Catalent Way.”

Raw Materials

We use a broad and diverse range of raw materials and other supplies in the design, development, and manufacture of our products. This includes, but is not limited to, key materials such as gelatin, starch, and iota carrageenan; packaging films; single-use production components for drug substance production, and glass vials and syringes for drug product. The raw materials and other supplies that we use are sourced externally on a global basis. Globally, our supplier relationships could be interrupted due to natural disasters and international supply disruptions, including those caused by pandemics or geopolitical and other issues. For example, commercially usable gelatin is available from a limited number of sources. In addition, much of the gelatin we use is bovine-derived. Past concerns of contamination from bovine spongiform encephalopathy have narrowed the number of possible sources of particular types of gelatin. If there were a future disruption in the supply of gelatin or any other key material from any one or more of our current principal suppliers, there can be no assurance that we could obtain an adequate alternative supply from our other suppliers. Any future restriction that were to emerge on the use of a key raw material used in our products from certain geographic sources or due to regulatory or consumer concerns could hinder our ability to timely supply our customers with products, and the use of alternative raw materials could be subject to lengthy formulation, testing and regulatory approval periods.