UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

______________________________

FORM 10-Q

______________________________

| ý | QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | ||||

For the Quarterly Period Ended December 31, 2018

or

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | ||||

001-36587

(Commission File Number)

_____________________________

Catalent, Inc.

(Exact name of registrant as specified in its charter)

_____________________________

| Delaware | 20-8737688 | |||||||

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |||||||

| 14 Schoolhouse Road, Somerset, NJ | 08873 | |||||||

| (Address of principal executive offices) | (Zip code) | |||||||

(732) 537-6200

Registrant's telephone number, including area code

______________________________

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). x Yes ¨ No

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer x | Accelerated filer ¨ | |||||||||||||

Non-accelerated filer ¨ | Smaller reporting company ¨ | |||||||||||||

Emerging growth company ¨ | ||||||||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ¨

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No x

On February 1, 2019, there were 145,632,701 shares of the Registrant's common stock, par value $0.01 per share, issued and outstanding.

CATALENT, INC. and Subsidiaries

INDEX TO FORM 10-Q

For the Three Months Ended December 31, 2018

| Item | Page | |||||||

| Part I. | ||||||||

| Item 1. | Financial Statements (unaudited) | |||||||

| Item 2. | ||||||||

| Item 3. | ||||||||

| Item 4. | ||||||||

| Part II. | ||||||||

| Item 1. | ||||||||

| Item 1A. | ||||||||

| Item 2. | ||||||||

| Item 3. | ||||||||

| Item 4. | ||||||||

| Item 5. | ||||||||

| Item 6. | ||||||||

2

Special Note Regarding Forward-Looking Statements

In addition to historical information, this Quarterly Report on Form 10-Q may contain “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933, as amended (the “Securities Act”), and Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”), which are subject to the “safe harbor” created by those sections. All statements, other than statements of historical facts, included in this Quarterly Report on Form 10-Q are forward-looking statements. In some cases, you can identify these forward-looking statements by the use of words such as “outlook,” “believes,” “expects,” “potential,” “continues,” “may,” “will,” “should,” “could,” “seeks,” “approximately,” “predicts,” “intends,” “plans,” “estimates,” “anticipates” or the negative version of these words or other comparable words.

These statements are based on assumptions and assessments made by our management in light of their experience and their perception of historical trends, current conditions, expected future developments, and other factors they believe to be appropriate. Any forward-looking statement is subject to various risks and uncertainties. Accordingly, there are or will be important factors that could cause actual outcomes or results to differ materially from those indicated in these statements.

Some of the factors that may cause actual results, developments and business decisions to differ materially from those contemplated by such forward-looking statements include, but are not limited to, those described under the section entitled “Risk Factors” in our Annual Report on Form 10-K for the fiscal year ended June 30, 2018 (the "Fiscal 2018 10-K") and the following:

•We participate in a highly competitive market, and increased competition may adversely affect our business.

•The demand for our offerings depends in part on our customers’ research and development and the clinical and market success of their products. Our business, financial condition, and results of operations may be harmed if our customers spend less on, or are less successful in, these activities.

•We are subject to product and other liability risks that could exceed our anticipated costs or adversely affect our results of operations, financial condition, liquidity, and cash flows.

•Failure to comply with existing and future regulatory requirements could adversely affect our results of operations and financial condition or result in claims from customers.

•Failure to provide quality offerings to our customers could have an adverse effect on our business and subject us to regulatory actions or costly litigation.

•The services and offerings we provide are highly exacting and complex, and if we encounter problems providing the services or support required, our business could suffer.

•Our global operations are subject to economic, political, and regulatory risks, including the risks of changing regulatory standards or changing interpretations of existing standards, that could affect the profitability of our operations or require costly changes to our procedures.

•The exit of the United Kingdom (the "U.K.") from the European Union could have future adverse effects on our operations, revenues, and costs, and therefore our profitability.

•If we do not enhance our existing or introduce new technology or service offerings in a timely manner, our offerings may become obsolete over time, customers may not buy our offerings, and our revenue and profitability may decline.

•We and our customers depend on patents, copyrights, trademarks, trade secrets, and other forms of intellectual property protections, but these protections may not be adequate.

•Our future results of operations are subject to fluctuations in the costs, availability, and suitability of the components of the products we manufacture, including active pharmaceutical ingredients, excipients, purchased components, and raw materials.

•Changes in market access or healthcare reimbursement for our customers’ products in the United States ("U.S.") or internationally, including possible changes to the U.S. Affordable Care Act, could adversely affect our results of operations and financial condition by affecting demand for our offerings or the financial health of our customers.

3

•As a global enterprise, fluctuations in the exchange rate of the U.S. dollar, our reporting currency, against foreign currencies could have a material adverse effect on our financial performance and results of operations.

•Tax legislative or regulatory initiatives or challenges to our tax positions could adversely affect our results of operations and financial condition.

•Our ability to use our net operating loss carryforwards and certain other tax attributes may be limited.

•Changes to the estimated future profitability of the business may require that we establish an additional valuation allowance against all or some portion of our net U.S. deferred tax assets.

•We are dependent on key personnel.

•We use advanced information and communication systems to run our operations, compile and analyze financial and operational data, and communicate among our employees, customers, and counter-parties, and the risks generally associated with information and communications systems could adversely affect our results of operations. We are continuously working to install new, and upgrade existing, systems and provide employee awareness training around phishing, malware, and other cyber-security risks to enhance the protections available to us, but such protections may be inadequate to address malicious attacks or inadvertent compromises of data security.

•We engage, from time to time, in acquisitions and other transactions that may complement or expand our business or divest of non-strategic businesses or assets. We may not be able to complete such transactions, and such transactions, if executed, pose significant risks, including risks relating to our ability to successfully and efficiently integrate acquisitions or execute on dispositions and realize anticipated benefits therefrom. The failure to execute or realize the full benefits from any such transaction could have a negative effect on our operations.

•Our offerings or our customers’ products may infringe on the intellectual property rights of third parties.

•We are subject to environmental, health, and safety laws and regulations, which could increase our costs and restrict our operations in the future.

•We are subject to labor and employment laws and regulations, which could increase our costs and restrict our operations in the future.

•Certain of our pension plans are underfunded, and additional cash contributions we may make to increase the funding level will reduce the cash available for our business, such as the payment of our interest expense.

•Our substantial leverage could adversely affect our ability to raise additional capital to fund our operations, limit our ability to react to changes in the economy or in our industry, expose us to interest-rate risk to the extent of our variable rate debt, and prevent us from meeting our obligations under our indebtedness.

We caution you that the risks, uncertainties and other factors referenced above may not contain all of the risks, uncertainties, and other factors that are important to you. In addition, we cannot assure you that we will realize the results, benefits, or developments that we expect or anticipate or, even if substantially realized, that they will result in the consequences or affect us or our business in the way expected. There can be no assurance that (i) we have correctly measured or identified all of the factors affecting our business or the extent of these factors’ likely impact, (ii) the available information with respect to these factors on which such analysis is based is complete or accurate, (iii) such analysis is correct, or (iv) our strategy, which is based in part on this analysis, will be successful. All forward-looking statements in this report apply only as of the date of this report or as of the date they were made, and we undertake no obligation to publicly update or review any forward-looking statement, whether as a result of new information, future developments, or otherwise, except as required by law.

4

Social Media

We use our website (www.catalent.com), our corporate Facebook page (https://www.facebook.com/CatalentPharmaSolutions), and our corporate Twitter account (@catalentpharma) as channels for the distribution of information. The information we post through these channels may be deemed material. Accordingly, investors should monitor these channels, in addition to following our press releases, Securities and Exchange Commission ("SEC") filings, and public conference calls and webcasts. The contents of our website and social media channels are not, however, a part of this report.

5

PART I. FINANCIAL INFORMATION

Item 1. FINANCIAL STATEMENTS

Catalent, Inc. and Subsidiaries

Consolidated Statements of Operations

(Unaudited; Dollars in millions, except per share data)

| Three Months Ended December 31, | Six Months Ended December 31, | ||||||||||||||||||||||

| 2018 | 2017 | 2018 | 2017 | ||||||||||||||||||||

| Net revenue | $ | $ | $ | $ | |||||||||||||||||||

| Cost of sales | |||||||||||||||||||||||

| Gross margin | |||||||||||||||||||||||

| Selling, general, and administrative expenses | |||||||||||||||||||||||

| Impairment charges and (gain)/loss on sale of assets | ( | ||||||||||||||||||||||

| Restructuring and other | |||||||||||||||||||||||

| Operating earnings | |||||||||||||||||||||||

| Interest expense, net | |||||||||||||||||||||||

| Other expense, net | |||||||||||||||||||||||

| Earnings from continuing operations before income taxes | |||||||||||||||||||||||

| Income tax expense | |||||||||||||||||||||||

| Net earnings/(loss) | $ | $ | ( | $ | $ | ( | |||||||||||||||||

| Earnings/(loss) per share: | |||||||||||||||||||||||

| Basic | |||||||||||||||||||||||

| Net earnings/(loss) | $ | $ | ( | $ | $ | ( | |||||||||||||||||

| Diluted | |||||||||||||||||||||||

| Net earnings/(loss) | $ | $ | ( | $ | $ | ( | |||||||||||||||||

The accompanying notes are an integral part of these unaudited consolidated financial statements.

6

Catalent, Inc. and Subsidiaries

Consolidated Statements of Comprehensive Income/(Loss)

(Unaudited; Dollars in millions)

| Three Months Ended December 31, | Six Months Ended December 31, | ||||||||||||||||||||||

| 2018 | 2017 | 2018 | 2017 | ||||||||||||||||||||

| Net earnings/(loss) | $ | $ | ( | $ | $ | ( | |||||||||||||||||

| Other comprehensive income/(loss), net of tax | |||||||||||||||||||||||

| Foreign currency translation adjustments | ( | ( | ( | ||||||||||||||||||||

| Pension and other post-retirement adjustments | |||||||||||||||||||||||

| Available for sale investments | ( | ( | |||||||||||||||||||||

| Other comprehensive income/(loss), net of tax | ( | ( | ( | ||||||||||||||||||||

| Comprehensive income/(loss) | $ | $ | ( | $ | $ | ||||||||||||||||||

The accompanying notes are an integral part of these unaudited consolidated financial statements.

7

Catalent, Inc. and Subsidiaries

Consolidated Balance Sheets

(Unaudited; Dollars in millions, except share and per share data)

| December 31, 2018 | June 30, 2018 | ||||||||||

| ASSETS | |||||||||||

| Current assets: | |||||||||||

| Cash and cash equivalents | $ | $ | |||||||||

| Trade receivables, net | |||||||||||

| Inventories | |||||||||||

| Prepaid expenses and other | |||||||||||

| Total current assets | |||||||||||

| Property, plant, and equipment, net | |||||||||||

| Other assets: | |||||||||||

| Goodwill | |||||||||||

| Other intangibles, net | |||||||||||

| Deferred income taxes | |||||||||||

| Other | |||||||||||

| Total assets | $ | $ | |||||||||

| LIABILITIES AND SHAREHOLDER’S DEFICIT | |||||||||||

| Current liabilities: | |||||||||||

| Current portion of long-term obligations and other short-term borrowings | $ | $ | |||||||||

| Accounts payable | |||||||||||

| Other accrued liabilities | |||||||||||

| Total current liabilities | |||||||||||

| Long-term obligations, less current portion | |||||||||||

| Pension liability | |||||||||||

| Deferred income taxes | |||||||||||

| Other liabilities | |||||||||||

| Commitment and contingencies (see Note 14) | |||||||||||

| Shareholders' equity: | |||||||||||

| Common stock $0.01 par value; 1.0 billion shares authorized on December 31, 2018 and June 30, 2018, 145,622,900 and 133,423,628 issued and outstanding on December 31, 2018 and June 30, 2018, respectively. | |||||||||||

| Preferred stock $0.01 par value; 100 million authorized on December 31, 2018 and June 30, 2018, 0 issued and outstanding on December 31, 2018 and June 30, 2018. | |||||||||||

| Additional paid in capital | |||||||||||

| Accumulated deficit | ( | ( | |||||||||

| Accumulated other comprehensive income/(loss) | ( | ( | |||||||||

| Total shareholder's equity | |||||||||||

| Total liabilities and shareholder’s equity | $ | $ | |||||||||

The accompanying notes are an integral part of these unaudited consolidated financial statements.

8

Catalent, Inc. and Subsidiaries

Consolidated Statement of Changes in Shareholders' Equity/(Deficit)

(Unaudited; Dollars in millions, except share data in thousands)

| Shares of Common Stock | Common Stock | Additional Paid in Capital | Accumulated Deficit | Accumulated Other Comprehensive Income/(Loss) | Total Shareholders' Equity/ (Deficit) | ||||||||||||||||||||||||||||||

| Balance at June 30, 2018 | $ | $ | $ | ( | $ | ( | $ | ||||||||||||||||||||||||||||

Cumulative effect of change in accounting for ASC 606, net of tax | |||||||||||||||||||||||||||||||||||

| Equity offering, sale of common stock | |||||||||||||||||||||||||||||||||||

Share issuances related to stock-based compensation | ( | ||||||||||||||||||||||||||||||||||

| Stock-based compensation | |||||||||||||||||||||||||||||||||||

Cash paid, in lieu of equity, for tax withholding | ( | ( | |||||||||||||||||||||||||||||||||

| Net earnings | |||||||||||||||||||||||||||||||||||

| Other comprehensive income/(loss), net of tax | ( | ( | |||||||||||||||||||||||||||||||||

| Balance at December 31, 2018 | $ | $ | $ | ( | $ | ( | $ | ||||||||||||||||||||||||||||

The accompanying notes are an integral part of these unaudited consolidated financial statements.

9

Catalent, Inc. and Subsidiaries

Consolidated Statements of Cash Flows

(Unaudited; Dollars in millions)

| Six Months Ended December 31, | |||||||||||

| 2018 | 2017 | ||||||||||

| CASH FLOWS FROM OPERATING ACTIVITIES: | |||||||||||

| Net earnings/(loss) | $ | $ | ( | ||||||||

Adjustments to reconcile earnings/(loss) from operations to net cash from operations: | |||||||||||

| Depreciation and amortization | |||||||||||

| Non-cash foreign currency transaction (gain)/loss, net | |||||||||||

Amortization and write-off of debt financing costs | |||||||||||

Asset impairments charges and (gain)/loss on sale of assets | |||||||||||

Reclassification of financing fees paid | |||||||||||

Stock-based compensation | |||||||||||

| Provision/(benefit) for deferred income taxes | ( | ||||||||||

| Provision for bad debts and inventory | |||||||||||

| Change in operating assets and liabilities: | |||||||||||

| Decrease/(increase) in trade receivables | |||||||||||

| Decrease/(increase) in inventories | ( | ||||||||||

| Increase/(decrease) in accounts payable | ( | ( | |||||||||

Other assets/accrued liabilities, net — current and non-current | ( | ( | |||||||||

| Net cash provided by operating activities | |||||||||||

| CASH FLOWS FROM INVESTING ACTIVITIES: | |||||||||||

| Acquisition of property and equipment and other productive assets | ( | ( | |||||||||

| Proceeds from sale of property and equipment | |||||||||||

| Proceeds from sale of subsidiaries | |||||||||||

| Payment for acquisitions, net of cash acquired | ( | ( | |||||||||

| Net cash (used in) investing activities | ( | ( | |||||||||

| CASH FLOWS FROM FINANCING ACTIVITIES: | |||||||||||

| Net change in other borrowings | ( | ( | |||||||||

| Proceeds from borrowing, net | |||||||||||

| Payments related to long-term obligations | ( | ( | |||||||||

Financing fees paid | ( | ||||||||||

| Proceeds from sale of common stock, net | |||||||||||

| Cash paid, in lieu of equity, for tax-withholding obligations | ( | ( | |||||||||

| Net cash (used in)/provided by financing activities | ( | ||||||||||

| Effect of foreign currency exchange on cash | ( | ||||||||||

| NET INCREASE/(DECREASE) IN CASH AND EQUIVALENTS | ( | ||||||||||

| CASH AND EQUIVALENTS AT BEGINNING OF PERIOD | |||||||||||

| CASH AND EQUIVALENTS AT END OF PERIOD | $ | $ | |||||||||

| SUPPLEMENTARY CASH FLOW INFORMATION: | |||||||||||

| Interest paid | $ | $ | |||||||||

| Income taxes paid, net | $ | $ | |||||||||

The accompanying notes are an integral part of these unaudited consolidated financial statements.

10

Catalent, Inc. and Subsidiaries

Notes to Unaudited Consolidated Financial Statements

1. BASIS OF PRESENTATION AND SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

Business

Catalent, Inc. ("Catalent" or the "Company") directly and wholly owns PTS Intermediate Holdings LLC ("Intermediate Holdings"). Intermediate Holdings directly and wholly owns Catalent Pharma Solutions, Inc. ("Operating Company"). The financial results of Catalent are comprised of the financial results of Operating Company and its subsidiaries on a consolidated basis.

Basis of Presentation

The accompanying unaudited consolidated financial statements have been prepared in accordance with generally accepted accounting principles in the United States ("GAAP") for interim financial information and with the instructions to Form 10-Q and Article 10 of Regulation S-X. Accordingly, they do not include all of the information and notes required by GAAP for complete financial statements. In the opinion of management, all adjustments (consisting of normal recurring adjustments) considered necessary for a fair presentation have been included. Operating results for the six months ended December 31, 2018 are not necessarily indicative of the results that may be expected for the year ending June 30, 2019. The consolidated balance sheet at June 30, 2018 has been derived from the audited consolidated financial statements at that date but does not include all of the information and footnotes required by GAAP for complete financial statements. For further information on the Company's accounting policies and footnotes, refer to the consolidated financial statements and footnotes thereto included in the Company’s Annual Report on Form 10-K for the year ended June 30, 2018 filed with the Securities and Exchange Commission (the "SEC").

In fiscal 2018, the Company engaged in a business reorganization to better align its internal business unit structure with its "Follow the Molecule" strategy and the increased focus on its biologics-related offerings. Under the revised structure, the Company created two new operating segments from the former Drug Delivery Solutions segment:

•Biologics and Specialty Drug Delivery, which encompasses biologic cell-line development and manufacturing, development and manufacturing services for blow-fill-seal unit doses, prefilled syringes, vials, and cartridges; analytical development and testing services for large molecules; and development and manufacturing for inhaled products for delivery via metered dose inhalers, dry powder inhalers, and intra-nasal sprays; and

•Oral Drug Delivery, which encompasses comprehensive formulation development, manufacturing, and analytical development capabilities using advanced processing technologies such as bioavailability enhancement, controlled release, particle size engineering, and taste-masking for solid oral-dose forms.

Foreign Currency Translation

The financial statements of the Company’s operations outside the U.S. are generally measured using the local currency as the functional currency. Adjustments to translate the assets and liabilities of these foreign operations into U.S. dollars are accumulated as a component of other comprehensive income/(loss) utilizing period-end exchange rates. In June 2018, as a result of the three-year cumulative consumer price index exceeding 100%, Argentina was classified as having a highly inflationary economy. Beginning on July 1, 2018, the Company accounts for its Argentine operations as highly inflationary.

Research and Development Costs

The Company expenses research and development costs as incurred. Costs incurred in connection with the development of new offerings and manufacturing process improvements are recorded within selling, general, and administrative expenses. Such research and development costs included in selling, general, and administrative expenses amounted to $1.0 million and $1.5 million for the three and six months ended December 31, 2018, respectively, and $1.5 million and $3.3 million for the three and six months ended December 31, 2017, respectively. Costs incurred in connection with research and

11

Recent Financial Accounting Standards

Recently Adopted Accounting Standards

In May 2014, the Financial Accounting Standard Board ("FASB") issued Accounting Standards Update ("ASU") 2014-09, Revenue from Contracts with Customers, which was codified as ASC 606 and superseded nearly all existing revenue-recognition guidance. The guidance’s core principle is that a company will recognize revenue when it transfers promised goods or services to customers in an amount that reflects the consideration to which the company expects to be entitled in exchange for those goods or services. In doing so, the guidance creates a five-step model that requires a company to exercise judgment when considering the terms of the contracts and all relevant facts and circumstances. The five steps require a company to identify customer contracts, identify the separate performance obligations, determine the transaction price, allocate the transaction price to the separate performance obligations, and recognize revenue when or as each performance obligation is satisfied. The guidance allows for either full retrospective adoption, where the standard is applied to all periods presented, or modified retrospective adoption, where the standard is applied only to the most current period presented in the financial statements. The Company adopted the guidance as of July 1, 2018 using the modified retrospective approach applied to contracts that were not completed as of that date. The Company recorded a cumulative effect adjustment to the fiscal 2019 opening balance of its accumulated deficit upon adoption of this guidance, which decreased beginning accumulated deficit by $15.1 million.

The following table provides the impact of adopting the guidance on the Company’s financial statements:

| Three months Ended December 31, 2018 | Six months Ended December 31, 2018 | ||||||||||||||||||||||||||||||||||

| (Dollars in millions) | As Reported | Effects of Change | Amount without Adoption of ASC 606 | As Reported | Effects of Change | Amount without Adoption of ASC 606 | |||||||||||||||||||||||||||||

| Net revenue | $ | $ | $ | $ | $ | $ | |||||||||||||||||||||||||||||

| Cost of sales | |||||||||||||||||||||||||||||||||||

| Gross margin | ( | ( | |||||||||||||||||||||||||||||||||

| Earnings from continuing operations before income taxes | ( | ( | |||||||||||||||||||||||||||||||||

| Income tax expense | ( | ( | ( | ( | |||||||||||||||||||||||||||||||

| Net earnings/(loss) | $ | $ | ( | $ | $ | $ | ( | $ | |||||||||||||||||||||||||||

The impact of ASC 606 on the Company's consolidated balance sheet is immaterial.

The adoption of ASC 606 resulted in three primary changes as compared to the previous revenue recognition guidance: (a) revenue from commercial product supply is recognized following successful completion of the required quality assurance process where it was previously recognized upon shipment of the product to the customer; (b) earlier recognition of revenue from certain commercial supply contract cancellations is recognized as variable consideration as the Company’s performance obligations are satisfied rather than only upon agreement of the amount with the customer; and (c) revenue from sourcing comparator drug product for clinical supply services is recorded net of the cost of procuring it rather than at full value with a corresponding expense. Refer to Note 2 for the Company's revenue recognition policy.

In March 2017, the FASB issued ASU 2017-07, Compensation—Retirement Benefits (Topic 715): Improving the Presentation of Net Periodic Pension Cost and Net Periodic Postretirement Benefit Cost, which requires entities to report the service cost component of the net periodic benefit cost in the same income statement line as other compensation costs arising from services rendered by employees during the reporting period. The other components of the net benefit costs will be presented in the income statement separately from the service cost and below the income from operations subtotal. The Company adopted this guidance as of July 1, 2018, on a retrospective basis, which had an effect on the consolidated statement of operations for the three and six months ended December 31, 2017. The following table summarizes the Company's As Previously Reported and As Adjusted changes to the consolidated statement of operations for the three and six months ended December 31, 2017:

12

| Three Months Ended December 31, 2017 | Six Months Ended December 31, 2017 | ||||||||||||||||||||||

| (Dollars in millions) | As Previously Reported | As Adjusted | As Previously Reported | As Adjusted | |||||||||||||||||||

| Selling, general, and administrative expenses | $ | $ | $ | $ | |||||||||||||||||||

| Operating earnings | |||||||||||||||||||||||

| Other expense, net | |||||||||||||||||||||||

In August 2017, the FASB issued ASU 2017-12, Derivatives and Hedging (Topic 815): Targeted Improvements to Accounting for Hedging Activities, which reduces the complexity of and simplifies the application of hedge accounting by issuers. The ASU is effective for fiscal years beginning after December 15, 2018 and interim periods within those years. Early adoption is permitted. The Company early adopted this guidance as of July 1, 2018 on a prospective basis. The adoption of this guidance was not material to the Company's consolidated financial statements.

In May 2017, the FASB issued ASU 2017-09, Compensation—Stock Compensation (Topic 718): Scope of Modification Accounting, which clarifies when an entity will apply modification accounting for changes to stock-based compensation arrangements. Modification accounting applies if the value, vesting conditions, or classification of an award changes. The Company adopted this guidance prospectively at the beginning of fiscal 2019. The adoption of this guidance was not material to the Company's consolidated financial statements.

In January 2017, the FASB issued ASU 2017-01, Business Combinations (Topic 805): Clarifying the Definition of a Business, which provides additional guidance on the definition of a business to assist entities with evaluating whether transactions should be accounted for as acquisitions of assets or businesses. The Company adopted this guidance prospectively at the beginning of fiscal 2019. The adoption of this guidance was not material to the Company's consolidated financial statements.

In January 2016, the FASB issued ASU 2016-01, Financial Instruments—Overall (Subtopic 825-10): Recognition and Measurement of Financial Assets and Financial Liabilities, which changes the accounting for equity investments and financial liabilities under the fair value option, and presentation and disclosure requirements for financial instruments. The ASU requires equity investments with readily determinable fair values to be measured at fair value and to recognize change in fair value in net earnings. The ASU is not applicable to equity investments accounted for under the equity method of accounting or those that result in consolidation of the investee. The Company adopted this guidance at the beginning of fiscal 2019. The adoption of this guidance was not material to the Company's consolidated financial statements.

New Accounting Standards Not Adopted as of December 31, 2018

In August 2018, the FASB issued ASU 2018-15, Intangibles—Goodwill and Other—Internal-Use Software (Subtopic 350-40): Customer's Accounting for Implementation Costs Incurred in a Cloud Computing Arrangement That Is a Service Contract, which aligns the requirements for capitalizing implementation costs incurred in a hosting arrangement that is a service contract with the requirements for capitalizing implementation costs incurred to develop or obtain internal-use software. The ASU will be effective for fiscal years beginning after December 15, 2019 and interim periods within those fiscal years and allows for either a retrospective or prospective application. The Company is currently evaluating the impact of adopting this guidance on its consolidated financial statements.

In February 2018, the FASB issued ASU 2018-02, Income Statement—Reporting Comprehensive Income (Topic 220): Reclassification of Certain Tax Effects from Accumulated Other Comprehensive Income, which permits an entity to reclassify to retained earnings the stranded tax effects caused by the Tax Cuts and Jobs Act of 2017 on items within accumulated other comprehensive income/(loss). The ASU will be effective for fiscal years beginning after December 15, 2018 and interim periods within those years. Early adoption is permitted. The Company is currently evaluating the impact of adopting this guidance on its consolidated financial statements.

In June 2016, the FASB issued ASU 2016-13, Financial Instruments—Credit Losses (Topic 326): Measurement of Credit Losses on Financial Instruments, which introduces a new accounting model Credit Expected Credit Losses model ("CECL"). CECL requires earlier recognition of credit losses, while also providing additional transparency about credit risk. The CECL model utilizes a lifetime expected credit loss measurement objective for the recognition of credit losses for receivables at the time the financial asset is originated or acquired. The expected credit losses are adjusted each period for changes in expected lifetime credit losses. This model replaces the multiple existing impairment models in current GAAP, which generally require that a loss be incurred before it is recognized. The new standard will also apply to receivables arising from revenue transactions such as contract assets and accounts receivables. The ASU will be effective for fiscal years beginning after December 15, 2019. The Company is currently evaluating the impact of adopting this guidance on its consolidated financial statements.

13

2. REVENUE RECOGNITION

The Company recognizes revenue in accordance with ASC 606. The Company generally earns its revenue by supplying goods or providing services under contracts with its customers in three primary revenue streams: manufacturing and commercial product supply, development services, and clinical supply services. The Company measures the revenue from customers based on the consideration specified in its contracts, excluding any sales incentive or amount collected on behalf of a third party.

The company generally expenses sales commissions as incurred because either the amortization period is one year or less, or the balance with an amortization period greater than one year is not material.

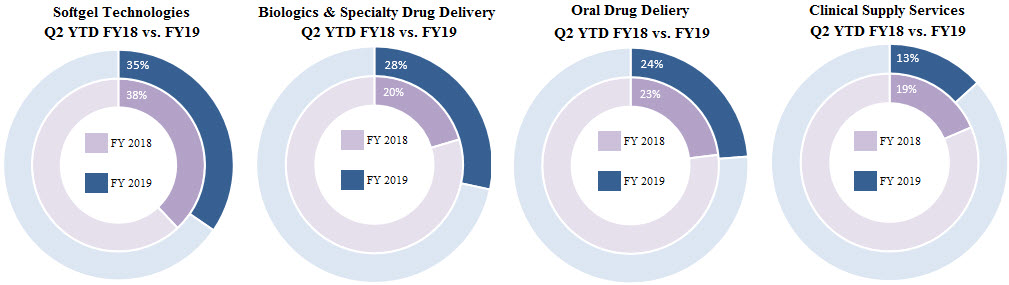

The following tables allocate revenue for the three and six months ended December 31, 2018 by type of activity and reporting segment (in millions):

| Three months ended December 31, 2018 | Softgel Technologies | Biologics & Specialty Drug Delivery | Oral Drug Delivery | Clinical Supply Services | Total | ||||||||||||||||||||||||

| Manufacturing & commercial product supply | $ | $ | $ | $ | $ | ||||||||||||||||||||||||

| Development services | |||||||||||||||||||||||||||||

| Clinical supply services | |||||||||||||||||||||||||||||

| Total | $ | $ | $ | $ | $ | ||||||||||||||||||||||||

| Inter-segment revenue elimination | ( | ||||||||||||||||||||||||||||

| Combined net revenue | $ | ||||||||||||||||||||||||||||

| Six months ended December 31, 2018 | Softgel Technologies | Biologics & Specialty Drug Delivery | Oral Drug Delivery | Clinical Supply Services | Total | ||||||||||||||||||||||||

| Manufacturing & commercial product supply | $ | $ | $ | $ | $ | ||||||||||||||||||||||||

| Development services | |||||||||||||||||||||||||||||

| Clinical supply services | |||||||||||||||||||||||||||||

| Total | $ | $ | $ | $ | $ | ||||||||||||||||||||||||

| Inter-segment revenue elimination | ( | ||||||||||||||||||||||||||||

| Combined net revenue | $ | ||||||||||||||||||||||||||||

The following table allocates revenue by the location where the goods were made or the service performed:

| (Dollars in millions) | Three months ended December 31, 2018 | Six months ended December 31, 2018 | ||||||||||||

| United States | $ | $ | ||||||||||||

| Europe | ||||||||||||||

| International Other | ||||||||||||||

| Elimination of revenue attributable to multiple locations | ( | ( | ||||||||||||

| Total | $ | $ | ||||||||||||

14

Manufacturing & Commercial Product Supply Revenue

Manufacturing and commercial product supply revenue consists of revenue earned by manufacturing products supplied to customers under long-term commercial supply arrangements. The Company recognizes revenue for manufacturing and supplying commercial products as control is transferred to the customer, which is measured based on product that has successfully completed contractually required quality assurance process. Revenue is measured based on the amount of consideration the Company expects to receive in exchange for providing these products and services. The contractual performance obligation generally includes manufacture and the completion of product quality release testing procedures specified in the contract. These activities are interdependent and thus are considered to be a single combined performance obligation. Payment is typically due 30 to 90 days after the goods are shipped to the customer based on the payment terms set forth in the applicable customer agreement.

Development Services Revenue

Development services contracts generally take the form of short-term, fee-for-service arrangements. Performance obligations vary, but frequently include (1) the delivery of a formulation report, analytical and stability testing report, or other report on product- or molecule-based studies or (2) the manufacture of products under development or otherwise not intended for commercial sale. The transaction prices for these arrangements include fixed consideration of the amounts stated in the contracts for each promised good or service, which are generally considered to be separate performance obligations. The Company recognizes revenue when or as control of each individual performance obligation is transferred to the customer and exercises judgment in determining the timing of revenue recognition by analyzing the point in time or period over which the customer has the ability to direct the use of and obtain substantially all of the remaining benefits of the arrangement. Control generally transfers to the customer when services have been completed or the customer has accepted the product or service deliverable and the Company has right to payment based on the terms of the agreement.

In certain arrangements, the Company recognizes revenue over time as the Company satisfies performance obligations. Satisfaction of the performance obligations is measured using an output method measure of progress based on effort expended by the Company. In other arrangements, revenue is recognized when the customer has taken legal title to or accepted the product or service deliverable and the Company has a right to payment based on the terms of the arrangement.

Development services contracts may also include certain success-based milestone payments for completed performance obligations, such as regulatory approval and product validation prior to the commencement of commercial supply. Revenue associated with developmental milestones is considered variable consideration and is typically recognized when the success-based milestone is achieved, and no significant revenue reversal is anticipated.

The Company allocates consideration to each performance obligation based on the relative selling price. Payment is typically due 30 to 90 days following the completion of services provided to the customer based on the payment terms set forth in the applicable customer agreement. Certain development service arrangements require a portion of the contract consideration to be received in advance at the commencement of the contract and is initially recorded as a contract liability.

Clinical Supply Services Revenue

Clinical supply services contracts generally take the form of fee-for-service arrangements. Performance obligations for clinical supply services revenue typically include a combination of the following services: the manufacturing, packaging, storage, distribution, destruction, and inventory management of customer clinical trials materials. Performance obligations can also include the sourcing of comparator drug products on behalf of customers to be used in clinical trials to compare performance with the drug under clinical investigation. In certain arrangements, the Company recognizes revenue over time when the Company satisfies performance obligations. Satisfaction of the performance obligations is measured using an output method measure of progress based on effort expended by the Company. In other arrangements, revenue is recognized when the customer has taken legal title or accepted the product or service deliverable and the Company has right to payment based on the terms of the arrangement. Payment is typically due 30 to 90 days following the completion of services provided to the customer based on the payment terms set forth in the applicable customer agreement.

The Company records revenue for comparator sourcing arrangements on a net basis because it is acting as an agent that does not control the product or service before it is transferred to the customer. Payment for comparator sourcing activity is typically received in advance at the commencement of the contract and is initially recorded as a contract liability.

Contract Liabilities

Contract liabilities relate to cash consideration that the Company receives in advance of satisfying the related performance obligations. Changes in the contractual liabilities balance during the six months ended December 31, 2018 are as follows:

15

| (Dollars in millions) | ||||||||

| Contract liability | ||||||||

| Balance at June 30, 2018 | $ | |||||||

| Balance at December 31, 2018 | $ | |||||||

| Revenue recognized in the period from: | ||||||||

| Amounts included in contracts liability at the beginning of the period | $ | |||||||

Remaining Performance Obligations

3. BUSINESS COMBINATIONS

Juniper Pharmaceuticals Acquisition

On August 14, 2018, Operating Company acquired Juniper Pharmaceuticals, Inc. , a Delaware corporation ("Juniper") through a tender offer and back-end merger, pursuant to the terms of an agreement and plan of merger (the "Juniper Merger Agreement"), and Juniper became a wholly owned subsidiary of Operating Company. Under the terms of the Juniper Merger Agreement, all outstanding options to purchase Juniper shares were canceled in exchange for cash equal to the product of the number of Juniper shares subject to the option and the difference between the price per share paid in the tender offer and the exercise price. Similarly, all outstanding restricted stock units in respect of Juniper shares were canceled in exchange for cash equal to the product of the number of units and the price per share paid in the tender offer. Juniper has expertise in formulation development and supply and augments the Company's pre-existing portfolio of solid-state screening, pre-formulation, formulation, analytical, and bioavailability enhancement solutions, including the development of drug products produced using spray-dried dispersion, with integrated development, analytical, and clinical manufacturing. Juniper also owns the ex-U.S. rights to and supplies for sale to its licensee of such rights CRINONE®, a reproductive therapy. The primary operations of the acquired business are located in owned facilities aggregating 38,000 square feet in Nottingham, U.K. and is now included in the Oral Drug Delivery segment. Results of this segment include the results of Juniper for the period since the acquisition.

The aggregate purchase consideration, net of cash acquired, was $127.5 million, which was funded by cash on hand. As a result of the preliminary fair value allocations, the Company recognized intangible assets of $69.0 million and $10.0 million for product relationships and customer relationships, respectively. The remainder of the preliminary fair value was allocated to tangible assets acquired and goodwill. The fair value allocation is expected to be completed upon finalization of an independent appraisal over the next several months, but no later than one year from the acquisition date.

4. GOODWILL

The following table summarizes the changes between June 30, 2018 and December 31, 2018 in the carrying amount of goodwill in total and by reporting segment:

| (Dollars in millions) | Softgel Technologies | Biologics and Specialty Drug Delivery | Oral Drug Delivery | Clinical Supply Services | Total | ||||||||||||||||||||||||

| Balance at June 30, 2018 | $ | $ | $ | $ | $ | ||||||||||||||||||||||||

| Additions | |||||||||||||||||||||||||||||

| Foreign currency translation adjustments | ( | ( | ( | ( | ( | ||||||||||||||||||||||||

| Balance at December 31, 2018 | $ | $ | $ | $ | $ | ||||||||||||||||||||||||

16

5. DEFINITE-LIVED LONG-LIVED ASSETS

The Company’s definite-lived long-lived assets include property, plant, and equipment as well as intangible assets with definite lives. Refer to Note 16, Supplemental Balance Sheet Information for details related to property, plant, and equipment.

The details of other intangibles, net as of December 31, 2018 and June 30, 2018 are as follows:

| (Dollars in millions) | Weighted Average Life | Gross Carrying Value | Accumulated Amortization | Net Carrying Value | |||||||||||||||||||

| December 31, 2018 | |||||||||||||||||||||||

| Amortized intangibles: | |||||||||||||||||||||||

| Core technology | $ | $ | ( | $ | |||||||||||||||||||

| Customer relationships | ( | ||||||||||||||||||||||

| Product relationships | ( | ||||||||||||||||||||||

| Total intangible assets | $ | $ | ( | $ | |||||||||||||||||||

The increases in customer relationships and product relationships as of December 31, 2018 are associated with the acquisition of Juniper in August 2018.

| (Dollars in millions) | Weighted Average Life | Gross Carrying Value | Accumulated Amortization | Net Carrying Value | |||||||||||||||||||

| June 30, 2018 | |||||||||||||||||||||||

| Amortized intangibles: | |||||||||||||||||||||||

| Core technology | $ | $ | ( | $ | |||||||||||||||||||

| Customer relationships | ( | ||||||||||||||||||||||

| Product relationships | ( | ||||||||||||||||||||||

| Total intangible assets | $ | $ | ( | $ | |||||||||||||||||||

Amortization expense was $19.5 million and $37.7 million for the three and six months ended December 31, 2018, respectively, and $16.1 million and $27.5 million for the three and six months ended December 31, 2017, respectively. Future amortization expense for the next five fiscal years is estimated to be:

| (Dollars in millions) | Remainder Fiscal 2019 | 2020 | 2021 | 2022 | 2023 | 2024 | |||||||||||||||||||||||||||||

| Amortization expense | $ | $ | $ | $ | $ | $ | |||||||||||||||||||||||||||||

17

6. LONG-TERM OBLIGATIONS AND SHORT-TERM BORROWINGS

Long-term obligations and short-term borrowings consist of the following at December 31, 2018 and June 30, 2018:

| (Dollars in millions) | Maturity as of December 31, 2018 | December 31, 2018 | June 30, 2018 | ||||||||||||||

| Senior Secured Credit Facilities | |||||||||||||||||

| Term loan facility U.S. dollar-denominated | May 2024 | $ | $ | ||||||||||||||

| Term loan facility euro-denominated | May 2024 | ||||||||||||||||

| Euro-denominated 4.75% Senior Notes due 2024 | December 2024 | ||||||||||||||||

| U.S. dollar-denominated 4.875% Senior Notes due 2026 | January 2026 | ||||||||||||||||

| Deferred purchase consideration | October 2021 | ||||||||||||||||

| $200 million revolving credit facility | May 2022 | ||||||||||||||||

| Capital lease obligations | 2020 to 2032 | ||||||||||||||||

| Other obligations | 2018 to 2019 | ||||||||||||||||

| Total | |||||||||||||||||

| Less: Current portion of long-term obligations and other short-term borrowings | |||||||||||||||||

| Long-term obligations, less current portion | $ | $ | |||||||||||||||

Senior Secured Credit Facilities and Third Amendment

On October 18, 2017, Operating Company completed Amendment No. 3 (the "Third Amendment") to its Amended and Restated Credit Agreement, dated as of May 20, 2014 (as subsequently amended, the "Credit Agreement"), governing the senior secured credit facilities that provide U.S. dollar, denominated term loans, euro-denominated term loans, and a revolving credit facility. The Third Amendment lowered the interest rate on U.S. dollar-denominated and euro-denominated term loans and the revolving credit facility and extended the maturity dates on the senior secured credit facilities by three years. From the Third Amendment, the applicable rate for U.S. dollar-denominated term loans is LIBOR (the London Interbank Offered Rate, subject to a floor of 1.00 %) plus 2.25 %, and the applicable rate for euro-denominated term loans is Euribor (the Euro Interbank Offered Rate published by the European Money Markets Institute, subject to a floor of 1.00 %) plus 1.75 %. The applicable rate for the revolving loans was initially set at LIBOR plus 2.25 %, and such rate can additionally be reduced to LIBOR plus 2.00 % in future periods based on a measure of Operating Company's total leverage ratio. The term loans and revolving loans will now mature in May 2024 and May 2022, respectively.

On July 27, 2018, the Company completed an underwritten public equity offering (the "2018 Equity Offering") and used the net proceeds coupled with cash on hand to repay $450.0 million of the outstanding borrowings under its U.S. dollar-denominated term loans on July 31, 2018.

Euro-denominated 4.75% Senior Notes due 2024

On December 9, 2016, Operating Company completed a private offering of €380.0 million aggregate principal amount of 4.75% Senior Notes due 2024 (the "Euro Notes"). The Euro Notes are fully and unconditionally guaranteed, jointly and severally, by all of the wholly owned U.S. subsidiaries of Operating Company that guarantee its senior secured credit facilities. The Euro Notes were offered in the United States to qualified institutional buyers in reliance on Rule 144A under the Securities Act of 1933, as amended (the "Securities Act") and outside the United States only to non-U.S. investors pursuant to Regulation S under the Securities Act. The Euro Notes will mature on December 15, 2024, bear interest at the rate of 4.75 % per annum and are payable semi-annually in arrears on June 15 and December 15 of each year.

18

U.S. Dollar-denominated 4.875% Senior Notes due 2026

On October 18, 2017, Operating Company completed a private offering (the "Debt Offering") of $450.0 million aggregate principal amount of 4.875% Senior Notes due 2026 (the "USD Notes"). The USD Notes are fully and unconditionally guaranteed, jointly and severally, by all of the wholly owned U.S. subsidiaries of Operating Company that guarantee its senior secured credit facilities. The USD Notes were offered in the United States to qualified institutional buyers in reliance on Rule 144A under the Securities Act and outside the United States only to non-U.S. investors pursuant to Regulation S under the Securities Act. The USD Notes will mature on January 15, 2026, bear interest at the rate of 4.875 % per annum, and are payable semi-annually in arrears on January 15 and July 15 of each year, beginning on July 15, 2018. The net proceeds of the Debt Offering, after payment of the initial purchasers' discount and related fees and expenses, were used to fund a portion of the consideration for the Catalent Indiana acquisition due at its closing.

Deferred Purchase Consideration

In connection with the acquisition of Catalent Indiana in October 2017, $200.0 million of the $950.0 million aggregate nominal purchase price is payable in $50

Bridge Loan Facility

On September 18, 2017, contemporaneous with the Company entering into the agreement to acquire Catalent Indiana, Operating Company entered into a debt commitment letter with Morgan Stanley Senior Funding, Inc., JP Morgan Chase Bank, N.A., Royal Bank of Canada, RBC Capital Markets, Bank of America, N.A., and Merrill Lynch, Pierce, Fenner & Smith Incorporated, as commitment parties. Pursuant to the debt commitment letter and subject to its terms and conditions, the commitment parties agreed to provide a senior unsecured bridge loan facility (the "Bridge Facility") of up to $700.0 million in the aggregate for the purpose of providing any back-up financing necessary to fund a portion of the consideration to be paid in the acquisition and related fees, costs, and expenses (the "Bridge Loan Commitment"). In connection with entering into the Bridge Facility, Operating Company incurred $6.1 million of associated fees. Operating Company did not draw on it to fund the acquisition and the Company expensed the $6.1 million in the second quarter of fiscal 2018 as part of other expense, net and the facility was closed.

Debt Covenants

Senior Secured Credit Facilities

The Credit Agreement contains a number of covenants that, among other things, restrict, subject to certain exceptions, Operating Company’s (and Operating Company’s restricted subsidiaries’) ability to incur additional indebtedness or issue certain preferred shares; create liens on assets; engage in mergers and consolidations; sell assets; pay dividends and distributions or repurchase capital stock; repay subordinated indebtedness; engage in certain transactions with affiliates; make investments, loans, or advances; make certain acquisitions; enter into sale and leaseback transactions; amend material agreements governing Operating Company’s subordinated indebtedness; and change Operating Company’s lines of business.

The Credit Agreement also contains change-of-control provisions and certain customary affirmative covenants and events of default. The revolving credit facility requires compliance with a net leverage covenant when there is a 30% or more draw outstanding at a period end. As of December 31, 2018, Operating Company was in compliance with all material covenants under the Credit Agreement.

Subject to certain exceptions, the Credit Agreement permits Operating Company and its restricted subsidiaries to incur certain additional indebtedness, including secured indebtedness. None of Operating Company’s non-U.S. subsidiaries or Puerto Rico subsidiaries is a guarantor of the loans.

Under the Credit Agreement, Operating Company’s ability to engage in certain activities such as incurring certain additional indebtedness, making certain investments, and paying certain dividends is tied to ratios based on Adjusted EBITDA (which is defined as “Consolidated EBITDA” in the Credit Agreement). Adjusted EBITDA is based on the definitions in the Credit Agreement, is not defined under GAAP, and is subject to important limitations.

The Euro Notes and the USD Notes

The Indentures governing the Euro Notes and the USD Notes (the "Indentures") contain certain covenants that, among other things, limit the ability of Operating Company and its restricted subsidiaries to incur or guarantee more debt or issue certain preferred shares; pay dividends on, repurchase, or make distributions in respect of their capital stock or make other

19

restricted payments; make certain investments; sell certain assets; create liens; consolidate, merge, sell; or otherwise dispose of all or substantially all of their assets; enter into certain transactions with their affiliates, and designate their subsidiaries as unrestricted subsidiaries. These covenants are subject to a number of exceptions, limitations, and qualifications as set forth in the Indentures. The Indentures also contain customary events of default including, but not limited to, nonpayment, breach of covenants, and payment or acceleration defaults in certain other indebtedness of Operating Company or certain of its subsidiaries. Upon an event of default, either the holders of at least 30% in principal amount of each of the then-outstanding Euro Notes or the then-outstanding USD Notes, or either of the Trustees under the Indentures, may declare the applicable notes immediately due and payable; or in certain circumstances, the applicable notes will become automatically immediately due and payable. As of December 31, 2018, Operating Company was in compliance with all material covenants under the Indentures.

Fair Value of Debt Instruments

The estimated fair value of the senior secured credit facility, a Level 2 fair-value estimate, is based on the quoted market prices for the same or similar issues or on the current rates offered for debt of the same remaining maturities and considers collateral, if any. The estimated fair value of the Euro and USD Notes, a Level 1 fair-value estimate, is based on the quoted market prices of the instruments. The carrying amounts and the estimated fair values of financial instruments as of December 31, 2018 and June 30, 2018 are as follows:

| December 31, 2018 | June 30, 2018 | |||||||||||||||||||||||||

| (Dollars in millions) | Fair Value Measurement | Carrying Value | Estimated Fair Value | Carrying Value | Estimated Fair Value | |||||||||||||||||||||

| Euro-denominated 4.75% Senior Notes | Level 1 | $ | $ | $ | $ | |||||||||||||||||||||

| U.S. Dollar-denominated 4.875% Senior Notes | Level 1 | |||||||||||||||||||||||||

| Senior Secured Credit Facilities & Other | Level 2 | |||||||||||||||||||||||||

| Total | $ | $ | $ | $ | ||||||||||||||||||||||

7. EARNINGS PER SHARE

The reconciliations between basic and diluted earnings per share attributable to Catalent common shareholders for the three and six months ended December 31, 2018 and 2017, respectively, are as follows (in millions, except share and per share data):

| Three Months Ended December 31, | Six Months Ended December 31, | ||||||||||||||||||||||

| 2018 | 2017 | 2018 | 2017 | ||||||||||||||||||||

| Net earnings/(loss) | $ | $ | ( | $ | $ | ( | |||||||||||||||||

| Weighted average shares outstanding | |||||||||||||||||||||||

| Dilutive securities issuable-stock plans | |||||||||||||||||||||||

| Total weighted average diluted shares outstanding | |||||||||||||||||||||||

| Earnings/(loss) per share: | |||||||||||||||||||||||

| Basic | $ | $ | ( | $ | $ | ( | |||||||||||||||||

| Diluted | $ | $ | ( | $ | $ | ( | |||||||||||||||||

The computation of diluted earnings per share for the three and six months ended December 31, 2018 excludes the effect of the potential common shares issuable under employee-held stock options and restricted stock units of approximately 1.1 million and 1.0 million shares, respectively, because they are anti-dilutive. The computation of diluted earnings per share for the three and six months ended December 31, 2017 excludes the maximum effect of the potential common shares issuable under employee-held stock options and restricted stock units of approximately 2.6 million shares, and excludes restricted share awards of 2.1 million shares, because the Company had a net loss for the period and the effect would therefore be anti-dilutive.

20

8. OTHER EXPENSE, NET

The components of other expense, net for the three and six months ended December 31, 2018 and 2017 are as follows:

| Three Months Ended December 31, | Six Months Ended December 31, | ||||||||||||||||||||||

| (Dollars in millions) | 2018 | 2017 | 2018 | 2017 | |||||||||||||||||||

| Other expense, net | |||||||||||||||||||||||

Debt refinancing costs (1) | |||||||||||||||||||||||

Foreign currency (gains) and losses (2) | |||||||||||||||||||||||

| Other | ( | ||||||||||||||||||||||

| Total other expense, net | $ | $ | $ | $ | |||||||||||||||||||

(1) The expense in the six months ended December 31, 2018 includes a write-off of $4.2 million of previously capitalized financing charges related to the Company's U.S. dollar term loan under its senior secured credit facility. The prior-year debt refinancing costs include financing charges related to the offering of the USD Notes and the Third Amendment and also include a $6.1 million charge for commitment fees paid during the first quarter of fiscal 2018 on the Bridge Facility.

(2) Foreign currency remeasurement (gains) and losses include both cash and non-cash transactions.

9. RESTRUCTURING AND OTHER COSTS

Restructuring Costs

From time to time, the Company has implemented plans to restructure certain operations, both domestically and internationally. The restructuring plans focused on various aspects of operations, including closing and consolidating certain manufacturing operations, rationalizing headcount and aligning operations in a strategic and more cost-efficient structure. In addition, the Company may incur restructuring charges in the future in cases where a material change in the scope of operation with its business occurs. Employee-related costs consist primarily of severance costs and also include outplacement services provided to employees who have been involuntarily terminated and duplicate payroll costs during transition periods. Facility exit and other costs consist of accelerated depreciation, equipment relocation costs and costs associated with planned facility expansions and closures to streamline Company operations.

Other Costs/(Income)

Other costs/(income) includes settlement charges, net of any insurance recoveries, related to the probable resolution of certain customer claims related to a previous temporary suspension of operations at a softgel manufacturing facility.

The following table summarizes the significant costs recorded within restructuring and other costs:

| Three Months Ended December 31, | Six Months Ended December 31, | ||||||||||||||||||||||

(Dollars in millions) | 2018 | 2017 | 2018 | 2017 | |||||||||||||||||||

| Restructuring costs: | |||||||||||||||||||||||

Employee-related reorganization | $ | $ | $ | $ | |||||||||||||||||||

Facility exit and other costs | ( | ( | |||||||||||||||||||||

| Total restructuring costs | $ | $ | $ | $ | |||||||||||||||||||

Other - customer claims, net of insurance recoveries | ( | ( | |||||||||||||||||||||

| Total restructuring and other costs | $ | $ | $ | $ | |||||||||||||||||||

10. DERIVATIVE INSTRUMENTS AND HEDGING ACTIVITIES

21

the translation gains or losses are reported in the statement of operations. The following table includes net investment hedge activity during the three and six months ended December 31, 2018 and 2017.

| Three Months Ended December 31, | Six Months Ended December 31, | |||||||||||||||||||

| (Dollars in millions) | 2018 | 2017 | 2018 | 2017 | ||||||||||||||||

Unrealized foreign exchange gain/(loss) within other comprehensive income | $ | $ | ( | $ | $ | ( | ||||||||||||||

Unrealized foreign exchange gain/(loss) within statement of operations | $ | $ | ( | $ | $ | ( | ||||||||||||||

11. INCOME TAXES

U.S. Tax Reform

On December 22, 2017, the U.S. government enacted wide-ranging tax legislation, the Tax Cuts and Jobs Act (the "2017 Tax Act"). The 2017 Tax Act significantly revises U.S. tax law by, among other provisions, (a) lowering the applicable U.S. federal statutory income tax rate from 35 % to 21 %, (b) creating a partial territorial tax system that includes imposing a mandatory one-time transition tax on previously deferred foreign earnings, (c) creating provisions regarding the (1) Global Intangible Low Tax Income ("GILTI"), (2) the Foreign Derived Intangible Income ("FDII") deduction, and (3) the Base Erosion Anti-Abuse Tax ("BEAT"), and (d) eliminating or reducing certain income tax deductions, such as interest expense, executive compensation expenses, and certain employee expenses. While the impact of the mandatory one-time transition tax was recognized in fiscal 2018, the remaining provisions are effective for fiscal years after 2018.

ASC 740, Income Taxes ("ASC 740") requires the effects of changes in tax laws to be recognized in the period in which the legislation is enacted. However, due to the complexity and significance of the 2017 Tax Act’s provisions, the SEC staff issued Staff Accounting Bulletin No. 118 ("SAB 118"), which allowed companies to record the tax effects of the 2017 Tax Act on a provisional basis based on a reasonable estimate and then, if necessary, subsequently adjust such amounts during a limited measurement period as more information became available. The measurement period ended December 22, 2018 and our accounting for the tax effects of the Act through December 31, 2018 is complete as of December 31, 2018. For the three and six months ended December 31, 2018, the Company recorded a net benefit of $6.9 42.5 million previously recorded during fiscal 2018, to $35.6 million. This reduction was primarily related to additional foreign tax credit benefits associated with the mandatory transition tax charge for deemed repatriation of deferred foreign income. There were no other changes recorded to the tax provision related to the 2017 Tax Act. The Company continues to evaluate the potential impact of all provisions of the 2017 Tax Act, as the U.S. Treasury Department has and is expected to continue issuing guidance related to the 2017 Tax Act during the Company’s fiscal year 2019.

As noted above, the 2017 Tax Act subjects a US Company to tax on GILTI earned by certain foreign subsidiaries. The Company will account for GILTI in the year the tax is incurred as a period cost.

Other Tax Matters

The Company accounts for income taxes in accordance with ASC 740. Generally, fluctuations in the effective tax rate are primarily due to changes in U.S. and non-U.S. pretax income resulting from the Company’s business mix and changes in the tax impact of special items and other discrete tax items, which may have unique tax implications depending on the nature of the item. Such discrete items include, but are not limited to, changes in foreign statutory tax rates, the amortization of certain assets, and the tax impact of changes in its ASC 740 unrecognized tax benefit reserves. In the normal course of business, the Company is subject to examination by taxing authorities around the world, including such major jurisdictions as the United States, Germany, France, and the United Kingdom. The Company is no longer subject to examinations by the relevant tax authorities for years prior to fiscal year 2009. Under the terms of the 2007 purchase agreement by which the stockholders at that time acquired their interest in the Company, the Company is indemnified by its former owner for tax liabilities that may arise after the 2007 purchase that relate to tax periods prior to April 10, 2007. The indemnification agreement applies to, among other taxes, any and all federal, state, and international income-based taxes as well as related interest and penalties. As of December 31, 2018 and June 30, 2018, approximately $0.6 million and $0.7 million, respectively, of unrecognized tax benefit are subject to indemnification by the Company's former owner.

22

ASC 740 includes guidance on the accounting for uncertainty in income taxes recognized in the financial statements. This standard provides that a tax benefit from an uncertain tax position may be recognized when it is more likely than not that the position will be sustained upon examination, including resolution of any related appeal or litigation process, based on the technical merits. As of December 31, 2018 and June 30, 2018, the Company had a total of $2.0 million and $2.2 million of unrecognized tax benefits, respectively.

As of December 31, 2018 and June 30, 2018, the Company had a total of $3.7 million and $4.1 million, respectively, of uncertain tax positions (including accrued interest and penalties). As of these dates, $2.0 million and $2.2 million, respectively, represent the amount of unrecognized tax benefits, which, if recognized, would favorably affect the effective income tax rate. The Company recognizes interest and penalties related to uncertain tax positions as a component of income tax expense. As of December 31, 2018 and June 30, 2018, the Company has approximately $1.7 million and $2.0 million, respectively, of accrued interest and penalties related to uncertain tax positions. As of these dates, the portion of such interest and penalties subject to indemnification by its former owner is $1.3 million and $1.6 million, respectively.

12. EMPLOYEE RETIREMENT BENEFIT PLANS

Components of the Company’s net periodic benefit costs are as follows:

| Three Months Ended December 31, | Six Months Ended December 31, | ||||||||||||||||||||||

| (Dollars in millions) | 2018 | 2017 | 2018 | 2017 | |||||||||||||||||||

| Components of net periodic benefit cost: | |||||||||||||||||||||||

| Service cost | $ | $ | $ | $ | |||||||||||||||||||

| Interest cost | |||||||||||||||||||||||

| Expected return on plan assets | ( | ( | ( | ( | |||||||||||||||||||

Amortization (1) | |||||||||||||||||||||||

| Net amount recognized | $ | $ | $ | $ | |||||||||||||||||||

(1) Amount represents the amortization of unrecognized actuarial gains/(losses) .

13. EQUITY AND ACCUMULATED OTHER COMPREHENSIVE INCOME/(LOSS)

Description of Capital Stock

The Company is authorized to issue 1,000,000,000 shares of common stock, par value $0.01 per share ("Common Stock"), and 100,000,000 shares of preferred stock, par value $0.01 per share. Under the Company's certificate of incorporation, each share of Common Stock has one vote, and the Common Stock votes together as a single class.

Public Stock Offering

On July 27, 2018, the Company completed the 2018 Equity Offering, a public offering in which the Company sold 11.4 million shares, including the underwriters' over-allotment option, of Common Stock at a price of $40.24 per share, before underwriting discounts and commissions. Net of these discounts and commissions and other offering expenses, the Company obtained total net proceeds from the 2018 Equity Offering, including the over-allotment exercise, of $445.5 million. The net proceeds of the 2018 Equity Offering were used to repay a corresponding portion of the outstanding borrowings under Operating Company's U.S. dollar-denominated term loans.

On September 29, 2017, the Company completed a public offering (the "2017 Equity Offering"), pursuant to which the Company sold 7.4 million shares, including the underwriters' over-allotment option, of Common Stock at a price of $39.10 per share, before underwriting discounts and commissions. Net of these discounts and commissions and other offering expenses, the Company obtained total net proceeds from the 2017 Equity Offering, including the over-allotment exercise, of $277.8 million. The net proceeds of the 2017 Equity Offering were used to fund a portion of the consideration for the Catalent Indiana acquisition due at its closing.

23

Outstanding Stock

Shares outstanding include shares of unvested restricted stock. Unvested restricted stock included in reportable shares outstanding was 0.7 million shares as of December 31, 2018. Shares of unvested restricted stock are excluded from our calculation of basic weighted average shares outstanding, but their dilutive impact is added back in the calculation of diluted weighted average shares outstanding, except when the effect would be anti-dilutive.

Stock Repurchase Program

On October 29, 2015, the Company’s Board of Directors authorized a share repurchase program to use up to $100.0 million to repurchase shares of outstanding Common Stock. Under the program, the Company is authorized to repurchase shares through open market purchases, privately negotiated transactions, or otherwise as permitted by applicable federal securities laws. There has been no purchase pursuant to this program as of December 31, 2018.

Accumulated Other Comprehensive Income/(loss)

The components of the changes in the cumulative translation adjustment, minimum pension liability, and available for sale investment for the three and six months ended December 31, 2018 and 2017 are presented below.

| Three Months Ended December 31, | Six Months Ended December 31, | ||||||||||||||||||||||

| (Dollars in millions) | 2018 | 2017 | 2018 | 2017 | |||||||||||||||||||

| Foreign currency translation adjustments: | |||||||||||||||||||||||

| Net investment hedge | $ | $ | ( | $ | $ | ( | |||||||||||||||||

| Long-term intercompany loans | ( | ( | ( | ||||||||||||||||||||

| Translation adjustments | ( | ( | ( | ||||||||||||||||||||

| Total foreign currency translation adjustment, pretax | ( | ( | ( | ||||||||||||||||||||

| Tax expense/(benefit) | ( | ||||||||||||||||||||||

| Total foreign currency translation adjustment, net of tax | $ | ( | $ | ( | $ | ( | $ | ||||||||||||||||

| Net change in minimum pension liability | |||||||||||||||||||||||

| Net gain recognized during the period | $ | $ | |||||||||||||||||||||

| Total pension liability, pretax | |||||||||||||||||||||||

| Tax expense | |||||||||||||||||||||||

| Net change in minimum pension liability, net of tax | $ | $ | $ | $ | |||||||||||||||||||

| Net change in available for sale investment: | |||||||||||||||||||||||

| Net loss recognized during the period | $ | $ | ( | ( | |||||||||||||||||||

| Total available for sale investment, pretax | ( | ( | |||||||||||||||||||||

| Tax benefit | ( | ( | |||||||||||||||||||||

| Net change in available for sale investment, net of tax | $ | $ | ( | $ | $ | ( | |||||||||||||||||

For the three months ended December 31, 2018, the changes in accumulated other comprehensive income/(loss), net of tax by component are as follows:

| (Dollars in millions) | Foreign Exchange Translation Adjustments | Pension and Liability Adjustments | Available for Sale Investment Adjustments | Total | |||||||||||||||||||

| Balance at September 30, 2018 | $ | ( | $ | ( | $ | ( | $ | ( | |||||||||||||||

| Other comprehensive income/(loss) before reclassifications | ( | ( | |||||||||||||||||||||

| Amounts reclassified from accumulated other comprehensive income/(loss) | |||||||||||||||||||||||

| Net current period other comprehensive income/(loss) | ( | ( | |||||||||||||||||||||

| Balance at December 31, 2018 | $ | ( | $ | ( | $ | ( | $ | ( | |||||||||||||||

24

For the six months ended December 31, 2018, the changes in accumulated other comprehensive income/(loss), net of tax by component are as follows:

| (Dollars in millions) | Foreign Exchange Translation Adjustments | Pension and Liability Adjustments | Available for Sale Investment Adjustments | Total | |||||||||||||||||||

| Balance at June 30, 2018 | $ | ( | $ | ( | $ | ( | $ | ( | |||||||||||||||

| Other comprehensive income/(loss) before reclassifications | ( | ( | |||||||||||||||||||||

| Amounts reclassified from accumulated other comprehensive income/(loss) | |||||||||||||||||||||||

| Net current period other comprehensive income/(loss) | ( | ( | |||||||||||||||||||||

| Balance at December 31, 2018 | $ | ( | $ | ( | $ | ( | $ | ( | |||||||||||||||

14. COMMITMENTS AND CONTINGENCIES

SEC inquiry into Juniper Pharmaceuticals, Inc.

On August 14, 2018, Operating Company acquired Juniper pursuant to the Juniper Merger Agreement. On November 14, 2016, Juniper filed with the SEC restated audited consolidated financial statements for the fiscal years ended December 31, 2013 through December 31, 2015, including the unaudited consolidated financial information for each quarterly period within the fiscal years ended December 31, 2014 and 2015, and restated unaudited consolidated financial statements for the quarters ended March 31, 2016 and June 30, 2016 and the related quarters in 2015, in order to correct certain timing errors regarding how it recognized revenue from a supply contract with an affiliate of Merck KGaA. On January 24, 2017, Juniper received a subpoena from the SEC requesting information concerning these restatements and related issues. Juniper responded to the subpoena and is cooperating with the SEC’s inquiry, including the taking of testimony from former Juniper employees and others. The Company understands that the inquiry is ongoing but does not believe the outcome of the investigation will be material to it; nonetheless, the Company cannot provide any assurance regarding that outcome.

Other