EXHIBIT 1.1

SHOPIFY INC.

2021 ANNUAL INFORMATION FORM

February 16, 2022

ANNUAL INFORMATION FORM

SHOPIFY INC.

TABLE OF CONTENTS

| Section | Page Number | ||||

| General Matters | |||||

| Forward-Looking Information | |||||

| Corporate Structure | |||||

| Description of the Business | |||||

| General Development of the Business | |||||

| Risk Factors | |||||

| Dividends and Distributions | |||||

| Capital Structure | |||||

| Market for Securities | |||||

| Directors and Officers | |||||

| Legal Proceedings and Regulatory Actions | |||||

| Interest of Management and Others in Material Transactions | |||||

| Transfer Agents and Registrars | |||||

| Material Contracts | |||||

| Interests of Experts | |||||

| Additional Information | |||||

| Exhibit A - Audit Committee Charter | |||||

ANNUAL INFORMATION FORM

SHOPIFY INC.

GENERAL MATTERS

Information Contained in this Annual Information Form

In this Annual Information Form ("AIF") "we", "our", "Shopify", and the "Company" refer to Shopify Inc. and its consolidated subsidiaries, unless the context requires otherwise. References to our "solutions" means the combination of products and services that we offer to merchants, and references to "our merchants" as of a particular date means the total number of unique shops that are paying for a subscription to our platform. Words importing the singular, where the context requires, include the plural and vice versa and words importing any gender include all genders.

Unless otherwise indicated, all information in this AIF is presented as at February 10, 2022, and references to specific years are references to the fiscal years of Shopify ended December 31.

This AIF should be read in conjunction with the Company's 2021 audited consolidated financial statements and notes ("2021 Financial Statements") and the Company's 2021 Management’s Discussion and Analysis ("2021 MD&A"), but which, for greater certainty, are not incorporated by reference herein.

Shopify and the associated logo are registered trademarks of Shopify Inc. or its subsidiaries. All other marks used herein are trademarks or registered trademarks belonging to their respective owners.

Presentation of Financial Information

We prepare and report our consolidated financial statements in accordance with accounting principles generally accepted in the United States of America ("U.S. GAAP"). Our reporting currency is U.S. dollars, and we express all amounts in this AIF in U.S. dollars, except where otherwise indicated. All references in this AIF to "dollars", "$" and "US$" refer to United States dollars, and all references to "CAD$" refer to Canadian dollars, unless otherwise expressly stated. On February 10, 2022, the Bank of Canada rate of exchange for the conversion of U.S. dollars into Canadian dollars was $1.00 = CAD$1.2682.

FORWARD-LOOKING INFORMATION

This AIF contains forward-looking statements under the provisions of the U.S. Private Securities Litigation Reform Act of 1995, Section 27A of the U.S. Securities Act of 1933 (as amended, the "Securities Act"), and Section 21E of the U.S. Securities Exchange Act of 1934 (as amended, the "Exchange Act"), and forward-looking information within the meaning of applicable Canadian securities legislation.

In some cases, you can identify forward-looking statements by terminology such as "may", "might", "will", "should", "could", "expects", "intends", "plans", "anticipates", "believes", "predicts", "potential", "continue", "become", "seek", "strive", or the negative of these terms or other similar words. In addition, any statements or information that refer to expectations, beliefs, plans, projections, objectives, performance or other characterizations of future events or circumstances, including any underlying

3

assumptions, are forward-looking. In particular, forward-looking statements in this AIF include, but are not limited to, statements about:

•our ability to make it easier for merchants to manage their storefronts via their mobile devices;

•our exploration of new ways to accelerate checkout;

•whether a merchant using Shopify will ever need to re-platform;

•our ability to expand our merchant base;

•our plans to localize the Shopify platform;

•our ability to offer more sales channels that can connect to our platform;

•our ability to invest in and develop new solutions to extend the functionality of our platform and catalyze merchants' sales growth;

•enhancement of our ecosystem and partner programs;

•our ability to provide a high level of merchant service and support;

•our ability to hire, retain and motivate qualified personnel;

•the ability of Shopify Fulfillment Network partners to increase the speed and reliability of their warehouse operations by leveraging 6 River Systems, LLC ("6 River Systems") solutions;

•our expectation that seasonality will continue to affect our quarterly results;

•our expectation that our business may become more seasonal in the future;

•the rapid evolution of multi-channel commerce and ecommerce and our ability to bring to market new and better selling and buying experiences;

•our investment in developing online and point of sale assets with a single commerce operating system;

•our ability to grow our base of merchants by offering new and better ways to market and sell their products and expanding the range of our solutions;

•the size of our addressable markets and our ability to serve those markets;

•our expectation that we will continue to invest in data analytics and machine learning;

•our ability to grow our addressable market and meet our merchants' needs;

•the intended growth of our business and making investments to drive future growth, and the impact of those investments;

•the growth of our merchants’ revenues and our ability to retain merchants as they grow;

•our intention to continue strategically investing in marketing programs that enhance the awareness of our brand;

•our belief in the importance of establishing relationships with merchants early in the business lifecycle;

•our intention to grow our merchant base by inspiring entrepreneurship through marketing programs;

•our investment in additional sales capacity;

•continued improvement of our platform to help our merchants sell more;

•expansion of our platform's capabilities;

•the growth and strengthening of our third-party ecosystem and partner program, including formation of strategic partnerships;

•our intention to optimize our cloud-based infrastructure;

•our investment in end-to-end automation and comprehensive test suites for our platform;

•our expectation of increased competition;

•our expectation that leveraging third-party providers of infrastructure will increase engineering velocity;

•our expectation that the majority of employees will work remotely permanently;

•our intention to support Operation HOPE by providing up to $130 million in in-kind resources;

4

•the extent of the impact of the COVID-19 pandemic and related restrictions and actions we may take in response on our business, financial performance, revenues, and results of operations;

•disruption to our operations due to the impact of COVID-19 and the impact of COVID-19 on our employees, suppliers, partners, and our merchants and their customers, the success of and risk related to new products and initiatives launched in response to COVID-19, and the effect of economic conditions as a result of COVID-19 on the value of our investments and our share price;

•the impact of strategic decisions on short-term revenue or profitability;

•the trend in our future growth;

•the need to devote additional resources to manage future growth and our ability to satisfy obligations and effectively manage such growth;

•our intention to expand our business and increase headcount;

•our plan to continue investing in our network infrastructure;

•our expectation that we will incur additional general and administrative expenses as a result of our growth;

•the expansion of our platform internationally and our ability to maintain our corporate culture as we grow and shift to a digital-by-design, remote-first global workforce;

•our expectation regarding the continued expansion of Shopify Plus;

•an increase in cyberattacks including as attackers exploit any vulnerabilities introduced by the COVID-19 pandemic and any related changes by business operations;

•the evolution of competitive pressure as our business evolves to encompass a wider range of products;

•our plan to increase our investments in research and development and maintain our high level of merchant service and support;

•our intention to pursue additional relationships with other third parties, such as technology and content providers and implementation consultants;

•growth in the number of sales personnel and increasing expenses in connection with marketing our brand;

•our intention to issue stock options or other equity awards as key components of our overall compensation and employee attraction and retention efforts;

•the evolution of laws governing internet-based platforms and the impact of such laws on our business including as we develop consumer-facing products and services;

•our intention to continue our use and development of open source software;

•potential selective acquisitions and investments;

•our exploration of other products, models and structures for Shopify Capital;

•our operation and optimization of Shopify Fulfillment Network;

•changes in our pricing models;

•our transfer pricing procedures;

•requirements upon a fundamental change, conversion or maturity of our 0.125% convertible senior notes due 2025 (the "Notes");

•our expectation that we will not pay any cash dividends in the foreseeable future; and

•our intention to invest our future earnings, if any, to fund our growth.

5

The forward-looking statements contained in this AIF are based on our management’s perception of historic trends, current conditions and expected future developments, as well as other assumptions that management believes are appropriate in the circumstances, which include, but are not limited to:

•our ability to increase the functionality of our platform;

•our ability to offer more sales channels that can connect to the platform;

•our belief in the increasing importance of a multi-channel platform that is both fully integrated and easy to use;

•our belief that commerce transacted over mobile will continue to grow more rapidly than desktop transactions;

•our ability to expand our merchant base, retain revenue from existing merchants as they grow their businesses, and increase sales to both new and existing merchants;

•our ability to manage our growth effectively;

•our ability to protect our intellectual property rights;

•our belief that our merchant solutions make it easier for merchants to start a business and grow on our platform;

•our ability to develop new solutions to extend the functionality of our platform and provide a high level of merchant service and support;

•our ability to build with a focus on long-term value;

•our ability to enhance our ecosystem and partner programs, and the assumption that this will drive growth in our merchant base, further accelerating growth of the ecosystem;

•our belief that strategic investments and acquisitions will increase our revenue base, improve the retention of this base and strengthen our ability to increase sales to our merchants and help drive our growth;

•our ability to achieve our revenue growth objectives while controlling costs and expenses, and our ability to achieve or maintain profitability;

•our belief that monthly recurring revenue is most closely correlated with the long-term value of our merchant relationships;

•our assumptions regarding the principal competitive factors in our markets;

•our ability to predict future commerce trends and technology;

•our assumptions that higher-margin solutions such as Shopify Capital and Shopify Shipping will continue to grow through increased adoption and international expansion;

•our expectation that Shopify Payments will continue to expand internationally;

•our expectation that Shopify Fulfillment Network will scale and grow as we optimize the network;

•our belief that our investments in sales and marketing initiatives will continue to be effective in growing the number of merchants using our platform, in retaining revenue from existing merchants and increasing revenues from both;

•our ability to develop processes, systems and controls to enable our internal support functions to scale with the growth of our business;

•our ability to hire, retain and motivate qualified personnel and to manage our operations in a digital-by-design model;

•our belief that the near-term costs of reducing our leased footprint and transitioning our remaining spaces to their future intended purposes will yield longer-term benefits;

•the impact of legislation or governmental action on our platform;

•increasing restrictions on the ability of parties to access or use data;

•our ability to retain key personnel;

•our ability to protect against currency, interest rate, concentration of credit and inflation risks;

•our assumptions as to our future expenses and financing requirements;

6

•our assumptions as to our critical accounting policies and estimates; and

•our assumptions as to the effects of accounting pronouncements to be adopted.

Factors that may cause actual results to differ materially from current expectations may include, but are not limited to, risks and uncertainties that are discussed in greater detail in the "Risk Factors" section of this AIF.

Although we believe that the plans, intentions, expectations, assumptions and strategies reflected in our forward-looking statements are reasonable, these statements relate to future events or our future financial performance, and involve known and unknown risks, uncertainties and other factors which are, in some cases, beyond our control. If one or more of these risks or uncertainties occur, or if our underlying assumptions prove to be incorrect, actual results may vary significantly from those implied or projected by the forward-looking statements. No forward-looking statement is a guarantee of future results. You should read this AIF and the documents that we reference in this AIF completely and with the understanding that our actual future results may be materially different from any future results expressed or implied by these forward-looking statements.

The forward-looking statements in this AIF represent our views as of the date of this AIF. We anticipate that subsequent events and developments may cause our views to change. However, while we may elect to update these forward-looking statements at some point in the future, we have no current intention of doing so except to the extent required by applicable law. Therefore, these forward-looking statements do not represent our views as of any date other than the date of this AIF.

CORPORATE STRUCTURE

Name, Address and Incorporation

The Company was incorporated under the Canada Business Corporations Act (the "CBCA") on September 28, 2004 under the name 4261607 Canada Ltd. We filed articles of amendment on January 19, 2006 to change our name to Jaded Pixel Technologies Inc., and again on November 30, 2011 to change our name to Shopify Inc. On April 12, 2013, we filed articles of amendment to split all of our issued and outstanding common shares and all of our issued and outstanding Series A and Series B preferred shares on a 5-for-1 basis. On May 22, 2015, we filed articles of amendment to amend and re-designate our authorized and issued share capital in connection with our initial public offering. See “Capital Structure” for more information about our current share capital. On May 27, 2015, we restated our amended articles of incorporation.

While we consider the Company's location to be the internet, our registered office is 151 O'Connor Street, Ground Floor, Ottawa, Ontario, Canada K2P 2L8, and our telephone number is (613) 241-2828. Our website address is www.shopify.com. Information contained on, or accessible through, our website is not a part of this AIF.

7

Intercorporate Relationships

The following chart shows our current material subsidiaries. All of our subsidiaries are, directly or indirectly, wholly owned.

DESCRIPTION OF THE BUSINESS

Overview

Shopify is a leading provider of essential internet infrastructure for commerce, offering trusted tools to start, grow, market, and manage a retail business of any size. Shopify makes commerce better for everyone with a platform and services that are engineered for simplicity and reliability, while delivering a better shopping experience for consumers everywhere.

In an era where social media, cloud computing, mobile devices, augmented reality and data analytics are creating new possibilities for commerce, Shopify provides differentiated value by offering merchants:

A multi-channel front end. Our software enables merchants to easily display, manage, market and sell their products across over a dozen different sales channels, including web and mobile storefronts, physical retail locations, pop-up shops, social media storefronts, native mobile apps, buy buttons, and marketplaces. More than two-thirds of our merchants have installed two or more channels. The Shopify application program interface ("API") has been developed to support custom storefronts that let merchants sell anywhere, in any language.

A single integrated back end. Our software provides one single integrated, easy-to-use back end that merchants use to manage their business and buyers across these multiple sales channels. Merchants use their Shopify dashboard, which is available in 21 languages, to manage products and inventory, process orders and payments, fulfill and ship orders, discover new buyers and build customer relationships, source products, leverage analytics and reporting, manage cash, payments and transactions, and access financing.

A data advantage. Our software is delivered to merchants as a service, and operates on a shared infrastructure. This cloud-based infrastructure not only relieves merchants from running and securing their own hardware, it also consolidates data generated by the interactions between buyers and a merchant's products, providing rich data to inform merchant decisions. With a large, rapidly growing and highly qualified team of data personnel, we expect to continue leveraging data for the benefit of our merchants with critical safeguards in place to ensure privacy, security and compliance.

8

Shopify also enables merchants to build their own brand, leverage mobile technology, sell internationally, and handle massive traffic spikes with flexible infrastructure:

Brand ownership. Shopify is designed to help our merchants own their brand, develop a direct relationship with their buyers, and make their buyer experience memorable and distinctive. We recognize that in a world where buyers have more choices than ever before, a merchant’s brand is increasingly important. The Shopify platform is designed to allow a merchant to keep their brand present in every interaction to build buyer loyalty and competitive advantage. While our platform is designed to empower merchants first, merchants benefit when buyers are confident that their payments are secure. We believe that awareness among buyers that Shopify provides a superior and secure checkout experience is an additional advantage for our merchants in an increasingly competitive market. For merchants using Shopify Payments, buyers are already getting a superior experience, with features such as Shop Pay and Shop Pay Installments, and with our investments in additional buyer touchpoints, such as retail, shipping, fulfillment, and Shop, our all-in-one digital shopping companion app, brands that sell on Shopify can offer buyers an end-to-end, managed shopping experience that previously was only available to much larger businesses.

Mobile. As ecommerce expands as a percentage of overall retail transactions, a trend that accelerated in 2020 when the global COVID-19 pandemic necessitated physically distanced commerce, buyers expect to be able to transact anywhere, anytime, on any device through an experience that is simple, seamless, and secure. As transactions over mobile devices represent the majority of transactions across online stores powered by Shopify, the mobile experience is a merchant’s primary and most important interaction with online buyers. Shopify has focused on enabling mobile commerce, and the Shopify platform includes a mobile-optimized checkout system, designed to enable merchants’ buyers to more easily buy products over mobile websites. Our merchants are able to offer their buyers a quick and secure check-out option by using Shop Pay, Apple Pay, Facebook Pay, and Google Pay on the web, and we continue to explore other new ways to offer payment flexibility and accelerated checkout. Just as Shopify's tools enable retailers to sell directly to their buyers through online stores, the Shop app provides merchants that same direct sales power through an app. The Shop app is a digital shopping assistant that is available to buyers on iOS and Android mobile devices. Buyers use the Shop app to track packages, discover products from their favorite merchants, and engage with brands directly, which helps merchants increase the loyalty and lifetime value of their buyers. Shopify’s mobile capabilities are not limited to the front end: merchants who are often on-the-go find themselves managing their storefronts via their mobile devices, and Shopify continues to strive to make it easier to do so.

Global. Commerce thrives when merchants are able to build a global brand and commerce beyond their own borders with little friction. Shopify Markets, a product introduced in 2021, enables merchants to manage localized storefronts in different countries through one global store, making cross-border commerce easier for entrepreneurs. With Shopify Markets, merchants can easily set up market-specific buying experiences, enabling buyers to shop in their local currencies, languages, domains, and payment methods. Shopify Markets also automatically calculates duty and import fees. Such tailored experiences are designed to increase local buyer trust and conversion, enabling merchants to enter new geographies more easily. Shopify Markets complements our partnership with Global-E, an offering for merchants who want to fully outsource their cross-border business with an approved third-party partner.

Infrastructure. We build our platform to address the growing challenges facing merchants and with the aim of making complex tasks simple. The Shopify platform is engineered to enterprise-level standards and functionality and designed for simplicity and ease of use. We also design our platform with a robust technical infrastructure able to manage large spikes in traffic that accompany events such as new product

9

releases, holiday shopping seasons, and flash sales. We are constantly innovating and enhancing our platform, with our continuously deployed, multi-tenant architecture ensuring all of our merchants are always using the latest technology.

This combination of ease of use with enterprise-level functionality allows merchants to start with a Shopify store and grow with our platform to almost any size. Using Shopify, merchants may never need to re-platform. Our Shopify Plus subscription plan was created to accommodate larger merchants, with additional functionality, scalability and support requirements. The Shopify Plus plan also appeals to larger merchants not already on Shopify who want to migrate from their expensive and complex legacy solutions and get more functionality.

Sustainability

Shopify is a company that wants to see the next century, and has taken many steps to build a sustainable company, including committing to carbon neutrality. As part of this commitment, in 2019, we decommissioned our data centres and migrated our platform to Google Cloud, which is 100% powered by renewable energy.

Because we view commerce as a powerful vehicle for positive systemic change, as part of our focus on the long term, in 2019 Shopify launched a sustainability fund with the intent to commit at least $5 million annually to fund what Shopify believes are the most promising and impactful technologies and projects to combat climate change, with a bias toward solutions that remove carbon from the atmosphere and permanently lock it away, as opposed to traditional offsets that pay others to avoid carbon emissions. In 2021, our sustainability fund invested in offsetting our operational footprint during the year, purchasing renewable energy certificates for our office buildings and employee home offices as well as purchasing carbon removal to completely eliminate the impact of carbon emissions from shipping every single order on our platform over the Black Friday/Cyber Monday shopping weekend. In addition, we continuously offset all carbon emissions associated with shipping orders placed using Shop Pay, our checkout accelerator. We give our merchants the ability to offset the carbon emissions associated with shipping all their orders via Offset, an app we launched in 2020.

Our business model is driven by our ability to attract new merchants, retain revenue from existing merchants, and increase sales to both new and existing merchants. As such, we believe that our future success depends on many factors, including our ability to expand our merchant base; localize features for specific geographies; retain merchants as they grow their businesses on our platform and adopt more features; offer more sales channels that connect merchants with their specific target audience; develop new solutions to extend our platform’s functionality and catalyze merchants’ sales growth; enhance our ecosystem and partner programs; provide a high level of merchant support; hire, retain and motivate qualified personnel; and build with a focus on maximizing long-term value.

Our Merchants

Our mission is to make commerce better for everyone, and we believe we can help merchants of nearly all retail verticals and sizes, from aspirational entrepreneurs to companies with large-scale, direct-to-consumer operations, realize their potential at all stages of their business life cycle. Our marketing efforts primarily focus on selling to SMBs and entrepreneurs while our direct sales team primarily addresses the needs of large merchants. The large majority of our merchants are on subscription plans that cost less than $50 per month, which is in line with our focus on providing cost-effective solutions for early stage businesses.

10

As of December 31, 2021, we had approximately 2,063,000 merchants from approximately 175 countries using our platform, geographically dispersed as follows: 55% North America, 25% Europe Middle East and Africa, 15% Asia Pacific, Australia and China and 5% in Latin America (Mexico and South America).

Our merchants represent a wide array of retail verticals and business sizes and no single merchant has ever represented more than five percent of our total revenues in a single reporting period.

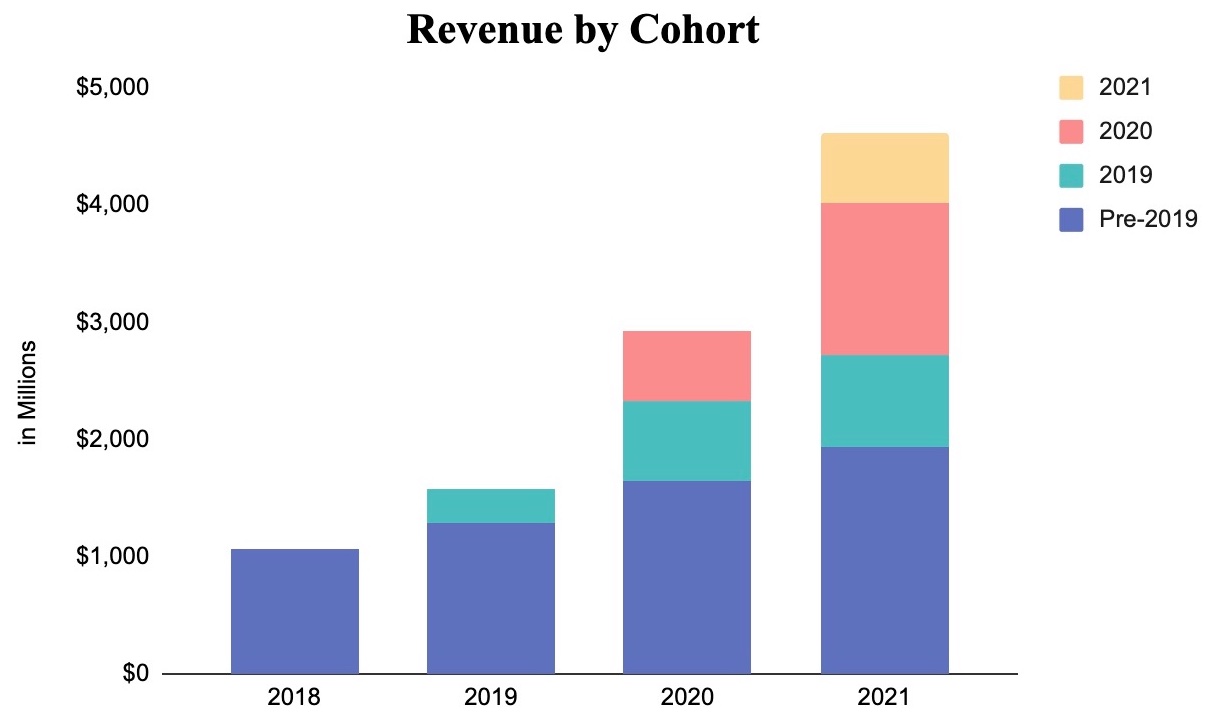

When our merchants grow their sales and become more successful, they consume more of our merchant solutions, upgrade to higher subscription plans, and purchase additional apps. We consider our merchants' success to be one of the most powerful drivers of our business model. The chart below displays the annual revenue for merchant cohorts that joined the Shopify platform at different times in our history. The strength of our business model lies in the consistent revenue growth coming from each cohort: the increase in revenue from remaining merchants growing within a cohort offsets the decline in revenue from merchants leaving the platform.

For example, revenue from our pre-2019 cohort expanded in 2020, as the revenue impact from merchants within the cohort leaving the platform was offset by revenue growth from remaining merchants within that cohort. In 2021, revenue from the pre-2019 cohort continued its growth as merchant retention improved, and the remaining merchants increased their gross merchandise volume ("GMV") and adopted additional solutions provided through the Shopify platform.

Moreover, the total combined revenue of all previous cohorts once they have annualized and become comparable to prior years has also grown consistently.

11

Merchant Acquisition

Our merchant acquisition strategy is primarily focused on marketing that builds awareness of our offerings with sales and marketing efforts supported by regional resources. Our approach includes a strong emphasis on the use of data and analytics while continuously innovating and testing new ideas to drive growth.

Because our merchant base includes a wide array of retail verticals and business sizes, spanning from aspirational startups to long-established enterprises, we use a broad variety of means to attract new merchants. We actively grow our audience through digital channels, including organic search, paid search, and social media. We also engage our merchants through events in our offline strategy. In 2021, we largely conducted events virtually due to the ongoing COVID-19 pandemic, and reintroduced in-person events in the latter half of the year, including hosting workshops and community-based events at our New York City and Los Angeles spaces.

We intend to grow our base of merchants primarily by inspiring entrepreneurship through marketing programs. We invest in awareness-driven brand campaigns, authoring various Shopify blogs and podcasts, earned media and public relations campaigns, and providing thought leadership to help our merchants succeed and to build their own brand.

We also offer self-serve onboarding, and employ outbound sales representatives to help drive adoption of our platform and certain solutions, such as Shopify Plus and our Point-of-Sale ("POS") Pro offering.

In addition to direct channels, we leverage relationships with third-party design agencies, developers, influencers, and freelancers around the world who actively refer merchants to us.

Ecosystem

A rich ecosystem of app developers, theme designers and other partners, such as digital and service professionals, marketers, photographers, and affiliates has evolved around the Shopify platform. We believe our partner ecosystem helps drive the growth of our merchant base in two ways: by referring new merchants, and by extending the functionality of the Shopify platform through the development of apps. More than 40,000 of these partners referred merchants to Shopify over the last year, and this strong, symbiotic relationship was further strengthened in the second half of 2021 when we extended more generous revenue sharing terms with app and theme developers. We believe this ecosystem has grown in part due to the platform’s functionality, which is highly extensible and can be expanded through our API and the more than 8,000 apps available in the Shopify App Store. The partner ecosystem helps drive the growth of our merchant base, which in turn further accelerates growth of the ecosystem.

Our Offerings

Our business model has two revenue streams: a recurring subscription component we call subscription solutions, and a merchant success-based component we call merchant solutions.

Subscription Solutions

We generate subscription solutions revenues primarily through the sale of subscriptions to our platform, including variable platform fees, as well as through the sale of subscriptions to our POS Pro offering, the sale of themes, the sale of apps, and the registration of domain names.

12

We offer pricing plans designed to meet the needs of our current and prospective merchants. Offering different service and pricing levels allows entrepreneurs to scale without leaving the Shopify platform: as a merchant upgrades to the higher-priced options, they receive more powerful tools. We believe this ability to retain merchants as they grow is an important factor for our success in serving the SMB market. While most merchants subscribe to our Basic and Shopify plans, the majority of our GMV comes from merchants subscribing to our Shopify Plus plans. Merchant retention rates are also higher among merchants on higher-priced plans. Offered at a starting rate that is several times that of our Advanced plan, the Shopify Plus plan solves for the complexity of merchants as they grow and scale globally, offering additional functionality, and support, including features like Shopify Flow and Launchpad for ecommerce automation, and dedicated account management where appropriate. Allbirds, Gymshark, Heinz, Tupperware, FTD, Netflix, and FIGS are among the more than 14,000 Shopify Plus merchants leveraging our reliable, cost-effective, and scalable commerce solution.

Our subscription plans typically have a one-month term, although merchants can elect to make an annual commitment. Those who sign on to Shopify Plus initially have annual or multi-year subscription terms. Subscription terms automatically renew unless notice of cancellation is provided in advance. Merchants purchase subscription plans directly from us. Subscription fees are paid to us at the start of the applicable subscription period, regardless of the length of the subscription period, with the exception of Shopify Plus subscription contracts, which are paid in arrears on a ratable basis. Subscription fees are non-refundable. POS Pro enables brick and mortar merchants to seamlessly bridge online and offline commerce operations and offer their buyers a smooth shopping experience through features such as smart inventory management and buy online-pickup/return in store or curbside. POS Pro subscriptions fees are charged on a per month and per location basis.

To attract the best developers in the world, in 2021, Shopify changed its revenue share model with app and theme developer partners to offer a zero percent revenue share on the first million dollars that they make annually on the Shopify App Store. App and theme developers pay a 15% revenue share on earnings after the first $1 million, a threshold that resets annually, down from the previous 20% revenue share on their overall revenue.

Merchant Solutions

We offer a variety of merchant solutions to augment those provided through a subscription to address the broad array of functionality merchants commonly require, including accepting payments, shipping and fulfillment, and securing working capital. We believe that offering merchant solutions creates additional value for merchants, saving them time and money by making additional functionality available within a single centralized commerce platform, and creates additional value for Shopify by increasing merchants’ use of our platform.

We principally generate merchant solutions revenues from payment processing fees and currency conversion fees from Shopify Payments. In addition to payment processing fees and currency conversion fees from Shopify Payments, we also generate merchant solutions revenue from other transaction services, referral fees, advertising revenue on the Shopify App Store, Shopify Capital, Shop Pay Installments, Shopify Balance, Shopify Shipping, Shopify Fulfillment Network, collaborative warehouse fulfillment solutions, non-cash consideration obtained for services rendered as part of strategic partnerships, the sale of POS hardware, Shopify Email and Shopify Markets.

13

Shopify Payments is a fully integrated payment processing service that allows our merchants to accept and process payment cards online and offline, and is also designed to drive higher retention among merchants. Shopify Payments eliminates the need for merchants to set up and maintain a direct relationship with a third-party payment gateway, gives merchants access to low credit card processing rates, and allows us to cross-sell additional solutions to our merchant base. We introduced Shopify Payments in the United States and Canada in 2013, and have been expanding into additional geographies in subsequent years. Today, more than two-thirds of our merchants have enabled Shopify Payments, which is available in 17 countries. As a result of introducing Shopify Payments, our revenues from merchant solutions and associated costs have increased. Shopify merchants that have adopted Shopify Payments also have access to Shop Pay, our accelerated checkout, which has been proven to improve speed-to-checkout and sales conversion rates for our merchants, as well as Shop Pay Installments, our 'buy now, pay later' product, which has been proven to boost repeat purchases among first time customers, benefiting merchant solutions revenue.

Transaction fees are typically charged based in part on a percentage of GMV processed on subscription plans where the merchant has not signed up for Shopify Payments. We generate referral fees from partners to whom we direct business and with whom we have an arrangement in place. Pursuant to terms of the agreements with our partners, these revenues can be recurring or non-recurring. Where the agreement provides for recurring payments to us, we typically earn revenues so long as the merchant that we have referred to the partner continues to use the services of the partner. Non-recurring revenues generally take the form of one-time payments that we receive when we initially refer the merchant to the partner.

We generate non-cash revenue from strategic partners related to performance obligations with respect to Shop Pay Installments and cross-border commerce offerings. These revenues were valued at the start of their commercial contracts and are recognized ratably over the expected life of the contracts, which range from three to seven years.

Advertising revenue is earned on the Shopify App Store as merchants click on the apps being advertised by our partners. We recognize advertising revenues when we are entitled to receive payment from the partner.

Shopify Capital was launched in the United States in 2016, and in the United Kingdom and Canada in 2020, to help eligible merchants secure financing and accelerate the growth of their business by providing access to simple, fast, and convenient working capital. We apply underwriting criteria prior to purchasing the eligible merchant's future receivables or making a loan to help ensure collectability. Under Shopify Capital, we purchase a designated amount of future receivables at a discount or make a loan. The advance, or the loan, is forwarded to the merchant at the time the related agreement is entered into, and the merchant remits a fixed percentage of their daily sales until the outstanding balance has been remitted. For Shopify Capital merchant cash advances ("MCAs"), we apply a percentage of the remittances collected against the merchant's receivable balance, and a percentage, which is related to the discount, as merchant solutions revenue. For Shopify Capital loans, because there is a fixed maximum repayment term, we calculate an effective interest rate based on the merchant's expected future payment volume to determine how much of a merchant's repayment to recognize as revenue and how much to apply against the merchant's receivable balance. We have mitigated some of the risks associated with Shopify Capital by entering into an agreement with a third party to insure some of the MCAs and loans offered by Shopify Capital in the United States, United Kingdom and Canada.

Shop Pay Installments, which was made generally available in June 2021 to merchants and buyers in the United States, enables merchants to sell their goods to buyers on an interest-free payment plan. Merchants receive upfront payment for a sale, net of fees, without the worry associated with collecting future

14

payments from the buyer. We recognize revenue when a merchant sale is made through the use of the product based on a percentage of the total order value. We earn and recognize a portion of the revenue from each merchant sale, with the majority of revenue earned and recognized by our third-party provider that bears the buyer underwriting and buyer credit risk associated with the product.

Shopify Shipping was launched in the United States in 2015, Canada in 2016, Australia in 2020, and the United Kingdom in 2021, and allows merchants doing their own fulfillment and shipping to select from available shipping partners to buy and print outbound and return shipping labels and track orders directly within the Shopify platform. In June 2019, we announced Shopify Fulfillment Network for merchants looking to outsource fulfillment. Leveraging a network of fulfillment centers dispersed across the United States, Shopify Fulfillment Network is designed to help ensure merchants’ orders are delivered to buyers quickly and cost-effectively by leveraging Shopify’s scale with deep machine learning tools, including demand forecasting, smart inventory allocation across warehouses and intelligent order routing. In October 2019, to accelerate the growth of Shopify Fulfillment Network, and to participate in the rapidly growing warehouse automation space, we acquired 6 River Systems, a provider of collaborative warehouse fulfillment solutions. Shopify Fulfillment Network partners leveraging 6 River Systems’ cloud-based software and collaborative mobile robots can increase the speed and reliability of their warehouse operations by empowering on-site associates with daily tasks, including inventory replenishment, picking, sorting, and packing. 6 River Systems also sells its collaborative warehouse fulfillment solutions to retail and third-party fulfillment customers independent of Shopify Fulfillment Network.

Shopify POS is a sales channel that lets merchants sell their products and accept payments in person from a mobile device in a physical or retail setting. While the majority of the POS-compatible hardware we sell has been designed and manufactured by third-party vendors, we designed our own hardware including our POS card reader with integrated payments and retail stand with expanded functionality to better meet the needs of our merchant base and increase the visibility of the Shopify brand. Our POS card reader and retail stand are available in the United States and Canada. In 2021, we introduced a new card reader with integrated payments in the United Kingdom and Ireland, and later expanded this offering to Australia, New Zealand, Germany, and the Netherlands, bringing its availability to eight countries. Merchants can purchase POS card readers from Shopify's hardware store and Shopify generates incremental Shopify Payments revenue for transactions conducted via our card readers with integrated payments.

Shopify Email, launched in 2019, is our native email marketing tool designed to enable merchants to create, run, and track email marketing campaigns from within the merchant admin, and help merchants build direct relationships with buyers. Since email is a critical channel to build relationships with buyers, merchants can send a certain number of emails for free and then will pay a nominal rate above that threshold.

Shopify Markets, announced in 2021, is a product that makes cross-border commerce easier for merchants, enabling them to enter new markets, and increase buyer trust and conversion with tailored experiences for each market. By managing all cross-border commerce in the merchant admin, Shopify Markets gives merchants a unified view of their entire business across borders. Shopify generates revenue when duty and import taxes and currencies are converted for buyer orders, and on international payment processing. Global-E, an offering that gives merchants the option for a more full-service, outsourced solution for cross-border commerce, complements Shopify Markets.

Shopify Balance, our money management product, began rolling out to merchants in the United States in 2021. Shopify Balance offers merchants a no fee money management account, providing merchants with fast access to their cash, a card for spending online, on mobile, or in-store, and rewards featuring cash

15

back, perks, and discounts on everyday business spending. While Shopify earns a small fee upon the use of its card, we expect to use Shopify Balance primarily as a way to introduce and centralize more financial services to simplify our merchants’ financial lives.

Seasonality

Our merchant solutions revenues are directionally correlated with the level of GMV that our merchants facilitated through our platform. Our merchants typically process additional GMV during the fourth quarter holiday season. As a result, we have historically generated higher merchant solutions revenues in our fourth quarter than in other quarters. While we believe that this seasonality has affected and will continue to affect our quarterly results, our rapid growth has largely masked seasonal trends to date. As a result of the continued growth of our merchant solutions offerings, we believe that our business may become more seasonal in the future and that historical patterns in our business may not be a reliable indicator of our future performance.

Research and Development

Shopify is building the internet infrastructure for commerce that enables merchants of all sizes around the world to successfully start and scale their businesses on Shopify. We are simplifying the user experience for smaller merchants, arming them with new and innovative ways to compete with larger, better-funded competitors, as well as for larger merchants seeking technology and support for higher volumes and global reach. As such, research and development at Shopify is currently focused on product management, product development, and product design to accomplish these goals. In order to best serve merchants seeking to develop a commerce presence wherever their buyers are across multiple channels, we invest in developing online and point of sale assets with a single commerce operating system, an area of the market we feel is currently underserved.

Multi-channel commerce, including ecommerce, is a relatively new industry that is rapidly evolving, as mobile device makers continue to innovate on features and functionality, media channels become more interactive and develop their commerce capabilities, and merchants continually strive to create new ways to stand out in an increasingly digital economy. Traditional brick and mortar retailers seek to join the digital revolution by leveraging their brand and physical presence in new and innovative ways, particularly in the wake of the global COVID-19 pandemic, which accelerated digital commerce starting in 2020. Shopify strives, on behalf of merchants, to not just keep pace in this dynamic environment, but to bring to market new and better selling and buying experiences by leveraging what technology and connectivity have made possible.

We also invest in developing the tools to make it easier for our ecosystem partners to build on and for Shopify to extend the functionality and flexibility of the platform. We believe that by deepening the capabilities of our current solution set to meet the needs of more merchants in more geographies, by offering new and better ways for merchants to market, sell, and get their products to buyers, and by expanding the range of solutions we offer, we will be able to grow our addressable market and meet the needs of merchants in years ahead. Data analytics and machine learning are increasingly informing our product development efforts and we expect to continue investing in this area.

Growth Strategy

We have focused on rapidly growing our business and plan to continue heavily investing to drive future growth. We believe that our investments will increase our revenue base, improve the retention of our

16

global base of merchants and strengthen our ability to increase sales to our merchants. Our growth strategy is driven by our mission: make commerce better for everyone. Key elements of our strategy include:

•Grow our Base of Merchants. We believe that we have a significant opportunity to increase the size of our current merchant base. We intend to grow our base of merchants primarily by inspiring entrepreneurship through marketing programs with a dedicated focus on product marketing and awareness-driven campaigns paired with global earned media efforts and ongoing content creation and distribution with an aim to educate. We also continue to invest in functionality to boost adoption of Shopify by merchants around the world. While we believe it is important to establish relationships early in the business lifecycle and grow along with our merchants, we also see opportunity with larger businesses looking for faster time-to-market and better value as they innovate to meet rapidly evolving buyer demands. As such, we are investing in direct sales efforts focused on acquiring larger merchants as well as brick and mortar retail merchants.

•Grow our Merchants’ Revenue. Our goals are closely aligned with the goals of our merchants. The more a merchant sells on our platform, the longer they are likely to remain with Shopify and the more revenue we generate as they process more transactions, upgrade plans, sell through new sales channels, ship more products, and use additional solutions. We intend to continue to improve our platform to help our merchants sell more and expect to continue to use initiatives such as Shopify blogs, our digital community, our online business training platform, Shopify Learn, global events and meetups, as well as exclusive learning and engagement initiatives to educate our merchants on how they can be even more successful with Shopify. Shopify’s support advisors, available 24/7, also may introduce our merchants to features of the platform at certain points in their journey that help them expand revenue. Shopify blogs are now available in nine languages and we continue to develop our many learning programs, such as Shopify Learn, a free online training program to help entrepreneurs build and grow a business. We are also investing in commercial efforts to help merchants unlock more of the value in Shopify's offerings by educating them about how our solutions can help them continue to grow their businesses.

•Continuous Innovation and Expansion of our Platform. Our platform is built to support innovation and the rapid technology changes in commerce and we have consistently expanded the functionality of our platform over the last decade. In addition to the suite of merchant solutions Shopify has added over time, we are continuously advancing our technologies, tooling, and infrastructure so merchants can not only keep pace with the rapid changes in commerce, but be among the earliest adopters of commerce innovation.

•Continue to Grow and Develop our Ecosystem. We have a thriving third-party ecosystem that includes app developers, theme designers, and other partners that bolster the functionality of our platform. In 2021, we made our terms more favorable to our app and theme developer partners by reducing our revenue share on the first $1 million of earnings in a calendar year to $0, and retaining 15% on subsequent revenue. These competitive terms increase the appeal of Shopify as a platform on which to build and enable partners to reinvest in their own growth and innovation. We also host an annual conference, Shopify Unite, to demonstrate to partners the opportunities that exist to collaborate in building the future of commerce technology. Our ecosystem has grown in part due to the platform’s functionality, which is highly extensible and can be expanded through our API. We believe that growing our ecosystem makes the Shopify platform more attractive and stickier, which further expands our merchant base, and in turn drives additional growth of our ecosystem.

17

•Continue to Expand our Referral Partner Programs. We have strong relationships with thousands of design and marketing agencies throughout the world. These agencies build merchant web and mobile shops on our platform. We intend to strengthen our existing relationships with referral partners and create new ones with the goal of expanding our overall merchant base.

•Continue to Build for the Long-term. We have a culture of iteration and experimentation with a focus on maximizing long-term value, and many of our investments are made with an eye toward what we believe merchants will require several years from now. Such longer-term initiatives include localizing the platform for international expansion, promoting our brand, expanding our existing services, introducing new solutions, and entering into strategic partnerships and acquisitions.

Technology

The Shopify platform is a multi-tenant cloud-based system that is engineered for high scalability, reliability, and performance. Open source has played a major role at Shopify from the beginning when our founder was active on the core team that built Ruby on Rails, the technology that powers much of the Shopify platform. We host the Shopify platform using cloud-based servers. Maintaining the integrity and security of our technology infrastructure is critical to our business, and we plan to invest further in our infrastructure to meet our merchants’ needs and maintain their trust. Our investment plans include increasingly optimizing our cloud-based infrastructure to deliver local performance and global reach to more merchants than ever before, with consistent levels of availability, performance and resiliency. The key attributes of the Shopify platform are:

•Security. Shopify conducts regular security assessments, which include but are not limited to third-party penetration tests, a bug bounty program, and vulnerability assessments. The findings that result from these security assessments feed into Shopify's risk management process for further assessment. Credit card processing on the Shopify platform is performed by a dedicated, highly scalable, geographically redundant, high-security environment with specialized policies and procedures in place. The environment is designed to be isolated and secure and exceeds the requirements of PCI DSS. We have been certified as a PCI DSS Level 1-compliant service provider, which is the highest level of compliance available, and we undergo external audits for PCI and SOC 2 Type 2. To keep our merchants' data secure, we use technology including firewalls, advanced encryption, and intrusion detection systems, and offer two-factor authentication.

Further to building trust with our merchants and their buyers, our partners, and other stakeholders, Shopify makes its Privacy Policy available on its website, which describes how we collect, use and protect personal information.

•Scalability. The cloud-based architecture of our platform has been designed to support sudden traffic and order spikes from our merchants. We use a technology called “containerization” to efficiently scale our computing resources across our platform. We have benchmarked the Shopify platform to handle at least 540,000 requests per second and 27,000 orders per minute based on platform load testing.

•Reliability. Our platform includes cloud-based servers that are fault-tolerant and ensure that our platform is highly reliable. Because Shopify is at the heart of our merchants’ businesses, we

18

employ a highly redundant, horizontally scalable, shared architecture to ensure resiliency and high availability.

•Performance. We believe that the faster and more accessible our merchants’ shops appear to their buyers, the more our merchants will sell. We have a dedicated team that is constantly profiling and optimizing the performance of the Shopify platform. We leverage content delivery networks with global points of presence to ensure that content and data is delivered quickly to users across the globe. In 2021, online shops hosted on our platform had sub-100 millisecond median response times; our merchants’ shops averaged 7.1 billion monthly browsing sessions, most of which were from mobile devices; and we processed an average of 152.6 million orders per month.

•Deployment. The Shopify platform is “single branch” software, which means that all of our merchants use the latest version of Shopify at all times. The result is that we have no overhead in maintaining older versions of our platform. Our software deployment process enables us to quickly distribute new software as soon as it is ready. This is made possible by our ongoing investment in end-to-end automation and comprehensive test suites.

Competition

Our market is transforming, competitive, and highly fragmented, and we expect competition to increase in the future. We believe the principal competitive factors in our market are:

•vision for commerce and product strategy;

•simplicity and ease of use for merchants and their buyers;

•integration of multiple sales channels;

•embedding of commerce functionality onto more surfaces;

•cost-effective solutions;

•vast and growing app ecosystem;

•breadth and depth of functionality;

•pace of innovation;

•powerful data analytics;

•ability to scale;

•security and reliability;

•support for a merchant’s brand development; and

•brand recognition and reputation.

With respect to each of these factors, we believe that we compare favorably to our competitors.

While we believe no competitor currently offers an integrated, multi-channel, cloud-based commerce platform with comparable functionality to ours, the rapid growth of ecommerce and of independent brands may attract new entrants or new offerings from existing competitors. Additionally, some merchants may elect to piece together technology that overlaps with our own from other providers such as:

•ecommerce software vendors;

•content management systems;

•payment processors;

•POS software providers;

•domain registrars;

•shipping label providers;

19

•fulfillment service providers;

•alternative lenders;

•financial services;

•cross-border services providers; and

•marketplaces.

Intellectual Property

Our intellectual property and proprietary rights are important to our business. In our efforts to safeguard them, we rely on a combination of copyright, trade secret, trade dress, domain names, trademarks, patents, and other rights in Canada, the United States, and other jurisdictions in which we conduct our business. We also have confidentiality agreements, assignment agreements, and license agreements with employees, contractors, merchants, distributors, and other third parties, which limit access to and use of our proprietary intellectual property. Although we rely, in part, upon these legal and contractual protections, we believe that factors such as the skills and ingenuity of our employees, as well as the functionality and frequent enhancements to our platform, make our intellectual property difficult to replicate.

We are subject to certain risks related to our intellectual property. For more information, see "Risk Factors - Risks Related to our Business and Industry."

Property

We are headquartered in Ottawa, Canada. We do not own any real property. We believe that our current facilities are adequate to meet our current needs and we expect to continue to adapt our facilities as we respond to the evolving circumstances driven by the COVID-19 pandemic.

Culture and Talent

Culture and Employees

If you have ambitious goals, you need an equally ambitious team. Shopify is composed of highly talented, deeply caring individuals all working on making commerce better for everyone. Our culture is continuously being redefined with every person that joins our company, but, at our core, we value people who:

•are impactful;

•are merchant-obsessed;

•make great decisions quickly;

•thrive on change;

•are constant learners; and

•build for the long term.

Our values work in concert with our rules of engagement, which govern how we agree to interact with one another. We believe the more voices in entrepreneurship the better. We embrace being multicultural and celebrate the differences that occur naturally within teams, departments, and locations.

20

How We Work

Shopify employees began working remotely in 2020 following the onset of the COVID-19 pandemic. The effects of COVID-19 led us to reimagine the way we work, resulting in the decision to become a digital-first company. We have coined this way of working 'digital-by-design'. In 2021, we continued to reduce our leased footprint and transition remaining spaces to their future intended purpose, including use for team collaboration and events, to align with our digital-by-design principle of enabling our employees to have high-intent in-person interactions with their teams several times a year. Shopify is also providing employees with the technology and resources to have quality remote work experiences and deliver high-impact work. We believe digital-by-design will yield longer-term benefits, including helping our employees stay healthy and safe, unlocking a diverse global talent pool, eliminating unnecessary commutes and fast-tracking new and better ways to work together that are more productive and rewarding.

Learning and Development

Shopify values continuous learning and personal development. We are a fast-growing company that is constantly striving to get better. We expect to see similar growth from everyone on our team. We offer opportunities to our employees to learn and grow so they feel engaged and are progressing in their careers, which include:

Hack Days. We deeply value innovation and experimentation. Every few months we take a break from our regular work for “Hack Days”, three full days when we encourage our employees to step out of their “day jobs” to tackle a new problem or project that inspires them and adds value to Shopify. “Hack Days” is an expression of Shopify’s culture of innovation and experimentation. Coming together to solve problems outside of their day-to-day work, Shopify employees collaborate across different teams and regions, learn together, and have fun while producing something that will make Shopify better. This global, cross-discipline collaboration promotes a sense of community and belonging on the Shopify team, which is especially important as we grow globally and have more employees distributed internationally.

Own Your Own Development Program. Personal growth and development and constant learning are central to Shopify's culture. We encourage Shopify employees to map their personal learning journey through our "Own Your Own Development" program. Employees around the world can access courses, conferences, and workshops to build their skills and mastery, no matter where they're located.

Leading at Shopify. People leadership is critical to help employees and teams develop into their most impactful selves. Shopify offers Leading at Shopify, a leadership development program that focuses on mission-critical topics to support leadership learning for people-leads of all levels.

Coaching. Shopify employs professional coaches who fuel our mission every day by helping to grow the people and teams that make our mission a reality. We offer customized programs for individuals and teams to accelerate their development in order to generate greater impact and sustainable performance.

We are intentional in building a culture and environment that empowers care and growth in high-impact people. We offer wellness resources and programs across four pillars: financial, mental, physical, and social wellness, including an Employee Assistance Program that provides employees with confidential help for any work, health, or life concern. We measure employee engagement through regular pulse checks, including an annual survey. In a 2021 company-wide employee survey, nearly three out of four respondents reported that Shopify motivates them to go above and beyond what they would in a similar role elsewhere. We consider our relationship with our employees to be excellent.

21

We recruit our employees through multiple avenues including internships, campus recruiting, and global outreach.

As of December 31, 2021, we had more than 10,000 employees and contractors worldwide. None of our employees is represented by a labor organization or is a party to a collective bargaining arrangement, with the exception of a small number of employees in France and Spain who are covered by mandatory industry-wide collective bargaining agreements in accordance with local law.

Government Regulation

We are subject to a number of foreign and domestic laws and regulations that affect companies conducting business on the internet, many of which are still evolving and could be interpreted in ways that could harm our business. Concern about the use of software as a service ("SaaS") platforms for illegal conduct, such as money laundering or supporting terrorist activities, may in the future result in legislation or other governmental action that could require changes to our platform. Similarly, concerns around online platforms facilitating, enabling, or hosting the distribution of illegal or otherwise harmful content, goods, or services, may in the future result in legislation or other governmental action that could require changes to our platform.

We are subject to U.S. and Canadian laws and regulations that govern or restrict our business and activities in certain countries and with certain persons, including the economic sanctions regulations administered by the U.S. Treasury Department’s Office of Foreign Assets Control, the sanctions regulations administered or enforced by the Office of the Superintendent of Financial Institutions in Canada, and the export control laws administered by the U.S. Commerce Department’s Bureau of Industry and Security, the U.S. State Department’s Directorate of Defense Trade Controls and the Canadian Export and Import Controls Bureau. We are currently subject to a variety of laws and regulations in Canada, the United States, the European Economic Area and elsewhere related to payment processing and other financial services. Depending on how Shopify Payments, Shop Pay Installments, Shopify Balance and our other merchant solutions evolve, we may be subject to additional laws in Canada, the United States, the United Kingdom, Australia, Ireland, New Zealand, Singapore, Hong Kong, Japan, Germany, Spain, Italy, Denmark, the Netherlands, Sweden, Austria, Belgium, and elsewhere.

We are also subject to federal, state, provincial, and foreign laws regarding cybersecurity, privacy, and the protection of data. Some jurisdictions have enacted laws requiring companies to notify individuals of data security breaches involving certain types of personal information data and our agreements with certain merchants require us to notify them in the event of a security incident. Additionally, some jurisdictions as well as our contracts with certain merchants require us to use industry-standard or reasonable measures to safeguard personal information or confidential information, and thereby mitigate the risk of a security incident.

In addition, our reputation and brand may be negatively affected by the actions of merchants or their users or partners that are deemed to be hostile, offensive, inappropriate or unlawful. While we use technology to monitor for compliance with and eligibility for certain Shopify offerings, we do not proactively and comprehensively monitor or review the appropriateness of all content on all of our merchants’ shops in connection with our services, and we do not have control over the activities in which merchants’ buyers engage. While we have adopted policies regarding illegal or offensive use of our platform, merchants or their customers could nonetheless engage in these activities without our knowledge. The safeguards we have in place may not be sufficient to avoid harm to our reputation and brand, especially if such hostile,

22

offensive or inappropriate use was high profile, which could adversely affect our ability to expand our merchant subscription base, could attract regulatory scrutiny or litigation threats, and could harm our business and financial results.

We could also be subject to liability related to the content on merchants’ shops, products and services sold by merchants, or other activities of our merchants. In many jurisdictions, new laws, regulations or rules relating to the liability of providers of online services for activities of their customers and other third parties are currently being proposed and debated, or otherwise being tested in court. This liability could relate to a number of different types of legal claims or concerns, including concerns relating to unfair competition, copyright and trademark infringement, defamation, invasion of privacy or other torts, products liability, and other theories based on the nature of the relevant goods, services, or content. Any legislation, court ruling or other governmental regulation or action that imposes liability on providers of online services in connection with the activities of their customers or their customers’ users could harm our business. In such circumstances we may also be subject to liability under applicable law, which may not be fully mitigated by our terms of service. Any liability attributed to us could adversely affect our brand, reputation, ability to expand our subscriber base, and financial results.

GENERAL DEVELOPMENT OF THE BUSINESS

As of December 31, 2021, the Company operated in a single operating and reportable segment.

Three-Year History

In the fourth quarter of 2021:

Shopify launched our integrated retail hardware with payments to retail merchants in the Netherlands.

Shopify launched the Shopify Global ERP Program, which allows select ERP partners, initially including Microsoft, Oracle NetSuite, Infor, Acumatica, and Brightpearl, to build direct integrations into the Shopify App Store.

Shopify launched the Spotify channel, enabling artist-entrepreneurs on Spotify to connect their Spotify for Artists accounts with their Shopify online stores, where they can sync their product catalogues and seamlessly showcase products directly on their Spotify profile.

In the third quarter of 2021:

Shopify launched Shopify Markets, a product that makes cross-border commerce easier for entrepreneurs by enabling merchants to enter new markets, and increase buyer trust and conversion with tailored experiences for each market.

Shopify began rolling out Shopify Balance, our money management product, to merchants in the United States.

Shopify introduced TikTok Shopping to merchants, enabling merchants with a TikTok For Business account to add products that link directly to their online store checkout.

23

Shopify launched our All-New POS Pro software for Android devices, and launched our integrated retail hardware with payments to retail merchants in Germany and New Zealand.

Shopify opened a brick and mortar space in New York City featuring Shopify’s products, services, and technology, and serving as a hub where merchants can receive hands-on support, inspiration, and education to help grow their business.

Shopify launched Shopify Shipping in the United Kingdom, enabling British merchants to easily purchase shipping labels directly from the Shopify merchant admin, saving them time and money.

Shopify eliminated its revenue share on the first million dollars made by app and theme developer partners annually in the Shopify App Store and Shopify Theme Store, respectively, extending more generous terms in order to increase our support for developers, expand what gets built on Shopify, and attract the best developers in the world to support Shopify’s mission.

In the second quarter of 2021:

Shopify introduced a new retail integrated card reader with payments using our All-New POS software in the United Kingdom, Ireland, and Australia.

Shopify made Shop Pay Installments, a ‘buy now, pay later’ product that lets merchants offer their buyers more payment choice and flexibility at checkout, generally available to all eligible merchants in the United States.

Shopify announced that Shop Pay will become available to all merchants selling in the United States on Facebook and Google, even if they don’t use Shopify’s online store.

In the first quarter of 2021:

Shopify sold 1,180,000 Class A subordinate voting shares at a price to the public of $1,315 per share for aggregate gross proceeds, before underwriting discounts and offering costs, of $1,551,700,000, to strengthen its balance sheet and provide flexibility to fund its growth strategies.

Shopify announced, on March 9, 2021, that it had purchased more Direct Air Capture carbon removal (i.e. atmospheric carbon dioxide stored underground and not for enhanced oil recovery or any other type of fossil fuel extraction) than any other company in history with our agreement to purchase 10,000 tonnes of removal from Carbon Engineering in addition to our previous commitment to purchase 5,000 tonnes from Climeworks.

In the fourth quarter of 2020:

Shopify began collecting subscription revenue for our Retail POS Pro subscription offering, which was launched in the second quarter.

Shopify announced a collaboration with Operation HOPE to support that organization’s goal to create one million new Black-owned businesses in the U.S. by 2030. Shopify intends to provide up to $130 million of in-kind resources to support Operation HOPE’s efforts to reduce systemic barriers to entry to entrepreneurship historically faced by the Black community.

24

Shopify launched the TikTok channel, enabling merchants to market their products using TikTok for Business. Merchants are able to create in-feed video ads that autoplay between videos while users scroll through their For You page.

Shopify partnered with the Victoria State government in Australia to participate in the Small Business Digital Adaptation Program and the New York State government to participate in Empire State Digital. The aim of both programs is to more easily bring small businesses online and help them adapt to a digital economy.

In the third quarter of 2020:

Shopify launched Shopify Payments in Belgium, enabling iDEAL as a local payment method and supporting Bancontact debit payments, expanding the availability of Shopify Payments to 17 countries.

Shopify announced a partnership with the Government of Canada through the ‘Go Digital Canada’ program to bring thousands of small Canadian businesses online and help them adapt to a digital economy.

Shopify Studios debuted its first series with a major television network. ‘I Quit’, which aired on the Discovery channel, is a premium docuseries featuring real-life entrepreneurs who give up their “9-5” jobs to focus 100% on launching their own businesses.

Shopify issued $920,000,000 aggregate principal amount of 0.125% convertible senior notes due 2025 and sold 1,265,000 Class A subordinate voting shares at a price to the public of $900 per share for aggregate gross proceeds, before underwriting discounts and offering costs, of $1,138,500,000, to strengthen our balance sheet and provide flexibility to fund our growth strategies.

In the second quarter of 2020:

Shopify held its first virtual partner event, Shopify Reunite, where we announced new products and features to help our merchants adapt to the future of commerce.

Shopify made the new Shopify Plus Admin generally available to all Shopify Plus merchants, enabling them to operate their business as an organization by managing multiple stores, analytics, staff accounts, user permissions, and automation tools like Shopify Flow in one place.

Shopify introduced the Facebook Shops channel, enabling Shopify merchants to customize and merchandise their storefronts within Facebook and Instagram through Facebook Shops, while managing their products, inventory orders, and fulfillment directly within Shopify.

Shopify launched the Walmart channel, enabling Shopify merchants to sell their products on Walmart.com.

Shopify launched the all-new Shopify POS, a faster, more intuitive, and more scalable POS software designed to meet the needs of our most complex brick and mortar retailers.

Shopify launched the Shopify Tap & Chip Card Reader in Canada, bringing contactless payments hardware to Canadian retailers using Shopify POS.

25

Shopify launched Shop, an innovative mobile shopping app that creates a more intuitive online shopping experience, bringing together our expertise in commerce and proven features from Shop Pay, our accelerated checkout, and Arrive, an app to track online orders.

Shopify launched Shopify Capital in Canada, expanding the availability of Shopify Capital to three countries.

Shopify launched Shopify Shipping in Australia partnering with courier services company, Sendle.

Shopify launched Shopify Payments in Austria, expanding the availability of Shopify Payments to 16 countries.

Shopify sold 2,127,500 Class A subordinate voting shares at a price to the public of $700 per share for aggregate gross proceeds, before underwriting discounts and offering costs, of $1,489,250,000, to strengthen its balance sheet to support further growth initiatives.

In the first quarter of 2020:

Shopify introduced a number of initiatives to support our merchants and protect our stakeholders during the ongoing COVID-19 pandemic, including an extended 90-day free trial for all new standard plan signups, availability of gift card capabilities to merchants on all plans, and introduction of local in-store/curbside pickup and delivery.

Shopify launched Shopify Capital in the UK, working with a UK-based partner, expanding the availability of Shopify Capital to two countries.

Shopify opened an R&D Centre in Ottawa, Canada to trial new robotics and fulfillment technologies and initially fulfill Canadian-based orders.

Shopify joined the Libra Association, an independent not-for-profit membership association collaborating to build a simple, inclusive, and global cryptocurrency.