UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-K

| ☒ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(D) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2014

| ☐ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(D) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission file number: 001-36267

BLUE BIRD CORPORATION

(Exact name of registrant as specified in its charter)

| Delaware | 46-3891989 | |

(State

or other jurisdiction of |

(I.R.S. Employer Identification Number) |

402

Blue Bird Boulevard |

31030 | |

| (Address of principal executive offices) | (Zip Code) |

Issuer’s telephone number: (478) 822-2130

Securities registered pursuant to Section 12(b) of the Act:

Title of Each Class: |

Name of Each Exchange on Which Registered: | |

| Common Stock, par value $.0001 per share | The NASDAQ Stock Market LLC | |

| Warrants to purchase Common Stock | The NASDAQ Stock Market LLC |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐ No ☒

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Exchange Act. Yes ☐ No ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ☒

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See definition of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer ☐ | Accelerated filer ☐ |

| Non-accelerated filer ☒ | Smaller reporting company ☐ |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

The aggregate market value of the shares of common stock outstanding, other than shares held by persons who may be deemed affiliates of the registrant, computed by reference to the closing sales price for the registrant’s common stock on June 30, 2014, as reported on the Nasdaq Capital Market, was $111,992,300. As of February 19, 2015, there were 14,375,000 shares of common stock, par value $.0001 per share, of the registrant issued and outstanding.

Documents incorporated by reference: None

TABLE OF CONTENTS

| PART I | |||

| Item 1. | Business | 4 | |

| Item 1A. | Risk Factors | 22 | |

| Item 2. | Properties | 44 | |

| Item 3. | Legal Proceedings | 44 | |

| Item 4. | Mine Safety Disclosure | 44 | |

| PART II | |||

| Item 5. | Market For Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities | 45 | |

| Item 6. | Selected Financial Data | 46 | |

| Item 7. | Management’s Discussion and Analysis of Financial Condition and Results of Operations | 47 | |

| Item 7A. | Quantitative and Qualitative Disclosures About Market Risk | 51 | |

| Item 8. | Financial Statements and Supplementary Data | 51 | |

| Item 9. | Changes in and Disagreements with Accountants on Accounting and Financial Disclosure | 52 | |

| Item 9A. | Controls and Procedures | 53 | |

| Item 9B. | Other Information | 53 | |

| PART III | |||

| Item 10. | Directors, Executive Officers and Corporate Governance | 54 | |

| Item 11. | Executive Compensation | 59 | |

| Item 12. | Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters | 60 | |

| Item 13. | Certain Relationships and Related Transactions, and Director Independence | 62 | |

| Item 14. | Principal Accountant Fees and Services | 63 | |

| PART IV | |||

| Item 15. | Exhibits and Financial Statement Schedules | 64 | |

| 2 |

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K (the “Report”) includes forward-looking statements within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934. These forward-looking statements can be identified by the use of forward-looking terminology, including the words “believes,” “estimates,” “anticipates,” “expects,” “intends,” “plans,” “may,” “will,” “potential,” “projects,” “predicts,” “continue,” or “should,” or, in each case, their negative or other variations or comparable terminology. There can be no assurance that actual results will not materially differ from expectations. Such statements include, but are not limited to, any statements relating to our ability to consummate any acquisition or other business combination and any other statements that are not statements of current or historical facts. These statements are based on management’s current expectations, but actual results may differ materially due to various factors, including, but not limited to:

| ● | our ability to complete our initial business combination with The Traxis Group B.V. or another entity; |

| ● | our success in retaining or recruiting, or changes required in, our officers, key employees or directors following our initial business combination; |

| ● | our officers and directors allocating their time to other businesses and potentially having conflicts of interest with our business or in approving our initial business combination, as a result of which they would then receive expense reimbursements; |

| ● | our potential ability to obtain additional financing to complete our initial business combination; |

| ● | our pool of prospective target businesses; |

| ● | failure to maintain the listing on, or the delisting of our securities from, Nasdaq or an inability to have our securities listed on Nasdaq or another national securities exchange following our initial business combination; |

| ● | the ability of our officers and directors to generate a number of potential investment opportunities; |

| ● | our public securities’ potential liquidity and trading; |

| ● | the lack of a market for our securities; |

| ● | the use of proceeds not held in the trust account or available to us from interest income on the trust account balance; or |

| ● | our financial performance. |

The forward-looking statements contained in this Report are based on our current expectations and beliefs concerning future developments and their potential effects on us. Future developments affecting us may not be those that we have anticipated. These forward-looking statements involve a number of risks, uncertainties (some of which are beyond our control) and other assumptions that may cause actual results or performance to be materially different from those expressed or implied by these forward-looking statements. These risks and uncertainties include, but are not limited to, those factors described under the heading “Risk Factors.” Should one or more of these risks or uncertainties materialize, or should any of our assumptions prove incorrect, actual results may vary in material respects from those projected in these forward-looking statements. We undertake no obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise, except as may be required under applicable securities laws.

These risks and others described under “Risk Factors” may not be exhaustive.

By their nature, forward-looking statements involve risks and uncertainties because they relate to events and depend on circumstances that may or may not occur in the future. We caution you that forward-looking statements are not guarantees of future performance and that our actual results of operations, financial condition and liquidity, and developments in the industry in which we operate may differ materially from those made in or suggested by the forward-looking statements contained in this Report. In addition, even if our results of operations, financial condition and liquidity, and developments in the industry in which we operate are consistent with the forward-looking statements contained in this Report, those results or developments may not be indicative of results or developments in subsequent periods.

| 3 |

Introductory Note

On February 24, 2015, the registrant consummated the previously announced business combination (the “Business Combination”) pursuant to which the registrant acquired all of the outstanding capital stock of School Bus Holdings Inc. (“SBH”) from The Traxis Group B.V. (the “Seller”), in accordance with the purchase agreement, dated as of September 21, 2014, by and between the registrant and the Seller, as amended (as amended, the “Purchase Agreement”). SBH, through its subsidiaries, conducts its business under the “Blue Bird” name.

In connection with the closing of the Business Combination, the registrant changed its name from Hennessy Capital Acquisition Corp. to Blue Bird Corporation. This Annual Report on Form 10-K principally describes the business and operations of the registrant prior to the Business Combination. Unless the context otherwise requires, “we,” “us,” “our,” “Hennessy”, “Hennessy Capital” and “the Company” refer to the registrant prior to the closing of the Business Combination.

The business and operations of SBH, conducted under the name “Blue Bird”, are described in the registrant’s proxy statement dated January 20, 2015 and will be further described in a Current Report on Form 8-K to be filed by the registrant on or before March 2, 2015.

PART I

Item 1. Business

Introduction

Until we consummated the Business Combination, we were a blank check company. We were incorporated on September 24, 2013 as a Delaware corporation formed for the purpose of effecting a merger, capital stock exchange, asset acquisition, stock purchase, reorganization or similar business combination with one or more businesses.

While we may pursue an acquisition opportunity in any business industry or sector, we intend to focus on industries that complement our management team’s background, and to capitalize on the ability of our management team to identify, acquire and operate a business, focusing on the diversified industrial manufacturing and distribution sector in the United States (which may include a business based in the United States which has operations or opportunities outside the United States).

Business Opportunity Overview

Our acquisition and value creation strategy is to identify, acquire and, after our initial business combination, to build, a diversified industrial manufacturing or distribution business. Diversified industrial manufacturers and distributors are companies that either manufacture or distribute a broad range of products for various customers and end use markets. Our strategy is based on our management’s belief that an industrial “renaissance” is now underway in the United States. Our management believes that this resurgence is primarily the result of three critical cost factors: labor, natural gas energy (as represented by natural gas prices) and logistics, each of which management believes is quite favorable to the United States when compared with advanced manufacturing nations and increasingly competitive when compared with emerging manufacturing nations such as China.

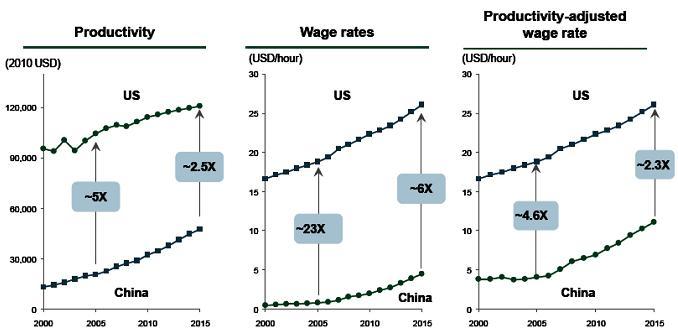

| ● | According to Boston Consulting Group, or BCG, the United States has a labor cost advantage compared to other major manufacturing economies and is becoming increasingly competitive with emerging economies such as China: Productivity-adjusted labor costs in the United States are 50% to 80% of those in other major manufacturing economies such as Japan, Germany, France, the U.K., and Italy. In China, the average wage has increased by 15-20% annually compared to the United States at only 2%. The average American worker is also 3x more productive than their Chinese counterpart driving an even further deterioration of China’s advantage on a productivity-adjusted basis. |

Source: “Made in America Again... The New Economics of Global Manufacturing”, BCG (January 16th, 2013).

| 4 |

| ● | We believe that energy costs in the United States will become comparatively cheaper, especially with the recent discoveries of abundant shale gas and new technologies in oil and gas extraction: The United States has a significant energy cost advantage over other advanced economies which can result in lower utility and energy bills and raw material input prices for certain industries. In addition to increased manufacturing costs, just-in-time inventory requirements and shorter product life cycles necessitate that production and end-markets be co-located. |

World

LNG Landed Prices (USD / MMBtu)

Source: World LNG Prices — Federal Energy Regulatory Commission (FERC) Market Oversight, December 2014

Note: Prices estimated for January 2015; U.S. price estimates are an average of Cove Point and Lake Charles price estimates.

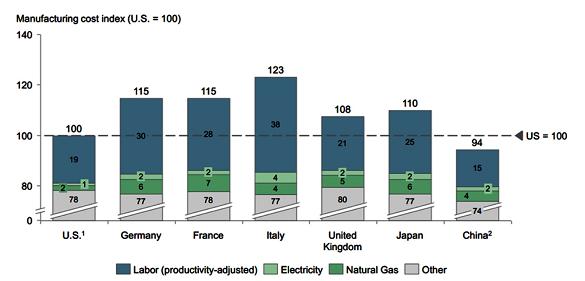

| ● | We believe these factors will come together and leave the United States with an advantage on a total landed cost basis, as represented by Average Manufacturing Cost Structures: According to BCG, taking into account items such as increased productivity-adjusted wage costs, energy costs and supply chain costs, the United States is expected to have lower manufacturing costs than other major advanced manufacturing nations and become increasingly competitive with China. It is estimated that China will retain only a 4% cost advantage over the United States. |

Top

25 Exporting Nation Average Manufacturing Costs: 2014 Projections (Index U.S. = 100)

1 Adjusted for productivity.

Source: US Census; Bureau of Labor Statistics; Bureau of Economic Analysis; ILO; Euromonitor International; Economist Intelligence Unit; “The Shifting Economics of Global Manufacturing”, BCG (August 2014).

| 5 |

Note: The index covers four direct costs only. No difference is assumed for other costs, such as raw-material inputs and machine and tool depreciation. Cost structure is calculated as a weighted average across all industries.

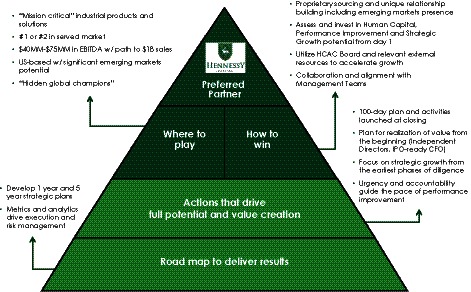

Business Strategy Summary

The chart below summarizes the origination,

investment management and value creation strategy that our Chairman and Chief Executive Officer, Daniel J. Hennessy, has developed

for Hennessy Capital LLC, an affiliate of our sponsor, and which we would seek to replicate:

Competitive Strengths

Mr. Daniel J. Hennessy. Hennessy Capital is the managing member of our sponsor and was founded by Daniel J. Hennessy, our Chairman and Chief Executive Officer in 2013. Mr. Hennessy is also a partner at Code Hennessy & Simmons (n/k/a CHS Capital or “CHS”) a middle market private equity investment firm he co-founded in 1988. Over a 25 year period, CHS invested $2.8 billion in 395 operating companies with aggregate revenues of approximately $15 billion. Mr. Hennessy serves as a member of CHS’s Investment Committee, and served as the lead partner for a number of CHS’s industrial, infrastructure and energy industry platform company investments. Most recently he originated and co-led the portfolio company acquisitions of Thermon Group Holdings (NYSE: THR), or Thermon, in 2010 and Dura-Line Holdings, or Dura-Line, in 2012 for CHS Private Equity V LP. Thermon designs and manufactures electric heat-tracing and thermal control systems for energy and process industries. Dura-Line manufactures high density polyethylene (HDPE) conduit and pressure pipe solutions for telecom, datacom, water infrastructure and upstream energy and natural gas distribution markets. Mr. Hennessy has over 25 years of middle-market private equity investment experience, dedicated almost entirely to investments in industrial manufacturing and distribution operating companies. He has initiated and overseen numerous add-on acquisitions, divestitures, IPOs and debt capital markets issues for CHS-owned companies and is well known by the most active middle-market investment banks and debt financing sources that will be called upon to assist us in executing on our strategy.

Our board of directors. We have assembled a group of independent directors that bring us public company governance, executive leadership, operations oversight, private equity investment management and capital markets experience. Our board members have extensive experience, having served as directors, CEOs, CFOs or in other executive and advisory capacities for numerous publicly-listed and privately-owned companies. Our directors have experience with acquisitions, divestitures and corporate strategy and implementation, which we believe will be of significant benefit to us as we evaluate potential acquisition or merger candidates, including SBH as described below, as well as following the completion of our initial business combination.

Our network of third party advisors. We utilize what our management believes is an accomplished and proven network of third party advisors to help assist with target company evaluation, due diligence and implementation of value creation programs and activities following our initial business combination. This network has assisted Mr. Hennessy in executing on human capital, performance improvement, strategic growth and equity capital markets initiatives. We believe this combination of resources is unique and provides us with a truly differentiated value proposition for investors, sellers, target companies and their management teams.

| 6 |

Initial Business Combination

Nasdaq rules require that our initial business combination must be with one or more target businesses that together have a fair market value equal to at least 80% of the balance in the trust account (less any deferred underwriting commissions and taxes payable on interest earned) at the time of our signing a definitive agreement in connection with our initial business combination. If our board is not able to independently determine the fair market value of the target business or businesses, we will obtain an opinion from an independent investment banking firm that is a member of the Financial Industry Regulatory Authority, or FINRA, with respect to the satisfaction of such criteria.

We anticipate structuring our initial business combination so that the post-transaction company in which our public stockholders own shares will own or acquire 100% of the equity interests or assets of the target business or businesses. We may, however, structure our initial business combination such that the post-transaction company owns or acquires less than 100% of such interests or assets of the target business in order to meet certain objectives of the target management team or shareholders or for other reasons, but we will only complete such business combination if the post-transaction company owns or acquires 50% or more of the outstanding voting securities of the target or otherwise acquires a controlling interest in the target sufficient for it not to be required to register as an investment company under the Investment Company Act of 1940, as amended, or the Investment Company Act. Even if the post-transaction company owns or acquires 50% or more of the voting securities of the target, our stockholders prior to the business combination may collectively own a minority interest in the post-transaction company, depending on valuations ascribed to the target and us in the business combination transaction. For example, we could pursue a transaction in which we issue a substantial number of new shares in exchange for all of the outstanding capital stock of a target. In this case, we would acquire a 100% controlling interest in the target. However, as a result of the issuance of a substantial number of new shares, our stockholders immediately prior to our initial business combination could own less than a majority of our outstanding shares subsequent to our initial business combination. If less than 100% of the equity interests or assets of a target business or businesses are owned or acquired by the post-transaction company, the portion of such business or businesses that is owned or acquired is what will be valued for purposes of the 80% of net assets test. If the business combination involves more than one target business, the 80% of net assets test will be based on the aggregate value of all of the target businesses.

Consistent with this strategy, we have identified the following general criteria and guidelines that we believe are important in evaluating prospective target businesses. We have and will continue to use these criteria and guidelines in evaluating acquisition opportunities, but we may decide to enter into our initial business combination with a target business that does not meet these criteria and guidelines.

| ● | Middle-Market Business. We seek to acquire one or more businesses with an enterprise value of approximately $200,000,000 to $500,000,000, determined in the sole discretion of our officers and directors according to reasonably accepted valuation standards and methodologies. We believe that the middle market segment provides the greatest number of opportunities for investment and is the market consistent with our sponsor’s previous investment history. This segment is where we believe we have the strongest network to identify opportunities. | |

| ● | Established Companies with Proven Track Records. We seek to acquire established companies with consistent historical financial performance. We focus on companies with a history of strong operating and financial results and strong fundamentals. We do not intend to acquire start-up companies or companies with recurring negative free cash flow. | |

| ● | Companies with, or with the Potential For, Strong Free Cash Flow Generation. We seek to acquire one or more businesses that already have, or have the potential to generate, consistent, stable and increasing free cash flow. We focus on one or more businesses that have predictable revenue streams. | |

| ● | Strong Competitive Position. We focus on targets that have a leading, growing or niche market position in their respective industries. We analyze the strengths and weaknesses of target businesses relative to their competitors. We seek to acquire a business that demonstrates advantages when compared to their competitors, which may help to protect their market position and profitability. |

| 7 |

| ● | Experienced Management Team. We seek to acquire one or more businesses with a complete, experienced management team that provides a platform for us to further develop the acquired business’ management capabilities. We seek to partner with a potential target’s management team and expect that the operating and financial abilities of our executive team and board will complement their own capabilities. | |

| ● | Companies with Revenue and Earnings Growth or Potential for Revenue and Earnings Growth. We seek to acquire one or more businesses that have achieved or have the potential for significant revenue and earnings growth through a combination of organic growth, new product markets and geographies, increased production capacity, expense reduction, synergistic add-on acquisitions and increased operating leverage. | |

| ● | Sectors Exhibiting Secular Growth or with Potential for Cyclical Uptick. We focus on targets in sectors which exhibit positive secular growth or potential for near-term cyclical uptick. We identify sectors that have demonstrated strong positive growth in recent years, possess drivers for continued growth and are strategically positioned to benefit from upswings in their respective industry cycles. | |

| ● | Benefit from Being a Public Company. We intend to acquire a company that will benefit from being publicly traded and can effectively utilize the broader access to capital and public profile that are associated with being a publicly traded company. |

These criteria are not intended to be exhaustive. Any evaluation relating to the merits of a particular initial business combination may be based, to the extent relevant, on these general guidelines as well as other considerations, factors and criteria that our management may deem relevant.

Over the course of their careers, the members of our management team and board of directors have developed a broad network of contacts and corporate relationships that we believe will serve as a useful source of investment opportunities. This network has been developed through our management team’s:

| ● | experience in sourcing, acquiring, operating, developing, growing, financing and selling businesses; and |

| ● | experience in executing transactions under varying economic and financial market conditions. |

This network has provided our management team with a flow of referrals that have resulted in numerous transactions. We believe that the network of contacts and relationships of our management team is an important source of investment opportunities. In addition, we anticipate that target business candidates will be brought to our attention from various unaffiliated sources, including investment market participants, private equity groups, investment banking firms, consultants, accounting firms and large business enterprises.

Certain members of our management team have spent significant portions of their careers working with businesses in the diversified industrial manufacturing and distribution sector, and have developed a wide network of professional services contacts and business relationships in that industry. The members of our board of directors also have significant executive management and public company experience with diversified industrial manufacturing and distribution companies.

In evaluating a prospective target business we expect to conduct a thorough due diligence review which will encompass, among other things, meetings with incumbent management and employees, document reviews, inspection of facilities, as well as a review of financial and other information which will be made available to us.

We are not prohibited from pursuing an initial business combination with a company that is affiliated with our sponsor, officers or directors. In the event we seek to complete our initial business combination with a company that is affiliated with our sponsor, officers or directors, we, or a committee of independent directors, will obtain an opinion from an independent investment banking firm which is a member of FINRA, that our initial business combination is fair to our company from a financial point of view.

Members of our management team directly or indirectly own our common stock and warrants, and, accordingly, may have a conflict of interest in determining whether a particular target business is an appropriate business with which to effectuate our initial business combination. Further, each of our officers and directors may have a conflict of interest with respect to evaluating a particular business combination if the retention or resignation of any such officers and directors was included by a target business as a condition to any agreement with respect to our initial business combination.

| 8 |

Each of our officers and directors presently has, and any of them in the future may have additional, fiduciary or contractual obligations to another entity pursuant to which such officer or director is required to present a business combination opportunity to such entity. Accordingly, if any of our officers or directors becomes aware of a business combination opportunity which is suitable for an entity to which he or she has then current fiduciary or contractual obligations, he or she will honor his or her fiduciary or contractual obligations to present such business combination opportunity to such entity, and only present it to us if such entity rejects the opportunity. We do not believe, however, that the fiduciary duties or contractual obligations of our executive officers or directors will materially affect our ability to complete our business combination.

Our sponsor, executive officers and directors have agreed, pursuant to a written letter agreement, not to participate in the formation of, or become an officer or director of, any other blank check company until we have entered into a definitive agreement regarding our initial business combination or we have failed to complete our initial business combination by October 23, 2015 (or January 23, 2016, as applicable). None of our officers or directors has been involved with any blank check companies or special purpose acquisition corporations in the past.

Business Combination with School Bus Holdings Inc.

On September 21, 2014, we entered into a stock purchase agreement, which was subsequently amended on February 10, 2015 and February 19, 2015 (as so amended, the “Purchase Agreement”) with The Traxis Group B.V. (sometimes referred to as “Seller”), a limited liability company existing under the laws of the Netherlands and an entity that is majority owned by funds affiliated with Cerberus Capital Management, L.P. The Purchase Agreement provides for the acquisition by the Company from Seller of all of the outstanding shares of capital stock of School Bus Holdings Inc. (“SBH”), which, through its subsidiaries, conducts its business under the “Blue Bird” name (the “Business Combination”). Pursuant to the Purchase Agreement, the aggregate equity purchase price for the Business Combination is $220.0 million (the “Total Purchase Price”). The Company will pay the Total Purchase Price partially in cash and partially in common stock. Following the closing of the Business Combination, SBH will become a wholly-owned subsidiary of the Company.

Consummation of the transactions contemplated by the Purchase Agreement is subject to customary conditions of the respective parties, including the approval of the Business Combination by the Company’s stockholders in accordance with the Company’s amended and restated certificate of incorporation and the completion of a redemption offer whereby the Company will be providing its public stockholders with the opportunity to redeem their shares of Company common stock for cash equal to their pro rata share of the aggregate amount on deposit in the Company’s trust account.

The Purchase Agreement and related agreements are further described in the Forms 8-K filed by the Company on September 24, 2014, February 11, 2015 and February 19, 2015. For additional information regarding the Purchase Agreement and the Business Combination, see the Definitive Proxy Statement on Schedule 14A filed by the Company on January 20, 2015, as amended and supplemented by the proxy supplement filed on February 11, 2015.

Other than as specifically discussed, this Report does not assume the closing of the Business Combination.

Our

executive offices are located at 700 Louisiana Street, Suite 900, Houston, Texas 7702 and our telephone number at that location

is (713) 300-8242.

Status as a Public Company

We believe our structure will make us an attractive business combination partner to target businesses. As an existing public company, we offer a target business an alternative to the traditional initial public offering through a merger or other business combination. In this situation, the owners of the target business would exchange their shares of stock in the target business for shares of our stock or for a combination of shares of our stock and cash, allowing us to tailor the consideration to the specific needs of the sellers. Although there are various costs and obligations associated with being a public company, we believe target businesses will find this method a more certain and cost effective method to becoming a public company than the typical initial public offering. In a typical initial public offering, there are additional expenses incurred in marketing, road show and public reporting efforts that may not be present to the same extent in connection with a business combination with us.

| 9 |

Furthermore, once a proposed business combination is completed, the target business will have effectively become public, whereas an initial public offering is always subject to the underwriters’ ability to complete the offering, as well as general market conditions, which could prevent the offering from occurring. Once public, we believe the target business would then have greater access to capital and an additional means of providing management incentives consistent with stockholders’ interests. It can offer further benefits by augmenting a company’s profile among potential new customers and vendors and aid in attracting talented employees.

We are an “emerging growth company,” as defined in the JOBS Act. We will remain an emerging growth company until the earlier of (1) the last day of the fiscal year (a) following the fifth anniversary of the completion of our initial public offering, (b) in which we have total annual gross revenue of at least $1.0 billion, or (c) in which we are deemed to be a large accelerated filer, which means the market value of our common stock that is held by non-affiliates exceeds $700 million as of the prior June 30th, and (2) the date on which we have issued more than $1.0 billion in non-convertible debt during the prior three-year period.

Financial Position

With funds available for a business combination of approximately $111,262,000 assuming no redemptions and after payment of up to approximately $3,738,000 of deferred underwriting fees, we offer a target business a variety of options such as creating a liquidity event for its owners, providing capital for the potential growth and expansion of its operations or strengthening its balance sheet by reducing its debt ratio. Because we are able to complete our business combination using our cash, debt or equity securities, or a combination of the foregoing, we have the flexibility to use the most efficient combination that will allow us to tailor the consideration to be paid to the target business to fit its needs and desires. However, we have not taken any steps to secure third party financing and there can be no assurance it will be available to us.

Significant Activities Since Inception

The registration statement for our initial public offering was declared effective January 16, 2014. On January 23, 2014, the Company consummated its initial public offering of 11,500,000 units (“Public Units”), including the full exercise of the underwriters’ overallotment option of 1,500,000 units (the “Over-Allotment Units”; collectively with the Public Units, the “Units”). Each Unit consists of one share of common stock, $0.0001 par value per share, and one warrant to purchase one-half of one share of common stock at an exercise price of $5.75 per half share ($11.50 per full share). The Units were sold at an offering price of $10.00 per Unit, generating gross proceeds of $115,000,000.

Simultaneously with the consummation of the initial public offering and the sale of the Overallotment Units, the Company consummated the private placement (“Private Placement”) of 12,125,000 warrants (“Placement Warrants”) at a price of $0.50 per Placement Warrant, generating total proceeds of approximately $6,063,000. The Placement Warrants which were purchased by Hennessy Capital Partners I, LLC, are substantially similar to the warrants underlying the Public Units, except that if held by the original holder or their permitted assigns, they (i) may be exercised for cash or on a cashless basis, (ii) are not subject to being called for redemption and (iii) subject to certain limited exceptions, will be subject to transfer restrictions until 30 days following the consummation of the Company’s initial business combination. If the Placement Warrants are held by holders other than its initial holders, the Placement Warrants will be redeemable by the Company and exercisable by the holders on the same basis as the warrants included in the Units sold in the initial public offering.

Subsequent to the offering, a total of $115,000,000 of the net proceeds from the initial public offering, the sale of the Overallotment Units and the Private Placement were placed in a trust account established for the benefit of the Company’s public stockholders at JP Morgan Chase Bank, N.A., with Continental Stock Transfer & Trust Company acting as trustee. Except for the withdrawal of interest to pay taxes, for the most part, none of the funds held in the trust account will be released until the earlier of the completion of the Company’s initial business combination or the redemption of 100% of the common stock issued by the Company in the initial public offering if the Company is unable to consummate an initial business combination by October 23, 2015 (or January 23, 2016, as applicable).

On January 17, 2014, our Units commenced trading on Nasdaq under the symbol “HCACU”. Holders of our Units were able to separately trade the common stock and warrants included in such Units commencing on March 10, 2014 and the trading in the Units has continued under the symbol HCACU. The common stock and warrants are listed on Nasdaq under the symbols “HCAC” and “HCACW”, respectively.

| 10 |

We will provide our stockholders with the opportunity to redeem their shares of common stock upon the consummation of our initial business combination at a per-share price, payable in cash, equal to the aggregate amount then on deposit in the trust account, including any amounts representing interest earned on the trust account, less any interest released to us for the payment of taxes, divided by the number of then outstanding public shares, subject to the limitations described herein. The amount in the trust account is initially anticipated to be approximately $10.00 per public share. There will be no redemption rights upon the consummation of our initial business combination with respect to our warrants. Our initial stockholders have agreed to waive their redemption rights with respect to any public shares they may acquire following our initial public offering, in connection with a tender offer or stockholder vote. Each of our initial stockholders and Hennessy Capital Partners I LLC (as applicable) has agreed to waive its redemption rights with respect to the founder shares (i) in connection with the consummation of a business combination, (ii) if we fail to consummate our initial business combination by October 23, 2015 (or January 23, 2016, as applicable), and (iii) upon our liquidation prior October 23, 2015 (or January 23, 2016, as applicable).

On September 21, 2014, we entered into a Purchase Agreement with the Seller for the acquisition by the Company from Seller of all of the outstanding shares of capital stock of SBH, which, through its subsidiaries, conducts its business under the “Blue Bird” name. We are seeking stockholder approval for the Business Combination and expect to consummate the Business Combination in the first quarter of 2015. For more information about SBH and the Business Combination, see the section entitled “Business Combination with School Bus Holdings Inc.,” our Forms 8-K filed on September 24, 2014, February 11, 2015 and February 19, 2015 and our Definitive Proxy Statement on Schedule 14A filed on January 20, 2015, as amended and supplemented by the proxy supplement filed on February 11, 2015.

Effecting our Initial Business Combination

The section below discusses factors relevant to the Company’s effecting any initial business combination. This general discussion may not apply in all respects in the context of the Business Combination. For more specific information concerning the Business Combination, see the section entitled “Business Combination with School Bus Holdings Inc.,” our Forms 8-K filed on September 24, 2014, February 11, 2015 and February 19, 2015 and our Definitive Proxy Statement on Schedule 14A filed on January 20, 2015, as amended and supplemented by the proxy supplement filed on February 11, 2015. There can be no assurance that the Business Combination will be consummated.

General

We are not presently engaged in, and we will not engage in, any operations until the consummation of an initial business combination. We intend to effectuate our initial business combination using cash from the proceeds of our initial public offering and the private placement of the private placement warrants, our capital stock, debt or a combination of these as the consideration to be paid in our initial business combination. We may seek to complete our initial business combination with a company or business that may be financially unstable or in its early stages of development or growth, which would subject us to the numerous risks inherent in such companies and businesses.

If our initial business combination is paid for using stock or debt securities, or not all of the funds released from the trust account are used for payment of the consideration in connection with our business combination or used for redemptions of purchases of our common stock, we may apply the balance of the cash released to us from the trust account for general corporate purposes, including for maintenance or expansion of operations of the post-transaction company, the payment of principal or interest due on indebtedness incurred in completing our initial business combination, to fund the purchase of other companies or for working capital.

We may seek to raise additional funds through a private offering of debt or equity securities in connection with the completion of our initial business combination, and we may effectuate our initial business combination using the proceeds of such offering rather than using the amounts held in the trust account. Subject to compliance with applicable securities laws, we would complete such financing only simultaneously with the completion of our business combination. In the case of an initial business combination funded with assets other than the trust account assets, our tender offer documents or proxy materials disclosing the business combination would disclose the terms of the financing and, only if required by law, we would seek stockholder approval of such financing. There are no prohibitions on our ability to raise funds privately or through loans in connection with our initial business combination.

| 11 |

Origination and Sourcing of Target Business Opportunities

We believe our management team’s extensive private equity investment and transaction experience, along with relationships with intermediaries and companies, will provide us with a substantial number of potential business combination targets. Over the course of their careers, the members of our board and management team have developed a broad network of contacts and corporate relationships around the world. This network has been developed over the course of 25 years, in the case of our Chairman and Chief Executive Officer.

Specifically our Chairman and Chief Executive Officer has evaluated hundreds of industrial sector targets in the last three years on behalf of CHS Capital, which has led to two platform company acquisitions: Thermon and Dura-Line. In addition, numerous add-on acquisition targets have been sourced for those two platform companies with three successfully closed and several more pending, all at valuations substantially lower than the original platform company valuation. However, you should not rely on these valuations as indicative of our future performance. We expect that the management team’s network of existing contacts and relationships will be able to deliver a flow of potential platform and add-on acquisition opportunities which are proprietary or where a limited group of established, credentialed buyers have been invited to participate in the sale process. In addition, we anticipate that target business candidates will be brought to our attention from various unaffiliated sources, including investment market participants, private equity funds and large business enterprises seeking to divest non-core assets or divisions.

We are not prohibited from pursuing an initial business combination with a company that is affiliated with our sponsor, executive officers or directors, or making the acquisition through a joint venture or other form of shared ownership with our sponsor, executive officers or directors. In the event we seek to complete an initial business combination with a target that is affiliated with our sponsor, executive officers or directors, we, or a committee of independent directors, would obtain an opinion from an independent investment banking or accounting firm that is a member of FINRA that such an initial business combination is fair to our company from a financial point of view. We are not required to obtain such an opinion in any other context.

If any of our executive officers becomes aware of a business combination opportunity that falls within the line of business of any entity to which he or she has pre-existing fiduciary or contractual obligations, he or she may be required to present such business combination opportunity to such entity prior to presenting such business combination opportunity to us. All of our executive officers currently have certain relevant fiduciary duties or contractual obligations that may take priority over their duties to us.

We anticipate that target business candidates will also be brought to our attention from various unaffiliated sources, including investment bankers, private investment funds and other intermediaries. Target businesses may be brought to our attention by such unaffiliated sources as a result of being solicited by us through calls or mailings. These sources may also introduce us to target businesses in which they think we may be interested on an unsolicited basis, since many of these sources will have read our initial public offering prospectus or this Report and know what types of businesses we are targeting. Our officers and directors, as well as their affiliates, may also bring to our attention target business candidates that they become aware of through their business contacts as a result of formal or informal inquiries or discussions they may have, as well as attending trade shows or conventions. In addition, we expect to receive a number of proprietary deal flow opportunities that would not otherwise necessarily be available to us as a result of the track record and business relationships of our officers and directors.

Selection of a target business and structuring of our initial business combination

Nasdaq rules require that our initial business combination must be with one or more target businesses that together have a fair market value equal to at least 80% of the balance in the trust account (less any deferred underwriting commissions and taxes payable on interest earned) at the time of our signing a definitive agreement in connection with our initial business combination. The fair market value of the target or targets will be determined by our board of directors based upon one or more standards generally accepted by the financial community, such as discounted cash flow valuation or value of comparable businesses. If our board is not able to independently determine the fair market value of the target business or businesses, we will obtain an opinion from an independent investment banking firm that is a member of FINRA with respect to the satisfaction of such criteria. Subject to this requirement, our management will have virtually unrestricted flexibility in identifying and selecting one or more prospective target businesses, although we will not be permitted to effectuate our initial business combination with another blank check company or a similar company with nominal operations.

In any case, we will only complete an initial business combination in which we own or acquire 50% or more of the outstanding voting securities of the target or otherwise acquire a controlling interest in the target sufficient for it not to be required to register as an investment company under the Investment Company Act. If we own or acquire less than 100% of the equity interests or assets of a target business or businesses, the portion of such business or businesses that is owned or acquired by the post-transaction company is what will be valued for purposes of the 80% of net assets test.

| 12 |

To the extent we effect our business combination with a company or business that may be financially unstable or in its early stages of development or growth we may be affected by numerous risks inherent in such company or business. Although our management will endeavor to evaluate the risks inherent in a particular target business, we cannot assure you that we will properly ascertain or assess all significant risk factors.

In evaluating a prospective target business, we expect to conduct a thorough due diligence review which will encompass, among other things, meetings with incumbent management and employees, document reviews, inspection of facilities, as well as a review of financial and other information which will be made available to us.

The time required to select and evaluate a target business and to structure and complete our initial business combination, and the costs associated with this process, are not currently ascertainable with any degree of certainty. Any costs incurred with respect to the identification and evaluation of a prospective target business with which our business combination is not ultimately completed will result in our incurring losses and will reduce the funds we can use to complete another business combination.

Lack of business diversification

For an indefinite period of time after the consummation of our initial business combination, the prospects for our success may depend entirely on the future performance of a single business. Unlike other entities that have the resources to complete business combinations with multiple entities in one or several industries, it is probable that we will not have the resources to diversify our operations and mitigate the risks of being in a single line of business. By consummating a business combination with only a single entity, our lack of diversification may:

| ● | subject us to negative economic, competitive and regulatory developments, any or all of which may have a substantial adverse impact on the particular industry in which we operate after our initial business combination, and |

| ● | cause us to depend on the marketing and sale of a single product or limited number of products or services. |

Limited ability to evaluate the target’s management team

Although we intend to closely scrutinize the management of a prospective target business when evaluating the desirability of effecting our business combination with that business, our assessment of the target business’ management may not prove to be correct. In addition, the future management may not have the necessary skills, qualifications or abilities to manage a public company. Furthermore, the future role of members of our management team, if any, in the target business cannot presently be stated with any certainty. While it is possible that one or more of our directors will remain associated in some capacity with us following our business combination, it is unlikely that any of them will devote their full efforts to our affairs subsequent to our business combination. Moreover, we cannot assure you that members of our management team will have significant experience or knowledge relating to the operations of the particular target business.

We cannot assure you that any of our key personnel will remain in senior management or advisory positions with the combined company. The determination as to whether any of our key personnel will remain with the combined company will be made at the time of our initial business combination.

Following a business combination, we may seek to recruit additional managers to supplement the incumbent management of the target business. We cannot assure you that we will have the ability to recruit additional managers, or that additional managers will have the requisite skills, knowledge or experience necessary to enhance the incumbent management.

If the Business Combination with Seller is consummated, it is expected that our current Chairman of the Board of Directors and Chief Executive Officer will be a member of the Board of Directors following the Business Combination.

| 13 |

Stockholders may not have the ability to approve our initial business combination

We may conduct redemptions without a stockholder vote pursuant to the tender offer rules of the SEC. However, we will seek stockholder approval if it is required by law or applicable stock exchange rule, or we may decide to seek stockholder approval for business or other legal reasons. Presented in the table below is a graphic explanation of the types of initial business combinations we may consider and whether stockholder approval is currently required under Delaware law for each such transaction.

Type of Transaction | Whether | |||

| Purchase of assets | No | |||

| Purchase of stock of target not involving a merger with the company | No | |||

| Merger of target into a subsidiary of the company | No | |||

| Merger of the company with a target | Yes |

Under Nasdaq’s listing rules, stockholder approval would be required for our initial business combination if, for example:

| ● | we issue common stock that will be equal to or in excess of 20% of the number of shares of our common stock then outstanding; |

| ● | any of our directors, officers or substantial shareholders (as defined by Nasdaq rules) has a 5% or greater interest (or such persons collectively have a 10% or greater interest), directly or indirectly, in the target business or assets to be acquired or otherwise and the present or potential issuance of common stock could result in an increase in outstanding common shares or voting power of 5% or more; or |

| ● | the issuance or potential issuance of common stock will result in our undergoing a change of control. |

Permitted purchases of our securities

In the event we seek stockholder approval of our business combination and we do not conduct redemptions in connection with our business combination pursuant to the tender offer rules, our sponsor, directors, officers, advisors or their affiliates may purchase shares in privately negotiated transactions or in the open market either prior to or following the completion of our initial business combination. However, they have no current commitments, plans or intentions to engage in such transactions and have not formulated any terms or conditions for any such transactions. None of the funds in the trust account will be used to purchase shares in such transactions. They will not make any such purchases when they are in possession of any material non-public information not disclosed to the seller or if such purchases are prohibited by Regulation M under the Exchange Act. Such a purchase may include a contractual acknowledgement that such stockholder, although still the record holder of our shares is no longer the beneficial owner thereof and therefore agrees not to exercise its redemption rights. We have adopted an insider trading policy which will require insiders to: (i) refrain from purchasing shares during certain blackout periods and when they are in possession of any material nonpublic information and (ii) to clear all trades with our legal counsel prior to execution. Such policy may be superseded by a new policy upon consummation of a business combination. We cannot currently determine whether our insiders will make such purchases pursuant to a Rule 10b5-1 plan, as it will be dependent upon several factors, including but not limited to, the timing and size of such purchases. Depending on such circumstances, our insiders may either make such purchases pursuant to a Rule 10b5-1 plan or determine that such a plan is not necessary.

In the event that our sponsor, directors, officers, advisors or their affiliates purchase shares in privately negotiated transactions from public stockholders who have already elected to exercise their redemption rights, such selling stockholders would be required to revoke their prior elections to redeem their shares. We do not currently anticipate that such purchases, if any, would constitute a tender offer subject to the tender offer rules under the Exchange Act or a going-private transaction subject to the going-private rules under the Exchange Act; however, if the purchasers determine at the time of any such purchases that the purchases are subject to such rules, the purchasers will comply with such rules.

The purpose of such purchases would be to (i) vote such shares in favor of the business combination and thereby increase the likelihood of obtaining stockholder approval of the business combination or (ii) to satisfy a closing condition in an agreement with a target that requires us to have a minimum net worth or a certain amount of cash at the closing of our business combination, where it appears that such requirement would otherwise not be met. This may result in the completion of our business combination that may not otherwise have been possible.

| 14 |

In addition, if such purchases are made, the public “float” of our common stock may be reduced and the number of beneficial holders of our securities may be reduced, which may make it difficult to maintain or obtain the quotation, listing or trading of our securities on a national securities exchange.

Our sponsor, officers, directors and/or their affiliates anticipate that they may identify the stockholders with whom our sponsor, officers, directors or their affiliates may pursue privately negotiated purchases by either the stockholders contacting us directly or by our receipt of redemption requests submitted by stockholders following our mailing of proxy materials in connection with our initial business combination. To the extent that our sponsor, officers, directors, advisors or their affiliates enter into a private purchase, they would identify and contact only potential selling stockholders who have expressed their election to redeem their shares for a pro rata share of the trust account or vote against the business combination. Our sponsor, officers, directors, advisors or their affiliates will only purchase shares if such purchases comply with Regulation M and the other federal securities laws.

Any purchases by our sponsor, officers, directors and/or their affiliates who are ″affiliated purchasers″ under Rule 10b-18 under the Exchange Act will only be made to the extent such purchases are able to be made in compliance with Rule 10b-18, which is a safe harbor from liability for manipulation under Section 9(a)(2) and Rule 10b-5 of the Exchange Act. Rule 10b-18 has certain technical requirements that must be complied with in order for the safe harbor to be available to the purchaser. Our sponsor, officers, directors and/or their affiliates will not make purchases of common stock if the purchases would violate Section 9(a)(2) or Rule 10b-5 of the Exchange Act.

Redemption rights for public stockholders upon consummation of our initial business combination

We will provide our public stockholders with the opportunity to redeem all or a portion of their shares of common stock upon the completion of our initial business combination at a per-share price, payable in cash, equal to the aggregate amount then on deposit in the trust account as of two business days prior to the consummation of the initial business combination, including interest (which interest shall be net of taxes payable) divided by the number of then outstanding public shares, subject to the limitations described herein. The amount in the trust account is initially anticipated to be approximately $10.00 per public share. The per-share amount we will distribute to investors who properly redeem their shares will not be reduced by the deferred underwriting commissions we will pay to the underwriters. Our initial stockholders have entered into letter agreements with us, pursuant to which they have agreed to waive their redemption rights with respect to their founder shares and any public shares they may hold in connection with the completion of our business combination.

Manner of Conducting Redemptions

We will provide our public stockholders with the opportunity to redeem all or a portion of their shares of common stock upon the completion of our initial business combination either (i) in connection with a stockholder meeting called to approve the business combination or (ii) by means of a tender offer. The decision as to whether we will seek stockholder approval of a proposed business combination or conduct a tender offer will be made by us, solely in our discretion, and will be based on a variety of factors such as the timing of the transaction and whether the terms of the transaction would require us to seek stockholder approval under the law or stock exchange listing requirement. Asset acquisitions and stock purchases would not typically require stockholder approval while direct mergers with our company where we do not survive and any transactions where we issue more than 20% of our outstanding common stock or seek to amend our amended and restated certificate of incorporation would require stockholder approval. We intend to conduct redemptions without a stockholder vote pursuant to the tender offer rules of the SEC unless stockholder approval is required by law or stock exchange listing requirement or we choose to seek stockholder approval for business or other legal reasons.

If a stockholder vote is not required and we do not decide to hold a stockholder vote for business or other legal reasons, we will, pursuant to our amended and restated certificate of incorporation:

| ● | conduct the redemptions pursuant to Rule 13e-4 and Regulation 14E of the Exchange Act, which regulate issuer tender offers, and |

| ● | file tender offer documents with the SEC prior to completing our initial business combination which contain substantially the same financial and other information about the initial business combination and the redemption rights as is required under Regulation 14A of the Exchange Act, which regulates the solicitation of proxies. |

| 15 |

Upon the public announcement of our business combination, we or our sponsor will terminate any plan established in accordance with Rule 10b5-1 to purchase shares of our common stock in the open market if we elect to redeem our public shares through a tender offer, to comply with Rule 14e-5 under the Exchange Act.

In the event we conduct redemptions pursuant to the tender offer rules, our offer to redeem will remain open for at least 20 business days, in accordance with Rule 14e-1(a) under the Exchange Act, and we will not be permitted to complete our initial business combination until the expiration of the tender offer period. In addition, the tender offer will be conditioned on public stockholders not tendering more than a specified number of public shares which are not purchased by our sponsor, which number will be based on the requirement that we may not redeem public shares in an amount that would cause our net tangible assets to be less than $5,000,001 (so that we are not subject to the SEC’s “penny stock” rules) or any greater net tangible asset or cash requirement which may be contained in the agreement relating to our initial business combination. If public stockholders tender more shares than we have offered to purchase, we will withdraw the tender offer and not complete the initial business combination.

If, however, stockholder approval of the transaction is required by law or stock exchange listing requirement, or we decide to obtain stockholder approval for business or other legal reasons, we will, pursuant to our amended and restated certificate of incorporation:

| ● | conduct the redemptions in conjunction with a proxy solicitation pursuant to Regulation 14A of the Exchange Act, which regulates the solicitation of proxies, and not pursuant to the tender offer rules, and |

| ● | file proxy materials with the SEC. |

In the event that we seek stockholder approval of our initial business combination, we will distribute proxy materials and, in connection therewith, provide our public stockholders with the redemption rights described above upon completion of the initial business combination.

If we seek stockholder approval, we will complete our initial business combination only if a majority of the outstanding shares of common stock voted are voted in favor of the business combination. In such case, our initial stockholders have agreed to vote their founder shares and any public shares purchased since our initial public offering in favor of our initial business combination. Each public stockholder may elect to redeem their public shares irrespective of whether they vote for or against the proposed transaction. In addition, our initial stockholders have entered into letter agreements with us, pursuant to which they have agreed to waive their redemption rights with respect to their founder shares and public shares in connection with the completion of a business combination.

Our amended and restated certificate of incorporation provides that in no event will we redeem our public shares in an amount that would cause our net tangible assets to be less than $5,000,001 (so that we are not subject to the SEC’s “penny stock” rules). Redemptions of our public shares may also be subject to a higher net tangible asset test or cash requirement pursuant to an agreement relating to our initial business combination. For example, the proposed business combination may require: (i) cash consideration to be paid to the target or its owners, (ii) cash to be transferred to the target for working capital or other general corporate purposes or (iii) the retention of cash to satisfy other conditions in accordance with the terms of the proposed business combination. In the event the aggregate cash consideration we would be required to pay for all shares of common stock that are validly submitted for redemption plus any amount required to satisfy cash conditions pursuant to the terms of the proposed business combination exceed the aggregate amount of cash available to us, we will not complete the business combination or redeem any shares, and all shares of common stock submitted for redemption will be returned to the holders thereof.

Limitation on redemption upon consummation of our initial business combination if we seek stockholder approval

Notwithstanding the foregoing, if we seek stockholder approval of our initial business combination and we do not conduct redemptions in connection with our business combination pursuant to the tender offer rules, our amended and restated certificate of incorporation provides that a public stockholder, together with any affiliate of such stockholder or any other person with whom such stockholder is acting in concert or as a “group” (as defined under Section 13 of the Exchange Act), will be restricted from seeking redemption rights with respect to Excess Shares. We believe this restriction will discourage stockholders from accumulating large blocks of shares, and subsequent attempts by such holders to use their ability to exercise their redemption rights against a proposed business combination as a means to force us or our management to purchase their shares at a significant premium to the then-current market price or on other undesirable terms. Absent this provision, a public stockholder holding more than an aggregate of 10% of the shares sold in our initial public offering could threaten to exercise its redemption rights if such holder’s shares are not purchased by us or our management at a premium to the then-current market price or on other undesirable terms. By limiting our stockholders’ ability to redeem no more than 10% of the shares sold in the initial public offering, we believe we will limit the ability of a small group of stockholders to unreasonably attempt to block our ability to complete our business combination, particularly in connection with a business combination with a target that requires as a closing condition that we have a minimum net worth or a certain amount of cash. However, we would not be restricting our stockholders’ ability to vote all of their shares (including Excess Shares) for or against our business combination.

| 16 |

Tendering stock certificates in connection with a tender offer or redemption rights

We may require our public stockholders seeking to exercise their redemption rights, whether they are record holders or hold their shares in “street name,” to either tender their certificates to our transfer agent prior to the date set forth in the tender offer documents or proxy materials mailed to such holders, or up to two business days prior to the vote on the proposal to approve the business combination in the event we distribute proxy materials, or to deliver their shares to the transfer agent electronically using Depository Trust Company’s DWAC (Deposit/Withdrawal At Custodian) System, at the holder’s option. The tender offer or proxy materials, as applicable, that we will furnish to holders of our public shares in connection with our initial business combination will indicate whether we are requiring public stockholders to satisfy such delivery requirements. Accordingly, a public stockholder would have from the time we send out our tender offer materials until the close of the tender offer period, or up to two days prior to the vote on the business combination if we distribute proxy materials, as applicable, to tender its shares if it wishes to seek to exercise its redemption rights. Given the relatively short exercise period, it is advisable for stockholders to use electronic delivery of their public shares.

There is a nominal cost associated with the above-referenced tendering process and the act of certificating the shares or delivering them through the DWAC System. The transfer agent will typically charge the tendering broker $35.00 and it would be up to the broker whether or not to pass this cost on to the redeeming holder. However, this fee would be incurred regardless of whether or not we require holders seeking to exercise redemption rights to tender their shares. The need to deliver shares is a requirement of exercising redemption rights regardless of the timing of when such delivery must be effectuated.

The foregoing is different from the procedures used by many blank check companies. In order to perfect redemption rights in connection with their business combinations, many blank check companies would distribute proxy materials for the stockholders’ vote on an initial business combination, and a holder could simply vote against a proposed business combination and check a box on the proxy card indicating such holder was seeking to exercise his or her redemption rights. After the business combination was approved, the company would contact such stockholder to arrange for him or her to deliver his or her certificate to verify ownership. As a result, the stockholder then had an “option window” after the completion of the business combination during which he or she could monitor the price of the company’s stock in the market. If the price rose above the redemption price, he or she could sell his or her shares in the open market before actually delivering his or her shares to the company for cancellation. As a result, the redemption rights, to which stockholders were aware they needed to commit before the stockholder meeting, would become “option” rights surviving past the completion of the business combination until the redeeming holder delivered its certificate. The requirement for physical or electronic delivery prior to the meeting ensures that a redeeming holder’s election to redeem is irrevocable once the business combination is approved.

Any request to redeem such shares, once made, may be withdrawn at any time up to the date set forth in the tender offer materials or the date of the stockholder meeting set forth in our proxy materials, as applicable. Furthermore, if a holder of a public share delivered its certificate in connection with an election of redemption rights and subsequently decides prior to the applicable date not to elect to exercise such rights, such holder may simply request that the transfer agent return the certificate (physically or electronically). It is anticipated that the funds to be distributed to holders of our public shares electing to redeem their shares will be distributed promptly after the completion of our business combination.

If our initial business combination is not approved or completed for any reason, then our public stockholders who elected to exercise their redemption rights would not be entitled to redeem their shares for the applicable pro rata share of the trust account. In such case, we will promptly return any certificates delivered by public holders who elected to redeem their shares.

If our initial proposed business combination is not completed, we may continue to try to complete a business combination with a different target until October 23, 2015 (or January 23, 2016 if we have executed a letter of intent, agreement in principle or definitive agreement for an initial business combination by October 23, 2015 but have not completed the initial business combination by such date).

| 17 |

Redemption of public shares and liquidation if no initial business combination

Our sponsor, executive officers and directors have agreed that we will have only until October 23, 2015 to complete our initial business combination (or January 23, 2016, as applicable). If we are unable to complete our business combination within such period, we will: (i) cease all operations except for the purpose of winding up, (ii) as promptly as reasonably possible but not more than ten business days thereafter, redeem the public shares, at a per-share price, payable in cash, equal to the aggregate amount then on deposit in the trust account, including interest (less up to $50,000 of interest to pay dissolution expenses (which interest shall be net of taxes payable) divided by the number of then outstanding public shares, which redemption will completely extinguish public stockholders’ rights as stockholders (including the right to receive further liquidation distributions, if any), subject to applicable law, and (iii) as promptly as reasonably possible following such redemption, subject to the approval of our remaining stockholders and our board of directors, dissolve and liquidate, subject in each case to our obligations under Delaware law to provide for claims of creditors and the requirements of other applicable law. There will be no redemption rights or liquidating distributions with respect to our warrants, which will expire worthless if we fail to complete our business combination by October 23, 2015 (or January 23, 2016, as applicable).

Our initial stockholders have entered into letter agreements with us, pursuant to which they have waived their rights to liquidating distributions from the trust account with respect to their founder shares if we fail to complete our initial business combination by October 23, 2015 (or January 23, 2016, as applicable). However, if our initial stockholders acquire public shares after our initial public offering, they will be entitled to liquidating distributions from the trust account with respect to such public shares if we fail to complete our initial business combination by October 31, 2015 (or January 23, 2016, as applicable).

Our sponsor, executive officers and directors have agreed, pursuant to a written letter agreement with us, that they will not propose any amendment to our amended and restated certificate of incorporation that would affect the substance or timing of our obligation to redeem 100% of our public shares if we do not complete our initial business combination by October 23, 2015 (or January 23, 2016, as applicable), unless we provide our public stockholders with the opportunity to redeem their shares of common stock upon approval of any such amendment at a per-share price, payable in cash, equal to the aggregate amount then on deposit in the trust account, including interest (which interest shall be net of taxes payable) divided by the number of then outstanding public shares. However, we may not redeem our public shares in an amount that would cause our net tangible assets to be less than $5,000,001 (so that we are not subject to the SEC’s “penny stock” rules).

We expect that all costs and expenses associated with implementing our plan of dissolution, as well as payments to any creditors, will be funded from amounts remaining out of the approximately $1,000,000 of proceeds initially held outside the trust account, although we cannot assure you that there will be sufficient funds for such purpose. However, if those funds are not sufficient to cover the costs and expenses associated with implementing our plan of dissolution, to the extent that there is any interest accrued in the trust account not required to pay taxes, we may request the trustee to release to us an additional amount of up to $50,000 of such accrued interest to pay those costs and expenses.