UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-K

| [X] | ANNUAL REPORT UNDER SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2018

OR

| [ ] | TRANSITION REPORT UNDER SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from_____________ to _____________.

Commission file number 000-55053

Blow & Drive Interlock Corporation

(Exact name of registrant as specified in its charter)

| Delaware | 46-3590850 | |

(State or other jurisdiction of incorporation or organization) |

(I.R.S. Employer Identification No.) |

1427 S. Robertson Blvd. Los Angeles, CA |

90035 | |

| (Address of principal executive offices) | (Zip Code) |

Registrant’s telephone number, including area code (877) 238-4492

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Name of each exchange on which registered | |

| None | None |

Securities registered pursuant to Section 12(g) of the Act:

Common Stock, par value $0.0001

(Title of class)

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes [ ] No [X]

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act. Yes [ ] No [X]

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes [ ] No [X]

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to and post such files). Yes [ ] No [X]

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. [ ]

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer [ ] | Accelerated filer [ ] | ||

| Non-accelerated filer [ ] | Smaller reporting company [X] | ||

| Emerging growth company [ ] |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. [ ]

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes [ ] No [X]

Aggregate market value of the voting stock held by non-affiliates: $3,355,232 as based on last reported sales price of such stock on June 30, 2018. The voting stock held by non-affiliates on that date consisted of 18,640,182 shares of common stock the closing stock price was $0.18.

Applicable Only to Registrants Involved in Bankruptcy Proceedings During the Preceding Five Years:

Indicate by check mark whether the registrant has filed all documents and reports required to be filed by Sections 12, 13 or 15(d) of the Exchange Act of 1934 subsequent to the distribution of securities under a plan confirmed by a court. Yes [ ] No [ ]

Indicate the number of shares outstanding of each of the registrant’s classes of common stock, as of the latest practicable date. As of July 15, 2019, there were 31,350,683 shares of common stock, $0.001 par value, issued and outstanding.

Documents Incorporated by Reference

List hereunder the following documents if incorporated by reference and the Part of the Form 10-K (e.g., Part I, Part II, etc.) into which the document is incorporated: (1) Any annual report to security holders; (2) Any proxy or information statement; and (3) Any prospectus filed pursuant to rule 424(b) or (c) of the Securities Act of 1933. The listed documents should be clearly described for identification purposes (e.g., annual report to security holders for fiscal year ended December 24, 1980). None.

Blow & Drive Interlock Corporation

TABLE OF CONTENTS

| i |

Forward Looking Statements

This Annual Report includes forward-looking statements within the meaning of the Securities Exchange Act of 1934 (the “Exchange Act”). These statements are based on management’s beliefs and assumptions, and on information currently available to management. Forward-looking statements include the information concerning possible or assumed future results of operations of the Company set forth under the heading “Management’s Discussion and Analysis of Financial Condition or Plan of Operation.” Forward-looking statements also include statements in which words such as “expect,” “anticipate,” “intend,” “plan,” “believe,” “estimate,” “consider,” or similar expressions are used.

Forward-looking statements are not guarantees of future performance. They involve risks, uncertainties, and assumptions. The Company’s future results and shareholder values may differ materially from those expressed in these forward-looking statements. Readers are cautioned not to put undue reliance on any forward-looking statements.

Corporate History

We were incorporated under the name Jam Run Acquisition Corporation on July 2, 2013 in the State of Delaware. From inception through early February 2014, we were a blank check company and qualified as an “emerging growth company” as defined in the Jumpstart Our Business Startups Act which became law in April, 2012, with a business plan of entering into a transaction with a foreign or domestic private company in order for that company to become a reporting company as part of the process toward the public trading of its stock.

On February 6, 2014, we issued 9,700,000 shares of our common stock, representing approximately 97% of our then-outstanding shares to Laurence Wainer for $1,970. In connection with this transaction, we changed our name Blow & Drive Interlock Corporation and Mr. Wainer became our sole officer and director.

On March 7, 2017, we entered into an Debt Conversion and Series A Preferred Stock Purchase Agreement (the “SPA”) with Mr. Wainer, one of our officers and directors at that time, under which we agreed to create a new series of non-convertible preferred stock entitled “Series A Preferred Stock,” with One Million (1,000,000) shares authorized and the following rights: (i) no dividend rights; (ii) no liquidation preference over the Company’s common stock; (iii) no conversion rights; (iv) no redemption rights; (v) no call rights by the Company; (vi) each share of Series A Convertible Preferred stock will have one hundred (100) votes on all matters validly brought to the Company’s common stockholders; and Mr. Wainer agreed to acquire 1,000,000 shares of our Series A Preferred Stock, once created, in exchange for Mr. Wainer forgiving $25,537 in accrued salary we owed to him as of December 31, 2016. The Series A Preferred Stock was created with the State of Delaware by filing a Certificate of Designation on March 13, 2017. The description of the SPA set forth in this report is qualified in its entirety by reference to the full text of that document, which is attached hereto as Exhibit 10.26 and is incorporated herein by reference.

On January 2, 2019, Mr. Wainer closed the transaction that was the subject of an Agreement to Purchase Common Stock and Preferred Stock (the “Agreement”) between Mr. Wainer and The Doheny Group, LLC, a Nevada limited liability company (“Doheny Group”), under which Doheny Group acquired 8,924,000 shares of our common stock (the “Common Shares”) and One Million (1,000,000) shares of our Series A Preferred Stock (the “Preferred Shares” and together with the Common Shares, the “Shares”), from Mr. Wainer in exchange for $30,000. Combined, the Shares represent approximately 84% of our outstanding voting rights. Mr. David Haridim is the principal of Doheny and was appointed to our Board of Directors and as our sole executive officer. We were a party to the Agreement solely for the purpose of acknowledging certain representations and warranties about the company in the Agreement. The description of the Agreement set forth in this report is qualified in its entirety by reference to the full text of that document, which is attached hereto as Exhibit 10.20 and is incorporated herein by reference.

| 2 |

Our offices are located at 1427 S. Robertson Blvd., Los Angeles, CA 90035, telephone number (877) 238-4492.

Business Overview

General

We manufacture, market, lease, install and monitor a Breath Alcohol Ignition Interlock Device (BAIID) we developed known as the BDI-747 Ignition Interlock Device (the “BDI-747/1”), which is a mechanism that is installed on the steering column of an automobile and into which a driver exhales prior to starting their vehicle. The device in turn provides a blood-alcohol concentration analysis. If the driver’s blood-alcohol content is higher than a certain pre-programmed limit, the device prevents the ignition from engaging and the automobile from starting. These devices are often required for use by DUI or DWI (“driving under the influence” or “driving while intoxicated”) offenders as part of a mandatory court or motor vehicle department program. The BDI-747/1 has met the 2013 National Highway Traffic Safety Administration (NHTSA) guidelines for Breath Alcohol Ignition Interlock Devices [Federal Register Volume 78, Number 89] as an authorized BAIID [Element Materials Technology/Report # ESP018444P June 17, 2015]. The BDI-747/1 is manufactured by BDI Manufacturing Inc., a subsidiary of Blow & Drive Interlock, Inc., from parts and supplies from C4 Development Ltd.

The primary market for the BDI-747/1 Ignition Interlock Device is as a breathalyzer device to be used by persons convicted of a driving under the influence of alcohol. In order for the BDI-747/1 to be used in states for persons convicted of driving under the influence the device must be approved by each individual state. The process to get the device approved varies greatly state-to-state. As of December 31, 2018, the BDI-747/1 device was approved in Oregon, Texas, Arizona, and Kentucky. As of March 31, 2019, the BDI-747/1 device was only approved in Arizona and Texas. The states where our BDI-747/1 device is approved has decreased primarily as a result of new state certification rules that require increased capital investment that we are not able to afford.

In states where the BDI-747/1 is approved as a BAIID, we lease the BDI-747/1 devices to offenders, typically for twelve months, but the time could differ on a case-by-case basis depending on the sentence received by the offender. In some states we market, lease, install and support the devices directly and in other states we sell distributorships to authorized distributors allowing them to lease, install, service, remove and support the BDI-747/1 devices. Currently, we lease the devices directly in the states we are approved, except West Phoenix, Arizona and Lubbock, Texas, where we have licensed distributors that lease the devices.

In states where we lease the devices directly to consumers, we typically charge between $89-$189 in upfront fees for the user (which covers one month of the lease payment), and then between $69-$89/month for the other eleven months of the lease for the typical one year lease. The lease payment covers the installation of the device in the consumer’s vehicle, the rental of the device, recalibration of the device as required by each state (typically every 30 to 60 days) and the monitoring services for the device, which are then reported to the state in accordance with each state’s requirements. In states and areas where we do not have a direct presence, which we only have in Phoenix, Arizona, we contract with independent service centers, such as car alarm installation companies or other auto services companies, to perform the installations of our BDI-747/1 device, which centers must be approved by the states in which we perform the installations. Because our devices are installed in consumers’ vehicles are part of a judicially-mandated program, and since the use of the device controls the individual’s driving privileges, collection rates of the monthly leasing fees is close to 100%. The failure to make the payment could be a violation of the consumer’s sentence or probation and could cause them to lose the device and their driving privileges.

| 3 |

In areas where we have a distributor, in our typical distributorship arrangement, we charge the distributor a flat fee distributorship territory fee up front (which fee varies based on the size and location of the distributorship), a $150 per unit registration fee, and then a $35 monthly fee for each device the distributor has in its inventory. These fees may vary on a case-by-case basis. The relationship with our distributors may either be on an exclusive or non-exclusive basis depending upon the location of the distributorship and the fees charged.

As of December 31, 2018, we had approximately 1,100 units on the road, with approximately 885 devices being leased directly from us and approximately 215 devices leased through our distributors, compared to December 31, 2017, when we had approximately 1,558 units on the road, with approximately 1,451 devices being leased directly from us and approximately 107 devices leased through our distributors. The decrease in the total number of devices we have on the road is primarily due to the fact the BDI-747/1 devices was approved in fewer states in 2018 compared to 2017.

Due to the decrease in the number of states where our BDI-747/1 device is approved, and the resulting decrease in the number of devices we have on the road, our management is currently exploring all options related to our business, including, but not limited to: (i) taking out loans or selling our stock in order to raise money to continue, and try to expand, our current business; (ii) trying to acquire a synergistic business and grow our current business; or (iii) selling our current business and trying to find another business to, in or out of our current business segment, to take over the public corporation.

Our website is www.blowanddrive.com.

Principal Products and Services

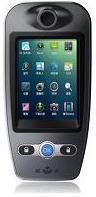

Our only product is the BDI-747/1 Breath Alcohol Ignition Interlock Device. The BDI-747/1 device is used to detect alcohol in a person’s system by measuring the level of alcohol in a person’s breath by having them blow into the device and determining whether that level is over or under a preset level set by the installer or a trained technician. The pre-determined level differs by state, but is typically around .02. The device is approximately the size of a smartphone which is installed directly onto a vehicle’s steering column. The device requires the driver to exhale into the device prior to starting the vehicle. The device will prevent the vehicle from starting if the driver’s blood-alcohol content exceeds the predetermined set level.

(photo of BDI-747/1)

Our device, designed by Well Electric, incorporates the latest technology and design in the market for such devices. The device has both GPS and video capabilities. The device has a fuel cell sensor and a color display screen. The external camera mounting can wrap around the automobile’s rear view mirror. The device is powered by either an internal battery or a power cable from a control box which supports both 24V and 12V batteries. The device has both USB communication capabilities and WiFi (with approval from service provider).

The specifications for our ignition interlock device are as follows:

| Sample head | |

| Sensor | Fuel cell |

| Working Temperature | -40˚C to 85˚C |

| Display Screen | Color screen |

| Memory and Save | 80,000 events with pictures save and download form sample head |

| Communication | USB, WiFi, 3G(user need to get US approval with service provider) |

| Communication with control box | Wireless |

| Power supply | Internal battery or power cable from control box |

| Human checking | Flow sensing, air temperature sensing |

| External | |

| Camera | External camera mounting around the review mirror |

| Night photo | White LED, and IR light |

| Control box | Support 24V and 12V |

| Motor Start Checking | Ignition checking, power checking, moving checking |

| PC software | One client side software, which able to set sample and input user information. Picture and events may also be downloaded. This is not web or server side software |

| 4 |

The BDI-747/1 unit takes about 30-45 minutes to install in a vehicle, depending on the vehicle. The ignition interlock component is installed on the steering column. Currently, our cost to order the requisite supplies and assemble the BDI-747/1 units is approximately $350-$500 per unit depending on the specifications of the unit. The device requires recalibration in accordance with state requirements, typically every 30 to 60 days.

Marketing

In 2017, most of our marketing consisted of getting approval for our BDI-747/1 device in as many states as possible. By gaining approval in a state our BDI-747/1 device appears on that state’s list of approved breathalyzer ignition interlock devices. Someone convicted of driving under the influence that is required to use a breathalyzer ignition interlock device must choose one from the list of state-approved devices. As a result, by gaining approvals in states, our device is automatically disseminated to our targeted consumers by the state. In addition to trying to obtain approvals in as many states as we can, our other marketing efforts related to our BDI-747/1 device have largely consisted of speaking with various individuals and companies that are in the breathalyzer ignition interlock device industry, such as companies in the business of conducting educational courses for individuals convicted of driving under the influence of alcohol, companies in the business of installing ignition interlock devices, and individuals involved in the approval process for breathalyzer ignition interlock devices.

In addition to marketing our BDI-747/1 device directly to consumers, we have also marketed our distributorship opportunities to various individuals and companies that are in the breathalyzer ignition interlock device industry. In the past, the efforts have included radio and television advertisements of our distributorship program. Although we are not currently running any radio or television advertisements for our distributorship program, we may do so again in the future. We have also discussed these opportunities with various companies and individuals in the industry, similar to what we have done with our marketing of our BDI-747/1 device.

Manufacturing

We are the primary manufacturer of our BDI-747/1 device, through our wholly-owned subsidiary, BDI Manufacturing, Inc., an Arizona corporation. However, we do utilize a supply and assembly company called C4 Development Ltd., a Hong Kong corporation (“C4 Development”). On June 29, 2015, we entered into a Supply Agreement with C4 Development, under which C4 Development supplies us with a part known as the “PCB with Alcohol Tester.” This device has certain parts utilized in our BDI-747/1 device, but the PCB with Alcohol Tester is not a device, by itself, that is capable of obtaining approval from the NHTSA as a breath alcohol interlock device. Once we obtain these parts for a device from C4 Development, we compile the components to the devices at our facility in Phoenix, Arizona in order to create our BDI-747/1 device.

Competition

The business of breathalyzer ignition interlock device industry is competitive, and from time-to-time new companies may appear on the list of approved providers in various states, however, there is a high barrier to entry due to the cost of development fees, manufacturing fees, NHSTA-approved testing, and state field testing. We compete with a number of successful companies in the industry, including, but not limited to, LifeSafer®, Smart Start®, Intoxalock®, Guardian Interlock Systems and Dräger. These larger companies have greater financial resources than we do, have approval in most (if not all) states, and likely have 50,000 of their respective ignition interlock devices on the road each. By comparison as of March 31, 2019, we were approved in two states and had approximately 1,100 units on the road. Although we believe our BDI-747/1 device compares favorably to the interlock devices provided by our competitors, we will need to raise significant capital and gain approval in most states in order capitalize on our BDI-747/1 device. We believe if we do this we will be able to compete better with these larger competitors.

| 5 |

Due to the state approvals necessary to service the judicially-mandated breath analyzer ignition interlock market we believe there is a barrier to entry that will discourage too many other companies from entering the industry. Not only must a new entrant develop and manufacture a breathalyzer device, it must meet the NHTSA requirements, and then get approved by state regulators, all of which can be costly. The complexities and costs of meeting all these steps should keep new entrants into the industry to a minimum.

Intellectual Property

We currently have a utility patent for our BDI Model #1 power line filter, which is used with our BDI-747 Breath Alcohol Ignition Interlock Device to prevent interference from electromagnetic waves. Although we do not have any other formal intellectual property protection over our BDI-747/1 device (such as device patents or trademarks), we do have general intellectual property protections provided by federal and state laws that prohibit unfair business practices, etc.

Government Regulation

Ignition interlock devices must be certified by the states in which a company intends to market and lease the devices. Before applying for certification to any state, the devices are sent to an independent laboratory for testing and certification that the device meets or exceeds the guidelines published by the National Highway Traffic Safety Administration as the Model Specifications for Breath Alcohol Ignition Interlock Devices. Each state has its own set of certification guidelines that must be met. Typically the requirements for state certification are met once the device is certified by an independent laboratory as meeting or exceeding the National Highway Traffic Safety Administration’s published guidelines.

Our BDI-747/1 device was certified by an independent testing laboratory in June 2015. As of As of December 31, 2018, the BDI-747/1 device was approved in Oregon, Texas, Arizona, and Kentucky. As of March 31, 2019, the BDI-747/1 device was only approved in Arizona and Texas.

Employees

As of December 31, 2018, we had four independent contractors, which primarily install, calibrate, remove and monitor our BDI-747/1 devices. Mr. Laurence Wainer, our President and Secretary at December 31, 2018, was an independent contractor. We have approximately 25 installers and technicians working in the states where we approved that are independent contractors.

Available Information

We are a fully reporting issuer, subject to the Securities Exchange Act of 1934. Our Quarterly Reports, Annual Reports, and other filings can be obtained from the SEC’s Public Reference Room at 100 F Street, NE., Washington, DC 20549, on official business days during the hours of 10 a.m. to 3 p.m. You may also obtain information on the operation of the Public Reference Room by calling the Commission at 1-800-SEC-0330. The Commission maintains an Internet site that contains reports, proxy and information statements, and other information regarding issuers that file electronically with the Commission at http://www.sec.gov.

| 6 |

As a smaller reporting company we are not required to provide a statement of risk factors. However, we believe this information may be valuable to our shareholders for this filing. We reserve the right to not provide risk factors in our future filings. Our primary risk factors and other considerations include:

We have a limited operating history and historical financial information upon which you may evaluate our performance.

You should consider, among other factors, our prospects for success in light of the risks and uncertainties encountered by companies that, like us, are in their early stages of development. We may not successfully address these risks and uncertainties or successfully implement our existing and new products. If we fail to do so, it could materially harm our business and impair the value of our common stock. Even if we accomplish these objectives, we may not generate the positive cash flows or profits we anticipate in the future. We were incorporated in Delaware on July 2, 2013. Our business to date business focused on developing, manufacturing, and getting independent certification and state approvals for our BDI-747/1 device, hiring management and staff personnel, contracting with distributors and leasing and servicing our products. Unanticipated problems, expenses and delays are frequently encountered in establishing a new business and developing new products. These include, but are not limited to, inadequate funding, lack of consumer acceptance, competition, product development, and inadequate sales and marketing. The failure by us to meet any of these conditions would have a materially adverse effect upon us and may force us to reduce or curtail operations. No assurance can be given that we can or will ever operate profitably.

We may not be able to meet our future capital needs.

To date, we have not generated sufficient revenue to meet our capital needs, and we may not be able to in the future. Our future capital requirements will depend on many factors, including our ability to develop our products, cash flow from operations, and competing market developments. We will need additional capital in the near future. Any equity financings will result in dilution to our then-existing stockholders. Sources of debt financing may result in high interest expense. Any financing, if available, may be on unfavorable terms. If adequate funds are not obtained, we will be required to reduce or curtail operations.

If we cannot obtain additional funding, our product development and commercialization efforts may be reduced or discontinued and we may not be able to continue operations.

We have historically experienced negative cash flows from operations since our inception and we expect the negative cash flows from operations to continue for the foreseeable future. Unless and until we are able to generate higher revenues, we expect such losses to continue for the foreseeable future. As discussed in our financial statements, there exists substantial doubt regarding our ability to continue as a going concern.

Product manufacturing and development efforts are highly dependent on the amount of cash and cash equivalents on hand combined with our ability to raise additional capital to support our future operations through one or more methods, including but not limited to, issuing additional equity or debt.

In addition, we may also raise additional capital through additional equity offerings, and licensing our future products in development. While we will continue to explore these potential opportunities, there can be no assurances that we will be successful in raising sufficient capital on terms acceptable to us, or at all, or that we will be successful in licensing our future products. Based on our current projections, we believe we have insufficient cash on hand to meet our obligations as they become due based on current assumptions. The uncertainties surrounding our future cash inflows have raised substantial doubt regarding our ability to continue as a going concern.

| 7 |

Current economic conditions and capital markets are in a period of disruption and instability which could adversely affect our ability to access the capital markets, and thus adversely affect our business and liquidity.

The current economic conditions and financial crisis have had, and will continue to have, a negative impact on our ability to access the capital markets, and thus have a negative impact on our business and liquidity. The shortage of liquidity and credit combined with the substantial losses in worldwide equity markets could lead to an extended worldwide recession. We may face significant challenges if conditions in the capital markets do not improve. Our ability to access the capital markets has been and continues to be severely restricted at a time when we need to access such markets, which could have a negative impact on our business plans. Even if we are able to raise capital, it may not be at a price or on terms that are favorable to us. We cannot predict the occurrence of future disruptions or how long the current conditions may continue.

Because we face intense competition, we may not be able to operate profitably in our markets.

The market for our product is highly competitive and is becoming more so, which could hinder our ability to successfully market our products. We may not have the resources, expertise or other competitive factors to compete successfully in the future. We expect to face additional competition from existing competitors and new market entrants in the future. Many of our competitors have greater name recognition and more established relationships in the industry than we do. As a result, these competitors may be able to:

| ● | develop and expand their product offerings more rapidly; | |

| ● | adapt to new or emerging changes in customer requirements more quickly; | |

| ● | take advantage of acquisition and other opportunities more readily; and | |

| ● | devote greater resources to the marketing and sale of their products and adopt more aggressive pricing policies than we can. |

If our products do not gain state approvals, are removed in jurisdictions where previously approved, and/or do not meet expected market acceptance, prospects for our sales revenue may be affected.

We use the BDI-747/1 device in the judicially-mandated market for DUI offenders. The judicially-mandated market is where a breathalyzer device is required by law as a punishment for the committing a crime. As a result, sales and servicing of our product is dependent upon us gaining approval in each individual state and/or locality where we want to lease our products. This result can be expensive and time-consuming and there is no guarantee we will be successful in obtaining approval in all the states where we apply and if we don’t get approval in a sufficient number of states the market for our products will suffer. Additionally, even if we gain state approval, there is no guarantee our products will stay as an approved device (we could get our approval revoked in one or more states) or will be chosen by a sufficient number of DUI offenders in those states to provide us with sufficient revenues to pay our expenses.

We plan to lease the BDI-747/1 device in many states through third-party distributors. If we are unsuccessful in finding qualified distributors or our distributors do not perform well, our business could suffer.

While we have a retail location in Phoenix, Arizona, and may open more in the future, under our current business plan we plan to lease the BDI-747/1 device through third-party distributors in many regions and states. If we are unable to find qualified distributors in certain regions and/or states, and/or the distributors we contract with do not perform well, then we may not lease and service as many of our BDI-747/1 devices as we anticipate, and our business would suffer as a result.

| 8 |

If critical components become unavailable or our suppliers delay their production of our key components, our business will be negatively impacted.

Currently, we rely on a primary supplier to supply us with the primary components for our BDI-747/1 device, which we then use to complete the assembly at our location in Phoenix, Arizona. As a result, the stability of component supply is crucial to our ability to get sufficient supplies to manufacture our products. Due to the fact we currently assemble our device from “off the shelf” parts and components, some of our critical devices and components are supplied by certain third-party manufacturers, and we may be unable to acquire necessary amounts of key components at competitive prices.

If we are successful in our growth, outsourcing the production of certain parts and components would be one way to reduce manufacturing costs. We plan to select these particular manufacturers based on their ability to consistently produce these products according to our requirements in an effort to obtain the best quality product at the most cost effective price. However, the loss of all or one of these suppliers or delays in obtaining shipments would have an adverse effect on our operations until an alternative supplier could be found, if one may be located at all. If we get to that stage of growth, such loss of manufacturers could cause us to breach any contracts we have in place at that time and would likely cause us to lose sales.

If our contract manufacturers fail to meet our requirements for quality, quantity and timeliness, our business growth could be harmed.

We obtain the primary components for the BDI-747/1 device from a third party supplier. This supplier likely procures most of the raw materials to make our device from third parties. If these companies were to terminate their agreements with our supplier, or our supplier with us, without adequate notice, or fail to provide the required capacity and quality on a timely basis, we would be delayed in our ability or unable to process and deliver our products to our customers.

Our products could contain defects or they may be installed or operated incorrectly, which could reduce sales of those products or result in claims against us.

Although we have quality assurance practices to ensure good product quality, defects still may be found in the future in our future products.

End-users could lose their confidence in our products and us if they unexpectedly use defective products or use our products improperly. This could result in loss of revenue, loss of profit margin, or loss of market share. Moreover, because our products may be employed in the automotive industry, if one of our products is a cause, or perceived to be the cause, of injury or death in a car accident, we would likely be subject to a claim. If we were found responsible it could cause us to incur liability which could interrupt or even cause us to terminate some or all of our operations.

If we are unable to recruit and retain qualified personnel, our business could be harmed.

Our growth and success highly depend on qualified personnel. Competition in the industry could cause us difficulty in recruiting or retaining a sufficient number of qualified technical personnel, which could harm our ability to develop new products. If we are unable to attract and retain necessary key talents, it would harm our ability to develop competitive product and retain good customers and could adversely affect our business and operating results.

Our BDI-747/1 device has lost its approval in a number of states and our number of devices on the road has been declining. At some point our business may not be viable. Our management is currently exploring all options regarding our current business, as well as other businesses.

Due to the decrease in the number of states where our BDI-747/1 device is approved, and the resulting decrease in the number of devices we have on the road, our management is currently exploring all options related to our business, including, but not limited to: (i) taking out loans or selling our stock in order to raise money to continue, and try to expand, our current business; (ii) trying to acquire a synergistic business and grow our current business; or (iii) selling our current business and trying to find another business to, in or out of our current business segment, to take over the public corporation. In the event we take out loans to fund our operations and/or public filing requirements, the terms of such financing may be on terms not favorable to us and could lead to a significant decrease in our stock price. In the event we sell our existing business or undergo a merger or business combination transaction our shareholders could incur significant dilution due to shares of our stock being issued to any incoming business.

| 9 |

As of December 31, 2018, our internal controls were not effective which led to material weaknesses in our internal controls over financial reporting and, as a result, we may not be able to report our financial results accurately or timely and in the future could have a problem to detecting fraud, which could have a material adverse effect on our business.

An effective internal control environment is necessary for us to produce reliable financial reports and is an important part of our effort to prevent financial fraud. We are required to periodically evaluate the effectiveness of the design and operation of our internal controls over financial reporting. Based on these evaluations, we may conclude that enhancements, modifications, or changes to internal controls are necessary or desirable. While management evaluates the effectiveness of our internal controls on a regular basis, these controls may not always be effective, and as of December 31, 2018 they were not effective. There are inherent limitations on the effectiveness of internal controls, including collusion, management override, and failure of human judgment. In addition, control procedures are designed to reduce rather than eliminate business risks. If we fail to maintain an effective system of internal controls, or if management or our independent registered public accounting firm discovers material weaknesses in our internal controls, we may be unable to produce reliable financial reports or prevent fraud, which could have a material adverse effect on our business, including subjecting us to sanctions or investigation by regulatory authorities, such as the Securities and Exchange Commission. Any such actions could result in an adverse reaction in the financial markets due to a loss of confidence in the reliability of our financial statements, which could cause the market price of our common stock to decline or limit our access to capital.

Our common stock has been thinly traded and we cannot predict the extent to which a trading market will develop.

Our common stock is quoted on the OTC Pink-tier of OTC Markets. Our common stock is thinly traded compared to larger more widely known companies. Thinly traded common stock can be more volatile than common stock trading in an active public market. We cannot predict the extent to which an active public market for our common stock will develop or be sustained after this offering.

Because we are subject to the “penny stock” rules, the level of trading activity in our stock may be reduced.

Our common stock is traded on the OTC Markets. Broker-dealer practices in connection with transactions in “penny stocks” are regulated by certain penny stock rules adopted by the Securities and Exchange Commission. Penny stocks, like shares of our common stock, generally are equity securities with a price of less than $5.00, other than securities registered on certain national securities exchanges or quoted on NASDAQ. The penny stock rules require a broker-dealer, prior to a transaction in a penny stock not otherwise exempt from the rules, to deliver a standardized risk disclosure document that provides information about penny stocks and the nature and level of risks in the penny stock market. The broker-dealer also must provide the customer with current bid and offer quotations for the penny stock, the compensation of the broker-dealer and its salesperson in the transaction, and, if the broker-dealer is the sole market maker, the broker-dealer must disclose this fact and the broker-dealer’s presumed control over the market, and monthly account statements showing the market value of each penny stock held in the customer’s account. In addition, broker-dealers who sell these securities to persons other than established customers and “accredited investors” must make a special written determination that the penny stock is a suitable investment for the purchaser and receive the purchaser’s written agreement to the transaction. Consequently, these requirements may have the effect of reducing the level of trading activity, if any, in the secondary market for a security subject to the penny stock rules, and investors in our common stock may find it difficult to sell their shares.

| 10 |

ITEM 1B – UNRESOLVED STAFF COMMENTS

This Item is not applicable to us as we are not an accelerated filer, a large accelerated filer, or a well-seasoned issuer; however, we have not received written comments from the Commission staff regarding our periodic or current reports under the Securities Exchange Act of 1934 within the last 180 days before the end of our last fiscal year.

As of December 31, 2018, our executive offices, consisted of approximately 1,200 square feet, were located at 5503 Cahuenga Blvd., #203, Los Angeles, California 91601. Under our lease of these premises, we were paying $2,212 per month and the lease was to run through January 2020, but this lease was transferred to another entity when Mr. Wainer sold his controlling interest to Doheny Group, LLC, a limited liability company controlled by David Haridim, our sole officer and director.

As of January 2, 2019, our executive offices are located at 1427 S. Robertson Blvd., Los Angeles, CA 90035, and we have this location rent free from our executive officer.

As of January 2, 2019, our manufacturing facility is located at 2352 E. University Drive, Suite D-105, Phoenix, AZ 85034, under the terms of a two year lease that ran from October 31, 2016 to October 31, 2018, at $1,030 per month. Beginning in November 2018 the lease went to month-to-month at $1,696 per month.

On February 21, 2018, we filed a Complaint in the Superior Court of the State of Arizona, County of Maricopa against EZ Interlock, LLC (Blow & Drive Interlock Corp. v. EZ Interlock, LLC (Case No. CV2018-051689, Superior Court of the State of Arizona, Maricopa County) for Conversion, Implied/Quasi Contract and Quantum Meruit, Unjust Enrichment, Tortious Interference with Business Expectancy/Prospective Business Relations, and Lost Profits. The basis for our lawsuit was that EZ Interlock an authorized installer of ours in the State of Arizona, was a customer of BDI Interlock, LLC, one of our distributors, and EZ Interlock was installing our BDI-747/1 devices for customers in Arizona and collecting fees from such customers, but stopped remitting payment to BDI Interlock, LLC, which, in turn, was unable to remit funds to us. We filed the lawsuit to have EZ Interlock stop installing our devices, return our devices in its possession, and pay the amounts owed to BDI Interlock and us for the customers paying EZ Interlock for our devices. EZ Interlock filed an Answer and Counterclaim on July 23, 2018. Shortly after filing our Complaint, the Court granted our request for a Temporary Restraining Order and Preliminary Injunction from continuing to install devices and return the devices in its possession. On February 7, 2019, our new management elected to dismiss the lawsuit, without prejudice, based on their opinion that our chances of recovering money from EZ Interlock was slim compared to amount that would be necessary to fund the litigation. We received most of our devices back from EZ Interlock. No discovery was conducted during the litigation.

In the ordinary course of business, we are from time to time involved in various pending or threatened legal actions. The litigation process is inherently uncertain and it is possible that the resolution of such matters might have a material adverse effect upon our financial condition and/or results of operations. However, in the opinion of our management, other than as set forth herein, matters currently pending or threatened against us are not expected to have a material adverse effect on our financial position or results of operations.

ITEM 4 – MINE SAFETY DISCLOSURES

There is no information required to be disclosed under this Item.

| 11 |

ITEM 5 - MARKET FOR REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES

Market Information

Our common stock is currently quoted on the OTCQB-tier of OTC Markets under the symbol “BDIC.” We were listed on June 30, 2015. The following table sets forth the high and low bid information for each quarter within the fiscal years ended December 31, 2018 and 2017, as best we could estimate from publicly-available information. The information reflects prices between dealers, and does not include retail markup, markdown, or commission, and may not represent actual transactions.

Fiscal Year Ended |

Bid Prices | |||||||||

| December 31, | Period | High | Low | |||||||

| 2017 | First Quarter | $ | 0.55 | $ | 0.28 | |||||

| Second Quarter | $ | 0.40 | $ | 0.19 | ||||||

| Third Quarter | $ | 0.36 | $ | 0.22 | ||||||

| Fourth Quarter | $ | 0.29 | $ | 0.22 | ||||||

| 2018 | First Quarter | $ | 0.39 | $ | 0.17 | |||||

| Second Quarter | $ | 0.30 | $ | 0.18 | ||||||

| Third Quarter | $ | 0.22 | $ | 0.07 | ||||||

| Fourth Quarter | $ | 0.08 | $ | 0.05 | ||||||

The Securities Enforcement and Penny Stock Reform Act of 1990 requires additional disclosure relating to the market for penny stocks in connection with trades in any stock defined as a penny stock. The Commission has adopted regulations that generally define a penny stock to be any equity security that has a market price of less than $5.00 per share, subject to a few exceptions which we do not meet. Unless an exception is available, the regulations require the delivery, prior to any transaction involving a penny stock, of a disclosure schedule explaining the penny stock market and the risks associated therewith.

We have not adopted any stock option or stock bonus plans.

Holders

As of December 31, 2018, there were 30,211,875 shares of our common stock outstanding held by 137 holders of record and numerous shares held in brokerage accounts. As of July 15, 2019, there were 31,350,683 shares of our common stock outstanding held by 140 holders of record. Of these shares, 19,779,768 were held by non-affiliates. As of June 30, 2018, we had 18,640,182 shares held by non-affiliates. On the cover page of this filing we value the 18,640,182 shares held by non-affiliates as of June 30, 2018 at $3,355,232. These shares were valued at $0.18 per share, based on our closing share price on June 30, 2018.

As of December 31, 2018, there were 1,000,000 shares of our preferred stock outstanding, with all shares being Series A Preferred Stock. Our Series A Preferred has One Million (1,000,000) shares authorized and the following rights: (i) no dividend rights; (ii) no liquidation preference over our common stock; (iii) no conversion rights; (iv) no redemption rights; (v) no call rights; (vi) each share of Series A Convertible Preferred stock will have one hundred (100) votes on all matters validly brought to our common stockholders. As of December 31, 2018, all 1,000,000 shares of Series A Preferred Stock were held by Laurence Wainer, our then sole officer and director. As of March 20, 2019, the 1,000,000 shares of Series A Preferred Stock are held by The Doheny Group, LLC, a limited liability company controlled by David Haridim, our sole officer and director.

| 12 |

Warrants

We currently have warrants to acquire 5,787,586 shares of our common stock held by 105 holders. The warrants have expiration dates ranging from three to four years from the date of grant and exercise prices ranging from $0.10 to $1.00.

Dividends

There have been no cash dividends declared on our common stock, and we do not anticipate paying cash dividends in the foreseeable future. Dividends are declared at the sole discretion of our Board of Directors.

Securities Authorized for Issuance Under Equity Compensation Plans

There are no outstanding options or warrants to purchase shares of our common stock under any equity compensation plans.

Currently, we do not have any equity compensation plans. As a result, we did not have any options, warrants or rights outstanding under equity compensation plans as of December 31, 2018.

Recent Issuance of Unregistered Securities

During the three months ended December 31, 2018, we did not issue any unregistered securities.

If our stock is listed on an exchange we will be subject to the Securities Enforcement and Penny Stock Reform Act of 1990 requires additional disclosure relating to the market for penny stocks in connection with trades in any stock defined as a penny stock. The Commission has adopted regulations that generally define a penny stock to be any equity security that has a market price of less than $5.00 per share, subject to a few exceptions which we do not meet. Unless an exception is available, the regulations require the delivery, prior to any transaction involving a penny stock, of a disclosure schedule explaining the penny stock market and the risks associated therewith.

ITEM 6 – SELECTED FINANCIAL DATA

As a smaller reporting company we are not required to provide the information required by this Item.

ITEM 7 - MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATION

Disclaimer Regarding Forward Looking Statements

In this document we make a number of statements, referred to as “forward-looking statements”, that are intended to convey our expectations or predictions regarding the occurrence of possible future events or the existence of trends and factors that may impact our future plans and operating results. The safe harbor for forward-looking statements provided by the Private Securities Litigation Reform Act of 1995 does not apply to us. We note, however, that these forward-looking statements are derived, in part, from various assumptions and analyses we have made in the context of our current business plan and information currently available to us and in light of our experience and perceptions of historical trends, current conditions and expected future developments and other factors we believe to be appropriate in the circumstances. You can generally identify forward-looking statements through words and phrases such as “seek,” “anticipate,” “believe,” “estimate,” “expect,” “intend,” “plan,” “budget,” “project,” “may be,” “may continue,” “may likely result,” and similar expressions. When reading any forward looking-statement you should remain mindful that all forward-looking statements are inherently uncertain as they are based on current expectations and assumptions concerning future events or future performance of our company, and that actual results or developments may vary substantially from those expected as expressed in or implied by that statement for a number of reasons or factors, including those relating to:

| ● | whether or not our breath alcohol ignition interlock device receives the necessary certifications; | |

| ● | whether or not markets for our products develop and, if they do develop, the pace at which they develop; | |

| ● | our ability to attract and retain the qualified personnel to implement our growth strategies; | |

| ● | our ability to fund our short-term and long-term operating needs; | |

| ● | changes in our business plan and corporate strategies; and | |

| ● | other risks and uncertainties discussed in greater detail in the sections of this document. |

| 13 |

Each forward-looking statement should be read in context with, and with an understanding of, the various other disclosures concerning our company and our business made elsewhere in this document as well as other public reports filed with the Securities and Exchange Commission. You should not place undue reliance on any forward-looking statement as a prediction of actual results or developments. We are not obligated to update or revise any forward-looking statement contained in this document to reflect new events or circumstances unless and to the extent required by applicable law.

Overview and Outlook

We are a previous development stage company that was incorporated in the State of Delaware in July 2013. In the year ending December 31, 2018, we generated total revenues of $942,160, compared to $1,235,433 in the year ending December 31, 2017.

We market distributorships and lease a breath alcohol ignition interlock device called the BDI-747/1, which is a mechanism that is installed on the steering column of an automobile and into which a driver exhales. The device in turn provides a blood-alcohol concentration analysis. If the driver’s blood-alcohol content is higher than a certain pre-programmed limit, the device prevents the ignition from engaging and the automobile from starting. These devices are often required for use by DUI or DWI (“driving under the influence” or “driving while intoxicated”) offenders as part of a mandatory court or motor vehicle department program.

We paid Well Electric, a company located in China with experience in design and manufacture of ignition interlock devices, $30,000 to design and manufacture the prototype ignition interlock device for us. Well Electric produced six prototype devices for us which we received in November 2014.

At July 27, 2015 we began production of our patent pending BDI Model #1 power line filter to attach to our BDI-747 Breath Alcohol Ignition Interlock Device which together were certified by NHSTA on June 17, 2015 to work to together to meet or exceed 2013 NHSTA guidelines.

As of December 31, 2018, the BDI-747/1 device was approved in Oregon, Texas, Arizona, and Kentucky. As of March 31, 2019, the BDI-747/1 device was only approved in Arizona and Texas. The states where our BDI-747/1 device is approved has decreased primarily as a result of new state certification rules that require increased capital investment that we are not able to afford.

We have a storefront location in Phoenix, Arizona and contract with four qualified contractors to install, calibrate, remove and monitor the devices. Our business plan includes growth of the company by continuing to complete and submit more state applications and to build up our service infrastructure by utilizing our own retail infrastructure, distributors and franchisees.

As of December 31, 2018, we had approximately 1,100 units on the road, with approximately 885 devices being leased directly from us and approximately 215 devices leased through our distributors, compared to December 31, 2017, when we had approximately 1,558 units on the road, with approximately 1,451 devices being leased directly from us and approximately 107 devices leased through our distributors. The decrease in the total number of devices we have on the road is primarily due to the fact the BDI-747/1 devices was approved in fewer states in 2018 compared to 2017.

Due to the decrease in the number of states where our BDI-747/1 device is approved, and the resulting decrease in the number of devices we have on the road, our management is currently exploring all options related to our business, including, but not limited to: (i) taking out loans or selling our stock in order to raise money to continue, and try to expand, our current business; (ii) trying to acquire a synergistic business and grow our current business; or (iii) selling our current business and trying to find another business to, in or out of our current business segment, to take over the public corporation.

| 14 |

Results of Operations for the Years Ended December 31, 2018 and 2017

| Year Ended December 31, | ||||||||

| 2018 | 2017 | |||||||

| Monitoring revenue | $ | 862,330 | $ | 926,454 | ||||

| Distributorship revenues | 79,830 | 308,979 | ||||||

| Total revenues | 942,160 | 1,235,433 | ||||||

| Monitoring cost of revenue | 118,596 | 153,059 | ||||||

| Distributorship cost of revenues | - | 7,738 | ||||||

| Total cost of revenues | 118,596 | 160,797 | ||||||

| Gross profit | 823,564 | 1,074,636 | ||||||

| Operating expenses: | ||||||||

| Payroll | 888,498 | 473,620 | ||||||

| Professional fees | 157,764 | 146,406 | ||||||

| General and administrative | 763,683 | 841,961 | ||||||

| Depreciation | - | 338,044 | ||||||

| Impairment of fixed assets | - | 801,983 | ||||||

| Total operating expenses | 1,809,945 | 2,602,014 | ||||||

| Loss from operations | (986,381 | ) | (1,527,378 | ) | ||||

| Interest expense, net | (494,321 | ) | (943,415 | ) | ||||

| Change in fair value of derivative liability | 5,155 | 68,078 | ||||||

| Gain (loss) on extinguishment of debt | 311,670 | (305,000 | ) | |||||

| Loan default penalty | (635,000 | ) | - | |||||

| Total other income (expense) | (812,496 | ) | (1,180,337 | ) | ||||

| Loss before provision for income taxes | (1,798,877 | ) | (2,707,715 | ) | ||||

| Provision for income taxes | 800 | 1,600 | ||||||

| Net loss | $ | (1,799,677 | ) | $ | (2,709,315 | ) | ||

Operating Loss; Net Loss

Our net loss decreased by $909,638, from $2,709,315 to $1,799,677 from the year ended 2017 compared to 2018. Our operating loss decreased by $540,997, from $1,527,378 to $986,381 for the same periods. The change in our net loss for the year ended December 31, 2018, compared to the prior year is primarily a result of the fact we impaired our assets and had a significant depreciation expense in the year ended 2017, which we did not have in 2018, partially offset by a decrease in our revenues and an increase in our payroll expense. These changes are detailed below.

Revenue

During the year ended December 31, 2018 we had $942,160 in revenues, with $862,330 coming from revenue from the monthly recurring payments we received from our customers that rent our BDI-747/1 breathalyzer device for the ongoing monitoring services related to the devices, and $79,830 coming from revenues paid to us from our distributors, compared to $926,454 and $308,979 from these revenue sources for the same period one year ago. Our revenue decreased overall during the year ended December 31, 2018 due to us having approximately 1,100 units on the road, compared to the year ended December 31, 2017, when we had approximately 1,558 units on the road. Notably, the source of our revenue continued to shift from revenue received our distributors to the revenue we receive from the monthly recurring payments we received from our customers that rent our BDI-747/1 breathalyzer device for the ongoing monitoring services related to the devices in the period ended December 31, 2018, compared to December 31, 2017. We expect the majority of our revenue in the future to come from the monthly recurring payments we receive from our customers that rent our BDI-747/1 breathalyzer device for the ongoing monitoring services related to the devices and not from distributors as we shift away from using distributors and more towards direct retail of our devices. We expect the revenue we receive from monitoring our devices on the road, as well as revenue from distributors, will increase in any periods we have more devices on the road versus the comparable period and will decrease in any period we have fewer units on the road versus the comparable period. We do not believe our revenues will increase if our number of devices on the road decreases since we do not believe we will charge more for leasing the BDI-747/1 device than what we charge now in the foreseeable future.

| 15 |

Cost of Revenue

Our cost of revenue for the year ended December 31, 2018 was $118,596, compared to $160,797 for the year ended December 31, 2017. Our cost of revenue for the year ended December 31, 2018 was $118,596 for the revenue we received for the ongoing maintenance for units we lease to customers, and $0 related to the revenue we received from distributors. Our cost of revenue for the year ended December 31, 2017 was $153,059 for the revenue we received for the ongoing maintenance for units we lease to customers, and $7,738 related to the revenue we received from distributors. Again, we expect this shift in our cost of revenue to monitoring cost of revenue to continue as we move away from using distributors and more towards direct retail of our devices.

Payroll

Our payroll increased by $414,878, from $473,620 to $888,498, from the year ended December 31, 2017 compared to December 31, 2018. The significant increase in our payroll expense was primarily a result of us contracting with additional personnel in 2018 to service the units we had on the road during the year.

Professional Fees

Our professional fees increased during the year ended December 31, 2018 compared to the year ended December 31, 2017. Our professional fees were $157,764 for the year ended December 31, 2018 and $146,406 for the year ended December 31, 2017. These fees are largely related to fees paid for legal, accounting and audit services. We expect these fees to continue grow steadily if our business expands. In the event we undertake an unusual transaction, such as an acquisition or file a registration statement, we would expect these fees to substantially increase during that period.

General and Administrative Expenses

General and administrative expenses decreased by $78,278, from $841,961 for the year ended December 31, 2017 to $763,683 for the year ended December 31, 2018. This decrease was primarily related to a significant decrease in advertising expenses in 2018 compared to 2017, a fixed asset adjustment in 2018 when we returned a number of parts to our supplier, and lower commissions paid in 2018 since we paid our last commissions in 2017, partially offset by higher rent expense due to locations in Arizona, higher royalty payments in 2018 and an increase in special parts we ordered from our supplier in 2018.

Depreciation

Our depreciation decreased from $338,044 for the year ended December 31, 2017 to $0 for the year ended December 31, 2018. Our depreciation expense in the period ended September 30, 2017 was primarily related to the depreciation of the BDI-747/1 device. Since we fully impaired our remaining BDI-747/1 devices for the year ended December 31, 2017, due to the uncertainty with the direction of our business going forward, we did not have a depreciation expense for the year ended December 31, 2018.

| 16 |

Impairment of Fixed Assets

During the year ended December 31, 2017, we had impairment of fixed assets of $801,983, compared to $0 during 2018. The impairment of our fixed assets in the year ended December 31, 2017 is a result of our management currently determining whether our current business model and operations are viable. Until this determination has been made, we have elected to impair our assets.

Interest Expense

Interest expense decreased by $449,094 from $943,415 for the year ended December 31, 2017 to $494,321 for the year ended December 31, 2018. For both periods these amounts are largely due to the interest we owe on outstanding debt including amortization of debt discount costs. The interest expense significantly decreased for the period ended December 31, 2018, compared to the same period one year ago, due to our decrease in outstanding debt compared to one year ago, and the related accretion of the amount of debt discount associated with the debt.

Change in Fair Value of Derivative Liability

During the year ended December 31, 2018, we had a change in fair value of derivative liability of $5,155 compared to $68,078 for the same period in 2017. The change in fair value of derivative liability for both periods, relates to the conversion feature of a promissory note we had outstanding during this period. Since the conversion price on the promissory note is calculated based on a discount to the closing price of our common stock, as our closing price fluctuates it changes the fair value of the derivative liability.

Loss on Extinguishment of Debt

During the year ended December 31, 2018, we had a gain on extinguishment of debt of $311,670 compared to a loss of ($305,000) for the same period in 2017. The gain on extinguishment of debt in the year ended December 31, 2018, relates to the settlement of three notes payable and related accrued interest totaling $73,640 for a total payment of $17,000, resulting in gains totaling $56,640, and the release of two claims of accrued royalties totaling $255,030. The loss on extinguishment of debt in the year ended December 31, 2017, relates to the conversion of a note balance totaling $43,561.50 owed to Mr. Laurence Wainer into shares of our Series A Preferred Stock.

Liquidity and Capital Resources for Year Ended December 31, 2018 Compared to Year Ended December 31, 2017

Introduction

During the year ended December 31, 2018 and 2017, because of our operating losses, we did not generate positive operating cash flows. Our cash on hand as of December 31, 2018 was $775 and our cash used in operations is approximately $100,000 per month. As a result, we have short term cash needs. These needs are being satisfied through proceeds from the sales of our securities and loans from both related parties and third parties. We currently do not believe we will be able to satisfy our cash needs from our revenues for some time.

Our cash, current assets, total assets, current liabilities, and total liabilities as of December 31, 2018 and as of December 31, 2017, respectively, are as follows:

| December 31, 2018 | December 31, 2017 | Change | ||||||||||

| Cash | $ | 775 | $ | 31,874 | $ | (31,099 | ) | |||||

| Total Current Assets | 7,146 | 63,445 | (56,299 | ) | ||||||||

| Total Assets | 13,627 | 68,576 | (54,949 | ) | ||||||||

| Total Current Liabilities | 564,477 | 585,749 | (21,272 | ) | ||||||||

| Total Liabilities | $ | 2,616,143 | $ | 1,449,846 | $ | 1,166,297 | ||||||

| 17 |

Our current assets decreased as of December 31, 2018 as compared to December 31, 2017, due to us having less cash on hand, less accounts receivable, net, and less prepaid expenses. The decrease in our total assets between the two periods was also related to the decrease in our cash on hand, accounts receivable, net, and prepaid expenses, partially offset by a slight increase in deposits as of December 31, 2018.

Our current liabilities decreased by $21,272, as of December 31, 2018 as compared to December 31, 2017. This slight decrease was primarily due to decreases in our accounts payable, accrued royalty payable, deferred revenue, notes payable-related party, and convertible notes payable, partially offset by increases in accrued expenses, accrued interest, accrued interest – related party, derivative liability, and notes payable.

In order to repay our obligations in full or in part when due, we will be required to raise significant capital from other sources. There is no assurance, however, that we will be successful in these efforts.

Sources and Uses of Cash

Operations

We had net cash used in operating activities of $1,112,658 for the year ended December 31, 2018, as compared to $384,641 for the year ended December 31, 2017. For the period in 2018, the net cash used in operating activities consisted primarily of our net loss of ($1,799,677), adjusted primarily by shares issued for services of $114,642, gain on extinguishment of debt of ($311,670), change in fair value of derivative liability of ($5,155), loan default penalty of $635,000, and amortization of debt discount of $30,872, as well as changes in accrued expenses of $44,456, deferred revenue of ($92,216), accounts payable of ($39,695), prepaid expenses of $289, accrued royalties payable of ($101,922), accrued interest $19,773, accrued interest related party of $165,240, and accounts receivable of $23,561. For the period in 2017, the net cash used in operating activities consisted primarily of our net loss of ($2,709,315), adjusted primarily by impairment of long-lived assets of $804,322, depreciation of $338,044, shares and warrants issued for services of $14,191, loss on extinguishment of debt of $305,000, write off of debt discount due to refinance of $352,511, loss on disposal of property and equipment of $98,800, change in fair value of derivative liability of ($61,254), and amortization of debt discount of $361,676, as well as changes in accrued expenses of ($34,625), deferred revenue of $22,047, deposits of $1,123, accounts payable of $6,552, inventory of $10,650, prepaid expenses of ($294), accrued royalties payable of $58,026, income taxes payable of $230, accrued interest of $2,020 accrued interest related party of $23,330, and accounts receivable of $22,325.

Investments

We did not have cash used in investing activities in the year ended December 31, 2018, compared to $634,820 for December 31, 2017. For the year ended December 31, 2017, cash used in investing activities consisted of $884,820 of purchase of furniture and equipment, offset by $250,000 deposits used against the cost of purchasing interlock units.

Financing

Our net cash provided by financing activities for the year ended December 31, 2018 was $1,081,559, compared to $935,026 for the year ended December 31, 2017. For the year ended December 31, 2018, our net cash from financing activities consisted of proceeds from notes payable of $154,400, proceeds from notes payable-related party of $649,127, proceeds from issuance of common stock of $458,705, and proceeds from issuance of convertible notes payable of $20,000, partially offset by repayments of notes payable of ($74,623) and payments on note payable related party of ($126,050). For the year ended December 31, 2017, our net cash from financing activities consisted of proceeds from notes payable of $50,000, proceeds from notes payable-related party of $250,400, proceeds from issuance of common stock of $849,037, and proceeds from issuance of convertible notes payable of $5,000, partially offset by repayments of notes payable of ($56,662), payments on convertible notes payable of ($50,000), and payments on note payable related party of ($112,749).

| 18 |

Contractual Obligations

As of December 31, 2018, we had the following contractual obligations for 2018 through 2022:

| 2019 | 2020 | 2021 | 2022 | 2023 | Total | |||||||||||||||||||

| Debt obligations (1) | $ | 831,444 | $ | 637,004 | $ | 626,334 | $ | 606,000 | $ | 2,575,500 | $ | 5,276,282 | ||||||||||||

| Capital leases | - | - | - | - | - | - | ||||||||||||||||||

| Operating leases | - | - | - | - | - | - | ||||||||||||||||||

| $ | 831,444 | $ | 637,004 | $ | 626,334 | $ | 606,000 | $ | 2,575,500 | $ | 5,276,282 | |||||||||||||

| (1) | The interest amounts for the contractual obligation for each year have been estimated. |

Off Balance Sheet Arrangements

We have no off balance sheet arrangements.

ITEM 7A – QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK

As a smaller reporting company we are not required to provide the information required by this Item.

ITEM 8 - FINANCIAL STATEMENTS AND SUPPLEMENTARY DATA

For a list of financial statements and supplementary data filed as part of this Annual Report, see the Index to Financial Statements beginning at page F-1 of this Annual Report.

ITEM 9 - CHANGES IN AND DISAGREEMENTS WITH ACCOUNTANTS ON ACCOUNTING AND FINANCIAL DISCLOSURE

There are no items required to be reported under this Item.

ITEM 9A - CONTROLS AND PROCEDURES

(a) Evaluation of Disclosure Controls and Procedures

We carried out an evaluation, under the supervision and with the participation of our management, including our Chief Executive Officer and Chief Financial Officer (our Principal Accounting Officer), of the effectiveness of our disclosure controls and procedures (as defined) in Exchange Act Rules 13a – 15(c) and 15d – 15(e)). Based upon that evaluation, our Chief Executive Officer and Chief Financial Officer, who are our principal executive officer and principal financial officers, respectively, concluded that, as of the end of the period ended December 31, 2018, our disclosure controls and procedures were not effective (1) to ensure that information required to be disclosed by us in reports that we file or submit under the Exchange Act is recorded, processed, summarized and reported, within the time periods specified in the SEC’s rules and forms and (2) to ensure that information required to be disclosed by us in the reports that we file or submit under the Exchange Act is accumulated and communicated to us, including our chief executive and chief financial officers, as appropriate to allow timely decisions regarding required disclosure.

Our Chief Executive Officer and Chief Financial Officer (our Principal Accounting Officer) do not expect that our disclosure controls or internal controls will prevent all error and all fraud. No matter how well conceived and operated, our disclosure controls and procedures can provide only a reasonable level of assurance regarding the reliability of financial reporting and the preparation of financial statements for external purposes in accordance with generally accepted accounting principles. Further, the design of a control system must reflect the fact that there are resource constraints, and the benefits of controls must be considered relative to their costs. Because of the inherent limitations in all control systems, no evaluation of controls can provide absolute assurance that all control issues and instances of fraud, if any, within the Company have been detected. These inherent limitations include the realities that judgments in decision-making can be faulty, and that breakdowns can occur because of a simple error or mistake. Additionally, controls can be circumvented if there exists in an individual a desire to do so. There can be no assurance that any design will succeed in achieving its stated goals under all potential future conditions.

| 19 |

Furthermore, smaller reporting companies face additional limitations. Smaller reporting companies employ fewer individuals and find it difficult to properly segregate duties. Often, one or two individuals control every aspect of the company’s operation and are in a position to override any system of internal control. Additionally, smaller reporting companies tend to utilize general accounting software packages that lack a rigorous set of software controls.

(b) Management’s Annual Report on Internal Control Over Financial Reporting

Our management is responsible for establishing and maintaining adequate internal control over financial reporting. Internal control over financial reporting is defined in Rules 13a-15(f) and 15d-15(f) promulgated under the Exchange Act, as amended, as a process designed by, or under the supervision of, our Chief Executive Officer and Chief Financial Officer (our Principal Financial Officer), and effected by our board of directors, management and other personnel, to provide reasonable assurance regarding the reliability of financial reporting and the preparation of financial statements for external purposes in accordance with generally accepted accounting principles in the United States and includes those policies and procedures that:

| ● | Pertain to the maintenance of records that in reasonable detail accurately and fairly reflect our transactions and any disposition of our assets;

|

| ● | Provide reasonable assurance that transactions are recorded as necessary to permit preparation of financial statements in accordance with generally accepted accounting principles, and that our receipts and expenditures are being made only in accordance with authorizations of our management and directors; and |

| ● | Provide reasonable assurance regarding prevention or timely detection of unauthorized acquisition, use or disposition of our assets that could have a material effect on the financial statements. |

A material weakness is a deficiency, or a combination of deficiencies, in internal control over financial reporting, such that there is a reasonable possibility that a material misstatement of our annual or interim financial statements will not be prevented or detected on a timely basis. Our management assessed the effectiveness of our internal control over financial reporting as of December 31, 2018. In making this assessment, our management used the criteria set forth by the Committee of Sponsoring Organizations of the Treadway Commission (COSO) in Internal Control-Integrated Framework. Based on this assessment, Management has identified the following three material weaknesses that have caused management to conclude that, as of December 31, 2018, our disclosure controls and procedures, and our internal control over financial reporting, were not effective at the reasonable assurance level:

1. We do not have sufficient segregation of duties within accounting functions, which is a basic internal control. Due to our size and nature, segregation of all conflicting duties may not always be possible and may not be economically feasible. However, to the extent possible, the initiation of transactions, the custody of assets and the recording of transactions should be performed by separate individuals. Management evaluated the impact of our failure to have segregation of duties on our assessment of our disclosure controls and procedures and has concluded that the control deficiency that resulted represented a material weakness.