UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM

| ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For

the Fiscal Year Ended

OR

| TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For The Transition Period From ________ To ________

Commission

File Number

(Exact name of registrant as specified in its charter)

(State or other jurisdiction of incorporation or organization) |

(I.R.S. Employer Identification No.) | |

| (Address of principal executive offices) | (Zip Code) |

Registrant’s

telephone number, including area code:

Securities Registered Pursuant to Section 12(b) of the Exchange Act:

| Title of Each Class | Trading Symbols | Name of Each Exchange on Which Registered | ||

| The Capital Market | ||||

| The

|

Securities Registered Pursuant to Section 12(g) of the Exchange Act: None

Indicate

by check mark whether the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐

Indicate

by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Exchange Act. Yes ☐

Indicate

by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Exchange Act during

the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject

to such filing requirements for the past 90 days.

Indicate

by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data

File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period

that the registrant was required to submit and post such files).

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company”, and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ☐ | Accelerated filer | ☐ |

| ☒ | Smaller reporting company | ||

| Emerging growth company |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate

by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness

of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered

public accounting firm that prepared or issued its audit report. Yes ☐ No

If

securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant

included in the filing reflect the correction of an error to previously issued financial statements.

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate

by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No

The

aggregate market value of the voting common equity held by non-affiliates of the registrant was $

As of March 26, 2024, ordinary shares, par value $0.001 (USD) per share, were outstanding.

Documents Incorporated by Reference:

OXBRIDGE RE HOLDINGS LIMITED

Index to Annual Report on Form 10-K

Year Ended December 31, 2023

| 2 |

SPECIAL NOTE ABOUT FORWARD-LOOKING STATEMENTS

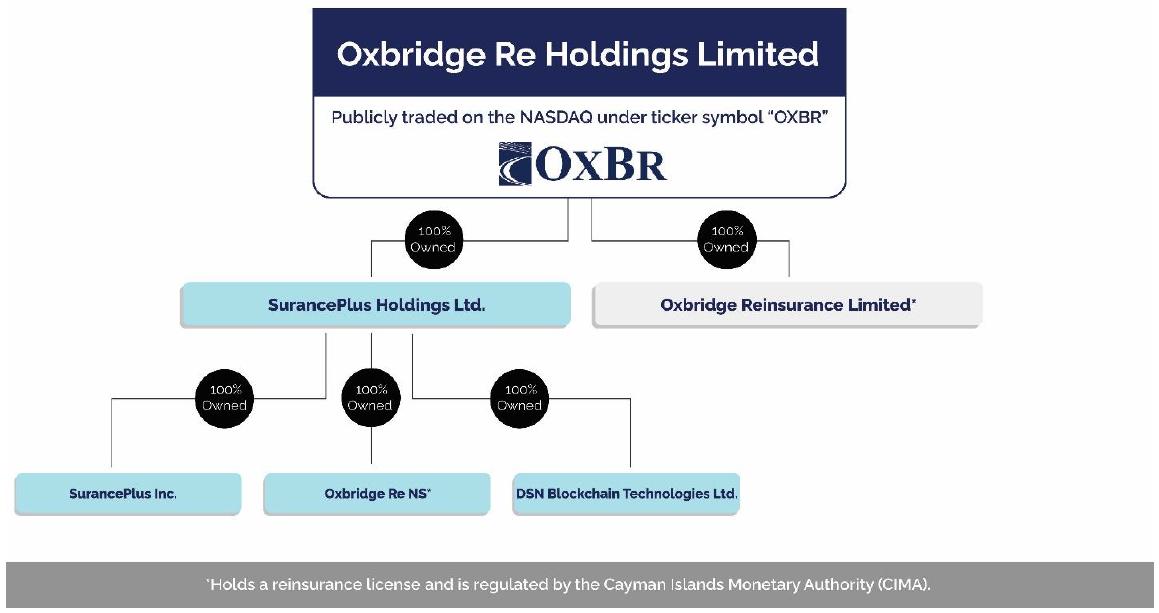

Unless the context dictates otherwise, references to “we,” “us,” “our,” “our company,” or “the Company” in this Annual Report on Form 10-K refer to Oxbridge Re Holdings Limited and its wholly-owned subsidiaries, Oxbridge Reinsurance Limited, SurancePlus Holdings Ltd., Oxbridge Re NS, SurancePlus Inc. and DSN Blockchain Technologies Ltd.

All statements in this Annual Report on Form 10-K, including in the section entitled “Management’s Discussion and Analysis of Financial Condition and Results of Operations” (refer to Part I, Item 7 of this Annual Report on Form 10-K), other than statements of historical fact, including estimates, projections, statements relating to our business plans, objectives and expected operating results, and the assumptions upon which those statements are based, are “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995, Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”). These forward-looking statements generally are identified by the words such as “believe,” “project,” “predict,” “expect,” “anticipate,” “estimate,” “intend,” “plan,” “may,” “should,” “will,” “would,” “will be,” “will continue,” “will likely result,” and similar expressions. Forward-looking statements are based on current expectations and assumptions that are subject to risks and uncertainties which may cause actual results to differ materially from our historical results and the forward-looking statements and you should not place undue reliance on the forward-looking statements. A detailed discussion of risks and uncertainties that could cause actual results and events to differ materially from such forward-looking statements is included in the section entitled “Risk Factors” (refer to Part I, Item 1A, of this Annual Report on Form 10-K). We undertake no obligation, other than imposed by law, to publicly update or revise any forward-looking statements, whether as a result of new information, future events, or otherwise. Readers are cautioned not to place undue reliance on the forward-looking statements which speak only to the dates on which they were made.

PART I

ITEM 1 BUSINESS

Overview

We are a Cayman Islands specialty property and casualty reinsurer that provides reinsurance solutions through our reinsurance subsidiaries, Oxbridge Reinsurance Limited and Oxbridge Re NS. We focus on underwriting fully collateralized reinsurance contracts primarily for property and casualty insurance companies in the Gulf Coast region of the United States, with an emphasis on Florida. We specialize in underwriting medium frequency, high severity risks, where we believe sufficient data exists to analyze effectively the risk/return profile of reinsurance contracts. Oxbridge Re NS functions as a reinsurance sidecar which increases the underwriting capacity of Oxbridge Reinsurance Limited. Oxbridge Re NS issues participating notes to third party investors, the proceeds of which are utilized to collateralize Oxbridge Reinsurance Limited’s reinsurance obligations.

In addition to our historical reinsurance business operations, in 2023, our new subsidiary SurancePlus Inc. (“SurancePlus”) began developing, offering, and selling a tokenized reinsurance security representing fractionalized interests in reinsurance contracts, with each token representing an interest in participating notes issued by Oxbridge Re NS. These efforts culminated in the development, launch, and issuance of our first tokenized reinsurance security, the DeltaCat Re Token, which we believe is the first “on-chain” reinsurance security of its kind to be developed by a subsidiary of a public company. Following the issuance of the DeltaCat Re Token, we intend to develop, launch, and issue additional series of tokenized reinsurance securities representing fractional interests in reinsurance contracts, and we are also using our tokenization experience and activities as a foundation for developing Web3-focused business offerings and products relating to the tokenization of other real-world assets (RWAs), including RWAs held or being acquired by third parties. Our tokenization business will be conducted through SurancePlus and through other subsidiaries of our wholly owned subsidiary, SurancePlus Holdings Ltd. (“SurancePlus Holdings”), a Cayman Islands exempted company that we have organized to serve as a holding company for subsidiaries that will operate our developing Web3-focused business operations.

In our historical reinsurance business operations, we underwrite reinsurance contracts on a selective and opportunistic basis as opportunities arise based on our goal of achieving favorable long-term returns on equity for our shareholders. Our goal is to achieve long-term growth in book value per share by writing business that generates attractive underwriting profits relative to the risk we bear. Additionally, we intend to complement our underwriting profits with investment profits on an opportunistic basis. Our underwriting business focus is on fully collateralized reinsurance contracts for property catastrophes, primarily in the Gulf Coast region of the United States. Within that market and risk category, we attempt to select the most economically attractive opportunities across a variety of property and casualty insurers. As we attempt to grow our capital base, we expect that we will consider growth opportunities in other geographic areas and risk categories.

Our level of profitability in our reinsurance business operations is primarily determined by how adequately our premiums assumed and investment income cover our costs and expenses, which consist primarily of acquisition costs and other underwriting expenses, claim payments and general and administrative expenses. One factor leading to variation in our operational results is the timing and magnitude of any follow-on offerings we undertake (if any), and issuance of participating notes to investors as we are able to deploy new capital to collateralize new reinsurance treaties and consequently, earn additional premium revenue. In addition, our results of operations may be seasonal in that hurricanes and other tropical storms typically occur during the period from June 1 through November 30. Further, our results of operations may be subject to significant variations due to factors affecting the property and casualty insurance industry in general, which include competition, legislation, regulation, general economic conditions, judicial trends, and fluctuations in interest rates and other changes in the investment environment.

| 3 |

Because we employ an opportunistic underwriting and investment philosophy, period-to-period comparisons of our underwriting results may not be meaningful. In addition, our historical investment results may not necessarily be indicative of future performance. Due to the nature of our reinsurance and investment strategies, our operating results will likely fluctuate from period to period.

Organizational Chart

Other Developments

Formation of SurancePlus

SurancePlus Inc., an indirect wholly-owned subsidiary of Oxbridge Re Holdings Limited, was incorporated as a British Virgin Islands Business Company on December 19, 2022 for the purposes of tokenizing reinsurance contracts underwritten by its affiliated licensed reinsurer, Oxbridge Re NS.

On March 27, 2023, we, through SurancePlus, issued a press release announcing the commencement of an offering by SurancePlus of up to $5.0 million of DeltaCat Re Tokens (“Tokens”) with a purchase price of $10.00 per Token and representing one share of Series DeltaCat Re Preferred Shares per Token (the “Private Placement”).

On June 27, 2023, SurancePlus completed the Private Placement. The aggregate amount raised in the Private Placement was $2,447,760 for the issuance of 244,776 Tokens, of which approximately $1,280,000 was received from third-party investors and approximately $1,167,000 was received from Oxbridge Re Holdings Limited.

On September 11, 2023, the DeltaCat Re tokens were reclassified as tokenized interests carrying rights equivalent to the DeltaCat Re Preferred Shares in accordance with the provisions of the British Virgin Islands law.

| 4 |

Oxbridge Acquisition Corp.

On February 28, 2023, the Company announced in a press release that Oxbridge Acquisition Corp. (“Oxbridge Acquisition”) filed a Current Report on Form 8-K with the Securities and Exchange Commission in connection with Oxbridge Acquisition’s business combination with Jet Token Inc., a Delaware corporation. Upon the closing of the transaction, the combined company became Jet.AI Inc. (“Jet.AI”). Jet.AI offers fractional aircraft ownership, jet card, aircraft brokerage and charter service through its fleet of private aircraft and those of Jet.AI’s Argus Platinum operating partner. Jet.AI’s charter app enables travelers to look, book and fly. The funding and capital markets access from this transaction is expected to enable Jet.AI to continue its growth strategy of AI software development and fleet expansion. The business combination was completed on August 10, 2023.

The Company’s wholly-owned licensed reinsurance subsidiary, Oxbridge Reinsurance Limited (“Oxbridge Reinsurance”), was the lead investor in Oxbridge Acquisition’s sponsor and currently indirectly holds the equivalent of 1,423,827 of Jet.AI common stock (NASDAQ: JTAI), 3,094,999 of Jet.AI public warrants (NASDAQ: JTAIW) and 285 of Jet.AI Series A-1 Convertible Preferred Stock with purchase price of $285,000.

Bridge Loan with Affiliate

On September 11, 2023, the Company, along with seven (7) other investors, entered into a binding term sheet (“Bridge Agreement”) with Jet.AI to provide Jet.AI with an aggregate sum of $500,000 of short-term bridge financing pending its receipt of funds from its other existing financing arrangements. During the month of September 2023, and prior to the Bridge Agreement, Jet.AI had engaged in discussions with numerous third parties to secure short-term bridge funding but was not offered terms it found acceptable.

The Bridge Agreement provides for the issuance of Notes in an aggregate principal amount of $625,000, reflecting a 20% original issue discount. The Notes bear interest at 5% per annum and mature on March 11, 2024. Jet.AI is required to redeem the Notes with 100% of the proceeds of any equity or debt financing at a redemption premium of 110% of the principal amount of the Notes. Jet.AI anticipates redeeming the Notes in full with proceeds expected to be received over the next several months from existing financing arrangements.

An event of default under the Notes includes failing to redeem the Notes as provided above and other typical bankruptcy events of Jet.AI. In an event of default, the outstanding principal amount of the Notes will increase by 120%, and the company may convert its Note into shares of common stock of Jet.AI at the conversion price set forth in the Bridge Agreement with registration rights associated with those shares.

The Company invested the sum of $100,000 in the Notes and is recorded as “Loan Receivable” on the consolidated balance sheets at cost. On March 11, 2024, the Notes matured and were redeemed by Jet.AI in accordance with the Bridge Agreement. The Company receive an aggregate of $140,000 upon the redemption of the Notes.

Our Business Strategy

Our goal is to achieve attractive risk-adjusted returns for our shareholders through the prudent management of underwriting and investments risks relative to our capital base. To achieve this objective, the following are the principal elements of our business strategy.

| ● | Maintain a Commitment to Disciplined Underwriting. We employ a disciplined and data-driven underwriting approach to select a diversified portfolio of risks that we believe will generate an attractive return to our shareholders over the long term. Neither our underwriting nor our investment strategies are designed to generate smooth or predictable quarterly earnings, but rather to optimize growth in book value per share over the long term. | |

| ● | Focus on Risk Management. We treat risk management as an integral part of our underwriting and business management processes. All of our reinsurance contracts contain loss limitation provisions that limit our losses to the value of the assets collateralizing our reinsurance contracts. |

| 5 |

| ● | Deployment of Capital. In order to eliminate the possibility of complete losses, we intend to place only a portion of our total capital at risk in any single year. This means that we expect lower returns than some of our competitors in years where there are lower than average catastrophe losses but that our capital will not be completely eroded in the event of multiple large losses. | |

| ● | Take Advantage of Market Opportunities. Although our business is initially focused on catastrophe coverage for Gulf Coast insurers we intend to continuously evaluate various market opportunities in which our business may be strategically or financially expanded or enhanced in the future. Such opportunities could take the form of investing into related party special purpose acquisition companies, further diversifying our business into other geographic or market areas, which could include quota share reinsurance contracts, joint ventures, renewal rights transactions, corporate acquisitions of other insurers or reinsurers, spinoffs, mergers or the formation of insurance or reinsurance platforms in new markets. | |

| ● | Develop and Pursue Additional Tokenization Business Opportunities. Through SurancePlus Holdings and our Web3-focused subsidiaries, we intend to leverage our experience and knowledge with the tokenization of RWAs (including the initial DeltaCat Re Token) to develop other Web3-focused business offerings and products relating to the tokenization of RWAs, including RWAs held or being acquired by third parties. | |

| We believe the environment in the reinsurance and insurance markets will continue to produce opportunities for us, either through organic expansion, through acquisitions, or a combination of both. |

The Reinsurance Industry

General

Reinsurance is an arrangement in which an insurance company, referred to as the reinsurer, agrees to assume from another insurance company, referred to as the ceding company or cedant, all or a portion of the insurance risks that the ceding company has underwritten under one or more insurance contracts. In return, the reinsurer receives a premium for the insured risks that it assumes from the ceding company, although reinsurance does not discharge the ceding company from its liabilities to policyholders. It is standard industry practice for primary insurers to reinsure portions of their insurance risks with other insurance companies under reinsurance agreements or contracts. This permits primary insurers to underwrite policies in amounts larger than the risks they are willing to retain. Reinsurance is generally designed to:

| ● | Reduce the ceding company’s net liability on individual risks, thereby assisting it in managing its risk profile and increasing its capacity to underwrite business as well as increasing the limit to which it can underwrite on a single risk; | |

| ● | assist the ceding company in meeting applicable regulatory and rating agency capital requirements; | |

| ● | assist the ceding company in reducing the short-term financial impact of sales and other acquisition costs; and | |

| ● | enhance the ceding company’s financial strength and statutory capital. |

When reinsurance companies purchase reinsurance to cover their own risks assumed from ceding companies, this is known as retrocessional reinsurance. Reinsurance or retrocessional reinsurance can benefit a ceding company or reinsuring company, referred to herein as a “retrocedant,” as applicable, in various ways, such as by reducing exposure to individual risks and by providing catastrophe protection from larger or multiple losses. Like ceding companies, retrocedants can use retrocessional reinsurance to manage their overall risk profile or to create additional underwriting capacity, allowing them to accept larger risks or to write more business than would otherwise be possible, absent an increase in their capital or surplus.

Reinsurance contracts do not discharge ceding companies from their obligations to policyholders. Ceding companies therefore generally require their reinsurers to have, and to maintain, either a strong financial strength rating or security, in the form of collateral, as assurance that their claims will be paid.

Insurers generally purchase multiple tranches of reinsurance protection above an initial retention elected by the insurer. The amount of reinsurance protection purchased by an insurer is typically determined by the insurer through both quantitative and qualitative methods. In the event of losses, the amount of loss that exceeds the amount of reinsurance protection purchased is retained by the insurer.

As a program is constructed from the ground up, each tranche added generally has a lower probability of loss than the prior tranche and therefore is generally subject to a lower reinsurance premium charged for the reinsurance protection purchased. Insurer catastrophe programs are typically supported by multiple reinsurers per program.

| 6 |

Reinsurance brokers play an important role in the reinsurance market. Brokers are intermediaries that assist the ceding company in structuring a particular reinsurance program and in negotiating and placing risks with third-party reinsurers. In this capacity, the broker is selected and retained by the ceding company on a contract-by-contract basis, rather than by the reinsurer. Though brokers are not parties to reinsurance contracts, reinsurers generally receive premium payments from brokers rather than ceding companies, and reinsurers that do not provide collateralized reinsurance are frequently required to pay amounts owed on claims under their policies to brokers. These brokers, in turn, pay these amounts to the ceding companies that have reinsured a portion of their liabilities with reinsurers.

Types of Reinsurance Contracts

Property reinsurance products are often written in the form of treaty reinsurance contracts, which are contractual arrangements that provide for the automatic reinsurance of a type or category of risk underwritten. Treaty reinsurance premiums, which are typically due in installments, are a function of the number and type of contracts written, as well as prevailing market prices. The timing of premiums written varies by line of business. The majority of property catastrophe business is written at the January and June annual renewal periods, depending on the type and location of the risks covered. Most hurricane and wind-storm coverage, particularly in the Gulf Coast region of the United States, is written at the June annual renewal periods.

Property catastrophe reinsurance contracts are typically “all risk” in nature, providing protection to the ceding company against losses from hurricanes and other natural and man-made catastrophes such as floods, earthquakes, tornadoes, storms and fires, referred to herein collectively as “perils.” The predominant exposures covered by these contracts are losses stemming from property damage and business interruption resulting from a covered peril. Coverage can also vary from “all natural” perils, which is the most expansive form, to more limited types such as windstorm-only coverage.

Property catastrophe reinsurance contracts are typically written on an “excess-of-loss” basis, which provides coverage to the ceding company when aggregate claims and claim expenses from a single occurrence for a covered peril exceed an amount that is specified in a particular contract. The coverage provided under excess-of-loss reinsurance contracts may be on a worldwide basis or may be limited in scope to specific regions or geographical areas. Under these contracts, protection is provided to an insurer for a portion of the total losses in excess of a specified loss amount, up to a maximum amount per loss specified in the contract.

Excess-of-loss contracts are typically written on a losses-occurring basis, which means that they cover losses that occur during the contract term, regardless of when the underlying policies came into force. Premiums from excess-of-loss contracts are earned rateably over the contract term, which is ordinarily 12 months. Most excess-of-loss contracts provide for a reinstatement of coverage following a covered loss event in return for an additional premium.

The Florida Property and Casualty Insurance Market

General Overview

Florida’s property and casualty insurance market has undergone significant changes in the past few decades. This market, which was formerly dominated by large, national, multi-line insurance companies, now includes Citizens Property Insurance Corporation (“Citizens”), a state-sponsored insurance company created by the Florida Legislature; Florida-based insurance companies that focus primarily on writing property insurance policies in the state of Florida; and Florida-based subsidiaries of national insurance companies that focus on writing property insurance policies in the state of Florida. While these four types of companies participate in the market at varying levels, Citizens and the Florida-based insurance companies are now the dominant market participants. Within the private market, which excludes Citizens, there is a strong dependence on small insurance companies, which have limited capitalization and a limited ability to diversify.

While the Florida property and casualty insurance market faces various challenges, the primary challenge is the potential for exposure to catastrophic windstorms. According to the Report, the state of Florida has:

| ● | more than $1.8 trillion in insured residential property exposure; | |

| ● | more than $4 billion in expected average annual losses due to windstorms (with respect to residential and commercial residential properties only); and | |

| ● | nearly $60 billion in 1-in-100 probable maximum losses due to windstorms (with respect to residential and commercial residential properties only). |

According to the National Oceanic and Atmosphere Administration (“NOAA”) Technical Memorandum NWS NHC-6, entitled “The Deadliest, Costliest, and Most Intense United States Tropical Cyclones from 1851 to 2010 (and Other Frequently Requested Hurricane Facts) (the “NOAA Memorandum”), “forty percent of all U.S. hurricanes and major hurricanes were in Florida,” and “sixty percent of category 4 or higher hurricane strikes have occurred in either Florida or Texas.” The NOAA Memorandum also indicates that, between 1851 and 2010, there were 114 hurricane strikes and 37 major hurricanes in Florida. (For these purposes, a “major hurricane” is a category 3, 4, or 5 hurricane.)

Our Reinsurance Contracts and Products

We write primarily property catastrophe reinsurance. We currently expect that substantially all of the reinsurance products we write in the foreseeable future will be in the form of treaty reinsurance contracts. When we write treaty reinsurance contracts, we do not evaluate separately each of the individual risks assumed under the contracts and are therefore largely dependent on the individual underwriting decisions made by the cedant. Accordingly, as part of our initial review and renewal process, we carefully review and analyze the cedant’s risk management and underwriting practices in evaluating whether to provide treaty reinsurance and in appropriately pricing the treaty.

Our portfolio of business continues to be characterized by relatively large transactions with a relatively few number of cedants. We anticipate that our business will continue to be characterized by a relatively small number of reinsurance contracts for the foreseeable future.

Our contracts are written on an excess-of-loss basis, generally with a per-event cap. We generally receive the premium for the risk assumed and indemnify the cedant against all or a specified portion of losses and expenses in excess of a specified dollar or percentage amount. Our contracts are generally both single-year or multi-year contracts and our policy years generally commence on June 1 of each year and end on May 31 of the following year.

| 7 |

The bulk of our portfolio of risks is assumed pursuant to traditional reinsurance contracts. However, from time to time we take underwriting risk by purchasing a catastrophe-linked bond, or via a transaction booked as an industry loss warranty (as described below) or an indemnity swap. An indemnity swap is an agreement which provides for the exchange between two parties of different portfolios of catastrophe exposure with similar expected loss characteristics (for example, U.S. earthquake exposure for Asian earthquake exposure).

We believe our most attractive near-term opportunity is in property catastrophe reinsurance coverage for insurance companies. In addition to seeking profitable pricing, we manage our risks with contractual limits on our exposure. Property catastrophe reinsurance contracts are typically “all risk” in nature, meaning that they protect against losses from earthquakes and hurricanes, as well as other natural and man-made catastrophes such as tornados, fires, winter storms, and floods (where the contract specifically provides for such coverage). Losses on these contracts typically stem from direct property damage and business interruption. We generally write property catastrophe reinsurance on an excess-of-loss basis. These contracts typically cover only specific regions or geographical areas.

We are not licensed or admitted as an insurer in any jurisdiction other than the Cayman Islands. In addition, we do not have a financial rating and do not expect to have one in the near future. Many jurisdictions such as the United States do not permit clients to take credit for reinsurance on their statutory financial statements if such reinsurance is obtained from unlicensed or non-admitted insurers without appropriate collateral. As a result, we anticipate that all of our clients will require us to fully collateralize the reinsurance contracts we bind with them. Each of our contracts are fully collateralized and separately structured, with our liability being limited to the value of the assets held in the trust. We are generally not required to top-up the value of the assets held as collateral in respect of a particular reinsurance agreement, unless such collateral is subject to market risk. For each reinsurance agreement, a reinsurance trust is established in favor of the cedant, and the trustee of the reinsurance trust is a large bank that is agreed upon by our company and the cedant.

The premium for the contract is ordinarily deposited into the trust, together with additional capital from our company, up to the coverage limit. Each reinsurance contract contains express limited recourse language to the effect that the liabilities of the relevant reinsurance contract are limited to the realizable value of the collateral held in respect of that contract. Upon the expiration of the reinsurance contract, the assets of the trust net of insured losses and other expenses are transferred to our company.

Underwriting

Most of our reinsurance contracts have other reinsurers participating as lead underwriters, and these lead underwriters generally set the premium for the risk. We follow the premium pricing of the lead underwriters in most cases subject to the guidance of the Underwriting Committee of our Board of Directors. Each quarter, our Board of Directors will set parameters for the maximum level of capital to be deployed for the quarter and the expected premium and risk profile that each of our contracts must meet.

Our reinsurance portfolio of business continues to be characterized by relatively large transactions with a relatively few number of cedants and anticipate that our reinsurance entities business will continue to be characterized by a relatively small number of reinsurance contracts for the foreseeable future.

The bulk of our portfolio of risks is assumed pursuant to traditional reinsurance contracts. However, from time to time we take underwriting risk by purchasing a catastrophe-linked bond, or via a transaction booked as an industry loss warranty (as described below) or an indemnity swap. An indemnity swap is an agreement which provides for the exchange between two parties of different portfolios of catastrophe exposure with similar expected loss characteristics (for example, U.S. earthquake exposure for Asian earthquake exposure).

Marketing and Distribution

We expect that, in the future, the majority of our business will be sourced through reinsurance brokers. Brokerage distribution channels provide us with access to an efficient, variable distribution system without the significant time and expense that would be incurred in creating an in-house marketing and distribution network. Reinsurance brokers receive a brokerage commission that is usually a percentage of gross premiums written.

We intend to build relationships with global reinsurance brokers and captive insurance companies located in the Cayman Islands. Our management team has significant relationships with most of the primary and specialty broker intermediaries in the reinsurance marketplace in our target market. We believe that maintaining close relationships with brokers will give us access to a broad range of reinsurance clients and opportunities.

Brokers do not have the authority to bind us to any reinsurance contract. We review and approve all contract submissions in our corporate offices located in the Cayman Islands. From time to time, we may also enter into relationships with managing general agents who could bind us to reinsurance contracts based on narrowly defined underwriting guidelines.

| 8 |

Investment Strategy

Our Company takes an opportunistic approach with respect to investment income and intend to increase shareholder value through supplemental investment income when favorable opportunities are available. The Company, from time to time, and dependent upon favorable investment conditions and our investment guidelines, may invest in real estate and other ventures that have the potential to increase shareholder value. Through its reinsurance subsidiaries, the Company has made and intend to make future investments that can contribute to the growth of capital and surplus in its licensed reinsurance subsidiaries over time.

Some of our company’s capital is held in trust accounts that collateralize the reinsurance policies that we write. The investment parameters for capital held in such trust accounts are generally established by the cedant for the relevant policy. Currently, all amounts held in trust accounts are in cash and cash equivalents.

Our Board of Directors periodically reviews our investment policy and returns.

Claims Management

Claims are managed internally by the company’s management team. Management reviews and responds to initial loss reports, administers claims databases, determines whether further investigation is required and where appropriate, retains outside claims counsel, establishes case reserves and approves claims for payment. In addition, we may conduct audits of any significant client throughout the year, and in the process, evaluate our clients’ claims handling abilities, reserving philosophies, loss notification processes and the overall quality of our clients’ performance.

Upon receipt, claims notices are recorded within our underwriting, financial and claims systems. When we are notified of insured losses or discover potential losses as part of our claims’ audits, we record a case reserve as appropriate for the estimated amount of the exposure at that time. The estimate reflects the judgment of management based on general reserving practices, the experience and knowledge of the manager regarding the nature of the specific claim and, where appropriate, advice of outside counsel. Reserves are also established to provide for the estimated expense of settling claims, including legal and other fees and the general expenses of administering the claims adjustment process.

Loss Reserves

Loss reserves represent estimates, including actuarial and statistical projections at a given point in time, of the ultimate settlement and administration costs of claims incurred (including claims incurred but not reported (“IBNR”)). Estimates are not precise in that, among other things, they are based on predictions of future developments and estimates of future trends in claims severity and frequency and other variable factors such as inflation. It is likely that the ultimate liability will be greater or less than such estimates and that, at times, this variance will be material.

For our property and other catastrophe policies, we initially establish our loss reserves based on loss payments and case reserves reported by ceding companies. As we are not the only reinsurer on most contracts, the lead reinsurer will set the loss amount estimates for the contract and the cedant will have the ability to pay for case losses consistent with that amount on our pro-rata share of the contract.

We then add to these case reserves our estimates for IBNR. To establish our IBNR estimates, in addition to the loss information and estimates communicated by cedants, we also use the services of an independent actuary. We may also use our computer-based vendor and proprietary modeling systems to measure and estimate loss exposure under the actual event scenario, if available. Although the loss modeling systems assist with the analysis of the underlying loss, and provide us with information and the ability to perform an enhanced analysis, the estimation of claims resulting from catastrophic events is inherently difficult because of the variability and uncertainty of property catastrophe claims and the unique characteristics of each loss.

If IBNR estimates are made, we assess the validity of the assumptions we use in the reserving process on a quarterly basis during an internal review process. During this process actuaries verify that the assumptions we have made continue to form what they consider to be a sound basis for projection of future liabilities.

| 9 |

Although we believe that we are prudent in our assumptions and methodologies, we cannot be certain that our ultimate payments will not vary, perhaps materially, from the estimates we have made. If we determine that adjustments to an earlier estimate are appropriate, such adjustments are recorded in the quarter in which they are identified. The establishment of new reserves, or the adjustment of reserves for reported claims, could result in significant upward or downward changes to our financial condition or results of operations in any particular period. We regularly review and update these estimates, using the most current information available to us.

Our estimates are reviewed quarterly by an independent actuary in order to provide additional insight into the reasonableness of our loss reserves.

Competition

The reinsurance industry is highly competitive. We expect to compete with major reinsurers, most of which are well established with significant operating histories, strong financial strength ratings and long-standing client relationships.

Our competitors include Renaissance Re, Berkshire Hathaway, PartnerRe Ltd, Aeolus and Nephila which are dominant companies in the reinsurance industry. Although we seek to provide coverage where capacity and alternatives are limited, we directly compete with these larger companies due to the breadth of their coverage across the property and casualty market in substantially all lines of business. We also compete with smaller companies and other niche reinsurers from time to time.

While we have a limited operating history, we believe that our unique approach to multi-year underwriting will allow us to be successful in underwriting transactions against more established competitors.

Our Tokenization Business

We have decided to develop and pursue business opportunities in the tokenization of RWAs based on the expectation that a successful expansion into this specialization will further increase the underwriting capacity and potential profitability of our reinsurance subsidiaries, Oxbridge Reinsurance Limited and Oxbridge Re NS. We believe this represents a unique opportunity to drive value to our shareholders. The Boston Consulting Group published research projecting the RWA asset tokenization market to reach $16.1 trillion by 2030. A separate publication by Bloomberg reported that, in 2023, reinsurance was one of the top performing hedge fund strategies. It is at the intersection of these two, i.e., RWA tokenization and reinsurance, that we believe there exist substantial growth opportunities for our business.

Accordingly, SurancePlus was incorporated to further innovate upon existing capital raising mechanisms of Oxbridge Re NS for collateralizing reinsurance contracts while simultaneously transforming the corresponding investment product into one that is more accessible to United States accredited investors under Rule 506(c) of Regulation D and to international investors under Regulation S. SurancePlus has since applied insights and technology from the Web3 digital ecosystem to create a multi-year series of real-world asset-backed digital securities, called the Cat Re (short for “catastrophe reinsurance”) token series. Ownership of the tokens confer an indirect fractional interest in reinsurance contracts entered into by Oxbridge Re NS or Oxbridge Reinsurance Limited. The DeltaCat Re token was the first of the token series, and it was issued in 2023 on the Avalanche blockchain network. The subsequent year’s offering of EpsilonCat Re tokens was announced in a Form 8-K filed with the SEC on March 18, 2024. SurancePlus intends to continue to issue the Cat Re token series over several years.

We project that SurancePlus Inc. may develop into a significant revenue generating stream for the Oxbridge Re group that may progressively reduces Oxbridge Re’s annual capital deployed into collateralizing reinsurance contracts.. As opportunities arise, Oxbridge Re intends to pursue, through its Web3-focused subsidiaries, additional expansion of its RWA tokenization business to further increase underwriting profit.

Employees

As of March 26, 2024, we had four employees, all of which were full-time. We believe that our relations with our employees are good. None of our employees are subject to collective bargaining agreements, and we are not aware of any current efforts to implement such agreements. We believe that we will continue to have relatively few employees and intend to outsource some functions to specialist firms in the Cayman Islands if and when we determine that such functions are necessary. We intend to use the expertise of our Board of Directors and where necessary, external consultants to provide any other service we may require from time to time.

Legal Proceedings

We are not currently involved in any litigation or arbitration. We anticipate that, similar to the rest of the insurance and reinsurance industry, we will be subject to litigation and arbitration in the ordinary course of business.

Regulation and Capital Requirements

Our wholly-owned reinsurance subsidiaries, Oxbridge Reinsurance Limited and Oxbridge Re NS, each holds a Class C Insurer’s License issued in accordance with the terms of the Insurance Law (as revised) of the Cayman Islands (the “Law”), and is subject to regulation by the Cayman Islands Monetary Authority (“CIMA”), in terms of the Law. As the holder of a Class C Insurer’s License, Oxbridge Reinsurance Limited and Oxbridge Re NS are permitted to undertake insurance business approved by CIMA.

Oxbridge Reinsurance Limited and Oxbridge Re NS are subject to minimum capital and surplus requirements, and our failure to meet these requirements could subject us to regulatory action. Pursuant to The Insurance (Capital and Solvency) (Classes B, C and D Insurers) Regulations, 2012 (the “Capital and Solvency Regulations”) published under the Law, Oxbridge Reinsurance Limited and Oxbridge Re NS are required to maintain the statutory minimum capital requirement (as defined under the Capital and Solvency Regulations) of $500 and prescribed capital requirement (as defined under the Capital and Solvency Regulations) of $500, and a minimum margin of solvency equal to or in excess of the total prescribed capital requirement. Any failure to meet the applicable requirements or minimum statutory capital requirements could subject us to further examination or corrective action by CIMA, including restrictions on dividend payments, limitations on our writing of additional business or engaging in finance activities, supervision or liquidation.

| 10 |

CIMA may at any time direct Oxbridge Reinsurance Limited and Oxbridge Re NS, in relation to a policy, a line of business or the entire business, to cease or refrain from committing an act or pursing a course of conduct and to perform such acts as in the opinion of CIMA are necessary to remedy or ameliorate the situation. See the discussion in “Risk Factors” under the heading “Any suspension or revocation of our reinsurance license would materially impact our ability to do business and implement our business strategy” for more information.

In addition, as a Cayman Islands exempted company, we may not carry on business or trade locally in the Cayman Islands except in furtherance of our business outside the Cayman Islands, and we are prohibited from soliciting the public of the Cayman Islands to subscribe for any of our securities or debt. We are further required to file a return with the Registrar of Companies in January of each year and to pay an annual registration fee at that time.

The Cayman Islands has no exchange controls restricting dealings in currencies or securities.

Available Information

Our website is located at www.oxbridgere.com. Copies of our Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K, and amendments to these reports filed or furnished pursuant to Section 13(a) or 15(d) of the Exchange Act are available, free of change, on our website as soon as reasonably practicable after we file such material electronically with or furnish it to the Securities and Exchange Commission (the “SEC”). The SEC also maintains a website that contains our SEC filings. The address of the SEC’s website is www.sec.gov.

Summary of Risk Factors

Our business is subject to numerous risks and uncertainties, including those highlighted in the section titled “Risk Factors,” that represent challenges that we face in connection with the successful implementation of our strategy. The occurrence of one or more of the events or circumstances described in the section titled “Risk Factors,” alone or in combination with other events or circumstances may have an adverse effect on our business, cash flows, financial condition and results of operations. In that case, the market price of our securities could decline, and you may lose some or all of your investment. Such risks include, but are not limited to:

| ● | We will need additional capital in the future in order to grow and operate our business. Such capital may not be available to us or may not be available to us on favorable terms. Furthermore, our raising additional capital could dilute your ownership interest in our company. |

| ● | Our results of operations will fluctuate from period to period and may not be indicative of our long-term prospects. | |

| ● | Our tokenization business operations are at an early stage of development and have a limited operating history, and our strategy of developing a Web3-focused tokenization business may not be successful. | |

| ● | Developing a Web3.0-focused business around the tokenization of RWAs involves significant risks. |

| ● | Failure to become rated by A.M. Best, or receipt of a negative rating, could significantly and negatively affect our ability to grow. |

| ● | Established competitors with greater resources may make it difficult for us to effectively market our products or offer our products at a profit. |

| ● | If actual renewals of our existing contracts do not meet expectations, our premiums assumed in future years and our future results of operations could be materially adversely affected. |

| ● | Reputation is an important factor in the reinsurance industry, and our lack of an established reputation may make it difficult for us to attract or retain business. |

| ● | If our losses and loss adjustment expenses greatly exceed our loss reserves, our financial condition may be significantly and negatively affected. |

| ● | The property and casualty reinsurance market may be affected by cyclical trends and over-supply. |

| ● | Our property and property catastrophe reinsurance operations will make us vulnerable to losses from catastrophes and may cause our results of operations to vary significantly from period to period. |

| ● | We could face unanticipated losses from war, terrorism, and political unrest, and these or other unanticipated losses could have a material adverse effect on our financial condition and results of operations. |

| ● | We depend on our clients’ evaluations of the risks associated with their insurance underwriting, which may subject us to reinsurance losses. |

| ● | Changing climate conditions may adversely affect our financial condition, profitability or cash flows. |

| ● | Operational risks, including human or systems failures, are inherent in our business. |

| ● | The effect of emerging claim and coverage issues on our business is uncertain |

| ● | We are required to maintain sufficient collateral accounts, which could significantly and negatively affect our ability to implement our business strategy. |

| ● | The inability to obtain business provided from brokers could adversely affect our business strategy and results of operations. |

| 11 |

| ● | The involvement of reinsurance brokers may subject us to their credit risk. |

| ● | Our use of fair value accounting of our significant investment in Jet.AI Inc. could result in income statement volatility, which in turn, could cause significant market price and trading volume fluctuations for our securities |

| ● | U.S. and global economic downturns could harm our business, our liquidity and financial condition and the price of our securities. |

| ● | Our ability to implement our business strategy could be delayed or adversely affected by Cayman Islands employment restrictions. |

| ● | Security breaches and other disruptions could compromise our information and expose us to liability, which would cause our business and reputation to suffer. |

| ● | If we lose or are unable to retain our senior management and other key personnel and are unable to attract qualified personnel, our ability to implement our business strategy could be delayed or hindered, which, in turn, could significantly and negatively affect our business. |

| ● | There are differences under Cayman Islands corporate law and Delaware corporate law with respect to interested party transactions which may benefit certain of our shareholders at the expense of other shareholders. |

| ● | Any suspension or revocation of our reinsurance license would materially impact our ability to do business and implement our business strategy. |

| ● | Our reinsurance subsidiaries are subject to minimum capital and surplus requirements, and our failure to meet these requirements could subject us to regulatory action. |

| ● | As a holding company, we will depend on the ability of our subsidiaries to pay dividends. |

| ● | We may be subject to the risk of possibly becoming an investment company under U.S. federal securities law. |

| ● | Insurance regulations to which we are, or may become, subject, and potential changes thereto, could have a significant and negative effect on our business. |

| ● | We will likely be exposed to credit risk due to the possibility that counterparties may default on their obligations to us. |

| ● | Provisions of our Third Amended and Restated Memorandum and Articles of Association (“Articles”) could adversely affect the value of our securities. |

| ● | Provisions of the Companies Law of the Cayman Islands could prevent a merger or takeover of our company. |

| ● | Holders of our securities may have difficulty obtaining or enforcing a judgment against us, and they may face difficulties in protecting their interests because we are incorporated under Cayman Islands law. |

| ● | Provisions of our Articles may reallocate the voting power of our ordinary shares. |

| ● | We do not currently have an effective registration statement registering the issuance of the shares underlying our publicly traded warrants, and therefore you may not be able to exercise the warrants in a cash exercise. |

| ● | We may become subject to taxation in the Cayman Islands which would negatively affect our results. |

| ● | We may be subject to United States federal income taxation. |

| ● | We may be treated as a PFIC, in which case a U.S. holder of our ordinary shares should be subject to disadvantageous rules under U.S. federal income tax laws. We may be treated as a CFC and may be subject to the rules for related person insurance income, and in either case this may subject a U.S. holder of our ordinary shares to disadvantageous rules under U.S. federal income tax laws. |

| ● | United States tax-exempt organizations who own ordinary shares may recognize unrelated business taxable income. |

| ● | Changes in United States tax laws may be retroactive and could subject us, and/or United States persons who own ordinary shares to United States income taxation on our undistributed earnings. |

| ● | We do not intend to resume paying cash dividends in the foreseeable future. |

| ● | Outages, computer viruses and similar events could disrupt our operations. |

| ● | Increased Information Technology (“IT”) security threats and more sophisticated computer crime could pose a risk to our systems, networks, and services. |

| ● | Increased scrutiny by and changing expectations from investors, employees, and other stakeholders regarding our environmental, social, and governance (“ESG”) practices and reporting could cause us to incur additional costs and adversely impact our reputation, tenant and employee acquisition and retention, and access to capital. |

| 12 |

ITEM 1A RISK FACTORS

Risks Relating to Our Business

We will need additional capital in the future in order to grow and operate our business. Such capital may not be available to us or may not be available to us on favorable terms. Furthermore, our raising additional capital could dilute your ownership interest in our company.

We expect that we will need to raise additional capital in the future through public or private equity or debt offerings or otherwise in order to:

| ● | further capitalize our reinsurance subsidiaries and implement our growth strategy; | |

| ● | fund liquidity needs caused by underwriting or investment losses; | |

| ● | replace capital lost in the event of significant reinsurance losses or adverse reserve developments; | |

| ● | meet applicable statutory jurisdiction requirements; | |

| ● | fund our business activities relating to our new tokenization business operations; and/or | |

| ● | respond to competitive pressures. |

Additional capital may not be available on terms favorable to us, or at all. Further, any additional capital raised through the sale of equity could dilute your ownership interest in our company and may cause the market price of our ordinary shares and warrants to decline. Additional capital raised through the issuance of debt may result in creditors having rights, preferences and privileges senior or otherwise superior to those of our ordinary shares and warrants.

Our results of operations will fluctuate from period to period and may not be indicative of our long-term prospects.

We anticipate that the performance of our reinsurance operations and our investment portfolio will fluctuate from period to period. Fluctuations will result from a variety of factors, including:

| ● | reinsurance contract pricing; | |

| ● | our assessment of the quality of available reinsurance opportunities; | |

| ● | the volume and mix of reinsurance products we underwrite; | |

| ● | loss experienced on our reinsurance liabilities; | |

| ● | our ability to assess and integrate our risk management strategy properly; and | |

| ● | the performance of our investment portfolio. |

In particular, we plan to underwrite products and make investments to achieve favorable return on equity over the long term. In addition, our opportunistic nature and focus on long-term growth in book value will result in fluctuations in total premiums written from period to period as we concentrate on underwriting contracts that we believe will generate better long-term, rather than short-term, results. Accordingly, our short-term results of operations may not be indicative of our long-term prospects.

Our tokenization business operations are at an early stage of development and have a limited operating history, and our strategy of developing a Web3-focused RWA tokenization business may not be successful.

Our Web3-focused RWA tokenization business is still in the development stage, and our operating history in such business has been limited to the development and issuance of a token for participation in reinsurance contracts underwritten by our Oxbridge Re NS subsidiary. We have not yet announced any revenue-producing activities for tokenization of RWAs that are held by or being acquired by third parties, and we may not be able to successfully complete the development of any products or services relating to tokenization of third-party RWAs. Accordingly, we have only a very limited operating history and limited experience in this business and have not earned any revenues to date in this business (other than limited management fees from the issuance of the DeltaCat Re Tokens). If we are not able to develop this business as planned, we may not be able to generate material revenues from our developing tokenization business.

Developing a Web3.0-focused business around the tokenization of RWAs involves significant risks.

Our planned tokenization business activities are based on a new area of technology and carries significant risks, including the following:

| ● | an active trading market for tokenized RWAs may not develop or be sustained; | |

| ● | there is no guarantee that tokenized RWAs will hold their value or increase in value; | |

| ● | tokenized RWAs of SurancePlus may not be listed on any securities exchange and may not be available to trade on any alternative trading system (“ATS”), which would result in limited liquidity for holders; | |

| ● | if the tokenized RWAs become available for trading on an ATS, the number of securities traded on such ATS may be very small, making the market price more easily manipulated; | |

| ● | technology on which an ATS relies for its operations may not function properly; | |

| ● | blockchain networks are relatively new technologies; | |

| ● | asset tokenization via blockchain technologies is a relatively new digital innovation; | |

| ● | blockchain network transaction fees may significantly increase over the duration of the investment; | |

| ● | smart contracts may have implementation errors that vitiate them; | |

| ● | blockchain transactions may be taken advantage of for financial crimes; and | |

| ● | the Avalanche blockchain the tokenized RWAs rely upon and the tokenized RWAs themselves may be the target of malicious cyberattacks. |

| 13 |

Failure to become rated by A.M. Best, or receipt of a negative rating, could significantly and negatively affect our ability to grow.

Companies, insurers and reinsurance brokers use ratings from independent ratings agencies as an important means of assessing the financial strength and quality of reinsurers. This rating reflects the rating agency’s opinion of our financial strength, operating performance and ability to meet obligations. It is not an evaluation directed toward the protection of investors or a recommendation to buy, sell or hold our securities. A.M. Best assigns ratings based on its analysis of balance sheet strength, operating performance and business profile.

Currently, A.M Best has not assigned us a financial strength rating, and we do not intend to seek a rating in the foreseeable future. Without a rating, or if we received a negative rating, our growth potential and business strategy will be limited because of the need to collateralize the insurance policies that we write.

Established competitors with greater resources may make it difficult for us to effectively market our products or offer our products at a profit.

The reinsurance industry is highly competitive. We compete with major reinsurers, all of which have substantially greater financial, marketing and management resources than we do. Competition in the types of business that we seek to underwrite is based on many factors, including:

| ● | premium charges; | |

| ● | the general reputation and perceived financial strength of the reinsurer; | |

| ● | relationships with reinsurance brokers; | |

| ● | terms and conditions of products offered; | |

| ● | ratings assigned by independent rating agencies; | |

| ● | speed of claims payment and reputation; and | |

| ● | the experience and reputation of the members of our underwriting team in the particular lines of reinsurance we seek to underwrite. |

Additionally, although the members of our underwriting team have general experience across many property and casualty lines, they may not have the requisite experience or expertise to compete for all transactions that fall within our strategy of offering customized frequency and severity contracts at times and in markets where capacity and alternatives may be limited.

Our competitors Renaissance Re, Berkshire Hathaway, PartnerRe Ltd, Aeolus Re, and Nephila which are dominant companies in the reinsurance industry, as well as smaller companies and other niche reinsurers. Although we seek to provide coverage where capacity and alternatives are limited, we will directly compete with these larger companies due to the breadth of their coverage across the property and casualty market in substantially all lines of business.

We cannot assure you that we will be able to compete successfully in the reinsurance market. Our failure to compete effectively could significantly and negatively affect our financial condition and results of operations and may increase the likelihood that we may be deemed to be a passive foreign investment company or an investment company.

If actual renewals of our existing contracts do not meet expectations, our premiums assumed in future years and our future results of operations could be materially adversely affected.

Many of our contracts are generally written for a one-year term. In our financial forecasting process, we make assumptions about the renewal of our prior year’s contracts. The insurance and reinsurance industries have historically been cyclical businesses with periods of intense competition, often based on price. If actual renewals do not meet expectations or if we choose not to write on a renewal basis because of pricing conditions, our premiums assumed in future years and our future operations would be materially adversely affected.

Reputation is an important factor in the reinsurance industry, and our lack of an established reputation may make it difficult for us to attract or retain business.

Reputation is a very important factor in the reinsurance industry, and competition for business is, in part, based on reputation. Although our reinsurance policies will be fully collateralized, we are a relatively newly formed reinsurance company and do not yet have a well-established reputation in the reinsurance industry. Our lack of an established reputation may make it difficult for us to attract or retain business. In addition, we do not have or currently intend to obtain financial strength ratings, which may discourage certain counterparties from entering into reinsurance contracts with us.

| 14 |

If our losses and loss adjustment expenses greatly exceed our loss reserves, our financial condition may be significantly and negatively affected.

Our results of operations and financial condition will depend upon our ability to accurately assess the potential losses and loss adjustment expenses associated with the risks we reinsure. Reserves are estimates at a given time of claims an insurer ultimately expects to pay, based upon facts and circumstances then known, predictions of future events, estimates of future trends in claim severity and other variable factors. The inherent uncertainties of estimating loss reserves are generally greater for reinsurance companies as compared to primary insurers, primarily due to:

| ● | the lapse of time from the occurrence of an event to the reporting of the claim and the ultimate resolution or settlement of the claim; | |

| ● | the diversity of development patterns among different types of reinsurance treaties; and | |

| ● | the necessary reliance on the client for information regarding claims. |

Our estimation of reserves may be less reliable than the reserve estimations of a reinsurer with a greater volume of business and an established loss history. Our actual losses and loss adjustment expenses paid may deviate substantially from the estimates of our loss reserves and could negatively affect our results of operations. If our loss reserves are later found to be inadequate, we would increase our loss reserves with a corresponding reduction in our net income and capital in the period in which we identify the deficiency, and such a reduction would also negatively affect our results of operations. If our losses and loss adjustment expenses greatly exceed our loss reserves, our financial condition may be significantly and negatively affected.

The property and casualty reinsurance market may be affected by cyclical trends and over-supply.

We write reinsurance in the property and casualty markets, which tend to be cyclical in nature. Ceding company underwriting results, prevailing general economic and market conditions, liability retention decisions of companies and ceding companies and reinsurance premium rates each influence the demand for property and casualty reinsurance. Prevailing prices and available surplus to support assumed business then influence reinsurance supply. Supply may fluctuate in response to changes in return on capital realized in the reinsurance industry, the frequency and severity of losses and prevailing general economic and market conditions.

Continued increases in the supply of reinsurance may have consequences for the reinsurance industry generally and for us, including lower premium rates, increased expenses for customer acquisition and retention, less favorable policy terms and conditions and/or lower premium volume. Furthermore, unpredictable developments, including courts granting increasingly larger awards for certain damages, increases in the frequency of natural disasters (such as hurricanes, windstorms, tornados, earthquakes, wildfires and floods), fluctuations in interest rates, changes in the investment environment that affect market prices of investments and inflationary pressures, affect the industry’s profitability. The effects of cyclicality could significantly and negatively affect our financial condition and results of operations.

Due to the influx of new risk capital from alternative capital market participants such as hedge funds and pension funds, we believe that the reinsurance industry is currently over-capitalized and will continue in this trend for the foreseeable future. The over-capitalization of the market is not uniform as there are a number of insurers and reinsurers that have suffered and continue to suffer from capacity issues. We continue to assess the opportunities that may be available to us with insurance and reinsurance companies with this profile. If the reinsurance market continues to soften, our strategy is to reduce premium writings rather than accept mispriced risk and conserve our capital for a more opportune environment. Significant rate increases could occur if financial and credit markets experience adverse shocks that result in the loss of capital of insurers and reinsurers, or if there are major catastrophic events, especially in North America.

Our property and property catastrophe reinsurance operations will make us vulnerable to losses from catastrophes and may cause our results of operations to vary significantly from period to period.

Our reinsurance operations expose us to claims arising out of unpredictable catastrophic events, such as hurricanes, hailstorms, tornados, windstorms, earthquakes, floods, fires, explosions, and other natural or man-made disasters. Because of our emphasis on Florida, we are particularly vulnerable to hurricanes and with windstorm losses occurring in Florida. The incidence and severity of catastrophes are inherently unpredictable but the loss experience of property catastrophe reinsurers has been generally characterized as low frequency and high severity. Claims from catastrophic events could reduce our earnings and cause substantial volatility in our results of operations for any fiscal quarter or year and adversely affect our financial condition. Corresponding reductions in our surplus levels could impact our ability to write new reinsurance policies.

| 15 |

Catastrophic losses are a function of the insured exposure in the affected area and the severity of the event. Because accounting standards do not permit reinsurers to reserve for catastrophic events until they occur, claims from catastrophic events could cause substantial volatility in our financial results for any fiscal quarter or year and could significantly and negatively affect our financial condition and results of operations.

We could face unanticipated losses from war, terrorism, and political unrest, and these or other unanticipated losses could have a material adverse effect on our financial condition and results of operations.

Like other reinsurers, we face potential exposure to large, unexpected losses resulting from man-made catastrophic events, such as acts of war, acts of terrorism and political instability. These risks are inherently unpredictable and recent events may indicate that the frequency and severity of these types of losses may increase. It is difficult to predict the timing of these events or to estimate the amount of loss that any given occurrence will generate. To the extent that losses from these risks occur, our financial condition and results of operations could be significantly and negatively affected.

We depend on our clients’ evaluations of the risks associated with their insurance underwriting, which may subject us to reinsurance losses.

In the proportional reinsurance business, in which we assume an agreed percentage of each underlying insurance contract being reinsured, or quota share contracts, we do not separately evaluate each of the original individual risks assumed under these reinsurance contracts. Therefore, we are largely dependent on the original underwriting decisions made by ceding companies. We are subject to the risk that the clients may not have adequately evaluated the insured risks and that the premiums ceded may not adequately compensate us for the risks we assume. We also do not separately evaluate each of the individual claims made on the underlying insurance contracts under quota share arrangements. Therefore, we are dependent on the original claims decisions made by our clients.

Changing climate conditions may adversely affect our financial condition, profitability or cash flows.

Climate change, to the extent it produces extreme changes in temperatures and changes in weather patterns, could impact the frequency or severity of weather events and wildfires. Further, it could impact the affordability and availability of homeowners insurance, which could have an impact on pricing. Changes in weather patterns could also affect the frequency and severity of other natural catastrophe events to which we may be exposed. The occurrence of these events would significantly and negatively affect our financial condition and results of operations.

Operational risks, including human or systems failures, are inherent in our business.

Operational risks and losses can result from, among other things, fraud, errors, failure to document transactions properly or to obtain proper internal authorization, failure to comply with regulatory requirements, information technology failures or external events.

We believe that our modeling, underwriting and information technology and application systems are critical to our business and our growth prospects. Moreover, we rely on our information technology and application systems to further our underwriting process and to enhance our ability to compete successfully. A major defect or failure in our internal controls or information technology and application systems could result in management distraction, harm to our reputation or increased expenses.

The effect of emerging claim and coverage issues on our business is uncertain.

As industry practices and legal, judicial and regulatory conditions change, unexpected issues related to claims and coverage may emerge. It is possible that certain provisions of our future reinsurance contracts, such as limitations or exclusions from coverage or choice of forum, may be difficult to enforce in the manner we intend, due to, among other things, disputes relating to coverage and choice of legal forum. These issues may adversely affect our business by either extending coverage beyond the period that we intended or by increasing the number or size of claims. In some instances, these changes may not manifest themselves until many years after we have issued insurance or reinsurance contracts that are affected by these changes. As a result, we may not be able to ascertain the full extent of our liabilities under our insurance or reinsurance contracts for many years following the issuance of our contracts. The effects of unforeseen development or substantial government intervention could adversely impact our ability to adhere to our goals.

| 16 |

We are required to maintain sufficient collateral accounts, which could significantly and negatively affect our ability to implement our business strategy.

We are not licensed or admitted as a reinsurer in any jurisdiction other than the Cayman Islands. Certain jurisdictions, including the United States, do not permit insurance companies to take credit for reinsurance obtained from unlicensed or non-admitted insurers on their statutory financial statements unless appropriate security measures are implemented. Consequently, we must continue to maintain sufficient funds in escrow accounts to serve as collateral for our reinsurance contracts. Because we intend to continue to utilize our funds (rather than utilizing the credit markets) to serve as collateral for our reinsurance obligations, we may not be able to fully utilize our capital to expand our reinsurance coverage as rapidly as other reinsurers.

The inability to obtain business provided from brokers could adversely affect our business strategy and results of operations.

We anticipate that a substantial portion of our business will be placed primarily through brokered transactions, which involve a limited number of reinsurance brokers. If we are unable to identify and grow the brokered business provided through one or more of these reinsurance brokers, many of whom may not be familiar with our Cayman Islands jurisdiction, this failure could significantly and negatively affect our business and results of operations.

The involvement of reinsurance brokers may subject us to their credit risk.

As a standard practice of the reinsurance industry, reinsurers frequently pay amounts owed on claims under their policies to reinsurance brokers, and these brokers, in turn, remit these amounts to the ceding companies that have reinsured a portion of their liabilities with the reinsurer. In some jurisdictions, if a broker fails to make such a payment, the reinsurer might remain liable to the client for the deficiency notwithstanding the broker’s obligation to make such payment. Conversely, in certain jurisdictions, when the client pays premiums for policies to reinsurance brokers for payment to the reinsurer, these premiums are considered to have been paid and the client will no longer be liable to the reinsurer for these premiums, whether or not the reinsurer has actually received them. Consequently, we assume a degree of credit risk associated with the brokers that we do business with.

Our use of fair value accounting of our significant investment in Jet.AI Inc. could result in income statement volatility, which in turn, could cause significant market price and trading volume fluctuations for our securities.

Our significant beneficial interests in Jet.AI Inc.’s common stock and public warrants are recorded at fair value with changes in fair value being recorded in the consolidated statements of operations during the period of change. Additionally, the fair value of the investment must be remeasured quarterly. Because of this, and due to significance of our investment in Jet.AI relative to our total assets, our earnings may experience greater volatility in the future as a decline in the fair value of our investment in Jet.AI Inc. could significantly reduce both our earnings and shareholders’ equity, which in turn, could cause significant market price and trading volume fluctuations for our securities.