UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM

(Mark One)

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended

OR

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission File No.

(Exact name of registrant as specified in its charter)

| ||

(State or Other Jurisdiction of | (I.R.S. Employer | |

Incorporation or Organization) | Identification No.) | |

(Address of Principal Executive Offices) | (Zip Code) |

Registrant’s telephone number, including area code:

SECURITIES REGISTERED PURSUANT TO SECTION 12(b) OF THE ACT:

Title of each class |

| Trading Symbol |

| Name of each exchange on which registered |

SECURITIES REGISTERED PURSUANT TO SECTION 12(g) OF THE ACT: NONE

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Large Accelerated Filer ☐ | Accelerated Filer ☐ |

Smaller reporting company | |

Emerging growth company |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report.

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements.

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes

The aggregate market value of the voting and non-voting common equity held by non-affiliates of the registrant was approximately $

On February 23, 2024, there were

DOCUMENTS INCORPORATED BY REFERENCE

Specified portions of the registrant’s definitive Proxy Statement to be issued in conjunction with the registrant’s 2024 Annual Meeting of Shareholders, which is expected to be filed not later than 120 days after the registrant’s fiscal year ended December 31, 2023, are incorporated by reference into Part III of this Annual Report. Except as expressly incorporated by reference, the registrant’s Proxy Statement shall not be deemed to be a part of this Annual Report on Form 10-K.

THERAVANCE BIOPHARMA, INC.

2023 Form 10-K Annual Report

Table of Contents

2

Special Note regarding Forward-Looking Statements

This Annual Report on Form 10-K contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended (the “Securities Act”), and Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”). Such forward-looking statements involve risks, uncertainties and assumptions. All statements in this Annual Report on Form 10-K, other than statements of historical facts, including statements regarding our strategy, future operations, future financial position, future revenues, projected costs, prospects, plans, intentions, designs, expectations, and objectives are forward-looking statements. The words “aim,” “anticipate,” “assume,” “believe,” “contemplate,” “continue,” “could,” “designed,” “developed,” “drive,” “estimate,” “expect,” “forecast,” “goal,” “indicate,” “intend,” “may,” “mission,” “opportunities,” “plan,” “possible,” “potential,” “predict,” “project,” “pursue,” “represent,” “seek,” “suggest,” “should,” “target,” “will,” “would,” and similar expressions (including the negatives thereof) are intended to identify forward looking statements, although not all forward looking statements contain these identifying words. These statements reflect our current views with respect to future events or our future financial performance, are based on assumptions, and involve known and unknown risks, uncertainties and other factors which may cause our actual results, performance or achievements to be materially different from any future results, performance or achievements expressed or implied by the forward-looking statements. We may not actually achieve the plans, intentions, expectations or objectives disclosed in our forward-looking statements and the assumptions underlying our forward-looking statements may prove incorrect. Therefore, you should not place undue reliance on our forward-looking statements. Actual results or events could differ materially from the plans, intentions, expectations, and objectives disclosed in the forward-looking statements that we make. Factors that we believe could cause actual results or events to differ materially from our forward-looking statements include, but are not limited to, those discussed in “Risk Factors,” in Item 1A, “Management’s Discussion and Analysis of Financial Condition and Results of Operations” in Item 7 and elsewhere in this Annual Report on Form 10-K. Our forward-looking statements in this Annual Report on Form 10-K are based on current expectations, and we do not assume any obligation to update any forward-looking statements for any reason, even if new information becomes available in the future. When used in this report, all references to “Theravance Biopharma”, the “Company”, or “we” and other similar pronouns refer to Theravance Biopharma, Inc. collectively with its subsidiaries.

3

PART I

ITEM 1. BUSINESS

Overview

Theravance Biopharma, Inc. (“we,” “our,” “Theravance Biopharma” or the “Company”) is a biopharmaceutical company primarily focused on the development and commercialization of medicines. Our focus is to deliver medicines that make a difference® in people’s lives.

In pursuit of our purpose, we leverage decades of expertise, which has led to the development of the United States (“US”) Food and Drug Administration (the “FDA”) approved YUPELRI® (revefenacin) inhalation solution indicated for the maintenance treatment of patients with chronic obstructive pulmonary disease (“COPD”). Ampreloxetine, our late-stage investigational once-daily norepinephrine reuptake inhibitor in development for the treatment of symptomatic neurogenic orthostatic hypotension (“nOH”) in patients with Multiple System Atrophy (“MSA”) has the potential to be a first in class therapy effective in treating a constellation of cardinal symptoms in MSA patients.

2023 Significant Developments

YUPELRI Sales Growth

In 2023, YUPELRI experienced sales growth and reached all-time high yearly net sales and profitability. Through the combined commercialization efforts with our partner Viatris Inc. (“Viatris”), total YUPELRI net sales increased by 9% to $221.0 million in 2023 compared to 2022. Hospital volumes, which we are directly responsible for, grew 46% in 2023 compared to 2022 and was a meaningful contributor to YUPELRI’s overall net sales growth for the year.

Initiation of Ampreloxetine New Phase 3 Clinical Study

In the first quarter of 2023, we initiated the ampreloxetine new Phase 3 clinical study (CYPRESS) in MSA patients with symptomatic nOH, using the Orthostatic Hypotension Symptom Assessment Scale (“OHSA”) composite score as the primary endpoint. In May 2023, we announced that the FDA granted Orphan Drug Designation status to ampreloxetine for the treatment of symptomatic nOH in patients with MSA. The study is currently enrolling patients with 42 clinical sites open across 11 countries, as of February 26, 2024.

Capital Return Program

In 2023, we repurchased 18.63 million of our shares on the open market at a weighted average cost of $10.551 per share for an approximate aggregate cost of $196.6 million, excluding fees and expenses. Since the inception of the capital return program in September 2022 through its completion in early January 2024, we repurchased a total of 31.41 million shares at a weighted average cost of $10.354 per share for an approximate aggregate cost of $325.3 million which reduced our shares by 37% since the inception of the capital return program.

Discontinued Investment in Research

In February 2023, we announced that we discontinued our research activities, including the inhaled Janus kinase (JAK) inhibitor program, and prioritized our R&D resources toward the ampreloxetine Phase 3 study and the completion of the YUPELRI Peak Inspiratory Flow Rate (PIFR-2) Phase 4 study. As a result of halting further investment in research activities, our headcount was reduced by approximately 17% in March 2023. We plan to seek a partnership to continue progression of our inhaled JAK inhibitor program.

Board Governance Changes

In 2023, we appointed three new independent directors reflecting our ongoing commitment to bringing new perspectives and complementary skills to the Company. In addition, we put forth a proposal to declassify the board of the directors over time which was approved at our May 2023 Annual General Meeting of Shareholders.

4

Our Programs

The chart below summarizes the status of our approved product, product candidate in development, and economic interest.

Glossary of Defined Terms used in Table Above:

COPD: Chronic Obstructive Pulmonary Disease;

FF: Fluticasone Furoate;

LAMA: Long-Acting Muscarinic Antagonist;

MSA: Multiple System Atrophy;

nOH: Neurogenic Orthostatic Hypotension;

NRI: Norepinephrine Reuptake Inhibitor;

UMEC: Umeclidinium; and

VI: Vilanterol

Core Program Updates

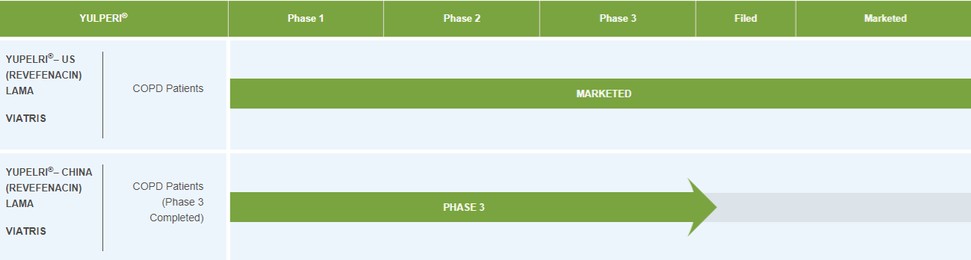

YUPELRI (revefenacin) Inhalation Solution

YUPELRI (revefenacin) inhalation solution is a once-daily, nebulized long-acting muscarinic antagonist (“LAMA”) approved for the maintenance treatment of COPD in the US. LAMAs are recognized by international COPD treatment guidelines as a cornerstone of maintenance therapy for COPD, regardless of severity of disease. Our market research indicates there is an enduring population of COPD patients in the US that either need or prefer nebulized delivery for maintenance therapy. The stability of revefenacin in both metered dose inhaler and dry powder inhaler (“MDI/DPI”) formulations suggests that revefenacin could also serve as a foundation for novel handheld combination products.

5

We co-developed YUPELRI with our collaboration partner, Viatris Inc. Under the terms of the Viatris Development and Commercialization Agreement (the “Viatris Agreement”), we led the US Phase 3 development program for YUPELRI in COPD, and Viatris was responsible for reimbursement of our costs related to the registrational program up until the approval of the first new drug application, after which costs were shared. YUPELRI was approved by the FDA for the maintenance treatment of patients with COPD in November 2018. In the US, Viatris is leading the commercialization of YUPELRI, and we co-promote the product under a profit and loss sharing arrangement (65% to Viatris; 35% to us). Outside the US (excluding China and adjacent territories), Viatris is responsible for development and commercialization and will pay us a tiered royalty on net sales at percentage royalty rates ranging from low double-digits to mid-teens. We retain worldwide rights to revefenacin delivered through other dosage forms, such as a MDI/DPI.

In 2019, we granted Viatris exclusive development and commercialization rights to nebulized revefenacin in China and adjacent territories, which include the Hong Kong SAR, the Macau SAR, and Taiwan, (collectively, the “China Region”) and we are eligible to receive low double-digit tiered royalties on net sales of nebulized revefenacin, if approved. As noted above, Viatris is responsible for all aspects of development and commercialization of nebulized revefenacin in the China Region, including pre- and post-launch activities and product registration and all associated costs.

Under the terms of the Viatris Agreement, as amended, as of December 31, 2023, we were eligible to receive from Viatris potential global development, regulatory and sales milestone payments (excluding the China Region) of up to $205.0 million in the aggregate with $160.0 million associated with YUPELRI monotherapy and $45.0 million associated with future potential combination products. Of the $160.0 million associated with monotherapy, $10.0 million relates to regulatory actions in the EU and $150.0 million relates to sales milestones based on achieving certain levels of annual US net sales as follows:

YUPELRI US Net Sales | Sales Milestones |

(In a Calendar Year) | Due from Viatris |

$250.0 million | $25.0 million |

$500.0 million | $50.0 million |

$750.0 million | $75.0 million |

As of December 31, 2023, we were also eligible to receive additional potential development and sales milestones of up to $52.5 million related to Viatris’ development and commercialization of nebulized revefenacin in the China Region with $45.0 million associated with YUPELRI monotherapy and $7.5 million associated with future potential combination products. Of the $45.0 million associated with monotherapy, $7.5 million relates to regulatory approval in the China Region and $37.5 million relates to sales milestones based on achieving certain levels of cumulative net sales in the China Region as follows:

YUPELRI China Region Net Sales | Sales Milestones |

(Cumulative) | Due from Viatris |

$100.0 million | $2.5 million |

$200.0 million | $5.0 million |

$400.0 million | $10.0 million |

$800.0 million | $20.0 million |

With respect to the China Region royalties, we are eligible to receive low double-digit tiered royalties on net sales of nebulized revefenacin as follows:

YUPELRI China Region Net Sales Thresholds | Royalty Rate |

(Annual) | Due from Viatris |

≤ $75.0 million | 14% |

> $75.0 million to ≤ $150.0 million | 17% |

> $150 million | 20% |

6

In November 2023, we learned that Viatris’ Phase 3 study of YUPELRI in China was positive, and the data were consistent with previous findings of YUPELRI’s strong efficacy. Viatris plans to move forward with a registrational filing for YUPELRI in China in mid-2024.

In August 2021, we announced that in collaboration with our partner Viatris, we were initiating a Phase 4 study comparing improvements in lung function in adults with severe to very severe COPD and suboptimal inspiratory flow rate following once-daily treatment with either revefenacin (YUPELRI) delivered via standard jet nebulizer or tiotropium delivered via a dry powder inhaler (Spiriva® HandiHaler®). This study was aimed at helping to better inform decisions when physicians are designing a personalized COPD treatment plan with patients. We agreed to pay 35% of the Phase 4 study costs, and Viatris agreed to pay 65% of the Phase 4 study costs. The first patient for the Phase 4 study was enrolled in January 2022. In January 2024, we announced that the Phase 4 study did not show a statistically significant difference between YUPELRI and Spiriva HandiHaler on the primary endpoint, change from baseline in trough forced expiratory volume in one second (FEV1) at day 85. While the primary endpoint in the Phase 4 study was not met, YUPELRI demonstrated an efficacy and safety profile consistent with its performance in other clinical studies.

While Viatris records total YUPELRI net sales, we are entitled to a 35% share of the net profit (loss). Our implied 35% share of total YUPELRI net sales is presented below:

Year Ended December 31, | Change | |||||||||||

(In thousands) |

| 2023 |

| 2022 |

| $ |

| % |

| |||

YUPELRI net sales (100% recorded by Viatris) | $ | 220,962 | $ | 201,866 | $ | 19,096 | 9 | % | ||||

YUPELRI net sales (Theravance Biopharma implied 35%) | 77,337 | 70,653 | 6,684 | 9 | ||||||||

Ampreloxetine (TD-9855)

Ampreloxetine is an investigational, once-daily norepinephrine reuptake inhibitor (“NRI”) that we are developing for the treatment of Multiple System Atrophy (“MSA”) patients with symptomatic neurogenic orthostatic hypotension (“nOH”). nOH is caused by primary autonomic failure conditions and the majority of patients with MSA experience symptoms of nOH. Ampreloxetine has high affinity for binding to the norepinephrine (“NE”) transporter. By blocking the action of the NE transporter, ampreloxetine causes an increase in extracellular concentrations of norepinephrine. Ampreloxetine is wholly owned by Theravance Biopharma.

Based on positive results from a small exploratory Phase 2 study in nOH and discussions with the FDA, we advanced ampreloxetine into a Phase 3 program. We announced the initiation of patient dosing in study in early 2019. The Phase 3 program consisted of two pivotal studies and one non-pivotal study. The first pivotal study (SEQUOIA), a four-week, randomized double-blind, placebo-controlled study, was designed to evaluate the efficacy and safety of ampreloxetine in Parkinson’s disease (“PD”), pure autonomic failure (“PAF”) and MSA patients with symptomatic nOH. The second pivotal study (REDWOOD), a four-month open label study followed by a six-week randomized withdrawal phase was designed to evaluate the durability of the same patient group’s response to ampreloxetine. The protocol for the pivotal studies stipulated an enrollment threshold of 40% MSA patients based on the hypothesis ampreloxetine would work the best in patients with MSA because they have more intact nerves on which ampreloxetine can exert its effect, relative to the other patient types in the study. The third, non-pivotal study (OAK), was a three and half year long-term extension study.

In September 2021, we reported that the SEQUOIA Phase 3 clinical study did not meet its primary endpoint. Most treatment-related adverse events were mild or moderate in severity. Serious adverse events occurred in two patients on placebo and four on ampreloxetine, none of which were considered related to the study drug. No deaths were reported, and there was no signal for supine hypertension.

In April 2022, we reported that the REDWOOD Phase 3 clinical study did not meet its primary endpoint as the results were not statistically significant for the overall population of patients which included patients with PD, PAF, and MSA. The pre-specified subgroup analysis by disease type suggested that the average benefit seen in patients receiving ampreloxetine was largely driven by a benefit to MSA patients. The benefit to MSA patients in the study was observed in multiple endpoints including Orthostatic Hypotension Symptom Assessment Scale (“OHSA”) composite, Orthostatic Hypotension Daily Activities Scale (“OHDAS”) composite, Orthostatic Hypotension Questionnaire (“OHQ”) composite

7

and OHSA #1. Throughout the study, there was no indication of worsening of supine hypertension among any of the patient sub-groups. Data suggest that ampreloxetine was well-tolerated and no new safety signals were identified among any of the patient sub-groups.

In June 2022, we held a Type C meeting with the FDA. From this meeting, we aligned on a path to a New Drug Application (“NDA”) filing with one additional Phase 3 clinical study (CYPRESS) in MSA patients with symptomatic nOH, using the OHSA composite score as the primary endpoint. This Phase 3 study was initiated in the first quarter of 2023, and the study is currently open to recruitment with the expectation of enrolling the final patient into the open label period of the study in the second half of 2024. In May 2023, we announced that the FDA granted Orphan Drug Designation status to ampreloxetine for the treatment of symptomatic nOH in patients with MSA.

In July 2022, Royalty Pharma Investments 2019 ICAV (“Royalty Pharma”) agreed to invest up to $40.0 million to advance the development of ampreloxetine in MSA in exchange for unsecured low single-digit royalties. Royalty Pharma’s $40.0 million investment in ampreloxetine included a $25.0 million upfront payment received in July 2022 and an additional $15.0 million payment upon the first regulatory approval of ampreloxetine. In exchange, Royalty Pharma will receive future unsecured royalties of 2.5% on annual ampreloxetine global net sales up to $500.0 million and 4.5% on annual global net sales over $500.0 million. If ampreloxetine regulatory approval is not achieved or if ampreloxetine sales are never recognized, the amounts invested by Royalty Pharma would not be repaid by us.

Skin-selective Pan-JAK inhibitor Program

In December 2019, we entered into a global license agreement with Pfizer Inc. (“Pfizer”) for our preclinical skin-selective, locally acting pan-JAK inhibitor program (the “Pfizer Agreement”). The compounds in this program are designed to target validated pro-inflammatory pathways and are specifically designed to possess skin-selective activity with minimal systemic exposure. Under the Pfizer Agreement, Pfizer had an exclusive license to develop, manufacture and commercialize certain compounds for all uses other than gastrointestinal, ophthalmic, and respiratory applications. We received an upfront cash payment of $10.0 million in 2019, and in March 2022, we received a $2.5 million development milestone payment from Pfizer for the first patient dosed in a Phase 1 clinical trial of the skin-selective pan-JAK inhibitor program. In June 2023, we received notice from Pfizer terminating the Pfizer Agreement, effective as of October 7, 2023, at which time the skin-selective pan-JAK inhibitor program was returned to us.

Economic Interests and Other Assets

Mid- and Long-Term Economic Interest in TRELEGY®

In July 2022, we completed the sale of all of our equity interests in Theravance Respiratory Company, LLC (“TRC”) representing our 85% economic interest in the sales-based royalty rights on worldwide net sales of GSK plc's (“GSK”) TRELEGY ELLIPTA (“TRELEGY”) to Royalty Pharma for approximately $1.1 billion in upfront cash while retaining future value through the right to receive contingent milestone payments and certain outer year-royalties (the “TRELEGY Royalty Transaction”).

From and after January 1, 2023, for any calendar year starting with the year ended December 31, 2023 and ending with the year December 31, 2026, upon certain milestone minimum royalty amounts for TRELEGY being met, Royalty Pharma is obligated to make certain cash payments to us (the “Milestone Payment(s)”). As of January 1, 2024, a total of $200.0 million in potential Milestone Payments remain available to us. For the next potential Milestone Payment, we are eligible to receive either (i) $25.0 million if Royalty Pharma receives $240.0 million or more in royalty payments from GSK with respect to 2024 TRELEGY global net sales, which we would expect to occur in the event TRELEGY global net sales are approximately $2.86 billion; or (ii) $50.0 million if Royalty Pharma receives $275.0 million or more in royalty payments from GSK with respect to 2024 TRELEGY global net sales, which we would expect to occur in the event TRELEGY global net sales exceed approximately $3.21 billion. Fourth quarter of 2023 global net sales were $737.0 million which represented an increase of 35% year-over-year, and total 2023 global net sales were $2.7 billion which represented an increase of 28% year-over-year.

In addition to potential Milestone Payments, we will receive from Royalty Pharma 85% of the royalty payments on TRELEGY payable (a) for sales or other activities occurring on and after January 1, 2031 related to TRELEGY in the

8

US, and (b) for sales or other activities occurring on and after July 1, 2029 related to TRELEGY outside of the US. US TRELEGY royalties payable to us by Royalty Pharma are expected to end in late 2032, and ex-US royalties are expected to end in the mid-2030s and are country specific. Royalty rates are upward tiering from 6.5% to 10% and based on total annual net sales.

The following information regarding the TRELEGY program is based solely upon publicly available information and may not reflect the most recent developments under the programs.

TRELEGY provides the activity of an inhaled corticosteroid (FF) plus two bronchodilators (UMEC, a LAMA, and VI, a long-acting beta2 agonist, or LABA) in a single delivery device administered once-daily. TRELEGY is approved for use in the US, European Union (“EU”), and other countries for the long-term, once-daily, maintenance treatment of patients with COPD. Additionally, the FDA approved an sNDA for the use of TRELEGY to treat asthma in adults in September 2020 making TRELEGY the first once-daily single inhaler triple therapy for the treatment of both asthma and COPD in the US. GSK has obtained approval for the asthma indication in ten additional markets. TRELEGY is currently expected to generate global peak sales of $3.7 billion in 2027 according to consensus estimates. Over the past three years, TRELEGY has shown substantial growth, with global net sales increasing annually from $661.4 million in 2019 to $2.7 billion in 2023.

See “Risk Factors—We do not control the commercialization of TRELEGY; accordingly, our receipt of Milestone Payments and receipt of the value we currently anticipate from the Outer Years Royalty will depend on, among other factors, GSK’s ability to further commercialize TRELEGY” for additional information.

Development Projects

Our focus remains on near-term value opportunities which consists of executing our ampreloxetine registration Phase 3 study (CYPRESS) and preparing for the NDA filing process. In February 2023, as part of our 2023 Strategic Actions, we announced the decision to discontinue research activities including our inhaled JAK program, including nezulcitinib, a nebulized, lung-selective JAK inhibitor positioned for the treatment of acute and chronic lung diseases.

Our Strategy

Our focus is to deliver medicines that make a difference® in people's lives. In pursuit of our purpose, we leverage decades of expertise, which has led to the development of FDA-approved YUPELRI® (revefenacin) inhalation solution indicated for the maintenance treatment of patients with COPD. Ampreloxetine, our late-stage investigational norepinephrine reuptake inhibitor in development for symptomatic nOH, has the potential to be a first in class therapy effective in treating a constellation of cardinal symptoms in MSA patients. We are committed to creating/driving shareholder value.

We follow these core guiding principles in our mission to drive value creation:

| ● | Focus on insight and innovation; |

| ● | Outsource non-core activities; |

| ● | Create and foster an integrated environment; and |

| ● | Aggressively manage uncertainty. |

We manage our pipeline with the goal of optimizing program value and allocation of resources. We employ multiple strategies for commercialization of our products. Our approach may involve retaining product rights and marketing a product independently in the US or we may partner a product to extend our commercial reach, to expand our geographic reach, and/or to manage the financial risk associated with the program. Alternatively, we may monetize or divest an asset that we designate as outside our core business, where we believe the program is optimized by leveraging partner capabilities and removing or limiting our research and development costs.

9

Manufacturing

We rely on a network of third-party contract manufacturing organizations to produce the active pharmaceutical ingredients (“API”) and drug products required for our clinical trials. We believe that we and our partners have in-house expertise to manage this network of third-party manufacturers, and we believe that we will be able to continue to negotiate third-party manufacturing arrangements on commercially reasonable terms and that it will not be necessary for us to rely on internal manufacturing capacity in order to develop or, potentially, commercialize our products. However, if we are unable to obtain contract manufacturing or obtain such manufacturing on commercially reasonable terms, or if manufacturing is interrupted at one of our suppliers, whether due to regulatory or other reasons, we may not be able to develop or commercialize our products as planned.

Any inability to acquire sufficient quantities of API or drug product in a timely manner from current or future sources could disrupt our development programs, the conduct of future clinical trials or our commercialization efforts. For more information, see the risk factor under the heading “There is a single source of supply for a number of our product candidates and for YUPELRI, and our business will be harmed if any of these single-source manufacturers are not able to satisfy demand and alternative sources are not available” of this Annual Report on Form 10-K.

Government Regulation

The development and commercialization of pharmaceutical products and our product candidates by us, our collaboration partners and licensees, and those commercializing products in which we have an economic interest, such as GSK, are subject to extensive regulation by governmental authorities in the US and other countries. Before marketing in the US, any medicine must undergo rigorous preclinical studies and clinical studies and an extensive regulatory approval process implemented by the FDA under the Federal Food, Drug, and Cosmetic Act. Outside the US, the ability to market a product depends upon receiving a marketing authorization from the appropriate regulatory authorities which are subject to equally rigorous regulatory obligations. The requirements governing the conduct of clinical studies, marketing authorization, pricing and reimbursement vary widely from country to country. In any country, however, the commercialization of pharmaceutical products is permitted only if the appropriate regulatory authority is satisfied that we have presented adequate evidence of the safety, quality and efficacy of the product.

Before commencing clinical studies in humans in the US, we must submit to the FDA an investigational new drug application (“IND”) that includes, among other things, the general investigational plan and protocols for specific human studies and the results of preclinical studies. An IND will go into effect 30 days following its receipt by the FDA unless the FDA issues a clinical hold. Once clinical studies have begun under the IND, they are usually conducted in three phases and under FDA oversight. These phases generally include the following:

Phase 1. The product candidate is introduced into patients or healthy human volunteers and is tested for safety, dose tolerance and pharmacokinetics.

Phase 2. The product candidate is introduced into a limited patient population to assess the efficacy of the drug in specific, targeted indications, assess dosage tolerance and optimal dosage, and identify possible adverse effects and safety risks.

Phase 3. Phase 3 clinical trials are undertaken to further evaluate dosage, clinical efficacy, potency and safety in an expanded patient population at geographically dispersed clinical trial sites. These clinical trials are intended to establish the overall risk/benefit profile of the product and provide an adequate basis for product labeling.

The results of product development, preclinical studies and clinical studies must be submitted to the FDA as part of an NDA. The NDA also must contain extensive manufacturing information, and under the Pediatric Research Equity Act (“PREA”), certain applications for approval must also include an assessment, generally based on clinical study data, of the safety and effectiveness of the subject drug in relevant pediatric populations. The submission of an NDA generally requires payment of a substantial user fee to the FDA under the Prescription Drug User Fee Act (“PDUFA”), subject to certain limited deferrals, waivers and reductions. FDA’s PDUFA performance goal is to review and act on 90 percent of priority new molecular entity (“NME”) NDA submissions within 6 months of the 60-day filing date, and to review and act on 90 percent of standard NME NDA submissions within 10 months of the 60-day filing

10

date. The FDA may determine that a Risk Evaluation and Management Strategy (“REMS”) is necessary to ensure that the benefits of a product outweigh its risks. At the end of the review period, the FDA communicates either approval of the NDA or issues a complete response letter (“CRL”) listing the application’s deficiencies. The CRL may require additional testing or information, including additional pre-clinical or clinical data, for the FDA to reconsider the application. Even if such additional information and data are submitted, the FDA may decide that the NDA still does not meet the standards for approval. Data from clinical trials are not always conclusive and the FDA may interpret data differently than the sponsor. FDA approval of any application may include many delays or never be granted. If FDA grants approval, an approval letter authorizes commercial marketing of the product candidate with specific prescribing information for specific indications. Post-approval modifications to the drug, such as changes in indications, labeling, or manufacturing processes or facilities, may require a sponsor to develop additional data or conduct additional pre-clinical studies or clinical trials, to be submitted in a new or supplemental NDA, which would require FDA approval.

If an application is approved, drug products are subject to continuing regulation by the FDA, and the FDA may withdraw the product approval if compliance with post-marketing regulatory standards is not maintained or if safety or quality issues are identified after the product reaches the marketplace. In addition, the FDA may require post-marketing studies, sometimes referred to as Phase 4 studies, to monitor the safety and effectiveness of approved products, and may limit further marketing of the product based on the results of these post-marketing studies. The FDA has broad post-market regulatory and enforcement powers, including the ability to require changes to a product’s approved labeling, including the addition of new warnings and contraindications, or the implementation of other risk management measures, including distribution-related restrictions, if there are new safety information developments, suspend or delay issuance of approvals, seize products, withdraw approvals, enjoin violations, and initiate criminal prosecution.

If regulatory approval for a medicine is obtained, the clearance to market the product will be limited to those diseases and conditions approved by FDA and for which the medicine was shown to be effective, as demonstrated through clinical studies and specified in the medicine’s labeling. If this regulatory approval is obtained, a marketed medicine, its manufacturer and its manufacturing facilities are subject to continual review and periodic inspections by the FDA. The FDA ensures the quality of approved medicines, carefully monitoring manufacturers’ compliance with its current Good Manufacturing Practice (“cGMP”) regulations by conducting regular, periodic visits to re-inspect equipment, facilities, and processes following the initial approval of a product. Failure to comply with applicable cGMP requirements and conditions of product approval may lead the FDA to take enforcement actions or seek sanctions, including fines, issuance of warning letters, civil penalties, injunctions, suspension of manufacturing operations, operating restrictions, withdrawal of FDA approval, seizure or recall of products, and criminal prosecution. The cGMP regulations for drugs contain minimum requirements for the methods, facilities, and controls used in manufacturing, processing, and packaging of a medicine. The regulations are intended to make sure that a medicine is safe for use, and that it has the ingredients and strength it claims to have. Discovery of previously unknown problems with a medicine, manufacturer or facility may result in restrictions on the medicine or manufacturer, including fines, issuance of warning letters, civil penalties, injunctions, suspension of manufacturing operations, operating restrictions, costly recalls, withdrawal of FDA approval, and criminal prosecution.

Additionally, the FDA and other federal regulatory agencies closely regulate the marketing and promotion of drugs through, among other things, standards and regulations for direct-to-consumer advertising, advertising and promotion to healthcare professionals, communications regarding unapproved uses, industry-sponsored scientific and educational activities, and promotional activities involving the Internet. A product cannot be promoted before it is approved. After approval, product promotion can include only those claims relating to safety and effectiveness that are consistent with the labeling approved by the FDA. Healthcare providers are permitted to prescribe drugs for “off-label” uses - that is, uses not approved by the FDA and not described in the product’s labeling - because the FDA does not regulate the practice of medicine. However, FDA regulations impose restrictions on manufacturers’ communications regarding off-label uses. Broadly speaking, a manufacturer may not promote a drug for off-label use, but under certain conditions may engage in non-promotional, balanced, scientific communication regarding off-label use. Failure to comply with applicable FDA requirements and restrictions in this area may subject a company to adverse publicity and enforcement action by the FDA, the Department of Justice, or the Office of the Inspector General of the Department of Health and Human Services, as well as state authorities. This could subject a company to a range of penalties that could have a significant commercial impact, including civil and criminal fines and agreements that materially restrict the manner in which a company promotes or distributes a drug.

11

We, our collaboration partners and licensees are also subject to various laws and regulations regarding laboratory practices, the experimental use of animals and the use and disposal of hazardous or potentially hazardous substances in connection with our drug development. In each of these areas, as above, the FDA and other regulatory authorities have broad regulatory and enforcement powers, including the ability to suspend or delay issuance of approvals, seize products, withdraw approvals, enjoin violations, and initiate criminal prosecution, any one or more of which could have a material adverse effect upon our business, financial condition and results of operations.

Outside the US, the ability to market products will also depend on receiving marketing authorizations from the appropriate regulatory authorities. Risks similar to those associated with FDA approval described above exist with the regulatory approval processes in other countries.

United States Healthcare Reform

The Patient Protection and Affordable Care Act, as amended (the “Healthcare Reform Act”), substantially changed the way healthcare is financed by both governmental and private insurers, and impacts pricing and reimbursement of YUPELRI and the marketed drugs with respect to which we are entitled to royalty or similar payments, and related commercial operations. Certain provisions of the Healthcare Reform Act have been subject to judicial challenges as well as efforts to modify them or to alter their interpretation or implementation. We expect that the Healthcare Reform Act, its implementation, efforts to modify, or invalidate, the Healthcare Reform Act or portions thereof, or its implementation, and other healthcare reform measures that may be adopted in the future, could have a material adverse effect on our industry generally and on the ability of us, our collaboration partners, or those commercializing products with respect to which we have an economic interest or right to receive royalties to maintain or increase sales of our existing products or to successfully commercialize our product candidates, if approved. For more information, see the risk factor under the heading “Changes in healthcare law and implementing regulations, including government restrictions on pricing and reimbursement, as well as healthcare policy and other healthcare payor cost-containment initiatives, may negatively impact us, our collaboration partners, or those commercializing products with respect to which we have an economic interest or right to receive royalties” of this Annual Report on Form 10-K.

Pharmaceutical Pricing

We participated in and had certain price reporting obligations under the Medicaid Drug Rebate and other programs and we remain responsible for data reported under those programs in past quarters, as described in greater detail under the risk factor “If we failed to comply with our reporting and payment obligations under the Medicaid Drug Rebate program or other governmental pricing programs, we could be subject to additional reimbursement requirements, penalties, sanctions and fines, which could have a material adverse effect on our business, financial condition, results of operations and growth prospects” of this Annual Report on Form 10-K.

Our ability, and the ability of our collaboration partners, licensees, or those commercializing products with respect to which we have an economic interest or right to receive royalties to commercialize our products successfully, and our ability to attract commercialization partners for our products, depends in significant part on the availability of adequate financial coverage and reimbursement from third-party payors, including, in the US, governmental payors such as the Medicare and Medicaid programs, managed care organizations, and private health insurers. The Inflation Reduction Act of 2022 (the “IRA”) establishes a new manufacturer discount program, Part B and Part D inflation rebates, and a Drug Price Negotiation Program under which the prices for Medicare units of certain high Medicare spend drugs without generic or biosimilar competition will be capped by reference to, among other things, a specified non-federal average manufacturer price, with negotiated prices set to take effect starting in 2026. Whether any of our products are selected for negotiation for a given year will depend on whether they are at least 7 years post-approval/licensure; whether they meet any of the exclusions from eligibility for selection for negotiation, such as the exclusion of certain orphan drugs; their expenditures under Medicare Part B or Part D during a statutorily specified period; and whether a generic of the product has been determined to have come to market. Ampreloxetine received an Orphan Drug Designation status from the FDA, which should mean it will not be selected for negotiation, assuming it continues to meet all other criteria for the exclusion from eligibility for selection. However, our understanding of whether and when our products are likely to be subject to selection for negotiation could evolve as the Drug Price Negotiation Program is implemented. We further expect continued scrutiny on pricing from Congress, agencies, and

12

other bodies with respect to drug pricing. The reimbursement environment is described in greater detail under the risk factor “Changes in healthcare law and implementing regulations, including government restrictions on pricing and reimbursement, as well as healthcare policy and other healthcare payor cost-containment initiatives, may negatively impact us, our collaboration partners, or those commercializing products with respect to which we have an economic interest or right to receive royalties” of this Annual Report on Form 10-K.

Coverage and Reimbursement

Market acceptance and sales of any one or more of our product candidates will depend on reimbursement policies and may be affected by future healthcare reform measures in the US. Significant uncertainty exists as to the coverage and reimbursement status of any drug products for which we obtain regulatory approval. In the US and markets in other countries, sales of any products for which we receive regulatory approval for commercial sale will depend in part on the availability of reimbursement from third-party payers. Third-party payers include government health administrative authorities, managed care providers, private health insurers and other organizations. The process for determining whether a payer will provide coverage for a drug product may be separate from the process for setting the price or reimbursement rate that the payer will pay for the drug product. Third-party payers may limit coverage to specific drug products on an approved list, or formulary, which might not include all of the FDA-approved drugs for a particular indication. Third-party payers are increasingly challenging the price and examining the medical necessity and cost-effectiveness of medical products and services, in addition to their safety and efficacy. We may need to conduct expensive pharmacoeconomic studies in order to demonstrate the medical necessity and cost-effectiveness of our products, in addition to the costs required to obtain FDA approvals. Any approved products we commercialize may not be considered by payers to be medically necessary or cost-effective for particular diseases or conditions. A payer’s decision to provide coverage for a drug product does not imply that an adequate reimbursement rate will be approved. Adequate third-party reimbursement may not be available to enable us to maintain price levels sufficient to realize an appropriate return on our investment in product development.

Fraud and Abuse Laws

Our interactions and arrangements with customers and third-party payors are subject to applicable US federal and state fraud and abuse laws and equivalent third country laws. These laws and the related risks are described in greater detail under the risk factor “Our relationships with customers and third-party payors are subject to applicable anti-kickback, fraud and abuse, transparency and other healthcare laws and regulations, which could expose us to criminal sanctions, civil penalties, exclusion, contractual damages, reputational harm and diminished profits and future earnings” of this Annual Report on Form 10-K.

Data Privacy and Protection

We are subject to laws and regulations that address privacy and data security. In the US, numerous federal and state laws and regulations, including state data breach notification laws, state health information and/or genetic privacy laws, and federal and state consumer protection laws (e.g., Section 5 of the Federal Trade Commission Act (“FTC Act”)), govern the collection, use, disclosure, and protection of health-related and other personal information. Similar obligations apply outside of the US. For example, the General Data Protection Regulation (“GDPR”) amplified existing data protection obligations in the EU. These laws and related risks are described in greater detail under the risk factor “If we fail to comply with data protection laws and regulations, we could be subject to government enforcement actions (which could include civil or criminal penalties), private litigation and/or adverse publicity, which could negatively affect our operating results and business” of this Annual Report on Form 10-K.

Patents and Proprietary Rights

We will be able to protect our technology from unauthorized use by third parties only to the extent that our technology is covered by valid and enforceable patents or is effectively maintained as trade secrets. Our success in the future will depend in part on obtaining patent protection for our product candidates. Accordingly, patents and other proprietary rights are essential elements of our business. Our policy is to seek patent protection in the US and selected foreign countries for novel technologies, including compositions of matter that are commercially important to the development of our business. Issued US and foreign patents generally expire 20 years after their filing date. For proprietary know-how that is not patentable, processes for which patents are difficult to enforce and any other elements

13

of our drug discovery process that involve proprietary know-how and technology that is not covered by patent applications, we rely on trade secret protection and confidentiality agreements to protect our interests. We require all of our employees, consultants, and advisors to enter into confidentiality agreements. Where it is necessary to share our proprietary information or data with outside parties, our policy is to make available only that information and data required to accomplish the desired purpose and only pursuant to a duty of confidentiality on the part of those parties.

As of December 31, 2023, we owned a total of 176 issued US patents and 1,002 granted foreign patents, as well as additional pending US patent applications and foreign patent applications. The claims in these various patents and patent applications are typically directed to compositions of matter, including claims covering product candidates, crystalline forms, lead compounds and key intermediates, pharmaceutical compositions, methods of use and/or processes for making our compounds. Our patents and patent applications are also directed to other inventions made during the research and development process. In particular, our wholly-owned subsidiary Theravance Biopharma R&D IP, LLC owns the following US patents that are listed in the FDA Approved Drug Products with Therapeutic Equivalence Evaluations (Orange Book) for YUPELRI (revefenacin) inhalation solution: US Patent No. 7,288,657, expiring on December 23, 2025; US Patent No. 7,491,736, expiring March 10, 2025; US Patent No. 7,521,041, expiring March 10, 2025; US Patent No. 7,550,595, expiring March 10, 2025; US Patent No. 7,585,879, expiring March 10, 2025; US Patent No. 7,910,608, expiring March 10, 2025; US Patent No. 8,034,946, expiring March 10, 2025; US Patent No. 8,053,448, expiring March 10, 2025; US Patent No. 8,273,894, expiring March 10, 2025; US Patent No. 8,541,451, expiring August 25, 2031; US Patent No. 9,765,028, expiring July 14, 2030; US Patent No. 10,106,503, expiring March 10, 2025; US Patent No. 10,343,995, expiring March 10, 2025; US Patent No. 10,550,081, expiring July 14, 2030; US Patent No. 11,008,289, expiring July 14, 2030; US Patent No. 11,247,969, expiring March 10, 2025; US Patent 11,484,531, expiring October 23, 2039; US Patent 11,691,948, expiring July 14, 2030; and US Patent 11,858,898, expiring July 14, 2030 (each of the aforementioned expiration dates not including any patent term extensions that may be available under the Drug Price Competition and Patent Term Restoration Act of 1984). Thus, the last to expire patent currently listed in the Orange Book for YUPELRI (revefenacin) inhalation solution expires on October 23, 2039. On December 19, 2018, we filed patent term extension (“PTE”) applications in the US Patent and Trademark Office (“USPTO”) for US Patent Nos. 7,288,657 and 7,585,879. These PTE applications are currently pending and, if granted, we will be permitted to extend the term of one of these patents for the period determined by the USPTO.

The patent rights relating to YUPELRI (revefenacin) inhalation solution currently consist of issued US patents, pending US patent applications and certain counterpart patents and patent applications in a number of jurisdictions, including Europe and China.

Additionally, some of our patents and patent applications are directed to products in development. Our patent rights relating to ampreloxetine include an issued US composition of matter patent that expires in 2030 and an issued US method of treatment patent that expires in 2037 (in each case, not including any patent term extensions that may be available under the Drug Price Competition and Patent Term Restoration Act of 1984). The patent portfolio for this development product includes additional pending patent applications and granted patents in a number of jurisdictions. Nevertheless, issued patents can be challenged, narrowed, invalidated, or circumvented, which could limit our ability to stop competitors from marketing similar products and threaten our ability to commercialize our product candidates. Our patent position, similar to other companies in our industry, is generally uncertain and involves complex legal and factual questions. To maintain our proprietary position, we will need to obtain effective claims and potentially enforce these claims once granted. It is possible that, before any of our products can be commercialized, any related patent may expire or remain in force only for a short period following commercialization, thereby reducing any advantage of the patent. Also, we do not know whether any of our patent applications will result in any issued patents or, if issued, whether the scope of the issued claims will be sufficient to protect our proprietary position.

Patent Term Restoration, Regulatory Exclusivities, and Hatch-Waxman Litigation

Depending upon the timing, duration, and specifics of FDA approval of our product candidates, some of our US patents may be eligible for limited patent term extension under the Drug Price Competition and Patent Term Restoration Act of 1984, referred to as the Hatch-Waxman Act. The Hatch-Waxman Act permits a patent restoration term of up to five years as compensation for patent term lost during product development and the FDA regulatory review process. However, patent term restoration cannot extend the remaining term of a patent beyond a total of 14 years from the product’s approval date. The patent term restoration period is generally one-half the time between the effective date of

14

an IND and the submission date of an NDA, plus the time between the submission date of an NDA and the approval of that application, except that the period is reduced by any time during which the applicant failed to exercise due diligence. Only one patent applicable to an approved drug is eligible for the extension, and the extension must be applied for prior to expiration of the patent and within 60 days of approval. The USPTO, in consultation with the FDA, reviews and approves the application for any patent term extension or restoration.

The Hatch-Waxman Act also provides periods of regulatory exclusivity for products that would serve as a reference listed drug, or RLD, for an abbreviated new drug application, or ANDA, or application submitted under section 505(b)(2) of the FDCA, or 505(b)(2) application. If a product is a new chemical entity, or NCE — generally meaning that the active moiety has never before been approved in any drug — there is a period of five years from the product’s approval during which the FDA may not accept for filing any ANDA or 505(b)(2) application for a drug with the same active moiety. An ANDA or 505(b)(2) application may be submitted after four years, however, if the sponsor of the application makes a “Paragraph IV” certification stating that one or more of the Orange Book listed patents are invalid or will not be infringed by the applicant’s product.

A product, if not an NCE, or a new product use may instead qualify for a three-year period of exclusivity if the NDA contains new clinical data (other than bioavailability studies), derived from studies conducted by or for the sponsor, that were necessary for approval. In that instance, the exclusivity period does not preclude filing or review of an ANDA or 505(b)(2) application; rather, the FDA is precluded from granting final approval to the ANDA or 505(b)(2) application until three years after approval of the RLD. Additionally, the exclusivity applies only to the conditions of approval that required submission of the clinical data.

Once the FDA accepts for filing an ANDA or 505(b)(2) application containing a Paragraph IV certification, the applicant must within 20 days provide notice to the RLD NDA holder and patent owner that the application has been submitted and provide the factual and legal basis for the applicant’s assertion that the patent is invalid or not infringed. If the NDA holder or patent owner files suit against the ANDA or 505(b)(2) applicant for patent infringement within 45 days of receiving the Paragraph IV notice, the FDA is prohibited from approving the ANDA or 505(b)(2) application for a period of 30 months or the resolution of the underlying suit, whichever is earlier. If the RLD has NCE exclusivity and the notice is given and suit filed during the fifth year of exclusivity, the regulatory stay extends until 7.5 years after the RLD approval. The FDA may approve the proposed product before the expiration of the regulatory stay if a court finds the patent invalid or not infringed or if the court shortens the period because the parties have failed to cooperate in expediting the litigation.

During January 2023, we received notice from Accord Healthcare, Inc.; Cipla USA, Inc. and Cipla Limited; Eugia Pharma Specialties Ltd.; Lupin Inc.; Mankind Pharma Ltd.; Orbicular Pharmaceutical Technologies Private Limited; and Teva Pharmaceuticals, Inc. (collectively, the “generic companies”), that they have each filed with FDA an ANDA, for a generic version of YUPELRI. The notices from the generic companies each included a Paragraph IV certification with respect to five of our patents listed in FDA’s Orange Book for YUPELRI. The asserted patents relate generally to polymorphic forms of and a method of treatment using YUPELRI. In February 2023, we filed patent infringement suits against the generic companies in federal district court, which continue in the United States District Court for the District of New Jersey. That complaint alleges that by filing the ANDAs, the generic companies have infringed five of our Orange Book listed patents. We are seeking a permanent injunction to prevent the generic companies from introducing a generic version of YUPELRI that would infringe our patents. As a result of this lawsuit, a stay of approval through May 2026 will be imposed by FDA on the generic companies’ ANDAs pending any adverse court decision.

We have subsequently filed further complaints and amended complaints regarding newly-granted Orange Book listed patents, as well as certain non-Orange Book listed patents. These new complaints do not result in any further stay of approval by FDA.

As of February 28, 2024, we have settled all litigation with Accord Healthcare, Inc.; Lupin Pharmaceuticals, Inc.; Orbicular Pharmaceutical Technologies Private Limited; and Teva Pharmaceuticals, Inc. pursuant to individual agreements in which we granted these companies a royalty-free, non-exclusive, non-sublicensable, non-transferable license to manufacture and market their respective generic versions of YUPELRI inhalation solution in the US on or

15

after the licensed launch date of April 23, 2039, subject to certain exceptions as is customary in these type of agreements. As required by law, the settlements are subject to review by the U.S. Department of Justice and the Federal Trade Commission. The patent litigation against the three remaining generic companies, along with certain affiliates, remains pending.

This litigation and the related risks are described in greater detail under the risk factor “Litigation to protect or defend our intellectual property or third-party claims of intellectual property infringement would require us to divert resources and may prevent or delay our drug discovery and development efforts” of this Annual Report on Form 10-K.

Competition

Our late-stage development programs, and the marketed products to which we are entitled to profit share revenue, royalty or similar payments are primarily focused on respiratory and neurological therapeutics. Our commercial infrastructure is focused primarily on the acute care setting. We expect that any medicines that we commercialize with our collaborative partners or on our own will compete with existing and future market-leading medicines.

Many of our competitors have substantially greater financial, technical and personnel resources than we have. In addition, many of these competitors have significantly greater commercial infrastructures than we have. Our ability to compete successfully will depend largely on our ability to leverage our experience in drug development and commercialization to:

| ● | develop medicines that are superior to other products in the market; |

| ● | attract and retain qualified scientific, clinical development and commercial personnel; |

| ● | obtain patent and/or other proprietary protection for our medicines and technologies; |

| ● | obtain required regulatory approvals; |

| ● | commercialize approved products; and |

| ● | successfully collaborate with pharmaceutical companies in the development and commercialization of new medicines. |

YUPELRI (revefenacin) inhalation solution

YUPELRI competes predominately with short acting nebulized bronchodilators that are dosed three to four times per day. During 2023, Sunovion Pharmaceuticals Inc. voluntarily withdrew Lonhala® Magnair® (glycopyrrolate) from the US market due to limited utilization, leaving YUPELRI as the only approved nebulized LAMA as of December 31, 2023.

Verona Pharma plc’s ensifentrine, a first-in-class, selective inhaled dual inhibitor of PDE3 and PDE4 is expected to launch in the US in the second half of 2024. Nebulized ensifentrine has the potential to be complementary to YUPELRI given that it is another nebulized treatment for COPD.

Sanofi and Regeneron Pharmaceutical, Inc. are expecting US approval for their first-in-class, IL-4/IL-13 monoclonal antibody (mAb) Dupixent® (dupilumab) for COPD in the second half of 2024. The expanded indication is expected to be a maintenance treatment for patients with moderate-to-severe COPD, who are uncontrolled with current SOC triple therapy (LAMA + LABA + ICS) and have evidence of Type 2 inflammation and frequent exacerbation history. Dupixent is currently indicated for atopic dermatitis, asthma, chronic rhinosinusitis with nasal polyposis, eosinophilic esophagitis and prurigo nodularis.

Ampreloxetine norepinephrine reuptake inhibitor (“NRI”)

If successfully developed and approved, ampreloxetine would be expected to serve as the only safe, convenient, and durably effective treatment option for MSA patients with symptomatic nOH. While droxidopa is currently the sole product approved for nOH patients, it was approved to treat dizziness, lightheadedness, or the “feeling that you are about to black out” in adults who experience nOH and who have MSA or other conditions. Droxidopa has never demonstrated

16

a durable effect on nOH symptoms including failure of a confirmatory study known as RESTORE which was required by the FDA as a condition of an accelerated approval. Northera®, marketed by Lundbeck NA Ltd., is the branded version of droxidopa and became generic in 2021. Midodrine, which is approved for OH, is not indicated to improve symptoms of nOH. Both midodrine and droxidopa must be taken 3 times daily and carry a black box warning for its potential to lead to a “marked elevation of supine blood pressure”. Pending confirmation of its clinical profile in the CYPRESS study, it is anticipated that ampreloxetine will represent a differentiated treatment option for MSA patients with symptomatic nOH.

Trelegy (the combination of fluticasone furoate/umeclidinium bromide/vilanterol)

For treatment of COPD, Trelegy competes in all major markets with AstraZeneca’s Breztri® Aerosphere® (budesonide/glycopyrronium/formoterol fumarate, dosed twice per day). Trimbow® (beclometasone dipropionate/formoterol fumarate/glycopyrronium bromide, dosed twice per day) from Chiesi Farmaceutici is an additional COPD competitor in Europe.

For treatment of asthma, TRELEGY is the only triple therapy approved in the US and competes in Japan with Novartis’s Enerzair® Breezhaler® (indacaterol acetate, glycopyrronium bromide and mometasone furoate, dosed once daily).

In both COPD and asthma, TRELEGY also competes with “open triple” therapy which can be accomplished by the concurrent use of two or three products. An example of such use includes a LABA/ICS combination, such as AstraZeneca’s Symbicort® and a LAMA such as Boehringer Ingelheim’s Spiriva®.

Human Capital

As of December 31, 2023, we had 99 employees. Of these employees, 88 were based in the US, and 11 were based in Dublin, Ireland.

Culture and Employee Engagement

We consider our employee relations first-rate and strive to provide a culture of purpose, engagement, and learning. We have a strong value proposition anchored in our Core Values—We Think it Through, We Find a Way, We Get it Done, and We Win Together. We strive to live these values across the Company every day, integrating them into everything from our interview, hiring, and onboarding processes to our PULSE performance process, total rewards, and recognition programs. In addition to valuing professional qualifications, we emphasize the importance of character and integrity, fostering a culture of empowerment where employees have ownership in business outcomes.

Reflected in our Core Values are behaviors that keep our people engaged and working collaboratively. Our employees are encouraged to ask questions, make suggestions, and provide input through many forms of corporate communication, such as an open-door policy, all-employee meetings, an anonymous online suggestion box, and an employee PULSE survey. Our employee PULSE survey is designed to assist us in measuring overall employee engagement, and we consistently achieve participation rates between 85% to 100%. Our 2023 survey scores averaged an overall score of 4.5 on a scale of 1 (Strongly Disagree) through 5 (Strongly Agree), and we received 100% participation from employees. These survey results provide important insight into organizational success and allow areas of opportunity to be identified and addressed.

We expect all employees to observe the highest levels of business ethics while delivering the highest levels of performance. These expectations are outlined and reinforced in various documents and forms of communication within and across our Company. The Company encourages employees to speak up and raise questions and concerns promptly about any situation that may violate our Code of Business Conduct, our Core Values, or our policies. We seek to promote an environment that fosters honest communications about matters of conduct related to our business activities, whether that conduct occurs within the Company, involves one of the Company’s contractors, suppliers, consultants, clients, or any other party with a business relationship with the Company. We work diligently to make clear that management is prepared to address any reported violations and ensure that it is known that any form of retaliation is strictly prohibited. In addition, we have an easily accessible hotline available to employees wishing to report complaints anonymously.

17

Diversity, Equity, and Inclusion

As an equal-opportunity employer, we strive to build and maintain a culture of diversity, equity, and inclusion through both our business and human resources practices and policies. We work to eliminate discrimination and harassment in all its forms, including related to color, race, sex or gender, sexual orientation, gender identity, age, pregnancy, caste, disability, ethnicity, national origin, ancestry, religious beliefs, veteran status, uniformed service member status, or physical or mental disability. We strive to build and foster a culture where all employees feel empowered to be their authentic selves. Our Diversity, Equity & Inclusion Council and Women’s Leadership Network are Company-sponsored, employee-led groups that aim to improve attraction, retention, development, inclusion, and engagement of a diverse and global workforce. For the benefit of our employees, patients, and community, we must celebrate, encourage, and support similarities and differences to drive innovation.

Talent, Development, and Total Rewards

We believe that our talent strategy of providing exciting career growth and development opportunities, recognizing, and rewarding performance, providing competitive compensation and benefits assists us in attracting and retaining the best talent. We believe we are successful in our retention efforts because we provide challenging work assignments, cross-functional teamwork experiences, and career progression supported by new skill-building. We invest in employee learning and development by identifying and providing training and development programs, speakers, tuition reimbursement, and cross-training in areas of interest beyond hired role.

We work diligently to attract the best talent from a diverse range of sources to meet the current and future demands of our business. We offer a competitive total rewards package that supports our business strategy to attract, retain and reward our employees in a highly competitive market. Our employees are provided with a strong base salary, cash bonus opportunities, equity incentives, health and wellness benefits, and programs. We regularly evaluate our compensation programs with an independent consultant and utilize industry benchmarking. In addition, we provide a variety of programs and services that meet our employees' needs and encourage work-life balance. These services include competitive and affordable healthcare and additional insurance benefits for both full-time and part-time employees, including eligible dependents. We also match contributions to tax-qualified defined contribution savings (401k) plans, offer an employee share purchase plan (“ESPP”), and provide training and development programs designed to improve workplace performance while supporting flexible, hybrid-remote working.

Understanding the importance of goal setting and ongoing career development conversations, we require managers and employees to play an active role in the PULSE performance management process at monthly, quarterly, and annual frequencies. PULSE is designed to increase clarity and accountability for roles and responsibilities, strengthen communication, and build trust, all while championing personal and professional growth, learning, and success.

Workplace Safety

Workplace safety is always a priority for us. To maintain a safe and healthy workplace, we have implemented initiatives, procedures, and policies designed to address risk and stay compliant with relevant national and international health and safety standards. We continue to focus on employee wellness and safety, policy updates based on Centers for Disease Control and Prevention (“CDC”), county, federal, and state guidelines, and ongoing employee communication.

Financial Information About Geographic Areas

Information on our total revenues attributed to geographic areas and customers who represented at least 10% of our total revenues is included in “Item 8, Note 3. Segment Information,” to our consolidated financial statements in this Annual Report on Form 10-K.

Corporation Information

Theravance Biopharma was incorporated in the Cayman Islands in July 2013 under the name Theravance Biopharma, Inc. Theravance Biopharma began operating as an independent, publicly-traded company on June 2, 2014 following a spin-off from Innoviva, Inc. Our corporate address in the Cayman Islands is P.O. Box 309, Ugland House,

18

Grand Cayman, KY1-1104, Cayman Islands, and the address of our wholly-owned US operating subsidiary is Theravance Biopharma US, Inc., 901 Gateway Boulevard, South San Francisco, California 94080, which also serves as our principal executive office. While Theravance Biopharma is incorporated under Cayman Island law, the Company became an Irish tax resident effective July 1, 2015. The office address of our wholly-owned Irish operating subsidiary, Theravance Biopharma Ireland Limited, is The Lennox Building, Suite 101, 50 Richmond Street South, Saint Kevin’s, Dublin, Ireland.

Available Information

Our Internet address is www.theravance.com. Our investor relations website is located at https://investor.theravance.com. We make available free of charge on our investor relations website under “SEC Filings” our Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K, our directors’ and officers’ Section 16 Reports and any amendments to those reports as soon as reasonably practicable after filing or furnishing such materials to the US Securities and Exchange Commission (“SEC”). The SEC maintains a website that contains the materials we file with or furnish to the SEC at www.sec.gov. Our current Code of Business Conduct, Corporate Governance Guidelines, Articles of Association, Board of Director Committee Charters, and other materials, including amendments thereto, may also be found on our investor relations website under “Corporate Governance.” The information found on our website is not part of this or any other report that we file with or furnish to the SEC. Theravance Biopharma and the Theravance Biopharma logo are registered trademarks of the Theravance Biopharma group of companies. Trademarks, tradenames, or service marks of other companies appearing in this report are the property of their respective owners.

19

ITEM 1A. RISK FACTORS

The risks described below and elsewhere in this Annual Report on Form 10-K and in our other public filings with the SEC are not the only risks facing us. Additional risks and uncertainties not currently known to us or that we currently deem to be immaterial also may materially adversely affect our business, financial condition and/or operating results.

Summary of Principal Risks Associated with Theravance Biopharma’s Business

| ● | We may never achieve or sustain profitability from our operations; |

| ● | If YUPELRI’s acceptance by physicians, patients, third party payors, or the medical community in general does not continue to grow, we may not receive significant additional revenues from sales of this product; |

| ● | In collaboration with Viatris, we are responsible for marketing and sales of YUPELRI in the US, which subjects us to certain risks; |

| ● | Any delay in commencing or completing clinical studies for product candidates or product and any adverse results from clinical or non-clinical studies or regulatory obstacles product candidates or product may face, would harm our business and the price of our securities could fall; |

| ● | If our product candidates are not approved by regulatory authorities, including the FDA, we will be unable to commercialize them; |

| ● | If our partners do not satisfy their obligations under our agreements with them, or if they terminate our partnerships with them, we may not be able to develop or commercialize our partnered product candidates as planned; |

| ● | Our ongoing drug development efforts might not generate additional approvable drugs; |

| ● | We face substantial competition from companies with more resources and experience than we have, which may result in others discovering, developing, receiving approval for or commercializing products before or more successfully than we do; |

| ● | We are subject to extensive and ongoing regulation, oversight and other requirements by the FDA and failure to comply with these regulations and requirements may subject us to penalties that may adversely affect our financial condition or our ability to commercialize any approved products; and |

| ● | We and/or our collaboration partners and those commercializing products with respect to which we have an economic interest or right to receive royalties may face competition from companies seeking to market generic versions of any approved products in which we have an interest, such as YUPELRI. |

RISKS RELATING TO THE COMPANY

We may never achieve or sustain profitability from our operations.

First as part of Innoviva, Inc., and since June 2, 2014 as Theravance Biopharma, we have been engaged in discovery and development of compounds and product candidates since 1997. We may never generate sufficient cash or revenue to achieve sustainable cash flow or profitability from our operations. For the year ended December 31, 2023, we recognized a net loss of $55.2 million. We reflect the cumulative net loss incurred after June 2, 2014, the effective date of our spin-off from Innoviva, Inc. (the “Spin-Off”), as accumulated deficit on our consolidated balance sheets, which was $909.1 million as of December 31, 2023. We may continue to incur net losses over the next several years due to expenditures relating to the development of our current product candidate, which we are advancing into and through

20