UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

ý | Annual Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 |

For the fiscal year ended December 31, 2017

¨ | Transition Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 |

Commission File Number: 001-36270

SANTANDER CONSUMER USA HOLDINGS INC.

(Exact Name of Registrant as Specified in Its Charter)

_______________________________________________________________

Delaware | 32-0414408 | |

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification Number) | |

1601 Elm Street, Suite 800

Dallas, Texas 75201

(214) 634-1110

(Address, including zip code, and telephone number, including area code, of principal executive offices)

_______________________________________________________________

Securities registered pursuant to Section 12(b) of the Act:

Title of Class | Name of Exchange on Which Registered | |

Common Stock, $0.01 par value per share | New York Stock Exchange | |

Securities registered pursuant to Section 12(g) of the Act:

None

_______________________________________________________________

Indicate by check mark whether the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ý No ¨

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act. Yes ¨ No ý

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ý No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation ST (Section 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ý No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of Registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ý

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See definition of “large accelerated filer”, “accelerated filer”, “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer | ý | Accelerated filer | ¨ | Emerging growth company | ¨ | ||||

Non-accelerated filer | ¨ | Smaller reporting company | ¨ | ||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ¨

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act) Yes ¨ No ý

As of June 30, 2017, the Registrant’s common stock, par value $0.01 per share, held by non-affiliates had an aggregate market value of approximately $1.4 billion based on the closing price on that date on the New York Stock Exchange of $12.76 per share.

Indicate the number of shares outstanding of each of the issuer’s classes of common stock, as of the latest practicable date.

Class | Outstanding at February 15, 2018 | |

Common Stock ($0.01 par value) | 360,608,237 shares | |

Documents Incorporated By Reference

Portions of the registrant’s definitive proxy statement to its 2018 annual meeting of stockholders (the Proxy Statement) are incorporated by reference into Part III of the Annual Report on Form 10-K where indicated.

INDEX

Unless otherwise specified or the context otherwise requires, the use herein of the terms “we,” “our,” “us,” “SC,” and the “Company” refer to Santander Consumer USA Holdings Inc. and its consolidated subsidiaries.

Cautionary Note Regarding Forward-Looking Information

This Annual Report on Form 10-K contains forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. Any statements about the Company's expectations, beliefs, plans, predictions, forecasts, objectives, assumptions, or future events or performance are not historical facts and may be forward-looking. These statements are often, but not always, made through the use of words or phrases such as “anticipates,” “believes,” “can,” “could,” “may,” “predicts,” “potential,” “should,” “will,” “estimate,” “plans,” “projects,” “continuing,” “ongoing,” “expects,” “intends,” and similar words or phrases. Although the Company believes that the expectations reflected in these forward-looking statements are reasonable, these statements are not guarantees of future performance and involve risks and uncertainties which are subject to change based on various important factors, some of which are beyond the Company's control. Among the factors that could cause the Company's actual performance to differ materially from those suggested by the forward-looking statements are:

2

• | the Company operates in a highly regulated industry and continually changing federal, state, and local laws and regulations could materially adversely affect its business; |

• | the Company's ability to remediate any material weaknesses in internal controls over financial reporting completely and in a timely manner; |

• | adverse economic conditions in the United States and worldwide may negatively impact the Company's results; |

• | the business could suffer if access to funding is reduced or if there is a change in the Company’s funding costs or ability to execute securitizations; |

• | the Company faces significant risks implementing its growth strategy, some of which are outside of its control; |

• | the Company may not realize the anticipated benefits from, and may incur unexpected costs and delays in connection with exiting its personal lending business; |

• | the Company's agreement with FCA may not result in currently anticipated levels of growth and is subject to performance conditions that could result in termination of the agreement; |

• | the business could suffer if the Company is unsuccessful in developing and maintaining relationships with automobile dealerships; |

• | the Company's financial condition, liquidity, and results of operations depend on the credit performance of its loans; |

• | loss of the Company's key management or other personnel, or an inability to attract such management and personnel, could negatively impact its business; |

• | the Company is directly and indirectly, through its relationship with SHUSA, subject to certain banking and financial services regulations, including oversight by the Office of the Comptroller of the Currency (OCC), the Consumer Financial Protection Bureau (CFPB), the European Central Bank, and the Federal Reserve Bank of Boston (FRBB); such oversight and regulation may limit certain of the Company's activities, including the timing and amount of dividends and other limitations on the Company's business; |

• | future changes in the Company's ownership by, or relationship with, SHUSA or Santander, could adversely affect its operations; and |

• | the other factors that are described in Part I, Item IA - Risk Factors of this Annual Report on Form 10-K. |

If one or more of the factors affecting the Company's forward-looking information and statements renders forward-looking information or statements incorrect, the Company's actual results, performance or achievements could differ materially from those expressed in, or implied by, forward-looking information and statements. Therefore, the Company cautions the reader not to place undue reliance on any forward-looking information or statements. The effect of these factors is difficult to predict. Factors other than these also could adversely affect the Company's results, and the reader should not consider these factors to be a complete set of all potential risks or uncertainties. New factors emerge from time to time, and management cannot assess the impact of any such factor on the Company's business or the extent to which any factor, or combination of factors, may cause results to differ materially from those contained in any forward-looking statement. Any forward-looking statements only speak as of the date of this document, and the Company undertakes no obligation to update any forward-looking information or statements, whether written or oral, to reflect any change, except as required by law. All forward-looking statements attributable to the Company are expressly qualified by these cautionary statements.

Glossary

The following is a list of abbreviations, acronyms, and commonly used terms used in this Annual Report on Form 10-K.

ABS | Asset-backed securities |

Advance Rate | The maximum percentage of unpaid principal balance that a lender is willing to lend |

ALG | Automotive Lease Guide |

APR | Annual Percentage Rate |

ASC | Accounting Standards Codification |

ASU | Accounting Standards Update |

Auto Finance Holdings | Sponsor Auto Finance Holdings Series LP, a former investor in SC |

Bluestem | Bluestem Brands, Inc., an online retailer for whose customers SC provides financing |

Board | SC’s Board of Directors |

Capmark | Capmark Financial Group Inc., an investment company |

3

CBP | Citizens Bank of Pennsylvania |

CCAR | Comprehensive Capital Analysis and Review |

CCART | Chrysler Capital Auto Receivables Trust, a securitization platform |

Centerbridge | Centerbridge Partners, L.P., a private equity firm |

CEO | Chief Executive Officer |

CFPB | Consumer Financial Protection Bureau |

CFO | Chief Financial Officer |

Chrysler Agreement | Ten-year private-label financing agreement with FCA |

Clean-up Call | The early redemption of a debt instrument by the issuer, generally when the underlying portfolio has amortized to 5% or 10% of its original balance |

Commission | U.S. Securities and Exchange Commission |

Credit Enhancement | A method such as overcollateralization, insurance, or a third-party guarantee, whereby a borrower reduces default risk |

Dealer Loan | A floorplan line of credit, real estate loan, working capital loan, or other credit extended to an automobile dealer |

Dodd-Frank Act | Comprehensive financial regulatory reform legislation enacted by the U.S. Congress on July 21, 2010 |

DOJ | U.S. Department of Justice |

DRIVE | Drive Auto Receivables Trust, a securitization platform |

ECB | European Central Bank |

ECOA | Equal Credit Opportunity Act |

ERMC | Enterprise Risk Management Committee |

Employment Agreement | The amended and restated employment agreement, executed as of December 31, 2011, by and among SC, Banco Santander, S.A. and Thomas G. Dundon |

Exchange Act | Securities Exchange Act of 1934, as amended |

FASB | Financial Accounting Standards Board |

FCA | Fiat Chrysler Automobiles US LLC, formerly Chrysler Group LLC |

FICO® | A common credit score created by Fair Isaac Corporation that is used on the credit reports that lenders use to assess an applicant’s credit risk. FICO® is computed using mathematical models that take into account five factors: payment history, current level of indebtedness, types of credit used, length of credit history, and new credit |

FIRREA | Financial Institutions Reform, Recovery and Enforcement Act of 1989 |

Floorplan Loan | A revolving line of credit that finances inventory until sold |

Federal Reserve Board | Board of Governors of the Federal Reserve System |

FRBB | Federal Reserve Bank of Boston |

FTC | Federal Trade Commission |

GAP | Guaranteed Auto Protection |

IPO | SC's Initial Public Offering |

ISDA | International Swaps and Derivative Association |

J.D. Power | J.D. Power and Associates |

LendingClub | LendingClub Corporation, a peer-to-peer personal lending platform company from which SC acquired loans under terms of flow agreements |

Managed Assets | Managed assets included assets (a) owned and serviced by the Company; (b) owned by the Company and serviced by others; and (c) serviced for others. |

MSA | Master Service Agreement |

Nonaccretable Difference | The difference between the undiscounted contractual cash flows and the undiscounted expected cash flows of a portfolio acquired with deteriorated credit quality |

NYSE | New York Stock Exchange |

OCC | Office of the Comptroller of the Currency |

Overcollateralization | A credit enhancement method whereby more collateral is posted than is required to obtain financing |

4

OEM | Original equipment manufacturer |

Private-label | Financing branded in the name of the product manufacturer rather than in the name of the finance provider |

Remarketing | The controlled disposal of leased vehicles that have reached the end of their lease term or of financed vehicles obtained through repossession |

Residual Value | The future value of a leased asset at the end of its lease term |

Santander | Banco Santander, S.A. |

SBNA | Santander Bank, N.A., a wholly-owned subsidiary of SHUSA. Formerly Sovereign Bank, N.A. |

SC | Santander Consumer USA Holdings Inc., a Delaware corporation, and its consolidated subsidiaries |

SCI | Santander Consumer International Puerto Rico, LLC |

SC Illinois | Santander Consumer USA Inc., an Illinois Corporation and wholly-owned subsidiary of SC |

SCRA | Servicemembers Civil Relief Act |

SDART | Santander Drive Auto Receivables Trust, a securitization platform |

SEC | U.S. Securities and Exchange Commission |

Separation Agreement | The Separation Agreement dated July 2, 2015 entered into by Thomas G. Dundon with SC, DDFS LLC, SHUSA, Santander Consumer USA Inc. (the wholly owned subsidiary of SC) and Banco Santander, S.A. |

Shareholders Agreement | The Shareholders Agreement dated January 28, 2014, by and among the Company, SHUSA, DDFS, Thomas G. Dundon, Sponsor Auto Finance Holdings Series LP, and, for the certain sections set forth therein, Banco Santander, as amended |

SHUSA | Santander Holdings USA, Inc., a wholly-owned subsidiary of Santander and the majority owner of SC |

SPAIN | Santander Prime Auto Issuing Note Trust, a securitization platform |

SRT | Santander Retail Auto Lease Trust, a lease securitization platform |

Subvention | Reimbursement of the finance provider by a manufacturer for the difference between a market loan or lease rate and the below-market rate given to a customer |

TDR | Troubled Debt Restructuring |

Trusts | Special purpose financing trusts utilized in SC’s financing transactions |

U.S. GAAP | U.S. Generally Accepted Accounting Principles |

VIE | Variable Interest Entity |

Warehouse Facility | A revolving line of credit generally used to fund finance receivable originations |

5

PART I

ITEM I. | BUSINESS |

General

Santander Consumer USA Holdings Inc. (SC or the Company) was incorporated in 2013 in the State of Delaware and is the holding company for Santander Consumer USA Inc., an Illinois corporation, and subsidiaries, a specialized consumer finance company focused on vehicle finance and third-party servicing. The Company’s primary business is the indirect origination and securitization of retail installment contracts, principally through manufacturer-franchised dealers in connection with their sale of new and used vehicles to retail consumers.

Since May 1, 2013, under the terms of a ten-year private-label financing agreement (the Chrysler Agreement) with Fiat Chrysler Automobiles US LLC (FCA), the Company has been FCA’s preferred provider for consumer loans and leases and dealer loans. Business generated under terms of the Chrysler Agreement is branded as Chrysler Capital. In conjunction with the Chrysler Agreement, the Company offers a full spectrum of auto financing products and services to FCA customers and dealers under the Chrysler Capital brand. These products and services include consumer retail installment contracts and leases, as well as dealer loans for inventory, construction, real estate, working capital and revolving lines of credit.

The Company also originates vehicle loans through a web-based direct lending program, purchases vehicle retail installment contracts from other lenders, and services automobile and recreational and marine vehicle portfolios for other lenders. Additionally, the Company has other relationships through which it holds personal loans, private-label credit cards and other consumer finance products. However, in October 2015, the Company announced its exit from personal lending, and accordingly, substantially all of its personal lending assets are classified as held for sale at December 31, 2017.

As of February 15, 2018, the Company was owned approximately 68.1% by SHUSA, a wholly-owned subsidiary of Santander, and approximately 31.9% by other shareholders.

The Company's Markets

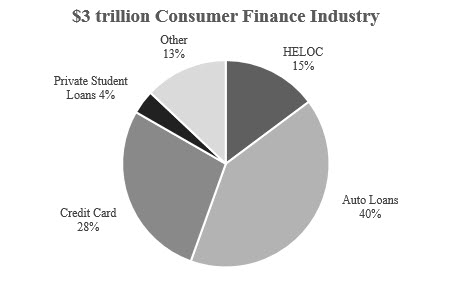

The consumer finance industry in the United States has approximately $3 trillion of outstanding borrowings as of December 31, 2017 and includes vehicle loans and leases, credit cards, home equity lines of credit, private student loans, and personal loans.

Sources: Federal Reserve Bank of New York; Consumer Financial Protection Bureau

The Company's primary focus is the vehicle finance segment of the U.S. consumer finance industry. Vehicle finance includes loans and leases taken out by consumers to fund the purchase of new and used automobiles, as well as other vehicles such as motorcycles, recreational vehicles, and watercraft. Within the vehicle finance segment, the Company maintains a strong presence in the auto finance market. The auto finance market features a fungible product resulting in an efficient pricing market, but it is highly fragmented, with no individual lender accounting for more than 10% of total market share. As of December 31, 2017, there were approximately $1.2 trillion of auto loans outstanding in the United States.

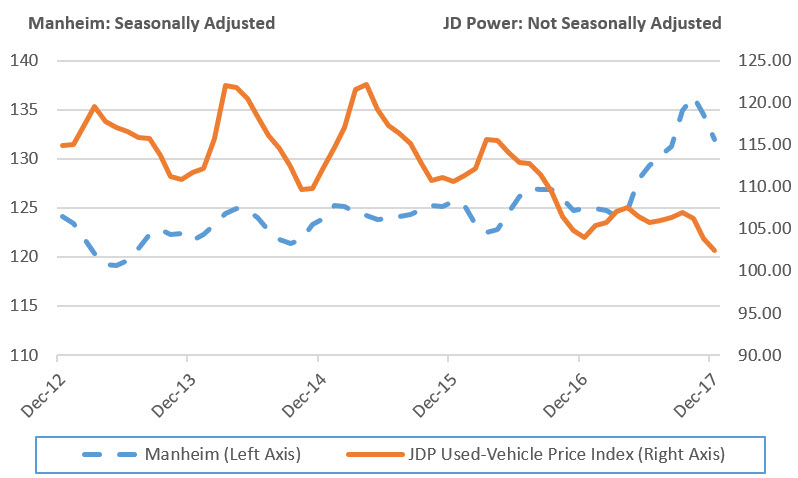

The Company originates both prime and nonprime vehicle loans, and maintains on its balance sheet primarily nonprime loans. The Company also originates leases, substantially all of which are extended to prime borrowers. Historically, used car financing has made up a majority of the Company's business. In 2017, through the third quarter, used automobiles accounted for 70% of total automobiles sold in the United States, and approximately 53% of used car purchases were financed. The primary metrics

6

used by the market to monitor the strength of the used car market are the Manheim Used Vehicle Index and J.D. Power Price Index, measures of wholesale used car prices adjusted by their mileage or vintage. As of December 31, 2017, used car financing represented 59% of the Company's outstanding retail installment contracts, of which 82% consisted of nonprime auto loans.

Source: Manheim Inc., as of December 31, 2017 & JP Power used-Vehicle Price Index, as of December 31, 2017

Note: Indexed to a basis of 100 at 1995 levels.

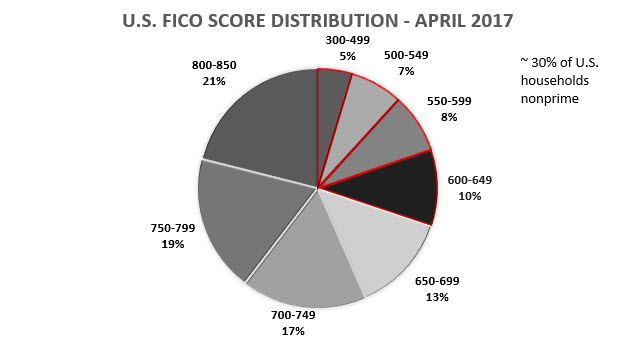

Most loans in the used auto finance space are extended to nonprime consumers, who comprise a significant portion of the U.S. population. Of the more than 300 million Americans with a credit history, 30% have Fair Isaac Corporation (FICO®) scores below 650. Although nonprime auto loans typically produce higher losses than prime loans, the Company's data-driven approach, extensive experience, and adaptive platform enhance the Company's ability to estimate future cash flows and effectively price loans for their inherent risk.

Source: FICO® Banking Analytics Blog Fair

Note: Nonprime based on FICO® Score <650

7

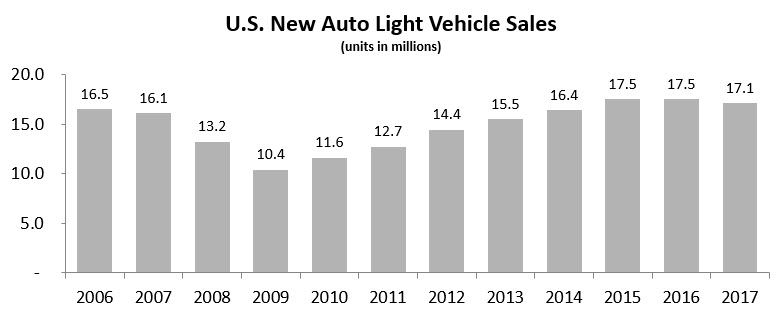

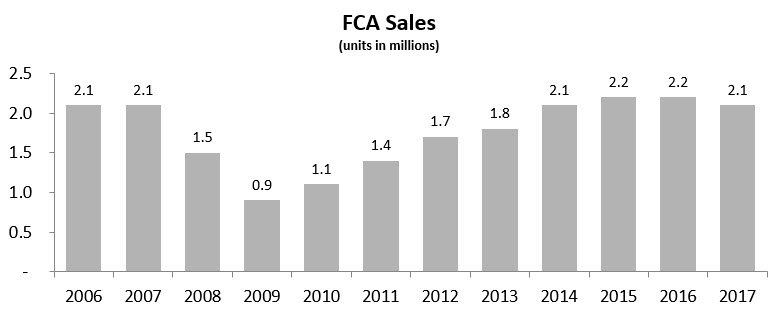

Through the Chrysler Capital brand, the Company is increasing its focus on the new auto finance space by providing financing for the acquisition of new FCA vehicles. In 2017, there were 17.1 million new cars sold in the U.S. In 2017, through the third quarter, approximately 86% of total new auto sales were financed. Future growth of new auto sales in the United States, and the parallel growth of consumer loans and leases to finance those sales, are driven by improving economic conditions, new automobile product offerings, and the need to replace aging automobiles. The average age of U.S. autos in 2017 remained at a record high of 11.6 years, which was reached in 2016 (Source: IHS Automotive/R. L. Polk Annual Press Release). Chrysler Capital loan and lease growth will be driven by the volume of new FCA vehicles sold in the United States.

Source: Ward's Automotive Reports; U.S. Department of Commerce: Bureau of Economic Analysis

Source: FCA US LLC

8

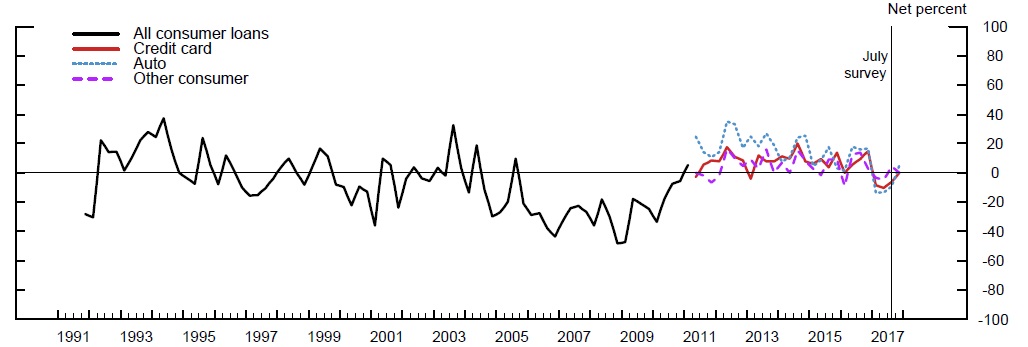

The Company is a leading originator of nonprime auto loans. National and regional banks have historically been the largest originators of used and nonprime vehicle loans and leases due to their broad geographic footprint and wide array of vehicle finance products. The Company primarily competes against national and regional banks, as well as automobile manufacturers’ captive finance businesses, to originate loans and leases to finance consumers’ purchases of new and used cars. The Company has a significant portfolio of prime loans and leases serviced for others, as it typically originates and then sells prime assets with servicing rights retained.

Net Percent of Banks Reporting Stronger Demand for Consumer Loans

Source: Federal Reserve Board - Senior Loan Officer Survey on Bank Lending Practices

In 2015, the Company made a strategic decision to exit the personal lending market to focus on its core objectives of expanding the reach and realizing the full value of its vehicle finance and serviced for others platforms. The Company believes this shift will create other opportunities, such as diversifying funding sources and growing capital. Throughout 2016 and 2017, the Company marketed personal lending assets to potential buyers. On February 1, 2016, the Company completed a sale of substantially all assets from its personal lending portfolio to an unrelated third party. On April 14, 2017, the Company sold the remaining portfolio comprised of personal installment loans to an unrelated third-party. The portfolio was comprised solely of LendingClub installment loans. Additionally, on March 24, 2016, the Company notified certain retailers that it would no longer fund new point-of-sale credit originations effective April 11, 2016. As the Company refocuses on core objectives, it continues to perform under various other agreements under which specified volumes of personal loans originated by third parties are purchased.

In both the vehicle finance and personal lending markets, the Company generates originations indirectly and directly. The indirect model requires relationships with third parties who are generally active in the market, are looking for an additional source of financing for their customers, and agree to direct certain customers to the Company. The direct model requires an internally-managed platform through which consumers are able to make requests for credit directly to the Company. While the Company has historically focused on the indirect model, it has a presence in the direct vehicle finance market through the RoadLoans.com platform. Additionally, the Company continues to develop relationships with third parties to further broaden its origination channels.

The Company's Business Strategy

The Company's primary goal is to create stockholder value by leveraging its efficient, scalable technology and risk infrastructure and data to underwrite, originate and service profitable assets while treating customers, dealers, stockholders, employees and all stakeholders in a simple, personal and fair manner.

Expand the Company's Vehicle Finance Franchise

Organic Growth in Indirect Auto Finance. The Company has extensive data on and experience with consumer behavior across the full credit spectrum and is a key player in the U.S. vehicle finance market. The Company expects to continue to increase market penetration in the vehicle finance sector, subject to favorable market conditions, via the number and depth of its dealer relationships. The Company plans to achieve this growth in part through alliance programs with national vehicle dealer groups and financial institutions, including banks, credit unions, and other lenders, in both the prime and nonprime vehicle finance markets. The Company's technology-based platform enables the Company to integrate seamlessly with other originators and thereby benefit from their channels and brands.

9

Growth in Direct-to-Consumer Exposure. The Company is working to further diversify its vehicle finance product offerings by expanding its web-based, direct-to-consumer offerings. The Company is focused on engaging the consumer at the early stages of the car buying experience. The RoadLoans.com program is a preferred finance resource for many major vehicle shopping websites, including Cars.com and AutoTrader.com, each of which have links on their websites promoting RoadLoans.com for financing. The Company will continue to focus on securing relationships with additional vehicle-related websites. The Company anticipates that the next generation of its web-based direct-to-consumer offerings will include additional strategic relationships, an enhanced online experience, and additional products and services to assist with all stages of the vehicle ownership life cycle, including research, financing, buying, servicing, selling, and refinancing.

Expansion of Fee-Based Income Opportunities. The Company seeks opportunities to leverage its technologically sophisticated and highly adaptable servicing platform for both prime and nonprime loans, as well as other vehicle finance (including recreational and marine vehicles) and personal lending products. The Company collects fees to service loan portfolios for third parties, and handles both secured and personal loan products across the full credit spectrum. Loans and leases sold to or sourced to banks through flow agreements and off-balance sheet securitizations also provide additional opportunities to service large vehicle loan and lease pools. The Company's loan servicing business is scalable and provides an attractive return on equity. The Company intends to continue to expand fee-based income opportunities through its relationship with Santander.

The Company's Products and Services

The Company offers vehicle-related financing products, primarily consisting of consumer loans and leases, and servicing of those assets.

Consumer Vehicle Loans

The Company's primary business is to indirectly originate vehicle loans through automotive dealerships throughout the United States. The Company has a substantial dealer network, most of which consists of manufacturer-affiliated or large and reputable independent dealers. The Company uses a risk-adjusted methodology to determine the price to pay the automotive dealer for a loan, which may be above or below the principal amount of the loan depending on characteristics such as the contractual annual percentage rate (APR) and the borrower’s credit profile. The consumer is obligated to make payments in an amount equal to the principal amount of the loan plus interest at the APR negotiated with the dealer. The consumer is also responsible for charges related to past-due payments. Dealers may retain some portion of the finance charge as compensation. The Company's agreements with dealers place a limit on the amount of the finance charges they are entitled to retain. Although the Company does not own the vehicles it finances through loans, it holds a perfected security interest in those vehicles. Loans with below-market APRs are frequently offered through manufacturer incentive programs. The manufacturer will compensate the originator of these loans for the amount of the financing rate that is below market. These payments are called rate subvention. The Company is entitled to receive rate subvention payments from FCA as its preferred provider through the Chrysler Agreement.

Since 2008, the Company has also directly originated loans through its branded online RoadLoans.com platform. Additionally, the Company has acquired loans in bulk from third parties. The loans acquired in bulk acquisitions have primarily been collateralized by automobiles. However, a small amount of such loans have been collateralized by marine and recreational vehicles. The Company generates revenue on these loans through finance charges.

Vehicle Leases

The Company acquires leases primarily from FCA-affiliated automotive dealers and, as a result, becomes titleholder for leased vehicles. The acquisition cost for these leases is based on the underlying value of the vehicle, the contractual lease payments and the residual value, which is the expected future value of the vehicle at the time of the lease termination. The Company uses projected residual values that are estimated by third parties, such as Automotive Lease Guide (ALG) and internal forecasts based on current market conditions, and other relevant data points. The residual value used to determine lease payments, or the contractual residual value, may be adjusted upward as part of marketing incentives provided by the manufacturer of the vehicle. When a contractual residual value is written up, the lease payments the Company offers become more attractive to consumers. The marketing incentive payment that manufacturers pay the Company is equal to the expected difference between the projected ALG residual value and the contractual residual value. This residual support payment is a form of subvention. The Company is a preferred provider of subvented leases through Chrysler Capital. Substantially all of these leases are to prime consumers. The consumer, or lessee, is responsible for the contractual lease payments and any excessive mileage or wear and tear on the vehicle that results in a lower residual value of the vehicle at the time of the lease’s termination. The consumer is also generally responsible for charges related to past due payments. The Company's leases are primarily closed-ended, meaning the consumer does not bear the residual risk.

10

The Company generates revenue on leases through monthly lease payments and fees and, depending on the market value of the off-lease vehicle, the Company may recognize a gain or loss upon remarketing. The Company's agreement with FCA permits the Company to share any residual losses over a threshold, determined on an individual lease basis, with FCA.

Servicing for Others

The Company services a portfolio of vehicle loans originated or otherwise independently acquired by SBNA, vehicle leases originated by SBNA under terms of a flow agreement and loans sold by the Company to Santander. The Company also services loans sold through flow agreements, through Chrysler Capital off-balance sheet securitizations and several smaller loan portfolios for various third-party institutions. The Company generates revenue on these assets through servicing and other fees collected from the institutional owners and the borrowers, and may also generate a gain or loss on the sale of assets. The Company intends to continue growing this off-balance sheet portfolio and the stream of revenue it provides.

Origination and Servicing

Vehicle Finance

The Company's origination platform delivers automated 24/7 underwriting decision-making through a proprietary credit-scoring system designed to provide consistency and efficiency, with dealers receiving a decision in under ten seconds for 95% of all requests. Every loan application received is processed by the Company's credit scoring system. The Company's credit- scoring system is supported by an extensive market database that includes multiple years of historical data on the loans that the Company has acquired as well as extensive consumer finance third-party data. The Company continuously evaluates loan performance and consumer behavior to improve underwriting decisions. The Company's systems are intended to be readily adaptable and scalable, with the ability to quickly implement changes in pricing and scoring credit policy rules and modify underwriting standards to match the economic environment. The Company's credit-scoring system supports underwriting decisions for consumers across the full credit spectrum and has been designed to allow the Company to maximize modeled risk-adjusted yield for a given consumer’s credit profile.

The Company has built a servicing approach based on years of experience as a nonprime lender. The Company's servicing activities consist largely of processing customer payments, responding to customer inquiries (such as requests for payoff quotes or complaints), processing customer requests for account revisions (such as payment deferrals), seeking to maintain a perfected security interest in the financed vehicle, monitoring vehicle insurance coverage, pursuing collection of delinquent accounts, and remarketing repossessed or off-lease vehicles. The Company has made significant investments in staffing and servicing systems technology intended to make servicing activities compliant with federal and local consumer lending rules in all 50 states.

Through its servicing platform, the Company seeks to maximize collections while providing outstanding customer service. The Company's servicing practices are closely integrated with the originations platform, resulting in an efficient exchange of customer related data, market information and understanding of the latest trends in consumer behavior. The customer account management process is model-driven and utilizes predictive customer service and collection strategies. The Company validates its models with data back-testing and can be adjusted to reflect new information received throughout the Company, such as new vehicle loan and lease applications, refreshed consumer credit data, and consumer behavior observed through servicing operations. The Company's robust processes and sophisticated technology support the servicing platform to maximize efficiency, consistent loan treatment, and cost control.

To provide the best possible customer service, the Company provides multiple convenient customer communication methods and has implemented strategies to monitor and improve the customer experience. In addition to live agent assistance, the Company's customers are offered a wide range of self-service options via an interactive voice response system and through its customer website. Self-service options include demographic management (such as updating a customer’s address, phone number, and other identifying information), payment and payoff capability, and payment history reporting, as well as online chat and communication requests. Quality assurance teams perform account reviews and are responsible for grading phone calls to monitor adherence to policies and procedures as well as compliance with regulatory requirements. The Company's analytics software converts speech from every call into text so that each conversation with a customer can be analyzed and subsequently data-mined. This is used to identify inappropriate words or phrases in real-time for potential intervention from a manager and to search for the omission of words or phrases that are required for specific conversations. A quality control team provides an independent, objective assessment of the servicing department’s internal control systems and underlying business processes. These processes help identify organizational improvements while protecting the Company's franchise reputation and brand. Lastly, complaint tracking processes are designed to ensure customer complaints are addressed appropriately and that the customers receive status updates. These systems assign the account to a specialized team until the complaint is deemed to be closed. This team tracks and resolves customer complaints and is subject to a robust quality assurance program.

11

The servicing process is divided into stages based on delinquency status and the servicing agents for each stage receive specialized training. In the event that a retail installment contract becomes delinquent, the Company follows an established set of procedures that maximizes ultimate recovery on the loan or lease. Late stage account managers employ skip tracing, utilize specialized negotiation skills, and are trained to tailor their collection attempts based on the proprietary borrower behavioral score assigned to each customer. Collection efforts include calling generally within one business day when an obligor has broken a promise to make a payment on a certain date, and using alternative methods of contact such as location gathering via references, employers, landlords, credit bureaus, and cross-directories. If the borrower is qualified, the account manager may offer an extension of the maturity date, a temporary reduction in payment, or a modification permanently lowering the interest rate or principal. If attempts to work with the customer to cure the delinquency are unsuccessful, the customer is sent a “right to cure” letter in accordance with state laws, and the loan is assigned a risk score based on the Company's historical days-to-repossess data. This score is used to prioritize repossessions, and each repossession is systematically assigned to a third-party repossession agent according to the agent's recent performance. Once the vehicle has been secured, any repairs required are performed and the vehicle is remarketed as quickly as possible, typically through an auction process.

Most of the Company's servicing processes and quality-control measures serve a dual purpose in that they are both designed to ensure that the Company complies with applicable laws and regulations and that the Company delivers the best possible customer service. Additionally, the servicing platform and all of the features offered to customers are scalable and can be tailored through statistical modeling and automation.

The Company's Relationship with FCA

In February 2013, the Company entered into the Chrysler Agreement, pursuant to which the Company became the preferred provider for FCA’s consumer loans and leases and dealer loans effective May 1, 2013. Business generated under terms of the Chrysler Agreement is branded as Chrysler Capital. During 2017, the Company originated more than $6.7 billion of Chrysler Capital retail installment contracts and approximately $6.0 billion of Chrysler Capital vehicle leases.

The Chrysler Agreement requires, among other things, that the Company bears the risk of loss on loans originated pursuant to the agreement, but also that FCA shares in residual gains and losses from consumer leases over a threshold, determined on an individual lease basis. The agreement also requires that Santander maintain at least $5.0 billion in funding available for dealer inventory financing and $4.5 billion of financing dedicated to FCA retail financing. In turn, FCA must provide designated minimum threshold percentages of its subvention business to the Company.

The Chrysler Agreement has a ten-year term, subject to early termination in certain circumstances, including the failure by either party to comply with certain of their ongoing obligations. These obligations include, for the Company, meeting specified escalating penetration rates for the first five years, and, for FCA, treating the Company in a manner consistent with comparable OEMs' treatment of their captive providers, primarily regarding sales support. In addition, FCA may also terminate the agreement if, among other circumstances, (i) a person other than Santander and its affiliates or its other stockholders owns 20% or more of its common stock and Santander and its affiliates own fewer shares of common stock than such person, (ii) the Company becomes, controls, or becomes controlled by, an OEM that competes with Chrysler, or (iii) if certain of the Company's credit facilities become impaired.

In connection with entering into the Chrysler Agreement, the Company paid FCA a $150 million upfront, nonrefundable fee on May 1, 2013. This fee is considered payment for future profits generated from the Chrysler Agreement. Accordingly, the Company amortizes the Chrysler Agreement over the expected ten-year term as a component of net finance and other interest income. The Company has also executed an Equity Option Agreement with FCA, whereby FCA may elect to purchase, at any time during the term of the Chrysler Agreement, at fair market value, an equity participation of any percentage in the Chrysler Capital portion of the Company's business.

For a period of 20 business days after FCA's delivery to the Company of a notice of intent to exercise its option, the Company is to discuss with FCA, in good faith, the structure and valuation of the proposed equity participation. If the parties are unable to agree on a structure and FCA still intends to exercise its option, the Company will be required to create a new company into which the Chrysler Capital assets will be transferred and which will own and operate the Chrysler Capital business. If FCA and the Company cannot agree on a fair market value during the 20-day negotiation period, each party will engage an investment bank and the appointed banks will mutually appoint a third independent investment bank to determine the value, with the cost of the valuation divided evenly between FCA and the Company. Each party has the right to a one-time deferral of the independent valuation process for up to nine months. FCA will have a period of 90 days after a valuation has been determined, either by negotiation between the parties or by an investment bank, to deliver a binding notice of exercise. Following this notice, FCA's purchase is to be paid and settled within 10 business days, subject to a delay of up to 180 days if necessary to obtain any required consents from governmental authorities.

12

Any new company formed to effect FCA's exercise of its equity option will be a Delaware limited liability company unless otherwise agreed to by the parties. As long as each party owns at least 20% of the business, FCA and the Company will have equal voting and governance rights without regard to ownership percentage. If either party has an ownership interest in the business of less than 20%, the party with less than 20% ownership will have the right to designate a number of directors proportionate to its ownership and will have other customary minority voting rights.

Because the equity option is exercisable at fair market value, the Company could recognize a gain or loss upon exercise if the fair market value is determined to be different from book value. The Company believes that the fair market value of its Chrysler Capital financing business currently exceeds book value and therefore has not recorded a contingent liability for potential loss upon FCA's exercise.

Subsequent to the exercise of the equity option, the Company's rights under the Chrysler Agreement would be assigned to the jointly owned business. Exercise of the equity option would be considered a triggering event requiring re-evaluation of whether or not the remaining unamortized balance of the upfront fee the Company paid to FCA on May 1, 2013 should be impaired.

Until January 31, 2017, the Company had a flow agreement with Bank of America whereby the Company was committed to sell a contractually determined amount of eligible Chrysler Capital loans to Bank of America on a monthly basis, depending on the amount and credit quality of eligible current month originations and prior month sales. The agreement originally extended through May 31, 2018. On July 27, 2016, the flow agreement was amended to reduce the maximum commitment to sell eligible loans each month to $300,000. On October 27, 2016, Bank of America notified the Company that it was terminating the flow agreement effective January 31, 2017, and accordingly, the flow agreement is now terminated. For loans sold under the agreement, the Company retains the servicing rights at contractually agreed-upon rates. The Company may also receive or pay a servicer performance payment based on an agreed-upon formula if performance on the sold loans is better or worse, respectively, than expected performance at the time of sale.

The Company has sold loans to Citizens Bank of Pennsylvania (CBP) under terms of a flow agreement and other predecessor sale agreements. The Company retains servicing on the sold loans and will owe CBP a loss-sharing payment capped at 0.5% of the original pool balance if losses exceed a specified threshold, established on a pool-by-pool basis. On June 25, 2015, the Company executed an amendment to the servicing agreement with CBP, which increased the servicing fees. This amendment amended the flow agreement between CBP and the Company, effective August 1, 2015, to reduce CBP's committed purchases of Chrysler Capital prime loans from a maximum of $600 million and a minimum of $250 million per quarter to a maximum of $200 million and a minimum of $50 million per quarter. On February 13, 2017, the Company and CBP entered into a mutual agreement to terminate the flow agreement effective May 1, 2017.

Segments

The Company has one reportable segment: Consumer Finance, which includes the Company's vehicle financial products and services, including retail installment contracts, vehicle leases, and dealer loans, as well as financial products and services related to motorcycles, RVs, and marine vehicles. It also includes the Company's personal loan and point-of-sale financing operations.

Subsidiaries

The Company has two principal consolidated wholly-owned subsidiaries: Santander Consumer USA Inc. and Santander Consumer International Puerto Rico, LLC (a wholly-owned subsidiary of Santander Consumer USA Inc.).

Employees

At December 31, 2017, the Company had approximately 5,076 employees, none of whom are represented by a collective bargaining agreement.

Geographic Financial Information

For the years ended December 31, 2017, 2016 and 2015, all of the Company's revenues were derived from the United States. As of December 31, 2017 and 2016, all of the Company's long-lived assets were located in the United States.

Seasonality

The Company's origination volume is generally highest in March and April each year due to consumers receiving tax refunds, which provides additional discretionary income. The Company's delinquencies are generally highest in the period from November through January due to consumers’ holiday spending, which reduces income available for car payments.

13

Intellectual Property

The Company has the right to use the Santander name on the basis of a non-exclusive, royalty-free, and non-transferable license from Santander, which only extends to uses in connection with the Company's current and future operations within the United States. Santander may terminate the license at any time Santander ceases to own, directly or indirectly, 50% or more of the Company's common stock.

In connection with the Company's agreement with FCA, the Company has been granted a limited, non-exclusive, non-transferable, royalty-free license to use certain FCA trademarks, including the term “Chrysler Capital,” for as long as the Chrysler Agreement is in effect. The Company is required to adhere to specified guidelines and other usage instructions related to these trademarks, as well as to obtain prior written approval of any materials, including financing documents and promotional materials, using the trademarks. This license does not grant the Company any ownership rights in FCA's trademarks.

In connection with the 2008 acquisition of Roadloan.com, a direct-to-consumer online platform, the Company purchased the "Roadloan.com" trade name which constitutes an intellectual property right.

Competition

The automotive finance industry is highly competitive. The Company competes on the pricing offered on loans and leases as well as the customer service provided to automotive dealer customers. Pricing for these loans and leases is transparent because the Company, along with industry competitors, posts pricing for loans and leases on web-based credit application aggregation platforms. When dealers submit applications for consumers acquiring vehicles, they can compare the Company's pricing against competitors’ pricing. Dealer relationships are important in the automotive finance industry. Vehicle finance providers tailor product offerings to meet each individual dealer’s needs.

The Company seeks to effectively compete through its proprietary credit-scoring system and industry experience, which are used to establish appropriate risk pricing. In addition, the Company benefits from FCA subvention programs through the Chrysler Agreement. The Company seeks to develop strong dealer relationships through a nationwide sales force and a long history in the automotive finance space. Further, the Company expects to continue deepening dealer relationships through the Chrysler Capital product offerings.

The Company's primary competitors in the vehicle finance space are:

• | national and regional banks; |

• | credit unions; |

• | independent financial institutions; and |

• | the affiliated finance companies of automotive manufacturers. |

While the used car financing market is fragmented with no single lender accounting for more than 10% of the market, there are a number of competitors in both the new and used car markets that have substantial positions nationally or in the markets in which they operate. Some of the Company's competitors may have lower cost structures, or funding costs, and be less reliant on securitizations. The Company believes it can compete effectively by continuing to expand and deepen its relationships with dealers. In addition, through its Chrysler Capital brand, the Company benefits from FCA’s subvention programs and relationships with its dealers.

Supervision and Regulation

The U.S. lending industry is highly regulated under various U.S. federal laws, including the Truth-in-Lending Act (TILA); Equal Credit Opportunity Act (ECOA), Electronic Fund Transfer Act (EFTA), Fair Credit Reporting Act (FCRA), Fair Debt Collection Practices Act (FDCPA), Consumer Leasing Act, Servicemembers Civil Relief Act (SCRA), Telephone Consumer Protection Act, Financial Institutions Reform, Recovery, and Enforcement Act, Dodd-Frank Act and Gramm-Leach-Bliley Act (GLBA), as well as various state laws. The Company is subject to inspections, examinations, supervision, and regulation by the Securities and Exchange Commission (SEC), the Consumer Financial Protection Bureau (CFPB), the Federal Trade Commission (FTC), and the Department of Justice (DOJ) and by regulatory agencies in each state in which the Company is licensed. In addition, the Company is directly and indirectly, through its relationship with SHUSA, subject to certain banking and financial services regulations, including oversight by the Office of the Comptroller of the Currency (OCC), the European Central Bank (ECB), and the Federal Reserve Bank of Boston (FRBB), which has the ability to limit certain of its activities, such as the timing and amount of dividends and certain transactions that it might otherwise desire to enter into, such as merger and acquisition opportunities, or to impose other limitations on the Company's growth. Additional legal and regulatory matters affecting the Company’s activities are further discussed in Part I, Item 1A—Risk Factors of this Annual Report on Form 10-K.

14

Dodd-Frank Wall Street Reform and Consumer Protection Act

Congress enacted comprehensive financial regulatory reform legislation on July 21, 2010. A significant focus of the new law (the Dodd-Frank Act) is heightened consumer protection. The Dodd-Frank Act established the CFPB, which has regulatory, supervisory, and enforcement powers over providers of consumer financial products and services, including the Company, and explicit supervisory authority to examine and require registration of non-depository lenders and promulgate rules that can affect the practices and activities of lenders. Although the Dodd-Frank Act expressly provides that the CFPB has no authority to establish usury limits, some consumer advocacy groups have suggested that various forms of alternative financial services or specific features of consumer loan products should be a regulatory priority. It is possible that at some time in the future the CFPB could propose and adopt rules making such lending services materially less profitable or impractical, which may impact finance loans or other products that the Company offers.

In addition to granting certain regulatory powers to the CFPB, the Dodd-Frank Act gives the CFPB authority to pursue administrative proceedings or litigation for violations of federal consumer financial laws. In these proceedings, the CFPB can obtain cease and desist orders (which can include orders for restitution or rescission of contracts, as well as other kinds of affirmative relief) and monetary penalties.

The Company is also subject to risk retention rules promulgated under the Dodd-Frank Act, which generally require sponsors of Asset Backed Securitizations (ABS) to retain at least five percent of the credit risk of the assets collateralizing the ABS issuance. The rules also prohibit the transfer or hedging of the credit risk that the sponsor is required to retain.

Dividend Restrictions

The Dodd-Frank Act also requires certain banks and bank holding companies, including SHUSA, to perform a stress test and submit a capital plan to the FRBB on an annual basis and to receive a notice of non-objection, or approval, to the plan from the FRBB before taking capital actions, such as paying dividends, implementing common equity repurchase programs, or redeeming or repurchasing capital instruments. In June 2017, SHUSA announced that the FRBB did not object to the planned capital actions described in SHUSA’s 2017 Capital Plan that was submitted as part of its annual CCAR submissions. Included in SHUSA’s capital actions were proposed dividend payments for the Company’s stockholders. As a result, we made a dividend payment in 2017 and in February 2018 and, subject to Board approval, plan to pay a dividend in the second quarter of 2018.

Regulation AB II

The Company is subject to final rules adopted by SEC known as "Regulation AB II". Regulation AB II, among other things, expanded ABS disclosure requirements and modified the offering and shelf registration process. All offerings of publicly registered ABS and all reports under the Exchange Act for outstanding publicly registered ABS must comply with these rules and disclosure requirements.

Additional legal and regulatory matters affecting the Company’s activities are further discussed in Part I, Item 1A—Risk Factors.

Disclosure Pursuant to Section 219 of the Iran Threat Reduction and Syria Human Rights Act

Pursuant to Section 219 of the Iran Threat Reduction and Syria Human Rights Act of 2012, which added Section 13(r) to the Securities Exchange Act of 1934, as amended (the Exchange Act), an issuer is required to disclose in its annual or quarterly reports, as applicable, whether it or any of its affiliates knowingly engaged in certain activities, transactions or dealings relating to Iran or with individuals or entities designated pursuant to certain Executive Orders. Disclosure is generally required even where the activities, transactions or dealings were conducted in compliance with applicable law.

The following activities are disclosed in response to Section 13(r) with respect to Santander UK and certain other affiliates of Santander (collectively, the Group). During the period covered by this annual report:

• | Santander UK holds two savings accounts and one current account for two customers resident in the U.K. who are currently designated by the U.S. under the Specially Designated Global Terrorist (SDGT) sanctions program. Revenues and profits generated by Santander U.K. on these accounts in the year ended December 31, 2017 were negligible relative to the overall profits of Santander. |

• | Santander UK holds two frozen current accounts for two U.K. nationals who are designated by the U.S. under the Specially Designated Global Terrorist (SDGT) sanctions program. The accounts held by each customer have been frozen since their designation and have remained frozen through 2017. The accounts are in arrears (£1,844.73 in debit |

15

combined) and are currently being managed by Santander UK Collections & Recoveries department. No revenues or profits were generated by Santander UK on these accounts in the year ended December 31, 2017.

The Group also has certain legacy performance guarantees for the benefit of Bank Sepah and Bank Mellat (stand-by letters of credit to guarantee the obligations - either under tender documents or under contracting agreements - of contractors who participated in public bids in Iran) that were in place prior to April 27, 2007.

In the aggregate, all of the transactions described above resulted in gross revenues and net profits in the year ended December 31, 2017, which were negligible relative to the overall revenues and profits of Santander. The Group has undertaken significant steps to withdraw from the Iranian market such as closing its representative office in Iran and ceasing all banking activities therein, including correspondent relationships, deposit taking from Iranian entities and issuing export letters of credit, except for the legacy transactions described above. The Group is not contractually permitted to cancel these arrangements without either (i) paying the guaranteed amount (in the case of the performance guarantees), or (ii) forfeiting the outstanding amounts due to it (in the case of the export credits). As such, the Group intends to continue to provide the guarantees and hold these assets in accordance with company policy and applicable laws.

Available Information

All reports filed electronically by the Company with the SEC, including Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q, and Current Reports on Form 8-K, as well as any amendments to those reports, are accessible on the SEC’s website at www.sec.gov. These forms are also accessible at no cost on the Company’s website at www.santanderconsumerusa.com. The information contained on the Company's website is not being incorporated herein.

16

ITEM 1A. | RISK FACTORS |

The Company is subject to a number of risks that could materially and adversely affect our business, financial condition and results of operations in addition to other possible adverse consequences. We operate in a continually changing business and regulatory environment and, therefore, new risks emerge from time to time. The following are the risks of which we are currently aware that could be material to our business.

Risks Related to our Business

Legal, Regulatory and Compliance Risks

We operate in a highly regulated industry and continually changing federal, state, and local laws and regulations could materially and adversely affect our business, financial condition and results of operations.

Due to the highly regulated nature of the consumer finance industry, we are required to comply with a wide and changing array of federal, state and local laws and regulations, including a significant number of banking, fair lending, consumer protection laws and anti-money laundering laws. These laws and regulations directly impact our origination and servicing operations and almost all other aspects of our business and require constant compliance, monitoring, and internal and external audits. Although we have an enterprise-wide compliance framework structured to continuously monitor our activities, compliance with applicable laws and regulations is costly, may create operational constraints and may not always be effective or perform as expected.

The enactment of new laws and regulations, including with respect to consumer financial protection measures and systematic risk oversight authority, could occur rapidly and unpredictably and could require us to change our business or operations, resulting in a loss of revenue or a reduction in our profitability. New laws and regulations could also result in financial loss due to regulatory fines or penalties, restrictions or suspensions of business, or costs associated with compliance or mandatory corrective action as a result of failure to adhere to applicable laws, regulations and supervisory guidance. Failure to comply with these laws and regulations could also give rise to regulatory sanctions, customer rescission rights, actions by state and local attorneys general, civil or criminal liability or damage to our reputation.

The volume, granularity, frequency and scale of regulatory and other reporting requirements necessitate a clear data strategy to enable consistent data aggregation, reporting and management. Inadequate management information systems or processes, including those relating to risk data aggregation and risk reporting, could lead to a failure to meet regulatory reporting requirements, or other internal or external information demands, and we may face supervisory measures or other liability as a result.

We are or may become involved in investigations, examinations and proceedings by government and self-regulatory agencies, which may materially and adversely affect our business, financial condition and results of operations.

From time to time, we are or may become involved in formal and informal reviews, investigations, examinations, proceedings and information-gathering requests by federal and state government and self-regulatory agencies, including, among others, the FRBB, the CFPB, the DOJ, the SEC, the FTC and various state regulatory and enforcement agencies. Given the inherent uncertainty involved in such matters, and the potentially large or indeterminate damages sought, there can be significant uncertainty regarding the liability we may incur as a result of these matters. The finding, or even the assertion of, legal liability against us could materially and adversely affect our business, financial condition and results of operations and may result in, among other actions, adverse judgments, significant settlements, fines, penalties, injunctions or substantial reputational harm.

We are and have been subject to such matters by many of these regulators in the past and have paid significant fines or provided significant other relief. We expect that regulators will continue to initiate new investigations or regulatory actions in the future and that we will continue to devote resources to complying with the requirements of consent orders, adverse judgments and other settlements to which we are subject.

We are subject to enhanced legal and regulatory scrutiny regarding credit bureau reporting and debt collection practices from regulators, courts and legislators.

Our balance sheet consists of predominantly nonprime consumers, which are associated with higher than average delinquency rates and charge-offs than prime consumers. Accordingly, we have significant involvement with credit bureau reporting and the collection and recovery of delinquent and charged-off debt, primarily through customer communications, the filing of litigation against customers in default, the periodic sale of charged-off debt and vehicle repossession. We are subject to enhanced legal

17

and regulatory scrutiny regarding credit bureau reporting and debt collection practices from regulators, courts and legislators. Any future changes to our business practices in these areas, including our debt collection practices, whether mandated by regulators, courts, legislators or otherwise, or any legal liabilities resulting from our business practices, including our debt collection practices, could materially and adversely affect our business, financial condition and results of operations.

We are subject to certain banking regulations that limit our business activities and may restrict our ability to pay dividends and enter into certain business transactions.

Because our controlling shareholder, SHUSA, is a bank holding company and because we provide third party services to banks, we are directly and indirectly subject to certain banking and financial services regulations, including oversight by the FRBB, the ECB and the OCC. We also are subject to oversight by the CFPB. Such regulations and oversight could limit the activities and the types of businesses that we may conduct. The FRBB has broad enforcement authority over bank holding companies and their subsidiaries. The FRBB could exercise its power to restrict SHUSA from having a non-bank subsidiary that is engaged in any activity that, in the FRBB’s opinion, is unauthorized or constitutes an unsafe or unsound business practice, and could exercise its power to restrict us from engaging in any such activity. This power includes the authority to prohibit or limit the payment of dividends if, in the FRBB’s opinion, such payment would constitute an unsafe or unsound practice. Moreover, certain banks and bank holding companies, including SHUSA, are required to perform a stress test and submit a capital plan to the FRBB on an annual basis, and to receive a notice of non-objection, or approval, to the plan from the FRBB before taking capital actions, such as paying dividends, implementing common equity repurchase programs, or redeeming or repurchasing capital instruments. Any future suspension of our ability to pay dividends or other limitations placed on us by the FRBB, the ECB or any other regulator and additional costs associated with regulatory compliance could materially and adversely affect us and the trading price of our common stock.

For example, due to the FRBB’s objections, based on qualitative concerns, in 2014, 2015 and 2016 to SHUSA’s capital plan submissions, we were prohibited from paying dividends until the FRBB issued a non-objection to SHUSA's next capital plan submission or otherwise approved a planned dividend payment. Also, in 2014, SHUSA and the FRBB entered into an agreement prohibiting SHUSA from allowing any of its non-wholly-owned non-bank subsidiaries, including us, to declare or pay any dividend, or to make any capital distribution, without the prior written approval of FRBB. Although the 2014 agreement was terminated in 2017 and we paid a dividend in November 2017 and in February 2018, there can be no assurance that SHUSA will not enter into similar agreements in the future or that other restrictions on the payment of dividends will not apply to us in the future.

SHUSA and the Company also are subject to stringent oversight by the FRBB due to the FRBB’s prior objections to SHUSA’s capital plan submissions, and SHUSA has made a concentrated effort to improve its and its subsidiaries' governance, oversight and internal controls, policies, procedures and functions, including as they relate to us. We have incurred, and expect to continue to incur, significant costs in connection with ensuring compliance with, and assisting SHUSA in, the CCAR process.

The FRBB, the ECB or any other regulator may also impose substantial fines and other penalties for violations that we may commit or disallow acquisitions or other activities we may contemplate, which may limit our future growth plans. These limitations could place us at a competitive disadvantage because some of our competitors are not subject to these limitations.

We are subject to enhanced prudential standards as a subsidiary of SHUSA, which could materially and adversely affect our business, financial condition and results of operations.

As a subsidiary of SHUSA, we are subject to certain enhanced prudential rules mandated by Section 165 of the Dodd-Frank Act. Among other requirements, these rules require SHUSA to maintain a sufficient quantity of highly liquid assets to survive a liquidity stress event and implement various liquidity-related corporate governance measures and imposes certain requirements, duties and qualifications for the risk committee and chief risk officers of SHUSA. SHUSA calculates its liquidity figures on a consolidated basis with certain of its subsidiaries, including us. As a result, our predicted performance under the liquidity stress event must be taken into account when SHUSA conducts its liquidity stress event analysis. Due to these requirements, we are required to have an increased amount of liquidity and will incur increased costs of funding and liquidity capacity, which could materially and adversely affect our business, financial condition and results of operations.

Our business, financial condition and results of operations may be materially and adversely affected upon our implementation of the revised capital requirements under the U.S. Basel III final rules.

SHUSA became subject to new federal banking regulations relating to capital, referred to as the U.S. Basel III final rules, beginning January 1, 2015. The U.S. Basel III final rules subject SHUSA to higher minimum risk-based capital ratios and a capital conservation buffer above these minimum ratios. SHUSA calculates its capital figures on a consolidated basis with certain of its subsidiaries, including us. Failure to comply with the capital buffer requirements, which become more stringent

18

until fully phased-in through January 2019, would result in restrictions on our ability to make capital distributions, including dividend payments and stock repurchases and redemptions, and to pay discretionary bonuses to executive officers.

If SHUSA were to fail to satisfy regulatory capital requirements, SHUSA, together with its subsidiaries, including us, may be subject to serious regulatory sanctions ranging in severity from being precluded from making acquisitions or engaging in new activities to becoming subject to informal or formal supervisory actions by the FRBB. If any of these were to occur, such actions could prevent us from successfully executing our business plan and could materially and adversely affect our business, financial condition and results of operations.

In June 2017, SHUSA announced that the FRBB did not object to the planned capital actions described in SHUSA’s 2017 Capital Plan that was submitted as part of its annual CCAR submissions. Included in SHUSA’s capital actions were proposed dividend payments for the Company’s stockholders. As a result, we made a dividend payment in November 2017 and in February 2018 and, subject to Board approval, plan to pay a dividend in the second quarter of 2018. However, there can be no assurance that the FRBB will not object to these or any of our other future planned capital actions, including as a result of the phasing-in of the more stringent capital requirements under the U.S. Basel III final rules.

The Dodd-Frank Act, and its associated rules and guidance, and CFPB supervisory audits will likely continue to increase our regulatory compliance burden and associated costs.

The Dodd-Frank Act introduced a substantial number of reforms that continue to reshape the tenor and structure of financial services industry regulation. In particular, the Dodd-Frank Act, among other things, created the CFPB, which is authorized to promulgate and enforce consumer protection regulations relating to financial products and services.

The CFPB continues to recommend that indirect vehicle lenders, a class that includes us, take steps to monitor and impose controls over dealer markup policies where dealers charge consumers higher interest rates as compensation for facilitating the loan, with the markup shared between the dealer and the lender. The CFPB has in the past, and continues to, conduct supervisory audits of large providers of vehicle financing, including us, with respect to possible ECOA “disparate impact” credit discrimination in indirect vehicle finance and other related matters. From 2013 to present, the CFPB and the DOJ have entered into consent orders, memoranda of understanding and settlements with multiple lenders pertaining to allegations of disparate impact regarding vehicle dealer markups, requiring lenders to revise their pricing and compensation systems to substantially reduce dealer discretion and other financial incentives to mark up interest rates and to pay restitution to borrowers as well as fines and penalties. For example, in November 2017, we entered into a confidential agreement with the CFPB to resolve an investigation regarding certain alleged violations by the Company of the ECOA.

If the CFPB continues to enter into consent decrees with lenders on disparate impact claims and related matters, it could negatively impact the business of the affected lenders, and potentially the business of dealers and other lenders in the vehicle finance market. This impact on dealers and lenders could increase our regulatory compliance requirements and associated costs. Unlike competitors that are banks, we are subject to the licensing and operational requirements of states and other jurisdictions, and our business would be adversely affected if we lost our licenses.

Unlike competitors that are banks, we are subject to the licensing and operational requirements of states and other jurisdictions, and our business would be adversely affected if we lost our licenses.

Because we are not a nationally-chartered depository institution, we do not benefit from exemptions to state loan servicing or debt collection licensing and regulatory requirements. To the extent that they exist, we must comply with state licensing and various operational compliance requirements in all 50 states and the District of Columbia. These include, among others, requirements regarding form and content of contracts, other documentation, collection practices and disclosures, and record keeping. We are sensitive to regulatory changes that may increase our costs through stricter licensing laws, disclosure laws or increased fees.

In addition, we are subject to periodic examinations by state and other regulators. The states that currently do not provide extensive regulation of our business may later choose to do so. The failure to comply with licensing or permit requirements and other local regulatory requirements could result in significant statutory civil and criminal penalties, monetary damages, attorneys’ fees and costs, possible review of licenses, and damage to reputation, brand and valued customer relationships.

We are subject to potential intervention by any of our regulators or supervisors.

As noted above, our business and operations are subject to increasingly significant rules and regulations applicable to conducting banking and financial services business. These apply to, among other things, financial reserves and financial reporting. These requirements are set by the relevant central banks and state and federal regulatory authorities that authorize, regulate and supervise us in the jurisdictions in which we operate.

19

In their supervisory roles, the regulators seek to maintain the safety and soundness of financial institutions and the financial system as a whole, with the aim of strengthening, but not guaranteeing, the protection of customers and the financial system. The supervisors' continuing supervision of financial institutions is conducted through a variety of regulatory tools, including the collection of information by way of prudential examinations and requests, reports obtained from skilled persons, visits to firms and regular meetings with management to discuss issues such as performance, risk management and strategy. In general, these regulators have a more outcome-focused regulatory approach that involves more proactive enforcement and more punitive penalties for infringement. As a result, we face increased supervisory intrusion and scrutiny (resulting in increasing internal compliance costs and supervision fees), and in the event we fail to meet regulatory obligations or expectations we are likely to face more stringent regulatory fines. Some of the regulators are focusing strongly on consumer protection and on conduct risk, and will continue to do so. This has included a focus on the design and operation of products, the treatment of customers and the operation of markets.

Some of the laws in the jurisdictions in which we operate give the regulators the power to make temporary product intervention rules either to improve a firm’s systems and controls in relation to product design, product management and implementation, or to address problems identified with financial products. These problems may potentially cause significant detriment to consumers because of certain product features or governance flaws or distribution strategies. Such rules may prevent institutions from entering into product agreements with customers until such problems have been solved. Some of the regulatory regimes in the relevant jurisdictions in which we operate require us to be in compliance across all aspects of our business, including the training, authorization and supervision of personnel, systems, processes and documentation. If we fail to be compliant with such regulations, there likely would be an adverse impact on our business from sanctions, fines or other actions imposed by the regulatory authorities.

Adverse outcomes to current and future litigation against us may materially and adversely affect our business, financial condition and results of operations.