Table of Contents

Filed Pursuant to Rule 424(b)(4)

Registration No. 333-189799

PROSPECTUS

6,296,098 American Depositary Shares

MiX TELEMATICS LIMITED

(incorporated in South Africa)

Representing 157,402,450 Ordinary Shares

This is the initial public offering of our American Depositary Shares, or “ADSs,” each of which represents 25 of our ordinary shares, no par value. The ADSs will be evidenced by American Depositary Receipts, or “ADRs.” Of the ADSs to be sold in the offering, we are selling 4,400,000 ADSs and the selling shareholders are selling 1,896,098 ADSs. We will not receive any of the proceeds from the ADSs being sold by the selling shareholders. The initial public offering price is $16.00 per ADS.

We are an “emerging growth company” under the federal securities laws.

Our ordinary shares are listed on the Johannesburg Stock Exchange (JSE Limited), or “JSE,” under the symbol “MIX.” On August 8, 2013, the closing price of our ordinary shares on the JSE was R6.00 per ordinary share, which is equivalent to $0.61 per ordinary share, based upon an exchange rate of R9.8878 to $1.00 on that date. The ADSs will trade, subject to notice of issuance, on The New York Stock Exchange, or “NYSE,” under the symbol “MIXT.”

Investing in the ADSs involves a high degree of risk. See “Risk Factors” beginning on page 13 of this prospectus for certain factors you should consider before investing in the ADSs.

| Per ADS |

Total | |||||||

| Initial public offering price |

$ | 16.00 | $ | 100,737,568.00 | ||||

| Underwriting discount |

$ | 1.12 | $ | 7,051,629.76 | ||||

| Proceeds to us (before expenses) |

$ | 14.88 | $ | 65,472,000.00 | ||||

| Proceeds to the selling shareholders (before expenses) |

$ | 14.88 | $ | 28,213,938.24 | ||||

The selling shareholders have granted the underwriters an option for a period of 30 days to purchase from them up to 944,414 additional ADSs to cover over-allotments, if any.

Neither the Securities and Exchange Commission nor any state securities commission nor the South African Financial Services Board has approved or disapproved of these securities or passed upon the adequacy or accuracy of this prospectus. Any representation to the contrary is a criminal offense.

Delivery of the ADSs will be made on or about August 14, 2013.

| RAYMOND JAMES | WILLIAM BLAIR |

| CANACCORD GENUITY | OPPENHEIMER & CO. |

Prospectus dated August 9, 2013

Table of Contents

Table of Contents

| 1 | ||||

| 13 | ||||

| 45 | ||||

| 47 | ||||

| 48 | ||||

| 49 | ||||

| 50 | ||||

| 51 | ||||

| 52 | ||||

| 53 | ||||

| MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS |

56 | |||

| 81 | ||||

| 96 | ||||

| 98 | ||||

| 113 | ||||

| 117 | ||||

| 119 | ||||

| 129 | ||||

| EXCHANGE CONTROLS AND OTHER LIMITATIONS AFFECTING SHAREHOLDERS |

137 | |||

| 139 | ||||

| 141 | ||||

| 153 | ||||

| 159 | ||||

| 160 | ||||

| 160 | ||||

| 160 | ||||

| 162 | ||||

| F-1 |

Until September 3, 2013 (25 days after the date of this prospectus), all dealers that buy, sell or trade in our ordinary shares in the form of ADSs, whether or not participating in this offering, may be required to deliver a prospectus. This is in addition to the dealer’s obligation to deliver a prospectus when acting as underwriters and with respect to their unsold allotments or subscriptions.

This offering is being made solely on the basis of the information contained in this prospectus. You should assume that the information appearing in this prospectus is accurate only as of the date on the front cover of this prospectus, regardless of the time of delivery of this prospectus or any sale of the ADSs. None of the selling shareholders, the underwriters or the Company has authorized anyone to provide any information other than that contained in this prospectus or in any free writing prospectus prepared by or on our behalf.

(i)

Table of Contents

This summary highlights information contained elsewhere in this prospectus. This summary does not contain all of the information you should consider before investing in our ADSs. You should read this entire prospectus carefully, especially the “Risk Factors” section of this prospectus and our consolidated financial statements and related notes appearing elsewhere in this prospectus, before making an investment decision. In this prospectus, unless otherwise indicated, “MiX,” “we,” “us,” “our,” “our company” and “Group” mean MiX Telematics Limited and its consolidated subsidiaries. Unless otherwise indicated, the “Company” means MiX Telematics Limited. Our fiscal year ends on March 31 and references to “fiscal year 2011” are to the fiscal year ended March 31, 2011, references to “fiscal year 2012” are to the fiscal year ended March 31, 2012 and references to “fiscal year 2013” are to the fiscal year ended March 31, 2013. References to “R” are to South African rand and references to “U.S. dollars” and “$” are to United States dollars.

Overview

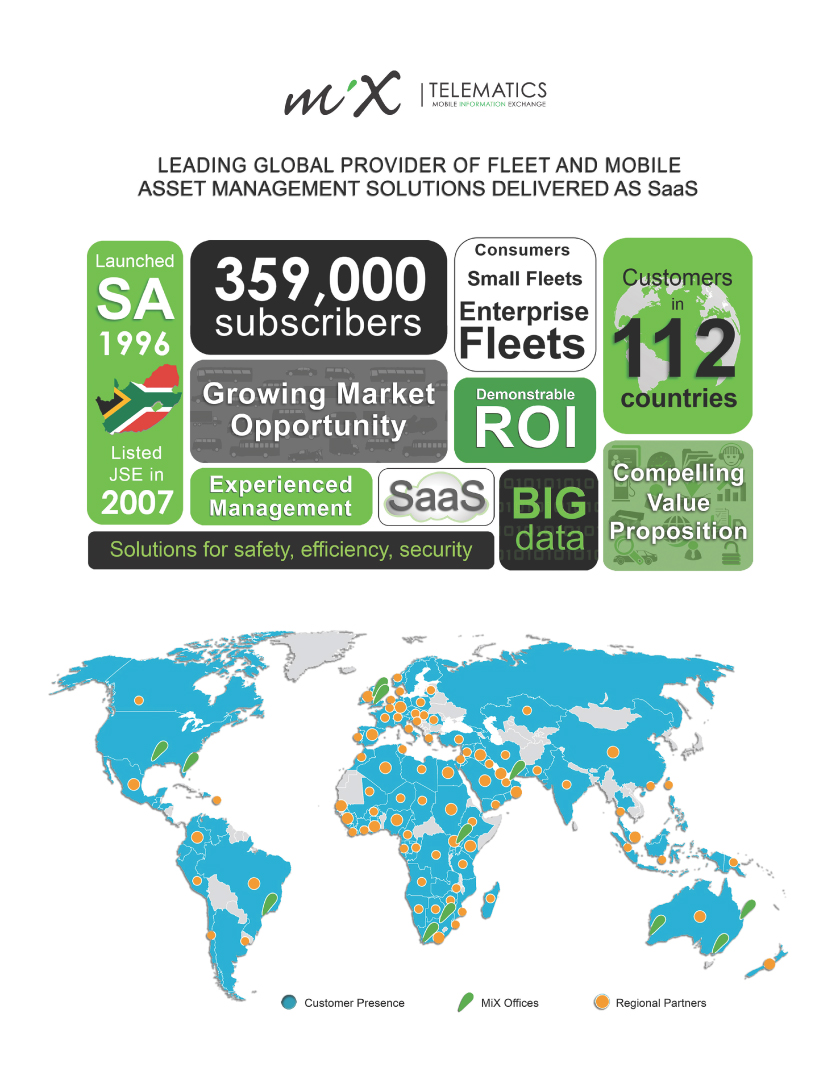

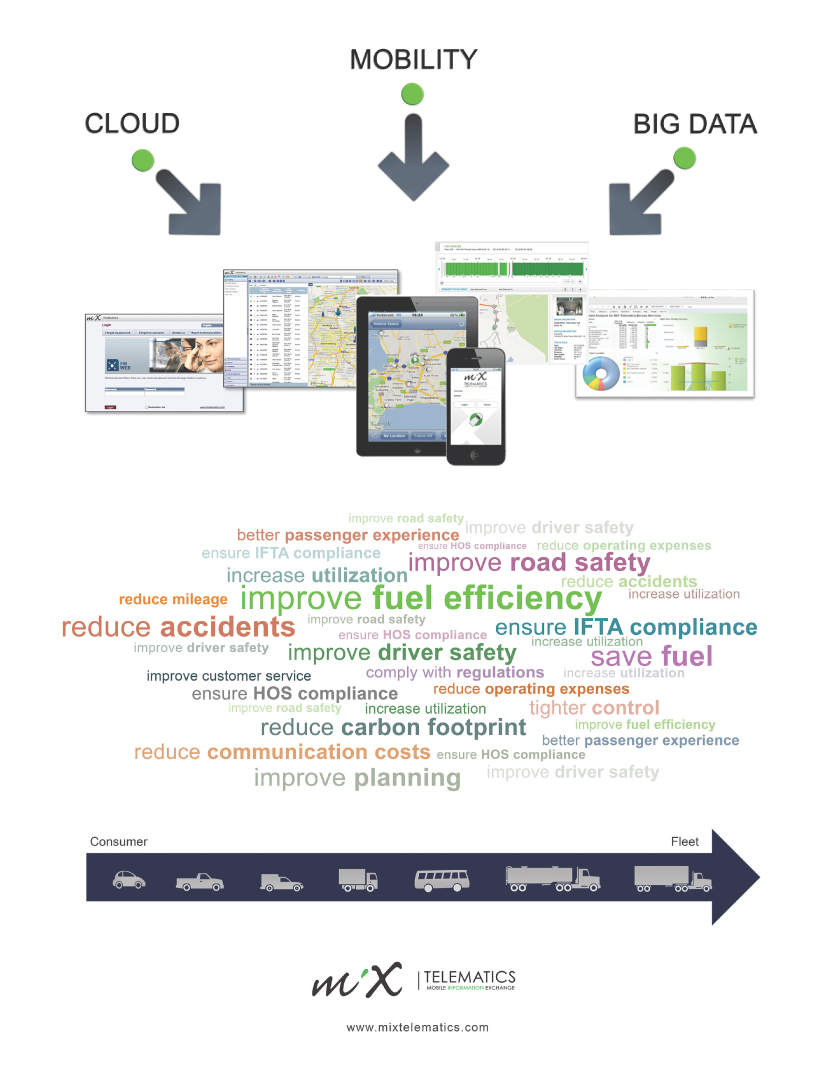

We are a leading global provider of fleet and mobile asset management solutions delivered as software-as-a-service, or SaaS. Our solutions deliver a measurable return by enabling our customers to manage, optimize and protect their investments in commercial fleets or personal vehicles. We generate actionable intelligence that enables a wide range of customers, from large enterprise fleets to small fleet operators and consumers, to reduce fuel and other operating costs, improve efficiency, enhance regulatory compliance, promote driver safety, manage risk and mitigate theft. Our solutions rely on our proprietary, highly scalable technology platform, which allows us to collect, analyze and deliver data from our customers’ vehicles. Using an intuitive, web-based interface, our fleet customers can access large volumes of historical and real-time data, monitor the location and status of their drivers and vehicles and view a wide selection of reports and key performance indicator dashboards.

We have a global presence with customers located in 112 countries across six continents. We currently serve a highly diverse customer base, including more than 4,000 fleet operators, which represented 64% of our subscription revenue for fiscal year 2013. We target sales of our enterprise fleet management solutions to customers who desire a premium solution, generally for large fleets, which we define as fleets of 100 or more vehicles. Large fleets accounted for approximately 74% of our fleet vehicles under subscription at March 31, 2013. We believe we have a satisfied customer base and, among our 224 large fleet operator customers, we experienced an annual customer retention rate in excess of 95% in fiscal year 2013. We have multinational enterprise fleet customer deployments with companies such as Baker Hughes, Bechtel Corporation, Chevron, Nestlé, PepsiCo, Rio Tinto and Schlumberger. We also offer a range of subscription-based fleet and vehicle management solutions to meet the needs and price points of small fleet operators and consumers. Our safety and security features, including driver performance and vehicle monitoring, are important attributes of our solutions for these customers.

We have consistently grown our customer base. As evidence of this growth, vehicles under subscription, one of our key operating metrics and a factor influencing our rate of subscription revenue growth, increased at a compound annual growth rate of 22.3% from April 1, 2011 to March 31, 2013 and as of March 31, 2013, we tracked and managed over 359,000 vehicles under subscription. As a further indicator of our scale, in fiscal year 2013, we collected data on an average of approximately 57 million trips per month representing as many as 3 billion vehicle locations per month. The monthly price charged per vehicle under subscription varies among our

1

Table of Contents

customers depending on services and features, hardware options, customer size and geographic location. Consequently, our rate of subscription revenue growth is influenced by not only the rate of growth in the number of vehicles under subscription but also by the evolving mix of our subscriber base. For fiscal year 2013, our subscription revenue was R686.7 million ($74.2 million), total revenue was R1,171.5 million ($126.6 million), Adjusted EBITDA was R290.8 million ($31.4 million) and profit for the year was R128.5 million ($13.9 million), representing 18.9%, 15.0%, 20.9% and 24.4% growth over the prior year, respectively. See “—Summary Financial and Operating Data—Adjusted EBITDA” for our definition of Adjusted EBITDA and a reconciliation of Adjusted EBITDA to profit for the year.

Industry Background and Market Opportunity

Fleet managers operate in an increasingly competitive and highly regulated global environment. Timely and accurate decision-making enabled by solutions that provide real-time visibility into vehicle location and driver performance is critical to managing a safe, efficient fleet. In some developing areas of the world, ensuring driver and vehicle safety and security is also particularly challenging given high crime rates which have resulted in automotive insurance mandates and regulatory requirements for vehicle tracking. Consequently, fleet managers and consumers demand solutions that promote driver and passenger safety, mitigate theft, improve stolen vehicle recovery rates and reduce automotive insurance rates. The business environment for fleet managers is further complicated by the large number of transportation-related regulatory and compliance requirements worldwide, and the frequency with which rules and regulations change.

There have been substantial advances in the performance, reliability and affordability of technologies that can be used to collect and disseminate large amounts of vehicle data remotely. GPS positioning and advanced on-board systems generate valuable, objective real-time information, which provides the basis for driver and vehicle management solutions. Similarly, significant advances in the performance, reliability and affordability of fixed and wireless networks, computing power and data storage capabilities have supported the rise of cloud computing. These technological advances and market shifts have helped to foster demand for subscription-based fleet and mobile asset management solutions like ours.

We believe that the addressable market for our fleet management solutions is large, growing and underpenetrated. According to a report by ABI Research, there were more than 333 million commercial vehicles in operation globally at the end of 2012 and commercial telematics market penetration was approximately 4%. The report forecasts that the number of commercial vehicles utilizing commercial telematics will nearly triple by the end of 2017.

In addition to the growing market opportunity in commercial fleet vehicles, we believe there is a large and underpenetrated market to provide a tailored set of safety and security solutions to non-commercial passenger vehicles. We estimate that there are approximately 33 million non-commercial passenger vehicles in operation in South Africa and Brazil, our current geographic focus for passenger vehicle mobile asset management solutions.

2

Table of Contents

Our Solutions

Our subscription-based solutions enable our customers to manage, optimize and protect their investments in their commercial fleets and personal vehicles efficiently. The key attributes of our solutions include:

| Ÿ | Highly scalable solutions. We have built our software solutions to scale and support geographically distributed fleets of any size. We currently provide services to more than 359,000 vehicles under subscription with customers ranging from small fleet operators and consumers to large enterprise fleets with more than 10,000 vehicles under subscription. |

| Ÿ | Robust portfolio of features addressing a full range of customer needs. We believe we offer one of the broadest ranges of features for fleet and mobile asset management available. For example, for fleet efficiency, we offer vehicle tracking and analysis, route optimization and enhanced dispatching; for regulatory compliance, we offer compliance monitoring, hours of service, or “HOS,” tracking and fuel tax reporting; for driver improvement, we offer in-vehicle video monitoring and real-time driver feedback; for risk management, we offer driver scoring and analysis; and for safety and security, we offer vehicle tracking, crash notifications and vehicle theft recovery. |

| Ÿ | Insightful business intelligence and reporting. Our fleet management software is designed to provide our customers with insightful, actionable business intelligence on demand. |

| Ÿ | Easily accessible, intuitive applications. Our web-based solutions are accessible from fixed and mobile computing devices, including Android and iOS mobile devices, and our fleet management solutions can be readily integrated with third-party software systems. |

| Ÿ | Software-as-a-service powered by a proven, reliable infrastructure. Our use of a multi-tenant SaaS architecture allows us to deliver fleet management applications that are highly functional, flexible and fast while reducing the cost and complexity associated with customer adoption. We support our SaaS delivered solutions with a proven infrastructure of redundant servers and other hardware located in five secure third-party data centers. Over the last three years, we have consistently maintained overall system uptime of over 99.8%. |

Key Competitive Strengths

The markets in which we operate are highly competitive and fragmented. We believe that the following attributes differentiate us from our competitors and are key factors to our success:

| Ÿ | Globalized sales, distribution and support capabilities. We currently maintain a direct or indirect sales and support presence, with localized application support for 24 languages, in countries across Africa, Asia, Australia, Europe, the Middle East, North America and South America. We believe our global presence gives us an important advantage in competing for business from multinational enterprise fleet customers such as Baker Hughes, Bechtel Corporation, Chevron, Nestlé, PepsiCo, Rio Tinto and Schlumberger, who often prefer to consolidate disparate fleet management systems. |

| Ÿ | Solutions adaptable to multiple customer segments. We believe that by leveraging our common core technologies, personnel and systems, we can cost-effectively develop and sell a range of subscription-based fleet and mobile asset management solutions that are |

3

Table of Contents

| designed to meet the functionality and price needs of multiple customer segments, including fleet operators and consumers. Our fleet management solutions include targeted functionality to address the distinct needs of key industry segments. |

| Ÿ | Focus on safety and security. Most of our offerings incorporate safety and security features enabling our customers to enhance their drivers’ personal safety, encourage safe driving behavior and protect their investment in their vehicles. We also offer web-based driver training, proactive journey management and other related services to provide a turnkey safety and security solution. Our differentiated safety and security features have particularly strong appeal to customers in regulated industries, such as oil and gas, customers in industries exposed to liability concerns, such as bus and coach, and customers operating in high crime regions. |

| Ÿ | Track record of innovation. Since inception, we have made significant investments in product development, and we have routinely been among the first to market with innovative solutions and features that cater to the needs of our customers. For example, in September 2011, we introduced the Beam-e solution, which leverages our large network of vehicles under subscription as a crowdsourcing platform to locate vehicles without the expense of utilizing a traditional cellular network connection. In April 2013, we introduced MiX Vision, which provides customers with a premium subscription-based, in-vehicle video surveillance solution. |

| Ÿ | Longstanding, established market position. We have a 17-year history, a geographically diverse sales and marketing footprint, a large established network of distributors and dealers, and a large base of satisfied customers. Our robust and referenceable customer base, including numerous Forbes Global 2000 enterprises, is a critical selling point to both large enterprise fleets and smaller fleet operators and consumers. |

Growth Strategy

We intend to expand our leadership in our market by:

| Ÿ | Acquiring new customers and increasing sales to existing customers. We believe the market for fleet and mobile asset management solutions is large and growing, creating a significant opportunity for us to expand our customer base. Additionally, we believe we have the opportunity to expand our fleet management market share among our existing customer base by demonstrating our value proposition, growing with the customer, introducing new and innovative value-added solutions and displacing legacy fleet management solutions. |

| Ÿ | Expanding our geographic presence. We market and distribute our solutions directly and through a global network of more than 100 distribution partners outside of South Africa. We are expanding our penetration in attractive geographic regions, such as Brazil this year. We also continue to expand our network of strategic and sales distribution partners in other regions of the world. |

| Ÿ | Broadening our customer segment focus. We currently have customers across numerous industry segments, with the resources of our direct sales organization focused on premium customers in certain key segments, including oil and gas, transportation and logistics, government and municipal, bus and coach, and rental and leasing. In the future, we may increase our product development initiatives and sales and distribution efforts in other industry segments, such as service fleets, and in other customer segments, such as small business fleets. We regularly evaluate opportunities to expand our target customer focus. |

4

Table of Contents

| Ÿ | Continuing to introduce new, innovative solutions to address market demand. We intend to continue to invest in product development to expand our portfolio of fleet and mobile asset management solutions. We recently introduced MiX Vision, which offers a premium subscription-based, in-vehicle video surveillance solution. We are currently developing other extensions to our solutions portfolio based on our assessment of market demand. For example, following our recent acquisition of Intellichain, a supply chain management software business, we are currently developing elements of integrated transportation management software. |

| Ÿ | Pursuing strategic acquisitions. Our industry is highly fragmented and, since our inception, we have consummated four acquisitions worldwide. We intend to selectively evaluate acquisition opportunities in certain geographic regions and industry segments. |

Risks Factors

You should carefully consider the risks described under “Risk Factors” beginning on page 13, and elsewhere in this prospectus. Some of these risks are:

| Ÿ | our ability to maintain our subscription-based relationships with our existing customers; |

| Ÿ | our ability to adapt to rapid technological change in our industry; |

| Ÿ | our ability to compete effectively; |

| Ÿ | the loss of one or more of our key personnel or our failure to attract, train and retain other highly qualified personnel; |

| Ÿ | our ability to integrate businesses we acquire; |

| Ÿ | our ability to increase sales of our solutions; |

| Ÿ | our dependence on key suppliers and vendors to manufacture our hardware; |

| Ÿ | our dependence on our network of dealers and distributors to sell our solutions; |

| Ÿ | the failure of businesses to adopt fleet management solutions; |

| Ÿ | existing and potential new international operations; |

| Ÿ | the impact of laws and regulations relating to the Internet and data privacy; |

| Ÿ | our ability to protect our intellectual property and proprietary technologies and address any infringement claims; |

| Ÿ | significant disruption in service on, or security breaches of, our websites or computer systems; |

| Ÿ | our dependence on third-party technology, including cellular and GPS networks, and any disruption, failure or increase in costs; |

| Ÿ | fluctuations in the value of the South African rand; |

5

Table of Contents

| Ÿ | economic, social, political and other conditions and developments in South Africa and globally; and |

| Ÿ | our ability to issue securities and access the capital markets in the future. |

These risks could materially and adversely impact our business, results of operations and financial condition, which could cause the trading price of the ADSs and our ordinary shares to decline and could result in a loss of your investment.

Emerging Growth Company Status

We are an “emerging growth company,” as defined in the Jumpstart Our Business Startups Act or the “JOBS Act.” Thus, we may take advantage of certain exemptions from various reporting requirements that are applicable to public companies generally. For example, we may elect not to have our independent registered public accounting firm provide an attestation report on the effectiveness of our internal control over financial reporting, as would otherwise be required by Section 404(b) of the Sarbanes-Oxley Act of 2002, as amended, or “SOX.”

We will cease to be an “emerging growth company” upon the earliest of:

| Ÿ | the last day of the fiscal year in which the fifth anniversary of this offering occurs; |

| Ÿ | the last day of the fiscal year in which our annual gross revenues are $1 billion or more; |

| Ÿ | the date on which we have, during the previous three-year period, issued more than $1 billion in non-convertible debt securities; or |

| Ÿ | the last day of any fiscal year in which the market value of our ordinary shares held by non-affiliates exceeded $700 million at the end of the second quarter of that fiscal year. |

Corporate Information

We were founded in South Africa in 1996. In November 2007, we successfully completed an initial public offering on the JSE. The address of our principal executive office is Howick Close, Waterfall Park, Midrand, South Africa 1686, and our telephone number is +(27) 11-654-8000. Our website address is www.mixtelematics.com. The reference to our website is intended to be an inactive textual reference and the information on, or accessible through, our website is not intended to be part of this prospectus.

6

Table of Contents

THE OFFERING

| ADSs offered by us |

4,400,000 ADSs. |

| ADSs offered by the selling shareholders |

1,896,098 ADSs. |

| Offering price |

The initial public offering price is $16.00 per ADS. |

| Ordinary shares outstanding immediately after this offering |

770,212,500 ordinary shares will be outstanding immediately upon the completion of this offering. |

| ADSs outstanding immediately after this offering |

6,296,098 ADSs |

| Over-allotment option |

The selling shareholders have granted to the underwriters an option, which is exercisable within 30 days from the date of this prospectus, to purchase up to 944,414 additional ADSs. |

| The ADSs |

Each ADS will represent 25 ordinary shares with no par value. |

| The depositary will hold ordinary shares underlying the ADSs. You will have rights as provided in the deposit agreement. |

| If we declare dividends on our ordinary shares, the depositary will pay you the cash dividends and other distributions it receives on our ordinary shares, after deducting its fees and expenses. |

| You may turn in the ADSs to the depositary in exchange for ordinary shares. The depositary will charge you fees for any exchange. |

| We may amend or terminate the deposit agreement without your consent. If you continue to hold the ADSs, you agree to be bound by the deposit agreement as amended. |

| To better understand the terms of the ADSs, you should carefully read the “Description of American Depositary Shares” section of this prospectus. You should also read the deposit agreement, which is filed as an exhibit to the registration statement that includes this prospectus. |

| Use of proceeds |

We intend to use the net proceeds from this offering to pursue future acquisitions and other strategic investments and for general corporate purposes. We have not yet identified any specific acquisitions or investments, and our |

7

Table of Contents

| management will have broad discretion over how to use the proceeds from this offering. Pending application of the net proceeds from this offering, we intend to invest the net proceeds of the offering in deposit accounts, money market funds, government-sponsored enterprise obligations and corporate obligations. See “Use of Proceeds” for additional information. |

| Lock-up Agreement |

We, our directors, executive officers and certain shareholders have agreed with the underwriters, subject to certain exceptions not to sell, transfer or dispose of, directly or indirectly, any of the ADSs or ordinary shares owned by such persons prior to this offering or securities convertible into or exercisable or exchangeable for the ADSs or ordinary shares until after 180 days after the date of this prospectus. In addition, through a letter agreement, we will instruct The Bank of New York Mellon, as depositary, not to accept any deposit of any ordinary shares from such persons or deliver any ADSs to such persons until after 180 days following the date of this prospectus unless we consent to such deposit or issuance. This letter agreement applies to all of our ordinary shares, options, restricted shares and restricted share units, including shares held by our directors, executive officers and certain shareholders that are parties to the lock-up agreements. We will not provide such consent without the prior written consent of the representatives of the underwriters. The foregoing does not affect the right of ADS holders to cancel their ADSs and withdraw the underlying ordinary shares. See “Shares Eligible for Future Sale” and “Underwriting” for more information. |

| New York Stock Exchange symbol |

The ADSs will trade, subject to notice of issuance, on the NYSE under the symbol “MIXT.” |

| Payment and settlement |

The underwriters expect to deliver the ADSs against payment therefor through the facilities of The Depository Trust Company on August 14, 2013. |

| Depositary |

The Bank of New York Mellon. |

| Risk factors |

See “Risk Factors” and other information included in this prospectus for a discussion of risks that you should carefully consider before investing in the ADSs. |

| Selling restrictions |

This offering of ADSs is being made in the United States and elsewhere outside South Africa solely in jurisdictions where such offering is permitted. This prospectus does not constitute an offer or sale of ADSs to the public in South Africa and no offer made in terms of this prospectus may be accepted by, nor any sale in terms of this prospectus made |

8

Table of Contents

| to, persons in South Africa. Offers and sales of ADSs to the public of South Africa may only be made in accordance with the requirements of South African laws and regulations. This prospectus will not be registered with any authority in South Africa. |

The number of ordinary shares that will be outstanding immediately after this offering is based on 660,212,500 ordinary shares outstanding at August 8, 2013 and excludes 63,425,000 ordinary shares issuable upon the exercise of options outstanding at August 8, 2013, at a weighted average exercise price of R1.38 (or approximately $0.15) per share.

Our executive officers, directors, current 5% or greater shareholders and entities affiliated with them beneficially owned approximately 65% of our ordinary shares outstanding at August 8, 2013 and, upon the completion of this offering and assuming that the over-allotment option has been exercised in full, will beneficially own approximately 50% of our ordinary shares.

9

Table of Contents

SUMMARY FINANCIAL AND OPERATING DATA

The following tables set forth summary financial and operating data at and for the fiscal years ended March 31, 2013, 2012 and 2011. The summary financial data set forth below at and for the fiscal years ended March 31, 2013 and 2012 have been derived from our audited consolidated financial statements for fiscal years 2013 and 2012 and the accompanying notes included in this prospectus and should be read together with such financial statements and with “Selected Financial and Operating Data.” The summary financial data at and for the fiscal year ended March 31, 2011 has been derived from consolidated financial statements which are not included in this prospectus. The results of operations for the periods presented below are not necessarily indicative of the results to be expected for any future period.

Our fiscal 2012 audited consolidated statements of financial position and statement of cash flows have been restated to correct the classification of in-vehicle devices (installed and uninstalled) and record such devices as property, plant, and equipment. See “Management’s Discussion and Analysis of Financial Condition and Results of Operations – Restatement of 2012 Financial Statements” and Note 42 to our audited consolidated financial statements for the years ended March 31, 2013 and March 31, 2012.

We prepare our consolidated financial statements in accordance with International Financial Reporting Standards, or “IFRS,” as issued by the International Accounting Standards Board, or the “IASB,” which differ in certain significant respects from Generally Accepted Accounting Principles in the United States, or “GAAP.”

Consolidated Income Statement Data

| For the Year Ended March 31, | ||||||||||||||||

| 2013 (*) | 2013 | 2012 | 2011 (Unaudited) |

|||||||||||||

| (In thousands) | ||||||||||||||||

| Revenue |

$ | 126,618 | R | 1,171,480 | R | 1,018,482 | R | 886,604 | ||||||||

| Cost of sales |

(45,886 | ) | (424,545 | ) | (390,926 | ) | (340,168 | ) | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Gross profit |

80,731 | 746,935 | 627,556 | 546,436 | ||||||||||||

| Sales and marketing |

(14,359 | ) | (132,849 | ) | (97,312 | ) | (82,805 | ) | ||||||||

| Administration and other charges (1) |

(46,788 | ) | (432,890 | ) | (383,856 | ) | (346,451 | ) | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Operating profit |

19,584 | 181,196 | 146,388 | 117,180 | ||||||||||||

| Finance income/(costs)—net |

(144 | ) | (1,330 | ) | (2,873 | ) | (11,432 | ) | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Profit before taxation |

19,441 | 179,866 | 143,515 | 105,748 | ||||||||||||

| Taxation |

(5,555 | ) | (51,400 | ) | (40,275 | ) | (34,247 | ) | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Profit for the year |

$ | 13,885 | R | 128,466 | R | 103,240 | R | 71,501 | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| (*) | We have translated U.S. dollar amounts from South African rand at the exchange rate of R9.2521 per $1.00, which was the R/$ exchange rate reported by the South African Reserve Bank for March 31, 2013. |

| (1) | Includes other income/(expenses)—net. |

10

Table of Contents

Other Financial and Operating Data

| For the Year Ended March 31, | ||||||||||||||||

| 2013 (*) | 2013 | 2012 | 2011 (Unaudited) |

|||||||||||||

| (In thousands, except vehicle data) | ||||||||||||||||

| Subscription revenue |

$ | 74,223 | R | 686,720 | R | 577,330 | R | 503,429 | ||||||||

| Adjusted EBITDA (1) |

31,433 | 290,821 | 240,622 | 201,833 | ||||||||||||

| Vehicles under subscription |

359,643 | 359,643 | 272,935 | 240,279 | ||||||||||||

| (*) | We have translated U.S. dollar amounts from South African rand at the exchange rate of R9.2521 per $1.00, which was the R/$ exchange rate reported by the South African Reserve Bank for March 31, 2013. |

| (1) | See “—Adjusted EBITDA” below for our definition of Adjusted EBITDA and a reconciliation of Adjusted EBITDA to profit for the year, the most directly comparable financial measure presented in accordance with IFRS. |

Consolidated Statement of Financial Position Data

| At March 31, | ||||||||||||||||

| 2013 (*) | 2013 | 2012 | 2011 (Unaudited) |

|||||||||||||

| (In thousands) | ||||||||||||||||

| Cash and cash equivalents |

$ | 15,964 | R | 147,702 | R | 118,695 | R | 110,007 | ||||||||

| Total assets |

124,597 | 1,152,788 | 1,068,416 | 994,208 | ||||||||||||

| Working capital |

12,349 | 114,252 | 56,347 | 8,914 | ||||||||||||

| Total indebtedness (1) |

6,428 | 59,477 | 73,106 | 103,546 | ||||||||||||

| Total shareholders’ equity (2) |

93,803 | 867,879 | 772,090 | 682,935 | ||||||||||||

| (*) | We have translated U.S. dollar amounts from South African rand at the exchange rate of R9.2521 per $1.00, which was the R/$ exchange rate reported by the South African Reserve Bank for March 31, 2013. |

| (1) | Total indebtedness includes amounts outstanding at March 31, 2013 for bank overdraft and borrowings. All of our indebtedness is secured and none of our debt is guaranteed. |

| (2) | Excludes non-controlling interest. |

Adjusted EBITDA

To provide investors with additional information regarding our financial results, we have disclosed within this prospectus Adjusted EBITDA, which is a non-IFRS, non-GAAP, financial measure. We define Adjusted EBITDA as the profit for the year before income taxes, net interest income/(expense), depreciation of property, plant and equipment including capitalized customer in-vehicle-devices, amortization of intangible assets including capitalized in-house development costs, share-based compensation costs, transaction costs arising from the acquisition of a business, restructuring costs, profits/(losses) on the disposal or impairments of assets, and unrealized foreign exchange profits/(losses). We present below a reconciliation of Adjusted EBITDA to profit for the year, the most directly comparable financial measure presented in accordance with IFRS.

We have included Adjusted EBITDA in this prospectus because it is a key measure that our management and Board of Directors intends to use instead of EBITDA to understand and evaluate our core operating performance and trends; to prepare and approve our annual budget; and to develop short- and long-term operational plans. In particular, the exclusion of certain expenses in calculating Adjusted EBITDA can provide a useful measure for period-to-period comparisons of our core business. Accordingly, we believe that Adjusted EBITDA provides useful information to investors and others in understanding and evaluating our operating results.

11

Table of Contents

Our use of Adjusted EBITDA has limitations as an analytical tool, and you should not consider this performance measure in isolation from, or as a substitute for, analysis of our results as reported under IFRS. Some of these limitations are:

| Ÿ | although depreciation and amortization are non-cash charges, the assets being depreciated and amortized may have to be replaced in the future, and Adjusted EBITDA does not reflect cash capital expenditure requirements for such replacements or for new capital expenditure requirements; |

| Ÿ | Adjusted EBITDA does not reflect changes in, or cash requirements for, our working capital needs; |

| Ÿ | Adjusted EBITDA does not consider the potentially dilutive impact of equity-based compensation; |

| Ÿ | Adjusted EBITDA does not reflect tax payments that may represent a reduction in cash available to us; |

| Ÿ | Adjusted EBITDA does not reflect the interest expense or the cash requirements necessary to service interest payments on our debt or any losses on the extinguishment of our debt; |

| Ÿ | Adjusted EBITDA does not include unrealized foreign currency transaction gains and losses; and |

| Ÿ | other companies, including companies in our industry, may calculate Adjusted EBITDA differently, which reduces its usefulness as a comparative measure. |

Because of these limitations, you should consider Adjusted EBITDA alongside other financial performance measures, including operating profit, profit for the year and our other results.

Reconciliation of Adjusted EBITDA to Profit for the Year

| For the Year Ended March 31, | ||||||||||||||||

| 2013 (*) | 2013 | 2012 | 2011 (Unaudited) |

|||||||||||||

| (In thousands) | ||||||||||||||||

| Adjusted EBITDA |

$ | 31,433 | R | 290,821 | R | 240,622 | R | 201,833 | ||||||||

| Add: |

||||||||||||||||

| Finance income |

218 | 2,018 | 2,392 | 2,193 | ||||||||||||

| Less: |

||||||||||||||||

| Depreciation and amortization (1) |

10,612 | 98,186 | 89,832 | 79,831 | ||||||||||||

| Taxation |

5,555 | 51,400 | 40,275 | 34,247 | ||||||||||||

| Impairment (2) |

557 | 5,158 | 1,332 | 3,132 | ||||||||||||

| Finance costs |

362 | 3,348 | 5,265 | 13,625 | ||||||||||||

| Share-based payment costs |

341 | 3,151 | 2,001 | 1,048 | ||||||||||||

| Foreign exchange—unrealized |

326 | 3,012 | 639 | 581 | ||||||||||||

| Non-recurring items (3) |

13 | 118 | 430 | 61 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Profit for the year |

$ | 13,885 | R | 128,466 | R | 103,240 | R | 71,501 | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| (*) | We have translated U.S. dollar amounts from South African rand at the exchange rate of R9.2521 per $1.00, which was the R/$ exchange rate reported by the South African Reserve Bank for March 31, 2013. |

| (1) | Includes depreciation of property, plant and equipment (including in-vehicle devices) and amortization of intangible assets. |

| (2) | Includes impairment of intangibles and impairment of available-for-sale financial assets. |

| (3) | Includes loss on disposal of subsidiary, loss on sale of intangibles, transaction costs arising from acquisition of a business, restructuring costs and (profit)/loss on sale of property, plant and equipment. |

12

Table of Contents

Our business, results of operations and financial condition could be materially and adversely affected if any of the risks described below occurs. As a result, the market price of the ADSs could decline, and you could lose all or part of your investment. We may face additional risks and uncertainties that are not currently known to us, or that we currently deem immaterial, which may also impair our business. You should carefully consider all of the risk factors set forth below before making an investment decision regarding the ADSs.

Risks Relating to Our Business

We may be unable to maintain our relationships with our existing customers, which could result in a loss of subscription revenue.

We provide our solutions principally on a subscription basis, typically with an initial subscription term of three years and renewal terms of either three years or successive one-year periods, or, for certain of our consumer customers, on a month-to-month basis. However, our customers have no obligation to renew their subscriptions after the initial term or any renewal term expires. We may be unable to retain existing customers and, as a result, our revenue would be adversely affected. Customers may choose not to renew their subscriptions for many reasons, including:

| Ÿ | the belief that our solutions are not required for their needs or are not cost-effective; |

| Ÿ | a desire to reduce discretionary spending; |

| Ÿ | a belief that our competitors’ solutions provide a better value; |

| Ÿ | changes in our customers’ business or in regulations impacting our customers’ business that may decrease the need for our fleet and mobile asset management solutions; or |

| Ÿ | because of a reduction in discounts offered by insurers to vehicle owners who have installed our products. |

Our enterprise fleet management customers may also not renew for reasons entirely out of their control, such as the dissolution of their business. Enterprise customers may also decrease the number of vehicles covered by subscription contracts if their fleet sizes decrease.

Our subscription contracts generally do not provide our customers with an early termination option. However, if customers do not honor their subscriptions for the full term, our remedies may be limited to re-negotiation of contract terms or legal recourse through the courts, which may not be successful or cost-effective, and we may not be able to recoup all of our costs.

A significant failure to maintain our customer relationships could result in a loss of subscription revenue.

Our inability to adapt to rapid technological change in our industry could impair our ability to remain competitive and result in a decline in market acceptance of our products.

The industries in which we compete are characterized by rapid technological change, frequent introductions of new products and evolving industry standards. In addition to the mobile asset management industry, we are subject to changes in the automotive, mobile handset, GPS navigation device, information technology, telecommunications and work flow software

13

Table of Contents

industries. As the technology used in each of these industries evolves, we will face new integration and competition challenges. For example, as truck and automobile manufacturers continue to develop in-vehicle technology, GPS-based tracking solutions may become standard equipment and result in new sources of competition. If we are unable to adapt to rapid technological change, it could impair our ability to remain competitive and result in a decline in market acceptance of our products.

The development of new or improved products, systems or technologies that compete with our products may render our products less competitive and we may not be able to enhance our technology in a timely manner. In addition to the competition resulting from new products, systems or technologies, our future product enhancements may not adequately meet the requirements of the marketplace and may not achieve the broad market acceptance necessary to generate significant revenues. Any of the foregoing could materially and adversely affect our business, results of operations and financial condition.

Industry consolidation may give our competitors advantages over us, which could result in a loss of customers and/or a reduction in revenue.

Some of our competitors have made or may make acquisitions or enter into partnerships or other strategic relationships to offer more comprehensive services or achieve greater economies of scale. In addition, new entrants not currently considered competitors may enter our market through acquisitions, partnerships or strategic relationships. For example, Danaher Corporation, a Fortune 250 science and technology company, recently announced the acquisition of Navman Wireless, which offers fleet tracking services. We expect these trends to continue as companies attempt to strengthen or maintain their market positions. Many potential entrants may have competitive advantages over us, such as greater name recognition, longer operating histories, more varied services and larger marketing budgets, as well as greater financial, technical and other resources. Industry consolidation may result in competitors with more compelling service offerings or greater pricing flexibility than we have or business practices that make it more difficult for us to compete effectively, including on the basis of price, sales and marketing programs, technology or service functionality. These pressures could result in a loss of subscribers and/or a reduction in revenue.

The loss of one or more of our key personnel, or our failure to attract, train and retain other highly qualified personnel, could prevent us from executing our growth plan.

We depend on the continued service and performance of our key personnel. The loss of one or more key members of our senior management team could prevent us from executing our growth plan. In addition, the loss of other key marketing, sales, product development or technology personnel could disrupt our operations and have a materially adverse effect on our ability to grow our business.

To execute our growth plan, we must continue to attract and retain highly qualified personnel. Competition for these employees is intense, and we may not be successful in attracting and retaining qualified personnel. We may experience difficulty in hiring and retaining highly skilled employees with appropriate qualifications. Our failure to attract and train new personnel, or our failure to retain, focus and motivate our current personnel, could materially and adversely affect our business, results of operations and financial condition.

14

Table of Contents

We may expand by acquiring or investing in other companies, which may divert our management’s attention, result in dilution to our shareholders and consume resources that are necessary to sustain our business.

We may in the future acquire complementary products, services, technologies or businesses. We also may enter into relationships with other businesses to expand our portfolio of solutions or to expand our ability to provide our solutions in foreign jurisdictions. Negotiating these transactions can be time-consuming, difficult and expensive, and our ability to complete these transactions may be subject to conditions or approvals that are beyond our control, including anti-takeover and antitrust laws in various jurisdictions. We may seek to acquire other companies or businesses using our shares as consideration. Under the South African Companies Act, 2008, or the “Companies Act,” we are prohibited from issuing shares representing 30% or more of our outstanding equity in connection with an acquisition without stockholder approval by way of special resolution. In terms of JSE listings requirements, an acquisition or disposal constituting 25% or more of the market capitalization of the acquiring entity, will require stockholder approval. Consequently, these transactions, even if undertaken and announced, may not close.

An acquisition, investment or new business relationship may result in unforeseen operating difficulties and expenditures. In particular, we may encounter difficulties assimilating or integrating the businesses, technologies, products, personnel or operations of acquired companies, particularly if the key personnel of the acquired company choose not to work for us, the acquired company’s technology is not easily compatible with ours or we have difficulty retaining the customers of any acquired business due to changes in management or otherwise. Acquisitions may also disrupt our business, divert our resources and require significant management attention that would otherwise be available for the development of our business. Moreover, the anticipated benefits of any acquisition, investment or business relationship may not be realized or we may be exposed to unknown liabilities, including litigation against the companies we may acquire. For one or more of those transactions, we may:

| Ÿ | issue additional equity securities that would dilute our shareholders; |

| Ÿ | use cash that we may need in the future to operate our business; |

| Ÿ | incur debt on terms unfavorable to us or that we are unable to repay or that may place burdensome restrictions on our operations; |

| Ÿ | incur large charges or substantial liabilities; or |

| Ÿ | become subject to adverse tax consequences, or substantial depreciation or amortization, deferred compensation or other acquisition-related accounting charges. |

Any of these risks could materially and adversely affect our business, results of operations and financial condition.

We may not be able to increase sales of our solutions, which could materially and adversely affect our ability to grow our business and increase revenue.

We intend to increase sales of our solutions by increasing penetration in our existing markets and by entering new markets that represent a large potential source of demand for these solutions. Our success in increasing sales may be tied to a wide variety of factors, including demand for our services, price and service competition, our relationships with third party distributors and dealers, the rate of new vehicle sales, general economic conditions and, in the case of our safety and security solutions, the perceived threat of vehicle theft and discounts offered by insurers.

15

Table of Contents

Additionally, some car and truck manufacturers have begun installing substitute products and services, such as certain GPS-based products, in new vehicles prior to their initial sale, which may preclude us from increasing sales to subscribers purchasing such vehicles. Our inability to market and sell our solutions to new customers could materially and adversely affect our ability to grow our business and increase revenue.

We depend on certain key suppliers and vendors to manufacture our hardware and an interruption in the supply of our hardware could impair our production capacity.

We currently purchase key GSM (Global System for Mobile communications) module components of our hardware from two key suppliers. These modules and many of the other components used in the manufacture of our products have extended lead times on orders. We do not have volume commitments to or from these suppliers, and therefore cannot require them to deliver components to us. Interruption in the supply of components from suppliers would significantly impact our operations and require us to identify and integrate our manufacturing and supply logistics with an alternate supplier or use a substitute component, which could materially and adversely affect our business, results of operations and financial condition.

In addition, we currently depend principally on three vendors in South Africa to manufacture our hardware on a contract basis. Each of these contracts is terminable on 12 months’ written notice. We have no financial control over and limited operational influence on these suppliers and the conduct of their businesses. These suppliers could, among other things, extend delivery times, raise prices and limit supply due to their own shortages and business requirements. Our three contract manufacturers produce different products for us and production capacities at these facilities are not interchangeable in the short term. If the facilities of one of our contract manufacturers were to suffer a major casualty event, it could take as much as three to five months or longer to replace production capacity. Interruption in the supply of hardware from our contract manufacturers could impair our production capacity and materially and adversely affect our business, results of operations and financial condition.

We depend on our network of dealers and distributors to sell our solutions and adverse changes in our relationships with significant dealers and distributors could cause a decline in sales.

We currently distribute our products to small fleet operators and consumers through various distribution channels, including automobile dealers, aftermarket automotive parts and service suppliers, and automobile insurers and retailers, which we collectively refer to as “distributors.”

We distribute our products to enterprise fleet customers both directly and through third parties who are assigned specific geographic territories in which they can sell, which we refer to as “dealers.”

We sell our solutions both directly and through our global network of independent dealers and distributors. We are dependent on our dealers and distributors, who account for a substantial percentage of our total sales. One group of distributors under common ownership accounts for a substantial portion of our sales in the Africa consumer segment. Additionally, the terms of our agreements with our dealers do not usually include minimum purchase obligations, are specific to a geographic territory and are nonexclusive. Our dealer agreements generally have a fixed initial term, after which they continue indefinitely, subject to the right of either party to terminate on specified notice generally ranging from 90 days to one year, or for breach. Similarly, our distributor agreements do not include minimum purchase obligations and consist principally of a commission agreement applicable to sales generated by the distributor. If our relationships with

16

Table of Contents

our dealers and distributors deteriorate, or if a dealer or distributor or group of related dealers and distributors accounting for a material portion of our sales elects not to do business with us in the future, our sales could decline materially.

We depend on our cellular network providers for the transmission of data from installed in-vehicle devices to our data centers and we would incur significant costs if the services of these network providers became unavailable to us.

We contract with cellular network providers in each of our markets to provide cellular network services. These cellular networks transmit data from our customers’ in-vehicle devices to our data centers, where it is managed for the benefit of our customers. Each installed in-vehicle device contains a SIM card that is compatible with a specific cellular network provider. If a cellular network provider in one of our markets were to refuse to continue contracting with us for any reason or were to go out of business, we could incur significant costs related to the replacement of SIM cards for our customers and could suffer damage to our reputation and customer relationships. Any of the foregoing could materially and adversely affect our business, results of operations and financial condition.

The markets in which we participate are highly fragmented and competitive, with relatively low barriers to entry, and such competition could result in reduced operating margins, increased sales and marketing expenses and the loss of market share.

The market for our solutions is highly fragmented, consisting of a significant number of vendors, with relatively low barriers to entry. Competition in our market is based primarily on:

| Ÿ | functionality and reliability; |

| Ÿ | total cost of ownership; |

| Ÿ | breadth and depth of application functionality for fleet deployments; |

| Ÿ | product performance; |

| Ÿ | interoperability; |

| Ÿ | brand and reputation; |

| Ÿ | customer service; |

| Ÿ | distribution channels; |

| Ÿ | regional geographic expertise, including localized language support, support for applicable government regulations and the ability to comply with local internet and data privacy regulations; |

| Ÿ | size of customer base and reference accounts within key industry segments; |

| Ÿ | ability to deliver ongoing value and return on investment; |

| Ÿ | ease of deployment and use; |

| Ÿ | relevant industry domain expertise and functionality; and |

| Ÿ | the financial resources of the vendor. |

17

Table of Contents

We compete with a number of companies in each of the geographic markets in which we operate. Such competition could result in reduced operating margins, increased sales and marketing expenses and the loss of market share, any of which would harm our operating results. We expect competition to intensify in the future with the introduction of new technologies and market entrants.

The market for safety and security solutions is highly competitive. We compete in the safety and security solutions market primarily on the basis of the technological innovation, value-added services offered, brand recognition, rate of successful recoveries of mobile assets, quality and price of our products and services. Our most competitive market is the vehicle and mobile asset tracking and recovery solutions market, due to the existence of a wide variety of competing products and services and alternative technologies that offer various levels of protection and tracking capabilities. Some of these competing products and services, such as certain GPS-based products, are installed in new cars by vehicle manufacturers prior to their initial sale, which may make it more difficult to compete for such subscribers. Furthermore, providers of competing services or products may extend their offerings to the locations in which we operate or new competitors may enter the safety and security solutions market.

We could be exposed to product liability claims, which could result in significant damage to our reputation and material economic loss.

Our products and the batteries that many of them contain could malfunction and cause damage to our customers’ property. In particular, the rechargeable batteries in our in-vehicle devices may be prone to leaking due to environmental factors such as unusual heat or overuse. Leaks in these batteries could damage our customers’ in-vehicle devices and vehicles. Our safety and security solutions may be disabled or prove to be ineffective as a result of techniques employed by car thieves or the discovery of technological weaknesses by such persons. If there were a systematic failure of any of our products, we could suffer significant damage to our reputation and any product liability insurance we maintain might not be sufficient to prevent us from suffering a material economic loss.

Failure of businesses to adopt fleet management solutions could reduce the demand for our solutions.

We derive, and expect to continue to derive, substantial revenue from the sale of subscriptions for fleet management solutions to commercial customers. Widespread acceptance and use of fleet management solutions is critical to our future revenue growth and success. If the market for fleet management solutions fails to grow or grows more slowly than we currently anticipate, demand for our solutions would be negatively affected.

The market for fleet management solutions is subject to changing customer demand and trends in preferences. Some of the potential factors that could affect interest in and demand for fleet management solutions include:

| Ÿ | the effectiveness and reliability of solutions; |

| Ÿ | fluctuations in fuel and vehicle maintenance costs, which are significant drivers of customer demand for fleet management solutions; |

| Ÿ | assumptions regarding general mobile workforce inefficiency and the extent to which efficiency can be improved through fleet management solutions; |

| Ÿ | the level of governmental and regulatory burdens on the fields of transportation and occupational health and safety; |

18

Table of Contents

| Ÿ | the price, performance, features and availability of products and services that compete with ours; |

| Ÿ | our ability to maintain high levels of customer satisfaction; and |

| Ÿ | the rate of acceptance of web-based solutions generally. |

Failure of businesses to adopt fleet management solutions could materially and adversely affect our business, results of operations and financial condition.

A decline in vehicle sales in our markets could result in reduced demand for our solutions, which could materially and adversely affect our revenue.

A reduction in sales of new vehicles could reduce our addressable market for solutions. New vehicle sales may decline for various reasons, including adverse changes in the general economic environment, a reduction in our customers’ discretionary spending or an increase in new vehicle tariffs, taxes or gas prices. A decline in vehicle production levels or labor disputes affecting the automobile industry in the markets where we operate may also impact the volume of new vehicle sales. A decline in sales of new vehicles in the markets in which we provide our solutions would result in reduced demand for such products and services.

Demand for our fleet management solutions decreases when prices for crude oil and natural gas decrease, which could materially and adversely affect our revenue.

Demand for our fleet management solutions can fluctuate with the prices for crude oil and natural gas, which impacts the attractiveness of our services and also directly affects our customers in the oil and gas industry, from whom we derive a significant portion of our revenues. Generally, lower oil and gas prices reduce the return on investment for many of our customers. Gains in fuel efficiency, including from the use of our solutions, may lead to a relative decrease in the return on investment of our solutions perceived by our customers. The oil and gas industry is complex, and numerous geopolitical, economic, environmental and other factors affect pricing. Expectations for future crude oil and natural gas prices may affect our customers’ spending habits. Prolonged or substantial declines in crude oil and/or natural gas prices, or the perception that such prices will decrease in the future, could materially and adversely affect our business, results of operations and financial condition.

Changes in practices of insurance companies in the markets in which we provide our solutions could materially and adversely affect demand for our products and services.

We depend in part on the practices of insurance companies in some of our markets to support demand for our products and services. For example, in South Africa, which is currently the largest market for our products and services, insurance companies either mandate the installation of tracking devices as a prerequisite for providing insurance coverage to owners of certain vehicles, or provide insurance premium discounts to encourage vehicle owners to subscribe to vehicle tracking and mobile asset recovery solutions such as ours. We benefit from insurance companies’ continued practice in the South African and certain other markets of:

| Ÿ | accepting mobile asset location technologies such as ours as a preferred security product; |

| Ÿ | providing premium discounts for using location and recovery products and services such as ours; and |

| Ÿ | mandating the use of our products and services, or similar products and services, for certain vehicles. |

19

Table of Contents

If any of these policies or practices change, revenues from sale of our products and services could decline, which would materially and adversely affect our business, results of operations and financial condition.

We face many risks associated with our existing and potential new international operations, which could prevent us from successfully expanding into new geographic markets or operating successfully in existing geographic markets.

We are a global company with substantial assets located in a number of countries. We provide our services in 112 countries with 12 offices in seven countries. In some international markets, customer preferences and buying behaviors may be different, and we may use business or pricing models that are different from our traditional subscription model to provide fleet management solutions to customers in those markets or we may be unsuccessful in implementing the appropriate business model. Our revenue from new foreign markets may not exceed the costs of establishing, marketing, and maintaining our international offerings.

In addition, expanding international operations into new territories may subject us to risks with which we have limited experience. These risks include:

| Ÿ | lack of familiarity with local markets; |

| Ÿ | difficulties in finding and maintaining, or potentially replacing, local dealers and distributors; |

| Ÿ | established local competitors; |

| Ÿ | laws favoring local competitors; |

| Ÿ | the cost and burden of complying with, lack of familiarity with, and unexpected changes in, legal and regulatory requirements in new territories, including those relating to the Internet and data privacy and security; |

| Ÿ | fluctuations in currency exchange rates or restrictions on currency exchange; |

| Ÿ | potentially adverse tax consequences, including the complexities of transfer pricing, value added or other tax systems, double taxation and restrictions and/or taxes on the repatriation of earnings; |

| Ÿ | dependence on third parties, including some commercial partners with whom we do not have extensive experience; |

| Ÿ | increased financial accounting and reporting burdens and complexities; |

| Ÿ | political, social, and economic instability, terrorist attacks, and security concerns in general; |

| Ÿ | reduced or varied protection for intellectual property rights in some countries; and |

| Ÿ | increased vulnerability to claims that we have infringed on the intellectual property of third parties. |

Operating in international markets requires significant management attention and financial resources. The investment and additional resources required to establish operations and manage growth in additional territories may not produce desired levels of revenue or profitability.

20

Table of Contents

If we are unable to detect and prevent unauthorized use of customer bank account numbers, we could be subject to financial liability, our reputation could be harmed and customers may be reluctant to use our solutions.

We rely on third-party encryption and authentication technology to provide secure transmission of confidential information over the Internet, including customer bank account numbers. Advances in technological capabilities, new discoveries in the field of cryptography or other events or developments could result in a compromise or breach of the technology we use to protect sensitive transaction data. If any such compromise of our security, or the security of our customers, were to occur, it could result in misappropriation of proprietary information or interruptions in operations and have an adverse impact on our reputation or the reputation of our customers. If we are unable to detect and prevent unauthorized use of bank account numbers, our business, results of operations and financial condition could be materially and adversely affected.

Our operating results may be harmed due to liabilities, penalties and an inability to compete for future sales if we are required to collect sales, use, services or other related taxes for our solutions in jurisdictions where we have not historically done so.

We do not believe that we are required to collect sales, use, services or other similar taxes from our customers in certain jurisdictions. However, one or more countries or states may seek to impose sales, use, services, or other tax collection obligations on us, including for past sales. A successful assertion by one or more jurisdictions that we should collect sales or other taxes on the sale of our solutions could result in substantial tax liabilities, including interest and penalty charges for past sales and decrease our ability to compete for future sales. We review applicable rules and regulations periodically and, when we believe sales and use taxes apply in a particular jurisdiction, we voluntarily engage tax authorities in order to determine how to comply with their rules and regulations. We cannot assure you that we will not be subject to sales and use taxes or related penalties for past sales in jurisdictions where we presently believe sales and use taxes are not due. Furthermore, we cannot be certain that we have made sufficient reserves on our financial statements to cover taxes.

Although our client contracts provide that our clients must pay all applicable sales and similar taxes, they may be reluctant to pay back taxes and may refuse responsibility for interest or penalties associated with those taxes. If we are unable to collect and pay back taxes and the associated interest and penalties, we will have incurred unplanned expenses that may be substantial.

An actual or perceived reduction in vehicle theft and crime rates may adversely impact demand for certain of our solutions, which could result in a loss of customers and a decline in growth.

Demand for our vehicle tracking and asset recovery solutions is influenced by prevailing or expected vehicle theft rates. Vehicle theft rates may decline as a result of various factors, such as the availability of improved security systems, implementation of improved or more effective law enforcement measures and improved economic or political conditions in markets that have high theft rates. If vehicle theft rates in our markets decline significantly, or if vehicle owners or insurance companies believe that vehicle theft rates have declined or are expected to decline, demand for some of our products and services may decline, which could result in a loss of customers and a decline in growth.

21

Table of Contents

We are subject to U.S. and other anti-corruption laws, trade controls, economic sanctions and similar laws and regulations, including those in the jurisdictions where we operate. Our failure to comply with these laws and regulations could subject us to civil, criminal and administrative penalties and harm our reputation.

Doing business on a worldwide basis requires us to comply with the laws and regulations of various foreign jurisdictions. These laws and regulations place restrictions on our operations, trade practices, partners and investment decisions. In particular, our operations are subject to U.S. and foreign anti-corruption and trade control laws and regulations, such as the Foreign Corrupt Practices Act, or the “FCPA,” export controls and economic sanctions programs, including those administered by the U.S. Treasury Department’s Office of Foreign Assets Control, or the “OFAC.” As a result of doing business in foreign countries and with foreign partners, we are exposed to a heightened risk of violating anti-corruption and trade control laws and sanctions regulations.

The FCPA prohibits us from providing anything of value to foreign officials for the purposes of obtaining or retaining business or securing any improper business advantage. It also requires us to keep books and records that accurately and fairly reflect our transactions. As part of our business, we may deal with state-owned business enterprises, the employees of which are considered foreign officials for purposes of the FCPA. In addition, the United Kingdom Bribery Act, or the “Bribery Act,” has been enacted and came into effect on July 1, 2011. The provisions of the Bribery Act extend beyond bribery of foreign public officials and also apply to transactions with individuals not employed by a government. The provisions of the Bribery Act are also more onerous than the FCPA in a number of other respects, including jurisdiction, non-exemption of facilitation payments and penalties. Some of the international locations in which we operate lack a developed legal system and have higher than normal levels of corruption.

Economic sanctions programs restrict our business dealings with certain sanctioned countries, persons and entities. In addition, because we act through dealers and distributors, we face the risk that our dealers and distributors and customers might further distribute our products to a sanctioned person or entity, or an ultimate end-user in a sanctioned country, which might subject us to an investigation concerning compliance with OFAC or other sanctions regulations.

Violations of anti-corruption and trade control laws and sanctions regulations are punishable by civil penalties, including fines, denial of export privileges, injunctions, asset seizures, debarment from government contracts and revocations or restrictions of licenses, as well as criminal fines and imprisonment. We have established policies and procedures designed to assist our compliance with applicable U.S. and international anti-corruption and trade control laws and regulations, including the FCPA, the Bribery Act and trade controls and sanctions programs administered by OFAC, and have trained our employees to comply with these laws and regulations. However, there can be no assurance that all of our employees, consultants, agents or other associated persons will not take actions in violation of our policies and these laws and regulations, and that our policies and procedures will effectively prevent us from violating these regulations in every transaction in which we may engage or provide a defense to any alleged violation. In particular, we may be held liable for the actions that our local, strategic or joint venture partners take inside or outside of the United States, even though our partners may not be subject to these laws. Such a violation, even if our policies prohibit it, could materially and adversely affect our reputation, business, results of operations and financial condition. Our continued international expansion, including in developing countries, and our development of new partnerships and joint venture relationships worldwide, could increase the risk of FCPA, OFAC or Bribery Act violations in the future.

22

Table of Contents

Operating in emerging markets subjects us to greater political, economic and market risks than those we would face if we only operated in more developed markets, which could increase our operating costs.

Emerging markets, including Africa, eastern Europe, the Middle East and South America, are subject to greater risks than more developed markets. The political, economic and market conditions in many emerging markets present risks that could make it more difficult to operate our business successfully. These risks include:

| Ÿ | political and economic instability, including higher rates of inflation and currency fluctuations; |

| Ÿ | higher levels of corruption, including bribery of public officials; |

| Ÿ | loss due to civil strife, acts of war or terrorism, guerrilla activities and insurrection; |

| Ÿ | a lack of well-developed legal systems which could make it difficult for us to enforce our intellectual property and contractual rights; |

| Ÿ | logistical and communications challenges; |

| Ÿ | potential adverse changes in laws and regulatory practices, including import and export license requirements and restrictions, tariffs, legal structures and tax laws; |

| Ÿ | difficulties in staffing and managing operations and ensuring the safety of our employees; |

| Ÿ | restrictions on the right to convert or repatriate currency or export assets; |

| Ÿ | greater risk of uncollectible accounts and longer collection cycles; and |

| Ÿ | introduction or changes to indigenization and empowerment programs. |

Laws and regulations relating to the Internet and data privacy in the markets in which we operate are complex and continuously evolving, and compliance costs are high. As these laws and regulations continue to evolve, we may be required to increase our compliance-related expenditures or limit the manner in which collect information, the types of information that we collect, or the solutions we offer, which may impede our ability to provide our solutions or reduce our profit margins in specific geographic regions.

Various laws and regulations associated with the Internet and data privacy are complex and increase our cost of doing business. Furthermore, these laws and regulations expose us to fines and penalties if we fail to comply with them as well as costs associated with privacy compliance audits. We have not completed a legal review to determine our compliance with data privacy and data security laws. We are conducting a data privacy and data security compliance review in our major markets. There can be no assurance that the policies and procedures we implement as a result of this review will be sufficient to prevent a regulatory agency or private party from asserting a claim based on data privacy or security laws or regulations. Furthermore, there can be no assurance that our employees, contractors and agents will not take actions in violation of the policies we have established or may establish in the future regarding data privacy and data security, particularly as we expand our operations through organic growth and acquisitions. Any violations could subject us to civil or criminal penalties, including substantial fines or prohibitions on our ability to offer our products in one or more countries, and could also materially damage our reputation, our brand, our international expansion efforts, our business, results of operations and financial condition.

23

Table of Contents

Additionally, as cloud computing continues to evolve, increased regulation by federal, state or foreign agencies becomes more likely, particularly in the areas of data privacy and data security. In addition, taxation of services provided over the Internet or other charges imposed by government agencies or by private organizations for accessing the Internet may be imposed. Any regulation imposing greater fees for Internet use or restricting information exchange over the Internet could result in a decline in the use of the Internet and the viability of Internet-based services, which could harm our business.