QuickLinks -- Click here to rapidly navigate through this document

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 20-F

o |

REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EXCHANGE ACT OF 1934 |

|

OR |

||

ý |

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

|

For the fiscal year ended December 31, 2013 |

||

OR |

||

o |

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

|

OR |

||

o |

SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

|

Commission file number 001-36158

![]()

WIX.COM LTD.

(Exact name of Registrant as specified in its charter)

ISRAEL

(Jurisdiction of incorporation or organization)

40 Namal Tel Aviv St.

Tel Aviv, 6350671 Israel

(Address of principal executive offices)

Eitan Israeli, Adv.

Vice President and General Counsel

Telephone: +972 (3) 545-4900

E-mail: israeli.eitan@wix.com

Wix.com Ltd.

40 Namal Tel Aviv St.

Tel Aviv, 6350671 Israel

(Name, telephone, e-mail and/or facsimile number and address of company contact person)

Securities registered or to be registered pursuant to Section 12(b) of the Act:

| Title of each class | Name of each exchange on which registered | |

|---|---|---|

| Ordinary shares, par value NIS 0.01 per share | NASDAQ Global Market |

Securities registered or to be registered pursuant to Section 12(g) of the Act: None.

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act: None.

Indicate the number of outstanding shares of each of the issuer's classes of capital or common stock as of the close of the period covered by the annual report: As of December 31, 2013, the registrant had outstanding 37,493,217 ordinary shares, par value NIS 0.01 per share.

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yes o No ý

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934.

Yes o No ý

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Yes ý No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§229.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

Yes o No o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated file, or a non-accelerated filer. See the definitions of "accelerated filer" and "large accelerated filer" in Rule 12b-2 of the Exchange Act (Check one):

| Large accelerated filer o | Accelerated filer o | Non-accelerated filer ý |

Indicate by check mark which basis for accounting the registrant has used to prepare the financing statements included in this filing:

| U.S. GAAP ý | International Financial Reporting Standards as issued by the International Accounting Standards Board o |

Other o |

If "Other" has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow.

o Item 17 o Item 18

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

Yes o No ý

FORM 20-F

ANNUAL REPORT FOR THE FISCAL YEAR ENDED DECEMBER 31, 2013

| Introduction | i | |||

| Special Note Regarding Forward-Looking Statements | i | |||

PART I |

||||

| Item 1. Identity of Directors, Senior Management and Advisers | 1 | |||

| Item 2. Offer Statistics and Expected Timetable | 1 | |||

| Item 3. Key Information | 1 | |||

| Item 4. Information on the Company | 29 | |||

| Item 4A. Unresolved Staff Comments | 43 | |||

| Item 5. Operating and Financial Review and Prospects | 43 | |||

| Item 6. Directors, Senior Management and Employees | 60 | |||

| Item 7. Major Shareholders and Related Party Transactions | 82 | |||

| Item 8. Financial Information | 88 | |||

| Item 9. The Offer and Listing | 90 | |||

| Item 10. Additional Information | 90 | |||

| Item 11. Quantitative and Qualitative Disclosures About Market Risk | 107 | |||

| Item 12. Description of Securities Other than Equity Securities | 108 | |||

PART II |

||||

| Item 13. Defaults, Dividend Arrearages and Delinquencies | 109 | |||

| Item 14. Material Modifications to the Rights of Security Holders and Use of Proceeds | 109 | |||

| Item 15. Controls and Procedures | 109 | |||

| Item 16. [Reserved] | 110 | |||

| Item 16A. Audit Committee Financial Expert | 110 | |||

| Item 16B. Code of Ethics | 110 | |||

| Item 16C. Principal Accountant Fees and Services | 110 | |||

| Item 16D. Exemptions from the Listing Standards for Audit Committees | 111 | |||

| Item 16E. Purchases of Equity Securities by the Issuer and Affiliated Purchasers | 111 | |||

| Item 16F. Change in Registrant's Certifying Accountant | 111 | |||

| Item 16G. Corporate Governance | 111 | |||

PART III |

||||

| Item 17. Financial Statements | 111 | |||

| Item 18. Financial Statements | 111 | |||

| Item 19. Exhibits | 111 | |||

| Signatures | 112 | |||

| Index to Consolidated Financial Statements | F-1 |

In this annual report, the terms "Wix," "we," "us," "our" and "the company" refer to Wix.com Ltd. and its subsidiaries.

This annual report includes other statistical, market and industry data and forecasts which we obtained from publicly available information and independent industry publications and reports that we believe to be reliable sources. These publicly available industry publications and reports generally state that they obtain their information from sources that they believe to be reliable, but they do not guarantee the accuracy or completeness of the information. Although we believe that these sources are reliable, we have not independently verified the information contained in such publications. Certain estimates and forecasts involve uncertainties and risks and are subject to change based on various factors, including those discussed under the headings "—Special Note Regarding Forward-Looking Statements" and "Item 3.D—Risk Factors" in this annual report.

Throughout this annual report, we refer to various trademarks, service marks and trade names that we use in our business. The "Wix.com" design logo is the property of Wix.com Ltd. Wix® is our registered trademark in the United States. We have several other trademarks, service marks and pending applications relating to our solutions. Other trademarks and service marks appearing in this annual report are the property of their respective holders.

SPECIAL NOTE REGARDING FORWARD-LOOKING STATEMENTS

We make forward-looking statements in this annual report that are subject to risks and uncertainties. These forward-looking statements include information about possible or assumed future results of our business, financial condition, results of operations, liquidity, plans and objectives. In some cases, you can identify forward-looking statements by terminology such as "believe," "may," "estimate," "continue," "anticipate," "intend," "should," "plan," "expect," "predict," "potential," or the negative of these terms or other similar expressions. The statements we make regarding the following matters are forward-looking by their nature:

- •

- our expectations regarding future changes in our cost of revenues and our operating expenses on an absolute basis and as a

percentage of our revenues;

- •

- our expectation that the percentage of revenues we derive from outside of North America will increase in the future;

- •

- our expectation that the percentage of revenues we derive from premium subscriptions will increase in the future;

- •

- our planned level of capital expenditures and our belief that our existing cash and cash from operations will be

sufficient to fund our operations for at least the next twelve months; and

- •

- our plans to make our product, support and communication channels available in additional languages and to expand our payment infrastructure to transact in additional local currencies and accept additional payment methods.

The preceding list is not intended to be an exhaustive list of all of our forward-looking statements. The forward-looking statements are based on our beliefs, assumptions and expectations of future performance, taking into account the information currently available to us. These statements are only predictions based upon our current expectations and projections about future events. There are important factors that could cause our actual results, levels of activity, performance or achievements to differ materially from the results, levels of activity, performance or achievements expressed or implied by the forward-looking statements. In particular, you should consider the risks provided under "Item 3.D—Risk Factors" in this annual report.

i

You should not rely upon forward-looking statements as predictions of future events. Although we believe that the expectations reflected in the forward-looking statements are reasonable, we cannot guarantee that future results, levels of activity, performance and events and circumstances reflected in the forward-looking statements will be achieved or will occur. Except as required by law, we undertake no obligation to update publicly any forward-looking statements for any reason after the date of this annual report, to conform these statements to actual results or to changes in our expectations.

ii

Item 1. IDENTITY OF DIRECTORS, SENIOR MANAGEMENT AND ADVISERS

Not applicable.

Item 2. OFFER STATISTICS AND EXPECTED TIMETABLE

Not applicable.

A. Selected Financial Data

The following tables set forth our selected consolidated financial data. You should read the following selected consolidated financial data in conjunction with "Item 5. Operating and Financial Review and Prospects" and our consolidated financial statements and related notes included elsewhere in this annual report. Historical results are not necessarily indicative of the results that may be expected in the future. Our financial statements have been prepared in accordance with U.S. Generally Accepted Accounting Principles, or U.S. GAAP.

The selected consolidated statements of operations data for each of the years in the three-year period ended December 31, 2013 and the consolidated balance sheet data as of December 31, 2012 and 2013 are derived from our audited consolidated financial statements appearing elsewhere in this annual report. The consolidated statements of operations data for the year ended December 31, 2010 and the consolidated balance sheet data as of December 31, 2010 and 2011 are derived from our audited consolidated financial statements that are not included in this annual report. Selected consolidated financial information as of December 31, 2009 and for the year ended December 31, 2009 has been omitted because such information could not be provided without unreasonable effort or expense.

| |

Year Ended December 31, | ||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| |

2010 | 2011 | 2012 | 2013 | |||||||||

| |

(in thousands except share and per share data) |

||||||||||||

Consolidated Statements of Operations: |

|||||||||||||

Revenues |

$ | 9,850 | $ | 24,600 | $ | 43,676 | $ | 80,473 | |||||

Cost of revenues(1) |

2,223 | 5,290 | 9,233 | 15,257 | |||||||||

| | | | | | | | | | | | | | |

Gross profit |

7,627 | 19,310 | 34,443 | 65,216 | |||||||||

| | | | | | | | | | | | | | |

Operating expenses: |

|||||||||||||

Research and development(1) |

7,315 | 14,746 | 16,782 | 29,660 | |||||||||

Selling and marketing(1) |

9,848 | 21,586 | 29,057 | 53,776 | |||||||||

General and administrative(1) |

1,779 | 5,338 | 3,565 | 8,307 | |||||||||

| | | | | | | | | | | | | | |

Total operating expenses |

18,942 | 41,670 | 49,404 | 91,743 | |||||||||

| | | | | | | | | | | | | | |

Operating loss |

(11,315 | ) | (22,360 | ) | (14,961 | ) | (26,527 | ) | |||||

Financial income (expenses), net |

(19 | ) | (41 | ) | 487 | (603 | ) | ||||||

Other expenses |

— | 127 | 2 | 18 | |||||||||

| | | | | | | | | | | | | | |

Loss before taxes on income |

(11,334 | ) | (22,528 | ) | (14,476 | ) | (27,148 | ) | |||||

Taxes on income |

155 | 212 | 496 | 1,572 | |||||||||

| | | | | | | | | | | | | | |

Net loss |

$ | (11,489 | ) | $ | (22,740 | ) | $ | (14,972 | ) | $ | (28,720 | ) | |

| | | | | | | | | | | | | | |

| | | | | | | | | | | | | | |

Basic and diluted net loss per ordinary share(2) |

$ | (4.30 | ) | $ | (8.31 | ) | $ | (2.71 | ) | $ | (3.33 | ) | |

| | | | | | | | | | | | | | |

| | | | | | | | | | | | | | |

Weighted average number of ordinary shares used in computing basic and diluted net loss per ordinary share(2) |

5,835,897 | 6,355,428 | 6,822,720 | 11,597,826 | |||||||||

| | | | | | | | | | | | | | |

| | | | | | | | | | | | | | |

1

| |

As of December 31, | ||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| |

2010 | 2011 | 2012 | 2013 | |||||||||

| |

(in thousands) |

||||||||||||

Consolidated Balance Sheet Data: |

|||||||||||||

Cash and cash equivalents |

$ | 4,501 | $ | 10,374 | $ | 7,510 | $ | 101,258 | |||||

Restricted deposits |

1,358 | 4,164 | 2,536 | 3,306 | |||||||||

Total assets |

7,631 | 18,577 | 16,055 | 115,355 | |||||||||

Deferred revenues |

5,133 | 10,181 | 18,984 | 37,184 | |||||||||

Total shareholders' equity (deficiency) |

(16 | ) | 3,086 | (10,571 | ) | 62,296 | |||||||

| |

Year Ended December 31, | ||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| |

2010 | 2011 | 2012 | 2013 | |||||||||

| |

(dollars in thousands) |

||||||||||||

Supplemental Financial and Operating Data: |

|||||||||||||

Collections(3) |

$ | 13,753 | $ | 29,648 | $ | 52,479 | $ | 98,673 | |||||

Free cash flow(4) |

$ | (6,374 | ) | $ | (12,353 | ) | $ | (4,555 | ) | $ | 1,173 | ||

Adjusted EBITDA(5) |

$ | (10,085 | ) | $ | (17,035 | ) | $ | (13,070 | ) | $ | (18,244 | ) | |

Number of registered users at period end(6) |

6,523,968 | 16,951,837 | 28,225,857 | 42,126,246 | |||||||||

Number of premium subscriptions at period end(7) |

149,084 | 298,143 | 469,589 | 789,753 | |||||||||

- (1)

- Includes share-based compensation expense as follows:

| |

Year Ended December 31, | ||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| |

2010 | 2011 | 2012 | 2013 | |||||||||

| |

(in thousands) |

||||||||||||

Cost of revenues |

$ | 14 | $ | 40 | $ | 105 | $ | 490 | |||||

Research and development |

659 | 1,939 | 553 | 3,149 | |||||||||

Selling and marketing |

95 | 222 | 101 | 1,185 | |||||||||

General and administrative |

343 | 2,532 | 261 | 2,230 | |||||||||

| | | | | | | | | | | | | | |

Total share-based compensation expense |

$ | 1,111 | $ | 4,733 | $ | 1,020 | $ | 7,054 | |||||

| | | | | | | | | | | | | | |

| | | | | | | | | | | | | | |

- (2)

- Basic

and diluted net loss per ordinary share is computed based on the weighted average number of ordinary shares outstanding during each period. For

additional information, see Notes 2p and 11 to our consolidated financial statements included elsewhere in this annual report.

- (3)

- Collections is a non-GAAP financial measure that we define as total cash collected by us from our customers in a given period. Collections is calculated by adding the change in deferred revenues for a particular period to revenues for the same period. Collections consists primarily of amounts from annual and monthly premium subscriptions by users, which are deferred and recognized as revenues over the terms of the subscriptions and payments by our users for domains, which are also recognized ratably over the term of the service period. The following table reconciles revenues, the most directly comparable U.S. GAAP measure, to collections for the periods presented:

| |

Year Ended December 31, | ||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| |

2010 | 2011 | 2012 | 2013 | |||||||||

| |

(in thousands) |

||||||||||||

Reconciliation of Revenues to Collections: |

|||||||||||||

Revenues |

$ | 9,850 | $ | 24,600 | $ | 43,676 | $ | 80,473 | |||||

Change in long-term and short-term deferred revenues |

3,903 | 5,048 | 8,803 | 18,200 | |||||||||

| | | | | | | | | | | | | | |

Collections |

$ | 13,753 | $ | 29,648 | $ | 52,479 | $ | 98,673 | |||||

| | | | | | | | | | | | | | |

| | | | | | | | | | | | | | |

For a description of how we use collections to evaluate our business, see "Item 5. Operating and Financial Review and Prospects—Key Financial and Operating Metrics." We believe that this non-GAAP financial measure is useful in evaluating our business because it is a leading indicator of our revenue growth and the growth of our overall business. Nevertheless, this information should be considered as supplemental in nature and is not meant as a substitute for revenues recognized in accordance with U.S. GAAP. Other companies, including companies in our industry, may calculate collections differently or not at all, which reduces their usefulness as a comparative measure. You should consider collections along with other

2

financial performance measures, including revenues, net cash used in operating activities, and our financial results presented in accordance with U.S. GAAP.

- (4)

- Free cash flow is a non-GAAP measure defined as cash flow from operating activities minus capital expenditures. The following table reconciles cash flow from operating activities, the most directly comparable U.S. GAAP measure, to free cash flow:

| |

Year Ended December 31, | ||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| |

2010 | 2011 | 2012 | 2013 | |||||||||

| |

(in thousands) |

||||||||||||

Reconciliation of cash flow provided by (used in) operating activities to free cash flow: |

|||||||||||||

Net cash provided by (used in) operating activities |

$ | (5,310 | ) | $ | (10,599 | ) | $ | (3,608 | ) | $ | 4,243 | ||

Capital expenditures(1) |

(1,064 | ) | (1,754 | ) | (947 | ) | (3,070 | ) | |||||

| | | | | | | | | | | | | | |

Free cash flow |

$ | (6,374 | ) | $ | (12,353 | ) | $ | (4,555 | ) | $ | 1,173 | ||

| | | | | | | | | | | | | | |

| | | | | | | | | | | | | | |

- (1)

- Capital expenditures consist primarily of investments in leasehold improvements for our office space and the purchase of computers and related equipment.

For a description of how we use free cash flow to evaluate our business, see "Item 5. Operating and Financial Review and Prospects—Key Financial and Operating Metrics." We believe that this non-GAAP financial measure is useful in evaluating our business because free cash flow reflects the cash surplus available or used to fund the expansion of our business after payment of capital expenditures relating to the necessary components of ongoing operations. Nevertheless, this information should be considered as supplemental in nature and is not meant as a substitute for net cash flows from operating activities presented in accordance with U.S. GAAP. Other companies, including companies in our industry, may calculate free cash flow differently or not at all, which reduces their usefulness as a comparative measure. You should consider free cash flow along with other financial performance measures, including revenues, net cash used in operating activities, and our financial results presented in accordance with U.S. GAAP.

- (5)

- Adjusted EBITDA is a non-GAAP financial measure that we define as net loss before financial expenses (income), net, other expenses, taxes on income, depreciation and share-based compensation expense. The following table reconciles net loss, the most directly comparable U.S. GAAP measure, to adjusted EBITDA for the periods presented:

| |

Year Ended December 31, | ||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| |

2010 | 2011 | 2012 | 2013 | |||||||||

| |

(in thousands) |

||||||||||||

Adjusted EBITDA |

|||||||||||||

Net loss |

$ | (11,489 | ) | $ | (22,740 | ) | $ | (14,972 | ) | $ | (28,720 | ) | |

Financial expenses (income), net |

19 | 41 | (487 | ) | 603 | ||||||||

Other expenses |

— | 127 | 2 | 18 | |||||||||

Taxes on income |

155 | 212 | 496 | 1,572 | |||||||||

Depreciation |

119 | 592 | 871 | 1,229 | |||||||||

Share-based compensation expense |

1,111 | 4,733 | 1,020 | 7,054 | |||||||||

Total adjustments |

1,404 | 5,705 | 1,902 | 10,476 | |||||||||

| | | | | | | | | | | | | | |

Adjusted EBITDA |

$ | (10,085 | ) | $ | (17,035 | ) | $ | (13,070 | ) | $ | (18,244 | ) | |

| | | | | | | | | | | | | | |

| | | | | | | | | | | | | | |

For a description of how we use adjusted EBITDA to evaluate our business, see "Item 5. Operating and Financial Review and Prospects—Key Financial and Operating Metrics." We believe that this non-GAAP financial measure is useful in evaluating our business because the exclusion of certain expenses in calculating adjusted EBITDA can provide a useful measure for period-to-period comparisons of our core business. Nevertheless, this information should be considered as supplemental in nature and is not meant as a substitute for net loss recognized in accordance with U.S. GAAP. Other companies, including companies in our industry, may calculate adjusted EBITDA differently or not at all, which reduces their usefulness as a comparative measure. You should consider adjusted EBITDA along with other financial performance measures, including revenues, net cash used in operating activities, and our financial results presented in accordance with U.S. GAAP.

- (6)

- Number of registered users at period end is defined as the total number of users, including those who purchase premium subscriptions, who are registered with Wix.com with a unique email address at the end of the period. The length of time that users take following registration to design and publish a website varies significantly from hours to years, and many users never publish a website. We have no means of assessing the level of engagement of a particular user following registration or how close a user is to potentially publishing their website. Accordingly, our use of the term "user" herein is not intended to necessarily indicate a level of engagement. See "—D. Risk Factors—Risks Related Our Business and Our

3

Industry—The number of our registered users may be higher than the number of actual users and we have no means of assessing the level of engagement of a particular user following registration."

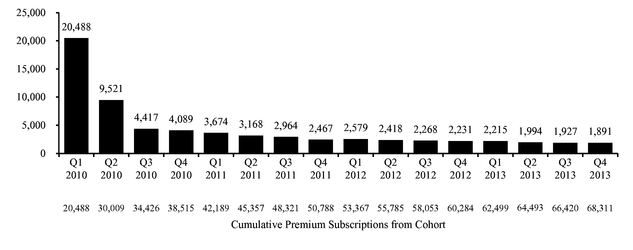

- (7)

- A single user can purchase multiple premium subscriptions. Our premium subscriptions in any given period are derived from users that registered with us during that period and a range of prior periods with the largest contribution from most recently registered users. See "Item 5. Operating and Financial Review and Prospects—Overview—Premium Subscription Analysis."

B. Capitalization and Indebtedness

Not applicable.

C. Reasons for the Offer and Use of Proceeds

Not applicable.

D. Risk Factors

Our business faces significant risks. You should carefully consider all of the information set forth in this annual report and in our other filings with the United States Securities and Exchange Commission ("SEC"), including the following risk factors which we face and which are faced by our industry. Our business, financial condition and results of operations could be materially and adversely affected by any of these risks. In that event, the trading price of our ordinary shares would likely decline and you might lose all or part of your investment. This report also contains forward-looking statements that involve risks and uncertainties. Our results could materially differ from those anticipated in these forward-looking statements, as a result of certain factors including the risks described below and elsewhere in this report and our other SEC filings. See "Special Note Regarding Forward-Looking Statements" on page i.

4

Risks Related to Our Business and Our Industry

Our results of operations and future prospects will be harmed if we are unable to attract new registered users and premium subscriptions at a sufficient rate.

The number of new registered users we attract is a key factor in growing our premium subscription base, which in turn drives our revenues and collections. To date, we have grown the number of registered users and premium subscriptions through the provision of complimentary user-friendly, drag-and-drop web development, design and management software, which can be upgraded to a subscription-based package with various additional solutions and services. Over half of our new premium subscriptions in any given month are generated by users who registered in earlier months. We therefore attribute considerable importance to continued growth of our user base since they are our primary source of premium subscriptions. Although we do not expect to maintain the same period-over-period user and premium subscription growth rate that we have experienced in recent quarters, we do seek to add a larger absolute number of registered users and premium subscriptions each quarter in the immediate future. A number of factors could impact our ability to attract new registered users and premium subscriptions, including:

- •

- the quality and design of our platform compared to other similar solutions and services;

- •

- our ability to develop new technologies or offer new products and service offerings;

- •

- the pricing of our solutions and services compared to our competitors;

- •

- the reliability and availability of our customer service; and

- •

- our ability to provide value-added third-party applications, solutions and services that integrate into our solutions.

Our results of operations would be adversely affected if our selling and marketing activities fail to generate traffic to our website, users and premium subscriptions at the levels that we anticipate.

We acquire many of our users through paid marketing channels, such as cost-per-click advertisements on search engines and social networking sites and targeted and generic banner advertisements on other sites. A portion of the users acquired through these channels purchase premium subscriptions over time. In order to maintain our current revenues and grow our business, we need to continuously optimize marketing campaigns aimed at acquiring new registered users and premium subscriptions. In the years ended December 31, 2011, 2012 and 2013, selling and marketing expenses were $21.6 million, $29.1 million and $53.8 million, respectively, representing 88%, 67% and 67% of our revenues, respectively. We conduct search engine optimization and A/B testing, a marketing approach which aims to identify which changes to our website will increase or maximize user interest and user acquisition. We also rely upon the assumption that historical user behavior can be extrapolated to predict future user behavior, and we structure our marketing activities in the manner that we believe is most likely to encourage the user behaviors that lead to desired future outcomes, such as purchasing premium subscriptions. However, we may fail to accurately predict user acquisition, interest, or to fully understand or estimate the conditions and behaviors that drove historical user behavior and thus, fail to generate the return on marketing we expected. For example, events outside our control, such as announcements by our competitors or other third-parties of significant business developments, have in the past adversely affected the returns we had anticipated on our marketing expenses in the short-term. In addition, we have recently started to direct a portion of our marketing expenses towards more traditional advertising, including radio and television commercials, the effectiveness of which is more difficult to track than online marketing. If any of our marketing campaigns prove less successful than anticipated in attracting users and premium subscriptions, we may not achieve our return-on-investment targets, and our rate of user and premium subscription acquisition may fail to meet market expectations, which could have a material adverse effect on our share price.

5

Our limited operating history in a new and developing market makes it difficult to evaluate our current business and future prospects, and may increase the risk that we will not be successful.

We were founded in 2006 and the majority of our revenue growth has occurred since 2011. This short history makes it difficult to assess effectively our future prospects. We also operate in a new and developing market that may not develop as expected. We believe that the growth in our user base and revenues may indicate that our business strategy is successful, but you should consider our future prospects in light of the challenges and uncertainties that we face, including the fact that our business has grown rapidly and it may not be possible to discern fully the trends that we are subject to, that we operate in a new and developing market, and that elements of our business strategy are new and subject to ongoing development.

We have a history of operating losses and may not be able to achieve profitability in the future.

We have incurred net losses in each fiscal year since our inception and, as of December 31, 2013, we had an accumulated deficit of $88.5 million. We expect that our operating expenses will continue to increase in the near term at a rate that will offset all or substantially all of any future growth in revenues. We believe that this increase in operating expenses will result primarily from increased selling and marketing expenses related to user acquisition activities and increased research and development expenses related to enhancing the functionality of our solutions. We seek to leverage these expenses across a growing base of premium subscriptions while maintaining or increasing the amount of revenues per premium subscription in order to achieve profitability. As a result, if we are unable to grow our premium subscriptions at the required rate or to maintain or increase revenues per user, or if we incur unexpected expenses, we may be unable to achieve or sustain profitable operations.

A decrease in annual subscriptions or renewal rates of our existing premium subscriptions could adversely impact our collections and revenues, and harm our ability to forecast our business.

The rate at which annual premium subscriptions are purchased and the rate at which premium subscriptions are renewed significantly impact the overall number of premium subscriptions and, as a result, our collections and our revenues. Our annual subscription renewal rates have historically increased based on the length of time a subscription has been active. One of the key drivers of renewal rates is whether premium subscriptions are annual or monthly. Annual subscriptions have higher renewal rates than monthly subscriptions since there is one-twelfth as many opportunities in a given annual period to fail to renew a subscription than a monthly subscription whether deliberately or through failure to update credit card information upon expiration. As such, our overall renewal rates may drop if there is a decrease in the number of premium annual subscriptions compared to premium monthly subscriptions, and will affect our ability to forecast our future results of operations. If the number of annual premium subscriptions or renewal rates fail to meet our expectations, our profitability and future prospects may be adversely impacted.

If we are unable to maintain and enhance our brand, or if events occur that damage our reputation and brand, our ability to expand our base of users and premium subscriptions may be impaired, and our business and financial results may be harmed.

Maintaining, promoting and enhancing the Wix brand is critical to expanding our base of users and premium subscriptions. For both users and premium subscriptions, we market our solutions and services primarily through cost-per-click advertisements on search engines and social networking sites, participation in social networking sites, and free and paid banner advertisements on other websites, and small Wix advertisements on our users' websites that do not currently have a premium subscription. Our ability to attract additional users depends in part on increasing our brand recognition. In addition, our solutions and services are also marketed through free traffic sources, including customer referrals, word-of-mouth and direct searches for our "Wix" name, or web presence solutions, in search engines.

6

Maintaining and enhancing our brand will depend largely on our ability to continue to provide high-quality, well-designed, useful, reliable, and innovative solutions and services, which we may not do successfully. We may introduce new solutions or terms of service that users do not like, which may negatively affect our brand. Additionally, if users have a negative experience using third-party applications and websites integrated with Wix, such an experience may affect our brand. Our Wix Arena Marketplace enables independent web designers to offer their services to users who engage them directly. As we conduct only a limited evaluation of these designers' credentials, our reputation may be harmed if any of the services provided by these independent designers do not meet users' quality expectations. Maintaining and enhancing our brand may require us to make substantial investments and these investments may not be successful. Additionally, errors, defects, disruptions or other performance problems with our products and platform, including the products and solutions we license from third parties, may reduce our revenue, harm our reputation and brand and adversely affect our ability to attract new users and premium subscriptions, especially if these errors occur when we introduce new services or features. If we fail to successfully promote and maintain the Wix brand or if we incur excessive expenses in this effort, we could be subject to claims regarding our business and financial results may be adversely affected.

Our results of operations and business could be harmed if we fail to manage the growth of our infrastructure effectively.

We have experienced rapid growth in our business and operations, which places substantial demands on our operational infrastructure. The scalability and flexibility of our cloud-based infrastructure depends on the functionality of our third-party servers and their ability to handle increased traffic and demand for bandwidth. The significant growth in the number of users and transactions has increased the amount of both our stored marketing and research data and the data of our users. Any loss of such data due to disruptions in our infrastructure could result in harm to our brand or reputation. Moreover, as our user base grows, and as users use our platform for more complicated tasks, we will need to devote additional resources to improving our infrastructure and continuing to enhance its scalability in order to maintain the performance of our platform and solutions. Our need to effectively manage our operations and growth will also require that we continue to assess and improve our operational, financial and management controls, reporting systems and procedures. We may encounter difficulties obtaining the necessary personnel or expertise to improve those controls, systems and procedures on a timely basis relative to our growth. If we do not manage the growth of our business and operations effectively, the quality of our platform and efficiency of our operations could suffer, which could harm our results of operations and business.

Failures or loss of the third-party hardware, software and infrastructure on which we rely, including third-party data center hosting facilities, could adversely affect our business.

We rely on leased servers, cloud service providers and other third-party hardware and infrastructure to support our operations. Our primary data centers are in two geographically separate locations in the United States with a back-up data center in Europe. We lease our primary data centers in the United States from Hostway Services, Inc. pursuant to purchase orders issued under an agreement that automatically renews on an annual basis unless terminated by us by notice at least 60 days before the annual renewal date or by either party at any time with 180 days advance notice. We currently sublease cloud storage from Amazon.com, Inc. and Google Inc. If Hostway ceases to make its data centers available to us without sufficient advance notice or if we are unable to utilize cloud services from Amazon and Google, we would likely experience delays in delivering our solutions until migration to an alternate data center provider is completed.

The owners and operators of these data centers and cloud services do not guarantee that our users' access to our platform will be uninterrupted or error-free. We do not control the operation of

7

these facilities and such facilities could be subject to break-ins, computer viruses, sabotage, intentional acts of vandalism and other misconduct. Additionally, cloud services could be subject to breaches of cyber security. We and our hosting providers have in the past been subject to cyber-attacks, which have caused interruptions in our service. For example, in February 2014, we were the target of a malicious denial-of-service, or DDoS, attack, a technique used by hackers to take an internet service offline by overloading its servers. While we have robust systems in place to counter such attacks, the scale of this particular attack caused us and some of our user websites to experience significant but intermittent downtime. While throughout this attack, we were able to guarantee that the vast majority of websites remained live and unaffected and all of our users' personal data, including billing information, were secure, we cannot guarantee that future attacks may not have more dire consequences. Further, our servers and data centers are vulnerable to damage or interruption from fires, natural disasters, terrorist attacks, power loss, telecommunications failures or similar catastrophic events. Moreover, if for any reason our arrangement with one or more of the providers of the servers that we use is terminated, we could incur additional expenses in arranging for new facilities and support. Disruptions to these servers could interrupt our ability to provide our platform and solutions and materially and adversely affect our business and results of operations.

We rely on search engines and social networking sites to attract a meaningful portion of our users, and if those search engines or social networking sites change their listings or policies regarding advertising, or increase their pricing or suffer problems, it may limit our ability to attract new users.

We rely on search engines and social networking sites to attract new users, and many of our users locate our website and solutions by clicking through on search results displayed by search engines such as Google and Yahoo!, and advertisements on social networking sites such as Facebook. Search engines typically provide two types of search results, natural (i.e., non-paid) and purchased listings. Natural search results are determined and organized solely by automated criteria set by the search engine and a ranking level cannot be purchased. Advertisers can also pay search engines to place listings more prominently in search results and websites in order to attract users to advertisers' websites. To some extent, we rely on natural searches in order to attract free traffic to our website. Search engines revise their algorithms from time to time in an attempt to optimize their search result listings. If search engines on which we rely for algorithmic listings modify their algorithms, our websites may appear less prominently or not at all in search results, which could result in fewer users clicking through to our website. For example, in one instance in the past, traffic was mistakenly directed to one of our homepages that was not in the language of the search performed and resulted in lower users and premium subscriptions for that period. Furthermore, competitors may in the future bid on our name from search services in an attempt to capture potential traffic. Preventing such actions and recapturing potential traffic could increase our expenses. Further, search engines or social networking sites may change their policies from time to time regarding pay-per-click or other means of advertising. If any change to these policies delays or prevents us from advertising these through channels, this could result in fewer users clicking through to our website.

We may face challenges expanding our premium subscription base and increasing revenues in emerging markets due to difficulties in these markets associated with payment collections as well as legal, economic, tax and political risks that are greater than more developed markets.

Expanding our business into emerging markets is an important component of our growth strategy and presents challenges that are different than those associated with more developed international markets. In particular, regulations limiting the use of local credit cards could constrain our growth in certain countries. For example, regulations in certain countries do not permit recurring charges on credit cards. In the last quarter of 2011, we established a Brazilian subsidiary to process local credit cards in Brazil in compliance with Brazilian currency controls. It is often difficult to establish an effective local business model, and we may need to enter into agreements with third-parties to process

8

credit cards on our behalf or modify our business plans or operations in order to establish a local presence in emerging countries, which may delay our entry into these markets or increase our costs. Additionally, in emerging markets we face the risk of more rapidly changing government policies and encountering sudden currency revaluations. It is possible that governments of one or more countries may censor or block access to the Internet due to political concerns or in response to certain incidents or significant events, thereby preventing people in these countries, including our users, from accessing our products. The growth of our business may be adversely affected if we are unable to expand our user base in emerging markets.

We face potential liability and expense for legal claims based on the content on our platform.

Our platform allows users to create websites. At present, we do not require that our users post on their websites, or require their visitors to agree to, any terms of service, privacy policy, disclaimer or any other contractual documentation or policy. If our users do not post or require agreement to the appropriate documentation and policies on their websites, or should our users fail to take steps necessary to enjoy the benefits of certain statutory safe harbors, such as those set forth in Section 512 of the United States Copyright Act and Section 230 of the Communication Decency Act, then they may expose themselves to civil and criminal liability under applicable law, for example, where the visitors post information which is libelous, defamatory, in breach of regulation concerning unacceptable content or publications, or in breach of any third-party intellectual property rights or where our users or their suppliers fail to process personal data in accordance with applicable law. It is possible that we could also be subject to liability. In many jurisdictions, including the United States and countries in Europe, laws relating to the liability of providers of online services for activities of their users and other third parties are currently being tested by a number of claims, including actions based on defamation, invasion of privacy and other torts, unfair competition, copyright and trademark infringement, and other theories based on the nature and content of the materials searched, the ads posted, or the content provided by users. Any court ruling or other governmental action that imposes liability on providers of online services for the activities of their users and other third parties could harm our business. In such circumstances we may also be subject to liability under applicable law in a way which may not be fully mitigated by the user terms of service we require our users to agree to. Any liability attributed to us could adversely affect our brand, reputation, our ability to expand our user base and our financial position. Further, our indemnity from the users may also not be fully effective as a matter of practice if any user does not have sufficient assets, insurance or other means to back that indemnity. In addition, rising concern about the use of the Internet for illegal conduct, such as the unauthorized dissemination of national security information, money laundering or supporting terrorist activities may in the future produce legislation or other governmental action that could require changes to our products, solutions or services, restrict or impose additional costs upon the conduct of our business or cause users to abandon material aspects of our service. Any such adverse legal or regulatory developments could substantially harm our operating results and business.

Activities of users or the content of their websites could damage our reputation and brand, or harm our ability to expand our base of users and premium subscriptions, and our business and financial results.

Our reputation and brand may be negatively affected by the actions of users that are deemed to be hostile, offensive or inappropriate to other users, or by users acting under false or inauthentic identities. This particularly applies to our users who do not have premium subscriptions and who therefore maintain the "Wix" logo on their websites. We do not monitor or review the appropriateness of the domain names our users register or the content of our users' websites, and we do not have control over the activities in which our users engage. While we have adopted policies regarding illegal or offensive use of our services by our users and retain authority to terminate domain name registrations and to take down websites that violate these policies, users could nonetheless engage in these activities. The safeguards we have in place may not be sufficient to avoid harm to our reputation and brand, especially if such hostile, offensive or inappropriate use was high profile, which could adversely affect our ability to expand our user base, and our business and financial results.

9

We are exposed to risks associated with credit card and debit card payment processing.

We accept payments primarily through credit and debit card transactions and currently use an internal billing system, as well as third-party billing systems that are integrated into our website and provide a portal for users to submit credit or debit card information for processing. We are subject to a number of risks related to credit and debit card payments, including:

- •

- we pay interchange and other fees, which may increase over time and could require us to either increase the prices we

charge for our products or experience an increase in our operating expenses;

- •

- if our billing systems fail to work properly and, as a result, we do not automatically charge our premium subscriptions'

credit cards on a timely basis or at all, we could lose revenues; and

- •

- if we are unable to maintain our chargeback rate at acceptable levels, our credit card fees for chargeback transactions, or our fees for other credit and debit card transactions or issuers, may increase, or issuers may terminate their relationship with us.

Our internal billing system interfaces with a number of different of gateway providers that link to a number of different payment card processors based on the jurisdiction and other factors. In connection with this system, we have implemented data security standards, operating rules and certification requirements in accordance with Payment Card Industry, or PCI, Data Security Standards in connection with internal controls requirements under Israeli law and we have maintained PCI compliance level 1 certification since February 2013. There can be no assurance that our billing system data security standards, or those of our third-party billing service providers, will adequately comply with the billing standards of any future jurisdiction in which we seek to market our service offering and establish a local billing solution.

If third-party applications change such that we do not or cannot maintain the compatibility of our platform and solutions with these applications or if we fail to provide third-party applications that our users desire to add to their websites, demand for our solutions and platform could decline.

The attractiveness of our platform depends, in part, on our ability to integrate third-party applications which our users desire into their websites. Third-party application providers may change the features of their applications and platforms or alter the terms governing use of their applications and platforms in an adverse manner. Further, third-party application providers may refuse to partner with us, or limit or restrict our access to their applications and platforms. Such changes could functionally limit or terminate our ability to use these third-party applications and platforms with our platform, which could negatively impact our offerings and harm our business. If we fail to integrate our platform with new third-party applications that our users need for their websites, or to adapt to the data transfer requirements of such third-party applications and platforms, we may not be able to offer the functionality that our users expect, which would negatively impact our offerings and, as a result, harm our business.

Our business and prospects would be harmed if changes to technologies used in our solutions or new versions or upgrades of operating systems and Internet browsers adversely impact the process by which users interface with our platform.

The user interface for our platform is currently simple and straightforward, which we believe has helped us to expand our user base even among users with little technical expertise. In the future, Microsoft, the dominant operating system provider, or any other provider of Internet browsers, could introduce new features that would make it difficult to use our platform. In addition, Internet browsers for desktop or mobile devices could introduce new features, or change existing browser specifications such that they would be incompatible with our products and solutions, or prevent end users from

10

accessing our users' sites. For example, operating systems or major Internet browsers such as Firefox, Internet Explorer or Safari, could become unstable or be incompatible with HTML5-based products and solutions. Any changes to technologies used in our solutions, including within operating systems or Internet browsers that make it difficult for users to access our platform or end-users to access our users' sites, may slow the growth of our user base, and adversely impact our business and prospects.

Our ability to enhance our products may be harmed if we are unable to attract and retain sufficient research and development personnel.

In order to remain competitive, we must continue to develop new solutions, applications and enhancements to our existing platform. Our principal research and development activities are conducted from our headquarters in Tel Aviv, Israel, and we face significant competition for suitably skilled developers in this region. We also engage a small number of developers in Ukraine through a third-party service organization in order to benefit from the significant pool of talent that is more readily available in that market. Many larger companies expend considerably greater amounts on employee recruitment and may be able to offer more favorable compensation and incentive packages than us. If we cannot attract or retain sufficient skilled research and development employees, our business, prospects and results of operations could be adversely affected.

Our future prospects may be adversely affected if we are unable to generate revenues from sources other than our premium subscription packages.

In addition to our editor, we provide all of our users with access to additional products and services that enhance their digital presence. For example, in the last quarter of 2012 we launched the Wix App Market, which is integrated into our platform. Through the App Market, we offer our users a range of software applications that can be integrated as add-ons to their free or premium websites. The App Market offers both applications that are developed by us and by third-party developers. We cannot offer any assurances that sales of applications or other value-added solutions and services we may offer in the future will be a significant part of our revenues. In addition, our selling efforts for these items may negatively impact our users' perception of us due to our email marketing to generate sales. If we do not succeed in selling these items, our future prospects may be adversely affected.

We may face increased competition in a highly competitive market.

While there are other providers who offer features similar to those features found in our solutions, we believe that we do not compete with traditional web development firms as we focus on not only web development but also technology, design and business work flow processes. Nevertheless, we do compete with aspects of the services provided by web-based website design platforms and software programs, as well as some of the service offerings of a number of smaller template-based web builder companies and designers, as well as those who offer domain registration services, particularly using a freemium business model similar to ours. In the future, we may experience increased competition from web design companies if they broaden their product and service offerings, or significantly lower their pricing. In addition, it is possible that other providers may in the future decide that offering a platform similar to our platform represents an attractive business opportunity. In particular, if a more established company were to target our market, we may face significant competition from a company that enjoys potential competitive advantages, such as greater name recognition, longer operating histories, substantially greater market share, larger existing user bases and substantially greater financial, technical and other resources. These companies may use these advantages to offer solutions and service similar to ours at a lower price, develop different solutions to compete with our current solutions and respond more quickly and effectively than we do to new or changing opportunities, technologies, standards or client requirements. Increased competition could result in us failing to attract users or obtain premium subscriptions at the same rate. It could also cause us to have higher acquisition costs

11

or force us to lower our prices or take other steps that may materially and adversely impact our results of operations.

If we fail to develop and introduce new products and services and keep up with rapid changes in design and technology, our business may be materially and adversely affected.

Our future success will depend on our ability to improve the look, function, performance and reliability of our solutions and services, including integrating Apps developed by third parties. The development of new and upgraded solutions and new service offerings involves a significant amount of time for our research and development team, as it can take our developers months to update, code and test new and upgraded solutions and integrate them into our platform. Further, our design team spends a significant amount of time and resources in order to incorporate various design elements, such as customized colors, fonts, content and other features into our new and upgraded solutions. The introduction of these new and upgraded design features, solutions and services also involves a significant amount of marketing spending. We must also manage our existing offerings, as we continually test, support, and market these solutions and applications. Our revenues and competitive position could be materially and adversely affected if we fail to improve our design features or technology, or if our solutions fail to achieve widespread acceptance.

Our corporate culture has contributed to our success, and if we cannot maintain this culture as we grow, we could lose the innovation, creativity, and teamwork fostered by our culture, and our business may be harmed.

We believe that an important contributor to our success has been our corporate culture, which we believe fosters innovation, teamwork, passion for our users, and a focus on attractive designs and technologically advanced products. Other than our executive officers, as a result of our growth most of our employees have been with us for fewer than two years. As we continue to grow, we must effectively integrate, develop and motivate a growing number of new employees, including employees in international markets. As a result, we may find it difficult to maintain important aspects of our corporate culture, which could limit our ability to innovate and operate effectively. Any failure to preserve our culture could also negatively affect our ability to retain and recruit personnel, continue to perform at current levels or execute on our business strategy.

If we fail to maintain a consistently high level of customer service, our brand, business and financial results may be harmed.

We believe our focus on customer support is critical to retaining, expanding and further penetrating our user base. As a result, we have invested in the quality and training of our customer support and call center personnel. If we are unable to maintain a consistently high level of customer service, we may lose existing users and find it more difficult to attract new users. In addition, regardless of the performance of our customer support and call center, users of online services base their purchasing decisions on a number of factors, including price, design, integration abilities, functionality of services, reputation and ease of use. If we fail to maintain adequate customer support which improves the functionality of our solutions and their ease of use, our reputation, financial results and business prospects may be harmed.

Our business relies on the experience and expertise of our senior management.

The success of our business is dependent to a large degree on the continued service of our executive officers. If we lose the services of any of our key personnel and fail to manage a smooth transition to new personnel, our business could suffer. We do not carry key person insurance on any of our executive officers or other key personnel. We have entered into employment and services agreements with our executive officers and key employees that contain non-compete covenants. Despite these agreements, we may not be able to retain these officers and employees. If we cannot enforce the

12

non-compete covenants, we may be unable to prevent our competitors from benefiting from the expertise of our former employees, which could materially and adversely affect our business and results of operations.

Our revenues may not increase if we are unable to maintain market share for mobile sites and applications, or if our mobile products fail to achieve widespread acceptance, which may affect our business and future prospects.

Consumers are increasingly accessing the Internet through devices other than personal computers, including mobile phones, smartphones and tablets. This trend has increased dramatically in the past few years and is projected to continue to increase. Acknowledging this trend, we launched our first free mobile offering in 2011, offering our users the ability to quickly and easily deploy an HTML5 mobile-optimized website and followed with a further enhanced mobile product in October 2013. The mobile device market is characterized by the frequent introduction of new products and solutions, short product life cycles, evolving industry standards, continuous improvement in performance characteristics and rapid adoption of technological and product advancements. We may incur additional costs in order to adapt our current functionalities to other operating systems and we may face technical challenges adapting our products to different versions of already supported operating systems, such as Android variants offered by different mobile phone manufacturers. If we are unable to offer continual improvements to our mobile solutions or adapt their functionalities to new and different operating systems, our mobile solutions may fail to achieve widespread acceptance by our users. Additionally, the providers of certain platforms, such as Apple, may limit or restrict access entirely to their platforms. Therefore, our revenues may not increase even if we continue to penetrate the mobile device market.

Exchange rate fluctuations may negatively affect our results of operations.

Our results of operations and cash flows are affected by fluctuations due to changes in foreign currency exchange rates. In 2013, approximately 80% of our revenues were denominated in U.S. dollars and approximately 20% in other currencies, primarily in euros, British pounds and the Brazilian Real. Conversely, in 2013, approximately 65% of our cost of revenues and operating expenses were denominated in U.S. dollars and approximately 35% in New Israeli Shekels, or NIS. Our NIS-denominated expenses consist primarily of personnel and overhead costs. Since a significant portion of our expenses are denominated in NIS, any appreciation of the NIS relative to the U.S. dollar would adversely impact our net loss or net income (if any). We estimate that a 10% increase (decrease) in the value of the NIS against the U.S. dollar would have decreased (increased) our net loss by approximately $3.8 million in 2013. To protect against the increase in value of forecasted foreign currency cash flow resulting from expenses paid in NIS during the year, we have instituted a foreign currency cash flow hedging program. We hedge portions of the anticipated payroll of our Israeli employees, Israeli suppliers and anticipated rent expenses of our Israeli premises denominated in NIS for a period of one to twelve months with forward contracts and other derivative instruments. In addition, in 2013, we also hedged a portion of our revenue transactions denominated in euros and British pounds. We cannot provide any assurances that our hedging activities will be successful in protecting us from adverse impacts from currency exchange rate fluctuations. See "Item 11. Quantitative and Qualitative Disclosures About Market Risk."

Because we recognize revenues from premium subscriptions over the term of an agreement, downturns or upturns in sales are not immediately reflected in full in our operating results.

We recognize revenues over the term of our contracts. During 2013, approximately 59% of our premium subscription revenues were from annual subscriptions and approximately 41% were from monthly subscriptions. As a result, much of the revenue we report each quarter is the recognition of deferred revenue from premium subscriptions entered into during previous quarters. Consequently, a

13

shortfall in demand for our solutions and services or a decline in new or renewed contracts in any one quarter may not significantly reduce our revenues for that quarter but could negatively affect our revenues in future quarters. Accordingly, the effect of significant downturns in new or renewed sales of our solutions and service offerings are not reflected in full in our results of operations until future periods.

The impact of worldwide economic conditions, including the resulting effect on spending by small to medium-sized businesses, may adversely affect our business, operating results and financial condition.

Our performance is subject to worldwide economic conditions and their impact on levels of spending by small and medium-sized businesses, which may be disproportionately affected by economic downturns. To the extent that worldwide economic conditions materially deteriorate, our existing and potential premium subscriptions may no longer consider investment in our solutions and platform a necessity, or may elect to reduce budgets for maintaining a digital presence. Economic conditions may adversely impact levels of user spending, which could adversely impact the numbers of users visiting our website. User purchases of discretionary items generally decline during recessionary periods and other periods in which disposable income is adversely affected, which could have a material adverse effect on our financial condition and results of operations.

Our business will suffer if the small business market for our solutions proves less lucrative than projected or if we fail to effectively acquire and service small business users.

We market and develop solutions for small businesses and a majority of our premium subscriptions are from small businesses. Small businesses frequently have limited budgets and may choose to allocate resources to items other than our solutions, especially in times of economic uncertainty or recessions. We believe that the small business market is underserved, and we intend to continue to devote substantial resources to it. We aim to grow our revenues by adding new small business customers, selling additional services to existing small business customers and encouraging existing small business customers to renew their subscriptions to our premium solutions. If the small business market fails to be as lucrative as we project or we are unable to market and sell our services to small businesses effectively, our ability to grow our revenues quickly and become profitable will be harmed.

We are subject to trade and economic sanctions and export laws that may govern or restrict our business and we, and our directors and officers, may be subject to fines or other penalties for non-compliance with those laws.

U.S. Laws and Regulations

We are subject to U.S. laws and regulations that may govern or restrict our business and activities in certain countries and with certain persons, including the trade and economic sanctions regulations administered by the U.S. Treasury Department's Office of Foreign Assets Control, or OFAC, and the export administration regulations administered by the U.S. Commerce Department's Bureau of Industry and Security, or BIS. In the course of an internal review in early 2013, we determined that we had 16 premium subscriptions, out of a total of approximately 583,000 premium subscriptions, with geographic internet protocols, or GEOIP, addresses in Cuba, Iran, North Korea, North Sudan or Syria ("U.S. Sanctioned Countries") or that had otherwise provided personal information indicating that they may be located in U.S. Sanctioned Countries. As part of a subsequent internal review, we also determined that we had 32,600 users, or less than 0.1% of our total user base of approximately 33 million as measured as of April 30, 2013, with GEOIP addresses in U.S. Sanctioned Countries.

In May 2013, we made a voluntary self-disclosure to OFAC and BIS. We cannot predict when OFAC and BIS will complete their respective reviews and determinations as to whether any violation of relevant U.S. sanctions or export laws occurred or is ongoing. In case of an apparent violation, OFAC

14

and/or BIS could decide not to impose penalties but issue only a warning or cautionary letter. However, if OFAC or BIS determines that we have violated applicable regulations, we may face civil and/or criminal penalties and may also suffer reputational harm, any of which could have a material adverse effect on our business and financial results.

We have undertaken a number of remedial measures, including terminating the users and the premium subscriptions that may have been from a U.S. Sanctioned Country, and blocking the ability of new users—with or without a premium subscription—that have a GEOIP address in a U.S. Sanctioned Country to access our cloud-based software or services. We have also since instituted new periodic screening practices and updated our systems to prevent users from U.S. Sanctioned Countries entering billing information with an address in that location. We are working to implement other measures related to our billing practices.

Israeli Laws and Regulations

The Israeli Trading with the Enemy Ordinance—1939 (the "Ordinance") prohibits any Israeli person from trading goods with enemy countries or with the residents of enemy countries. The Israeli Ministry of Finance, which is responsible for implementing the Ordinance, has currently determined enemy countries to be Iran, Lebanon and Syria ("Israeli Sanctioned Countries"). The Ordinance was enacted in 1939 and does not expressly address online services. We therefore cannot state with certainty how the provisions of the Ordinance apply to the type of services that we provide.

We voluntarily approached the Israeli Ministry of Finance in September 2013 and asked for its formal position regarding the applicability of the Ordinance to the type of services that we provide. We do not know the extent to which the Ministry of Finance will want to have further discussions with us, the timing of those discussions or the ultimate outcome of their deliberations. Although the Ordinance allows Israeli persons to apply for a permit to trade with Israeli Sanctioned Countries or their residents, we are not aware of a permit being granted or denied in the past to a person providing the type of services that we provide.

Lebanon is the only Israeli Sanctioned Country that is not also a U.S. Sanctioned Country. We have ceased providing services to users with a GEOIP address in a U.S. Sanctioned Country. The number of users and premium subscribers that we have in Lebanon is not material to our business. However, if we stop providing services in Lebanon, it may decrease the number of our current and future subscribers from other countries, particularly in the Middle East, who may cease using our services in protest to us blocking accounts in Israeli Sanctioned Countries.

In addition, if it is determined by a competent court that sanctions under the Ordinance cover the type of services that we provide, we, our officers and employees may be subject to criminal and/or civil actions. We believe that our initiation of voluntary discussions with the Israeli Ministry of Finance may reduce such exposure, but any liability to which we are subject to could adversely affect our personnel, brand and reputation.

We are subject to privacy and data protection laws and regulations as well as contractual privacy and data protection obligations, and our failure to comply with these or any future laws, regulations, or obligations could subject us to sanctions and damages and could harm our reputation and business.

We hold certain personal data of our users, primarily, username and email address, and may hold certain personal data of the visitors to our users' websites. We have implemented data security standards, operating rules and certification requirements in accordance with PCI Data Security Standards and we have maintained PCI compliance level 1 certification since February 2013. Since we began using our internal billing system in the first quarter of 2013, we have begun to also collect billing information, such as credit card numbers, full names, billing address and phone numbers in compliance with these data security standards. We do not regularly monitor or review the content that our users upload and store and, therefore, do not control the substance of the content within our hosted environment, including sensitive personal information.

15

We are subject to the privacy and data protection laws and regulations adopted by Israel and potentially, other jurisdictions. For example, although we do not have an operating entity in the Netherlands, the control that we exert over our servers in the Netherlands may result in our activities in Europe being deemed to be subject to Dutch law. Where the local data protection and privacy laws of a jurisdiction apply, we may be required to register our operations in that jurisdiction or make changes to our business so that user data is only collected and processed in accordance with applicable local law. Privacy laws restrict our storage, use, processing, disclosure, transfer and protection of personal information, including credit card data, provided to us by our users, and possibly the visitors to our users' websites. We strive to comply with all applicable laws, regulations, policies and legal obligations, as well as with certain industry standards (including voluntary third-party certification bodies such as TRUSTe) relating to privacy and data protection. We are also subject to the privacy and data security-related obligations set forth in our terms of use with our users, and we may be liable to third parties in the event we are deemed to have wrongfully processed personal data.

The regulatory framework for privacy and data security issues worldwide is currently in flux and is likely to remain so for the foreseeable future. In particular, the European Union has traditionally taken a broader view as to what is considered personal information and has imposed greater obligations under their privacy and data protection laws. For example, the European Union issued a proposal for a new General Data Protection Regulation at the beginning of 2012 which will replace the European Data Protection Directive and is likely to include more stringent obligations for online businesses, such as to conduct a data protection impact assessment for certain higher-risk processing operations, to introduce a more frequent need for the user's consent, to impose an obligation to act on data breaches, to restrict the collection and use of "sensitive" personal data and to expand the legislative requirements for data processors, as well as to introduce a stricter regime of enforcement. Additionally, the proposed regulation is stated to have extra-territorial effect and seeks to regulate the European activities of businesses regardless of their location or the locations of their servers. While it is currently expected that the proposed regulation will not take effect until 2015 or later, the more stringent requirements on privacy user notifications and data handling will require us to adapt our business and are likely to incur additional cost should we become subject to these and other laws and regulations, which could force us to incur material costs or require us to adapt our business.

A failure by us or a third-party contractor providing services to us to comply with applicable privacy and data security laws, regulations, self-regulatory requirements or industry guidelines, or our terms of use with our users, may result in sanctions, statutory or contractual damages or litigation. These proceedings or violations could force us to spend money in defense or settlement of these proceedings, result in the imposition of monetary liability, incur additional management resource, increase our costs of doing business, and adversely affect our reputation and the demand for our solutions.

If the security of the confidential information or personal information of our users and the visitors to our users' websites stored in our systems is breached or otherwise subjected to unauthorized access, our reputation may be harmed and we may be exposed to liability.