UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-Q

(Mark One)

For the quarterly period ended March 31, 2023

OR

For the transition period from to

Commission File Number 001-38088

(Exact name of registrant as specified in its charter)

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | ||||||||||||||||

(Address of Principal Executive Offices) | (Zip code) | ||||||||||||||||

(949 ) 349-1000

(Registrant’s telephone number, including area code)

Not Applicable

(Former name, former address, and former fiscal year, if changed since last report)

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||||||

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer | ☐ | ☒ | ||||||||||||

Non-accelerated filer | ☐ | Smaller reporting company | ||||||||||||

Emerging growth company | ||||||||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

As of April 14, 2023, 69,199,938 Class A common shares and 79,233,544 Class B common shares were outstanding.

FIVE POINT HOLDINGS, LLC

TABLE OF CONTENTS

FORM 10-Q

Page | ||||||||

PART I. FINANCIAL INFORMATION | ||||||||

ITEM 1. | ||||||||

ITEM 2. | ||||||||

ITEM 3. | ||||||||

ITEM 4. | ||||||||

PART II. OTHER INFORMATION | ||||||||

ITEM 1. | ||||||||

ITEM 1A. | ||||||||

ITEM 2. | ||||||||

ITEM 3. | ||||||||

ITEM 4. | ||||||||

ITEM 5. | ||||||||

ITEM 6. | ||||||||

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING STATEMENTS

This report contains forward-looking statements that are subject to risks and uncertainties. These statements concern expectations, beliefs, projections, plans and strategies, anticipated events or trends and similar expressions concerning matters that are not historical facts. When used, the words “anticipate,” “believe,” “expect,” “intend,” “may,” “might,” “plan,” “estimate,” “project,” “should,” “will,” “would,” “result” and similar expressions that do not relate solely to historical matters are intended to identify forward-looking statements. This report may contain forward-looking statements regarding: our expectations of our future revenues, costs and financial performance; future demographics and market conditions in the areas where our communities are located; the outcome of pending litigation and its effect on our operations; the timing of our development activities; and the timing of future real estate purchases or sales, including anticipated deliveries of homesites and anticipated amenities in our communities.

We caution you that any forward-looking statements presented in this report are based on our current views and information currently available to us. Forward-looking statements are subject to risks, trends, uncertainties and factors that are beyond our control. We believe these risks and uncertainties include, but are not limited to, the following:

•uncertainties and risks related to public health issues such as a major epidemic or pandemic, including COVID-19;

•risks associated with the real estate industry;

•downturns in economic conditions or demographic changes at the national, regional or local levels, particularly in the areas where our properties are located;

•uncertainty and risks related to zoning and land use laws and regulations, including environmental planning and protection laws;

•risks associated with development and construction projects;

•adverse developments in the economic, political, competitive or regulatory climate of California;

•loss of key personnel;

•uncertainties and risks related to adverse weather conditions, natural disasters and climate change;

•fluctuations in interest rates;

•the availability of cash for distribution and debt service and exposure to risk of default under debt obligations;

•exposure to liability relating to environmental and health and safety matters;

•exposure to litigation or other claims;

•insufficient amounts of insurance or exposure to events that are either uninsured or underinsured;

•intense competition in the real estate market and our ability to sell properties at desirable prices;

•fluctuations in real estate values;

•changes in property taxes;

•risks associated with our trademarks, trade names and service marks;

•conflicts of interest with our directors;

•general volatility of the capital and credit markets and the price of our Class A common shares; and

•risks associated with public or private financing or the unavailability thereof.

Please see Part I, Item 1A, “Risk Factors” in our Annual Report on Form 10-K for the year ended December 31, 2022, as well as other risks and uncertainties detailed from time to time in our subsequent Quarterly Reports on Form 10-Q and other filings with the Securities and Exchange Commission, for a more detailed discussion of these and other risks.

Should one or more of these risks or uncertainties materialize, or should underlying assumptions prove incorrect, actual results may vary materially from those anticipated, estimated or projected. We caution you therefore against relying on any of these forward-looking statements.

While forward-looking statements reflect our good faith beliefs, they are not guarantees of future performance. They are based on estimates and assumptions only as of the date of this report. We undertake no obligation to update or revise any forward-looking statement to reflect changes in underlying assumptions or factors, new information, data or methods, future events or other changes, except as required by applicable law.

PART I. FINANCIAL INFORMATION

ITEM 1. Financial Statements

FIVE POINT HOLDINGS, LLC

CONDENSED CONSOLIDATED BALANCE SHEETS

(In thousands, except shares)

(Unaudited)

| March 31, 2023 | December 31, 2022 | ||||||||||

ASSETS | |||||||||||

INVENTORIES | $ | $ | |||||||||

INVESTMENT IN UNCONSOLIDATED ENTITIES | |||||||||||

PROPERTIES AND EQUIPMENT, NET | |||||||||||

INTANGIBLE ASSET, NET—RELATED PARTY | |||||||||||

CASH AND CASH EQUIVALENTS | |||||||||||

RESTRICTED CASH AND CERTIFICATES OF DEPOSIT | |||||||||||

RELATED PARTY ASSETS | |||||||||||

OTHER ASSETS | |||||||||||

TOTAL | $ | $ | |||||||||

LIABILITIES AND CAPITAL | |||||||||||

LIABILITIES: | |||||||||||

Notes payable, net | $ | $ | |||||||||

Accounts payable and other liabilities | |||||||||||

Related party liabilities | |||||||||||

Deferred income tax liability, net | |||||||||||

Payable pursuant to tax receivable agreement | |||||||||||

Total liabilities | |||||||||||

| COMMITMENTS AND CONTINGENT LIABILITIES (Note 11) | |||||||||||

REDEEMABLE NONCONTROLLING INTEREST | |||||||||||

CAPITAL: | |||||||||||

Class A common shares; No par value; Issued and outstanding: March 31, 2023— | |||||||||||

Class B common shares; No par value; Issued and outstanding: March 31, 2023— | |||||||||||

Contributed capital | |||||||||||

Retained earnings | |||||||||||

Accumulated other comprehensive loss | ( | ( | |||||||||

Total members’ capital | |||||||||||

Noncontrolling interests | |||||||||||

Total capital | |||||||||||

TOTAL | $ | $ | |||||||||

See accompanying notes to unaudited condensed consolidated financial statements.

1

FIVE POINT HOLDINGS, LLC

CONDENSED CONSOLIDATED STATEMENTS OF OPERATIONS

(In thousands, except share and per share amounts)

(Unaudited)

| Three Months Ended March 31, | |||||||||||

| 2023 | 2022 | ||||||||||

REVENUES: | |||||||||||

Land sales | $ | ( | $ | ||||||||

Land sales—related party | |||||||||||

Management services—related party | |||||||||||

Operating properties | |||||||||||

Total revenues | |||||||||||

COSTS AND EXPENSES: | |||||||||||

Land sales | |||||||||||

Management services | |||||||||||

Operating properties | |||||||||||

Selling, general, and administrative | |||||||||||

| Restructuring | |||||||||||

Total costs and expenses | |||||||||||

| OTHER INCOME (EXPENSE): | |||||||||||

Interest income | |||||||||||

Miscellaneous | ( | ||||||||||

Total other income | |||||||||||

| EQUITY IN EARNINGS (LOSS) FROM UNCONSOLIDATED ENTITIES | ( | ||||||||||

| LOSS BEFORE INCOME TAX PROVISION | ( | ( | |||||||||

| INCOME TAX PROVISION | ( | ( | |||||||||

| NET LOSS | ( | ( | |||||||||

| LESS NET LOSS ATTRIBUTABLE TO NONCONTROLLING INTERESTS | ( | ( | |||||||||

| NET LOSS ATTRIBUTABLE TO THE COMPANY | $ | ( | $ | ( | |||||||

| NET LOSS ATTRIBUTABLE TO THE COMPANY PER CLASS A SHARE | |||||||||||

| Basic | $ | ( | $ | ( | |||||||

Diluted | $ | ( | $ | ( | |||||||

WEIGHTED AVERAGE CLASS A SHARES OUTSTANDING | |||||||||||

| Basic | |||||||||||

Diluted | |||||||||||

| NET LOSS ATTRIBUTABLE TO THE COMPANY PER CLASS B SHARE | |||||||||||

Basic and diluted | $ | ( | $ | ( | |||||||

WEIGHTED AVERAGE CLASS B SHARES OUTSTANDING | |||||||||||

| Basic and diluted | |||||||||||

See accompanying notes to unaudited condensed consolidated financial statements.

2

FIVE POINT HOLDINGS, LLC

CONDENSED CONSOLIDATED STATEMENTS OF COMPREHENSIVE LOSS

(In thousands)

(Unaudited)

| Three Months Ended March 31, | |||||||||||

| 2023 | 2022 | ||||||||||

| NET LOSS | $ | ( | $ | ( | |||||||

OTHER COMPREHENSIVE INCOME: | |||||||||||

| Reclassification of actuarial loss on defined benefit pension plan included in net loss | |||||||||||

Other comprehensive income before taxes | |||||||||||

INCOME TAX PROVISION RELATED TO OTHER COMPREHENSIVE INCOME | |||||||||||

OTHER COMPREHENSIVE INCOME—Net of tax | |||||||||||

| COMPREHENSIVE LOSS | ( | ( | |||||||||

| LESS COMPREHENSIVE LOSS ATTRIBUTABLE TO NONCONTROLLING INTERESTS | ( | ( | |||||||||

| COMPREHENSIVE LOSS ATTRIBUTABLE TO THE COMPANY | $ | ( | $ | ( | |||||||

See accompanying notes to unaudited condensed consolidated financial statements.

3

FIVE POINT HOLDINGS, LLC

CONDENSED CONSOLIDATED STATEMENTS OF CAPITAL

(In thousands, except share amounts)

(Unaudited)

| Class A Common Shares | Class B Common Shares | Contributed Capital | Retained Earnings | Accumulated Other Comprehensive Loss | Total Members’ Capital | Noncontrolling Interests | Total Capital | ||||||||||||||||||||||||||||||||||||||||

| BALANCE - December 31, 2022 | $ | $ | $ | ( | $ | $ | $ | ||||||||||||||||||||||||||||||||||||||||

| Net loss | — | — | — | ( | — | ( | ( | ( | |||||||||||||||||||||||||||||||||||||||

Share-based compensation expense | — | — | — | — | — | ||||||||||||||||||||||||||||||||||||||||||

| Reacquisition of share-based compensation awards for tax-withholding purposes | ( | — | ( | — | — | ( | — | ( | |||||||||||||||||||||||||||||||||||||||

| Issuance of share-based compensation awards, net of forfeitures | — | — | — | — | — | — | — | ||||||||||||||||||||||||||||||||||||||||

Other comprehensive income—net of tax of $ | — | — | — | — | |||||||||||||||||||||||||||||||||||||||||||

| Tax distributions to noncontrolling interests | — | — | — | — | — | — | ( | ( | |||||||||||||||||||||||||||||||||||||||

Adjustment to liability recognized under tax receivable agreement—net of tax of $ | — | — | ( | — | — | ( | — | ( | |||||||||||||||||||||||||||||||||||||||

Adjustment of noncontrolling interest in the Operating Company | — | — | — | ( | ( | ||||||||||||||||||||||||||||||||||||||||||

| BALANCE - March 31, 2023 | $ | $ | $ | ( | $ | $ | $ | ||||||||||||||||||||||||||||||||||||||||

| BALANCE - December 31, 2021 | $ | $ | $ | ( | $ | $ | $ | ||||||||||||||||||||||||||||||||||||||||

| Net loss | — | — | — | ( | — | ( | ( | ( | |||||||||||||||||||||||||||||||||||||||

Share-based compensation expense | — | — | — | — | — | ||||||||||||||||||||||||||||||||||||||||||

| Reacquisition of share-based compensation awards for tax-withholding purposes | ( | — | ( | — | — | ( | — | ( | |||||||||||||||||||||||||||||||||||||||

| Forfeitures of share-based compensation awards, net of issuances | ( | — | — | — | — | — | — | — | |||||||||||||||||||||||||||||||||||||||

Other comprehensive income—net of tax of $ | — | — | — | — | |||||||||||||||||||||||||||||||||||||||||||

| Tax distributions to noncontrolling interests | — | — | — | — | — | — | ( | ( | |||||||||||||||||||||||||||||||||||||||

Adjustment to liability recognized under tax receivable agreement—net of tax of $ | — | — | — | — | — | ||||||||||||||||||||||||||||||||||||||||||

Adjustment of noncontrolling interest in the Operating Company | — | — | ( | — | ( | ||||||||||||||||||||||||||||||||||||||||||

| BALANCE - March 31, 2022 | $ | $ | $ | ( | $ | $ | $ | ||||||||||||||||||||||||||||||||||||||||

See accompanying notes to unaudited condensed consolidated financial statements.

4

FIVE POINT HOLDINGS, LLC

CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS

(In thousands)

(Unaudited)

| Three Months Ended March 31, | |||||||||||

| 2023 | 2022 | ||||||||||

| CASH FLOWS FROM OPERATING ACTIVITIES: | |||||||||||

| Net loss | $ | ( | $ | ( | |||||||

| Adjustments to reconcile net loss to net cash used in operating activities: | |||||||||||

| Equity in (earnings) loss from unconsolidated entities | ( | ||||||||||

| Depreciation and amortization | |||||||||||

| Share-based compensation | |||||||||||

| Changes in operating assets and liabilities: | |||||||||||

| Inventories | ( | ( | |||||||||

| Related party assets | ( | ||||||||||

| Other assets | ( | ||||||||||

| Accounts payable and other liabilities | |||||||||||

| Related party liabilities | ( | ||||||||||

| Net cash used in operating activities | ( | ( | |||||||||

| CASH FLOWS FROM INVESTING ACTIVITIES: | |||||||||||

| Return of investment from Valencia Landbank Venture | |||||||||||

| Net cash provided by investing activities | |||||||||||

| CASH FLOWS FROM FINANCING ACTIVITIES: | |||||||||||

| Related party reimbursement obligation | ( | ( | |||||||||

| Reacquisition of share-based compensation awards for tax-withholding purposes | ( | ( | |||||||||

| Tax distributions to noncontrolling interests | ( | ( | |||||||||

| Net cash used in financing activities | ( | ( | |||||||||

| NET DECREASE IN CASH, CASH EQUIVALENTS, AND RESTRICTED CASH | ( | ( | |||||||||

| CASH, CASH EQUIVALENTS, AND RESTRICTED CASH—Beginning of period | |||||||||||

| CASH, CASH EQUIVALENTS, AND RESTRICTED CASH—End of period | $ | $ | |||||||||

SUPPLEMENTAL CASH FLOW INFORMATION (Note 12)

See accompanying notes to unaudited condensed consolidated financial statements.

5

FIVE POINT HOLDINGS, LLC

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(Unaudited)

1. BUSINESS AND ORGANIZATION

Five Point Holdings, LLC, a Delaware limited liability company (the “Holding Company” and, together with its consolidated subsidiaries, the “Company”), is an owner and developer of mixed-use planned communities in California. The Holding Company owns all of its assets and conducts all of its operations through Five Point Operating Company, LP, a Delaware limited partnership (the “Operating Company”), and its subsidiaries.

The Company has two classes of shares outstanding: Class A common shares and Class B common shares. Holders of Class A common shares and holders of Class B common shares are entitled to one vote for each share held of record on all matters submitted to a vote of shareholders, and are both entitled to receive distributions at the same time. However, the distributions paid to holders of Class B common shares are in an amount per share equal to 0.0003 multiplied by the amount paid per Class A common share.

The Company presents noncontrolling interests on the Company’s condensed consolidated balance sheet and classifies such interests within capital but separate from the Company’s Class A and Class B members’ capital. Noncontrolling interests represent equity interests in the Company’s consolidated subsidiaries held by partners in the Operating Company, excluding the Holding Company, and members in The Shipyard Communities, LLC (the “San Francisco Venture”), excluding the Operating Company (see Note 5).

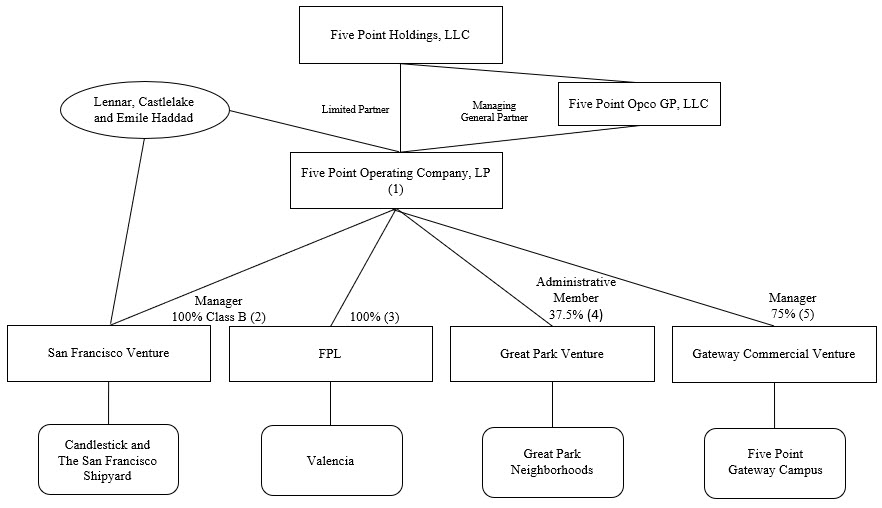

The Company has an entity structure in which the Company’s two largest equity owners, Lennar Corporation (“Lennar”) and Castlelake, LP (“Castlelake”), and the Company’s founder and Chairman Emeritus, Emile Haddad, separately hold, in addition to interests in the Company’s common shares, equity interests in either or both the Operating Company or the San Francisco Venture that can be exchanged for, at the Company’s option, either the Company’s Class A common shares or cash. The diagram below presents a simplified depiction of the Company’s organizational structure as of March 31, 2023:

(1) A wholly owned subsidiary of the Holding Company serves as the sole managing general partner of the Operating Company. As of March 31, 2023, the Company owned approximately 62.6 % of the outstanding Class A Common Units of the Operating Company. After a one year holding period, a holder of Class A Common Units of the Operating Company can exchange the units for, at the Company’s option, either Class A common shares of the Holding Company, on a one -for-one basis, or cash equal to the fair market value of such shares. Until Class A Common Units of the Operating Company are exchanged or redeemed, the capital associated with Class A Common Units of the Operating Company not held by the Holding Company is presented within "noncontrolling interests" on the Company’s condensed consolidated balance sheet. Assuming the exchange of all outstanding Class A Common Units of the Operating Company and all outstanding Class A units of the San Francisco Venture (see (2)

6

below), that are not held by the Company, based on the closing price of the Company’s Class A common shares on April 14, 2023 ($2.32 ), the equity market capitalization of the Company was approximately $344.4 million.

(2) The Operating Company owns all of the outstanding Class B units of the San Francisco Venture, the entity developing the Candlestick and The San Francisco Shipyard communities. The Class A units of the San Francisco Venture, which the Operating Company does not own, are intended to be economically equivalent to Class A Common Units of the Operating Company. As the holder of all outstanding Class B units of the San Francisco Venture, the Operating Company is entitled to receive 99 % of available cash from the San Francisco Venture after the holders of Class A units in the San Francisco Venture have received distributions equivalent to the distributions, if any, paid on Class A Common Units of the Operating Company. Class A units of the San Francisco Venture can be exchanged, on a one -for-one basis, for Class A Common Units of the Operating Company (See Note 5). Until exchanged or redeemed through the Operating Company, the capital associated with Class A units of the San Francisco Venture is presented within "noncontrolling interests" on the Company’s condensed consolidated balance sheet.

(3) Together, the Operating Company, Five Point Communities, LP, a Delaware limited partnership (“FP LP”), and Five Point Communities Management, Inc., a Delaware corporation (“FP Inc.” and together with FP LP, the “Management Company”) own 100 % of Five Point Land, LLC, a Delaware limited liability company (“FPL”), the entity developing Valencia, a mixed-use planned community located in northern Los Angeles County, California. The Operating Company has a controlling interest in the Management Company.

(4) Interests in Heritage Fields LLC, a Delaware limited liability company (the “Great Park Venture”), are either “Percentage Interests” or “Legacy Interests.” Holders of the Legacy Interests were entitled to receive priority distributions up to an aggregate amount of $565.0 million, of which $498.7 million had been distributed as of April 14, 2023 (See Note 4). The Company owns a 37.5 % Percentage Interest in the Great Park Venture and serves as its administrative member. However, management of the Great Park Venture is vested in the four voting members, who have a total of five votes. Major decisions generally require the approval of at least 75 % of the votes of the voting members. The Company has two votes, and the other three voting members each have one vote, so the Company is unable to approve any major decision without the consent or approval of at least two of the other voting members. The Company does not include the Great Park Venture as a consolidated subsidiary, but rather as an equity method investee, in its condensed consolidated financial statements.

(5) The Company owns a 75 % interest in Five Point Office Venture Holdings I, LLC, a Delaware limited liability company (the “Gateway Commercial Venture”). The Company manages the Gateway Commercial Venture, however, the manager’s authority is limited. Major decisions by the Gateway Commercial Venture generally require unanimous approval by an executive committee composed of two people designated by the Company and two people designated by another investor. Some decisions require approval by all of the members of the Gateway Commercial Venture. The Company does not include the Gateway Commercial Venture as a consolidated subsidiary, but rather as an equity method investee, in its condensed consolidated financial statements.

2. BASIS OF PRESENTATION

7

| Three Months Ended March 31, | |||||||||||

| 2023 | 2022 | ||||||||||

| Net periodic pension (cost) benefit | $ | ( | $ | ||||||||

| Total miscellaneous other (loss) income | $ | ( | $ | ||||||||

3. REVENUES

The following tables present the Company’s consolidated revenues disaggregated by revenue source and reporting segment (in thousands):

| Three Months Ended March 31, 2023 | |||||||||||||||||||||||||||||

| Valencia | San Francisco | Great Park(1) | Commercial(1) | Total | |||||||||||||||||||||||||

Land sales and land sales—related party | $ | $ | $ | $ | $ | ||||||||||||||||||||||||

Management services—related party | |||||||||||||||||||||||||||||

| Operating properties | |||||||||||||||||||||||||||||

| Operating properties leasing revenues | |||||||||||||||||||||||||||||

| $ | $ | $ | $ | $ | |||||||||||||||||||||||||

| Three Months Ended March 31, 2022 | |||||||||||||||||||||||||||||

| Valencia | San Francisco | Great Park(1) | Commercial(1) | Total | |||||||||||||||||||||||||

Land sales and land sales—related party | $ | $ | $ | $ | $ | ||||||||||||||||||||||||

Management services—related party | |||||||||||||||||||||||||||||

| Operating properties | |||||||||||||||||||||||||||||

| Operating properties leasing revenues | |||||||||||||||||||||||||||||

| $ | $ | $ | $ | $ | |||||||||||||||||||||||||

(1) The tables above do not include revenues of the Great Park Venture and the Gateway Commercial Venture, which are included in the Company’s reporting segment totals (see Notes 4 and 13).

The opening and closing balances of the Company’s contract assets for the three months ended March 31, 2023 were $86.5 million ($79.9 million related party, see Note 8) and $86.0 million ($80.4 million related party, see Note 8), respectively. The opening and closing balances of the Company’s contract assets for the three months ended March 31, 2022 were $87.6 million ($79.1 million related party, see Note 8) and $87.5 million ($79.1 million related party, see Note 8), respectively. The decrease of $0.5 million for the three months ended March 31, 2023 between the opening and closing balances of the Company’s contract assets primarily resulted from the receipt of marketing fees from homebuilders from prior period land sales offset by additional incentive compensation revenue earned during the period from the Company's amended and restated development management agreement ("A&R DMA") with the Great Park Venture (see Note 8). The decrease of $0.1 million for the three months ended March 31, 2022 between the opening and closing balances of the Company’s contract assets primarily resulted from the receipt of marketing fees from homebuilders

The opening and closing balances of the Company’s other receivables from contracts with customers and contract liabilities for the three months ended March 31, 2023 and 2022 were insignificant.

8

4. INVESTMENT IN UNCONSOLIDATED ENTITIES

Great Park Venture

The Great Park Venture has two classes of interests—“Percentage Interests” and “Legacy Interests.” The Operating Company owned 37.5 % of the Great Park Venture’s Percentage Interests as of March 31, 2023. As of March 31, 2023, Legacy Interest holders were entitled to receive a maximum of $66.3 million in distributions to be paid pro-rata with Percentage Interest holders. Approximately 10 % of future distributions will be paid to the Legacy Interest holders until such time as the remaining balance has been fully paid. The holders of the Percentage Interests will receive all other distributions.

The Great Park Venture is the owner of Great Park Neighborhoods, a mixed-use planned community located in Orange County, California. The Company, through the A&R DMA, as amended, manages the planning, development and sale of land at the Great Park Neighborhoods and supervises the day-to-day affairs of the Great Park Venture. The Great Park Venture is governed by an executive committee of representatives appointed by only the holders of Percentage Interests. The Company serves as the administrative member but does not control the actions of the executive committee. The Company accounts for its investment in the Great Park Venture using the equity method of accounting.

The carrying value of the Company’s investment in the Great Park Venture is higher than the Company’s underlying share of equity in the carrying value of net assets of the Great Park Venture, resulting in a basis difference. The Company’s earnings or losses from the equity method investment are adjusted by amortization and accretion of the basis differences as the assets (mainly inventory) and liabilities that gave rise to the basis difference are sold, settled or amortized.

During the three months ended March 31, 2023, the Great Park Venture recognized $5.5 million in land sale revenues to related parties of the Company and $3.1 million in land sale revenues to third parties.

During the three months ended March 31, 2022, the Great Park Venture recognized $1.5 million in land sale revenues to related parties of the Company and $0.3 million in land sale revenues to third parties.

The following table summarizes the statements of operations of the Great Park Venture for the three months ended March 31, 2023 and 2022 (in thousands):

| Three Months Ended March 31, | |||||||||||

| 2023 | 2022 | ||||||||||

| Land sale and related party land sale revenues | $ | $ | |||||||||

| Home sale revenues | |||||||||||

Cost of land sales | |||||||||||

| Cost of home sales | ( | ||||||||||

Other costs and expenses | ( | ( | |||||||||

| Net income (loss) of Great Park Venture | $ | $ | ( | ||||||||

| The Company’s share of net income (loss) | $ | $ | ( | ||||||||

| Basis difference accretion (amortization) | ( | ||||||||||

| Equity in earnings (loss) from Great Park Venture | $ | $ | ( | ||||||||

The following table summarizes the balance sheet data of the Great Park Venture and the Company’s investment balance as of March 31, 2023 and December 31, 2022 (in thousands):

| March 31, 2023 | December 31, 2022 | ||||||||||

Inventories | $ | $ | |||||||||

Cash and cash equivalents | |||||||||||

Receivable and other assets | |||||||||||

Total assets | $ | $ | |||||||||

Accounts payable and other liabilities | $ | $ | |||||||||

Redeemable Legacy Interests | |||||||||||

Capital (Percentage Interest) | |||||||||||

Total liabilities and capital | $ | $ | |||||||||

The Company’s share of capital in Great Park Venture | $ | $ | |||||||||

Unamortized basis difference | |||||||||||

The Company’s investment in the Great Park Venture | $ | $ | |||||||||

9

Gateway Commercial Venture

The Company owned a 75 % interest in the Gateway Commercial Venture as of March 31, 2023. The Gateway Commercial Venture is governed by an executive committee in which the Company is entitled to appoint two individuals. One of the other members of the Gateway Commercial Venture is also entitled to appoint two individuals to the executive committee. The unanimous approval of the executive committee is required for certain matters, which limits the Company’s ability to control the Gateway Commercial Venture, however, the Company is able to exercise significant influence and therefore accounts for its investment in the Gateway Commercial Venture using the equity method. The Company is the manager of the Gateway Commercial Venture, with responsibility to manage and administer its day-to-day affairs and implement a business plan approved by the executive committee.

The Gateway Commercial Venture owns one commercial office building and approximately 50 acres of commercial land with additional development rights at a 73 acre office, medical, research and development campus located within the Great Park Neighborhoods (the “Five Point Gateway Campus”). The Five Point Gateway Campus consists of four buildings totaling approximately one million square feet. The Company and a subsidiary of Lennar lease portions of the building owned by the Gateway Commercial Venture, and during the three months ended March 31, 2023 and 2022, the Gateway Commercial Venture recognized $2.2 million and $1.9 million, respectively, in rental revenues from those leasing arrangements.

The following table summarizes the statements of operations of the Gateway Commercial Venture for the three months ended March 31, 2023 and 2022 (in thousands):

| Three Months Ended March 31, | |||||||||||

| 2023 | 2022 | ||||||||||

| Rental revenues | $ | $ | |||||||||

| Rental operating and other expenses | ( | ( | |||||||||

| Depreciation and amortization | ( | ( | |||||||||

| Interest expense | ( | ( | |||||||||

| Net (loss) income of Gateway Commercial Venture | $ | ( | $ | ||||||||

| Equity in (loss) earnings from Gateway Commercial Venture | $ | ( | $ | ||||||||

The following table summarizes the balance sheet data of the Gateway Commercial Venture and the Company’s investment balance as of March 31, 2023 and December 31, 2022 (in thousands):

| March 31, 2023 | December 31, 2022 | ||||||||||

| Real estate and related intangible assets, net | $ | $ | |||||||||

| Cash | |||||||||||

| Other assets | |||||||||||

| Total assets | $ | $ | |||||||||

| Notes payable, net | $ | $ | |||||||||

| Other liabilities | |||||||||||

| Members’ capital | |||||||||||

| Total liabilities and capital | $ | $ | |||||||||

| The Company’s investment in the Gateway Commercial Venture | $ | $ | |||||||||

The debt of the Gateway Commercial Venture is non-recourse to the Company other than in the case of customary “bad act” exceptions or bankruptcy or insolvency events.

Valencia Landbank Venture

As of March 31, 2023, the Company owned a 10 % interest in the Valencia Landbank Venture, an entity organized in December 2020 for the purpose of taking assignment from homebuilders of purchase and sale agreements for the purchase of residential lots within the Valencia community. The Valencia Landbank Venture concurrently enters into option and development agreements with homebuilders pursuant to which the homebuilders retain the option to purchase the land to construct and sell homes. The Company does not have a controlling financial interest in the Valencia Landbank Venture, however, the Company has the ability to significantly influence the Valencia Landbank Venture’s operating and financial policies, and most major decisions require the Company’s approval in addition to the approval of the Valencia Landbank Venture’s other unaffiliated member, and therefore the Company accounts for its investment in the Valencia Landbank Venture using the equity method. At March 31, 2023 and December 31, 2022, the Company’s investment in the Valencia Landbank Venture was $1.9 million and $1.9 million, respectively, and the Company recognized $0.1 million and $0.2 million in equity in earnings for the three months ended March 31, 2023 and 2022, respectively.

10

5. NONCONTROLLING INTERESTS

The Operating Company

The Holding Company’s wholly owned subsidiary is the managing general partner of the Operating Company, and at March 31, 2023, the Holding Company and its wholly owned subsidiary owned approximately 62.6 % of the outstanding Class A Common Units and 100 % of the outstanding Class B Common Units of the Operating Company. The Holding Company consolidates the financial results of the Operating Company and its subsidiaries and records a noncontrolling interest for the remaining 37.4 % of the outstanding Class A Common Units of the Operating Company that are owned separately by affiliates of Lennar, affiliates of Castlelake and an entity controlled by Emile Haddad, the Company’s Chairman Emeritus of the Board of Directors (the “Management Partner”).

After a 12 month holding period, holders of Class A Common Units of the Operating Company may exchange their units for, at the Company’s option, either (i) Class A common shares on a one -for-one basis (subject to adjustment in the event of share splits, distributions of shares, warrants or share rights, specified extraordinary distributions and similar events), or (ii) cash in an amount equal to the market value of such shares at the time of exchange. In either situation, an equal number of that holder’s Class B common shares will automatically convert into Class A common shares, at a ratio of 0.0003 Class A common shares for each Class B common share. This exchange right is currently exercisable by all holders of outstanding Class A Common Units of the Operating Company.

With each exchange of Class A Common Units of the Operating Company for Class A common shares, the Holding Company’s percentage ownership interest in the Operating Company and its share of the Operating Company’s cash distributions and profits and losses will increase. Additionally, other issuances of common shares of the Holding Company or common units of the Operating Company result in changes to the noncontrolling interest percentage. Such equity transactions result in an adjustment between members’ capital and the noncontrolling interest in the Company’s condensed consolidated balance sheet and statement of capital to account for the changes in the noncontrolling interest ownership percentage as well as any change in total net assets of the Company.

During the three months ended March 31, 2023 and 2022, the Holding Company’s ownership interest in the Operating Company changed as a result of net equity transactions related to the Company’s share-based compensation plan.

The terms of the Operating Company's Limited Partnership Agreement (“LPA”) provide for the payment of tax distributions to the Operating Company's partners in an amount equal to the estimated income tax liabilities resulting from taxable income or gain allocated to those parties. The tax distribution provisions in the LPA were included in the Operating Company's governing documents adopted prior to the Company’s initial public offering and were designed to provide funds necessary to pay tax liabilities for income that might be allocated, but not paid, to the partners.

| Three Months Ended March 31, | |||||||||||

| 2023 | 2022 | ||||||||||

| Management Partner | $ | $ | |||||||||

| Other partners (excluding the Holding Company) | |||||||||||

| Total tax distributions | $ | $ | |||||||||

Generally, tax distributions are treated as advance distributions under the LPA and are taken into account when determining the amounts otherwise distributable under the LPA.

The San Francisco Venture

The San Francisco Venture has three classes of units—Class A, Class B and Class C units. The Operating Company owns all of the outstanding Class B units of the San Francisco Venture. All of the outstanding Class A units are owned by Lennar and Castlelake. The Class A units of the San Francisco Venture are intended to be substantially economically equivalent to the Class A Common Units of the Operating Company. The Class A units of the San Francisco Venture represent noncontrolling interests to the Operating Company.

Holders of Class A units of the San Francisco Venture can redeem their units at any time and receive Class A Common Units of the Operating Company on a one -for-one basis (subject to adjustment in the event of share splits, distributions of shares, warrants or share rights, specified extraordinary distributions and similar events). If a holder requests a redemption of Class A units of the San Francisco Venture that would result in the Holding Company’s ownership of the Operating Company falling below 50.1 %, the Holding Company has the option of satisfying the redemption with Class A common shares instead. The Company also has the option, at any time, to acquire outstanding Class A units of the San Francisco Venture in exchange for Class A Common Units of the Operating Company. The 12 month holding period for any Class A Common Units of the Operating Company issued in exchange for

11

Class A units of the San Francisco Venture is calculated by including the period that such Class A units of the San Francisco Venture were owned. This exchange right is currently exercisable by all holders of outstanding Class A units of the San Francisco Venture.

Redeemable Noncontrolling Interest

6. CONSOLIDATED VARIABLE INTEREST ENTITY

The Holding Company conducts all of its operations through the Operating Company, a consolidated VIE, and as a result, substantially all of the Company’s assets and liabilities represent the assets and liabilities of the Operating Company, other than items attributed to income taxes and the payable pursuant to a tax receivable agreement (“TRA”). The Operating Company has investments in and consolidates the assets and liabilities of the San Francisco Venture, FP LP and FPL, all of which have also been determined to be VIEs.

The San Francisco Venture is a VIE as the other members of the venture, individually or as a group, are not able to exercise kick-out rights or substantive participating rights. The Company applied the variable interest model and determined that it is the primary beneficiary of the San Francisco Venture and, accordingly, the San Francisco Venture is consolidated in the Company’s results. In making that determination, the Company evaluated that the Operating Company has unilateral and unconditional power to make decisions in regards to the activities that significantly impact the economics of the VIE, which are the development of properties, marketing and sale of properties, acquisition of land and other real estate properties and obtaining land ownership or ground lease for the underlying properties to be developed. The Company is determined to have more-than-insignificant economic benefit from the San Francisco Venture because, excluding Class C units, the Operating Company can prevent or cause the San Francisco Venture from making distributions on its units, and the Operating Company would receive 99 % of any such distributions made (assuming no distributions had been paid on the Class A Common Units of the Operating Company). In addition, the San Francisco Venture is only allowed to make a capital call on the Operating Company and not any other interest holders, which could be a significant financial risk to the Operating Company.

As of March 31, 2023, the San Francisco Venture had total combined assets of $1.33 billion, primarily comprised of $1.32 billion of inventories and $0.9 million in related party assets, and total combined liabilities of $68.3 million, including $61.5 million in related party liabilities.

As of December 31, 2022, the San Francisco Venture had total combined assets of $1.31 billion, primarily comprised of $1.31 billion of inventories and $0.8 million in related party assets, and total combined liabilities of $67.3 million, including $63.0 million in related party liabilities.

Those assets are owned by, and those liabilities are obligations of, the San Francisco Venture, not the Company. The San Francisco Venture’s operating subsidiaries are not guarantors of the Company’s obligations, and the assets held by the San Francisco Venture may only be used as collateral for the San Francisco Venture’s obligations. The creditors of the San Francisco Venture do not have recourse to the assets of the Operating Company, as the VIE’s primary beneficiary, or of the Holding Company.

The Company and the other members do not generally have an obligation to make capital contributions to the San Francisco Venture. In addition, there are no liquidity arrangements or agreements to fund capital or purchase assets that could require the Company to provide financial support to the San Francisco Venture. The Company does not guarantee any debt of the San Francisco Venture. However, the Operating Company has guaranteed the performance of payment by the San Francisco Venture in accordance with the redemption terms of the Class C units of the San Francisco Venture (see Note 5).

FP LP and FPL are VIEs because the other partners or members have disproportionately fewer voting rights, and substantially all of the activities of the entities are conducted on behalf of the other partners or members and their related parties. The Operating Company, or a wholly owned subsidiary of the Operating Company, is the primary beneficiary of FP LP and FPL.

12

As of March 31, 2023, FP LP and FPL had combined assets of $1.1 billion, primarily comprised of $936.7 million of inventories, $39.6 million of intangibles and $80.4 million in related party assets, and total combined liabilities of $76.1 million, including $68.6 million in accounts payable and other liabilities and $7.5 million in related party liabilities.

As of December 31, 2022, FP LP and FPL had combined assets of $1.1 billion, primarily comprised of $927.9 million of inventories, $40.3 million of intangibles and $79.9 million in related party assets, and total combined liabilities of $77.2 million, including $70.5 million in accounts payable and other liabilities and $6.7 million in related party liabilities.

The Company evaluates its primary beneficiary designation on an ongoing basis and assesses the appropriateness of the VIE’s status when events have occurred that would trigger such an analysis. During the three months ended March 31, 2023 and 2022, there were no VIEs that were deconsolidated.

7. INTANGIBLE ASSET, NET—RELATED PARTY

The intangible asset relates to the contract value of the incentive compensation provisions of the A&R DMA with the Great Park Venture. The intangible asset will be amortized over the expected contract period based on the pattern in which the economic benefits are expected to be received.

| March 31, 2023 | December 31, 2022 | ||||||||||

| Gross carrying amount | $ | $ | |||||||||

| Accumulated amortization | ( | ( | |||||||||

| Net book value | $ | $ | |||||||||

13

8. RELATED PARTY TRANSACTIONS

| March 31, 2023 | December 31, 2022 | ||||||||||

Related Party Assets: | |||||||||||

Contract assets (see Note 3) | $ | $ | |||||||||

| Operating lease right-of-use asset (corporate office lease at Five Point Gateway Campus) | |||||||||||

Other | |||||||||||

| $ | $ | ||||||||||

Related Party Liabilities: | |||||||||||

Reimbursement obligation | $ | $ | |||||||||

Payable to holders of Management Company’s Class B interests | |||||||||||

| Operating lease liability (corporate office lease at Five Point Gateway Campus) | |||||||||||

| Accrued advisory fees | |||||||||||

Other | |||||||||||

| $ | $ | ||||||||||

Development Management Agreement with the Great Park Venture (Incentive Compensation Contract Asset)

In 2010, the Great Park Venture, the Company’s equity method investee, engaged the Management Company under a development management agreement to provide management services to the Great Park Venture. The compensation structure in place consists of a base fee and incentive compensation. Incentive compensation is 9 % of distributions available to be made by the Great Park Venture to its Legacy and Percentage Interest Holders. In December 2022, the Company and the Great Park Venture entered into an amendment to the A&R DMA to extend the term to December 31, 2024 (the "First Renewal Term"). If the A&R DMA is not extended by mutual agreement of the parties beyond December 31, 2024 and the Company is no longer providing management services subsequent to December 31, 2024, the Company will be entitled to 6.75 % of distributions paid thereafter.

At March 31, 2023 and December 31, 2022, included in contract assets in the table above is $78.5 million and $77.4 million, respectively, attributed to Incentive Compensation revenue recognized but not yet due (see Note 3). Management fee revenues under the A&R DMA are included in management services—related party in the accompanying condensed consolidated statements of operations and are included in the Great Park segment. Management fee revenues under the A&R DMA were $4.1 million and $3.4 million for the three months ended March 31, 2023 and 2022, respectively.

9. NOTES PAYABLE, NET

| March 31, 2023 | December 31, 2022 | ||||||||||

| $ | $ | ||||||||||

Unamortized debt issuance costs and discount | ( | ( | |||||||||

| $ | $ | ||||||||||

Revolving Credit Facility

The Operating Company has a $125.0 million unsecured revolving credit facility with a maturity date in April 2024, with one option to extend the maturity date by an additional year, subject to the satisfaction of certain conditions including the approval of the administrative agent and lenders. As of March 31, 2023, no

14

10. TAX RECEIVABLE AGREEMENT

11. COMMITMENTS AND CONTINGENCIES

The Company is subject to the usual obligations associated with entering into contracts for the purchase, development and sale of real estate, which the Company does in the routine conduct of its business. The operations of the Company are conducted through the Operating Company and its subsidiaries, and in some cases, the Holding Company will guarantee the payment by or performance of the Operating Company or its subsidiaries. The Company has operating leases for its corporate office and other facilities and the Holding Company is a guarantor to some of these lease agreements. are included in other assets or related party assets, and are included in accounts payable and other liabilities or related party liabilities on the condensed consolidated balance sheets and were as follows as of March 31, 2023 and December 31, 2022 (in thousands):

| March 31, 2023 | December 31, 2022 | ||||||||||

Operating lease right-of-use assets ($ | $ | $ | |||||||||

Operating lease liabilities ($ | $ | $ | |||||||||

In addition to operating lease payment guarantees, the Holding Company had other contractual payment guarantees as of March 31, 2023 totaling $10.2 million.

Performance and Completion Bonding Agreements

In the ordinary course of business and as a part of the entitlement and development process, the Company is required to provide performance bonds to ensure completion of certain development obligations. The Company had outstanding performance bonds of $320.0 million and $315.0 million as of March 31, 2023 and December 31, 2022, respectively.

Candlestick and The San Francisco Shipyard Disposition and Development Agreement

The San Francisco Venture is a party to a disposition and development agreement with the Successor to the Redevelopment Agency of the City and County of San Francisco (the “San Francisco Agency”) in which the San Francisco Agency has agreed to convey portions of Candlestick and The San Francisco Shipyard to the San Francisco Venture for development. The San Francisco Venture has agreed to reimburse the San Francisco Agency for reasonable costs and expenses actually incurred and paid by the San Francisco Agency in performing its obligations under the disposition and development agreement. The San Francisco Agency can also earn a return of certain profits generated from the development and sale of Candlestick and The San Francisco Shipyard if certain thresholds are met.

At each of March 31, 2023 and December 31, 2022, the San Francisco Venture had outstanding guarantees benefiting the San Francisco Agency for infrastructure and construction of certain park and open space obligations with aggregate maximum obligations of $198.3

Letters of Credit

At each of March 31, 2023 and December 31, 2022, the Company had outstanding letters of credit totaling $1.0 1.0

Legal Proceedings

Hunters Point Litigation

In May 2018, residents of the Bayview Hunters Point neighborhood in San Francisco filed a putative class action in San Francisco Superior Court naming Tetra Tech, Inc. and Tetra Tech EC, Inc., an independent contractor hired by the U.S. Navy to conduct testing and remediation of toxic radiological waste at The San Francisco Shipyard (“Tetra Tech”), Lennar and the Company as defendants (the “Bayview Action”). The plaintiffs allege that, among other things, Tetra Tech fraudulently misrepresented its test

15

results and remediation efforts. The plaintiffs are seeking damages against Tetra Tech and the Company and have requested an injunction to prevent the Company and Lennar from undertaking any development activities at The San Francisco Shipyard. Given the preliminary nature of the claims, the Company cannot predict the outcome of the Bayview Action. The Company believes that it has meritorious defenses to the allegations in the Bayview Action and may have insurance and indemnification rights against third parties with respect to the claims.

Other

Other than the actions outlined above, the Company is also a party to various other claims, legal actions, and complaints arising in the ordinary course of business, the disposition of which, in the Company’s opinion, will not have a material adverse effect on the Company’s condensed consolidated financial statements.

As a significant land owner and developer of unimproved land it is possible that environmental contamination conditions could exist that would require the Company to take corrective action. In the opinion of the Company, such corrective actions, if any, would not have a material adverse effect on the Company’s condensed consolidated financial statements.

12. SUPPLEMENTAL CASH FLOW INFORMATION

| Three Months Ended March 31, | |||||||||||

| 2023 | 2022 | ||||||||||

| SUPPLEMENTAL CASH FLOW INFORMATION: | |||||||||||

| Cash paid for interest, all of which was capitalized to inventories | $ | $ | |||||||||

| Noncash lease expense | $ | $ | |||||||||

| NONCASH INVESTING AND FINANCING ACTIVITIES: | |||||||||||

| Adjustment to operating lease right-of-use assets from lease modification | $ | ( | $ | ||||||||

| Adjustment to liability recognized under TRA | $ | $ | ( | ||||||||

Noncash lease expense is included within the depreciation and amortization adjustment to net loss on the Company’s condensed consolidated statements of cash flows.

| March 31, 2023 | March 31, 2022 | ||||||||||

| Cash and cash equivalents | $ | $ | |||||||||

| Restricted cash and certificates of deposit | |||||||||||

| Total cash, cash equivalents, and restricted cash shown in the condensed consolidated statements of cash flows | $ | $ | |||||||||

Amounts included in restricted cash and certificates of deposit represent amounts held as collateral on open letters of credit related to development obligations or because of other contractual obligations of the Company that require the restriction.

13. SEGMENT REPORTING

The Company’s reportable segments consist of:

• Valencia—includes the community of Valencia being developed in northern Los Angeles County, California. The Valencia segment derives revenues from the sale of residential and commercial land sites to homebuilders, commercial developers and commercial buyers. The Company’s investment in the Valencia Landbank Venture is also reported in the Valencia segment.

• San Francisco—includes the Candlestick and The San Francisco Shipyard communities located on bayfront property in the City of San Francisco, California. The San Francisco segment derives revenues from the sale of residential and commercial land sites to homebuilders, commercial developers and commercial buyers.

• Great Park—includes the Great Park Neighborhoods being developed adjacent to and around the Orange County Great Park, a metropolitan park under construction in Orange County, California. This segment also includes management services provided by the Management Company to the Great Park Venture, the owner of the Great Park Neighborhoods. As of March 31, 2023, the Company had a 37.5 % Percentage Interest in the Great Park Venture and accounted for the investment

16

under the equity method. The reported segment information for the Great Park segment includes the results of 100% of the Great Park Venture at the historical basis of the venture, which did not apply push down accounting at acquisition date. The Great Park segment derives revenues at the Great Park Neighborhoods from sales of residential and commercial land sites to homebuilders, commercial developers and commercial buyers, sales of homes constructed and marketed under a fee build arrangement, and management services provided by the Company to the Great Park Venture.

• Commercial—includes the operations of the Gateway Commercial Venture, which owns an approximately 189,000 square foot office building at the Five Point Gateway Campus. The Five Point Gateway Campus is an office, medical and research and development campus located within the Great Park Neighborhoods and consists of four buildings and surrounding land. The Company and a subsidiary of Lennar lease portions of the building owned by the Gateway Commercial Venture. The Gateway Commercial Venture also owns approximately 50 acres of the surrounding commercial land with additional development rights at the campus. This segment also includes property management services provided by the Management Company to the Gateway Commercial Venture. As of March 31, 2023, the Company had a 75 % interest in the Gateway Commercial Venture and accounted for the investment under the equity method. The reported segment information for the Commercial segment includes the results of 100% of the Gateway Commercial Venture at the historical basis of the venture.

| Revenues | Profit (Loss) | ||||||||||||||||||||||

| Three Months Ended March 31, | |||||||||||||||||||||||

| 2023 | 2022 | 2023 | 2022 | ||||||||||||||||||||

Valencia | $ | $ | $ | ( | $ | ( | |||||||||||||||||

San Francisco | ( | ( | |||||||||||||||||||||

Great Park | ( | ||||||||||||||||||||||

Commercial | ( | ||||||||||||||||||||||

| Total reportable segments | ( | ||||||||||||||||||||||

Reconciling items: | |||||||||||||||||||||||

| Removal of results of unconsolidated entities— | |||||||||||||||||||||||

| Great Park Venture (1) | ( | ( | ( | ||||||||||||||||||||

| Gateway Commercial Venture (1) | ( | ( | ( | ||||||||||||||||||||

| Add equity in earnings (losses) from unconsolidated entities— | |||||||||||||||||||||||

| Great Park Venture | — | — | ( | ||||||||||||||||||||

| Gateway Commercial Venture | — | — | ( | ||||||||||||||||||||

Corporate and unallocated (2) | — | — | ( | ( | |||||||||||||||||||

Total consolidated balances | $ | $ | $ | ( | $ | ( | |||||||||||||||||

(1) Represents the removal of the Great Park Venture and Gateway Commercial Venture operating results, which are included in the Great Park segment and Commercial segment operating results at 100% of each venture’s historical basis, respectively, but are not included in the Company’s consolidated results and balances as the Company accounts for its investment in each venture using the equity method of accounting.

(2) Corporate and unallocated activity is primarily comprised of corporate general and administrative expenses and restructuring expenses.

17

Segment assets and reconciliations to the Company’s consolidated balances are as follows (in thousands):

| March 31, 2023 | December 31, 2022 | ||||||||||

Valencia | $ | $ | |||||||||

San Francisco | |||||||||||

Great Park | |||||||||||

Commercial | |||||||||||

| Total reportable segments | |||||||||||

Reconciling items: | |||||||||||

Removal of unconsolidated balances of Great Park Venture (1) | ( | ( | |||||||||

Removal of unconsolidated balances of Gateway Commercial Venture (1) | ( | ( | |||||||||

Other eliminations (2) | ( | ( | |||||||||

Add investment balance in Great Park Venture | |||||||||||

Add investment balance in Gateway Commercial Venture | |||||||||||

Corporate and unallocated (3) | |||||||||||

Total consolidated balances | $ | $ | |||||||||

(1) Represents the removal of the Great Park Venture and Gateway Commercial Venture balances, which are included in the Great Park segment and Commercial segment balances at 100% of each venture’s historical basis, respectively, but are not included in the Company’s consolidated balances as the Company accounts for its investment in each venture using the equity method of accounting.

(2) Represents intersegment balances that eliminate in consolidation.

14. SHARE-BASED COMPENSATION

| Share-Based Awards (in thousands) | Weighted-Average Grant Date Fair Value | ||||||||||

Nonvested at January 1, 2023 | $ | ||||||||||

Granted | $ | ||||||||||

Forfeited | $ | ||||||||||

Vested | ( | $ | |||||||||

Nonvested at March 31, 2023 | $ | ||||||||||

Share-based compensation expense was $0.8 million and $4.1 million for the three months ended March 31, 2023 and 2022, respectively. All share-based compensation for the three months ended March 31, 2023 is included in selling, general, and administrative expenses on the accompanying condensed consolidated statements of operations. In February 2022, the Company accelerated the expense attributed to the outstanding restricted share awards of two former officers of the Company resulting from a modification of the required service condition of the awards. As a result, for the three months ended March 31, 2022, share-based compensation expense of $3.0 million is included in restructuring expense and $1.1 million is included in selling, general, and administrative expenses on the accompanying condensed consolidated statement of operations.

The estimated fair value at vesting of share-based awards that vested during the three months ended March 31, 2023 was $1.5 million. In January 2023 and 2022, the Company reacquired vested restricted Class A common shares for $0.2 million and $2.7 million, respectively, for the purpose of settling tax withholding obligations of employees. The reacquisition cost is based on the fair value of the Company’s Class A common shares on the date the tax obligation is incurred.

15. EMPLOYEE BENEFIT PLANS

18

| Three Months Ended March 31, | |||||||||||

| 2023 | 2022 | ||||||||||

| Net periodic cost (benefit): | |||||||||||

Interest cost | $ | $ | |||||||||

Expected return on plan assets | ( | ( | |||||||||

Amortization of net actuarial loss | |||||||||||

| Net periodic cost (benefit) | $ | $ | ( | ||||||||

16. INCOME TAXES

Upon formation, the Holding Company elected to be treated as a corporation for U.S. federal, state, and local tax purposes. All operations are carried on through the Holding Company’s subsidiaries, the majority of which are pass-through entities that are generally not subject to federal or state income taxation, as all of the taxable income, gains, losses, deductions, and credits are passed through to the partners. The Holding Company is responsible for income taxes on its allocable share of the Operating Company’s income or gain.

Other than a small income tax provision attributed to one of the Company’s consolidated subsidiary corporations, during the three months ended March 31, 2023 and 2022, the Company recorded no 9.7 million and $36.8 million, respectively. The effective tax rates for the three months ended March 31, 2023 and 2022, differ from the 21% federal statutory rate and applicable state statutory rates primarily due to the Company’s valuation allowance on its book losses, disallowance of executive compensation expenses not deductible for tax, and to the pre-tax portion of income and losses that are passed through to the other partners of the Operating Company and the San Francisco Venture.

Largely due to a history of book losses, the Company continues to record a valuation allowance against its federal and state net deferred tax assets.

17. FINANCIAL INSTRUMENTS AND FAIR VALUE MEASUREMENTS AND DISCLOSURES

ASC Topic 820, Fair Value Measurement, emphasizes that a fair value measurement should be determined based on the assumptions that market participants would use in pricing the asset or liability. As a basis for considering market participant assumptions in fair value measurements, the guidance establishes a fair value hierarchy that distinguishes between market participant assumptions based on market data obtained from sources independent of the reporting entity and the reporting entity’s own assumptions about market participant assumptions. The following hierarchy classifies the inputs used to determine fair value into three levels:

Level 1—Quoted prices for identical instruments in active markets

Level 2—Quoted prices for similar instruments in active markets or inputs, other than quoted prices, that are observable for the instrument either directly or indirectly

Level 3—Significant inputs to the valuation model are unobservable

At each reporting period, the Company evaluates the fair value of its financial instruments compared to carrying values. Other than the Company’s notes payable, net, the carrying amount of the Company’s financial instruments, which includes cash and cash equivalents, restricted cash and certificates of deposit, certain related party assets and liabilities, and accounts payable and other liabilities, approximated the Company’s estimates of fair value at both March 31, 2023 and December 31, 2022.

The fair value of the Company’s notes payable, net, are estimated based on quoted market prices or discounting the expected cash flows based on rates available to the Company (level 2). At March 31, 2023, the estimated fair value of notes payable, net was $563.8 million compared to a carrying value of $621.0 million. At December 31, 2022, the estimated fair value of notes payable, net was $525.5 million compared to a carrying value of $620.7 million. During the three months ended March 31, 2023 and 2022, the Company had no assets that were measured at fair value on a nonrecurring basis.

19

18. EARNINGS PER SHARE

The Company uses the two-class method in its computation of earnings per share. The Company’s Class A common shares and Class B common shares are entitled to receive distributions at different rates, with each Class B common share receiving 0.03 % of the distributions paid on each Class A common share. Under the two-class method, the Company’s net income available to common shareholders is allocated between the two classes of common shares on a fully-distributed basis and reflects residual net income after amounts attributed to noncontrolling interests. In the event of a net loss, the Company determined that both classes share in the Company’s losses, and they share in the losses using the same mechanism as the distributions. The Company also has restricted share awards and performance restricted share awards (see Note 14) that have a right to non-forfeitable dividends while unvested and are contemplated as participating when the Company is in a net income position. These awards participate in distributions on a basis equivalent to other Class A common shares but do not participate in losses.

No distributions on common shares were declared for the three months ended March 31, 2023 or 2022.

Diluted income (loss) per share calculations for both Class A common shares and Class B common shares contemplate adjustments to the numerator and the denominator under the if-converted method for the convertible Class B common shares, the exchangeable Class A units of the San Francisco Venture and the exchangeable Class A Common Units of the Operating Company. The Company uses the treasury stock method or the two-class method when evaluating dilution for RSUs, restricted shares, and performance restricted units and shares. The more dilutive of the two methods is included in the calculation for diluted income (loss) per share.

The following table summarizes the basic and diluted loss per share calculations for the three months ended March 31, 2023 and 2022 (in thousands, except shares and per share amounts):

| Three Months Ended March 31, | |||||||||||

| 2023 | 2022 | ||||||||||

Numerator: | |||||||||||

| Net loss attributable to the Company | $ | ( | $ | ( | |||||||

| Adjustments to net loss attributable to the Company | |||||||||||

| Net loss attributable to common shareholders | $ | ( | $ | ( | |||||||

Numerator—basic common shares: | |||||||||||

| Numerator for basic net loss available to Class A common shareholders | $ | ( | $ | ( | |||||||

| Numerator for basic net loss available to Class B common shareholders | $ | ( | $ | ( | |||||||

Numerator—diluted common shares: | |||||||||||

| Net loss attributable to common shareholders | $ | ( | $ | ( | |||||||

| Reallocation of loss upon assumed exchange of dilutive potential securities | ( | ( | |||||||||

| Allocation of diluted net loss among common shareholders | $ | ( | $ | ( | |||||||

| Numerator for diluted net loss available to Class A common shareholders | $ | ( | $ | ( | |||||||

| Numerator for diluted net loss available to Class B common shareholders | $ | ( | $ | ( | |||||||

Denominator: | |||||||||||

| Basic weighted average Class A common shares outstanding | |||||||||||

Diluted weighted average Class A common shares outstanding | |||||||||||

| Basic and diluted weighted average Class B common shares outstanding | |||||||||||

| Basic loss per share: | |||||||||||

Class A common shares | $ | ( | $ | ( | |||||||

Class B common shares | $ | ( | $ | ( | |||||||

| Diluted loss per share: | |||||||||||

Class A common shares | $ | ( | $ | ( | |||||||

Class B common shares | $ | ( | $ | ( | |||||||

Anti-dilutive potential RSUs | |||||||||||

Anti-dilutive potential Performance RSUs | |||||||||||

Anti-dilutive potential Restricted Shares (weighted average) | |||||||||||

Anti-dilutive potential Performance Restricted Shares (weighted average) | |||||||||||

| Anti-dilutive potential Class A common shares from exchanges (weighted average) | |||||||||||

20

19. ACCUMULATED OTHER COMPREHENSIVE LOSS

21

ITEM 2. Management’s Discussion and Analysis of Financial Condition and Results of Operations

Forward-Looking Statements

The following discussion contains management’s discussion and analysis of our financial condition and results of operations and should be read in conjunction with our unaudited condensed consolidated financial statements and related notes included under Part I, Item 1 of this report and our audited consolidated financial statements included in our Annual Report on Form 10-K for the fiscal year ended December 31, 2022. “Us,” “we,” and “our” refer to Five Point Holdings, LLC, together with its consolidated subsidiaries. This discussion contains forward-looking statements and involves numerous risks and uncertainties, including but not limited to those described in the “Risk Factors” section of our Annual Report on Form 10-K for the fiscal year ended December 31, 2022, as well as other risks and uncertainties detailed from time to time in our subsequent Quarterly Reports on Form 10-Q and other filings with the Securities and Exchange Commission. Actual results could differ materially from those set forth in any forward-looking statements. See “Cautionary Statement Regarding Forward-Looking Statements.”

Overview

We conduct all of our business in or through our operating company, Five Point Operating Company, LP (the “operating company”). We are, through a wholly owned subsidiary, the sole managing general partner and owned, as of March 31, 2023, approximately 62.6% of the operating company. The operating company directly or indirectly owns equity interests in:

•Five Point Land, LLC, which owns The Newhall Land & Farming Company, a California limited partnership, the entity that is developing Valencia, our community in northern Los Angeles County, California;

•The Shipyard Communities, LLC (the “San Francisco Venture”), which is developing Candlestick and The San Francisco Shipyard, our communities in the City of San Francisco, California;

•Heritage Fields LLC (the “Great Park Venture”), which is developing Great Park Neighborhoods, our community in Orange County, California;

•Five Point Office Venture Holdings I, LLC (the “Gateway Commercial Venture”), which owns portions of the Five Point Gateway Campus, a commercial office, research and development and medical campus located within the Great Park Neighborhoods; and

•Five Point Communities, LP and Five Point Communities Management, Inc. (together, the “management company”), which provide development and property management services for the Great Park Neighborhoods and the Five Point Gateway Campus.

The operating company consolidates and controls the management of all of these entities except for the Great Park Venture and the Gateway Commercial Venture. The operating company owns a 37.5% percentage interest in the Great Park Venture and a 75% interest in the Gateway Commercial Venture and accounts for its interest in both using the equity method.

Operational Highlights

During the first quarter of the 2023, we continued to focus on execution of our three main priorities: generating revenue and positive cash flow, managing and limiting our capital spend, and managing our selling, general and administrative costs. No land sales closed during the first quarter at our communities, however, we did generate cash inflow of $17.7 million in communities facilities district reimbursements for portions of infrastructure costs we previously incurred in Valencia. As a result of our continued focus on cost rationalization and optimization, our selling, general and administrative costs were down 18% in the first quarter of 2023 compared to the same period in 2022.

The combination of a moderation in mortgage rates from their peaks in the fourth quarter of 2022, along with home buyers adjusting to the new mortgage interest rate environment and the limited inventory in the existing home markets, began to drive increased home buyer activity at our master planned communities during the first quarter of 2023. At Valencia, guest builders sold 75 homes during the first quarter of 2023 compared to 49 homes in the fourth quarter of 2022, increasing total homes sold to 1,022 since sales began in May 2021. At the Great Park Venture, in which we have a 37.5% percentage interest and manage all aspects of the development cycle, guest builders sold a total of 255 homes at the Great Park Neighborhoods during the first quarter of 2023 compared to 113 homes in the fourth quarter of 2022. Although there remains uncertainty with respect to the interest rate environment and other macroeconomic factors, we believe that builder demand will allow us to execute on both residential and commercial land sales over the remainder of 2023.

At March 31, 2023, we had $106.6 million in cash and $125.0 million available under our revolving credit facility, giving us total liquidity of $231.6 million.

22

Results of Operations

The timing of our land sale revenues is influenced by several factors, including the sequencing of the planning and development process and market conditions at our communities. As a result, we have historically experienced, and expect to continue to experience, variability in results of operations between comparable periods.

The following table summarizes our consolidated historical results of operations for the three months ended March 31, 2023 and 2022.

| Three Months Ended March 31, | |||||||||||

| 2023 | 2022 | ||||||||||

| (in thousands) | |||||||||||

Statement of Operations Data | |||||||||||

Revenues | |||||||||||

Land sales | $ | (25) | $ | 557 | |||||||

Land sales—related party | 624 | 1 | |||||||||

Management services—related party | 4,236 | 3,547 | |||||||||

Operating properties | 866 | 781 | |||||||||

Total revenues | 5,701 | 4,886 | |||||||||

Costs and expenses | |||||||||||

Land sales | — | — | |||||||||

Management services | 2,366 | 2,684 | |||||||||

Operating properties | 1,172 | 1,839 | |||||||||

Selling, general, and administrative | 13,752 | 16,791 | |||||||||

| Restructuring | — | 19,437 | |||||||||

Total costs and expenses | 17,290 | 40,751 | |||||||||

| Other income (expense) | |||||||||||

Interest income | 836 | 21 | |||||||||

Miscellaneous | (21) | 112 | |||||||||

Total other income | 815 | 133 | |||||||||

| Equity in earnings (loss) from unconsolidated entities | 1,048 | (1,032) | |||||||||

| Loss before income tax provision | (9,726) | (36,764) | |||||||||

| Income tax provision | (8) | (5) | |||||||||

| Net loss | (9,734) | (36,769) | |||||||||

| Less net loss attributable to noncontrolling interests | (5,198) | (19,639) | |||||||||

| Net loss attributable to the company | $ | (4,536) | $ | (17,130) | |||||||

23

Revenues. Revenues increased by $0.8 million, or 16.7%, to $5.7 million for the three months ended March 31, 2023, from $4.9 million for the three months ended March 31, 2022. The increase in revenues was primarily due to an increase in management services revenue at our Great Park segment during the three months ended March 31, 2023.

Selling, general, and administrative. Selling, general, and administrative expenses decreased by $3.0 million, or 18.1%, to $13.8 million for the three months ended March 31, 2023, from $16.8 million for the three months ended March 31, 2022. The decrease was mainly attributable to a decrease in employee related and selling and marketing expenses. We have had an approximately 38% reduction in headcount since the end of 2021. Most of the reductions were the result of layoffs that occurred at the end of the first quarter of 2022.

Restructuring. On February 9, 2022, Daniel Hedigan was appointed as our Chief Executive Officer. Preceding Mr. Hedigan’s appointment, Emile Haddad stepped down from his roles as Chairman, Chief Executive Officer and President effective as of September 30, 2021 and transitioned into a senior advisory role pursuant to a three-year advisory agreement. Mr. Haddad remains a member of the Board of Directors serving as Chairman Emeritus. Concurrent with Mr. Hedigan’s appointment, Lynn Jochim transitioned from her position as President and Chief Operating Officer into an advisory role pursuant to a three-year advisory agreement. Upon the appointment of Mr. Hedigan as our Chief Executive Officer, we accrued a related party liability of $15.6 million attributed to advisory agreement payments due to Mr. Haddad and Ms. Jochim over the term of the respective advisory agreements. In addition, we determined the service condition associated with Mr. Haddad and Ms. Jochim’s unvested restricted share awards had been modified. As a result of this modification, we recognized approximately $3.0 million in share-based compensation expense as a restructuring cost during the three months ended March 31, 2022.