UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-K

(Mark One)

x ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2018

OR

o TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from to

Commission File Number 001-38088

(Exact name of registrant as specified in its charter)

(949) 349-1000

Delaware | 27-0599397 | |

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |

15131 Alton Parkway, Suite 400 Irvine, California (Address of Principal Executive Offices) | 92618 (Zip code) | |

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

Title of Each Class | Name of each exchange on which registered |

Class A common shares | New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes o No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o No x

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No o

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes x No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. x

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer | o | Accelerated filer | x | |

Non-accelerated filer | o | Smaller reporting company | o | |

Emerging growth company | x | |||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. x

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes o No x

The aggregate market value of common shares held by non-affiliates of the registrant as of June 29, 2018, the last business day of the registrant’s most recently completed second fiscal quarter, based on the closing sale price per share as reported by the New York Stock Exchange on such date, was approximately $646.0 million.

As of February 28, 2019, 68,746,555 Class A common shares and 79,275,234 Class B common shares were outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the registrant's Proxy Statement for the 2019 Annual Meeting of Shareholders are incorporated herein by reference in Part III of this Annual Report on Form 10-K to the extent stated herein. Such proxy statement will be filed with the Securities and Exchange Commission within 120 days of the registrant's fiscal year ended December 31, 2018.

FIVE POINT HOLDINGS, LLC

TABLE OF CONTENTS

FORM 10-K

Page | ||

PART I. | ||

ITEM 1. | ||

ITEM 1A. | ||

ITEM 1B. | ||

ITEM 2. | ||

ITEM 3. | ||

ITEM 4. | ||

PART II. | ||

ITEM 5. | ||

ITEM 6. | ||

ITEM 7. | ||

ITEM 7A. | ||

ITEM 8. | ||

ITEM 9. | ||

ITEM 9A. | ||

ITEM 9B. | ||

PART III. | ||

ITEM 10. | ||

ITEM 11. | ||

ITEM 12. | ||

ITEM 13. | ||

ITEM 14. | ||

PART IV. | ||

ITEM 15. | ||

ITEM 16. | ||

Signatures | ||

Financial Statement Schedule | ||

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING STATEMENTS

This report contains forward-looking statements that are subject to risks and uncertainties. These statements concern expectations, beliefs, projections, plans and strategies, anticipated events or trends and similar expressions concerning matters that are not historical facts. When used, the words “anticipate,” “believe,” “expect,” “intend,” “may,” “might,” “plan,” “estimate,” “project,” “should,” “will,” “would,” “result” and similar expressions that do not relate solely to historical matters are intended to identify forward-looking statements. This report may contain forward-looking statements regarding: our expectations of our future revenues, costs and financial performance; future demographics and market conditions in the areas where our communities are located; the outcome of pending litigation and its effect on our operations; the timing of our development activities; and the timing of future real estate purchases or sales.

We caution you that any forward-looking statements presented in this report are based on our current views and information currently available to us. Forward-looking statements are subject to risks, trends, uncertainties and factors that are beyond our control. We believe these risks and uncertainties include, but are not limited to, the following:

• | risks associated with the real estate industry; |

• | downturns in economic conditions or demographic changes at the national, regional or local levels, particularly in the areas where our properties are located; |

• | uncertainty and risks related to zoning and land use laws and regulations, including environmental planning and protection laws; |

• | risks associated with development and construction projects; |

• | adverse developments in the economic, political, competitive or regulatory climate of California; |

• | loss of key personnel; |

• | uncertainties and risks related to adverse weather conditions, natural disasters and climate change; |

• | fluctuations in interest rates; |

• | the availability of cash for distribution and debt service and exposure to risk of default under debt obligations; |

• | exposure to liability relating to environmental and health and safety matters; |

• | exposure to litigation or other claims; |

• | insufficient amounts of insurance or exposure to events that are either uninsured or underinsured; |

• | intense competition in the real estate market and our ability to sell properties at desirable prices; |

• | fluctuations in real estate values; |

• | changes in property taxes; |

• | risks associated with our trademarks, trade names and service marks; |

• | conflicts of interest with our directors; |

• | general volatility of the capital and credit markets and the price of our Class A common shares; and |

• | risks associated with public or private financing or the unavailability thereof. |

Please see the “Risk Factors” under Part I, Item 1A of this report for a more detailed discussion of these and other risks.

Should one or more of these risks or uncertainties materialize, or should underlying assumptions prove incorrect, actual results may vary materially from those anticipated, estimated or projected. We caution you therefore against relying on any of these forward-looking statements.

While forward-looking statements reflect our good faith beliefs, they are not guarantees of future performance. They are based on estimates and assumptions only as of the date of this report. We undertake no obligation to update or revise any forward-looking statement to reflect changes in underlying assumptions or factors, new information, data or methods, future events or other changes, except as required by applicable law.

DEFINITIONS

In this report:

• | “acquired entities” refers, collectively, to the San Francisco Venture, the Great Park Venture and the management company, entities in which we acquired interests in the formation transactions; |

• | “acres” refers to gross acres, which includes unsaleable land, such as land on which major roads will be constructed, public parks, water quality basins, school sites and open space; |

• | “Castlelake” refers to Castlelake, L.P.; |

• | “company,” “our company,” “us,” “we,” and “our” refer to Five Point Holdings, LLC, together with its consolidated subsidiaries; |

• | “EB-5” refers to the Immigrant Investor Program under which employment-based visas are set aside for participants who invest in commercial enterprises associated with regional centers approved by the United States Citizenship and Immigration Services based on proposals for promoting economic growth; |

• | “Five Point Gateway Campus” refers to approximately 73 acres of commercial land in the Great Park Neighborhoods, on which four buildings have been newly constructed with an aggregate of one million square feet of research and development and office space; |

• | “formation transactions” refers to the transactions effected on May 2, 2016, in which, among other things, (1) we acquired an interest in, and became the managing member of, the San Francisco Venture, (2) the limited liability company agreement of the San Francisco Venture was amended and restated to provide for the possible future exchange of the remaining interests in the San Francisco Venture for interests in our operating company, (3) we acquired a 37.5% percentage interest in the Great Park Venture, and became the administrative member of the Great Park Venture, and (4) we acquired the management company. See “Part I, Item 1. Business—Structure and Formation of Our Company”; |

• | “FP LP” refers to Five Point Communities, LP, a Delaware limited partnership; |

• | “FP LP Class B partnership interests” or “Class B partnership interests in FP LP” refer to partnership interests in FP LP owned by Lennar and FPC-HF that are entitled to receive distributions equal to the amount of any incentive compensation payments under the amended and restated development management agreement that are attributable to payments on legacy interests in the Great Park Venture; |

• | “FP Inc.” refers to Five Point Communities Management, Inc., a Delaware corporation, which is the general partner of, and owns a 0.5% Class A limited partnership interest in, FP LP; |

• | “FPC-HF” refers to FPC-HF Venture I, LLC, a Delaware limited liability company, which is owned, directly or indirectly, by an affiliate of Castlelake, an affiliate of Lennar and certain employees of the management company; |

• | “FPL” refers to our subsidiary, Five Point Land, LLC, a Delaware limited liability company, which owns Newhall Land & Farming; |

• | “fully exchanged basis” assumes (1) the exchange of all outstanding Class A units of the operating company for our Class A common shares on a one-for-one basis, (2) the exchange of all outstanding Class A units of the San Francisco Venture for our Class A common shares on a one-for-one basis and (3) the conversion of all of our outstanding Class B common shares into Class A common shares; |

• |

• | “Gateway Commercial Venture” refers to Five Point Office Venture Holdings I, LLC, a Delaware limited liability company, which owns the Five Point Gateway Campus; |

• | “Great Park Venture” refers to Heritage Fields LLC, a Delaware limited liability company, which is developing Great Park Neighborhoods; |

• | “homes” includes single-family detached homes, single-family attached homes and apartments for rent; |

• | “homesite” refers to a residential lot or a portion thereof on which a home will be built; |

• | “legacy interests” refers to membership interests in the Great Park Venture, which are currently held by the entities that owned the Great Park Venture immediately prior to the formation transactions, and entitle them to receive priority distributions from the Great Park Venture in an aggregate amount equal to $565 million ($355 million of which has been paid); |

• | “Lennar” refers to Lennar Corporation and its subsidiaries; |

• | “Lennar-CL Venture” refers to a joint venture between Lennar and an affiliate of Castlelake, which acquired certain assets, and assumed certain liabilities, from the San Francisco Venture immediately prior to the formation transactions; |

• | “management company” refers, collectively, to FP LP and FP Inc., which have historically managed the development of Great Park Neighborhoods and Newhall Ranch; |

• | “Newhall Land & Farming” refers to The Newhall Land and Farming Company, a California limited partnership, which is developing Newhall Ranch; |

• | “operating company” refers to Five Point Operating Company, LP, a Delaware limited partnership; |

• | “our communities” refers to the communities that we are developing, including Newhall Ranch in Los Angeles County, Candlestick Point and The San Francisco Shipyard in the City of San Francisco, and Great Park Neighborhoods in Orange County, but excluding the Treasure Island community in the City of San Francisco and the Concord community in the San Francisco Bay Area, for which we are or have provided development management services, but in which we do not own any interest. |

• | “percentage interests” refers to membership interests in the Great Park Venture that entitle the holders to receive all distributions from the Great Park Venture after priority distributions have been paid to the holders of the legacy interests in the Great Park Venture; |

• | “San Francisco Agency” refers to the Office of Community Investment and Infrastructure, the successor to the Redevelopment Agency of the City and County of San Francisco; |

• | “San Francisco Venture” refers to The Shipyard Communities, LLC, a Delaware limited liability company, which is developing Candlestick Point and The San Francisco Shipyard; and |

• | “San Francisco Venture transactions” refers to the transactions effected on May 2, 2016, in which the San Francisco Venture agreed to transfer certain assets and liabilities to the Lennar-CL Venture. See “Part I, Item 1. Business—Our Communities—Candlestick Point and The San Francisco Shipyard.” |

PART I

ITEM 1. Business

We are an owner and developer of mixed-use, master-planned communities in California. Our three existing communities have the general plan and zoning approvals necessary for the construction of thousands of homesites and millions of square feet of commercial space, and they represent a significant portion of the real estate available for development in three major markets in California—Los Angeles County, San Francisco County and Orange County.

Structure and Formation of Our Company

In 2009, our company was formed as a limited liability company (under the name “Newhall Holding Company, LLC”) to acquire ownership of Newhall Land & Farming. Our management company was originally formed in 2009 as a joint venture between our Chairman and Chief Executive Officer, Emile Haddad, and Lennar Corporation to manage the properties owned by Newhall Land & Farming and to pursue similar development opportunities. Our management team was an integral part of the team in charge of developing and implementing land strategies on the west coast for Lennar prior to the formation of our management company. Key members of our management team have led the acquisition, entitlement, planning and development of all three of our communities since their inception. Our management team also has long-standing relationships with our principal equityholders, including Lennar.

In May 2016, we completed the formation transactions to combine the management company with ownership of our three California communities. In the formation transactions, among other things:

• | we acquired an interest in, and became the managing member of, the San Francisco Venture; |

• | we acquired a 37.5% percentage interest in the Great Park Venture, and we became the administrative member of the Great Park Venture; and |

• | we acquired the management company, which has historically managed the development of Great Park Neighborhoods and Newhall Ranch. |

In August 2017, we acquired a 75% interest in the Gateway Commercial Venture, the entity that owns the Five Point Gateway Campus.

1

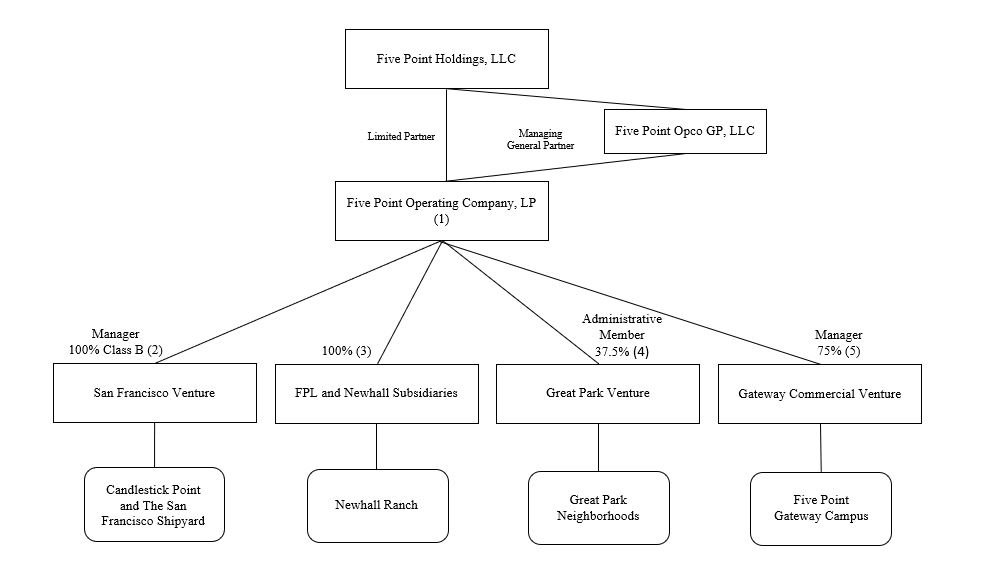

The diagram below presents a simplified depiction of our current organizational structure.

(1) Through a wholly owned subsidiary, we serve as sole managing general partner of the operating company and, as of December 31, 2018, we owned approximately 61.7% of the outstanding Class A units of the operating company. We conduct all of our businesses in or through the operating company, which owns, directly or indirectly, equity interests in, and controls the management of, FPL, the San Francisco Venture and the management company. Class A units of the operating company can be exchanged, on a one-for-one basis, for our Class A common shares, subject to certain holding periods. Based on the closing price of our Class A common shares on February 28, 2019, our market capitalization on a fully exchanged basis was approximately $1.2 billion.

(2) The operating company owns all of the outstanding Class B units of the San Francisco Venture. The Class A units of the San Francisco Venture, which the operating company does not own, are intended to be substantially economically equivalent to Class A units of the operating company. As the holder of all outstanding Class B units, the operating company is entitled to receive 99% of available cash from the San Francisco Venture after the holders of Class A units have received distributions equivalent to the distributions, if any, paid on Class A units of the operating company. Class A units of the San Francisco Venture can be exchanged, on a one-for-one basis, for Class A units of the operating company.

(3) We hold our interest in FPL directly and indirectly through the operating company and the management company.

(4) Through a wholly owned subsidiary, the operating company owns a 37.5% percentage interest in the Great Park Venture. Holders of legacy interests in the Great Park Venture are entitled to receive priority distributions in an amount equal to $565.0 million, of which $355.0 million has been distributed as of December 31, 2018. We are the administrative member of the Great Park Venture. Management of the venture is vested in the four voting members, who have a total of five votes. Major decisions generally require the approval of at least 75% of the votes of the voting members. We have two votes, and the other three voting members each have one vote, so we are unable to approve any major decision without the consent or approval of at least two of the other voting members. We do not include the Great Park Venture as a consolidated subsidiary in our consolidated financial statements.

(5) Through a wholly owned subsidiary, the operating company owns a 75% interest in the Gateway Commercial Venture and serves as its manager. However, the manager’s authority is limited. Major decisions by the Gateway Commercial Venture generally require unanimous approval by an executive committee composed of two people designated by us and two people designated by another investor. Some decisions require approval by

2

all of the members of the Gateway Commercial Venture. We do not include the Gateway Commercial Venture as a consolidated subsidiary in our consolidated financial statements.

Tax Classification

We have elected to be treated as a corporation for U.S. federal income tax purposes. As a result, an owner of our shares will not report our items of income, gain, loss and deduction on its U.S. federal income tax return, nor will an owner of our shares receive a Schedule K-1. Our shareholders also will not be subject to state income tax filings in the various states in which we conduct operations as a result of owning our shares. Distributions on our shares will be treated as dividends on corporate stock for U.S. federal income tax purposes to the extent of our current and accumulated earnings and profits and will be reported on Form 1099, to the extent applicable.

Our Competitive Strengths

We believe the following strengths will provide us with a competitive advantage in implementing our business strategy:

• | Attractive locations in desirable and supply constrained California coastal markets |

• | Significant scale with favorable zoning and entitlements |

• | Experienced and proven leadership |

• | Expertise in partnering with governmental entities |

• | Significant discretion in timing and amount of land development expenditures |

• | Flexible capital structure with a conservative operating philosophy |

Overview of Business Segments

Our four reportable segments are Newhall, San Francisco, Great Park and Commercial:

• | Our Newhall segment includes the Newhall Ranch community, as well as other land historically owned by FPL, including 16,000 acres in Ventura County and approximately 500 acres of remnant commercial, residential and open space land in Los Angeles County. |

• | Our San Francisco segment includes the Candlestick Point and The San Francisco Shipyard communities, as well as development management services that we provide to Lennar with respect to the Concord community in the San Francisco Bay Area. |

• | Our Great Park segment includes the Great Park Neighborhoods community and development management services provided by the management company for the Great Park Venture. |

• | Our Commercial segment includes the Five Point Gateway Campus and property management services provided by the management company for the Gateway Commercial Venture. |

For financial results and operating performance of our reportable segments, review Note 15 of our consolidated financial statements included under Part II, Item 8 of this report and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” under Part II, Item 7 of this report.

Our Business

We are primarily engaged in the business of planning and developing our three mixed-use, master-planned communities, and our principal source of revenue is the sale of residential and commercial land sites to homebuilders, commercial developers and commercial buyers. We may also retain a portion of the commercial and multi-family properties in our communities as income-producing assets.

3

Our planning and development process involves the following components:

Master planning. We design all aspects of our communities, creating highly desirable places to live, work, shop and enjoy an active lifestyle. Our designs include a wide range of amenities, such as high quality schools, parks and recreational areas, entertainment venues and walking and biking trails. Each community is comprised of several villages or neighborhoods, each of which offers a range of housing types, sizes and prices. In addition to the master land planning we undertake for each community, we typically create the floorplans and elevations for each home, as well as the landscape design for each neighborhood, considering each neighborhood’s individual character within the context of the overall plan for the community. For the commercial aspects of our communities, we look for commercial enterprises that will best add value to the community by providing needed services, additional amenities or local jobs. In designing the overall program at each community, we consider the appropriate balance of housing and employment opportunities, access to transportation, resource conservation and enhanced public open spaces and wildlife habitats. We continually evaluate our plans for each community, and make adjustments that we deem appropriate based on changes in local economic factors and other market dynamics.

Entitlements. We typically obtain all discretionary entitlements and approvals necessary to develop the infrastructure within our communities and prepare our residential and commercial lots for construction. We also typically obtain all discretionary entitlements and approvals that the homebuilder or commercial builder will need to build homes or commercial buildings on our lots, although we may from time to time allocate responsibility for obtaining certain discretionary entitlements to a homebuilder or commercial builder. Although we have general plan and zoning approvals for our communities, individual development areas within our communities are at various stages of planning and development and have received different levels of discretionary entitlements and approvals. For additional information, see “—Our Communities” below.

Horizontal development (infrastructure). We refer to the process of preparing the land for construction of homes or commercial buildings as “horizontal development.” This involves significant investments in a community’s infrastructure and common improvements, including grading and installing roads, sidewalks, gutters, utility improvements (such as storm drains, water, gas, sewer, power and communications), landscaping and shared amenities (such as community buildings, neighborhood parks, trails and open spaces) and other actions necessary to prepare residential and commercial lots for vertical development.

Land sales. After horizontal development for a given phase or parcel is completed, graded lots are typically sold to homebuilders, commercial builders or commercial buyers. We typically sell homesites to a diverse group of high-quality homebuilders in a competitive process, although in some cases we may negotiate directly with a single homebuilder. In addition to the base purchase price, our residential land sales typically involve participation provisions that allow us to share in the profits realized by the homebuilders. We sell commercial lots to developers through a competitive process or negotiate directly with the buyer. We also regularly assess our development plan and may retain a portion of the commercial and multi-family properties within our communities as income-producing assets.

Vertical development (construction). We refer to the process of building structures (buildings or houses) and preparing them for occupancy as “vertical development.” Single-family residences in our communities are built by third-party homebuilders. Commercial buildings in our communities are usually built by a third-party developer or the buyer. For commercial or multi-family properties that we retain, we may construct the building ourselves or enter into a joint venture with an established developer to construct a particular property (such as a retail development).

Community programming. Our community building efforts go beyond development and construction. We offer numerous community events, including music, food and art festivals, outdoor movies, educational programs, health and wellness programs, gardening lessons, cooking lessons, food truck events, bike tours and various holiday festivities. We plan and program all of our events with a goal of building a community that transcends the physical features of our development and connects neighbors through their interests. We believe community building efforts create loyal residents that can become repeat customers within our multi-generational communities.

4

Sequencing. In order to balance the timing of our revenues and expenditures, we typically sequence the development of individual neighborhoods or villages within our communities. As a result, many of the master planning, entitlement, development, sales and other activities described above may occur at the same time in different locations within a single community. Further, depending on the specific plans for each community and market conditions, we may vary the timing of certain of these phases. Throughout this process, we continually analyze each community relative to its market to determine which portions to sell, which portions to build and then sell, and which portions to retain as part of our portfolio of commercial and multi-family properties.

Our Communities

Newhall Ranch

Newhall Ranch is a mixed-use, master-planned community in Los Angeles County that spans approximately 15,000 acres and is designed to include approximately 21,500 homesites, approximately 11.5 million square feet of commercial space, approximately 50 miles of trails, approximately 275 acres of community parks and approximately 10,000 acres of protected open space. The actual commercial square footage and number of homesites are subject to change based on ultimate use and land planning. The land at Newhall Ranch is not subject to any material liens or encumbrances.

Newhall Ranch is located in an unincorporated portion of Los Angeles County along the Santa Clara River in the western portion of the Santa Clarita Valley. The property is located approximately 35 miles northwest of downtown Los Angeles, 15 miles north of the San Fernando Valley and is adjacent to the City of Santa Clarita. Newhall Ranch is adjacent to Interstate 5 and State Highway 126. Newhall Ranch is also approximately 45 miles north of the Los Angeles International Airport (LAX) and 21 miles northwest of the Bob Hope Airport (BUR) in Burbank.

The County of Los Angeles has approved the general plan and zoning for Newhall Ranch. Additionally, we have vesting tentative tract maps for two development areas within Newhall Ranch - Mission Village and Landmark Village. We commenced horizontal development activities for our first development area, Mission Village, in October 2017. We continued horizontal development activities throughout 2018 and expect to start delivering homesites to builders in late 2019. Mission Village is approved to include 4,055 homesites, including a mix of single-family detached homes, single-family attached homes, apartments and for rent affordable units, and approximately 1.6 million square feet of commercial development.

Candlestick Point and The San Francisco Shipyard

Candlestick Point and The San Francisco Shipyard, located on approximately 800 acres of bayfront property in the City of San Francisco, is designed to include approximately 12,000 homesites, approximately 6.3 million square feet of commercial space, approximately 100,000 square feet of community space, artist studios and approximately 355 acres of parks and open space. The actual commercial square footage and number of homesites are subject to change based on ultimate use and land planning. The land owned by us at Candlestick Point and The San Francisco Shipyard is not subject to any material liens or encumbrances.

Candlestick Point and The San Francisco Shipyard is located almost equidistant between downtown San Francisco and the San Francisco International Airport (SFO). It consists of two distinct, but contiguous, parcels of real estate. Candlestick Point, the southern parcel, consists of approximately 280 acres on San Francisco’s waterfront. This nationally recognized site was the location of Candlestick Park stadium, former home of the San Francisco 49ers and the San Francisco Giants. The San Francisco Shipyard, the northern parcel, consists of approximately 495 acres on the former site of the Hunters Point Navy Shipyard.

The City and County of San Francisco have approved the general plan and zoning for Candlestick Point and The San Francisco Shipyard. We have vesting tentative tract maps for the remaining development areas within Candlestick Point, and we commenced horizontal development activities there in 2015. We do not yet have vesting tentative tract maps for The San Francisco Shipyard or final maps for any of the remaining development areas.

5

At The San Francisco Shipyard, approximately 408 acres are still owned by the U.S. Navy and will not be conveyed to us until the U.S. Navy satisfactorily completes its finding of suitability to transfer, or “FOST,” process, which involves multiple levels of environmental and governmental investigation, analysis, review, comment and approval. Based on our discussions with the U.S. Navy, we had previously expected the U.S. Navy to deliver this property between 2019 and 2022. However, allegations that Tetra Tech, Inc. (“Tetra Tech”), a contractor hired by the U.S. Navy, misrepresented sampling results at The San Francisco Shipyard have resulted in data reevaluation, governmental investigations, criminal proceedings, lawsuits, and a determination by the U.S. Navy and other regulatory agencies to undertake additional sampling. As part of the 2018 Congressional spending bill, the U.S. Department of Defense allocated $36.0 million to help fund resampling efforts at The San Francisco Shipyard. An additional $60.4 million to fund resampling efforts was approved as part of a 2019 military construction spending bill. These activities have delayed the remaining land transfers from the U.S. Navy and could lead to additional legal claims or government investigations, all of which could further delay or impede our future development of such parcels. Our development plans were designed with the flexibility to adjust for potential land transfer delays, and we have the ability to shift the phasing of our development activities to account for delays caused by U.S. Navy retesting, but there can be no assurance that these matters and other related matters that may arise in the future will not materially impact our development plans. Accordingly, our immediate development focus is on our Candlestick Point community that is not subject to land transfers from the U.S. Navy. For additional information about the finding of suitability to transfer process, see “—Regulation—FOST Process.”

The San Francisco Venture previously entered into a project with a joint venture (the “Mall Venture”) between an affiliate of The Macerich Company (“Macerich”) and a venture between Lennar and Castlelake to construct an urban retail outlet shopping district at Candlestick Point (the “Retail Project”). Construction of the Retail Project commenced in 2015 with the demolition of the Candlestick Park stadium and other infrastructure work. In early 2019, however, we and the members of the Mall Venture decided not to proceed with the Retail Project. Accordingly, on February 13, 2019, transactions related to the termination of the Retail Project were consummated, which resulted in the termination of the obligation of the San Francisco Venture to convey parcels of property on which the Retail Project was intended to be developed by the Mall Venture. The San Francisco Venture was also released from certain development obligations. In return, the San Francisco Venture repaid Macerich a $65.1 million obligation related to a promissory note in the same principal amount, plus approximately $5.5 million of accrued interest associated with the promissory note. The San Francisco Venture also issued an aggregate of 436,498 of its Class A units (while we concurrently issued 436,498 Class B common shares) to affiliates of Lennar and Castlelake. The San Francisco Venture can now redevelop these parcels for alternative uses.

Great Park Neighborhoods

Great Park Neighborhoods, located in Irvine, California, is an approximately 2,100 acre mixed-use, master-planned community that is being developed on the former site of the U.S. Marine Corp’s El Toro Air base (“El Toro Base”) in Orange County. Great Park Neighborhoods is designed to include approximately 9,500 homesites (including up to 1,056 affordable homesites), approximately 4.9 million square feet of commercial space, approximately 61 acres of parks and approximately 138 acres of trails and open space. The actual commercial square footage and number of homesites are subject to change based on ultimate use and land planning. The land at Great Park Neighborhoods is not subject to any material liens or encumbrances.

Great Park Neighborhoods is approximately seven miles from the Pacific Ocean, approximately nine miles from the University of California, Irvine (UCI) and approximately 17 miles from Disneyland. It is adjacent to the Orange County Great Park, a metropolitan public park that will be nearly twice the size of New York’s Central Park upon completion. Great Park Neighborhoods is close to Interstate 5, Interstate 405, State Route 133 and John Wayne Airport (SNA) in Orange County.

The City of Irvine has approved the general plan and zoning for Great Park Neighborhoods. We have vesting tentative tract maps for almost all development areas within Great Park Neighborhoods and final maps for many of the development areas. The first homesites were sold in April 2013 and, as of December 31, 2018, the Great Park Venture had sold 5,409 homesites (including 544 affordable homesites) and commercial land allowing for

6

development of up to 2 million square feet of commercial (research and development) space. For additional information about the commercial land sale, see “—Commercial” below.

Commercial

In August 2017, the Gateway Commercial Venture, in which we own a 75% interest, acquired the Five Point Gateway Campus, consisting of approximately 73 acres of commercial land in the Great Park Neighborhoods containing four newly constructed buildings, two of which were leased back to the seller, Broadcom Limited (together with its subsidiaries, “Broadcom”). The Five Point Gateway Campus includes approximately one million square feet consisting of research and development and office space across the four buildings designed to accommodate thousands of employees. Broadcom is the largest tenant, leasing approximately 660,000 square feet of research and development space pursuant to a 20-year triple net lease. We and Lennar have entered into separate 130-month full service gross leases to occupy approximately 135,000 aggregate square feet.

We currently expect to develop and operate certain commercial properties within our existing master-planned communities. We may develop and operate these properties on our own, or we may choose from time to time to develop and/or operate a particular property or properties in a strategic joint venture or other financing or entity structure with a third-party

Factors we consider in determining whether or not to proceed with a particular commercial investment include (1) our existing knowledge of the master-planned communities we are currently developing and understanding their respective needs, (2) whether, in our judgment, a particular commercial property or investment will create additional value for our remaining land within the community, in addition to achieving desired investment returns on such property or investment on a stand-alone basis, (3) existing entitlements and our ability to change them, (4) compatibility of the physical site with our proposed uses, and (5) environmental considerations, traffic patterns and access to the site.

Other Properties

We own approximately 16,000 acres in Ventura County that are primarily used for agriculture and energy operations. We also own approximately 500 acres of remnant commercial, residential and open space land in Los Angeles County that is planned to be sold or deeded to third parties over the next five years.

Development Management Services

Through the management company, we receive fees for providing development management services for Great Park Neighborhoods and for providing property management services to the Gateway Commercial Venture.

Additionally, we provide certain (but not all) development management services to other ventures in which Lennar is an investor and to the Lennar-CL Venture in connection with their involvement in real estate activities at The San Francisco Shipyard. We also provided certain development management services to the Lennar-CL Venture related to the Retail Project at the Candlestick Point community until early 2019.

Competition

We compete with other residential, retail and commercial property developers in the development of properties in the Northern and Southern California markets. Significant factors that we believe allow us to compete effectively in this business include:

• | the size and scope of our mixed-use, master-planned communities; |

• | the recreational and cultural amenities available within our communities; |

• | the commercial centers in our communities; |

7

• | our relationships with homebuilders; and |

• | the proximity of our communities to major metropolitan areas. |

Seasonality

Our business and results of operations are not materially impacted by seasonality.

Regulation

Entitlement Process

Land use and zoning authority is exercised by local municipalities through the adoption of ordinances, regulations or zoning codes to direct the use and development of private property by controlling the use, size, density and location of and access to developments on private land. Such ordinances, regulations or codes typically divide uses of land into two categories—permitted uses and discretionary uses. Permitted uses are presumptively permitted, while discretionary uses are subject to a discretionary approval process, usually involving an application, an environmental review and a public hearing with input from other locally affected property owners and stake holders. In order to grant a discretionary use entitlement, the municipality must find that the use does not negatively impact surrounding properties and may condition such an entitlement with special requirements or limitations unique to each individual case. We typically obtain all discretionary entitlements and approvals necessary to develop the infrastructure within our communities and prepare our residential and commercial lots for construction. We also typically obtain all discretionary entitlements and approvals that the homebuilder or commercial builder will need to build homes or commercial buildings on our lots, although we may from time to time allocate responsibility for obtaining certain discretionary entitlements to a homebuilder or commercial builder.

We have incurred significant costs and expenses over the last 10 to 15 years in order to obtain the primary entitlements (general plan and zoning approvals) for our communities. Once these primary entitlements are obtained, we continue to refine the master plan for each community by planning specific development areas and obtaining the necessary governmental approvals for a development area. Among other things, we typically need to obtain the following approvals for each development area: (1) approval of the subdivision maps (such as vesting tentative tract maps and parcel maps) that allow the land to be divided into separate legal lots for residential, commercial and other improvements; (2) approval of the improvement plans that set forth certain design, engineering and other elements of infrastructure, parks, homes, commercial buildings and other improvements; (3) approval of the final map that allows for the conveyance of individual homesites and commercial lots; and (4) any other discretionary approvals needed to construct, finance, sell, lease or maintain the homes or commercial buildings within a development area.

We may also need to obtain state and federal permits for land development activities in certain development areas, including, for example, permits and approvals issued by state and federal resource agencies authorizing impacts to species covered by endangered species acts or impacts to state and federal waters or wetlands.

Development areas within our communities are at various stages of planning and development and, therefore, have received different levels of discretionary entitlements and approvals. In some cases, development areas have obtained entitlements and approvals allowing homes and commercial buildings to be built and sold, and in other cases development areas require further discretionary entitlements or approvals prior to the commencement of construction. In still other cases, our approvals have been challenged by third parties. For additional information on current legal challenges, see “Item 3. Legal Proceedings.”

Environmental Matters

Under various federal, state and local laws and regulations relating to the environment, as a current or former owner or operator of real property, we may be liable for costs and damages resulting from the presence or discharge

8

of hazardous or toxic substances, waste or petroleum products at, on, in, under or migrating from such property, including costs to investigate and clean up such contamination and liability for damage to natural resources. Such laws often impose liability without regard to whether the owner or operator knew of, or was responsible for, the presence of such contamination, and the liability may be joint and several. These liabilities could be substantial and the cost of any required remediation, removal, fines or other costs could exceed the value of the property or our aggregate assets. In addition, the presence of contamination or the failure to remediate contamination at our properties may expose us to third-party liability for costs of remediation or personal or property damage or materially adversely affect our ability to sell, lease or develop our properties or to borrow using the properties as collateral. In addition, environmental laws may create liens on contaminated sites in favor of the government for damages and costs it incurs to address such contamination. Moreover, if contamination is discovered on our properties, environmental laws may impose restrictions on the manner in which property may be used or businesses may be operated, and these restrictions may require substantial expenditures. Such remaining contamination encountered during our construction and development activities also may require investigation or remediation, and we could incur costs or experience construction delays as a result of such discoveries.

Some of our properties were used in the past for commercial or industrial purposes, or are currently used for commercial purposes, that involve or involved the use of petroleum products or other hazardous or toxic substances, or are adjacent to or near properties that have been or are used for similar commercial or industrial purposes. As a result, some of our properties have been or may be impacted by contamination arising from the releases of such substances. For example, oil and gas wells have formerly operated or are currently operating at Newhall Ranch. In certain cases, prior owners or operators have in the past investigated or remediated, or are currently investigating or remediating, such conditions, but contamination may continue to be present at these sites, and future remedial activities could delay or otherwise impede property development on sites where contamination is present.

In addition, The San Francisco Shipyard and Great Park Neighborhoods properties were formerly operated by the U.S. Navy as defense plants. As a result of these historic operations, portions of these properties have been or currently are listed on the U.S. Environmental Protection Agency’s (“USEPA”) National Priorities List as sites requiring cleanup under federal environmental laws. While investigation and cleanup activities have been substantially completed for Great Park Neighborhoods, significant work is contemplated over the next few years for certain parcels within The San Francisco Shipyard, which will delay the transfer of such parcels to us for development.

The National Environmental Policy Act (“NEPA”) requires federal agencies to integrate environmental values into their decision making processes by considering the environmental impacts of their proposed actions and reasonable alternatives to those actions. To meet NEPA requirements federal agencies prepare a detailed statement known as an Environmental Impact Statement (“EIS”). Additionally, all Department of Defense installations (such as The San Francisco Shipyard and the El Toro Base) selected for closure or realignment pursuant to the Base Closure and Realignment Acts of 1988 or 1990 and being considered for transfer by deed, and where a release or disposal of hazardous substances or petroleum products has occurred, are subject to an environmental review process and may not be transferred until a finding of suitability for transfer (“FOST”) is documented. In addition, our development projects are subject to the California Environmental Quality Act (“CEQA”), which is similar in scope to NEPA, and requires potential environmental impacts of projects subject to discretionary governmental approval to be studied by the California governmental entity approving the proposed projects. Projects with significant expected impacts require an Environmental Impact Report (“EIR”) while more limited projects may be approved based on a Mitigated Negative Declaration. All of our development sites and projects have either been or continue to be investigated, remediated or reviewed (with documented EISs, FOSTs and EIRs, as applicable) in accordance with the above-described and other applicable environmental laws to determine the suitability of their proposed uses and to protect human health and the environment.

New or additional permitting requirements, new interpretations of requirements, changes in our operations or litigation or community objections over the adequacy of conducted reviews and other response and mitigation actions could also trigger the need for either amended or new reviews or actions, which could result in increased costs or delays of, modification of, or denial of rights to conduct, our development programs. For additional information on legal challenges to our projects under environmental laws see “Item 3. Legal Proceedings.”

9

When we identify conditions that require a response under environmental laws, we endeavor to address identified contamination or mitigate risks associated with such contamination as required (or ensure that such actions are taken by other parties, such as prior owners and operators); however, we cannot assure you that we will not need to take additional action, incur additional costs, or delay or modify our development plans to address these conditions or other environmental conditions that may be discovered in the future. As a result of the foregoing, we could potentially incur material liabilities.

We are also subject to a variety of other local, state, federal and other laws and regulations concerning the environment, including those governing air emissions, wastewater discharges and use and disposal of hazardous or toxic substances. The particular environmental laws that apply to any given property vary according to multiple factors, including the property’s location, its environmental conditions and the present and former uses of the property, as well as adjoining properties. These issues may result in delays, may cause us to incur substantial compliance and other costs, and can prohibit or severely restrict development activity in environmentally sensitive regions or areas. For example, in those cases where wetlands or an endangered or threatened species are impacted by proposed development, environmental rules and regulations can result in the restriction or elimination of development in such identified environmentally sensitive areas.

Environmental laws also govern the presence, maintenance and removal of asbestos-containing materials (“ACM”), and may impose fines and penalties for failure to comply with these requirements or expose us to third-party liability (such as liability for personal injury associated with exposure to asbestos). Such laws require that owners or operators of buildings containing ACM (and employers in such buildings) properly manage and maintain the asbestos, adequately notify or train those who may come into contact with asbestos and undertake special precautions, including removal or other abatement, if asbestos would be disturbed during renovation or demolition of a building. In addition, soils at Candlestick Point and The San Francisco Shipyard are known to contain naturally occurring asbestos, which must be managed, including through dust management plans. In the past, we have been subject to penalties for failure to monitor asbestos dust during development activities at The San Francisco Shipyard, and, although we endeavor to maintain (and to cause our contractors to maintain) compliance, we could incur such fines or penalties in the future.

FOST Process

The U.S. Navy is implementing its cleanup program at The San Francisco Shipyard pursuant to various federal laws and authorities. The Comprehensive Environmental Response, Compensation, and Liability Act (“CERCLA”) requires the U.S. Navy to remediate The San Francisco Shipyard in accordance with a federal facilities agreement entered into with the USEPA and the State of California, which sets forth procedures and timeframes for remedial decisions and deliverables. In accordance with the federal facilities agreement, the National Contingency Plan, 40 C.F.R. Part 300 and Department of Defense procedures, the U.S. Navy’s cleanup process involves (1) preparation of a series of reports documenting various investigative and remedial activities and (2) securing approval of those reports from the USEPA and the State of California. The remedial steps and related reports, each of which is subject to review, comment and approval, are as follows:

Preliminary assessment/site inspection. This is an initial review of the site, including review of historical records and visual inspections. Limited sampling and analysis of soil, surface water and groundwater may also occur.

Remedial investigation. The remedial investigation involves a closer look into each of the areas of concern identified in the preliminary assessment/site inspection, and involves collecting and analyzing samples of multiple media (soil, soil gas, sediment, groundwater, etc.). The remedial investigation addresses the nature and extent of contamination at each area of concern identified in the parcel. The remedial investigation also includes preparation of a Human Health Risk Assessment and an Ecological Risk Assessment, as appropriate. The Human Health Risk Assessment identifies the contaminants that could pose a health risk under different exposure scenarios and identifies potential numeric remediation goals.

10

Feasibility study. The feasibility study evaluates the effectiveness, implementability and cost of various alternative remedial technologies that could be used to reduce site risk to acceptable levels, based on the results of the risk assessment and other data collected during the remedial investigation.

Proposed plan. The proposed plan summarizes the findings of the remedial investigation and proposes a preferred remedial approach for each area of concern in the parcel based on the options evaluated in the feasibility study. This step includes a public meeting to provide the public with relevant information and an opportunity to comment on the preferred cleanup alternative.

Record of decision. Once the U.S. Navy, the USEPA and the State of California select and approve the remedy for the parcel, the U.S. Navy documents and publishes the decision in the record of decision, which responds to all comments on the proposed plan.

Remedial design. The remedial design sets forth details of how the remedies identified in the record of decision will be carried out. The remedial design includes a detailed engineering design for implementing, operating and maintaining the selected cleanup alternative. The U.S. Navy also distributes a fact sheet to the public before beginning work on the cleanup.

Remedial action work plan/remedial action implementation. The U.S. Navy conducts remedial action in accordance with an approved remedial action work plan, which is based on the remedial design.

Remedial action completion report. Once complete, the cleanup is documented in a remedial action completion report.

FOST. Prior to conveyance of real property, CERCLA requires the U.S. Navy to remediate hazardous substances to a level consistent with the protection of human health and the environment. Following the completion and approval of the remedial action completion report, the U.S. Navy documents its findings that such remediation has occurred, and that the property is suitable for transfer, consistent with all applicable laws and authorities, in a FOST.

Investment Policies

Investments in Real Estate or Interests in Real Estate

We are a real estate development and operating company that specializes in the development and operation of mixed-use, master-planned communities. Our goal is to create sustainable, long-term growth and value for our shareholders. We do not currently have an investment policy; however, our board of directors may adopt one in the future.

We expect to pursue our investment objectives primarily through the ownership, development, operation and disposition of our communities: (1) Newhall Ranch; (2) Candlestick Point and The San Francisco Shipyard; and (3) Great Park Neighborhoods. Although we currently have no definitive agreements to acquire other properties, we may do so in the future. Our future investment or development activities will not necessarily be limited to any geographic area, product type or to a specified percentage of our assets.

We may also participate with third parties in property ownership, development and operation, through joint ventures, private equity real estate funds or other types of co-ownership. We also may acquire real estate or interests in real estate in exchange for the issuance of our Class A common shares, our preferred shares, options to purchase shares or Class A units of the operating company. These types of investments may permit us to own interests in larger assets without unduly restricting our diversification and, therefore, provide us with flexibility in structuring our portfolio.

11

We will limit our investment in any securities so that we do not fall within the definition of an “investment company” under the Investment Company Act of 1940, as amended.

Investments in Real Estate Mortgages

We may, at the discretion of our board of directors, invest in mortgages and other types of real estate interests, but we do not currently, nor do we currently intend to, engage in these activities. If we choose to invest in mortgages, we would expect to invest in mortgages secured by real property interests. The Company does not have a policy that restricts the proportion of our assets that may be invested in a type of mortgage or any single mortgage or type of mortgage loan.

Securities of, or Interests in, Persons Primarily Engaged in Real Estate Activities and Other Issuers

We do not currently intend to invest in securities of other entities engaged in real estate activities or securities of other issuers, including for the purpose of exercising control over such entities. However, we may do so in the future.

Investments in Other Securities

Other than as described above and for short-term securities pending long-term commitment, we do not currently intend to invest in any additional securities such as bonds, preferred shares or common shares.

Employees

At December 31, 2018, we had approximately 180 employees.

Available Information

Our website is www.fivepoint.com. We make available free of charge through our website our annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, and amendments to these reports filed or furnished pursuant to Section 13(d) or 15(d) of the Securities Exchange Act of 1934 (the “Exchange Act”) as soon as reasonably practicable after being filed with, or furnished to, the Securities and Exchange Commission (“SEC”). The information contained in, or that can be accessed through, our website is not incorporated by reference and is not a part of this annual report on Form 10-K. In addition, you may obtain the documents that we file with the SEC from the SEC’s website at www.sec.gov.

ITEM 1A. Risk Factors

You should carefully consider the following material risks, as well as the other information contained in this Annual Report on Form 10-K, including “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and the consolidated financial statements and the related notes. If any of the following risks actually occur, our business, financial condition, results of operations or prospects could be materially and adversely affected. In such an event, the trading price of our Class A common shares could decline and you could lose part or all of your investment.

Risks Related to Real Estate

Our performance is subject to risks associated with the real estate industry.

Our economic performance is subject to various risks and fluctuations in value and demand, many of which are beyond our control. Certain factors that affect real estate generally and our properties specifically may adversely affect our revenue from land sales or leasing of retail or other commercial space. The following factors, among others, may adversely affect the real estate industry, including our properties, and could therefore adversely impact our financial condition and results of operations:

12

• | downturns in economic conditions or demographic changes at the national, regional or local levels, particularly in the areas where our properties are located; |

• | significant job losses and unemployment levels, which may decrease demand for our properties; |

• | competition from other residential communities, retail properties, office properties or other commercial space; |

• | inflation or increases in interest rates; |

• | limitations on the availability, or increases in the cost, of financing for homebuilders, commercial builders or commercial buyers or mortgage financing for homebuyers; |

• | limitations, reductions or eliminations of tax benefits for homeowners; |

• | reductions in the level of demand for homes or retail or other commercial space in the areas where our properties are located; |

• | fluctuations in energy costs; |

• | decreases in the underlying value of properties in the areas where our properties are located; |

• | increases in the supply of homes or retail or other commercial space in the areas where our properties are located; |

• | declines in consumer confidence and spending; and |

• | public perception that any of the above events may occur. |

There are significant risks associated with our development and construction projects that may prevent completion on budget and on schedule.

At our projects, we are engaged in extensive construction activity to develop each community’s infrastructure, including grading and installing roads, sidewalks, gutters, utility improvements (such as storm drains, water, gas, sewer, power and communications), landscaping and shared amenities (such as community buildings, neighborhood parks, trails and open spaces) and other actions necessary to prepare each residential and commercial lot for construction. In addition, although we primarily rely on homebuilders to purchase homesites at our communities and construct homes, we may in the future construct a portion of the homes ourselves. For commercial or multi-family properties that we retain or acquire in the future, we may also construct the buildings ourselves. Our development and construction activities entail risks that could adversely impact our financial condition and results of operations, including:

• | construction costs, which may exceed our original estimates due to increases in materials, labor or other costs, which could make the project less profitable; |

• | permitting or construction delays, which may result in increased debt service expense and increased project costs, as well as deferred revenue; |

• | unavailability of raw materials when needed, which may result in project delays, stoppages or interruptions, which could make the project less profitable; |

• | federal, state and local grants to complete certain highways, interchange, bridge projects or other public improvements may not be available, which could increase costs and make the project less profitable; |

• | claims for warranty, product liability and construction defects after a property has been built; |

• | claims for injuries that occur in the course of construction activities; |

• | poor performance or nonperformance by, or disputes with, any of our contractors, subcontractors or other third parties on whom we rely; |

• | health and safety incidents and site accidents; |

13

• | unforeseen engineering, environmental or geological problems, which may result in delays or increased costs; |

• | labor stoppages, slowdowns or interruptions; |

• | compliance with environmental planning and protection regulations and related legal proceedings; |

• | liabilities, expenses or project delays, stoppages or interruptions as a result of challenges by third parties in legal proceedings; |

• | delay or inability to acquire property, rights of way or easements, which may result in delays or increased costs; and |

• | weather-related and geological interference, including landslides, earthquakes, floods, drought, wildfires and other events, which may result in delays or increased costs. |

At The San Francisco Shipyard, approximately 408 acres are still owned by the U.S. Navy and will not be conveyed to us until the U.S. Navy satisfactorily completes its finding of suitability to transfer, or “FOST,” process, which involves multiple levels of environmental and governmental investigation, analysis, review, comment and approval. Allegations that Tetra Tech, a contractor hired by the U.S. Navy, misrepresented sampling results at The San Francisco Shipyard have resulted in data reevaluation, governmental investigations, criminal proceedings, lawsuits, and a determination by the U.S. Navy and other regulatory agencies to undertake additional sampling. These activities have delayed the remaining land transfers from the U.S. Navy and could lead to additional legal claims or government investigations, all of which could in turn further delay or impede our future development of such parcels.

At Newhall Ranch, we are party to royalty-based lease agreements with oil and gas operators. Pursuant to the terms of these leases, the oil and gas operators are required to remediate certain environmental impacts caused by their operations following expiration of such leases. In the event that they take longer than expected to complete such remediation or default in their obligation, such that we are required to complete such remediation, we may be forced to delay development of Newhall Ranch until such remediation is complete or incur additional costs that are currently obligations of the oil and gas operators.

We cannot assure you that projects will be completed on schedule or that construction costs will not exceed budgeted amounts. Failure to complete development or construction activities on budget or on schedule may adversely affect our financial condition and results of operations.

Zoning and land use laws and regulations may increase our expenses, limit the number of homes or commercial square footage that can be built or delay completion of our projects and adversely affect our financial condition and results of operations.

Although there are agreements with the City of Irvine for Great Park Neighborhoods and the City and County of San Francisco for Candlestick Point and The San Francisco Shipyard that protect existing entitlements, our communities are subject to numerous local, state, and federal laws and other statutes, ordinances, rules and regulations concerning zoning, development, building design, construction and similar matters that impose restrictive zoning and density requirements in order to limit the number of homes or commercial square feet that can eventually be built within the boundaries of a particular area, as well as governmental taxes, fees and levies on the acquisition and development of land parcels. These regulations often provide broad discretion to the administering governmental authorities as to the conditions for our projects being approved, if approved at all. Further, if the terms and conditions of the development agreements with the Cities of Irvine and San Francisco are not complied with, existing entitlements under those agreements could be lost, including (in the case of San Francisco) the right to acquire certain portions of the land on which development activity is expected. New housing and commercial developments are often subject to determinations by the administering governmental authorities as to the adequacy of water and sewage facilities, roads and other local services, and may also be subject to various assessments for schools, parks, streets, affordable housing and other public improvements. As a result, the development of properties may be subject to periodic delays in certain areas due to the conditions imposed by the administering governmental authorities. Due to building moratoriums, zoning changes or “slow-growth” or “no-growth” initiatives that could be implemented in the future in the areas in which our properties are located, our communities may also be subject to

14

periodic delays, or we could be precluded entirely from developing in certain communities or otherwise restricted in our business activities. Such moratoriums or zoning changes can occur prior or subsequent to commencement of our development operations, without notice or recourse. Local and state governments also have broad discretion regarding the imposition of development fees for projects in their jurisdictions. Projects for which we have received land use and development entitlements or approvals may still require a variety of other governmental approvals and permits during the development process and can also be impacted adversely by unforeseen health, safety, and welfare issues, which can further delay these projects or prevent their development. As a result, revenue from land sales or leasing of retail or other commercial space may be adversely affected, or costs may increase, which could negatively affect our financial condition and results of operations.

In addition, laws and regulations governing the approval processes provide third parties the opportunity to challenge proposed plans and approvals. Certain of our plans and approvals have been challenged by third parties, such as environmental groups, and are currently the subject of ongoing legal proceedings. These and any future third-party challenges to our planned developments provide additional uncertainties in real estate development planning and entitlements. Third-party challenges in the form of litigation could result in the denial of our right to develop in accordance with our current development plans or could adversely affect the length of time or the cost required to obtain the necessary governmental approvals to develop. In addition, adverse decisions arising from any litigation could increase the cost and length of time to obtain ultimate approval of a project and could adversely affect the design, scope, plans and profitability of a project, which could negatively affect our financial condition and results of operations.

We incur significant costs, and may be subject to delays, in obtaining entitlements, permits and approvals before we can begin development or construction of our projects and begin to recover our costs.

Before any of our projects can generate revenues, we make material expenditures to obtain entitlements, permits and development approvals. It generally takes several years to complete this process and completion times vary based on complexity of the project and the community and regulatory issues involved. We could also be subject to delays in construction, which could lead to higher costs and adversely affect our results of operations. Changing market conditions during the entitlement and construction periods could negatively impact our revenue from land sales or leasing of retail or other commercial space. Historically, certain of our entitlements, permits and development approvals have been challenged by third parties, such as environmental groups. Future entitlements, permits and development approvals that we will need to obtain for development areas within our communities may be similarly challenged.

As a result of the time and complexity involved in construction and obtaining approvals for our projects, we face the risk that demand for residential and commercial properties may decline and we may be forced to sell or lease properties at prices or rates that generate lower profit margins than we anticipated, or would result in losses. If values decline, we may be required to make material write-downs of the book value of our real estate assets or real estate investments.

We will have to make significant investments at our properties before we realize significant revenues.

We currently plan to spend material amounts on horizontal development at our communities. Those expenditures primarily reflect the costs of developing the infrastructure at our properties, including grading and installing roads, sidewalks, gutters, utility improvements (such as storm drains, water, gas, sewer, power and communications), landscaping and shared amenities (such as community buildings, neighborhood parks, trails and open spaces) and other actions necessary to prepare each residential and commercial lot for construction. We currently expect to have sufficient capital to fund the horizontal development of our communities in accordance with our development plan for several years. However, we may experience cost increases, our plans may change, new regulations and regulatory plan modifications or court rulings may affect our ability to develop or the cost to develop the project or circumstances may arise that result in our needing additional capital to execute our development plan. If we are not successful in obtaining additional financing to enable us to complete our projects, we may experience further delays or increased costs, and our financial condition and results of our operations may be adversely affected.

15

Our projects are subject to environmental planning and protection laws and regulations that require us to obtain permits and approvals that may be delayed, withheld or challenged by third parties in legal proceedings.

Our projects are subject to various environmental and health and safety laws and regulations. These laws and regulations require us to obtain and maintain permits and approvals, undergo environmental review processes and implement environmental and health and safety programs and procedures to mitigate the physical impact our communities will have on the environment (such as traffic impacts, health and safety impacts, impacts on public services and impacts on endangered, threatened or other protected plants and species) and to control risks associated with the siting, development, construction and operation of our projects, all of which involve a significant investment of time and expense. The particular environmental requirements that apply to a project vary depending on, among other things, location, environmental conditions, current and former uses of a property, the presence or absence of certain wildlife or habitats, and nearby conditions. We expect that increasingly stringent environmental requirements will be imposed on developers in the future.

These future environmental requirements could affect the timing or cost of our development. In addition, future environmental requirements could reduce the number of homesites or amount of commercial square feet we are able to develop, increase our financial commitments to local or state agencies or organizations or otherwise reduce the profitability of the project. Failure to comply with these laws, regulations and permit requirements may result in delays, administrative, civil and criminal penalties, denial or revocation of permits or other authorizations, other liabilities and costs, the issuance of injunctions to limit or cease operations and the imposition of additional requirements for future compliance as a result of past failures.

Certain of our environmental permits and approvals have been challenged in the past by third parties, such as environmental groups. Future environmental permits and approvals that we will need to obtain for development areas within our communities may be similarly challenged.

We could incur significant costs related to regulation of and litigation over the presence of asbestos-containing materials at our properties.