UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

|

☑ |

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(D) |

|

|

|

OF THE SECURITIES ACT OF 1934 |

|

For the fiscal year ended December 31, 2016

OR

|

☐ |

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(D) |

|

|

|

OF THE SECURITIES ACT OF 1934 |

|

Commission File Number: 000-55345

ZERO GRAVITY SOLUTIONS, INC.

(Exact name of registrant as specified in its charter)

|

Nevada |

|

46-1779352 |

|

(State or other jurisdiction of Incorporation or organization) |

|

(IRS Employer Identification No.) |

190 NW Spanish River Boulevard, Boca Raton, Florida 33431

(Address, including zip code, of principal executive offices)

(561) 416-0400

(Registrant's telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act: None.

Securities registered pursuant to Section 12(g) of the Act:

|

Title of Each Class |

|

Name of Each Exchange on Which Registered |

|

Common Stock, $0.001 par value per share |

|

N/A |

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yes ☐ No ☑

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Exchange Act.

Yes ☐ No ☑

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☑ No ☐

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registration statement was required to submit and post such files). Yes ☑ No ☐

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer”, “accelerated filer”, “smaller reporting company”, and “emerging growth company” in Rule 12b-2 of the Exchange Act.

|

Large accelerated filer |

☐ |

|

Accelerated filer |

☐ |

|

Non-accelerated filer |

☐ |

|

(Do not check if a smaller reporting company) |

|

|

|

|

|

Smaller reporting company |

☒ |

|

|

|

|

Emerging growth company |

☐ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

Yes ☐ No ☑

As of June 30, 2016, the aggregate market value of the registrant's common stock held by non-affiliates of the registrant was $17,565,231 in a private placement transaction of approximately $.79 per share based on management's estimate of fair value (as there have been nominal to no trades that have occurred in the past twelve months on OTC Pink).

As of May 30, 2017, the registrant had 40,068,764 shares of common stock outstanding.

Documents incorporated by reference: None.

ZERO GRAVITY SOLUTIONS, INC.

FORM 10-K ANNUAL REPORT

DECEMBER 31, 2016

TABLE OF CONTENTS

|

|

|

Page |

|

PART I |

|

|

|

Item 1. |

Business |

1 |

|

Item 1A. |

Risk Factors |

20 |

|

Item 1B. |

Unresolved Staff Comments |

21 |

|

Item 2. |

Properties |

21 |

|

Item 3. |

Legal Proceedings |

21 |

|

Item 4. |

Mine Safety Disclosures |

21 |

|

|

|

|

|

PART II |

|

|

|

Item 5. |

Market for the Registrant’s Common Stock and Related Stockholder Matters |

21 |

|

Item 6. |

Selected Financial Data |

23 |

|

Item 7. |

Management’s Discussion and Analysis of Financial Condition and Results of Operations |

23 |

|

Item 7A. |

Quantitative and Qualitative Disclosures About Market Risk |

29 |

|

Item 8. |

Financial Statements and Supplementary Data |

29 |

|

Item 9. |

Changes in and/or Disagreements with Accountants on Accounting and Financial Disclosure |

29 |

|

Item 9A. |

Controls and Procedures |

30 |

|

Item 9B. |

Other Information |

31 |

|

|

|

|

|

PART III |

|

|

|

Item 10. |

Directors, Executive Officers and Corporate Governance |

31 |

|

Item 11. |

Executive Compensation |

35 |

|

Item 12. |

Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters |

38 |

|

Item 13. |

Certain Relationships and Related Transactions and Director Independence |

41 |

|

Item 14. |

Principal Accountant Fees and Services |

43 |

|

|

|

|

|

PART IV |

|

|

|

Item 15. |

Exhibits and Financial Statement Schedule |

44 |

FORWARD-LOOKING STATEMENTS

Statements in this report may be "forward-looking statements." Forward-looking statements include, but are not limited to, statements that express our intentions, beliefs, expectations, strategies, predictions or any other statements relating to our future activities or other future events or conditions. These statements are based on current expectations, estimates and projections about our business based, in part, on assumptions made by management. These statements are not guarantees of future performance and involve risks, uncertainties and assumptions that are difficult to predict. Therefore, actual outcomes and results may, and are likely to, differ materially from what is expressed or forecasted in the forward-looking statements due to numerous factors, including those described above and those risks discussed from time to time in this report, including the risks described under "Risk Factors" and any risks described in any other filings we make with the SEC. Any forward-looking statements speak only as of the date on which they are made, and we do not undertake any obligation to update any forward-looking statement to reflect events or circumstances after the date of this report.

Management’s discussion and analysis of financial condition and results of operations are based upon our financial statements, which have been prepared in accordance with accounting principles generally accepted in the United States. The preparation of these financial statements requires us to make estimates and judgments that affect the reported amounts of assets, liabilities, revenues and expenses. On an on-going basis, we evaluate these estimates, including those related to useful lives of property and equipment, the allowance for doubtful accounts and stock based compensation. We base our estimates on historical experience and on various other assumptions that are believed to be reasonable under the circumstances, the results of which form the basis for making judgments about the carrying values of assets and liabilities that are not readily apparent from other sources. There can be no assurance that actual results will not differ from those estimates.

PART I

|

ITEM 1. |

BUSINESS |

Company Overview

Organizational structure

Zero Gravity Solutions, Inc. (“we”, “us”, “our”, the "Company", “ZGSI” or the "Registrant"), a Nevada corporation, is an agricultural based biotechnology company focused on commercializing technology derived from, and designed for long term spaceflight and planetary colonization with significant applications to agriculture on Earth. These technologies are focused on improving world agriculture by providing valuable solutions to challenges facing humanity, including climate change stress and soil degradation threats to agricultural production and the increasing inability to feed the world’s rapidly growing population. The Company’s business model focuses on two primary business segments: 1) BAM-FX™ which is a cost effective, ionic nutrient delivery platform for plants that delivers minerals and micronutrients systemically at the cellular level of a plant, and 2) Directed Selection™ which relates to the production and alteration of new varieties of novel stem cells with unique and beneficial characteristics in the prolonged zero/micro gravity environment of the International Space Station. These novel stem cells, if developed, could be patented for commercial sale to third parties in the agricultural and human regenerative medical markets. ZGSI is headquartered in Boca Raton, Florida.

Our business activities are separated between two wholly owned subsidiaries BAM Agricultural Solutions, Inc. (“BAM Inc.”) oversees BAM-FX™ introduction and business development through product trials and validation with crop growers and distributors that have established business networks in agricultural markets, manufacturing, sales and agronomy support. Zero Gravity Life Sciences Inc. (“ZGLS”) is responsible for any space research projects, life science applications of our technology and conducting research on future BAM Inc. product lines. We believe that the separation of these functions and the corresponding allocation of management by expertise will enable us to improve our performance and provide focus on our different business activities.

A separate wholly owned subsidiary, Zero Gravity Solutions, LTD. (ZGS Ltd.), domiciled in England, was engaged in the European market and business development. During the first quarter of 2015, the Company conducted a review of its operating expenses and use of resources and determined that certain administrative and support costs were outside the scope of the 2015 business plan. Accordingly, the Company made reductions in personnel and curtailed operations of ZGS Ltd. during April 2015. ZGS Ltd. was liquidated during the fourth quarter of 2015. The Company expects to address European markets for BAM-FX™ at a future time when adequate resources are available to pursue the European markets and all local regulatory and import requirements are satisfied for import of BAM-FX™.

Operating Activity

The following time line highlights a number of the Company’s achievements during fiscal year 2016 and through February, 2017:

The Company is focused on near-term revenue generation through the introduction of the Company’s first commercial product, BAM-FX™, to domestic and international agricultural markets. BAM-FX™ is an ionic micro-nutrient delivery platform, registered as a fertilizer application with thirty-two (32) domestic states. The Company conducted product trials on a variety of crops in laboratory and academic settings as well as in field applications on grower/end-user crops during 2014 and expanded field applications with those and additional trial participants during 2015. During 2015, the Company initiated in excess of sixty (60) trials on a variety of field crops, vegetables and fruits with first year participants and commenced second year trials with first year participants. Results from these trials, validated by independent accredited third party laboratories and academic institutions, showed significant yield, nutrient and biomass improvements for crops treated.

Based on the results of the previous two years’ academic and field crop trial results, the Company redirected its sales efforts in the second half of 2016, from a direct approach to growers to developing relationships with channel partners. In general, channel partners are large agricultural product distributors with which the Company has executed a distribution agreement. Three distribution agreements with agricultural product distributors in Ohio and California were signed during the fourth quarter of 2016, including an agreement with Pinnacle Agriculture Distribution, Inc., ("Pinnacle"). The agreement with Pinnacle commenced with two distribution outlets, one near Salinas California and the second, near Yuma Arizona. We expect to expand to other distribution outlets in southern California in 2017. Pinnacle is a multifaceted agricultural retail distribution business with operations including agricultural chemicals, fertilizer bulk handling and precision agricultural services. Pinnacle services growers across the United States. The other two distributors, Cleveland Genomics LTD and Rainbow Valley Nursery Company, are regional growers in Ohio and California, respectively. The Company also executed a channel partner agreement with a distributor in Paraguay, which has a commitment to purchase a minimum of seventy-four (74,000) thousand gallons. We expect to increase our channel partner network in 2017.

We employ the technical talents of our certified crop advisors and agronomists, both domestically and internationally, to support our commercialization and revenue generation efforts. During 2016, the Company added qualified sales management and agronomy personnel to develop channel partner relationships and provide technical product support to growers and channel partners.

During the third quarter of 2016, the Company formed an agronomy and science team to integrate agronomy and crop advisor personnel and centralize technical product know-how in Asia and North and South America. The agronomy and science team is expected to provide technical leadership and support to growers and channel partners in those markets. In addition, the team was tasked with the management the Company’s research efforts with science advisors at the NASA-Ames Research Center, NASA ARC, as outlined in our Reimbursable Space Act Agreement ("RSAA") executed in January 2016. The Company expects to add agronomy trained personnel during 2017 and extend the team’s responsibility to include the Asia Pacific and China markets as these develop.

We expanded our commercial marketing and product introduction efforts to India, Malaysia, Thailand and China in 2016. In certain countries, this work was undertaken by a distributor, pursuant to a non-exclusive distribution agreement executed in 2015. This business development and product introduction effort is consistent with our domestic strategy and focuses on developing channel partners, all of which are within the distributor’s existing business network in Taiwan, Indonesia, Vietnam, India, Thailand, Malaysia and Singapore. Beginning in 2015 sample quantities of BAM-FX™ were shipped to potential channel partners in a number of these countries to validate product claims with the expectation of revenue in 2016. Due to the time required to perform and document the validation and then to obtain governmental commercial import approval, no orders were received in 2016. Product introduction in those countries is expected to continue in 2017. Distribution agreements with potential channel partners in India and China are currently being considered. Based on successful product validation, receiving governmental approval to import product for sale and finalizing distribution agreements with channel partners, commercial applications of BAM-FX™ could commence in certain Asia Pacific countries during 2017.

The Company modified its strategic business relationship with its Chilean distributor in 2016 to allow it to conduct business development and sales management directly and under the name of BAM Agricultural Solutions, Inc. as a Chilean office. The office conducted numerous validation tests with growers and potential channel partner distributors in the country with fourteen different crops during the year and expects to generate revenue in 2017.

We plan to enter agricultural markets in other South American countries either directly or through the Chilean branch operations in 2017. During 2016, Chilean branch personnel provided management to negotiate and conclude an agreement with an exclusive distributor in Paraguay. The distribution agreement is a three-year agreement with a minimum initial first year order requirement of 74,000 gallons of BAM-FX™. We expect the Chilean branch to provide ongoing management and technical support in Paraguay during 2017.

We expected to deliver an initial order of BAM-FX™ to our Paraguay distributor during the fourth quarter of 2016. The order was delayed until the second quarter 2017, due to the distributor’s need to finalize Paraguay’s government product testing requirements for commercial import of BAM-FX™ and obtain import approval from Servicio Nacional de Calidad y Sanidad Vegetal y de Semillas ("SENAVE"), the government agency overseeing agricultural imports. BAM-FX™ tests were successfully completed by the Paraguay Agricultural and Technological Center (CETAPAR) in January 2017 and submitted to SENAVE. We will provide ongoing business development and technical product support jointly with our Chilean branch to our channel partner in Paraguay during 2017

BAM-FX™ was also introduced to the South American countries of Colombia and Brazil during 2016. The Company contracted with Fundacao de Apoio A Pesquisa Agricola (FUNDAG), a private nonprofit entity established under the laws and registered with the Brazilian government, to provide product test results to the Brazilian government for product registration and import approval. Approval for commercial import is expected during the first quarter of 2017. Potential Brazilian channel partners have been identified and introduced to the Company by one of the Company’s agronomy and science consultants affiliated with the University of Florida who are familiar with agricultural markets and distributors in Brazil.

The Company contracted with an independent Colombian laboratory during 2016 to test and provide evidence of effectiveness of BAM-FX™ for the Colombian government’s registration and approval to commercially import product. We expect to receive approvals from the Colombian government during the second quarter of 2017. The Company’s work in Colombia is supported by an import-export company, with which we have entered into a foreign business development consulting agreement, having existing business affiliations and operations in Colombia. The Company intends to negotiate and conclude product distribution agreements with Colombian entities during the first half of 2017.

As a result of our international market development efforts, we received requests for and are in the process of developing BAM-FX™ protocols for crops not grown domestically. For example, tea, coffee and rubber are significant crops serviced by potential distributors in the international markets. For certain potential distributors, until technical trial results on those crops are received and validated, their engagement may be delayed for a number of months. We plan to address market impediments by adding agronomy personnel in 2017 and working directly with in-country agronomists and qualified third-party agricultural labs and universities.

During 2016, the Company started to develop its business strategy such as by undertaking effort to have products incorporating BAM-FX™ enter the home and garden ready to use retail market. We expect to test market acceptance using pilot programs in certain big box stores in 2017. We engaged a seasoned retail market consultant to assist us with our retail product business strategy and roll out.

We operate a manufacturing facility in Okeechobee, Florida. Manufacturing is currently conducted on an as needed batch process. The Company conducted a complete regulatory review of the manufacturing operations during the third quarter of 2015 and made certain policy and procedural changes to ensure compliance with good manufacturing processes and regulatory requirements including engaging a chemical process engineer to analyze plant operations and audit adherence to regulatory requirements. The Company believes the facility's operations comply with all regulatory requirements.

During 2016, the Company continued process improvements and modifications of existing equipment and facilities to enhance efficiency, comply with regulatory requirements, control the quality of raw materials used in production and consistently provide customers a quality product. The Company added a second product mixing line to increase production capability for expected product demand and a reverse osmosis water treatment system for consistent water quality.

Our chief scientist began developing new formulations of BAM-FX™ in 2015 to address nutritional needs of plants that are additive to our product’s current zinc and copper formulation. The new formulations address known plant deficiencies of boron, manganese, magnesium, and iron and can be manufactured to include all or numerous combinations of these elements. The new formulations were tested by an independent laboratory and, verified the existence of and the ability to combine those elements in solution. We expected to begin stability testing and limited trials of new formulations during 2016, however we focused our research and development resources on BAM-FX™ through our RSAA, university agricultural departments, and substantial potential channel partners. We plan to develop four to six products containing new mineral formulations during 2017 and obtain state licenses to sell those products once the commercial production capability is proven and all regulatory and labeling requirements are met.

The Company’s long term objectives include the commercialization of ZGSI’s space derived Directed Selection™ technology, which predicts that plant and animal stem cells exposed to prolonged microgravity in space can be endowed with new characteristics beneficial to society. In previous years, with our collaborators, the National Aeronautics and Space Administration (“NASA”), the United States Department of Agriculture (“USDA”), and the University of Florida, we conducted scientific studies on six NASA sponsored flights to the International Space Station (“ISS”). These experiments demonstrated that the gene expression of plant cells in zero/microgravity changes substantially, and furthermore, provided us with strong evidence that these changes can be directed toward beneficial attributes.

Our Directed Selection™ research aims to produce new varieties of proprietary, patentable stem cells for plants with desirable traits, such as the ability to better survive environmental challenges (i.e. temperature or climate change) or to resist disease. Adaptive changes in the plant will be accomplished without the need for additive or subtractive genetic engineering, thus eliminating public concerns about genetically modified organisms (“GMO”). The plant still uses the capabilities that are a natural part of its genetic potential through altered gene expression that enables adaptation toward valuable traits. Another important aspect of our space derived intellectual property capitalizes on space flight experiments showing the unique effects of zero/microgravity on mammalian cells. Space-based technology imparts the likely ability to reproduce undifferentiated multi-potent human stem cells in substantially larger quantities and more rapidly than is possible on Earth. Long-term goals include revolutionary advancements in stem cell differentiation, cellular macrostructure assembly, vascularization and wound healing. Because both humans and animals use very similar metabolic pathways, we also expect to produce patented stem cells that can provide beneficial treatments to commercial livestock. We believe that this area may lead to significant future business opportunities for the Company. We expect that research funding will be made available in 2017 if cash flows from our operations provide sufficient funds to support those efforts or funding is designated by equity investors or grants.

Research and Development Activity

The Company developed scientific relationships with NASA ARC, Ohio State University and Penn State University during 2016 to understand and validate the science incorporated in BAM-FX™ and identify additional commercial attributes. Pursuant to the Company's RSAA, with NASA ARC, the Company has access to NASA scientists and laboratories. Because the RSAA is reimbursable agreement, whereby the Company reimburses NASA for technical services, the Company retains ownership of intellectual property resulting from the research work performed.

The primary objectives of the RSAA are:

a. To establish the scientific basis for action of ZGSI products,

b. To quantify the impact of ZGSI products on plant growth and productivity,

c. To evaluate and test the impact of ZGSI products on yield physiology of selected crops important to commercial agriculture and NASA applications, and

d. To evaluate and test the potential utility of ZGSI products to NASA space biology and life support applications.

NASA ARC used its unique, ground-based, controlled environment facilities and research personnel to address a series of questions relevant to both ZGSI and NASA during 2016. The scientific data is jointly evaluated by ZGSI and NASA ARC to determine utility of the ZGSI products to commercial agriculture and NASA applications. If jointly agreed and based on evaluation of the scientific data, space flight and other opportunities could be developed to test our potential role in achieving NASA goals in plant-based space biology and life support pursuits.

The RSAA lays out a four-phase plan of work (each a “Phase”). Phases Two through Four depend both on the successful execution of the previous Phase and joint agreement between NASA ARC and ZGSI.

From the scientific work of NASA ARC, ZGSI expects to understand the BAM-FX’s mode of action and physiological effects leading to increased yields currently observed on earth in commercial agricultural systems. NASA ARC is currently using its unique facilities designed specifically to conduct ecophysiological studies of the type necessary to address the science questions of interest to ZGSI and queries from channel partners. Additionally, ZGSI expects to discover if BAM-FX™ truly has applications for growing plants in the controlled conditions of spaceflight and for human colonization of other worlds. ZGSI plans to optimize BAM-FX™ application methods in both controlled environment agricultures on earth and in space flight applications.

Preliminary results from NASA ARC biomass studies during 2016 show indications that BAM-FX™ applications result in:

|

● |

Increased photosynthetic efficiency within the plant leaf structure wherein light energy is converted into biomass; |

|

● |

Increased plant nitrogen use efficiency which increases the plant’s biomass production per unit of nitrogen, thereby reducing the amount of nitrogen needed for biomass production; and |

|

● |

The plant’s antioxidant production protects the plant from overheating although an increase in photosynthetic process also increases heat within the plant. |

These preliminary findings add scientific support for results we have seen from field, third party and academic tests performed over the last three years, distinguishing BAM-FX™’s zinc and copper micronutrient delivery platform from other zinc and copper based fertilizer products in the agricultural markets.

We plan to fund additional research and continue working with NASA ARC in 2017 to finalize: the preliminary results of our 2016 studies; identify the scientific evidence of the action of BAM-FX™ within the plant structure; develop predictable crop and environmental dosage application rates to support precision agricultural applications for growers; and obtain evidence of foliar wrap-around effect on plants including the speed with which BAM-FX™ enters the cells of the plant. Agreement on scientific objectives of Phase Two of the RSAA with NASA ARC should be completed in the second quarter of 2017.

The Company signed an agreement with Intrinsyx Technologies Corporation ("Intrinsyx"), to undertake a plant growth experiment on broccoli aboard the ISS during 2015. The experiment, housed by hardware developed by Intrinsyx, follows protocols designed jointly by the Company and Intrinsyx. Intrinsyx is a systems engineering, science and research company that has delivered innovative, high performance technical solutions to NASA for over fourteen years. The experiment, anticipated to take place in 2016, was postponed due to a number of launch vehicle problems with Space-X flights during 2016.

On February 21, 2017, the Company’s research experiment using BAM-FX™ was successfully delivered to the ISS, launched from the Kennedy Space Center on February 18, 2017. In collaboration with NASA and Inrinsyx, the experiments study the growth and nutritional effects of BAM-FX™ in broccoli seedlings in microgravity, advancing scientific knowledge to promote the growth of fresh, nutrient-dense food for astronauts on long duration space missions.

Jointly, Intrinsyx and NASA ARC issued in January 2017, results of their research showing BAM-FX™ is compatible with glyphosate resistant crops, primarily Roundup Ready crops. Roundup Ready crops are crops genetically modified to be resistant to the herbicide Roundup. Roundup is the brand name of a herbicide produced by Monsanto Corporation with the active ingredient, glyphosate. Glyphosate is a broad-spectrum systemic herbicide and plant desiccant or drying agent. The 2014 Agricultural Chemical Use Survey published by the United States Department of Agriculture’s National Agricultural Statistics Service reported that glyphosate was applied to 38% of domestic planted acres. The result of this joint scientific research allows the Company to remove restrictions that had been included in BAM-FX™ labeling and instructions warning against use with glyphosate, thereby eliminating a significant marketing impediment for our product.

We believe the Company’s proprietary technologies enable the development of a diverse product line with unique solutions to big problems, representing significant potential revenue and profit opportunities. Due to the market scope and the associated regulatory requirements to reach full profit potential, ZGSI’s strategy is to enter into channel partnerships by executing distribution agreements, domestically and internationally, with industry-leading agriculture product distributors which will leverage our collective resources and expedite revenue generation.

Corporate History and Structure

Zero Gravity Solutions, Inc. was initially incorporated in the State of Idaho as Hazelwood-Gable, Inc. on August 19, 1983 to engage in the business of developing mineral resources. The Company engaged in limited operations until 2003. On June 19, 2002, the Company changed its corporate domicile to the State of Nevada and, on November 25, 2003, changed its name to American Thorium, Inc. On December 10, 2003, the Company entered into an agreement to acquire certain mining claims and changed its name to Thorium Nuclear Energy, Inc. on March 5, 2004. On March 8, 2006, the Company changed its name to Hazelwood Ventures, Inc. and began looking for new business ventures. On June 14, 2006, the Company changed its name to Monarch Molybdenum & Resources, Inc. and on November 27, 2007 entered into a merger agreement, whereby it was to acquire certain mining claims from Thorium Energy, Inc. and changed the Company's name to Thorium Energy, Inc. The merger agreement was rescinded on March 19, 2008 and the Company changed its name to Monolith Ventures Inc. on April 2, 2008 and with the intent to acquire or merge with one or more businesses. On December 30, 2011, the Company acquired ElectroHealing Holdings, Inc., which held certain patents, patent applications and other technologies and/or licenses pertaining to medical device technology and changed its name to ElectroHealing Technologies, Inc. on January 12, 2012. Subsequent to the transaction, management re-evaluated the merits and benefits of the ElectroHealing Holdings, Inc. acquisition and began to explore possible alternatives. Accordingly, we executed a rescission agreement on December 20, 2012 that returned the previously acquired patents and technologies in exchange for the cancellation of the shares of our common stock previously issued in the acquisition.

Formation of ZGSI and the Company’s Current Structure

On December 3, 2012, we entered into a Patent Acquisition Agreement with John W. Kennedy whereby we acquired certain patents applications and technologies related to the Company’s current Directed Selection™ business segment. In connection with the acquisition of this technology, we changed our name to Zero Gravity Solutions, Inc. on January 11, 2013 to better reflect our new business endeavors, and issued 11,500,000 shares of our authorized, but previously unissued common stock. In connection with this acquisition, we moved our corporate headquarters from Salt Lake City, Utah to its current location at 190 NW Spanish River Boulevard, Suite 101, Boca Raton, FL 33431.

On July 30, 2013, John W. Kennedy assigned to the Company the entire right, title and interest in, to and under the invention and provisional patent application for Bioavailable Minerals for Plant Health which became the basis for the Company’s BAM-FX™ business segment.

The Company currently has two wholly owned subsidiaries: BAM Agricultural Solutions, Inc. (“BAM Inc.”) and Zero Gravity Life Sciences, Inc. (“ZGLS”). BAM Inc. is a Florida Corporation that holds and controls the manufacturing, sales and revenue generation of the Company's agricultural product, BAM-FX™. ZGLS is a Florida Corporation that holds and controls the Company’s Directed Selection™ business segment and the related research and development work. The Company had previously wholly owned Zero Gravity Solutions, LTD (ZGS Ltd.), and BAM Agricultural Solutions, LTD. (both private United Kingdom limited companies based in the United Kingdom) which had been created to service the Company's expected operations and interests in the European Union (EU). During the fourth quarter 2015, both UK companies were liquidated, and the financial resources redeployed to markets in the United States and Chile.

The Company currently has 32 employees, of which 31 are full-time employees. The Company has selected December 31st as its fiscal year end.

Principal Product Lines

BAM-FX™

BAM-FX™ is an ionic micro-nutrient delivery platform for food crops. BAM-FX™ was originally developed by John W. Kennedy, our Chief Science Officer and former director, to grow food crops in space vehicles designed for deep space human missions, but has been found to have potentially far reaching applications for agriculture on Earth. BAM-FX™ is a proprietary formulation of zinc and copper in a precise ratio used to treat plant mineral deficiencies by providing a delivery platform to move mineral ions to the mineral deficient areas in plants. The benefits of BAM-FX™ are accomplished without the use of genetic modification (“GMO”) or traditional fertilizers, soil amendments or supplements. Instead, the BAM-FX™ formula, working in connection with other agricultural plant treatment regiments, transports highly bio-available, balanced, ionic minerals systemically into the biological system of a plant using a mineral complex carrier in an ionic form, which penetrates and distributes nutrients throughout the plant's cellular structure. BAM-FX™ delivers a diversity of nutrients, in measurably larger quantities than can be achieved through standard and traditional methods, and it is capable of substantially cutting costs with its versatile application possibilities and its enhancement of multiple products.

BAM-FX™ can be applied by soaking/coating seeds, direct application at time of planting or as a foliar treatment of the plant at later stages of the plant’s development.

Academic and grower product trials, validated by independent laboratory’s and academic institutions, showed BAM-FX™ treated plants exhibit faster germination, higher yields, increased plant resistance to harmful environmental factors and higher quality fruit and vegetables. Trials have shown that applications of BAM-FX™ on various crops reduces the need for multiple applications of other products, which we believe will save growers time and money while creating faster growing, healthier, more robust plants. Additionally, we believe BAM-FX™ may provide significant value for farmers, growers, and world agriculture through:

|

● |

Observed increased plant stress tolerance; |

|

● |

Faster time to maturity and harvest with higher farm yields for food crops; |

|

● |

Systemic delivery of targeted nutrients and minerals to crops requiring lower energy to uptake which creates a more robust plant and nutritious crop; |

|

● |

Increased nutritional quality of grains and produce including the potential to engineer nutrition into our food (i.e. bio-fortifying lettuce and grapes with zinc and potassium); and |

|

● |

Reduced ecological concerns associated with agricultural runoff pollution into water sources as phosphate or nitrate usage is decreased. |

Food crops offer the best source of nutrition for humans since many supporting nutrients require organic carriers and are not normally absorbed by using vitamin and mineral supplements alone. As BAM-FX™ can be applied to any plant, we anticipate a substantial demand for BAM-FX™ to support improved crop health and nutrition.

BAM-FX™ Trials

In 2014, BAM-FX™ product development and commercialization activities spanned a wide range of studies in terms of crop plants, test parameters, geographic region, and potential customer base. In 2015, we conducted second season tests with a number of growers to replicate the first year’s positive results. The trials were primarily foliar applications during the growth cycle of the crops, including but not limited to wine grapes, table grapes, avocados, beans, tomatoes, rice, berries, stone fruit, corn, onions, barley, wheat, and leafy greens. We also initiated a number of first time trials with other growers, independent agricultural laboratories and potential channel partners. In addition to showing product efficacy, the trials enabled us to begin branding BAM-FX™ and provided word of mouth support within the local farming community to attract potential channel partner interest in BAM-FX™ and its performance.

To illustrate the field trial work conducted during 2014 and 2015, two of our multi-year trials and results are summarized, as follows:

High Value Crop: Wine Grape Trial

Field trial, analyses and harvest were conducted jointly by Intrinsyx and Guglielmo Winery staff during 2014 and 2015.

For the 2014 first season trial, a total of 300 mature Carignan vines were selected with 150 vines in three separate adjacent rows marked for BAM-FX™ treatment and 150 marked in three separate adjacent rows as untreated control. Additionally, 150 mature Zinfandel vines were selected with 75 marked for the BAM-FX™ treatment and 75 marked as control vines. The vines were chosen because all vines were of similar age, health, size and spacing. All vines were in environmentally stressed conditions.

These wine grapes are normally dry farmed but due to the local drought conditions, one quarter of an acre foot of water was applied by sprinkler sets during July 2014. This was the only water manually applied all year. Additionally, micronized wettable sulfur was applied as a fungicide, following manufacturer recommendations for wine grapes. Three foliar applications of BAM-FX™ were applied during the growing season through the date the grapes began to ripen.

During September 2014, bunches of grapes were randomly harvested from ten vines from both BAM-FX™ treated vines, and control vines, and taken to an onsite analytical lab for direct comparisons. Both the Carignan and Zinfandel grapes tested from vines treated with BAM-FX™ had increased sugar content.

The quantitative results obtained from the 2014 fall harvest showed that BAM-FX™ treated vines had an approximate two-fold increase in both bunch and berry weights for Carignan and Zinfandel vines.

For the 2015 second season field trial, a different area of the Guglielmo vineyard was chosen with applications made only on Zinfandel wine grapes. These vines were chosen because all vines were of similar age, health, size and spacing, and all were in environmentally stressed conditions. These wine grapes are normally dry farmed, but due to the drought conditions, one quarter of an acre foot of water, was applied by sprinkler sets during July 2015. This was the only water manually applied during the growing season. A micronized wettable sulfur was applied as a fungicide starting in early April with an additional application during each of the three following months (May-July), following manufacturer recommendations for wine grapes.

At first sign of early bud break in March 2015, BAM-FX™ was applied in a foliar spray and in the soil by slightly wetting the surrounding soil directly underneath vines above roots through an intentional overspray. Two additional foliar applications were made to the vines during the growing season.

Guglielmo personnel harvested each row in this trial with yield results showing an approximate doubling of yields obtained from the BAM-FX™ treated vines. Crush-juice quality parameters were again measured, showing only a slight average increase for sugar content (Brix) without any statistical differences.

Lab analyses showed a 45% average higher zinc and 14% average higher copper content in the juice from the BAM-FX™ treated vines showing that BAM-FX™ bioavailable ionic forms of zinc and copper are transported into berries and the resulting juice. The results confirmed protocols used in these environmental conditions were valid and use of the product as tested did not result in any entry barriers to the wine grape production market.

Our first season results demonstrated the ability to increase both the yields and quality sugar content/Brix in both Zinfandel and Carignan varieties, and total acids in Zinfandel. The second season results demonstrated the ability to increase Zinfandel yields, zinc content and quality in parameters measured. A third trial, conducted during 2016 on nine control acres and nine BAM-FX™ treated acres of Zinfandel grapes, resulted in a 28% increase in yield and quality improvement as seen in the prior years’ trials. We believe the product’s consistent positive performance over the three-year trial provides field based data needed to convince wine grape growers to purchase and commercially apply BAM-FX™ during 2017. We expect Guglielmo Winery will purchase BAM-FX™ from our channel partner, Pinnacle, for commercial application in 2017.

Row Crop: Corn Trials Summary

Corn is the largest crop in total acreage in the United States, with an estimated 91.4 million acres planted in 2016 reported by the United States Department of Agriculture in their release dated June 30, 2016. We believe the size of this market provides a significant opportunity for future revenue streams in addition to soybeans and wheat, which are the second and third largest row crops in the United States, by acreage.

During 2015, in a second-year corn trial, BAM-FX™ was evaluated on two farms in Iowa: one on twenty acres and the other on fifteen acres. The protocols in both trials applied thirty-two ounces of BAM-FX™ per acre with a reduction of nitrogen based fertilizer: a 25% reduction of nitrogen, phosphorous and potassium on the twenty-acre trial and a 25% reduction of nitrogen with no reduction in phosphorus and potassium on the fifteen-acre trial. The control acreage followed normal grower fertilizer application.

The trial results showed a 4% improvement in bushels per acre on the twenty-acre trial and a 1% improvement on the fifteen-acre trial. In both trails, the root ball on BAM-FX™ treated corn showed increased size, improved nutrient uptake, and strengthening of the plant’s anchor structure to withstand damage from wind, thereby reducing the grower’s crop loss.

These trials achieved a return on investment through improved crop yields and reduced fertilizer applications. As an additional environmental benefit, growers could reduce fertilizer run off into waterways, thereby reducing exposure to fines and penalties imposed by numerous municipalities on growers for nitrogen and phosphorus intrusion into water sources that feed drinking water processing facilities.

The prior years’ trials provided anecdotal data to establish product application guidelines to engage early adopters and to provide distributors and key industry leaders the tools for on-site product evaluation. For a variety of economically important crops, these tools include: acceptable BAM-FX™ concentration ranges and delivery rates, treatment methods, successful integration with a variety of commercial farming practices (i.e. soil application in furrow, drip irrigation, foliar spray, helicopter spray), and a series of evaluation criteria for demonstration of product success. Our 2015 testing was conducted on multiple crop acres. For most crops tested, the testing showed results similar to those in 2014: faster plant establishment (increased root growth, stronger plant crowns and greater leaf growth), faster crop maturation, tolerance to stress, improvement in nutritional value and overall increased yields. BAM-FX™ also showed the potential to support a reduction in fertilizer application rates.

Field trial modification during 2016

During 2016, we shifted our focus from field trials for performance data to scientific efforts with universities and NASA ARC. Our channel partners, although acknowledging the importance of the field trial results, requested third party data scientifically supporting the results and BAM-FX™ mode of action. This scientific data is currently being obtained through NASA ARC efforts under the RSAA and in connection with studies at the University of Florida, the Tropical Research and Education Center ("TREC") which is a division of the University of Florida, Ohio State University, Penn State University, University of Iowa and Florida International University.

Beginning in 2016, BAM Inc. focused its product marketing approach on grower’s field validation, whereby specific expected crop results were identified at the inception of the validation process and upon achieving the expected result, a grower would agree to purchase the product. The purpose of these trials, in addition to being part of our business development effort, is to develop brand name recognition and provide pull through business for prospective channel partners.

The Company has, over the last fiscal year, conducted trials on the effects of BAM-FX™ on medicinal cannabis. These trials were conducted with both certified licensed growers on outdoor crops as well as crops in a highly controlled internal environment. The same positive results we have seen with commercial agriculture crops were also evidenced with cannabis. The Company is evaluating its entry into this market in addition to its market strategy for that crop.

The Company formed an agronomy and science team during 2016 to centralize technical management, coordinate our trials, compile results, and focus our scientific work to address specific questions from the agricultural community and our channel partners regarding how and why BAM-FX™ works. We believe the team’s focus will maximize the value of our research. The agronomy team integrated our agronomy and crop advisor personnel in North America, South America and Asia and provides centralized leadership and technical expertise to support sales and marketing. The agronomy team is the interface between channel partners, NASA ARC and university research.

The commercialization cycle for new agricultural products is generally two to three growing seasons. Our 2015 trials included a mix of independent laboratory tests, first year small-scale trials with growers and second season multiple acre trials with growers. Demonstrating consistent product performance is one key to obtain product orders from growers in the United States. During 2016, in connection with NASA ARC, we began developing product application dose rates and response curves scientifically to enable us to predict outcomes and support consistent performance.

Although United States growers have not historically been innovators and have required multiple growing season trials before adopting new products and technologies, our 2014 and 2015 domestic trial results have been instrumental in opening commercial markets in Asia, Chile and other South American countries. Having completed a number of successful trials in Chile coupled with successful domestic trial data, we have seen a significant interest from Chilean growers and potential channel partners. We have product in Chile and expect orders for BAM-FX™ for commercial application through channel partners and direct sales to growers to commence in the second quarter of 2017.

During the fourth quarter of 2016, the Company entered into an agreement with Global Biotech, S.A.S. a Colombia agricultural testing and analytic laboratory, to evaluate BAM-FX™ through a series of product application tests to obtain approval for commercial import. We expect, assuming positive results, to apply for and obtain registration through the Colombia Institute of Agriculture (ICA) during the second quarter of 2017 for commercial import. We are working with a potential Colombian channel partner, landowner and grower who expects to sell, market and distribute BAM-FX™ within Colombia.

The Company has completed its efficacy studies in Brazil. We are currently undergoing the government’s approval process for sale in Brazil.

The Company conducted initial market analysis in China with the assistance of a contractor, Asia 21 Communications, LLC ("Asia 21"), focusing on the sale and distribution of products and solutions into China and providing local operational support, management and services. Asia 21 has offices in the United States and China. Registration with the China Ministry of Agriculture for approval to import BAM-FX™ began during the fourth quarter of 2016 and is expected to complete during the second quarter of 2017. In connection with BAM-FX™ registration testing requirements, the Company contracted with the Shanghai Agricultural Institute to develop BAM-FX™ test data and technical reports for government import approval.

The Company also began to introduce BAM-FX™ to Asia Pacific markets in 2016, targeting potential distributors through existing business relationships. High-value crop and row crop product validation is currently in process in a number of Asia Pacific countries including India, Malaysia, Indonesia, Philippines and Thailand.

During February 2017, the Company signed an exclusive distribution agreement with Bison Africa Capital (Pty) Ltd. (“Bison”). Bison is an emerging investment holding company based in South Africa and a leader in building competitive and representative South Africa companies. Under the terms of the agreement, Bison will be responsible for importing BAM-FX™ and will supervise the sales, marketing, legal and administrative tasks necessary to introduce and sell BAM-FX™ in South Africa. This agreement will be effective one month after BAM-FX is approved for commercial sale by the South African Department of Agriculture which is estimated to complete during the second quarter of 2017.

DIRECTED SELECTION™

Directed Selection™ is a proprietary technological method designed to use the unique conditions of near-zero gravity in low earth orbit to create plants and animal cells that have beneficial traits that we believe would have value to society. This technology predicts that plant and animal stem cells exposed to prolonged microgravity in space can be endowed with new characteristics.

Life on Earth has always developed within the confines of gravity. About 50% of the energy expended by terrestrial-bound plants is dedicated to structural support in order to overcome gravity. By removing gravity from the equation, plant cells in a weightless environment have an excess of energy. This relatively benign environmental change causes the plant to engage its survival mechanisms, thereby enabling differential gene expression. The plant is able to adapt quickly to changing environments or disease causing organisms, stressors that we introduce artificially while the plant is in microgravity thereby directing gene expression. This indicates that we can produce new varieties of plants, with required new attributes, faster than traditional methods.

All aspects of our Directed Selection™ technology must be conducted in a long-term microgravity environment, currently only available in space. We partnered with the University of Florida to conduct the initial experiments in order to validate the efficacy of this technology in space. Preliminary results showed that the Directed Selection™ technology was able to identify frost resistance capabilities in the Jatropha Curcas plant. This capability could allow cultivation in areas previously impossible.

The Company is using the Directed Selection™ platform technology to create more robust plant varieties adapted toward desirable characteristics. Our Directed Selection™ research aims to produce new varieties of proprietary, patentable stem cells for plants with desirable traits like the ability to better survive environmental challenges (i.e. temperature or climate change) or to resist disease. Adaptive changes in the plant will be accomplished without the need for additive or subtractive genetic engineering, thus eliminating public concerns about GMOs. The plant still uses the capabilities that are a natural part of its genetic potential through altered gene expression that enables adaptation toward valuable traits.

A key part of our ongoing operations is the expansion of these patents to cover additional crops, animals and humans, and the specific methods and tools that are developed from our research and development. The Company possesses patent applications that contain claims covering biological processes in microgravity, including the growth of cellular plant and animal tissues in orbit, stem cell replication and related processes.

The second part of the Directed Selection™ technology pertains to the mass replication or propagation of stem cells in space, something that can be done on Earth but at much slower rates. Although stem cells can be produced on Earth, current methods are inadequate to create large quantities of healthy cells in short periods of time. Our technology would allow for the increased production of healthy stem cells. Tests, which occurred over six space missions, have provided initial proof-of-concept that the Directed Selection™ technology allows stem cells to replicate en masse. We believe it may eventually allow us to produce large quantities of undifferentiated pluripotent stem cells in the same environment for commercial sale to third parties.

Directed Selection™ Research

A series of space microgravity experiments were executed by means of six space shuttle flights to the ISS spanning from 2007 through 2011, linked to and supported by the NASA Space Act Agreement entered into by ZGSI’s founder, Mr. John W. Kennedy. A new five-year RSAA, signed during January 2016, with NASA ARC, provides us access to NASA scientists and laboratories to continue research on earth. In addition, we expect that there are opportunities through a collaboration with Space Florida to continue research on the ISS. Space Florida is an economic development organization devoted to space research and drives Florida economic development across the global space enterprise. In prior years, tests of chemical compounds, plant cells, and mammalian stem cells in microgravity were conducted in conjunction with the USDA, Agricultural Research Service Labs (Beltsville, MD) and ("TREC").

Proof Of Concept Plant Research To Develop Jatropha Biofuel Strains.

The ZGSI space research program focused, in part, on Directed Selection™ of traits in plants, using microgravity. Initial research focused on in vitro cell culture methods for plants of interest for biofuels or valuable ornamentals. The tropical and sub-tropical plant, Jatropha Curcas (physic nut), produces an easily purified biodiesel or jet fuel, but Jatropha is intolerant of frost and subject to diseases like root rot, leaf spot, and rust. A Jatropha cultivar with a broader climate range, improved frost tolerance, and greater disease resistance, would be a valuable improvement to biofuel production. A parallel study of ornamentals tested an endangered orchid species, two types of tropical flowering tree, and a common plant model organism. Research encompassed a series of six flights, from 2007 through 2011, and was completed by Dr. Wagner Vendrame at TREC. Research support was provided by NASA, BioServe Space Technologies, the Vecellio Group, and Vecenergy Corporation.

Plant cells from test species were grown in microgravity aboard the ISS and returned to ground for follow-up testing. The series of experiments produced several important results. The research team discovered the means to produce and propagate plant stem cells using microgravity. Further, methods were developed to out-grow plants from microgravity stem cells. Plant cells in microgravity were able to form pro-embryonic masses, which would enable quick regeneration of clonal plant material in order to grow new, whole plants. Plant cells also had increased growth, and cell cultures acquired a high stress tolerance in microgravity based upon the ability to recover viable cells after a long-term (290 day) culture under very limited nutrient conditions. As predicted, plant cells grown in microgravity acquired different growth characteristics and differential gene expression, compared to growth in normal gravity conditions. Currently, proprietary Jatropha strains are in keeping at TREC.

Mammalian Stem Cell Research in Space

Mammalian stem cell research offers an immeasurable promise for human health through potential means of disease treatment or cure and for tissue or organ regeneration or repair. ZGSI scientists and collaborators recognized this valuable application of space research early on, in 2008, and used the STS-126 flight mission to attempt to grow porcine liver stem cells (PICM-19) in microgravity. The experiment verified that mammalian stem cells would propagate, differentiate, and even form biliary liver structures in microgravity. Cell viability was maintained and cell activity assays indicated that cells maintained hepatocyte detoxification function over the test period. An early stem cell experiment, the PICM-19 was an essential first step toward using microgravity to mass-propagate human differentiated or undifferentiated stem cells to accomplish a myriad of research goals.

Timeline and Plan of Operations

While we believe we can realize sustainable revenue executing our plan to leverage our technology and resources by developing strong business relationships with our channel partners, we cannot guarantee we will be successful. Our business is subject to risks inherent in the establishment of a new business enterprise including the financial risks associated with the limited capital resources currently available to us for the implementation of our business strategies. There can be no guarantee that we will be able to obtain the necessary levels of profitability or fundraising needed to remain operational on a long-term basis. Adequate additional financing may not be available to us on acceptable terms, or at all. If we are unable to raise capital when needed or on attractive terms, we would be forced to delay, reduce or eliminate our research and development programs or any future commercialization efforts. We will need to generate significant revenues to achieve profitability, and we may never do so.

Zero Gravity Solutions, Inc.

The Company is a fully reporting company and as such, provides general and financial administration, financial compliance with the SEC, marketing support and strategic planning to BAM Inc. and ZGLS. The Company also develops product marketing material, investor oriented materials and provides systems support and market reach on our websites and through social media programs.

During May 2016, the Company announced that it had closed the final tranche of its previous offering of the Company’s Units in an exempt private placement transaction (“Private Placement”). Each Unit in the Private Placement consisted of one share of the Company’s common stock and a five-year warrant to purchase one share of the Company’s common stock at $2.00 for $1.25 per Unit. The Company received gross proceeds of $6,260,000 million pursuant to the Private Placement.

Throughout 2016, the Company in cooperation with Space Florida, provided management assistance and strategic planning in the organization of the Planetary Sustainability Institute ("PSI"), a non-profit entity chartered to engage in research and commercialization of new sustainable technologies at the Kennedy Space Center. We expect to play an integral part in the development of PSI’s sustainable agricultural research programs including products the Company expects to develop during 2017.

During August 2016, the Company identified a need to raise additional funds to execute its business plan for the remainder of 2016 and future periods. In October 2016, the Company began addressing those requirements through a new private placement of common stock of up to $10,000,000 at $3.00 per share of common stock issued.

The Company expects to continue providing administrative and financial support to BAM Inc. and ZGLS as those subsidiaries execute their business strategies during 2017 in addition to collaborating with the PSI on agricultural research, economic development and identification of new technologies to improve worldwide agricultural operations.

BAM Agricultural Solutions, Inc.

BAM Inc.’s 2017 business strategy includes building product demand, brand recognition and generating revenue in domestic and international markets through its channel partner strategy. This strategy entails identifying, engaging and cooperating with multiple channel partners to include BAM-FX™ in their agricultural product offerings utilizing their existing sales and distribution networks. The relationship between BAM Inc. and its channel partners is contractually defined in a distribution agreement between the parties. The distribution agreements include and are expected to include geographic exclusivity based upon an initial stocking order and mutually agreed product sale volumes.

BAM Inc.’s primary obligations under a distribution agreement include, but are not limited to, technical product support based on scientific third-party research and field assistance with growers to generate pull through orders for channel partners. In connection with the channel partner strategy, BAM Inc. has been requested by its channel partners to provide and plans to address: additional ionic formulations to supplement its base product, BAM-FX™; scientific data targeting the marketplace; simple and factual market talking scripts; test data on head-to-head competition against leading micro-nutrient products; foliar dose response curves for performance predictability; and access to information and data generated through our RSAA with NASA ARC.

Although BAM-FX™ can be applied as a soil drench, seed soak/coat or foliar application, we plan to focus the majority of our 2017 sales, agronomy and science efforts on foliar applications to prove the product’s superiority to other micronutrient products in the foliar market. We believe the superior attributes in the foliar market include an electrostatic wrap around foliar effect, thereby accessing the entire leaf and stem structure, and accelerating speed of micronutrient delivery into the plant’s cells. In 2017, we expect to show scientifically that these attributes exist in foliar applications of the product. We expect our agronomy and science team will obtain necessary third-party science data to prove beneficial attributes we have seen in seed soak/coat applications during 2016 and finally, investigate the impact on soil health from beneficial drench applications.

The Company began investigating the retail markets for ready-to-use home and garden applications in 2016 and will continue exploring those opportunities in 2017 with home and garden distributors and big box retailers. Our entry into the retail market, if at all, would either be as a product branded foliar application provided to wholesalers or as a privately branded product through a licensing or distribution agreement. Due to our current production limitations, bottling, packaging and labeling would be conducted by a product fulfillment agreement with a third-party vendor.

BAM Inc. expects to develop a precision agricultural approach in agricultural markets, expand domestic sales in states not currently addressed, and prove its value proposition with grower return on investment statistics. BAM Inc. is currently licensed to sell its commercial product in thirty-two states.

The Company plans to add agronomists, field agricultural technical support personnel and additional field sales and marketing management during 2017. The Company also expects to expand its brand recognition and market penetration by developing its channel partner network. We expect that introduction of new formulations of BAM-FX™ will allow us to address broad agricultural markets and expand the sale of product through an expanded product offering, in agricultural markets.

The Company’s manufacturing facility in Okeechobee, Florida, could have insufficient capacity to fulfill domestic and international orders dependent upon product demand in 2017. We expect to begin designing and engineering a continual production process facility during the first quarter of 2017. The decision to add a second newly designed and engineered production facility for redundancy, product demand and continual improvement in quality control and efficiency will be made when production requirements dictate and adequate financial resources are available. Although no specific location has been identified, we believe this facility would be located in a domestic southwestern State to service channel partners in the western and mid-west United States and expected channel partners in the Asia-Pacific region.

Zero Gravity Life Sciences, Inc.

We expect ZGLS will assist with agricultural research and identify complimentary technologies for agricultural and any space related initiatives and assist in developing and testing new BAM-FX™-based formulations for specific crops and varying geographic soils and weather conditions. In addition, ZGLS will manage our intellectual property portfolio and assist BAM Inc. with patent strategies related to commercialization of new products. The Company also expects ZGLS to provide focus on the Company’s Planetary Sustainability Institute efforts in 2017 in cooperation with Space Florida.

Strategy for Growth

BAM Agricultural Solutions, Inc.

BAM Inc. is executing the commercial roll out of BAM-FX™ following three years of initial product testing with several universities, end product users, and laboratory work supplementing the science of BAM-FX™ during 2016 through work performed under the RSAA with NASA ARC. BAM-FX™ has been licensed as a fertilizer product and approved for sale in thirty-two states in the United States and in Chile. BAM Inc. is pursuing registration and approval for commercial sale and distribution in Paraguay, Brazil, Colombia, South Africa, China, Indonesia and the Philippines.

BAM Inc. is currently addressing the need for additional domestic personnel requirements in sales and agronomy to support domestic and South American channel partners in 2017. Currently, sales and agronomy personnel are sufficient to support the Chilean market and our channel partner in Paraguay. Additional personnel will be required as sales and distribution expands domestically and begins in other South American countries. When operations commence in South Africa and in Asia Pacific countries, BAM Inc. expects to increase agronomy resources resident in the countries of operation.

The Company is executing a brand awareness and marketing support strategy, which includes:

|

● |

Implementing a comprehensive online and social media presence integrating website development aimed at channel partner and consumer audiences, search engine optimization and core message reach through social media platforms. |

|

● |

Coordinating direct, indirect and cross marketing activities to support our channel partner’s sales efforts, including placement of advertisements and articles in leading print and electronic agricultural publications such as Western Grower & Shipper, World Ag Outlook and others. |

|

● |

Participation, including speaking engagements, at seminars and industry tradeshows to extend our core message reach into the agricultural community by highlighting the unique attributes of the BAM-FX™ products. |

The Company’s growth strategy engages and supports channel partners in domestic and international agricultural markets. In addition, our strategy includes supporting our product’s value proposition scientifically in collaboration with NASA ARC through the RSAA, Ohio State University and Penn State University. Domestic field validation tests, conducted on potential customer locations, will be coordinated by our national sales director, conducted by our certified crop advisors, and directed by our agronomy team. Our branch office personnel in Chile are expected to manage channel partner engagement, registration and validation efforts in South America with oversight from the Company’s chief executive officer. Other international channel partner engagements and validation requirements will be managed by our Chief Technology Officer, supported by in-country consultants.

We believe our marketing approach for 2017 will focus primarily on foliar and seed soak/coat applications. Science supporting competitive market advantages in foliar markets will be collaboratively developed with NASA ARC under our RSAA. Testing of seed soak/coat application is planned to continue through field trail applications both domestically and internationally.

In anticipation of product demand exceeding our current production capacity, we will commence designing, engineering and developing a continual process flow facility expected to complete in late 2017.

Zero Gravity Life Sciences, Inc.

ZGLS’s short to mid-term plans includes the utilization of NASA and PSI relationships to research BAM-FX™ related to space program applications, as well as engaging in research based upon the Company’s zero/micro gravity intellectual property leading toward the development and patenting of unique stem cells developed on the ISS. These potentially patentable plant stem cell lines could lead to new global food cash crops resistant to climate change and other adverse environmental factors.

ZGLS, in cooperation with our agronomy team, is also continuing ground-based research on a pipeline of additional derivative BAM-FX™ products utilizing other minerals and micronutrients other than our original zinc-copper compound and complementary products for inclusion in an expanded product offering. In addition, ZGSL is investigating select in-licensing opportunities, particularly those addressing challenges to the NASA space program along with clear terrestrial healthcare needs.

Sales and Distribution Strategy

The Company implemented a channel partner sales and distribution strategy during the second and third quarter of 2016 for the United States and selected global markets. The Company believes channel partner alliances, as they are developed and strengthened, will result in effective market penetration leading to revenue growth. Channel partner sales and customer support will combine the talents of our internal sales organization and agronomy team. This market strategy and its impact on future revenue and product distribution will continue to evolve throughout 2017. One of our principle areas of focus is to provide technical and marketing support to our channel partners.

Intellectual Property

We have made protection of our intellectual property a strategic priority. We rely on a combination of patent applications, trademarks, trade secrets and other intellectual property laws to protect our proprietary rights.

Patent Applications

We are the owners or licensees of two U.S. patents and many U.S. and foreign pending patent applications that form an important part of our immediate and future business plans. We have been assigned or licensed the rights to these patent applications through agreements with our chief science officer and former director, John W. Kennedy.

We are the assignee of a portfolio of patent applications that pertain to the second-generation bioavailable mineral compositions ("BAM-FX™"). The BAM-FX™ composition is highly useful as a nutrient additive that may fortify against disease or environmental stresses and promotes growth. The basis of which is the ability of the ionized micro nutrient platform to deliver selected minerals into a plant or other complex organism systemically at the cellular level. The U.S. Patent and Trademark Office issued U.S. Patent No. 9,266,785, titled Bioavailable Minerals for Plant Health, on February 23, 2016. The patent will expire on December 27, 2026. Related applications are pending in Chile, Thailand, and Malaysia as well as a child U.S. application.

We are also the licensee of a patent application that pertains to the use of artificial Superoxide Dismutase ("SOD") compositions for the treatment of several plant and animal diseases, including amyotrophic lateral sclerosis (also known as ALS disease). Superoxide is naturally produced by plants and animals, including humans, and its production is accelerated in times of trauma or stress. SOD is produced by the cells to counteract the effects of an over-production of superoxide. Adequate amounts of SOD may increase life-span in humans and may be capable of remediating (and saving) severely stressed plants. This patent application discusses an artificial SOD that can be easily applied and used for treating over-production of superoxide, particularly ALS and other neural disorders. Animal studies of the SOD are being discussed on an ongoing basis with NASA and academic entities. The plant and space radiation applications of the patent applications are being licensed to ZGSI exclusively from Mr. John W. Kennedy for specialized testing and research.

ZGSI is the exclusive assignee of a patent application directed to the replication of stems cells in a weightless environment. This patent application contains claims covering biological processes in microgravity, including the growth of cellular plant and animal tissues on-orbit, stem cell replication and related processes. The technology accelerates the evolution of organisms, particularly plants, to adapt the organism to thrive in a hostile environment including cold and/or arid climates. Plants adapted using the technology show increased tolerance for the selected hostile environment relative to traditional plants. Specific applications include the development of food crops that are tolerant of cold climates (e.g. frost resistant crops) and arid environments (drought resistant crops). A key part of our ongoing operations is the expansion of this technology to cover additional crops, animals and potentially humans, and the specific methodologies and tools that are developed from our R&D. It is therefore a part of our technology that holds much promise and, from a commercial standpoint, falls into the medium to longer term plans of the Company.

Trade Secrets

Parts of our portfolio of intellectual property includes trade secrets pertaining to the manufacturing of several of the materials previously mentioned. In particular, BAM-FX™ and its derivatives are made in a complex and very specific process utilizing purpose-built equipment. These manufacturing processes are a separate technology, distinct from the patent applications, and remain highly secure and confidential. Reverse engineering of a product is always possible with sufficient resources. However, attempting to manufacture BAM-FX™ without the correct purpose-built equipment requisite to the task may result in a runaway exothermic reaction. We believe that the experience we have honed over several years of manufacturing these products gives us a substantial competitive edge over any potential newcomers.

Trademarks

In 2015, we filed a trademark application to protect BAM-FX™ which was registered with the USPTO on November 8, 2016. Our trademark "UNLOCKING NUTRITION FOR THE WORLD™" was registered with the USPTO on September 8, 2015. We also hold a number of other common law trademarks that we may register in the future.

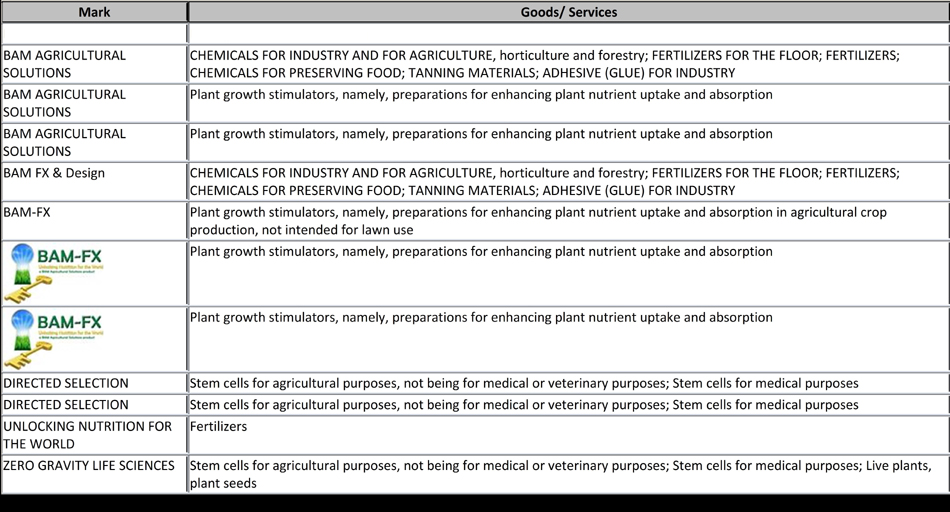

As of March 29, 2017, the Company has the following trademark inventory :

Strategic Relationships

|

1. |

UC Davis, Department of Land, Air & Water Resources: The Company is currently conducting field trials of BAM-FX™ initially with walnut trees in conjunction with the Department of Land, Air & Water Resources at the University of California, Davis. |

|

2. |