UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form

For the quarterly period ended

For the transition period from to

Commission File No. No.

(Exact name of registrant as specified in its charter) | |

| 7380 |

| ||

(State or Other Jurisdiction of Incorporation or Organization) |

| (Primary Standard Industrial Classification Number) |

| (IRS Employer Identification Number) |

(Address and telephone of principal executive offices)

Securities registered pursuant to Section 12(b) of the Exchange Act: None.

Securities registered pursuant to Section 15(d) of the Exchange Act:

(Title of class)

Former address: 1255 W, Rio Salado Parkway, Suite 215, Tempe, Arizona, 85281

(Former name, former address and former fiscal year, if changed since last report)

Indicate by checkmark whether the issuer: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Exchange Act during the past 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer | ☐ | Accelerated filer | ☐ |

☐ | Smaller reporting company | ||

|

| Emerging growth company |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes

Applicable Only to Issuer Involved in Bankruptcy Proceedings During the Preceding Five Years. N/A

Indicate by checkmark whether the issuer has filed all documents and reports required to be filed by Section 12, 13 and 15(d) of the Securities Exchange Act of 1934 after the distribution of securities under a plan confirmed by a court. Yes ☒ No ☐

No market value has been computed as of June 30, 2022 based upon the fact that no active trading market has been established.

Applicable Only to Corporate Issuers:

Indicate the number of shares outstanding of each of issuer’s classes of common stock, as of the most practicable date: As of August 22, 2022, there were

TABLE OF CONTENTS

| 2 |

| Table of Contents |

PART I. FINANCIAL INFORMATION

ITEM: 1 FINANCIAL STATEMENTS

GREEN VISION BIOTECHNOLOGY CORP. AND SUBSIDIARIES

CONSOLIDATED BALANCE SHEETS

|

| Note |

|

| June 30, 2022 |

|

| December 31, 2021 |

| |||

ASSETS |

|

|

| (Unaudited) |

|

| (Audited) |

| ||||

Cash and cash equivalents |

|

|

|

| $ |

|

| $ |

| |||

Accounts receivable, net of allowance for doubtful accounts |

|

|

|

|

|

|

|

|

| |||

Inventories, net |

|

| 7 |

|

|

|

|

|

|

| ||

Advance to suppliers |

|

|

|

|

|

|

|

|

|

| ||

Other receivables |

|

| 4 |

|

|

|

|

|

|

| ||

Total current assets |

|

|

|

|

|

|

|

|

|

| ||

|

|

|

|

|

|

|

|

|

|

|

|

|

Property, plant and equipment, net |

|

| 5 |

|

|

|

|

|

|

| ||

Intangible assets |

|

| 6 |

|

|

|

|

|

|

| ||

Restricted cash |

|

|

|

|

|

|

|

|

|

| ||

Total non-current assets |

|

|

|

|

|

|

|

|

|

| ||

TOTAL ASSETS |

|

|

|

|

| $ |

|

| $ |

| ||

LIABILITIES AND STOCKHOLDERS’ EQUITY |

|

|

|

|

|

|

|

|

|

|

|

|

Accounts payable |

|

|

|

|

| $ |

|

| $ |

| ||

Advances from customer |

|

|

|

|

|

|

|

|

|

| ||

Accrued expenses |

|

|

|

|

|

|

|

|

|

| ||

Accrued payroll |

|

|

|

|

|

|

|

|

|

| ||

Other payables |

|

| 9 |

|

|

|

|

|

|

| ||

Other tax payables |

|

|

|

|

|

|

|

|

|

| ||

Amount due to related parties |

|

| 11 |

|

|

|

|

|

|

| ||

Amount due to shareholder |

|

|

|

|

|

|

|

|

|

| ||

Total current liabilities |

|

|

|

|

|

|

|

|

|

| ||

TOTAL LIABILITIES |

|

|

|

|

| $ |

|

| $ |

| ||

|

|

|

|

|

|

|

|

|

|

|

|

|

Stockholders’ equity |

|

|

|

|

|

|

|

|

|

|

|

|

Common stock, $ |

|

|

|

|

|

|

|

|

|

| ||

Additional paid-in capital |

|

|

|

|

|

| ( | ) |

|

| ( | ) |

Accumulated other comprehensive loss |

|

|

|

|

|

| ) |

|

| ( | ) | |

Accumulated deficit |

|

|

|

|

|

| ( | ) |

|

| ( | ) |

TOTAL STOCKHOLDERS’ DEFICIT |

|

|

|

|

|

| ( | ) |

|

| ( | ) |

TOTAL LIABILITIES AND STOCKHOLDERS’ DEFICIT |

|

|

|

|

| $ |

|

| $ |

| ||

See accompanying notes to unaudited consolidated financial statements

| 3 |

| Table of Contents |

GREEN VISION BIOTECHNOLOGY CORP. AND SUBSIDIARIES

CONSOLIDATED STATEMENTS OF OPERATIONS

(UNAUDITED)

|

| Note |

|

| Three Months Ended Jun 30, 2022 |

|

| Three Months Ended Jun 30, 2021 |

|

| Six Months Ended Jun 30,2022 |

|

| Six Months Ended Jun 30,2021 |

| |||||

|

|

|

|

| $ |

|

| $ |

|

| $ |

|

| $ |

| |||||

Continuing operations |

|

|

| (Unaudited) |

|

| (Unaudited) |

|

| (Unaudited) |

|

| (Unaudited) |

| ||||||

Revenue, net |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||

Cost of goods sold |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||

Gross profit |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

Operating expenses |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

Selling expenses |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||

General and Administrative expenses |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||

Total operating expenses |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

(Loss)/Income from operations |

|

|

|

|

| ( | ) |

|

| ( | ) |

|

| ( | ) |

|

| ( | ) | |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

Non-operating income(expense) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

Interest income |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||

Interest expenses |

|

|

|

|

| ( | ) |

|

| ( | ) |

|

| ( | ) |

|

| ( | ) | |

Other income |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||

Other expense |

|

|

|

|

| ( | ) |

|

|

|

|

| ( | ) |

|

| ( | ) | ||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

(Loss)/Income before income taxes |

|

|

|

|

| ( | ) |

|

| ( | ) |

|

| ( | ) |

|

| ( | ) | |

Income taxes |

|

| 12 |

|

|

|

|

|

|

|

|

|

|

|

|

| ||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Net (loss)/income |

|

|

|

|

|

| ( | ) |

|

| ( | ) |

|

| ( | ) |

|

| ( | ) |

Net (loss)/income attributable to the Company |

|

|

|

|

|

| ( | ) |

|

| ( | ) |

|

| ( | ) |

|

| ( | ) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Foreign currency translation adjustment |

|

|

|

|

|

|

|

|

| ( | ) |

|

|

|

|

| ( | ) | ||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Comprehensive (Loss)/Income |

|

|

|

|

|

|

|

|

| ( | ) |

|

| ( | ) |

|

| ( | ) | |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Loss per share of common stock |

|

| 10 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Basic and diluted |

|

|

|

|

|

| ( |

|

| ( |

|

| ( |

|

| ( | ||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Weighted average number of common shares outstanding – basic and diluted |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||

See accompanying notes to unaudited consolidated financial statements

| 4 |

| Table of Contents |

GREEN VISION BIOTECHNOLOGY CORP. AND SUBSIDIARIES

CONSOLIDATED STATEMENTS OF STOCKHOLDERS’DEFICIT AND COMPREHENSIVE INCOME

(UNAUDITED)

|

| Number of common shares outstanding |

|

| Amount |

|

| Additional paid-in capital |

|

| Accumulated other comprehensive income |

|

| Accumulated deficits |

|

| Total stockholders’ equity/ (deficit) |

| ||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||

Balance, January 1, 2021 |

|

|

|

| $ |

|

|

| ( | ) |

|

| ( | ) |

|

| ( | ) |

| $ | ( | ) | ||

Net loss |

|

| - |

|

|

|

|

|

|

|

|

|

|

|

| ( | ) |

|

| ( | ) | |||

Foreign currency translation adjustment |

|

| - |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Balance, March 31, 2021 |

|

|

|

| $ |

|

|

| ( | ) |

|

| ( | ) |

|

| ( | ) |

| $ | ( | ) | ||

Net loss |

|

| - |

|

|

|

|

|

|

|

|

|

|

|

| ( | ) |

|

| ( | ) | |||

Foreign currency translation adjustment |

|

| - |

|

|

|

|

|

|

|

|

| ( | ) |

|

|

|

|

| ( | ) | |||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Balance, June 30, 2021 |

|

|

|

| $ |

|

|

| ( | ) |

|

| ( | ) |

|

| ( | ) |

| $ | ( | ) | ||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Balance, January 1, 2022 |

|

|

|

| $ |

|

|

| ( | ) |

|

| ( | ) |

|

| ( | ) |

| $ | ( | ) | ||

Net loss |

|

| - |

|

|

|

|

|

|

|

|

|

|

|

| ( | ) |

|

| ( | ) | |||

Foreign currency translation adjustment |

|

| - |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Balance, March 31, 2022 |

|

|

|

| $ |

|

|

| ( | ) |

|

| ( | ) |

|

| ( | ) |

| $ | ( | ) | ||

Net loss |

|

| - |

|

|

|

|

|

|

|

|

|

|

|

| ( | ) |

|

| ( | ) | |||

Foreign currency translation adjustment |

|

| - |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Balance, June 30, 2022 |

|

|

|

| $ |

|

|

| ( | ) |

|

|

|

|

| ( | ) |

| $ | ( | ) | |||

| 5 |

| Table of Contents |

GREEN VISION BIOTECHNOLOGY CORP. AND SUBSIDIARIES

CONSOLIDATED STATEMENTS OF CASH FLOWS

|

| (Unaudited) |

| |||||

|

| Six Months Ended June 30, |

| |||||

|

| 2022 |

|

| 2021 |

| ||

Cash flows provided by (used in) continuing operating: activities: |

|

|

|

|

|

| ||

Net loss |

| $ | ( | ) |

| $ | ( | ) |

Adjustments to reconcile net income (loss) to net cash provided by (used in) operating activities: |

|

|

|

|

|

|

|

|

Depreciation |

|

|

|

|

|

| ||

Amortization of intangible assets |

|

|

|

|

|

| ||

Inventory provision reversal |

|

| ( | ) |

|

| ( | ) |

Disposal loss of property, plant and equipment |

|

|

|

|

|

| ||

Changes in assets and liabilities: |

|

|

|

|

|

|

|

|

Accounts receivable |

|

|

|

|

|

| ||

Inventories |

|

|

|

|

|

| ||

Advances to suppliers |

|

|

|

|

|

| ||

Other receivables |

|

|

|

|

|

| ||

Restricted cash |

|

| ( | ) |

|

| ( | ) |

Accounts payable |

|

|

|

|

|

| ||

Advances from customer |

|

|

|

|

|

| ||

Other payables |

|

|

|

|

|

| ||

Other tax payables |

|

| ( | ) |

|

|

| |

Accrued payroll |

|

|

|

|

| ( | ) | |

Accrued expenses |

|

|

|

|

|

| ||

Amount due to related parties |

|

|

|

|

|

| ||

Net cash flows provided by (used in) operating activities |

|

| ( | ) |

|

| ( | ) |

Cash flows provided by (used in) investing activities: |

|

|

|

|

|

|

|

|

Proceeds from sale of property, plant and equipment |

|

|

|

|

|

| ||

Net cash flows used for investing activities |

|

|

|

|

|

| ||

Cash flows provided by (used in) financing activities: |

|

|

|

|

|

|

|

|

Amounts due to shareholder |

|

|

|

|

|

| ||

Net cash flows provided by (used in) financing activities |

|

|

|

|

|

| ||

Cash flows provided by (used in) discontinued operating activities: |

|

|

|

|

|

|

|

|

Net cash provided by (used in) investing activities of discontinued operations |

|

|

|

|

|

| ||

Net cash flows provided by discontinued operations |

|

|

|

|

|

| ||

|

|

|

|

|

|

|

|

|

Net increase (decrease) in cash and cash equivalents |

|

| ( | ) |

|

|

| |

Effect of foreign currency translation |

|

|

|

|

| ( | ) | |

Cash – beginning of period |

|

|

|

|

|

| ||

Cash – end of period |

| $ |

|

| $ |

| ||

Supplemental disclosures of cash flow information: |

|

|

|

|

|

|

|

|

Interest paid |

| $ |

|

| $ |

| ||

Income taxes |

| $ |

|

| $ |

| ||

See accompanying notes to unaudited consolidated financial statements

| 6 |

| Table of Contents |

GREEN VISION BIOTECHNOLOGY CORP.AND SUBSIDIARIES

NOTES TOUNAUDITEDCONSOLIDATEDFINANCIAL STATEMENTS

NOTE 1. ORGANIZATION AND NATURE OF BUSINESS

Green Vision Biotechnology Corp. (formerly known as Vibe Wireless Corp., originally known as Any Translation Corp.), (the “Company”, “GVBT”), was incorporated under the laws of the State of Nevada on July 5, 2012. The Company was founded to be in the business of translation and interpretation. On November 12, 2015, the Company changed its name from Any Translation Corp. to Vibe Wireless Corp. On September 30, 2016, we changed our name from Vibe Wireless Corp. to Green Vision Biotechnology Corp.

On September 30, 2016, the Company filed a Certificate of Amendment with the Nevada Secretary of State (the “Nevada SOS”) whereby it amended its Articles of Incorporation to increase the Company’s authorized number of shares of common stock from

On the same date, September 30, 2016, the Company filed Articles of Merger with the Nevada SOS whereby it entered into a statutory merger with its wholly-owned subsidiary, Green Vision Biotechnology Corp. pursuant to Nevada Revised Statutes 92A.200 et. seq. The effect of such merger is that the Company is the sole surviving entity and changed its name to “Green Vision Biotechnology Corp.”

The investment transaction under the share exchange agreements and contractual agreements as described below (collectively the “Transaction Agreements”) was entered into, between each of the Shareholders of Lutu International Biotechnology Limited (“Lutu”), a company incorporated under the laws of Cayman Islands and GVBT (the “Investment Transaction”) on May 12, 2017. As a result of closing the Investment Transaction, GVBT acquired part of the shares of Lutu International and assumed management of Lutu and all its direct and indirect subsidiaries (“the Lutu Group”).

On May 12, 2017, GVBT entered into a share exchange agreement with Harcourt Capital Limited (“Harcourt”), a limited company incorporated in the British Virgin Islands, which holds 6% of the issued and outstanding shares of Lutu; and Woodhead Investments Limited (“Woodhead”), a limited company incorporated in the British Virgin Islands, which holds 5% of the issued and outstanding shares of Lutu (the “Minority Interest Exchange Agreement”). Under the Minority Interest Exchange Agreement, Woodhead agreed to transfer GVBT a total of 5% of the issued and outstanding shares of Lutu. In consideration, GVBT agreed to grant Woodhead, or persons designated by Woodhead, a right to receive a total of 5 million shares of GVBT’s common stock. Under the Minority Interest Exchange Agreement, Harcourt agreed to transfer to GVBT a total of 6% of the issued and outstanding shares of Lutu. In consideration, GVBT agreed to grant Harcourt, or persons designated by Harcourt, a right to receive a total of 6 million shares of GVBT’s common stock. The transactions under the Minority Interest Exchange Agreement were completed on May 12, 2017.

Able Lead, an 89% shareholder of Lutu, has an outstanding loan of $

| 7 |

| Table of Contents |

GREEN VISION BIOTECHNOLOGY CORP. AND SUBSIDIARIES

NOTES TOUNAUDITEDCONSOLIDATEDFINANCIAL STATEMENTS

NOTE 1. ORGANIZATION AND NATURE OF BUSINESS (CONTINUED)

Pursuant to an escrow agreement (the “Escrow Agreement”) entered into between Booth Udall Fuller, PLC (the “Escrow Agent”) and GVBT on May 12, 2017, the Escrow Shares shall be held by Booth Udall Fuller, PLC for a year following the execution of the Majority Interest Exchange Agreement. The Escrow Shares shall not be subject to any lien, attachment, or any other judicial process of any creditor of GVBT, and shall be held and disbursed solely for the purposes and in accordance with the terms of the Majority Interest Exchange Agreement.

On May 12, 2017, GVBT entered into the Contractual Agreements with Lutu and/or Able Lead. Upon execution of the Contractual Arrangements, GVBT assumed management of Lutu and its subsidiaries (the “Lutu Group”) and received economic benefits which includes the right to receive the expected residual returns and and/or obligation to absorb expected loss from the Lutu Group. Each agreement in the Contractual Arrangements constitutes valid and binding obligations of the parties of such agreements and is enforceable and valid in accordance with the laws of Cayman Islands. All agreements executed by Lutu were duly approved by its board of directors and the Shareholders of Lutu.

Consulting Services Agreement

Pursuant to the exclusive consulting services agreement entered into between GVBT and Lutu on May 12, 2017, GVBT has the exclusive right to provide to the Lutu Group general business operation services, including advice and strategic planning, as well as consulting services related to the technological research and development of bio-fertilizers. Further, GVBT owns the intellectual property rights developed or discovered through research and development, in the course of providing the consulting services, or derived from the provision of the consulting services. In consideration, Lutu pays an annual consulting service fees to GVBT in the amount equivalent to all of Lutu’s net profits for the relevant financial year. The term of this consulting service agreement is five (5) years from its effective date and may be terminated upon GVBT’s written confirmation prior to the expiration of this agreement.

Unless otherwise expressly agreed in writing by GVBT and Able Lead, the Consulting Services Agreement shall be automatically terminated upon the termination of any of the agreements in the Contractual Arrangements or the Majority Interest Exchange Agreement.

We hereby confirmed that we have not received any consulting fees from Lutu and Lutu Group during the periods presented.

Operating Agreement

Pursuant to the operating agreement entered into between GVBT, Lutu and Able Lead on May 12, 2017, GVBT agreed to provide guidance and instructions on the Lutu Group’s daily operations, financial management and employment issues. Able Lead agreed to designate candidates recommended by GVBT as their representatives on the boards of directors of each member of the Lutu Group. GVBT has the right to appoint senior executives of each member of the Lutu Group. In addition, GVBT agreed to guarantee the Lutu Group’s performance under any agreements or arrangements relating to the Lutu Group’s business arrangements with any third party. In consideration, Lutu agrees that it will not, and will cause the Lutu Group not to, without the prior consent of GVBT, engage in any transactions that could materially affect their respective assets, liabilities, rights or operations, including but not limited to, incurrence or assumption of any indebtedness, sale or purchase of any assets or rights, incurrence of any encumbrance on any of their assets or intellectual property rights in favor of a third party or transfer of any agreements relating to their business operation to any third party. The term of this operating agreement is five (5) years from its effective date and may be extended and terminated only upon GVBT’s written confirmation prior to the expiration of this agreement.

Unless otherwise expressly agreed in writing by GVBT and Able Lead, the Operating Agreement shall be automatically terminated upon the termination of any of the agreements in the Contractual Arrangements or the Majority Interest Exchange Agreement.

| 8 |

| Table of Contents |

GREEN VISION BIOTECHNOLOGY CORP. AND SUBSIDIARIES

NOTES TOUNAUDITEDCONSOLIDATEDFINANCIAL STATEMENTS

NOTE 1. ORGANIZATION AND NATURE OF BUSINESS (CONTINUED)

Proxy Agreement

Pursuant to the proxy agreement entered into between Able Lead, Lutu, and GVBT on May 12, 2017, Able Lead agreed to irrevocably grant a person to be designated by GVBT the right to exercise its voting rights and other rights, including the attendance of, and the voting at the shareholders’ meetings of Lutu for and on behalf of Able Lead (or the signing of written resolutions in lieu of such meetings) in accordance with applicable laws and its articles of association, including but not limited to the appointment and voting for the directors and chairman of the board as the authorized representative of Able Lead to exercise controlling power in the Lutu Group. The proxy agreement may be terminated by joint consent of the parties or upon 7-day written notice from GVBT. The proxy right granted by the proxy agreement has never been exercised.

The Expiration of the Consulting Services Agreement, Operating Agreement and Proxy Agreement

On July 30, 2019, the Company cancelled the

The above-mentioned Consulting Services Agreement, Operating Agreement and Proxy Agreement entered between the Company, Lutu and Able Lead on May 12, 2017 were for

Furthermore, since the issuance of common stock to Able Lead Holdings Limited on July 30, 2019, the Company became the 100% shareholder of Lutu, the Company is of the view that there is no longer any need for the Company to renew and extend these agreements to achieve the previous objectives of these agreements.

Changes Resulting from the Investment Transaction

The closing of the Investment Transaction occurred on May 12, 2017, resulting in a change of control of GVBT. Prior to closing of the Investment Transaction, GVBT had a total of

Following the closing of the Investment Transaction, GVBT began carrying on the business of the Lutu Group. The Lutu Group, with its operation primarily located in the Shanxi Province of China, is engaged in the biotechnology industry, in particular, the production and distribution of bio-fertilizers. Revenues of the Lutu Group are currently generated from China.

Changes to the Board of Directors and Officers

Simultaneous with the closing of the Investment Transaction, there was a change in the officers and directors of GVBT. As authorized by the bylaws, the existing director of GVBT, Mr. Ma Wai Kin, appointed two (2) additional members to the Board of GVBT. Such members are Mr. Lam Ching Wan (also known as William Lam) and Mr. Leung Kwong Tak (also known as Dr. Michael Leung). Mr. Ma also appointed Mr. William Lam as GVBT’s Chief Executive Officer and Mr. Lo Kwok Leung as GVBT’s Chief Financial Officer. Mr. Lo Kwok Leung is not related to Dr. Michael Leung.

All members of the Board shall hold their respective offices for a term of one year from their respective dates of appointment, or until the election and qualification of their successors, and thereafter to resign as a director of GVBT. In accordance with the bylaws, officers are elected by the board of directors and serve at the discretion of the board of directors.

| 9 |

| Table of Contents |

GREEN VISION BIOTECHNOLOGY CORP. AND SUBSIDIARIES

NOTES TOUNAUDITEDCONSOLIDATEDFINANCIAL STATEMENTS

NOTE 1. ORGANIZATION AND NATURE OF BUSINESS (CONTINUED)

Accounting Treatment

The Investment Transaction was accounted for as a reverse-merger and recapitalization. For financial reporting purposes, Lutu is the acquirer and GVBT is the acquired company. After completion of the transaction, the assets, liabilities, operations results and cash flow of GVBT that will be reflected in the historical consolidated financial statements prior to the Investment Transaction will be those of Lutu and its subsidiaries and will be recorded at the historical cost basis of Lutu and its subsidiaries. Number of shares deemed to be outstanding for the period from January 1, 2018 to the acquisition date will be reflected in the balance of the common stock and paid in capital. The Company changed its fiscal year ended from January 31 to December 31.

Tax Treatment and SEC Filer Status: Small Business Issuer

The Investment Transaction is intended to constitute a reorganization within the meaning of Section 368(a) of the Internal Revenue Code of 1986, as amended (the “Code”), or such other tax-free reorganization exemptions that may be available under the Code. Immediately following the Investment Transaction, the filer status of GVBT will be a “smaller reporting company” as defined in Item 10(f)(1) of Regulation S-K, as promulgated by SEC.

As we are a Smaller Reporting Company under 12b-2 under the Exchange Act, we will be describing the development of our business pursuant to Item 101(h).

(1) | Form and year of organization Our Holding Company (defined hereunder) was formed in Nevada USA as a corporation on May 7, 2012. |

|

|

(2) | There is no bankruptcy, receivership or similar proceeding against the Holding Company. |

|

|

(3) | During this period, the Holding Company has not undergone any material reclassification, merger, consolidation, or purchase or sale of a significant amount of assets not in the ordinary course of business. |

|

|

(4) | Business of the smaller reporting company. |

| (i). | Principal products or services and their markets Shanxi Green Biotechnology Industry Company Limited has been producing biofertilizers in China, with the China local market as its main distribution area. The Company has signed a Memorandum of Understanding (non-legally binding) with ISCA on April 27, 2022, whereby details of the collaboration is under further discussion (please refer to the Company announcement on May 03, 2022). |

|

|

|

| (ii). | Distribution methods of the products or services The Company was utilizing sales channels to distribute products, mixed with some direct sales through sales team (who are employees of the Company or independent contractors). |

|

|

|

| (iii). | Status of any publicly announced new product or service Since the more stringent environment rules were put in place, the Company has not developed any new product. |

|

|

|

| (iv). | Competitive business conditions and the smaller reporting company’s competitive position in the industry and methods of competition The Company’s biofertilizer products are quite unique because they have made use of the local mineral products in the Shanxi Province of China. The Company has obtained patents of production both in the US and China. |

|

|

|

| (v). | Sources and availability of raw materials and the names of principal suppliers Sources of raw materials are mainly from the local areas in Shanxi, supplied by Mr. He Qun (in respect of Potassium Shale), and Mr. Li Jianli (in respect of Humic Acid). |

|

|

|

| (vi). | Dependence on one or a few major customers When the Company was active in pursuing sales and marketing of the products, there are several major customers, including Heilongjiang Longhui Agricultural Cooperative, Yunnan Kunming Dong Chuan Jin Rui Commerce and Trade Company Limited and Shanxi Fuda Industrial Company Limited. |

| 10 |

| Table of Contents |

GREEN VISION BIOTECHNOLOGY CORP. AND SUBSIDIARIES

NOTES TOUNAUDITEDCONSOLIDATEDFINANCIAL STATEMENTS

NOTE 1. ORGANIZATION AND NATURE OF BUSINESS (CONTINUED)

| (vii). | Patents, trademarks, licenses, franchises, concessions, royalty agreements or labor contracts, including duration The Company owns patents both in the US (pending PCT Application) and China, details of which are as follows :- |

|

| 1. | Patent Certificate No. ZL201410324943.X; |

|

|

|

|

|

| 2. | Patent Certificate No. ZL201410324985.3; |

|

|

|

|

|

| 3. | Patent Certificate No. ZL200910073705.5; |

|

|

|

|

|

| 4. | Shanxi Green Biotechnology Industry Co., Ltd., for BACILLUS MUCILAGINOSUS AND HIGH-DENSITY FERMENTATION METHOD AND USE THEREOF, U.S. Serial No. 17/535,580, filed November 25, 2021, Continuation application of U.S. Serial No. 16/375,011, filed April 4, 2019, Continuation application of U.S. Serial No. 15/324,772, filed January 9, 2017, which is National Stage of International Application No. PCT/CN2015/083366, filed July 6, 2015, which claims the priority of Chinese Application No. 201410324943.X, filed July 9, 2014. |

|

|

|

|

|

| The Company also owns several trademarks in China, details of which are as follows :- | |

|

|

|

|

|

| 1. | Trademark Certificate No. 4162106; |

|

|

|

|

|

| 2. | Trademark Certificate No. 9924290; |

|

|

|

|

|

| 3. | Trademark Certificate No. 55181933. |

| (viii). | Need for any government approval of principal products or services. If government approval is necessary and the smaller reporting company has not yet received that approval, discuss the status of the approval within the government approval process The China Subsidiary has obtained all necessary permits from the Chinese government on the production of biofertilizers. Please refer to above for a list of these permits. |

|

|

|

| (ix). | Effect of existing or probable governmental regulations on the business The Chinese government encourages and promotes productions which are of agricultural nature, including fertilizers. Further, the Chinese government has placed more focus on promoting environmental-friendly products, including biofertilizers which are green and environmental-friendly. The Company’s biofertilizer products fall under this category. |

|

|

|

| (x). | [Reserved] |

|

|

|

| (xi). | Costs and effects of compliance with environmental laws (federal, state and local) Due to the enforcement on new environmental regulations over industrial production by coal-fired boilers by local authorities in Shanxi, the Company’s production was restricted to a certain extent in 2017. To fully comply with the new environmental regulations in place, management of the Company had planned to carry our rectification work and expected that the rectification work could be completed by mid of 2018 and full-scale production might resume in the second half of 2018. However, due to the shortage of funding to carry out the rectification work on our coal-powered generators, our production activities were restricted since second quarter in 2018.Our production and our production capacity were reduced as a result, significantly affected our ability to generate income and to meet the demand of our customers, which in turn had a material adverse effect on our financial condition and results of operations. |

|

|

|

|

| On January 20, 2020, with the approval of the Company, the China Subsidiary has resolved to dispose the non-current assets which were lying idle for the production. The China Subsidiary also resolved to carry out its future production by sub-contracting the production and goods assessment procedure to other production companies, with its other operations remain unchanged. The China Subsidiary is also planning to move its production process to other parts of China. |

|

|

|

|

| The Company has been considering other business opportunity in recent months and to utilize the current resources, including the property and equipment. Accordingly, the Company has signed a Memorandum of Understanding with ISCA (non-legally binding) on April 27, 2022, whereby details of the collaboration is under further discussion (please refer to the Company announcement on May 03, 2022). |

|

|

|

| (xii). | Number of total employees and number of full-time employees: 9 |

| 11 |

| Table of Contents |

GREEN VISION BIOTECHNOLOGY CORP.AND SUBSIDIARIES

NOTES TOUNAUDITEDCONSOLIDATEDFINANCIAL STATEMENTS

NOTE 1.ORGANIZATION AND NATURE OF BUSINESS (CONTINUED)

(5) | Reports to security holders. The following in any registration statement will be disclosed when filing under the Securities Act of 1933: |

| (i). | As the Company has filed current reports with updated audited financial statements, we are of the view that there may not be necessary to send annual report to the security holders at this moment. Secondly, we only have a small base of security holders (12 holders as at December 31, 2021) in the shareholders list, and that we have no public trading at this moment, we would choose to save expenses by not sending the reports to the shareholders. |

|

|

|

| (ii). | We are a current reporting company with regular filings including Forms 10-Q, 10-K and 8-K. All these reports have been filed with the Commission. |

|

|

|

| (iii). | The Commission maintains an internet site (http://www.sec.gov) that contains reports, proxy and information statements, and other information regarding GVBT that file electronically with the Commission. The current internet address of GVBT is http://www.gvbt.com. |

(6) | Foreign issuers. |

|

|

Since we are a Nevada corporation, provide the information required by Item 101(g) of Regulation S-K (§ 229.101(g)) is not applicable to us. |

Memorandum of Understanding

On April 29, 2022, the Company announced that the Company entered into a Memorandum of Understanding (“MOU”) with International Supply Chain Alliance Company Limited (“ISCA”), a provider of logistics knowhow and software to warehouse operators and shippers in China and Southeast Asia countries on the even date. The MOU states, inter alia, that the Company intends to collaborate with ISCA by acquiring all of its subsidiaries and existing contractual benefits.

The Company and ISCA shall utilize their best endeavors in entering into Definitive Agreements to realize the intended collaboration prior to October 31, 2022. The intended collaboration with ISCA, as described in the MOU, allows the Company to expand its existing business scope beyond the green product sector and further into the agricultural sector. The Company intends to fully utilize ISCA’s trading platform and data in delivering to existing and future alliance members the resulting product suite which could include a new and wide array of agricultural products.

| 12 |

| Table of Contents |

GREEN VISION BIOTECHNOLOGY CORP. AND SUBSIDIARIES

NOTES TOUNAUDITEDCONSOLIDATEDFINANCIAL STATEMENTS

NOTE 2. BASIS OF PRESENTATION AND SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

BASIS OF PRESENTATION

The accompanying consolidated financial statements of the Company have been prepared in accordance with United States generally accepted accounting principles and the rules and regulations of the Securities and Exchange Commission (the “SEC”) for consolidated financial reporting.

Summary of significant accounting policies

Principles of Consolidation and Presentation

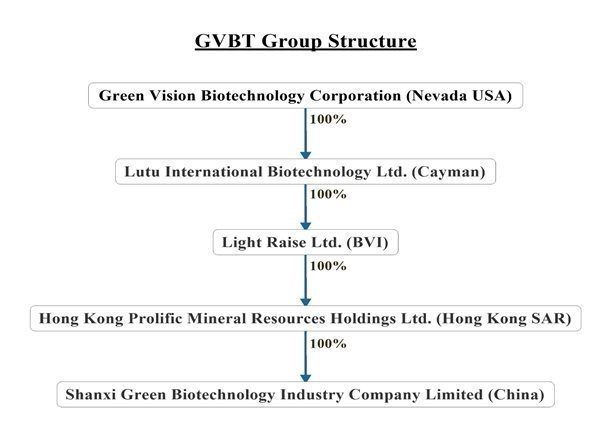

The consolidated financial statements have been prepared in accordance with U.S. generally accepted accounting principles (“U.S. GAAP”). The historical presentation of the consolidated financial statements includes the financial statements of LUTU INTERNATIONAL BIOTECHNOLOGY LIMITED, and its wholly-owned subsidiaries (collectively referred to herein as the “Company”). All intercompany accounts, transactions, and profits have been eliminated upon consolidation.

The following table depicts the identity of the subsidiaries:

Name of Subsidiary |

| Place of Incorporation |

| Attributable Equity Interest % |

|

| Registered Capital | ||

Lutu International Biotechnology Limited (RTO accounting acquirer) (1) |

|

|

|

|

| USD | |||

Light Raise Limited (2) |

|

|

|

|

| USD | |||

Hong Kong Prolific Mineral Resources Holdings Limited (3) |

|

|

|

|

| HKD | |||

Shanxi Green Biotechnology Industry Company Limited (4) |

|

|

|

|

| RMB | |||

Note: | (1) | Wholly owned subsidiary of Green Vision Biotechnology Corp. |

| (2) | Wholly owned subsidiary of Lutu International Biotechnology Limited |

| (3) | Wholly owned subsidiary of Light Raise Limited |

| (4) | Wholly owned subsidiary of Hong Kong Prolific Mineral Resources Holdings Limited |

Use of estimates

America requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenues and expenses during the reporting period. Actual results could materially differ from those estimates.

Significant estimates and judgments inherent in the preparation of these consolidated financial statements include, among other things, accounting for asset impairments, allowances for doubtful accounts, depreciation and amortization, the collection of revenues from the Agricultural Cooperative.

Economic and political risks

The Company’s operations are mainly conducted in the Hong Kong Special Administrative Region (“Hong Kong”) and the People’s Republic of China (“China”) (for the purpose of this Current Report on Form 10-Q, China does not include Hong Kong, Macau Special Administrative Region of the People's Republic of China and Taiwan (The Republic of China) and a large number of customers are located in northern China. Accordingly, the Company’s business, financial condition and results of operations may be influenced by the political, economic and legal environment in Hong Kong and China, and by the general state of the economy in Hong Kong and China.

The Company’s operations and customers in Hong Kong and China are subject to special considerations and significant risks not typically associated with companies in North America and Western Europe. These include risks associated with, among others, the political, economic and legal environments, and foreign currency exchange. The Company’s results may be adversely affected by changes in the political and social conditions in Hong Kong and China, and by changes in governmental policies with respect to laws and regulations, anti-inflationary measures, currency conversion, remittances abroad, and rates and methods of taxation, among other things.

| 13 |

| Table of Contents |

GREEN VISION BIOTECHNOLOGY CORP. AND SUBSIDIARIES

NOTES TOUNAUDITEDCONSOLIDATEDFINANCIAL STATEMENTS

NOTE 2. SUMMARY OF SIGNIFICANT ACCOUNTING (CONTINUED)

Foreign Currency Translation

The Company’s financial statements are presented in the U.S. dollar ($), which is the Company’s reporting currency, while its functional currency are Chinese Renminbi (RMB) and Hong Kong Dollar (HKD). Transactions in foreign currencies are initially recorded at the functional currency rate ruling at the date of transaction. Any differences between the initially recorded amount and the settlement amount are recorded as a gain or loss on foreign currency transaction in the consolidated statements of income. Monetary assets and liabilities denominated in foreign currency are translated at the functional currency rate of exchange ruling at the balance sheet date. Any differences are taken to profit or loss as a gain or loss on foreign currency translation in the statements of income.

In accordance with ASC 830, Foreign Currency Matters, the Company translated the assets and liabilities into US $ using the rate of exchange prevailing at the applicable balance sheet date and the statements of income and cash flows are translated at an average rate during the reporting period. Adjustments resulting from the translation are recorded in shareholders’ equity as part of accumulated other comprehensive income.

Below is a table with foreign exchange rates used for translation:

For the six months and year ended, (Average Rate) |

| Jun 30, 2022 |

|

| Dec 31, 2021 |

|

| Jun 30, 2021 |

| |||||||||||

Chinese Renminbi (RMB) |

| RMB |

|

|

|

| RMB |

|

|

|

|

|

| RMB |

|

|

| |||

United States dollar ($) |

|

|

| $ |

|

|

|

|

|

| $ |

|

|

|

| $ |

| |||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

As of (Closing Rate) |

| Jun 30, 2022 |

|

| Dec 31, 2021 |

|

| Jun 30, 2021 |

| |||||||||||

Chinese Renminbi (RMB) |

| RMB |

|

|

|

| RMB |

|

|

|

|

|

| RMB |

|

|

| |||

United States dollar ($) |

|

|

| $ |

|

|

|

|

|

| $ |

|

|

|

| $ |

| |||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

For the six months and year ended, (Average Rate) |

| Jun 30, 2022 |

|

| Dec 31, 2021 |

|

| Jun 30, 2021 |

| |||||||||||

Hong Kong (HKD) |

| HKD |

|

|

|

| HKD |

|

|

|

|

|

| HKD |

|

|

| |||

United States dollar ($) |

|

|

| $ |

|

|

|

|

|

| $ |

|

|

|

| $ |

| |||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

As of (Closing Rate) |

| Jun 30, 2022 |

|

| Dec 31, 2021 |

|

| Jun 30, 2021 |

| |||||||||||

Hong Kong (HKD) |

| HKD |

|

|

|

| HKD |

|

|

|

|

|

| HKD |

|

|

| |||

United States dollar ($) |

|

|

| $ |

|

|

|

|

|

| $ |

|

|

|

| $ |

| |||

For the six months and year ended, (Average Rate) |

| Jun 30, 2022 |

|

| Dec 31, 2021 |

|

| Jun 30, 2021 |

| |||||||||||

Hong Kong (HKD) |

| HKD |

|

|

|

| HKD |

|

|

|

|

|

| HKD |

|

|

| |||

Chinese Renminbi (RMB) |

|

|

| $ |

|

|

|

|

|

| $ |

|

|

|

| $ |

| |||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

As of (Closing Rate) |

| Jun 30, 2022 |

|

| Dec 31, 2021 |

|

| Jun 30, 2021 |

| |||||||||||

Hong Kong (HKD) |

| HKD |

|

|

|

| HKD |

|

|

|

|

|

| HKD |

|

|

| |||

Chinese Renminbi (RMB) |

|

|

| $ |

|

|

|

|

|

| $ |

|

|

|

| $ |

| |||

Revenue Recognition

The Company earns revenue by selling merchandise to end using customers primarily through distribution agent and directly to customers.

Revenue is recognized in accordance with the following five steps: when merchandise is purchased by the customer which identifies the contract (step 1) and performance obligations in the contract (step 2) with Customers. When the Company confirmed the price and collectability is reasonably assured which indicates that the transaction price is determined (step 3) and allocated to the performance obligations in the contract (step 4). When the merchandise is delivered to the customer, the performance obligation is satisfied (step 5). Revenue from wholesale distribution agent is recognized after goods delivered, amount fixed or determined and collectability is reasonably assured when the above mentioned five steps are completed.

All revenues are shown net of estimated returns during the relevant period represented by measuring the returns obligations with estimated allowance for sales returns based upon historical experience.

| 14 |

| Table of Contents |

GREEN VISION BIOTECHNOLOGY CORP. AND SUBSIDIARIES

NOTES TOUNAUDITEDCONSOLIDATEDFINANCIAL STATEMENTS

NOTE 2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (CONTINUED)

Revenue Recognition (continued)

The Company records sales tax collected from its customers on a net basis, and therefore excludes it from revenue as defined in ASC 606, Revenue from Contracts with Customers.

During the six months ended June 30, 2022 and 2021, the provision of sales return were $Nil respectively.

Cost of Goods Sold

Cost of goods sold includes the cost of materials, labor, and relevant manufacturing expenses.

Selling Expenses

Selling expenses include packaging and shipping costs, as well as advertising and certain expenses associated with operating the Company’s corporate headquarters.

Advertising Costs

The Company expensed all advertising costs as incurred. Advertising expense, net of reimbursement from suppliers, amounted to $Nil and $Nil for the six months ended June 30, 2022 and 2021 respectively. Advertising expense is included in selling expense and general and administrative expenses in the accompanying consolidated statements of income.

Leases

On January 1, 2019, the Company adopted Topic 842 using the modified retrospective transition approach by applying the new standard to all leases existing at the date of initial application. Results and disclosure requirements for reporting periods beginning after January 1, 2019 are presented under Topic 842, while prior period amounts have not been adjusted and continue to be reported in accordance with its historical accounting under Topic 840.

The Company elected the package of practical expedients permitted under the transition guidance, which allowed it to carry forward its historical lease classification, its assessment on whether a contract was or contains a lease, and its initial direct costs for any leases that existed prior to January 1, 2019. The Company also elected to combine its lease and non-lease components and to keep leases with an initial term of 12 months or less off the balance sheet and recognize the associated lease payments in the consolidated statements of income on a straight-line basis over the lease term.

Upon adoption, the Company recognized ROU assets with corresponding liabilities on the consolidated balance sheets. The ROU assets include adjustments for prepayments and accrued lease payments. The adoption did not impact its beginning retained earnings, or its prior year consolidated statements of income and statements of cash flows.

Under Topic 842, the Company determines if an arrangement is a lease at inception. ROU assets and liabilities are recognized at commencement date based on the present value of remaining lease payments over the lease term. For this purpose, the Company considers only payments that are fixed and determinable at the time of commencement. As most of its leases do not provide an implicit rate, it uses its incremental borrowing rate based on the information available at commencement date in determining the present value of lease payments. The Company’s incremental borrowing rate is a hypothetical rate based on its understanding of what its credit rating would be. The ROU asset also includes any lease payments made prior to commencement and is recorded net of any lease incentives received. The Company’s lease terms may include options to extend or terminate the lease when it is reasonably certain that it will exercise such options.

Operating leases are included in operating lease right-of-use assets, operating lease liabilities, current and non-current operating lease liabilities, on the consolidated balance sheets.

The Company did not have a lease that met the criteria of a capital lease. Leases that do not qualify as a capital lease are classified as an operating lease. Operating lease rental expenses included in selling, general and administrative expenses for the six months ended June 30, 2022 and 2021 were $Nil and $Nil respectively.

| 15 |

| Table of Contents |

GREEN VISION BIOTECHNOLOGY CORP.AND SUBSIDIARIES

NOTES TOUNAUDITEDCONSOLIDATEDFINANCIAL STATEMENTS

NOTE 2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (CONTINUED)

Accounts Receivable

Accounts receivable is recognized and carried at the original invoice amount less allowance for any uncollectible amounts. An allowance for doubtful accounts is maintained for all customers based on a variety of factors, including the industry practice, the length of time the receivables are past due, significant one-time events and historical experience. The Company is selling products delivered to certain customers which are closed to Agriculture Cooperatives as defined by ASC 905 “Agriculture”. The collection cycle may be varied and depended on the growing crops cycle.

Management reviews and adjusts this allowance periodically based on historical experience and its evaluation of the collectability of outstanding accounts receivable. The Company evaluates the credit risk of its customers utilizing historical data and estimates of future performance. Bad debts are written off as incurred.

Outstanding accounts balances are reviewed individually for collectability. The Company does not charge any interest income on trade receivables. Accounts balances are charged off against the allowance after all means of collection have been exhausted and the potential for recovery is considered remote. To date, the Company has not charged off any balances as it has yet to exhaust all means of collection.

During the six months ended June 30, 2022 and year ended December 31, 2021, the provision of doubtful debts were $Nil and $Nil respectively.

Inventories

Inventories primarily consists raw materials, work in progress, finished goods and goods on consignment of manufactured products and merchandise. Inventories are stated at lower of cost or market and net realizable value.

Cost of inventories is calculated on the weighted average basis which approximates cost.

Management regularly reviews inventories and records valuation reserves for damaged and defective returns, inventories with slow-moving or obsolescence exposure and inventories with carrying value that exceeds market value.

Inventory shrinkage is accrued as a percentage of revenues based on historical inventory shrinkage trends. The Company performs physical inventory count of its warehouse once per quarter throughout the year. The reserve for inventory shrinkage represents an estimate for inventory shrinkage since the last physical inventory date through the reporting date.

These reserves are estimates, which could vary significantly, either favorably or unfavorably, from actual results if future economic conditions, consumer demand and competitive environments differ from expectations.

During the six months ended June 30, 2022 and year ended December 31, 2021, the provision of inventory reversal were $

Property, Plant and Equipment

Property, plant and equipment are recorded at cost. Significant additions or improvements extending useful lives of assets are capitalized. Maintenance and repairs are charged to expense as incurred. Depreciation is provided over the estimated useful lives, using the

Buildings |

| |

Machinery & equipment |

| |

Office equipment |

| |

Motor vehicles |

|

| 16 |

| Table of Contents |

GREEN VISION BIOTECHNOLOGY CORP. AND SUBSIDIARIES

NOTES TOUNAUDITEDCONSOLIDATEDFINANCIAL STATEMENTS

NOTE 2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (CONTINUED)

Land Use Rights

According to the laws of the PRC, the government owns all the land in the PRC. Companies or individuals are authorized to possess and use the land only through the land use rights granted by the government. The land use rights represent cost of the rights to use the land in respect of properties located in the PRC. Land use rights are carried at cost and amortized on a

Goodwill

Goodwill represents the excess of purchase price over fair value of net assets acquired. Under ASC 350, Intangibles — Goodwill and Other, goodwill is not amortized but evaluated for impairment annually or whenever events or changes in circumstances indicate that the value may not be recoverable.

The Company performed an annual impairment test as of the fiscal year ended December 31, 2021, and a quarter review as of the period ended June 30, 2022, and determined that the impairment loss in the amount of $Nil and $Nil were recorded respectively.

Long-lived Assets

The Company reviews long-lived assets for impairment annually or whenever events or changes in circumstances indicate that the carrying amount of an asset may not be recoverable.

Long-lived assets are reviewed for recoverability at the lowest level in which there are identifiable cash flows, usually at the store level. The carrying amount of a long-lived asset is not considered recoverable if it exceeds the sum of the undiscounted cash flows expected to result from the use of the asset. If the asset is determined not to be recoverable, then it is considered to be impaired and the impairment to be recognized is the amount by which the carrying amount of the asset exceeds the fair value of the asset, determined using discounted cash flow valuation techniques, as defined in ASC 360, Property, Plant, and Equipment.

The Company determined the sum of the undiscounted cash flows expected to result from the use of the asset by projecting future revenue and operating expense for each store under consideration for impairment. The estimates of future cash flows involve management judgment and are based upon assumptions about expected future operating performance. The actual cash flows could differ from management’s estimates due to changes in business conditions, operating performance and economic conditions.

During the reporting periods, the Company performed the evaluation and there was no impairment loss.

Cash and Concentration of Credit Risk

The Company maintains cash in bank deposit accounts in Hong Kong and PRC, and considers all highly liquid investments purchased with original maturities of six months or less to be cash equivalents. The Company performs ongoing evaluations of the institution to limit its concentration risk exposure.

The Company’s customers are mainly located in the northeastern China. Because of this, the Company is subject to regional risks, such as the economy, regional financial conditions and unemployment, weather conditions, power outages, and other natural disasters specific to the region in which the Company operates.

Retirement Benefit Plans

Full time employees of the Company in China participate in a government mandated defined contribution plan, pursuant to which certain pension benefits, medical care, employee housing fund and other welfare benefits are provided to employees. Chinese labor regulations require the Company to make contributions to the government for these benefits based on certain percentages of the employees’ salaries. The Company accounts the mandated defined contribution plan under the vested benefit obligations approach based on the guidance of ASC 715, Compensation—Retirement Benefits.

The total amounts for such employee benefits which were expensed were $

| 17 |

| Table of Contents |

SIXSIXGREEN VISION BIOTECHNOLOGY CORP. AND SUBSIDIARIES

NOTES TOUNAUDITEDCONSOLIDATEDFINANCIAL STATEMENTS

NOTE 2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (CONTINUED)

Income Taxes

The Company accounts for income tax using an asset and liability approach and allows for recognition of deferred tax benefits in future years. Under the asset and liability approach, deferred taxes are provided for the net tax effects of temporary differences between the carrying amounts of assets and liabilities for financial reporting purposes and the amounts used for income tax purposes. A valuation allowance is provided for deferred tax assets if it is more likely than not these items will either expire before the Company is able to realize their benefits, or that future realization is uncertain.

Segment Reporting

The Company operates in one industry segment, operating manufacturing and selling of organic bio-fertilizer. ASC 280, Segment Reporting, establishes standards for reporting information about operating segments. Given the economic characteristics of the similar nature of the products sold, the type of customer and the method of distribution, the Company operates as one reportable segment as defined by ASC 280, Segment Reporting.

Basic and diluted earnings (loss) per share

In accordance with ASC No. 260 “Earnings Per Share”, the basic earnings (loss) per common share is computed by dividing net earnings (loss) available to common stockholders by the weighted average number of common shares outstanding. Diluted earnings (loss) per common share is computed similarly to basic earnings (loss) per common share, except that the denominator is increased to include the number of additional common shares that would have been outstanding if the potential common shares had been issued and if the additional common shares were dilutive.

Recently Issued Accounting Guidance

In June 2016, the FASB issued ASU 2016-13, Financial Instruments-Credit Losses (Topic 326) – Measurement of Credit Losses on Financial Instruments (ASU 2016-13). The main objective of the standard is to provide financial statement users with more decision-useful information about the expected credit losses on financial instruments and other commitments to extend credit held by a reporting entity at each reporting date. In issuing this standard, the FASB is responding to criticism that today’s guidance delays recognition of credit losses. The standard will replace today’s “incurred loss” approach with an “expected loss” model. The new model, referred to as the current expected credit loss (“CECL”) model, will apply to: (1) financial assets subject to credit losses and measured at amortized cost, and (2) certain off-balance sheet credit exposures. The standard is applicable to loans, accounts receivable, trade receivables, and other financial assets measured at amortized cost, loan commitments and certain other off-balance sheet credit exposures, debt securities (including those held-to-maturity) and other financial assets measured at fair value through other comprehensive income, and beneficial interests in securitized financial assets. The CECL model does not apply to available-for-sale debt securities. For available-for-sale debt securities with unrealized losses, entities will measure credit losses in a manner similar to what they do today, except that the credit losses will be recognized as allowances rather than reductions in the amortized cost of the securities. Accordingly, the new methodology will be utilized when assessing the Company’s financial instruments for impairment. As a result, entities will recognize improvements to estimated credit losses immediately in earnings rather than as interest income over time, as they do today. The ASU also simplifies the accounting model for purchased credit-impaired debt securities and loans. ASU 2016-13 also expands the disclosure requirements regarding an entity’s assumptions, models, and methods for estimating the allowance for loan and lease losses. ASU 2016-13 is effective for years beginning after December 15, 2019, including interim periods within those fiscal years under a modified retrospective approach. Early adoption is permitted for the periods beginning after December 15, 2018. The Company adopted the guidance from July 1, 2020. The Company finalized its analysis and the adoption of this guidance has no material impact on the Company’s consolidated financial statements and its internal controls over financial reporting.

| 18 |

| Table of Contents |

GREEN VISION BIOTECHNOLOGY CORP.AND SUBSIDIARIES

NOTES TOUNAUDITEDCONSOLIDATEDFINANCIAL STATEMENTS

NOTE 2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (CONTINUED)

In August 2018, the FASB issued ASU 2018-13, Fair Value Measurement (Topic 820) – Disclosure Framework – Changes to the Disclosure Requirements for Fair Value Measurement (ASU 2018-13), which modifies the disclosure requirements on fair value measurements, including removing the requirement to disclose (1) the amount of and reasons for transfers between Level 1 and Level 2 of the fair value hierarchy, (2) the policy for timing of transfers between levels and (3) the valuation processes for Level 3 fair value measurements. ASU 2018-13 also added new disclosures including the requirement to disclose (a) the changes in unrealized gains and losses for the period included in other comprehensive income for recurring Level 3 fair value measurements held at the end of the reporting period and (b) the range and weighted average of significant unobservable inputs used to develop Level 3 fair value measurements. ASU 2018-13 is effective for fiscal years (and interim reporting periods within those years) beginning after December 15, 2019 and early adoption is permitted. This standard will only impact the disclosures pertaining to fair value measurements. The Company adopted the guidance from July 1, 2020. The Company finalized its analysis and the adoption of this guidance has no material impact on the Company’s consolidated financial statements and its internal controls over financial reporting.

In December 2019, the FASB issued ASU No. 2019-12, “Income Taxes” (Topic 740): Simplifying the Accounting for Income Taxes (“ASU 2019-12”). ASU 2019-12 will simplify the accounting for income taxes by removing certain exceptions to the general principles in Topic 740. The amendments also improve consistent application of and simplify GAAP for other areas of Topic 740 by clarifying and amending existing guidance. For public business entities, the amendments in this Update are effective for fiscal years, and interim periods within those fiscal years, beginning after December 15, 2020. For all other entities, the amendments are effective for fiscal years beginning after December 15, 2021, and interim periods within fiscal years beginning after December 15, 2022. The Company does not expect that the requirements of ASU 2019-12 will have a material impact on its consolidated financial statements.

NOTE 3. GOING CONCERN

As of June 30, 2022 and December 31, 2021, the Company has an accumulated deficit of $

Management has taken the following steps to revise its operating and financial requirements, which it believes are sufficient to provide the Company with the ability to continue as a going concern. The Company is actively pursuing (i) additional funding which would enhance capital employed; and (ii) strategic partners which would increase revenue bases or reduce operation expenses. Management believes that the above actions will allow the Company to continue its operations throughout this fiscal year.

| 19 |

| Table of Contents |

GREEN VISION BIOTECHNOLOGY CORP. AND SUBSIDIARIES

NOTES TOUNAUDITEDCONSOLIDATEDFINANCIAL STATEMENTS

NOTE 4. OTHER RECEIVABLES

Other receivables consisted of the following:

|

| June 30, 2022 |

|

| December 31, 2021 |

| ||

|

| (unaudited) |

|

| (audited) |

| ||

Deposits |

| $ |

|

| $ |

| ||

Prepaid expenses |

|

|

|

|

|

| ||

Advance to employee |

|

|

|

|

|

| ||

|

|

|

|

|

|

| ||

Less: Allowance for doubtful debts |

|

| ( | ) |

|

| ( | ) |

|

|

|

|

|

|

|

|

|

Total |

| $ |

|

| $ |

| ||

NOTE 5. PROPERTY, PLANT AND EQUIPMENT, NET

Property, plant and equipment consisted of the following:

|

| June 30, 2022 |

|

| December 31, 2021 |

| ||

|

| (unaudited) |

|

| (audited) |

| ||

Buildings |

| $ |

|

| $ |

| ||

Machinery & equipment |

|

|

|

|

|

| ||

Office equipment |

|

|

|

|

|

| ||

Motor vehicles |

|

|

|

|

|

| ||

|

|

|

|

|

|

|

|

|

Total property, plant and equipment |

|

|

|

|

|

| ||

Less: accumulated depreciation and impairment charges |

|

| ( | ) |

|

| ( | ) |

|

|

|

|

|

|

|

|

|

Total property, plant and equipment, net |

| $ |

|

| $ |

| ||

The depreciation expenses for the six months ended June 30, 2022 and 2021 were $

The depreciation expenses for the three months ended June 30, 2022 and 2021 were $

NOTE 6. INTANGIBLE ASSETS

Intangible assets consisted of the following:

| 20 |

| Table of Contents |

GREEN VISION BIOTECHNOLOGY CORP. AND SUBSIDIARIES

NOTES TO UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS

|

| June 30, 2022 |

|

| December 31, 2021 |

| ||

|

| (unaudited) |

|

| (audited) |

| ||

Land use rights |

| $ |

|

| $ |

| ||

Software system |

|

|

|

|

|

| ||

Less – accumulated amortization |

|

| ( | ) |

|

| ( | ) |

|

|

|

|

|

|

|

|

|

Total intangible assets, net |

| $ |

|

| $ |

| ||

The amortization expenses of land use rights and software systems for the six months ended June 30, 2022 and 2021 were $

The amortization expenses of land use rights and software systems for the three months ended June 30, 2022 and 2021 were $

Future amortization of land use rights and software systems is as follows:

Years ending December 31, |

| Amount |

| |

2022 |

| $ |

| |

2023 |

|

|

| |

2024 |

|

|

| |

2025 |

|

|

| |

2026 |

|

|

| |

Thereafter |

|

|

| |

|

|

|

|

|

Total |

| $ |

| |

NOTE 7. INVENTORIES

Inventories consisted of the following:

|

| June 30, 2022 |

|

| December 31, 2021 |

| ||

|

| (unaudited) |

|

| (audited) |

| ||

Raw material |

| $ |

|

| $ |

| ||

Finished goods |

|

|

|

|

|

| ||

Goods on consignment |

|

|

|

|

|

| ||

Less: Provision of inventory |

|

| ( | ) |

|

| ( | ) |

|

|

|

|

|

|

|

|

|

Inventories, net |

| $ |

|

| $ |

| ||

During the six months ended June 30, 2022 and 2021, the additional provision of inventory were $Nil and $Nil respectively.

During the six months ended June 30, 2022 and 2021, the reversal of provision for inventory were $

NOTE 8. CONCENTRATIONS OF CREDIT RISK AND MAJOR CUSTOMERS

Sales:

Customer |

| As at June 30, 2022 |

|

| As at December 31, 2021 |

| |||||||||

A |

| $ | - |

|

| - | % |

| $ |

|

|

| % | ||

B |

|

| - |

|

| - | % |

|

|

|

|

| % | ||

C |

|

| - |

|

| - | % |

|

|

|

|

| % | ||

D |

|

| - |

|

| - | % |

|

| - |

|

| - | % | |

E |

|

| - |

|

| - | % |

|

| - |

|

| - | % | |

Total |

| $ | - |

|

| - | % |