UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

_____________________________

FORM 10-K

_____________________________

For the fiscal year ended December 31 , 2020

or

For the transition period from to

Commission File Number: 001-38381

_____________________________

(Exact name of registrant as specified in its charter)

_____________________________

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification Number) | |||||||

( (Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices) | ||||||||

_____________________________

| Securities registered pursuant to Section 12(b) of the Act: | ||||||||

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||||||

| Securities registered pursuant to Section 12(g) of the Act: | ||||||||

| None | ||||||||

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐ No ☒

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ☐ | Accelerated filer | ☐ | ||||||||

| ☒ | Smaller reporting company | ||||||||||

| Emerging growth company | |||||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards pursuant to Section 13(a) of the Exchange Act. ☒

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. Yes ☐ No ☒

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ☐ No ☒

The aggregate market value of the registrant’s common stock held by non-affiliates of the registrant as of the last business day of the registrant’s most recently completed second fiscal quarter was approximately $120.0 million, based on the closing price of the registrant’s common stock on the Nasdaq Global Market of $5.30 per share for such date.

As of March 25, 2021, 43,733,316 shares of the registrant’s sole class of common stock were outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

EVOLUS, INC. | ||||||||

TABLE OF CONTENTS | ||||||||

| Page | ||||||||

| PART I | ||||||||

| Item 1 | ||||||||

| Item 1A | ||||||||

| Item 1B | ||||||||

| Item 2 | ||||||||

| Item 3 | ||||||||

| Item 4 | ||||||||

| PART II | ||||||||

| Item 5 | ||||||||

| Item 6 | ||||||||

| Item 7 | ||||||||

| Item 7A | ||||||||

| Item 8 | ||||||||

| Item 9 | ||||||||

| Item 9A | ||||||||

| Item 9B | ||||||||

| PART III | ||||||||

| Item 10 | ||||||||

| Item 11 | ||||||||

| Item 12 | ||||||||

| Item 13 | ||||||||

| Item 14 | ||||||||

| PART IV | ||||||||

| Item 15 | ||||||||

| Item 16 | ||||||||

i

Special Note Regarding Forward-Looking Statements

This Annual Report on Form 10-K, or Annual Report, contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, or the Securities Act, and Section 21E of the Securities Exchange Act of 1934, as amended, or the Exchange Act, that involve risks and uncertainties, including statements based on our current expectations, assumptions, estimates and projections about future events, our business, financial condition, results of operations and prospects, our industry and the regulatory environment in which we operate. Any statements contained herein that are not statements of historical facts may be deemed to be forward-looking statements. In some cases, you can identify forward-looking statements by terms such as “anticipate,” “believe,” “could,” “estimate,” “expect,” “intend,” “may,” “plan,” “potential,” “predict,” “project,” “should,” “will,” “would” or the negative of those terms, or other comparable terms intended to identify statements about the future. The forward-looking statements included herein are subject to risks and uncertainties that could cause actual results to differ materially from those expressed in the forward-looking statements. These risks and uncertainties, all of which are difficult or impossible to predict accurately and many of which are beyond our control, include, but are not limited to, those made below under “Summary of Risk Factors” and in Item 1A Risk Factors in this Annual Report.

You should carefully consider these risks, as well as the additional risks described in other documents we file with the SEC in the future, including subsequent Annual Reports on Form 10-K and Quarterly Reports on Form 10-Q, which may from time to time amend, supplement or supersede the risks and uncertainties we disclose. We also operate in a very competitive and rapidly changing environment. New risks emerge from time to time and it is not possible for our management to predict all risks, nor can we assess the impact of all factors on our business or the extent to which any factor, or combination of factors, may cause actual results to differ materially from those contained in, or implied by, any forward-looking statements.

The forward-looking statements included herein are based on current expectations of our management based on available information and are believed to be reasonable. In light of the significant risks and uncertainties inherent in the forward-looking statements included herein, the inclusion of such information should not be regarded as a representation by us or any other person that such results will be achieved, and readers are cautioned not to place undue reliance on such forward-looking statements, which speak only as of the date hereof. Except as required by law, we undertake no obligation to revise the forward-looking statements contained herein to reflect events or circumstances after the date hereof or to reflect the occurrence of unanticipated events. You should read this Annual Report on Form 10-K and the other documents we file with the SEC with the understanding that our actual future results, levels of activity, performance and achievements may be materially different from what we expect. We qualify all of our forward-looking statements by the cautionary statements referenced above.

Summary of Risk Factors

An investment in our securities involves various risks and you are urged to carefully consider the risks discussed under Item 1A “Risk Factors,” in this Annual Report on Form 10-K prior to making an investment in our securities. If any of the risks below or in Item 1A “Risk Factors” occurs, our business could be materially and adversely affected. As more fully described in Item 1A “Risk Factors”, the principal risks and uncertainties that may affect our business, financial condition and results of operations include, but are not limited to, the following:

•We will require additional financing to fund our future operations, and a failure to obtain additional capital when so needed on acceptable terms, or at all, could force us to delay, limit, reduce or terminate our operations and as a result, there is substantial doubt about our ability to continue as a going concern.

•We currently depend entirely on the successful commercialization of our only product, Jeuveau®. If we are unable to successfully commercialize Jeuveau®, we may never generate sufficient revenue to continue our business.

•We have a limited operating history and have incurred significant losses since our inception and anticipate that we will continue to incur losses for the foreseeable future. We have only one product and limited commercial sales, which, together with our limited operating history, make it difficult to assess our future viability.

•If we or our counterparties do not comply with the terms of our settlement agreements with Medytox, Inc., or Medytox, and Allergan Limited, Allergan, Inc. and Allergan Pharmaceuticals Ireland, or, collectively, Allergan, we may face litigation or lose our ability to commercialize Jeuveau® which would materially and adversely affect our ability to carry out our business, and our financial condition and ability to continue as a going concern.

1

•The terms of the Medytox/Allergan Settlement Agreements with Medytox and Allergan will reduce our profitability and may affect the extent of any discounts we may offer to our customers.

•Our business, financial condition and operations may be materially adversely affected by the COVID-19 outbreak or other similar outbreaks.

•We rely on the license and supply agreement, as amended, with Daewoong, which we refer to as the Daewoong Agreement, to provide us exclusive rights to distribute Jeuveau® in certain territories. Any termination or loss of significant rights, including exclusivity, under the Daewoong Agreement would materially and adversely affect our development or commercialization of Jeuveau®.

•Our failure to successfully in-license, acquire, develop and market additional product candidates or approved products would impair our ability to grow our business.

•Jeuveau® faces, and any of our future product candidates will face, significant competition and our failure to effectively compete may prevent us from achieving significant market penetration and expansion.

•Jeuveau® may fail to achieve the broad degree of physician adoption and use or consumer demand necessary for commercial success.

•Our ability to market Jeuveau® is limited to use for the treatment of glabellar lines, and if we want to expand the indications for which we market Jeuveau®, we will need to obtain additional regulatory approvals, which will be expensive and may not be granted.

•Third party claims of intellectual property infringement may prevent or delay our commercialization efforts and interrupt our supply of products.

•If we or any of our current or future licensors, including Daewoong, are unable to maintain, obtain or protect intellectual property rights related to Jeuveau® or any of our future product candidates, we may not be able to compete effectively in our market.

•We may need to increase the size of our organization, including our sales and marketing capabilities in order to further commercialize Jeuveau® and we may experience difficulties in managing this growth.

•We rely on our digital technology and applications and our business and operations would suffer in the event of system failures or breach by hackers.

•We are subject to extensive government regulation, and we may face delays in or not obtain regulatory approval of our product candidates and our compliance with ongoing regulatory requirements may result in significant additional expense, limit or delay regulatory approval or subject us to penalties if we fail to comply.

Unless the context indicates otherwise, as used in this Annual Report on Form 10-K, the terms “Evolus,” “company,” “we,” “us” and “our” refer to Evolus, Inc., a Delaware corporation, and our subsidiaries taken as a whole, unless otherwise noted.

EVOLUS™, Jeuveau®, Evolux™ are three of our trademarks that are used in this Annual Report on Form 10-K. Jeuveau® is the trade name in the United States for our approved product with non-proprietary name, prabotulinumtoxinA-xvfs. The product has different trade names outside of the United States, but is referred to throughout this Annual Report on Form 10-K as Jeuveau®. This Annual Report on Form 10-K also includes trademarks, trade names and service marks that are the property of other organizations, such as BOTOX® and BOTOX® Cosmetic, which we refer to throughout this Annual Report on Form 10-K as BOTOX. Solely for convenience, trademarks and trade names referred to in this Annual Report on Form 10-K may appear without the ® and ™ symbols, but those references are not intended to indicate that we will not assert, to the fullest extent under applicable law, our rights, or that the applicable owner will not assert its rights, to these trademarks and trade names. We do not intend our use or display of other companies’ trade names or trademarks to imply a relationship with, or endorsement or sponsorship of us by, any other companies.

2

Part I

Item 1. Business.

Overview

We are a performance beauty company with a customer-centric approach focused on delivering breakthrough products in the self-pay aesthetic market.

Our first commercial product is Jeuveau®, which is a proprietary 900 kilodalton, or kDa, purified botulinum toxin type A formulation indicated for the temporary improvement in the appearance of moderate to severe glabellar lines, also known as “frown lines,” in adults. Our primary market is the self-pay aesthetic market, which includes medical products purchased by physicians and other customers that are then sold to consumers or used in procedures for aesthetic indications that are not reimbursed by any third-party payor, such as Medicaid, Medicare or commercial insurance. We believe we offer customers and consumers a compelling value proposition with Jeuveau®. Currently, BOTOX (onabotulinumtoxinA) is the neurotoxin market leader, and prior to the approval of Jeuveau®, was the only known 900 kDa botulinum toxin type A complex approved in the United States. We believe aesthetic physicians generally prefer the performance characteristics of the complete 900 kDa neurotoxin complex and are accustomed to injecting this formulation.

United States

In February 2019, we received the approval of our first product Jeuveau® (prabotulinumtoxinA-xvfs) from the U.S. Food and Drug Administration, or FDA. In May 2019, we commercially launched Jeuveau® in the United States, and our net sales totaled $56.5 million for fiscal year 2020 and $20.6 million for the fourth quarter of 2020.

International

In August 2018, we received approval from Health Canada for the temporary improvement in the appearance of moderate to severe glabellar lines in adult patients under 65 years of age. We began marketing Jeuveau® in Canada in October 2019 through our distribution partner, Clarion Medical Technologies, Inc., or Clarion.

In September 2019, we received approval from the European Commission, to market Jeuveau® in all 28 EU member states, Iceland, Norway and Liechtenstein. In January 2021, we received a positive decision from the European Commission, to add the 50 unit product to the existing approval obtained in September 2019. We plan to launch Jeuveau® in Europe in early 2022.

Our Market

Our primary market is self-pay aesthetic healthcare, which includes medical products purchased by physicians that are then sold to consumers or used in procedures for aesthetic indications that are not reimbursed by any third-party payor, such as Medicaid, Medicare or commercial insurance. By focusing on the self-pay medical aesthetics market, we believe we are not exposed to reimbursement risk associated with a reliance on payments from such third-party payors, and we are subject to fewer regulations that place limits on the types of marketing and other interactions we have with physicians.

Within the self-pay aesthetic market, the global aesthetic neurotoxin market was estimated to generate approximately $2.5 billion of revenue in 2020 and is estimated to grow to approximately $3.8 billion in 2023. The U.S. aesthetic neurotoxin market was estimated to generate $1.3 billion in sales in 2020 and is expected to grow to approximately $2.1 billion in 2023.

We believe the growth in the medical aesthetics market is driven by a number of factors, including:

•increased use by millennials who are increasingly seeking medical aesthetic treatments and utilizing neurotoxins as an entry point for aesthetic procedures due to their minimally invasive nature;

•an aging population together with an increasing life expectancy, which is resulting in more consumers with a desire for improved appearance and well-being over a longer period of time;

•rising disposable income, with the U.S. Bureau of Economic Analysis reporting that real disposable income in the United States increased approximately 21% from December 2012 to December 2020;

•growing awareness, utilization and acceptance of elective or minimally invasive aesthetic procedures; and

3

•continued innovation and improved accessibility to these treatments due to an increase in the number of physicians who perform these procedures.

Within the multiple age groups that receive aesthetic neurotoxin treatments, we strategically focus our marketing efforts on the millennial segment which is the largest cohort in the U.S. population. In 2019 there were estimated to be approximately 73 million millennials, defined as individuals born between 1981 and 1996. We believe that approximately 1.7 million females between the age of 30 and 39, which includes many individuals we define as millennials, are considering neurotoxins in the next twelve months.

Our Competitive Strengths

We offer physicians and consumers a compelling value proposition because:

•Jeuveau® offers the U.S. market the first known 900 kDa neurotoxin alternative to BOTOX. The manufacture of both Jeuveau® and BOTOX starts with a 900 kDa complex, includes adding the excipients human serum albumin, or HSA, and sodium chloride, and finishes by vacuum drying. We believe Jeuveau® is the only known neurotoxin product in the United States with a 900 kDa neurotoxin complex other than BOTOX. We also believe an important component of competitiveness in the neurotoxin market relates to the characteristics associated with the 900 kDa complex and the potential of the accessory proteins to increase the effectiveness of the active toxin portion of the complex.

•Results from our TRANSPARENCY global clinical program in more than 2,100 patients provides robust data to physicians evaluating the purchase of Jeuveau®. We believe the comprehensive TRANSPARENCY clinical data set, including a head-to-head Phase III study comparing Jeuveau® and BOTOX, provides physicians with confidence in recommending Jeuveau® to their patients.

•We offer a unique technology platform. We provide a simple, personal and connected experience for physicians utilizing our proprietary technology platform. We have built and continue to improve our platform with the goal of limiting friction and enhancing the overall experience for physicians and ultimately consumers. We are modernizing the customer engagement with our proprietary “Evolus Practice” app. We not only leverage technology for operational efficiency, but more importantly, to enhance a customer’s experience. The combination of a highly specialized sales force and our technology platform is an effective and competitive model.

•Enhanced level of physician-customer interaction through a self-pay, aesthetic-only marketing strategy. We have elected to specifically target the self-pay aesthetic market. With a reduced regulatory burden compared to third-party payor reimbursed therapeutic products, there is a number of benefits that market participants in reimbursed markets are unable to achieve, such as an enhanced level of interaction with our physician-customers. Jeuveau® is the only U.S. neurotoxin without a therapeutic indication. We believe pursuing an aesthetic-only non-reimbursed product strategy creates meaningful strategic advantages in the United States, including pricing and marketing flexibility. We utilize this flexibility to drive market adoption through programs such as promotional events, experience product programs and pricing strategies.

•We have strong relationships with aesthetic key opinion leaders, or KOLs. We have established relationships with aesthetic KOLs as a result of our management team’s industry experience and engagement of our clinical trial investigators. KOLs are important information resources to the general physician-customer market due to their clinical expertise, academic reputations, active clinical practices and their status as medical innovators. The broader physician community often looks to KOLs for their experience with products and procedures as part of their new product and procedure adoption process.

•Our management team has significant experience and expertise in medical aesthetics. Our management team has extensive experience in self-pay healthcare markets, in the development, market launch and commercialization of major medical products, execution and integration of business development transactions, identification of and partnerships with KOLs, and understanding of the regulatory environment of the healthcare markets. Key members of our leadership team have also served in relevant senior leadership positions with leading aesthetic companies.

Our Strategy

In May 2019, we launched Jeuveau® in the United States with our own specialty sales organization now consisting of over 70 positions between representatives, management and other sales employees and in Canada through our distribution partner,

4

Clarion. We plan to expand our product offerings over time through in-licensing, partnerships and acquisitions and by launching our products internationally. The key components of our strategy are:

•Pursue an aesthetic-only strategy to enhance marketing and pricing flexibility along with improving transparency for our customers.

•Leverage our strong KOL relationships to assist in scientific presentations, publications, and other methods to drive success of our commercial launch of Jeuveau®.

•Launch directly or partner outside of the United States to reach and serve physicians and consumers in those territories.

•Leverage our differentiated digital platform to efficiently open new accounts, personalize the purchasing process and efficiently deploy marketing programs at scale.

•Establish a leading medical aesthetics company with a diversified product offering by in-licensing technology, developing partnerships and potentially acquiring products.

Final Ruling by the U.S. International Trade Commission and the Subsequent Settlement Agreements

On January 30, 2019, Allergan, plc (now Allergan Limited) and Allergan, Inc., who we refer to collectively as Allergan, and Medytox, Inc., or Medytox, filed a complaint against us and Daewoong Pharmaceuticals Co., Ltd., or Daewoong in the International Trade Commission, or ITC, alleging that Jeuveau® is manufactured based on misappropriated trade secrets of Medytox and therefore the importation of Jeuveau® is an unfair act. The ITC matter, which we refer to as the ITC Action, is entitled In the Matter of Certain Botulinum Toxin Products. The ITC instituted an investigation as ITC Inv. No. 337-TA-1145.

On December 16, 2020, the ITC issued a final determination in the ITC Action and issued (1) a limited exclusion order prohibiting the importation of Jeuveau® into the United States for a period of 21 months and (2) a cease and desist order preventing the Company from, among other things, selling, marketing, or promoting such imported Jeuveau® in the United States for a period of 21 months. We refer to the limited exclusion order and the cease and desist order collectively as the remedial orders. The Final Determination was subject to a 60-day presidential review period before taking effect. During the presidential review period, the Company was permitted to continue importation and sales of Jeuveau® subject to payment of a bond of $441 per vial.

Effective February 18, 2021, we entered into a Settlement and License Agreement with Medytox and Allergan, which we refer to as the U.S. Settlement Agreement and another Settlement and License Agreement with Medytox, which we refer to as the ROW Settlement Agreement. We refer to the U.S. Settlement Agreement and the ROW Settlement Agreement collectively as the Medytox/Allergan Settlement Agreements.

Under the Medytox/Allergan Settlement Agreements, we obtained (i) a license to commercialize, manufacture and to have manufactured for us certain products identified in the Medytox/Allergan Settlement Agreements, including Jeuveau® (the “Licensed Products”) in the United States and other territories where we license Jeuveau®, (ii) the dismissal of outstanding litigation against us, including the ITC Action, a rescission of the related remedial orders, and the dismissal of a civil case in the Superior Court of California against us, which we refer to together with any claims (including claims brought in Korean courts) with a common nexus of fact as the Medytox/Allergan Actions, and (iii) releases of claims against us for the Medytox/Allergan Actions. In exchange, we agreed to (i) make cash payments of $35.0 million in multiple payments over two years to Allergan and Medytox, (ii) pay to Allergan and Medytox certain royalties on the sale of Jeuveau®, based on a certain dollar amount per vial sold of Licensed Product by or on our behalf in the United States, from December 16, 2020 to September 16, 2022, (iii) from December 16, 2020 to September 16, 2022, pay to Medytox a low-double digit royalty on net sales of Jeuveau® sold by us or on our behalf in territories we have licensed outside the United States; (iv) from September 16, 2022 to September 16, 2032, pay to Medytox a mid-single digit royalty percentage on net sales of Jeuveau® in the United States and all territories we have licensed outside the United States, (v) issue to Medytox of 6,762,652 shares of our common stock, par value $0.00001 per share, which we issued on February 18, 2021, and (vi) enter into a Registration Rights Agreement pursuant to which we granted certain registration rights to Medytox with respect to such shares of common stock

5

beginning as of March 31, 2022. In addition, under the Medytox/Allergan Settlement Agreements, we made certain representations and warranties and agreed to positive and negative covenants.

On March 23, 2021, we entered into a Confidential Settlement and Release Agreement with Daewoong Pharmaceuticals Co. Ltd., or Daewoong, which we refer to as the Daewoong Settlement Agreement, a Convertible Promissory Note Conversion Agreement, which we refer to as the Conversion Agreement and the Third Amendment to the Supply Agreement (which amends the Daewoong Agreement), which we refer to as the Daewoong Agreement Amendment. We refer to the Daewoong Settlement Agreement, the Conversion Agreement and the Daewoong Agreement Amendment collectively as the 2021 Daewoong Arrangement.

Under the 2021 Daewoong Arrangement, (i) Daewoong agreed to (a) pay us an amount equal to $25.5 million, (b) pay certain reasonable legal fees incurred by our litigation counsel in connection with its defense of the ITC Action (including any appeal of the resulting remedial orders), (c) cancel up to $10.5 million in aggregate milestone payments under our Daewoong Agreement, and (d) reimburse us certain amounts (calculated on a dollar amount per vials sold basis in the United States) for sales of certain products with respect to which we are required to pay Medytox and Allergan royalties pursuant to the U.S. Settlement Agreement; and (ii) we agreed to (y) release certain claims we may have against Daewoong or certain of its affiliates and representatives related to the allegations made in or the subject matter of the Medytox/Allergan Actions, or any orders, remedies and losses resulting from the Medytox/Allergan Actions, and (z) coordinate with Daewoong on certain matters related to the Medytox/Allergan Actions. In the Conversion Agreement, among other things, the parties agreed that (i) the principal balance of the $40.0 million aggregate principal amount convertible promissory note we issued to Daewoong on July 30, 2020, which we refer to as the Daewoong Convertible Note, and accrued and unpaid interest thereon shall be automatically converted, at the conversion price of $13.00 per share, into 3,136,869 shares of our common stock; and (ii) the Daewoong Convertible Note shall be deemed cancelled and satisfied in full in connection with such conversion.

Under the Daewoong Agreement Amendment, the parties agreed to amend the Daewoong Agreement to: (i) expand the territory within which we may distribute Jeuveau® to certain countries in Europe; (ii) reduce the period of time with respect to which we are required to deliver binding forecasts to Daewoong; (iii) introduce certain limitations on Daewoong’s ability to convert our exclusive license for certain territories to a non-exclusive license in the event we fail to meet certain minimum purchase requirements for such territory; (iv) adjust the minimum purchase requirements and reduce the transfer price per vial of Jeuveau® applicable to various territories; (v) require that any Jeuveau® supplied by Daewoong match certain shelf-life thresholds; and (vi) prohibit us from sharing certain confidential information regarding Daewoong with Medytox or its affiliates or representatives.

For additional information on the final ruling by the ITC and the subsequent Settlement Agreements, see “Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations— Impact on Our Business of Final Ruling by the U.S. International Trade Commission and the Subsequent Settlement.”

Jeuveau® Overview

Jeuveau® is an injectable formulation of a 900 kDa botulinum toxin type A complex designed to address the needs of the large and growing facial aesthetics market. We completed the TRANSPARENCY global clinical program which enrolled over 2,100 adult subjects. The results of the TRANSPARENCY global clinical program were used to support our applications for regulatory approvals in the United States, EU and Canada.

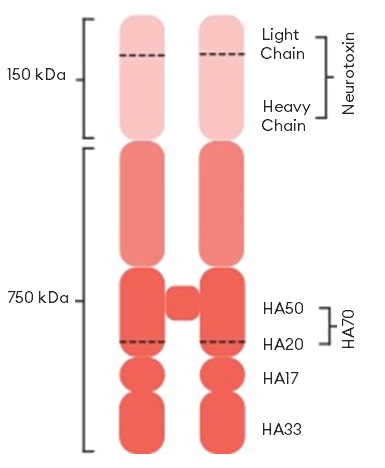

As demonstrated in the figure below, Jeuveau® contains a 900 kDa botulinum toxin type A complex produced by the bacterium Clostridium botulinum. The active part of the neurotoxin is the 150 kDa component, and the remaining 750 kDA of the complex is made up of accessory proteins that we believe help with the function of the active portion of the toxin. Jeuveau® has the same mechanism of action as other type A botulinum toxins. When injected intramuscularly at therapeutic doses, botulinum toxin causes a chemical denervation of the muscle resulting in localized reduction of muscle activity. Botulinum toxin type A specifically blocks peripheral acetylcholine release at presynaptic cholinergic nerve terminals by cleaving SNAP-25, a protein integral to the successful docking and release of acetylcholine from vesicles situated within the nerve endings leading to denervation and relaxation of the muscle.

6

Diagram of Botulinum Toxin Type A

TRANSPARENCY: Evolus Clinical Development for Glabellar Lines

TRANSPARENCY was a comprehensive five-study clinical development program for Jeuveau® and was used to meet the regulatory requirements for a Biologics License Application, or BLA, in the United States, a Marketing Authorisation Application, or MAA, in the EU, and a New Drug Submission, or NDS, in Canada, for the treatment of moderate to severe glabellar lines. The TRANSPARENCY program, which was developed in consultation with the FDA, Canadian, and European regulatory bodies, included three multicenter, randomized, double-blinded, controlled, single dose Phase III studies titled EV-001, EV-002 and EVB-003. Each Phase III study lasted 150 days. The TRANSPARENCY program also included two open label, multiple dose, long-term Phase II studies titled EV-004 and EV-006, each lasting one year. Between September 2014 and August 2016, over 2,100 adult male and female subjects with moderate to severe glabellar lines at maximum frown participated in this program.

In our clinical trials, subjects received intramuscular injections in five target sites in muscles that contribute to the formation of glabellar lines: the midline of the procerus, the inferomedial aspect of each corrugator, and the superior middle aspect of each corrugator. Each of the five target sites was injected with 0.1 milliliters, or mL, for a total of 0.5mL. Subjects assigned (in the open label studies) or randomized (in the controlled studies) to Jeuveau® received a total of 20 units per treatment, administered as 4 units per 0.1mL and those subjects who were randomized to the placebo group received 0.5mL saline. In our EVB-003 Phase III trial, the only study of the five with both a placebo and active control arm, subjects randomized to the active control received a total of 20 units of BOTOX administered as 4 units per 0.1mL.

All five studies contributed data to the evaluation of efficacy and safety of Jeuveau®.

Phase III U.S. Based Clinical Trials. The two identical U.S. Phase III studies, EV-001 and EV-002, enrolled subjects who were selected from a population of healthy adults, at least 18 years of age, who had moderate to severe glabellar lines at maximum frown, as independently assessed by the investigator and subject using the 4-point photonumeric Glabellar Line Scale, or GLS, where 0=no lines, 1=mild lines, 2=moderate lines and 3=severe lines. On Day 0, eligible subjects were randomly assigned in a 3:1 ratio to receive a single treatment of either Jeuveau® or placebo. Subjects were followed for 150 days after treatment.

The primary efficacy endpoint was defined as the proportion of subjects classified as responders on Day 30. This was a composite endpoint in which a responder was a subject with a 2 point improvement or greater on the GLS from Day 0 to Day 30 at maximum frown, only if independently agreed by both investigator and subject assessment.

Both studies met the primary endpoint of superiority over placebo. The percentages of responders in the intent to treat population for the composite primary endpoint, a two point or greater score composite improvement, in each of the two controlled single dose studies were:

•EV-001: 1.2% placebo, 67.5% Jeuveau®, with an absolute difference between the groups of 66.3%, 95% CI (59.0, 72.4)

7

•EV-002: 1.3% placebo, 70.4% Jeuveau®, with an absolute difference between the groups of 69.1%, 95% CI (61.5, 75.1)

In the EV-002 study, the adverse event, or AE, rate was 26.9% in the placebo group and 28.5% in the Jeuveau® group. Placebo and Jeuveau® groups were similar in the overall incidence of subjects who experienced one or more AEs. Four Jeuveau® subjects (4/246, 1.6%) experienced a serious adverse event, or SAE, but none were assessed as study drug related. Placebo and Jeuveau® groups were also similar in the percentages of subjects who experienced an AE assessed by the investigator as study drug related: 7.7% of placebo subjects and 9.8% of Jeuveau® subjects. The drug related eyelid and eyebrow ptosis rates in the Jeuveau® arm were 1.2% and 0.4% respectively. Overall, AEs with an incidence of 1% or greater were headache at 9.3% in the Jeuveau® groups and 7.6% in the placebo groups and eyelid ptosis at 1% in the Jeuveau® groups and 0% in the placebo groups.

Phase III European and Canadian Clinical Trial for Glabellar Lines

The EVB-003 study was the third Phase III safety and efficacy study in the Jeuveau® clinical development program, and was conducted in Europe and Canada. 540 subjects with moderate to severe glabellar lines, or a GLS score of 2 or 3, as assessed by the investigator, were eligible to be enrolled provided that subjects also felt their glabellar lines had an important psychological impact, such as on their mood, anxiety or depressive symptoms. On Day 0, eligible subjects were randomly assigned in a 5:5:1 ratio to receive a single treatment of 20 units of Jeuveau®, 20 units of BOTOX or placebo.

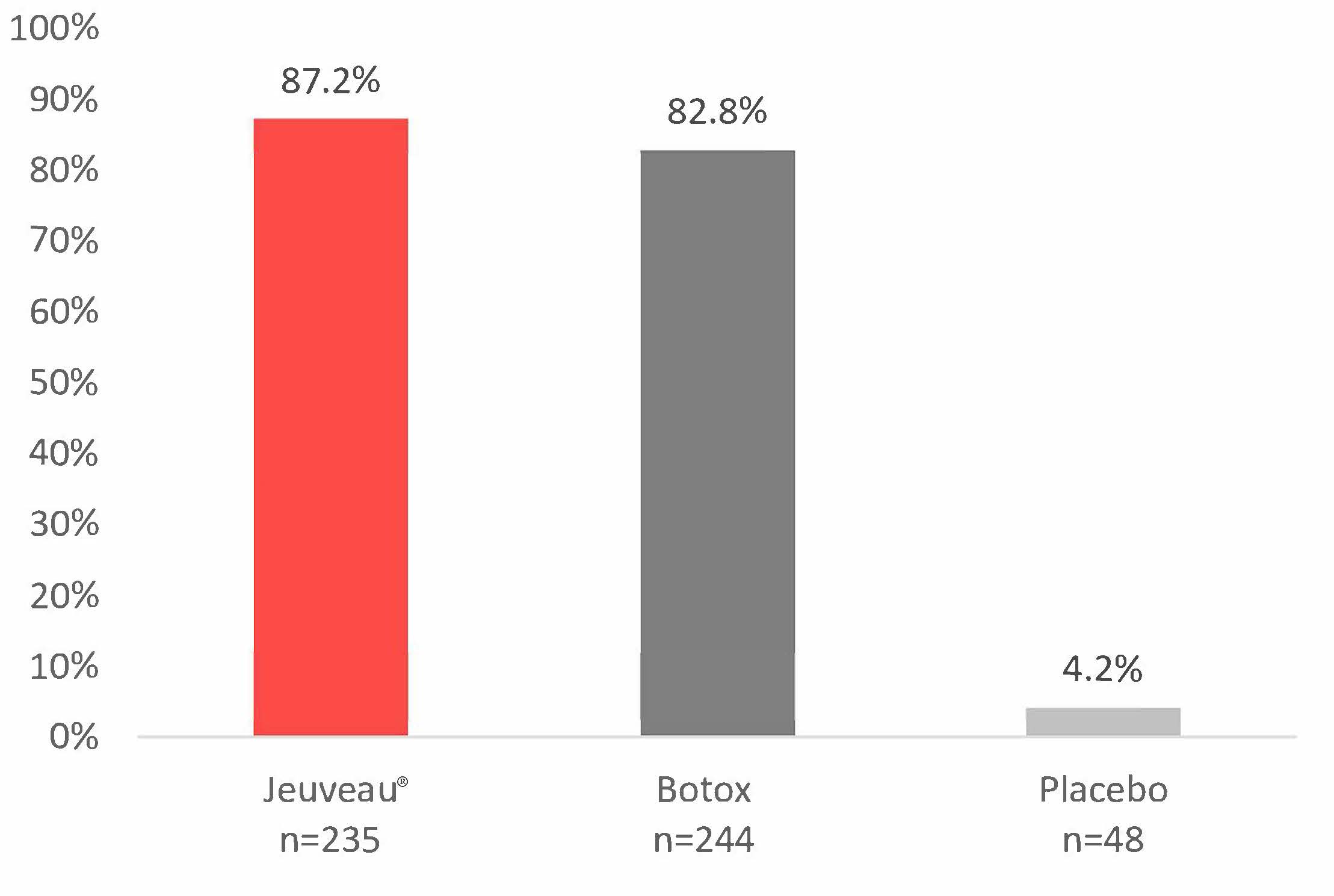

The primary efficacy endpoint was defined as the proportion of subjects classified as responders on Day 30. A responder was a subject with a GLS score of 0 or 1, as assessed by the investigator at maximum frown. The primary analysis of the primary efficacy endpoint in the EVB-003 study showed the superiority of Jeuveau® over placebo, and established non-inferiority of Jeuveau® to BOTOX. The percentages of responders for the primary efficacy endpoint were:

•4.2% in the placebo group, 95% CI (0.0, 9.8);

•82.8% in the BOTOX group, 95% CI (78.1, 87.5); and

•87.2% in the Jeuveau® group, 95% CI (83.0, 91.5).

A confidence interval, or CI, is a range of values in which, statistically, there is a specified level of confidence where the result lies. As an example, in the results above for this Phase III study, the results indicate that there is a 95% level of confidence that the responder rate for placebo was between 0.0% and 9.8%, which we express as: 95% CI (0.0, 9.8).

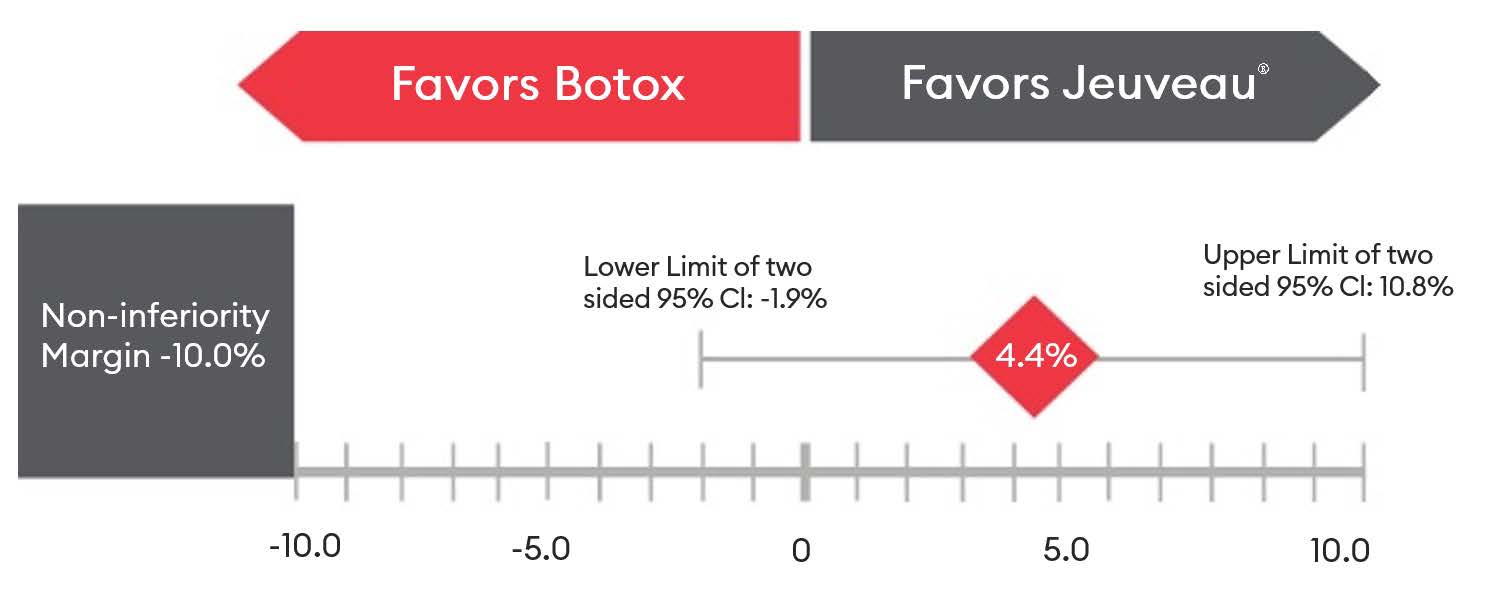

The absolute differences between the treatment groups were:

•83.1% between Jeuveau® and placebo groups, 95% CI (70.3, 89.4), (p<0.001), indicating Jeuveau® was superior to placebo; and

•4.4% between Jeuveau® and BOTOX groups, 95% CI (-1.9, 10.8), with non‑inferiority of Jeuveau® versus BOTOX concluded based on the lower bound of the 95% CI for the absolute difference exceeding -10.0%.

| EU Phase III Primary Endpoint - Responder Rates at Maximum Frown on Day 30 (GLS = 0 or 1) by Investigator Assessment | EU Phase III Primary Endpoint - Non-Inferiority, at Maximum Frown on Day 30 by Investigator Assessment | |||||||

|  | |||||||

8

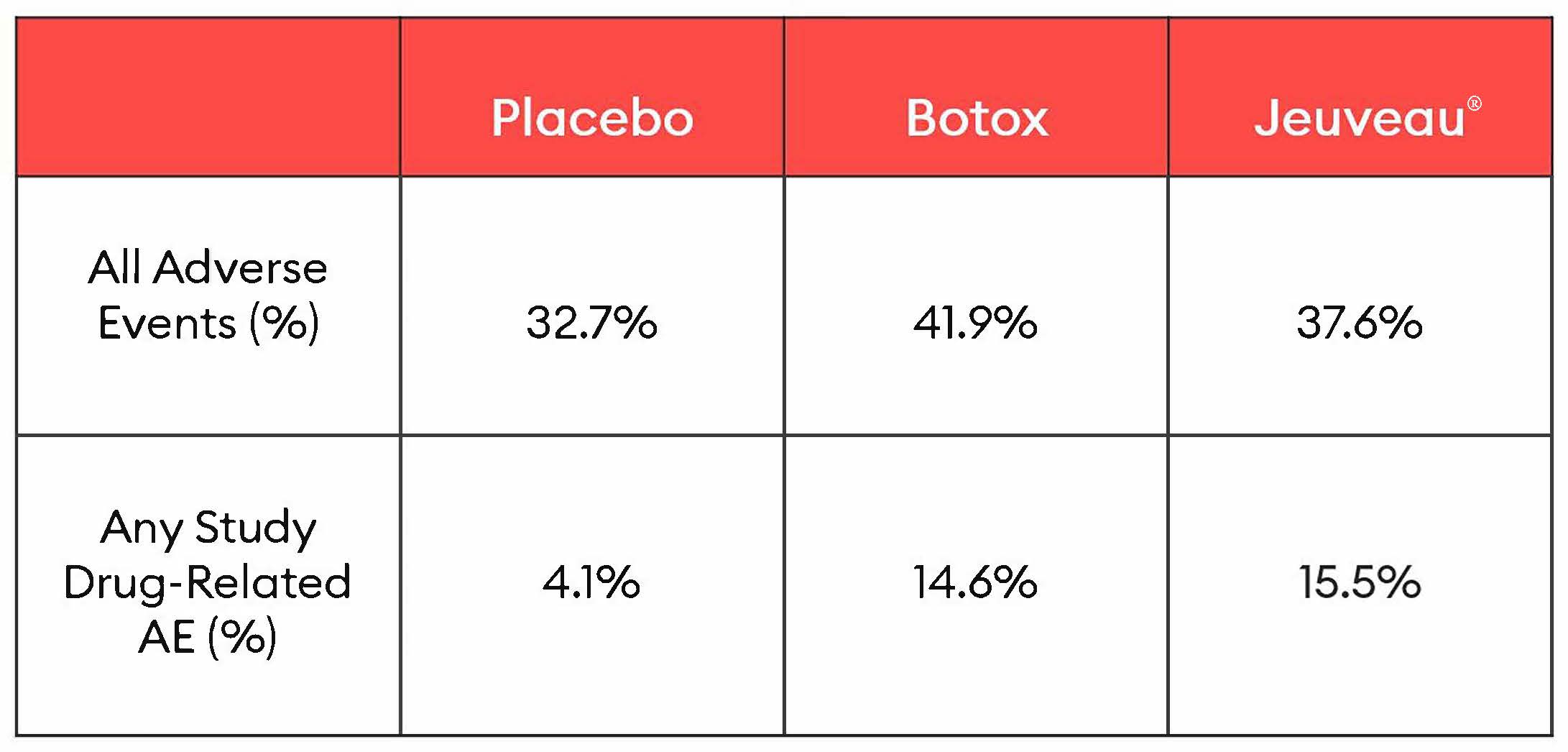

As presented in the table below, within each group, 32.7% of placebo subjects, 41.9% of BOTOX subjects and 37.6% of Jeuveau® subjects experienced AEs. One placebo subject (1/49, 2.0%), one BOTOX subject (1/246, 0.4%) and three Jeuveau® subjects (3/245, 1.2%) experienced a total of 11 SAEs and none were assessed as study drug related. The drug related eyelid ptosis rates were 1.6% in the Jeuveau® arm and 0% in the BOTOX arm and the eyebrow ptosis rates were 0% in the Jeuveau® arm and 0.4% in the BOTOX arm.

EU and Canadian Phase III Trial - Adverse Event Rate Summary

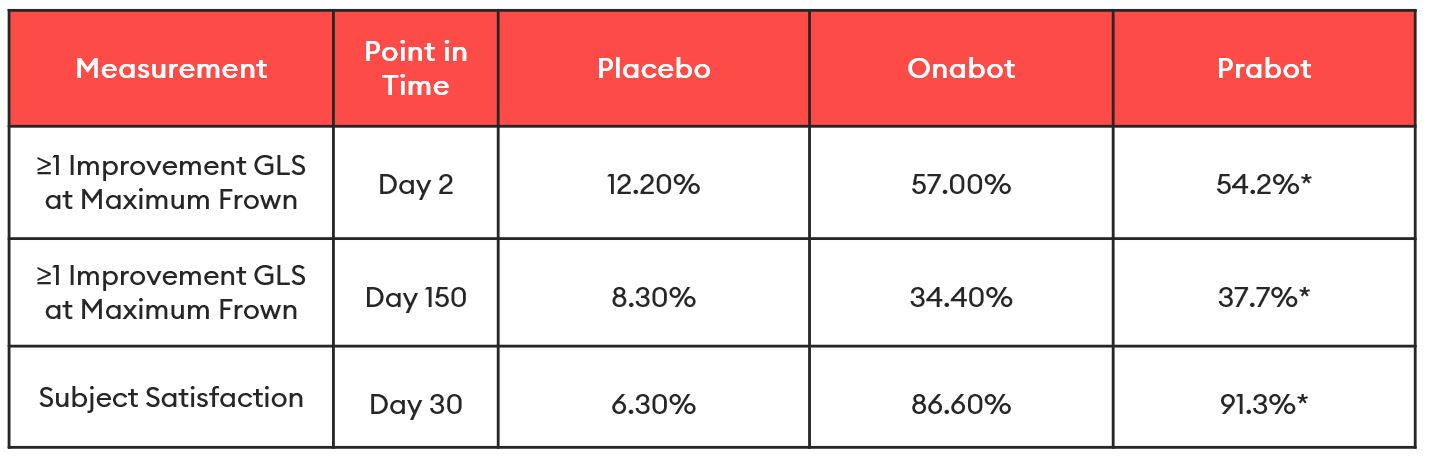

As presented in the table below, in EVB-003, we also assessed as a secondary endpoint ≥ 1 point improvement GLS at maximum frown for both investigator and patient satisfaction. The investigator assessment at Day 2, the beginning of the study, and at Day 150, at the end of the study, Jeuveau® is statistically superior to placebo as measured by a one-point improvement on the GLS scale by investigator assessment. We also looked at subject satisfaction on Day 30, and Jeuveau® was superior to placebo at 91% versus 6% in the placebo arm.

EU and Canadian Phase III Trial - Select Secondary Endpoints

| ||

*P-Value Placebo vs Jeuveau® <0.001 | ||

Manufacturing

Daewoong Pharmaceuticals Co. Ltd., or Daewoong, manufactures and supplies Jeuveau® to us. Daewoong has over 70 years of experience manufacturing pharmaceutical products and is one of the largest pharmaceutical companies in South Korea. Daewoong constructed a facility in South Korea where Jeuveau® is produced. We believe this facility will be sufficient to meet demand for Jeuveau® for the foreseeable future. The FDA conducted a current Good Manufacturing Practice, or cGMP, and pre-approval inspection of the facility in November 2017 in connection with our BLA for Jeuveau®. The UK Medicines and Healthcare Products Regulatory Agency, or MHRA, also completed an inspection of the manufacturing facility in February 2018 in connection with our MAA. The U.S. FDA approval of Jeuveau® in February 2019 included approval to manufacture Jeuveau® at Daewoong’s facility.

9

Daewoong License and Supply Agreement

On September 30, 2013, we entered into the Daewoong Agreement with Daewoong, pursuant to which Daewoong agreed to manufacture and supply Jeuveau® and grant us an exclusive license to import, distribute, promote, market, develop, offer for sale and otherwise commercialize and exploit Jeuveau® for aesthetic indications in the United States, EU, Great Britain, European Economic Area, Switzerland, Canada, Australia, Russia, Commonwealth of Independent States, or CIS, and South Africa, each, a covered territory. Provided that if we do not apply for approvals or commence clinical trials in certain covered territories within 12 months of the Daewoong Agreement Amendment, we may no longer have rights to that covered territory. Daewoong also granted us a non-exclusive license to do the same in Japan. In connection with our entry into the Daewoong Agreement, we made an upfront payment to Daewoong of $2.5 million and agreed to make milestone payments upon certain confidential development and commercial milestones, including payment to Daewoong upon each of FDA and EMA approval of Jeuveau®. Under the Daewoong Agreement, the maximum aggregate amount of milestone payments that could have been owed to Daewoong upon the satisfaction of all milestones is $13.5 million. Upon the FDA approval in February 2019 and EMA approval in September 2019, we paid $2.0 million and $1.0 million milestone payment, respectively. As of December 31, 2020, Daewoong was eligible to receive remaining contingent milestone payments of up to $10.5 million, all of which were cancelled in March 2021 as part of the Daewoong Settlement Agreement. Daewoong is responsible for all costs related to the manufacturing of Jeuveau®, including costs related to the operation and upkeep of its manufacturing facility, and we are responsible for all costs related to obtaining regulatory approval, including clinical expenses, and commercialization of Jeuveau®.

Under the Daewoong Agreement, Daewoong has agreed to supply us with Jeuveau® at an agreed-upon, transfer price, and we have agreed to make milestone payments upon completion of certain confidential development and commercial milestones. Our exclusivity is subject to certain minimum annual purchases for each covered territory upon commercialization and if we fail to meet these targets, Daewoong may, at its option, convert the exclusive license for such covered territory to a non-exclusive license. These potential minimum purchase obligations are contingent upon the occurrence of future events, including receipt of governmental approvals and our future market share in various jurisdictions. During the term of the Daewoong Agreement, we cannot purchase, sell or distribute any competing products in a covered territory or Japan or sell Jeuveau® outside a covered territory or Japan. We also have the option to negotiate first with Daewoong to secure a distribution license for any product that Daewoong directly or indirectly develops or commercializes that is classified as an injectable botulinum toxin (other than Jeuveau®) in a covered territory or Japan.

The initial term of the Daewoong Agreement expires September 30, 2023, and automatically renews for unlimited additional three-year terms if we meet certain performance requirements. The Daewoong Agreement will terminate (A) upon written notice by either us or Daewoong upon a continuing default that remains uncured within 90 days (or 30 days for a payment default) by the other party, or (B) without notice upon the bankruptcy or insolvency of our company.

We are the sole owner of any marketing authorization and clinical trial results we pursue in a covered territory. However, if we do not renew the Daewoong Agreement or upon termination of the Daewoong Agreement due to a breach by us, we are obligated to transfer our rights to Daewoong.

The Daewoong Agreement also provides that Daewoong will indemnify us for any losses arising out of (i) Daewoong’s willful misconduct or gross negligence in performing its obligations under the agreement, (ii) Daewoong’s breach of the agreement, or (iii) any allegation that Jeuveau® or Daewoong’s trademark infringes or misappropriates the rights of a third party, except, in each case, as a result of our willful misconduct or gross negligence. We have agreed to indemnify Daewoong for any losses arising out of (A) our willful misconduct or gross negligence in performing our obligations under the agreement, or (B) our breach of the agreement, except, in each case, as a result of Daewoong’s willful misconduct or gross negligence.

Competition

Our primary competitors in the pharmaceutical market are companies offering injectable dose forms of botulinum toxin. There are only four approved injectable botulinum toxin type A neurotoxins in the United States, including Jeuveau®. There are also other injectable botulinum toxin type A products being developed for the U.S. market. We believe the primary competing products in this market include BOTOX, Dysport and Xeomin:

•BOTOX, marketed by Allergan plc, or Allergan, received FDA approval in 2002 for glabellar lines. Allergan was the first company to market neurotoxins for aesthetic purposes.

•Dysport, marketed by Galderma S.A., or Galderma, received FDA approval in 2009 for glabellar lines.

10

•Xeomin, marketed by Merz Pharma GmbH & Co., or Merz, received FDA approval in 2011 for glabellar lines.

We are also aware that Revance Therapeutics, Inc. has submitted a BLA to the FDA for an injectable botulinum toxin type A neurotoxin and received a target date action date of November 25, 2020 under the Prescription Drug User Fee Act; however the FDA has deferred its decision on the BLA and the BLA has not yet been approved. If Revance’s BLA is approved, we expect the competition in the U.S. injectable botulinum toxin market to further increase.

In addition to the companies commercializing and developing neurotoxins, there are other products and treatments that may indirectly compete with Jeuveau®, such as dermal fillers, laser treatments, brow lifts, chemical peels, fat injections and cold therapy. We compete with various companies that have products in these medical aesthetic categories. Among these companies are Allergan, Sanofi, Sun Pharma, Valeant Pharmaceuticals International, Inc., or Valeant, Mentor Worldwide LLC, a division of Johnson & Johnson, Merz, Galderma, and Skinceuticals, a division of L’Oreal SA. In addition, we are aware of other companies also developing and/or marketing products in one or more of our target markets, including competing injectable botulinum toxin type A formulations that are in various phases of development in North America for the treatment of glabellar lines.

Seasonality

We launched Jeuveau® into the U.S. aesthetic neurotoxin market in May 2019. Given the early stage of our launch of Jeuveau®, the impact of the COVID-19 outbreak and the impact of the ITC remedial orders, we have not observed significant seasonality in our net revenue to date. However, we are aware that historically the aesthetic neurotoxin market experiences higher revenue in the second and fourth calendar quarters as compared to the first and third calendar quarters.

Government Regulation in the United States

We operate in a highly regulated industry that is subject to significant federal, state, local and foreign regulation. Our business has been, and will continue to be, subject to a variety of laws including the Federal Food Drug and Cosmetic Act, or FFDCA, and the Public Health Service Act, or the PHS Act, among others. Biologics and medical devices are subject to regulation under the FFDCA and PHS Act.

In the United States, cosmetics, dietary supplements, biopharmaceutical products and medical devices are subject to extensive regulation by the FDA. The FFDCA, PHS Act, and other federal and state statutes and regulations, govern, among other things, the research, development, testing, manufacture, storage, recordkeeping, regulatory approval, license or clearance, labeling, promotion and marketing, distribution, post-approval monitoring and reporting, sampling, and import and export of these products. Failure to comply with applicable U.S. requirements may subject a company to a variety of administrative or judicial sanctions, such as FDA refusal to approve pending license or marketing applications, warning letters and other enforcement actions, product recalls, product seizures, total or partial suspension of production or distribution, injunctions, fines, civil penalties and criminal prosecution.

FDA Marketing Approval

The process required by the FDA before a biological product may be marketed in the United States generally involves the following:

•completion of nonclinical laboratory tests and animal studies according to good laboratory practices, or GLPs, and applicable requirements for the humane use of laboratory animals or other applicable regulations;

•submission to the FDA of an investigative new drug application, or IND, which must become effective before human clinical trials may begin;

•performance of adequate and well-controlled human clinical trials to establish the safety and efficacy of the proposed biological product for its intended use, according to the FDA’s regulations, commonly referred to as good clinical practices, or GCPs, and any additional requirements including those for the protection of human research subjects and their health and other personal information;

•submission to the FDA of a BLA for marketing approval that includes substantive evidence of safety;

•purity and potency from results of nonclinical testing and clinical trials;

11

•satisfactory completion of an FDA inspection of the manufacturing facility or facilities where the biological product is produced to assess compliance with cGMP, to assure that the facilities, methods and controls are adequate to preserve the biological product’s identity, strength, quality and purity and, if applicable, the FDA’s current good tissue practices for the use of human cellular and tissue products;

•potential FDA audits of the nonclinical study and clinical trial sites that generated the data in support of the BLA; and

•FDA review and approval of the BLA.

Post-Approval Requirements

Once a BLA is approved, a product is subject to certain post-approval requirements. For instance, the FDA closely regulates the post-approval marketing and promotion of biologics, including standards and regulations, off-label promotion, industry-sponsored scientific and educational activities and promotional activities involving the internet. Biologics may be marketed only for the approved indications and in accordance with the provisions of the approved labeling. Adverse event reporting and submission of periodic reports is required following FDA approval of a BLA. The FDA also may require post-marketing testing, known as Phase IV testing, Risk Evaluation and Mitigation Strategies, or REMS, and surveillance to monitor the effects of an approved product or place conditions on an approval that could restrict the distribution or use of the product. In addition, quality control as well as product manufacturing, packaging and labeling procedures must continue to conform to cGMP after approval. Manufacturers and certain of their subcontractors are required to register their establishments with the FDA and certain state agencies, and are subject to periodic unannounced inspections by the FDA during which the agency inspects manufacturing facilities to assess compliance with applicable regulations such as cGMP and the Quality System Regulation. Accordingly, manufacturers must continue to expend time, money and effort in the areas of production and quality control to maintain compliance with cGMP. Regulatory authorities may withdraw product approvals or request product recalls if a company fails to comply with regulatory standards, if it encounters problems following initial marketing, or if previously unrecognized problems are subsequently discovered.

Other Regulation of the Healthcare Industry

While we do not currently have plans for our neurotoxin product to be covered by insurance or government reimbursement programs, if we were to offer reimbursable products, we could be subject to federal laws and regulations covering reimbursable products, such as the Anti-Kickback Statute, Stark Law and Physician Payment Sunshine Act. These laws that may affect our ability to operate include, but are not limited to:

•The Anti-Kickback Statute, which prohibit persons from knowingly and willfully soliciting, offering, receiving or providing remuneration, directly or indirectly, in cash or in kind, to induce either the referral of an individual, or furnishing or arranging for a good or service, for which payment may be made under a federal healthcare program;

•The Federal False Claims Act which imposes civil and criminal liability on individuals and entities who submit, or cause to be submitted, false or fraudulent claims for payment to the government;

•the Federal Civil Monetary Penalties Law, which prohibits, among other things, offering or transferring remuneration to a federal healthcare beneficiary that a person knows or should know is likely to influence the beneficiary’s decision to order or receive items or services reimbursable by the government from a particular provider or supplier;

•The Foreign Corrupt Practices Act (“FCPA”), which prohibits certain payments made to foreign government officials;

•the Federal Health Insurance Portability and Accountability Act of 1996, or HIPAA, which created new federal criminal statutes that prohibit knowingly and willfully executing, or attempting to execute, a scheme to defraud or to obtain, by means of false or fraudulent pretenses, representations, or promises, any of the money or property owned by, or under the custody or control of, any healthcare benefit program, including private third-party payors and knowingly and willfully falsifying, concealing or covering up by trick, scheme or device a material fact or making any materially false, fictitious or fraudulent statement in connection with the delivery of or payment for healthcare benefits, items or services relating to healthcare matters;

12

•the Federal Physician Payments Sunshine Act, and its implementing regulations, which require that certain manufacturers of drugs, medical devices, biologics, and medical supplies for which payment is available under Medicare, Medicaid, or the Children’s Health Insurance Program (with certain exceptions) to report to the CMS information related to certain payments or other transfers of value made or distributed to physicians, which is defined broadly to include other healthcare providers, teaching hospitals, and ownership and investment interests held by physicians and their immediate family members; and

•State and foreign law equivalents of the foregoing and state laws regarding pharmaceutical company marketing compliance, reporting and disclosure obligations.

If our operations are found to be in violation of any of these laws, regulations, rules or policies or any other law or governmental regulation, or if interpretations of the foregoing change, we may be subject to civil and criminal penalties, damages, fines and the curtailment or restructuring of our operations.

Government Regulation in Europe

In the European Economic Area, or EEA (which is composed of the 28 Member States of the EU plus Norway, Iceland and Liechtenstein), medicinal products can only be commercialized after obtaining a Marketing Authorization, or MA.

There are two types of MAs:

•The Community MA, which is issued by the European Commission through the Centralized Procedure, based on the opinion of the Committee for Medicinal Products for Human Use, or CHMP, of the EMA and which is valid throughout the entire territory of the EEA. The Centralized Procedure is mandatory for certain types of products, such as biotechnology medicinal products, orphan medicinal products, and medicinal products indicated for the treatment of AIDS, cancer, neurodegenerative disorders, diabetes, auto-immune and viral diseases. The Centralized Procedure is optional for products containing a new active substance not yet authorized in the EEA, or for products that constitute a significant therapeutic, scientific or technical innovation or which are in the interest of public health in the EU.

•National MAs, which are issued by the competent authorities of the Member States of the EEA and only cover their respective territory, are available for products not falling within the mandatory scope of the Centralized Procedure.

Because we are a biotechnology medicinal products company, we are eligible for a Community MA under the Centralized Procedure.

Under the above described procedures, before granting the MA, the EMA or the competent authorities of the Member States of the EEA make an assessment of the risk-benefit balance of the product on the basis of scientific criteria concerning its quality, safety and efficacy.

Product Approval Process Outside the United States and Europe

In addition to regulations in the United States and EU, we may be subject to a variety of regulations in other jurisdictions governing manufacturing, clinical trials, commercial sales and distribution of our future products. Whether or not we obtain FDA approval or MA approval for a product candidate, we must obtain approval of the product by the comparable regulatory authorities of foreign countries before commencing clinical trials or marketing in those countries. The approval process varies from country to country, and the time may be longer or shorter than that required for FDA approval or MA approval. The requirements governing the conduct of clinical trials, product licensing, pricing and reimbursement vary greatly from country to country.

Data Privacy and Security Laws and Regulations

We are also subject to data privacy and security regulation by the federal government, states and non-U.S. jurisdictions in which we conduct our business. For example, HIPAA, as amended by the Health Information Technology and Clinical Health Act, or HITECH, and its implementing regulations, imposes certain requirements relating to the privacy, security and transmission of individually identifiable health information. Among other things, HITECH makes HIPAA’s privacy and security standards directly applicable to “business associates,” those independent contractors or agents of covered entities that create, receive, maintain, transmit or obtain protected health information in connection with providing a service on behalf of a covered entity. HITECH also increased the civil and criminal penalties that may be imposed against covered entities, business associates and possibly other persons, and gave state attorneys general new authority to file civil actions for damages or

13

injunctions in federal courts to enforce the federal HIPAA laws and seek attorney’s fees and costs associated with pursuing federal civil actions. In addition, state and non-U.S. laws, including the General Data Protection Regulation adopted by the EU, govern the privacy and security of health and other personal information in certain circumstances, many of which differ from each other in significant ways and may not have the same effect, thus complicating compliance efforts.

There are numerous other laws and legislative and regulatory initiatives at the federal and state levels addressing privacy and security concerns. We also remain subject to federal or state privacy-related laws that are more restrictive than the privacy regulations issued under HIPAA. These laws vary and could impose additional penalties. For example, the Federal Trade Commission uses its consumer protection authority to initiate enforcement actions in response to alleged privacy and data security violations. Further, certain states have proposed or enacted legislation that will create new data privacy and security obligations for certain entities, such as the California Consumer Privacy Act, or CCPA, which came into effect January 1, 2020 and was recently amended and expanded by the California Privacy Rights Act, or the CRPA, passed on November 3, 2020. The CCPA and CPRA, among other things, create new data privacy obligations for covered companies and provides new privacy rights to California residents, including the right to opt out of certain disclosures of their information. The CCPA also created a private right of action with statutory damages for certain data breaches, thereby potentially increasing risks associated with a data breach. It remains unclear what, if any, additional modifications will be made to the CPRA by the California legislature or how it will be interpreted. Therefore, the effects of the CCPA and CPRA are significant and will likely require us to modify our data processing practices and may cause us to incur substantial costs and expenses to comply, particularly given our base of operations in California.

Environmental Regulation

We are subject to numerous foreign, federal, state, and local environmental, health and safety laws and regulations relating to, among other matters, safe working conditions, manufacturing practices, fire hazard control, product stewardship and end-of-life handling or disposition of products, and environmental protection, including those governing the generation, storage, handling, use, transportation and disposal of hazardous or potentially hazardous substances and biological materials.

Our History

We were incorporated in November 2012 and are headquartered in Newport Beach, California. In a series of related transactions in 2013, Strathspey Crown Holdings Group, LLC (formerly known as Strathspey Crown Holdings, LLC), or SCH, acquired all of our outstanding equity in exchange for membership interests in SCH. In 2014, SCH contributed our equity that it had acquired in 2013 to its subsidiary operating entity, ALPHAEON Corporation, or Alphaeon. As a result of these transactions, prior to our initial public offering we were a wholly-owned subsidiary of Alphaeon. In 2019 Alphaeon changed its name to AEON Biopharma, Inc. and contributed all of the shares it held in the Company to Alphaeon 1, LLC. The Company continues to refer to the renamed AEON Biopharma, Inc. as “Alphaeon” and Alphaeon 1, LLC as Alphaeon 1, LLC.

As of December 31, 2020 and March 25, 2021, Alphaeon owned 25.7% and 19.8% of our outstanding shares of common stock, respectively.

Human Capital Resources

As of December 31, 2020, we had 119 employees, all of whom are full-time in the United States, and 63% of our full-time employees were women. None of our employees are represented by labor unions or covered by collective bargaining agreements, and we have never experienced any work stoppage. We believe we have good relations with our employees.

We believe that our future success largely depends upon our continued ability to attract and retain highly qualified management and technical personnel. Talent management is critical to our ability to execute on our long-term growth strategy. To facilitate talent attraction and retention, we strive to make our company a safe and rewarding workplace, with opportunities for our employees to grow and develop in their careers, supported by strong compensation and benefits, and by programs that build connections among our employees. We continue to be committed to an inclusive culture which values equity, opportunity, and respect. In support of our inclusive culture, we offer competitive compensation and benefits, including stock awards; provide unconscious bias training to strengthen employee awareness; and strive to recruit a diverse talent pool across all levels of the organization. In response to the COVID-19 pandemic, we implemented changes that we determined were in the best interest of our employees, as well as the communities in which we operate, and which comply with government regulations. This included implementing a work-from-home policy for all employees who are able to perform their duties remotely and restricting all nonessential travel.

14

Corporate Information

We were incorporated in the State of Delaware in November 2012. Our principal executive offices are located at 520 Newport Center Drive, Suite 1200, Newport Beach, California 92660, and our telephone number is (949) 284-4555. Our website address is www.evolus.com. We do not incorporate the information on or accessible through our website into this Annual Report on Form 10-K, and you should not consider any information on, or that can be accessed through, our website a part of this Annual Report on Form 10-K or any other filing we make with the SEC. We are an emerging growth company under the Jumpstart Our Business Startups Act of 2012 and also a smaller reporting company, and therefore we are subject to reduced public company reporting requirements.

Available Information

We make available, free of charge, on our website at www.evolus.com our annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and any amendments to such reports, as soon as reasonably practicable after such reports are electronically filed with, or furnished to, the SEC. All such reports are also available free of charge via EDGAR through the SEC website at www.sec.gov. We do not incorporate the information on or accessible through these websites into this Annual Report on Form 10-K, and you should not consider any information on, or that can be accessed through, these websites a part of this Annual Report on Form 10-K or any other filing we make with the SEC.

15

Item 1A. Risk Factors.

An investment in our company involves a high degree of risk. You should carefully consider the risks and uncertainties described below, together with all the other information in this Annual Report on Form 10-K, including Item 7“Management’s Discussion and Analysis of Financial Condition and Results of Operations” and the financial statements and the related notes included in Item 8 “Financial Statements and Supplementary Data.” If any of the following risks actually occurs, our business, reputation, financial condition, results of operations, revenue, and future prospects could be seriously harmed. The risks and uncertainties described below are not the only ones we face. Additional risks and uncertainties that we are unaware of, or that we currently believe are not material, may also become important factors that adversely affect our business. Unless otherwise indicated, references to our business being seriously harmed in these risk factors will include harm to our business, reputation, financial condition, results of operations, revenue, and future prospects. In that event, the market price of our common stock could decline, and you could lose part or all of your investment.

Risks Related to Our Business and Strategy

We will require additional financing to fund our future operations, and a failure to obtain additional capital when so needed on acceptable terms, or at all, could force us to delay, limit, reduce or terminate our operations and as a result, there is substantial doubt about our ability to continue as a going concern.

We believe that our current capital resources, after taking into account the repayment of the Oxford loan are not sufficient to meet our obligations and fund operations through at least the next 12 months. We will be required to raise additional capital to meet our operating, debt and settlement obligations coming due.

We have utilized substantial amounts of cash since our inception in order to conduct clinical development to support regulatory approval of Jeuveau® in the United States, EU and Canada and in connection with the launch of Jeuveau® in the United States and Canada. We expect that we will continue to expend substantial resources for the foreseeable future in order to pay costs associated with our settlement agreements with Medytox and Allergan, payments to the founders of our company under a promissory note issued to them in 2017 and for the continued commercialization of Jeuveau® in the United States and abroad.

As described in our notes to the financial statements in this Annual Report on Form 10-K, we have incurred recurring losses and negative cash flows from operations and have an accumulated deficit at December 31, 2020 of $376.1 million, which raises substantial doubt about our ability to continue as a going concern. As of December 31, 2020, we had cash and cash equivalents of $102.6 million and short-term investments of $5.0 million. On January 4, 2021, we entered into a letter agreement with Oxford Finance, LLC, or Oxford , pursuant to which we paid Oxford $76.4 million to discharge in full all outstanding obligations, included accrued interest, under that certain Loan and Security Agreement, dated as of March 15, 2019.

In the near term, we expect expenditures associated with our settlement agreements with Medytox and Allergan, including a $15.0 million payment due in the second quarter of 2021, and a $20.0 million payment in the fourth quarter of 2021 due to the founders of our company under a promissory note issued to them in 2017. This will be partially offset by a $25.5 million payment from Daewoong to us. Additionally, we expect to expend resources furthering the development and continuation of our marketing programs and commercialization infrastructure in connection with commercializing Jeuveau® within and outside of the United States. In the long term, our expenditures will include costs associated with the continued commercialization of Jeuveau® and any of our future product candidates, such as research and development, conducting preclinical studies and clinical trials and manufacturing and supplying as well as marketing and selling any products approved for sale. In addition, other unanticipated costs may arise. Because the commercialization expenditures needed to meet our sales objectives are highly uncertain, we cannot reasonably estimate the actual amounts necessary to successfully commercialize Jeuveau®. We expect to incur additional costs as we continue to operate as a public company, hire additional personnel and expand our operations.

If we raise additional capital through marketing and distribution arrangements, royalty financing arrangements, or other collaborations, strategic alliances or licensing arrangements with third parties, we may have to relinquish certain valuable rights to our product candidates, technologies, future revenue streams or research programs or grant licenses on terms that may not be favorable to us. If we raise additional capital through public or private equity offerings or offerings of securities convertible into our equity, the ownership interest of our existing stockholders will be diluted and the terms of any such securities may have a preference over our common stock. Debt financing, receivables financing and royalty financing may also be coupled with an equity component, such as warrants to purchase our capital stock, which could also result in dilution

16

of our existing stockholders’ ownership, and such dilution may be material. Additionally, if we raise additional capital through debt financing, we will have increased fixed payment obligations and may be subject to covenants limiting or restricting our ability to take specific actions, such as incurring additional debt or making capital expenditures to meet specified financial ratios, and other operational restrictions, any of which could restrict our ability to commercialize Jeuveau® or any future product candidates or operate as a business and may result in liens being placed on our assets. If we were to default on any of our indebtedness, we could lose such assets.

In the event we are unable to raise sufficient capital to fund our commercialization efforts to achieve specified minimum sales targets under the Daewoong Agreement, we will lose exclusivity of the license that we have been granted under the Daewoong Agreement. In addition, if we are unable to raise additional capital when required or on acceptable terms, we will be required to take actions to address our liquidity needs which may include the following: significantly reduce operating expenses and delay, reduce the scope of or discontinue some of our development programs, commercialization efforts or other aspects of our business plan, out-license intellectual property rights to our product candidates and sell unsecured assets, or a combination of the above. As a result, our ability to achieve profitability or to respond to competitive pressures would be significantly limited and may have a material adverse effect on our business, results of operations, financial condition and/or our ability to fund our scheduled obligations on a timely basis or at all.

We currently depend entirely on the successful commercialization of our only product, Jeuveau®. If we are unable to successfully commercialize Jeuveau®, we may never generate sufficient revenue to continue our business.

We currently have only one product, Jeuveau®, and our business presently depends entirely on our ability to successfully commercialize it in a timely manner. While the product was commercially launched in the United States in May 2019 and through a distribution partner in Canada in October 2019, we have a limited history of generating revenue for Jeuveau®. Our near-term prospects, including our ability to generate revenue, as well as our future growth, depend entirely on the successful commercialization of Jeuveau®. The commercial success of Jeuveau® will depend on a number of factors, including our ability to successfully commercialize Jeuveau®, whether alone or in collaboration with others, including our ability to hire, retain and train sales representatives in the United States. Our ability to commercialize Jeuveau® is also dependent on the willingness of consumers to pay for Jeuveau® relative to other discretionary items, especially during economically challenging times. Additional factors necessary for the successful commercialization of Jeuveau® include the availability, perceived advantages, relative cost, relative safety of Jeuveau® and relative efficacy of competing products, the timing of new product introductions by our competitors, and the sales and marketing tactics of our competitors, including bundling of multiple products, in response to our launch of Jeuveau®.

If we do not achieve one or more of these factors, many of which are beyond our control, in a timely manner or at all, we could experience significant issues commercializing Jeuveau®. Further, we may never be able to successfully commercialize Jeuveau® or any future product candidates. In addition, our experience as a commercial company is limited. Accordingly, we may not be able to generate sufficient revenue through the sale of Jeuveau® or any future product candidates to continue our business.

We have a limited operating history and have incurred significant losses since our inception and anticipate that we will continue to incur losses for the foreseeable future. We have only one product and limited commercial sales, which, together with our limited operating history, make it difficult to assess our future viability.

We are a performance beauty company with a limited operating history. To date, we have invested substantially all of our efforts and financial resources in the clinical development, regulatory approval, and commercial launch of Jeuveau®, which is currently our only product. We began selling Jeuveau® in the United States in May 2019 and through a distribution partner in Canada in October 2019 and have a limited history of generating revenue. We are not profitable and have incurred losses in each year since our inception in 2012. We have a limited operating history upon which you can evaluate our business and prospects. Consequently, any predictions about our future success, performance or viability may not be as accurate as they could be if we had a longer operating history or greater experience commercializing a product. In addition, we have limited experience and have not yet demonstrated an ability to successfully overcome many of the risks and uncertainties frequently encountered by companies in the medical aesthetics field. We continue to incur significant expenses related to the commercialization of Jeuveau®. We have recorded net losses of $163.0 million and $90.0 million for the years ended December 31, 2020 and 2019, respectively, and had an accumulated deficit as of December 31, 2020 of $376.1 million. We expect to continue to incur losses for the foreseeable future, and we anticipate these losses will continue as we commercialize Jeuveau®. Our ability to achieve revenue and profitability is dependent on our ability to successfully market and commercialize Jeuveau®. Even if we achieve profitability in the future, we may not be able to sustain profitability in

17

subsequent periods. Our prior losses, combined with expected future losses, may adversely affect the market price of our common stock and our ability to raise capital and continue operations.

If we or our counterparties do not comply with the terms of our settlement agreements with Medytox, Inc., or Medytox, and Allergan Limited, Allergan, Inc. and Allergan Pharmaceuticals Ireland, or, collectively, Allergan, we may face litigation or lose our ability to commercialize Jeuveau® which would materially and adversely affect our ability to carry out our business, and our financial condition and ability to continue as a going concern.