|

UNITED STATES SECURITIES

|

|

AND EXCHANGE COMMISSION

|

|

WASHINGTON, DC 20549

|

FORM 20-F

|

o

|

Registration Statement Pursuant to Section 12(b) or (g) of the Securities Exchange Act of 1934

|

or

|

x

|

Annual Report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934

|

For the fiscal year ended December 31, 2015

or

|

o

|

Transition Report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934

|

or

|

o

|

Shell Company Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934

|

Date of event requiring this shell company report: __________

For the transition period from ________ to _______________

Commission file no.:

|

MAZOR ROBOTICS LTD.

|

|

(Exact name of registrant as specified in its charter)

|

Translation of registrant’s name into English: Not applicable

|

State of Israel

|

7 HaEshel Street

|

|

|

(Jurisdiction of incorporation or organization)

|

Caesarea Industrial Park South

|

|

|

3088900 Israel

|

||

|

(Address of principal executive offices)

|

Sharon Levita

Chief Financial Officer

+972-4-618-7101

Sharon.Levita@MazorRobotics.com

7 HaEshel Street

Caesarea Industrial Park South

3088900 Israel

(Name, Telephone, E-mail and/or Facsimile number and Address of Company Contact Person)

Securities registered or to be registered pursuant to Section 12(b) of the Act:

|

Title of each class:

|

Name of each exchange on which registered or to be

|

|

|

American Depository Shares each representing 2

|

registered:

|

|

|

Ordinary Shares, par value NIS 0.01 per share(1)

|

NASDAQ Global Market

|

|

|

Ordinary Shares, par value NIS 0.01 per share(2)

|

|

(1)

|

Evidenced by American Depositary Receipts.

|

|

(2)

|

Not for trading, but only in connection with the listing of the American Depositary Shares.

|

Securities registered or to be registered pursuant to Section 12(g) of the Exchange Act: None

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Exchange Act: None

Number of outstanding shares of each of the issuer’s classes of capital or common stock as of April 28, 2016: 42,514,698 ordinary shares.

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yes o No x

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Exchange Act.

Yes o No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Exchange Act during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Yes x No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months.

Yes o No o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer or a non-accelerated filer.

|

Large accelerated filer o

|

Accelerated filer x

|

Non-accelerated filer o

|

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing.

U.S. GAAP o

International Financial Reporting Standards as issued by the International Accounting Standards Board x

Other o

If “Other” has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow.

o Item 17 o Item 18

If this is an annual report, indicate by check mark whether the registrant is a shell company.

o Yes x No

2

TABLE OF CONTENTS

|

Page

|

||

|

5

|

||

|

5

|

||

|

6

|

||

|

PART I

|

7

|

|

|

7

|

||

|

7

|

||

|

8

|

||

|

A.

|

Selected Financial Data.

|

8

|

|

B.

|

Capitalization and Indebtedness.

|

9

|

|

C.

|

Reasons for the Offer and Use of Proceeds.

|

9

|

|

D.

|

Risk Factors.

|

9

|

|

43

|

||

|

A.

|

History and Development of the Company.

|

43

|

|

B.

|

Business Overview.

|

44

|

|

C.

|

Organizational Structure.

|

69

|

|

D.

|

Property, Plants and Equipment.

|

69

|

|

70

|

||

|

70

|

||

|

A.

|

Operating Results.

|

70

|

|

B.

|

Liquidity and Capital Resources.

|

80

|

|

C.

|

Research and Development, Patents and Licenses, Etc.

|

82

|

|

D.

|

Trend Information.

|

82

|

|

E.

|

Off-Balance Sheet Arrangements.

|

83

|

|

F.

|

Tabular Disclosure of Contractual Obligations.

|

84

|

|

84

|

||

|

A.

|

Directors and Senior Management.

|

84

|

|

B.

|

Compensation.

|

87

|

|

C.

|

Board Practices.

|

91

|

|

D.

|

Employees.

|

104

|

|

E.

|

Share Ownership.

|

105

|

|

108

|

||

|

A.

|

Major Shareholders.

|

108

|

|

B.

|

Related Party Transactions.

|

109

|

|

C.

|

Interests of Experts and Counsel.

|

109

|

|

110

|

||

|

A.

|

Consolidated Statements and Other Financial Information.

|

110

|

|

B.

|

Significant Changes.

|

110

|

|

111

|

||

|

A.

|

Offer and Listing Details.

|

111

|

|

B.

|

Plan of Distribution.

|

112

|

|

C.

|

Markets.

|

112

|

|

D.

|

Selling Shareholders.

|

112

|

|

E.

|

Dilution.

|

112

|

|

F.

|

Expenses of the Issue.

|

112

|

|

113

|

||

|

A.

|

Share Capital.

|

113

|

|

B.

|

Memorandum and Articles of Association.

|

113

|

|

C.

|

Material Contracts.

|

113

|

|

D.

|

Exchange Controls.

|

113

|

3

|

E.

|

Taxation.

|

114

|

|

F.

|

Dividends and Paying Agents.

|

125

|

|

G.

|

Statement by Experts.

|

125

|

|

H.

|

Documents on Display.

|

126

|

|

I.

|

Subsidiary Information.

|

126

|

|

126

|

||

|

128

|

||

|

A.

|

Debt Securities.

|

128

|

|

B.

|

Warrants and Rights.

|

128

|

|

C.

|

Other Securities.

|

128

|

|

D.

|

American Depositary Shares.

|

128

|

|

PART II

|

129

|

|

|

129

|

||

|

129

|

||

|

129

|

||

|

130

|

||

|

130

|

||

|

130

|

||

|

131

|

||

|

131

|

||

|

131

|

||

|

131

|

||

|

133

|

||

|

PART III

|

133

|

|

|

133

|

||

|

133

|

||

|

134

|

||

|

136

|

||

4

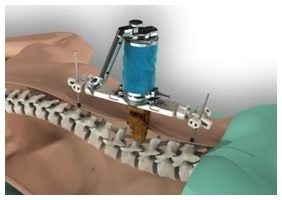

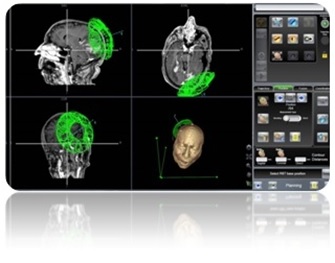

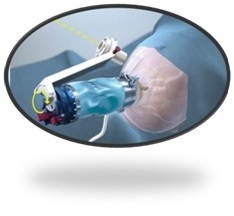

Mazor Robotics, an Israeli Company, is a leading innovator that has pioneered surgical guidance systems and complementary products in the spine surgical markets which we believe provide a safer surgical environment for patients, surgeons and operating room staff. We engage in the development, production and marketing of innovative medical devices for supporting surgical procedures in the fields of orthopedics and neurosurgery. We operate in the fields of image guided surgery and computer-assisted surgery enabling the use of surgical instruments with high precision and minimal invasiveness and aiming to simplify complex and minimally-invasive surgical procedures. We believe that our flagship product, the Renaissance® Surgical Guidance System, or Renaissance, is transforming spine surgery from freehand procedures to highly accurate, state-of-the-art, guided procedures that raise the standard of care with better clinical results. Our Renaissance and SpineAssist (our predecessor to the Renaissance) systems have been used to perform over 16,000 procedures worldwide (over 98,000 implants) in a wide variety of spinal procedures, many of which would not have been attempted without this technology. In 2014 we introduced the Renaissance for brain surgery and in 2015 we introduced the PRO (Predictable Renaissance Operation) product line, which currently includes three solutions designed to support brain procedures, as well as, trauma and lateral spine procedures. We are continuing the development of the Renaissance platform for additional spine and brain surgery procedures.

We were incorporated under the laws of the State of Israel on September 12, 2000. Our ordinary shares are listed on the Tel Aviv Stock Exchange, or TASE, under the symbol “MZOR”. In May 2013, our American Depositary Shares, or ADSs, representing our Ordinary Shares commenced trading on the NASDAQ Capital Market under the trading symbol “MZOR” and are currently traded on the NASDAQ Global Market. Each ADS represents two of our Ordinary Shares.

Unless the context otherwise indicates or requires, “Mazor Robotics”, “Mazor,” the Mazor Robotics logo and all product names and trade names used by us in this annual report, including Renaissance™, are our proprietary trademarks and service marks. These trademarks and service marks are important to our business. Although we have omitted the “®” and “TM” trademark designations for such marks in this annual report, all rights to such trademarks and service marks are nevertheless reserved.

Unless derived from our financial statements or otherwise indicated, U.S. dollar translations of NIS amounts presented in this annual report are translated using a rate of NIS 4.00 to USD 1.00.

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

Certain information included or incorporated by reference in this annual report may be deemed to be “forward-looking statements”. Forward-looking statements are often characterized by the use of forward-looking terminology such as “may,” “will,” “expect,” “anticipate,” “estimate,” “continue,” “believe,” “should,” “intend,” “project” or other similar words, but are not the only way these statements are identified.

These forward-looking statements may include, but are not limited to, statements relating to our objectives, plans and strategies, statements that contain projections of results of operations or of financial condition, statements relating to the research, development and use of our products, and all statements (other than statements of historical facts) that address activities, events or developments that we intend, expect, project, believe or anticipate will or may occur in the future.

Forward-looking statements are not guarantees of future performance and are subject to risks and uncertainties. We have based these forward-looking statements on assumptions and assessments made by our management in light of their experience and their perception of historical trends, current conditions, expected future developments and other factors they believe to be appropriate.

5

Important factors that could cause actual results, developments and business decisions to differ materially from those anticipated in these forward-looking statements include, among other things:

|

|

●

|

the overall global economic environment;

|

|

|

●

|

the impact of competition and new technologies;

|

|

|

●

|

general market, political and economic conditions in the countries in which we operate;

|

|

|

●

|

projected capital expenditures and liquidity;

|

|

|

●

|

changes in our strategy;

|

|

|

●

|

government regulations and approvals;

|

|

|

●

|

changes in customers’ budgeting priorities;

|

|

|

●

|

litigation and regulatory proceedings; and

|

|

|

●

|

those factors referred to in “Item 3. Key Information - D. Risk Factors”, “Item 4. Information on the Company,” and “Item 5. Operating and Financial Review and Prospects”, as well as in this annual report generally.

|

Readers are urged to carefully review and consider the various disclosures made throughout this annual report, which are designed to advise interested parties of the risks and factors that may affect our business, financial condition, results of operations and prospects.

In addition, the section of this annual report entitled “Item 4. Information on the Company” contains information obtained from independent industry and other sources that we have not independently verified. You should not put undue reliance on any forward-looking statements. Any forward-looking statements in this annual report are made as of the date hereof, and we undertake no obligation to publicly update or revise any forward-looking statements, whether as a result of new information, future events or otherwise, except as required by law.

DEFINITION OF CERTAIN TERMS

In this Form 20-F, unless the context otherwise requires, references to:

|

|

●

|

“Mazor Robotics”, “Mazor,” the “Company”, the “registrant”, “us”, “we” and “our” refer to Mazor Robotics Ltd., an Israeli company, and, unless the context indicates otherwise, the Subsidiaries;

|

|

|

●

|

“ADSs” are to our American Depositary Shares, each representing two of our Ordinary Shares;

|

|

|

●

|

“Companies Law” are to Israel’s Companies Law, 5759-1999, as amended;

|

|

|

●

|

“Dollars”, “U.S. dollars”, “U.S. $” and “$” are to United States Dollars;

|

|

|

●

|

“Exchange Act” are to the United States Securities Exchange Act of 1934, as amended;

|

6

|

|

●

|

“FDA” are to the United States Food and Drug Administration;

|

|

|

●

|

“IRS” are to the United States Internal Revenue Service;

|

|

|

●

|

“NASDAQ” are to the NASDAQ Global Market;

|

|

|

●

|

“OCS” are to the Israel’s Office of the Chief Scientist of the Ministry of Economy;

|

|

|

●

|

“Ordinary Shares”, “our shares” and similar expressions refer to our ordinary shares, par value NIS 0.01 per share;

|

|

|

●

|

“SEC” are to the United States Securities and Exchange Commission;

|

|

|

●

|

“Securities Act” are to the United States Securities Act of 1933, as amended;

|

|

|

●

|

“Shekels” and “NIS” are to New Israel Shekels, the Israeli currency;

|

|

|

●

|

“Subsidiaries” are to the U.S. Subsidiary and to Mazor Robotics Pte Ltd., a Singapore company, and a wholly owned subsidiary of Mazor;

|

|

|

●

|

“TASE” are to the Tel Aviv Stock Exchange; and

|

|

|

●

|

“U.S. Subsidiary” are to Mazor Robotics, Inc., a Delaware corporation, and a wholly owned subsidiary of Mazor.

|

PART I

|

ITEM 1.

|

IDENTITY OF DIRECTORS, SENIOR MANAGEMENT AND ADVISERS

|

Not applicable.

|

ITEM 2.

|

OFFER STATISTICS AND EXPECTED TIMETABLE

|

Not applicable.

7

|

ITEM 3.

|

KEY INFORMATION

|

|

A.

|

Selected Financial Data

|

The selected consolidated financial data for the fiscal years set forth in the table below have been derived from our consolidated financial statements and notes thereto. The selected consolidated statement of profit or loss data for fiscal years 2015, 2014 and 2013, and the selected consolidated statement of financial position data as of December 31, 2015 and 2014, have been derived from our audited consolidated financial statements and notes thereto set forth elsewhere in this Form 20-F. The selected consolidated statement of profit or loss data for fiscal years 2012 and 2011, and the selected consolidated statement of financial position data as of December 31, 2013, 2012, and 2011, respectively, has been derived from other audited consolidated financial statements not included herein. The selected financial data should be read in conjunction with our consolidated financial statements, and are qualified entirely by reference to such consolidated financial statements. Additionally, and as explained in Note 2B to the December 31, 2015 consolidated financial statements, our functional currency is U.S. dollars.

|

(in thousands except net loss per share data)

|

||||||||||||||||

|

Years Ended December 31,

|

||||||||||||||||||||

|

2015

|

2014

|

2013

|

2012

|

2011

|

||||||||||||||||

|

Statement of Profit or Loss Data

|

||||||||||||||||||||

|

Revenues

|

$ | 26,096 | $ | 21,208 | $ | 19,983 | $ | 12,175 | $ | 5,904 | ||||||||||

|

Cost of sales

|

$ | 5,827 | $ | 4,396 | $ | 4,280 | $ | 2,893 | $ | 1,879 | ||||||||||

|

Gross profit

|

$ | 20,269 | $ | 16,812 | $ | 15,703 | $ | 9,282 | $ | 4,025 | ||||||||||

|

Operating costs and expenses:

|

||||||||||||||||||||

|

Research and development expenses, net

|

$ | 6,324 | $ | 5,776 | $ | 4,174 | $ | 2,760 | $ | 3,062 | ||||||||||

|

Selling and marketing expenses

|

$ | 24,947 | $ | 21,352 | $ | 15,692 | $ | 8,887 | $ | 6,990 | ||||||||||

|

General and administrative expenses

|

$ | 4,305 | $ | 4,392 | $ | 2,766 | $ | 1,845 | $ | 1,639 | ||||||||||

|

Total operating costs and expenses

|

$ | 35,576 | $ | 31,520 | $ | 22,632 | $ | 13,492 | $ | 11,691 | ||||||||||

|

Operating loss

|

$ | (15,307 | ) | $ | (14,708 | ) | $ | (6,929 | ) | $ | (4,210 | ) | $ | (7,666 | ) | |||||

|

Loss for the year

|

$ | (15,385 | ) | $ | (15,272 | ) | $ | (20,529 | ) | $ | (7,064 | ) | $ | (7,782 | ) | |||||

|

Loss per share – Basic and diluted

|

$ | (0.36 | ) | $ | (0.37 | ) | $ | (0.57 | ) | $ | (0.29 | ) | $ | (0.36 | ) | |||||

|

Weighted average number of ordinary shares used to calculate basic and diluted loss per share

|

42,284 | 41,808 | 35,781 | 24,011 | 21,815 | |||||||||||||||

8

|

(in thousands)

|

As of December 31,

|

|||||||||||||||||||

|

2015

|

2014

|

2013

|

2012

|

2011

|

||||||||||||||||

|

Statement of Financial Position Data:

|

||||||||||||||||||||

|

Cash and cash equivalents

|

$ | 13,519 | $ | 22,255 | $ | 19,803 | $ | 12,797 | $ | 1,655 | ||||||||||

|

Short-term investments

|

$ | 21,687 | $ | 24,507 | $ | 45,014 | $ | 4,156 | $ | 14,455 | ||||||||||

|

Long-term investments

|

$ | 5,023 | $ | 5,473 | $ | — | $ | — | $ | — | ||||||||||

|

Total assets

|

$ | 50,970 | $ | 60,686 | $ | 70,889 | $ | 21,334 | $ | 20,424 | ||||||||||

|

Total non-current liabilities

|

$ | 299 | $ | 278 | $ | 332 | $ | 4,490 | $ | 616 | ||||||||||

|

Accumulated loss

|

$ | (103,192 | ) | $ | (87,807 | ) | $ | (72,535 | ) | $ | (52,006 | ) | $ | (44,942 | ) | |||||

|

Total equity

|

$ | 42,400 | $ | 54,267 | $ | 64,093 | $ | 12,820 | $ | 13,484 | ||||||||||

|

B.

|

Capitalization and Indebtedness

|

Not applicable.

|

C.

|

Reasons for the Offer and Use of Proceeds

|

Not applicable.

|

D.

|

Risk Factors

|

You should carefully consider the risks described below, together with all of the other information in this Form 20-F. The risks described below are not the only risks facing us. Additional risks and uncertainties not currently known to us or that we currently deem to be immaterial may also materially and adversely affect our business operations. If any of these risks actually occurs, our business and financial condition could suffer and the price of our shares could decline.

9

Risks Related to Our Business

We are an emerging growth company, and we have incurred significant losses since our inception.

We are an emerging growth company. The future success of our business depends on our ability to continue to develop and obtain regulatory clearances or approvals for innovative and commercially successful products in our field, which we may be unable to do in a timely manner, or at all. Our success and ability to generate revenue or be profitable also depends on our ability to establish our sales and marketing force, generate product sales and control costs, all of which we may be unable to do. Our limited operating history also limits your ability to make a comparative evaluation of us, our products and our prospects.

We have sustained net losses in every fiscal year since our inception in 2000, including a net loss of $15.4 million for the year ended December 31, 2015. As of December 31, 2015, we had total shareholders’ equity of $42.4 million and cash and cash equivalents, short term investments and long term investments of approximately $40.2 million. Our accumulated deficit as of December 31, 2015 was $103.2 million. We anticipate that we will continue to incur substantial net losses for at least the next two years as we expand our sales and marketing capabilities in the spine and neurosurgery products market, continue our commercialization of Renaissance, expand its adoption and clinical implementation, and continue to develop the corporate infrastructure required to sell and market our products and invest in product development. Our losses have had and will continue to have an adverse effect on our shareholders’ equity and working capital. Any failure to achieve and maintain profitability would continue to have an adverse effect on our shareholders’ equity and working capital and could result in a decline in our share price or cause us to cease operations.

We cannot assure investors that our existing cash and investment balances will be sufficient to meet our future capital requirements.

We believe our existing cash, cash equivalents, investment balances, and interest income we earn on these balances, if any, will be sufficient to meet our anticipated cash requirements through at least the next 24 months. To the extent our available cash, cash equivalents and investment balances are insufficient to satisfy our operating requirements or other strategic needs, we will either need to seek additional sources of funds, including selling additional equity or debt securities or entering into a credit facility. However, we may be unable to obtain additional financing. As a result, we may be required to reduce the scope of, or delay or eliminate, some or all of our current and planned research, development and commercialization activities. We also may have to reduce marketing, customer service or other resources devoted to our products. Any of these actions could materially harm our business and results of operations. Even if we are able to continue to finance our business, the sale of additional equity and debt securities may result in dilution to our current shareholders or may require us to grant a security interest in our assets. If we raise additional funds through the issuance of debt securities, these securities may have rights senior to those of our Ordinary Shares and could contain covenants that could restrict our operations. We may require additional capital beyond our currently forecasted amounts. Any such required additional capital may not be available on reasonable terms, or at all.

We depend on the success of one product for our revenue, which could impair our ability to achieve profitability.

We expect to derive most of our revenue from sales of Renaissance, recurring sales of disposable products required to use Renaissance in each surgical procedure, and service plans that are sold with Renaissance. Our future growth and success is dependent on successfully increasing the commercialization of Renaissance and the adoption of Renaissance by the end users. If we are unable to achieve increased commercial adoption of Renaissance, are unable to obtain regulatory clearances or approvals for future products, or experience a decrease in the utilization of our product line or procedure volume, our revenue would be adversely affected and we would not become profitable. If adverse economic, industry or regulatory events or changes occur, we may have to write off inventory as obsolete, which could negatively impact our business and revenue.

10

If surgeons and hospitals do not broadly adopt the concept of computer assisted spine surgeries and do not perceive such technology and related products as valuable and having significant advantages over the current “freehand” standard-of-care procedures, patients will be less likely to accept or be offered surgery with Renaissance, and we will fail to meet our business objectives.

Surgeons’ and hospitals’ perceptions of our technology having significant advantages are likely to be based on a determination that, among other factors, our products are safe, reliable, cost-effective and represent acceptable methods of treatment. Even if we can prove the clinical value of Renaissance through continued clinical use, surgeons may elect not to use our current and future Renaissance solutions for any number of other reasons. For example, surgeons may continue to operate freehand simply because such surgeries are already widely accepted. In addition, surgeons may be slow to adopt our current and future Renaissance solutions because of the perceived liability risks arising from the use of new products. Surgeons may not accept our current and future Renaissance solutions if we fail to maintain an acceptable level of product reliability or if we encounter regulatory approval or compliance issues. Hospitals may not accept Renaissance because of the capital expense, which may represent a significant portion of a hospital’s capital budget. Renaissance may not be cost-efficient if hospitals are not able to perform a significant volume of procedures using it.

If our current and future Renaissance solutions fail to achieve increased market acceptance for any of these or other reasons or if we are not successful in enforcing the contractual commitment to purchase disposable products exclusively from us, we will not be able to generate the revenue necessary to develop a sustainable, profitable business.

We depend on key employees, and if we fail to attract and retain employees with the expertise required for our business and to provide for the succession of senior management, we cannot grow or achieve profitability.

We are dependent on members of our senior management, in particular Ori Hadomi and Eliyahu Zehavi. Our future success will depend in part on our ability to retain our management and scientific teams, to identify, hire and retain additional qualified personnel with expertise in research and development and sales and marketing, and to effectively provide for the succession of senior management. Competition for qualified personnel in the medical device industry is intense and finding and retaining qualified personnel with experience in our industry is very difficult. We believe that there are only a limited number of individuals with the requisite skills to serve in many of our key positions, particularly in Israel, and we compete for key personnel with other medical equipment and software manufacturers and technology companies, as well as research institutions. It is often difficult to hire and retain these persons, and we may be unable to replace key persons if they leave or to fill new positions requiring key persons with appropriate experience. A significant portion of our compensation to our key employees is in the form of stock option grants. A prolonged depression in our stock price could make it difficult for us to retain our employees and recruit additional qualified personnel.

We do not maintain life insurance on any of our personnel. The loss of key employees, the failure of any key employee to perform or our inability to attract and retain skilled employees, as needed, or an inability to effectively plan for and implement a succession plan for key employees could harm our business.

Adverse changes in economic conditions and reduced spending on innovative medical technology may adversely impact our business.

The purchase of Renaissance is discretionary and requires our customers to make significant initial commitments of capital and other resources. In addition, purchase of Renaissance requires a commitment to purchase exclusively from us other products and services, including our single-use disposable components. Continuing weak economic conditions or reduction in healthcare technology spending, even if economic conditions improve, could adversely impact our business, operating results and financial condition in a number of ways, including by causing longer sales cycles, lower prices for our products and services and reduced unit sales.

11

Fluctuations in credit and financial market conditions could delay or prevent our customers from obtaining financing to purchase or lease a Renaissance system, which would adversely affect our business, financial condition and results of operations.

Due to the fluctuations in credit markets and currency exchange rates, our customers and overseas distributors may be delayed in obtaining, or may not be able to obtain, necessary financing for their purchases or leases of Renaissance. Shifts in the world economy that have systemic or local impact, the effects of EU sanctions on Russia and the drop in oil prices that affect its economy, or the continuing uncertainty regarding Greece’s solvency and its status as a member state in the European Union are examples of scenarios that might cause a significant effect on the European and even global markets. Such changes might in some instances lead to our customers or overseas distributors postponing ordering of a Renaissance system or the shipment and installation of previously ordered systems, cancelling their system orders, or cancelling their agreements with us. An increase in delays and order cancellations of this nature could adversely affect our product sales and revenues and, therefore, harm our business and results of operations.

Long lead times required by certain suppliers could prevent us from accurately forecasting demand for our products, which could adversely affect our operating results.

Market uncertainty makes it difficult for us, our customers, our overseas distributors and our suppliers to accurately forecast future product demand trends, which could cause us to order and/or produce excess products that can increase our inventory costs and result in obsolete inventory. Alternatively, this forecasting difficulty could cause a shortage of products, or materials used in our products, that could result in an inability to satisfy demand for our products and a resulting material loss of potential revenue.

In addition, some of our suppliers may require extensive advance notice of our requirements in order to produce products in the quantities we desire. This long lead time, which can be up to six months, may require us to place orders far in advance of the time when certain products will be offered for sale, thereby also making it difficult for us to accurately forecast demand for our products, exposing us to risks relating to shifts in consumer demand and trends and adversely affecting our operating results.

Because of the numerous risks and uncertainties associated with the development of medical devices, including future products, we are unable to estimate the exact amounts of capital outlays and operating expenditures necessary to complete the development of our products and successfully deliver commercial products to the market.

Our future capital requirements will depend on many factors, including but not limited to the following:

|

|

●

|

the revenue generated by sales of our current and future products;

|

|

|

●

|

our ability to manage our inventory;

|

|

|

●

|

the expenses we incur in selling and marketing our products and supporting our growth;

|

|

|

●

|

the costs and timing of regulatory clearance or approvals for new products or upgrades or changes to our current products;

|

|

|

●

|

the rate of progress, cost, and success or failure of on-going development activities;

|

|

|

●

|

the emergence of competing or complementary technological developments;

|

|

|

●

|

the costs of filing, prosecuting, defending and enforcing any patent or license claims and other intellectual property rights, or participating in litigation related activities;

|

|

|

●

|

the terms and timing of any collaborative, licensing, or other arrangements that we may establish;

|

|

|

●

|

the acquisition of businesses, products and technologies; and

|

|

|

●

|

general economic conditions and interest rates, including the continuing weak conditions.

|

12

Our reliance on third-party suppliers, including single source suppliers, for most of the components of Renaissance could harm our ability to meet demand for our products in a timely and cost effective manner.

We rely on third-party suppliers to manufacture and supply almost all of the components used in Renaissance, including a number of single source suppliers to provide us with several of the major components of Renaissance. We currently do not have long-term contracts with most of our suppliers. As a result, some of our suppliers are not required to provide us with any guaranteed minimum production levels, and we cannot guarantee that we will be able to obtain sufficient quantities of key components in the future. In addition, our reliance on third-party suppliers involves a number of risks, including, among other things:

|

|

●

|

our suppliers may encounter financial hardships as a result of unfavorable economic and market conditions unrelated to our demand for components, which could inhibit their ability to fulfill our orders and meet our requirements;

|

|

|

●

|

suppliers may fail to comply with regulatory requirements, be subject to lengthy compliance, validation or qualification periods, or make errors in manufacturing components that could negatively affect the efficacy or safety of our products or cause delays in supplying of our products to our customers;

|

|

|

●

|

newly identified suppliers may not qualify under the stringent regulatory standards to which our business is subject;

|

|

|

●

|

we or our suppliers may not be able to respond to unanticipated changes in customer orders, and if orders do not match forecasts, we or our suppliers may have excess or inadequate inventory of materials and components;

|

|

|

●

|

we may be subject to price fluctuations due to a lack of long-term supply arrangements for key components;

|

|

|

●

|

we may experience delays in delivery by our suppliers due to changes in demand from us or their other customers;

|

|

|

●

|

we or our suppliers may lose access to critical services and components, resulting in an interruption in the manufacture, assembly and shipment of our systems;

|

|

|

●

|

our suppliers may be subject to allegations by other parties of misappropriation of proprietary information in connection with their supply of products to us, which could inhibit their ability to fulfill our orders and meet our requirements;

|

|

|

●

|

fluctuations in demand for products that our suppliers manufacture for others may affect their ability or willingness to deliver components to us in a timely manner;

|

|

|

●

|

our suppliers may wish to discontinue supplying components or services to us (e.g., for risk management reasons); and

|

|

|

●

|

we may not be able to find new or alternative components or reconfigure our system and manufacturing processes in a timely manner if the necessary components become unavailable.

|

If any of these risks materialize, costs could significantly increase and our ability to meet demand for our products could be impacted. If we are unable to satisfy commercial demand for Renaissance or for our single-use disposable components in a timely manner, our ability to generate revenue would be impaired, market acceptance of our products could be adversely affected, and customers may instead purchase or use alternative products. In addition, we could be forced to secure new or alternative components through a replacement supplier. Securing a replacement supplier could be difficult, especially for complex components such as Renaissance components that are manufactured in accordance with our custom specifications. The introduction of new or alternative components may require design changes to our system that may be subject to FDA and other regulatory clearances or approvals. We may also be required to assess the new manufacturer’s compliance with all applicable regulations and guidelines, which could further impede our ability to manufacture our products in a timely manner. As a result, we could incur increased production costs, experience delays in deliveries of our products, suffer damage to our reputation and experience an adverse effect on our business and financial results.

13

The overall size and risk of turnover in our sales and marketing teams might impair our ability to generate revenues.

To reach our revenue targets, we need to expand and strengthen our U.S. direct sales force and our foreign sales channels. Developing a sales and marketing infrastructure is expensive and time consuming and an inability to develop such an organization in a timely manner could delay the successful adoption of our products. Additionally, any sales and marketing organization that we develop may be competing against the experienced and well-funded sales and marketing infrastructure of some of our competitors. We will face significant challenges and risks in developing our sales and marketing organization, including, among others:

|

|

●

|

our ability to recruit, train and retain adequate numbers of qualified sales and marketing personnel;

|

|

|

●

|

the ability of sales personnel to obtain access to surgeons and persuade adequate numbers of hospitals to purchase our products;

|

|

|

●

|

costs associated with hiring, maintaining and expanding a sales and marketing organization; and

|

|

|

●

|

government scrutiny with respect to promotional activities in the healthcare industry both domestically and abroad.

|

We believe that to sell and market our products effectively, we must establish a compelling clinical and commercial offering with our products. However, potential customers (e.g., surgeons and hospitals) sometimes have long-standing relationships with large, better known companies that dominate the medical devices industry through collaborative research programs and other relationships. Because of these existing relationships, some of which may be contractually enforced, surgeons and hospitals may be reluctant to adopt Renaissance, particularly if it competes with or has the potential to compete with or diminish the need/utilization of products supported through their own collaborative research program or by these existing relationships. Even if these surgeons and hospitals purchase Renaissance, they may be unwilling to enter into collaborative relationships with us to promote joint marketing programs or to provide us with clinical and financial data.

We face competition from large, well-established medical device companies that are likely to launch new navigation or robotic–based products, as well as new techniques and devices for minimally invasive approaches in spine surgeries.

Large, well-established medical device companies, such as Medtronic Inc., Stryker Corporation, and Brainlab AG, have navigation-based products with applications for spine surgeries that have a relatively low market share but which could be further developed and marketed with greater success. These companies are actively innovating in the field and offer their navigation systems with intra-operative 3-dimensional imaging systems that are often valuable to hospitals and physicians beyond spine surgeries but also in fields such as trauma, ear, nose and throat, and brain surgeries. Other companies, including Intuitive Surgical Inc. and Stryker Corporation, have developed or acquired robotic devices for use in other parts of the human anatomy that could be modified or improved to better compete in the spine and brain surgery markets. Even if these companies currently do not have an established presence in our fields, they may attempt to enter our markets and to apply their technologies to compete directly with us. For example, Intuitive Surgical’s da Vinci® robot has been clinically applied in several medical centers to perform anterior-approach spine surgeries. Based on information published by Globus Medical Inc., or Globus, it expects to receive FDA clearance for its surgical robotic positioning platform for spine, brain and trauma markets in the first half of 2016 and generate significant revenues in 2017. Globus’s robot is described as a robotic surgical aid for navigating and facilitating surgical access, implant sizing, positioning and placement, designed to enable surgeons to perform procedures more quickly and with greater accuracy, safety and reproducibility. Medtech SA, or Medtech, announced on December 1, 2014 the first surgical intervention with its ROSA™ Spine robot since it received the CE mark earlier that year. Medtech announced that they received FDA clearance in January 2016. This means that a surgeon interested in computer assisted spine surgery in 2016 will have a choice between 3 different robots for spine surgery and at least 3 intra-operative imaging systems coupled with navigation systems. We cannot assure that the surgeon will prefer our product over the current and evolving competition.

14

While we are unaware of any other current computer-assisted product or robotic-device that could directly compete with Renaissance at this time in the spine surgery market, it is likely that at some point there will be new market entrants, such as KB Medical with their AQrate robot. Many medical device competitors enjoy competitive advantages over us, including:

|

|

●

|

significantly greater name recognition;

|

|

|

●

|

longer operating histories;

|

|

|

●

|

established exclusive relations with healthcare professionals, customers and third-party payors;

|

|

|

●

|

established distribution networks;

|

|

|

●

|

a more compelling technology with greater clinical value;

|

|

|

●

|

competitive pricing;

|

|

|

●

|

additional lines of products and the ability to offer rebates or bundle products to offer higher discounts or incentives to gain a competitive advantage;

|

|

|

●

|

greater experience in conducting research and development, manufacturing, clinical trials, obtaining regulatory clearance for products and marketing approved products; and

|

|

|

●

|

greater financial and human resources for product development, sales and marketing and patent litigation.

|

There can be no assurance that we will be able to compete successfully against current or future competitors or that competition will not have a material adverse effect on our future revenues and, consequently, on our business, operating results and financial condition.

Medical device development is costly and involves continual technological change, which may render our current or future products obsolete.

Innovation is rapid and continuous in the medical device industry, and our competitors in the medical device industry make significant investments in research and development. If new products or technologies emerge that provide the same or superior benefits as our products at equal or lower cost, they could render our products obsolete or unmarketable. Because our products can have long development and regulatory clearance or approval cycles, we must anticipate changes in the marketplace and the direction of technological innovation and customer demands. In addition, we face increasing competition from well-financed medical device companies in our attempts to acquire such new technologies, products and businesses. As a result, we cannot be certain that our products will be competitive with current or future products and technologies.

Our success depends, in part, on our ability to enter the brain-surgery market, and this market has significant barriers to entry.

Computer-assisted surgeries are the accepted standard-of-care in brain procedures, and stereotactic frames and frameless navigation devices have dominated this market for almost two decades. There are currently 2 other dominant robotic devices for brain surgeries, which are Medtech’s ROSA™ robot and Renishaw’s Neuromate©. These products compete directly with Renaissance. As a result, we cannot be certain that surgeons will use our products or that our products will be competitive with current or future products and technologies. If we are unable to penetrate the brain-surgery market, we may not be able to generate the revenue necessary to develop a sustainable, profitable business.

15

We may encounter problems or delays in the assembly of our products or fail to meet certain regulatory requirements.

The current and intended future versions of Renaissance are complex and require the integration of a number of separate components and processes. To become profitable, we must assemble and test Renaissance in commercial quantities in compliance with regulatory requirements and at an acceptable cost. Increasing our capacity to assemble and test our products on a commercial scale will require us to improve internal efficiencies. We may encounter a number of difficulties in increasing our assembly and testing capacity, including:

|

|

●

|

managing production yields;

|

|

|

●

|

maintaining quality control and assurance;

|

|

|

●

|

providing component and service availability;

|

|

|

●

|

managing subcontractors;

|

|

|

●

|

hiring and retaining qualified personnel; and

|

|

|

●

|

complying with state, federal and foreign regulations.

|

If we are unable to satisfy commercial demand for our Renaissance system due to our inability to assemble and test the system in compliance with applicable regulations, our business and financial results, including our ability to generate revenue, would be impaired, market acceptance of our products could be materially adversely affected and customers may instead purchase or use competing products.

Any failure in our efforts to train surgeons or hospital staff adequately could result in lower than expected product sales and potential liabilities.

A critical component of our sales and marketing efforts is the training of surgeons and operating room staff to properly use Renaissance. We rely on surgeons and hospital staff to devote adequate time to learn to use our products. Convincing surgeons and hospital staff to dedicate the time and energy necessary for adequate training in the use of our system is challenging, and we cannot assure that we will be successful in these efforts. If surgeons or hospital staffs are not properly trained, they may misuse or ineffectively use our products. If nurses or other members of the hospital staff are not adequately trained to assist in using our Renaissance system, surgeons may be unable to use our products. Insufficient training may result in reduced system use, unsatisfactory patient outcomes, patient injury and related liability or negative publicity, which could have an adverse effect on our product sales or create substantial potential liabilities.

We will likely continue to experience extended and variable sales cycles, which could cause significant variability in our results of operations for any given quarter.

Our Renaissance system has a lengthy sales cycle because it is a major piece of capital equipment, the purchase of which will generally require the approval of senior management at hospitals, inclusion in the hospitals’ budget process for capital expenditures and, in some instances, a certificate of need from the state or other regulatory clearance. As a result, a relatively small number of units are currently installed each quarter. We estimate that the sales cycle of Renaissance will continue to take an average of nine months from the point of initial identification and contact with a qualified surgeon until closing of the purchase with the hospital. In addition, the introduction of new products could adversely impact our sales cycle as customers take additional time to assess them. Because of the lengthy sales cycle, the unit price of Renaissance and the relatively small number of systems installed each quarter, each installation of a Renaissance system can represent a significant component of our revenue for a particular quarter, particularly in the near term and during any other periods in which our sales volume is relatively low.

16

Certain factors that may contribute to variability in our operating results may include:

|

|

●

|

delays in shipments due, for example, to natural disasters or labor disturbances;

|

|

|

●

|

delays or unexpected difficulties in the manufacturing processes of our suppliers or in our assembly process;

|

|

|

●

|

timing of the announcement, introduction and delivery of new products or product upgrades by us and by our competitors;

|

|

|

●

|

timing and level of expenditures associated with expansion of sales and marketing activities and our overall operations;

|

|

|

●

|

changes in third-party coverage and reimbursement, changes in government regulation, or a change in a customer’s financial condition or ability to obtain financing; and

|

|

|

●

|

hospitals’ tendency to group purchases at the beginning of their budgetary cycle, which is different among hospitals.

|

These factors are difficult to forecast and may contribute to substantial fluctuations in our quarterly revenue and substantial variation from our projections, particularly during the periods in which our sales volume is low. Moreover, many of our expenses, such as office leases and most personnel costs, are relatively fixed. We may be unable to adjust spending quickly enough to offset any unexpected revenue shortfall. Accordingly, any shortfall in revenue may cause significant variation in operating results in any quarter. Based on the above factors, we believe that quarter-to-quarter comparisons of our operating results are not a good indication of our future performance. These and other potential fluctuations also mean that you will not be able to rely upon our operating results in any particular period as an indication of future performance.

We may fail to respond to cost containment efforts by our customers, which could have an adverse impact on our sales, financial condition and results of operations.

Some of our customers and potential customers have joined group purchasing organizations in an effort to contain costs; these group purchasing organizations negotiate pricing arrangements with medical supply manufacturers and distributors and make these negotiated prices available to the group purchasing organization’s affiliated hospitals and other members. If we fail to respond to the cost containment efforts of our customers and potential customers, we may lose sales or face downward pricing pressure, which could result in an adverse impact on our financial condition and results of operations.

If we receive a significant number of warranty claims or our Renaissance system units require significant amounts of service after sale, our costs will increase and our business and financial results will be adversely affected.

Sales of the our Renaissance system generally include a warranty and maintenance obligation on our part for services for a period of twelve months from the date Renaissance is installed at a customer’s facility. We also provide technical and other services to customers beyond the warranty period pursuant to a supplemental service plan sold with each system. If product returns or warranty claims are significant or exceed our expectations, we could incur unanticipated reductions in sales or additional expenditures for parts and service. In addition, our reputation could be damaged and our products may not achieve market acceptance.

17

Software defects may be discovered in our products.

Our Renaissance system incorporates sophisticated computer software. Complex software frequently contains errors, especially when first introduced. Because our products are designed to be used to perform complex surgical procedures, we expect that physicians and hospitals will have an increased sensitivity to the potential for software defects. We cannot assure you that our software will not experience errors or performance problems in the future. If we experience software errors or performance problems, we would likely also experience:

|

|

●

|

loss of revenue;

|

|

|

●

|

delay in market acceptance of our products;

|

|

|

●

|

damage to our reputation;

|

|

|

●

|

additional regulatory filings;

|

|

|

●

|

product recalls;

|

|

|

●

|

increased service or warranty costs; and

|

|

|

●

|

product liability claims relating to the software defects.

|

We may be subject to product liability claims, product actions, including product recalls, and other field or regulatory actions that could be expensive, divert management’s attention and harm our business.

Our business exposes us to potential liability risks, product actions and other field or regulatory actions that are inherent in the manufacturing, marketing and sale of medical device products, particularly those used in surgery. We may be held liable if our products cause injury or death or are found otherwise unsuitable or defective during usage. Renaissance incorporates mechanical and electrical parts, complex computer software and other sophisticated components, any of which can contain errors or failures. Complex computer software is particularly vulnerable to errors and failures, especially when first introduced. In addition, new products or enhancements to our existing products may contain undetected errors or performance problems that, despite testing, are discovered only after installation.

If any of our products are defective, whether due to design or manufacturing defects, improper use of the product or other reasons, we may voluntarily or involuntarily undertake an action to remove, repair, or replace the product at our expense. In some circumstances we will be required to notify regulatory authorities of an action pursuant to a product failure. We are also required to submit a Medical Device Report, or MDR, to the FDA for any incident in which our product may have caused or contributed to a death or serious injury or in which our product malfunctioned and, if the malfunction were to recur, would likely cause or contribute to death or serious injury.

A required notification to a regulatory authority or a failure to make a timely required notification could result in an investigation by regulatory authorities of our products, which could in turn result in field corrective actions, restrictions on the sale of the products, and civil or criminal penalties. In addition, because our products are designed to perform complex surgical procedures, defects could result in a number of complications, some of which could be serious and could cause significant harm to the patient or even cause death. The adverse publicity resulting from any of these events could cause surgeons or hospitals to review and potentially terminate their relationships with us.

The medical device industry has historically been subject to extensive litigation over product liability claims. We anticipate that as part of our ordinary course of business we will be subject to product liability claims alleging defects in the design, manufacture or labeling of our products. A product liability claim, regardless of its merit or eventual outcome, could result in significant legal defense costs and high punitive damage payments. Although we maintain product liability insurance, the coverage is subject to deductibles and limitations, and may not be adequate to cover future claims. Additionally, we may be unable to maintain our existing product liability insurance in the future at satisfactory rates or adequate amounts.

18

If coverage or reimbursement from third-party payors for procedures in which Renaissance is used, namely spinal fusions, is decreased or limited, hospitals may not purchase Renaissance and surgeons may perform fewer spinal fusions, which would harm our business and financial results.

Our ability to successfully commercialize Renaissance depends significantly on the availability of coverage and reimbursement for thoracic-lumbar spinal fusion procedures from third-party payors, including governmental programs such as Medicare and Medicaid, as well as private insurance and private health plans. Reimbursement is a significant factor considered by hospitals in determining whether to acquire new capital equipment such as our technology. Although our customers have been successful in obtaining coverage and reimbursement for procedures using our products, we cannot be assured that procedures using our technology will be covered or reimbursed by third-party payors in the future or that such reimbursements will not be reduced to the extent that they will adversely affect capital allocations for purchase of our Renaissance system.

As part of healthcare reform and other cost containment initiatives, the U.S. Congress, or the Congress, may pass legislation impacting coverage and reimbursement for healthcare services, including Medicare reimbursement to physicians and hospitals. Many private third-party payors look to Medicare’s coverage and reimbursement policies in setting their coverage policies and reimbursement amounts. If the Centers for Medicare & Medicaid Services, or CMS, the federal agency that administers the Medicare program, or Medicare contractors limit payments to hospitals or surgeons for thoracic-lumbar spinal fusion surgeries, private payors may similarly limit payments. In addition, state legislatures may enact laws limiting or otherwise affecting the level of Medicaid reimbursements. As a result, hospitals may not purchase Renaissance and surgeons may choose to decrease their volume of thoracic-lumbar spinal fusions, and, as a result, our business and financial results would be adversely affected.

Because hospitals receive a fixed reimbursement amount from Medicare for specified procedures or conditions, a hospital must absorb the cost of our products as part of the reimbursement payment it receives, which makes the hospital’s purchasing decisions more risky, particularly those related to expensive capital equipment.

Medicare pays acute care hospitals a prospectively determined amount for inpatient operating costs under the Medicare hospital inpatient prospective payment system, or PPS. Under the Medicare PPS, the prospective payment for a patient’s stay in an acute care hospital is determined by the patient’s condition and other patient data and procedures performed during the inpatient stay using a classification system known as diagnosis related groups, or DRGs. CMS implemented a revised version of the DRG system that uses Medicare Severity DRGs, or MS-DRGs, instead of the DRGs which Medicare used previously. The MS-DRGs are intended to more accurately account for the patient’s severity of illness when assigning each patient’s stay to a payment classification. Medicare pays a fixed amount to the hospital based on the MS-DRG into which the patient’s stay is assigned, regardless of the actual cost to the hospital of furnishing the procedures, items and services provided. Accordingly, acute care hospitals generally do not receive direct Medicare reimbursement under the PPS for the specific costs incurred in purchasing medical devices, except under limited circumstances. Rather, reimbursement for these costs is deemed to be included within the MS-DRG based payments made to hospitals for the services furnished to Medicare eligible inpatients in which the devices are utilized. Accordingly, a hospital must absorb the cost of our products as part of the payment it receives for the procedure in which the device is used. In addition, physicians that perform procedures in hospitals are paid a set amount by Medicare for performing such services under the Medicare Physician Fee Schedule. Medicare payment rates for both systems are established annually.

At this time, we do not know the extent to which hospitals and physicians would consider third-party reimbursement levels adequate to cover the cost of our products. Failure by hospitals and surgeons to receive an amount that they consider to be adequate reimbursement for procedures in which our products are used could deter them from purchasing or using our products and limit our sales growth. In addition, pre-determined MS-DRG payments or Medicare Physician Fee Schedule payments may decline over time, which could deter hospitals from purchasing our products or physicians from using them. If hospitals are unable to justify the costs of our products or physicians are not adequately compensated for procedures in which our products are utilized, they may refuse to purchase or use them, which would significantly harm our business.

Notwithstanding current or future FDA clearances, if granted, third-party payors may deny coverage and reimbursement if the payor determines that a therapeutic medical device is unnecessary, inappropriate, not cost-effective or experimental, or is used for a non-approved indication. Although we are not aware of any potential customer that has declined to purchase our Renaissance system based upon third-party payors’ coverage and reimbursement policies, cost control measures adopted by third-party payors may have a significant effect on surgeries performed using Renaissance or as to the levels of reimbursement.

19

Broad-based domestic and international government initiatives to reduce spending, particularly those related to healthcare costs, may reduce reimbursement rates for spinal surgery procedures, which will reduce the cost-effectiveness of our products.

Healthcare reforms, changes in healthcare policies and changes to third-party coverage and reimbursement, including recently enacted legislation reforming the U.S. healthcare system, may affect demand for our products and may have a material adverse effect on our financial condition and results of operations. There can be no assurance that current levels of reimbursement will not be decreased in the future, or that future legislation, regulation, or reimbursement policies of third-party payors will not adversely affect the demand for our products or our ability to sell products on a profitable basis.

The Patient Protection and Affordable Care Act, or PPACA, adopted in the United States in March 2010 and related regulations include new taxes impacting certain health-related industries, including medical device manufacturers. The legislation imposes significant new taxes on medical device makers in the form of a 2.3% excise tax on all U.S. medical device sales beginning in 2013. This excise tax applies to our medical devices. The Consolidated Appropriations Act, 2016, signed into law on December 18, 2015, includes a two-year suspension on the medical device excise tax. Thus, the medical device excise tax does not apply to the sale of a taxable medical device by the manufacturer, producer, or importer of the device during the period beginning on January 1, 2016, and ending on December 31, 2017. However, there is no guarantee that the excise tax will continue to be suspended by congressional action after this two-year period ends, and absent further congressional action, the excise tax will be reinstated for medical device sales beginning January 1, 2018.

Other significant measures contained in PPACA include initiatives to revise Medicare payment methodologies, initiatives to promote quality indicators in payment methodologies, initiatives related to the coordination and promotion of research on comparative clinical effectiveness of different technologies and procedures, and annual reporting requirements related to payments to physicians and teaching hospitals.

In addition, other legislative changes have been proposed and adopted since the PPACA was enacted. On August 2, 2011, the President of the United States, or the President, signed into law the Budget Control Act of 2011, which, among other things, created the Joint Select Committee on Deficit Reduction to recommend to Congress proposals in spending reductions. The Joint Select Committee did not achieve a targeted deficit reduction of at least $1.2 trillion for the years 2013 through 2021, triggering the legislation’s automatic reduction to several government programs. This includes reductions to Medicare payments to providers of 2% per fiscal year. On January 2, 2013, the President signed into law the American Taxpayer Relief Act of 2012, or the ATRA, which delayed for another two months the budget cuts mandated by these sequestration provisions of the Budget Control Act of 2011. On March 1, 2013, the President signed an executive order implementing sequestration, and on April 1, 2013, the 2% Medicare payment reductions went into effect. The ATRA also, among other things, reduced Medicare payments to several providers, including hospitals, imaging centers and cancer treatment centers, and increased the statute of limitations period for the government to recover overpayments to providers from three to five years. We expect that additional state and federal healthcare reform measures will be adopted in the future, any of which could limit the amounts that federal and state governments will pay for healthcare products and services, which could result in reduced demand for our products or additional pricing pressure.

We cannot predict whether future healthcare initiatives will be implemented at the federal or state level or internationally, or the effect any future legislation or regulation will have on us. The taxes imposed by PPACA and the expansion of government’s role in the U.S. healthcare industry may result in decreased profits to us, lower reimbursements by third-party payors for surgeries in which our products are used, and reduced medical procedure volumes, all of which may adversely affect our business, financial condition and results of operations, possibly materially.

20

Changing models for the provision of healthcare may affect the cost-effectiveness of Renaissance.

All third-party payors, whether governmental or private, whether within the United States or abroad, are developing increasingly sophisticated methods of controlling healthcare costs. These cost control methods include PPSs, capitated rates, benefit redesigns, pre-authorization or second opinion requirements prior to major surgery, an emphasis on wellness and healthier lifestyle interventions and an exploration of other cost-effective methods of delivering healthcare. These cost control methods also potentially limit the amount which healthcare providers may be willing to pay for medical technology which could, as a result, adversely affect our business and financial results. In addition, no uniform policy of coverage and reimbursement for medical technology exists among all these payors. Therefore, coverage and reimbursement for medical technology can differ significantly from payor to payor, and country to country.

We may attempt to acquire new products or technologies, and if we are unable to successfully complete these acquisitions or to integrate acquired businesses, products, technologies or employees, we may fail to realize expected growth.

Our success will depend, in part, on our ability to expand our product offerings and continue to offer the advanced computer assisted solutions for spine surgery and grow our business in response to changing technologies, customer demands and competitive pressures. In some circumstances, we may determine to do so through the acquisition of complementary businesses, products or technologies rather than through internal development. Successful acquisitions present a number of hurdles and risk, including:

|

|

●

|

the identification of suitable acquisition candidates can be difficult, time consuming and costly;

|

|

|

●

|

integrating any acquisitions that we make into our operations is difficult, time consuming, and expensive, and may involve new regulatory requirements; and

|

|

|

●

|

future acquisitions could result in potentially dilutive issuances of equity securities or the incurrence of debt, contingent liabilities or expenses, or other charges such as amortization of intangible assets, any of which could harm our business and materially adversely affect our financial results or cause a reduction in the price of our Ordinary Shares.

|

If we do not effectively manage our growth, we may be unable to successfully develop, market and sell our products.

In order to achieve our business objectives, we must continue to grow. Continued growth presents numerous challenges, including:

|

|

●

|

implementing appropriate operational and financial systems and controls;

|

|

|

●

|

expanding manufacturing and assembly capacity and increasing production;

|

|

|

●

|

developing our sales and marketing infrastructure and capabilities;

|

|

|

●

|

identifying, attracting and retaining qualified personnel in our areas of activity;

|

|

|

●

|

hiring, training, managing and supervising our personnel; and

|

|

|

●

|

continuous compliance with regulatory and quality assurance requirements.

|

We cannot be certain that our systems, controls, infrastructure and personnel will be adequate to support our future operations. Any failure to effectively manage our growth could impede our ability to successfully develop, market and sell our products and our business will be harmed.

21

If we are successful in our efforts to market and sell Renaissance outside of the United States, we will be subject to various risks relating to our international activities, which could adversely affect our business and financial results.

We are continuing to pursue international markets for the sale of our products and, as of December 31, 2015, there were 44 SpineAssist and Renaissance systems installed in Europe, Asia and Australia. As a result of these efforts and sales, we are exposed to risks separate and distinct from those we face in our U.S. operations. Our international business may be adversely affected by changing economic conditions in foreign countries. In addition, because international sales may be denominated in the functional currency of the country where the product is being shipped, increases or decreases in the value of the U.S. dollar relative to foreign currencies could affect our results of operations. Engaging in international business inherently involves a number of other difficulties and risks, including:

|

|

●

|

approval of product submissions with healthcare systems outside the United States;

|

|

|

●

|

gathering the clinical data that may be required for product submissions with healthcare systems outside the United States;

|

|

|

●

|

import restrictions and controls and other government regulation relating to technology;

|

|

|

●

|

pricing pressures that we may experience internationally;

|

|

|

●

|

the availability and level of reimbursement within prevailing foreign healthcare payment systems;

|

|

|

●

|

compliance with existing and changing applicable foreign regulatory laws and requirements, including but not limited to the European Medical Device Directive (Council Directive 93/42/EEC), the U.S. Foreign Corrupt Practices Act of 1977, or FCPA, OECD Convention on Combating Bribery of Foreign Public Officials in International Business Transactions;

|

|

|

●

|

foreign laws and business practices favoring local companies;

|

|

|

●

|

longer payment cycles; and

|

|

|

●

|

shipping delays.

|

Our exposure to each of these risks may increase our costs, impair our ability to market and sell our products and require significant management attention, resulting in harm to our business and financial results.

Our Renaissance system is used mainly for vertebral fixation procedures during thoracic-lumbar spinal fusion surgeries. Should the standard of care change and these procedures be abandoned as the treatment of choice for the current indications, it might negatively affect our business.

According to the Orthopedic Network News report dated October 2015, an estimated 409,400 thoracic-lumbar fusion surgeries will be performed in the United States during 2015. These surgeries are the standard of care in several common spinal pathologies. However, new treatment methods continue to be innovated, such as motion preserving techniques and devices that might not be benefitted by the use of Renaissance during such surgical procedures. In such a case, the appeal to surgeons in using Renaissance could be diminished and have a negative effect on our business performance.

We may face both reputational and SEC enforcement risks with respect to conflict minerals obligations.