UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

______________________________________________________

FORM 10-K

______________________________________________________

(Mark One)

| ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the fiscal year ended December 31 , 2023

OR

| TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 FOR THE TRANSITION PERIOD FROM TO | |||||

Commission File Number 001-38017

______________________________________________________

(Exact name of registrant as specified in its charter)

______________________________________________________

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | ||||

| (Address of principal executive offices, including zip code) | |||||

(Registrant’s telephone number, including area code)

______________________________________________________

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||||||||||||

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the Registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☒ No ☐

Indicate by check mark if the Registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act. Yes ☐ No ☒

Indicate by check mark whether the Registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the Registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the Registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark whether the Registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or emerging growth company. See the definition of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

☒ | Accelerated filer | ☐ | |||||||||

| Non-accelerated filer | ☐ | Smaller reporting company | |||||||||

| Emerging growth company | |||||||||||

If an emerging growth company, indicate by checkmark if the Registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☒

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to § 240.10D-1(b). ☐

Indicate by check mark whether the Registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

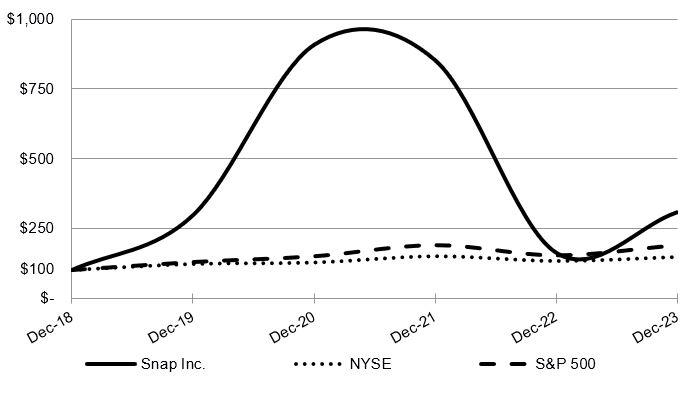

The aggregate market value of the voting and non-voting common equity held by non-affiliates of the Registrant, based on the closing price of the shares of Class A common stock on the New York Stock Exchange on June 30, 2023, the last business day of the Registrant’s most recently completed second fiscal quarter, was approximately $14.8 billion.

As of February 2, 2024, the Registrant had 1,396,476,171 shares of Class A common stock, 22,528,406 shares of Class B common stock, and 231,626,943 shares of Class C common stock outstanding.

Auditor Firm Id: 42 Auditor Name: Ernst & Young LLP Auditor Location: Los Angeles, CA, United States

TABLE OF CONTENTS

| Page | ||||||||

ii

NOTE REGARDING FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, or the Securities Act, and Section 21E of the Securities Exchange Act of 1934, as amended, or the Exchange Act, about us and our industry that involve substantial risks and uncertainties. All statements other than statements of historical facts contained in this report, including statements regarding guidance, our future results of operations or financial condition, our future stock repurchase programs or stock dividends, business strategy and plans, user growth and engagement, product initiatives, objectives of management for future operations, and advertiser and partner offerings, are forward-looking statements. In some cases, you can identify forward-looking statements because they contain words such as “anticipate,” “believe,” “contemplate,” “continue,” “could,” “estimate,” “expect,” “going to,” “intend,” “may,” “plan,” “potential,” “predict,” “project,” “should,” “target,” “will,” or “would” or the negative of these words or other similar terms or expressions. We caution you that the foregoing may not include all of the forward-looking statements made in this report.

You should not rely on forward-looking statements as predictions of future events. We have based the forward-looking statements contained in this Annual Report on Form 10-K primarily on our current expectations and projections about future events and trends, including our financial outlook, macroeconomic uncertainty, and geo-political conflicts, that we believe may continue to affect our business, financial condition, results of operations, and prospects. These forward-looking statements are subject to risks, uncertainties, and other factors described under “Risk Factor Summary” below, “Risk Factors” in Part I, Item 1A, and elsewhere in this Annual Report on Form 10-K, including among other things:

•our financial performance, including our revenues, cost of revenues, operating expenses, and our ability to attain and sustain profitability;

•our ability to generate and sustain positive cash flow;

•our ability to attract and retain users and partners;

•our ability to attract and retain advertisers;

•our ability to compete effectively with existing competitors and new market entrants;

•our ability to effectively manage our growth and future expenses;

•our ability to comply with modified or new laws, regulations, and executive actions applying to our business;

•our ability to maintain, protect, and enhance our intellectual property;

•our ability to successfully expand in our existing market segments and penetrate new market segments;

•our ability to attract and retain qualified team members and key personnel;

•our ability to repay or refinance outstanding debt, or to access additional financing;

•future acquisitions of or investments in complementary companies, products, services, or technologies; and

•the potential adverse impact of climate change, natural disasters, health epidemics, macroeconomic conditions, and war or other armed conflict on our business, operations, and the markets and communities in which we and our partners, advertisers, and users operate.

Moreover, we operate in a very competitive and rapidly changing environment. New risks and uncertainties emerge from time to time, and it is not possible for us to predict all risks and uncertainties that could have an impact on the forward-looking statements contained in this Annual Report on Form 10-K. The results, events, and circumstances reflected in the forward-looking statements may not be achieved or occur, and actual results, events, or circumstances could differ materially from those described in the forward-looking statements.

In addition, statements that “we believe” and similar statements reflect our beliefs and opinions on the relevant subject. These statements are based on information available to us as of the date of this Annual Report on Form 10-K. And while we believe that information provides a reasonable basis for these statements, that information may be limited or incomplete. Our statements should not be read to indicate that we have conducted an exhaustive inquiry into, or review of, all relevant information. These statements are inherently uncertain, and investors are cautioned not to unduly rely on these statements.

1

The forward-looking statements made in this Annual Report on Form 10-K relate only to events as of the date on which the statements are made. We undertake no obligation to update any forward-looking statements made in this report to reflect events or circumstances after the date of this report or to reflect new information or the occurrence of unanticipated events, including future developments related to geo-political conflicts and macroeconomic conditions, except as required by law. We may not actually achieve the plans, intentions, or expectations disclosed in our forward-looking statements, and you should not place undue reliance on our forward-looking statements. Our forward-looking statements do not reflect the potential impact of any future acquisitions, dispositions, joint ventures, restructurings, legal settlements, or investments.

Investors and others should note that we may announce material business and financial information to our investors using our websites (including investor.snap.com), filings with the U.S. Securities and Exchange Commission, or SEC, webcasts, press releases, investor letters, and conference calls. We use these mediums, including Snapchat and our website, to communicate with our members and the public about our company, our products, and other issues. It is possible that the information that we make available may be deemed to be material information. We therefore encourage investors and others interested in our company to review the information that we make available on our websites.

2

Risk Factor Summary

Our business is subject to significant risks and uncertainties that make an investment in us speculative and risky. Below we summarize what we believe are the principal risk factors but these risks are not the only ones we face, and you should carefully review and consider the full discussion of our risk factors in the section titled “Risk Factors,” together with the other information in this Annual Report on Form 10-K.

1. Our Strategy and Advertising Business

We operate in a highly competitive and rapidly changing environment so we must continually innovate our products and evolve our business model for us to succeed.

We emphasize rapid innovation and prioritize long-term user engagement over short-term financial conditions or results if we believe that it will benefit the aggregate user experience and improve our financial performance over the long term. Although we have achieved profitability in certain periods, we have a history of operating losses and, as a result of our long-term focus, we may prioritize investments and expenses we believe are necessary for our long-term growth over achieving short-term profitability. Investments in our future, including through new products or acquisitions, are inherently risky and may not pay off, which would adversely affect our ability to settle the principal and interest payments on our outstanding convertible senior notes or other indebtedness when due, and further delay or hinder our ability to sustain profitability. This in turn would hinder our ability to secure additional financing to meet our current and future financial needs on favorable terms, or at all.

We generate substantially all of our revenue from advertising. Our advertising business is most effective when our advertisers succeed. Driving their success requires continual investment in our advertising products and may be hindered by competitive challenges and various legal, regulatory, and operating system changes that make it more difficult for us to achieve and demonstrate a meaningful return for our advertisers. For example, on-going changes to privacy and data protection laws and mobile operating systems continue to present issues for us in measuring the effectiveness of advertisements on our services. Additionally, individuals are becoming increasingly resistant to the processing of personal data to deliver behavioral, interest-based, or targeted advertisements, and regulators are likewise scrutinizing such data processing activities, which could reduce the demand for our products and services and threaten our primary revenue stream. Alternative methods, to the extent we can develop such methods in compliance with current or future privacy and data protection laws, mobile operating system requirements, and other requirements, may take time to develop and be adopted by our advertisers and users, and may not be as effective as prior methods.

We believe that this impact on our targeting, measurement, and optimization capabilities has negatively affected and may continue to negatively affect our operating results. In addition, our advertising business is seasonal, volatile, and cyclical, which could result in fluctuations in our quarterly revenues and operating results, including the expectations of our business prospects.

Our business and operations have been, and in the future could be, adversely affected by events beyond our control, such as health epidemics and geo-political events and conflicts. In addition, macroeconomic factors like labor shortages and disruptions, supply chain disruptions, banking instability, and inflation continue to cause logistical challenges, increased input costs, and inventory constraints for our advertisers, which in turn may also halt or decrease advertising spending, and harm our business.

2. Our Community and Competition

We need to continually innovate and create new products, and enhance our existing products, to attract, retain, and grow our global community. Products that we create may fail to attract or retain users or partners, or to generate meaningful revenue, if any. In addition, we have and expect to continue to expand organically and through acquisitions, including in international markets, which we may not be able to effectively manage or scale. If our community does not see the value in our products or brand, or if competitors offer better alternatives, our community could easily switch to other services. Although we have experienced rapid growth in our community over the last few years, we have also experienced declines and there can be no assurance that declines won’t happen again.

Many of our competitors have significantly more resources and larger market shares than we do, which gives them advantages over us that can make it more difficult for us to succeed.

3

3. Our Partners

We primarily rely on Google, Apple, and Amazon to provide their mobile operating systems and other services for our applications and other core services, including our platform. If these partners do not provide their services as we expect, terminate their services, or change the terms, or their interpretation of the terms, of our agreements, or change the functionality of their mobile operating systems in ways that are adverse to us, our service may be interrupted and our product experience could be degraded, which may harm our reputation, increase our costs, or make it harder for us to sustain profitability. Many other parts of our business depend on partners, including content partners and advertising partners, so our success depends on our ability to attract and retain these partners.

4. Our Technology and Regulation

Our business is complex and success depends on our ability to rapidly innovate, the interoperability of our service on many different smartphones and mobile operating systems, and our ability to handle sensitive user data with the care our users expect. Because our systems and our products are constantly changing, we are susceptible to data breaches, cyberattacks, security incidents, bugs, and other vulnerabilities and errors in how our products work and are measured. We may also fail to maintain effective processes that report our metrics or financial results. Given the complexity of the systems involved and the rapidly changing nature of mobile devices and operating systems, we expect to encounter issues, particularly if we continue to expand in parts of the world where mobile data systems and connections are less stable.

We are also subject to complex and evolving federal, state, local, and foreign laws and regulations regarding privacy, data protection, biometric processing, content, artificial intelligence, taxes, and other matters, which are subject to change and have uncertain interpretations. Given the nature of our business, we are particularly susceptible to changes in such laws regarding privacy and data protection, which may require us to change our products and may impact our revenue stream. Any actual or perceived failure to comply with such legal and regulatory obligations, including in connection with our consent decree with the U.S. Federal Trade Commission, may lead to costly litigation or otherwise adversely impact our business.

We also must actively protect our intellectual property. We are subject to various legal proceedings, claims, class actions, inquiries, and investigations related to our intellectual property, which may be costly or distract management. We also rely on a variety of statutory and common-law frameworks for the content we provide our users, including the Digital Millennium Copyright Act, the Communications Decency Act, and the fair-use doctrine, each of which has been subject to adverse judicial, political, and regulatory scrutiny in recent times.

5. Our Team and Capital Structure

We need to attract and retain a high caliber team to maintain our competitive position. We may incur significant costs and expenses in maintaining and growing our team, and may lose valuable members of our team as we compete globally, including with our competitors, for key talent. A substantial portion of our employment costs is paid in our common stock, the price of which has been volatile, and our ability to attract and retain talent may be adversely affected if our shares decline in value.

Our two co-founders, who serve as our Chief Executive Officer and Chief Technology Officer, control over 99% of the voting power of our outstanding capital stock, which means they control substantially all outcomes submitted to stockholders. Class A common stockholders have no voting rights, unless required by Delaware law. This concentrated control may result in our co-founders voting their shares in their best interest, which might not always be in the interest of our stockholders generally.

4

NOTE REGARDING USER METRICS AND OTHER DATA

We define a Daily Active User, or DAU, as a registered Snapchat user who opens the Snapchat application at least once during a defined 24-hour period. We calculate average DAUs for a particular quarter by adding the number of DAUs on each day of that quarter and dividing that sum by the number of days in that quarter. DAUs are broken out by geography because markets have different characteristics. We define average revenue per user, or ARPU, as quarterly revenue divided by the average DAUs. For purposes of calculating ARPU, revenue by user geography is apportioned to each region based on our determination of the geographic location in which advertising impressions are delivered, as this approximates revenue based on user activity. This allocation differs from our components of revenue disclosure in the notes to our consolidated financial statements, where revenue is based on the billing address of the advertising customer. For information concerning these metrics as measured by us, see “Management’s Discussion and Analysis of Financial Condition and Results of Operations.”

Unless otherwise stated, statistical information regarding our users and their activities is determined by calculating the daily average of the selected activity for the most recently completed quarter included in this report.

While these metrics are determined based on what we believe to be reasonable estimates of our user base for the applicable period of measurement, there are inherent challenges in measuring how our products are used across large populations globally. For example, there may be individuals who attempt to create accounts for malicious purposes, including at scale, even though we forbid that in our Terms of Service and Community Guidelines. We implement measures in our user registration process and through other technical measures to prevent, detect and suppress that behavior, although we have not determined the number of such accounts.

Changes in our products, infrastructure, mobile operating systems, or metric tracking system, or the introduction of new products, may impact our ability to accurately determine active users or other metrics and we may not determine such inaccuracies promptly. We also believe that we don’t capture all data regarding each of our active users. Technical issues may result in data not being recorded from every user’s application. For example, because some Snapchat features can be used without internet connectivity, we may not count a DAU because we don’t receive timely notice that a user has opened the Snapchat application. This undercounting may increase as we grow in Rest of World markets where users may have poor connectivity. We do not adjust our reported metrics to reflect this underreporting. We believe that we have adequate controls to collect user metrics, however, there is no uniform industry standard. We continually seek to identify these technical issues and improve both our accuracy and precision, including ensuring that our investors and others can understand the factors impacting our business, but these technical issues and new issues may continue in the future, including if there continues to be no uniform industry standard.

Some of our demographic data may be incomplete or inaccurate. For example, because users self-report their dates of birth, our age-demographic data may differ from our users’ actual ages. And because users who signed up for Snapchat before June 2013 were not asked to supply their date of birth, we may exclude those users from our age demographics or estimate their ages based on a sample of the self-reported ages that we do have. If our active users provide us with incorrect or incomplete information regarding their age or other attributes, then our estimates may prove inaccurate and fail to meet investor expectations.

We count a DAU only when a user opens the application and only once per user per day. We believe this methodology more accurately measures our user engagement. We have multiple pipelines of user data that we use to determine whether a user has opened the application during a particular day, and becoming a DAU. This provides redundancy in the event one pipeline of data were to become unavailable for technical reasons, and also gives us redundant data to help measure how users interact with our application.

If we fail to maintain an effective analytics platform, our metrics calculations may be inaccurate. We regularly review, have adjusted in the past, and are likely in the future to adjust our processes for calculating our internal metrics to improve their accuracy. As a result of such adjustments, our DAUs or other metrics may not be comparable to those in prior periods. Our measures of DAUs may differ from estimates published by third parties or from similarly titled metrics of our competitors due to differences in methodology or data used.

5

PART I

Item 1. Business.

Overview

Snap Inc. is a technology company. We believe the camera presents the greatest opportunity to improve the way people live and communicate. We contribute to human progress by empowering people to express themselves, live in the moment, learn about the world, and have fun together.

Our flagship product, Snapchat, is a visual messaging application that enhances your relationships with friends, family, and the world. Visual messaging is a fast, fun way to communicate with friends and family using augmented reality, video, voice, messaging, and creative tools. Snaps are deleted by default to mimic real-life conversations, so there is less pressure to look popular or perfect when creating and sending images on Snapchat. By reducing the friction typically associated with creating and sharing content, Snapchat has become one of the most used cameras in the world.

The camera is a powerful tool for communication and the entry point for augmented reality experiences. By opening directly to the camera, Snapchat empowers our community to express themselves instantly and offers millions of augmented reality Lenses for self expression, learning, and play. In the way that the flashing cursor became the starting point for most products on desktop computers, we believe the camera screen will be the starting point for most products on smartphones. This is because images created by smartphone cameras contain more context and richer information than other forms of input like text entered on a keyboard. Given the magnitude of this opportunity, we are investing and innovating to continue to deliver products and services that are differentiated and that are better able to reflect and improve our life experiences.

Snapchat

Snapchat is our core mobile device application and contains five distinct tabs, complemented by additional tools that function outside of the application. With a breadth of visual messaging and content experiences available within the application, Snapchatters can interact with any or all of the five tabs.

Camera: The Camera is a powerful tool for communication and the entry point for augmented reality experiences in Snapchat. Snapchat opens directly to the Camera, making it easy to create a Snap and send it to friends. Our augmented reality, or AR, capabilities within our Camera allow for creativity and self-expression. We offer millions of Lenses, created by both us and our community, along with creative tools and licensed music and audio clips, which make it easy for people to personalize and contextualize their Snaps. We also offer voice and scanning technology within our Camera. While Snaps are deleted by default to mimic real-life conversations, users can save their creativity through a searchable collection of Memories stored on both their Snapchat account and their mobile device. A user can also create Snaps on our wearable devices, Spectacles. Spectacles connect seamlessly with Snapchat and capture photos and video from a human perspective. Our latest version of Spectacles, designed for creators, overlays AR Lenses directly onto the world.

Visual Messaging: Visual Messaging is a fast, fun way to communicate with friends and family using augmented reality, video, voice, messaging, and creative tools. We also offer My AI, our AI-powered chatbot, which helps our community foster creativity and connection with friends, receive real-world recommendations, and learn more about their interests and favorite subjects. They can also communicate through our proprietary personalized avatar tool, Bitmoji, and its associated contextual stickers and images, which integrate seamlessly into both mobile devices and desktop browsers.

Snap Map: Snap Map is a live and highly personalized map that allows Snapchatters to connect with friends and explore what is going on in their local area. Snap Map makes it easy to locate nearby friends who choose to share their location, view a heatmap of recent Snaps posted to Our Story by location, and locate local businesses. Places, rich profiles of local businesses that include information such as store hours and reviews, overlay specialized experiences from select partners on top of Snap Map, and allow Snapchatters to take direct actions from Snap Map, such as sharing a favorite store, ordering takeout, or making a reservation.

Stories: Stories are a fun way to stay connected with people you care most about. Stories feature content from a Snapchatter’s friends, our community, and our content partners. Friends Stories allow our community to express themselves in narrative form through photos and videos, shown in chronological order, to their friends. The Discover section of this tab displays curated content based on a Snapchatter’s subscriptions and interests, and features news and

6

entertainment from both our creator community and publisher partners. We also offer Public Profiles, as a way for our creator community and our advertising partners to memorialize and scale their content and AR Lenses on our platform.

Spotlight: Spotlight showcases the best of Snapchat, helping people discover new creators and content in a personalized way. Here we surface the most entertaining Snaps from our community all in one place, which becomes tailored to each Snapchatter over time based on their preferences and favorites. The Trending page allows Snapchatters to discover and engage with popular topics and genres.

Additionally, we offer Snapchat+, our subscription product that provides subscribers access to exclusive, experimental, and pre-release features. Snapchat+ offers a variety of features from allowing Snapchatters to customize the look and feel of their app, to giving special insights into their friendships. We also offer Snapchat for Web, a browser-based product that brings Snapchat’s signature capabilities to the web.

Our Partner Ecosystem

Many elements and features of Snapchat are enhanced by our expansive partner ecosystem that includes developers, creators, publishers, and advertisers, among others. We help them create and bring diverse content and experiences into Snapchat, leverage Snapchat capabilities in their own applications and websites, and use advertising to promote these and other experiences to our large, engaged, and differentiated user base. We seek to reward our partner ecosystem for their creativity, and continue to support them as they grow their audience and build their business on Snapchat.

Developers are able to integrate with Snapchat and its core technologies, like Snap’s AR Camera and Bitmoji, through a variety of tools. Creative Kit gives developers and their communities a seamless sharing experience from their app directly to Snapchat. Through Camera Kit, our partners can embed Snap’s AR platform directly into their application, extending the use of AR beyond self-expression and communication use cases. We also provide developers a turnkey suite of tools and services that enable them to create AR Lenses and track the performance of those through analytics. Finally, developers can bring an inclusive mode of identity and expression to their apps and games with our Bitmoji for Developers APIs and SDKs.

AR creators can use Lens Studio, our powerful desktop application designed for creators and developers, to build augmented reality experiences for Snapchatters. Spotlight creators can utilize our content creation tools to reach millions of Snapchatters and build their businesses through various monetization opportunities. Our Creator Marketplace connects both AR and Spotlight creators directly with our advertising partners. We provide monetizable opportunities through programs like the Snap Lens Network and Ghost, which provide grants to support AR product development across many industries. We also support our content creator community through a number of programs, including advertising revenue sharing on our mid-roll advertisements in Snap Stars’ Stories.

Publisher partners can expand their audiences and monetize content through our Discover platform. In addition, we work with various telecommunications providers and original equipment manufacturers, particularly as we build our presence in new markets.

Our Advertising Products

We connect both brand and direct response advertisers to Snapchatters globally. Our ad products are built on the same foundation that makes our consumer products successful. This means that we can take the things we learn while creating our consumer products and apply them to building innovative and engaging advertising products familiar to our community.

AR Ads: Advertising through Snap’s AR tools unlocks the ability to reach a unique audience in a highly differentiated way through AR Lenses. AR Lenses are designed through our camera to take advantage of the reach and scale of our augmented reality platform to create visually engaging 3D experiences, including the ability to visualize and try on products such as beauty, apparel, accessories, and footwear. AR Lenses can be memorialized on Snapchat, through Public Profiles that aggregate content and lenses in a single, easy to find place.

7

Snap Ads: We let advertisers tell their stories the same way our users do, using full screen videos with sound. These also allow advertisers to integrate additional experiences and actions directly within these advertisements, including watching a long-form video, visiting a website, or installing an app. Snap Ads include the following:

•Single Image or Video Ads: These are full screen ads that are skippable, and can contain an attachment to enable Snapchatters to swipe up and take action.

•Story Ads: Story Ads are branded tiles that live within the Discover section of the Stories tab that can be either video ads or a series of 3 to 20 images.

•Collection Ads: Collection Ads feature four tappable tiles to showcase multiple products, giving Snapchatters a frictionless way to browse and buy.

•Dynamic Ads: Dynamic ads leverage our machine learning algorithm to match a product catalog to serve the right ad to the right Snapchatter at the right time.

•Commercials: Commercials are non-skippable for six seconds, but can last up to three minutes. These ads appear within Snapchat’s curated content.

Campaign Management and Delivery: We aim to continually improve the way these ad formats are purchased and delivered. We have invested heavily to build our self-serve advertising platform, which provides automated, sophisticated, and scalable ad buying and campaign management.

We offer the ability to bid for advertisements that are designated to drive Snapchatters to: visit a website, make a purchase, visit a local business, call or text a business, watch a story or video, download an app, or return to an app, among others. Additionally, our delivery framework continues to optimize relevance of ads across the entire platform by determining the best ad to show to any given user based on their real-time and historical attributes and activity. This decreases the number of wasted impressions while improving the effectiveness of the ads that are shown to our community. This helps advertisers increase their return on investment by providing more refined targeting, the ability to test and learn with different creatives or campaign attributes in real time, and the dynamics of our self-serve pricing.

Measuring Advertising Effectiveness: We offer first-party measurement solutions and we support our advertising partners preferred third-party measurement solutions to provide a vast array of analytics on campaign attributes like reach, frequency, demographics, and viewability; changes in perceptions like brand favorability or purchase intent; and lifts in actual behavior like purchases, foot traffic, app installs, and online purchases.

Technology

Our research and development efforts focus on product development, advertising technology, and large-scale infrastructure.

Product Development: We work relentlessly and invest deliberately to create and improve products for our community and our partners. We develop a wide range of products related to visual messaging and storytelling that are powered by a variety of new technologies.

Advertising Technology: We constantly develop and expand our advertising products and technology. In an effort to provide a strong and scalable return on investment to our advertisers, our advertising technology roadmap centers around improving our delivery framework, measurement capabilities, and self-serve tools.

Large-scale Infrastructure: We spend considerable resources and investment on the underlying architecture that powers our products, such as optimizing the delivery of billions of videos to hundreds of millions of people around the world every day. We currently partner with third party providers to support the infrastructure for our growing needs. These partnerships have allowed us to scale quickly without upfront physical infrastructure costs, allowing us to focus our efforts on product innovation.

Employees and Culture

We seek to be a force for good through our products, our work to strengthen our communities, our efforts to make a positive impact on the planet, and our inclusive workplace.

8

Supporting Our Team: Our values at Snap are being kind, smart, and creative, and we put those values into action through how we support our team and how our team supports one another. Council, which is a practice of active listening that promotes open-mindedness and cultivates empathy and compassion among participants, helps us build and sustain a community steeped in integrity, connection, collaboration, creativity, and kindness. Our talent development programs seek to unlock potential by helping team members advance, learn, and grow in a fair and equitable way at Snap. We focus on the health and well-being of our employees through programs and benefits that support their physical, emotional, and financial fitness. To attract and retain the best talent, we aim to offer challenging work in an environment that enables our employees to have a direct meaningful contribution to new and exciting projects. Underlying these values is our commitment to ethical conduct where we work to instill in our team that acting with integrity means being your whole self, being honest, and doing the right thing.

Diversity, Equity, and Inclusion: Snap has long supported Diversity, Equity and Inclusion, or DEI, initiatives, and we have made progress on a number of fronts, including diversifying our board of directors and executive leadership, introducing new accountability around DEI outcomes, maintaining an allyship program to inspire a more inclusive culture, and enhancing our recruiting process to continue driving diverse hiring. To aid in our mission, we publish a Diversity Annual Report that discusses our goals with respect to diversity, equity, and inclusion efforts. This report outlines our beliefs around the idea that an inclusive workplace and inclusive products are central to achieving that purpose. This report is excerpted in our broader CitizenSnap Report that details the work we’re doing to support our communities, our planet, and our team, and is available on our website at www.snap.com.

Human Capital: As part of our human capital resource objectives, we seek to recruit, retain, and incentivize our highly talented existing and future employees. We believe that creating an inclusive environment where team members can grow, develop, and be their true selves is critical to attracting and retaining talent. Our compensation philosophies also align to that belief.

Our compensation philosophy is based around building a culture of ownership and high performance by putting both impact and our values at the center of our performance feedback process and pay outcomes. We utilize equity as part of our compensation practices to drive a long-term orientation and have committed to paying a minimum living wage for all employees globally.

As of December 31, 2023, we had 5,289 full-time employees, of whom approximately 54% are in engineering roles involved in the design, development, support, and manufacture of new and existing products and processes.

Climate Change: Our commitment to combating climate change remains unchanged. In 2021, we adopted science-based emissions reduction targets approved by the Science Based Targets Initiative. Additionally, in 2021, we achieved carbon neutrality from our founding in 2011 through 2020. In 2023 and 2022, we maintained our carbon-neutral status by purchasing offsets to emissions attributable to Snap as of December 31, 2022 and 2021, respectively. We remain committed to achieve net negative carbon emissions by 2030. In 2023 and 2022, we purchased renewable energy certificates covering all electricity consumed in our global operations for the years ended December 31, 2022 and 2021, respectively.

Our Commitment to Privacy

Our approach to privacy is simple: Be upfront, offer choices, and never forget that our community comes first.

We built Snapchat as an antidote to the context-less communication that has plagued “social media.” Not so long ago, a conversation among friends would be just that: a private communication in which you knew exactly who you were talking to, what you were talking about, and whether what you were saying was being memorialized for eternity. Somewhere along the way, social media—by prioritizing virality and permanence—sapped conversations of this valuable context and choice. When we began to communicate online, we lost some of what made communication great: spontaneity, emotion, honesty—the full range of human expression that makes us human in the first place.

We don’t think digital communication has to be this way. That’s why choice matters. We build products and services that emphasize the context of a conversation—who, when, what, and where something is being said. If you don’t have the autonomy to shape the context of a conversation, the conversation will simply be shaped by the permanent feeds that homogenize online conversations.

9

When you read our Privacy Policy, we hope that you’ll notice how much we care about the integrity of personal communication. For starters, we’ve written our Privacy Policy in plain language because we think it’s important that everyone understands exactly how we handle their information. Otherwise, it’s hard to make informed choices about how you communicate. We’ve also created a robust Safety and Privacy Hub where we show that context and choice are more than talking points. There, we point out the many ways that users can control who sees their Snaps and Stories, and explain how long content will remain on our servers, how users can manage the information that we do have about them, and much more. This is where you’ll also find our Transparency Report in which we provide insight into these efforts and visibility into the nature and volume of content reported on our platform.

We also understand that privacy policies—no matter how ambitious—are only as good as the people and practices behind those policies. When someone trusts us to transmit or store their information, we know we have a responsibility to protect that information and we work hard to keep it secure. New features go through an intense privacy-review process—we debate pros and cons, and we work hard to build products we’re proud of and that we’ll want to use. We use Snapchat constantly, both at work and in our personal lives, and we handle user information with the same care that we want for our family, our friends, and ourselves.

Competition

We compete with other companies in every aspect of our business, particularly with companies that focus on mobile engagement and advertising. Many of these companies, such as Alphabet (including Google and YouTube), Apple, ByteDance (including TikTok), Meta (including Facebook, Instagram, Threads, and WhatsApp), Pinterest, and X (formerly Twitter), may have greater financial and human resources and, in some cases, larger user bases. Given the breadth of our product offerings, we also compete with companies that develop products or otherwise operate in the mobile, camera, communication, content, and advertising industries that offer, or will offer, products and services that may compete with Snapchat features or offerings. Our competitors span from internet technology companies and digital platforms, to traditional companies in print, radio, and television sectors to underlying technologies like default smartphone cameras and messaging. Additionally, our competition for engagement varies by region. For instance, we face competition from companies like Kakao, LINE, Naver (including Snow), and Tencent in Asia.

We compete to attract and retain our users’ attention, both in terms of reach and engagement. Since our products and those of our competitors are typically free, we compete based on our brand and the quality and nature of our product offerings rather than on price. As such, we invest heavily in constantly improving and expanding our product lines.

We also compete with other companies to attract and retain partners and advertisers, which depends primarily on our reach and ability to deliver a strong return on investment.

Finally, we compete to attract and retain highly talented individuals, including software engineers, designers, and product managers. In addition to providing competitive compensation packages, we compete for talent by fostering a culture of working hard to create great products and experiences and allowing our employees to have a direct meaningful contribution to new and exciting projects.

Seasonality in Our Business

We have historically seen seasonality in our business. Overall advertising spend tends to be strongest in the fourth quarter of the calendar year, and we have observed a similar pattern in our historical revenue. We have also experienced seasonality in our user engagement, generally seeing lower engagement during summer months and higher engagement in December.

Intellectual Property

Our success depends in part on our ability to protect our intellectual property and proprietary technologies. To protect our proprietary rights, we rely on a combination of intellectual property rights in the United States and other jurisdictions, including patents, trademarks, copyrights, trade secret laws, license agreements, internal procedures, and contractual provisions. We also enter into confidentiality and invention assignment agreements with our employees and contractors and sign confidentiality agreements with third parties. Our internal controls are designed to restrict access to proprietary technology.

10

As of December 31, 2023, we had approximately 3,174 issued patents and approximately 3,111 filed patent applications in the United States and foreign countries relating to our camera platform and other technologies. Our issued patents will expire between 2024 and 2047. We may not be able to obtain protection for our intellectual property, and our existing and future patents, trademarks, and other intellectual property rights may not provide us with competitive advantages or distinguish our products and services from those of our competitors.

We license content, trademarks, technology, and other intellectual property from our partners, and rely on our license agreements with those partners to use the intellectual property. We also enter into licensing agreements with third parties to receive rights to patents and other know-how. Third parties may assert claims related to intellectual property rights against our partners or us.

Other companies and “non-practicing entities” that own patents, copyrights, trademarks, trade secrets, and other intellectual property rights related to the mobile, camera, communication, content, internet, and other technology-related industries frequently enter into litigation based on allegations of infringement, misappropriation, and other violations of intellectual property or other rights. As our business continues to grow and competition increases, we will likely face more claims related to intellectual property and litigation matters.

Government Regulation

We are subject to many federal, state, local, and foreign laws and regulations, including those related to privacy, rights of publicity, data protection, content regulation, intellectual property, health and safety, competition, protection of minors, consumer protection, employment, money transmission, import and export restrictions, gift cards, electronic funds transfers, anti-money laundering, advertising, algorithms, encryption, and taxation. These laws and regulations are constantly evolving and may be interpreted, applied, created, or amended in a manner that could harm our business. Compliance with these laws and regulations has not had, and is not expected to have, a material effect on our capital expenditures, results of operations, and competitive position as compared to prior periods, and we do not currently anticipate material capital expenditures for environmental control facilities.

In December 2014, the Federal Trade Commission resolved an investigation into some of our early practices by handing down a final order. That order requires, among other things, that we establish a robust privacy program to govern how we treat user data. During the 20-year lifespan of the order, we must complete biennial independent privacy audits. In June 2014, we entered into a 10-year assurance of discontinuance with the Attorney General of Maryland implementing similar practices, including measures to prevent minors from creating accounts and providing annual compliance reports. Violating existing or future regulatory orders or consent decrees could subject us to substantial monetary fines and other penalties that could negatively affect our financial condition and results of operations.

Furthermore, foreign data protection, privacy, consumer protection, content regulation, and other laws and regulations are often more restrictive than those in the United States. It is possible that certain governments may seek to block or limit our products or otherwise impose other restrictions that may affect the accessibility or usability of any or all our products for an extended period of time or indefinitely. Not all of our products are available in all locations and may not be due to such laws and regulations. Our public policy team monitors legal and regulatory developments in the United States, as well as many foreign countries, and communicates with policymakers and regulators in the United States and internationally.

Information about Segment and Geographic Revenue

Information about segment and geographic revenue is set forth in Notes 1 and 2 of the notes to our consolidated financial statements included in “Financial Statements and Supplementary Data” in this Annual Report on Form 10-K.

Available Information

Our website address is www.snap.com. Our Annual Report on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K, and amendments to these reports filed pursuant to Sections 13(a) and 15(d) of the Exchange Act are filed with the SEC. Such reports and other information filed or furnished by us with the SEC are available free of charge on our website at investor.snap.com when such reports are available on the SEC’s website. We use our website, including investor.snap.com, as a means of disclosing material non-public information and for complying with our disclosure obligations under Regulation FD.

11

Information contained in, or accessible through, the websites referred to in this Annual Report on Form 10-K is not incorporated into this filing. Further, our references to website addresses are only as inactive textual references.

Item 1A. Risk Factors.

You should carefully consider the risks and uncertainties described below, together with all the other information in this Annual Report on Form 10-K, including “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and the consolidated financial statements and the related notes. If any of the following risks actually occurs (or if any of those discussed elsewhere in this Annual Report on Form 10-K occurs), our business, reputation, financial condition, results of operations, revenue, and future prospects could be seriously harmed. The risks and uncertainties described below are not the only ones we face. Additional risks and uncertainties that we are unaware of, or that we currently believe are not material, may also become important factors that adversely affect our business. Unless otherwise indicated, references to our business being seriously harmed in these risk factors will include harm to our business, reputation, financial condition, results of operations, revenue, and future prospects. In that event, the market price of our Class A common stock could decline, and you could lose part or all of your investment.

Risks Related to Our Business and Industry

Our ecosystem of users, advertisers, and partners depends on the engagement of our user base. Our user base growth rate has declined in the past and it may do so again in the future. If we fail to retain current users or add new users, or if our users engage less with Snapchat, our business would be seriously harmed.

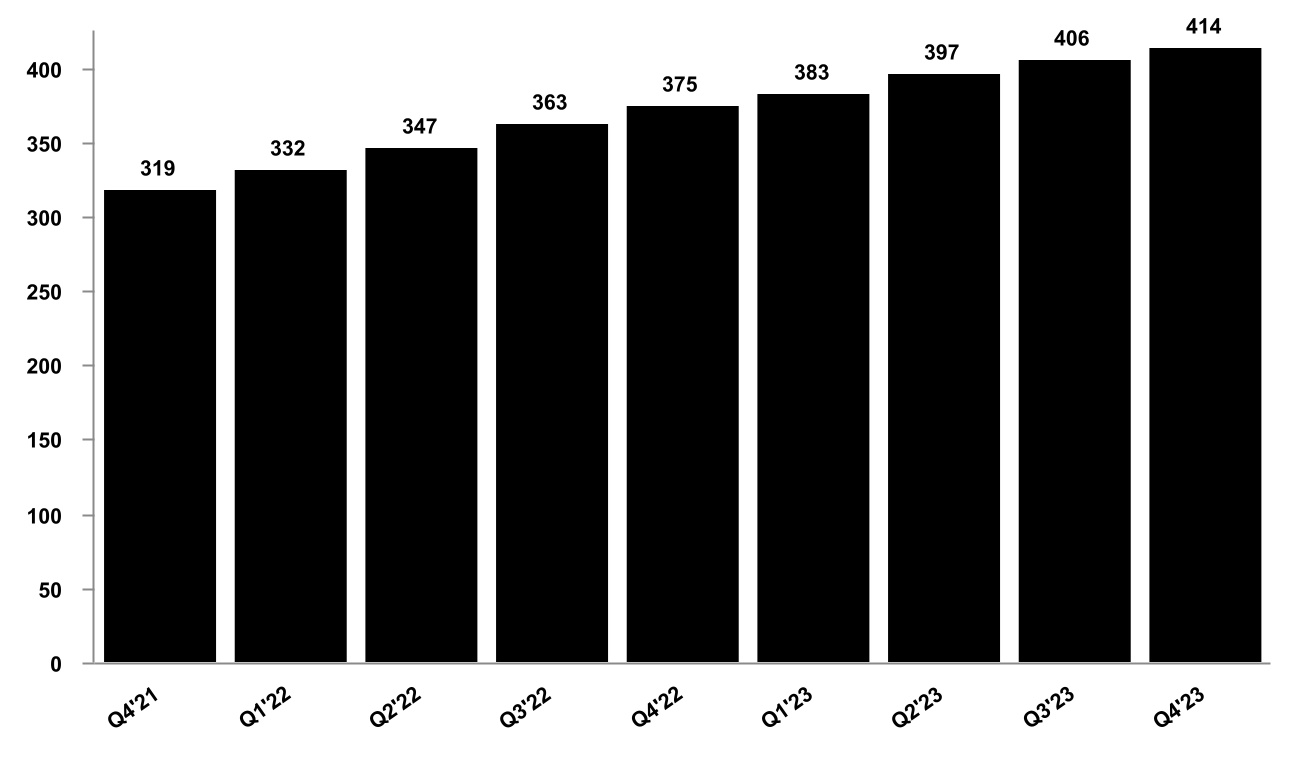

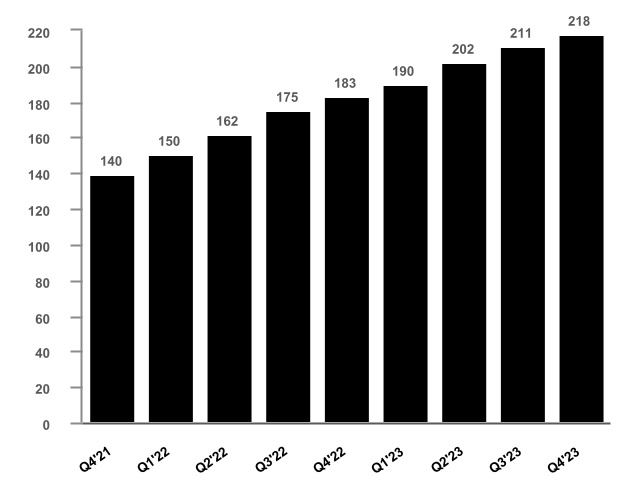

We had 414 million daily active users, or DAUs, on average in the quarter ended December 31, 2023. We view DAUs as a critical measure of our user engagement, and adding, maintaining, and engaging DAUs have been and will continue to be necessary. Our DAUs and DAU growth rate have declined in the past and they may decline in the future due to various factors, including as the size of our active user base increases, as we achieve higher market penetration rates, as we face continued competition for our users and their time, or if there are performance issues with our service. In addition, as we achieve maximum market penetration rates among younger users in developed markets, future growth in DAUs will need to come from older users in those markets or from developing markets, which may not be possible or may be more difficult, expensive, or time-consuming for us to achieve. While we may experience periods when our DAUs increase due to products and services with short-term popularity, we may not always be able to attract new users, retain existing users, or maintain or increase the frequency and duration of their engagement if current or potential new users do not perceive our products to be fun, engaging, or useful. In addition, because our products typically require high bandwidth data capabilities for users to benefit from all of the features and capabilities of our application, many of our users live in countries with high-end mobile device penetration and high bandwidth capacity cellular networks with large coverage areas. We therefore do not expect to experience rapid user growth or engagement in regions with either low smartphone penetration or a lack of well-established and high bandwidth capacity cellular networks. As our DAU growth rate continues to slow or if the number of DAUs becomes stagnant, or we have a decline in DAUs, our financial performance will increasingly depend on our ability to elevate user activity or increase the monetization of our users.

Snapchat is free and easy to join, the barrier to entry for new entrants in our business is low, and the switching costs to another platform are also low. Moreover, the majority of our users are 18-34 years old. This demographic may be less brand loyal and more likely to follow trends, including viral trends, than other demographics. These factors may lead users to switch to another product, which would negatively affect our user retention, growth, and engagement. Snapchat also may not be able to penetrate other demographics in a meaningful manner. Falling user retention, growth, or engagement could make Snapchat less attractive to advertisers and partners, which may seriously harm our business. In addition, we continue to compete with other companies to attract and retain our users’ attention. There are many factors that could negatively affect user retention, growth, and engagement, including if:

•users engage more with competing products instead of ours;

•our competitors continue to mimic our products or improve on them;

•we fail to introduce new and exciting products and services or those we introduce or modify are poorly received;

•our products fail to operate effectively or compatibly on the iOS or Android mobile operating systems;

•we are unable to continue to develop products that work with a variety of mobile operating systems, networks, and smartphones;

•we do not provide a compelling user experience because of the decisions we make regarding the type and frequency of advertisements that we display or the structure and design of our products;

12

•we are unable to combat bad actors, spam, or other hostile or inappropriate usage on our products;

•there are changes in user sentiment about the quality or usefulness of our products in the short-term, long-term, or both;

•there are concerns about the privacy implications, safety, or security of our products and our processing of personal data;

•our content partners do not create content that is engaging, useful, or relevant to users;

•our content partners decide not to renew agreements or devote the resources to create engaging content, or do not provide content exclusively to us;

•advertisers and partners display ads that are untrue, offensive, or otherwise fail to follow our guidelines;

•our products are subject to increased regulatory scrutiny or approvals, including from foreign privacy regulators, or there are changes in our products that are mandated or prompted by legislation, regulatory authorities, executive actions, or litigation, including settlements or consent decrees, that adversely affect the user experience;

•technical or other problems frustrate the user experience or negatively impact users' trust in our service, including by providers that host our platforms, particularly if those problems prevent us from delivering our product experience in a fast and reliable manner, or cyberattacks, breaches, or other security incidents that compromise our sensitive user data;

•we fail to provide adequate service to users, advertisers, or partners;

•we do not provide a compelling user experience to entice users to use the Snapchat application on a daily basis, or our users don’t have the ability to make new friends to maximize the user experience;

•we, our partners, or other companies in our industry segment are the subject of adverse media reports or other negative publicity, some of which may be inaccurate or include confidential information that we are unable to correct or retract;

•we do not maintain our brand image or our reputation is damaged; or

•our current or future products reduce user activity on Snapchat by making it easier for our users to interact directly with our partners.

Any decrease to user retention, growth, or engagement could render our products less attractive to users, advertisers, or partners, and would seriously harm our business.

We generate substantially all of our revenue from advertising. The failure to attract new advertisers, the loss of advertisers, or a reduction in how much they spend could seriously harm our business.

Substantially all of our revenue is generated from third parties advertising on Snapchat. For the years ended December 31, 2023, 2022, and 2021, advertising revenue accounted for approximately 96%, 99%, and 99% of our total revenue, respectively. Even though we have introduced other revenue streams, including a subscription model for one of our products, we still expect this trend to continue for the foreseeable future. Most advertisers do not have long-term advertising commitments with us, and our efforts to establish long-term commitments may not succeed.

Our advertising customers range from small businesses to well-known brands, and may include advertising resellers. Many of our customers spend a relatively small portion of their overall advertising budget with us, but some customers have devoted meaningful budgets that contribute more significantly to our total revenue. In addition, advertisers may view some of our advertising solutions as experimental and unproven, or prefer certain of our products over others. Advertisers, including our customers who have devoted meaningful advertising budgets to our product, will not continue to do business with us if we do not deliver advertisements in an effective manner, or if they do not believe that their investment in advertising with us will generate a competitive return relative to other alternatives. As our business continues to develop, there may be new or existing customers, including from different geographic regions, that contribute more significantly to our total revenue, and a loss of such customers or a significant reduction in how much they spend with us could adversely impact our business. Any economic or political instability, whether as a result of the macroeconomic climate, war or other armed conflict, terrorism, or otherwise, in a specific country or region, may negatively impact the global or local economy, advertising ecosystem, our customers and their budgets with us, or our ability to forecast our advertising revenue, and could seriously harm our business.

13

Moreover, we rely heavily on our ability to collect and disclose data and metrics to our customers so we can attract new customers and retain existing customers. Any restriction, whether by law, regulation, policy, or other reason, on our ability to collect and disclose data and metrics that our customers find useful would impede our ability to attract and retain advertisers. Regulators in many of the countries in which we operate or have users are increasingly scrutinizing and regulating the collection, use, and sharing of personal data related to advertising, which could materially impact our revenue and seriously harm our business. Many of these laws and regulations expand the rights of individuals to control how their personal data is collected and processed, and place restrictions on the use of personal data of teens. The processing of personal data for personalized advertising continues to be under increased scrutiny from regulators, which includes ongoing regulatory action against large technology companies like ours, the outcomes of which may be uncertain and subject to appeal. These laws may prohibit us and our customers from targeting advertising to teens based on the profiling of personal data. Other legislative proposals and present laws and regulations may also apply to our or our advertisers’ activities and require significant operational changes to our business. These laws and regulations could have a material impact on the development and deployment of AI and machine learning in the context of our targeted advertising activities. Other laws to which we are or may become subject further regulate behavioral, interest-based, or targeted advertising, making certain online advertising activities more difficult and subject to additional scrutiny. These laws grant users the right to opt-out of sharing of their personal data for certain advertising purposes in exchange for money or other valuable consideration, or require parental consent to be obtained for the processing of personal data of users under a certain age and restrict tracking and use of teens’ data, including for advertising. Regulators have issued significant monetary fines in certain circumstances where the regulators alleged that appropriate consent was not obtained in connection with targeted advertising activities. In addition, legislative proposals and present laws and regulations in countries where we operate regulate the use of cookies and other tracking technologies, electronic communications, and marketing.

Furthermore, in April 2021, Apple issued an iOS update that imposed heightened restrictions on our access and use of user data by allowing users to more easily opt-out of tracking of activity across devices. Additionally, Google announced that it will implement similar changes with respect to its Android operating system, and major web browsers, like Firefox, Safari, and Chrome, have or plan to make similar changes as well. The implemented changes have had, and the announced or planned changes likely will have, an adverse effect on our targeting, measurement, and optimization capabilities, and in turn our ability to target advertisements and measure the effectiveness of advertisements on our services. This has resulted in, and in the future is likely to continue to result in, reduced demand and pricing for our advertising products and could seriously harm our business. The longer-term impact of these changes on the overall mobile advertising ecosystem, our competitors, our business, and the developers, partners, and advertisers within our community remains uncertain, and depending on how we, our competitors, and the overall mobile advertising ecosystem adjusts, and how our partners, advertisers, and users respond, our business could be seriously harmed. Any alternative solutions we implement are subject to rules and standards set by the owners of such mobile operating systems which may be unclear, change, or be interpreted in a manner adverse to us and require us to halt or change our solutions, any of which could seriously harm our business. In addition, if we are unable to mitigate or respond to these and future developments, and alternative solutions do not become widely adopted by our advertisers, then our targeting, measurement, and optimization capabilities will be materially and adversely affected, which would in turn continue to negatively impact our advertising revenue. Our advertising revenue could also be seriously harmed by many other factors, including:

•diminished or stagnant growth, or a decline, in the total or regional number of DAUs on Snapchat;

•our inability to deliver advertisements to all of our users due to legal restrictions or hardware, software, or network limitations;

•a decrease in the amount of time spent on Snapchat, a decrease in the amount of content that our users share, or decreases in usage of our Camera, Visual Messaging, Map, Stories, and Spotlight platforms;

•our inability to create new products that sustain or increase the value of our advertisements;

•changes in our user demographics that make us less attractive to advertisers;

•lack of ad creative availability by our advertising partners;

•a decline in our available content, including if our content partners do not renew agreements, devote the resources to create engaging content, or provide content exclusively to us;

•decreases in the perceived quantity, quality, usefulness, or relevance of the content provided by us, our community, or partners;

•increases in resistance by users to our collecting, using, and sharing their personal data for advertising-related purposes;

14

•changes in our analytics and measurement solutions, including what we are permitted to collect and disclose under the terms of Apple’s and Google’s mobile operating systems, that demonstrate the value of our advertisements and other commercial content;

•competitive developments or advertiser perception of the value of our products that change the rates we can charge for advertising or the volume of advertising on Snapchat;

•product changes or advertising inventory management decisions we may make that change the type, size, frequency, or effectiveness of advertisements displayed on Snapchat or the method used by advertisers to purchase advertisements;

•adverse legal developments relating to advertising, including changes mandated or prompted by legislation, regulation, executive actions, or litigation regarding the collection, use, and sharing of personal data for certain advertising-related purposes;

•adverse media reports or other negative publicity involving us, our founders, our partners, or other companies in our industry;

•advertiser or user perception that content published by us, our users, or our partners is objectionable;

•the degree to which users skip advertisements and therefore diminish the value of those advertisements to advertisers;

•changes in the way advertising is priced or its effectiveness is measured;

•our inability, or perceived inability, to achieve an advertiser’s intended performance metric, measure the effectiveness of our advertising, or target the appropriate audience for advertisements;

•our inability to access, collect, and disclose user’s personal data, including advertising or similar deterministic identifiers that new and existing advertisers may find useful;

•difficulty and frustration from advertisers who may need to reformat or change their advertisements to comply with our guidelines;

•volatility in the equity markets, which may reduce our advertisers’ capacity or desire for aggressive advertising spending towards growth; and

•the political, economic, and macroeconomic climate and the status of the advertising industry in general, including impacts related to labor shortages and disruptions, supply chain disruptions, banking instability, inflation, and as a result of war, terrorism, or armed conflict.

Moreover, individuals are also becoming increasingly aware of and resistant to the collection, use, and sharing of personal data in connection with advertising. Individuals are becoming more aware of options and certain rights related to consent and other options to opt-out of such data processing, including through media attention about privacy and data protection. Some users have opted out of allowing Snap to combine certain data from third-party apps and websites with certain data from Snapchat for advertising purposes, which has negatively impacted our ability to collect certain user data and our advertising partners’ ability to deliver relevant content, all of which could negatively impact our business

These and other factors could reduce demand for our advertising products, which may lower the prices we receive, or cause advertisers to stop advertising with us altogether. Either of these would seriously harm our business.

Snapchat depends on effectively operating with mobile operating systems, hardware, networks, regulations, and standards that we do not control. Changes in our products or to those mobile operating systems, hardware, networks, regulations, or standards may seriously harm our user retention, growth, and engagement.

Because Snapchat is used primarily on mobile devices, the application must remain interoperable with popular mobile operating systems, primarily Android and iOS, application stores, and related hardware, including mobile-device cameras. The owners and operators of such mobile operating systems and application stores, primarily Google and Apple, each have approval authority over whether to feature our core products on their application stores and make available to consumers third-party products that compete with ours. Furthermore, there is no guarantee that any approval previously provided by such owner or operator will not be rescinded in the future. Additionally, mobile devices and mobile-device cameras are manufactured by a wide array of companies. Those companies have no obligation to test the interoperability of new mobile devices, mobile-device cameras, or related devices with Snapchat, and may produce new products that are incompatible with or not optimal for Snapchat. We have no control over these mobile operating systems, application stores,

15

or hardware, and any changes may degrade our products’ functionality, or give preferential treatment to competitive products. Actions by government authorities may also impact our access to these systems or hardware and could seriously harm Snapchat usage. Our competitors that control the mobile operating systems and related hardware could make interoperability of our products more difficult or display their competitive offerings more prominently than ours. Additionally, our competitors that control the standards for the application stores could make Snapchat, or certain features of Snapchat, inaccessible for a potentially significant period of time or require us to make changes to maintain access. We plan to continue to introduce new products and features regularly, including some features that may only work on the latest systems and hardware, and have experienced that it takes significant time to optimize new products and features to function with the variety of existing mobile operating systems, hardware, and standards, impacting the popularity of such products, and we expect this trend to continue.

Moreover, our products require high-bandwidth data capabilities. If the costs of data usage increase or access to cellular networks is limited, our user retention, growth, and engagement may be seriously harmed. Additionally, to deliver high-quality video and other content over mobile cellular networks, our products must work well with a range of mobile technologies, systems, networks, regulations, and standards that we do not control and which may be subject to future changes. In addition, the proposal or adoption of any laws, regulations, or initiatives that adversely affect the growth, popularity, or use of the internet, including laws governing internet neutrality, could decrease the demand for our products, including by impairing our ability to retain existing users or attract new users, make Snapchat a less attractive alternative to our competitors' applications, and increase our cost of doing business.

We may not successfully cultivate relationships with key industry participants or develop products that operate effectively with these technologies, systems, networks, regulations, or standards. If it becomes more difficult for our users to access and use Snapchat, if our users choose not to access or use Snapchat, or if our users choose to use products that do not offer access to Snapchat, our business and user retention, growth, and engagement could be seriously harmed.

We rely on Google Cloud and Amazon Web Services, or AWS, for the vast majority of our computing, storage, bandwidth, and other services. Any disruption of or interference with our use of either platform would negatively affect our operations and seriously harm our business.

Google and Amazon provide distributed computing infrastructure platforms for business operations, commonly referred to as a “cloud” computing service. We currently run the vast majority of our computing on Google Cloud and AWS and have built our software and computer systems to use computing, storage capabilities, bandwidth, and other services provided by Google and AWS. Our systems are not fully redundant on the two platforms. Any transition of the cloud services currently provided by either Google Cloud or AWS to the other platform or to another cloud provider would be difficult to implement and would cause us to incur significant time and expense. Given this, any significant disruption of or interference with Google Cloud or AWS, whether temporary, regular, or prolonged, would negatively impact our operations and our business would be seriously harmed. If our users or partners are not able to access Snapchat or specific Snapchat features, or encounter difficulties in doing so, due to issues or disruptions with Google Cloud or AWS, we may lose users, partners, or advertising revenue. The level of service provided by Google Cloud and AWS or similar providers may also impact our users’, advertisers’, and partners’ usage of and satisfaction with Snapchat and could seriously harm our business and reputation if the level of service decreases. Hosting costs also have and will continue to increase as our user base and user engagement grows and may seriously harm our business if we are unable to grow our revenues faster than the cost of utilizing the services of Google Cloud, AWS, or similar providers.

In addition, Google or Amazon may take actions beyond our control that could seriously harm our business, including:

•discontinuing or limiting our access to its cloud platform;

•increasing pricing terms;

•terminating or seeking to terminate our contractual relationship altogether;

•establishing more favorable relationships or pricing terms with one or more of our competitors; or

•modifying or interpreting its terms of service or other policies in a manner that impacts our ability to run our business and operations.

16

If we are unable to protect our intellectual property, the value of our brand and other intangible assets may be diminished, and our business may be seriously harmed. If we need to license or acquire new intellectual property, we may incur substantial costs.

We aim to protect our confidential proprietary information, in part, by entering into confidentiality agreements and invention assignment agreements with our employees, consultants, advisors, and third parties who access or contribute to our proprietary know-how, information, or technology. We, however, cannot assure you that these agreements will be effective in controlling access to, or preventing unauthorized distribution, use, misuse, misappropriation, reverse engineering, or disclosure of our proprietary information, know-how, and trade secrets. These agreements may be breached, and we may not have adequate remedies for any such breach. Enforcing a claim that a party illegally disclosed or misappropriated a trade secret or know-how can be difficult, expensive, and time-consuming, and the outcome can be unpredictable. Furthermore, these agreements do not prevent our competitors or partners from independently developing offerings that are substantially equivalent or superior to ours.