Exhibit 4.1

Execution version

USD 375,000,000

TERM LOAN AND REVOLVING CREDIT FACILITIES AGREEMENT

dated 4 September 2018

for

KNOT SHUTTLE TANKERS AS

KNUTSEN SHUTTLE TANKERS XII KS

KNUTSEN SHUTTLE TANKERS 13 AS

KNUTSEN NYK SHUTTLE TANKERS 16 AS

KNOT SHUTTLE TANKERS 17 AS

KNOT SHUTTLE TANKERS 18 AS

as Borrowers

with

KNOT OFFSHORE PARTNERS L.P.

as Parent Guarantor

arranged by

THE FINANCIAL INSTITUTIONS listed in Part B of Schedule 1 (The Original Parties) acting as Mandated Lead Arranger and Bookrunners

with

THE FINANCIAL INSTITUTIONS listed in Part A of Schedule 1 (The Original Parties) acting as Original Lenders

THE FINANCIAL INSTITUTIONS listed in Part C of Schedule 1 (The Original Parties) acting as Hedging Banks

and

NORDEA BANK AB (PUBL), FILIAL I NORGE

as Co-Ordinator

and

DNB BANK ASA

acting as Agent

schjodt.no | Page 2 of 146

CONTENTS

| Clause | Page | |||||

| 1. |

Definitions And Interpretation | 5 | ||||

| 2. |

The Credit Facility | 30 | ||||

| 3. |

Purpose | 31 | ||||

| 4. |

Conditions Of Utilisation | 32 | ||||

| 5. |

Utilisation | 33 | ||||

| 6. |

Joint And Several Liability | 34 | ||||

| 7. |

Repayment | 37 | ||||

| 8. |

Prepayment And Cancellation | 38 | ||||

| 9. |

Interest | 44 | ||||

| 10. |

Interest Periods | 45 | ||||

| 11. |

Changes To The Calculation Of Interest | 46 | ||||

| 12. |

Fees | 47 | ||||

| 13. |

Tax Gross Up And Indemnities | 47 | ||||

| 14. |

Increased Costs | 51 | ||||

| 15. |

Other Indemnities | 52 | ||||

| 16. |

Mitigation By The Lenders | 53 | ||||

| 17. |

Costs And Expenses | 54 | ||||

| 18. |

Security | 54 | ||||

| 19. |

Guarantee And Indemnity | 56 | ||||

| 20. |

Representations | 61 | ||||

| 21. |

Information Undertakings | 67 | ||||

| 22. |

Financial Covenants | 69 | ||||

| 23. |

General Undertakings | 71 | ||||

| 24. |

Vessel Undertakings | 77 | ||||

| 25. |

Events Of Default | 82 | ||||

| 26. |

Changes To The Lenders | 86 | ||||

| 27. |

Changes To The Obligors | 90 | ||||

| 28. |

Role Of The Agent, The Co-Ordinator, The Mandated Lead Arrangers And The Reference Banks | 90 | ||||

| 29. |

Conduct Of Business By The Finance Parties And The Hedging Banks | 100 | ||||

| 30. |

Sharing Among The Finance Parties | 100 | ||||

| 31. |

Payment Mechanics | 101 | ||||

| 32. |

Set-Off | 104 | ||||

schjodt.no | Page 3 of 146

| 33. |

Notices | 104 | ||||

| 34. |

Calculations And Certificates | 106 | ||||

| 35. |

Partial Invalidity | 107 | ||||

| 36. |

Remedies And Waivers | 107 | ||||

| 37. |

Amendments And Waivers | 107 | ||||

| 38. |

Counterparts | 114 | ||||

| 39. |

Conflict | 114 | ||||

| 40. |

Confidential Information | 114 | ||||

| 41. |

Confidentiality Of Funding Rates And Reference Bank Quotations | 118 | ||||

| 42. |

Disclosure By The Parent Guarantor | 120 | ||||

| 43. |

“Know Your Customer” Checks | 120 | ||||

| 44. |

Governing Law | 121 | ||||

| 45. |

Enforcement | 122 | ||||

| SCHEDULE 1 THE ORIGINAL PARTIES |

123 | |||||

| SCHEDULE 2 CONDITIONS PRECEDENT |

125 | |||||

| SCHEDULE 3 REQUESTS |

132 | |||||

| Part I Utilisation Request |

||||||

| Part II Selection Notice |

||||||

| SCHEDULE 4 FORM OF TRANSFER CERTIFICATE |

135 | |||||

| SCHEDULE 5 FORM OF LENDER ASSIGNMENT AGREEMENT |

137 | |||||

| SCHEDULE 6 FORM OF COMPLIANCE CERTIFICATE |

140 | |||||

| SCHEDULE 7 STRUCTURE CHART |

141 | |||||

| SCHEDULE 8 REPAYMENT SCHEDULE |

142 | |||||

| SCHEDULE 9 LIST OF EXISTING HEDGING TRANSACTIONS |

143 | |||||

schjodt.no | Page 4 of 146

THIS AGREEMENT is dated 4 September 2018 and made between:

| (1) | KNOT SHUTTLE TANKERS AS, Norwegian registration no. 998 942 829, with registered offices at Smedasundet 40, N-5529 Haugesund, Norway as borrower (in that capacity, the “RCF Borrower”); |

KNUTSEN SHUTTLE TANKERS XII KS, Norwegian registration no. 991 959 610, with registered offices at Smedasundet 40, N-5529 Haugesund, Norway as a borrower (in that capacity, “Borrower A”);

KNUTSEN SHUTTLE TANKERS 13 AS, Norwegian registration no. 996 661 016, with registered offices at Smedasundet 40, N-5529 Haugesund, Norway as a borrower (in that capacity, “Borrower B”);

KNUTSEN NYK SHUTTLE TANKERS 16 AS, Norwegian registration no. 997 404 009, with registered offices at Smedasundet 40, N-5529 Haugesund, Norway as a borrower (in that capacity, “Borrower C”);

KNOT SHUTTLE TANKERS 17 AS, Norwegian registration no. 998 942 969, with registered offices at Smedasundet 40, N-5529 Haugesund, Norway as a borrower (in that capacity, “Borrower D”);

KNOT SHUTTLE TANKERS 18 AS, Norwegian registration no. 998 943 035, with registered offices at Smedasundet 40, N-5529 Haugesund, Norway as a borrower (in that capacity, “Borrower E”),

as borrowers (in that capacity, the “Borrowers”);

| (2) | KNOT OFFSHORE PARTNERS L.P., a master limited partnership listed on the New York Stock Exchange, with registered offices at 2 Queen’s Cross, Aberdeen, Aberdeenshire, AB15 4YB, United Kingdom as parent guarantor (the “Parent Guarantor”); |

KNOT SHUTTLE TANKERS AS, Norwegian registration no. 998 942 829, with registered offices at Smedasundet 40, N-5529 Haugesund, Norway (in that capacity, “Guarantor 1”);

KNUTSEN SHUTTLE TANKERS 13 AS, Norwegian registration no. 996 661 016, with registered offices at Smedasundet 40, N-5529 Haugesund, Norway (in that capacity, “Guarantor 2”);

KNUTSEN NYK SHUTTLE TANKERS 16 AS, Norwegian registration no. 997 404 009, with registered offices at Smedasundet 40, N-5529 Haugesund, Norway (in that capacity, “Guarantor 3”);

KNOT SHUTTLE TANKERS 17 AS, Norwegian registration no. 998 942 969, with registered offices at Smedasundet 40, N-5529 Haugesund, Norway (in that capacity, “Guarantor 4”);

KNOT SHUTTLE TANKERS 18 AS, Norwegian registration no. 998 943 035, with registered offices at Smedasundet 40, N-5529 Haugesund, Norway as a borrower (in that capacity, “Guarantor 5”),

as guarantors (in that capacity, the “Guarantors”);

schjodt.no | Page 5 of 146

| (3) | THE FINANCIAL INSTITUTIONS listed in Part B of Schedule 1 (The Original Parties) as mandated lead arrangers (in that capacity, the “Mandated Lead Arrangers”) and bookrunners (in that capacity, the “Bookrunners”); |

| (4) | THE FINANCIAL INSTITUTIONS listed in Part A of Schedule 1 (The Original Parties) as lenders (the “Original Lenders”); |

| (5) | THE FINANCIAL INSTITUTIONS listed in Part C of Schedule 1 (The Original Parties) as hedging banks (the “Hedging Banks”); |

| (6) | NORDEA BANK AB (PUBL), FILIAL I NORGE, Norwegian registration no. 983 258 344, a banking institution organised under the laws of Norway acting through its office at Essendrops gate 7, N-0368 Oslo as co-ordinator (the “Co-Ordinator”); and |

| (7) | DNB BANK ASA, Norwegian registration no. 984 851 006, a banking institution organised under the laws of Norway acting through its office at Solheimsgaten 7C, N-5058 Bergen, Norway as facility agent and security trustee for the other Finance Parties and the Hedging Banks (the “Agent”). |

IT IS AGREED as follows:

SECTION 1

INTERPRETATION

| 1. | DEFINITIONS AND INTERPRETATION |

| 1.1 | Definitions |

In this Agreement:

“Account Bank” means DNB Bank ASA, Norwegian registration no. 984 851 006, a banking institution organised under the laws of Norway acting through its office at Solheimsgaten 7C, N-5058 Bergen, Norway.

“Affiliate” means, in relation to any person, a Subsidiary of that person or a Holding Company of that person or any other Subsidiary of that Holding Company.

“Agreement” means this facility agreement, as it may be amended, supplemented and varied in writing from time to time, including its schedules.

“Approved Brokers” means Fearnleys AS, Clarksons Platou AS and Lorentzen & Stemoco.

“Approved Ship Registry” means the Norwegian Ordinary Ship Registry (NOR), the Norwegian International Ship Registry (NIS), the Danish International Ship Register (DIS), the ship registries of Malta, the United Kingdom, the Isle of Man, the Bahamas, or any ship registry as approved in writing by the Agent (on behalf of all Lenders).

“Authorisation” means an authorisation, consent, approval, resolution, licence, exemption, filing, notarisation or registration.

“Availability Period” means:

| (a) | in relation to the Term Loan Facilities, the period from and including the Closing Date to and including 30 September 2018; and |

schjodt.no | Page 6 of 146

| (b) | in relation to the Revolving Credit Facility, the period from and including the Closing Date to and including the date falling three (3) months prior to the Final Maturity Date. |

“Available Commitment” means, in relation to a Facility, a Lender’s Commitment under that Facility minus (subject as set out below):

| (a) | the amount of its participation in any outstanding Utilisation under that Facility; and |

| (b) | in relation to any proposed Utilisation, the amount of its participation in any other Utilisation that are due to be made under that Facility on or before the proposed Utilisation Date, |

other than that Lender’s participation in any Loans that are due to be repaid or prepaid on or before the proposed Utilisation Date.

“Available Facility” means, in respect of a Facility or a Tranche, the aggregate for the time being of each Lender’s Available Commitment in respect of that Facility or Tranche.

“Bail-In Action” means the exercise of any Write-down and Conversion Powers.

“Bail-In Legislation” means:

| (a) | in relation to an EEA Member Country which has implemented, or which at any time implements, Article 55 of Directive 2014/59/EU establishing a framework for the recovery and resolution of credit institutions and investment firms , the relevant implementing law or regulation as described in the EU Bail-In Legislation Schedule from time to time; and |

| (b) | in relation to any other state, any analogous law or regulation from time to time which requires contractual recognition of any Write-down and Conversion Powers contained in that law or regulation. |

“Basel II Accord” means the “International Convergence of Capital Measurement and Capital Standards, a Revised Framework” published by the Basel Committee on Banking Supervision in June 2004 as updated prior to, and in the form existing on, the date of this Agreement, excluding any amendment thereto arising out of the Basel III Accord.

“Basel II Approach” means, in relation to any Finance Party, either the Standardised Approach or the relevant Internal Ratings Based Approach (each as defined in the Basel II Accord) adopted by that Finance Party (or any of its Affiliates) for the purposes of implementing or complying with the Basel II Accord.

“Basel II Regulation” means:

| (a) | any law or regulation implementing the Basel II Accord (including the relevant provisions of directive 2013/36/EU (“CRD IV”) and regulation 575/2013 (“CRR”) of the European Union) to the extent only that such law or regulation re-enacts and/or implements the requirements of the Basel II Accord but excluding any provision of such law or regulation implementing the Basel III Accord; and |

| (b) | any Basel II Approach adopted by a Finance Party or any of its Affiliates. |

schjodt.no | Page 7 of 146

“Basel III Accord” means, together:

| (a) | the agreements on capital requirements, a leverage ratio and liquidity standards contained in “Basel III: A global regulatory framework for more resilient banks and banking systems”, “Basel III: International framework for liquidity risk measurement, standards and monitoring” and “Guidance for national authorities operating the countercyclical capital buffer” published by the Basel Committee on Banking Supervision in December 2010, each as amended, supplemented or restated; |

| (b) | the rules for global systemically important banks contained in “Global systemically important banks: assessment methodology and the additional loss absorbency requirement—Rules text” published by the Basel Committee on Banking Supervision in November 2011, as amended, supplemented or restated; and |

| (c) | any further guidance or standards published by the Basel Committee on Banking Supervision relating to “Basel III”. |

“Basel III Regulation” means any law or regulation implementing the Basel III Accord (including CRD IV and CRR) save to the extent that such law or regulation re-enacts a Basel II Regulation.

“Borrower A Assignment Agreement” means an agreement dated on or about the hereof for the pledge with first priority of the Borrower A Earnings Account and the assignment with first priority of the Earnings and the Insurances in respect of Vessel 1 and Vessel 2 and Borrower A’s benefits under the Hedging Agreements, entered or to be entered into between Borrower A and the Agent (on behalf of the Finance Parties and the Hedging Banks) in form and substance satisfactory to the Agent (on behalf of the Finance Parties and the Hedging Banks).

“Borrower A Earnings Account” means USD account no. NO51 1250 0413 857, held in the name of Borrower A with the Account Bank.

“Borrower A Factoring Agreement” means a first priority Norwegian law factoring agreement in the amount of USD 138,000,000 dated on or about the date hereof between Borrower A and the Agent (on behalf of the Finance Parties and the Hedging Banks) in form and substance satisfactory to the Agent (on behalf of the Finance Parties and the Hedging Banks), to be registered against Borrower A with the Norwegian Registry of Movable Property (Nw. Løsøreregisteret).

“Borrower A Mortgage I” means the first priority cross-collateralized mortgage in the amount of USD 138,000,000 (and deed of covenants or declaration of pledge collateral thereto (if applicable)), to be executed and recorded by Borrower A against Vessel 1 in favour of the Agent (on behalf of the Finance Parties and the Hedging Banks) in the relevant Approved Ship Registry, in form and substance satisfactory to the Agent (on behalf of the Finance Parties and the Hedging Banks).

“Borrower A Mortgage II” means the first priority cross-collateralized mortgage in the amount of USD 138,000,000 (and deed of covenants or declaration of pledge collateral thereto (if applicable)), to be executed and recorded by Borrower A against Vessel 2 in favour of the Agent (on behalf of the Finance Parties and the Hedging Banks) in the relevant Approved Ship Registry, in form and substance satisfactory to the Agent (on behalf of the Finance Parties and the Hedging Banks).

schjodt.no | Page 8 of 146

“Borrower A Share Pledge” means an agreement for the charge/pledge with first priority of 100% of the shares Knutsen Shuttle Tankers XII AS (owning 10% of the partnership shares in Borrower A) and KNOT Shuttle Tankers 12 AS (owning 90% of the partnership shares in Borrower A) dated on or about the date hereof, entered or to be entered into between the RCF Borrower and the Agent (on behalf of the Finance Parties and the Hedging Banks) in form and substance satisfactory to the Agent (on behalf of the Finance Parties and the Hedging Banks).

“Borrower B Earnings Account” means USD account no. NO12 1250 0469 461, held in the name of Borrower B with the Account Bank.

“Borrower B Factoring Agreement” means a first priority Norwegian law factoring agreement in the amount of USD 450,000,000 dated on or about the date hereof between Borrower B and the Agent (on behalf of the Finance Parties and the Hedging Banks) in form and substance satisfactory to the Agent (on behalf of the Finance Parties and the Hedging Banks), to be registered against Borrower B with the Norwegian Registry of Movable Property (Nw. Løsøreregisteret).

“Borrower B Mortgage” means the first priority cross- collateralized mortgage in the amount of USD 450,000,000 (and deed of covenants or declaration of pledge collateral thereto (if applicable)), to be executed and recorded by Borrower B against Vessel 3 in favour of the Agent (on behalf of the Finance Parties and the Hedging Banks) in the relevant Approved Ship Registry, in form and substance satisfactory to the Agent (on behalf of the Finance Parties and the Hedging Banks).

“Borrower B Assignment Agreement” means an agreement dated on or about the hereof for the pledge with first priority of the Borrower B Earnings Account and the assignment with first priority of the Earnings and the Insurances in respect of Vessel 3 and Borrower B’s benefits under the Hedging Agreements, entered or to be entered into between Borrower B and the Agent (on behalf of the Finance Parties and the Hedging Banks) in form and substance satisfactory to the Agent (on behalf of the Finance Parties and the Hedging Banks).

“Borrower B Share Pledge” means an agreement for the charge/pledge with first priority of 100% of the shares in Borrower B dated on or about the date hereof or on or about, entered or to be entered into between the RCF Borrower and the Agent (on behalf of the Finance Parties and the Hedging Banks) in form and substance satisfactory to the Agent (on behalf of the Finance Parties and the Hedging Banks).

“Borrower C Earnings Account” means USD account no. NO60 1250 0477 618, held in the name of Borrower C with the Account Bank.

“Borrower C Factoring Agreement” means a first priority Norwegian law factoring agreement in the amount of USD 450,000,000 dated on or about the date hereof between Borrower C and the Agent (on behalf of the Finance Parties and the Hedging Banks) in form and substance satisfactory to the Agent (on behalf of the Finance Parties and the Hedging Banks), to be registered against Borrower C with the Norwegian Registry of Movable Property (Nw. Løsøreregisteret).

schjodt.no | Page 9 of 146

“Borrower C Mortgage” means the first priority cross-collateralized mortgage in the amount of USD 450,000,000 (and deed of covenants or declaration of pledge collateral thereto (if applicable)), to be executed and recorded by Borrower C against Vessel 4 in favour of the Agent (on behalf of the Finance Parties and the Hedging Banks) in the relevant Approved Ship Registry, in form and substance satisfactory to the Agent (on behalf of the Finance Parties and the Hedging Banks).

“Borrower C Assignment Agreement” means an agreement dated on or about the hereof for the pledge with first priority of the Borrower C Earnings Account and the assignment with first priority of the Earnings and the Insurances in respect of Vessel 4 and Borrower C’s benefits under the Hedging Agreements, entered or to be entered into between Borrower C and the Agent (on behalf of the Finance Parties and the Hedging Banks) in form and substance satisfactory to the Agent (on behalf of the Finance Parties and the Hedging Banks).

“Borrower C Share Pledge” means an agreement for the charge/pledge with first priority of 100% of the shares in Borrower C dated on or about the date hereof, entered or to be entered into between the RCF Borrower and the Agent (on behalf of the Finance Parties and the Hedging Banks) in form and substance satisfactory to the Agent (on behalf of the Finance Parties and the Hedging Banks).

“Borrower D Earnings Account” means USD account no. NO90 1250 0495 993, held in the name of Borrower D with the Account Bank.

“Borrower D Factoring Agreement” means a first priority Norwegian law factoring agreement in the amount of USD 450,000,000 dated on or about the date hereof between Borrower D and the Agent (on behalf of the Finance Parties and the Hedging Banks) in form and substance satisfactory to the Agent (on behalf of the Finance Parties and the Hedging Banks), to be registered against Borrower D with the Norwegian Registry of Movable Property (Nw. Løsøreregisteret).

“Borrower D Mortgage” means the first priority cross-collateralized mortgage in the amount of USD 450,000,000 (and deed of covenants or declaration of pledge collateral thereto (if applicable)), to be executed and recorded by Borrower D against Vessel 5 in favour of the Agent (on behalf of the Finance Parties and the Hedging Banks) in the relevant Approved Ship Registry, in form and substance satisfactory to the Agent (on behalf of the Finance Parties and the Hedging Banks).

“Borrower D Assignment Agreement” means an agreement dated on or about the hereof for the pledge with first priority of the Borrower D Earnings Account and the assignment with first priority of the Earnings and the Insurances in respect of Vessel 5 and Borrower D’s benefits under the Hedging Agreements, entered or to be entered into between Borrower D and the Agent (on behalf of the Finance Parties and the Hedging Banks) in form and substance satisfactory to the Agent (on behalf of the Finance Parties and the Hedging Banks).

“Borrower D Share Pledge” means an agreement for the charge/pledge with first priority of 100% of the shares in Borrower D dated on or about the date hereof or on or about, entered or to be entered into between the RCF Borrower and the Agent (on behalf of the Finance Parties and the Hedging Banks) in form and substance satisfactory to the Agent (on behalf of the Finance Parties and the Hedging Banks).

schjodt.no | Page 10 of 146

“Borrower E Earnings Account” means USD account no. NO67 1250 0496 019, held in the name of Borrower E with the Account Bank.

“Borrower E Factoring Agreement” means a first priority Norwegian law factoring agreement in the amount of USD 450,000,000 dated on or about the date hereof between Borrower E and the Agent (on behalf of the Finance Parties and the Hedging Banks) in form and substance satisfactory to the Agent (on behalf of the Finance Parties and the Hedging Banks), to be registered against Borrower E with the Norwegian Registry of Movable Property (Nw. Løsøreregisteret).

“Borrower E Mortgage” means the first priority cross-collateralized mortgage in the amount of USD 450,000,000 (and deed of covenants or declaration of pledge collateral thereto (if applicable)), to be executed and recorded by Borrower E against Vessel 6 in favour of the Agent (on behalf of the Finance Parties and the Hedging Banks) in the relevant Approved Ship Registry, in form and substance satisfactory to the Agent (on behalf of the Finance Parties and the Hedging Banks).

“Borrower E Assignment Agreement” means an agreement dated on or about the hereof for the pledge with first priority of the Borrower E Earnings Account and the assignment with first priority of the Earnings and the Insurances in respect of Vessel 6 and Borrower E’s benefits under the Hedging Agreements, entered or to be entered into between Borrower E and the Agent (on behalf of the Finance Parties and the Hedging Banks) in form and substance satisfactory to the Agent (on behalf of the Finance Parties and the Hedging Banks).

“Borrower E Share Pledge” means an agreement for the charge/pledge with first priority of 100% of the shares in Borrower E dated on or about the date hereof, entered or to be entered into between the RCF Borrower and the Agent (on behalf of the Finance Parties and the Hedging Banks) in form and substance satisfactory to the Agent (on behalf of the Finance Parties and the Hedging Banks).

“Break Costs” means the amount (if any) by which:

| (a) | the interest (excluding the Margin) which a Lender should have received for the period from the date of receipt of all or any part of its participation in a Loan or Unpaid Sum to the last day of the current Interest Period in respect of that Loan or Unpaid Sum, had the principal amount or Unpaid Sum received been paid on the last day of that Interest Period; |

exceeds:

| (b) | the amount which that Lender would be able to obtain by placing an amount equal to the principal amount or Unpaid Sum received by it on deposit with a leading bank in the Relevant Interbank Market for a period starting on the Business Day following receipt or recovery and ending on the last day of the current Interest Period. |

“Business Day” means a day (other than a Saturday or Sunday) on which banks are open for general business in London, New York City, Paris and Norway.

“Change of Control” means the occurrence of any of the following:

schjodt.no | Page 11 of 146

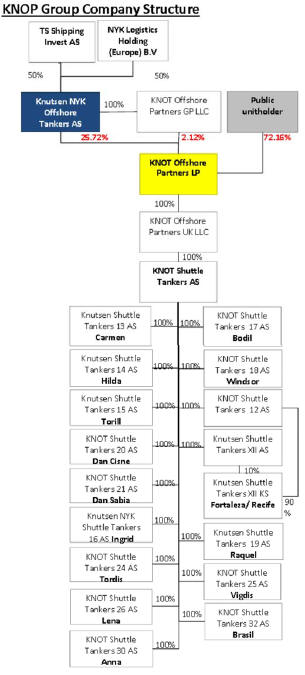

| (a) | TS Shipping Invest AS (or a 100% owned subsidiary of TS Shipping Invest AS) and NYK Logistics Holding (Europe) B.V. (or Nippon Yusen Kabushiki Kaisha or another 100% owned subsidiary of Nippon Yusen Kabushiki Kaisha) each does not own or is not able to vote for (directly or indirectly) 50% of the shares in KNOT; or |

| (b) | the Parent Guarantor does not own or is not able to vote for (directly or indirectly) all of the shares in the Borrowers; or |

| (c) | KNOT does not own or is not able to vote for (directly or indirectly) all of the shares in the General Partner (being the general partner in the Parent Guarantor); or |

| (d) | the General Partner ceases to be the general partner of the Parent Guarantor; or |

| (e) | KNOT does not own (directly or indirectly) at least 25% of the common and general partner units in the Parent Guarantor (capital and voting rights to be subject to the limitations on voting rights relating to election of board members, amendments and certain other matters as set out in the limited partnership agreement entered into in relation to the Parent Guarantor); or |

| (f) | any person or group of persons acting in concert (other than KNOT and/or any of its wholly owned Subsidiaries) acquires, legally or beneficially, and either directly or indirectly, more than thirty three point thirty three per cent. (33.33%) of the common and general partner units or voting rights in the Parent Guarantor. |

“Closing Date” means the date of this Agreement, which shall be a date falling on or before 4 September 2018.

“Code” means the US Internal Revenue Code of 1986.

“Commitment” means a Term Loan Facility A Commitment, a Term Loan Facility B Commitment or a Revolving Credit Facility Commitment.

“Companies Act” means the Norwegian Limited Liability Companies Act of 13 June 1997 No. 44 (Nw. aksjeloven).

“Compliance Certificate” means a certificate substantially in the form set out in Schedule 6 (Form of Compliance Certificate).

“Confidential Information” means all information relating to the Borrowers, any Obligor, the Group, the Finance Documents or a Facility of which a Finance Party becomes aware in its capacity as, or for the purpose of becoming, a Finance Party or which is received by a Finance Party in relation to, or for the purpose of becoming a Finance Party under, the Finance Documents or a Facility from either:

| (a) | any member of the Group or any of its advisers; or |

| (b) | another Finance Party, if the information was obtained by that Finance Party directly or indirectly from any member of the Group or any of its advisers, |

in whatever form, and includes information given orally and any document, electronic file or any other way of representing or recording information which contains or is derived or copied from such information but excludes:

| (i) | information that: |

schjodt.no | Page 12 of 146

| (A) | is or becomes public information other than as a direct or indirect result of any breach by that Finance Party of Clause 40 (Confidential Information); or |

| (B) | is identified in writing at the time of delivery as non-confidential by any member of the Group or any of its advisers; or |

| (C) | is known by that Finance Party before the date the information is disclosed to it in accordance with paragraphs (a) or (b) above or is lawfully obtained by that Finance Party after that date, from a source which is, as far as that Finance Party is aware, unconnected with the Group and which, in either case, as far as that Finance Party is aware, has not been obtained in breach of, and is not otherwise subject to, any obligation of confidentiality; and |

| (ii) | any Funding Rate or Reference Bank Quotation. |

“Credit Facility” means the Term Loan Facilities and the Revolving Credit Facility, and “Facility” means either of them.

“Default” means an Event of Default or any event or circumstance specified in Clause 25 (Events of Default) which would (with the expiry of a grace period, the giving of notice, the making of any determination under the Finance Documents or any combination of any of the foregoing) be an Event of Default.

“Defaulting Lender” means any Lender:

| (a) | which has failed to make its participation in a Loan available (or has notified the Agent or the Borrowers (which have notified the Agent) that it will not make its participation in a Loan available) by the Utilisation Date of that Loan in accordance with Clause 5.4 (Lenders’ participation); |

| (b) | which has otherwise rescinded or repudiated a Finance Document; or |

| (c) | with respect to which an Insolvency Event has occurred and is continuing, |

unless, in the case of paragraph (a) above:

| (i) | its failure to pay is caused by: |

| (A) | administrative or technical error; or |

| (B) | a Disruption Event, and |

| payment is made within three (3) Business Days of its due date; or |

| (ii) | the Lender is disputing in good faith whether it is contractually obliged to make the payment in question. |

“Disruption Event” means either or both of:

| (a) | a material disruption to those payment or communications systems or to those financial markets which are, in each case, required to operate in order for payments to be made in connection with the Credit Facility (or otherwise in order for the transactions contemplated by the Finance Documents to be carried out) which disruption is not caused by, and is beyond the control of, any of the Parties; or |

schjodt.no | Page 13 of 146

| (b) | the occurrence of any other event which results in a disruption (of a technical or systems-related nature) to the treasury or payments operations of a Party preventing that, or any other Party: |

| (i) | from performing its payment obligations under the Finance Documents; or |

| (ii) | from communicating with other Parties in accordance with the terms of the Finance Documents, |

and which (in either such case) is not caused by, and is beyond the control of, the Party whose operations are disrupted.

“DOC” means in relation to the Manager of a Vessel a valid document of compliance issued to such company pursuant to paragraph 13.2 of the ISM Code.

“Earnings” means all moneys whatsoever which are now or later become, payable (actually or contingently) to a Borrower in respect of and/or arising out of the use of or operation of a Vessel, including (but not limited to):

| (a) | all freight, hire and passage moneys payable to that Borrower, including (without limitation) payments of any nature under any contract or any other agreement for the employment, use, possession, management and/or operation of that Vessel; |

| (b) | any claim under any guarantees related to hire payable to that Vessel as a consequence of the operation of that Vessel; |

| (c) | any compensation payable to that Borrower in the event of any requisition of that Vessel or for the use of that Vessel by any government authority or other competent authority; |

| (d) | remuneration for salvage, towage and other services performed by that Vessel payable to that Borrower; |

| (e) | demurrage and retention money receivable by that Borrower in relation to that Vessel; |

| (f) | all moneys which are at any time payable under the Insurances in respect of loss of earnings from that Vessel; |

| (g) | if and whenever that Vessel is employed on terms whereby any moneys falling within paragraph a) to f) above are pooled or shared with any other person, that proportion of the net receipts of the relevant pooling or sharing arrangement which is attributable to that Vessel; and |

| (h) | any other money which arise out of the use of or operation of that Vessel and moneys whatsoever due or to become due to that Borrower from third parties in relation to that Vessel. |

“Earnings Accounts” means together:

| (a) | the Borrower A Earnings Account; |

schjodt.no | Page 14 of 146

| (b) | the Borrower B Earnings Account; |

| (c) | the Borrower C Earnings Account; |

| (d) | the Borrower D Earnings Account; and |

| (e) | the Borrower E Earnings Account, |

and “Earnings Account” means any of them.

“EEA Member Country” means any Member State of the European Union, Iceland, Liechtenstein and Norway.

“Eligible Institution” means any Lender or other bank or financial institution selected by the Borrower and which, in each case, is not a member of the Group or an affiliate of any member of the Group.

“Environmental Approval” means any permit, licence, consent, approval and other authorisations and the filing of any notification, or assessment required under any Environmental Law for the operation of the Vessel.

“Environmental Claim” means any claim, proceeding, formal notice or investigation by any person or company in respect of any Environmental Law or Environmental Permits.

“Environmental Law” means any applicable law or regulation which relates to:

| (a) | the pollution or protection of the environment or to the carriage of material which is capable of polluting the environment; |

| (c) | harm to or the protection of human health; |

| (d) | the conditions of the workplace; or |

| (e) | any emission or substance capable of causing harm to any living organism or the environment. |

“Environmental Permits” means any permit, licence, consent, approval and other and other authorisation and the filing of any notification, report or assessment required under any Environmental Law for the operation of business conducted on or from the properties owned or used by an Obligor.

“EU Bail-In Legislation Schedule” means the document described as such and published by the Loan Market Association (or any successor person) from time to time.

“Event of Default” means any event or circumstance specified as such in Clause 25 (Events of Default).

“Existing Hedging Transactions” means the hedging transactions listed and specified in Schedule 9 (List of Existing Hedging Transactions).

“Existing Loans” means:

schjodt.no | Page 15 of 146

| (a) | a USD 90,000,000 term loan facility agreement dated 7 June 2012 (as amended, supplemented and restated from time to time) (the “Ingrid Facility”) between (a) Borrower C as borrower (b) the RCF Borrower and the Parent Guarantor as guarantors, (c) DNB Bank ASA and Nordea Bank AB (publ), filial i Norge as commercial lenders, bookrunners and mandated lead arrangers, (d) the Norwegian Government represented by the Norwegian Ministry of Trade, Industry and Fisheries as export credit lender, (e) the Nordea Bank AB (publ), filial i Norge and DNB Bank ASA as swap banks and (f) DNB Bank ASA as facility agent and security trustee; |

| (b) | a USD 140,000,000 term loan facility agreement dated 10 June 2014 (as amended, supplemented and restated from time to time) (the “Fortaleza/Recife Facility”) between (a) Borrower A as borrower, (b) the RCF Borrower and the Parent Guarantor as guarantors, (c) the Financial Institutions listed in Schedule 1 thereto as lenders, (d) Nordea Bank AB (publ), filial i Norge, DNB Bank ASA, ABN AMRO Bank N.V., Oslo Branch and BNP Paribas as arrangers, (e) DNB Bank ASA, ABN AMRO Bank N.V., BNP Paribas and Nordea Bank AB (publ) as hedging banks and (f) DNB Bank ASA as facility agent and security trustee; and |

| (c) | a USD 240,000,000 term and revolving loan facility agreement dated 10 June 2014 (as amended, supplemented and restated from time to time) (the “Windsor/Bodil/Carmen Facility”) between (a) Borrower B, D and E as borrowers, (b) the RCF Borrower and the Parent Guarantor as guarantors, (c) Nordea Bank AB (publ), filial i Norge, DNB Bank ASA, ABN AMRO Bank N.V., Oslo Branch and BNP Paribas as lenders and arrangers, (d) DNB Bank ASA, ABN AMRO Bank N.V., BNP Paribas and Nordea Bank AB (publ) as hedging banks and (e) Nordea Bank AB (publ), filial i Norge, as facility agent and security trustee. |

“FA Act” means the Norwegian Financial Agreements Act of 25 June 1999 No. 46 (Nw. finansavtaleloven).

“Facility Office” means:

| (a) | the office or offices notified by a Lender to the Agent in writing on or before the date it becomes a Lender (or, following that date, by not less than five (5) Business Days’ written notice) as the office or offices through which it will perform its obligations under this Agreement; or |

| (b) | in respect of any other Finance Party, the office in the jurisdiction in which it is resident for tax purposes. |

“FATCA” means:

| (a) | sections 1471 to 1474 of the Code or any associated regulations; |

| (b) | any treaty, law or regulation of any other jurisdiction, or relating to an intergovernmental agreement between the US and any other jurisdiction, which (in either case) facilitates the implementation of any law or regulation referred to in paragraph (a) above; or |

| (c) | any agreement pursuant to the implementation of any treaty, law or regulation referred to in paragraphs (a) or (b) above with the US Internal Revenue Service, the US government or any governmental or taxation authority in any other jurisdiction. |

schjodt.no | Page 16 of 146

“FATCA Application Date” means:

| (a) | in relation to a “withholdable payment” described in section 1473(1)(A)(i) of the Code (which relates to payments of interest and certain other payments from sources within the US), 1 July 2014; |

| (b) | in relation to a “withholdable payment” described in section 1473(1)(A)(ii) of the Code (which relates to “gross proceeds” from the disposition of property of a type that can produce interest from sources within the US), 1 January 2019; or |

| (c) | in relation to a “passthru payment” described in section 1471(d)(7) of the Code not falling within paragraphs (a) or (b) above, 1 January 2019, |

or, in each case, such other date from which such payment may become subject to a deduction or withholding required by FATCA as a result of any change in FATCA after the date of this Agreement.

“FATCA Deduction” means a deduction or withholding from a payment under a Finance Document required by FATCA.

“FATCA Exempt Party” means a Party that is entitled to receive payments free from any FATCA Deduction.

“Fee Letter” means

| (a) | any letter or letters dated on or about the Closing Date between the Agent and the Borrower (or the Arrangers and the Borrower) setting out any fee referred to in Clause 12 (Fees); and |

| (b) | any agreement setting out fees payable to a Finance Party referred to under any other Finance Document. |

“Final Maturity Date” means the date falling five (5) years from the Closing Date.

“Finance Document” means this Agreement, any Security Document, any Fee Letter, any Manager’s Undertaking, any Compliance Certificate, any Selection Notice, any Utilisation Request, any Letter of Quiet Enjoyment, any other document designated as such by the Agent and the Borrowers and, as long as there is an Event of Default which is continuing and for the purposes of Clause 30 (Sharing among the Finance Parties), Clause 31 (Payment mechanics) and Clause 32 (Set-off) only, “Finance Document” shall also include any Hedging Agreement.

“Finance Party” means the Agent, a Mandated Lead Arranger, a Bookrunner, a Lender, the Co-Ordinator or, as long as there is an Event of Default which is continuing and for the purposes of Clause 30 (Sharing among the Finance Parties), Clause 31 (Payment mechanics) and Clause 32 (Set-off) only, “Finance Party” shall also include the Hedging Banks.

“Financial Indebtedness” means any indebtedness for or in respect of:

| (a) | moneys borrowed; |

| (b) | any amount raised by acceptance under any acceptance credit facility or dematerialised equivalent; |

schjodt.no | Page 17 of 146

| (c) | any amount raised pursuant to any note purchase facility or the issue of bonds, notes, debentures, loan stock or any similar instrument; |

| (d) | the amount of any liability in respect of any lease or hire purchase contract which would, in accordance with GAAP, be treated as a finance or capital lease; |

| (e) | receivables sold or discounted (other than any receivables to the extent they are sold on a non-recourse basis); |

| (f) | any amount raised under any other transaction (including any forward sale or purchase agreement) of a type not referred to in any other paragraph of this definition having the commercial effect of a borrowing; |

| (g) | any derivative transaction entered into in connection with protection against or benefit from fluctuation in any rate or price (and, when calculating the value (or, if any actual amount is due as a result of the termination or close-out of that derivative transaction, that amount) of any derivative transaction, only the marked to market value shall be taken into account), including any Hedging Agreement; |

| (h) | any counter-indemnity obligation in respect of a guarantee, indemnity, bond, standby or documentary letter of credit or any other instrument issued by a bank or financial institution; and |

| (i) | the amount of any liability in respect of any guarantee or indemnity for any of the items referred to in paragraphs (a) to (h) above. |

“Funding Rate” means any individual rate notified by a Lender to the Agent pursuant to paragraph (a)(ii) of Clause 11.4 (Cost of funds).

“GAAP” means generally accepted accounting principles in Norway or the United States of America, including, if applicable, IFRS.

“General Partner” means KNOT Offshore Partners GP LLC, a company incorporated under the laws of the Marshall Islands and having its registered office at 2 Queen’s Cross, Aberdeen, Aberdeenshire, AB15 4YB, United Kingdom being the general partner in the Parent Guarantor.

“Group” means the Parent Guarantor and its Subsidiaries.

“Guarantee” means the guarantee liabilities of Guarantors pursuant to Clause 19 (Guarantee and indemnity).

“Hedging Agreement” means any ISDA Master Agreement or other master agreement, including any schedule or confirmation (as amended at any time, a “Master Agreement”) and/or any transaction or hedging arrangement, including Existing Hedging Transactions, pursuant to such Master Agreement (the “Hedging Transaction(s)”) entered or to be entered into between a Borrower (except the RCF Borrower) and a Hedging Bank, for the purpose of hedging interest rate, currency exchange or other non-speculative swap facility in relation to the Credit Facility and for the Borrowers’ (except the RCF Borrower) currency needs.

“Holding Company” means, in relation to a company or corporation, any other company or corporation in respect of which it is a Subsidiary.

schjodt.no | Page 18 of 146

“IFRS” means international accounting standards within the meaning of the IAS Regulation 1606/2002 to the extent applicable to the relevant financial statements.

“Initial Borrowing Date” means the date the first drawing of any Loan under the Credit Facility occurs, however no later than the last day of the Availability Period of the Term Loan Facilities.

“Insolvency Event” in relation to an entity means that the entity:

| (a) | is dissolved (other than pursuant to a consolidation, amalgamation or merger); |

| (b) | becomes insolvent or is unable to pay its debts or fails or admits in writing its inability generally to pay its debts as they become due; |

| (c) | makes a general assignment, arrangement or composition with or for the benefit of its creditors; |

| (d) | institutes or has instituted against it, by a regulator, supervisor or any similar official with primary insolvency, rehabilitative or regulatory jurisdiction over it in the jurisdiction of its incorporation or organisation or the jurisdiction of its head or home office, a proceeding seeking a judgment of insolvency or bankruptcy or any other relief under any bankruptcy or insolvency law or other similar law affecting creditors’ rights, or a petition is presented for its winding-up or liquidation by it or such regulator, supervisor or similar official; |

| (e) | has instituted against it a proceeding seeking a judgment of insolvency or bankruptcy or any other relief under any bankruptcy or insolvency law or other similar law affecting creditors’ rights, or a petition is presented for its winding-up or liquidation, and, in the case of any such proceeding or petition instituted or presented against it, such proceeding or petition is instituted or presented by a person or entity not described in paragraph (d) above and: |

| (i) | results in a judgment of insolvency or bankruptcy or the entry of an order for relief or the making of an order for its winding-up or liquidation; or |

| (ii) | is not dismissed, discharged, stayed or restrained in each case within 30 days of the institution or presentation thereof; |

| (f) | has a resolution passed for its winding-up, official management or liquidation (other than pursuant to a consolidation, amalgamation or merger); |

| (g) | seeks or becomes subject to the appointment of an administrator, provisional liquidator, conservator, receiver, trustee, custodian or other similar official for it or for all or substantially all its assets (other than, for so long as it is required by law or regulation not to be publicly disclosed, any such appointment which is to be made, or is made, by a person or entity described in paragraph (d) above); |

| (h) | has a secured party take possession of all or substantially all its assets or has a distress, execution, attachment, sequestration or other legal process levied, enforced or sued on or against all or substantially all its assets and such secured party maintains possession, or any such process is not dismissed, discharged, stayed or restrained, in each case within thirty (30) days thereafter; |

schjodt.no | Page 19 of 146

| (i) | causes or is subject to any event with respect to it which, under the applicable laws of any jurisdiction, has an analogous effect to any of the events specified in paragraphs (a) to (g) above; or |

| (j) | takes any action in furtherance of, or indicating its consent to, approval of, or acquiescence in, any of the foregoing acts. |

“Insurances” means, in relation to a Vessel, all policies and contracts of insurance (which expression includes all entries of that Vessel in a protection and indemnity or war risk association) which are from time to time during the Security Period in place or taken out or entered into by or for the benefit of the relevant Borrower (whether in the sole name of that Borrower or in the joint names of that Borrower and any other person) in respect of that Vessel or otherwise in connection with that Vessel and all benefits thereunder (including claims of whatsoever nature and return of premiums).

“Interest Period” means, in relation to a Loan, each period determined in accordance with Clause 10 (Interest Periods) and, in relation to an Unpaid Sum, each period determined in accordance with Clause 9.3 (Default interest).

“Interpolated Screen Rate” means, in relation to LIBOR for any Loan, the rate (rounded to the same number of decimal places as the two relevant Screen Rates) which results from interpolating on a linear basis between:

| (a) | the applicable Screen Rate for the longest period (for which that Screen Rate is available) which is less than the Interest Period of that Loan; and |

| (b) | the applicable Screen Rate for the shortest period (for which that Screen Rate is available) which exceeds the Interest Period of that Loan, |

each as of 11. a.m. in London on the Quotation Day for USD.

“Inventory of Hazardous Materials” means a document describing the materials present in each Vessel’s structure and equipment that may be hazardous to human health or the environment along with their respective location and approximate quantities.

“ISM Code” means the International Safety Management Code for the Safe Operation of Ships and for Pollution Prevention.

“ISPS Code” means the International Ship and Port Facility Security (ISPS) Code as adopted by the International Maritime Organization’s (IMO) Diplomatic Conference of December 2002.

“ISSC” means an International Ship Security Certificate issued by the Classification Society confirming that a Vessel is in compliance with the ISPS Code.

“KNOT” means Knutsen NYK Offshore Tankers AS, Norwegian registration no. 995 221 713, with registered offices at Smedasundet 40, N-5529 Haugesund, Norway.

“Lender” means:

schjodt.no | Page 20 of 146

| (a) | any Original Lender; and |

| (b) | any bank, financial institution, trust, fund or other entity which has become a Party in accordance with Clause 26 (Changes to the Lenders), |

which in each case has not ceased to be a Party in accordance with the terms of this Agreement.

“Lender Assignment Agreement” means an agreement substantially in the form set out in Schedule 5 (Form of Lender Assignment Agreement) or any other form agreed between the relevant assignor and assignee.

“Letter of Quiet Enjoyment” means, in respect of a Vessel, a letter of quiet enjoyment entered or to be entered into between the Agent, the relevant charterer and the relevant Borrower in respect of that charterer’s quiet enjoyment of that Vessel under the relevant charterparty, in form and substance satisfactory to the Lenders.

“LIBOR” means, in relation to any Loan:

| (a) | the applicable Screen Rate; |

| (b) | (if no Screen Rate is available for the Interest Period of that Loan) the Interpolated Screen Rate for that Loan; or |

| (c) | if: |

| (i) | no Screen Rate is available for USD; or |

| (ii) | no Screen Rate is available for the Interest Period of that Loan and it is not possible to calculate an Interpolated Screen Rate for that Loan, |

the Reference Bank Rate,

as of, in the case of paragraph (a) above, 11.00 a.m. London time and in the case of paragraph (c) above, 12:00 noon London time on the Quotation Day for USD and for a period equal in length to the Interest Period of that Loan and, if that rate is less than zero (0), LIBOR shall be deemed to be zero (0).

“Loan” means a loan made or to be made under a Facility or the principal amount outstanding for the time being of that loan.

“Majority Lenders” means:

| (a) | if there are no Loans then outstanding, a Lender or Lenders whose Commitments aggregate more than 662/3% of the Total Commitments (or, if the Total Commitments have been reduced to zero, aggregated more than 662/3% of the Total Commitments immediately prior to the reduction); or |

| (b) | at any other time, a Lender or Lenders whose participations in the Loans then outstanding aggregate more than 662/3% of all the Loans then outstanding. |

“Management Agreement” means any agreement made or to be made between a Borrower and a Manager for the technical and/or commercial management of a Vessel.

schjodt.no | Page 21 of 146

“Manager” means KNOT Management AS or one of its Affiliates acceptable to the Majority Lenders.

“Manager’s Undertaking” means an undertaking to be provided by each Manager in form to be determined by Agent.

“Margin” means two hundred and twelve point five basis points (212.5 bps) per annum.

“Market Value” means the fair market value of a Vessel, being the arithmetic average of valuations of that Vessel obtained from two (2) Approved Brokers, with or without physical inspection of that Vessel (as the Agent may require) on the basis of a sale for prompt delivery for cash at arm’s length on normal commercial terms as between a willing buyer and a willing seller, on an “as is, where is” basis, free of any existing charter or other contract of employment and/or pool arrangement.

“Material Adverse Effect” means any event or occurrence that in the reasonable opinion of the Lenders has or would have materially adversely affected or could adversely affect:

| (a) | the business, condition (financial or otherwise), operations, performance, assets or prospects of an Obligor or the Group taken as a whole since the date at which its latest audited financial statements were prepared; or |

| (b) | the ability of an Obligor to perform its obligations under the Finance Documents or the Hedging Agreements; or |

| (c) | the validity or enforceability of, or the effectiveness or ranking of any Security granted or purporting to be granted pursuant to, any Finance Document or Hedging Agreement; or |

| (d) | the right or remedy of a Finance Party or a Hedging Bank in respect of a Finance Document or a Hedging Agreement. |

“Month” means a period starting on one day in a calendar month and ending on the numerically corresponding day in the next calendar month, except that:

| (a) | if the numerically corresponding day is not a Business Day, that period shall end on the next Business Day in that calendar month in which that period is to end if there is one, or if there is not, on the immediately preceding Business Day; |

| (b) | if there is no numerically corresponding day in the calendar month in which that period is to end, that period shall end on the last Business Day in that calendar month. |

The above rules will only apply to the last Month of any period.

“Mortgaged Assets” means:

| (a) | the Vessels; |

| (b) | the Earnings; |

| (c) | the Insurances; |

| (d) | the Earnings Accounts; |

schjodt.no | Page 22 of 146

| (e) | the Borrowers’ (other than the RCF Borrower) trade receivables; |

| (f) | the Borrowers’ (other than the RCF Borrower) benefits under the Hedging Agreements; |

| (g) | the shares in each Borrower (other than the RCF Borrower and Borrower A) and the shares in Knutsen Shuttle Tankers XII AS (the general partner of Borrower A, which owns 10% of the partnership shares in Borrower A) and KNOT Shuttle Tankers 12 AS (a limited partner in Borrower A, which in turn owns 90% of the partnership shares in Borrower A). |

“Obligors” means the Borrowers and the Guarantors, and “Obligor” means any of them.

“Original Financial Statements” means:

| (a) | in relation to each Borrower, the audited financial statements for the financial year ended 31 December 2017; and |

| (b) | in relation to the Parent Guarantor, its audited consolidated financial statements for its financial year ended 31 December 2017. |

“Outstanding Indebtedness” means the aggregate of all sums of money at any time and from time to time owing to the Finance Parties under or pursuant to the Finance Documents.

“Party” means a party to this Agreement.

“Quotation Day” means, in relation to any period for which an interest rate is to be determined, two (2) Business Days before the first day of that period unless market practice differs in the Relevant Interbank Market in which case the Quotation Day will be determined by the Agent in accordance with market practice in the Relevant Interbank Market (and if quotations would normally be given by leading banks in the Relevant Interbank Market on more than one day, the Quotation Day will be the last of those days).

“Reference Bank Quotation” means any quotation supplied to the Agent by a Reference Bank.

“Reference Bank Rate” means the arithmetic mean of the rates (rounded upwards to four decimal places) as supplied to the Agent at its request by the Reference Banks as the rate at which the relevant Reference Bank could borrow funds in the London interbank market in USD for the relevant period were it to do so by asking for and then accepting interbank offers for deposits in reasonable market size in that currency and for that period.

“Reference Banks” means each Lender (other than BNP Paribas) or such other banks as may be appointed by the Agent in consultation with the Borrowers.

“Related Fund” in relation to a fund (the “first fund”), means a fund which is managed or advised by the same investment manager or investment adviser as the first fund or, if it is managed by a different investment manager or investment adviser, a fund whose investment manager or investment adviser is an Affiliate of the investment manager or investment adviser of the first fund.

“Relevant Interbank Market” means the London interbank market.

“Relevant Person” means:

schjodt.no | Page 23 of 146

| (a) | each member of the Group; and |

| (b) | each of its directors, officers, employees, agents and representatives. |

“Repeating Representations” means each of the representations set out in Clause 20 (Representations), except that any repetition of Clause 20.27 (Sanctions) shall not include representation on behalf of joint ventures which are not Affiliates.

“Representative” means any delegate, agent, manager, administrator, nominee, attorney, trustee or custodian.

“Resolution Authority” means any body which has authority to exercise any Write-down and Conversion Powers.

“Restricted Party” means a person that is:

| (a) | listed on any Sanctions List or targeted by Sanctions (whether designated by name or by reason of being included in a class of person); or |

| (b) | located, organised or resident in or incorporated under the laws of any country or territory that is, or whose government is, the target of Sanctions broadly prohibiting dealings with such government, country, or territory (including, without limitation, at the date of this Agreement, Crimea/Sevastopol, Cuba, Iran, North Korea, Syria and Sudan); or |

| (c) | directly or indirectly owned or controlled by, or acting on behalf, at the direction or for the benefit of, a person referred to in (a) and/or (to the extent relevant under Sanctions) (b) above; or |

| (d) | otherwise a subject of Sanctions. |

“Revolving Credit Facility” means the revolving credit facility made available under this Agreement as described in Clause 2.2 (The Revolving Credit Facility), for which the RCF Borrower shall be liable and responsible.

“Revolving Credit Facility Commitment” means:

| (a) | in relation to an Original Lender, the amount set opposite its name under the heading “Revolving Credit Facility Commitment” in Part A of Schedule 1 (The Original Parties); and |

| (b) | in relation to any other Lender, the amount of any Revolving Credit Commitment transferred to it under this Agreement, |

to the extent not cancelled, reduced or transferred by it under this Agreement.

“Revolving Credit Facility Loan” means a loan made or to be made under the Revolving Credit Facility or the principal amount outstanding for the time being of that loan.

“Rollover Loan” means one or more Revolving Credit Facility Loans:

| (a) | made or to be made on the same day that a maturing Revolving Credit Facility Loan is due to be repaid; |

schjodt.no | Page 24 of 146

| (b) | the aggregate amount of which is equal to or less than the amount of the maturing Revolving Credit Facility Loan; and |

| (c) | made or to be made to the same Borrower for the purpose of refinancing that maturing Revolving Credit Facility Loan |

“Sanctions” means any economic, trade or financial sanctions or embargoes or other restrictive measures implemented, adapted, imposed, administered, enacted and/or enforced by any Sanctions Authority.

“Sanctions Authority” means the Norwegian State, the United Nations, the European Union, the United Kingdom, the member states of the European Union, the United States of America, Australia, any country to which any Obligor is bound and any authority acting on behalf of any of them in connection with Sanctions (including (without limitation)_the U.S. Office of Foreign Assets Control (“OFAC”), the U.S. Department of State, Her Majesty’s Treasury (“HMT”) and the United Nations Security Council.

“Sanctions List” means (a) the lists of Sanctions designations and/or targets maintained by any Sanctions Authority (including but not limited to the Specially Designated Nationals and Blocked Persons list maintained by OFAC, the Consolidated List of Financial Sanctions Targets maintained by HMT) and/or (b) any other Sanctions designation or target listed and/or adopted by a Sanctions Authority, in all cases, from time to time.

“Screen Rate” means the London interbank offered rate administered by ICE Benchmark Administration Limited (or any other person which takes over the administration of that rate) for USD for the relevant period displayed (before any correction, recalculation or republication by the administrator) on page LIBOR01/LIBOR02 of the Thomson Reuters Screen (or any replacement Thomson Reuters page which displays that rate) or on the appropriate page of such other information service which publishes that rate from time to time in place of Thomson Reuters. If such page or service ceases to be available, the Agent may specify another page or service displaying the relevant rate after consultation with the Borrowers and the Lenders.

“Security” means a mortgage, charge, pledge, lien or other security interest securing any obligation of any person or any other agreement or arrangement having a similar effect.

“Security Document” means each document listed in Clause 18 (Security) and any other document agreement agreed between the Parties to be a Security Document.

“Security Period” means the period commencing on the date of this Agreement and ending the date on which the Agent notifies the Borrowers, the other Finance Parties and the Hedging Banks that:

| (a) | all amounts which have become due for payment by the Borrowers under the Finance Documents and the Hedging Agreements have been paid; |

| (b) | no amount is owing or has accrued (without yet having become due for payment) under any of the Finance Documents and the Hedging Agreements; |

| (c) | none of the Obligors have any future or contingent liability under any provision of this Agreement, the other Finance Documents and the Hedging Agreements; and |

schjodt.no | Page 25 of 146

| (d) | the Agent, the Lenders and the Hedging Banks do not consider that there is a significant risk that any payment or transaction under a Finance Document or a Hedging Agreement would be set aside, or would have to be reversed or adjusted, in any present or possible future proceeding relating to a Finance Document a Hedging Agreement or any asset covered (or previously covered) by a Security created by a Finance Document a Hedging Agreement. |

“Selection Notice” means a notice substantially in the form set out in Part II (Selection Notice) of Schedule 3 (Requests) given in accordance with Clause 10 (Interest Periods).

“Share Pledges” means together Borrower A Share Pledge, Borrower B Share Pledge, Borrower C Share Pledge, Borrower D Share Pledge and Borrower E Share Pledge, and “Share Pledge” means either of them.

“Shareholder Loans” means shareholder loans and/or loans from other companies within the Group and/or loans from other Affiliates.

“SMC” means a valid safety management certificate issued for a Vessel issued by the Classification Society pursuant to paragraph 13.7 of the ISM Code.

“SMS” means a safety management system for a Vessel developed and implemented in accordance with the ISM Code and including the functional requirements duties and obligations that follow from the ISM Code.

“SOLAS” means the International Convention for Safety of Life at Sea, 1974, as amended from time to time.

“Subsidiary” means an entity of which a person has direct or indirect control (whether through the ownership of voting capital, by contract or otherwise) or owns directly or indirectly more than 50% of the shares and for this purpose an entity shall be treated as controlled by another if that entity is able to direct its affairs and/or to control the composition of the board of directors or equivalent body.

“Tax” means any tax, levy, impost, duty or other charge or withholding of a similar nature (including any penalty or interest payable in connection with any failure to pay or any delay in paying any of the same).

“Term Loan” means a loan made or to be made under the Term Loan Facility A or the Term Loan Facility B.

“Term Loan Facilities” means the Term Loans Facility A and Term Loan Facility B.

“Term Loan Facility A” means a term loan facility in the aggregate principal amount of up to USD 115,000,000, for which the Borrower A is liable and responsible, split into Term Loan Facility A Tranches.

“Term Loan Facility A Commitment” means:

| (a) | in relation to an Original Lender the amount set opposite its name under the heading “Term Loan Facility A” in Part A of Schedule 1 (The Original Parties); and |

| (b) | in relation to any other Lender, the amount of any Term Loan Facility A Commitment transferred to it under this Agreement, to the extent not cancelled, reduced or transferred by it under this Agreement. |

schjodt.no | Page 26 of 146

“Term Loan Facility A Tranches” means together the Term Loan Facility Tranche 1 and the Term Loan Facility Tranche 2.

“Term Loan Facility Tranche 1” means a tranche in the principal amount of up to USD 57,500,000, which relates to the refinancing of Vessel 1.

“Term Loan Facility Tranche 2” means a tranche in the principal amount of up to USD 57,500,000, which relates to the refinancing of Vessel 2.

“Term Loan Facility B” means a term loan facility in the aggregate principal amount of up to USD 205,000,000, for which the Term Loan Facility B Borrowers are jointly and severally responsible and liable, split into the Term Loan Facility B Tranches.

“Term Loan Facility B Borrowers” means Borrower B, Borrower C, Borrower D and Borrower E.

“Term Loan Facility B Commitment” means:

| (a) | in relation to an Original Lender the amount set opposite its name under the heading “Term Loan Facility B” in Part A of Schedule 1 (The Original Parties); and |

| (b) | in relation to any other Lender, the amount of any Term Loan Facility A Commitment transferred to it under this Agreement, |

to the extent not cancelled, reduced or transferred by it under this Agreement.

“Term Loan Facility B Tranches” means together the Term Loan Facility Tranche 3, the Term Loan Facility Tranche 4, the Term Loan Facility Tranche 5 and the Term Loan Facility Trance 6.

“Term Loan Facility Tranche 3” means a tranche in the principal amount of up to USD 51,724,363, which relates to the refinancing of Vessel 3.

“Term Loan Facility Tranche 4” means a tranche in the principal amount of up to USD 55,121,815, which relates to the refinancing of Vessel 4.

“Term Loan Facility Tranche 5” means a tranche in the principal amount of up to USD 54,574,891, which relates to the refinancing of Vessel 5.

“Term Loan Facility Tranche 6” means a tranche in the principal amount of up to USD 43,578,931, which relates to the refinancing of Vessel 6.

“Total Commitments” means the aggregate of the Commitments, being on the date of this Agreement USD 375,000,000.

“Total Revolving Credit Facility Commitments” means the aggregate of the Revolving Credit Facility Commitments, being USD 55,000,000 on the date of this agreement.

“Total Term Loan Facility A Commitments” means the aggregate of the Term Loan Facility A Commitments, being USD 115,000,000 on the date of this agreement.

schjodt.no | Page 27 of 146

“Total Term Loan Facility B Commitments” means the aggregate of the Term Loan Facility B Commitments, being USD 205,000,000 on the date of this agreement.

“Total Loss” means, in relation to a Vessel:

| (a) | the actual, constructive, compromised, agreed, arranged or other total loss of that Vessel; |

| (b) | the requisition for title or compulsory acquisition of that Vessel by any government or other competent authority; |

| (c) | the capture, seizure, destruction, abandonment, condemnation, arrest, detention or confiscation of that Vessel by any government or by persons acting or purporting to act on behalf of any government or public authority, unless that Vessel is released and returned to the possession of the relevant Borrower within thirty (30) days after the capture, seizure, arrest, detention or confiscation in question; or |

| (d) | any piracy, hijacking or theft of that Vessel, unless that Vessel is released and restored to the relevant Borrower within thirty (30) days after the occurrence of such incident. |

“Total Loss Date” means:

| (a) | in the case of an actual total loss of a Vessel, the date on which it occurred or, if that is unknown, the date when that Vessel was last heard of; |

| (b) | in the case of a constructive, compromised, agreed or arranged total loss of a Vessel, the earlier of: (i) the date on which a notice of abandonment is given to the insurers (provided a claim for total loss is admitted by such insurers) or, if such insurers do not forthwith admit such a claim, at the date at which either a total loss is subsequently admitted by the insurers or a total loss is subsequently adjudged by a competent court of law or arbitration panel to have occurred or, if earlier, the date falling three (3) Months after notice of abandonment of that Vessel was given to the insurers; and (ii) the date of compromise, arrangement or agreement made by or on behalf of the relevant Borrower with that Vessel’s insurers in which the insurers agree to treat that Vessel as a total loss; or |

| (c) | in the case of any other type of total loss, on the date (or the most likely date) on which it appears to the Agent that the event constituting the total loss occurred. |

“Tranches” means together the Term Loan Facility A Tranches and the Term Loan Facility B Tranches, and “Tranche” means any of them.

“Transaction Documents” means the Management Agreements, together with the other documents contemplated herein or therein or otherwise designated as a Transaction Document by the Agent and the Borrowers, and “Transaction Document” means any of them.

“Transfer Certificate” means a certificate substantially in the form set out in Schedule 4 (Form of Transfer Certificate) or any other form agreed between the Agent and the Borrowers.

“Transfer Date” means, in relation to a transfer, the later of:

| (a) | the proposed Transfer Date specified in the relevant Transfer Certificate; and |

schjodt.no | Page 28 of 146

| (b) | the date on which the Agent executes the relevant Transfer Certificate. |

“US” means the United States of America.

“US Tax Obligor” means:

| (a) | a Borrower which is resident for tax purposes in the US; or |

| (b) | an Obligor some or all of whose payments under the Finance Documents are from sources within the US for US federal income tax purposes. |

“Unpaid Sum” means any sum due and payable but unpaid by an Obligor under the Finance Documents.

“Utilisation” means a utilisation of a Facility.

“Utilisation Date” means the date of a Utilisation, being the date on which the relevant Loan is to be made.

“Utilisation Request” means a notice substantially in the form set out in Part I (Utilisation Request) of Schedule 3 (Requests).

“VAT” means value added tax as provided for in the Norwegian Value Added Tax Act of 19 June 2009 no. 58 (Nw. Merverdiavgiftsloven) and any other tax of a similar nature.

“Vessel 1” means MT “Fortaleza Knutsen”, IMO no. 9499876, registered in the name of Borrower A in an Approved Ship Registry.

“Vessel 2” means MT “Recife Knutsen”, IMO no. 9499888, registered in the name of Borrower A in an Approved Ship Registry.

“Vessel 3” means MT “Carmen Knutsen”, IMO no. 9623635, registered in the name of Borrower B in an Approved Ship Registry.

“Vessel 4” means MT “Ingrid Knutsen”, IMO no. 9649225, registered in the name of Borrower C in an Approved Ship Registry.

“Vessel 5” means MT “Bodil Knutsen”, IMO no. 9472529, registered in the name of Borrower D in an Approved Ship Registry.

“Vessel 6” means MT “Windsor Knutsen”, IMO no. 9316115, registered in the name of Borrower E in an Approved Ship Registry.

“Vessels” means together Vessel 1, Vessel 2 and Vessel 3, Vessel 4, Vessel 5, Vessel 6, and “Vessel” means any of them.

“Write-down and Conversion Powers” means:

| (a) | in relation to any Bail-In Legislation described in the EU Bail-In Legislation Schedule from time to time, the powers described as such in relation to that Bail-In Legislation in the EU Bail-In Legislation Schedule; and |

| (b) | in relation to any other applicable Bail-In Legislation: |

schjodt.no | Page 29 of 146

| (i) | any powers under that Bail-In Legislation to cancel, transfer or dilute shares issued by a person that is a bank or investment firm or other financial institution or affiliate of a bank, investment firm or other financial institution, to cancel, reduce, modify or change the form of a liability of such a person or any contract or instrument under which that liability arises, to convert all or part of that liability into shares, securities or obligations of that person or any other person, to provide that any such contract or instrument is to have effect as if a right had been exercised under it or to suspend any obligation in respect of that liability or any of the powers under that Bail-In Legislation that are related to or ancillary to any of those powers; and |

| (ii) | any similar or analogous powers under that Bail-In Legislation. |

| 1.2 | Construction |

| (a) | Unless a contrary indication appears, any reference in this Agreement to: |

| (i) | the “Agent”, the “Co-Ordinator”, a “Mandated Lead Arranger”, a “Bookrunner”, any “Finance Party”, any “Lender”, or any “Party” shall be construed so as to include its successors in title, permitted assigns and permitted transferees to, or of, its rights and/or obligations under the Finance Documents; |

| (ii) | “Nordea Bank AB (publ), filial i Norge” (either directly or indirectly in its capacity as Lender, Mandated Lead Arranger, Bookrunner, Co-Ordinator or any other capacity) in the Finance Documents shall be automatically construed as a reference to Nordea Bank Abp in the event of any corporate reconstruction, merger, amalgamation, consolidation between Nordea Bank AB (publ) and Nordea Bank Abp where Nordea Bank Abp is the surviving entity and acquires all the rights of and assumes all the obligations of Nordea Bank AB (publ), Finnish Branch and nothing in the Finance Documents shall be construed so as to restrict, limit or impose any notification or other requirement or condition on either Nordea Bank AB (publ), Finnish Branch or Nordea Bank Abp in respect of the acquisition of rights to or assumption of obligations by Nordea Bank Abp hereunder pursuant to such merger; |

| (iii) | a “Hedging Bank”, shall be construed so as to include its successors in title, permitted assigns and permitted transferees to, or of, its rights and/or obligations under any Hedging Agreement; |

| (iv) | “assets” includes present and future properties, revenues and rights of every description; |

| (v) | a “Finance Document”, “Transaction Document” or any other agreement or instrument is a reference to that Finance Document, Transaction Document or other agreement or instrument as amended, novated, supplemented, extended or restated; |

| (vi) | a “group of Lenders” includes all the Lenders; |

schjodt.no | Page 30 of 146

| (vii) | “indebtedness” includes any obligation (whether incurred as principal or as surety) for the payment or repayment of money, whether present or future, actual or contingent; |

| (viii) | a “person” includes any individual, firm, company, corporation, government, state or agency of a state or any association, trust, joint venture, consortium, partnership or other entity (whether or not having separate legal personality); |

| (ix) | a “regulation” includes any regulation, rule, official directive, request or guideline (whether or not having the force of law) of any governmental, intergovernmental or supranational body, agency, department or of any regulatory, self-regulatory or other authority or organisation; |

| (x) | a provision of law is a reference to that provision as amended or re-enacted; |

| (xi) | words importing the singular shall include the plural and vice versa; and |

| (xii) | a time of day is a reference to Central European time (CET) unless specified otherwise. |

| (b) | Section, Clause and Schedule headings are for ease of reference only. |

| (c) | Unless a contrary indication appears, a term used in any other Finance Document or in any notice given under or in connection with any Finance Document has the same meaning in that Finance Document or notice as in this Agreement. |

| (d) | Each Hedging Agreement shall operate subject to the terms of this Agreement and, accordingly, in the event of any inconsistency between the terms of a Hedging Agreement and this Agreement, the terms of this Agreement will prevail. |

| (e) | A Default is “continuing” if it has not been remedied or waived and an Event of Default is “continuing” if it has not been waived. |

| 1.3 | Currency symbols and definitions |

“$”, “USD” and “dollars” denote the lawful currency of the United States of America and “kr”, “NOK” and “norske kroner” denote the lawful currency of Norway.

SECTION 2

THE CREDIT FACILITY

| 2. | THE CREDIT FACILITY |

| 2.1 | The Term Loan Facilities |

| (a) | Subject to the terms of this Agreement, the Lenders make available to Borrower A a senior secured USD term loan facility in an aggregate amount equal to the Total Term Loan Facility A Commitments. |