Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 20-F

| ¨ | REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EXCHANGE ACT OF 1934

| |

| OR

| ||

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

| |

| For the fiscal year ended December 31, 2013

| ||

| OR

| ||

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

| |

| OR

| ||

| ¨ |

SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Commission File Number 001-35931

Constellium N.V.

(Exact Name of Registrant as Specified in its Charter)

Constellium N.V.

(Translation of Registrant’s name into English)

The Netherlands

(Jurisdiction of incorporation or organization)

Tupolevlaan 41-61,

1119 NW Schiphol-Rijk

The Netherlands

(Address of principal executive offices)

Securities registered or to be registered pursuant to Section 12(b) of the Act.

| Title of each class |

Name of each exchange on which registered | |

| Ordinary Shares | New York Stock Exchange |

Securities registered or to be registered pursuant to Section 12(g) of the Act:

None

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act:

None

Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the period covered by the annual report:

104,076,718 Class A Ordinary Shares, Nominal Value €0.02 per share

950,337 Class B Ordinary Shares, Nominal Value €0.02 per share

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. ¨ Yes x No

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934. ¨ Yes x No

Note—Checking the box above will not relieve any registrant required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 from their obligations under those Sections.

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. x Yes ¨ No

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). ¨ Yes ¨ No

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer. See definition of “accelerated filer and large accelerated filer” in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer ¨ Accelerated filer ¨ Non-accelerated filer x

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

| U.S. GAAP ¨ |

International Financial Reporting Standards as issued by the International Accounting Standards Board x | Other ¨ |

If “Other” has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow: Item 17 ¨ Item 18 ¨

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). ¨ Yes x No

Table of Contents

Table of Contents

SPECIAL NOTE ABOUT FORWARD-LOOKING STATEMENTS

This annual report on Form 20-F (the “Annual Report”) contains “forward-looking statements” with respect to our business, results of operations and financial condition, and our expectations or beliefs concerning future events and conditions. You can identify certain forward-looking statements because they contain words such as, but not limited to, “believes,” “expects,” “may,” “should,” “approximately,” “anticipates,” “estimates,” “intends,” “plans,” “targets,” “likely,” “will,” “would,” “could” and similar expressions (or the negative of these terminologies or expressions). All forward-looking statements involve risks and uncertainties. Many risks and uncertainties are inherent in our industry and markets. Others are more specific to our business and operations. The occurrence of the events described and the achievement of the expected results depend on many events, some or all of which are not predictable or within our control. Actual results may differ materially from the forward-looking statements contained in this Annual Report.

Important factors that could cause actual results to differ materially from those expressed or implied by the forward-looking statements are disclosed under the heading “Item 3. Key Information–D. Risk Factors” and elsewhere in this Annual Report, including, without limitation, in conjunction with the forward-looking statements included in this Annual Report. All forward-looking statements in this Annual Report and subsequent written and oral forward-looking statements attributable to us, or persons acting on our behalf, are expressly qualified in their entirety by the cautionary statements. Some of the factors that we believe could materially affect our results include:

| • | our ability to implement our business strategy, including our productivity and cost reduction initiatives; |

| • | our susceptibility to cyclical fluctuations in the metals industry, our end-markets and our customers’ industries, and changes in general economic conditions; |

| • | the highly competitive nature of the metals industry and the risk that aluminum will become less competitive compared to alternative materials; |

| • | the possibility of unplanned business interruptions and equipment failure; |

| • | adverse conditions and disruptions in regional and global economies, including Europe and North America; |

| • | the risk associated with being dependent on a limited number of suppliers for a substantial portion of our primary and scrap aluminum; |

| • | the risk that we may be required to bear increases in operating costs under our multi-year contracts with customers, or certain fixed costs in the event of early termination of contracts; |

| • | competition and consolidation in the industries in which we operate; |

| • | our ability to maintain and continuously improve our information technology and operational systems and financial reporting and internal controls; |

| • | our ability to manage our labor costs and labor relations and attract and retain qualified employees; |

| • | losses or increased funding and expenses related to our pensions, other post-employment benefits and other long-term employee benefits plans; |

| • | the risk that regulation and litigation pose to our business, including our ability to maintain required licenses and regulatory approvals and comply with applicable laws and regulations, and the effects of potential changes in governmental regulations; |

| • | risk associated with our global operations, including natural disasters and currency fluctuations; |

| • | changes in our effective income tax rate or accounting standards; |

| • | costs or liabilities associated with environmental, health and safety matters; and |

| • | the other factors presented under the heading “Item 3. Key Information–D. Risk Factors.” |

We caution you that the foregoing list may not contain all of the factors that are important to you. In addition, in light of these risks and uncertainties, the matters referred to in the forward-looking statements contained in this Annual Report may not in fact occur. We undertake no obligation to publicly update or revise any forward-looking statement as a result of new information, future events or otherwise, except as required by law.

-1-

Table of Contents

Item 1. Identity of Directors, Senior Management and Advisers

Not applicable.

Item 2. Offer Statistics and Expected Timetable

Not applicable.

A. Selected Financial Data

The following tables set forth our selected historical financial and operating data.

On January 4, 2011, Omega Holdco B.V., which later changed its name to Constellium Holdco B.V., and then again to Constellium N.V. (“Constellium” or the “Successor”) acquired the Alcan Engineered Aluminum Products business unit (the “AEP Business” or the “Predecessor”) from affiliates of Rio Tinto, a leading international mining group, combining Rio Tinto plc, a London listed public company headquartered in the United Kingdom, and Rio Tinto Limited, which is listed on the Australian Stock Exchange, with executive offices in Melbourne (the two companies are joined in a dual listed companies structure as a single economic entity, called the Rio Tinto Group (“Rio Tinto”) (the “Acquisition”). For comparison purposes, our results of operations for the years ended December 31, 2011, 2012 and 2013 are presented alongside the results of operations of the Predecessor for the years ended December 31, 2009 and 2010. However, our Successor and Predecessor periods are not directly comparable due to the impact of the application of purchase accounting and the preparation of the Predecessor accounts on a carve-out basis. The financial position, results of operations and cash flows of the Predecessor do not necessarily reflect what our financial position or results of operations would have been if we had been operated as a standalone entity during the periods covered by the Predecessor financial statements and are not indicative of our future results of operations and financial position.

The selected historical financial information of the Predecessor as of and for the years ended December 31, 2009 and 2010 has been prepared to present the assets, liabilities, revenues and expenses of the combined AEP Business on a standalone basis up to the date of divestment from Rio Tinto.

The selected historical financial information as of and for the years ended December 31, 2011, 2012 and 2013 has been derived from the audited consolidated financial statements included elsewhere in this Annual Report.

The audited consolidated financial statements included elsewhere in this Annual Report have been prepared according to the International Financial Reporting Standards (“IFRS”), as issued by the International Accounting Standards Board (the “IASB”), and as endorsed by the European Union (“EU”).

Effective January 1, 2013, we have adopted IAS 19 “Employee Benefits” (revised) (IAS 19) in our audited consolidated financial statements as of and for the year ended December 31, 2013 and in accordance with transition rules in IAS 19 we have retrospectively applied this standard to the two years ending December 31, 2012 and 2011. We have not restated our audited combined financial statements for the years ended December 31, 2009 and 2010 as the impact of this revised standard is not material to our results of operations and financial position.

-2-

Table of Contents

References to “tons” throughout this Annual Report are to metrics tons.

| Successor as of and for the year ended December 31, |

Predecessor as of and for the year ended December 31, |

|||||||||||||||||||

| (€ in millions other than per share and per ton data) | 2013 | 2012(1) | 2011(1) | 2010 | 2009 | |||||||||||||||

| Statement of income data: |

||||||||||||||||||||

| Revenue |

3,495 | 3,610 | 3,556 | 2,957 | 2,292 | |||||||||||||||

| Gross profit |

471 | 474 | 317 | 242 | 42 | |||||||||||||||

| Operating profit/(loss) |

209 | 263 | (63 | ) | (248 | ) | (240 | ) | ||||||||||||

| Profit/(loss) for the period—continuing operations |

96 | 149 | (170 | ) | (209 | ) | (215 | ) | ||||||||||||

| Profit/(loss) for the period |

100 | 141 | (178 | ) | (207 | ) | (218 | ) | ||||||||||||

| Profit/(loss) per share—basic and diluted |

1.0 | 1.6 | (2.0 | ) | n/a | n/a | ||||||||||||||

| Profit/(loss) per share—basic and diluted—continuing operations |

1.0 | 1.6 | (1.9 | ) | n/a | n/a | ||||||||||||||

| Weighted average number of shares outstanding |

98,890,945 | 89,442,416 | 89,338,433 | n/a | n/a | |||||||||||||||

| Dividends per ordinary share (euro)(3) |

— | — | — | — | — | |||||||||||||||

| Balance sheet data: |

||||||||||||||||||||

| Total assets |

1,764 | 1,631 | 1,612 | 1,837 | 2,040 | |||||||||||||||

| Net liabilities or total invested equity |

36 | (37 | ) | (113 | ) | 199 | 108 | |||||||||||||

| Share capital |

2 | — | — | n/a | n/a | |||||||||||||||

| Other operational and financial data (unaudited): |

||||||||||||||||||||

| Net trade working capital(2) |

222 | 289 | 381 | 519 | 416 | |||||||||||||||

| Capital expenditure |

144 | 126 | 97 | 51 | 61 | |||||||||||||||

| Volumes (in kt) |

1,025 | 1,033 | 1,058 | 972 | 868 | |||||||||||||||

| Revenue per ton (€ per ton) |

3,410 | 3,495 | 3,362 | 3,042 | 2,641 | |||||||||||||||

| (1) | Comparative financial statements have been restated following the application of IAS 19 revised. The impacts of the restatements are disclosed in Note 32 of the audited consolidated financial statements included elsewhere in this Annual Report. |

| (2) | Net trade working capital represents total inventories plus trade receivables less trade payables. |

| (3) | Prior to our initial public offering in May 2013 (the “IPO”), we paid certain dividends to holders of our ordinary shares, as well as to holders of our preferred shares, as is further described in “Item 4. Information on the Company–A. History and Development of the Company.” |

B. Capitalization and Indebtedness

Not applicable.

C. Reasons for the Offer and Use of Proceeds

Not applicable.

D. Risk Factors

Risks Related to Our Business

If we fail to implement our business strategy, including our productivity and cost reduction initiatives, our financial condition and results of operations could be materially adversely affected.

Our future financial performance and success depend in large part on our ability to successfully implement our business strategy, including investing in high-return opportunities in our core markets, focusing on higher-margin, technologically advanced products, differentiating our products, expanding our strategic relationships with customers in selected international regions, fixed-cost containment and cash management, and executing on our Lean manufacturing program, which is described in “Item 4. Information on the Company–B. Business

-3-

Table of Contents

Overview.” We cannot assure you that we will be able to successfully implement our business strategy or be able to continue improving our operating results. For example, we have recently announced the intention to create a joint venture in the United States, to serve the North American market. The proposed Body-in-White joint venture is currently in the planning stages, and any inability to create or execute on our strategy with respect to the joint venture may cause a decline in the trading price of our ordinary shares. Implementation of our business strategy could be affected by a number of factors beyond our control, such as increased competition, legal and regulatory developments, general economic conditions or an increase in operating costs. Any failure to successfully implement our business strategy could adversely affect our financial condition and results of operations. In addition, we may decide to alter or discontinue certain aspects of our business strategy at any time. Although we have undertaken and expect to continue to undertake productivity and cost reduction initiatives to improve performance, such as the Lean manufacturing program, we cannot assure you that all of these initiatives will be completed or that any estimated cost savings from such activities will be fully realized. Even when we are able to generate new efficiencies in the short- to medium-term, we may not be able to continue to reduce cost and increase productivity over the long term.

The cyclical and seasonal nature of the metals industry, our end-use markets and our customers’ industries, in particular our aerospace, automotive, heavy duty truck and trailer industries, could negatively affect our financial condition and results of operations.

The metals industry is generally cyclical in nature, and these cyclical fluctuations tend to directly correlate with changes in general and local economic conditions. These conditions include the level of economic growth, financing availability, the availability of affordable energy sources, employment levels, interest rates, consumer confidence and housing demand. Historically, in periods of recession or periods of minimal economic growth, metals companies have often tended to underperform other sectors. In addition, economic downturns in regional and global economies, including in Europe, or a prolonged recession in our principal industry segments, have had a negative impact on our operations in the past and could have a negative impact on our future financial condition or results of operations. Although we continue to seek to diversify our business on a geographic and end-market basis, we cannot assure you that diversification would mitigate the effect of cyclical downturns.

We are particularly sensitive to cycles in the aerospace, defense, automotive, other transportation, building and construction and general engineering end-markets, which are highly cyclical. During recessions or periods of low growth, these industries typically experience major cutbacks in production, resulting in decreased demand for aluminum products. This leads to significant fluctuations in demand and pricing for our products and services. Because our operations are capital intensive and we generally have high fixed costs and may not be able to reduce costs and production capacity on a sufficiently rapid basis, our near-term profitability may be significantly affected by decreased processing volumes. Accordingly, reduced demand and pricing pressures may significantly reduce our profitability and materially adversely affect our financial condition, results of operations and cash flows.

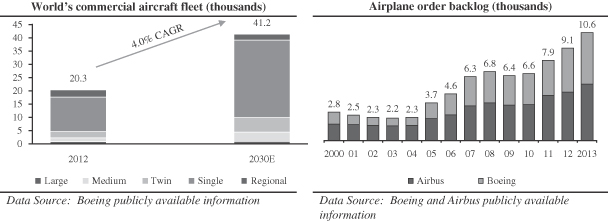

In particular, we derive a significant portion of our revenues from products sold to the aerospace industry, which is highly cyclical and tends to decline in response to overall declines in the general economy. The commercial aerospace industry is historically driven by the demand from commercial airlines for new aircraft. Demand for commercial aircraft is influenced by airline industry profitability, trends in airline passenger traffic, the state of the U.S. and global economies and numerous other factors, including the effects of terrorism. A number of major airlines have undergone Chapter 11 bankruptcy or comparable insolvency proceedings and experienced financial strain from volatile fuel prices. The aerospace industry also suffered significantly in the wake of the events of September 11, 2001, resulting in a sharp decrease globally in new commercial aircraft deliveries and order cancellations or deferrals by the major airlines. Despite existing backlogs, continued financial uncertainty in the industry, inadequate liquidity of certain airline companies, production issues and delays in the launch of new aircraft programs at major aircraft manufacturers, stock variations in the supply chain, terrorist acts or the increased threat of terrorism may lead to reduced demand for new aircraft that utilize our products, which could materially adversely affect our financial position, results of operations and cash flows.

-4-

Table of Contents

Further, the demand for our automotive extrusions and rolled products and many of our general engineering and other industrial products is dependent on the production of cars, light trucks, and heavy duty vehicles and trailers. The automotive industry is highly cyclical, as new vehicle demand is dependent on consumer spending and is tied closely to the strength of the overall economy. We note that the demand for luxury vehicles in China has become significant over the past several years and therefore fluctuations in the Chinese economy may adversely affect the demand for our products. Production cuts by manufacturers may adversely affect the demand for our products. Many automotive related manufacturers and first tier suppliers are burdened with substantial structural costs, including pension, healthcare and labor costs that have resulted in severe financial difficulty, including bankruptcy, for several of them. A worsening of these companies’ financial condition or their bankruptcy could have further serious effects on the conditions of the markets, which directly affects the demand for our products. In addition, the loss of business with respect to, or a lack of commercial success of, one or more particular vehicle models for which we are a significant supplier could have a materially adverse impact on our financial position, results of operations and cash flows.

Customer demand in the aluminum industry is also affected by holiday seasons, weather conditions, economic and other factors beyond our control. Our volumes are impacted by the timing of the holiday seasons in particular, with August and December typically being the lowest months and January to June being the strongest months. Our business is also impacted by seasonal slowdowns and upturns in certain of our customers’ industries. Historically, the can industry is strongest in the spring and summer season, whereas the automotive and construction sectors encounter slowdowns in both the third and fourth quarters of the calendar year. Therefore, our quarterly financial results could fluctuate as a result of climatic or other seasonal changes, and a prolonged period of unusually cool summers in different regions in which we conduct our business could have a negative effect on our financial results and cash flows.

We are subject to unplanned business interruptions that may materially adversely affect our business.

Our operations may be materially adversely affected by unplanned events such as explosions, fires, war or terrorism, inclement weather, accidents, equipment, information technology systems and process failures, electrical blackouts or outages, transportation interruptions and supply interruptions. Operational interruptions at one or more of our production facilities could cause substantial losses and delays in our production capacity or increase our operating costs. In addition, replacement of assets damaged by such events could be difficult or expensive, and to the extent these losses are not covered by insurance or our insurance policies have significant deductibles, our financial position, results of operations and cash flows may be materially adversely affected by such events. For example, in 2008, a stretcher at Constellium’s Ravenswood facility was damaged due to a defect in its hydraulic system, causing a substantial outage at that facility that had a material impact on our production volumes at this facility and on our financial results for the affected period. Furthermore, because customers may be dependent on planned deliveries from us, customers that have to reschedule their own production due to our delivery delays may be able to pursue financial claims against us, and we may incur costs to correct such problems in addition to any liability resulting from such claims. Interruptions may also harm our reputation among actual and potential customers, potentially resulting in a loss of business.

Our business involves significant activity in Europe, and adverse conditions and disruptions in European economies could have a material adverse effect on our operations or financial performance.

A material portion of our sales are generated by customers located in Europe. The financial markets remain concerned about the ability of certain European countries to finance their deficits and service growing debt burdens amidst difficult economic conditions. This loss of confidence has led to rescue measures by Eurozone countries and the International Monetary Fund. Despite these measures, concerns persist regarding the debt burden of certain Eurozone countries and their ability to meet future financial obligations, the overall stability of the euro and the suitability of the euro as a single currency given the diverse economic and political circumstances in individual Eurozone countries. In addition, the actions required to be taken by those countries as a condition to rescue packages, and by other countries to mitigate similar developments in their economies, have

-5-

Table of Contents

resulted in increased political discord within and among Eurozone countries. The interdependencies among European economies and financial institutions have also exacerbated concern regarding the stability of European financial markets generally. These concerns could lead to the re-introduction of individual currencies in one or more Eurozone countries, or, in more extreme circumstances, the possible dissolution of the euro currency entirely. Should the euro dissolve entirely, the legal and contractual consequences for holders of euro-denominated obligations would be determined by laws in effect at such time. These potential developments, or market perceptions concerning these and related issues, could materially adversely affect the value of the Company’s euro-denominated assets and obligations. In addition, concerns over the effect of this financial crisis on financial institutions in Europe and globally could have a material adverse impact on the capital markets generally. Persistent disruptions in the European financial markets, the overall stability of the euro and the suitability of the euro as a single currency or the failure of a significant European financial institution, could have a material adverse impact on our operations or financial performance.

In addition, there can be no assurance that the actions we have taken or may take in response to global economic conditions may be sufficient to counter any continuation or reoccurrence of the downturn or disruptions. A significant global economic downturn or disruptions in the financial markets would have a material adverse effect on our financial position, results of operations and cash flows.

Adverse changes in currency exchange rates could negatively affect our financial results.

The financial condition and results of operations of some of our operating entities are reported in various currencies and then translated into euros at the applicable exchange rate for inclusion in our consolidated financial statements. As a result, the appreciation of the euro against the currencies of our operating local entities may have a negative impact on reported revenues and operating profit, and the resulting accounts receivable, while depreciation of the euro against these currencies may generally have a positive effect on reported revenues and operating profit. We do not hedge translation of forecasted results or actual results.

In addition, while the majority of costs incurred are denominated in local currencies, a portion of the revenues are denominated in U.S. dollars. As a result, appreciation in the U.S. dollar may have a positive impact on earnings while depreciation of the U.S. dollar may have a negative impact on earnings. While we engage in significant hedging activity to attempt to mitigate this foreign transactions currency risk, this may not fully protect us from adverse effects due to currency fluctuations on our business, financial condition or results of operations.

A portion of our revenues is derived from our international operations, which exposes us to certain risks inherent in doing business globally.

We have operations primarily in the United States, Germany, France, Slovakia, Switzerland, the Czech Republic and China and primarily sell our products across Europe, Asia and North America. We also continue to explore opportunities to expand our international operations, particularly in other parts of Asia. Our operations generally are subject to financial, political, economic and business risks in connection with our global operations, including:

| • | changes in international governmental regulations, trade restrictions and laws, including those relating to taxes, employment and repatriation of earnings; |

| • | currency exchange rate fluctuations; |

| • | tariffs and other trade barriers; |

| • | the potential for nationalization of enterprises or government policies favoring local production; |

| • | renegotiation or nullification of existing agreements; |

| • | interest rate fluctuations; |

-6-

Table of Contents

| • | high rates of inflation; |

| • | currency restrictions and limitations on repatriation of profits; |

| • | differing protections for intellectual property and enforcement thereof; |

| • | divergent environmental laws and regulations; and |

| • | political, economic and social instability. |

The occurrence of any of these events could cause our costs to rise, limit growth opportunities or have a negative effect on our operations and our ability to plan for future periods. In certain emerging markets, the degree of these risks may be higher due to more volatile economic conditions, less developed and predictable legal and regulatory regimes and increased potential for various types of adverse governmental action.

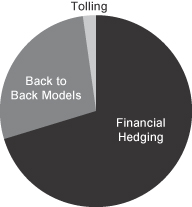

Our results of operations, cash flows and liquidity could be adversely affected if we are unable to execute on our hedging policy, if counterparties to our derivative instruments fail to honor their agreements or if we are unable to purchase derivative instruments.

We purchase and sell London Metal Exchange (the “LME”) and other forwards, futures and options contracts as part of our efforts to reduce our exposure to changes in currency exchange rates, aluminum prices and other raw materials prices. Our ability to realize the benefit of our hedging program is dependent upon many factors, including factors that are beyond our control. For example, our foreign exchange hedges are scheduled to mature on the expected payment date by the customer; therefore, if the customer fails to pay an invoice on time and does not warn us in advance, we may be unable to reschedule the maturity date of the foreign exchange hedge, which could result in an outflow of foreign currency that will not be offset until the customer makes the payment. We may realize a gain or a loss in unwinding such hedges. In addition, our metal-price hedging programs depend on our ability to match our monthly exposure to sold and purchased metal, which can be made difficult by seasonal variations in metal demand, unplanned changes in metal delivery dates by either us or by our customers and other disruptions to our inventories, including for maintenance.

We may also be exposed to losses if the counterparties to our derivative instruments fail to honor their agreements. Further, if major financial institutions continue to consolidate and are forced to operate under more restrictive capital constraints and regulations, there could be less liquidity in the derivative markets, which could have a negative effect on our ability to hedge and transact with creditworthy counterparties.

To the extent our hedging transactions fix prices or exchange rates and primary aluminum prices, energy costs or foreign exchange rates are below the fixed prices or rates established by our hedging transactions, our income and cash flows will be lower than they otherwise would have been. Similarly, if we do not adequately hedge for prices and premiums of our aluminum and other raw materials, our financial results may also be negatively impacted. Further, we do not apply hedge accounting to our forwards, futures or option contracts. As a result, unrealized gains and losses on our derivative financial instruments must be reported in our consolidated results of operations. The inclusion of such unrealized gains and losses in earnings may produce significant period to period earnings volatility that is not necessarily reflective of our underlying operating performance. In addition, in certain scenarios when market price movements result in a decline in value of our current derivatives position, our mark-to-market expense may exceed our credit line and counterparties may request the posting of cash collateral which, in turn, can be a significant demand on our liquidity.

At certain times, hedging instruments may simply be unavailable or not available on terms acceptable to us. In addition, recent legislation has been adopted to increase the regulatory oversight of over-the-counter derivatives markets and derivative transactions. Which companies and which transactions are subject to these regulations continues to evolve. If future regulations subject us to additional capital or margin requirements or other restrictions on our trading and commodity positions, they could have an adverse effect on our financial condition and results of operations.

-7-

Table of Contents

Aluminum may become less competitive with alternative materials, which could reduce our share of industry sales, lower our selling prices and reduce our sales volumes.

Our fabricated aluminum products compete with products made from other materials—such as steel, glass, plastics and composites—for various applications. Higher aluminum prices relative to substitute materials tend to make aluminum products less competitive with these alternative materials. Environmental and other regulations may also increase our costs and may be passed on to our customers, and may restrict the use of chemicals needed to produce aluminum products. These regulations may make our products less competitive as compared to materials that are subject to fewer regulations.

Customers in our end-markets, including the aerospace, automotive and can sectors, use and continue to evaluate the further use of alternative materials to aluminum in order to reduce the weight and increase the efficiency of their products. Although trends in “lightweighting” have generally increased rates of using aluminum as a substitution of other materials, the willingness of customers to accept substitutions for aluminum, or the ability of large customers to exert leverage in the marketplace to reduce the pricing for fabricated aluminum products, could adversely affect the demand for our products, and thus materially adversely affect our financial position, results of operations and cash flows.

We are dependent on a limited number of suppliers for a substantial portion of our aluminum supply and a failure to successfully renew, renegotiate or re-price our long-term agreements or related arrangements with our suppliers may adversely affect our results of operations, financial condition and cash flows.

We have supply arrangements with a limited number of suppliers for aluminum and other raw materials. Our top 10 suppliers accounted for approximately 50% of our total purchases at December 31, 2013. Increasing aluminum demand levels have caused regional supply constraints in the industry, and further increases in demand levels could exacerbate these issues. We maintain long-term contracts for a majority of our supply requirements, and for the remainder we depend on annual and spot purchases. There can be no assurance that we will be able to renew, or obtain replacements for, any of our long-term contracts or any related arrangements when they expire on terms that are as favorable as our existing agreements or at all. Additionally, if any of our key suppliers is unable to deliver sufficient quantities of this material on a timely basis, our production may be disrupted and we could be forced to purchase primary metal and other supplies from alternative sources, which may not be available in sufficient quantities or may only be available on terms that are less favorable to us. As a result, an interruption in key supplies required for our operations could have a material adverse effect on our ability to produce and deliver products on a timely or cost-efficient basis and therefore on our financial condition, results of operations and cash flows. In addition, a significant downturn in the business or financial condition of our significant suppliers exposes us to the risk of default by the supplier on our contractual agreements, and this risk is increased by weak and deteriorating economic conditions on a global, regional or industry sector level.

We also depend on scrap aluminum for our operations and acquire our scrap inventory from numerous sources. These suppliers generally are not bound by long-term contracts and have no obligation to sell scrap metal to us. In periods of low inventory prices, suppliers may elect to hold scrap until they are able to charge higher prices. In addition, the slowdown in industrial production and consumer consumption during the recent economic crisis reduced and may continue to reduce the supply of scrap metal available. If an adequate supply of scrap metal is not available to us, we would be unable to recycle metals at desired volumes and our results of operation, financial condition and cash flows could be materially adversely affected.

If we were to lose order volumes from any of our largest customers, our sales volumes, revenues and cash flows would be reduced.

Our business is exposed to risks related to customer concentration. Our ten largest customers accounted for approximately 45% of our consolidated revenues for the year ended December 31, 2013. A significant downturn in the business or financial condition of our significant customers exposes us to the risk of default on contractual

-8-

Table of Contents

agreements and trade receivables, and this risk is increased by weak and deteriorating economic conditions on a global, regional or industry sector level.

If we fail to successfully renew, renegotiate or re-price our long-term agreements or related arrangements with our largest customers, our results of operations, financial condition and cash flows could be materially adversely affected.

We have long-term contracts and related arrangements with a significant number of our customers, some of which are subject to renewal, renegotiation or re-pricing at periodic intervals or upon changes in competitive and regulatory supply conditions. Our failure to successfully renew, renegotiate or re-price such agreements at all or on terms as favorable as our existing contracts and arrangements, or a material deterioration in or termination of these customer relationships, could result in a reduction or loss in customer purchase volume or revenue, and if we are not successful in replacing business lost from such customers, our results of operations, financial condition and cash flows could be materially adversely affected.

In addition, our strategy of having dedicated facilities and arrangements with customers subjects us to the inherent risk of increased dependence on a single or a few customers with respect to these facilities. In such cases, the loss of such a customer, or the reduction of that customer’s business at one or more of our facilities, could negatively affect our financial condition and results of operations, and we may be unable to timely replace, or replace at all, lost order volumes and revenue.

We may not be able to compete successfully in the highly competitive markets in which we operate, and new competitors could emerge, which could negatively impact our share of industry sales, sales volumes and selling prices.

We are engaged in a highly competitive industry. We compete in the production and sale of rolled aluminum products with a number of other aluminum rolling mills, including large, single-purpose sheet mills, continuous casters and other multi-purpose mills, some of which are larger and have greater financial and technical resources than we do. Producers with a different cost basis may, in certain circumstances, have a competitive pricing advantage. Our competitors may be better able to withstand reductions in price or other adverse industry or economic conditions.

In addition, a current or new competitor may also add or build new capacity, which could diminish our profitability by decreasing the equilibrium prices in our markets. New competitors could emerge from within Europe or North America or globally, including from China, Russia and the Middle East. Emerging or transitioning markets in these regions with abundant natural resources, low-cost labor and energy, and lower environmental and other standards may pose a significant competitive threat to our business. Our competitive position may also be affected by exchange rate fluctuations that may make our products less competitive. Changes in regulation that have a disproportionately negative effect on us or our methods of production may also diminish our competitive advantage and industry position. In addition, technological innovation is important to our customers who require us to lead or keep pace with new innovations to address their needs. If we do not compete successfully, our share of industry sales, sales volumes and selling prices may be negatively impacted.

In addition, the aluminum industry has experienced consolidation over the past years and there may be further industry consolidation in the future. Although industry consolidation has not yet had a significant negative impact on our business, if we do not have sufficient market presence or are unable to differentiate ourselves from our competitors, we may not be able to compete successfully against other companies. If as a result of consolidation, our competitors are able to obtain more favorable terms from suppliers or otherwise take actions that could increase their competitive strengths, our competitive position and therefore our business, results of operations and financial condition may be materially adversely affected.

-9-

Table of Contents

The price volatility of energy costs may adversely affect our profitability.

Our operations use natural gas and electricity, which represent the third largest component of our cost of sales, after metal and labor costs. We purchase part of our natural gas and electricity on a spot-market basis. The volatility in costs of fuel, principally natural gas, and other utility services, principally electricity, used by our production facilities affect operating costs. Fuel and utility prices have been, and will continue to be, affected by factors outside our control, such as supply and demand for fuel and utility services in both local and regional markets as well as governmental regulation and imposition of further taxes on energy. Although we have secured some of our natural gas and electricity under fixed price commitments, future increases in fuel and utility prices, or disruptions in energy supply, may have an adverse effect on our financial position, results of operations and cash flows.

Regulations regarding carbon dioxide emissions, and unfavorable allocation of rights to emit carbon dioxide or other air emission related issues, could have a material adverse effect on our business, financial condition and results of operations.

Substantial quantities of greenhouse gases are released as a consequence of our operations. Compliance with existing, new or proposed regulations governing such emissions tend to become more stringent over time and could lead to a need for us to further reduce such greenhouse gas emissions, to purchase rights to emit from third parties, or to make other changes to our business, all of which could result in significant additional costs or could reduce demand for our products. In addition, we are a significant purchaser of energy. Existing, new and proposed regulations relating to the emission of carbon dioxide by our energy suppliers could result in materially increased energy costs for our operations, and we may be unable to pass along these increased energy costs to our customers, which could have a material adverse effect on our business, financial condition and results of operations.

Measures to reduce carbon dioxide and other greenhouse gas emissions that could directly or indirectly affect us or our suppliers are currently being developed or may be developed in the future. Many scientists, legislators and others attribute climate change to increased levels of greenhouse gases, including carbon dioxide, which has led to significant legislative and regulatory efforts to limit greenhouse gas emissions. Existing and possible new regulations regarding carbon dioxide and other greenhouse gas emissions, especially a revised European emissions trading system or a successor to the Kyoto Protocol under the United Nations Framework Convention on Climate Change, could have a material adverse effect on our business, financial condition and results of operations.

Our fabrication process is subject to regulations that may hinder our ability to manufacture our products. Some of the chemicals we use on our fabrication processes are subject to government regulation, such as REACH (“Registration, Evaluation, Authorisation, and Restriction of Chemicals substances”) in the EU. Under REACH, we are required to register some of our products with the European Chemicals Agency, and this process could cause significant delays or costs. If we fail to comply with these or similar laws and regulations, we may be required to make significant expenditures to reformulate the chemicals that we use in our products and materials or incur costs to register such chemicals to gain and/or regain compliance, and we may lose customers or revenue as a result. Additionally, we could be subject to significant fines or other civil and criminal penalties should we not achieve such compliance. To the extent that other nations in which we operate also require chemical registration, potential delays similar to those in Europe may delay our entry into these markets. Any failure to obtain or delay in obtaining regulatory approvals for chemical products used in our facilities could have a material adverse effect on our business, financial condition and results of operations.

We may not be able to successfully develop and implement new technology initiatives and other strategic investments in a timely manner.

We have invested in, and are involved with, a number of technology and process initiatives, including the development of new aluminum-lithium products. Being at the forefront of technological development is

-10-

Table of Contents

important to remain competitive. Several technical aspects of certain of these initiatives are still unproven and/or the eventual commercial outcomes and feasibility cannot be assessed with any certainty. Even if we are successful with these initiatives, we may not be able to bring them to market as planned before our competitors or at all, and the initiatives may end up costing more than expected. As a result, the costs and benefits from our investments in new technologies and the impact on our financial results may vary from present expectations.

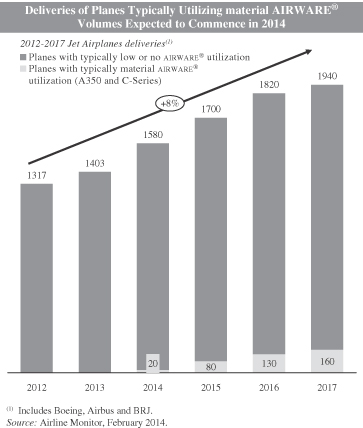

In addition, we have undertaken and may continue to undertake growth, streamlining and productivity initiatives to improve performance, including with respect to AIRWARE®, a lightweight specialty aluminum-lithium alloy, for our aerospace customers to address demand for lighter and more environmentally sound aircraft. We cannot assure you that these initiatives will be completed or that they will have their intended benefits, such as the realization of estimated cost savings from such activities. Capital investments in debottlenecking or other organic growth initiatives may not produce the returns we anticipate. Even if we are able to generate new efficiencies successfully in the short- to medium-term, we may not be able to continue to reduce cost and increase productivity over the long term.

Our business requires substantial capital investments that we may be unable to fulfill.

Our operations are capital intensive. Our total capital expenditures were €144 million for the year ended December 31, 2013 and €126 million and €97 million for the years ended December 31, 2012 and 2011, respectively. We may not generate sufficient operating cash flows and our external financing sources may not be available in an amount sufficient to enable us to make anticipated capital expenditures, service or refinance our indebtedness or fund other liquidity needs. If we are unable to make upgrades or purchase new plants and equipment, our financial condition and results of operations could be materially adversely affected by higher maintenance costs, lower sales volumes due to the impact of reduced product quality, and other competitive factors.

As part of our ongoing evaluation of our operations, we may undertake additional restructuring efforts in the future which could in some instances result in significant severance-related costs and other restructuring charges.

We recorded restructuring charges of €8 million for the year ended December 31, 2013, €25 million for the year ended December 31, 2012 and €20 million for the year ended December 31, 2011. Restructuring costs in 2013 were primarily related to corporate and other European sites restructuring operations. The 2012 costs were primarily in relation to an efficiency improvement program ongoing at our Sierre, Switzerland facility and corporate restructuring. Restructuring costs in 2011 were primarily in relation to corporate restructuring and full-time employee reductions throughout our operations. We may pursue additional restructuring activities in the future, which could result in significant severance-related costs, impairment charges, restructuring charges and related costs and expenses, including resulting labor disputes, which could materially adversely affect our profitability and cash flows.

A deterioration in our financial position or a downgrade of our ratings by a credit rating agency could increase our borrowing costs and our business relationships could be adversely affected.

A deterioration of our financial position or a downgrade of our credit ratings for any reason could increase our borrowing costs and have an adverse effect on our business relationships with customers, suppliers and hedging counterparties. As discussed above, we enter into various forms of hedging arrangements against currency, interest rate or metal price fluctuations and trade metal contracts on the LME. Financial strength and credit ratings are important to the availability and pricing of these hedging and trading activities. As a result, any downgrade of our credit ratings may make it more costly for us to engage in these activities, and changes to our level of indebtedness may make it more difficult or costly for us to engage in hedging and trading activities in the future.

-11-

Table of Contents

In addition, a downgrade could adversely affect our existing financing, limit access to the capital or credit markets, or otherwise adversely affect the availability of other new financing on favorable terms, if at all, result in more restrictive covenants in agreements governing the terms of any future indebtedness that we incur, increase our borrowing costs, or otherwise impair our business, financial condition and results of operations.

Our indebtedness could materially adversely affect our ability to invest in or fund our operations, limit our ability to react to changes in the economy or our industry or force us to take alternative measures.

Our indebtedness impacts our flexibility in operating our business and could have important consequences for our business and operations, including the following: (i) it may make us more vulnerable to downturns in our business or the economy; (ii) a substantial portion of our cash flows from operations will be dedicated to the repayment of our indebtedness and will not be available for other purposes; (iii) it may restrict us from making strategic acquisitions, introducing new technologies or exploiting business opportunities; and (iv) it may adversely affect the terms under which suppliers provide goods and services to us. As further described in “Item 10. Additional Information–C. Material Contracts,” on March 25, 2013 we refinanced our $200 million term loan (the “Original Term Loan”) (€151 million at the 2012 year-end exchange rate) by entering into a seven-year term loan in the aggregate principal amount of $360 million and €75 million (equivalent to €336 million in the aggregate at the 2013 year-end exchange rate) (the “New Term Loan” or “Term Loan”). By increasing our indebtedness as a result of the refinancing, we have made ourselves more susceptible to the risks discussed above.

If we are unable to meet our debt service obligations and pay our expenses, we may be forced to reduce or delay business activities and capital expenditures, sell assets, obtain additional debt or equity capital, restructure or refinance all or a portion of our debt before maturity or take other measures. Such measures may materially adversely affect our business. If these alternative measures are unsuccessful, we could default on our obligations, which could result in the acceleration of our outstanding debt obligations and could have a material adverse effect on our business, results of operations and financial condition.

The terms of our indebtedness contain covenants that restrict our current and future operations, and a failure by us to comply with those covenants may materially adversely affect our business, results of operations and financial condition.

Our indebtedness contains, and any future indebtedness we may incur would likely contain, a number of restrictive covenants that will impose significant operating and financial restrictions on our ability to, among other things: (i) incur or guarantee additional debt; (ii) pay dividends and make other restricted payments; (iii) create or incur certain liens; (iv) make certain loans, acquisitions or investments; (v) engage in sales of assets and subsidiary stock; (vi) enter into transactions with affiliates; (vii) transfer all or substantially all of our assets or enter into merger or consolidation transactions; and (viii) enter into sale and lease-back transactions. In addition, our Term Loan requires us to maintain a consolidated secured net leverage ratio of no more than 3.00 to 1.00. As a result of these covenants, we may be limited in the manner in which we conduct our business, and we may be unable to engage in favorable business activities or finance future operations or capital needs.

A failure to comply with our debt covenants could result in an event of default that, if not cured or waived, could have a material adverse effect on our business, results of operations and financial condition. If we default under our indebtedness, we may not be able to borrow additional amounts and our lenders could, in certain circumstances, elect to declare all outstanding borrowings, together with accrued and unpaid interest and fees, to be due and payable, or take other remedial actions. Our existing indebtedness also contains cross-default provisions, which means that if an event of default occurs under certain material indebtedness, such event of default will trigger an event of default under our other indebtedness. If our indebtedness were to be accelerated, we cannot assure you that our assets would be sufficient to repay such indebtedness in full and our lenders could foreclose on our pledged assets. See “Item 10. Additional Information–C. Material Contracts.”

-12-

Table of Contents

Our variable rate indebtedness subjects us to interest rate risk, which could cause our annual debt service obligations to increase significantly.

A portion of our indebtedness is subject to variable rates of interest and exposes us to interest rate risk. See “Item 10. Additional Information–C. Material Contracts.” If interest rates increase, our debt service obligations on the variable rate indebtedness would increase, resulting in a reduction of our net income, even though the amount borrowed would remain the same.

We could be required to make unexpected contributions to our defined benefit pension plans as a result of adverse changes in interest rates and the capital markets.

Most of our pension obligations relate to funded defined benefit pension plans for our employees in the United States and Switzerland, unfunded pension benefits in France and Germany, and lump sum indemnities payable to our employees in France and Germany upon retirement or termination. Our pension plan assets consist primarily of funds invested in listed stocks and bonds. Our estimates of liabilities and expenses for pensions and other post-retirement benefits incorporate a number of assumptions, including interest rates used to discount future benefits. Our results of operations, liquidity or shareholders’ equity in a particular period could be materially adversely affected by capital market returns that are less than their assumed long-term rate of return or a decline in the rate used to discount future benefits. If the assets of our pension plans do not achieve assumed investment returns for any period, such deficiency could result in one or more charges against our earnings for that period. In addition, changing economic conditions, poor pension investment returns or other factors may require us to make unexpected cash contributions to the pension plans in the future, preventing the use of such cash for other purposes.

A substantial percentage of our workforce is unionized or covered by collective bargaining agreements that may not be successfully renegotiated.

A significant number of our employees (approximately 80% of our total headcount) are represented by unions or equivalent bodies or are covered by collective bargaining or similar agreements that are subject to periodic renegotiation. Although we believe that we will be able to successfully negotiate new collective bargaining agreements when the current agreements expire, these negotiations may not prove successful, may result in a significant increase in the cost of labor, or may break down and result in the disruption or cessation of our operations.

We could experience labor disputes and work stoppages that could disrupt our business and have a negative impact on our financial condition and results of operations.

From time to time, we may experience labor disputes and work stoppages at our facilities. For example, we experienced work stoppages and labor disturbances at our Ravenswood facility in 2012 in conjunction with the renegotiation of the collective bargaining agreement. Additionally, we experienced work stoppages and labor disturbances at our Issoire and Neuf-Brisach facilities in November 2013 and resumed normal operations in early December 2013. Existing collective bargaining agreements, mainly in Europe, may not prevent a strike or work stoppage at our facilities in the future. Any such stoppages or disturbances may have a negative impact on our financial condition and results of operations by limiting plant production, sales volumes, profitability and operating costs.

The loss of certain members of our management team may have a material adverse effect on our operating results.

Our success will depend, in part, on the efforts of our senior management and other key employees. These individuals possess sales, marketing, engineering, technical, manufacturing, financial and administrative skills that are critical to the operation of our business. If we lose or suffer an extended interruption in the services of

-13-

Table of Contents

one or more of our senior officers or other key employees, our ability to operate and expand our business, improve our operations, develop new products, and, as a result, our financial condition and results of operations, may be negatively affected. Moreover, the pool of qualified individuals is highly competitive, and we may not be able to attract and retain qualified personnel to replace or succeed members of our senior management or other key employees, should the need arise.

In addition, in light of demographic trends in the labor markets where we operate, we expect that our factories will be confronted with high levels of natural attrition in the coming years due to retirements. Strategic workforce planning will be a challenge to ensure a controlled exit of skills and competencies and the timely acquisition of new talent and competencies, in line with changing technological and industrial needs.

We have a short history as a standalone company which may pose operational challenges to our management.

Our management team has faced and could continue to face operational and organizational challenges and costs related to establishing ourselves and operating as a standalone company, such as establishing various corporate functions, formulating policies, preparing standalone financial statements and integrating the management team. These challenges may divert their attention from running our core business or otherwise materially adversely affect our operating results.

If we do not adequately maintain and evolve our financial reporting and internal controls, we may be unable to accurately report our financial results or prevent fraud and may, as a result, become subject to sanctions by the Securities and Exchange Commission (the “SEC”). Establishing effective internal controls may also result in higher than anticipated operating expenses.

We will need to continue to improve existing, and implement new, financial reporting and management systems, procedures and controls to manage our business effectively and support our growth in the future, especially because we lack a history of operations as a standalone entity. Any delay in the implementation of, or disruption in the transition to, new or enhanced systems, procedures and controls, or the obsolescence of existing financial control systems, could harm our ability to accurately forecast sales demand and record and report financial and management information on a timely and accurate basis.

Moreover, to comply with our obligations as a public company under Section 404 of the Sarbanes-Oxley Act of 2002, we must enhance and maintain our internal controls. Effective internal controls are necessary for us to provide reliable financial reports and prevent fraud. We are in the process of refining and enhancing our internal controls to satisfy the requirements of Section 404, which requires annual management assessments of the effectiveness of our internal controls over financial reporting and a report by our independent registered public accounting firm on the effectiveness of our internal control over financial reporting, starting with our annual report for the year ending December 31, 2014. We are working to establish internal controls that will facilitate compliance with these requirements, and we may accordingly experience higher than anticipated operating expenses, as well as increased independent registered public accounting firm fees as we continue our compliance efforts.

If we fail to comply with the requirements of Section 404 in a timely manner, we might be subject to sanctions or investigations by regulatory authorities such as the SEC. If we do not adequately implement improvements to our disclosure controls and procedures or to our internal controls in a timely manner, our independent registered public accounting firm may not be able to certify as to the effectiveness of our internal control over financial reporting. This may subject us to adverse regulatory consequences or a loss of confidence in the reliability of our financial statements.

We could also suffer a loss of confidence in the reliability of our financial statements if our independent registered public accounting firm reports a material weakness in our internal controls, if we do not develop and

-14-

Table of Contents

maintain effective controls and procedures or if we are otherwise unable to deliver timely and reliable financial information. Any loss of confidence in the reliability of our financial statements or other negative reaction to our failure to develop timely or adequate disclosure controls and procedures or internal controls could result in a decline in the trading price of our ordinary shares. In addition, if we fail to remedy any material weakness, our financial statements may be inaccurate, we may face restricted access to the capital markets and the price of our ordinary shares may be materially adversely affected.

We may not be able to adequately protect proprietary rights to our technology.

Our success depends in part upon our proprietary technology and processes. We believe that our intellectual property has significant value and is important to the marketing of our products and maintaining our competitive advantage. Although we attempt to protect our intellectual property rights both in the United States and in foreign countries through a combination of patent, trademark, trade secret and copyright laws, as well as through confidentiality and nondisclosure agreements and other measures, these measures may not be adequate to fully protect our rights. For example, we have a growing presence in China, which historically has afforded less protection to intellectual property rights than the United States or the Netherlands. Our failure to obtain or maintain adequate protection of our intellectual property rights for any reason could have a material adverse effect on our business, results of operations and financial condition.

We have applied for patent protection relating to certain existing and proposed products and processes. While we generally apply for patents in those countries where we intend to make, have made, use or sell patented products, we may not accurately predict all of the countries where patent protection will ultimately be desirable. If we fail to timely file a patent application in any such country, we may be precluded from doing so at a later date. Furthermore, we cannot assure you that any of our patent applications will be approved. We also cannot assure you that the patents issuing as a result of our foreign patent applications will have the same scope of coverage as our United States patents. The patents we own could be challenged, invalidated or circumvented by others and may not be of sufficient scope or strength to provide us with any meaningful protection or commercial advantage. Further, we cannot assure you that competitors will not infringe our patents, or that we will have adequate resources to enforce our patents.

We also rely on unpatented proprietary technology. It is possible that others will independently develop the same or similar technology or otherwise obtain access to our unpatented technology. To protect our trade secrets and other proprietary information, we require employees, consultants, advisors and collaborators to enter into confidentiality agreements. We cannot assure you that these agreements will provide meaningful protection for our trade secrets, know-how or other proprietary information in the event of any unauthorized use, misappropriation or disclosure of such trade secrets, know-how or other proprietary information. If we are unable to maintain the proprietary nature of our technologies, we could be materially adversely affected.

We rely on our trademarks, trade names and brand names to distinguish our products from the products of our competitors, and have registered or applied to register many of these trademarks. We cannot assure you that our trademark applications will be approved. Third parties may also oppose our trademark applications, or otherwise challenge our use of the trademarks. In the event that our trademarks are successfully challenged, we could be forced to rebrand our products, which could result in loss of brand recognition, and could require us to devote resources to advertising and marketing new brands. Further, we cannot assure you that competitors will not infringe our trademarks, or that we will have adequate resources to enforce our trademarks.

We may institute or be named as a defendant in litigation regarding our intellectual property and such litigation may be costly and divert management’s attention and resources.

Any attempts to enforce our intellectual property rights, even if successful, could result in costly and prolonged litigation, divert management’s attention and resources, and materially adversely affect our results of operations and cash flows. The unauthorized use of our intellectual property may adversely affect our results of

-15-

Table of Contents

operations as our competitors would be able to utilize such property without having had to incur the costs of developing it, thus potentially reducing our relative profitability.

Furthermore, we may be subject to claims that we have infringed the intellectual property rights of another. Even if without merit, such claims could result in costly and prolonged litigation, cause us to cease making, licensing or using products or technologies that incorporate the challenged intellectual property, require us to redesign, reengineer or rebrand our products, if feasible, divert management’s attention and resources, and materially adversely affect our results of operations and cash flows. We may also be required to enter into licensing agreements in order to continue using technology that is important to our business, or we may be unable to obtain license agreements on acceptable terms, either of which could negatively affect our financial position, results of operations and cash flows.

Failure to protect our information systems against cyber-attacks or information security breaches could have a material adverse effect on our business.

Information security risks have generally increased in recent years because of the proliferation of new technologies and the increased sophistication and activities of perpetrators of cyber-attacks. A failure in or breach of our information systems as a result of cyber-attacks or information security breaches could disrupt our business, result in the disclosure or misuse of confidential or proprietary information, damage our reputation, increase our costs or cause losses. As cyber threats continue to evolve, we may be required to expend additional resources to continue to enhance our information security measures or to investigate and remediate any information security vulnerabilities.

Current liabilities under, as well as the cost of compliance with, environmental, health and safety laws could increase our operating costs and negatively affect our financial condition and results of operations.

Our operations are subject to federal, state and local laws and regulations in the jurisdictions where we do business, which govern, among other things, air emissions, wastewater discharges, the handling, storage and disposal of hazardous substances and wastes, the remediation of contaminated sites, and employee health and safety. At December 31, 2013, we had close-down and environmental restoration costs provisions of €48 million. Future environmental regulations could impose stricter compliance requirements on the industries in which we operate. Additional pollution control equipment, process changes, or other environmental control measures may be needed at some of our facilities to meet future requirements. If we are unable to comply with these laws and regulations, we could incur substantial costs, including fines and civil or criminal sanctions, or costs associated with upgrades to our facilities or changes in our manufacturing processes in order to achieve and maintain compliance.

Financial responsibility for contaminated property can be imposed on us where current operations have had an environmental impact. Such liability can include the cost of investigating and remediating contaminated soil or ground water, fines and penalties sought by environmental authorities, and damages arising out of personal injury, contaminated property and other toxic tort claims, as well as lost or impaired natural resources. Certain environmental laws impose strict, and in certain circumstances joint and several, liability for certain kinds of matters, such that a person can be held liable without regard to fault for all of the costs of a matter even though others were also involved or responsible.

We have accrued, and expect to accrue, costs relating to the above matters that are reasonably expected to be incurred based on available information. However, it is possible that actual costs may differ, perhaps significantly, from the amounts expected or accrued. Similarly, the timing of those expenditures may occur faster than anticipated. These differences could negatively affect our financial position, results of operations and cash flows.

-16-

Table of Contents

Other legal proceedings or investigations, or changes in applicable laws and regulations, could increase our operating costs and negatively affect our financial condition and results of operations.

We may from time-to-time be involved in, or be the subject of, disputes, proceedings and investigations with respect to a variety of matters, including matters related to personal injury, intellectual property, employees, taxes, contracts, anti-competitive or anti-corruption practices as well as other disputes and proceedings that arise in the ordinary course of business. It could be costly to address these claims or any investigations involving them, whether meritorious or not, and legal proceedings and investigations could divert management’s attention as well as operational resources, negatively affecting our financial position, results of operations and cash flows. Additionally, as with the environmental laws and regulations, other laws and regulations which govern our business are subject to change at any time. Compliance with changes to existing laws and regulations could have a material adverse effect on our financial position, results of operations and cash flows.

Product liability claims against us could result in significant costs and could materially adversely affect our reputation and our business.

If any of the products that we sell are defective or cause harm to any of our customers, we could be exposed to product liability lawsuits and/or warranty claims. If we were found liable under product liability claims or are obligated under warranty claims, we could be required to pay substantial monetary damages. Even if we successfully defend ourselves against these types of claims, we could still be forced to spend a substantial amount of money in litigation expenses, our management could be required to devote significant time and attention to defending against these claims, and our reputation could suffer, any of which could harm our business.

Our operations present significant risk of injury or death.

Because of the heavy industrial activities conducted at our facilities, there exists a risk of injury or death to our employees or other visitors, notwithstanding the safety precautions we take. Our operations are subject to regulation by national, state and local agencies responsible for employee health and safety, which has from time to time levied fines against us for certain isolated incidents. While such fines have not been material and we have in place policies to minimize such risks, we may nevertheless be unable to avoid material liabilities for any employee death or injury that may occur in the future, and any such incidents may materially adversely impact our reputation.

The insurance that we maintain may not fully cover all potential exposures.

We maintain property, casualty and workers’ compensation insurance, but such insurance does not cover all risks associated with the hazards of our business and is subject to limitations, including deductibles and maximum liabilities covered. We may incur losses beyond the limits, or outside the coverage, of our insurance policies, including liabilities for environmental compliance or remediation. In addition, from time to time, various types of insurance for companies in our industries have not been available on commercially acceptable terms or, in some cases, have not been available at all. In the future, we may not be able to obtain coverage at current levels, and our premiums may increase significantly on coverage that we maintain.

Increases in our effective tax rate and exposures to additional income tax liabilities due to audits could materially adversely affect our business.

We operate in multiple tax jurisdictions and pay tax on our income according to the tax laws of these jurisdictions. Various factors, some of which are beyond our control, determine our effective tax rate and/or the amount we are required to pay, including changes in or interpretations of tax laws in any given jurisdiction, our ability to use net operating loss and tax credit carry forwards and other tax attributes, changes in geographical allocation of income and expense, and our judgment about the realizability of deferred tax assets. Such changes

-17-

Table of Contents

to our effective tax rate could materially adversely affect our financial position, liquidity, results of operations and cash flows.