UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-Q

[X] QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the quarterly period ended March 31, 2018

Commission File Number: 333-189731

DIEGO PELLICER WORLDWIDE, INC.

(Name of registrant as specified in its charter)

| Delaware | 33-1223037 | |

| (State or other jurisdiction of | (I.R.S. Employer | |

| incorporation or organization) | Identification No.) |

9030 Seward Park Ave, S, #501, Seattle, WA 98118

(Address of principal executive offices) (Zip Code)

(516) 900-3799

(Registrant’s telephone number, including area code)

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes [X] No [ ]

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes [X] No [ ]

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| Large accelerated Filer | [ ] | Accelerated Filer | [ ] | |||

| Non-accelerated Filer | [ ] | Small Reporting Company | [X] | |||

| (Do not check if smaller reporting company) | ||||||

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes [ ] No [X]

As of May 07, 2018 there were 263,535,887 shares of common stock issued and outstanding.

TABLE OF CONTENTS

| Page | ||

| PART I – FINANCIAL INFORMATION | ||

| Item 1. | Financial Statements | 4 |

| Item 2. | Management’s Discussion and Analysis of Financial Condition and Results of Operations | 13 |

| Item 3. | Quantitative and Qualitative Disclosures About Market Risk | 19 |

| Item 4. | Controls and Procedures | 19 |

| PART II – OTHER INFORMATION | ||

| Item 1. | Legal Proceedings | 21 |

| Item 1A. | Risk Factors | 21 |

| Item 2. | Unregistered Sales of Equity Securities and Use of Proceeds | 21 |

| Item 3. | Defaults Upon Senior Securities | 21 |

| Item 4. | Mine Safety Disclosures | 21 |

| Item 5. | Other Information | 21 |

| Item 6. | Exhibits | 21 |

| 2 |

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

This Quarterly Report on Form 10-Q (this “Report”) contains “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933, as amended (the “Securities Act”), and Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”). Forward-looking statements discuss matters that are not historical facts. Because they discuss future events or conditions, forward-looking statements may include words such as “anticipate,” “believe,” “estimate,” “intend,” “could,” “should,” “would,” “may,” “seek,” “plan,” “might,” “will,” “expect,” “predict,” “project,” “forecast,” “potential,” “continue” negatives thereof or similar expressions. Forward-looking statements speak only as of the date they are made, are based on various underlying assumptions and current expectations about the future and are not guarantees. Such statements involve known and unknown risks, uncertainties and other factors that may cause our actual results, level of activity, performance or achievement to be materially different from the results of operations or plans expressed or implied by such forward-looking statements.

We cannot predict all of the risks and uncertainties. Accordingly, such information should not be regarded as representations that the results or conditions described in such statements or that our objectives and plans will be achieved and we do not assume any responsibility for the accuracy or completeness of any of these forward-looking statements. These forward-looking statements are found at various places throughout this Report and include information concerning possible or assumed future results of our operations, including statements about potential acquisition or merger targets; business strategies; future cash flows; financing plans; plans and objectives of management; any other statements regarding future acquisitions, future cash needs, future operations, business plans and future financial results, and any other statements that are not historical facts.

These forward-looking statements represent our intentions, plans, expectations, assumptions and beliefs about future events and are subject to risks, uncertainties and other factors. Many of those factors are outside of our control and could cause actual results to differ materially from the results expressed or implied by those forward-looking statements. In light of these risks, uncertainties and assumptions, the events described in the forward-looking statements might not occur or might occur to a different extent or at a different time than we have described. You are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date of this Report. All subsequent written and oral forward-looking statements concerning other matters addressed in this Report and attributable to us or any person acting on our behalf are expressly qualified in their entirety by the cautionary statements contained or referred to in this Report.

Except to the extent required by law, we undertake no obligation to update or revise any forward-looking statements, whether as a result of new information, future events, a change in events, conditions, circumstances or assumptions underlying such statements, or otherwise.

| 3 |

PART I – FINANCIAL INFORMATION

DIEGO PELLICER WORLDWIDE, INC.

CONDENSED CONSOLIDATED BALANCE SHEETS

(Unaudited)

| March 31, 2018 | December 31, 2017 | |||||||

| (Audited) | ||||||||

| Assets | ||||||||

| Current assets: | ||||||||

| Cash and cash equivalents | $ | 146,318 | $ | 158,702 | ||||

| Accounts receivable | 238,827 | 170,677 | ||||||

| Prepaid expenses | 7,241 | 21,621 | ||||||

| Inventory | 28,966 | 32,945 | ||||||

| Total current assets | 421,352 | 383,945 | ||||||

| Property and equipment, net | 510,737 | 409,128 | ||||||

| Investments, at cost | - | - | ||||||

| Security deposits | 320,000 | 320,000 | ||||||

| Total assets | $ | 1,252,089 | $ | 1,113,073 | ||||

| Liabilities and deficiency in stockholders’ equity | ||||||||

| Current liabilities: | ||||||||

| Accounts payable | $ | 444,942 | $ | 626,258 | ||||

| Accrued payable - related party | 418,863 | 449,064 | ||||||

| Accrued expenses | 375,769 | 207,558 | ||||||

| Notes payable - related party | 140,958 | 307,312 | ||||||

| Notes payable | 133,403 | 133,403 | ||||||

| Convertible notes, net of discount and costs | 410,088 | 468,116 | ||||||

| Deferred rent | 245,925 | 251,878 | ||||||

| Deferred revenue | 53,000 | 53,000 | ||||||

| Derivative liabilities | 1,103,373 | 4,106,521 | ||||||

| Warrant liabilities | 72,754 | 192,350 | ||||||

| Total current liabilities | 3,399,075 | 6,795,460 | ||||||

| Deferred revenue | 248,500 | 262,000 | ||||||

| Total liabilities | 3,647,575 | 7,057,460 | ||||||

| Deficiency in stockholders’ equity: | ||||||||

| Preferred stock, Series A and B, par value $.0001 per share; 5,000,000 shares authorized, none issued and outstanding | - | - | ||||||

| Common stock, par value $.000001 per share; 495,000,000 shares authorized, 229,650,261 and 142,576,974 shares issued, respectively | 230 | 143 | ||||||

| Additional paid-in capital | 36,927,394 | 34,422,338 | ||||||

| Stock to be issued | 1,580,330 | 2,397,218 | ||||||

| Accumulated deficit | (40,903,440 | ) | (42,764,086 | ) | ||||

| Total deficiency in stockholders’ equity | (2,395,486 | ) | (5,944,387 | ) | ||||

| Total liabilities and deficiency in stockholders’ equity | $ | 1,252,089 | $ | 1,113,073 | ||||

See Accompanying Notes to Unaudited Condensed Consolidated Financial Statements.

| 4 |

DIEGO PELLICER WORLDWIDE, INC.

CONDENSED CONSOLIDATED STATEMENTS OF OPERATIONS

(Unaudited)

| Three Months Ended | Three Months Ended | |||||||

| March 31, 2018 | March 31, 2017 | |||||||

| REVENUES | ||||||||

| Net Rental Revenue | $ | 383,298 | $ | 309,962 | ||||

| Rental Expense | (269,087 | ) | (347,203 | ) | ||||

| Gross Profit | 114,211 | (37,241 | ) | |||||

| Operating expenses: | ||||||||

| General and administrative expenses | 644,773 | 892,995 | ||||||

| Selling Expense | 6,269 | 12 | ||||||

| Depreciation Expense | 127,257 | 130,790 | ||||||

| Loss from Operations | (664,088 | ) | (1,061,038 | ) | ||||

| Other Income (Expense) | ||||||||

| Licensing Revenue | 13,500 | 13,500 | ||||||

| Other Income (Expense) | 2,691 | 3,624 | ||||||

| Interest Expense | (710,474 | ) | (288,236 | ) | ||||

| Impairment Loss | - | (27,500 | ) | |||||

| Extinguishment of Debt | 42,167 | - | ||||||

| Change in Derivative Liabilities | 3,057,254 | 50,839 | ||||||

| Change in Value of Warrants | 119,596 | - | ||||||

| Total Other Income (Loss) | 2,524,734 | (247,773 | ) | |||||

| Provision for taxes | ||||||||

| NET INCOME (LOSS) | $ | 1,860,646 | $ | (1,308,811 | ) | |||

| Income (loss) per share | ||||||||

| Basic | $ | 0.01 | $ | (0.03 | ) | |||

| Diluted | $ | (0.00 | ) | $ | (0.03 | ) | ||

| Weighted average common shares outstanding | ||||||||

| Basic | 164,940,612 | 50,868,784 | ||||||

| Diluted | 260,016,862 | 50,868,784 | ||||||

See Accompanying Notes to Unaudited Condensed Consolidated Financial Statements.

| 5 |

DIEGO PELLICER WORLDWIDE, INC.

CONDENSED CONSOLIDATED STATEMENT OF CASH FLOW

(Unaudited)

| Three Months Ended | Three Months Ended | |||||||

| March 31, 2018 | March 31, 2017 | |||||||

| Cash flows from operating activities: | ||||||||

| Net income (loss) | $ | 1,860,646 | $ | (1,308,810 | ) | |||

| Adjustments to reconcile net income (loss) to net cash used by operating activities: | ||||||||

| Depreciation | 127,257 | 130,790 | ||||||

| Impairment | - | 54,565 | ||||||

| Change in fair value of derivative liability | (3,057,254 | ) | (50,839 | ) | ||||

| Change in value of warrants | (119,596 | ) | - | |||||

| Amortization of discount | 643,966 | 53,678 | ||||||

| Amortization of debt costs | 19,382 | - | ||||||

| Extinguishment of debt | (42,168 | ) | - | |||||

| Stock based compensation | 423,124 | 1,057,175 | ||||||

| Changes in operating assets and liabilities: | ||||||||

| Accounts receivable | (68,150 | ) | (42,457 | ) | ||||

| Inventory | 3,979 | 9,079 | ||||||

| Prepaid expenses | 14,380 | (2,298 | ) | |||||

| Other assets | - | (555,657 | ) | |||||

| Accounts payable | (134,062 | ) | (235,169 | ) | ||||

| Accrued liability - related parties | 88,019 | 167,312 | ||||||

| Accrued expenses | (15,826 | ) | 34,341 | |||||

| Change in derivative liability, net of discount | - | 186,086 | ||||||

| Deferred rent | 5,953 | 153,984 | ||||||

| Deferred revenue | (13,500 | ) | (13,500 | ) | ||||

| Cash used by operating activities | (275,756 | ) | (361,720 | ) | ||||

| Cash flows from investing activities: | ||||||||

| Purchase of property and equipment | - | (135,000 | ) | |||||

| Cash used by investing activities | - | (135,000 | ) | |||||

| Cash flows from financing activities: | ||||||||

| Stock issued for convertible notes | - | 50,000 | ||||||

| Debt costs | (16,000 | ) | - | |||||

| Proceeds from convertible notes payable | 258,500 | 565,000 | ||||||

| Repayments of notes payable | - | (50,000 | ) | |||||

| Proceeds from sale of common stock | 20,872 | - | ||||||

| Cash provided by financing activities | 263,372 | 565,000 | ||||||

| Net increase (decrease) in cash | (12,384 | ) | 68,280 | |||||

| Cash, beginning of period | 158,702 | 51,333 | ||||||

| Cash, end of period | $ | 146,318 | $ | 119,613 | ||||

| Cash paid for interest | $ | - | $ | - | ||||

| Cash paid for taxes | $ | - | $ | - | ||||

| Supplemental schedule of noncash financial activities: | ||||||||

| Stock issued for debt settlement | $ | - | $ | 50,000 | ||||

| Notes converted to stock | $ | 568,268 | $ | - | ||||

| Accrued interest converted to stock | $ | 44,829 | $ | - | ||||

| Value of common stock to be issued for conversion of notes and accrued interest | $ | 1,078,786 | $ | - | ||||

| Value of derivative liability extinguished upon conversion of notes and accrued interest | $ | 547,476 | $ | - | ||||

| Accounts payable and accrued expenses paid with common stock | $ | 165,474 | $ | - | ||||

| Leasehold improvements paid by tenant | $ | 228,866 | $ | - | ||||

See Accompanying Notes to Unaudited Condensed Consolidated Financial Statements.

| 6 |

Diego Pellicer Worldwide, Inc.

March 31, 2018 and 2017

Notes to the Consolidated Financial Statements

Note 1 – Organization and Operations

History

On March 13, 2015 (the “closing date”), Diego Pellicer Worldwide, Inc. (f/k/a Type 1 Media, Inc.) (the “Company”) closed on a merger and share exchange agreement (the “Merger Agreement”) by and among (i) the Company, and (ii) Diego Pellicer World-wide 1, Inc., a Delaware corporation, (“Diego”), and (iii) Jonathan White, the majority shareholder of the Company (the “Majority Shareholder”). Pursuant to the terms of the Merger Agreement, Diego was merged with and into the Company, with the Company to continue as the surviving corporation (the “Surviving Corporation”) in the Merger, and the Company succeeding to and assuming all the rights, assets, liabilities, debts, and obligations of Diego (the “Merger”).

Prior to the Merger, 62,700,000 shares of Type 1 Media, Inc. were issued and outstanding. The principal owners of the Company agreed to transfer their 55,000,000 issued and outstanding shares to a third party in consideration for $169,000 and cancellation of their 55,000,000 shares. The remaining issued and outstanding shares are still available for trading in the marketplace. At the time of the Merger, Type 1 Media, Inc. had no assets or liabilities. Accordingly, the business conducted by Type 1 prior to the Merger is not being operated by the combined entity post-Merger.

At the closing of the Merger, Diego common stock issued and outstanding immediately prior to the closing of the Merger was exchanged for the right to receive 1 share of the surviving legal entity. An aggregate of 21,632,252 common shares of the surviving entity were issued to the holders of Diego in exchange for their common shares, representing approximately 74% of the combined entity.

The Merger has been accounted for as a reverse merger and recapitalization in which Diego is treated as the accounting acquirer and Diego Pellicer Worldwide, Inc. (f/k/a Type 1 Media, Inc.) is the surviving legal entity.

Business Operations

The Company leases real estate to licensed marijuana operators providing complete turnkey growing space, processing space, recreational and medical retail sales space and related facilities to licensed marijuana growers, processors, dispensary and recreational store operators. Additionally, the Company plans to explore ancillary opportunities in the regulated marijuana industry as well as offering for wholesale distribution branded non-marijuana clothing and accessories.

Until Federal law allows, the Company will not grow, harvest, process, distribute or sell marijuana or any other substances that violate the laws of the United States of America or any other country.

Note 2 – Significant and Critical Accounting Policies and Practices

The management of the Company is responsible for the selection and use of appropriate accounting policies and the appropriateness of accounting policies and their application. Critical accounting policies and practices are those that are both most important to the portrayal of the Company’s financial condition and results and require management’s most difficult, subjective, or complex judgments, often because of the need to make estimates about the effects of matters that are inherently uncertain. The Company’s significant and critical accounting policies and practices are disclosed below as required by generally accepted accounting principles.

Basis of Presentation

The accompanying condensed consolidated financial statements of Diego Pellicer Worldwide, Inc. were prepared in accordance with the instructions to Form 10-Q and, therefore, do not include all disclosures required for financial statements prepared in conformity with U.S. GAAP.

This Form 10-Q relates to the three months ended March 31, 2018 (the “Current Quarter”) and the three months March 31, 2017 (the “Prior Quarter”). The Company’s annual report on Form 10-K for the year ended December 31, 2017 (“2017 Form 10-K”) includes certain definitions and a summary of significant accounting policies and should be read in conjunction with this Form 10-Q. All material adjustments which, in the opinion of management, are necessary for a fair statement of the results for the interim periods have been reflected. The results for the current quarter are not necessarily indicative of the results to be expected for the full year.

Principles of Consolidation

The financial statements include the accounts of Diego Pellicer Worldwide, Inc., and its wholly-owned subsidiary Diego Pellicer World-wide 1, Inc. Intercompany balances and transactions have been eliminated in consolidation.

Reclassifications

Certain prior year amounts were reclassified to conform to the manner of presentation in the current period. These reclassifications had no effect on the Company’s balance sheet, net loss or stockholders’ equity.

Use of Estimates

The preparation of the financial statements in conformity with GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the dates of the financial statements and the reported amounts of revenue and expenses during the reporting periods. Actual results could differ from those estimates. These estimates and assumptions include valuing equity securities and derivative financial instruments issued in financing transactions and share based payment arrangements, determining the fair value of the warrants received for a licensing agreement, the collectability of accounts receivable and deferred taxes and related valuation allowances.

Certain estimates, including evaluating the collectability of accounts receivable, could be affected by external conditions, including those unique to our industry, and general economic conditions. It is possible that these external factors could influence our estimates that could cause actual results to differ from our estimates. The Company intends to re-evaluate all its accounting estimates at least quarterly based on these conditions and record adjustments when necessary.

| 7 |

Fair Value Measurements

The Company evaluates its financial instruments to determine if such instruments are derivatives or contain features that qualify as embedded derivatives. For derivative financial instruments that are accounted for as liabilities, the derivative instrument is initially recorded at its fair value and is then re-valued at each reporting date, with changes in the fair value reported in the condensed consolidated statements of operations. The classification of derivative instruments, including whether such instruments should be recorded as liabilities or as equity, is evaluated at the end of each reporting period. Derivative instrument liabilities are classified in the balance sheet as current or non-current based on whether net-cash settlement of the derivative instrument could be required within 12 months of the balance sheet date.

Fair Value of Financial Instruments

As required by the Fair Value Measurements and Disclosures Topic of the FASB ASC, fair value is measured based on a three-tier fair value hierarchy, which prioritizes the inputs used in measuring fair value as follows:

Level 1: Unadjusted quoted prices in active markets that are accessible at the measurement date for identical, unrestricted assets or liabilities;

Level 2: Quoted prices in markets that are not active, or inputs that are observable, either directly or indirectly, for substantially the full term of the asset or liability; and

Level 3: Prices or valuation techniques that require inputs that are both significant to the fair value measurement and unobservable (supported by little or no market activity).

Fair value estimates discussed herein are based upon certain market assumptions and pertinent information available to management as of March 31, 2018 and December 31, 2017. The respective carrying value of certain on-balance-sheet financial instruments approximated their fair values. These financial instruments include cash, prepaid expenses and accounts payable. Fair values were assumed to approximate carrying values for cash and payables because they are short term in nature and their carrying amounts approximate fair values or they are payable on demand.

Cash

The Company maintains cash balances at various financial institutions. Accounts at each institution are insured by the Federal Deposit Insurance Corporation, and the National Credit Union Share Insurance Fund, up to $250,000. The Company’s accounts at these institutions may, at times, exceed the federal insured limits. The Company has not experienced any losses in such accounts.

Revenue recognition

The Company recognizes revenue from rent, tenant reimbursements, and other revenue sources once all the following criteria are met in accordance with SEC Staff Accounting Bulletin 104, Revenue Recognition : (a) the agreement has been fully executed and delivered; (b) services have been rendered; (c) the amount is fixed or determinable; and (d) the collectability of the amount is reasonably assured. Thus, during the initial term of the lease, management has a policy of partial rent forbearance when the tenant first opens the facility to assure that the tenant has the opportunity for success.

When the collectability is reasonably assured, in accordance with ASC Topic 840 “Leases” as amended and interpreted, minimum annual rental revenue is recognized for rental revenues on a straight-line basis over the term of the related lease.

When management concludes that the Company is the owner of tenant improvements, management records the cost to construct the tenant improvements as a capital asset. In addition, management records the cost of certain tenant improvements paid for or reimbursed by tenants as capital assets when management concludes that the Company is the owner of such tenant improvements. For these tenant improvements, management records the amount funded or reimbursed by tenants as deferred revenue, which is amortized as additional rental income over the term of the related lease. When management concludes that the tenant is the owner of tenant improvements for accounting purposes, management records the Company’s contribution towards those improvements as a lease incentive, which is amortized as a reduction to rental revenue on a straight-line basis over the term of the lease.

The Company records rents due from the tenants on a current basis. The Company has deferred collection of such rents until the tenants receive the proper governmental licenses to begin operation. Prior to 2017, management had reserved these deferred amounts due to the unlikelihood of collection.

Leases as Lessor

The Company currently leases properties to licensed cannabis operators for locations that meet the regulatory criteria applicable by the respective regulatory jurisdiction for the sale, production, and development of cannabis products. The Company evaluates the lease to determine its appropriate classification as an operating or capital lease for financial reporting purposes. The Company leases are currently all classified as operating leases.

Minimum base rent is recorded on a straight-line basis over the lease term after an initial period during which the tenant is establishing the business and during which the Company may forbear some or all of the rent. The Company is more likely than not to forbear some or all of the rental income which it considers uncollectable during the tenant’s initial ramp-up period (see Revenue Recognition above). The tenant is still liable for the full rent, although the collectability may be unlikely and the Company may not expect to collect it.

Leases as Lessee

The Company recognizes rent expense on a straight-line basis over the non-cancelable lease term and certain option renewal periods where failure to exercise such options would result in an economic penalty in such amount that renewal appears, at the inception of the lease, to be reasonably assured. Deferred rent is presented on current liabilities section on the consolidated balance sheets.

| 8 |

Income Taxes

Income taxes are provided for using the liability method of accounting in accordance with the Income Taxes Topic of the FASB ASC. Deferred tax assets and liabilities are determined based on differences between the financial reporting and tax basis of assets and liabilities and are measured using the enacted tax rates and laws that will be in effect when the differences are expected to reverse. A valuation allowance is established when necessary to reduce deferred tax assets to the amount expected to be realized and when, in the opinion of management, it is more likely than not that some portion or all of the deferred tax assets will not be realized. The computation of limitations relating to the amount of such tax assets, and the determination of appropriate valuation allowances relating to the realizing of such assets, are inherently complex and require the exercise of judgment. As additional information becomes available, the Company continually assesses the carrying value of their net deferred tax assets.

Common Stock Purchase Warrants and Other Derivative Financial Instruments

The Company classifies as equity any contracts that require physical settlement or net-share settlement or provide us a choice of net cash settlement or settlement in our own shares (physical settlement or net-share settlement) provided that such contracts are indexed to our own stock as defined in ASC Topic 815-40 “Contracts in Entity’s Own Equity.” The Company classifies as assets or liabilities any contracts that require net-cash settlement including a requirement to net cash settle the contract if an event occurs and if that event is outside our control or give the counterparty a choice of net-cash settlement or settlement in shares. The Company assesses classification of its common stock purchase warrants and other free-standing derivatives at each reporting date to determine whether a change in classification between assets and liabilities is required.

Stock-Based Compensation

The Company recognizes compensation expense for stock-based compensation in accordance with ASC Topic 718. The Company calculates the fair value of the award on the date of grant using the Black-Scholes method for stock options and the quoted price of our common stock for unrestricted shares; the expense is recognized over the service period for awards expected to vest. The estimation of stock-based awards that will ultimately vest requires judgment, and to the extent actual results or updated estimates differ from original estimates, such amounts are recorded as a cumulative adjustment in the period estimates are revised. The Company considers many factors when estimating expected forfeitures, including types of awards, employee class, and historical experience.

Income (loss) per common share

The Company utilizes ASC 260, “Earnings Per Share” for calculating the basic and diluted loss per share. In accordance with ASC 260, the basic and diluted loss per share is computed by dividing net loss available to common stockholders by the weighted average number of common shares outstanding. Diluted net loss per share is computed similar to basic loss per share except that the denominator is adjusted for the potential dilution that could occur if stock options, warrants, and other convertible securities were exercised or converted into common stock. Potentially dilutive securities are not included in the calculation of the diluted loss per share if their effect would be anti-dilutive. The Company has 106,252,743 and 12,934,555 common stock equivalents at March 31, 2018 and 2017, respectively. For the three month period ended March 31, 2017 the 12,934,555 potential shares were excluded from the shares used to calculate diluted earnings per share as their inclusion would reduce net loss per share.

Diluted earnings per share for the three months ended March 31, 2018 have been calculated as follows:

| Net income | $ | 1,860,646 | ||

| Income attributable to convertible instruments | (3,219,017 | ) | ||

| Expense attributable to convertible instruments | 455,642 | |||

| Diluted loss | $ | (902,729 | ) | |

| Basic shares outstanding | 164,940,612 | |||

| Shares to be issued | 41,096,070 | |||

| Convertible instruments | 53,980,180 | |||

| Diluted shares outstanding | 260,016,862 | |||

| Diluted EPS | $ | (0.00 | ) |

Legal and regulatory environment

The cannabis industry is subject to numerous laws and regulations of federal, state and local governments. These laws and regulations include, but are not limited to, matters such as licensure, accreditation, and different taxation between federal and state. Federal government activity may increase in the future with respect to companies involved in the cannabis industry concerning possible violations of federal statutes and regulations.

Management believes that the Company is in compliance with local, state and federal regulations, While no regulatory inquiries have been made, compliance with such laws and regulations can be subject to future government review and interpretation, as well as regulatory actions unknown or unasserted at this time.

Recent accounting pronouncements.

On December 22, 2017 the SEC staff issued Staff Accounting Bulletin 118 (SAB 118), which provides guidance on accounting for the tax effects of the Tax Cuts and Jobs Act (the TCJA). SAB 118 provides a measurement period that should not extend beyond one year from the enactment date for companies to complete the accounting under ASC 740. In accordance with SAB 118, a company must reflect the income tax effects of those aspects of the TCJA for which the accounting under ASC 740 is complete. To the extent that a company’s accounting for certain income tax effects of the TCJA is incomplete but for which they are able to determine a reasonable estimate, it must record a provisional amount in the financial statements. Provisional treatment is proper in light of anticipated additional guidance from various taxing authorities, the SEC, the FASB, and even the Joint Committee on Taxation. If a company cannot determine a provisional amount to be included in the financial statements, it should continue to apply ASC 740 on the basis of the provisions of the tax laws that were in effect immediately before the enactment of the TCJA. The Company has applied this guidance to its financial statements.

In May 2014, the FASB issued ASU No. 2014-09, Revenue from Contracts with Customers for guidance to clarify the principles for recognizing revenue and to develop a common revenue standard for GAAP and International Financial Reporting Standards. The standard outlines a single comprehensive model for entities to use in accounting for revenue arising from contracts with customers. Lease contracts will be excluded from this revenue recognition criteria. For other transactions the standard requires that an entity recognizes revenue to depict the transfer of promised goods or services to customers in an amount that reflects the consideration to which the company expects to be entitled in exchange for those goods or services. The Company revenues are principally from leasing. Therefore, this ASU has minimal applicability to the Company.

In February 2016, the Financial Accounting Standards Board (FASB) issued guidance that requires a lessee to recognize assets and liabilities arising from leases on the balance sheet. Previous GAAP did not require lease assets and liabilities to be recognized for most leases. Additionally, companies are permitted to make an accounting policy election not to recognize lease assets and liabilities for leases with a term of 12 months or less. For both finance leases and operating leases, the lease liability should be initially measured at the present value of the remaining contractual lease payments. The recognition, measurement and presentation of expenses and cash flows arising from a lease by a lessee will not significantly change under this new guidance. This new guidance is effective for the company as of the first quarter of fiscal year 2020. The Company is evaluating the effect that this ASU will have on its financial statements and related disclosures.

In August 2016, the FASB issued ASU No. 2016-15, Classification of Certain Cash Receipts and Cash Payments. ASU 2016-15 clarifies the presentation and classification of certain cash receipts and cash payments in the statement of cash flows. This ASU is effective for public business entities for fiscal years, and interim periods within those years, beginning after December 15, 2017. The Company did comply with this for the quarter ended March 31, 2018. The adoption of ASU 2016-15 did not have a material impact on the financial statements and related disclosures.

| 9 |

In April 2016 the FASB issued ASU 2016-10, Revenue from Contracts with Customers (Topic 606). The core principle of Topic 606 is that an entity should recognize revenue to depict the transfer of promised goods or services to customers in an amount that reflects the consideration to which the entity expects to be entitled in exchange for those goods or services This ASU is effective for public business entities for fiscal years, and interim periods within those years, beginning after January 1. 2018. The adoption of ASU 2016-10 did not have a material impact on the financial statements and related disclosures.

The Company believes that other recently issued accounting pronouncements and other authoritative guidance for which the effective date is in the future either will not have an impact on its accounting or reporting or that such impact will not be material to its financial position, results of operations and cash flows when implemented.

Note 3 – Going Concern

The accompanying financial statements have been prepared assuming that the Company will continue as a going concern. The Company has incurred losses since inception, its current liabilities exceed its current assets by $2,977,723, and has an accumulated deficit of $40,903,440 at March 31, 2018. These factors, among others raise substantial doubt about its ability to continue as a going concern. The financial statements do not include any adjustments that might result from the outcome of this uncertainty.

The Company believes that it has sufficient cash on hand and cash generated by real estate leases to sustain operations provided that management and board members continue to agree to be paid company stock in exchange for accrued compensation. Through March 31, 2018, management and board members have accepted stock for accrued compensation at the same discount that has been extended to the convertible noteholders of fifty percent. There are other future noncash charges in connection with financing such as a change in derivative liability that will affect income but have no effect on cash flow.

Although the Company has been successful raising additional capital, there is no assurance that the company will sell additional shares of stock or borrow additional funds. The Company’s inability to raise additional cash could have a material adverse effect on its financial position, results of operations, and its ability to continue in existence. These financial statements do not include any adjustments that might result from the outcome of this uncertainty. Management believes that the Company’s future success is dependent upon its ability to achieve profitable operations, generate cash from operating activities and obtain additional financing. There is no assurance that the Company will be able to generate sufficient cash from operations, sell additional shares of stock or borrow additional funds. However, cash generated from lease revenues is currently exceeding lease costs, but is insufficient to cover operating expenses.

Note 4 – Property and Equipment

As of March 31, 2018 and December 31, 2017, fixed assets and the estimated lives used in the computation of depreciation are as follows:

| Estimated | ||||||||||

| Useful Lives | March 31, 2018 | December 31, 2017 | ||||||||

| Leasehold improvements | 10 years | 1,082,279 | 853,413 | |||||||

| Less: Accumulated depreciation and amortization | (571,542 | ) | (444,285 | ) | ||||||

| Property and equipment, net | $ | 510,737 | $ | 409,128 | ||||||

Note 5 – Related Party

As of March 31, 2018 and December 31, 2017, the Company has accrued fees to related parties in the amount of $418,863 and $449,064, respectively. For the three months ended March 31, 2018 and 2017, total cash-based compensation to related parties was $188,756 and $143,996, respectively. For the three months ended March 31, 2018 and 2017, total share-based compensation to related parties was $377,964 and $509,518, respectively. These amounts are included in general and administrative expenses in the accompanying financial statements.

During the three months ended March 31, 2018, we issued 13,381,637 shares of common stock for payment of a related party note in the amount of $166,354, plus accrued interest of $21,658.

At March 31, 2018, the Company owed Mr. Throgmartin $140,958 pursuant to a promissory note dated August 12, 2016. This note accrued interest at the rate of 8% per annum and payable upon the earlier date of (i) the second anniversary date of the promissory notes, (ii) the date all of the current investor notes, in the outstanding aggregate principal and accrued interest amount of approximately $1,480,000 at June 30, 2016, have been paid in full and the Company has achieved gross revenues of at least $3,000,000 over any consecutive 12-month period.

The balance of related party notes was $140,958 and $307,312 at March 31, 2018 and December 31, 2017, respectively.

Note 6 – Notes Payable

On August 31, 2015, the Company issued a note in total amount of $126,000 with third parties for use as operating capital. The note was amended to include accrued interest on October 31, 2016 and extended the maturity date to October 31, 2018. As of March 31, 2018 and December 31, 2017 the outstanding principal balance of the note was $133,403.

Note 7 – Convertible Notes Payable

The Company has issued several convertible notes which are outstanding. The note holders shall have the right to convert principal and accrued interest outstanding into shares of common stock at a discounted price to the market price of our common stock. The conversion feature was recognized as an embedded derivative and was valued using a Black Scholes model that resulted in a derivative liability of $1,103,373 at March 31, 2018. In connection with the issuance of certain of these notes, the Company also issued warrants to purchase its common stock. The Company allocated the proceeds of the notes and warrants based on the relative fair value at inception.

Several convertible note holders elected to convert their notes to stock during the three months ended March 31, 2018. The table below provides a reconciliation of the beginning and ending balances for the liabilities measured using fair significant unobservable inputs (Level 3) for the three months ended March 31, 2018:

| 10 |

| Convertible notes | Discount | Convertible Note Net of Discount | Derivative Liabilities | |||||||||||||

| Balance, December 31, 2017 | 971,455 | 503,339 | 468,116 | 4,106,521 | ||||||||||||

| Issuance of convertible notes | 331,459 | 274,500 | 56,959 | 601,582 | ||||||||||||

| Conversion of convertible notes | (401,914 | ) | (39,619 | ) | (362,295 | ) | (547,476 | ) | ||||||||

| Change in fair value of derivatives | — | — | — | (3,057,254 | ) | |||||||||||

| Amortization | — | (247,308 | ) | 247,308 | — | |||||||||||

| Balance March 31, 2018 | $ | 901,000 | $ | 490,912 | $ | 410,088 | $ | 1,103,373 | ||||||||

During the three months ended March 31, 2018, $401,914 of notes and $23,171 of accrued interest was converted into 25,615,827 shares of common stock. A gain on extinguishment of debt of $42,167 has been recorded related to these conversions.

The following assumptions were used in calculations of the Black Scholes model for the periods ended March 31, 2018 and December 31, 2017.

| March 31, 2018 | December 31, 2017 | |||||||

| Risk-free interest rates | 1.28-1.76 | % | 1.28-1.76 | % | ||||

| Expected life | 0.05-1 year | 0.02-1.23 year | ||||||

| Expected dividends | 0 | % | 0 | % | ||||

| Expected volatility | 70-247 | % | 211-354 | |||||

| Diego Pellicer Worldwide, Inc. Common Stock fair value | $ | 0.03 | $ | 0.08 | ||||

Note 8 – Stockholders’ Equity (Deficit)

On January 14, 2018, the Company’s Board of Directors approved an amendment to our Certificate of Incorporation to increase the number of authorized shares of common stock from 195,000,000 to 495,000,000 shares.

During the three months ended March 31, 2018:

Holders of convertible notes converted $401,914 of notes and $23,171 of accrued interest into 25,615,827 shares of common stock valued at $890,774. Additionally, 196,983 shares, valued at $18,713, for the conversion of notes, were authorized but not issued as of March 31, 2018. Shares authorized but unissued at December 31, 2017 totaling 370,450 shares were issued during 2018.

The Company issued 809,994 common shares as security for the payment of convertible notes. The shares, valued at $26,730 are held in escrow, are refundable and are recorded in a contra equity account.

We sold 880,005 shares of common stock and received proceeds of $20,872. Of these shares,395,005 valued at $9,777, were not issued as of March 31, 2018. We issued 336,071 shares of common stock that were sold in 2017 and classified as shares to be issued at December 31, 2017.

We issued 10,312,394 shares of common stock, valued at $140,380 as share-based compensation to related parties. Additionally, 25,000 shares, valued at $7,500, were authorized to be issued for related party services, but were not issued as of March 31, 2018. We issued 20,827,986 shares of common stock that were authorized as share-based compensation to related parties in 2017 and classified as shares to be issued at December 31, 2017.

We issued 437,902 shares of common stock, valued at $15,433, for services. Additionally, 1,071,245 shares, valued at $36,400 for services, were authorized but not issued as of March 31, 2018. We issued 1,968,335 shares of common stock that were authorized as share-based compensation in 2017 and classified as shares to be issued at December 31, 2017.

We issued 13,381,637 shares of common stock for payment of a related party note in the amount of $166,354, plus accrued interest of $21,658.

We issued 1,500,000 shares of common stock, valued at $47,254, were issued to settle accounts payable to a consultant.

We issued an excess 5,464,891 shares of common stock to a related party; these shares are in the process of being cancelled.

As a condition of their employment, the Board of Directors approved employment agreements with three key executives. This agreement provided that additional shares will be granted each year at February 1 over the term of the agreement should their shares as a percentage of the total shares outstanding fall below prescribed ownership percentages. The CEO received an annual grant of additional shares each year to maintain his ownership percentage at 10% of the outstanding stock. The other two executives receive a similar grant to maintain each executive’s ownership percentage at 7.5% of the outstanding stock. At March 31, 2018, there is $1,359,777 accrued for the annual grants at February 1, 2018, representing 38,525,196 shares. We recorded compensation expense of $144,554 for the three months ended March 31, 2018, resulting from the decline in shares price at the vesting date of February 1, 2018. We issued 5,562,806 shares of common stock that were accrued in 2017 and classified as shares to be issued at December 31, 2017.

Common stock warrant activity:

The Company has determined that certain of its warrants are subject to derivative accounting. The table below provides a reconciliation of the beginning and ending balances for the warrant liabilities measured using fair significant unobservable inputs (Level 3) for the three months ended March 31, 2018:

| Balance at December 31, 2017 | $ | 192,350 | ||

| Issuance of warrants | - | |||

| Change in fair value during period | (119,596 | ) | ||

| Balance at March 31, 2018 | $ | 72,754 |

| 11 |

The following assumptions were used in calculations of the Black Scholes model for the periods ended March 31, 2018 and December 31, 2017.

| March 31, 2018 | December 31, 2017 | |||||||

| Annual dividend yield | 0 | % | 0 | % | ||||

| Expected life (years) | 2-9 | 3-10 | ||||||

| Risk-free interest rate | 2.27 - 2.74 | % | 1.50 – 2.40 | % | ||||

| Expected volatility | 194 - 235 | % | 177 - 284 | % | ||||

Common stock option activity:

During the three months ended March 31, 2018, the Company recorded total option expense of $197,076.

Note 9 – Subsequent Events

In April, 2018, one of the Denver cultivation warehouses experienced a fire, burning 25 percent of the facility. All plants in the facility had to be destroyed. At the time, it had all the most up-to-date growing equipment and was at about 50 percent capacity. However, the other Denver cultivation warehouse was at 100 percent capacity and produced enough plants to completely supply the Denver Diego Pellicer store. Also, the price of the product on the wholesale market had become low enough that the Diego Pellicer Denver retail facility could buy product on the market at the same cost as it took to grow product in its own facilities to. As a result, Diego Pellicer Worldwide and the tenant Diego Pellicer Colorado decided repair the warehouse with the insurance proceeds and to offer both production warehouses for sale rather than restart production at the damaged facility. Management expects this to generate cash for Diego Pellicer Worldwide providing capital for future growth.

We issued 22,102,025 shares of common stock that were recorded as shares to be issued at March 31, 2018.

We issued 10,783,601 shares of common stock upon the conversion of $46,641 principal amount of notes and $11,166 of accrued interest.

We issued 1,000,000 shares of common stock as settlement for services rendered.

We entered into two convertible notes with an aggregate principal amount of $350,000 and received proceeds of $330,750.

| 12 |

ITEM 2. MANAGEMENT’S DISCUSSION AND ANALYSIS OF OPERATIONS

The following discussion and analysis of the results of operations and financial condition of Diego Pellicer Worldwide, Inc. (the “Company”, “we”, “us” or “our”) should be read in conjunction with the financial statements of Diego Pellicer Worldwide, Inc. and the notes to those financial statements that are included elsewhere in this Form 10-Q. This discussion includes forward-looking statements based upon current expectations that involve risks and uncertainties, such as our plans, objectives, expectations and intentions. Actual results and the timing of events could differ materially from those anticipated in these forward-looking statements as a result of a number of factors, including those set forth under the Risk Factors and Business sections in the financial statements and footnotes included in the Company’s Form 10-K filed on April 17, 2018 for the year ended December 31, 2017. Words such as “anticipate,” “estimate,” “plan,” “project,” “continuing,” “ongoing,” “expect,” “believe,” “intend,” “may,” “will,” “should,” “could,” and similar expressions are used to identify forward-looking statements.

Opportunity in an untapped industry with multi-billion-dollar potential

The demand for marijuana products is a multi-billion-dollar market that has only recently begun to become mainstream. Many challenges face the marijuana entrepreneur. Therein lies the opportunity.

Regulation and reality

Sales of marijuana on the black market topped $46.4 billion in 2016. that becomes a very conservative estimate of the size of the market in the United States. Distribution was driven underground for years by the Controlled Substance Act passed by Congress nearly 50 years ago. The favorable public opinion towards the legalization is rapidly changing the political attitude toward marijuana not only on the state level but on the federal level.

Financing and banking

As doubts remain, financing is still a challenge for this industry with banks in many states not only avoiding lending to these businesses but also refusing deposits because of complicated FDIC requirements. Financing has been largely equity raises, vendor financing, and expensive convertible debt. However, with the legalization and subsequent public capital raises in Canada and the change in the political attitude, there has been an indication of more interest by institutional investors in providing capital to this industry and more banks are accepting deposits.

A fragmented industry

Most industries evolve through the same business cycle. Many small independent companies initially operate in fragmented markets in the early stages. Then there is a consolidation of the industry, with the consolidators thriving and the independent companies dwindling. The larger companies have access to less expensive capital, lower costs, better merchandising, brand name recognition, and more efficient operations. This what we offer our tenants when negotiating the lease: an agreement to acquire them when marijuana is federally legalized. This gives the tenant the ultimate opportunity to participate in the rapid consolidation that we believe will happen when marijuana is federally legalized. This consolidation will result in companies that have heretofore been unable to participate in the rapidly growing industry to be scrambling to enter the space. Diego and its tenants will already be established and consolidated. As an exit strategy, we want to position Diego to be a likely candidate for acquisition or a major player in the marketplace.

The opportunity

The first mover advantage will continue to be possible for those willing to deal with the regulatory, banking, and financial challenges in today’s market. The fragmented market, the shortage of executives skilled in challenges of the industry, scarcity of brand names, provides a company like Diego, who has proven their business model, to be a consolidator in this industry.

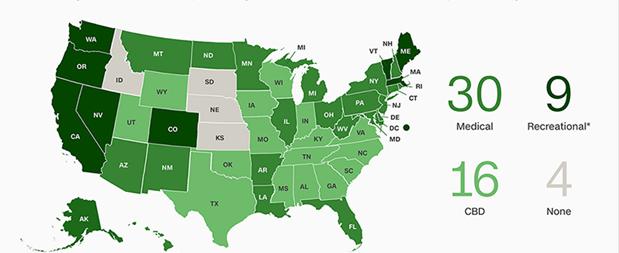

States with legalized marijuana

Thirty states and the District of Columbia have laws broadly legalizing marijuana in some form. Eight states and the District of Columbia have legalized marijuana for recreational use with the largest market by far, California, becoming legal on January 1, 2018. In another huge market, Massachusetts, recreational sales of cannabis is expected to start later this year in July.

The majority of all states allow for use of medical marijuana under certain circumstances. Some states have also decriminalized the possession of small amounts of marijuana. The industry is operating under stringent regulations within the various state jurisdictions.

This map shows current state laws and recently approved ballot measures legalizing marijuana for medical or recreational purposes. 2

There are 9,397 active licenses for marijuana businesses in the U.S., according to Ed Keating, chief data officer for Cannabiz Media, which tracks marijuana licenses. This includes cultivators, manufacturers, retailers, dispensaries, distributors, deliverers and test labs. Now 306 million Americans live in a jurisdiction that has legalized some form of cannabis use. 3 BDS Analytics estimates that the industry paid $1 billion in state taxes in 2016 and owes another $1.4 billion for 2017. 4

1 “Illegal Pot Sales Topped $46.4 Billion in 2016, and that’s Good News for Marijuana Entrepreneurs,” Inc., January 17, 2017, Will Yakowicz.

2 CNN Money, “The Legal Marijuana Market is Booming,” January 31, 2018, by Aaron Smith

3 Frontier Financial Group, ‘The Cannabis Industry Annual Report: 2017 Legal Marijuana Outlook,”

4 CNN Money, “The Legal Marijuana Market is Booming,” January 31, 2018, by Aaron Smith

The recent legalization in states such as California and probable legalization in Florida present opportunities many times that of Washington and Colorado. The Company is exploring opportunities in Oregon, California and Florida and is getting inquiries from other potential operators in other jurisdictions such as Michigan.

| 13 |

States introducing and expanding legalized marijuana laws

The legalized cannabis market is about to get a lot bigger, with Canada planning to legalize in July and Eastern states in the U.S. rushing towards legalization. States that have bills to legalize marijuana

| Arizona | Louisiana | New Jersey |

| Arkansas | Maryland | New Mexico |

| Connecticut | Michigan | Ohio |

| Delaware | Minnesota | Pennsylvania |

| Florida | Missouri | Rhode Island |

| Georgia | Mississippi | Vermont |

| Hawaii | Missouri | West Virginia |

| Illinois | Montana | Wisconsin |

| Kansas | New Hampshire | |

| Kentucky | New York |

Recent developments at the federal level

Pressures from the states with legalized cannabis industries have been exerted by those state’s Senators and Congressmen. Both informal and formal efforts have been increased by these states. The following are the most recent:

| ● | New York Democratic Senator Chuck Schumer introducing legislation to remove cannabis from the DEA’s list of controlled substances, to decriminalize pot at a federal level and effectively allow states to decide how to regulate the use of medical or recreational marijuana without concern for federal law. | |

| ● | President Trump cut a deal with Colorado Senator Corey Gardner, R-Colo. to allow states to decide what to do about cannabis. | |

| ● | Senator Mitch McConnell’s R-KY introduced his own legislation to make hemp farming legal in the U.S. | |

| ● | Former Speaker of the House John Boehner became a director with cannabis company Acreage Holdings. | |

| ● | The Food and Drug Administration setting up for an approval of the first cannabis-based drug from GW Pharmaceuticals Plc (GWPH). | |

| ● | The Veteran’s Administration now wants to study the effectiveness of cannabis for chronic pain and PTSD.5 | |

| ● | Marijuana-specific legislation recently introduced before the 115 U.S. Congress:6 |

| o | House Bill 974-Respect State Marijuana Laws Act of 2017- amending the Controlled Substance Act so that its language does not apply to people complying with state marijuana laws. | |

| o | House Bill 1227-Ending Marijuana Prohibition Act of 2017-deregulate marijuana federally. | |

| o | House Bill 1823-Marijuana Revenue and Regulation Act-amending the Internal Revenue Code for taxation and regulation of marijuana products. | |

| o | House Bill 1841-Regulate Marijuana Like Alcohol Act- removing marijuana from the Controlled Substance Act |

The projected U.S. cannabis industry’s growth

The Cannabis Industry’s Annual Report for 2017 projects the following robust growth of legal marijuana sales:7

5 The Street, “Cannabis Industry Sits on Precipice of Major Expansion, March 28, 2018, by Bill Meagher

6 The Cannbist, Federal Marijuana Bills Boosted by New Supporters as Congress Gets Back to Work, January 9, 2018, Alicia Wallace.

7 New Frontier, “The Cannabis Industry Annual Report: 2017 Legal Marijuana Outlook,”

| 14 |

Diego’s value proposition

Value proposition 1: By providing branding, training, unique accessories, purchasing services, site selection, standardized design, and experienced construction supervision, the tenant reduces his startup time, reduces expenses, increases their efficiency, and builds their gross margin. Diego provides the capital for preopening lease costs and tenant improvements. This results in a turnkey retail location for the tenant. Thus, Diego’s real estate, consulting and accessory sales are positioned to deliver a premium return on our investment.

Value proposition 2: With a demonstrated profitability, Diego has the choice of selling the operations of a selected facility in combination with the tenant and then securing a management contract for that facility. The proceeds can be used to further expand our branded stores and production facilities.

Value proposition 3: On select leases, Diego negotiates an acquisition contract with selected licensed tenants to acquire their operations. This contract will be executed at Diego’s option, and upon changes to federal law, introduces our second value proposition—ownership of operations in an industry that is projected to exceed $8 billion by 2018.

What is Diego’s Strategy?

Phase 1-brand and develop facilities and lease to licensed operators

Diego is initially a real estate and a consumer retail development company that is focused on high quality recurring revenues resulting from leasing real estate to licensed cannabis operators. Diego provides a competitive advantage to these operators by developing Diego Pellicer as the world’s first premium marijuana brand and by establishing the highest quality standards for its facilities and products.

The Company’s first phase strategy is to acquire and develop the most prominent and convenient real estate locations for the purposes of leasing them to state licensed operators in the cannabis industry. Diego’s first phase revenues result from leasing real estate and selling non-cannabis related accessories to our tenants. The company has developed a brand name strategy, providing training, design services, branded accessories, systems and systems training, locational selection, and other advisory services to their tenants. We enter into branding agreements with our tenants. In addition, part of the vetting process in finding the proper tenant is selecting a tenant that shares the Company’s values and strictly complies with state laws, follows strict safety and testing requirements and provides consistent, high-quality products. If the tenants do not comply, they will not be allowed to use the brand.

Simultaneous to the signing of the lease, Diego may secure an option to purchase the tenant’s operations with selected Diego operators/tenants.

Phase 2-Sell facilities and retain a management contract

Having developed a brand name and demonstrated operational excellence, the company has facilities with a proven superior earning power. The company, in combination with the licensed tenant, may choose to sell the real estate and the operating company and secure a management contract to manage the property the “Diego Way.” This will generate capital with which we can further expand our network of stores.

Phase 3-excersize the option to purchase and roll up licensed cannabis operations

When it becomes federally legal to do so, Diego will execute the acquisition contracts, consolidate our selected tenants and become a nationally branded marijuana retailer and producer concurrent with the change of federal law. We expect this to be a frantic time for larger companies to look for acquisitions, the opportunity to raise capital for further expansion or the exercise an exit strategy.

| 15 |

What does our premium branding accomplish?

A very important aspect of our marketing plan is to build Diego Pellicer as a luxury brand. This not only enables us to establish a premium brand, but also to generate significant revenues from non- cannabis products.

The Company is establishing several levels of branding and will use these to appeal to the various segments of the marketplace depending upon the location, competition, legal constraints, and budget. Standard store templates are being developed, complimentary accessories selectively designed, and customer preferences and segments analyzed.

Our Seattle and Denver stores have been met with enthusiastic demand growing revenues quickly. This is proving the initial Diego concept.

We have proven this to be a winning strategy

Diego is positioning itself to be a dominate player in the marijuana marketplace. Diego has proven this by being a fully integrated marijuana retail operation and premium brand, capitalizing on the beautifully designed retail stores offering the finest quality products at competitive prices.

What we accomplished in 2017

2017 was a time of great transition for the Company. An effective and experienced team had to be assembled to complement the current executives with knowledge and experience in real estate operations, banking, site selection, branding, facility design, corporate finance, investor relations, Additional capital needed to be raised in order to have sufficient capital to finish construction of the four facilities, build more facilities, and achieve a positive cash flow. Much of the Company’s debt was delinquent and needed to be repaid or renegotiated. New markets had to be explored, new alliances forged, and opportunities prioritized.

Two experienced executives joined the management team in the first quarter 2017 after having served in a consulting capacity since the summer of 2016. One executive had been the CEO of a publicly traded company for 15 years and the other had founded and operated several financial institutions and served on the boards of several public companies. The Company also engaged an advisor with extensive experience in national brand retail site selection, a consultant for branding and design that had been instrumental in the design of Apple stores and other facilities, and a world-renowned architect to design and standardize our retail facilities.

$1,278,500 in new capital was raised. New markets were explored. Four facilities were opened and began generating rents. All delinquent notes were renegotiated, consolidated, and extended. In 2017, Diego opened three Colorado facilities. With the Washington facility having opened in the latter part of 2016, Diego now had four facilities generating rent in 2017 for nearly the full year. The tenants in their first year of operation were quickly growing their sales and improving operational efficiency. Diego worked with these tenants, partially forbearing on their rent so as to allow these operators to strengthen their position and become capable of paying full rents. The properties generating rents in 2017 are as follows:

Table 1: Property Portfolio

| Purpose | Size | City | State | |||

| Retail store (recreational and medical) | 3,300 sq. | Denver | CO | |||

| Cultivation warehouse | 18,600 sq. | Denver | CO | |||

| Cultivation warehouse | 14,800 sq. | Denver | CO | |||

| Retail store (recreational and medical) | 4,500 sq. | Seattle | WA |

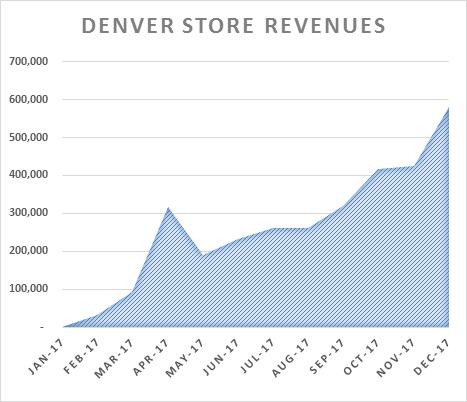

Diego’s Washington tenant opened our first flagship store in Seattle in October 2016. The Colorado tenant opened the Diego Denver branded flagship store in February 2017. In addition, Diego’s two cultivation facilities in Denver, CO began production in late 2016. The initial year’s sales by the retail stores showed rapid improvement as the year progressed. The capacity

| 16 |

Diego Pellicer Seattle

| 17 |

Diego Pellicer Denver

Diego will continue this strategy in states where recreational or medical marijuana sales and cultivation are legal under state law. Our business model is recurring lease revenue and is entirely scalable. Our success will dependent upon continuing to raise capital for expansion, continual improvement of our business model, standardizing store design, controlling costs, and continuing to develop the brand.

Summary of first quarter of 2018 results

As the result of increased revenues and decreased expenses, the loss from operations declined for the quarter ended March 31, 2018 compared to the prior year’s quarter ended March 31, 2017.

RESULTS OF OPERATIONS

After rental expense the gross margins on the lease were as follows:

Three Months Ended |

Three Months Ended |

Increase (Decrease) | ||||||||||||||

| March 31, 2018 | March 31, 2017 | $ | % | |||||||||||||

| Total revenues | ||||||||||||||||

| Rental Income | $ | 383,298 | $ | 309,962 | $ | 73,336 | 24 | % | ||||||||

| Rent expense | 269,087 | 347,203 | (78,116 | ) | (22 | )% | ||||||||||

| Gross Profit | 114,211 | $ | (37,241 | ) | $ | 151,452 | 407 | % | ||||||||

| Depreciation expense | 127,257 | 130,790 | (3,533 | ) | (3) | % | ||||||||||

| General and administrative expense | 651,042 | 893,007 | (241,965 | ) | (27 | )% | ||||||||||

| Loss from operations | $ | (664,088 | ) | $ | (1,061,038 | ) | $ | 396,950 | 37 | % | ||||||

Revenues. For the three months ended March 31, 2018 and 2017, the Company leased three facilities to licensees in Colorado and one in Washington. The three months ended March 31, 2018 is the beginning of the second year of operations for these licensees and Diego is now collecting some premium rents. Diego, however, is still forbearing on the premium rents contractually due from the tenant as a result of the cost of leasehold improvements and the deferral of preopening rents. These will become recorded as revenue when the Company considers the premium rents collectible considering the relative success of the tenant’s operations. These licensees have now had their opening year behind them and are experiencing increasing revenues in the second year of operations. This is a significant event for the company. For the first time in the company’s history there are four facilities generating some premium rental revenue. As a result, total revenue for the three months ended March 31, 2018 was $383,298, as compared to $309,962 for the three months ended March 31, 2017, an increase of $73,336.

Gross profit. While rental revenue for the quarter ended March 31, 2018 improved over the prior year’s first quarter, rental expense declined resulting in a gross profit of $114,211, an improvement over the quarter ended March 31, 2017 of $37,241.

General and administrative. Our general and administrative expenses for the three months ended March 31, 2018 were $651,042, compared to $893,007 for the three months ended March 31, 2017. The decline of $241,965 was largely attributable a reduction in executive stock compensation and consulting fees during three months ended March 31, 2018.

Three Months Ended |

Three Months Ended |

Increase (Decrease) | ||||||||||||||

| March 31, 2018 | March 31, 2017 | $ | % | |||||||||||||

| Other income (expense): | ||||||||||||||||

| Interest expense | $ | (710,474 | ) | $ | (288,236 | ) | $ | (422,238 | ) | (146 | )% | |||||

| Other income and expense | 58,358 | 10.376 | 68,734 | 662 | % | |||||||||||

| Change in fair value of derivative liabilities | 3,176,850 | 50,839 | 3,126,011 | 6,149 | % | |||||||||||

| Net other income | $ | 2,524,734 | $ | (247,773 | ) | $ | 2,772,507 | 1,119 | % | |||||||

* Not divisible by zero

The Net Other Income was the effect of the decline in market value of the company’s stock had on the derivative liability of $3,176,850 offset by recorded the cost of triggering technical default penalties on certain convertible notes of $219,013 and the financing costs of new debt incurred by the Company of $212,027.

| 18 |

LIQUIDITY AND CAPITAL RESOURCES

| Three Months Ended | Three Months Ended |

Increase (Decrease) | ||||||||||||||

| March 31, 2018 | March 31, 2017 | $ | % | |||||||||||||

| Net Cash provided by (used in) operating activities | $ | (275,756 | ) | $ | (361,720 | ) | $ | 85,964 | 24 | % | ||||||

| Net Cash used in investing activities | - | (135,000 | ) | $ | 135,000 | * | % | |||||||||

| Net Cash used in financing activities | 263,372 | 565,000 | (301,628 | ) | (53 | )% | ||||||||||

| Net Decrease in Cash | (12,384 | ) | 68,280 | (80,664 | ) | (118 | )% | |||||||||

| Cash - beginning of period | 158,702 | 51,333 | 107,369 | 209 | % | |||||||||||

| Cash - end of period | $ | 146,318 | $ | 119,613 | $ | 26,705 | 22 | % | ||||||||

Operating Activities. For the three months ended March 31, 2018, the net cash used of $275,756 was an improvement over the same quarter of the prior year of $361,720 the loss from operations after non-cash adjustments increased by 93,659 over the prior year offset by an increase in net operating assets and liabilities of $179.623.

Investing Activities. There were no investing activities for the three months ended March 31, 2018

Financing Activities. During the three months ended March 31, 2018, $258,500 in proceeds were from convertible notes payable and 20,872 from the sale of common stock.

Non-Cash Investing and Financing Activities. Non-cash activities for the three months ended March 31, 2018 was the conversion of convertible note of $568,268 plus interest of $44,829 to common stock valued at $1,078,786, the issuance of common stock for accounts payable, and the assuming of a tenant’s liabilities for leasehold improvements of $228,866.

Off-Balance Sheet Arrangements

We have no off-balance sheet arrangements.

ITEM 3. QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK.

We are a smaller reporting company as defined by Rule 12b-2 of the Exchange Act and are not required to provide the information under this item.

ITEM 4. CONTROLS AND PROCEDURES.

We carried out an evaluation required by Rule 13a-15 of the Exchange Act under the supervision and with the participation of our management, including our principal executive officer and principal financial officer, of the effectiveness of the design and operation of the Company’s “disclosure controls and procedures” and “internal control over financial reporting” as of the end of the period covered by this Report.

Evaluation of Disclosure Controls and Procedures

We maintain disclosure controls and procedures as defined in Rules 13a-15(e) and 15d-15(e) of the Exchange Act that are designed to ensure that information required to be disclosed in our reports filed or submitted to the SEC under the Exchange Act is recorded, processed, summarized and reported within the time periods specified by the SEC’s rules and forms, and that information is accumulated and communicated to management, including the principal executive and financial officer as appropriate, to allow timely decisions regarding required disclosures. Our principal executive officer and principal financial officer evaluated the effectiveness of disclosure controls and procedures as of the end of the period covered by this Annual Report (the “Evaluation Date”), pursuant to Rule 13a-15(b) under the Exchange Act.

Based on that evaluation, our principal executive officer and principal financial officer concluded that, as of the Evaluation Date, our disclosure controls and procedures were not effective to ensure that information required to be disclosed in our reports under the Exchange Act is recorded, processed, summarized, and reported within the time periods specified in the SEC’s rules and forms, and that such information is accumulated and communicated to management, including our principal executive officer and principal financial officer, as appropriate to allow timely decisions regarding required disclosure, due to material weaknesses in our control environment and financial reporting process.

| 19 |

Limitations on the Effectiveness of Controls

Our management, including our principal executive officer and principal financial officer, does not expect that our Disclosure Controls and internal controls will prevent all errors and all fraud. A control system, no matter how well conceived and operated, can provide only reasonable, not absolute, assurance that the objectives of the control system are met. Further, the design of a control system must reflect the fact that there are resource constraints, and the benefits of controls must be considered relative to their costs. Because of the inherent limitations in all control systems, no evaluation of controls can provide absolute assurance that all control issues and instances of fraud, if any, within the Company have been detected. These inherent limitations include the realities that judgments in decision- making can be faulty, and that breakdowns can occur because of a simple error or mistake. Additionally, controls can be circumvented by the individual acts of some persons, by collusion of two or more people, or by management or board override of the control.

The design of any system of controls also is based in part upon certain assumptions about the likelihood of future events, and there can be no assurance that any design will succeed in achieving its stated goals under all potential future conditions; over time, controls may become inadequate because of changes in conditions, or the degree of compliance with the policies or procedures may deteriorate.

Because of the inherent limitations in a cost-effective control system, misstatements due to error or fraud may occur and not be detected.

Changes in Internal Control over Financial Reporting

There were no changes in our internal control over financial reporting during the three months ended March 31, 2018 that materially affected, or are reasonably likely to materially affect, the Company’s internal control over financial reporting.

| 20 |

We are currently not involved in any litigation that we believe could have a material adverse effect on our financial condition or results of operations. There is no action, suit, proceeding, inquiry or investigation before or by any court, public board, government agency, self- regulatory organization or body pending or, to the knowledge of the executive officers of our company or any of our subsidiaries, threatened against or affecting our company, our common stock, any of our subsidiaries or of our companies or our subsidiaries’ officers or directors in their capacities as such, in which an adverse decision could have a material adverse effect.

We are a smaller reporting company as defined by Rule 12b-2 of the Exchange Act and are not required to provide the information under this item.

ITEM 2. UNREGISTERED SALES OF EQUITY SECURITIES AND USE OF PROCEEDS

None.

ITEM 3. DEFAULTS UPON SENIOR SECURITIES

None.

ITEM 4. MINE SAFETY DISCLOSURES

Not applicable.

None.

| 101.INS | XBRL Instance Document |

| 101.SCH | XBRL Taxonomy Schema |

| 101.CAL | XBRL Taxonomy Calculation Linkbase |

| 101.DEF | XBRL Taxonomy Definition Linkbase |

| 101.LAB | XBRL Taxonomy Label Linkbase |

| 101.PRE | XBRL Taxonomy Presentation Linkbase |

*In accordance with SEC Release 33-8238, Exhibit 32.1 and 32.2 are being furnished and not filed.

| 21 |

SIGNATURES

Pursuant to the requirements of the Securities Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by the undersigned thereunto duly authorized.

| DIEGO PELLICER WORLDWIDE, INC. | ||

| Date: May 15, 2018 | By: | /s/ Ron Throgmartin |

| Ron Throgmartin, Chief Executive Officer | ||

| (Principal Executive Officer) | ||

| 22 |