UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 20-F

| (Mark One) | |

| ¨ | REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| OR | |

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| For the fiscal year ended December 31, 2015 | |

| OR | |

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| OR | |

| ¨ | SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| Date of event requiring this shell company report | |

| For the transition period from to . | |

Commission file number: 001-36535

GLOBANT S.A.

(Exact name of Registrant as specified in its charter)

Not applicable

(Translation of Registrant’s name into English)

Grand Duchy of Luxembourg

(Jurisdiction of incorporation or organization)

37A, avenue J.F. Kennedy,

L-1855 Luxembourg

Tel: + 352 20 30 15 96

(Address of principal executive offices)

Patricio Pablo Rojo

37A, avenue J.F. Kennedy,

L-1855 Luxembourg

E-Mail: pablo.rojo@globant.com

Tel: + 352 20 30 15 96

(Name, Telephone, E-Mail and/or Facsimile number and Address of Company Contact Person)

Securities registered or to be registered pursuant to Section 12(b) of the Act.

| Title of each class | Name of each exchange on which registered |

| Common shares value $ 1.20 per share | NYSE |

Securities registered or to be registered pursuant to Section 12(g) of the Act.

None

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act.

None

Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of the period covered by the annual report: 34,208,406 common shares.

Indicate

by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

¨ Yes x No

If this report is an annual or transaction report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934. ¨ Yes x No

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. x Yes ¨ No

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). (*) ¨ Yes ¨ No

(*) This requirement does not apply to the registrant in respect of this filing.

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer.

| Large accelerated filer ¨ | Accelerated filer x | Non-accelerated filer ¨ |

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

U.S. GAAP ¨ International Financial Reporting Standards as issued by the International Accounting Standards Board x Other ¨

If “Other” has been checked in response to the previous question indicate by check mark which financial statement item the registrant has elected to follow. ¨ Item 17 ¨ Item 18

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). ¨ Yes x No

TABLE OF CONTENTS

CAUTIONARY STATEMENTS REGARDING FORWARD-LOOKING STATEMENTS

This annual report includes forward-looking statements. These forward-looking statements include, but are not limited to, all statements other than statements of historical facts contained in this annual report, including, without limitation, those regarding our future financial position and results of operations, strategy, plans, objectives, goals and targets, future developments in the markets in which we operate or are seeking to operate or anticipated regulatory changes in the markets in which we operate or intend to operate. In some cases, you can identify forward-looking statements by terminology such as “aim,” “anticipate,” “believe,” “continue,” “could,” “estimate,” “expect,” “forecast,” “guidance,” “intend,” “may,” “plan,” “potential,” “predict,” “projected,” “should” or “will” or the negative of such terms or other comparable terminology.

You should carefully consider all the information in this annual report, including the information set forth under “Risk Factors.” We believe our primary challenges are:

| • | If we are unable to maintain current resource utilization rates and productivity levels, our revenues, profit margins and results of operations may be adversely affected; |

| • | If we are unable to manage attrition and attract and retain highly-skilled IT professionals, we may not have the necessary resources to maintain client relationships, and competition for such IT professionals could materially adversely affect our business, financial condition and results of operations; |

| • | If the pricing structures we use for our client contracts are based on inaccurate expectations and assumptions regarding the cost and complexity of performing our work, our contracts could be unprofitable; |

| • | We may not be able to achieve our anticipated growth, which could materially adversely affect our revenues, results of operations, business and prospects; |

| • | We may be unable to effectively manage our rapid growth, which could place significant strain on our management personnel, systems and resources; |

| • | If we were to lose the services of our senior management team or other key employees, our business operations, competitive position, client relationships, revenues and results of operation may be adversely affected. |

| • | If we do not continue to innovate and remain at the forefront of emerging technologies and related market trends, we may lose clients and not remain competitive, which could cause our results of operations to suffer; |

| • | If any of our largest clients terminates, decreases the scope of, or fails to renew its business relationship or short-term contract with us, our revenues, business and results of operations may be adversely affected; |

| • | We derive a significant portion of our revenues from clients located in the United States and, to a lesser extent, Europe. Worsening general economic conditions in the United States, Europe or globally could materially adversely affect our revenues, margins, results of operations and financial condition; |

| • | Uncertainty concerning the instability in the current economic, political and social environment in Argentina may have an adverse impact on capital flows and could adversely affect our business, financial condition and results of operations; |

| • | Argentina’s regulations on proceeds from the export of services may increase our exposure to fluctuations in the value of the Argentine peso, which, in turn, could have an adverse effect on our operations and the market price of our common shares. The imposition in the future of additional regulations on proceeds collected outside Argentina for services rendered to non-Argentine residents or of export duties and controls could also have an adverse effect on us; |

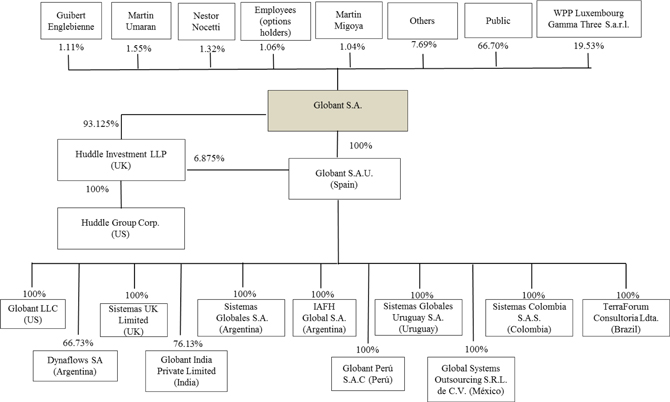

| • | Our greater than 5% shareholders, directors and executive officers and entities affiliated with them beneficially own approximately 47.81% of our outstanding common shares, of which approximately 19.53% of our outstanding common shares is owned by affiliates of WPP. These insiders therefore continue to have substantial control over us at the date of this annual report and could prevent new investors from influencing significant corporate decisions, such as approval of key transactions, including a change of control; and |

| • | By their nature, forward-looking statements involve risks and uncertainties because they relate to events and depend on circumstances that may or may not occur in the future. Forward-looking statements are not guarantees of future performance and are based on numerous assumptions. Our actual results of operations, financial condition and the development of events may differ materially from (and be more negative than) those made in, or suggested by, the forward-looking statements. Readers should read “Risk Factors” in this annual report and the description of our business under “Business” in this annual report for a more complete discussion of the factors that could affect us. |

| 1 |

Unless required by law, we undertake no obligation to update or revise any forward-looking statement, whether as a result of new information, future events or developments or otherwise.

CURRENCY PRESENTATION AND DEFINITIONS

In

this annual report, all references to “U.S. dollars” and “$” are to the lawful currency of the United

States, all references to “Argentine pesos” are to the lawful currency of the Republic of Argentina, all references

to “Colombian pesos” are to the lawful currency of the Republic of Colombia, all references to “Uruguayan pesos”

are to the lawful currency of the Republic of Uruguay, all references to “Mexican pesos” are to the lawful currency

of Mexico, all references to “ ” or “Rupees” or “Indian rupees” are to the lawful currency

of the Republic of India and all references to “euro” or “€” are to the single currency of the participating

member states of the European and Monetary Union of the Treaty Establishing the European Community, as amended from time to time.

All references to the “pound,” “British Sterling pound” or “£” are to the lawful currency

of the United Kingdom.

” or “Rupees” or “Indian rupees” are to the lawful currency

of the Republic of India and all references to “euro” or “€” are to the single currency of the participating

member states of the European and Monetary Union of the Treaty Establishing the European Community, as amended from time to time.

All references to the “pound,” “British Sterling pound” or “£” are to the lawful currency

of the United Kingdom.

Unless otherwise specified or the context requires otherwise in this annual report:

| · | “IT” refers to information technology; |

| · | “ISO” means the International Organization for Standardization, which develops and publishes international standards in a variety of technologies and in the IT services sector; |

| · | “ISO 9001:2008” means a quality management software developed by the ISO designed to help companies ensure they meet the standards of customers and other stakeholders; |

| · | “Agile development methodologies” means a group of software development methods based on iterative and incremental development, where requirements and solutions evolve through collaboration between self-organizing, cross-functional teams; |

| · | “Attrition rate,” during a specific period, refers to the ratio of IT professionals that left our company during the period to the number of IT professionals that were on our payroll on the last day of the period; |

| · | “Globers” refers to the employees that work in our company; and |

| · | “Digital journey” means a context-aware interaction between an end user and a brand or business whereby the interaction becomes a digital conversation in which technology establishes and builds a powerful experience with deep emotional connections through three key values: simplification, surprise, and anticipation. |

“GLOBANT” and its logo are our trademarks. Solely for convenience, we refer to our trademarks in this annual without the TM and ® symbols, but such references are not intended to indicate, in any way, that we will not assert, to the fullest extent under applicable law, our rights to our trademarks. Other service marks, trademarks and trade names referred to in this annual report are the property of their respective owners.

PRESENTATION OF FINANCIAL INFORMATION

Our consolidated financial statements are prepared under International Financial Reporting Standards (“IFRS”) as issued by the International Accounting Standards Board (“IASB”) and presented in U.S. dollars because the U.S. dollar is our functional currency. Our fiscal year ends on December 31 of each year. Accordingly, all references to a particular year are to the year ended December 31 of that year. Some percentages and amounts included in this annual report have been rounded for ease of presentation. Accordingly, figures shown as totals in certain tables may not be an exact arithmetic aggregation of the figures that precede them.

PRESENTATION OF INDUSTRY AND MARKET DATA

In this annual report, we rely on, and refer to, information regarding our business and the markets in which we operate and compete. The market data and certain economic and industry data and forecasts used in this annual report were obtained from International Data Corporation (“IDC”), Gartner, Inc. (“Gartner”), internal surveys, market research, governmental and other publicly available information, independent industry publications and reports prepared by industry consultants. Industry publications, surveys and forecasts generally state that the information contained therein has been obtained from sources believed to be reliable, but that the accuracy and completeness of such information is not guaranteed. We believe that these industry publications, surveys and forecasts are reliable, but we have not independently verified them and cannot guarantee their accuracy or completeness.

Certain market share information and other statements presented herein regarding our position relative to our competitors are not based on published statistical data or information obtained from independent third parties, but reflect our best estimates. We have based these estimates upon information obtained from our clients, trade and business organizations and associations and other contacts in the industries in which we operate.

| 2 |

ITEM 1. IDENTITY OF DIRECTORS, SENIOR MANAGEMENT AND ADVISERS

Not applicable.

ITEM 2. OFFER STATISTICS AND EXPECTED TIMETABLE

Not applicable.

| 3 |

The following summary consolidated financial and other data of Globant S.A. should be read in conjunction with, and are qualified by reference to, “Operating and Financial Review and Prospects” and our audited consolidated financial statements and notes thereto included elsewhere in this annual report. The summary consolidated financial data as of December 31, 2015 and 2014 and for the years ended December 31, 2015, 2014 and 2013 are derived from the audited consolidated financial statements of Globant S.A. included elsewhere in this annual report and should be read in conjunction with those audited consolidated financial statements and notes thereto. Our summary consolidated financial data as of December 31, 2013 and 2012 and for the years ended December 31, 2013 and 2012 set forth below was derived from our consolidated financial statements for the years ended December 31, 2013 and 2012 filed with the SEC on July 18, 2014 in Registration Statement No. 333-190841 on Form F-1, which are not included in this annual report. Our summary consolidated financial data as of December 31, 2011 set forth below was derived from our consolidated financial statements for the year ended December 31, 2012, which are not included in this annual report.

| Year ended December 31, | ||||||||||||||||||||

| 2015 | 2014 | 2013 | 2012 | 2011 | ||||||||||||||||

| (in thousands, except for percentages and per share data) | ||||||||||||||||||||

| Consolidated Statements of profit or loss and other comprehensive income: | ||||||||||||||||||||

| Revenues (1) | $ | 253,796 | $ | 199,605 | $ | 158,324 | $ | 128,849 | $ | 90,073 | ||||||||||

| Cost of revenues (2) | (160,292 | ) | (121,693 | ) | (99,603 | ) | (80,612 | ) | (53,604 | ) | ||||||||||

| Gross profit | 93,504 | 77,912 | 58,721 | 48,237 | 36,469 | |||||||||||||||

| Selling, general and administrative expenses (3) | (71,594 | ) | (57,288 | ) | (54,841 | ) | (47,680 | ) | (26,538 | ) | ||||||||||

| Impairment of tax credits, net of recoveries | 1,820 | 1,505 | (9,579 | ) | - | - | ||||||||||||||

| Profit (Loss) from operations | 23,730 | 22,129 | (5,699 | ) | 557 | 9,931 | ||||||||||||||

| Gain on transaction with bonds (4) | 19,102 | 12,629 | 29,577 | - | - | |||||||||||||||

| Finance income | 27,555 | 10,269 | 4,435 | 378 | - | |||||||||||||||

| Finance expense | (20,952 | ) | (11,213 | ) | (10,040 | ) | (2,687 | ) | (1,151 | ) | ||||||||||

| Finance income (expense), net (5) | 6,603 | (944 | ) | (5,605 | ) | (2,309 | ) | (1,151 | ) | |||||||||||

| Other income and expenses, net (6) | 605 | 380 | 1,505 | 291 | (3 | ) | ||||||||||||||

| Profit (Loss) before income tax | 50,040 | 34,194 | 19,778 | (1,461 | ) | 8,777 | ||||||||||||||

| Income tax (7) | (18,420 | ) | (8,931 | ) | (6,009 | ) | 160 | (1,689 | ) | |||||||||||

| Net Income (Loss) for the year | 31,620 | 25,263 | 13,769 | (1,301 | ) | 7,088 | ||||||||||||||

| Earnings (Loss) per share: | ||||||||||||||||||||

| Basic | 0.93 | 0.81 | 0.50 | (0.06 | ) | 0.25 | ||||||||||||||

| Diluted | 0.90 | 0.79 | 0.48 | (0.06 | ) | 0.25 | ||||||||||||||

| Weighted average number of outstanding shares (in thousands) | ||||||||||||||||||||

| Basic | 33,960 | 30,926 | 27,891 | 27,288 | 27,019 | |||||||||||||||

| Diluted | 35,013 | 31,867 | 28,884 | 27,288 | 27,019 | |||||||||||||||

| (1) | Includes transactions with related parties for an amount of $6,655, $7,681 and $8,532 for the years ended December 31, 2015, 2014 and 2013, respectively. |

| (2) | Includes depreciation and amortization expense of $4,441, $3,813, $3,215, $1,964 and $1,545 for the years ended December 31, 2015, 2014, 2013, 2012 and 2011, respectively. Also includes transactions with related parties for an amount of $2,901 and $1,169 for the years ended December 31, 2012 and 2011, respectively. Finally, it includes share based compensation for $735, $35, $190 and $4,644 for the years ended December 31, 2015, 2014, 2013 and 2012, respectively. |

| (3) | Includes depreciation and amortization expense of $4,860, $4,221, $3,941, $2,806 and $954 for the years ended December 31, 2015, 2014, 2013, 2012 and 2011, respectively. Also includes transactions with related parties for an amount of $1,381 and $931 for the years ended December 31, 2012 and 2011, respectively. Finally, it includes share based compensation for $1,647, $582, $603 and $7,065 for the years ended December 31, 2015, 2014, 2013 and 2012, respectively. |

| (4) | Includes gain on transactions with bonds of $19,102 and $12,629, and $29,577 acquired with funds from capitalizations and proceeds received by our Argentine subsidiaries as payments from exports for the years ended December 31, 2015, 2014 and 2013, respectively. See note 3.18 to our audited consolidated financial statements. |

| 4 |

| (5) | Includes foreign exchange loss of $10,136, $2,946, $4,238, $1,098 and $548 for the years ended December 31, 2015, 2014, 2013, 2012 and 2011, respectively. |

| (6) | Includes the gain related to the valuation at fair value of the 22.75% of share interest held in Dynaflows S.A of $625 for the year ended December 31, 2015. Includes the gain related to the bargain business combination of Bluestar Peru of $472 for the year ended December 31, 2014. See note 23 to our audited consolidated financial statements. Includes a gain of $1,703 on remeasurement of the contingent consideration related to the acquisition of TerraForum for the year ended December 31, 2013. See note 27.10.1 to our audited consolidated financial statements. |

| (7) | Includes deferred tax charge of $370 for the year ended December 31, 2014 and a gain of $1,102, $529, $2,479 and $109 for the years ended December 31, 2015, 2013, 2012 and 2011, respectively. |

| 5 |

Reconciliation of Non-IFRS Financial Data

| Year ended December 31, | ||||||||||||||||||||

| 2015 | 2014 | 2013 | 2012 | 2011 | ||||||||||||||||

| Reconciliation of adjusted gross profit | ||||||||||||||||||||

| Gross profit | $ | 93,504 | $ | 77,912 | $ | 58,721 | $ | 48,237 | $ | 36,469 | ||||||||||

| Adjustments | ||||||||||||||||||||

| Depreciation and amortization expense | 4,441 | 3,813 | 3,215 | 1,964 | 1,545 | |||||||||||||||

| Share-based compensation expense | 735 | 35 | 190 | 4,644 | - | |||||||||||||||

| Adjusted gross profit | $ | 98,680 | $ | 81,760 | $ | 62,126 | $ | 54,845 | $ | 38,014 | ||||||||||

| Reconciliation of adjusted selling, general and administrative expenses | ||||||||||||||||||||

| Selling, general and administrative expenses | $ | (71,594 | ) | $ | (57,288 | ) | $ | (54,841 | ) | $ | (47,680 | ) | $ | (26,538 | ) | |||||

| Adjustments | ||||||||||||||||||||

| Acquisition-related costs | 337 | - | - | - | - | |||||||||||||||

| Depreciation and amortization expense | 4,860 | 4,221 | 3,941 | 2,806 | 954 | |||||||||||||||

| Share-based compensation expense | 1,647 | 582 | 603 | 7,065 | - | |||||||||||||||

| Adjusted selling, general and administrative expenses | $ | (64,750 | ) | $ | (52,485 | ) | $ | (50,297 | ) | $ | (37,809 | ) | $ | (25,584 | ) | |||||

| Reconciliation of adjusted profit from operations | ||||||||||||||||||||

| Profit (Loss) from operations | 23,730 | 22,129 | (5,699 | ) | 557 | 9,931 | ||||||||||||||

| Adjustments | ||||||||||||||||||||

| Acquisition-related costs | 337 | - | - | - | - | |||||||||||||||

| Impairment of tax credits, net of recoveries | (1,820 | ) | (1,505 | ) | 9,579 | - | - | |||||||||||||

| Share-based compensation expense | 2,382 | 617 | 793 | 11,709 | - | |||||||||||||||

| Adjusted profit from operations | $ | 24,629 | $ | 21,241 | $ | 4,673 | $ | 12,266 | $ | 9,931 | ||||||||||

| Reconciliation of adjusted net income for the year | ||||||||||||||||||||

| Net income (loss) for the year | $ | 31,620 | $ | 25,263 | $ | 13,769 | $ | (1,301 | ) | $ | 7,088 | |||||||||

| Adjustments | ||||||||||||||||||||

| Acquisition-related costs | 337 | - | - | - | - | |||||||||||||||

| Share-based compensation expense | 2,382 | 617 | 793 | 11,709 | - | |||||||||||||||

| Adjusted net income for the year | $ | 34,339 | $ | 25,880 | $ | 14,562 | $ | 10,408 | $ | 7,088 | ||||||||||

| Other data: | ||||||||||||||||||||

| Adjusted gross profit (1) | 98,680 | 81,760 | 62,126 | 54,845 | 38,014 | |||||||||||||||

| Adjusted gross profit margin percentage (1) | 38.9 | % | 41.0 | % | 39.2 | % | 42.6 | % | 42.2 | % | ||||||||||

| Adjusted selling, general and administrative expenses (1) | (64,750 | ) | (52,485 | ) | (50,297 | ) | (37,809 | ) | (25,584 | ) | ||||||||||

| Adjusted profit from operations (2) | 24,629 | 21,241 | 4,673 | 12,266 | 9,931 | |||||||||||||||

| Adjusted profit from operations margin percentage (2) | 9.7 | % | 10.6 | % | 3.0 | % | 9.5 | % | 11.0 | % | ||||||||||

| Adjusted net income for the year (3) | 34,339 | 25,880 | 14,562 | 10,408 | 7,088 | |||||||||||||||

| Adjusted net income margin percentage for the year (3) | 13.5 | % | 13.0 | % | 9.2 | % | 8.1 | % | 7.9 | % | ||||||||||

| (1) | To supplement our gross profit presented in accordance with IFRS, we use the non-IFRS financial measure of adjusted gross profit, which is adjusted from gross profit, the most comparable IFRS measure, to exclude depreciation and amortization expense and share-based compensation expense included in cost of revenues. We also present the non-IFRS financial measure of adjusted gross profit margin percentage, which reflects adjusted gross profit margin as a percentage of revenues. To supplement our selling, general and administrative expenses presented in accordance with IFRS, we use the non-IFRS financial measure of adjusted selling, general and administrative expenses, which is adjusted from selling, general and administrative expenses, the most comparable IFRS measure, to exclude depreciation and amortization expense, acquisition-related costs and share-based compensation expense included in selling, general and administrative expenses. We believe that excluding such depreciation and amortization, acquisition-related costs and share-based compensation expense amounts from gross profit and selling, general and administrative expenses and depreciation and amortization expense and share-based compensation expense included in cost of revenues as a percentage of revenues from gross profit margin helps investors compare us and similar companies that exclude depreciation and amortization expense and share-based compensation expense from gross profit and selling, general and administrative expenses and depreciation and amortization expense and share-based compensation expense included in cost of revenues as a percentage of revenues from gross profit margin. These non-IFRS financial measures are provided as additional information to enhance investors’ overall understanding of the historical and current financial performance of our operations. We believe these measures help illustrate underlying trends in our business and use such measures to establish budgets and operational goals, communicated internally and externally, for managing our business and evaluating its performance. These non-IFRS financial measures should be considered in addition to results prepared in accordance with IFRS, but should not be considered as substitutes for or superior to IFRS results. In addition, our calculation of these non-IFRS financial measures may be different from the calculation used by other companies, and therefore comparability may be limited. |

| 6 |

| (2) | To supplement our profit (loss) from operations presented in accordance with IFRS, we use the non-IFRS financial measure of adjusted profit from operations, which is adjusted from profit (loss) from operations the most comparable IFRS measure, to exclude share-based compensation expense, acquisition-related costs and impairment of tax credits, net of recoveries. In addition, we present the non-IFRS financial measure of adjusted profit from operations margin percentage, which reflects adjusted profit from operations as a percentage of revenues. These non-IFRS financial measures are provided as additional information to enhance investors’ overall understanding of the historical and current financial performance of our operations. We believe these measures help illustrate underlying trends in our business and use such measures to establish budgets and operational goals, communicated internally and externally, for managing our business and evaluating its performance. These non-IFRS financial measures should be considered in addition to results prepared in accordance with IFRS, but should not be considered as substitutes for or superior to IFRS results. In addition, our calculation of these non-IFRS financial measures may be different from the calculation used by other companies, and therefore comparability may be limited. |

| (3) | To supplement our net income (loss) presented in accordance with IFRS, we use the non-IFRS financial measure of adjusted net income for the year, which is adjusted from net income (loss) for the year, the most comparable IFRS measure, to exclude share-based compensation expense and acquisition-related costs. In addition, we present the non-IFRS financial measure of adjusted net income margin percentage for the year, which reflects adjusted net income for the year as a percentage of revenues. These non-IFRS financial measures are provided as additional information to enhance investor’s overall understanding of the historical and current financial performance of our operations. We believe these measures help illustrate underlying trends in our business and use such measures to establish budgets and operational goals, communicated internally and externally, for managing our business and evaluating its performance. These non-IFRS financial measures should be considered in addition to results prepared in accordance with IFRS, but should not be considered as substitutes for or superior to IFRS results. In addition, our calculation of these non-IFRS financial measures may be different from the calculation used by other companies, and therefore comparability may be limited. |

| 7 |

Consolidated Statements of Financial Position Data

| As of December 31, | ||||||||||||||||||||

| 2015 | 2014 | 2013 | 2012 | 2011 | ||||||||||||||||

| Consolidated statements of financial position data: | ||||||||||||||||||||

| Cash and cash equivalents | $ | 36,720 | $ | 34,195 | $ | 17,051 | $ | 7,685 | $ | 7,013 | ||||||||||

| Investments | 25,660 | 27,984 | 9,634 | 914 | 2,234 | |||||||||||||||

| Trade receivables | 45,952 | 40,056 | 34,418 | 27,847 | 19,865 | |||||||||||||||

| Other receivables (current and non-current) | 38,692 | 15,169 | 12,333 | 17,997 | 13,735 | |||||||||||||||

| Deferred tax assets | 7,983 | 4,881 | 3,117 | 2,588 | 109 | |||||||||||||||

| Investment in associates | 300 | 750 | - | - | - | |||||||||||||||

| Other financial assets (current and non-current) | 2,121 | - | 1,284 | - | - | |||||||||||||||

| Property and equipment | 25,720 | 19,213 | 14,723 | 10,865 | 8,540 | |||||||||||||||

| Intangible assets | 7,209 | 6,105 | 6,141 | 4,305 | 1,488 | |||||||||||||||

| Goodwill | 32,532 | 12,772 | 13,046 | 9,181 | 6,389 | |||||||||||||||

| Total assets | 222,889 | 161,125 | 111,747 | 81,382 | 59,373 | |||||||||||||||

| Trade payables | 4,436 | 5,673 | 8,016 | 3,994 | 2,848 | |||||||||||||||

| Payroll and social security taxes payable | 25,551 | 20,967 | 17,823 | 13,703 | 9,872 | |||||||||||||||

| Borrowings (current and non-current) | 548 | 1,285 | 11,795 | 11,782 | 8,936 | |||||||||||||||

| Other financial liabilities (current and non-current) | 21,285 | 1,308 | 8,763 | 6,537 | 4,046 | |||||||||||||||

| Tax liabilities | 10,225 | 3,446 | 5,190 | 1,440 | 584 | |||||||||||||||

| Other liabilities and provisions | 659 | 967 | 295 | 988 | 338 | |||||||||||||||

| Total liabilities | 62,704 | 33,646 | 51,882 | 38,444 | 26,624 | |||||||||||||||

| Total equity | 160,185 | 127,479 | 59,865 | 42,938 | 32,749 | |||||||||||||||

| Total equity and liabilities | 222,889 | 161,125 | 111,747 | 81,382 | 59,373 | |||||||||||||||

B. Capitalization and Indebtedness

Not applicable.

C. Reasons for the Offer and Use of Proceeds

Not applicable.

You should carefully consider the risks and uncertainties described below, together with the other information contained in this annual report, before making any investment decision. Any of the following risks and uncertainties could have a material adverse effect on our business, prospects, results of operations and financial condition. The market price of our common shares could decline due to any of these risks and uncertainties, and you could lose all or part of your investment. The risks described below are those that we currently believe may materially affect us.

Risks Related to Our Business and Industry

If we are unable to maintain current resource utilization rates and productivity levels, our revenues, profit margins and results of operations may be adversely affected.

Our profitability and the cost of providing our services are affected by our utilization rate of the Globers in our Studios. If we are not able to maintain appropriate utilization rates for our professionals, our profit margin and our profitability may suffer. Our utilization rates are affected by a number of factors, including:

| 8 |

| • | our ability to transition Globers from completed projects to new assignments and to hire and integrate new employees; |

| • | our ability to forecast demand for our services and thereby maintain an appropriate headcount in each of our delivery centers; |

| • | our ability to manage the attrition of our IT professionals; and |

| • | our need to devote time and resources to training, professional development and other activities that cannot be billed to our clients. |

Our revenue could also suffer if we misjudge demand patterns and do not recruit sufficient employees to satisfy demand. Employee shortages could prevent us from completing our contractual commitments in a timely manner and cause us to pay penalties or lose contracts or clients. In addition, we could incur increased payroll costs, which would negatively affect our utilization rates and our business.

Increases in our current levels of attrition may increase our operating costs and adversely affect our future business prospects.

The total attrition rate among our Globers was 17.7%, 20.2% and 22.2% for the years ended December 31, 2015, 2014 and 2013, respectively. If our attrition rate were to increase, our operating efficiency and productivity may decrease. We compete for talented individuals not only with other companies in our industry but also with companies in other industries, such as software services, engineering services and financial services companies, among others, and there is a limited pool of individuals who have the skills and training needed to help us grow our company. High attrition rates of qualified personnel could have an adverse effect on our ability to expand our business, as well as cause us to incur greater personnel expenses and training costs.

If the pricing structures that we use for our client contracts are based on inaccurate expectations and assumptions regarding the cost and complexity of performing our work, our contracts could be unprofitable, which could adversely affect our results of operations, financial condition and cash flows from operation.

We perform our services primarily under time-and-materials contracts (where materials costs consist of travel and out-of-pocket expenses). We charge out the services performed by our Globers under these contracts at hourly rates that are agreed to at the time the contract is entered into. The hourly rates and other pricing terms negotiated with our clients are highly dependent on the complexity of the project, the mix of staffing we anticipate using on it, internal forecasts of our operating costs and predictions of increases in those costs influenced by wage inflation and other marketplace factors. Our predictions are based on limited data and could turn out to be inaccurate. Typically, we do not have the ability to increase the hourly rates established at the outset of a client project in order to pass through to our client increases in salary costs driven by wage inflation and other marketplace factors. Because we conduct the majority of our operations through our operating subsidiaries located in Argentina, we are subject to the effects of wage inflation and other marketplace factors in Argentina, which have increased significantly in recent years. If increases in salary and other operating costs at our Argentine subsidiaries exceed our internal forecasts, the hourly rates established under our time-and-materials contracts might not be sufficient to recover those increased operating costs, which would make those contracts unprofitable for us, thereby adversely affecting our results of operations, financial condition and cash flows from operations.

In addition to our time-and-materials contracts, we undertake some engagements on a fixed-price basis. Revenues from our fixed-price contracts represented approximately 3.7%, 9.3% and 15.2% of total revenues for the years ended December 31, 2015, 2014 and 2013, respectively. Our pricing in a fixed-price contract is highly dependent on our assumptions and forecasts about the costs we will incur to complete the related project, which are based on limited data and could turn out to be inaccurate. Any failure by us accurately to estimate the resources and time required to complete a fixed-price contract on time and on budget or any unexpected increase in the cost of our Globers assigned to the related project, office space or materials could expose us to risks associated with cost overruns and could have a material adverse effect on our business, results of operations and financial condition. In addition, any unexpected changes in economic conditions that affect any of the foregoing assumptions and predictions could render contracts that would have been favorable to us when signed unfavorable.

We may not be able to achieve anticipated growth, which could materially adversely affect our revenues, results of operations, business and prospects.

We intend to continue our expansion in the foreseeable future and to pursue existing and potential market opportunities. As we add new Studios, introduce new services or enter into new markets, we may face new market, technological and operational risks and challenges with which we are unfamiliar, and we may not be able to mitigate these risks and challenges to successfully grow those services or markets. We may not be able to achieve our anticipated growth, which could materially adversely affect our revenues, results of operations, business and prospects.

If we are unable to effectively manage the rapid growth of our business, our management personnel, systems and resources could face significant strains, which could adversely affect our results of operations.

We have experienced, and continue to experience, rapid growth in our headcount, operations and revenues, which has placed, and will continue to place, significant demands on our management and operational and financial infrastructure. Additionally, the longer-term transition in our delivery mix from Argentina-based staffing to increasingly decentralized staffing in other locations in Latin America (and, recently, the United States) has also placed additional operational and structural demands on our resources. Our future growth depends on recruiting, hiring and training technology professionals, growing our international operations, expanding our delivery capabilities, adding effective sales staff and management personnel, adding service offerings, maintaining existing clients and winning new business. Effective management of these and other growth initiatives will require us to continue to improve our infrastructure, execution standards and ability to expand services. Failure to manage growth effectively could have a material adverse effect on the quality of the execution of our engagements, our ability to attract and retain IT professionals and our business, results of operations and financial condition.

| 9 |

If we were to lose the services of our senior management team or other key employees, our business operations, competitive position, client relationships, revenues and results of operation may be adversely affected.

Our future success heavily depends upon the continued services of our senior management team and other key employees. We currently do not maintain key man life insurance for any of our founders, members of our senior management team or other key employees. If one or more of our senior executives or key employees are unable or unwilling to continue in their present positions, it could disrupt our business operations, and we may not be able to replace them easily, on a timely basis or at all. In addition, competition for senior executives and key employees in our industry is intense, and we may be unable to retain our senior executives and key employees or attract and retain new senior executives and key employees in the future, in which case our business may be severely disrupted.

If any of our senior management team or key employees joins a competitor or forms a competing company, we may lose clients, suppliers, know-how and key IT professionals and staff members to them. Also, if any of our sales executives or other sales personnel, who generally maintain a close relationship with our clients, joins a competitor or forms a competing company, we may lose clients to that company, and our revenues may be materially adversely affected. Additionally, there could be unauthorized disclosure or use of our technical knowledge, practices or procedures by such personnel. If any dispute arises between any members of our senior management team or key employees and us, any noncompetition, non-solicitation and nondisclosure agreements we have with our founders, senior executives or key employees might not provide effective protection to us in light of legal uncertainties associated with the enforceability of such agreements.

If we are unable to attract and retain highly-skilled IT professionals, we may not be able to maintain client relationships and grow effectively, which may adversely affect our business, results of operations and financial condition.

Our business is labor intensive and, accordingly, our success depends upon our ability to attract, develop, motivate, retain and effectively utilize highly-skilled IT professionals. We believe that there is significant competition for technology professionals in Latin America, the United States, Europe, Asia and elsewhere who possess the technical skills and experience necessary to deliver our services, and that such competition is likely to continue for the foreseeable future. As a result, the technology industry generally experiences a significant rate of turnover of its workforce. Our business plan is based on hiring and training a significant number of additional technology professionals each year in order to meet anticipated turnover and increased staffing needs. Our ability to properly staff projects, to maintain and renew existing engagements and to win new business depends, in large part, on our ability to hire and retain qualified IT professionals.

We cannot assure you that we will be able to recruit and train a sufficient number of qualified professionals or that we will be successful in retaining current or future employees. Increased hiring by technology companies, particularly in Latin America, the United States, Asia and Europe, and increasing worldwide competition for skilled technology professionals may lead to a shortage in the availability of qualified personnel in the locations where we operate and hire. Failure to hire and train or retain qualified technology professionals in sufficient numbers could have a material adverse effect on our business, results of operations and financial condition.

If we do not continue to innovate and remain at the forefront of emerging technologies and related market trends, we may lose clients and not remain competitive, which could cause our revenues and results of operations to suffer.

Our success depends on delivering digital journeys that leverage emerging technologies and emerging market trends to drive increased revenues and effective communication with customers. Technological advances and innovation are constant in the technology services industry. As a result, we must continue to invest significant resources in research and development to stay abreast of technology developments so that we may continue to deliver digital journeys that our clients will wish to purchase. If we are unable to anticipate technology developments, enhance our existing services or develop and introduce new services to keep pace with such changes and meet changing client needs, we may lose clients and our revenues and results of operations could suffer. Our results of operations would also suffer if our innovations are not responsive to the needs of our clients, are not appropriately timed with market opportunities or are not effectively brought to market. Our competitors may be able to offer engineering, design and innovation services that are, or that are perceived to be, substantially similar or better than those we offer. This may force us to compete on other fronts in addition to the quality of our services and to expend significant resources in order to remain competitive, which we may be unable to do.

If the current effective income tax rate payable by us in any country in which we operate is increased or if we lose any country-specific tax benefits, then our financial condition and results of operations may be adversely affected.

We conduct business globally and file income tax returns in multiple jurisdictions. Our consolidated effective income tax rate could be materially adversely affected by several factors, including changes in the amount of income taxed by or allocated to the various jurisdictions in which we operate that have differing statutory tax rates; changing tax laws, regulations and interpretations of such tax laws in multiple jurisdictions; and the resolution of issues arising from tax audits or examinations and any related interest or penalties.

We report our results of operations based on our determination of the amount of taxes owed in the various jurisdictions in which we operate. We have transfer pricing arrangements among our subsidiaries in relation to various aspects of our business, including operations, marketing, sales and delivery functions. Transfer pricing regulations require that any international transaction involving associated enterprises be on arm’s-length terms. We consider the transactions among our subsidiaries to be on arm’s-length terms. The determination of our consolidated provision for income taxes and other tax liabilities requires estimation, judgment and calculations where the ultimate tax determination may not be certain. Our determination of tax liability is always subject to review or examination by authorities in various jurisdictions.

| 10 |

Under Argentina’s Law No. 25,922 (Ley de Promoción de la Industria de Software), as amended by Law No. 26,692 (the “Software Promotion Law”), our operating subsidiaries in Argentina benefit from a 60% reduction in their corporate income tax rate (as applied to income from promoted software activities) and a tax credit of up to 70% of amounts paid for certain social security taxes (contributions) that may be offset against value-added tax liabilities. Law No. 26,692, the 2011 amendment to the Software Promotion Law (“Law No. 26,692”), also allows such tax credits to be applied to reduce our Argentine subsidiaries’ corporate income tax liability by a percentage not higher than the subsidiaries’ declared percentage of exports and extends the tax benefits under the Software Promotion Law until December 31, 2019.

On September 16, 2013, the Argentine government published Regulatory Decree No. 1315/2013, which governs the implementation of the Software Promotion Law. Regulatory Decree No. 1315/2013 introduced specific requirements to qualify for the tax benefits contemplated by the Software Promotion Law. In particular, Regulatory Decree No. 1315/2013 provides that from September 17, 2014 through December 31, 2019, only those companies that are accepted for registration in the National Registry of Software Producers (Registro Nacional de Productores de Software y Servicios Informaticos) maintained by the Secretary of Industry (Secretaria de Industria del Ministerio de Industria) will be entitled to participate in the benefits of the Software Promotion Law. On June 25, 2014, our Argentine subsidiaries Huddle Group S.A., IAFH Global S.A. and Sistemas Globales S.A. applied for registration in the National Registry of Software Producers.

On March 11, 2014, the Argentine Federal Administration of Public Revenue (Administración Federal de Ingresos Publicos, or “AFIP”) issued General Resolution No. 3,597 (“General Resolution No. 3,597”). This measure provides that, as a further prerequisite to participation in the benefits of the Software Promotion Law, exporters of software and related services must register in a newly established Special Registry of Exporters of Services (Registro Especial de Exportadores de Servicios). On March 14, May 21 and May 28, 2014, our Argentine subsidiaries Huddle Group S.A., IAFH Global S.A. and Sistemas Globales S.A., respectively, were accepted for registration in the Special Registry of Exporters of Services. In addition, General Resolution No. 3,597 states that any tax credits generated under the Software Promotion Law by a participant in the Software Promotion Law will only be valid until September 17, 2014.

On March 26, 2015, the Secretary and Subsecretary of Industry issued rulings approving the registration in the National Registry of Software Producers of Sistemas Globales S.A. and IAFH Global S.A. On April 17, 2015, the Secretary and Subsecretary of Industry issued rulings approving the registration in the National Registry of Software Producers of Huddle Group S.A. In each case, the ruling made the effective date of registration retroactive to September 18, 2014 and provided that the benefits enjoyed under the Software Promotion Law as originally enacted were not extinguished until the ruling goes into effect (which have occurred upon its date of publication in the Argentine government’s official gazette on before mentioned dates).

On May 7, 2015, we applied to the Subsecretary of Industry for deregistration of Huddle Group S.A. from the National Registry of Software Producers, as the subsidiary had discontinued activities since January 1, 2015. Although resolution by the Subsecretary of Industry is still pending, as a result of the cessation of its activities, Huddle Group S.A. is subject to a 35% corporate income tax rate effective January 1, 2015.

Our subsidiary in Uruguay, which is situated in a tax-free zone, benefits from a 0% income tax rate and an exemption from value-added tax.

Our subsidiary in India is primarily export-oriented and is eligible for certain income tax holiday benefits granted by the government of India for export activities conducted within Special Economic Zones (a “SEZ”). Under the Special Economic Zones Act, 2005, our Indian software development center located in Pune currently operates in a SEZ. The services provided by our Pune development center are eligible for a deduction of 100% of the profits or gains derived from the export of services for the first five years from the financial year in which the center commenced the provision of services and 50% of such profits or gains for the five years thereafter. Certain tax benefits are also available for a further five years subject to the center meeting defined conditions. Indian profits ineligible for SEZ benefits are subject to corporate income tax at the rate of 34.61%, including surcharges. In addition, all Indian profits, including those generated within SEZs, are subject to the Minimum Alternative Tax (“MAT”), at the current rate of approximately 21.34%, including surcharges. If the Indian government changes its policies affecting SEZs in a manner that adversely impacts the incentives for establishing and operating facilities in SEZs, our business, results of operations and financial condition may be adversely affected.

If these tax incentives in Argentina, India and Uruguay are changed, terminated, not extended or made unavailable, or comparable new tax incentives are not introduced, we expect that our effective income tax rate and/or our operating expenses would increase significantly, which could materially adversely affect our financial condition and results of operations. See “Operating and Financial Review and Prospects — Operating Results — Certain Income Statement Line Items — Income Tax Expense” and “Operating and Financial Review and Prospects — Liquidity and Capital Resources — Future Capital Requirements.”

If any of our largest clients terminates, decreases the scope of, or fails to renew its business relationship or short-term contract with us, our revenues, business and results of operations may be adversely affected.

We generate a significant portion of our revenues from our ten largest clients. During the years ended December 31, 2015, 2014 and 2013, our largest customer based on revenues, Walt Disney Parks and Resorts Online, accounted for 12.3%, 8.7% and 6.4% of our revenues, respectively. During the years ended December 31, 2015, 2014 and 2013, our ten largest clients accounted for 46.7%, 43.9% and 39.7% of our revenues, respectively.

| 11 |

Our ability to maintain close relationships with these and other major clients is essential to the growth and profitability of our business. However, most of our client contracts are limited to short-term, discrete projects without any commitment to a specific volume of business or future work, and the volume of work performed for a specific client is likely to vary from year to year, especially since we are generally not our clients’ exclusive technology services provider. A major client in one year may not provide the same level of revenues for us in any subsequent year. The technology services we provide to our clients, and the revenues and income from those services, may decline or vary as the type and quantity of technology services we provide changes over time. In addition, our reliance on any individual client for a significant portion of our revenues may give that client a certain degree of pricing leverage against us when negotiating contracts and terms of service.

In addition, a number of factors, including the following, other than our performance could cause the loss of or reduction in business or revenues from a client and these factors are not predictable:

| · | our need to devote time and resources to training, professional development and other activities that cannot be billed to our clients. |

| · | the business or financial condition of that client or the economy generally; |

| · | a change in strategic priorities by that client, resulting in a reduced level of spending on technology services; |

| · | a demand for price reductions by that client; and |

| · | a decision by that client to move work in-house or to one or several of our competitors. |

The loss or diminution in business from any of our major clients could have a material adverse effect on our revenues and results of operations.

Our revenues, margins, results of operations and financial condition may be materially adversely affected if general economic conditions in the United States, Europe or the global economy worsen.

We derive a significant portion of our revenues from clients located in the United States and, to a lesser extent, Europe. The 2008-2009 crisis in the financial and credit markets in United States, Europe and Asia led to a global economic slowdown, with the economies of those regions, particularly the Eurozone, continuing to show significant signs of weakness. The technology services industry is particularly sensitive to the economic environment, and tends to decline during general economic downturns. If the U.S. or European economies further weaken or slow, pricing for our services may be depressed and our clients may reduce or postpone their technology spending significantly, which may, in turn, lower the demand for our services and negatively affect our revenues and profitability.

The ongoing financial crisis in Europe (including concerns that certain European countries may default in payments due on their national debt) and the resulting economic uncertainty could adversely impact our operating results unless and until economic conditions in Europe improve and the prospect of national debt defaults in Europe decline. To the extent that these adverse economic conditions continue or worsen, they will likely have a negative effect on our business.

If we are unable to successfully anticipate changing economic and political conditions affecting the markets in which we operate, we may be unable to effectively plan for or respond to those changes, and our results of operations could be adversely affected.

We face intense competition from technology and IT services providers, and an increase in competition, our inability to compete successfully, pricing pressures or loss of market share could materially adversely affect our revenues, results of operations and financial condition.

The market for technology and IT services is intensely competitive, highly fragmented and subject to rapid change and evolving industry standards and we expect competition to intensify. We believe that the principal competitive factors that we face are the ability to innovate; technical expertise and industry knowledge; end-to-end solution offerings; reputation and track record for high-quality and on-time delivery of work; effective employee recruiting; training and retention; responsiveness to clients’ business needs; scale; financial stability; and price.

We face competition primarily from large global consulting and outsourcing firms, digital agencies and design firms, traditional technology outsourcing providers, and the in-house product development departments of our clients and potential clients. Many of our competitors have substantially greater financial, technical and marketing resources and greater name recognition than we do. As a result, they may be able to compete more aggressively on pricing or devote greater resources to the development and promotion of technology and IT services. Companies based in some emerging markets also present significant price competition due to their competitive cost structures and tax advantages.

| 12 |

In addition, there are relatively few barriers to entry into our markets and we have faced, and expect to continue to face, competition from new technology services providers. Further, there is a risk that our clients may elect to increase their internal resources to satisfy their services needs as opposed to relying on a third-party vendor, such as our company. The technology services industry is also undergoing consolidation, which may result in increased competition in our target markets in the United States and Europe from larger firms that may have substantially greater financial, marketing or technical resources, may be able to respond more quickly to new technologies or processes and changes in client demands, and may be able to devote greater resources to the development, promotion and sale of their services than we can. Increased competition could also result in price reductions, reduced operating margins and loss of our market share. We cannot assure you that we will be able to compete successfully with existing or new competitors or that competitive pressures will not materially adversely affect our business, results of operations and financial condition.

Our business depends on a strong brand and corporate reputation, and if we are not able to maintain and enhance our brand, our ability to expand our client base will be impaired and our business and operating results will be adversely affected.

Since many of our specific client engagements involve highly tailored solutions, our corporate reputation is a significant factor in our clients’ and prospective clients’ determination of whether to engage us. We believe the Globant brand name and our reputation are important corporate assets that help distinguish our services from those of our competitors and also contribute to our efforts to recruit and retain talented IT professionals. However, our corporate reputation is susceptible to damage by actions or statements made by current or former employees or clients, competitors, vendors, adversaries in legal proceedings and government regulators, as well as members of the investment community and the media. There is a risk that negative information about our company, even if based on false rumor or misunderstanding, could adversely affect our business. In particular, damage to our reputation could be difficult and time-consuming to repair, could make potential or existing clients reluctant to select us for new engagements, resulting in a loss of business, and could adversely affect our recruitment and retention efforts. Damage to our reputation could also reduce the value and effectiveness of our Globant brand name and could reduce investor confidence in us and result in a decline in the price of our common shares.

We are seeking to expand our presence in the United States, which entails significant expenses and deployment of employees on-site with our clients. If we are unable to manage our operational expansion into the United States, it may adversely affect our business, results of operations and prospects.

A key element of Globant’s strategy is to expand our delivery footprint, including by increasing the number of employees that are deployed onsite at our clients or near client locations. In particular, we intend to focus our recruitment efforts on the United States. Client demands, the availability of high-quality technical and operational personnel at attractive compensation rates, regulatory environments and other pertinent factors may vary significantly by region and our experience in the markets in which we currently operate may not be applicable to other regions. As a result, we may not be able to leverage our experience to expand our delivery footprint effectively into our target markets in the United States. If we are unable to manage our expansion efforts effectively, if our expansion plans take longer to implement than expected or if our costs for these efforts exceed our expectations, our business, results of operations and prospects could be materially adversely affected.

If a significant number of our Globers were to join unions, our labor costs and our business could be negatively affected.

As of December 31, 2015, we had 79 Globers, 73 working at our delivery center located in Rosario and Santa Fe City, Argentina, who are covered by a collective bargaining agreement with the Federación Argentina de Empleados de Comercio y Servicios (“FAECYS”), which is renewed on an annual basis. In addition, our primary Argentine subsidiary is defending a lawsuit filed by FAECYS in which FAECYS is demanding the application of its collective labor agreement to unspecified categories of employees of that subsidiary. According to FAECYS’s claim, our principal Argentine subsidiary would have been required to withhold and transfer to FAECYS an amount equal to 0.5% of the gross monthly salaries of that subsidiary’s payroll from October 2006 to October 2011. Furthermore, FAECYS’ claim may be increased to cover withholdings from October 2006 through the date of a future judgment. Several Argentine technology companies are facing similar lawsuits filed by FAECYS which have been decided in favor of both the companies and FAECYS. Under Argentine law, judicial decisions only apply to the particular case at hand. There is no stare decisis and courts’ decisions are not binding on lower courts even in the same jurisdiction although they may be used as guidelines on other similar cases. See “Financial Information — Consolidated Statements and Other Financial Information — Legal Proceedings” and the notes to our consolidated financial statements. If a significant additional number of our Globers were to join unions, our labor costs and our business could be negatively affected.

Our revenues are dependent on a limited number of industries, and any decrease in demand for technology services in these industries could reduce our revenues and adversely affect our results of operations.

A substantial portion of our clients are concentrated in the following industries: professional services; media and entertainment; technology and telecommunications; and banks, financial services and insurance, which industries, in the aggregate, constituted 71.8%, 75.1% and 78.5% of our total revenues for the years ended December 31, 2015, 2014 and 2013, respectively. Our business growth largely depends on continued demand for our services from clients in these industries and other industries that we may target in the future, as well as on trends in these industries to purchase technology services or to move such services in-house.

A downturn in any of these or our targeted industries, a slowdown or reversal of the trend to spend on technology services in any of these industries could result in a decrease in the demand for our services and materially adversely affect our revenues, financial condition and results of operations. For example, a worsening of economic conditions in the media and entertainment industry and significant consolidation in that industry may reduce the demand for our services and negatively affect our revenues and profitability.

Other developments in the industries in which we operate may also lead to a decline in the demand for our services in these industries, and we may not be able to successfully anticipate and prepare for any such changes. For example, consolidation in any of these industries or acquisitions, particularly involving our clients, may adversely affect our business. Our clients may experience rapid changes in their prospects, substantial price competition and pressure on their profitability. This, in turn, may result in increasing pressure on us from clients in these key industries to lower our prices, which could adversely affect our revenues, results of operations and financial condition.

| 13 |

We have a relatively short operating history and operate in a rapidly evolving industry, which makes it difficult to evaluate our future prospects, may increase the risk that we will not continue to be successful and, accordingly, increases the risk of your investment.

Our company was founded in 2003 and, therefore, has a relatively short operating history. In addition, the technology services industry itself is continuously evolving. Competition, fueled by rapidly changing consumer demands and constant technological developments, renders the technology services industry one in which success and performance metrics are difficult to predict and measure. Because services and technologies are rapidly evolving and each company within the industry can vary greatly in terms of the services it provides, its business model, and its results of operations, it can be difficult to predict how any company’s services, including ours, will be received in the market. While enterprises have been willing to devote significant resources to incorporate emerging technologies and related market trends into their business models, enterprises may not continue to spend any significant portion of their budgets on our services in the future. Neither our past financial performance nor the past financial performance of any other company in the technology services industry is indicative of how our company will fare financially in the future. Our future profits may vary substantially from those of other companies, and those we have achieved in the past, making investment in our company risky and speculative. If our clients’ demand for our services declines, as a result of economic conditions, market factors or shifts in the technology industry, our business would suffer and our results of operations and financial condition would be adversely affected.

We are investing substantial cash in new facilities and physical infrastructure, and our profitability and cash flows could be reduced if our business does not grow proportionately.

We have made and continue to make significant contractual commitments related to capital expenditures on construction or expansion of our delivery centers. We may encounter cost overruns or project delays in connection with opening new facilities. These expansions will likely increase our fixed costs and if we are unable to grow our business and revenues proportionately, our profitability and cash flows may be negatively affected.

If we cause disruptions in our clients’ businesses or provide inadequate service, our clients may have claims for substantial damages against us, which could cause us to lose clients, have a negative effect on our corporate reputation and adversely affect our results of operations.

If our Globers make errors in the course of delivering services to our clients or fail to consistently meet service requirements of a client, these errors or failures could disrupt the client’s business, which could result in a reduction in our revenues or a claim for substantial damages against us. In addition, a failure or inability to meet a contractual requirement could seriously damage our corporate reputation and limit our ability to attract new business.

The services we provide are often critical to our clients’ businesses. Certain of our client contracts require us to comply with security obligations including maintaining network security and backup data, ensuring our network is virus-free, maintaining business continuity planning procedures, and verifying the integrity of employees that work with our clients by conducting background checks. Any failure in a client’s system or breach of security relating to the services we provide to the client could damage our reputation or result in a claim for substantial damages against us. Any significant failure of our equipment or systems, or any major disruption to basic infrastructure like power and telecommunications in the locations in which we operate, could impede our ability to provide services to our clients, have a negative impact on our reputation, cause us to lose clients, and adversely affect our results of operations.

Under our client contracts, our liability for breach of our obligations is in some cases limited pursuant to the terms of the contract. Such limitations may be unenforceable or otherwise may not protect us from liability for damages. In addition, certain liabilities, such as claims of third parties for which we may be required to indemnify our clients, are generally not limited under our contracts. The successful assertion of one or more large claims against us in amounts greater than those covered by our current insurance policies could materially adversely affect our business, financial condition and results of operations. Even if such assertions against us are unsuccessful, we may incur reputational harm and substantial legal fees.

We may face losses or reputational damage if our software solutions turn out to contain undetected software defects.

A significant amount of our business involves developing software solutions for our clients as part of our provision of technology services. We are required to make certain representations and warranties to our clients regarding the quality and functionality of our software. Any undetected software defects could result in liability to our clients under certain contracts as well as losses resulting from any litigation initiated by clients due to any losses sustained as a result of the defects. Any such liability or losses could have an adverse effect on our financial condition as well as on our reputation with our clients and in the technology services market in general.

Our client relationships, revenues, results of operations and financial condition may be adversely affected if we experience disruptions in our Internet infrastructure, telecommunications or IT systems.

Disruptions in telecommunications, system failures, Internet infrastructure or computer virus attacks could damage our reputation and harm our ability to deliver services to our clients, which could result in client dissatisfaction and a loss of business and related reduction of our revenues. We may not be able to consistently maintain active voice and data communications between our various global operations and with our clients due to disruptions in telecommunication networks and power supply, system failures or computer virus attacks. Any significant failure in our ability to communicate could result in a disruption in business, which could hinder our performance and our ability to complete projects on time. Such failure to perform on client contracts could have a material adverse effect on our business, results of operations and financial condition.

| 14 |

If our computer system is or becomes vulnerable to security breaches, or if any of our employees misappropriates data, we may face reputational damage, lose clients and revenues, or incur losses.

We often have access to or are required to collect and store confidential client and customer data. Many of our client contracts do not limit our potential liability for breaches of confidentiality. If any person, including any of our Globers or former Globers, penetrates our network security or misappropriates data or code that belongs to us, our clients, or our clients’ customers, we could be subject to significant liability from our clients or from our clients’ customers for breaching contractual confidentiality provisions or privacy laws.

Unauthorized disclosure of sensitive or confidential client and customer data, whether through breach of our computer systems, systems failure, loss or theft of confidential information or intellectual property belonging to our clients or our clients’ customers, or otherwise, could damage our reputation, cause us to lose clients and revenues, and result in financial and other potential losses by us.

Our business, results of operations and financial condition may be adversely affected by the various conflicting and/or onerous legal and regulatory requirements imposed on us by the countries where we operate.

Since we provide services to clients throughout the world, we are subject to numerous, and sometimes conflicting, legal requirements on matters as diverse as import/export controls, content requirements, trade restrictions, tariffs, taxation, sanctions, government affairs, anti-bribery, whistle blowing, internal and disclosure control obligations, data protection and privacy and labor relations. Our failure to comply with these regulations in the conduct of our business could result in fines, penalties, criminal sanctions against us or our officers, disgorgement of profits, prohibitions on doing business and adverse impact on our reputation. Our failure to comply with these regulations in connection with the performance of our obligations to our clients could also result in liability for monetary damages, fines and/or criminal prosecution, unfavorable publicity, restrictions on our ability to process information and allegations by our clients that we have not performed our contractual obligations. Due to the varying degree of development of the legal systems of the countries in which we operate, local laws might be insufficient to defend us and preserve our rights.

Due to our operating in a number of countries in Latin America, the United States, the United Kingdom and India, we are also subject to risks relating to compliance with a variety of national and local laws including multiple tax regimes, labor laws, employee health safety and wages and benefits laws. We may, from time to time, be subject to litigation or administrative actions resulting from claims against us by current or former Globers individually or as part of class actions, including claims of wrongful terminations, discrimination, misclassification or other violations of labor law or other alleged conduct. We may also, from time to time, be subject to litigation resulting from claims against us by third parties, including claims of breach of noncompete and confidentiality provisions of our employees’ former employment agreements with such third parties. Our failure to comply with applicable regulatory requirements could have a material adverse effect on our business, results of operations and financial condition.

We may not be able to prevent unauthorized use of our intellectual property and our intellectual property rights may not be adequate to protect our business, competitive position, results of operations and financial condition.

Our success depends in part on certain methodologies, practices, tools and technical expertise our company utilizes in designing, developing, implementing and maintaining applications and other proprietary intellectual capital. In order to protect our rights in this intellectual capital, we rely upon a combination of nondisclosure and other contractual arrangements as well as trade secret, patent, copyright and trademark laws. We also generally enter into confidentiality agreements with our employees, consultants, clients and potential clients and limit access to and distribution of our proprietary information.

We hold several trademarks and intend to submit additional U.S. federal and foreign trademark applications for developments relating to additional service offerings in the future. We cannot assure you that we will be successful in maintaining existing or obtaining future intellectual property rights or registrations. There can be no assurance that the laws, rules, regulations and treaties in the countries in which we operate in effect now or in the future or the contractual and other protective measures we take are adequate to protect us from misappropriation or unauthorized use of our intellectual capital or that such laws, rules, regulations and treaties will not change.

We cannot assure you that we will be able to detect unauthorized use of our intellectual property and take appropriate steps to enforce our rights or that any such steps will be successful. We cannot assure you that we have taken all necessary steps to enforce our intellectual property rights in every jurisdiction in which we operate and we cannot assure you that the intellectual property laws of any jurisdiction in which we operate are adequate to protect our interest or that any favorable judgment obtained by us with respect thereto will be enforced in the courts. Misappropriation by third parties of, or other failure to protect, our intellectual property, including the costs of enforcing our intellectual property rights, could have a material adverse effect on our business, competitive position, results of operations and financial condition.

If we incur any liability for a violation of the intellectual property rights of others, our reputation, business, financial condition and prospects may be adversely affected.