UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM

(Mark One)

For the fiscal year ended

or

For the transition period from ____________ to ____________

Commission file number:

(Exact name of registrant as specified in its charter)

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) |

(Address of principal executive offices) (Zip Code)

(Registrant’s telephone number, including area code)

Securities registered under Section 12(b) of the Act:

| Title of each class registered | Trading Symbol(s) | Name of each exchange on which registered | ||

Securities registered under Section 12(g) of the Act: None.

Indicate by check mark

if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐

Indicate by check mark

if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐

Indicate by check mark

whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during

the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to

such filing requirements for the past 90 days.

Indicate by check mark

whether the registrant has submitted electronically, every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation

S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit

and post such files).

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ☐ | Accelerated filer | ☐ |

| ☒ | Smaller reporting company | ||

| Emerging growth company |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark

whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal

control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting

firm that prepared or issued its audit report.

If securities are registered

pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing

reflect the correction of an error to previously issued financial statements.

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark

whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ☐ No

As of June 30, 2023,

the last business day of the registrant’s second quarter of most recently completed fiscal year, the aggregate market value of the

common stock held by non-affiliates of the registrant was approximately $

As of March

22, 2024, there were

DOCUMENTS INCORPORATED BY REFERENCE

BAIYU Holdings, Inc.

Annual Report on Form 10-K

For the Fiscal Year Ended December 31, 2023

TABLE OF CONTENTS

Unless the context requires otherwise, reference to “BAIYU” refers to BAIYU Holdings, Inc., our Delaware holding company; reference to the “Company,” “we,” “our” or “us” refers to BAIYU Holdings, Inc., together as a group with its subsidiaries, and, in the context of describing the substantive operations and consolidated financial information relating to such operations of BAIYU Holdings, Inc. and its subsidiaries as a whole, refers to BAIYU and its subsidiaries; references to “VIE” or “Tongdow Internet Technology” refers to Shenzhen Tongdow Internet Technology Co., Ltd., the variable interest entity.

“PRC” or “China” refers to the People’s Republic of China, and only in the context of describing PRC laws, regulations, rules, regulatory authority and other legal or tax matters in this annual report, excludes Taiwan, Hong Kong and Macau; the legal and operational risks associated with operating in the PRC also apply to our operations in Hong Kong.

“RMB” or “Renminbi” refers to the legal currency of China and “$,” “US$” or “U.S. Dollars” refers to the legal currency of the United States.

i

Note Regarding Forward-Looking Statements

The information contained in this annual report on Form 10-K includes statements that are not historical facts and are “forward-looking statements.” Such forward-looking statements include, but are not limited to, statements regarding our Company and our management’s expectations, hopes, beliefs, intentions or strategies regarding the future, including our financial condition and results of operations. In addition, any statements that refer to projections, forecasts or other characterizations of future events or circumstances, including any underlying assumptions, are forward-looking statements. The words “anticipates,” “believes,” “continue,” “could,” “estimates,” “expects,” “intends,” “may,” “might,” “plans,” “possible,” “potential,” “predicts,” “projects,” “seeks,” “should,” “will,” “would” and similar expressions, or the negatives of such terms, may be identified as forward-looking statements, but the absence of these words does not mean that a statement is not forward-looking.

The forward-looking statements contained herein are based on current expectations and beliefs concerning future developments and the potential effects on us. Future developments that actually affect us may not be those anticipated. These forward-looking statements involve a number of risks, uncertainties (some of which are beyond our control) or other assumptions that may cause actual results or performance to be materially different from those expressed or implied by these forward-looking statements. Examples are statements regarding future developments with respect to the following:

| ● | expand our customer base; |

| ● | broaden our service and product offerings; |

| ● | enhance our risk management capabilities; |

| ● | improve our operational efficiency; |

| ● | our ability to raise sufficient funds to expand our operations; |

| ● | attract, retain and motivate talented employees; |

| ● | a decrease in demand for commodities trading and weakness in the commodities trading industry generally; |

| ● | navigate an evolving regulatory environment; |

| ● | defend ourselves against litigation, regulatory, privacy or other claims; |

| ● | development of a liquid trading market for our securities; |

| ● | our plan to maintain compliance with Nasdaq’s continued listing requirements; |

| ● | financial market volatility and declines in financial market prices of equity securities; |

| ● | liquidity and/or capital resources changes and the impact of any changes or limitations, including, without limitation, ability to borrow funds and/or renew or roll over existing indebtedness; and |

| ● | ongoing or new supply chain and product distribution/logistics issues. |

You should not rely upon forward-looking statements as predictions of future events. The events and circumstances reflected in the forward-looking statements may not be achieved or occur. Although we believe that the expectations reflected in the forward-looking statements are reasonable, we cannot guarantee future results, levels of activity, performance or achievements. Moreover, neither we nor any other person assume responsibility for the accuracy and completeness of the forward-looking statements. Except as required by law, we undertake no obligation to update publicly any forward-looking statements for any reason after the date of this report to conform these statements to actual results or to changes in our expectations.

We qualify all of our forward-looking statements by these cautionary statements. The Company assumes no obligation to revise or update any forward-looking statements for any reason, except as required by law.

ii

PART I

Item 1. Description of Business.

Overview and Corporate History

BAIYU Holdings, Inc. (formerly known as TD Holdings, Inc.), has become a business engaging in commodities trading business (the “Commodities Trading Business”) and supply chain service business (the “Supply Chain Service Business”) in China since the disposition of its direct loans, loan guarantees and financial leasing services to small-to-medium sized businesses, farmers and individuals in July 2018 and its used luxurious car leasing business in August 2020.

The Commodities Trading Business primarily involves purchasing non-ferrous metal products from upstream metal and mineral suppliers and then selling to downstream customers. The Supply Chain Service Business primarily has served as a one-stop commodity supply chain service and digital intelligence supply chain platform integrating upstream and downstream enterprises, warehouses, logistics, information, and futures trading.

BAIYU Holdings, Inc. is a Delaware holding company that conducts its operations and operates its business in China through its PRC subsidiaries. Such structure involves unique risks to our investors. The Chinese government may intervene in or influence the operation of PRC subsidiaries and exercise significant oversight and discretion over the conduct of our business or may exert more control over offerings conducted overseas by, and/or foreign investment in, China-based issuers, which could result in a material change in our operations and/or the value of our common stock. Furthermore, rules and regulations in China may change quickly with short advance notice, If the PRC imposes limitations on the ownership structure of the Company or disallows our current ownership structure all together in the future, or if the PRC government takes other future actions resulting in a material change in our operations, the value of our shares may depreciate significantly or become worthless.

There are significant legal and operational risks associated with being based in or having the substantial all of its operations in China, including those changes in the legal, political and economic policies of the Chinese government, the relations between China and the United States, or Chinese or U.S. regulations, all of which may materially and adversely affect our business, financial condition and results of operations. Any such changes could cause the value of our securities to significantly decline or become worthless. The PRC government has significant authority to exert influence on the ability of a company with substantive operations in China, such as us, to conduct its business, accept foreign investments or list on a U.S. or other foreign exchanges. For example, we face risks associated with regulatory approvals of offshore offerings, anti-monopoly regulatory actions, oversight on cybersecurity and data privacy. As of the date of this report, we do not believe that we are subject to (a) the cybersecurity review with the Cyberspace Administration of China, or CAC, as we do not qualify as a critical information infrastructure operator or possess a large amount of personal information in our business operations, and our business does not involve data possessing that affects or may affect national security, implicates cybersecurity, or involves any type of restricted industry; or (b) merger control review by China’s anti-monopoly enforcement agency due to the fact that we do not engage in monopolistic behaviors that are subject to these statements or regulatory actions. However, since these statements and regulatory actions are new, it is highly uncertain how soon legislative or administrative regulation making bodies will respond and what existing or new laws or regulations or detailed implementations and interpretations will be modified or promulgated, and, if any, the potential impact such modified or new laws and regulations will have on our daily business operation, ability to accept foreign investments and listing of our securities. In particular, as we are a holding company with substantive business operations in China, you should pay special attention to disclosures included in this annual report and risk factors included herein, including but not limited to risk factor such as “Risk Factors — Risks Relating to Our Corporate Structure” and “Risk Factors — Risks Related to Doing Business in China”.

The PRC government has significant oversight and discretion over the conduct of our business and may intervene with or influence our operations as the government deems appropriate to further regulatory, political and societal goals. The PRC government has recently published new policies that significantly affected certain industries, and we cannot rule out the possibility that it will in the future release regulations or policies regarding the industry where we operate, which could adversely affect our business, financial condition and results of operations. These risks could result in a material change in our operations and the value of our ordinary shares, or could significantly limit or completely hinder our ability to offer or continue to offer securities to investors and cause the value of such securities to significantly decline or become worthless. For more information on various risks related to doing business in China, see “Risk Factors — Risks Related to Doing Business in China”.

1

Pursuant to the Holding Foreign Companies Accountable Act, or the HFCAA, if the Public Company Accounting Oversight Board, or the PCAOB, is unable to inspect an issuer’s auditors for three consecutive years, the issuer’s securities are prohibited to trade on a U.S. stock exchange. The PCAOB issued a Determination Report on December 16, 2021 which found that the PCAOB is unable to inspect or investigate completely registered public accounting firms headquartered in: (1) mainland China of the People’s Republic of China because of a position taken by one or more authorities in mainland China; and (2) Hong Kong, a Special Administrative Region and dependency of the PRC, because of a position taken by one or more authorities in Hong Kong. Furthermore, the PCAOB’s report identified the specific registered public accounting firms which are subject to these determinations. On June 22, 2021, the U.S. Senate passed the Accelerating Holding Foreign Companies Accountable Act, and on December 29, 2022, legislation entitled “Consolidated Appropriations Act, 2023” (the “Consolidated Appropriations Act”) was signed into law by President Biden, which contained, among other things, an identical provision to the Accelerating Holding Foreign Companies Accountable Act and amended the HFCAA by requiring the SEC to prohibit an issuer’s securities from trading on any U.S stock exchanges if its auditor is not subject to PCAOB inspections for two consecutive years instead of three, thus reducing the time period for triggering the prohibition on trading. On August 26, 2022, the PCAOB announced that it had signed a Statement of Protocol (the “SOP”) with the China Securities Regulatory Commission, or the CSRC, and the Ministry of Finance of China. The SOP, together with two protocol agreements governing inspections and investigations (together, the “SOP Agreement”), establishes a specific, accountable framework to make possible complete inspections and investigations by the PCAOB of audit firms based in mainland China and Hong Kong, as required under U.S. law. On December 15, 2022, the PCAOB announced that it was able to secure complete access to inspect and investigate PCAOB-registered public accounting firms headquartered in mainland China and Hong Kong completely in 2022. The PCAOB Board vacated its previous 2021 determinations that the PCAOB was unable to inspect or investigate completely registered public accounting firms headquartered in mainland China and Hong Kong. However, whether the PCAOB will continue to be able to satisfactorily conduct inspections of PCAOB-registered public accounting firms headquartered in mainland China and Hong Kong is subject to uncertainties and depends on a number of factors out of our and our auditor’s control. The PCAOB continues to demand complete access in mainland China and Hong Kong moving forward and is making plans to resume regular inspections in early 2023 and beyond, as well as to continue pursuing ongoing investigations and initiate new investigations as needed. The PCAOB has also indicated that it will act immediately to consider the need to issue new determinations with the HFCAA if needed.

As of the date of this annual report, neither Audit Alliance LLP, our previous auditor, nor Enrome LLP, our current auditor, is not subject to the determinations as to inability to inspect or investigate completely as announced by the PCAOB on December 16, 2021. Each of Audit Alliance LLP and Enrome LLP is based in Singapore and is registered with PCAOB and subject to PCAOB inspection.

We are not an operating company based in the PRC, rather, we are a holding company incorporated in Delaware. Investors are purchasing securities of a Delaware holding company rather than securities of our subsidiaries that have substantive business operations in China. The Company is a Delaware holding company that conducts its operations and operates its business in China through (i) its subsidiaries incorporated in mainland China, and (ii) contractual agreements with a variable interest entity, namely, Shenzhen Tongdow Internet Technology Co., Ltd. (the “VIE” or “Tongdow Internet Technology”) based in mainland China. The VIE structure was established through a series of contractual agreements (collectively, the “Tongdow VIE Agreements”), comprising (i) that certain exclusive business cooperation agreement, entered into by and between the VIE and Shenzhen Baiyu Jucheng Data Technology Co., Ltd. (“Shenzhen Baiyu Jucheng”) dated as of October 17, 2022, (ii) that certain share pledge agreement, entered into by and among Shenzhen Baiyu Jucheng, Shanghai Zhuotaitong Industry Co., Ltd (“VIE Sole Original Shareholder”), and the VIE, dated as of October 17, 2022, (iii) that certain Exclusive Option Agreement entered into by and among Shenzhen Baiyu Jucheng, VIE Sole Original Shareholder, and the VIE, dated as of October 17, 2022, (iv) that certain Power of Attorney entered in to by VIE Sole Original Shareholder, dated as of October 17, 2022, and (v) that certain Timely Reporting Agreement entered into by and between the VIE and Shenzhen Baiyu Jucheng, dated as of October 17, 2022. The VIE structure is used to provide investors with exposure to foreign investment in China-based companies where the PRC law restricts direct foreign investment in certain operating companies. BAIYU does not own any equity interest in the VIE. Our contractual arrangements with the VIE are not equivalent of an investment in the equity interest of the VIE, and investors of BAIYU may never hold equity interests in the Chinese operating companies, including the VIE. Instead, we are regarded as the primary beneficiary of the VIE, for accounting purposes, based upon the Tongdow VIE Agreements.. Accordingly, under U.S. GAAP, the results of the VIE will be consolidated in our financial statements. Investors are purchasing the equity securities of BAIYU, the Delaware holding company, rather than the equity securities of the VIE. However, neither the investors in BAIYU nor BAIYU itself have an equity ownership in, direct foreign investment in, or control of, through such ownership or investment, the VIE.

2

The VIE structure involves unique risks to our investors. It may not provide effective operational control over the VIE and also faces risks and uncertainties associated with, among others, the interpretation and the application of the current and future PRC laws, regulations and rules to such contractual arrangements. As of the date of this annual report, the agreements under the contractual arrangements with respect to the VIE have not been tested in a court of law. If the PRC regulatory authorities find these contractual arrangements non-compliant with the restrictions on direct foreign investment in the relevant industries, or if the relevant PRC laws, regulations and rules or their interpretation change in the future, we could be subject to severe penalties or be forced to relinquish our interests in the VIE or forfeit our rights under the contractual arrangements. The PRC regulatory authorities could disallow the VIE structure at any time in the future, which would cause a material adverse change in our operations and cause the value of our securities you invested in this offering to significantly decline or become worthless.

The Chinese government may disallow the Company’s current holding structure, which could result in a material change in our operations and materially and adversely affect the value of shares of our common stock or our other securities and could cause the value of our shares or other securities to significantly decline or become worthless. Furthermore, the Chinese regulatory authorities may intervene in or influence the operation of PRC subsidiaries and exercise significant oversight and discretion over the conduct of their business or may exert more control over offerings conducted overseas by, and/or foreign investment in, China-based issuers, which could result in a material change in our operations and/or the value of our common stock. Further, rules and regulations in China may be changed from time to time, and any actions by the Chinese government to exert more oversight and supervision over offerings that are conducted overseas by, and/or foreign investment in, China-based issuers could significantly limit or completely hinder our ability to offer or continue to offer securities to investors and cause the value of such securities to significantly decline or be worthless.

Our Current Business

Commodities Trading Business

The Commodities Trading Business primarily involves purchasing non-ferrous metal products, such as aluminum ingots, copper, silver, and gold, from upstream metal and mineral suppliers and then selling to downstream customers. In connection with the Company’s commodity sales, in order to help customers to obtain sufficient funds to purchase various metal products and also help upstream metal and mineral suppliers to sell their metal products, the Company launched its Supply Chain Service Business in December 2019. The Company primarily generates revenues from bulk non-ferrous commodity products, and from providing related supply chain management services in the PRC.

In order to diversify the Company’s business, the Company has operated the Commodities Trading Business through Shenzhen Huamucheng Trading Co., Ltd. since November 2019, which was renamed as Shenzhen Baiyu Jucheng Data Technology Co., Ltd. (“Shenzhen Baiyu Jucheng”) in 2021. On November 22, 2019, Hao Limo Technology (Beijing) Co., Ltd. (“Hao Limo”), our indirectly wholly-owned subsidiary, entered into a series of agreements with Shenzhen Baiyu Jucheng and the shareholders of Shenzhen Baiyu Jucheng pursuant to which we obtained control of Shenzhen Baiyu Jucheng (the “Baiyu VIE Agreements”). We initially entered into certain agreements with the previous shareholders Shenzhen Baiyu Jucheng. On June 25, 2020, the Baiyu VIE Agreements were terminated and Shanghai Jianchi Supply Chain Co., Ltd., our wholly-owned subsidiary incorporated in China, acquired 100% equity interest of Shenzhen Baiyu Jucheng from the shareholders of Shenzhen Baiyu Jucheng for nominal consideration.

Through Shenzhen Baiyu Jucheng’s business, we source bulk commodity products from non-ferrous metals and mines or its designated distributors and then sell to manufacturers who need these metals in large quantities. We also work with upstream suppliers in the sourcing of commodities.

Through Shenzhen Qianhai Baiyu Supply Chain Co., Ltd. (“Qianhai Baiyu”), our wholly-owned subsidiary incorporated in China, we provide supply chain management services to our customers. On October 26, 2020, Shenzhen Baiyu Jucheng entered into certain share purchase agreements to acquire 100% shares of Qianhai Baiyu. Qianhai Baiyu is engaged in the supply chain service business and covers a full range of commodities, including non-ferrous metals, ferrous metals, coal, metallurgical raw materials, soybean oils, oils, rubber, wood and various other types of commodities. It also has a supply chain infrastructure, which includes processing, logistics, warehousing and terminals. Utilizing its customer base, industry experience, and expertise in the commodity trading industry, Qianhai Baiyu serves as a one-stop commodity supply chain service and digital intelligence supply chain platform integrating upstream and downstream enterprises, warehouses, logistics, information, and futures trading.

3

The acquisition of Qianhai Baiyu has laid a solid foundation for the Company to further expand its operations in the commodity supply chain field. The Company plans to strengthen and upgrade its supply chain services platform by introducing a systematic quantitative risk control system, which will be based on the Qianhai Baiyu’s massive historical market data and complex data analysis models. The platform is expected to establish a quantitative risk management system utilizing ETL data integration (Extract, Transform, Load) as its core, and then optimize trading portfolios by incorporating various factors and strategies in order to effectively control risks and sustain business development.

For the fiscal year ended December 31, 2023, the Company generated revenue of $134,558,086 from its commodities trading business and $67,981 from its supply chain management services.

VIE Agreements

We have operated the Commodities Trading Business through Shenzhen Huamucheng Trading Co., Ltd. since November 2019, which was renamed as Shenzhen Baiyu Jucheng Data Technology Co., Ltd. (“Shenzhen Baiyu Jucheng”) in 2021. On November 22, 2019, Hao Limo Technology (Beijing) Co., Ltd. (“Hao Limo”), our previously indirectly wholly-owned subsidiary, entered into the Baiyu VIE Agreements. On June 25, 2020, Hao Limo and Shenzhen Baiyu Jucheng entered into certain VIE termination agreements to terminate the Baiyu VIE Agreements. As a result of the termination of the Baiyu VIE Agreements, Hao Limo no longer has the control rights and rights to the assets, property and revenue of Shenzhen Baiyu Jucheng. At the same time, Shanghai Jianchi Supply Chain Co., Ltd., our wholly-owned subsidiary incorporated in China, acquired 100% equity interest of Shenzhen Baiyu Jucheng from the shareholders of Shenzhen Baiyu Jucheng for nominal consideration.

On October 17, 2022, Shenzhen Baiyu Jucheng entered into the Tongdow VIE Agreements, comprising (i) that certain exclusive business cooperation agreement, entered into by and between the VIE and Shenzhen Baiyu Jucheng dated as of October 17, 2022 (the “Exclusive Business Cooperation Agreement”), (ii) that certain share pledge agreement, entered into by and among Shenzhen Baiyu Jucheng, Shanghai Zhuotaitong Industry Co., Ltd (“VIE Sole Original Shareholder”), and the VIE, dated as of October 17, 2022 (the “Share Pledge Agreement”), (iii) that certain Exclusive Option Agreement entered into by and among Shenzhen Baiyu Jucheng, VIE Sole Original Shareholder, and the VIE, dated as of October 17, 2022 (the “Exclusive Option Agreement”), (iv) that certain Power of Attorney entered in to by VIE Sole Original Shareholder, dated as of October 17, 2022 (the “POA”), and (v) that certain Timely Reporting Agreement entered into by and between the VIE and Shenzhen Baiyu Jucheng, dated as of October 17, 2022 (the “Reporting Agreement”).

The Tongdow VIE Agreements allow us to (1) be considered as the primary beneficiary of the VIE for accounting purposes and consolidate the financial results of the VIE, (2) receive substantially all of the economic benefits of the VIE, (3) have the pledge right over the equity interests in the VIE as the pledgee, and (4) have an exclusive option to purchase all or part of the equity interests in the VIE when and to the extent permitted by PRC law.

As a result of our direct ownership in Shenzhen Baiyu Jucheng and the contractual arrangements with the VIE, we have become the primary beneficiary of the VIE for accounting purposes, and, therefore, have consolidated the financial results of the VIE in our consolidated financial statements in accordance with U.S. GAAP.

The following is a summary of the Tongdow VIE Agreements:

Exclusive Business Cooperation Agreement. Pursuant to the terms thereof, Shenzhen Baiyu Jucheng agrees to provide the VIE with customer support, business support and related supply chain management services during the term of the agreement and the VIE agrees not to engage any other party for the same or similar consultation and/or management services without Shenzhen Baiyu Jucheng’s prior consent. The VIE agrees to pay Shenzhen Baiyu Jucheng service fees substantially equal to all of its net income, subject to any requirement by PRC law and its articles of association.

4

Share Pledge Agreement. Pursuant to the terms thereof, VIE Sole Original Shareholder pledged all of its equity interest in the VIE to Shenzhen Baiyu Jucheng in order to guarantee the performance of the VIE’s obligations under the Exclusive Business Cooperation Agreement. The agreement will be terminated upon full payment of consulting and service fees and termination of the VIE’s contractual obligations under the Exclusive Business Cooperation Agreement.

Exclusive Option Agreement. Pursuant to the terms thereof, VIE Sole Original Shareholder has irrevocably granted Shenzhen Baiyu Jucheng an exclusive option to purchase at any time, in part or in whole, its equity interests in the VIE for a purchase price equal to the capital paid by VIE Sole Original Shareholder, adjusted pro rata for purchase of less than all of the equity interests.

Powers of Attorney. Pursuant to the terms thereof, VIE Sole Original Shareholder has irrevocably authorized Shenzhen Baiyu Jucheng to act on its behalf as the exclusive agent and attorney with respect to all rights as a shareholder, including but not limited to, (1) convening, attending and presiding over shareholders’ meetings, (2) exercising all the shareholder’s rights, including voting, that shareholders are entitled to under PRC law and the Articles of Association of the VIE, including but not limited to the sale, transfer, pledge or disposition of the equity interests of the VIE owned by such shareholder in part or in whole, (3) designating and appointing on behalf of the shareholders the legal representative, executive director, supervisor, chief executive officer and other senior management members of the VIE, (4) signing and executing all legal documents related to the shareholder’s rights, and (5) receiving the dividends paid by the VIE to its shareholder.

Reporting Agreement. Pursuant to the terms thereof, the VIE agrees to promptly provide all information required by Shenzhen Baiyu Jucheng so that it can make necessary SEC and other regulatory reports in a timely fashion.

In the opinion of our PRC counsel, Tahota (Beijing) Law Firm, (i) the ownership structures of the VIE and Shenzhen Baiyu Jucheng are not in any violation of applicable PRC laws and regulations currently in effect; and (ii) the contractual arrangements between Shenzhen Baiyu Jucheng, the VIE and its shareholder governed by PRC laws and regulations are currently valid, binding and enforceable and will not result in any violation of applicable PRC laws and regulations currently in effect.

However, we have been advised by our PRC counsel, Tahota (Beijing) Law Firm, that there are substantial uncertainties regarding the interpretation and application of current PRC laws and regulations. The PRC government may ultimately take a view contrary to or otherwise different from the opinion of our PRC counsel. As of the date of this report, the agreements under the contractual arrangements among Shenzhen Baiyu Jucheng, the VIE, and its shareholder have not been tested in a court of law. Investors in our securities are not purchasing equity interest in the VIE in China but, instead, are purchasing equity interest in a holding company incorporated in the laws of State of Delaware. The contractual arrangements may be less effective from direct ownership in providing us with control over the VIE and we may incur substantial costs to enforce the terms of the arrangements. Our corporate structure is subject to risks associated with our contractual arrangements with the VIE. It is uncertain whether any new PRC laws or regulations relating to variable interest entity structures will be adopted or if adopted, what they would provide. If we or the VIE is found to be in violation of any existing or future PRC laws or regulations, or fail to obtain or maintain any of the required permits or approvals, the relevant PRC regulatory authorities would have broad discretion to take action in dealing with such violations or failures. We could be subject to severe penalties or be forced to relinquish our interests in those operations. Our Delaware holding company, Shenzhen Baiyu Jucheng, and the VIE, and investors in securities in BAIYU face uncertainty with respect to potential future actions by the PRC government that could affect the enforceability of the contractual arrangements with the VIE and, consequently, significantly affect the financial performance of our company as a whole and the VIE. See “Risk Factors — Risks Related to Doing Business in China — The contractual arrangements with the VIE and its shareholder may be less effective than direct ownership in providing operational control” and “— We face uncertainty with respect to the enforceability of the contractual arrangements with the VIE and its shareholder, and any failure by the VIE or its shareholder to perform their obligations under our contractual arrangements with them would have a material adverse effect on our business.”

5

Convertible Promissory Notes Issuance and Settlement

On May 6, 2022, the Company entered into a securities purchase agreement with Streeterville Capital, LLC, pursuant to which the Company issued the investor a convertible promissory note in the original principal amount of $3,320,000, convertible into shares of the Company’s common stock, for $3,000,000 in gross proceeds. By written consent dated May 10, 2022, as permitted by Section 228 of the Delaware General Corporation Law and Section 8 of Article II of our bylaws, the stockholders who have the authority to vote a majority of the outstanding shares of Common Stock approved the following corporate actions: (i) the entry into a purchase agreement dated of May 6, 2022 by and between the Company and the investor, pursuant to which the Company issued the note dated of May 6, 2022 to the investor; and (ii) the issuance of shares of common stock in excess of 19.99% of the currently issued and outstanding shares of common stock of the Company upon the conversion of the note. The Company settled a convertible promissory note of $375,000 on November 16, 2022, $200,000 on January 18, 2023, $200,000 on February 3, 2023, $175,000 on February 8, 2023, $250,000 on February 15, 2023, $250,000 on March 8, 2023, $125,000 on March 24, 2023, $150,000 on September 14, 2023, $200,000 on November 7, 2023, and $175,000 on November 8, 2023, respectively, and issued 445,749, 235,960, 234,389, 205,090, 292,987, 279,567, 145,660, 1,153,846, 131,585 and 115,137 shares of the Company’s Common Stock on November 17, 2022, January 19, 2023, February 6, 2023, February 8, 2023, February 15, 2023, March 15, 2023, March 29, 2023, September 15, 2023, November 7, 2023, and November 8, 2023, respectively.

The above unsettled convertible promissory note, issued on May 6, 2022, has a maturity date of 12 months with an interest rate of 10% per annum. The Company retains the right to prepay the note at any time prior to conversion with an amount in cash equal to 125% of the principal that the Company elects to prepay at any time six months after the issue date, subject to maximum monthly redemption amount of $250,000 and $375,000, respectively. On or before the close of business on the third trading day of redemption, the Company should deliver conversion shares via “DWAC” (DTC’s Deposit/Withdrawal at Custodian system). The Company will be required to pay the redemption amount in cash, or chooses to satisfy a redemption in registered stock or unregistered stock, such stock shall be issued at 80% of the average of the lowest “VWAP” (the volume-weighted average price of the Common Stock on the principal market for a particular trading day or set of trading days) during the fifteen trading days immediately preceding the redemption notice is delivered.

On March 13, 2023, the Company entered into a securities purchase agreement with Streeterville and issued a convertible note due 2024 (the “Note”) to Streeterville. The Note has a principal amount of $3,320,000 (the “Principal”) and bears an interest rate that equals to ten percent (10%) per annum. The purchase price for the Note is $3,000,000 (the “Purchase Price”), and the date on which the Purchase Price is delivered by Streeterville Capital to the Company, (the “Purchase Price Date”). The Principal and the interest payable under the Note will become due and payable twelve (12) months from the Purchase Price Date (the “Maturity Date”), unless earlier converted or prepaid by us. The Note has a conversion price (the “Redemption Conversion Price”) equal to eighty percent (80%) multiplied by the lowest VWAP (the dollar volume-weighted average price for shares of our common stock on the Nasdaq Capital Market) during the fifteen (15) trading days immediately preceding the date a redemption notice is delivered (the “Redemption Date”). In this report, the company refers to all shares issued by us pursuant to conversion of the Note as “Conversion Shares.” The Investor has the right to redeem the Note at any time beginning on the date that is ninety (90) days from the Purchase Price Date until the outstanding balance has been paid in full, subject to the maximum monthly redemption amount of $375,000 (the “Maximum Monthly Redemption Amount”). Redemptions may be satisfied in cash, common stock at the Redemption Conversion Price, or any combination of the foregoing. We have the right, but not the obligation, to prepay all or any portion of the outstanding balance under this Note prior to the Maturity Date at a cash prepayment price equal to 125% of the outstanding balance to be prepaid. The Company settled the Note of $300,000 on September 7, 2023, $2000,000 on October 10, 2023, $175,000 on October 13, 2023, $150,000 on November 16, 2023, $150,000 on December 5, 2023, and $150,000 on December 29, 2023, respectively, and issued 2,091,466, 2,086,811, 1,845,991, 109,075, 109,075 and 137,644 shares of the Company’s common stock on September 7, 2023, October 10, 2023, October 13, 2023, November 16, 2023, December 5, 2023, December 29, 2023, respectively.

6

Reverse Stock Split of Common Stock, Change of Company Name, Ticker Change, and Amendment to Certificate of Incorporation

On May 15, 2023, the Company received a letter from NASDAQ Stock Market LLC (“Nasdaq”) stating that the Company was not in compliance with the Nasdaq Listing Rule 5550(a)(2) (the “Minimum Bid Price Requirement”) because the closing bid price for the Company’s common stock had remained below $1.00 per share for the previous 30 consecutive business days. An initial grace period to regain compliance was provided, which ended on November 11, 2023.

To achieve compliance with the Minimum Bid Price Requirements, the Company proposed a stock reverse split.

On September 15, 2023, our board of directors unanimously approved the amendments to the Company’s Certificate of Incorporation (as amended) to effect (i) a reverse stock split of our issued and outstanding common stock to comply with Nasdaq’s Minimum Bid Price Requirements, at a ratio of one-for-twenty to one-for-fifty immediately following the reverse split, with the exact ratio to be set at a whole number within this range, and (ii) change the Company’s name to BAIYU Holdings, Inc (the “Name Change”). On September 18, 2023, by written consent of stockholders in lieu of special meeting, the company’s stockholders who have the authority to vote a majority of the outstanding shares have approved and adopted the filing of certificate of amendment of certificate of incorporation to effect, among other things, (i) a reverse stock split of our common stock at a reverse stock split ratio of no less than one-for-twenty to no more than one-for-fifty, with the final decision of whether to proceed with the reverse stock split and the exact ratio and timing of the reverse split to be determined by our board of directors (“Board of Directors”), in its discretion, and (ii) the Name Change, with the final decision of whether to proceed with the Name Change and the timing for implementing the Name Change to be determined by our Board of Directors. On October 16, 2023, our Board of Directors unanimously approved, among other things, (x) the filing of the certificate of amendment of certificate of incorporation to effect the reverse stock split at the ratio of one-for-fifty(the “Reverse Stock Split”) and the Name Change, and (y) the change of our ticker on the Nasdaq to “BYU”. Subsequently, on October 19, 2023, we filed a Certificate of Amendment of Certificate of Incorporation with the Delaware Secretary of State to effect the Reverse Stock Split and the Name Change. The Company’s common stock began trading on Nasdaq on a Reverse Stock Split-adjusted basis under the new name “BAIYU Holdings, Inc” and the new ticker symbol “BYU” on October 30, 2023. As a result of the Reverse Stock Split, every fifty shares of the Company’s common stock issued and outstanding were automatically reclassified into one new share of common stock, without modifying any rights or preferences of the shares of the Company’s common stock.

On November 13, 2023, the Company received a notification letter from Nasdaq informing it that compliance with the Minimum Bid Price Requirement had been regained, and the matter was closed.

November 2023 Private Placement

On November 16, 2023, the Company entered into that certain securities purchase agreement with certain purchasers who are “non-U.S. Persons” as defined in Regulation S as promulgated under the Securities Act of 1933, as amended, pursuant to which the Company agreed to sell an aggregate of 15,000,000 shares of Common Stock, par value $0.001 per share at a per share purchase price of $2.09 (representing the number equal to (i) the average Nasdaq Official Closing Price of the Company’s Common Stock (as reflected on Nasdaq.com) for the five trading days immediately preceding the date of the securities purchase agreement, times (ii) 1.1) (the “Common Stock PIPE”). The transaction was consummated on November 29, 2023 by the issuance of 15,000,000 shares of common stock.

July 2023 Private Placement

On July 31, 2023, the Company entered into a securities purchase agreement with certain purchasers who are “non-U.S. Persons” as defined in Regulation S as promulgated under the Securities Act of 1933, as amended, pursuant to which, the Company agreed to sell such Purchasers an aggregate of 28,000,000 shares of its common stock, par value $0.001 per share at a price of $0.35 per share to the purchasers for gross proceeds of approximately $9.8 million. The offering is being made pursuant to the Company’s shelf registration statement on Form S-3 (File No. 333-239757), which was filed with the Securities and Exchange Commission on July 8, 2020, and declared effective by on August 4, 2020, as supplemented by the prospectus supplement dated August 3, 2023, relating to the sale of the shares thereof.

January 2023 Private Placement

On January 9, 2023, the Company entered into that certain Securities Purchase Agreement with Ms. Huiwen Hu, an affiliate of the Company, and certain other purchasers who are “non-U.S. Persons” (as defined in Regulation S of the Securities Act of 1933, as amended, pursuant to which the Company agreed to sell an aggregate of 35,000,000 shares of its common stock, par value $0.001 per share, at a per share purchase price of $1.21. The gross proceeds to the Company were $42.35 million. Since Ms. Huiwen Hu is an affiliate of the Company, the transaction has been approved by the Audit Committee of the Board of Directors of the Company as well as the Board of Directors of the Company.

7

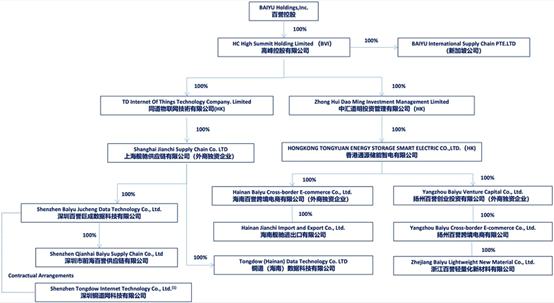

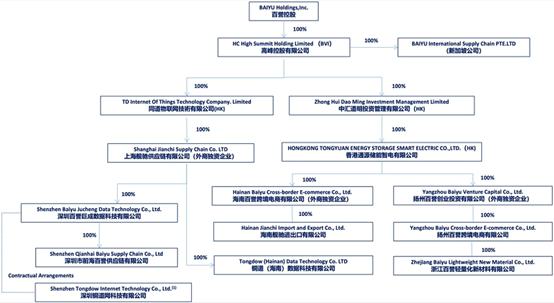

Corporate Structure

BAIYU Holdings, Inc. is a holding company that was incorporated under the laws of the State of Delaware on December 19, 2011. HC High Summit Holding Limited (“HC High BVI”), a company incorporated under the laws of the British Virgin Islands on May 22, 2018, is wholly owned by the Company. On April 2, 2020, HC High BVI established TD Internet Of Things Technology Company Limited (“TD Internet Of Things Technology”, formerly known as Tongdow Block Chain Information Technology Company Limited), a holding company incorporated in accordance with the laws and regulations of Hong Kong. TD Internet Of Things Technology is wholly owned by HC High BVI. On April 2, 2020 and July 16, 2020, Tongdow Block Chain established Shanghai Jianchi and Tongdow (Hainan) Data Technology Co., Ltd. (“Tondow Hainan”), respectively, as its wholly-owned subsidiaries. Both Shanghai Jianchi and Tongdow Hainan are holding companies incorporated in accordance with the laws and regulations of the People’s Republic of China (“PRC”).

On March 5, 2020, the Company filed a Certificate of Amendment of the Certificate of Incorporation with the Delaware Secretary of State to effect a name change from Bat Group, Inc. to TD Holdings, Inc. (the “March Charter Amendment”). The March Charter Amendment became effective on March 6, 2020.

On June 25, 2020, Hao Limo, the Company’s wholly-owned subsidiary incorporated in the PRC, and Huamucheng, which was renamed Shenzhen Baiyu Jucheng in 2021, a former VIE of the Company, entered into certain VIE termination agreements to terminate the Shenzhen Baiyu Jucheng VIE agreements. On the same date, Shanghai Jianchi, Shenzhen Baiyu Jucheng and Shenzhen Baiyu Jucheng Shareholders entered into certain share acquisition agreements pursuant to which Shanghai Jianchi acquired 100% equity interest of Shenzhen Baiyu Jucheng. As a result, Shenzhen Baiyu Jucheng transitioned from a variable interest entity controlled by the Company into a wholly owned subsidiary of the Company.

On September 11, 2020, the Company acquired Zhong Hui Dao Ming Investment Management Limited (“ZHDM HK”) and its wholly owned subsidiary, Tongdow E-Trading Limited (“Tongdow HK”). Both entities were holding companies incorporated in accordance with the laws and regulations of Hong Kong.

On October 26, 2020, Shenzhen Baiyu Jucheng entered into a certain share purchase agreement to acquire 100% shares of Qianhai Baiyu. The acquisition of Qianhai Baiyu has laid a solid foundation for the Company to further expand its operations in the commodity supply chain field.

On April 20, 2021, the Company effected a Certificate of Amendment of the Certificate of Incorporation (the “April Charter Amendment”) with the Delaware Secretary of State to increase the number of authorized shares of its common stock, par value $0.001 per share, from 100,000,000 shares to 600,000,000 shares and the number of authorized shares of its preferred stock, par value $0.001 per share, from 10,000,000 shares to 50,000,000 shares. The April Charter Amendment was approved by the Company’s Board of Directors on March 9, 2021, and by shareholders holding a majority of the Company’s issued and outstanding capital stock on March 10, 2021. The April Charter Amendment does not affect the rights of the Company’s shareholders.

On August 11, 2022, the Company has filed a Certificate of Amendment of the Certificate of Incorporation with the Delaware Secretary of State to effect a reverse stock split.

On October 17, 2022, Shenzhen Baiyu Jucheng, entered into a set of variable interest entity agreements with Shenzhen Tongdow Internet Technology and Shanghai Zhuotaitong Industry Co., Ltd., the sole shareholder of Tongdow Internet Technology. On October 25, 2022, the parties completed the transaction. The contractual arrangements allow us to (1) be considered as the primary beneficiary of the VIE for accounting purposes and consolidate the financial results of the VIE, (2) receive substantially all of the economic benefits of the VIE, (3) have the pledge right over the equity interests in the VIE as the pledgee, and (4) have an exclusive option to purchase all or part of the equity interests in the VIE when and to the extent permitted by PRC law.

On October 19, 2023, the Company has filed a Certificate of Amendment of the Certificate of Incorporation with the Delaware Secretary of State to effect, among other things, the Reverse Stock Split and the Name Change. See section entitled “Reverse Stock Split of Common Stock, Change of Company Name, Ticker Change, and Amendment to Certificate of Incorporation” above.

8

BAIYU Holdings, Inc. is not an operating company based in the PRC, but a holding company incorporated in Delaware. Our operations are primarily conducted through (i) our subsidiaries incorporated in mainland China, and (ii) contractual agreements with a variable interest entity, namely, Tongdow Internet Technology based in mainland China. The VIE structure was established through a series of contractual agreements, comprising (i) that certain exclusive business cooperation agreement, entered into by and between the VIE and Shenzhen Baiyu Jucheng Data Technology Co., Ltd. (“Shenzhen Baiyu Jucheng”) dated as of October 17, 2022, (ii) that certain share pledge agreement, entered into by and among Shenzhen Baiyu Jucheng, Shanghai Zhuotaitong Industry Co., Ltd (“VIE Sole Original Shareholder”), and the VIE, dated as of October 17, 2022, (iii) that certain Exclusive Option Agreement entered into by and among Shenzhen Baiyu Jucheng, VIE Sole Original Shareholder, and the VIE, dated as of October 17, 2022, (iv) that certain Power of Attorney entered in to by VIE Sole Original Shareholder, dated as of October 17, 2022, and (v) that certain Timely Reporting Agreement entered into by and between the VIE and Shenzhen Baiyu Jucheng, dated as of October 17, 2022. See “Our Current Business — VIE Agreements” for details.

The contractual arrangements allow us to (1) be considered as the primary beneficiary of the VIE for accounting purposes and consolidate the financial results of the VIE, (2) receive substantially all of the economic benefits of the VIE, (3) have the pledge right over the equity interests in the VIE as the pledgee, and (4) have an exclusive option to purchase all or part of the equity interests in the VIE when and to the extent permitted by PRC law.

However, these contractual agreements may be less effective than direct ownership in providing us with control over the VIE, and we may incur significant costs to enforce the terms of these agreements. For instance, the VIE and its shareholder could breach their contractual arrangements with us by, among other things, failing to conduct the operations of the VIE in an acceptable manner or taking other actions that are detrimental to our interests. If we had direct ownership of the VIE in China, we would be able to exercise our rights as a shareholder to effect changes in the board of directors of the VIE, which in turn could implement changes, subject to any applicable fiduciary obligations, at the management and operational level. However, under the current contractual arrangements, we rely on the performance by the VIE and its shareholder of their obligations under the contracts to direct the VIE’s activities. The shareholder of the VIE may not act in the best interests of our company or may not perform its obligations under these contracts. If any dispute relating to these contracts remains unresolved, we will have to enforce our rights under these contracts through the operations of PRC law and arbitration, litigation and other legal proceedings and therefore will be subject to uncertainties in the PRC legal system. See “Risk Factors — Risks Related to Doing Business in China — The contractual arrangements with the VIE and its shareholder may be less effective than direct ownership in providing operational control.”

The VIE structure is not equivalent to an investment in the equity interest of such entities. BAIYU does not own any equity interests in the VIE. Our contractual arrangements with the VIE and its nominee shareholder are not equivalent to an investment in the equity interest of the VIE. Investors are purchasing securities in BAIYU, the Delaware holding company, and are not purchasing, and may never hold, equity interest in the VIE. Such corporate structure involves unique risks associated with our contractual arrangements with the VIE. As of the date of this report, the agreements under the contractual arrangements with respect to the VIE have not been tested in a court of law. It is uncertain whether any new PRC laws or regulations relating to variable interest entity structures will be adopted or if adopted, what they would provide. Our Delaware holding company, our subsidiaries incorporated in mainland China and the VIE, and investors in securities of BAIYU face uncertainty with respect to potential future actions by the PRC government that could affect the enforceability of the contractual arrangements with the VIE and, consequently, significantly affect the financial performance of our company as a whole and the VIE. In addition, all the agreements under our contractual arrangements with the VIE are governed by PRC law and provide for the resolution of disputes through arbitration in China. However, uncertainties in the PRC legal system could limit our ability to enforce these contractual arrangements. Meanwhile, there are very few precedents and little formal guidance as to how contractual arrangements in the context of a consolidated variable interest entity should be interpreted or enforced under PRC law. There remain significant uncertainties regarding the ultimate outcome of such arbitration should legal action become necessary. In the event we are unable to enforce these contractual arrangements, or if we suffer significant delay or other obstacles in the process of enforcing these contractual arrangements, we may not be able to exert effective contractual control over the VIE, and our ability to conduct our business may be negatively affected. See “Risk Factors — Risks Related to Doing Business in China — We face uncertainty with respect to the enforceability of the contractual arrangements with the VIE and its shareholder, and any failure by the VIE or its shareholder to perform their obligations under our contractual arrangements with them would have a material adverse effect on our business.”

9

The following diagram illustrates our corporate structure as of the date of this annual report:

| (1) | a variable interest entity. |

Summary Consolidated Financial Data

The following are historical statements of operations and statements of cash flows for the fiscal years ended December 31, 2022, and December 31, 2023, and balance sheet data as of December 31, 2022 and December 31, 2023, which have been derived from our audited financial statements for those periods. Our historical results are not necessarily indicative of the results that may be expected in the future. You should read this data together with our consolidated financial statements and related notes appearing elsewhere in this report. Solely for the purposes of this summary, (i) “Parent” refers to BAIYU Holdings, Inc.; (ii) “WFOE and its subsidiary” refers to Shenzhen Baiyu Jucheng Data Technology Co., Ltd. and its subsidiary Shenzhen Qianhai Baiyu Supply Chain Co., Ltd.; (iii) “VIE” refers to Shenzhen Tongdow Internet Technology Co., Ltd.; and (iv) “Other Subsidiaries” refers to all subsidiaries of BAIYU (other than WFOE and its subsidiary and VIE).

10

Selected Condensed Consolidation Balance Sheets

| As of December 31, 2022 | ||||||||||||||||||||||||

| Parent | WFOE and its subsidiary | VIE | Other Subsidiaries | Elimination Entries and Reclassification Entries | Consolidated | |||||||||||||||||||

| Cash | $ | 391,660 | $ | 392,627 | $ | 777 | $ | 107,993 | $ | - | $ | 893,057 | ||||||||||||

| Intercompany receivable | 291,834,086 | 72,031,748 | - | 72,054,524 | (435,920,358 | ) | - | |||||||||||||||||

| Total Current Assets | 292,299,062 | 218,976,607 | 1,806 | 73,205,406 | (435,916,556 | ) | 148,566,325 | |||||||||||||||||

| Total Non-current Assets | 410,000 | 189,712,925 | 38,408,523 | 18,179,851 | (32,179,826 | ) | 214,531,473 | |||||||||||||||||

| Intercompany payable | - | 361,819,711 | 3,249,921 | 70,850,726 | (435,920,358 | ) | - | |||||||||||||||||

| Total Liabilities | 4,238,152 | 376,465,664 | 42,024,382 | 73,481,743 | (431,086,312 | ) | 65,123,629 | |||||||||||||||||

| Total Shareholders’ Equity | 288,470,910 | 32,223,868 | (3,614,053 | ) | 17,903,514 | (37,010,070 | ) | 297,974,169 | ||||||||||||||||

| As of December 31, 2023 | ||||||||||||||||||||||||

| Parent | WOFE and WOFE’s Subsidiary | VIE and VIE’s Subsidiary | Other Subsidiaries | Elimination Entries and Reclassification Entries | Consolidated | |||||||||||||||||||

| Cash | $ | 1,080,145 | $ | 145,105 | $ | 2,396 | $ | 288,712 | $ | - | $ | 1,516,358 | ||||||||||||

| Intercompany receivable | 375,855,716 | 96,510,811 | 25,415 | 32,842,956 | (505,234,898 | ) | 0 | |||||||||||||||||

| Total Current Assets | 377,977,860 | 343,920,024 | 28,124 | 35,646,943 | (505,231,093 | ) | 252,341,858 | |||||||||||||||||

| Total Non-current Assets | 410,000 | 186,484,801 | 33,532,410 | 18,298,729 | (35,782,777 | ) | 202,943,163 | |||||||||||||||||

| Intercompany payable | 0 | 469,738,028 | 3,393,550 | 32,004,086 | (505,135,664 | ) | 0 | |||||||||||||||||

| Total Liabilities | 4,292,512 | 491,057,639 | 41,510,542 | 36,383,900 | (501,104,877 | ) | 72,139,716 | |||||||||||||||||

| Total Shareholders’ Equity | 374,095,348 | 39,347,186 | (7,950,008 | ) | 17,561,772 | (39,908,993 | ) | 383,145,305 | ||||||||||||||||

11

Selected Condensed Consolidated Statements of Operations Data

| For the fiscal year ended December 31, 2022 | ||||||||||||||||||||||||

| Parent Only | WFOE and its subsidiary | VIE | Other Subsidiaries | Eliminating adjustments | Consolidated | |||||||||||||||||||

| Revenue | $ | - | $ | 32,171,691 | $ | - | $ | 124,663,610 | $ | - | $ | 156,835,301 | ||||||||||||

| Intercompany revenue | - | - | - | - | - | |||||||||||||||||||

| Cost of revenue and related tax | - | 31,336,404 | - | 124,460,640 | - | 155,797,044 | ||||||||||||||||||

| Cost from intercompany | - | - | - | - | - | |||||||||||||||||||

| Gross Profit | - | 835,287 | - | 202,970 | - | 1,038,257 | ||||||||||||||||||

| Total operating expenses | 1,654,555 | 1,407,523 | 776,138 | 1,305,773 | 3,744,750 | 8,888,739 | ||||||||||||||||||

| Operating Income (expense) | (1,654,555 | ) | (572,236 | ) | (776,138 | ) | (1,102,803 | ) | (3,744,750 | ) | (7,850,482 | ) | ||||||||||||

| Net Income(expense) | (3,332,404 | ) | 8,271,574 | (775,970 | ) | (2,862,299 | ) | 2,952,636 | 4,253,537 | |||||||||||||||

| For the year ended December 31, 2023 | ||||||||||||||||||||||||

| Parent Only | WOFE and WOFE’s Subsidiary | VIE and VIE’s Subsidiary | Other Subsidiaries | Elimination Entries and Reclassification Entries | Consolidated | |||||||||||||||||||

| Revenue | $ | - | $ | 19,159,124 | $ | 1,351 | $ | 115,465,592 | $ | - | $ | 134,626,067 | ||||||||||||

| Intercompany revenue | - | - | - | - | - | |||||||||||||||||||

| Cost of revenue and related tax | - | 19,294,710 | - | 115,520,831 | - | 134,815,541 | ||||||||||||||||||

| Cost from intercompany | - | - | - | - | - | |||||||||||||||||||

| Gross Profit | - | (135,586 | ) | 1,351 | (55,239 | ) | - | (189,474 | ) | |||||||||||||||

| Total operating expenses | 7,478,472 | 793,101 | 4,420,038 | 875,775 | 3,024,302 | 16,591,688 | ||||||||||||||||||

| Operating Income (expense) | (7,478,472 | ) | (928,687 | ) | (4,418,687 | ) | (931,014 | ) | (3,024,302 | ) | (16,781,162 | ) | ||||||||||||

| Net Income(expense) | (8,972,849 | ) | 14,310,543 | (4,418,675 | ) | (917,117 | ) | (2,268,227 | ) | (2,266,325 | ) | |||||||||||||

12

Selected Condensed Consolidated Statements of Cash Flows

| For the fiscal year ended December 31, 2022 | ||||||||||||||||||||||||

| Parent | WFOE and its subsidiary | VIE | Other Subsidiaries | Eliminating adjustments | Consolidated | |||||||||||||||||||

| OPERATING ACTIVITIES | ||||||||||||||||||||||||

| Net income (Loss) | $ | (3,332,404 | ) | $ | 8,271,574 | $ | (775,970 | ) | $ | (2,862,299 | ) | $ | 2,952,636 | $ | 4,253,537 | |||||||||

| Intercompany receive | - | - | - | - | - | - | ||||||||||||||||||

| Intercompany payment | - | - | - | - | - | - | ||||||||||||||||||

| Net cash provided by (used in) operating activities | (117,310,991 | ) | 144,785,800 | 94 | (22,548,042 | ) | (591,502 | ) | 4,335,359 | |||||||||||||||

| Net cash provided by (used in) investing activities | - | (147,366,777 | ) | - | 21,829,031 | - | (125,537,746 | ) | ||||||||||||||||

| Net cash provided (used in) financing activities | 117,420,000 | (29,735 | ) | - | - | - | 117,390,265 | |||||||||||||||||

| Intercompany receive | - | - | - | - | - | - | ||||||||||||||||||

| Intercompany payment | - | - | - | - | - | - | ||||||||||||||||||

| Effect of exchange rate fluctuation on cash | 394,111 | - | - | - | - | 394,111 | ||||||||||||||||||

| For the year ended December 31, 2023 | ||||||||||||||||||||||||

| Parent Only | WOFE and WOFE’s Subsidiary | VIE and VIE’s Subsidiary | Other Subsidiaries | Eliminating adjustments | Consolidated | |||||||||||||||||||

| OPERATING ACTIVITIES | ||||||||||||||||||||||||

| Net income (Loss) | $ | (8,972,849 | ) | $ | 14,310,543 | $ | (4,418,675 | ) | $ | (917,117 | ) | $ | (2,268,227 | ) | $ | (2,266,325 | ) | |||||||

| Intercompany receive | - | - | - | - | - | - | ||||||||||||||||||

| Intercompany payment | - | - | - | - | - | - | ||||||||||||||||||

| Net cash provided by (used in) operating activities | (92,058,589 | ) | 99,875,335 | 1,640 | 87,614 | 1,641,516 | 9,547,516 | |||||||||||||||||

| Net cash provided by (used in) investing activities | 0 | (100,187,219 | ) | 0 | 94,170 | 6,350 | (100,086,699 | ) | ||||||||||||||||

| Net cash provided (used in) financing activities | 92,747,073 | 69,678 | 0 | 0 | 92,816,751 | |||||||||||||||||||

| Intercompany receive | - | - | - | - | - | - | ||||||||||||||||||

| Intercompany payment | - | - | - | - | - | - | ||||||||||||||||||

| Effect of exchange rate fluctuation on cash | (1,654,267 | ) | - | 0 | - | - | (1,654,267 | ) | ||||||||||||||||

13

Cash Transfer and Dividend Payment

BAIYU Holdings, Inc., our holding company, or the Parent, may transfer cash to our offshore intermediary holding entities in the British Virgin Islands and Hong Kong and their respective subsidiaries, through capital injections and intra-group loans. Our offshore intermediary holding entities, in turn, may transfer cash to our PRC subsidiaries through capital injections and intra-group loans. Similarly, our PRC subsidiaries may in turn transfer cash to their respective subsidiaries in the PRC through capital injections and intra-group loans. Cash may also be transferred through our organization by way of intra-group transactions. If our wholly owned subsidiaries in the PRC realize accumulated after-tax profits, they may, upon satisfaction of relevant statutory conditions and procedures, pay dividends or distribute earnings to our offshore intermediary holding entities, which, in turn, may transfer cash to the Parent through dividends or other distributions. With necessary funds, the Parent may pay dividends or make other distributions to U.S. investors and service any debt it may have incurred outside of the PRC. No assets other than cash were transferred between the Parent and a subsidiary, no subsidiaries paid dividends or made other distributions to the Parent, and no dividends or distributions were paid or made to U.S. investors. The Company and its subsidiaries currently do not have a cash management policy in place. In 2022 and 2023, the Parent transferred cash in the amount of US$2.3 million and nil to our PRC subsidiaries through our offshore intermediary holding entities by way of capital contribution to the PRC subsidiaries. In 2022, the Company owed TD E-Commerce an unpaid amount of $38 million, which remained outstanding in 2023.

To the extent cash in the business is in the mainland PRC or Hong Kong or a PRC or Hong Kong entity, the funds may not be available to fund operations or for other use outside of the PRC or Hong Kong due to restrictions under the PRC laws and regulations to transfer cash. Under PRC laws and regulations, we are subject to restrictions on foreign exchange and cross-border cash transfers, including to U.S. investors. Our ability to distribute earnings to the holding company and U.S. investors is also limited. We are a Delaware holding company and we may rely on dividends and other distributions on equity paid by our PRC subsidiaries for our cash and financing requirements, including the funds necessary to pay dividends and other cash distributions to our shareholders and service any debt we may incur. When any of our PRC subsidiaries incurs debt on its own behalf, the instruments governing the debt may restrict its ability to pay dividends or make other distributions to us. Under PRC laws and regulations, each of our PRC subsidiaries may pay dividends only out of its respective accumulated profits as determined in accordance with PRC accounting standards and regulations. In addition, a PRC enterprise is required to set aside at least 10% of its after-tax profits each year, if any, to fund a certain statutory reserve fund, until the aggregate amount of such fund reaches 50% of its registered capital. At its discretion, a PRC enterprise may allocate a portion of its after-tax profits based on PRC accounting standards to a staff welfare and bonus fund. These reserve fund and staff welfare and bonus fund cannot be distributed to us as dividends. In addition, our PRC subsidiaries generate their revenue primarily in Renminbi, which is not freely convertible into other currencies. As a result, any restriction on currency exchange may limit the ability of our PRC subsidiaries to pay dividends to us. See “Risk Factor — Risks Related to Doing Business in China — Regulations relating to offshore investment activities by PRC residents may limit our ability to acquire PRC companies and could adversely affect our business”, “Risk Factors — Risks Related to Doing Business in China — PRC regulation of loans to and direct investment in PRC entities by offshore holding companies and governmental control of currency conversion may delay or prevent us from using the proceeds of this offering to make loans or additional capital contributions to our PRC subsidiaries in China, which could materially and adversely affect our liquidity and our ability to fund and expand our business”, “Risk Factors — Risks Related to Doing Business in China — To the extent cash in the business is in the mainland PRC or Hong Kong or a PRC or Hong Kong entity, the funds may not be available to fund operations or for other use outside of the PRC or Hong Kong due to interventions in or the imposition of restrictions and limitations under the PRC laws and regulations.”

Recent Developments

Settlement of Convertible Promissory Notes

The Company settled the convertible promissory notes issued on March 13, 2023 in favor of Streeterville Capital, LLC, of $150,000 on February 1, 2024, and $150,000 on February 15, 2024, respectively, and issued 160,174 and 152,650 shares of the Company’s common stock to Streeterville Capital, LLC on February 1, 2024 and February 15, 2024, respectively.

14

Our Business

As of December 31, 2023, the Company has two business lines, the commodities trading business and supply chain management services set forth below.

Commodities Trading Business

Industry Overview

Bulk commodities trading refers to the trading of materials used in industrial and agricultural production that are continuously purchased in bulk, and are unable to be purchased from the retail sector. Commodities belong at the upstream stage of production processes of various industrial chains, and the supply and demand conditions of commodities can cause price fluctuations and affect the development of these industrial chains.

Commodities can be divided into four categories, metals, energy, livestock and meat, and agricultural. Metal commodities include gold, silver, platinum, and copper. Energy commodities include crude oil, heating oil, natural gas, and gasoline. Livestock and meat include lean hogs, pork bellies, live cattle, and feeder cattle. Agricultural commodities include corn, soybeans, wheat rice, cocoa, coffee, cotton, and sugar.

Operation of Commodities Trading Business

The Company’s commodities trading operations via Shenzhen Baiyu Jucheng are focused on non-ferrous metal commodities such as aluminum, copper, silver, and gold. We strive to become an emerging platform in the non-ferrous metal e-commerce industry by offering all participants in the non-ferrous metal e-commerce industry a seamless, one-stop transaction experience.

Business Model

We source bulk commodities from non-ferrous metal mines or its designated distributors and sell them to manufacturers who need these metals in large quantities. We work with many suppliers in the sourcing of commodities, including various metal and mineral suppliers such as Kunsteel Group, Baosteel Group, Aluminum Corporate of China Limited, Yunnan Benyuan, Yunnan Tin, and Shanghai Copper. Potential customers include large infrastructure companies such as China National Electricity, Datang Power, China Aluminum Foshan International Trade, Tooke Investment (China), CSSC International Trade Co., Ltd., Shenye Group, and Keliyuan.

The Company has entered into a warehousing lease agreement with Shanghai Quansheng Logistics Co., Ltd (“Shanghai Quansheng”) to designate it as the Company’s warehouse in Shanghai. The Company’s criteria for choosing its warehouses are based primarily on the convenience of its location for transportation, which is highly conducive to the transportation of non-ferrous metal commodities, and secondarily based on its storage price.

15

Our inventory management procedure involves (1) an Application for Storage, (2) Storage of the Commodities, (3) an Application for Shipment, and (4) Shipment of Commodities, which are further described below.

| 1) | Application for Storage |

| ● | The upstream suppliers apply for storage with the Company’s leased warehouse center upon the sale of commodities to the Company. The application requires information including the commodities’ production company, brand, specifications, weight, quantity, and storage time. |

| 2) | Storage of the Commodities |

| ● | Upon the arrival of the commodities at the warehouse, the warehouse checks and accepts the commodities according to the delivery instructions provided by the transportation company, ensuring that the delivery instructions, storage application, and the delivered commodities are all consistent. |

| ● | Upon acceptance, the warehouse scans and places the commodities into sorted storage. The warehouse then issues a certificate of inspection, which includes information such as the brand name, specifications, weight, quantity, packaging information, arrival time, storage location and other information of the received commodities. The certificate of inspection is then signed and stamped by the delivery driver, the warehouse manager, and the warehouse. Four copies of the certificate of inspection are made, two of which are provided to the transportation company and the supplier. |

| 3) | Application for Shipment |

| ● | The downstream customers apply for shipment with the warehouse upon the purchase of Commodities from the Company. The application requires information including the production company, brand, specifications, weight, quantity, delivery time, and storage location number. |

| ● | The downstream customers also fill in a delivery entrustment letter, including the name of the delivery company, the name of the delivery person, his or her ID number, the delivery vehicle’s license plate number, the time, quantity, and information regarding the warehouse for delivery. |

| 4) | Shipment of Commodities |

| ● | The warehouse prepares the commodities in advance according to the pick-up time and the Application for Shipment. |

| ● | Upon arrival of the pick-up driver at the warehouse, the Company reviews the identity of the pick-up driver according to the delivery entrustment letter. | |

| ● | Upon completing the loading of the commodities for shipment, the warehouse issues a certificate of sale, which includes information such as the brand name, specifications, weight, quantity, delivery time, and storage location number. The pick-up driver, warehouse manager, and the warehouse signs and stamps the certificate of sale. Four copies of the certificate of sale are made, two of which are provided to the transportation company and the customer. |

16

We use a prepaid unified purchase and distribution model (“Prepaid Model”) in our business, which is further detailed below.

Under the Prepaid Model, we make advance prepayments between one to three months in advance when purchasing from the Company’s upstream suppliers. The process involves first obtaining purchase orders from one or more downstream purchasers and entering into sales agreements with such purchasers. After the Company receives the down payment from the downstream purchasers, it aggregates the total amount of commodities required to fulfill the orders and enters into purchase agreements with upstream suppliers to fulfill its purchase orders. Once the upstream suppliers have received the prepayment from the Company, they produce and deliver the commodities to the Company’s designated warehouse on the purchase agreement. Upon receipt of the commodities in the designated warehouse, the Company is notified by the warehouse and obtains the full payment from the downstream purchasers. After the Company pays its remaining balance to the upstream suppliers, it issues delivery instructions to the designated warehouse on the sales agreement and has the commodities delivered to the downstream purchasers.

Through the Prepaid Model, which is further illustrated below, the Company maintains a stable distribution volume and thereby generates profit margins via purchase discounts from upstream suppliers and mark-up pricing to downstream customers.

Warehousing Arrangement

Shenzhen Baiyu Jucheng has entered into a certain warehousing agreement with Shanghai Quansheng pursuant to which Shenzhen Baiyu Jucheng designated Shanghai Quansheng as its warehouse for the storage of its commodities.

Pursuant to the warehousing agreement with Shanghai Quansheng, Shenzhen Baiyu Jucheng and Shanghai Quansheng agreed to various customary representations, warranties and covenants, including, among other things, (1) details regarding the procedures for the storage and retrieval of the commodities, (2) storage and penalty fees, and (3) negotiation and litigation in the event of any breach of contract.

17

Suppliers

We source the non-ferrous metal from various sources including but not limited to smelters, non-ferrous metal wholesalers and metal traders. For the year ended December 31, 2023, the Company purchased non-ferrous metal products from ten third party suppliers.

Customers

We sell to various businesses in need of large quantity of non-ferrous metal including home appliance manufacturing enterprises, cable manufacturing enterprises and wire manufacturing enterprises. For the years ended December 31, 2023 and 2022, the Company sold non-ferrous metals to 23 and 29 customers, respectively.

Supply Chain Management Services

Commodity Distribution Services

We offer a distribution service to bulk suppliers of precious metals by acting as a sales intermediary, procuring small to medium-sized buyers through our own professional sales team and channels and distributing to them the bulk precious metals of the suppliers. Upon the execution of a purchase order from our sourced buyers, we charge the suppliers with a commission fee ranging from 1% to 2% of the distribution order, depending on the size of the order. For the year ended December 31, 2023, the Company earned commodity distribution commission fees of $67,981 from facilitating such sales transactions with nine third party customers. For the year ended December 31, 2022, the Company earned commodity distribution commission fees of $1,391,903 from facilitating such sales transactions with 23 third party customers.

Marketing