UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-Q/A

Amendment No. 1

☒ QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the quarterly period ended September 30, 2020

☐ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from ____________ to ____________

Commission file number: 001-36055

TD Holdings, Inc.

(Exact name of registrant as specified in its charter)

| Delaware | 45-4077653 | |

| (State or other jurisdiction of incorporation or organization) |

(I.R.S. Employer Identification No.) |

|

25th Floor, Block C, Tairan Building No. 31 Tairan 8th Road, Futian District Shenzhen, Guangdong, PRC |

518000 | |

| (Address of principal executive offices) | (Zip Code) |

+86 (0755) 88898711

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||

| Common Stock, par value $0.001 | GLG | Nasdaq Capital Market |

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ☐ | Accelerated filer | ☐ |

| Non-accelerated filer | ☒ | Smaller reporting company | ☒ |

| Emerging growth company | ☐ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

As of November 12, 2020, 71,131,207 shares of the Company’s Common Stock, $0.001 par value per share, were issued and outstanding.

EXPLANATORY NOTE

As disclosed in our Current Report on Form 8-K filed with the Securities and Exchange Commission (the “SEC”) on March 29, 2021, as amended, on March 26, 2021, the Audit Committee (the “Audit Committee”) of the Board of Directors of TD Holdings, Inc. (the “Company”), after discussion with the Company’s management, concluded that the Company’s previously issued financial statements contained in the Company’s Quarterly Reports (“2020 Quarterly Reports”) on Form 10-Q for the periods ended March 31, 2020, June 30, 2020, and September 30, 2020 (collectively “Non-Reliance Periods”), originally filed on June 26, 2020, August 14, 2020, and November 13, 2020, respectively, should no longer be relied upon. Similarly, related press releases, earnings releases, and investor communications describing the Company’s financial statements for the Non-Reliance Periods should no longer be relied upon.

We are therefore filing this this amended Form 10-Q (“Amended Form 10-Q”) to our Quarterly Report on Form 10-Q for the quarter ended September 30, 2020 (the “Original Form 10-Q”), to restate our interim financial statements and revise related disclosures (including, without limitation, those contained under Item 1, Financial Statements and Item 2, Management’s Discussion and Analysis of Financial Condition and Results of Operations, contained in the Original Form 10-Q to reflect reversal of revenues from supply chain management, which impacted the Company’s net income (loss) and earnings (loss) per share, and related disclosures and Management’s Discussion and Analysis of Financial Condition and Results of Operations. In addition, the identification of related parties changes the footnote for related parties.

As several parts of the Original Form 10-Q are amended and/or restated by this Amended Form 10-Q, for convenience, we have repeated the entire text of the Original Form 10-Q, as amended and/or restated by this Amended Form 10-Q. Readers should therefore read and rely on this Amended Form 10-Q in lieu of the Original Form 10-Q.

Except as amended and/or restated by this Amended Form 10-Q, no other information included in the Original Form 10-Q is being amended or updated by this Amended Form 10-Q. This Amended Form 10-Q continues to describe the conditions as of the date of the Original Form 10-Q and, except as contained therein, we have not updated or modified the disclosures contained in the Original Form 10-Q. Accordingly, this Amended Form 10-Q should be read in conjunction with our filings made with the SEC subsequent to the filing of the Original Form 10-Q, including any amendment to those filings.

PART 1. FINANCIAL INFORMATION

ITEM 1. FINANCIAL STATEMENTS

TD HOLDINGS, INC.

UNAUDITED CONDENSED CONSOLIDATED BALANCE SHEETS

As of September 30, 2020 and December 31, 2019

| September 30, 2020 | December 31, 2019 | |||||||

| (restated) | ||||||||

| ASSETS | ||||||||

| Current Assets | ||||||||

| Cash | $ | 2,967,557 | $ | 1,777,276 | ||||

| Loans receivable from third parties | 87,310,943 | 576,647 | ||||||

| Prepayments | 5,432,099 | - | ||||||

| Due from related parties | 1,469,875 | 2,840,728 | ||||||

| Other current assets | 183,810 | 39,960 | ||||||

| Escrow account receivable | 369,552 | - | ||||||

| Assets of discontinued operations | - | 2,645,269 | ||||||

| Total current assets | 97,733,836 | 7,879,880 | ||||||

| Investments in equity investees | 410,000 | 410,000 | ||||||

| Right-of-use lease assets, net | 237,524 | - | ||||||

| Assets of discontinued operations, noncurrent | - | 3,098,520 | ||||||

| Total noncurrent assets | 647,524 | 3,508,520 | ||||||

| Total Assets | $ | 98,381,360 | $ | 11,388,400 | ||||

| LIABILITIES AND EQUITY | ||||||||

| Current Liabilities | ||||||||

| Advances from customers | $ | 1,896,139 | $ | - | ||||

| Third party loans payable | - | 315,729 | ||||||

| Due to related parties | 2,076,573 | 166,332 | ||||||

| Stock subscription advance | - | 1,600,000 | ||||||

| Income tax payable | 1,633,121 | 14,735 | ||||||

| Lease liabilities | 215,658 | - | ||||||

| Other current liabilities | 656,940 | 200,602 | ||||||

| Current liabilities of discontinued operations | - | 3,138,016 | ||||||

| Total Current Liabilities | 6,478,431 | 5,435,414 | ||||||

| Noncurrent liabilities of discontinued operations | - | 152,124 | ||||||

| Total Non-current Liabilities | - | 152,124 | ||||||

| Total Liabilities | 6,478,431 | 5,587,538 | ||||||

| Commitments and Contingencies (Note 12) | ||||||||

| Equity | ||||||||

| Common stock (par value $0.001 per share, 100,000,000 shares authorized; 71,130,512 and 11,585,111 shares issued and outstanding at September 30, 2020 and December 31, 2019, respectively) | 71,130 | 11,585 | ||||||

| Stock subscription receivable | (5,000,000 | ) | - | |||||

| Additional paid-in capital | 131,393,177 | 38,523,170 | ||||||

| Accumulated deficit | (37,654,136 | ) | (32,391,040 | ) | ||||

| Accumulated other comprehensive income (loss) | 3,092,758 | (334,281 | ) | |||||

| Total Shareholders’ Equity | 91,902,929 | 5,809,434 | ||||||

| Non-controlling interests | - | (8,572 | ) | |||||

| Total Equity | 91,902,929 | 5,800,862 | ||||||

| Total Liabilities and Equity | $ | 98,381,360 | $ | 11,388,400 | ||||

The accompanying notes are an integral part of the unaudited condensed consolidated financial statements.

1

TD HOLDINGS, INC.

UNAUDITED CONDENSED CONSOLIDATED STATEMENTS OF OPERATIONS AND COMPREHENSIVE INCOME (LOSS)

For the Three and Nine Months Ended September 30, 2020 and 2019

(Expressed in U.S. dollars, except for the number of shares)

| For the Three Months Ended September 30, | For the Nine Months Ended September 30, | |||||||||||||||

| 2020 | 2019 | 2020 | 2019 | |||||||||||||

| (restated) | (restated) | |||||||||||||||

| Revenues | ||||||||||||||||

| Sales of commodity products | $ | 2,722,836 | $ | - | $ | 2,722,836 | $ | - | ||||||||

| Sales of commodity products – related parties | 958,108 | 3,575,409 | ||||||||||||||

| Supply chain management services | 1,148,839 | - | 1,609,469 | - | ||||||||||||

| Supply chain management services – related parties | 2,041,570 | 2,112,166 | ||||||||||||||

| Total Revenue | 6,871,353 | - | 10,019,880 | - | ||||||||||||

| Cost of revenue | ||||||||||||||||

| Commodity product sales | (88,543 | ) | - | (1,458,212 | ) | - | ||||||||||

| Commodity product sales – related parties | (3,609,639 | ) | - | (4,865,857 | ) | - | ||||||||||

| Supply chain management services | (16,463 | ) | - | (24,417 | ) | - | ||||||||||

| Total cost of revenue | (3,714,645 | ) | - | (6,348,486 | ) | - | ||||||||||

| Gross profit | 3,156,708 | - | 3,671,394 | - | ||||||||||||

| Operating expenses | ||||||||||||||||

| Selling, general, and administrative expenses | (292,080 | ) | (259,945 | ) | (1,032,660 | ) | (2,123,191 | ) | ||||||||

| Total operating cost and expenses | (292,080 | ) | (259,945 | ) | (1,032,660 | ) | (2,123,191 | ) | ||||||||

| Other income (expenses), net | ||||||||||||||||

| Interest income | 1,836,016 | - | 3,736,079 | 636 | ||||||||||||

| Interest expenses | (15,164 | ) | - | (69,644 | ) | - | ||||||||||

| Amortization of beneficial conversion feature relating to issuance of convertible notes | - | - | (3,400,000 | ) | - | |||||||||||

| Amortization of relative fair value of warrants relating to issuance of convertible notes | - | - | (3,060,000 | ) | - | |||||||||||

| Total other income (expenses), net | 1,820,852 | - | (2,793,565 | ) | 636 | |||||||||||

| Income (Loss) from Continuing Operations Before Income Taxes | 4,685,480 | (259,945 | ) | (154,831 | ) | (2,122,555 | ) | |||||||||

| Income tax expenses | (1,149,563 | ) | - | (1,573,531 | ) | - | ||||||||||

| Net Income (Loss) from Continuing Operations | 3,535,917 | (259,945 | ) | (1,728,362 | ) | (2,122,555 | ) | |||||||||

| Net Loss from Discontinued Operations | (2,989,116 | ) | (132,898 | ) | (3,541,807 | ) | (1,140,439 | ) | ||||||||

| Net Income (Loss) | 546,801 | (392,843 | ) | (5,270,169 | ) | (3,262,994 | ) | |||||||||

| Less: Net (income) loss attributable to non-controlling interests | - | (5 | ) | 7,073 | 486 | |||||||||||

| Net income (loss) attributable to TD Holdings, Inc.’s Stockholders | $ | 546,801 | $ | (392,848 | ) | $ | (5,263,096 | ) | $ | (3,262,508 | ) | |||||

| Comprehensive Income (Loss) | ||||||||||||||||

| Net Income (Loss) | $ | 546,801 | $ | (392,843 | ) | $ | (5,270,169 | ) | $ | (3,262,994 | ) | |||||

| Foreign currency translation adjustment | 3,515,011 | (57,232 | ) | 3,427,039 | (74,256 | ) | ||||||||||

| Comprehensive income (loss) | 4,061,812 | (450,075 | ) | (1,843,130 | ) | (3,337,250 | ) | |||||||||

| Less: Total comprehensive (income) loss attributable to non-controlling interests | - | (5 | ) | 7,073 | 486 | |||||||||||

| Comprehensive income (loss) attributable to TD Holdings, Inc. | $ | 4,061,812 | $ | (450,080 | ) | $ | (1,836,057 | ) | $ | (3,336,764 | ) | |||||

| Income (Loss) per share – basic and diluted | $ | 0.01 | $ | (0.05 | ) | $ | (0.12 | ) | $ | (0.46 | ) | |||||

| Income (Loss) per share from continuing operations – basic and diluted | $ | 0.06 | $ | (0.03 | ) | $ | (0.03 | ) | $ | (0.30 | ) | |||||

| Income (Loss) per share from discontinued operations – basic and diluted | $ | (0.05 | ) | $ | (0.02 | ) | $ | (0.09 | ) | $ | (0.16 | ) | ||||

| Weighted Average Shares Outstanding-Basic and Diluted | 58,625,143 | 8,646,297 | 43,695,789 | 7,122,560 | ||||||||||||

The accompanying notes are an integral part of the unaudited condensed consolidated financial statements.

2

TD HOLDINGS, INC.

UNAUDITED CONDENSED CONSOLIDATED STATEMENTS OF CHANGES IN EQUITY

For the Nine Months Ended September 30, 2020 and 2019

(Expressed in U.S. dollars, except for the number of shares)

| Common Stock | Additional paid-in | Accumulated | Subscription advanced from a Shareholder (Stock Subscription | Accumulated other comprehensive | Non-controlling | Total (Deficit) | ||||||||||||||||||||||||||

| Shares | Amount | capital | Deficit | receivable) | loss | interests | Equity | |||||||||||||||||||||||||

| Balance as at December 31, 2018 | 5,023,906 | $ | 5,024 | $ | 28,765,346 | $ | (25,457,090 | ) | $ | - | $ | (511,057 | ) | $ | - | $ | 2,802,223 | |||||||||||||||

| Issuance of common stock to service providers | 502,391 | 502 | 883,706 | - | - | - | - | 884,208 | ||||||||||||||||||||||||

| Issuance of common stocks pursuant to registered direct offering, net of transaction cost | 3,120,000 | 3,120 | 4,650,320 | - | - | - | - | 4,653,440 | ||||||||||||||||||||||||

| Net loss | - | - | - | (3,262,508 | ) | - | - | (486 | ) | (3,262,994 | ) | |||||||||||||||||||||

| Foreign currency translation adjustments | - | - | - | - | - | (74,256 | ) | - | (74,256 | ) | ||||||||||||||||||||||

| Balance as at September 30, 2019 | 8,646,297 | $ | 8,646 | $ | 34,299,372 | $ | (28,719,598 | ) | $ | - | $ | (585,313 | ) | $ | (486 | ) | $ | 5,002,621 | ||||||||||||||

| Balance as at December 31, 2019 | 11,585,111 | $ | 11,585 | $ | 38,523,170 | $ | (32,391,040 | ) | $ | - | $ | (334,281 | ) | $ | (8,572 | ) | $ | 5,800,862 | ||||||||||||||

| Issuance of common stocks in connection with private placements | 19,000,000 | 19,000 | 20,081,000 | - | (18,500,000 | ) | - | - | 1,600,000 | |||||||||||||||||||||||

| Issuance of common stocks in connection with exercise of convertible notes | 20,000,000 | 20,000 | 29,980,000 | - | - | - | - | 30,000,000 | ||||||||||||||||||||||||

| Beneficial conversion feature relating to issuance of convertible notes | - | - | 3,400,000 | - | - | - | - | 3,400,000 | ||||||||||||||||||||||||

| Relative fair value of warrants relating to issuance of convertible notes | 3,060,000 | 3,060,000 | ||||||||||||||||||||||||||||||

| Issuance of common stocks in connection with exercise of warrants | 20,545,401 | 20,545 | 36,349,007 | - | - | - | - | 36,369,552 | ||||||||||||||||||||||||

| Collection of subscription fee | - | - | - | - | 13,500,000 | - | - | 13,500,000 | ||||||||||||||||||||||||

| Disposal of subsidiaries | - | - | - | - | - | (35,673 | ) | 15,645 | (20,028 | ) | ||||||||||||||||||||||

| Net income | - | - | - | (5,263,096 | ) | - | - | (7,073 | ) | (5,270,169 | ) | |||||||||||||||||||||

| Foreign currency translation adjustments | - | - | - | - | - | 3,462,712 | - | 3,462,712 | ||||||||||||||||||||||||

| Balance as at September 30, 2020 (restated) | 71,130,512 | $ | 71,130 | $ | 131,393,177 | $ | (37,654,136 | ) | $ | (5,000,000 | ) | $ | 3,092,758 | $ | - | $ | 91,902,929 | |||||||||||||||

The accompanying notes are an integral part of the unaudited condensed consolidated financial statements

3

TD HOLDINGS, INC.

UNAUDITED CONDENSED CONSOLIDATED STATEMENTS OF CHANGES IN EQUITY

For the Three Months Ended September 30, 2020 and 2019

(Expressed in U.S. dollars, except for the number of shares)

| Common Stock | Additional paid-in | Accumulated | Subscription advanced from a Shareholder (Stock Subscription | Accumulated income | Non-controlling | Total (Deficit) | ||||||||||||||||||||||||||

| Shares | Amount | capital | Deficit | receivable) | (loss) | interests | Equity | |||||||||||||||||||||||||

| Balance as at June 30, 2019 | 8,646,297 | $ | 8,646 | $ | 34,299,372 | $ | (28,326,750 | ) | $ | - | $ | (528,081 | ) | $ | (491 | ) | $ | 5,452,696 | ||||||||||||||

| Net loss | - | - | - | (392,848 | ) | - | - | 5 | (392,843 | ) | ||||||||||||||||||||||

| Foreign currency translation adjustments | - | - | - | - | - | (57,232 | ) | - | (57,232 | ) | ||||||||||||||||||||||

| Balance as at September 30, 2019 | 8,646,297 | $ | 8,646 | $ | 34,299,372 | $ | (28,719,598 | ) | $ | - | $ | (585,313 | ) | $ | (486 | ) | $ | 5,002,621 | ||||||||||||||

| Balance as at June 30, 2020 | 68,585,111 | $ | 68,585 | $ | 126,026,170 | $ | (38,200,937 | ) | $ | - | $ | (422,253 | ) | $ | (15,645 | ) | $ | 87,455,920 | ||||||||||||||

| Issuance of common stocks in connection with private placements | 2,000,000 | 2,000 | 4,998,000 | - | (5,000,000 | ) | - | - | - | |||||||||||||||||||||||

| Issuance of common stocks in connection with exercise of warrants | 545,401 | 545 | 369,007 | - | - | - | - | 369,552 | ||||||||||||||||||||||||

| Disposal of subsidiaries | - | - | - | - | - | (35,673 | ) | 15,645 | (20,028 | ) | ||||||||||||||||||||||

| Net income | - | - | - | 546,801 | - | - | - | 546,801 | ||||||||||||||||||||||||

| Foreign currency translation adjustments | - | - | - | - | - | 3,550,684 | - | 3,550,684 | ||||||||||||||||||||||||

| Balance as at September 30, 2020 (restated) | 71,130,512 | $ | 71,130 | $ | 131,393,177 | $ | (37,654,136 | ) | $ | (5,000,000 | ) | $ | 3,092,758 | $ | - | $ | 91,902,929 | |||||||||||||||

The accompanying notes are an integral part of the unaudited condensed consolidated financial statements

4

TD HOLDINGS, INC.

UNAUDITED CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS

For the Nine Months Ended September 30, 2020 and 2019

(Expressed in U.S. dollar)

| For

the Nine Months Ended September 30, | ||||||||

| 2020 | 2019 | |||||||

| (restated) | ||||||||

| Cash Flows from Operating Activities: | ||||||||

| Net loss | $ | (5,270,169 | ) | $ | (3,262,994 | ) | ||

| Less: net loss from discontinued operations | 3,541,807 | 1,140,439 | ||||||

| Net loss from continuing operations | (1,728,362 | ) | (2,122,555 | ) | ||||

| Adjustments to reconcile net loss to net cash used in operating activities: | ||||||||

| Amortization of right of use assets | 222,840 | - | ||||||

| Stock-based compensation to service providers | - | 884,208 | ||||||

| Amortization of beneficial conversion feature relating to issuance of convertible notes | 3,400,000 | - | ||||||

| Amortization of relative fair value of warrants relating to issuance of convertible notes | 3,060,000 | - | ||||||

| Changes in operating assets and liabilities: | ||||||||

| Prepayments | (5,282,703 | ) | - | |||||

| Escrow account receivable | (369,552 | ) | - | |||||

| Other current assets | (139,114 | ) | (13,000 | ) | ||||

| Advances from customers | 1,843,990 | - | ||||||

| Due to related parties | 296,611 | - | ||||||

| Income tax payable | 1,573,531 | - | ||||||

| Other current liabilities | 439,422 | 51,103 | ||||||

| Lease liabilities | (244,104 | ) | - | |||||

| Net Cash Provided by (Used in) Operating Activities from Continuing Operations | 3,072,559 | (1,200,244 | ) | |||||

| Net Cash Used in Operating Activities from Discontinued Operations | (700,039 | ) | (802,446 | ) | ||||

| Net Cash Provided by (Used in) Operating Activities | 2,372,520 | (2,002,690 | ) | |||||

| Cash Flows from Investing Activities: | ||||||||

| Investments in equity investees | - | (200,000 | ) | |||||

| Investments in financial products | - | (1,000,000 | ) | |||||

| Collection of loans from related parties | 3,404,953 | - | ||||||

| Loans made to related parties | (4,826,640 | ) | - | |||||

| Collection of loans from third parties | 74,999,934 | - | ||||||

| Loans made to third parties | (157,087,880 | ) | (499,000 | ) | ||||

| Net Cash Used in Investing Activities from Continuing Operations | (83,509,633 | ) | (1,699,000 | ) | ||||

| Net Cash Used in Investing Activities from Discontinued Operations | 368,612 | (3,758,537 | ) | |||||

| Net Cash Used in Investing Activities | (83,141,021 | ) | (5,457,537 | ) | ||||

| Cash Flows from Financing Activities: | ||||||||

| Proceeds from third party borrowings | 1,558,595 | - | ||||||

| Proceeds from a private placement | 13,500,000 | 5,241,440 | ||||||

| Proceeds from issuance of convertible notes | 30,000,000 | - | ||||||

| Proceeds from exercise of warrants | 36,369,552 | - | ||||||

| Net Cash Provided by Financing Activities from Continuing Operations | 81,428,147 | 5,241,440 | ||||||

| Net Cash Provided by (Used in) Financing Activities from Discontinued Operations | (381,554 | ) | 2,157,822 | |||||

| Net Cash Provided by Financing Activities | 81,046,593 | 7,399,262 | ||||||

| Effect of exchange rate changes on cash and cash equivalents | 912,189 | (14,197 | ) | |||||

| Net increase (decrease) in cash and cash equivalents | 1,190,281 | (75,162 | ) | |||||

| Cash at beginning of period | 1,777,276 | 416,459 | ||||||

| Cash at end of period | $ | 2,967,557 | $ | 341,297 | ||||

| Supplemental Cash Flow Information | ||||||||

| Cash paid for interest expense | $ | - | $ | - | ||||

| Cash paid for income tax | $ | - | $ | - | ||||

| Supplemental disclosure of Non-cash investing and financing activities | ||||||||

| Right-of-use assets obtained in exchange for operating lease obligations | $ | 455,635 | $ | - | ||||

| Issuance of common stocks in connection with private placements, net of issuance costs with proceeds collected in advance in November 2019 | $ | 1,600,000 | $ | - | ||||

| Issuance of common stocks in connection with conversion of convertible notes | $ | 30,000,000 | $ | - | ||||

| Issuance of common stocks in connection with private placements, net of issuance costs with proceeds uncollected | $ | 5,000,000 | $ | - | ||||

| Issuance of common stocks in connection with cashless exercise of 1,502,022 warrants | $ | 868,530 | $ | - | ||||

The accompanying notes are an integral part of the unaudited condensed consolidated financial statements

5

TD HOLDINGS, INC.

NOTES TO UNAUDITED CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

| 1. | ORGANIZATION AND BUSINESS DESCRIPTION |

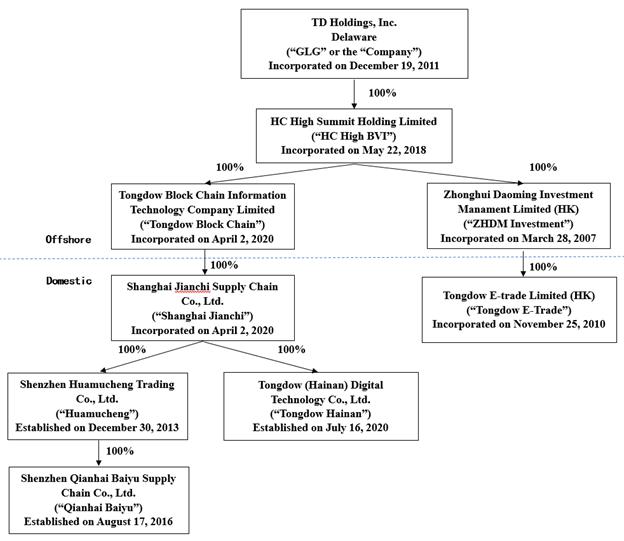

TD Holdings, Inc. (“TD” or “the Company”), is a holding company that was incorporated under the laws of the State of Delaware on December 19, 2011. On January 11, 2019, the Company changed its name to China Bat Group, Inc. and on June 3, 2019, further changed its name to Bat Group, Inc. On March 6, 2020, the Company amended its Certificate of Incorporation with the Secretary of State of Delaware to effect a name change to TD Holdings, Inc.

On April 2, 2020, HC High Summit Holding Limited (“HC High BVI”), the Company’s wholly owned subsidiary, established Tongdow Block Chain Information Technology Company Limited (“Tongdow Block Chain”), a holding company incorporated in accordance with the laws and regulations of Hong Kong. Tongdow Block Chain is wholly owned by HC High BVI. On April 2, 2020 and July 16, 2020, Tongdow Block Chain established Shanghai Jianchi Supply Chain Company Limited (“Shanghai Jianchi”) and Tongdow Hainan Digital Technology Co., Ltd. (“Tondow Hainan”), respectively, as its wholly owned subsidiaries. Both Shanghai Jianchi and Tongdow Hainan are holding companies incorporated in accordance with the laws and regulations of People’s Republic of China (“PRC”).

On June 25, 2020, Hao Limo Technology (Beijing) Co. Ltd. (“Hao Limo”), the Company’s wholly owned subsidiary incorporated in PRC, and Shenzhen Huamucheng Trading Co., Ltd. (“Huamucheng”), a former VIE of the Company, entered into certain VIE Termination Agreement (the “VIE Termination Agreement”) to terminate the Huamucheng VIE Agreements. As such, Hao Limo will no longer have the control rights and rights to the assets, property and revenue of Huamucheng. On the same date, Shanghai Jianchi, Huamucheng and the shareholders of Huamucheng (the “Huamucheng Shareholders”) entered into certain Share Acquisition Agreement (the “Acquisition Agreement”) pursuant to which Shanghai Jianchi acquired 100% equity interest of Huamucheng from the Huamucheng Shareholders for nominal consideration.

As a result of the above reorganization, Huamucheng transitioned from being a variable interest entity (“VIE”) controlled by Company into a wholly owned subsidiary of the Company. The Company remained in control of Huamucheng both before and after the reorganization and its operating results are consolidated into the Company’s consolidated financial statements.

On August 28, 2020, the Company closed the sales of HC High Summit Limited and its subsidiaries and Beijing Tianxing Kunlun Technology Co. Ltd. (“Beijing Tianxing”), the VIE with Vision Loyal Limited (“Vision Loyal”), at a nominal consideration of $1.00 based on a valuation report presented by a third party valuation firm.

On September 11, 2020, the Company acquired Zhong Hui Dao Ming Investment Management Limited (“ZHDM HK”) and its wholly owned subsidiary, Tongdow E-trading Limited (“Tongdow HK”). Both entities were holding companies incorporated in accordance with the laws and regulations of Hong Kong. The consideration was zero because both entities have not commenced any operations before the date of acquisition.

As of September 30, 2020, the Company conducts business through Huamucheng, a subsidiary of the Company, which is engaged in the commodity trading business and providing supply chain management services to customers in the PRC. Supply chain management services consist of loan recommendation services and commodity product distribution services.

6

| 1. | ORGANIZATION AND BUSINESS DESCRIPTION (CONTINUED) |

The accompanying consolidated financial statements reflect the activities of Huamucheng and each of the following holding entities:

| Name | Background | Ownership | ||

| HC High Summit Holding Limited (“HC High BVI”) | ● A BVI company ● Incorporated on March 22, 2018 ● A holding company |

100% owned by the Company | ||

| Tongdow Block Chain Information Technology Company Limited (“Tongdow Block Chain”) | ● A Hong Kong company ● Incorporated on April 2, 2020 ● A holding company |

100% owned by HC High BVI | ||

| Shanghai Jianchi Supply Chain Company Limited (“Shanghai Jianchi”) | ● A PRC company and deemed a wholly foreign owned enterprise (“WFOE”) ● Incorporated on April 2, 2020 ● Registered capital of $10 million ● A holding company |

WFOE, 100% owned by Tongdow Block Chain | ||

| Shenzhen Huamucheng Trading Co., Ltd. (“Huamucheng”) | ● A PRC limited liability company ● Incorporated on December 30, 2013 ● Registered capital of $1,417,736 (RMB 10 million) with registered capital fully paid-up ● Engaged in commodity trading business and providing supply chain management services to customers |

VIE of Hao Limo before June 25, 2020, and a wholly owned subsidiary of Shanghai Jianchi | ||

Tongdow Hainan Digital Technology Co., Ltd. (“Tondow Hainan”) |

● A PRC limited liability company ● Incorporated on July 16, 2020 ● Registered capital of $1,417,736 (RMB 10 million) with registered capital fully paid-up ● Engaged in commodity trading business and providing supply chain management services to customers |

A wholly owned subsidiary of Shanghai Jianchi | ||

Zhong Hui Dao Ming Investment Management Limited (“ZHDM HK”) |

● A Hong Kong company ● Incorporated on March 28, 2007 ● A holding company |

100% owned by HC High BVI | ||

| Tongdow E-trading Limited (“Tongdow HK”) | ● A Hong Kong company ● Incorporated on November 25, 2010 ● A holding company |

100% owned by HC High BVI |

DISPOSITION OF HC High Summit Limited

Historically, one of the Company’s core businesses had been the used luxurious car leasing business conducted through Beijing Tianxing Kunlun Technology Co. Ltd. (“Beijing Tianxing”), an entity that the Company controlled via certain contractual arrangements.

On August 28, 2020, the Company entered into certain share purchase agreement (the “Disposition SPA”) with Vision Loyal, HC High Summit Limited (“HC High HK”) and HC High BVI. Pursuant to the Disposition SPA, Vision Loyal agreed to purchase HC High HK in exchange for nominal consideration of $1.00 based on a valuation report presented by an independent third party valuation firm, Beijing North Asia Asset Assessment Firm. The Company’s board of directors (the “Board”) approved the transaction contemplated by the Disposition SPA (the “Disposition”). The Disposition closed on August 28, 2020.

HC High HK is the sole shareholder of Hao Limo, and controls Beijing Tianxing via a series of contractual arrangements. The list of disposed entities are as follows:

| Name | Relationship | |

| HC High Summit Limited (“HC High HK”) | 100% owned by HC High BVI before August 28, 2020 | |

| Hao Limo Technology (Beijing) Co. Ltd. (“Hao Limo”) |

WOFE, 100% owned by HC High HK | |

| Beijing Tianxing Kunlun Technology Co.

Ltd. (“Beijing Tianxing”)* |

VIE of Hao Limo |

| * | Upon disposition, Beijing Tianxing’ six wholly owned subsidiaries and one 60% owned subsidiary were also disposed. |

| ● | Beijing Tianrenshijia Apparel Co., Ltd. | |

| ● | Beijing Blue Light Marching Technology Co., Ltd. | |

| ● | Beijing Eighty Weili Technology Co., Ltd. | |

| ● | Beijing Bat Riding Technology Co., Ltd | |

| ● | Beijing Blue Light Riding Technology Co., Ltd., and |

| ● | Car Master (Beijing) Information Consulting Co., Ltd. | |

| ● | Beijing Blue Light Supercar Technology Co., Ltd. (over which the Company previously held 60% equity interest) |

7

| 1. | ORGANIZATION AND BUSINESS DESCRIPTION (CONTINUED) |

Upon closing of the Disposition on August 28, 2020, Vision Loyal became the sole shareholder of HC High HK and as a result, assumed all assets and obligations of all the subsidiaries and VIE entities owned or controlled by HC High HK. See Note 4 for details of assets and liabilities of discontinued operations.

The following diagram illustrates our corporate structure as of the date of this report, reflecting the Disposition and acquisition of Qianhai Baiyu as discussed further in “Note 14. Subsequent Events” .

8

| 2. | SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES |

| (a) | Basis of Presentation |

The interim unaudited condensed consolidated financial statements are prepared and presented in accordance with accounting principles generally accepted in the United States (“U.S. GAAP”).

The unaudited condensed consolidated financial statements as of and for the three and nine months ended September 30, 2020, have been restated (see Note 15). The unaudited condensed consolidated financial information as of September 30, 2020 and for the three and nine months ended September 30, 2020 and 2019 has been prepared without audit, pursuant to the rules and regulations of the SEC and pursuant to Regulation S-X. Certain information and footnote disclosures, which are normally included in annual financial statements prepared in accordance with U.S. GAAP, have been omitted pursuant to those rules and regulations. The unaudited interim financial information should be read in conjunction with the audited financial statements and the notes thereto, included in the Form 10-K for the fiscal year ended December 31, 2019, which was filed with the SEC on May 29, 2020.

In the opinion of management, the accompanying unaudited condensed consolidated financial statements reflect all normal recurring adjustments, which are necessary for a fair presentation of financial results for the interim periods presented. The Company believes that the disclosures are adequate to make the information presented not misleading. The accompanying unaudited condensed consolidated financial statements have been prepared using the same accounting policies as used in the preparation of the Company’s consolidated financial statements for the year ended December 31, 2019. The results of operations for the three and nine months ended September 30, 2020 and 2019 are not necessarily indicative of the results for the full years.

| (b) | Loans receivable due from third parties |

The Company provided loans to certain third parties for the purpose of making use of its cash.

The Company monitors all loans receivable for delinquency and provides for estimated losses for specific receivables that are not likely to be collected. As of September 30, 2020 and December 31, 2019, the Company did not accrue allowance against loans receivables due from third parties.

| (c) | Discontinued operation |

In accordance with ASC 205-20, Reporting Discontinued Operations and Disclosures of Disposals of Components of an Entity, a disposal of a component of an entity or a group of components of an entity is required to be reported as discontinued operations if the disposal represents a strategic shift that has (or will have) a major effect on an entity’s operations and financial results when the components of an entity meets the criteria in paragraph 205-20-45-1E to be classified as held for sale. When all of the criteria to be classified as held for sale are met, including management, having the authority to approve the action, commits to a plan to sell the entity, the major current assets, other assets, current liabilities, and noncurrent liabilities shall be reported as components of total assets and liabilities separate from those balances of the continuing operations. At the same time, the results of all discontinued operations, less applicable income taxes (benefit), shall be reported as components of net income (loss) separate from the net income (loss) of continuing operations in accordance with ASC 205-20-45.

On August 28, 2020 when the Company closed disposition of HC High Summit Limited, the Company’s used luxurious car leasing business met all the conditions required in order to be classified as a discontinued operation (Note 1). Accordingly, the operating results of used luxurious car leasing business are reported as a loss from discontinued operations in the accompanying consolidated financial statements for all periods presented. In addition, the assets and liabilities related to our used luxurious car leasing business are reported as assets and liabilities of discontinued operations in the accompanying consolidated balance sheets at December 31, 2019. For additional information, see Note 4, “Disposition of HC High Summit Limited”.

| (d) | Segment reporting |

The Company has two operating business lines, including business with metal products trading and supply chain management services business conducted by Huamucheng (“Commodity Trading and Supply Chain Management Services”) and used luxurious car leasing business (“Used Car Leasing”) conducted by Beijing Tianxing. However, due to changes in our organizational structure associated with the used luxurious car leasing business as a discontinued operation (Note 2(c)), management has determined that the Company now operates in one operating segment with one reporting segment. The accounting policies of our one reportable segment are the same as those described in this Note 2.

| (e) | Reclassification |

Certain items in the financial statements of comparative period have been reclassified to conform to the financial statements for the current period, primarily for the effects of discontinued operations.

9

| 2. | SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (CONTINUED) |

| (f) | Recent accounting pronouncement |

In June 2016, the FASB issued ASU No. 2016-13, “Measurement of Credit Losses on Financial Instruments (Topic 326)”, which significantly changes the way entities recognize impairment of many financial assets by requiring immediate recognition of estimated credit losses expected to occur over their remaining life, instead of when incurred. In November 2018, the FASB issued ASU No. 2018-19, “Codification Improvements to Topic 326, Financial Instruments—Credit Losses”, which amends Subtopic 326-20 (created by ASU No.2016-13) to explicitly state that operating lease receivables are not in the scope of Subtopic 326-20. Additionally, in April 2019, the FASB issued ASU No.2019-04, “Codification Improvements to Topic 326, Financial Instruments—Credit Losses, Topic 815, Derivatives and Hedging, and Topic 825, Financial Instruments”, in May 2019, the FASB issued ASU No. 2019-05, “Financial Instruments—Credit Losses (Topic 326): Targeted Transition Relief”, and in November 2019, the FASB issued ASU No. 2019-10, “Financial Instruments—Credit Losses (Topic 326), Derivatives and Hedging (Topic 815), and Leases (Topic 842): Effective Dates”, and ASU No. 2019-11, “Codification Improvements to Topic 326, Financial Instruments—Credit Losses”, to provide further clarifications on certain aspects of ASU No. 2016-13 and to extend the nonpublic entity effective date of ASU No. 2016-13. The changes (as amended) are effective for the Company for annual and interim periods in fiscal years beginning after December 15, 2022, and the Company is in the process of evaluating the potential effect on its consolidated financial statements.

In August 2020, the FASB issued ASU No. 2020-06 (“ASU 2020-06”) “Debt—Debt with Conversion and Other Options (Subtopic 470-20) and Derivatives and Hedging—Contracts in Entity’s Own Equity (Subtopic 815-40): Accounting for Convertible Instruments and Contracts in an Entity’s Own Equity.” ASU 2020-06 will simplify the accounting for convertible instruments by reducing the number of accounting models for convertible debt instruments and convertible preferred stock. For public business entities, the amendments in ASU 2020-06 are effective for public entities which meet the definition of a smaller reporting company are effective for fiscal years, and interim periods within those fiscal years, beginning after December 15, 2023. The Company will adopt ASU 2020-06 effective January 1, 2024. Management is currently evaluating the effect of the adoption of ASU 2020-06 on the consolidated financial statements. The effect will largely depend on the composition and terms of the financial instruments at the time of adoption.

| 3. | LIQUIDITY |

In assessing the Company’s liquidity, the Company monitors and analyzes its cash and its ability to generate sufficient cash flow in the future to support its operating and capital expenditure commitments. The Company’s liquidity needs are to meet its working capital requirements and operating expenses obligations.

As of September 30, 2020, the Company had a positive working capital of approximately $91.3 million, among which the Company had a loan due from Shenzhen Xinsuniao Technology Co., Ltd. (“Shenzhen Xinsuniao”) of approximately $85.6 million for the purpose of developing supply chain financing business. Pursuant to the loan agreement, the loan term for each individual loan was twelve months from disbursement, but in practice the loans are revolving every 3 – 4 months. From October 1, 2020 to the date of the report, the Company fully collected outstanding balance.

Going forward, the Company plans to fund its operations through revenue generated from its commodity trading business, funds from its private placements as well as financial support commitments from the Company’s Chief Executive Officer and major shareholders.

Based on above operating plan, the management believes that the Company will continue as a going concern in the following 12 months.

10

| 4. | DISPOSITION OF HC HIGH SUMMIT LIMITED |

On August 28, 2020, the Company entered into the Disposition SPA by and among Vision Loyal, HC High HK and HC High BVI. Pursuant to the Disposition SPA, Vision Loyal agreed to purchase the HC High HK in exchange for nominal consideration of $1.00 based on a valuation report presented by a third party valuation firm. The Board approved the transaction contemplated by the Disposition SPA. The Disposition closed on August 28, 2020.

Upon completion of the Disposition, the Company does not bear any contractual commitment or obligation to the used luxurious car leasing business or the employees of HC High HK, nor to Vision Loyal.

On August 28, 2020, management was authorized to approve and commit to a plan to sell HC High HK, therefore the major assets and liabilities relevant to the disposal are reported as components of total assets and liabilities separate from those balances of the continuing operations. At the same time, the results of all discontinued operations, less applicable income taxes, are reported as components of net income (loss) separate from the net loss of continuing operations in accordance with ASC 205-20-45. The assets relevant to the sale of HC High Summit Limited with a carrying value of $5.32 million were classified as assets held for sale as of August 28, 2020. The assets of discontinued operations mainly consisted of loan receivables due from third parties of $1.57 million due from third parties and leasing business assets (used luxurious cars) of $2.23 million. The liabilities relevant to the sale of HC High Summit Limited with a carrying value of $2.61 million were classified as liabilities held for sale, which was comprised of loans of $1.17 million due to third parties and due to related parties of $1.06 million. A net loss of $2.99 million was recognized as the net loss from disposal of discontinued operation, all attributable to the Company’s shareholders. The following is a reconciliation of net loss of $2.99 million from disposition in the consolidated statements of operations and comprehensive income (loss):

| Fair value | ||||

| Consideration in exchange for the disposal | $ | 1 | ||

| Noncontrolling interest of HC High Summit Limited | (15,645 | ) | ||

| Less: Net assets (comprised of assets of $5,320,768 and liabilities of $2,606,257) | (2,714,511 | ) | ||

| Loss from disposal | (2,730,155 | ) | ||

| Other comprehensive income | (258,961 | ) | ||

| Net loss from discontinued operations | $ | (2,989,116 | ) | |

The following is a reconciliation of the carrying amounts of major classes of assets and liabilities held for sale in the in the consolidated balance sheet as of August 28, 2020 and December 31, 2019.

| August 28, 2020 | December 31, 2019 | |||||||

| Carrying amounts of major classes of assets held for sale: | ||||||||

| Cash | $ | 84 | $ | 669,407 | ||||

| Loans receivable from third parties | 1,568,418 | 1,379,050 | ||||||

| Due from related parties | 463,391 | 470,154 | ||||||

| Other current assets | 488,911 | 167,846 | ||||||

| Investments in equity investees | 554,711 | 562,807 | ||||||

| Leasing business assets, net | 2,229,819 | 2,426,109 | ||||||

| Other noncurrent assets | 15,434 | 68,416 | ||||||

| Total assets of disposal group classified as held for sale | $ | 5,320,768 | $ | 5,743,789 | ||||

| Carrying amounts of major classes of liabilities held for sale: | ||||||||

| Third party loans payable | $ | 1,168,660 | $ | 2,052,236 | ||||

| Due to related parties | 1,056,249 | 1,003,154 | ||||||

| Other current liabilities | 381,348 | 234,750 | ||||||

| Liabilities directly associated with the assets classified as held for sale | $ | 2,606,257 | $ | 3,290,140 | ||||

11

| 4. | DISPOSITION OF HC HIGH SUMMIT LIMITED (CONTINUED) |

The following is a reconciliation of the amounts of major classes of income from operations classified as discontinued operations in the consolidated statements of operations and comprehensive income (loss) for the three and nine months ended September 30, 2020 and 2019.

| For the Three Months Ended September 30, | For the Nine Months Ended September 30, | |||||||||||||||

| 2020 | 2019 | 2020 | 2019 | |||||||||||||

| Discontinued Operations | ||||||||||||||||

| Income from operating leases | $ | - | $ | 564,614 | $ | 13,946 | $ | 1,505,508 | ||||||||

| Cost of operating lease | - | (372,632 | ) | (323,608 | ) | (1,063,305 | ) | |||||||||

| Total operating cost and expenses | - | (351,969 | ) | (175,959 | ) | (1,569,833 | ) | |||||||||

| Total other income (expenses), net | - | 27,089 | (67,070 | ) | (12,809 | ) | ||||||||||

| Income tax expenses | - | - | - | - | ||||||||||||

| Net loss from disposal of discontinued operations | (2,989,116 | ) | - | (2,989,116 | ) | - | ||||||||||

| Net Loss from Discontinued Operations | $ | (2,989,116 | ) | $ | (132,898 | ) | $ | (3,541,807 | ) | $ | (1,140,439 | ) | ||||

| 5. | LOANS RECEIVABLE FROM THIRD PARTIES |

| September 30, 2020 | December 31, 2019 | |||||||

| Loans receivable from Shenzhen Xinsuniao | $ | 85,641,601 | $ | - | ||||

| Loans receivable from Shenzhen Qianhai Baiyu Supply Chain Co., Ltd. (“Qianhai Baiyu”) | 1,669,342 | - | ||||||

| Loans receivable from others | - | 576,647 | ||||||

| Loan receivable from other third parties | $ | 87,310,943 | $ | 576,647 | ||||

Loans receivable from Shenzhen Xinsuniao

On March 25, 2020, the Company entered into a revolving credit facility with Shenzhen Xinsuniao to provide a credit line of RMB 568 million or approximately $80 million to Shenzhen Xinsuniao. Shenzhen Xinsuniao was reputable for their extensive experiences in supply chain services for commodities trading.

Pursuant to the loan agreement, the proceeds should solely be used for the operations of the commodity trading business including sales and purchase of commodity products, and supply chain management services. Each loan was repayable in twelve months from disbursement, with a per annum interest rate of 10%. However in practice, the loans are generally revolving every three months, which matches the transaction turnover of Shenzhen Xinsuniao and Qianhai Baiyu. From October 1, 2020 to the date of this report, the Company fully collected the outstanding balance.

The revolving credit facility lasts for a period of two years. Shenzhen Xinsuniao pledged 100% of its equity interest in Qianhai Baiyu, which enterprise value was estimated at approximately $106 million. For the nine months ended September 30, 2020, the Company made loans aggregating $155.9 million to Shenzhen Xinsuniao and recognized interest income of $3.6 million. As of September 30, 2020, the Company collected interest income from Shenzhen Xinsuniao. For the nine months ended September 30, 2020, the Company also collected loans principal and interest of $72.6 million and $1.8 million, respectively, from Shenzhen Xinsuniao.

12

| 5. | LOANS RECEIVABLE FROM THIRD PARTIES (CONTINUED) |

Management periodically assesses the collectability of these loans receivable. Delinquent account balances are written-off against the allowance for doubtful accounts after management has determined that the likelihood of collection is not probable. As of September 30, 2020, there was no allowance recorded as the Company considers all of the loans receivable fully collectible.

Loans receivable from Qianhai Baiyu

The Company had a balance of $1,669,342 due from Qianhai Baiyu, which was recorded as a balance due from a related party because Qianhai Biayu was controlled by Mr. Zhiping Chen, the legal representative of Huamucheng before March 31, 2020. On March 31, 2020, Mr. Zhiping Cheng transferred its equity interest in Qianhai Baiyu to unrelated third parties, and Qianhai Baiyu became a third party to the Company. As of September 30, 2020, the Company classified the balance due from Qianhai Baiyu to the account of “loans receivable due from third parties.” The Company charged an interest rate of 10% per annum. Principal and interest are repaid on maturity of the loan. For the nine months ended September 30, 2020, the Company made loans of $1,665,495 to and collected $2,846,325 from Qianhai Baiyu. For the three and nine months ended September 30, 2020, the Company recognized interest income of $18,275 and $96,833, respectively, from Qianhai Baiyu.

Management periodically assesses the collectability of these loans receivable. Delinquent account balances are written-off against the allowance for doubtful accounts after management has determined that the likelihood of collection is not probable. As of September 30, 2020, there was no allowance recorded as the Company considers all of the loans receivable fully collectible.

Loans receivable from other third parties

As of December 31, 2019, the Company had balance of $576,647 due from three third party individuals who were engaged in used luxurious car leasing business. Pursuant to the loan agreements, these loans matured before December 2020, and the Company charged the third parties interest rates ranging between 11% and 13% per annum. Principal and interest are repaid on maturity of the loan. Upon disposition of the used luxurious car leasing business, the management assessed the collectability of these third-party loans receivable was remoted and wrote off the balance of $576,647 into “net loss from discontinued operations”.

Interest income of $1,828,080 and $nil was recognized for the three months ended September 30, 2020 and 2019, respectively. Interest income of $3,728,093 and $nil was accrued for the nine months ended September 30, 2020 and 2019. As of September 30, 2020 and December 31, 2019, the Company recorded an interest receivable of $126,048 and $nil as reflected under “other current assets” in the unaudited condensed consolidated balance sheets.

| 6. | INVESTMENTS IN EQUITY INVESTEES |

As of September 30, 2020, the Company’s investments in equity investees were comprised of the following:

| Investment | % of ownership | Investment dates | ||||||||

| Hangzhou Yihe Network Technology Co., Ltd. (“Hangzhou Yihe”) | 410,000 | 20 | % | December 17, 2019 | ||||||

| Less: Share of results of equity investees | - | |||||||||

| $ | 410,000 | |||||||||

October 14, 2019, the Company entered into an agreement with Hangzhou Yihe and agreed to issue 1,253,814 shares of the Company’s common stock to acquire 20% equity interest in Hangzhou Yihe. On December 17, 2019, the Company closed the acquisition.

For the three and nine months ended September 30, 2020, Hangzhou Yihe did not resume operations as affected by COVID-19. As a result, the Company had no share of results of equity investees for the period. Because the closure of business was temporary, the management determined the decline in fair value below the carrying value is not other-than-temporary. As of September 30, 2020, the Company did not provide impairment against the investments in equity investees.

13

| 7. | OTHER CURRENT LIABILITIES |

| September 30, 2020 | December 31, 2019 | |||||||

| Other payable | $ | - | $ | 128,301 | ||||

| Accrued interest expenses | - | 163 | ||||||

| Accrued payroll and benefit | 30,867 | 29,466 | ||||||

| Other tax payable | 610,574 | 35,169 | ||||||

| Others | 15,499 | 7,503 | ||||||

| $ | 656,940 | $ | 200,602 | |||||

| 8. | STOCK SUBSCRIPTION ADVANCE FROM SHAREHOLDERS/STOCK SUBSCRIPTION RECEIVABLE |

On November 21, 2019, the Company entered into a securities purchase agreement with certain investors (the “Purchasers”), pursuant to which the Company agreed to sell an aggregate of 2,000,000 shares of its common stock, par value $0.001 per share, at a per share purchase price of $0.80. As of December 31, 2019, the Company received the proceeds of $1,600,000 in advance from the Purchasers and recorded the amount as “stock subscription advance from shareholder”. On February 5, 2020, the Company issued 2,000,000 shares of Common Stock to the Purchasers, and reversed the amount in the account of “stock subscription advance from shareholder”.

On September 1, 2020, the Company entered into a securities purchase agreement with certain investors, pursuant to which the Company agreed to sell an aggregate of 2,000,000 shares of its common stock, par value $0.001 per share, at a per share purchase price of $2.50. As of September 30, 2020, the Company issued the shares but has not received the proceeds of $5,000,000. The Company recorded the amount in the account of “stock subscription receivable”.

| 9. | CAPITAL TRANSACTIONS |

Common Stock

On January 22, 2020, the Company entered into certain securities purchase agreement with certain investors, pursuant to which the Company agreed to sell an aggregate of 15,000,000 shares of Common Stock, at a per share purchase price of $0.90. The transaction was consummated on March 23, 2020 by issuance of 15,000,000 shares of Common Stock. The Company received proceeds of $13,500,000 in April 2020.

On January 22, 2020, the Company also agreed to sell unsecured senior convertible promissory notes (“Notes”) in the aggregate principal amount of $30,000,000 accompanied by warrants to purchase 20,000,000 shares of Common Stock issuable upon conversion of the Notes at an exercise price of $1.80 (the “2020 Warrants” ). On March 23, 2020, the Company issued the Notes and Warrants to the investors. In April 2020, the Company received the proceeds of $30,000,000 from the issuance of Notes and 2020 Warrants.

The Notes have a maturity date of 12 months with an interest rate of 7.5% per annum. Holders have the right to convert all or any part of the Notes into shares of Common Stock at a conversion price of $1.50 per share 30 days after its date of issuance. The Company retains the right to prepay the Note at any time prior to conversion with an amount in cash equal to 107.5% of the principal that the Company elects to prepay.

The 2020 Warrants are exercisable immediately upon the date of issuance at the exercise price of $1.80 for cash (the “Warrant Shares”). The 2020 Warrants may also be exercised cashless if at any time after the six-month anniversary of the issuance date. There is no effective registration statement registering, or no current prospectus available for the resale of the Warrant Shares, if exercised, the 2020 Warrants will expire five years from date of issuance. The 2020 Warrants are subject to anti-dilution provisions to reflect stock dividends and splits or other similar transactions. The 2020 Warrants contain a mandatory exercise right for the Company to force exercise of the 2020 Warrants if the Company’s common stock trades at or above $3.00 for 20 consecutive trading days, provided, among other things, that the shares issuable upon exercise of the are registered or may be sold pursuant to Rule 144 and the daily trading volume exceeds 300,000 shares of Common stock per trading day on each trading day in a period of 20 consecutive trading days prior to the applicable date.

The Company applied Black-Scholes model to determine the fair value of the 2020 Warrants at $3.42 million. Significant estimates and assumptions used included stock price on January 22, 2020 of $1.52 per share, risk-free interest rate of six month of 1.52%, time to maturity of 2.5 years, and volatility of 25.99%.

14

| 9. | CAPITAL TRANSACIONS (CONTINUED) |

The proceeds of $30 million must be allocated between the Note and the 2020 Warrants, based on the relative fair value. The ratio of the relative fair values of the Notes and the Warrants was 89.8% to 10.2%. After allocating 10.2%, or $3.06 million, of the proceeds to the 2020 Warrants, the Company estimated the embedded conversion option within the Notes is beneficial to the holders, because the effective conversion price was $1.35 ($27.0 million/20 million shares), which was below the Company’s share price of $1.52 on January 22, 2020. The fair value of this beneficial conversion feature was estimated to be $3.4 million, and was recorded to debt discount, to be amortized to interest expense using the effective interest method over the term of the Note.

The total Notes discount was recognized at $6.46 million ($3.06 million from the allocation of proceeds to the Warrants and an additional $3.4 million from the measurement of the intrinsic value of the conversion option). The Note discount was initially recognized as a reduction to the carrying amount of the Notes and an addition to paid-in capital, and was to be subsequently amortized to interest expense using the effective interest method over the Note period.

In April 2020, the Holders elected to convert the Notes at a conversion price of $1.50 per share and also exercise the Warrants at an exercise price of $1.80 per share, and paid cash consideration of $36,000,000 for the exercise of the Warrants by April 15, 2020. As a result, an aggregate of 40,000,000 shares of the Company’s Common Stock were issued on May 18, 2020. The Company received proceeds aggregating $66,000,000 from the transaction, and upon settlement of the Note and the 2020 Warrants, the Company immediately expensed the Note discount of $6.46 million For the nine months ended September 30, 2020, the Company recognized amortization of beneficial conversion feature relating to issuance of convertible notes of $3.4 million and amortization of relative fair value of warrants relating to issuance of conversion notes of $3.06 million.

During July 2020 through August 2020, the holders of warrants issued in direct offering closed on April 11, 2019 (“April Offer”) elected to exercise 167,978 shares of warrants at an exercise price of $2.2, and exercise 1,502,022 shares of warrants at cashless exercise. The Company received proceeds of $369,522 through escrow account and issued 545,401 shares of common stocks.

On March 10, 2021, the Company entered into certain waiver and warrant exercise agreements (the “Exercise Agreement”) with each holders. Pursuant to the Exercise Agreement, in order to induce the holders to exercise all of the outstanding Original Warrants cashlessly, pursuant to the terms of and subject to beneficial ownership limitations contained in the Original Warrants, the Company agreed to waive the Holders’ obligation to pay such portion of the exercise price of each of the May Warrants in excess of $0.95 per share and each of the April Warrants in excess of $1.17 per share, immediately prior to the time of exercise of such Original Warrants. Upon the exercise of all the Original Warrants, the Company will issue a total of 808,891 shares of Common Shares (the “Warrant Shares”) to the Holders.

Warrants

A summary of warrants activity for the nine months ended September 30, 2020 was as follows:

| Number of shares | Weighted average life | Weighted average exercise price | ||||||||

| Balance of warrants outstanding as of December 31, 2019 | 3,033,370 | 4.38 years | 1.58 | |||||||

| Granted | 20,000,000 | 1.80 | ||||||||

| Exercised | (21,670,000 | ) | 1.68 | |||||||

| Balance of warrants outstanding as of September 30, 2020 | 1,363,370 | 3.63 years | 1.90 | |||||||

15

| 9. | CAPITAL TRANSACIONS (CONTINUED) |

As of September 30, 2020 and December 31, 2019, the Company had 3,033,370 shares of warrants, among which 273,370 shares of warrants were issued to two individuals in private placements, and 2,760,000 shares of warrants were issued in two direct offerings closed on May 20, 2019 (“May Offering”) and April 11, 2019 (“April Offering”)

In connection with April Offering, the Company issued warrants to investors to purchase a total of 1,680,000 ordinary shares with a warrant term of five (5) years. The warrants have an exercise price of $2.20 per share. On May 20, 2019, the exercise price was reduced to $1.32, and on August 30, 2019 the exercise price was revised to $2.20.

In connection with May Offering, the Company issued warrants to investors to purchase a total of 1,080,000 ordinary shares with a warrant term of five and a half (5.5) years. The warrants have an exercise price of $1.32 per share.

On August 30, 2019, the Company updated the estimation of fair value of warrants issued on April 11, 2019 as a result of the change in exercise price of the warrants from $1.32 to $2.20. Accordingly the fair value of the Replacement Warrant decreased from $1,638,000 to $1,357,440.

Both warrants are subject to anti-dilution provisions to reflect stock dividends and splits or other similar transactions, but not as a result of future securities offerings at lower prices. The warrants did not meet the definition of liabilities or derivatives, and as such they are classified as equity.

On April 11, 2019 and May 20, 2019, the Company estimated fair value of the both warrants at $1,638,000 and $762,480, respectively, using the Black-Scholes valuation model, which took into consideration the underlying price of ordinary shares, a risk-free interest rate, expected term and expected volatility. As a result, the valuation of the warrant was categorized as Level 3 in accordance with ASC 820, “Fair Value Measurement”.

The key assumptions used in estimates are as follows:

| April 11, | August 30, | May 20, | ||||||||||

| 2019 | 2019 | 2019 | ||||||||||

| (Replacement Warrants) | ||||||||||||

| Price of underlying stock | $ | 1.71 | $ | 1.71 | $ | 1.32 | ||||||

| Terms of warrants (in months) | 60.0 | 55.3 | 66.0 | |||||||||

| Exercise price | $ | 1.32 | $ | 2.20 | $ | 1.32 | ||||||

| Risk free rate of interest | 2.77 | % | 2.77 | % | 2.77 | % | ||||||

| Dividend yield | 0.00 | % | 0.00 | % | 0.00 | % | ||||||

| Annualized volatility of underlying stock | 55.6 | % | 63.45 | % | 57.04 | % | ||||||

16

| 10. | INCOME TAXES |

Effective January 1, 2008, the New Taxation Law of PRC stipulates that domestic enterprises and foreign invested enterprises (the “FIEs”) are subject to a uniform tax rate of 25%. Under the PRC tax law, companies are required to make quarterly estimate payments based on 25% tax rate; companies that received preferential tax rates are also required to use a 25% tax rate for their installment tax payments. The overpayment, however, will not be refunded and can only be used to offset future tax liabilities.

The Company evaluates the level of authority for each uncertain tax position (including the potential application of interest and penalties) based on the technical merits, and measures the unrecognized benefits associated with the tax positions. For the three and nine months ended September 30, 2020, the Company had no unrecognized tax benefits. Due to uncertainties surrounding future utilization, the Company estimates there will not be sufficient future income to realize the deferred tax assets for certain subsidiaries. As of September 30, 2020 and December 31, 2019, the Company had deferred tax assets of $5,305,479 and $2,933,705, respectively. The Company maintains a full valuation allowance on its net deferred tax assets as of September 30, 2020.

The Company does not anticipate any significant increase to its liability for unrecognized tax benefit within the next 12 months. The Company will classify interest and penalties related to income tax matters, if any, in income tax expense.

For the three months ended September 30, 2020 and 2019, the Company had current income tax expenses of $1,149,563 generated by Huamucheng and $nil, respectively, and deferred income tax expenses of $nil and $nil, respectively. For the nine months ended September 30, 2020 and 2019, the Company had current income tax expenses of $1,573,531 generated by Huamucheng and $nil, respectively, and deferred income tax expenses of $nil and $nil, respectively.

The Company accounts for uncertainty in income taxes using a two-step approach to recognizing and measuring uncertain tax positions. The first step is to evaluate the tax position for recognition by determining if the weight of available evidence indicates that it is more likely than not that the position will be sustained on audit, including resolution of related appeals or litigation processes, if any. The second step is to measure the tax benefit as the largest amount that is more than 50% likely of being realized upon settlement. Interest and penalties related to uncertain tax positions are recognized and recorded as necessary in the provision for income taxes. The Company is subject to income taxes in the PRC. According to the PRC Tax Administration and Collection Law, the statute of limitations is three years if the underpayment of taxes is due to computational errors made by the taxpayer or the withholding agent. The statute of limitations is extended to five years under special circumstances, where the underpayment of taxes is more than RMB 100,000. In the case of transfer pricing issues, the statute of limitation is ten years. There is no statute of limitation in the case of tax evasion. There were no uncertain tax positions as of September 30, 2020 and December 31, 2019 and the Company does not believe that its unrecognized tax benefits will change over the next twelve months.

17

| 11. | RELATED PARTY TRANSACTIONS AND BALANCES |

| 1) | Nature of relationships with related parties |

| Name | Relationship with the Company | ||

|

Shenzhen Qianhai Baiyu Supply Chain Co., Ltd. (“Qianhai Baiyu”) |

Controlled by Mr. Zhiping Chen, the legal representative of Huamucheng, prior to March 31, 2020 | ||

| Guangzhou Chengji Investment Development Co., Ltd. (“Guangzhou Chengji”) |

Controlled by Mr. Weicheng Pan, who is an independent director of the Company. | ||

|

Yunfeihu International E-commerce Group Co., Ltd (“Yunfeihu”) |

An affiliate of the Company, over which an immediate family member of Chief Executive Officer owns equity interest and plays a role of director and senior management | ||

|

Shenzhen Tongdow International Trade Co., Ltd. (“TD International Trade”) |

Controlled by an immediate family member of Chief Executive Officer of the Company | ||

|

Guangdong Tongdow Xinyi Cable New Material Co., Ltd. (“Guangdong TD”) |

Controlled by an immediate family member of Chief Executive Officer of the Company | ||

|

Yangzhou Tongdow E-commerce Co., Ltd. (“Yangzhou TD”) |

Controlled by an immediate family member of Chief Executive Officer of the Company | ||

|

Shenzhen Meifu Capital Co., Ltd. (“Shenzhen Meifu”) |

Controlled by Chief Executive Officer of the Company | ||

| Guotao Deng | Legal representative of Huamucheng before December 31, 2019 | ||

| 2) | Balances with related parties |

As of September 30, 2020 and December 31, 2019, the balances with related parties were as follows:

| - | Due from related parties |

| September 30, 2020 | December 31, 2019 | |||||||

| Qianhai Baiyu (i) | $ | - | $ | 2,840,728 | ||||

| TD International Trade (ii) | 1,469,875 | - | ||||||

| Total due from related parties | $ | 1,469,875 | $ | 2,840,728 | ||||

| (i) | The balance due from Qianhai Baiyu represented a loan principal and interest due from the related party. The Company charged the related party interest rates 10% per annum. Principal and interest are repaid on maturity of the loan. On March 31, 2020, Mr. Zhiping Chen transferred his controlling equity interest to an unrelated third party and Qianhai Baiyu was not a related party of the Company. As of September 30, 2020, the Company classified the balance due from Qianhai Baiyu to “Loans receivable from third parties” (Note 5). |

| (ii) |

The balance due from TD International Trade represented prepayments for commodity metal products. |

18

| 11. | RELATED PARTY TRANSACTIONS AND BALANCES (CONTINUED) |

| 2) | Balances with related parties (continued) |

| - | Due to related parties, current |

| September 30, 2020 | December 31, 2019 | |||||||

| Guangzhou Chengji (1) | $ | 1,771,574 | $ | 164,897 | ||||

| Shenzhen Meifu (2) | 304,999 | - | ||||||

| Guotao Deng (3) | - | 1,435 | ||||||

| Total | $ | 2,076,573 | $ | 166,332 | ||||

| (1) | The balance due to Guangzhou Chengji represents loan principal and interest due to the related parties. For the nine months ended September 30, 2020, the Company borrowed a loan of $1,441,461 from Guangzhou Chengji. The Loan has an annual interest rate of 8% and a maturity date of December 4, 2020. For the three and nine months ended September 30, 2020, the Company accrued interest expenses of $29,949 and $67,106, respectively. |

| (2) |

As of September 30, 2020, the balance due to Shenzhen Meifu represented advances from the related party for supply chain management services.

|

| (3) |

The balances due to Guotao Deng represent the operating expenses paid by the related parties on behalf of the Company. The balance is payable on demand and interest free.

Mr. Guotao Deng was a legal representative before December 31, 2019, thus he was not a related party of the Company from January 1, 2020. |

| 3) | Transactions with related parties |

| - | Revenues generated from related parties |

For the three and nine months ended September 30, 2020, the Company generated revenues from below related party customers:

| For the Three Months Ended September 30, | For the Nine Months Ended September 30, | |||||||||||||||

| 2020 | 2019 | 2020 | 2019 | |||||||||||||

| Revenue from sales of commodity products | ||||||||||||||||

| Yunfeihu | $ | - | $ | - | $ | 1,921,586 | $ | - | ||||||||

| TD International Trade | - | - | 695,715 | - | ||||||||||||

| Yangzhou TD | 958,108 | - | 958,108 | - | ||||||||||||

| 958,108 | - | 3,575,409 | - | |||||||||||||

| Revenue from supply chain management services | ||||||||||||||||

| Yunfeihu | 1,353,735 | - | 1,424,331 | - | ||||||||||||

| TD International Trade | 418,047 | 418,047 | ||||||||||||||

| Guangdong TD | 269,788 | 269,788 | ||||||||||||||

| 2,041,570 | 2,112,166 | |||||||||||||||

| Total revenues generated from related parties | $ | 2,999,678 | $ | - | $ | 5,687,575 | $ | - | ||||||||

| - | Purchases from a related party |

For the three and nine months ended September 30, 2020, the Company purchased commodity products from below related party vendors:

| For the Three Months Ended September 30, | For the Nine Months Ended September 30, | |||||||||||||||

| 2020 | 2019 | 2020 | 2019 | |||||||||||||

| Purchase of commodity products | ||||||||||||||||

| Yunfeihu | $ | 943,553 | $ | - | $ | 943,553 | $ | - | ||||||||

| TD International Trade | - | - | 1,256,218 | - | ||||||||||||

| Yangzhou TD | 2,666,086 | - | 2,666,086 | - | ||||||||||||

| $ | 3,609,639 | $ | - | $ | 4,685,857 | $ | - | |||||||||

19

| 12. | COMMITMENTS AND CONTINGENCIES |

| 1) | Lease Commitments |

The Company’s VIEs lease their offices which are classified as operating leases in accordance with Topic 842. Under Topic 842, lessees are required to recognize the following for all leases (with the exception of short-term leases) on the commencement date: (i) lease liability, which is a lessee’s obligation to make lease payments arising from a lease, measured on a discounted basis; and (ii) right-of-use asset, which is an asset that represents the lessee’s right to use, or control the use of, a specified asset for the lease term.

The Company leases offices space with terms ranging from one to two years. The Company considers those renewal or termination options that are reasonably certain to be exercised in the determination of the lease term and initial measurement of right of use assets and lease liabilities. Lease expense for lease payment is recognized on a straight-line basis over the lease term. Leases with initial term of 12 months or less are not recorded on the balance sheet.

The Company determines whether a contract is or contains a lease at inception of the contract and whether that lease meets the classification criteria of a finance or operating lease. When available, the Company uses the rate implicit in the lease to discount lease payments to present value; however, most of the Company’s leases do not provide a readily determinable implicit rate. Therefore, the Company discount lease payments based on an estimate of its incremental borrowing rate.

As of September 30, 2020, the Company had one lease contract with lease expiration in June 2021. The lease contract does not contain any material residual value guarantees or material restrictive covenants. The table below presents the operating lease related assets and liabilities recorded on the balance sheet.

| September 30, 2020 | December 31, 2019 | |||||||

| Rights of use lease assets | $ | 237,524 | $ | - | ||||

| Operating lease liabilities, current | $ | 215,658 | $ | - | ||||

| Operating lease liabilities, noncurrent | - | - | ||||||

| Total operating lease liabilities | $ | 215,658 | $ | - | ||||

The Company did not enter into lease agreements until January 1, 2020. As of September 30, 2020, the weighted average remaining lease term was 0.75 years and discount rates were 4.75%.

Lease expenses for the three and nine months ended September 30, 2020 were $79,098 and $234,744, respectively. Lease expenses for the three and nine months ended September 30, 2019 were $nil.

The following is a schedule, by years, of maturities of lease liabilities as of September 30, 2020:

| Twelve months ended September 30, 2021 | $ | 219,517 | ||

| Total lease payments | 219,517 | |||

| Less: imputed interest | (3,859 | ) | ||

| Present value of lease liabilities | $ | 215,658 |

20

| 12. | COMMITMENTS AND CONTINGENCIES (CONTINUED) |

| 2) | Contingencies |

| a | 2015 Derivative Action |

On February 3, 2015, a purported shareholder Kiran Kodali filed a putative shareholder derivative complaint against the Company, alleging that the Company and its former officers and directors violated their fiduciary duties, grossly mismanaged the Company and were unjustly enriched based upon the transfer that was the subject of the Internal Review and other grounds substantially similar to those asserted in the class action complaints.

On July 16, 2019, the Company received a copy of the final order and judgment that the Court entered on July 11, 2019, approving the settlement set forth in the Stipulation. The Stipulation provides for dismissal of the Derivative Action as to the Company and the Individual Defendants, and the Company agrees to adopt or maintain certain corporate governance reforms for at least three years. The Stipulation also provides for attorneys’ fees and expenses to be paid by the Individual Defendants’ insurance carriers to plaintiffs’ counsel.

| b | 2017 Arbitration with Sorghum |

On December 21, 2017, the Company delivered notice (“Notice”) to Sorghum notifying Sorghum that certain recent actions of Sorghum constituted breaches of Sorghum’s covenants under the Exchange Agreement. Specifically, we believe that Sorghum is in breach of Section 6.9 (a and Section 6.11 (b of the Exchange Agreement which required Sorghum to use commercially reasonable efforts and to cooperate fully with the other parties to consummate the transactions contemplated by the Exchange Agreement and to make its directors, officers and employees available in connection with responding in a timely manner to SEC comments. According to the terms of the Exchange Agreement, the Company is entitled to terminate the Exchange Agreement if the breach is not cured within twenty (20 days after the Notice is provided to Sorghum.

On January 25, 2018, the Company filed an arbitration demand (“Arbitration Demand” with the American Arbitration Association (“AAA” against Sorghum in connection with Sorghum’s breach of the Exchange Agreement.

On July 30, 2018, Arbitrator entered a reasoned award, accepting the Company’s proposal for resolution, awarding the Company damages of $1,436,522 against Sorghum and denying Sorghum’s Counterclaim against the Company in its entirety with prejudice. Sorghum has sought to vacate the arbitration award by filing a petition to vacate the arbitration award in the Supreme Court for the State of New York, New York County. The Court heard the Company and Sorghum’s arguments on May 1, 2019, and entered an order vacating the arbitration award. The Company vigorously opposed and moved to confirm the arbitration award on May 6, 2019. On June 5, 2019, the Company filed a notice of appeal with the New York Supreme Court Appellate Division First Department. The appeal was scheduled to be mediated on November 20, 2019. On November 15, 2019, the Company withdrew its appeal filed June 5, 2019, upon the stipulation of the parties and accordingly, the arbitration award is deemed to be vacated.

21

| 12. | COMMITMENTS AND CONTINGENCIES (CONTINUED) |

| c | 2018 Court Matter with Shanghai Nonobank Financial Information Service Co. Ltd. |